Embed Size (px)

Citation preview

See important disclosures, including any required research certifications, beginning on page 81

China Consumer Staples

What's new: We are cutting 2016-17E EPS for 9 of the 12 China

Consumer Staples companies by 2-33%. On our new numbers, the stocks

under Daiwa coverage are trading at PER discounts to international peers

(16x 2016E PER vs. 21x), despite the peers having slower EPS growth

(9% vs. 16% for packaged food companies, per Bloomberg). We believe

this disparity indicates the risk of an EPS growth slowdown for the China

players is priced in. In 2016E, we expect: 1) the revenue of most staples

players to slow further YoY from a relatively high base, and 2) gross-margin

expansion to slow as cost tailwinds ease. We remain Neutral on the sector.

What's the impact: Shift from big to small, old to new. We cut 2015-

17E revenue for 11 of the 12 companies by 1-14%, due mainly to: 1) shifts

in market share and channels, which often favour small players with new hit

products and foreign brands, and 2) a high consumption base for items like

beer and noodles, which means that market-share leaders can no longer

rely on their strengths (traditional distribution networks, dominant shares in

key categories), whereas small players are well placed because of their

flexibility in product launches. For example, we forecast Vinda to see a

revenue CAGR of 23% over 2015-17 due to its increasing exposure to

online channels, as well as acquisitions, vs. a flat (0%) CAGR for Hengan.

Cost tailwinds to subside: We still expect slight gross-margin expansion

for most of the staples downstream companies in 2016E (up <1pp YoY),

driven mainly by product-mix changes. Our growth forecasts are much

weaker than the surge seen in 2015E (2-4pp), as we believe some

commodity costs will rebound from a low base. At the same time, the weak

CNY:USD will likely weigh on companies with large proportions of USD

debt and/or imported raw materials. Hengan and Vinda have the most USD

exposure in terms of their COGS (30-60%).

What we recommend: We like relatively small companies with the potential

for revenue growth on market-share gains and/or product-mix

improvements. Hence, we upgrade Uni-President China (UPCH) (220 HK,

HKD5.20) to Buy (1), from Underperform (4); we also like Vinda (3331 HK,

HKD13.0, Outperform [2]). Want Want (151 HK, HKD4.96, Buy [1]) is our

sole Buy (1) among the large-cap staples companies (strong cash flow,

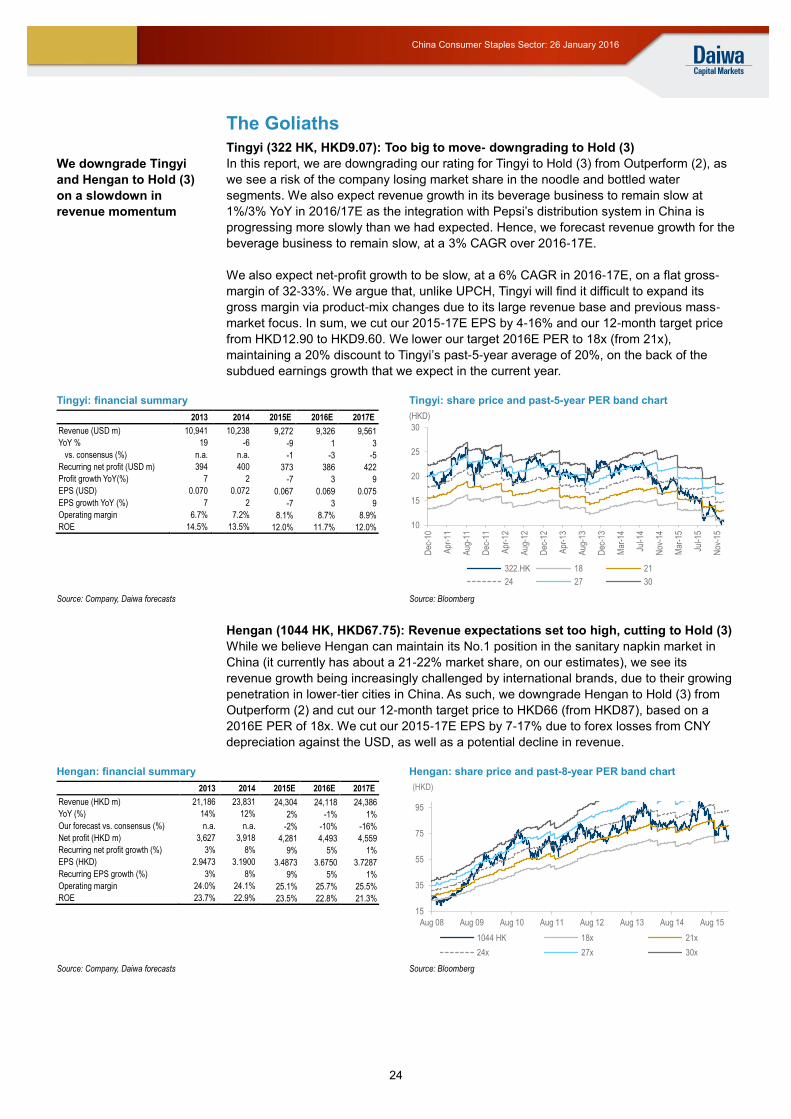

share buyback support). Meanwhile, we downgrade Hengan (1044 HK,

HKD67.75), Tingyi (322 HK, HKD9.07) and Fufeng (546 HK, HKD2.61) to

Hold (3) on price competition and potentially slow volume growth.

How we differ: Our 2016-17E revenue and EPS are 1-9% and 2-39%,

respectively, lower than consensus, reflecting our concern about market-

share losses among the big players, and our bearish CNY assumptions.

26 January 2016

China Consumer Staples Sector

Switch focus to the small wonders

With cost tailwinds likely to ease in 2016, we recommend focusing on fast-growing categories and premium products

We prefer small companies with revenue upside (“Davids”) over giants that can’t respond quickly to changing market dynamics (“Goliaths”)

Buy selectively: we like Vinda and upgrade UPCH to Buy (1); we downgrade Hengan, Tingyi and Fufeng to Hold (3)

Key stock calls

Source: Daiwa forecasts

Daiwa’s China Staples Sector coverage

Recommendation

The Davids

Vinda Outperform (2)

Modern Dairy Buy (1)

Huishan Sell (5)

Uni-President China Buy (1)

