Embed Size (px)

Citation preview

SUZUKI MOTOR CORPORATION

Winter, 2020

P 2

1. Company Outline

2. Mid-Term Management Plan

3. Car Business - India

4. Car Business - other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

Agenda

P 3

Agenda

1. Company Outline 2. Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

P 4

1909 Suzuki Loom Works established 1920 Suzuki Loom Manufacturing Co. incorporated 1952 Started motorcycle business 1954 Name changed to Suzuki Motor Co., Ltd 1955 Started Automobile business 1965 Started Marine business 1968 First overseas motorcycle production (Thailand) 1975 First overseas automobile production (Pakistan) 1979 ALTO mini-vehicle debuts 1981 Business tie-up with General Motors(dissolved in 2008) 1983 Start of automobile production at Maruti Suzuki 1990 Name changed to Suzuki Motor Corporation 1993 WAGON R mini-vehicle debuts 2004 Launch of global strategic model, SWIFT 2013 Accumulated automobile sales reached 50 million 2015 New management and mid-term management plan “SUZUKI NEXT 100” 2016 Started exploration of business partnership with Toyota(Capital Alliance

Agreement in 2019)

Suzuki Loom Works, circa 1909

Place of foundation Nakajima-cho, Hamamatsu

Suzuki historical timeline

P 5

Japan

(Automobiles/Motorcycles/

Marine)

Hungary(Automobiles)

Thailand

(Automobiles/

Motorcycles/

Marine

28 production sites in 20 countries/regions

Production in 20 countries/regions outside Japan, mainly in Asia

U.S.(ATV)

Colombia (Motorcycles)

Egypt (Automobiles)

Vietnam (Automobiles/Motorcycles) Philippines (Motorcycles)

Major production facilities

China (Motorcycles)

Indonesia (Automobiles/Motorcycles)

Brazil (Automobiles/Motorcycles)

Pakistan (Automobiles/Motorcycles)

Myanmar (Automobiles)

India (Automobiles/Motorcycles)

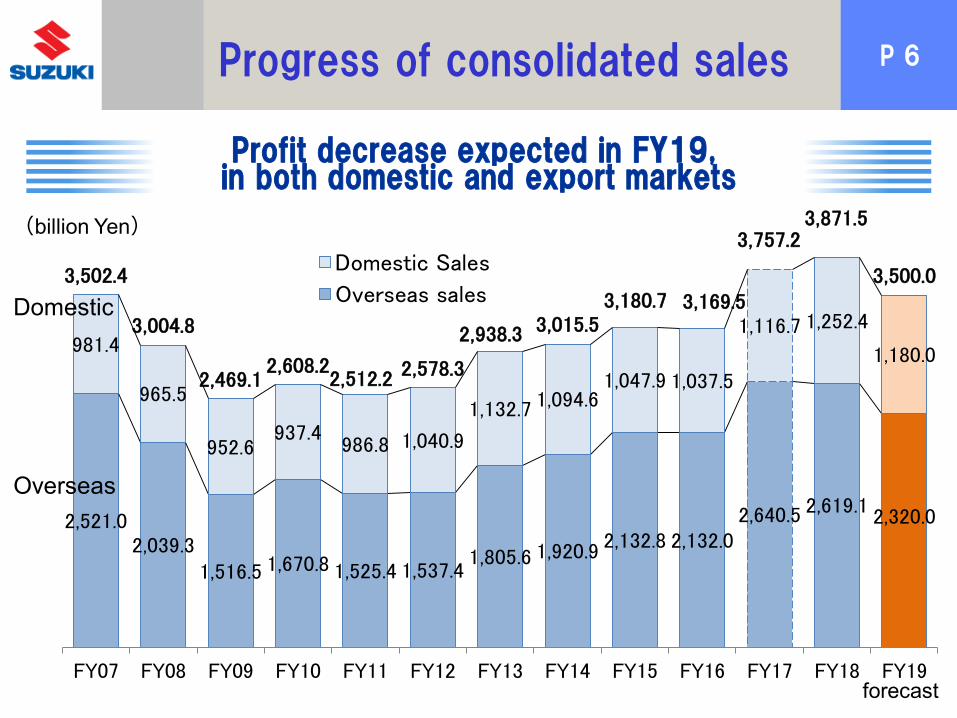

P 6

2,521.0 2,039.3

1,516.5 1,670.8 1,525.4 1,537.4 1,805.6 1,920.9 2,132.8 2,132.0

2,640.5 2,619.1 2,320.0

981.4

965.5

952.6 937.4

986.8 1,040.9

1,132.7 1,094.6 1,047.9 1,037.5

1,116.7 1,252.4

1,180.0

3,502.4

3,004.8

2,469.1 2,608.2

2,512.2 2,578.3

2,938.3 3,015.5 3,180.7 3,169.5

3,757.2 3,871.5

3,500.0

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Domestic Sales

Overseas sales

(billion Yen)

Progress of consolidated sales

Profit decrease expected in FY19, in both domestic and export markets

Domestic

forecast

Overseas

P 7

0

50

100

150

200

(billion yen)

1979 Introduction of ALTO

Constantly profitable since 1950 FY2019 forecast

1993 Introduction of WAGON R

2002 Obtained majority of Indian and Indonesian production JVs

2004 Introduction of SWIFT

2008 Economic crisis

Note Figures from FY1950 to FY1976 are non-consolidated figures, FY1977 and onwards are consolidated figures

Progress of net income

Constant profit for almost 70 years: solid management

Stayed profitable through economic crisis of 2008

FY2018 result: 178.8

P 8

596 672 728 756 630 639 668 725 689

223 197 205 195 207 245 281 278 256 32

1,006 1,051 1,054 1,171 1,305 1,445 1,654 1,754 1,738

543 540 542 550 536

425 439

384

160 204 181 196 183 164

182 186

166 2,560 2,664 2,709 2,867 2,861 2,918

3,224 3,327

2,849

0

500

1,000

1,500

2,000

2,500

3,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

(1,000 units)

Decrease in Japan and Asia in FY19

North America

Progress of global car sales

forecast

Others Asia (excl.India) India Europe Japan

Others Asia (incl.India) Europe Japan

P 9

Agenda

1. Company Outline 2. Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

• All-new “SWIFT” compact car • A global compact car representing Suzuki

Brand

SWIFT

P 10

3,180.7 3,169.5

3,757.2 3,871.5

3,700.0

2,861 2,918 3,224 3,327 3,400

1,501 1,367 1,580 1,743 2,000

FY15 FY16 FY17 FY18 FY19

Auto

mobile

s

Moto

rcyc

les

6.1% 8.4%

10.0% 8.4%

7.0%

9.6%

15.4% 17.9%

13.3%

10.0%

Net S

ale

s In June 2015, Suzuki announced “SUZUKI NEXT 100”, a 5-year plan for

FY2015-19 Key targets (Net sales, Operating profit ratio and ROE) achieved in FY17

≪Target≫

ROE(%)

Operating profit(%)

Sales units (1,000)

Consolidated sales (bln yen)

