Embed Size (px)

Citation preview

Daniel Staib, Economic Research & Consulting Mutual insurance and takaful conference, Istanbul, 13 November 2012

Swiss Re Retakaful

2

Table of contents

1. Introduction 2. Market potential & outlook 3. Retakaful at Swiss Re

Operating model (Wakalah-Waqf) 4. Challenges in retakaful

3

2 Market potential & outlook

3

4

2 Market potential & outlook

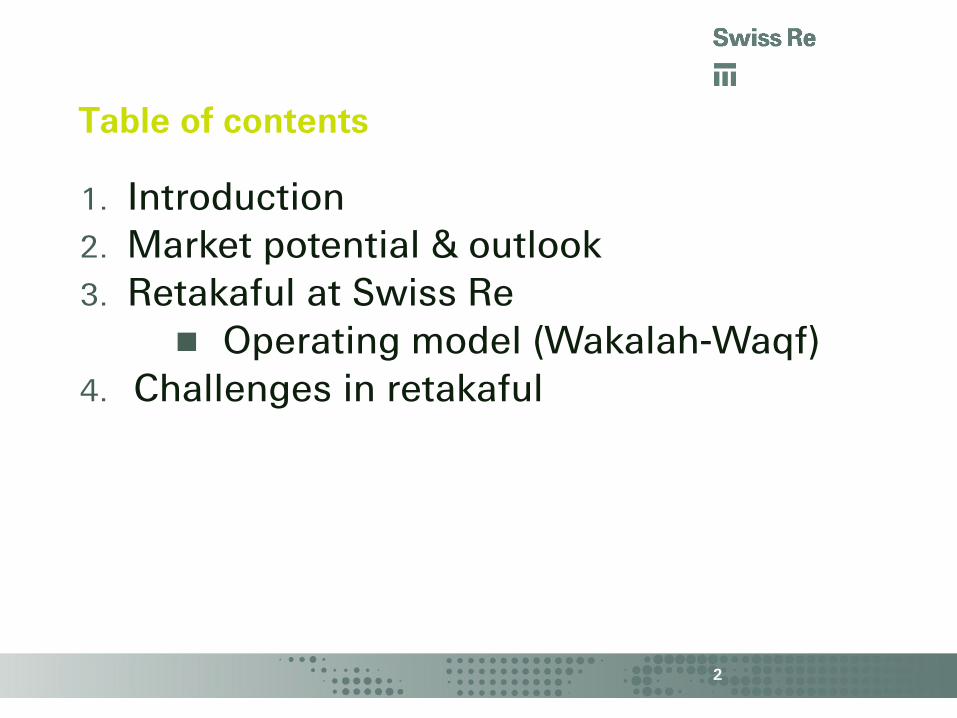

25% of world population is Muslim (1.5 bn people). In addition, Takaful is also an attractive solution to non-Muslims.

Market premium written in Muslim countries (2010): USD 73bn.

Islamic insurance premium (2010): USD 3.2 bn (takaful) + USD 4.0bn (cooperative model – KSA) + USD 5.1bn (conventional insurance within Islamic financial system): Total: USD 12.3bn.

Low level of insurance penetration compared to other emerging markets.

Population of Muslim countries are rapidly growing; favourable demographics.

Increasing Islamic consciousness.

Growth of Takaful has been exceptional over past four years (almost 30% p.a.) & is expected to continue in same way.

Until 2015 Takaful contribution could surpass USD 7bn.