The Goliaths

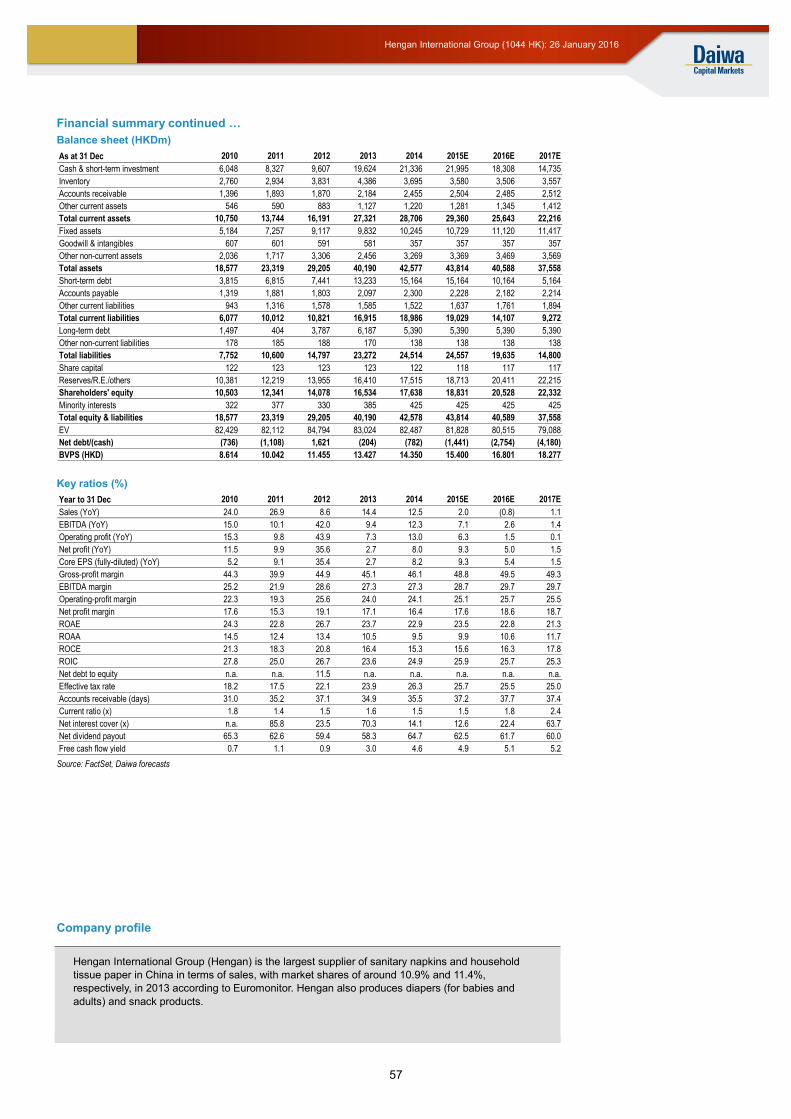

Hengan Hold (3)

Mengniu Hold (3)

Tingyi Hold (3)

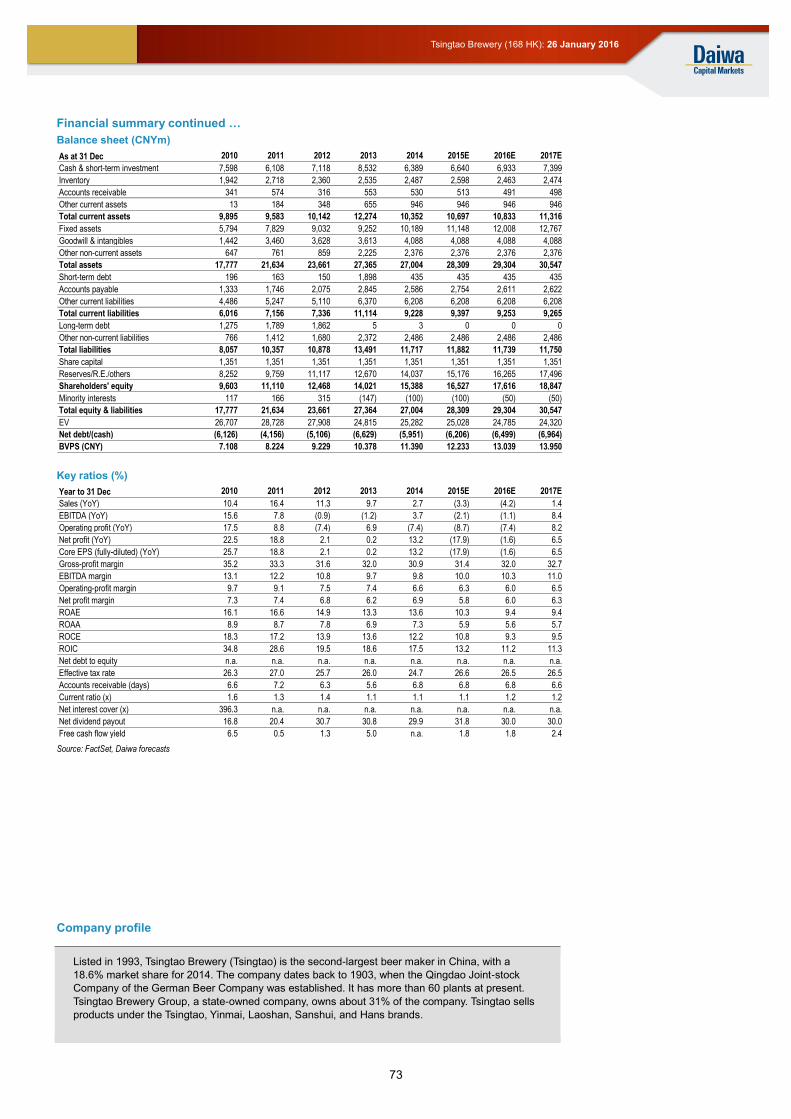

Tsingtao Underperform (4)

China Resources Beer Hold (3)

Fufeng Hold (3)

The Somewhere in betweens

Want Want Buy (1)

WH Group Outperform (2)

Source: Daiwa

Anson Chan, CFA(852) 2532 4350

New Prev.