Mid-Term Management Plan Key targets achieved in FY17

P 11

FY17 FY18 FY19

Forecast

Annual payout per share 74 yen 74 yen 74 yen

Payout ratio 15.1% 18.7% -

5 yen 6 yen 7 yen 8 yen 10 yen 10 yen 15 yen 17 yen 30 yen

37 yen 37 yen

7 yen 7 yen 8 yen 10 yen 14 yen 17 yen

17 yen 27 yen

44 yen 37 yen 37 yen

12 yen 13 yen 15 yen 18 yen 24 yen 27 yen

32 yen

44 yen

74 yen 74 yen 74 yen

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Year end Interim

FY18 Dividend : 74 yen

Dividend payout ratio 18.7% in FY18 = Target 15% or more(FY19)

・Target set at 15% or more, placing priority on growth investment

・Purchased own shares totaling 120 million (460.3 billion Yen) in FY15

・Recovery of equity capital ratio (40.9% as of Mar. 2019) is priority issue

・Net income decreased in FY18, but maintains dividend amount in view of

stable payout

Mid-Term Management Plan “Shareholder return” Dividend payout ratio

Forecast

P 12 Mid-Term Management Plan “Team Suzuki” Corporate Governance enhancement

FY12 FY13 FY14 FY15 FY16 FY17 FY18

Term

SupervisionExecution

Outside directors,total directors 2/7

Supporting div.

Seats

Corporatemission

Code of conduct

FY19

2 outside directorsamong 8 total

pre FY11

Toshihiro Suzuki

Committees

Advisory Committee on Personneland Remuneration, etc.

Corporate Governance Committee

Chairman

President

Board

of Directo

rs

New Mid-Term Management PlanSUZUKI NEXT 100(FY15~FY19)

Mid-Term Management Target(FY10~FY14)

Mid-TermManagement Plan

Vis

ion

Drafted Suzuki Activity Charter, Suzukiemployees Activity Charter in 2003

Suzuki Group Code of Conduct

Drafted "Mission Statement" in 1962

Osamu SuzukiChairman and President between

2008 and 2015

Term of board members shortened to 1 year from 2002

Introduced executive officers system in 2006

2 outside directorsamong 9 total

Not more than 30 from 1989

Corporate Governance Dept.Secretariat of Audit&Supervisory Board

Reduced to 15

P 13

Directors/Auditors after the 154th AGM (Nominees) Increase of one Outside Directors to total of 3 (incl. one female nominee)

Name Position Current position new nominees

Osamu Suzuki

Yasuhito Harayama

Toshihiro Suzuki

Osamu Honda

Masahiko Nagao

Masakazu Iguchi * Outside Director Toshiaki SuzukiManaging Officer & Executive General ManagerDomestic Marketing I, Domestic Marketing

Sakutaro Tanino * Outside Director Osamu Kawamura *Representative Director and Chairman,Chanson Cosmetics Inc.

Hideaki Domichi *Former Ambassador Extraordinary and Plenipotentiaryof Japan to India/Bhutan

Yuriko Kato *Representative Director and President,M2Labo. Inc.

Toyokazu Sugimoto

Masato Kasai

Norio Tanaka

Nobuyuki Araki

Norihisa Nagano

* Outside Directors

Auditors

Current members Management to be approved at 154th General Meeting(Nominees)Name

Directo

rs

Osamu SuzukiRepresentative Director and Chairman

Yasuhito HarayamaRepresentative Director and Vice Chairman

Toshihiro SuzukiRepresentative Director and President

Osamu HondaDirector and Senior Technical Executive

Masahiko NagaoDirector and Managing Officer

Toyokazu SugimotoAudit & Supervisory Board Member

Masato KasaiAudit & Supervisory Board Member

Norio TanakaAudit & Supervisory Board Member (Outside)

Nobuyuki ArakiAudit & Supervisory Board Member (Outside)

Norihisa NaganoAudit & Supervisory Board Member (Outside)

New

New

New

New

Mid-Term Management Plan “Team Suzuki” Corporate Governance enhancement

P 14

Objective…sustainable growth, increase enterprise value in the mid and long term Standard …following criteria is applied

Holdings …Appropriateness of individual cross-shareholdings (enhancement of

corporate value, capital costs) is examined by the Board of Directors every year Advance reduction of stocks to be sold

Exercise of voting rights

Recent disposals

Basic principles

Create business opportunity Business partnership

Establish, maintain or strengthen stable transaction and cooperation

Decision is to be made by respecting management policy of the investment company and in view of our mid-and long-term enterprise value

Mid-Term Management Plan “Capital Efficiency” Policy shareholding guidelines

Volkswagen AG 4,397 thousand shares (2015) SUBARU CORPORATION 13,690 thousand shares (2016) Asahi Group Holdings 527 thousand shares (2017)

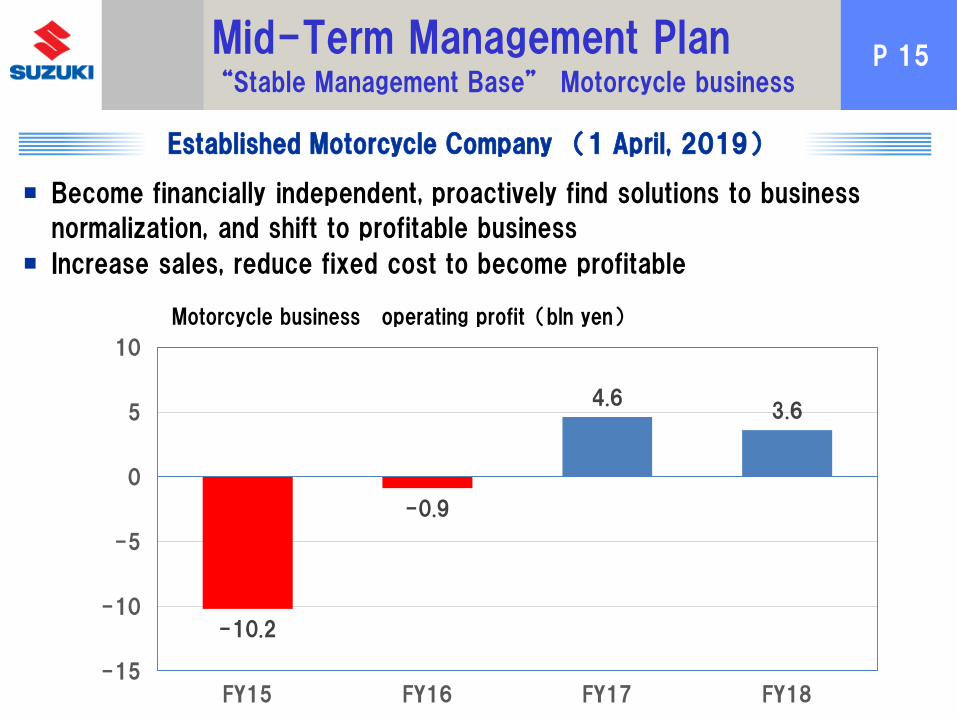

P 15

Become financially independent, proactively find solutions to business

normalization, and shift to profitable business Increase sales, reduce fixed cost to become profitable

-10.2

-0.9

4.6 3.6

-15

-10

-5

0

5

10

FY15 FY16 FY17 FY18

Motorcycle business operating profit(bln yen)

