Embed Size (px)

Citation preview

SWEET CORN REGULAR ANALYSISYEAR TO 04/10/2014

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

2

1. Market Overview

2. Demographics

3. Retail Health Situation by State

Agenda

This analysis is part of a vegetable consumer purchase data project funded by HAL using the vegetable levy and matched funds from the Australian Government.

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

4

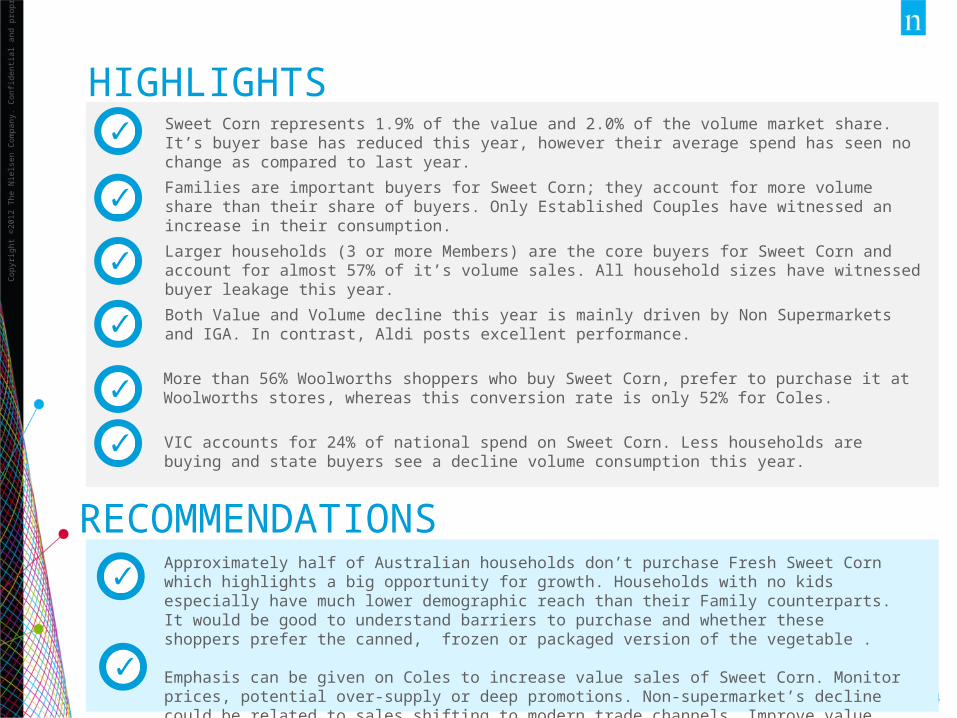

HIGHLIGHTS

RECOMMENDATIONSApproximately half of Australian households don’t purchase Fresh Sweet Corn which highlights a big opportunity for growth. Households with no kids especially have much lower demographic reach than their Family counterparts. It would be good to understand barriers to purchase and whether these shoppers prefer the canned, frozen or packaged version of the vegetable .

Emphasis can be given on Coles to increase value sales of Sweet Corn. Monitor prices, potential over-supply or deep promotions. Non-supermarket’s decline could be related to sales shifting to modern trade channels. Improve value proposition in Green Grocers to remain competitive.

Sweet Corn represents 1.9% of the value and 2.0% of the volume market share. It’s buyer base has reduced this year, however their average spend has seen no change as compared to last year.

Families are important buyers for Sweet Corn; they account for more volume share than their share of buyers. Only Established Couples have witnessed an increase in their consumption.

Larger households (3 or more Members) are the core buyers for Sweet Corn and account for almost 57% of it’s volume sales. All household sizes have witnessed buyer leakage this year.

Both Value and Volume decline this year is mainly driven by Non Supermarkets and IGA. In contrast, Aldi posts excellent performance.

More than 56% Woolworths shoppers who buy Sweet Corn, prefer to purchase it at Woolworths stores, whereas this conversion rate is only 52% for Coles.

VIC accounts for 24% of national spend on Sweet Corn. Less households are buying and state buyers see a decline volume consumption this year.