Uni-President China (220 HK)Rating Buy Underperform

Target 6.20 7.00

Upside p 19.2%

Vinda International (3331 HK)Rating Outperform Outperform

Target 14.30 17.40

Upside p 10%

Want Want China (151 HK)Rating Buy Buy

Target 7.30 8.50

Upside p 47.2%

Hengan International Group (1044 HK)Rating Hold Outperform

Target 66.00 87.00

Downside q 2.6%

Tingyi Cayman Islands (322 HK)Rating Hold Outperform

Target 9.60 12.90

Upside p 5.8%

2

China Consumer Staples Sector: 26 January 2016

Sector stocks: key indicators

Source: Bloomberg, Daiwa forecasts

Daiwa’s China Staples Sector coverage: the Davids, the Goliaths, and the somewhere in-betweens

Recommendation Product Revenue YoY% Gross profit margin %

2015E 2016E 2017E 2015E 2016E 2017E

The Davids

Vinda Outperform (2) Tissue paper and personal hygiene products 18.0% 31.0% 16.2% 31.5% 32.1% 32.1%

Modern Dairy Buy (1) Raw milk and dairy products -0.9% 8.5% 7.8% 34.4% 35.5% 40.6%

Huishan # Sell (5) Raw milk and dairy products 13.9% 24.3% 13.8% 57.5% 55.9% 56.5%

Uni-President China Buy (1) Instant noodles and bottled drinks 5.1% 8.0% 4.9% 35.4% 36.2% 36.1%

The Goliaths

Hengan Hold (3) Tissue paper and personal hygiene products 2.0% -0.8% 1.1% 48.8% 49.5% 49.3%

Mengniu Hold (3) Dairy products -1.9% 3.7% 2.5% 32.2% 31.2% 31.5%

Tingyi Hold (3) Instant noodles and bottled drinks -9.4% 0.6% 2.5% 32.5% 32.3% 32.8%

Tsingtao Underperform (4) Beer -3.3% -4.2% 1.4% 31.4% 32.0% 32.7%

China Resources Beer Hold (3) Beer n.a. 3.8% 4.5% 34.6% 35.8% 36.4%

Fufeng Hold (3) MSG 4.1% 9.4% 1.0% 16.2% 14.7% 15.5%

The Somewhere in betweens

Want Want Buy (1) Snacks, dairy products -6.5% 6.1% 6.9% 43.6% 43.9% 43.8%

WH Group Outperform (2) Fresh and processed pork -1.0% 6.1% 5.4% 15.9% 15.6% 15.6%

Source: Daiwa forecasts Note: #FY16-18E numbers for Huishan as the company’s year-end is on 31 March

China Consumer Staples Sector: contribution of commodities to 2016E COGS (downstream) and revenue (upstream) (%)

Industry Snacks/

Soft drinks and noodles Dairy products Brewery Personal-care products Packaged meat dairy beverage

Company Want Want Tingyi UPC Mengniu Huishan Modern Dairy Tsingtao/CRB Hengan Vinda WH Group

Locally sourced /sourced in non-USD currencies

Palm oil <2 7 7

Flour <3 8 8

Sugar 5 5 5 3-5%

PET chips <5 30 30 <10 <5%

Pork

China: 70-80% of COGS

Raw Milk <3

30-40 ~30% of revenue

~80% of revenue

Corn

Feed: 70% of upstream operation

Sourced overseas

Milk powder 15%

10%

Wood pulp – short fibre

~10-15% 50-60%

Wood pulp – long fibre

Source: Daiwa estimates

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

China Huishan Dairy Holdings 6863 HK 2.95 Sell Sell 1.87 1.60 16.9% 0.055 0.056 (1.9%) 0.073 0.088 (17.9%)

China Mengniu Dairy 2319 HK 11.08 Hold Hold 11.70 14.50 (19.3%) 0.663 0.695 (4.5%) 0.636 0.752 (15.4%)

China Modern Dairy Holdings 1117 HK 1.45 Buy Buy 3.00 3.30 (9.1%) 0.126 0.156 (19.5%) 0.172 0.214 (19.6%)

China Resources Beer 291 HK 12.30 Hold Hold 12.40 13.40 (7.5%) 0.361 0.399 (9.6%) 0.530 0.517 2.5%

Fufeng Group 546 HK 2.61 Hold Buy 2.55 5.00 (49.0%) 0.241 0.254 (5.0%) 0.260 0.348 (25.1%)

Hengan International Group 1044 HK 67.75 Hold Outperform 66.00 87.00 (24.1%) 3.487 3.742 (6.8%) 3.675 4.195 (12.4%)

Tingyi Cayman Islands 322 HK 9.07 Hold Outperform 9.60 12.90 (25.6%) 0.067 0.069 (3.9%) 0.069 0.079 (12.4%)

Tsingtao Brewery 168 HK 28.80 Underperform Underperform 26.80 32.00 (16.3%) 1.211 1.305 (7.2%) 1.191 1.330 (10.4%)

Uni-President China 220 HK 5.20 Buy Underperform 6.20 7.00 (11.4%) 0.195 0.197 (0.9%) 0.232 0.219 6.2%

Vinda International 3331 HK 13.00 Outperform Outperform 14.30 17.40 (17.8%) 0.479 0.641 (25.3%) 0.570 0.851 (33.1%)

Want Want China 151 HK 4.96 Buy Buy 7.30 8.50 (14.1%) 0.042 0.046 (9.7%) 0.050 0.054 (7.8%)

WH Group 288 HK 4.40 Outperform Outperform 4.80 5.50 (12.7%) 0.042 0.041 1.8% 0.056 0.054 2.6%

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

3

China Consumer Staples Sector: 26 January 2016

Table of contents

2016: the year when strengths become weaknesses ............................................ 4

Big players are likely to underperform this year..................................................................4

Prefer the Davids to the Goliaths ..................................................................................... 10

Cost tailwinds to subside .......................................................................................13

Cost trends turned neutral on gross margins ................................................................... 13

Impact of CNY depreciation – mainly on the debt side ..................................................... 18

Valuations and recommendations .........................................................................20

Rerating opportunity for selected stocks .......................................................................... 20

The Davids ...................................................................................................................... 22

The Goliaths .................................................................................................................... 24

The somewhere in-betweens ........................................................................................... 27

Risk ..................................................................................................................................... 28

Commodity prices – main risks, upside or downside ........................................................ 28

Downside ........................................................................................................................ 28

Company Section

Uni-President China ......................................................................................................... 29

Vinda International ........................................................................................................... 33

Want Want China ............................................................................................................. 37

China Modern Dairy Holdings .......................................................................................... 41

WH Group ........................................................................................................................ 46

China Resources Beer ..................................................................................................... 50

Hengan International Group ............................................................................................. 54

Tingyi Cayman Islands ..................................................................................................... 58

China Mengniu Dairy ....................................................................................................... 62

Fufeng Group .................................................................................................................. 66

Tsingtao Brewery ............................................................................................................. 70

China Huishan Dairy Holdings ......................................................................................... 74

4

China Consumer Staples Sector: 26 January 2016

2016: the year when strengths become weaknesses

We believe a combination of consumers’ changing preferences and macro headwinds led

to a slowdown in revenue growth (and in some cases declines in revenue) for the big

China staples players in 2015, and we see this situation persisting into 2016.

Amid cost normalisation, we think promotions in commodity-like segments such as UHT

milk and bottled water will weigh on companies’ gross margins in 2016E. Hence, we prefer

the small players, which we see as more nimble and quicker to adapt to changes in the

macro picture through product premiumisation and new business initiatives (eg, M&A and

from a low revenue base). By contrast, we believe the big players will struggle to expand

their top lines from a high base.