Mid-Term Management Plan “Stable Management Base” Motorcycle business

Established Motorcycle Company (1 April, 2019)

P 16

Suzuki cars selected as Top 3 of World Urban Car by WCA for 3 years in a row (2017 Ignis, 2018 Swift, 2019 Jimny)

Jimny won “2019 World Urban Car”, selected as top 3 of “2019 World Car Design of the Year”

Swift was awarded Car of the Year for 3 generations in Japan (RJC) and India (ICOTY)

Attractive big motorcycles introduced such as GSX-R/V-Strom series and KATANA

Automobiles

Motorcycles

Marine

New flagship outboard motor DF350A Innovation Award at 2017 IBEX Show

(Highest award count of 8 times for 4-stroke outboards)

Example of 4x DF350A (350×4=1,400ps)

Mid-Term Management Plan “Strengthening of Manufacturing” Creative Products

P 17

Disadvantages of local production ・Increased production cost due to multiple locations

・Duplicated jigs and facilities

Partial review of local production and distribution

Local model-Local production ・Part of Indian export production shifted to ASEAN

Designate production site by model ・Model sharing among ASEAN nations

・SWIFT production shifted from Europe to Japan

Indian production for ASEAN ⇒ Shift to production in ASEAN ・Allocate production capacity for Indian market needs

・Improve occupancy rate in ASEAN factories

Production of SWIFT in Europe ⇒ Japan ・Improve occupancy rate in Sagara Plant

・Improve efficiency of Hungarian plant by concentrating in production of a single platform

Effect

Improvement in profit in Japan, Europe and

Asia

Mid-Term Management Plan “Strengthening of Manufacturing”

Optimal Global Production

Optimal global production & procurement systems

P 18

Illustrate the future of 10-15 years in a

long term perspective instead of extension from the present, and plan backwards

Indian market has possibility to grow to a large market in circa 2030 Even in such a case, Suzuki intends to maintain the current market share of 50%

We need to determine, what we can do to realize the long term perspective Effectively allocate management resources of people, goods and money by

changing viewpoint Immediate actions required, to confront this challenge towards the future

Automobile sector faces a drastic change

Indian market in 2030

A challenge towards the future

Drafting new Management Plan on a long-term perspective

Drafting new management plan considering the above

30 25 20FY

Backcast

Drafting new Management Plan

P 19

Outline of cooperation with Toyota Environmental

technologies Safety

technologies Information

technologies

Mutual supply of products and components

Toyota’s strength: Provision of electrified technology and products

Supply HEV systems (Global) Penetration of HEV Technology (India), Supply Electrified vehicles (Europe)

Suzuki’s strength: Provision of compact vehicles and powertrains

Supply of Suzuki compact cars (India), Toyota to produce new Suzuki engine supported by Denso and Toyota at Toyota’s Polish plant (Europe), Supply of Suzuki cars produced in India (Africa)

Development & production leveraging strength of both companies

Joint development and supply of C segment MPV (India) Production of Vitara Brezza at Toyota plant in India (India)

Cooperation with Toyota

Supply of Suzuki developed EVs to Toyota in India

Development of compact,

ultrahigh-efficiency powertrain

Production of Suzuki vehicles in

Toyota plant in India

Supply of Suzuki models to

African markets

Mutual supply of products such as Hybrids in India

Toyota and Suzuki announced that the two companies entered into an agreement regarding a capital alliance, in order to establish and promote a long-term partnership between the two companies for promoting collaboration in new fields, including the field of autonomous driving. Toyota plans to acquire 24,000,000 shares of common stock in Suzuki (total value of JPY 96 billion) by underwriting the disposition of treasury shares by way of third-party allotment conducted by Suzuki. Suzuki plans to acquire, through purchase in the market, shares in Toyota equivalent to JPY 48 billion. Completion of Payment of 96 billion for Disposition of Treasury Shares on 9 December, 2019.

20 M

arc

h, 2019

28 A

ugust

, 2019

P 20 SDGs and CSR activities of the Suzuki Group

(ENVIRONMENT) Improvement in fuel efficiency, Development of

next-generation vehicles, Reduction of

substances of concern and use of their

alternatives, Purification of plant effluent,

Thorough water-saving at plants and offices,

Control of air pollution, Promotion of 3Rs,

Promotion of green procurement, Life Cycle

Assessment

(SOCIAL) Welfare vehicles,

A range of products equipped with Suzuki Safety

Support, Traffic safety

Suzuki Foundation, Suzuki Education and Culture

Foundation, Educational support activity, Suzuki Plaza,

Activities by domestic plants and distributors, and

overseas group companies, Diversity, Actions to

promote participation by women, With our business

partners, Improving corporate value (GOVERNANCE)

Efforts for compliance

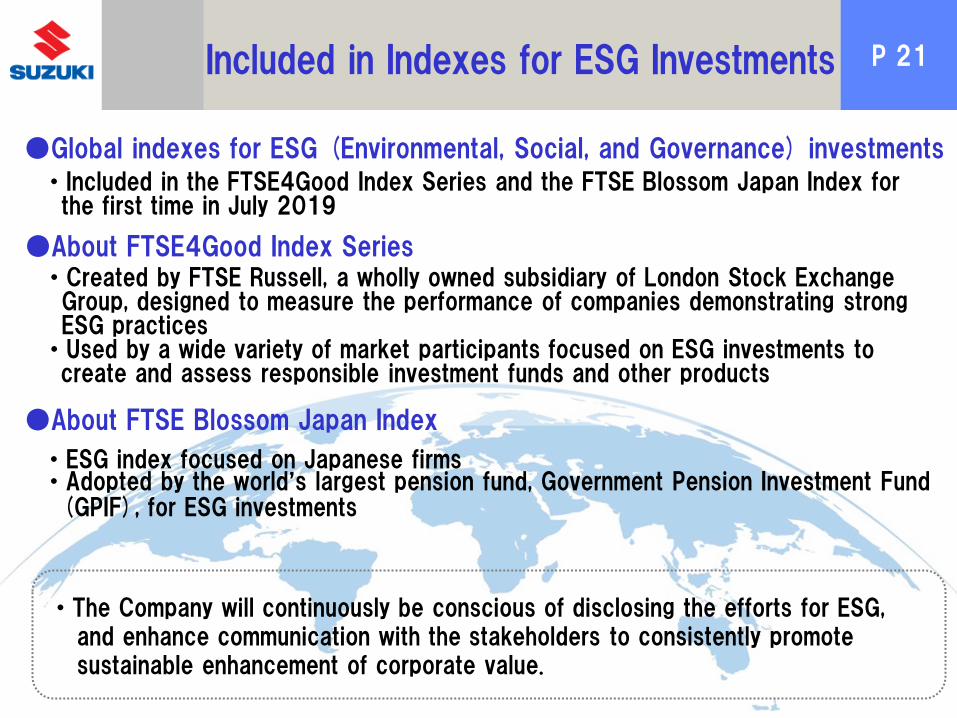

P 21 Included in Indexes for ESG Investments

・Included in the FTSE4Good Index Series and the FTSE Blossom Japan Index for the first time in July 2019

●Global indexes for ESG (Environmental, Social, and Governance) investments

●About FTSE4Good Index Series ・Created by FTSE Russell, a wholly owned subsidiary of London Stock Exchange

Group, designed to measure the performance of companies demonstrating strong ESG practices

・Used by a wide variety of market participants focused on ESG investments to create and assess responsible investment funds and other products

●About FTSE Blossom Japan Index

・ESG index focused on Japanese firms ・Adopted by the world’s largest pension fund, Government Pension Investment Fund

(GPIF), for ESG investments

・The Company will continuously be conscious of disclosing the efforts for ESG, and enhance communication with the stakeholders to consistently promote sustainable enhancement of corporate value.

