Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Swaps in Loan Transactions:

Coordinating Loan Document Terms

with the ISDA Master Agreement Documenting Covenants, Security, Required Consents,

Voting and Control, Reporting, and Regulatory Issues

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, JANUARY 26, 2017

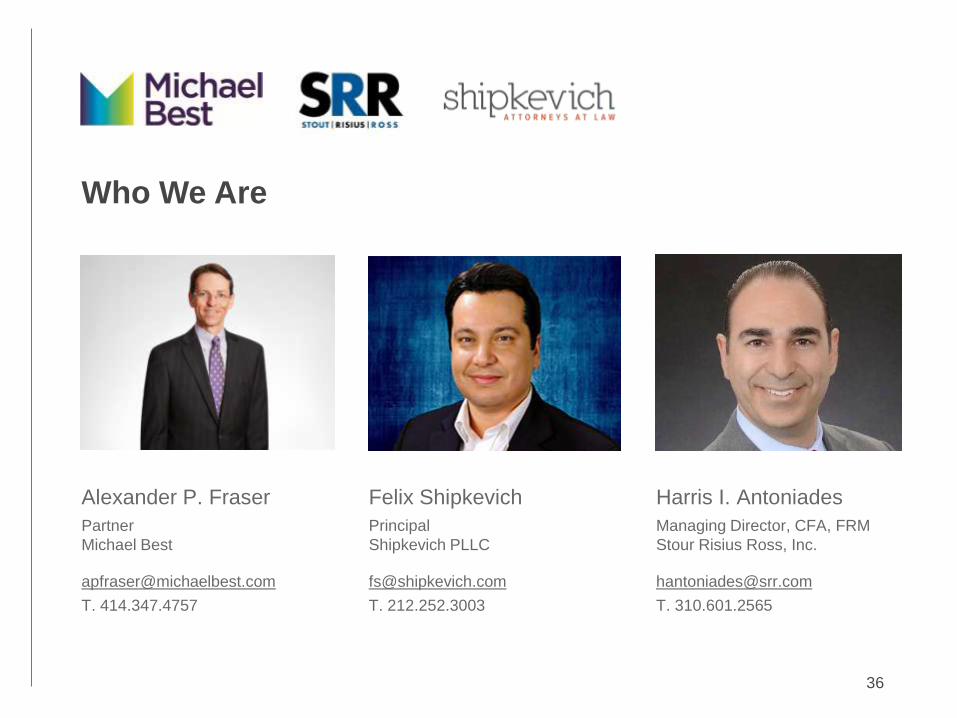

Alexander P. Fraser, Partner, Michael Best & Friedrich, Milwaukee

Harris I. Antoniades, CFA, FRM, Managing Director, Stout Risius Ross, Los Angeles

Felix Shipkevich, Principal, Shipkevich, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Swap Documentation in Loan Transactions: Coordinating Loan Document Terms with the ISDA Master Agreement

Alexander P. Fraser, Esq., Michael Best & Friedrich LLP Felix Shipkevich, Esq., Shipkevich PLLC Harris I. Antoniades, CFA, FRM, Stout Risius Ross

January 26, 2017

Agenda

1. Financial Overview – Use of Derivatives to Obtain

Fixed Rate Loan

2. ISDA Document and Regulatory Overview

3. Coordinating Loan Documents with the ISDA Master

Agreement

6

Use of Interest Rate Swaps (IRS) to Hedge Interest

Rate Risk

• Interest Rate Swaps are derivatives that can be used to hedge against exposure

to fluctuations in interest rates

• An agreement between two parties (the counterparties) where future interest

payments are exchanged based on a specific principal (notional) amount

• Typically, companies enter into credit agreements with banks based on a

benchmark interest rate such as LIBOR or prime, plus a “spread” for a total

interest rate

• Companies usually get loans with floating interest payments and then enter into

swap agreements as the Fixed Payer in order to transform the loan to a fixed rate

loan by hedging the interest rate risk (cash flow hedge)

• Eliminates or reduces the exposure that arises from changes in interest rate

payments due to changes in the benchmark interest rate on a floating rate debt

instrument

7

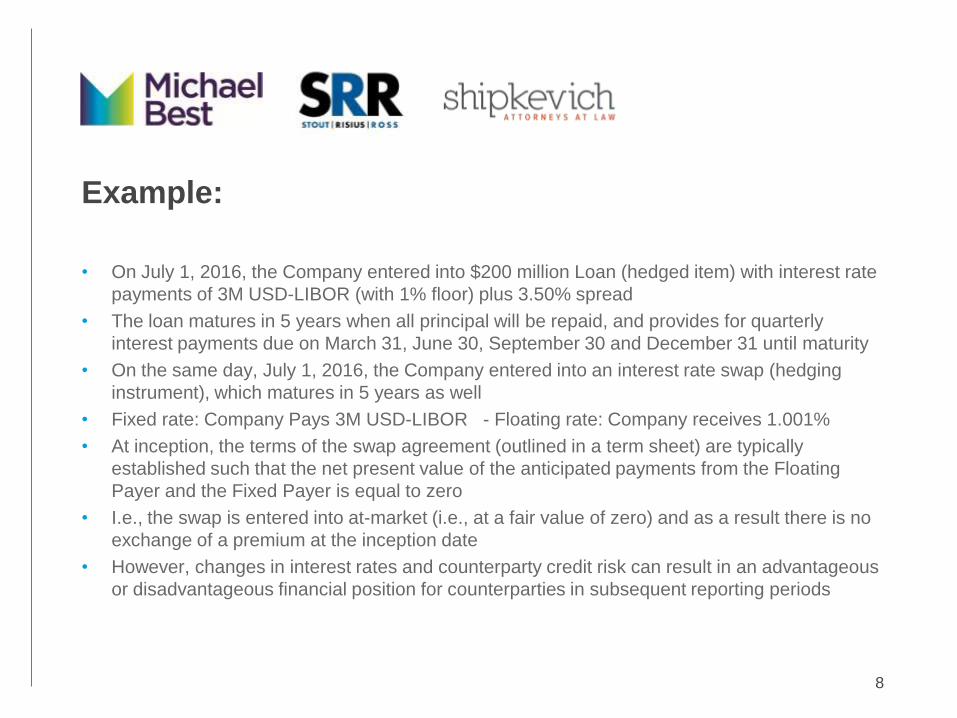

Example:

• On July 1, 2016, the Company entered into $200 million Loan (hedged item) with interest rate

payments of 3M USD-LIBOR (with 1% floor) plus 3.50% spread

• The loan matures in 5 years when all principal will be repaid, and provides for quarterly

interest payments due on March 31, June 30, September 30 and December 31 until maturity

• On the same day, July 1, 2016, the Company entered into an interest rate swap (hedging

instrument), which matures in 5 years as well

• Fixed rate: Company Pays 3M USD-LIBOR - Floating rate: Company receives 1.001%

• At inception, the terms of the swap agreement (outlined in a term sheet) are typically

established such that the net present value of the anticipated payments from the Floating

Payer and the Fixed Payer is equal to zero

• I.e., the swap is entered into at-market (i.e., at a fair value of zero) and as a result there is no

exchange of a premium at the inception date

• However, changes in interest rates and counterparty credit risk can result in an advantageous

or disadvantageous financial position for counterparties in subsequent reporting periods

8

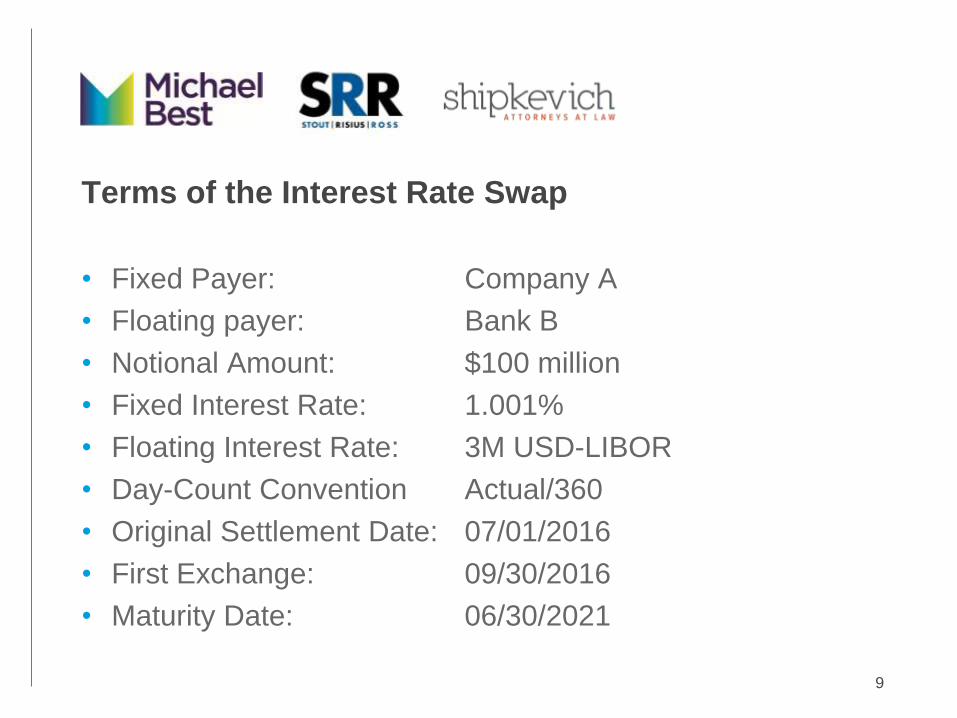

Terms of the Interest Rate Swap

• Fixed Payer: Company A

• Floating payer: Bank B

• Notional Amount: $100 million

• Fixed Interest Rate: 1.001%

• Floating Interest Rate: 3M USD-LIBOR

• Day-Count Convention Actual/360

• Original Settlement Date: 07/01/2016

• First Exchange: 09/30/2016

• Maturity Date: 06/30/2021

9

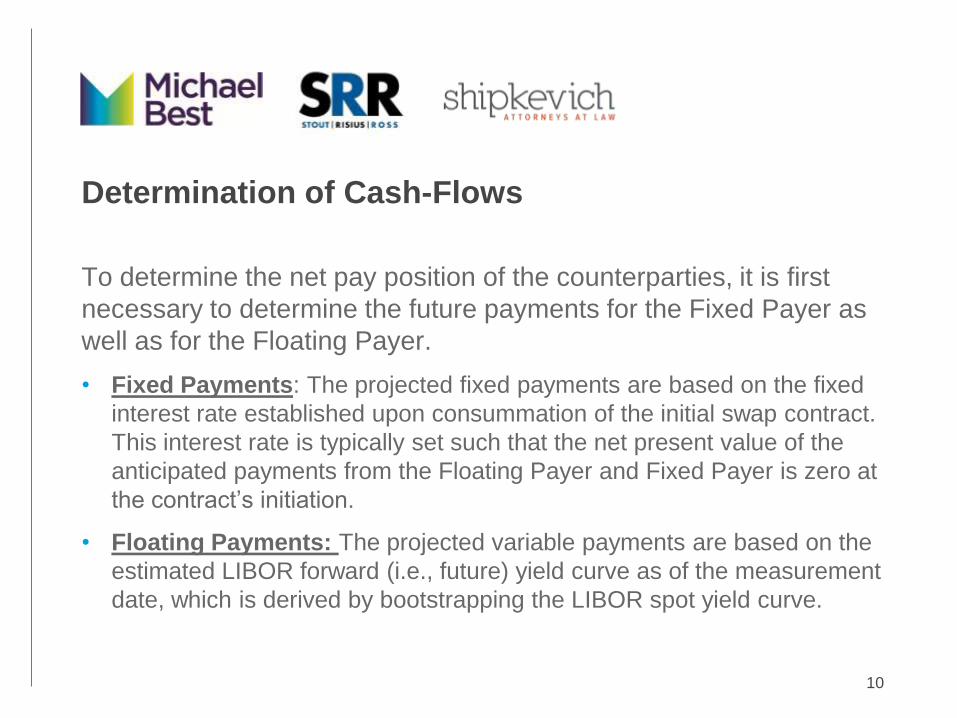

Determination of Cash-Flows

To determine the net pay position of the counterparties, it is first

necessary to determine the future payments for the Fixed Payer as

well as for the Floating Payer.