For example, we expect Modern Dairy’s gross margin to expand significantly over 2015-

17E despite its exposure to pricing risks, as we forecast an increasing revenue and profit

contribution from its downstream operation.

We show below our coverage universe split into 3 groups: the big players (the Goliaths),

the small players (the Davids), and then those in between. For the purposes of this report,

‘big’ means a company with a dominant or near-dominant market share and/or a national

presence with its distribution network. Among the Goliaths, we note that, since 2014,

revenue growth has turned negative or at best has been flat.

However, among the Davids, we see potential for even faster revenue growth and ASP

hikes (vs. the Goliaths) on the back of improving penetration and expanding production/

distribution scale. We think the Davids have also shown more flexible sales and marketing

strategies than the Goliaths, as evidenced by their accelerated revenue growth in 2015.

Our third group, those companies “somewhere in between”, are involved in a few sub-

segments (some fast-growing, others slow-growing) or are the leading players in

fragmented industries with low per-capita consumption.

Daiwa’s China Staples Sector coverage: the Davids, Goliaths, and somewhere in-betweens

Recommendation Product Revenue YoY% Gross-profit margin %

2015E 2016E 2017E 2015E 2016E 2017E

The Davids

Vinda Outperform (2) Tissue paper and personal hygiene products 18.0% 31.0% 16.2% 31.5% 32.1% 32.1%

Modern Dairy Buy (1) Raw milk and dairy products -0.9% 8.5% 7.8% 34.4% 35.5% 40.6%

Huishan # Sell (5) Raw milk and dairy products 13.9% 24.3% 13.8% 57.5% 55.9% 56.5%

Uni-President China Buy (1) Instant noodles and bottled drinks 5.1% 8.0% 4.9% 35.4% 36.2% 36.1%

The Goliaths

Hengan Hold (3) Tissue paper and personal hygiene products 2.0% -0.8% 1.1% 48.8% 49.5% 49.3%

Mengniu Hold (3) Dairy products -1.9% 3.7% 2.5% 32.2% 31.2% 31.5%

Tingyi Hold (3) Instant noodles and bottled drinks -9.4% 0.6% 2.5% 32.5% 32.3% 32.8%

Tsingtao Underperform (4) Beer -3.3% -4.2% 1.4% 31.4% 32.0% 32.7%

China Resources Beer Hold (3) Beer n.a. 3.8% 4.5% 34.6% 35.8% 36.4%

Fufeng Hold (3) MSG 4.1% 9.4% 1.0% 16.2% 14.7% 15.5%

The somewhere in betweens

Want Want Buy (1) Snacks, dairy products -6.5% 6.1% 6.9% 43.6% 43.9% 43.8%

WH Group Outperform (2) Fresh and processed pork -1.0% 6.1% 5.4% 15.9% 15.6% 15.6%

Source: Daiwa Note: #FY16-18E numbers for Huishan as the company’s year-end is on 31 March

Big players are likely to underperform this year

Challenging conditions for big players to realise revenue growth

In a fast-growing economy and consumer market like China, it is natural for the revenue

growth of large companies with significant market shares (say, 25-50%) to track the

revenue growth of the broader sector. At the same time, given the high bases for

comparison, it becomes ever more difficult for giant companies to expand their revenue

Most staples categories

in China have seen flat

revenue, if not YoY

declines, since 2014

5

China Consumer Staples Sector: 26 January 2016

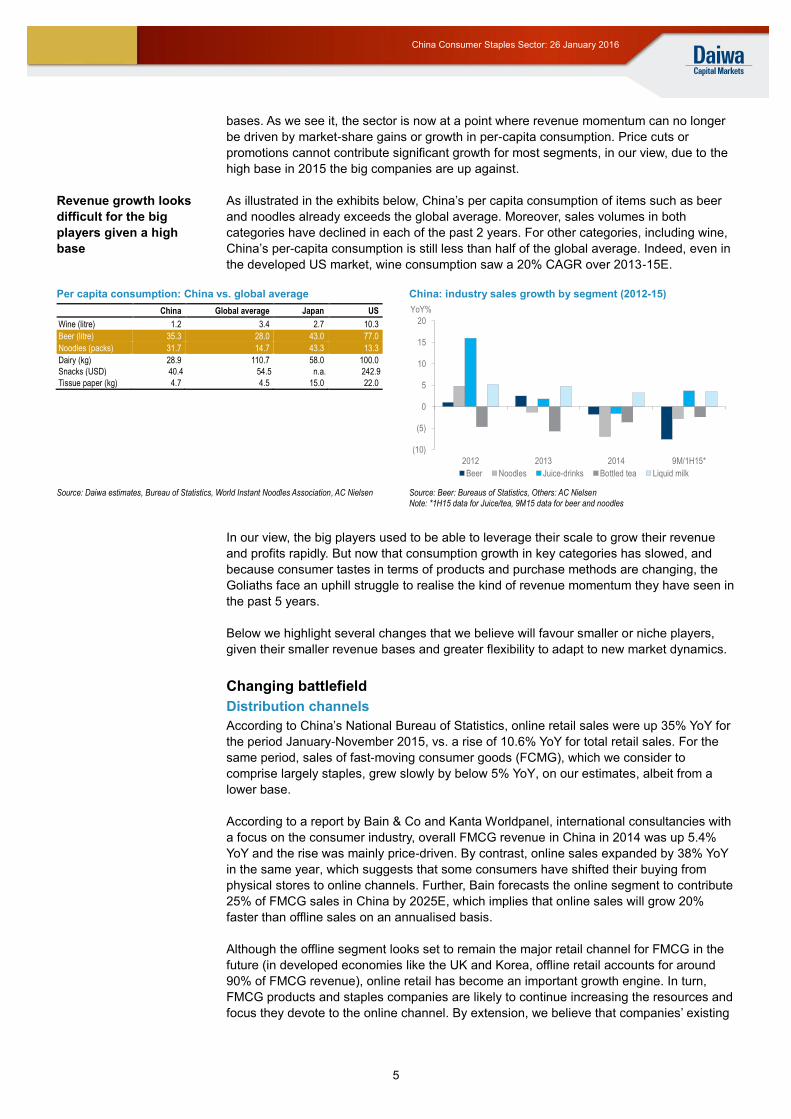

bases. As we see it, the sector is now at a point where revenue momentum can no longer

be driven by market-share gains or growth in per-capita consumption. Price cuts or

promotions cannot contribute significant growth for most segments, in our view, due to the

high base in 2015 the big companies are up against.