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

5Copy

right

© 2

014

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

Market OverviewSweet Corn

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

6

Share of Market VolumeOver Total VegetablesAustralia

Share of Market ValueOver Total VegetablesAustralia

Source: Nielsen Homescan

Last Year This Year

22.0% 21.9%

23.0% 22.5%

10.5% 10.9%

11.0% 10.7%

10.4% 10.1%

5.5% 5.4%

5.6% 5.8%

4.6% 5.2%3.1% 3.2%2.1% 2.3%2.0% 2.0%

Last Year This Year

38.3% 38.9%

12.1% 11.2%

4.8% 4.5%

13.9% 14.6%

4.4% 3.9%3.8% 4.2%3.0% 3.1%2.3% 2.5%7.9% 7.6%7.5% 7.4%

2.1% 1.9%

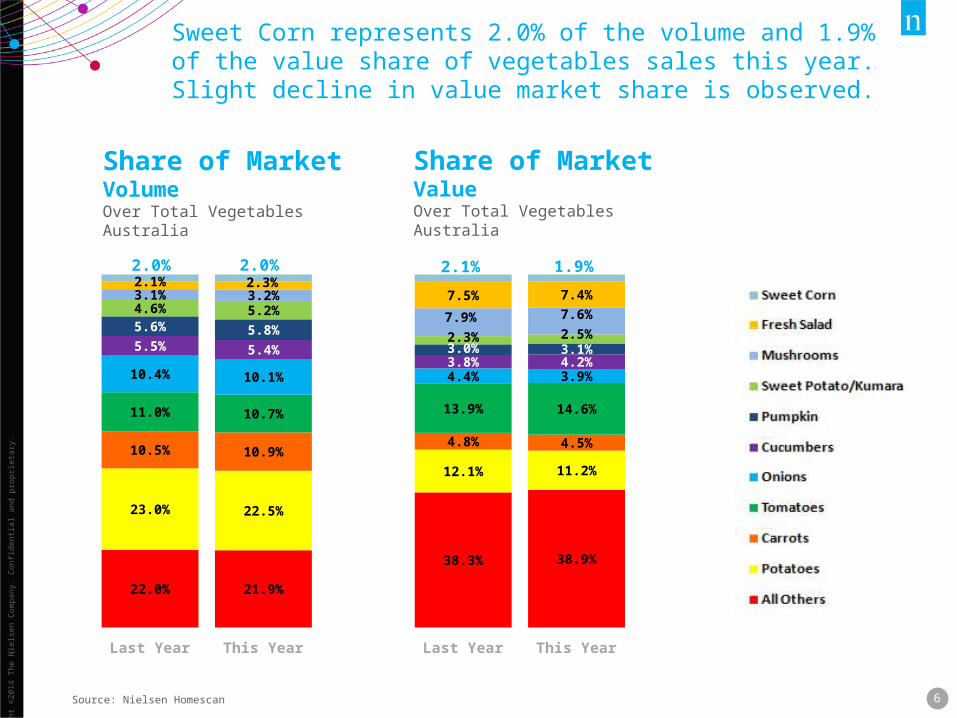

Sweet Corn represents 2.0% of the volume and 1.9% of the value share of vegetables sales this year. Slight decline in value market share is observed.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

7

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

357.9

13.7 18.0 13.045.4

13.9 19.5

380.9

13.7 18.2 14.944.8

15.3 21.9

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

89.4

3.39.9 6.4

21.6

6.4 5.3

88.2

3.210.2 7.1

20.96.7 5.1

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

99.6

55.2

94.4

64.2

95.1

76.9 77.2

99.7

53.6

94.3

64.9

94.6

76.2 76.4

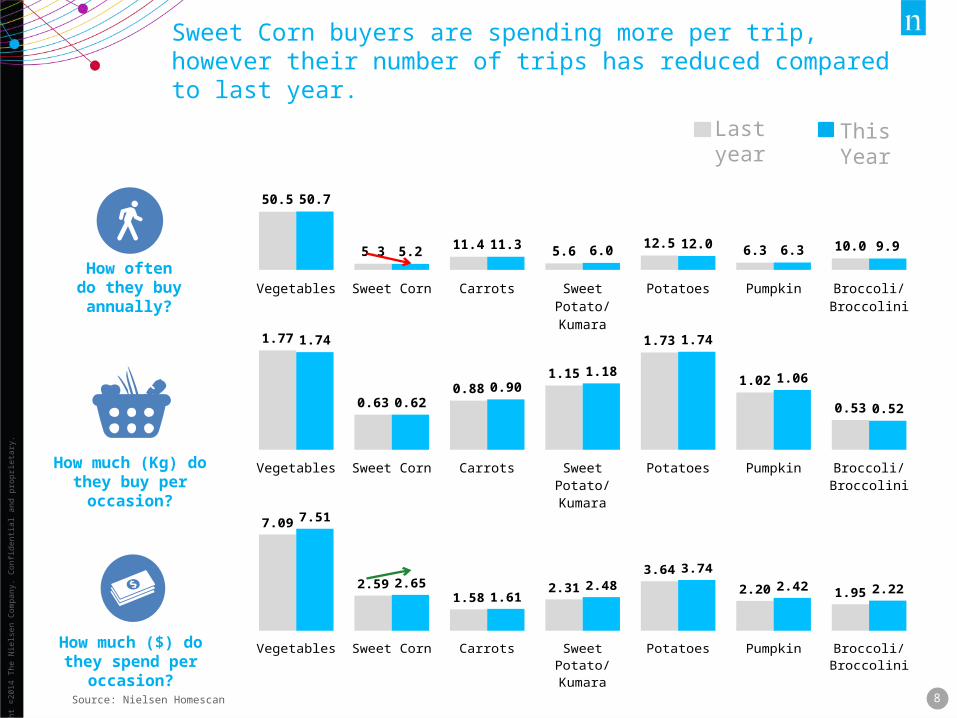

How many Households buy

annually?

How much (Kg) do they buy per year?

How much ($) do they spend per year?

Source: Nielsen Homescan

This YearLast year

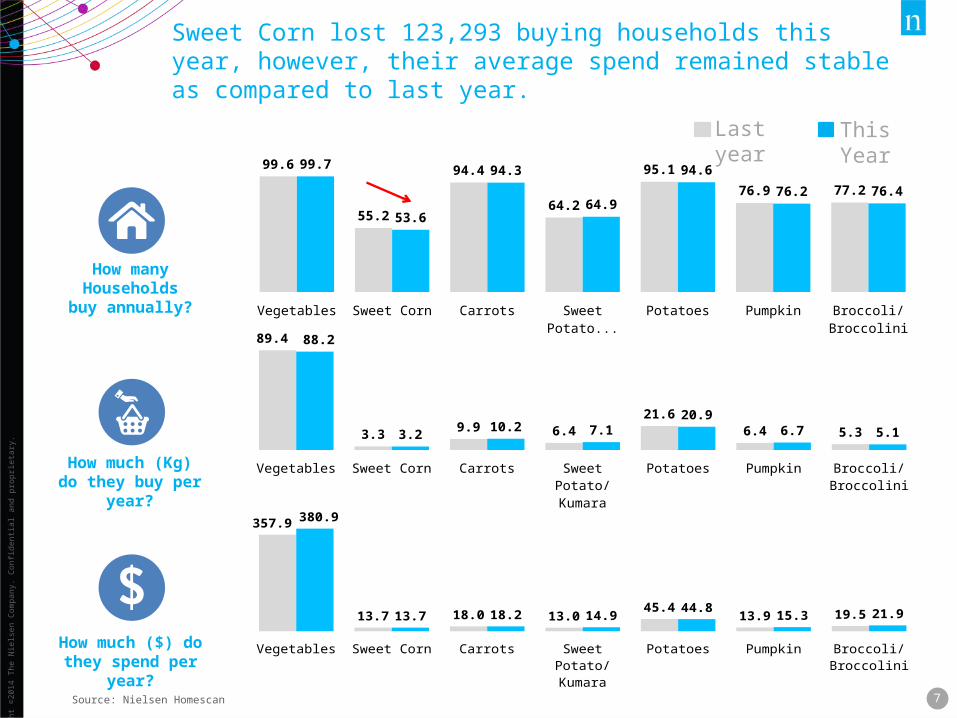

Sweet Corn lost 123,293 buying households this year, however, their average spend remained stable as compared to last year.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

8

How much ($) do they spend per occasion?

How much (Kg) do they buy per occasion?

How often do they buy annually?