• Fixed Payments: The projected fixed payments are based on the fixed

interest rate established upon consummation of the initial swap contract.

This interest rate is typically set such that the net present value of the

anticipated payments from the Floating Payer and Fixed Payer is zero at

the contract’s initiation.

• Floating Payments: The projected variable payments are based on the

estimated LIBOR forward (i.e., future) yield curve as of the measurement

date, which is derived by bootstrapping the LIBOR spot yield curve.

10

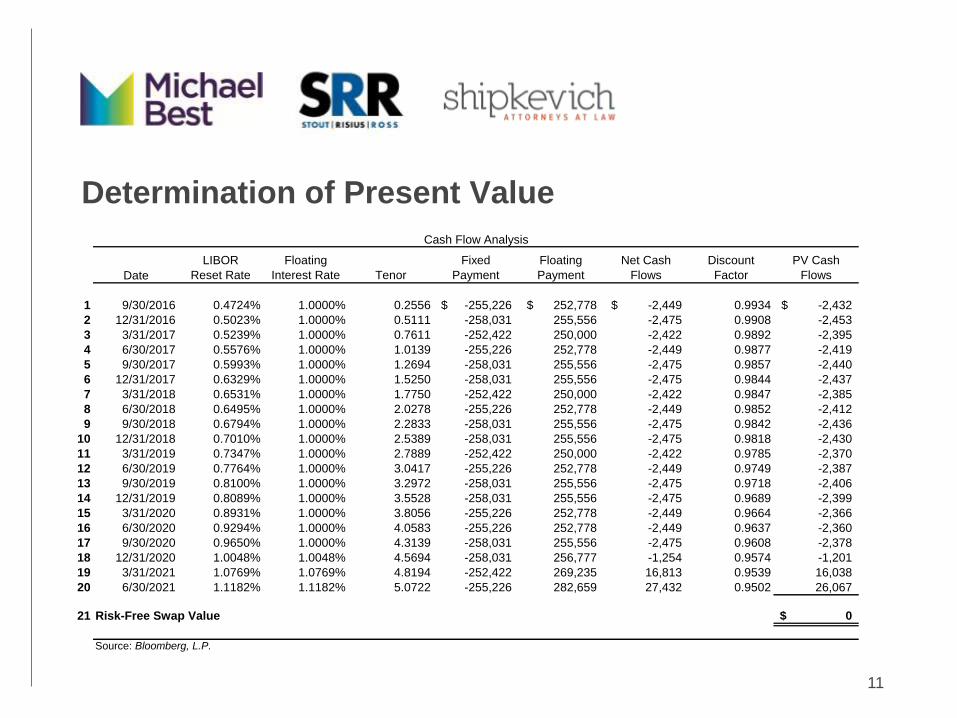

Determination of Present Value

11

Cash Flow Analysis

Date

LIBOR

Reset Rate

Floating

Interest Rate Tenor

Fixed

Payment

Floating

Payment

Net Cash

Flows

Discount

Factor

PV Cash

Flows

1 9/30/2016 0.4724% 1.0000% 0.2556 -255,226$ 252,778$ -2,449$ 0.9934 -2,432$

2 12/31/2016 0.5023% 1.0000% 0.5111 -258,031 255,556 -2,475 0.9908 -2,453

3 3/31/2017 0.5239% 1.0000% 0.7611 -252,422 250,000 -2,422 0.9892 -2,395

4 6/30/2017 0.5576% 1.0000% 1.0139 -255,226 252,778 -2,449 0.9877 -2,419

5 9/30/2017 0.5993% 1.0000% 1.2694 -258,031 255,556 -2,475 0.9857 -2,440

6 12/31/2017 0.6329% 1.0000% 1.5250 -258,031 255,556 -2,475 0.9844 -2,437

7 3/31/2018 0.6531% 1.0000% 1.7750 -252,422 250,000 -2,422 0.9847 -2,385

8 6/30/2018 0.6495% 1.0000% 2.0278 -255,226 252,778 -2,449 0.9852 -2,412

9 9/30/2018 0.6794% 1.0000% 2.2833 -258,031 255,556 -2,475 0.9842 -2,436

10 12/31/2018 0.7010% 1.0000% 2.5389 -258,031 255,556 -2,475 0.9818 -2,430

11 3/31/2019 0.7347% 1.0000% 2.7889 -252,422 250,000 -2,422 0.9785 -2,370

12 6/30/2019 0.7764% 1.0000% 3.0417 -255,226 252,778 -2,449 0.9749 -2,387

13 9/30/2019 0.8100% 1.0000% 3.2972 -258,031 255,556 -2,475 0.9718 -2,406

14 12/31/2019 0.8089% 1.0000% 3.5528 -258,031 255,556 -2,475 0.9689 -2,399

15 3/31/2020 0.8931% 1.0000% 3.8056 -255,226 252,778 -2,449 0.9664 -2,366

16 6/30/2020 0.9294% 1.0000% 4.0583 -255,226 252,778 -2,449 0.9637 -2,360

17 9/30/2020 0.9650% 1.0000% 4.3139 -258,031 255,556 -2,475 0.9608 -2,378

18 12/31/2020 1.0048% 1.0048% 4.5694 -258,031 256,777 -1,254 0.9574 -1,201

19 3/31/2021 1.0769% 1.0769% 4.8194 -252,422 269,235 16,813 0.9539 16,038

20 6/30/2021 1.1182% 1.1182% 5.0722 -255,226 282,659 27,432 0.9502 26,067

21 Risk-Free Swap Value 0$

Source: Bloomberg, L.P.

Counterparty Risk

• The fair value of the swap should also reflect the Counterparty Credit Risk (CCR),

which is the exposure to loss as a result of a counterparty failing to meets its

contractual obligations due to default

• Prior to the financial crisis OTC derivatives were valued without incorporating

CCR due to the assumption that large derivative counterparties will never default

• Derivatives can be classified as unilateral, which have only one sided CCR

(options) and bilateral derivatives (swaps, forwards, etc.)