P 22

Compact SUV VITARA BREZZA (India)

・ Strong and dynamic exterior ・ Wide range of body colors including two

tone variant ・ Developed to meet the requirement and

needs in the Indian market

Agenda

1. Company Outline 2. Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

P 23

23.9 27.8 37.1

53.6

73.4 77.2 75.0

42.2

28.0

14.9

15.6

426.1 426.4 486.1

564.4

669.1

781.0 830.3

622.9

545.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

43.6

<Apr.-Dec. YoY>

57.1 Oct.-Dec.

Apr.-Sept.

Maruti Suzuki Financial Performance

Decline in both sales and profit in 3Q FY19 3Q FY19 saw decline in sales and profit, mainly due to increase in

discounts, poor sales mix, cost to meet safety and emissions regulations, in addition to sales decrease Maruti Suzuki financial performance

※Figures post FY15 are based on IndAS (Indian IFRS)

Sales (rs. billion)

Net income (Rs. billion)

3Q results

P 24

1,006 1,051 1,054 1,171 1,305 1,444 1,643 1,730 1,308 1,065

1,622 1,607 1,450 1,430 1,484

1,603 1,644 1,648

1,225 1,053

2,628 2,658 2,504 2,601 2,790

3,047 3,288 3,377

2,533

2,118

38.3% 39.5%

42.1% 45.0% 46.8% 47.4%

50.0% 51.2% 51.7% 50.3%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

Maruti Others Share

<Apr.-Dec. YoY>

Progress of Car Sales in India

Wholesale of Maruti and market total

3Q FY19 saw decrease YoY due to overall market decline Oct.-Dec. results were positive due to festive season demand

Wholesales 407k units (+0.4% YoY) Retail sales 501k units (+1.0% YoY)

1,000 units

※Wholesale volume excluding commercial vehicles

P 25

426 433 414 427 369 304 178

496 542 585 748 872

641 593

33 54 64

59 46

36

20

68 94

196

254 264

194

184

129 143

152

155 179

132

89

1,171 1,305

1,444

1,643 1,730

1,308

1,065

36% 33% 29% 26%

21% 23% 17%

0

500

1,000

1,500

2,000

FY14 FY15 FY16 FY17 FY18 FY18 FY19

Vans

Utility vehicles

Mid-Size

Compact

Mini

<Apr.-Dec. YoY>

Maruti Suzuki Sales of automobiles by model type

Change in model mix in the domestic market New Wagon R is now classified as compact, and proportion of Mini further

decreased

※Wholesale volume excluding commercial vehicles

(1,000 units)

P 26

DZIRE (1200ccGE, 1300ccDE)

BALENO (1200ccGE,1300ccDE)

IGNIS (1200ccGE)

S-CROSS (1300ccDE)

SWIFT (1200ccGE, 1300ccDE)

CELERIO (1000ccGE)

Utility vehicles

Mini Compact

Mid-Size

CIAZ (1500ccGE/DE, 1300ccDE)

ALTO 800 (800ccGE)

VITARA BREZZA (1500ccGE ,1300ccDE )

NEW

WAGON R (1000ccGE,1200ccGE)

ERTIGA (1500ccGE/DE,1300ccDE)

ALTO K10 (1000ccGE)

XL6 (1500ccGE)

NEW

S-PRESSO (1000ccGE)

NEW

NEW

NEW

Maruti Suzuki cars

Lineup of models

P 27

Strengthen Dealer Network … 4 sales channels

Maruti Suzuki Arena ・Urban (Large dealers, site to be provided by Maruti) ・Rural (Small/Mid-size dealers, Circuit service)

NEXA ・Premium car dealership

Commercial ・SUPER CARRY pickups

True Value ・New concept pre-owned car dealerships ・264 dealerships as of end Dec. 2019

Strengthen Sales Network

SUPER CARRY

Sales Outlets

40 190 310 322 127 252 316 360 370 1,619

1,820 2,020

2,121 2,264 2,349 1,619

1,947 2,312

2,627 2,934 3,041

0

1000

2000

3000

Mar. 15 Mar. 16 Mar. 17 Mar. 18 Mar. 19 Dec. 19

Arena

NEXA

Comercial

Model dealership

Large ARENA dealership

Mid-size ARENA dealership

Small-size ARENA dealership

P 28

Gujarat Plant A began its operations (Feb. 2017) Gujarat Plant B began its operations (Jan. 2019) Plant C planned (SOP July 2020)

700 700 700

800 800 800

250 250 250 250 250

250

0

1000

2000

Existing +Plant A +Plant B

1,500

2,000 1,750

Gujarat Plant C 〃 B 〃 A

(17.2) (19.1)

Manesar Plant Gurgaon Plant

750

JV with Toshiba and Denso Constructed in supplier park next to Gujarat Plant Penetration of Hybrid vehicles will contribute to

environmental issues in India

Production of Lithium-ion batteries in India

Strengthen Production Base

Start-up of Gujarat Plant

Production capacity in India (2 shifts, 1,000 units)

⇨Total 750,000 units p.a.

P 29

Ceremony held in Sep.2017 among the events during PM Abe’s visit to India

Participation of PM Abe, PM Modi and 5,000 government and business people

Suzuki is committed to Indian Government’s “Make in India” and “Skill India” initiative, and contribute to growth of the Indian automotive industry

Ceremonies for opening of Gujarat Plant and

cornerstone laying of lithium-ion battery plant

Development of EV

Started field testing of 50 prototype vehicles from October 2018

Feedback will be incorporated in future EV production

Proto-type EV

Expansion of production capacity and development of EV in India

P 30

VITARA

• Carries forward the SUV excellence that Suzuki has nurtured over the years

• Suzuki’s latest compact SUV that embodies advances that meet diverse contemporary needs

• Advanced safety technologies and outstanding fuel economy

Agenda

1. Company Outline 2. Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

P 31

In addition to decrease in 1H production due to restructuring of final inspection structure, typhoon disaster, consumption tax increase in 2H resulted in decrease YoY Mini: -4.7% YoY Compact: -10.1% YoY

Reduced production, typhoon disaster and tax increase resulted in decrease YoY

Automobile sales: Japan

(1,000 units)

Sales of Mini-cars and Compact Cars in Japan Market share of mini-vehicles <Apr.-Dec. YoY>

80 85 81 76 81 107 112 131 93 83

516 586 647 679 549 532 556 594

421 401

596

672 728

756 630 639

668 725

514 485

30.5% 29.7% 28.6% 31.3% 30.3% 30.9% 29.9% 30.9% 30.9% 29.8%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY190