5

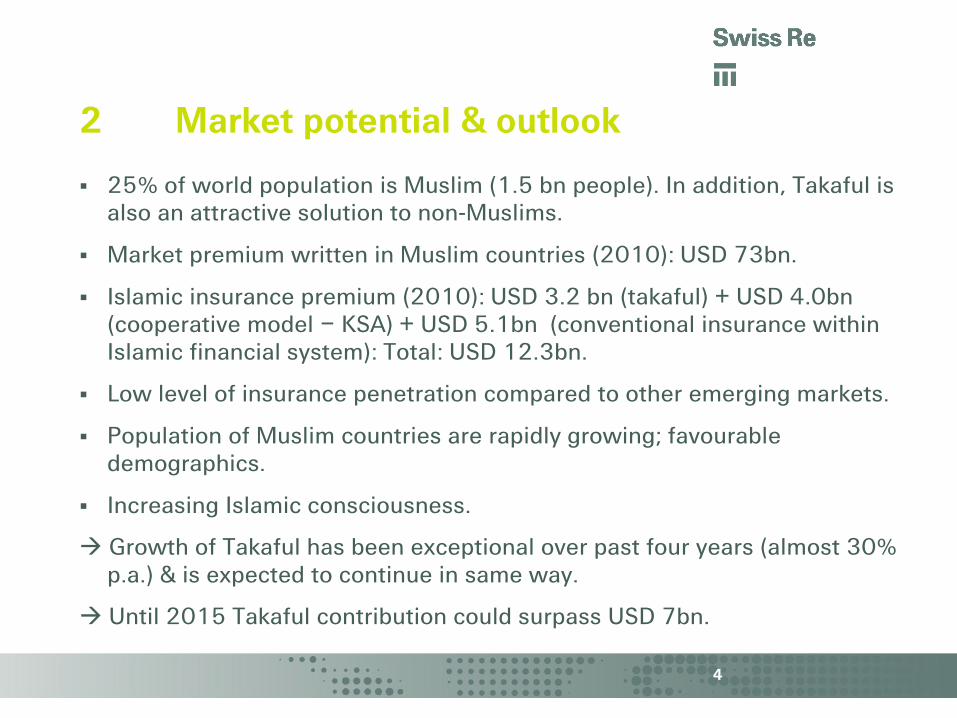

2 Takaful contributions by country 2010: USD 3.2 bn

Malaysia 31%

Saudi Arabia 12%

Sudan 9%

Other South East Asia 8%

Indonesia 13%

United Arab Emirates

12%

Bahrain 3%

Other Middle East 12% Malaysia

Saudi Arabia

Sudan

Other South EastAsia

Indonesia

United Arab Emirates

Bahrain

Other Middle East

Source: Swiss Re Economic Research & Consulting

Malaysia is leading in terms of size and development of its takaful markets

Assumptions:

Muslim countries only

Business only included if written on the basis of wakalah, mudarabah or hybrid models

6

3 Retakaful at Swiss Re

6

7

3 Retakaful at Swiss Re

SR has been offering Family (L&H) Retakaful solutions to clients in the Middle East since 2006.

As a sign of our clear commitment to Islamic insurance we have opened a dedicated Retakaful operation in Kuala Lumpur (Malaysia) in 2009 which enables Swiss Re to offer Family and General (P&C) Retakaful solutions to Takaful operators worldwide

Swiss Re Retakaful is a branch of Swiss Re Zurich and has the same rating as the parent company i.e. “A+” by S& P, “A1”by Moody’s and “A” by A.M. Best.

We are about to set up the retakaful solution for property fac. risks via Swift Re for a Takaful client in South Africa.

We are setting up a global high risk/high limit fund for facultative risks.

8

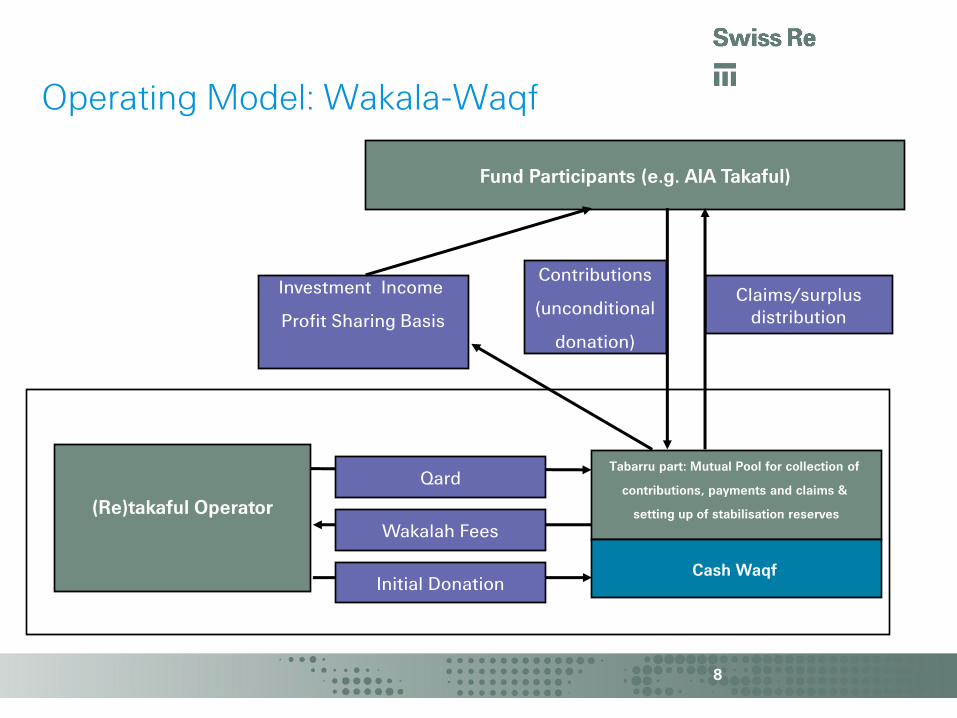

Slide 8

Fund Participants (e.g. AIA Takaful)

Contributions

(unconditional

donation)