• Bilateral derivatives are more complex, with two way counterparty risk, since both

the company and the counterparty are exposed to each other

• CCR may be mitigated through netting and offsetting positions in case of default

through ISDA master agreements

• There may also be an ISDA Credit Support Annex (CSA) that provides for posting

of collateral to cover all or a portion of the net market value of the positions to limit

the exposure

12

Counterparty Risk: Credit Value Adjustment (CVA)

Valuation Methodologies

• They are not standardized and vary amongst market participants, ranging from very simple to

very complex methodologies, driven by the sophistication and resources of the company and

also by the purpose of the analysis

• The simplest approach is to calculate the risk free value of the derivative and then repeat the

calculation by adjusting the discount rates by the credit spread of the counterparty that is in

the liability position. There is a few variations of this, either looking at each cash flow leg or

looking at the present value of the remaining cumulative position at the time of each payment

• More sophisticated approaches involve modeling and simulating interest rate volatilities and

revalue the derivative under thousands of simulations. The resulting simulations are then

aggregated to generate an expected exposure profile for each counterparty

• Collaterized positions based on the ISDA CSA are also incorporating in the analysis if

applicable

• Using hedge accounting a company is hedging for a particular risk, i.e., interest rate risk, so

one could perform the hedge effectiveness testing ignoring CVA, but will need to incorporate it

when fair value the derivatives for mark-to-market purposes

• In most cases, CVA reduces the value of the asset or liability, but not always

13

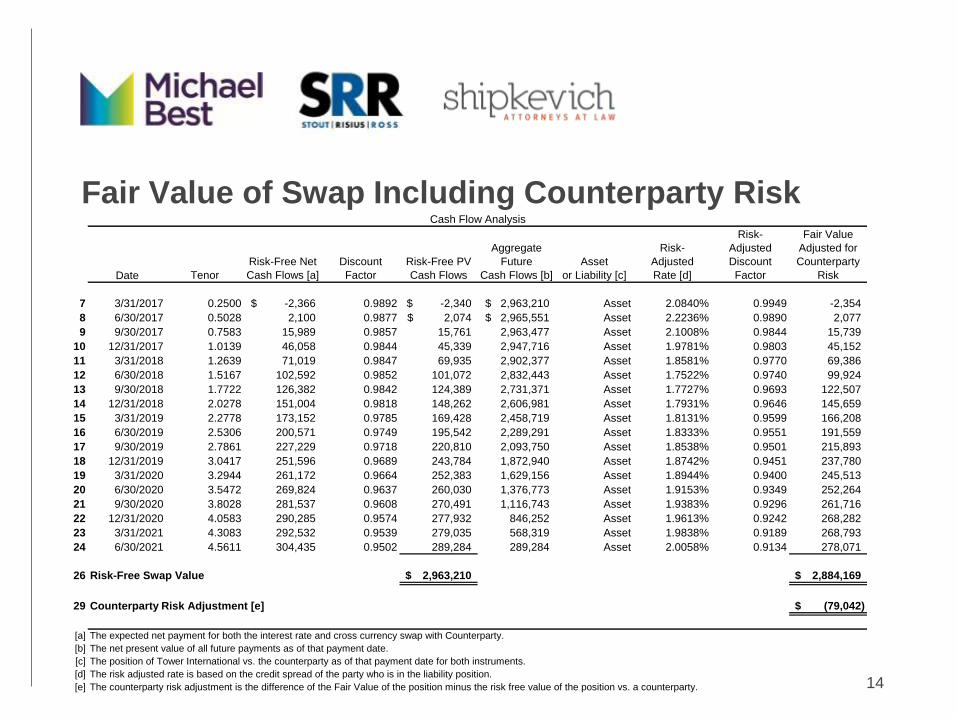

Fair Value of Swap Including Counterparty Risk

Value

14

Cash Flow Analysis

Date Tenor

Risk-Free Net

Cash Flows [a]

Discount

Factor

Risk-Free PV

Cash Flows

Aggregate

Future

Cash Flows [b]

Asset

or Liability [c]

Risk-

Adjusted

Rate [d]

Risk-

Adjusted

Discount

Factor

Fair Value

Adjusted for

Counterparty

Risk

7 3/31/2017 0.2500 -2,366$ 0.9892 -2,340$ 2,963,210$ Asset 2.0840% 0.9949 -2,354

8 6/30/2017 0.5028 2,100 0.9877 2,074$ 2,965,551$ Asset 2.2236% 0.9890 2,077

9 9/30/2017 0.7583 15,989 0.9857 15,761 2,963,477 Asset 2.1008% 0.9844 15,739

10 12/31/2017 1.0139 46,058 0.9844 45,339 2,947,716 Asset 1.9781% 0.9803 45,152

11 3/31/2018 1.2639 71,019 0.9847 69,935 2,902,377 Asset 1.8581% 0.9770 69,386

12 6/30/2018 1.5167 102,592 0.9852 101,072 2,832,443 Asset 1.7522% 0.9740 99,924

13 9/30/2018 1.7722 126,382 0.9842 124,389 2,731,371 Asset 1.7727% 0.9693 122,507

14 12/31/2018 2.0278 151,004 0.9818 148,262 2,606,981 Asset 1.7931% 0.9646 145,659

15 3/31/2019 2.2778 173,152 0.9785 169,428 2,458,719 Asset 1.8131% 0.9599 166,208

16 6/30/2019 2.5306 200,571 0.9749 195,542 2,289,291 Asset 1.8333% 0.9551 191,559

17 9/30/2019 2.7861 227,229 0.9718 220,810 2,093,750 Asset 1.8538% 0.9501 215,893

18 12/31/2019 3.0417 251,596 0.9689 243,784 1,872,940 Asset 1.8742% 0.9451 237,780

19 3/31/2020 3.2944 261,172 0.9664 252,383 1,629,156 Asset 1.8944% 0.9400 245,513

20 6/30/2020 3.5472 269,824 0.9637 260,030 1,376,773 Asset 1.9153% 0.9349 252,264

21 9/30/2020 3.8028 281,537 0.9608 270,491 1,116,743 Asset 1.9383% 0.9296 261,716

22 12/31/2020 4.0583 290,285 0.9574 277,932 846,252 Asset 1.9613% 0.9242 268,282

23 3/31/2021 4.3083 292,532 0.9539 279,035 568,319 Asset 1.9838% 0.9189 268,793

24 6/30/2021 4.5611 304,435 0.9502 289,284 289,284 Asset 2.0058% 0.9134 278,071

26 Risk-Free Swap Value 2,963,210$ 2,884,169$

29 Counterparty Risk Adjustment [e] (79,042)$

[a] The expected net payment for both the interest rate and cross currency swap with Counterparty.