As illustrated in the exhibits below, China’s per capita consumption of items such as beer

and noodles already exceeds the global average. Moreover, sales volumes in both

categories have declined in each of the past 2 years. For other categories, including wine,

China’s per-capita consumption is still less than half of the global average. Indeed, even in

the developed US market, wine consumption saw a 20% CAGR over 2013-15E.

Per capita consumption: China vs. global average China: industry sales growth by segment (2012-15)

China Global average Japan US

Wine (litre) 1.2 3.4 2.7 10.3

Beer (litre) 35.3 28.0 43.0 77.0

Noodles (packs) 31.7 14.7 43.3 13.3

Dairy (kg) 28.9 110.7 58.0 100.0

Snacks (USD) 40.4 54.5 n.a. 242.9

Tissue paper (kg) 4.7 4.5 15.0 22.0

Source: Daiwa estimates, Bureau of Statistics, World Instant Noodles Association, AC Nielsen

Source: Beer: Bureaus of Statistics, Others: AC Nielsen

Note: *1H15 data for Juice/tea, 9M15 data for beer and noodles

In our view, the big players used to be able to leverage their scale to grow their revenue

and profits rapidly. But now that consumption growth in key categories has slowed, and

because consumer tastes in terms of products and purchase methods are changing, the

Goliaths face an uphill struggle to realise the kind of revenue momentum they have seen in

the past 5 years.

Below we highlight several changes that we believe will favour smaller or niche players,

given their smaller revenue bases and greater flexibility to adapt to new market dynamics.

Changing battlefield

Distribution channels

According to China’s National Bureau of Statistics, online retail sales were up 35% YoY for

the period January-November 2015, vs. a rise of 10.6% YoY for total retail sales. For the

same period, sales of fast-moving consumer goods (FCMG), which we consider to

comprise largely staples, grew slowly by below 5% YoY, on our estimates, albeit from a

lower base.

According to a report by Bain & Co and Kanta Worldpanel, international consultancies with

a focus on the consumer industry, overall FMCG revenue in China in 2014 was up 5.4%

YoY and the rise was mainly price-driven. By contrast, online sales expanded by 38% YoY

in the same year, which suggests that some consumers have shifted their buying from

physical stores to online channels. Further, Bain forecasts the online segment to contribute

25% of FMCG sales in China by 2025E, which implies that online sales will grow 20%

faster than offline sales on an annualised basis.

Although the offline segment looks set to remain the major retail channel for FMCG in the

future (in developed economies like the UK and Korea, offline retail accounts for around

90% of FMCG revenue), online retail has become an important growth engine. In turn,

FMCG products and staples companies are likely to continue increasing the resources and

focus they devote to the online channel. By extension, we believe that companies’ existing

(10)

(5)

0

5

10

15

20

2012 2013 2014 9M/1H15*

Beer Noodles Juice-drinks Bottled tea Liquid milk

YoY%

Revenue growth looks

difficult for the big

players given a high

base

6

China Consumer Staples Sector: 26 January 2016

strengths in the traditional channel will be less effective in driving revenue growth and

defending their market share going forward.

Staples items now sold online in China include infant formula (>15% of total sales in China

by channel) and nappies/diapers (>30%), relatively high-value products (per item) for

which international brands tend to be the most popular. But we are also seeing rapid

growth in online revenue for daily-use items such as tissue paper (less than 5% YoY

growth by volume in hypermarket channels in 2015, vs. 20%-plus growth online, on our

estimates).

We believe the disparity in sales growth between online and offline channels will continue,

underlining the need for staples brands to expand their presence online. On our estimates,

most of the staples companies under our coverage currently derive less than 3% of their

revenue from online platforms. The one exception is Vinda, which derived 10% of its

revenue from online retail channels in 1H15.

In 2016E, we believe revenue growth from online platforms for personal hygiene products

will outpace that for other staples segments, since consumers seem to have adapted

quickly to buying such products online.

FMCG: online market share by country China FMCG: market share by channel

Source: Kanta Worldpanel Source: Kanta Worldpanel

Demographics

Consumers are still price-sensitive, but many are now starting to consider food quality,

safety and taste when purchasing FMCGs. As shown below, the income levels of urban

citizens increased by a 13% CAGR between 2004 and 2014 (10% on an inflation-adjusted

base), showing real consumption power increased. Moreover, the dependency ratio also

declined to 36% in 2014 from 41% in 2004 according to government statistics, meaning

that the new consumption class (from students to working class) has more money than

their parents did to spend on themselves.

China: income levels – 10 years ago vs now, adjusted for CPI Chine: no. of households by monthly income (CNY 000)

Source: : Bureau of Statistics, Daiwa estimate Source: Boston Consulting Group report

1.6 2.2

15

0

5

10

15

20

25

30

35

2012 2014 2025E

China France Korea UK

0%

20%

40%

60%

80%

100%

2012 2013 2014

Other Convenience store

Grocery stores Hypermarket

Supermarkets and minimarts E-commerce

0

10

20

30

40

50

0

10,000

20,000

30,000

40,000

50,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Annual salary of urban employee (inflation-adjusted)

Dependency ratio (RHS)

CNY %

6 2160

0

100

200

300

400

500

2014 2020E 2030E

Affluent (>23) Upper middle ( 12- 23)Middle ( 8 - 12) Emerging Middle ( 5 -8 )Aspirant (2.8 - 5) Poor <2.8

Chinese consumption

power is still growing

7

China Consumer Staples Sector: 26 January 2016

During 2H15, we met the managements of a number of consumer companies across

different segments – packaged food, beverages, sportswear distribution, personal care

products, etc. Many of them said they had developed a product mix and marketing

strategies to target the top 20-30% of the household/income class. We note that Tingyi and

UPCH launched new products in high-end categories in 2Q-4Q15 (at retail ASPs at least

20% above their mass-market products). Their new products have also focused on the

value of nutrients and health (eg, MSG free instant noodles, sugar-free tea, nectars, etc).

Faster category shift and shorter product life cycle

However, the life cycles for new products are becoming shorter, a trend that is particularly

obvious for beverage products. Over the past 5 years, we have seen revenue growth for

pear juice accelerate and then slow down (up 50% YoY in 2012, then flat/declining over

2013-15), the market size for milk tea almost double (revenue rising by 82% YoY for 2012,

falling to 9% YoY in 2013), and revenue growth for room temperature yoghurt drinks rise by

more than 100% pa over 2011-13, then slow to 35% in 2014. In other words, these new

beverage categories experienced fast revenue growth within the first 2-3 years of launch,

but most saw revenue growth slow significantly, or even reverse to a decline, thereafter.