Claims/surplus distribution

Tabarru part: Mutual Pool for collection of

contributions, payments and claims &

setting up of stabilisation reserves

(Re)takaful Operator

Investment Income

Profit Sharing Basis

Qard

Cash Waqf Initial Donation

Wakalah Fees

Operating Model: Wakala-Waqf

9

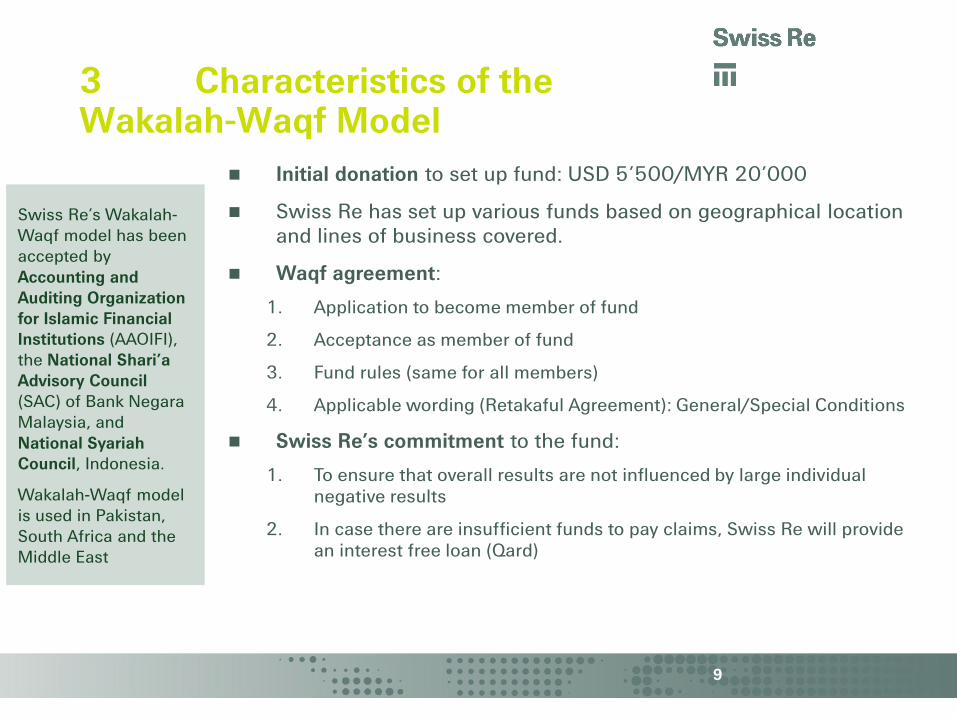

3 Characteristics of the Wakalah-Waqf Model

Initial donation to set up fund: USD 5’500/MYR 20’000

Swiss Re has set up various funds based on geographical location and lines of business covered.

Waqf agreement:

1. Application to become member of fund

2. Acceptance as member of fund

3. Fund rules (same for all members)

4. Applicable wording (Retakaful Agreement): General/Special Conditions

Swiss Re’s commitment to the fund:

1. To ensure that overall results are not influenced by large individual negative results

2. In case there are insufficient funds to pay claims, Swiss Re will provide an interest free loan (Qard)

Swiss Re’s Wakalah-Waqf model has been accepted by Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), the National Shari’a Advisory Council (SAC) of Bank Negara Malaysia, and National Syariah Council, Indonesia.