[b] The net present value of all future payments as of that payment date.

[c] The position of Tower International vs. the counterparty as of that payment date for both instruments.

[d] The risk adjusted rate is based on the credit spread of the party who is in the liability position.

[e] The counterparty risk adjustment is the difference of the Fair Value of the position minus the risk free value of the position vs. a counterparty.

Derivatives Accounting Treatment Mismatch

• When a company is using derivatives to hedge against market risk exposures,

that are not measured at fair value through the P&L, an accounting treatment

mismatch can occur

• This lead to volatility in the income statement, due to the different basis of

accounting treatment between the hedged item and the hedging instrument (a

derivative)

• Hedge accounting in dealing with this accounting mismatch. A company can

reduce this income statement volatility by adjusting the basis of accounting for the

hedging item (in a Cash flow hedge) or hedged item (in a Fair Value hedge)

• A company can apply hedge accounting if they show that the hedge relationship

has been and will be highly effective through the term of the relationship

• Highly effective does not mean 100% match, it means the changes in fair value or

cash flow of the hedged item and the derivative offset each other for the most

part. Certain amount of ineffectiveness is permissible

15

Hedge Documentation Example

• The Company designates the swap as the hedging instrument to hedge of the variability of the

interest rate payments of the floating-rate loan due to changes in the designated LIBOR

benchmark interest rate. The Company designates the changes in the 3-month USD LIBOR

swap rate in arrears as the benchmark interest rate in hedging interest rate risk

• Hedge Relationship: The hedging relationship is designated on July 1, 2016. The hedge of

the interest rate exposure in a recognized fixed-rate liability is considered a cash flow hedge

per ASC 815-20-25

• Risk Management Objective: Offset the variability of the interest rate payments of the

Company’s float-rate loan attributable to changes in the designated benchmark LIBOR

interest rate. In essence, the objective is to economically convert the Company’s float-rate

loan to fixed-rate loan

• Designated Risk Being Hedged: Variability of the quarterly interest rate payments of the

Company’s float-rate loan, due to changes in the 3-month LIBOR swap rate (“hedged risk”)

• Hedging Instrument: The interest rate swaps is designated as the hedging instrument

• Hedged Item: The Company is hedging 50% of the $200 million floating-rate notes ($100

million in total). The quarterly payments dates are March 31, June 30, September 30 and

December 31 until maturity

16

Qualify for Hedge Accounting

In order for a company to be eligible to apply for hedge accounting, three basic requirements

must be satisfied:

• At the time of designation, a formal hedge documentation of the hedge relationship must exist

that details the following:

• Risk management objective and strategy of the hedge

• The nature of the risk being hedged

• Identification of the hedge item and the hedge derivative

• Description of the methods that the effectiveness of the hedge relationship will be assessed on both

prospective and retrospective basis

• How ineffectiveness will be measured, if any

• At inception and at each reporting period after that the company must demonstrate that the

hedge relationship is expected to be highly effective on a forward looking basis (prospectively)

and has actually been effective since the designation date (retrospectively)

• Each reporting period any ineffectiveness must be recognized in the Income Statement as

profit or loss

17

Hedge Effectiveness

• Hedge effectiveness is the extent to which changes in the fair value or cash flows

of the derivative offset the changes in the fair value or cash flows of the hedged

item

• Hedge effectiveness is tested at the inception of the hedge relationship (hedge

designation date) by using a prospective hedge effectiveness test

• After inception, hedge effectiveness is tested at each reporting period by using a

retrospective test (to demonstrate that the relationship has been effective) and a

prospective test (to demonstrate that the relationship is still expected to be

effective in the future)

• Methods of hedge effectiveness testing:

• Qualitative

• Critical Terms Match method

• Short-Cut method

• Quantitative

• The Dollar Offset Method

• Regression Analysis 18

Hedge Effectiveness: Critical Terms Match method

The critical terms approach can be applied if the key terms of the hedging instrument

and that of the hedged item are the same. In other words, the changes in the fair

value and cash flow of the derivative are likely to offset those of the hedged item,

both retrospectively and prospectively. To ensure compliance with the critical terms

method the following criteria must be met:

• The notional amount of the derivative is equal to the notional amount of the

hedged item

• The maturity of the derivative equals the maturity of the hedged position

• The underlying of the derivative matches the underlying hedged risk

• The fair value of the derivative is zero at inception

• No change in counterparty credit risk

• Critical terms must be checked at each effectiveness testing date

19

Hedge Effectiveness: Shortcut Method

The shortcut method is similar to the critical-terms method but is only allowed in

limited cases involving interest rate swaps. Effectiveness is automatically assumed to

be 100% between the hedged risk and the derivative (no ineffectiveness) and there

is no need to perform effectiveness testing retrospectively or prospectively. This

saves a significant amount of time and effort. The following items must be met before

this method can be used:

• Notional amount must match between the swap and hedged item

• Fair value of the swap is zero at inception

• Fixed rate on the swap, the index used for determining the floating rate and any

spread adjustment (if any) must remain the same over the life of the swap

• No embedded options (ex. Pre-pay option)