Source: Nielsen Homescan

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

50.5

5.311.4

5.612.5

6.3 10.0

50.7

5.211.3 6.0

12.0 6.3 9.9

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

1.77

0.630.88

1.15

1.73

1.02

0.53

1.74

0.620.90

1.18

1.74

1.06

0.52

Vegetables Sweet Corn Carrots Sweet Potato/Ku-

mara

Potatoes Pumpkin Broccoli/Broccol-ini

7.09

2.591.58

2.31

3.64

2.20 1.95

7.51

2.651.61

2.48

3.74

2.42 2.22

This YearLast year

Sweet Corn buyers are spending more per trip, however their number of trips has reduced compared to last year.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

9Source: Nielsen Homescan

4 W

/E 0

3/11

/201

2

4 W

/E 0

1/12

/201

2

4 W

/E 2

9/12

/201

2

4 W

/E 2

6/01

/201

3

4 W

/E 2

3/02

/201

3

4 W

/E 2

3/03

/201

3

4 W

/E 2

0/04

/201

3

4 W

/E 1

8/05

/201

3

4 W

/E 1

5/06

/201

3

4 W

/E 1

3/07

/201

3

4 W

/E 1

0/08

/201

3

4 W

/E 0

7/09

/201

3

4 W

/E 0

5/10

/201

3

4 W

/E 0

2/11

/201

3

4 W

/E 3

0/11

/201

3

4 W

/E 2

8/12

/201

3

4 W

/E 2

5/01

/201

4

4 W

/E 2

2/02

/201

4

4 W

/E 2

2/03

/201

4

4 W

/E 1

9/04

/201

4

4 W

/E 1

7/05

/201

4

4 W

/E 1

4/06

/201

4

4 W

/E 1

2/07

/201

4

4 W

/E 0

9/08

/201

4

4 W

/E 0

6/09

/201

4

4 W

/E 0

4/10

/201

4

15.2 14.5 14.1

17.816.2 16.3

17.5

14.8

17.516.0

17.9

15.317.4

15.7

12.5 12.915.0

16.918.7 19.3

17.9

13.9 14.7

12.0

15.4 14.9

0.9 0.9 0.8

0.9 1.0 0.9

0.8

0.90.8

0.8

0.9

0.8

0.9 0.9

0.8

0.90.8

1.01.0 1.0

0.80.8 0.8

0.8

0.9

0.8

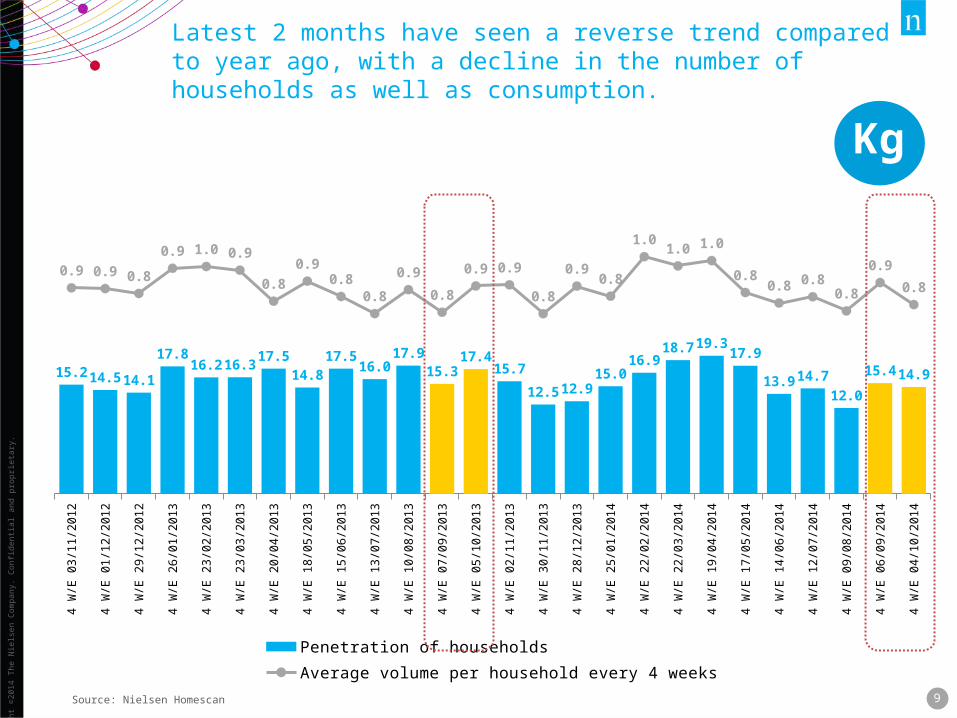

Penetration of households Average volume per household every 4 weeks

Kg

Latest 2 months have seen a reverse trend compared to year ago, with a decline in the number of households as well as consumption.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