250

500

750

Mini

Compact

P 32

Following 18 Oct., reported implementation status of preventive measures to MLIT (Final inspection operations)

Complete measures in the current inspection lines where inspectors can stably conduct accurate inspection by Mar. 2020 ⇒ Normalize production • Management of final inspection process and operation

…【Operating (partially prepared)】 • Collection of voices from worksite …【Operating】 • Maintenance of rules …【Conducted】 • Reduction of inspectors’ load …【Increasing inspectors】 • Improvement and reinforcement of inspection facilities…【Conducted】

Further improve from FY2020 and onward, including to unify layout of inspection lines so as to inspect in the same way throughout all plants, secure number of certified inspectors in preparation of future production changes, and meet inspections for changes in cars with new technologies

(Companywide measures) • Establishment of permanent exhibit area to study improper conducts

【by Mar. 2020】 • Handing out Compliance Handbook to all employees 【by Feb. 2020】 • Introduction of service to feedback revision of laws to in-house regulations in

timely manner 【by Mar. 2020】 • Fulfill and continuously conduct training for improving communication, etc.

Implementation Status of Preventive Measures regarding the Improper Conducts of the Final Vehicle Inspection in the Plants

Conducted the second report to the Japanese Ministry of Land, Infrastructure, Transport and Tourism (MLIT) on 31 January

P 33

3Q FY19 resulted in 107% YoY

Increase of sales in Germany, France, Italy and Spain resulted in 107% YoY in total of 5 European markets

96 87 96 99 107

128 142 146

104 111

1.0% 1.0% 1.0% 1.0% 1.0%

1.1% 1.3% 1.3%

1.3% 1.3%

0

50

100

150

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

<Apr.-Dec. YoY>

Automobile sales: Europe

* Total of retail sales in UK, Germany, France, Italy and Spain

Share

Sales in 5 major European markets* (1,000 units)

P 34

100 86 76 89 133 112

137 136 100

75

61.2% 58.8%

54.7% 55.3%

59.5%

53.4% 55.2% 54.2% 53.7%

61.7%

0

50

100

150

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

<Apr.-Dec. YoY>

(千台)

Suzuki first started overseas production (1975)

Taxis are called “SUZUKI” in Pakistan

3Q FY19 saw increase in interest rates, price hike owing to weak Rupees, and was 75% YoY

Launched ALTO in Apr. same car as sold in Japan

Suzuki secures majority market share

Automobile sales: Pakistan

Sales in Pakistan

Special taxi demand

Share (1,000 units)

P 35

Due to decline in total market since 18 Nov., 3Q FY19 resulted in 91% YoY

In February, the XL7 a three-row, seven-seater crossover vehicle that combines the design of an SUV with the convenience of an MPV was launched.

94

142 165 148

120 92 114 111

88 79

10.3%

12.2% 13.3% 12.9%

11.6%

8.6%

10.3% 9.9% 10.2% 10.1%

0

50

100

150

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

(1,000 units)

Automobile sales: Indonesia

Retail Sales in Indonesian Market(figures pre FY12 are wholesales)

Share

Decline in total market, tough condition continues

<Apr.-Dec. YoY>

P 36

1 1 1 1

4

12

9 11

0

5

10

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY18 FY19

Retail Sales in Myanmar

Jan. 2018: Thilawa plant SOP

Automobile sales: Myanmar

Ertiga and Swift selling well

Gradual import restrictions of used cars from Apr. 2017 resulted in growth of new car market

3Q FY19 saw 118% YoY owing to sales of Ertiga and Swift

(1,000 units)

<Apr.-Dec. YoY>

P 37

NEW Hybrid system (Equipped on SOLIO models) ・ A Suzuki unique parallel hybrid system

combining Motor Generator Unit (MGU) with Auto Gear Shift (AGS)*

・ MGU supplements traction during gear shift, enabling smooth acceleration

* Manual transmission with automatic gearshift and clutch operation by electro hydraulic actuator

Agenda

1. Company Outline 2. New Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

P 38

1,754

725

202

278

0

123 26

25

12 44

139

2018 Suzuki global

automobile sales:

3,327 thousand units (1,000 units)

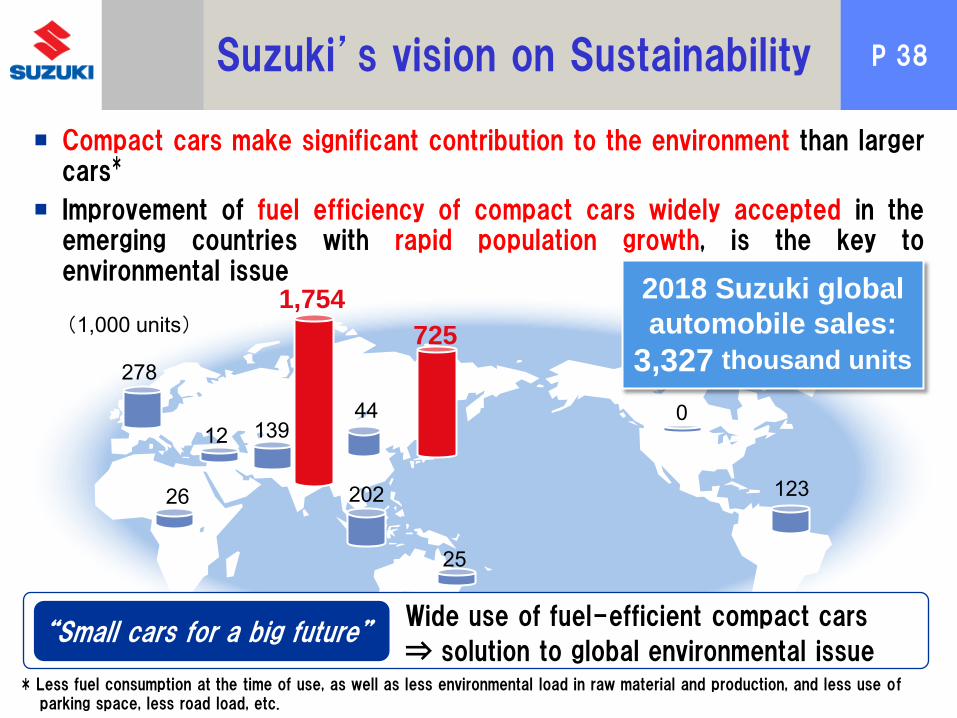

Suzuki’s vision on Sustainability

Compact cars make significant contribution to the environment than larger cars*

Improvement of fuel efficiency of compact cars widely accepted in the emerging countries with rapid population growth, is the key to environmental issue

“Small cars for a big future” Wide use of fuel-efficient compact cars

⇒ solution to global environmental issue * Less fuel consumption at the time of use, as well as less environmental load in raw material and production, and less use of

parking space, less road load, etc.