20

Overnight Index Swap (OIS) Rate

• The valuation of interest rate swaps is based on a discount cash flow model,

where a stream of future cash flows is discounted using an appropriate discount

rate

• Prior to the financial crisis, it was common industry practice to use the LIBOR

swap curve to construct the forward yield curve that used to project the floating

rate cash flows and to also use it to discount the cash flows of the swap

• During and after the crisis, market participants start using the OIS curve for

discounting those cash flows for collateralized instruments

• The use of the OIS curve reflects the funding basis of these collateralized

instruments and is a more appropriate valuation approach. It has become the

market standard for pricing collateralized deals in a number of currencies

• The move to the use of OIS discounting for purposes of valuing derivatives

reflects move to a better valuation methodology that better considers the

economics of the instruments and the relationship of the counterparties

21

Practical Issues with OIS Rate

• Need for better integration of valuation and credit/ collateral management

• Need for using a separate curve for discounting and a separate curve for

estimating the expected floating cash flow

• The market reference swap is now using the LIBOR curve as the cash flow

forecast curves, but the OIS as the discounting curve. For the same swap

instrument, the par coupon would now be different based on the different

discounting curves

• Additional source of ineffectiveness, i.e., the use of different discount curve

between the hedged item (LIBOR) vs. the derivative (OIS)

• Change in valuation methodology may trigger de-designation and re-designation

of the hedging relationship

22

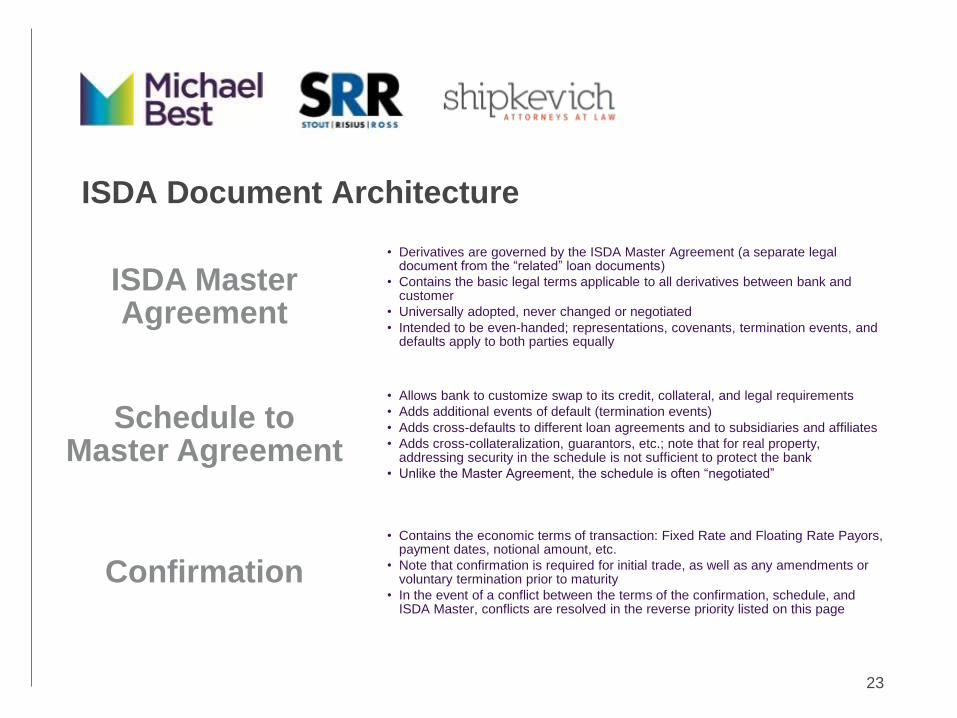

ISDA Document Architecture

23

• Derivatives are governed by the ISDA Master Agreement (a separate legal document from the “related” loan documents)

• Contains the basic legal terms applicable to all derivatives between bank and customer

• Universally adopted, never changed or negotiated

• Intended to be even-handed; representations, covenants, termination events, and defaults apply to both parties equally

ISDA Master Agreement

• Allows bank to customize swap to its credit, collateral, and legal requirements

• Adds additional events of default (termination events)

• Adds cross-defaults to different loan agreements and to subsidiaries and affiliates

• Adds cross-collateralization, guarantors, etc.; note that for real property, addressing security in the schedule is not sufficient to protect the bank

• Unlike the Master Agreement, the schedule is often “negotiated”

Schedule to Master Agreement

• Contains the economic terms of transaction: Fixed Rate and Floating Rate Payors, payment dates, notional amount, etc.

• Note that confirmation is required for initial trade, as well as any amendments or voluntary termination prior to maturity

• In the event of a conflict between the terms of the confirmation, schedule, and ISDA Master, conflicts are resolved in the reverse priority listed on this page

Confirmation

Regulatory Overview

• Dodd-Frank imposes new regulations on “Swaps,” a previously

unregulated area

• Registered “Swap Dealers” are subject to “business conduct”

rules, most of which do not apply to non-Swap Dealers

• Counterparty Verification (ECP and non-Special Entity status)

• Risk Disclosures (of the material risks and characteristics of swaps)

• Notification of right to clear, daily mark, etc.

• Special requirements for dealing with Special Entities

• Some rules apply to everyone

• Only “Eligible Contract Participants” can enter into swaps

• Recordkeeping and reporting requirements – typically dealer complies

• Clearing; however “small” banks and commercial end-users (i.e. bank

customers) usually qualify for an exception.