10Source: Nielsen Homescan

4 W

/E 0

3/11

/201

2

4 W

/E 0

1/12

/201

2

4 W

/E 2

9/12

/201

2

4 W

/E 2

6/01

/201

3

4 W

/E 2

3/02

/201

3

4 W

/E 2

3/03

/201

3

4 W

/E 2

0/04

/201

3

4 W

/E 1

8/05

/201

3

4 W

/E 1

5/06

/201

3

4 W

/E 1

3/07

/201

3

4 W

/E 1

0/08

/201

3

4 W

/E 0

7/09

/201

3

4 W

/E 0

5/10

/201

3

4 W

/E 0

2/11

/201

3

4 W

/E 3

0/11

/201

3

4 W

/E 2

8/12

/201

3

4 W

/E 2

5/01

/201

4

4 W

/E 2

2/02

/201

4

4 W

/E 2

2/03

/201

4

4 W

/E 1

9/04

/201

4

4 W

/E 1

7/05

/201

4

4 W

/E 1

4/06

/201

4

4 W

/E 1

2/07

/201

4

4 W

/E 0

9/08

/201

4

4 W

/E 0

6/09

/201

4

4 W

/E 0

4/10

/201

4

15.2 14.5 14.1

17.816.2 16.3

17.5

14.8

17.516.0

17.9

15.317.4

15.7

12.5 12.915.0

16.918.7 19.3

17.9

13.9 14.7

12.0

15.4 14.9

4.13.9

3.7

3.4 3.4 3.4 3.43.6

3.3

3.7 3.63.7

3.53.7 3.8 3.7 3.6

3.33.2 3.1

3.4

3.93.6

4.7

4.3 4.4

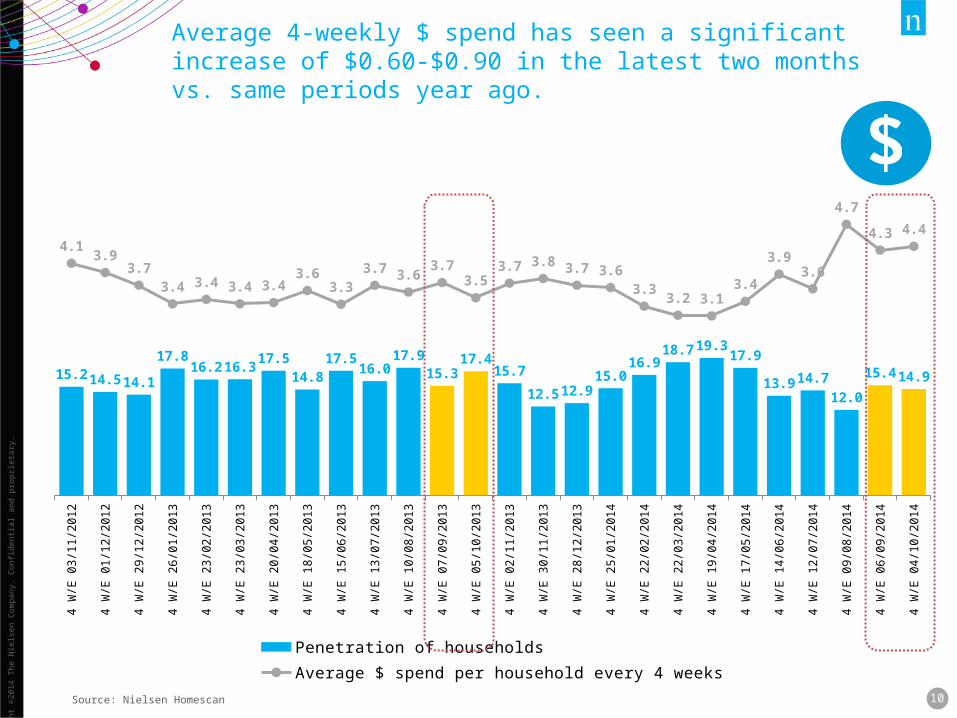

Penetration of households Average $ spend per household every 4 weeks

Average 4-weekly $ spend has seen a significant increase of $0.60-$0.90 in the latest two months vs. same periods year ago.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

11Source: Nielsen Homescan

4 W

/E 0

3/11

/201

2

4 W

/E 0

1/12

/201

2

4 W

/E 2

9/12

/201

2

4 W

/E 2

6/01

/201

3

4 W

/E 2

3/02

/201

3

4 W

/E 2

3/03

/201

3

4 W

/E 2

0/04

/201

3

4 W

/E 1

8/05

/201

3

4 W

/E 1

5/06

/201

3

4 W

/E 1

3/07

/201

3

4 W

/E 1

0/08

/201

3

4 W

/E 0

7/09

/201

3

4 W

/E 0

5/10

/201

3

4 W

/E 0

2/11

/201

3

4 W

/E 3

0/11

/201

3

4 W

/E 2

8/12

/201

3

4 W

/E 2

5/01

/201

4

4 W

/E 2

2/02

/201

4

4 W

/E 2

2/03

/201

4

4 W

/E 1

9/04

/201

4

4 W

/E 1

7/05

/201

4

4 W

/E 1

4/06

/201

4

4 W

/E 1

2/07

/201

4

4 W

/E 0

9/08

/201

4

4 W

/E 0

6/09

/201

4

4 W

/E 0

4/10

/201

4

4.1 3.9 3.73.4 3.4 3.4 3.4 3.6

3.33.7 3.6 3.7

3.53.7 3.8 3.7 3.6

3.3 3.2 3.13.4

3.93.6

4.74.3 4.4

2.91 2.77 2.752.52 2.54 2.46 2.46 2.60 2.47

2.73 2.60 2.692.51

2.70 2.77 2.77 2.76

2.35 2.27 2.282.48

2.902.62

3.363.06 3.07

1.4 1.4 1.3 1.3 1.4 1.4 1.4 1.4 1.4 1.3 1.4 1.4 1.4 1.4 1.4 1.3 1.3 1.4 1.4 1.4 1.4 1.3 1.4 1.4 1.4 1.4

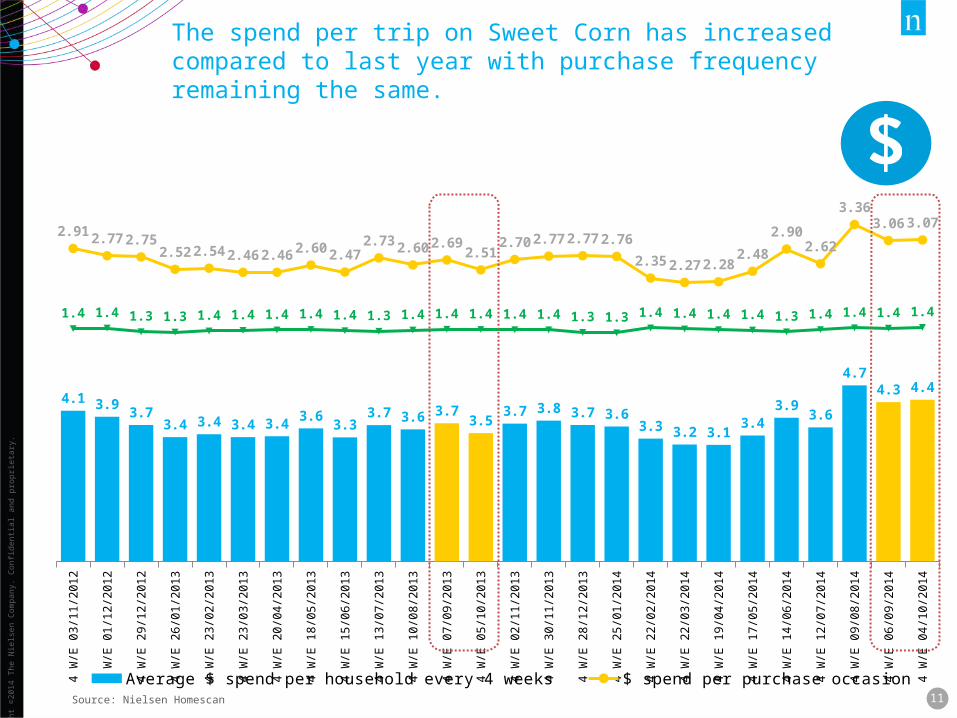

Average $ spend per household every 4 weeks $ spend per purchase occasionAverage purchase occasions every 4 weeks