P 39

Improvement of powertrain

Lightweight New Lightweight Platform

Electrification

Introduction with ALTO (weight reduction of 60kg)

Sustainable Technologies

New SWIFT (weight reduction of 120kg)

SOLIO IGNIS

WAGON R

SWIFT ALTO

0.8L 2-cylinder diesel engine DDiS Engine

Proto-type EV (India)

P 40

Sales of automobiles with hybrid systems (Thousand units)

FY16 Global Sales FY17 Global Sales FY18 Global Sales

Hybrids % Hybrids % Hybrids %

Japan 639 287 44.9% 668 350 52.4% 725 382 52.7%

India 1,445 85 5.9% 1,654 85 5.2% 1,754 149 8.5%

Others 835 17 2.0% 902 27 3.0% 848 29 3.5%

Total 2,918 389 13.3% 3,224 462 14.3% 3,327 561 16.9%Note: Hybrid cars include mild hybrid, S-enecharge and SHVS Hybrid sales in Others are export from Japan and India

System configuration of hybrid system

Hybrid cars account for 17% of global sales*

Sales of Suzuki hybrid cars

System configuration of mild hybrid system

ISG (Generator with motor function)

Exclusive lithium ion battery Reducer AGS (Auto Gear Shift) Power Pack

P 41

New Hustler for Japanese market equipped with latest advanced safety technologies

・Safety Support Car S Wide certification ・Advanced Emergency Brake Support (AEBS) certification

・Dual camera brake support (day/night) ・Reverse mode brake support

SUZUKI SAFETY SUPPORT Suzuki's Advanced Safety Technologies

Preceding car departure notice

Weaving alert function

Dual camera brake support

Lane departure warning

Traffic sign recognition

Adaptive cruise control

Lane departure prevention

High beam assist

Camera for 360° view

Unintended start prevention

Unintended start prevention (rear)

Reverse mode brake support

Collision mitigation brake Safety Support Car S Wide

P 42

・A new concept compact crossover wagon XBEE launched in Japan in December 2017

・Combination of utility of a wagon with Fun element of an SUV

・Equipped with Suzuki Safety Support preventive safety technologies

・Rated as Support car S Wide in the Safety Support Car ratings

Agenda

1. Company Outline 2. New Mid-Term

Management Plan 3. Car Business - India

4. Car Business – Other markets

5. Environment/Safety Technologies

(Appendix)

Q3 FY2019 Summary

XBEE

P 43 3Q FY2019 Highlights

FY2019 9 months FY2018 9 months

(’19/4-12) (’18/4-12) Ratio

Net Sales 2,626.1 2,838.8 -212.7 -7.5% First decrease in 3 periods (since Dec. 2016)

Operating Income 170.4 256.5 (Margin) (6.5%) (9.0%)

Ordinary Income 194.8 306.1 (Margin) (7.4%) (10.8%)

Net Income* 116.6 180.8 (Margin) (4.4%) (6.4%)

・Decreased net sales …Decrease in sales in India and Pakistan, impact of yen appreciation, etc.

・Decreased operating income…Appreciation of yen and increase in various expenses, in addition to decreased net sales

・Decreased ordinary income …Decrease in interest income in India, etc., in addition to decreased operating income

Automobile 2,160 2,480 -320 -12.9% Decrease in India, Japan, Pakistan, etc.

Motorcycle 1,344 1,307 +36 +2.8% Increase in India, the Philippines, etc.

WorldwideSales

Volume(Thousand

-units)

-36.4%

Decreased for the secod consecutive periodConsoli-dated

FinancialResults

(Billions ofyen)

First decrease in 8 periods (since Dec. 2011)

First decrease in 5 periods (since Dec. 2014)

Record

-64.2 -35.5%

Change

-86.1 -33.6%

-111.3

… Kept unchanged ・Kept unchanged from the previous forecast on 10 October

Third Quarter Results

*Net income attributable to owners of the parent

Full Year Forecast

… Lower earnings on lower sales

P 44 Trends in Operating Results by Quarters

85.1 87.8 86.9

114.4 116.5

82.0

58.0 67.9

62.7 55.9 51.8

869.3 961.8

893.8

1,032.3 987.5

941.9 909.4

1,032.7

907.5 847.9 870.7

0.0

40.0

80.0

120.0

160.0

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q0.0

300.0

600.0

900.0

1,200.0Net Sales

Operating Income

(Net Sales)

FY2017 FY2018 FY2019

(Operating

Income) (Billions of yen) Trends in Operating Results by Quarters

Slowdown since 2Q of FY2018, partly owing to production decrease in Japan, in addition to slowdown in Indian automobile continuing from prev. year

P 45 Net Sales: 3Q FY19

FY2019

9 months

('19/4-12)

FY2018

9 months

('18/4-12)Change

FY2019

9 months

('19/4-12)

FY2018

9 months

('18/4-12)Change

FY2019

9 months

('19/4-12)

FY2018

9 months

('18/4-12)Change

FY2019

9 months

('19/4-12)

FY2018

9 months

('18/4-12)Change

Japan total 832.7 870.4 -37.7 15.4 14.7 +0.7 13.4 10.9 +2.5 861.5 896.0 -34.5

764.1 787.5 -23.4 15.4 14.7 +0.7 13.4 10.9 +2.5 792.9 813.1 -20.2

OEM 68.6 82.9 -14.3 68.6 82.9 -14.3

1,544.4 1,726.2 -181.8 166.8 167.5 -0.7 53.4 49.1 +4.3 1,764.6 1,942.8 -178.2 -78.2

Europe 315.8 329.4 -13.6 25.1 26.5 -1.4 13.2 11.2 +2.0 354.0 367.1 -13.1 -23.3

N. America 1.0 0.9 +0.1 20.4 21.1 -0.7 26.9 25.7 +1.2 48.4 47.7 +0.7 -1.2

Asia 1,069.2 1,230.4 -161.2 97.1 96.2 +0.9 5.7 4.8 +0.9 1,172.0 1,331.4 -159.4 -44.0

India 807.7 947.0 -139.3 47.7 40.7 +7.0 0.4 0.4 -0.0 855.8 988.1 -132.3 -27.4

Other 261.5 283.4 -21.9 49.4 55.5 -6.1 5.3 4.4 +0.9 316.2 343.3 -27.1 -16.6

Other 158.4 165.5 -7.1 24.2 23.7 +0.5 7.6 7.4 +0.2 190.2 196.6 -6.4 -9.7

Grandtotal 2,377.1 2,596.6 -219.5 182.2 182.2 -0.0 66.8 60.0 +6.8 2,626.1 2,838.8 -212.7 -78.2

of whicheffect of

ForEX ratesconversion

-6.0 -78.2-1.5-70.7

Total

Suzukibrand

Overseastotal

of whicheffect of

ForEX ratesconversion

MotorcycleAutomobile Marine, etc.(Billionsof yen)

Note: North America…United States and Canada Automobile in North America…sales of parts and accessories, etc.