24

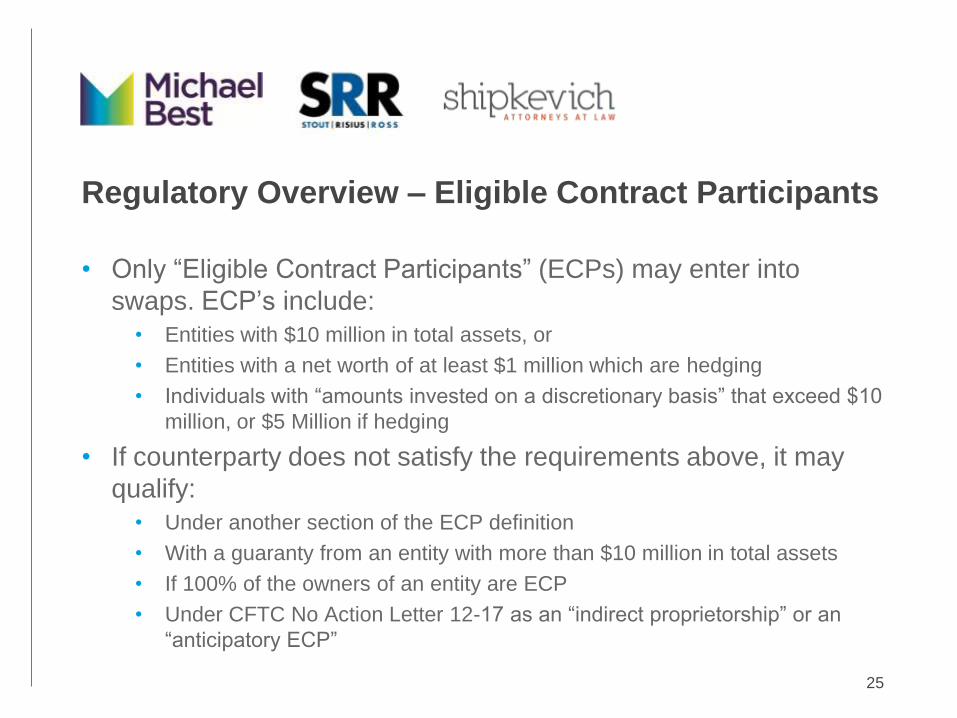

Regulatory Overview – Eligible Contract Participants

• Only “Eligible Contract Participants” (ECPs) may enter into

swaps. ECP’s include:

• Entities with $10 million in total assets, or

• Entities with a net worth of at least $1 million which are hedging

• Individuals with “amounts invested on a discretionary basis” that exceed $10

million, or $5 Million if hedging

• If counterparty does not satisfy the requirements above, it may

qualify:

• Under another section of the ECP definition

• With a guaranty from an entity with more than $10 million in total assets

• If 100% of the owners of an entity are ECP

• Under CFTC No Action Letter 12-17 as an “indirect proprietorship” or an

“anticipatory ECP”

25

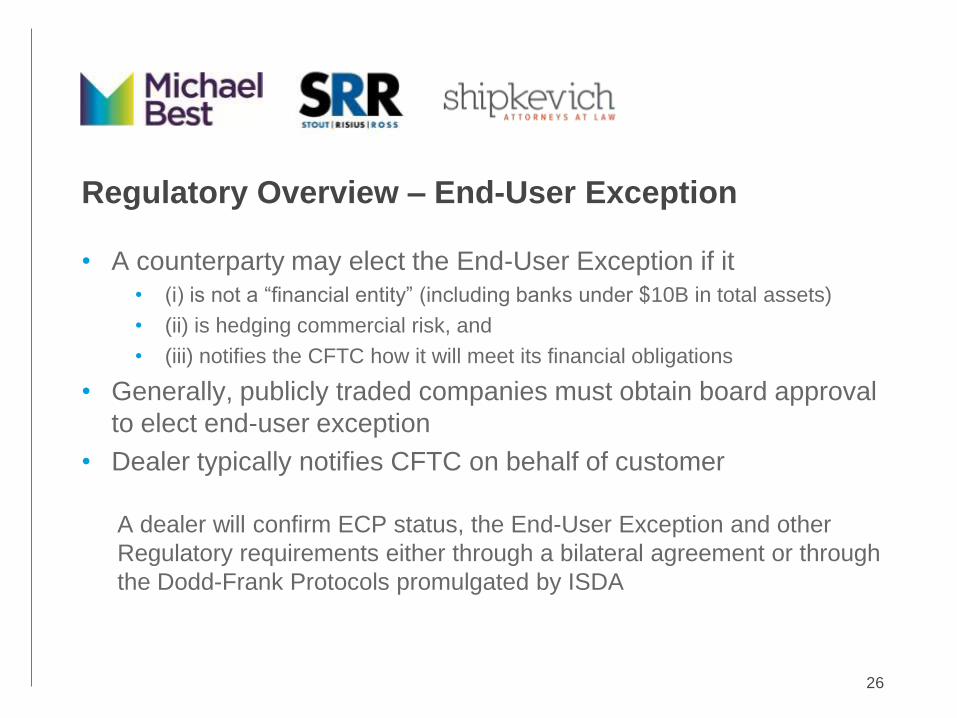

Regulatory Overview – End-User Exception

26

• A counterparty may elect the End-User Exception if it

• (i) is not a “financial entity” (including banks under $10B in total assets)

• (ii) is hedging commercial risk, and

• (iii) notifies the CFTC how it will meet its financial obligations

• Generally, publicly traded companies must obtain board approval

to elect end-user exception

• Dealer typically notifies CFTC on behalf of customer

A dealer will confirm ECP status, the End-User Exception and other

Regulatory requirements either through a bilateral agreement or through

the Dodd-Frank Protocols promulgated by ISDA

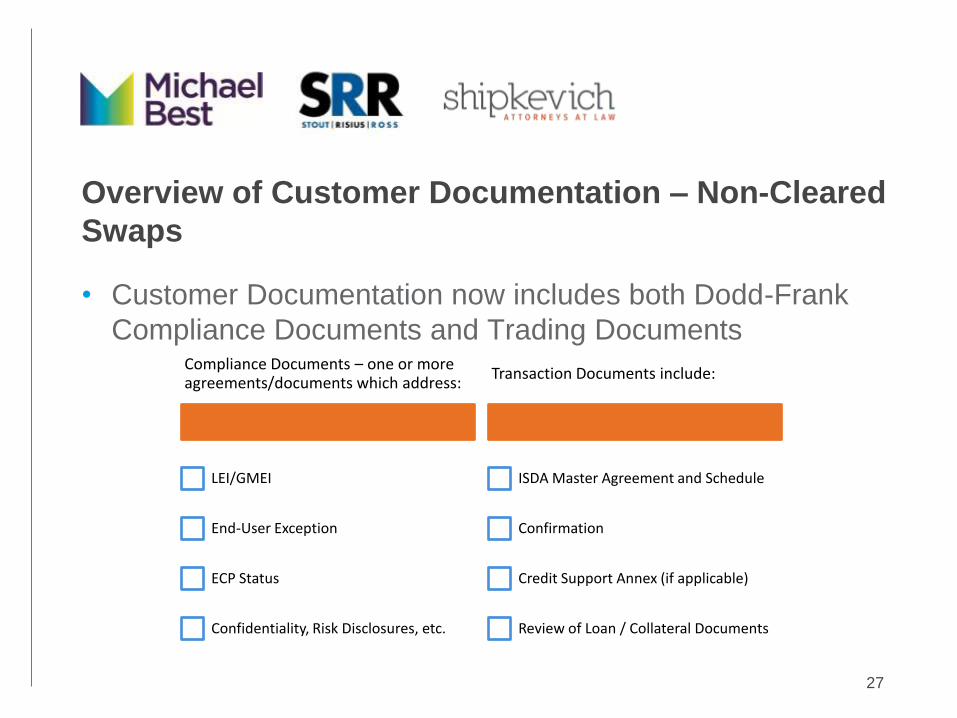

Overview of Customer Documentation – Non-Cleared

Swaps

• Customer Documentation now includes both Dodd-Frank

Compliance Documents and Trading Documents

27

Compliance Documents – one or more agreements/documents which address:

LEI/GMEI

End-User Exception

ECP Status

Confidentiality, Risk Disclosures, etc.