The spend per trip on Sweet Corn has increased compared to last year with purchase frequency remaining the same.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

12

DemographicsSweet Corn

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

14Source: Nielsen Homescan

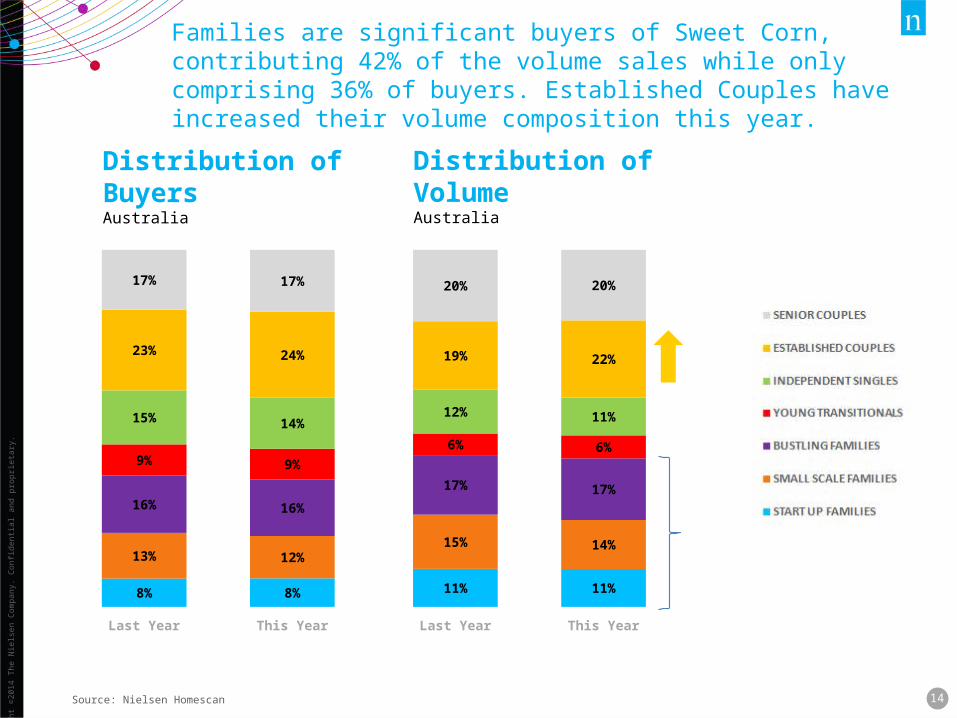

Distribution of BuyersAustralia

Distribution of VolumeAustralia

Last Year This Year

8% 8%

13% 12%

16% 16%

9% 9%

15% 14%

23% 24%

17% 17%

Last Year This Year

11% 11%

15% 14%

17% 17%

6% 6%

12% 11%

19% 22%

20% 20%

Families are significant buyers of Sweet Corn, contributing 42% of the volume sales while only comprising 36% of buyers. Established Couples have increased their volume composition this year.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

15

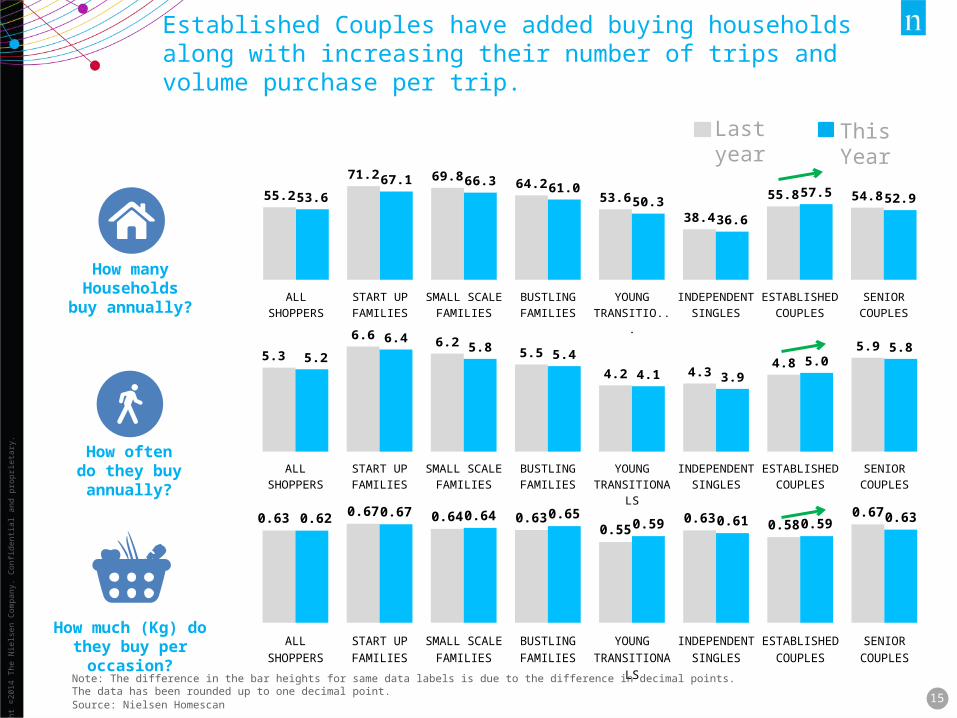

How many Households buy

annually?

How often do they buy annually?

How much (Kg) do they buy per occasion?