For new beverage categories, it’s easier for newcomers and small players to compete

against the big players as new and niche markets are fast-growing and have few historical

price-reference points. We observe that, in the past 5 years, it has not usually been the

No.1 player in the market that has launched a new niche product that has seen fast

revenue growth. For example, milk tea and room-temperature yoghurt drinks were

launched by 2nd

or lower ranked players, like UPCH and Bright Dairy (600597 CH, not

rated), with less than 20% nationwide market share.

We believe big players are less keen to launch new flavours for fear of them causing

product cannibalisation (ie, leading to a sales shift among different divisions rather than

gaining market share from competitors. For example, Mengniu’s sales growth for its

premium UHT milk and room temperature yoghurt in 1H15 was largely offset by the sales

decline for milk beverages as well as mass market UHT milk). Even if a big player

launches a new product successfully and posts fast revenue growth initially, the impact on

the company’s revenue and profit is likely to be lower than that for a small player due to the

bigger company’s higher revenue base.

China: beverage consumption breakdown 2010 vs. 2012 vs. 2014

China: growth rates of various “start products” (2011-15)

Source: AC Nielsen, Tingyi Source: Companies, Daiwa estimates Note: Juice-drinks – estimated from Tingyi financials; Milk tea/Laotan noodles: from UPCH, Hot-

kid milk – Want Want. Room-temperature yoghurt: Bright Dairy numbers

Price promotions not effective in driving bottom lines

Due to the distribution and production scale advantages of the Goliaths, they usually enjoy

lower production costs (as a result of economies of scale, bulk purchases of raw materials,

etc.) and are more keen on price cuts to promote sales volumes (reference Hengan’s

reduction of its tissue paper prices in 2014; Tsingtao’s expansion in the mass-market

segment since 2013 by selling more mid-to-low end sub-brand products). However, since

19.1 16.9 15.5

30.9 31.2 33.1

28.523.6 22.1

1817.8 15.4

3.5 10.5 13.9

0%

20%

40%

60%

80%

100%

2010 2012 2014

RTD tea Bottled water

carbonated drinks Juice

Sportsdrink, herbal tea and others

(50%)

0%

50%

100%

150%

200%

2011 2012 2013 2014 2015E

Juice-drinks Hot-kid milk

Milk tea Room-temperature yogurt

Laotan noodles

New products can attract

new customers but also

lead to cannibalisation

Price cuts offset volume

growth and lead to

gross-margin pressure

8

China Consumer Staples Sector: 26 January 2016

the beginning of 2015, price competition does not seem to have been such an effective

tool for gaining market share, as evidenced by Hengan and Tsingtao’s YoY revenue

declines in 1H15.

We believe that health consciousness, variety and image are now important factors

determining consumer purchases, as affordability of FMCG items increases (supported by

increasing income levels). Consumers seem willing to pay a premium if the products can

provide value such as quality, safety (eg, personal hygiene products) or are purchased at

high-profile locations (eg, entertainment clubs or high-end restaurants). Moreover, in some

categories like the dairy segment, the number of brands available to Chinese consumers

has expanded rapidly over the past 5 years due to dairy farms moving into downstream

production, and foreign companies aggressively promoting their products in China (in

particular through e-commerce). As a result, existing domestic players have not been able

to grow their sales volumes by cutting prices because many competitors have followed the

same strategy.

To follow are some trends we see in a variety of markets:

Rice crackers: in 1H15, Want Want’s rice cracker sales rose by 10% YoY, driven mainly

by gift packs (up 41% YoY) and core brands (up 8% YoY); while revenue for the sub-

brands, which are at least 30% cheaper than the core brands, was up only 5% YoY. We

believe consumers continue to favour Want Want’s core brand products due to their better

quality and brand image, in particular if they are purchased as gift items.

Dairy: for both Yili and Mengniu, their premium UHT milk products and star product sales

exceeded their total revenue growth in 1H15. Those products’ ASPs are at least 50%

above mass-market product prices, but they are perceived to have better nutrient value.

According to Frost and Sullivan, high-end UHT milk retail sales in China will reach

CNY89bn by 2017E, representing a 3-year CAGR of 21% (vs. 5% for mass-market

products) and the revenue contribution of high-end UHT milk to the total UHT market will

reach 45% in 2017E, from 31% at present.

Want Want: rice cracker sales YoY – sub-brands vs. core brands (1H15)

China: premium UHT milk sales vs. mass-market sales

Source: Want Want Source: Frost and Sullivan

Bottled water: We believe Tingyi’s loss of bottled water market share since 1Q15 is

evidence of consumers’ increasing awareness of brand image and the difficulty of

companies remaining competitive on price alone. According to AC Nielsen, Tingyi’s bottled

water market share slid by 2pp YoY in 1Q15, when it raised its bottled water retail ASP by

about 20% (from CNY1 for a 500ml bottle, the cheapest national brand we found in the

market, to CNY1.2, in line with most peers, based on our estimates). Although Tingyi at the

same time has increased the weight of its bottle to make it look more high-quality, and

rebranded the product “Youyue” (meaning excellent and joy, in English), we believe Tingyi

has long been regarded as a cheap brand in the eyes of consumers due to its below-peer

pricing since launching its bottled-water product in 2004. In our view, it will take more effort

on the part of the company to step up its advertising and marketing to build brand loyalty.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Core brands Gift brands Sub-brands

YoY

64.9 71.3 76.1 78.9 92 97 103 109.7 116 121.7 126.9 131.112.2 16.1 17.9 20.829 34.6 41.7

50.661.2

73.889

107.2

0

50

100

150

200

250

300

2007

2008

2009

2010

2011

2012

2013

2014

2015

E

2016

E

2017

E

2018

E

Mass market Premium

CNY bn

Brand loyalty has

become a more

important factor in

beverage purchasing

decisions

9

China Consumer Staples Sector: 26 January 2016

Tingyi: market share (%) and revenue (USDm) of bottled water segment

Source: Company

International brands more attractive than local brands, mainly in personal-care products

According to Kantar Worldpanel, most domestic players gained market share in major F&B

categories in China in 2014. We believe that since 2014 domestic players have been, and

are still, responding more quickly than international players to adapt to changes in local

preferences and to accommodate the appetite of Chinese consumers. Exceptions include

beer (which we believe is due to ABInBev’s successful penetration of the high-end market

segment in China), instant noodles (from a low base) and chocolate (more imported goods

available).

Foreign players though have gained market share in personal-care products, particularly

facial and toilet tissue. Foreign brands also gained share in the baby diaper market in

2014, according to Euromonitor, while Hengan (the biggest domestic player) lost market

share. The Japanese players seemed to take market share in sanitary napkins in 2014

(around 7%) albeit at a gradual pace – Unicharm’s market share was up 0.8pp YoY to

5.7% in volume terms, slightly faster than market leader Hengan.