Asia, esp. Indian automobile net sales largely decreased

P 46

% %

Net Sales 2,377.1 2,596.6 -219.5 -8.5% Net Sales 1,471.3 1,551.0 -79.7 -5.1%OperatingIncome 156.6 244.1 -87.5 -35.9%

OperatingIncome 91.9 112.6 -20.7 -18.3%

(%) (6.6%) (9.4%) (%) (6.2%) (7.3%)

Net Sales 182.2 182.2 0.0 - Net Sales 430.5 434.5 -4.0 -0.9%OperatingIncome 0.0 0.1 -0.1 -

OperatingIncome 15.1 14.7 0.4 +2.8%

(%) (0.0%) (0.1%) (%) (3.5%) (3.4%)

Net Sales 66.8 60.0 6.8 +11.3% Net Sales 1,266.9 1,419.7 -152.8 -10.8%

OperatingIncome 13.8 12.3 1.5 +12.9%

OperatingIncome 54.1 121.6 -67.5 -55.5%

(%) (20.7%) (20.4%) (%) (4.3%) (8.6%)

Net Sales 2,626.1 2,838.8 -212.7 -7.5% Net Sales 138.4 130.2 8.2 +6.3%OperatingIncome 170.4 256.5 -86.1 -33.6%

OperatingIncome 5.6 4.3 1.3 +30.8%

(%) (6.5%) (9.0%) (%) (4.1%) (3.3%)

Change

Mar

ine

Asi

a

Tota

l

Oth

ers

bln yenChange

Moto

rcyc

les

Japan

Auto

mobile

s

Euro

pe

FY20199 months

('19/4-12)

FY20189 months

('18/4-12)

FY20199 months

('19/4-12)

FY20189 months

('18/4-12)

Automobiles, Japan and Asia showed significant decrease 《Results by Geographical Areas》 《Results by Business Segment》

Operating Results by Segment: 3Q FY19

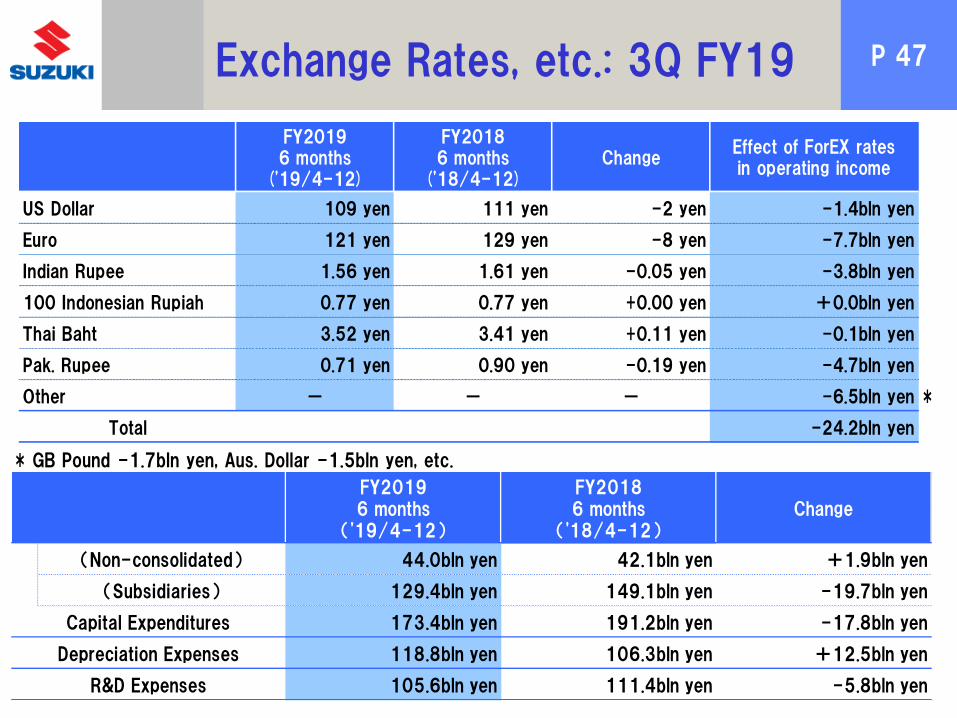

P 47

(Non-consolidated) 44.0bln yen 42.1bln yen +1.9bln yen

(Subsidiaries) 129.4bln yen 149.1bln yen -19.7bln yen

173.4bln yen 191.2bln yen -17.8bln yen

118.8bln yen 106.3bln yen +12.5bln yen

105.6bln yen 111.4bln yen -5.8bln yen

Depreciation Expenses

R&D Expenses

Change

Capital Expenditures

FY20196 months

('19/4-12)

FY20186 months

('18/4-12)

US Dollar 109 yen 111 yen -2 yen -1.4bln yen

Euro 121 yen 129 yen -8 yen -7.7bln yen

Indian Rupee 1.56 yen 1.61 yen -0.05 yen -3.8bln yen

100 Indonesian Rupiah 0.77 yen 0.77 yen +0.00 yen +0.0bln yen

Thai Baht 3.52 yen 3.41 yen +0.11 yen -0.1bln yen

Pak. Rupee 0.71 yen 0.90 yen -0.19 yen -4.7bln yen

Other - - - -6.5bln yen *

Total -24.2bln yen

Change

FY20186 months

('18/4-12)

FY20196 months

('19/4-12)

Effect of ForEX ratesin operating income

* GB Pound -1.7bln yen, Aus. Dollar -1.5bln yen, etc.

Exchange Rates, etc.: 3Q FY19

P 48

Production Sales

Change % Change %

<Automobiles>696 760 -64 -8.4% 485 514 -29 -5.7%

122 125 -2 -2.0% 215 201 +14 +6.7%

1,381 1,652 -271 -16.4% 1,325 1,623 -298 -18.4%

(1,167) (1,381) (-214) (-15.5%) (1,083) (1,325) (-242) (-18.3%)

1 2 -0 -21.1% 135 142 -6 -4.5%

2,200 2,539 -338 -13.3% 2,160 2,480 -320 -12.9%

<Motorcycles>68 83 -15 -18.0% 38 43 -5 -12.3%

- - - - 32 34 -2 -6.0%

2 3 -1 -21.8% 28 28 -0 -0.9%

1,209 1,185 +24 +2.0% 1,110 1,073 +37 +3.5%

46 39 +7 +18.3% 136 129 +7 +5.3%

1,324 1,309 +16 +1.2% 1,344 1,307 +36 +2.8%

Japan

(1,000units)

FY20199 months

('19/4-12)

FY20189 months

('18/4-12)

FY20199 months

('19/4-12)

FY20189 months

('18/4-12)

Japan

EuropeN. America

Asia

Others

Total

Europe

Asia(India)

Others

Total

Production and Sales: 3Q FY19

Decreased YoY owing to decrease in production and sales in India and Japan

P 49 Full year forecast (Overview)

Forecast('19/4-'20/3) ('18/4-'19/3) Change Ratio ('19/4-'20/3) Change Ratio

Net Sales 3,500.0 3,871.5 -371.5 -9.6% 3,900.0 -400.0 -10.3%

Operating Income 200.0 324.4 330.0

(Margin) (5.7%) (8.4%) (8.5%)

Ordinary Income 220.0 379.5 340.0

(Margin) (6.3%) (9.8%) (8.7%)

Net Income* 140.0 178.8 200.0

(Margin) (4.0%) (4.6%) (5.1%)