ALL SHOPPERS START UP FAM-ILIES

SMALL SCALE FAMILIES

BUSTLING FAMILIES

YOUNG TRANSITION-

ALS

INDEPENDENT SINGLES

ESTABLISHED COUPLES

SENIOR COUPLES

55.2

71.2 69.8 64.253.6

38.4

55.8 54.853.667.1 66.3 61.0

50.336.6

57.5 52.9

ALL SHOPPERS START UP FAM-ILIES

SMALL SCALE FAMILIES

BUSTLING FAM-ILIES

YOUNG TRANSITION-

ALS

INDEPENDENT SINGLES

ESTABLISHED COUPLES

SENIOR COUPLES

5.3

6.66.2

5.5

4.2 4.34.8

5.95.2

6.45.8

5.4

4.1 3.9

5.05.8

ALL SHOPPERS START UP FAM-ILIES

SMALL SCALE FAMILIES

BUSTLING FAM-ILIES

YOUNG TRANSITION-

ALS

INDEPENDENT SINGLES

ESTABLISHED COUPLES

SENIOR COUPLES

0.630.67 0.64 0.63

0.550.63

0.580.670.62 0.67 0.64 0.65

0.59 0.61 0.59 0.63

This YearLast year

Note: The difference in the bar heights for same data labels is due to the difference in decimal points. The data has been rounded up to one decimal point. Source: Nielsen Homescan

Established Couples have added buying households along with increasing their number of trips and volume purchase per trip.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

16Source: Nielsen Homescan

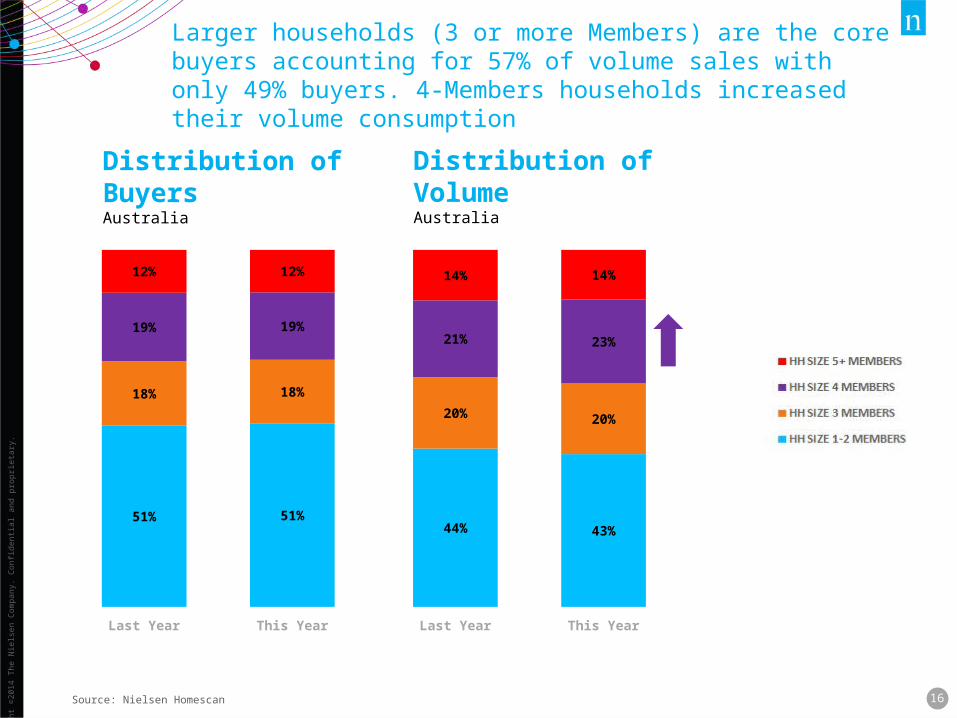

Distribution of BuyersAustralia

Distribution of VolumeAustralia

Last Year This Year

51% 51%

18% 18%

19% 19%

12% 12%

Last Year This Year

44% 43%

20% 20%

21% 23%

14% 14%

Larger households (3 or more Members) are the core buyers accounting for 57% of volume sales with only 49% buyers. 4-Members households increased their volume consumption

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

17

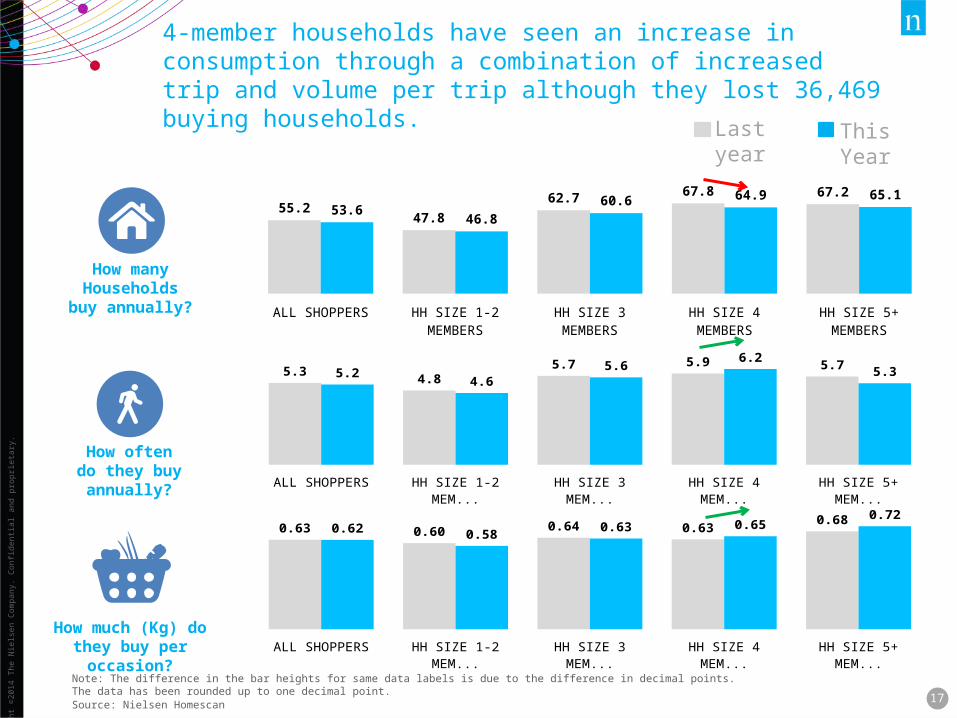

How many Households buy

annually?

How often do they buy annually?

How much (Kg) do they buy per occasion?