We attribute the better performance of foreign brands in personal care products than in

F&B items to: 1) their production technology and raw-material quality (Japanese brands in

particular) being perceived as better than domestic peers’; consumers are more concerned

about quality (convenience and hygiene) than prices in those products, and 2) lower

logistical costs (smaller size and lower weight of diapers and sanitary napkins vs. F&B)

which makes personal care products high-margin and frequently purchased products for e-

commerce retail platforms. For staples companies to ride on that trend they would need to

cooperate with strategic investors/JVs to introduce foreign products in China, in particular

personal hygiene products.

We believe Vinda has been aggressively promoting its premium foreign brand, Tempo,

after obtaining its licensing and distribution rights in China in 2013, while Hengan has not

sought any international partnership yet. While both Davids and Goliaths can seek co-

operation with international partners, there have been successful cases for Goliaths in the

past 2 years (eg, both Tingyi and Tsingtao ended their co-operation with Japanese partners

in 2015).

20%22% 22%

19%18% 18%

19%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

Revenue Market share

USD m

10

China Consumer Staples Sector: 26 January 2016

International brands: market-share changes (2014)

Foreign brands are

gaining market share in

beer, chocolate and

instant noodles, as well

as personal care

products

Source: Kanta Worldpanel

Prefer the Davids over the Goliaths

In consideration of the above demographic and consumption pattern changes, we prefer

the Davids (small players) to the Goliaths (big players) in most staples sub-segments, as

we believe it is easier for the Davids to grow revenue (volume) from a low base compared

with the Goliaths. In our view, it is difficult for Goliaths to leverage on their past strengths

(eg, strong traditional channels, cost advantage, etc.) to grow revenue or expand gross

margins, as many are already operating amid optimal conditions (in terms of utilization

rates, cost reduction through bulk-purchases, etc.). We discuss below what Goliaths and

Davids are doing.

The Goliaths’ strategy – co-operation with foreign players

In our opinion, the Goliaths need to think about how to tap their existing assets (consumer

bases, brands and networks) by finding new revenue sources, such as new product

categories (through partnerships with foreign brands or in-house development), upgrading

their existing products (for higher ASPs and gross margins) or engaging in more R&D in

order to reduce costs. Some examples are shown below.

Tingyi formed JVs with a number of foreign players (Calibee, Wakado and Prima) in 2013

to launch snacks and other new products. Tingyi eyed the product development and brand

recognition of those partners overseas and wanted to distribute such new products by

leveraging on its own distribution network in China. However, all those JVs still contribute

less than 2% of the company’s revenue at present based on our estimates, and Tingyi

terminated one of the co-operation agreements (with Calibee) in 4Q15, as it had remained

unprofitable for years and Calibee wanted to seek other opportunities to grow in China.

Tsingtao formed a JV with Suntory in 2013 to expand in eastern China. Suntory is

responsible for production and Tsingtao for distribution and marketing. However, Suntory

sold its stake in the JV to Tsingtao in 4Q15 after years of loss-making, leaving Tsingtao

with the losses to deal with.

Mengniu formed a JV with strategic investor Danone in 2014 to develop yoghurt and other

cold-chain products in China. We estimate Danone’s yoghurt products gained 1pp market

share for Mengniu in 2015E and helped upgrade Mengniu’s production technology and

brand recognition. In December 2015, Yashili (1230 HK, not rated), Mengniu’s infant

formula subsidiary, also announced that it planned to acquire Danone’s infant formula

business in China for HKD1.2bn. However, we are cautious on Mengniu’s co-operation

with Danone in the infant formula business, as it is not an exclusive partnership. Danone is

developing an imported and premium infant formula brand, Nutricia, on its own in China,

and because of the non-exclusive nature of its partnership, Mengniu will not benefit from

the fast growth of this high-end infant formula segment.

2.1 1.8 1.6 1.6 1.3 1.2 1.20.2

-0.1 -0.2 -0.3 -0.6 -0.6 -0.9 -1 -1.1 -1.1 -1.4 -1.7 -1.8-2.4 -2.8 -3.1

-3.8 -3.8-4.8(6)

(5)(4)(3)(2)(1)

0123

Tol

iet t

issu

e

Bee

r

Hai

r co

nditi

oner

Inst

ant n

oodl

es

Che

win

g gu

m

Cho

cola

te

Car

bona

ted

drin

ks

Fac

il tis

sue

Sha

mpo

o

Bab

y di

aper

s

Yog

urt

Milk

Per

sona

l was

h

Fab

ric d

eter

gent

s

Bot

tled

tea

toot

hbru

sh

cand

y

bottl

ed w

ater

toot

hpas

te

kitc

hen

clea

ner

Bis

cuits

Juic

e

Infa

nt fo

rmul

a

Col

or c

osm

ecits

fabr

ic s

ofte

ner

Ski

ncar

e

Market share changes (%)

11

China Consumer Staples Sector: 26 January 2016

Want Want co-operated with Morinaga to launch pudding products in 1H15. We estimate

the products contribute only about 0.5% of the company’s revenue at present, but this

figure should expand further in 2016E.

The Davids’ strategy – niche products, new distribution channels

Davids – based on our observations, the Davids are more flexible and quicker in terms of

decision-making and responding to changes in the market. For example, in provinces or

cities where there are no direct distributors of their products, the Davids can make use of

the e-commerce channel without cannibalising the benefits of distributors, while big players

with national distributors may find it difficult to provide incentives for new (online)

distributors to promote products without jeopardising existing distributors. The risk of

cannibalization between old and new products is also lower for Davids due to their

relatively smaller product portfolios.

Vinda has been the No.1 household paper brand on the e-commerce platform in China

since mid-June 2015 (No. 3 in the total market). It has developed different packaging for its

online platform to differentiate these items from its offline items. E-commerce transactions

accounted for about 10% of its revenue in 1H15 (vs. <5% for its closest competitor,

Hengan) and were profitable. Moreover, competitor Hengan has low exposure to e-

commerce (3% of revenue in 2015E). With the acquisition impact, we expect Vinda’s

revenue growth to rise at a 23% CAGR over 2015-17E, on our forecasts, due to its

increasing exposure to online channels and acquisitions, vs. a flat (0%) CAGR for Hengan

over the same period.

Modern Dairy was a late-comer to the China dairy downstream market, launching its own-

branded products only in 2010 (pasteurized milk) on a small scale, followed by its first UHT

product in 2013. To differentiate itself from market leaders like Mengniu and Yili, Modern

Dairy focuses on premium products and selected regions only. The company also seldom

uses TV commercials for advertising and promotions. Modern Dairy has around an 8%

market share in the premium UHT milk market in China (AC Nielsen data in 3Q15), and its

downstream net margin (of 12%) is higher than the large players’ (6-10%), thanks to its

vertically-integrated model.