Wakalah-Waqf model is used in Pakistan, South Africa and the Middle East

10

3 Characteristics of the Wakalah-Waqf Model

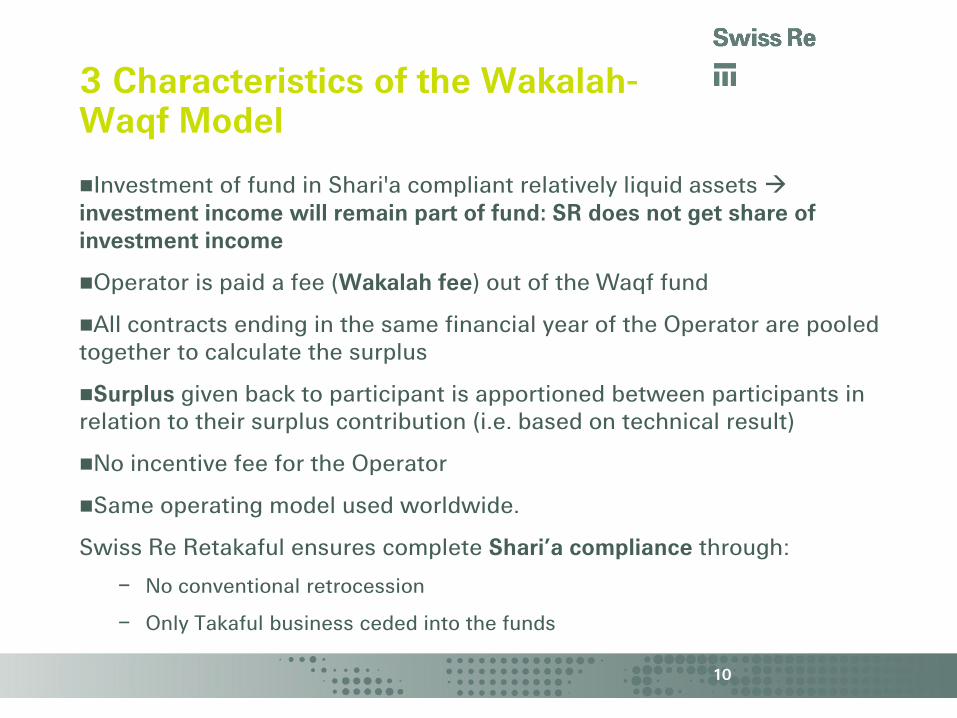

Investment of fund in Shari'a compliant relatively liquid assets investment income will remain part of fund: SR does not get share of investment income

Operator is paid a fee (Wakalah fee) out of the Waqf fund

All contracts ending in the same financial year of the Operator are pooled together to calculate the surplus

Surplus given back to participant is apportioned between participants in relation to their surplus contribution (i.e. based on technical result)

No incentive fee for the Operator

Same operating model used worldwide.

Swiss Re Retakaful ensures complete Shari’a compliance through:

– No conventional retrocession

– Only Takaful business ceded into the funds

11

4 Challenges in retakaful

11

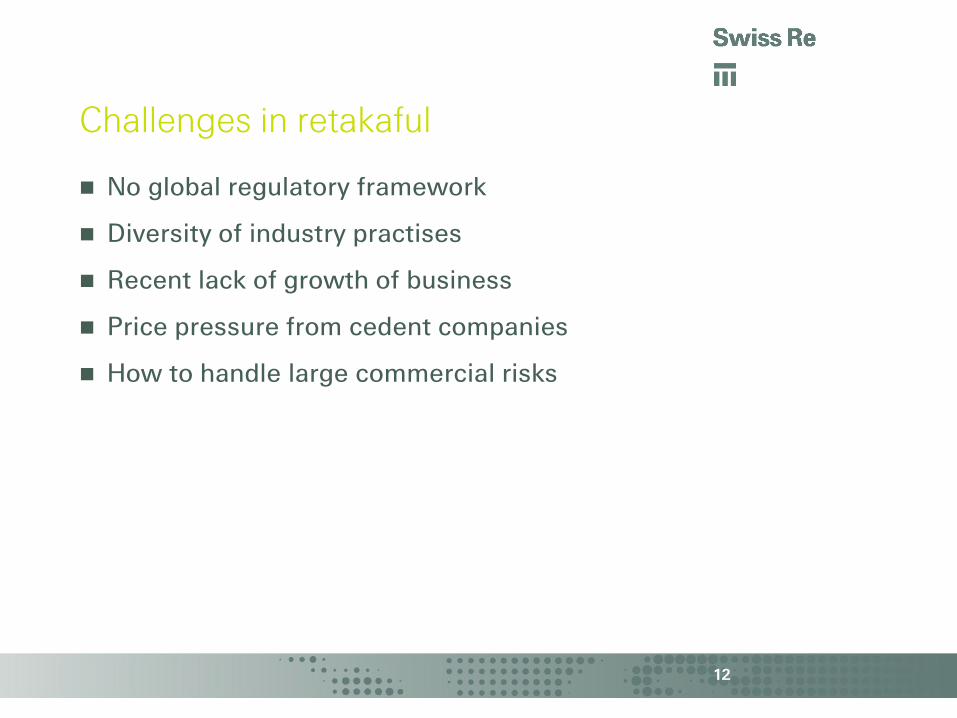

Challenges in retakaful

No global regulatory framework

Diversity of industry practises

Recent lack of growth of business

Price pressure from cedent companies

How to handle large commercial risks

12

Thank you

14

Basic Copyright Notice & Disclaimer for Swiss Re Presentations provided to External Parties

©2009 Swiss Re. All rights reserved. You are not permitted to create any modifications or derivatives of this presentation without the prior written permission of Swiss Re.

This presentation is for information purposes only and contains non-binding indications as well as personal judgment. It does not contain any recommendation, advice, solicitation, offer or commitment to effect any transaction or to conclude any legal act. Any opinions or views expressed are of the author and do not necessarily represent those of Swiss Re. Swiss Re makes no warranties or representations as to this presentation’s accuracy, completeness, timeliness or suitability for a particular purpose. Anyone shall at its own risk interpret and employ this presentation without relying on it in isolation. In no event will Swiss Re or one of its affiliates be liable for any loss or damages of any kind, including any direct, indirect or consequential damages, arising out of or in connection with the use of this presentation.