Transaction Documents include:

ISDA Master Agreement and Schedule

Confirmation

Credit Support Annex (if applicable)

Review of Loan / Collateral Documents

Coordinating Loan Documents with the ISDA Master

Agreement

• Key Loan Documents to Coordinate:

• Promissory Note

• Loan Agreement

• Security/Pledge Agreements

• Mortgage/Deed of Trust

• Guaranties

• Collateral Assignment of Swap

• Authorizing Resolutions

28

Loan Documents – Coordinating Financial Terms

• Confirm Floating Rate on loan and swap is based on the same index (i.e.,

one month LIBOR which resets two business days before the 1st day of each

calendar month)

• Confirm swap payment dates and interest payment dates are the same

• Confirm treatment of negative interest rates/zero rate floor is the same in

loan and swap documents

• Confirm notional and principal amounts match, and amortization is the same

• Obligation to make loan and swap payments should be independent of each

other

• Confirm prepayment language does not preclude or conflict with early

termination payments on swap

• Generally, swap should mature before or contemporaneously with loan

maturity to avoid credit and documentation risk of extending beyond loan

maturity

29

Loan Agreement Terms – Covenants

• Negative Covenants – permit or prohibit swaps as

appropriate in the following covenants:

• Indebtedness

• Liens

• Loans

• Investments

• Hedging – this may restrict hedging generally or limit changes to

existing swaps

• Affirmative Covenants – A specific hedging requirement is

permitted, but tying to a specific lender may violate anti-

tying rules

30

Loan Agreement Terms – Default, Payoff and

Termination

• Events of Default • Bankruptcy

• Cross-default to ISDA Documents

• Failure to maintain hedge

• Other typical loan defaults

• Acceleration – make sure acceleration language does not include swap,

including in the event of automatic loan acceleration resulting from

bankruptcy

• Payoff and Default Letters: Consider swaps when drafting, and avoid “all

obligations” language which might inadvertently include the swap

• Termination/Prepayment Mechanics: In the event of a default, the ISDA

termination mechanics are very specific and easy to get wrong;

experienced swap counsel in this instance is an absolute must

31

Loan Agreement Terms – Miscellaneous

• Definitions:

• Hedging/swap/rate management definitions

• “Obligations” and “Loan Documents” – Consider whether hedging should be included and

impact on cross-default, acceleration, and payoff

• Conditions Precedent – Ok to require swap and general swap terms, but do not

tie to lender (i.e., “counterparty reasonably acceptable to Lender”)

• Waterfall/application of proceeds – if there is a waterfall for application of

proceeds upon a default, consider where swap obligations (i.e., early termination

payments) should fall. Usually pari passu with loan principal

• Notice Requirements – On agented facilities, a notice requirement to agent is

common. The specific notice requirements vary, so it is important to closely

review and tailor the notice as required by the loan agreement

• Voting Rights – Consider whether a swap provider who is not a lender has voting

rights and how, if at all, swap impact voting percentages. Interests of swap

providers and lenders may not always be aligned

32

Loan Agreement Terms – Security

• Most lenders expect that the loan collateral will also secure the swap. This requires a thoughtful analysis of

collateral documents. A failure to do this can result in incomplete rights in a default/termination scenario.

• For personal property, source of security interest may be in a loan and security agreement, stand-alone

security agreement, pledge agreement, collateral assignment or similar document, or in a granting clause

contained in the ISDA Schedule itself.

• Generally, a security interest in personal property is perfected by filing a UCC financing statement, but in

certain cases (i.e., securities) it may be perfected by possession or control. This is important to understand

and coordinate with loan counsel

• For real estate collateral, swap obligations must be specifically described in the recorded mortgage or deed of

trust:

• Drafting trap – Use “all obligations and liabilities” in connection with swap rather than amounts “due and

payable,” since the latter does not recognize the indeterminate and contingent nature of early termination

payments.

• Swap endorsements to loan policy – Consider coverage and cost.

• Special care must be taken if the lienholder and swap provider are not the same (i.e., bank provides the loan

but a bank affiliate provides the swap)

• State law must be reviewed where the real estate is located, as many states have special requirements, such

as (i) mortgage registration tax, or (ii) requirement that mortgage/DOT state maximum secured amount.

33

Swap Guaranties

• Post-Dodd-Frank, swap guaranties have become more complicated

• A guaranty of a swap is a “Swap” under Dodd-Frank, so only an Eligible

Contract Participant may guaranty a swap; this applies to any new and

amended swaps

• Bank must confirm ECP status; if a loan guarantor does not qualify, often

the swap must be re-reviewed from a credit standpoint

• Swap guaranties must exclude swaps which are entered into at a time

when the guarantor is not an ECP

• ISDA published “exclusionary terms” which can be incorporated into loan

documents and guaranties to exclude swaps for non-eligible guarantors

• When entering into a new or amended swap, banks must consider old

loan guaranties: formerly well-drafted guaranties covering “all

obligations” are now a potential trap

34

Conclusion

1. Conclusion

2. Questions

3. Thank You!

35

Who We Are

36

Alexander P. Fraser

Partner

Michael Best

T. 414.347.4757

Felix Shipkevich

Principal

Shipkevich PLLC

T. 212.252.3003

Harris I. Antoniades

Managing Director, CFA, FRM

Stour Risius Ross, Inc.

T. 310.601.2565