ALL SHOPPERS HH SIZE 1-2 MEMBERS HH SIZE 3 MEMBERS HH SIZE 4 MEMBERS HH SIZE 5+ MEMBERS

55.247.8

62.7 67.8 67.2

53.646.8

60.6 64.9 65.1

ALL SHOPPERS HH SIZE 1-2 MEMBERS HH SIZE 3 MEMBERS HH SIZE 4 MEMBERS HH SIZE 5+ MEMBERS

5.3 4.85.7 5.9 5.7

5.24.6

5.66.2

5.3

ALL SHOPPERS HH SIZE 1-2 MEMBERS HH SIZE 3 MEMBERS HH SIZE 4 MEMBERS HH SIZE 5+ MEMBERS

0.63 0.60 0.64 0.630.68

0.62 0.58 0.63 0.650.72

This YearLast year

Note: The difference in the bar heights for same data labels is due to the difference in decimal points. The data has been rounded up to one decimal point. Source: Nielsen Homescan

4-member households have seen an increase in consumption through a combination of increased trip and volume per trip although they lost 36,469 buying households.

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

18Copy

right

© 2

014

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

Retail HealthSituation by stateSweet Corn

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

19

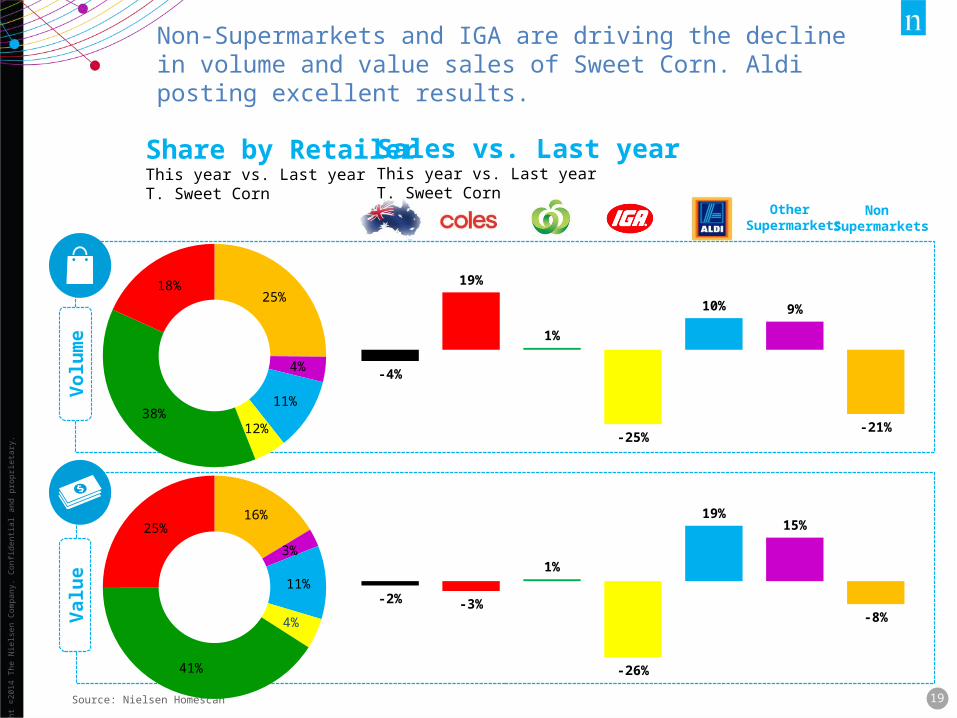

Share by RetailerThis year vs. Last yearT. Sweet Corn

Sales vs. Last yearThis year vs. Last yearT. Sweet Corn

Other Supermarkets

Non Supermarkets

Volu

me

Valu

e

Source: Nielsen Homescan

16%

3%

11%

4%

41%

25%

25%

4%

11%

12%38%

18%

-21%

9%10%

-25%

1%

19%

-4%

-8%

15%19%

-26%

1%

-3%-2%

Non-Supermarkets and IGA are driving the decline in volume and value sales of Sweet Corn. Aldi posting excellent results.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

21

Source: Nielsen Homescan Total Market: AUS Shared to: T. Fresh Frt Veg Dried Frt Nut Condition: Defined Market: AUS Defined Product: T. Fresh Frt Veg Dried Frt Nut Defined Fact: Purchase Value Defined Period: MAT TO 04/10/2014

Copyright © Page 1 of 1

Homescan isights v3.0 .Dictionary v1.5

Source: Nielsen Homescan

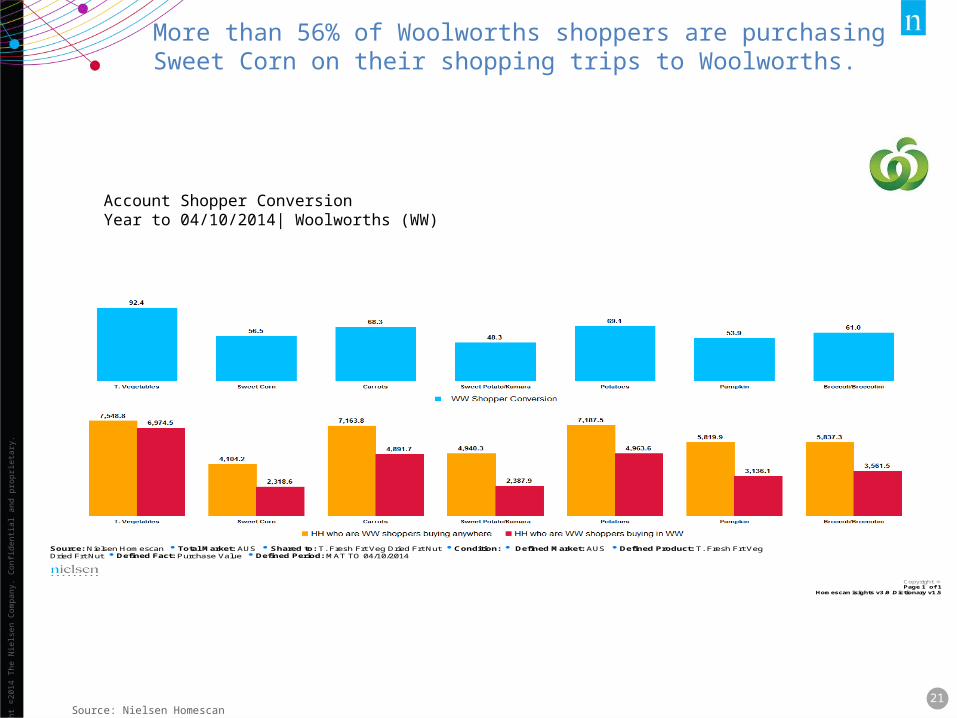

Account Shopper ConversionYear to 04/10/2014| Woolworths (WW)