Automobile 2,849 3,327 -478 -14.4% 3,340 -491 -14.7%

Motorcycle 1,771 1,745 +26 +1.5% 1,825 -54 -3.0%

・Decrease in net sales… Decrease year-on-year and from original forecast owing to production decrease in Japan and decrease in automobile sales in India ・Decrease in operating income…Decrease partly owing to ForEX, in addition to decrease in net sales ・Decrease in ordinary income… Expansion of decrease amount year-on-year partly owing to decrease in interest income in India ・Decrease in net income*… Decrease amount shrinks year-on-year owing to accounting of \81.3 billion as extraordinary losses in the previous year

Comparison with FY 2018

-130.0 -39.4%

-120.0 -35.3%

-60.0 -30.0%

WorldwideSales

Volume(Thousand

units)

-42.0%

Consoli-dated

FinancialResult

(Billions ofyen)

Comparison with original forecast

-38.8 -21.7%

-124.4 -38.3%

-159.5

*Net income attributable to owners of the parent

Full Year Forecast … Kept unchanged from 10 October forecast

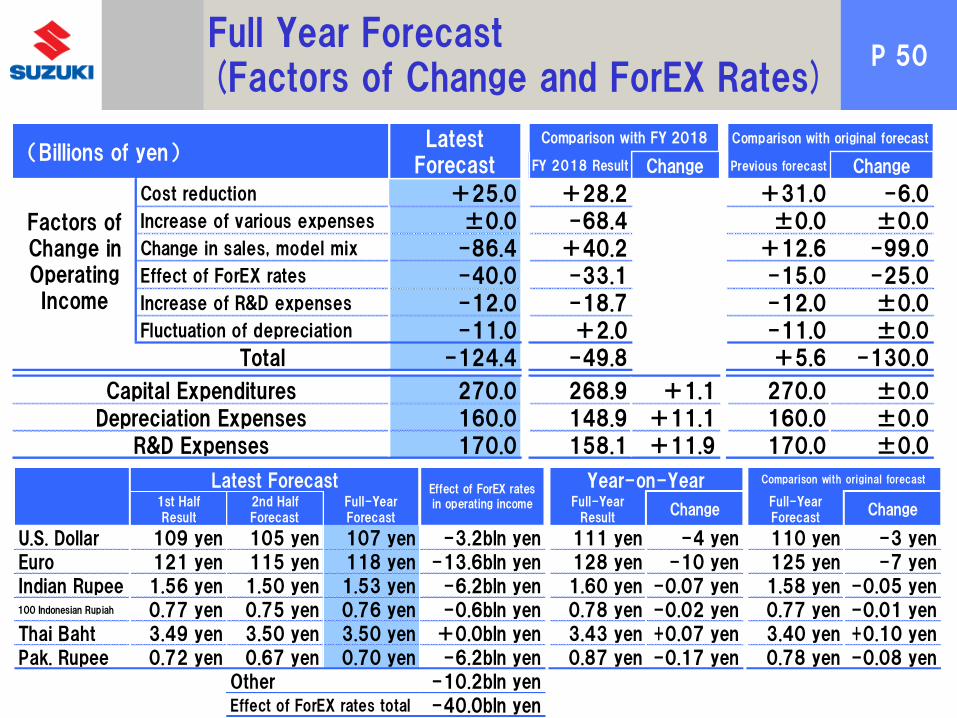

P 50 Full Year Forecast (Factors of Change and ForEX Rates)

1st HalfResult

2nd HalfForecast

Full-YearForecast

Full-YearResult

ChangeFull-YearForecast

Change

U.S. Dollar 109 yen 105 yen 107 yen -3.2bln yen 111 yen -4 yen 110 yen -3 yen

Euro 121 yen 115 yen 118 yen -13.6bln yen 128 yen -10 yen 125 yen -7 yen

Indian Rupee 1.56 yen 1.50 yen 1.53 yen -6.2bln yen 1.60 yen -0.07 yen 1.58 yen -0.05 yen100 Indonesian Rupiah 0.77 yen 0.75 yen 0.76 yen -0.6bln yen 0.78 yen -0.02 yen 0.77 yen -0.01 yen

Thai Baht 3.49 yen 3.50 yen 3.50 yen +0.0bln yen 3.43 yen +0.07 yen 3.40 yen +0.10 yen

Pak. Rupee 0.72 yen 0.67 yen 0.70 yen -6.2bln yen 0.87 yen -0.17 yen 0.78 yen -0.08 yen

-10.2bln yen

-40.0bln yenEffect of ForEX rates total

Comparison with original forecastLatest Forecast

Other

Year-on-YearEffect of ForEX rates

in operating income

FY 2018 Result Change Previous forecast Change

Cost reduction +25.0 +28.2 +31.0 -6.0Increase of various expenses ±0.0 -68.4 ±0.0 ±0.0Change in sales, model mix -86.4 +40.2 +12.6 -99.0Effect of ForEX rates -40.0 -33.1 -15.0 -25.0Increase of R&D expenses -12.0 -18.7 -12.0 ±0.0Fluctuation of depreciation -11.0 +2.0 -11.0 ±0.0

Total -124.4 -49.8 +5.6 -130.0

270.0 268.9 +1.1 270.0 ±0.0

160.0 148.9 +11.1 160.0 ±0.0

170.0 158.1 +11.9 170.0 ±0.0R&D Expenses

Comparison with FY 2018 Comparison with original forecast

Capital Expenditures

Depreciation Expenses

Factors ofChange inOperatingIncome

LatestForecast

(Billions of yen)

P 51

Forecast Forecast

(FY2019) (FY2018) Change Ratio (FY2019) (FY2018) Change Ratio

<Automobile>

Japan 956 1,011 -55 -5.4% -53 689 725 -36 -5.0% -31

Europe 166 180 -14 -7.8% -8 256 278 -22 -8.0% ±0

Asia 1,823 2,201 -378 -17.2% -449 1,738 2,138 -400 -18.7% -444

Other 2 2 -0 -7.4% ±0 166 186 -20 -10.8% -16

Total 2,947 3,394 -447 -13.2% -510 2,849 3,327 -478 -14.4% -491

<Motorcycle>

Japan 101 115 -14 -12.1% -10 52 57 -5 -8.0% -8

Europe - - - - - 45 44 +1 +1.2% -2

N.America 3 4 -1 -25.5% ±0 37 36 +1 +2.3% -2

Asia 1,629 1,576 +53 +3.4% -51 1,468 1,436 +32 +2.2% -68

Other 61 52 +9 +16.6% +9 169 171 -2 -1.3% +26

Total 1,794 1,747 +47 +2.7% -52 1,771 1,745 +26 +1.5% -54

(Thousandunits)

FY2018 ResultFY2018 Result Revisedunits fromoriginalforecast

Production SalesRevised

units fromoriginalforecast

Kept unchanged from 10 October forecast

Automobile sales in India forecasts -20%

Full Year Forecast (Production and Sales)

P 52 Caution with respect to Forward-Looking Statements

The forward-looking statements mentioned in this presentation are based

on currently available information and assumptions, contain risks and

uncertainty and do not constitute guarantees of future achievement.

Please note that the future results may greatly vary by the changes of

various factors.

Those factors, which may influence the future results, include economic conditions and the trend of demand in major markets and the fluctuations

of foreign exchange rates (mainly U.S. dollar/Yen rate, Euro/Yen rate,

Indian Rupee/Yen rate).