More than 56% of Woolworths shoppers are purchasing Sweet Corn on their shopping trips to Woolworths.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

22

Source: Nielsen Homescan Total Market: AUS Shared to: T. Fresh Frt Veg Dried Frt Nut Condition: Defined Market: AUS Defined Product: T. Fresh Frt Veg Dried Frt Nut Defined Fact: Purchase Value Defined Period: MAT TO 04/10/2014

Copyright © Page 1 of 1

Homescan isights v3.0 .Dictionary v1.5

Source: Nielsen Homescan

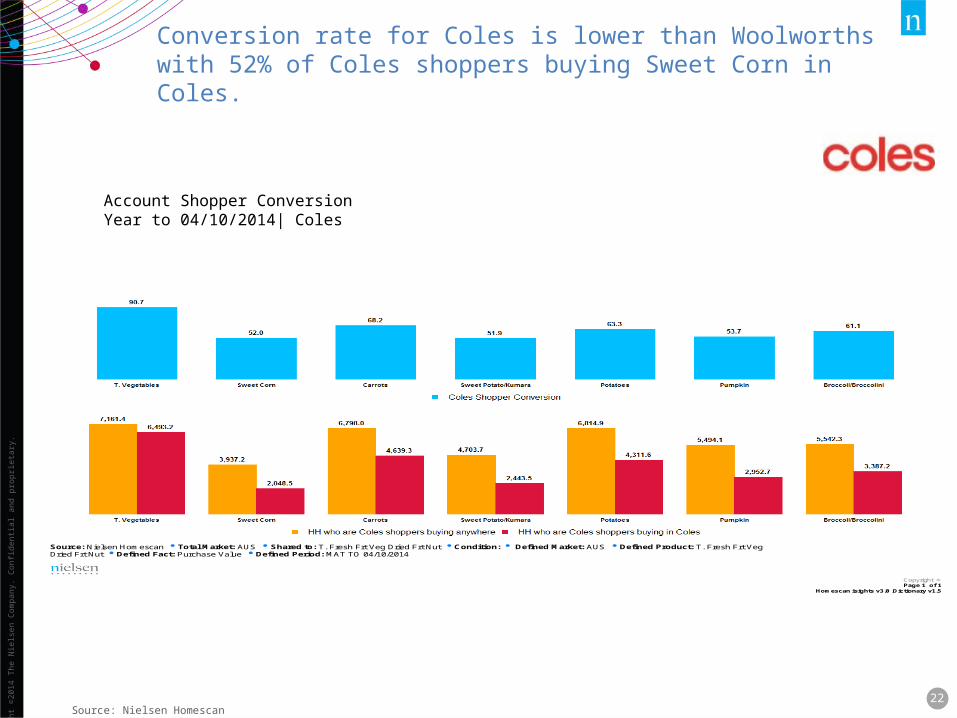

Account Shopper ConversionYear to 04/10/2014| Coles

Conversion rate for Coles is lower than Woolworths with 52% of Coles shoppers buying Sweet Corn in Coles.

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

23

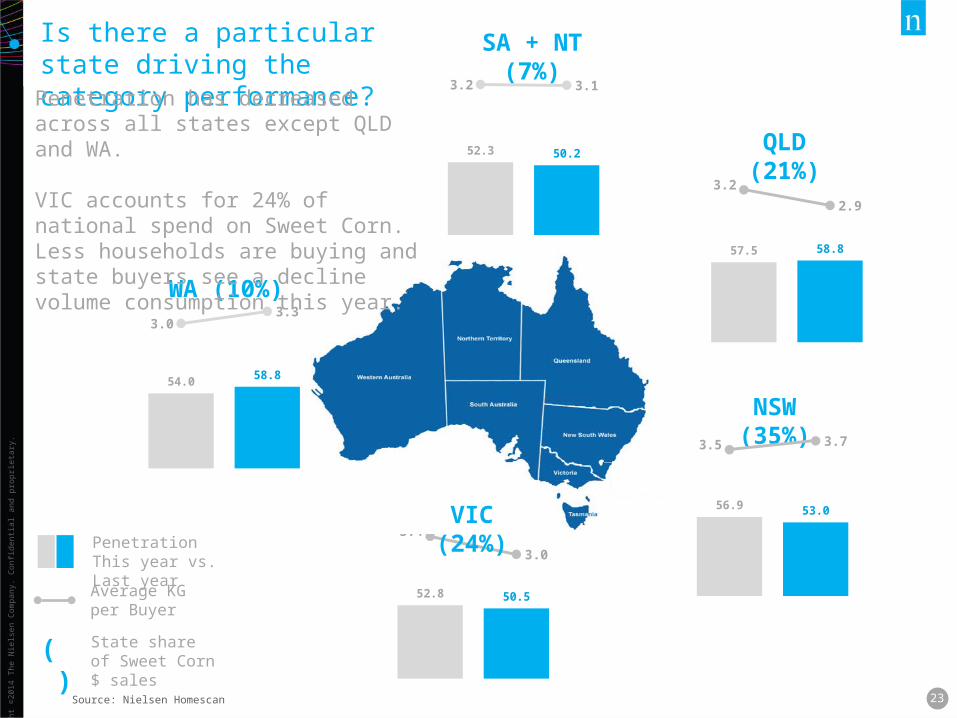

52.8 50.5

3.4

3.0

SA + NT (7%)

VIC (24%)

NSW (35%)

QLD (21%)

WA (10%)

Average KG per Buyer

Penetration This year vs. Last year

( ) State share of Sweet Corn $ sales

Is there a particular state driving the category performance?

Penetration has decreased across all states except QLD and WA.

VIC accounts for 24% of national spend on Sweet Corn. Less households are buying and state buyers see a decline volume consumption this year.

Source: Nielsen Homescan

54.0 58.8

3.03.3

52.3 50.2

3.2 3.1

57.5 58.8

3.2

2.9

56.9 53.0

3.5 3.7

THANK YOU