Vinda: revenue breakdown by channel Modern Dairy: revenue contribution from downstream

Source: Company, Daiwa estimates Source: Company, Daiwa forecasts

Uni-President China (UPCH) regained market share in instant noodles in China (from

around 11% in 2011 to ~18% in 2015E, according to AC Nielsen) through introducing new

flavours and categories (eg, Laotan pickled vegetable noodles, Soup Daren brand, etc.)

and had successfully turned the business around in 2H14. The company also launched a

number of new beverages in 2014-15 targeting the high-end market and consumers in top-

tier Chinese cities.

Want Want has a strong record of product diversification (>600 SKUs of snack items,

based on our estimates) and product development capability, such that it resembles a

group of Davids rather than a big Goliath. We are confident that WW’s snack business can

1.6% 3.6% 5.1% 8.6% 9.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1H13 2H13 1H14 2H14 1H15

Traditonal KA Corporate clients E-Commerce

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

500

1,000

1,500

2,000

2,500

3,000

2012 2013 2014 2015F 2016E 2017E

Downstream revenue as a ratio of total

CNY m

The Davids and Goliaths

have to adopt different

strategies — and we

believe the Davids stand

a better chance of

growth

12

China Consumer Staples Sector: 26 January 2016

still grow in volume terms as the market is still fragmented. According to Frost and Sullivan,

the top-10 players only accounted for 30% of the market in 2014, while WW stood out at

No. 1 with a 5% share. The market is divided up amongst the big and small Davids, each

with its niche (eg, WW’s rice cracker is No.1 with a c70% market share).

UPCH: products launched in the past 24 months

Beverage No. of flavours Suggested retail price Launch date What's special about the product?

Xiaoming classmate tea 4 CNY 5 Mar-15 Special bottle design and cold-brewed

Haizhiyen 3 CNY 5 Apr-14 Sea-salted low-sugar fruit juice

Chinese mixed fruit drinks 2 CNY 5 May-15 Mixed Chinese fruit juice for health

Nectars 3 n.a. Soon Nutritious and Western-style

Asamu in little bottles 2 CNY 6 3Q15 Using chilled milk instead of milk powder

Xiaoye milk tea 3 CNY 3 1H15 Targets primary and secondary students

Noodles No. of flavours Suggested retail price Launch date What's special about the product?

Champion 2 CNY 10-12 Nov-14

Soup Dairen 4 (2 more to come) CNY 8 Re-launched with new flavours 2 years ago

Vege-light Noodles 3 CNY 5 Oct-15

Gemien 2 CNY 5 4Q14

Noodles No. of flavours Suggested retail price Launch date What's special about the product?

Champion 2 CNY 10-12 Nov-14

Soup Dairen 4 (2 more to come) CNY 8 Re-launched with new flavours 2 years ago

Vege-light Noodles 3 CNY 5 Oct-15

Source: Company, Daiwa

13

China Consumer Staples Sector: 26 January 2016

Cost tailwinds to subside

Cost trends turned neutral on gross margins

Most of the downstream staples companies that we cover are likely to see significant gross

margin expansion over 2014-15E, on the back of lower raw-material costs. However, this

trend could reverse in 2016E as the prices of some raw materials rebounded in 4Q15, and

those of many others turned steady in 2H15. Furthermore, CNY depreciation against the

USD is also likely to have a negative impact on the cost of imported raw materials (eg,

wood pulp).

As shown in the following chart, we expect the gross margins of the downstream staples

companies to have expanded by 1.3-3.4pp YoY for 2015E. For the upstream dairy farm

and grain processing companies, we forecast their gross margins to have declined for the

same period due to lower ASPs. For 2016E, we expect the gross margins for the upstream

companies to change by only 1pp (plus or minus), mainly due to price promotions or

product mix upgrades, rather than changing raw material costs. For the upstream

companies, we expect a slight improvement in their gross margins due to a slight increase

in ASP.

China Consumer Staples Sector: gross margins

Gross-margin expansion

could slow in 2016E

Source: Company, Daiwa forecasts

Outlook for raw-material costs

The following table shows the contribution to COGS of various raw materials for the

consumer staples companies for 2015E. Most of the necessary raw materials can be

sourced locally in China or the rest of Asia (not denominated in USDs and hence, are

cushioned from the rising USD). The personal-care product companies have the highest

exposure to imported raw materials.

China Consumer Staples Sector: contribution of commodities to 2016E COGS (downstream) and the revenue (upstream) (%)

Industry Snacks/

Soft drinks and noodles Dairy products Brewery Personal-care products Packaged meat dairy beverage

Company Want Want Tingyi UPC Mengniu Huishan Modern Dairy Tsingtao/CRB Hengan Vinda WH Group

Locally sourced /sourced in non-USD currencies

Palm oil <2 7 7

Flour <3 8 8

Sugar 5 5 5 3-5%

PET chips <5 30 30 <10 <5%

Pork

China: 70-80% of COGS

Raw Milk <3

30-40 ~30% of revenue

~80% of revenue

Corn

Feed: 70% of upstream operation

Sourced overseas

Milk powder 15%

10%

Wood pulp – short fibre

~10-15% 50-60%

Wood pulp – long fibre

Source: Daiwa estimates

35.4%

43.6%

32.6%

16.2%

34.9%30.9% 32.2%

48.8%

31.5%

58.6%

32.3%

16.9%

10%

20%

30%

40%

50%

60%

UPCH Want Want Tingyi WH Group CRB Tsingtao Mengniu Hengan Vinda Huishan ModernDairy

Fufeng

2014 2015 2016E 2017E

14

China Consumer Staples Sector: 26 January 2016

Milk powder

We believe the price of milk powder imported into China will bottom out in 1Q16 and

gradually pick up throughout 2016E. In December 2015, Fonterra, the operator of the

largest dairy-product trading platform globally and the key co-operative for dairy farms in

New Zealand, maintained its milk payout rate to its suppliers until May 2016 (at

NZD4.6/kg). Fonterra expects the price of milk powder to rise in 2016 as the global glut

dissipates and the China manufacturers (food processing companies and dairy beverage

producers) start to purchase more after the milk powder inventory has normalised.

The milk powder spot price on the international market has risen by 42% from its trough of

USD1,560/tonne in August 2015, while China’s powder import price (the actual cost for

producers in China) declined by an average of 17% in 2015. As the import price at China

customs typically lags the international spot price by 4-6 months due to transportation

factors, we expect the powder price in China to be relatively low in 1H16 before trending

up in 2H16.

Raw milk (China)

According to the Ministry of Agriculture, the price of raw milk price increased by 3%QoQ for

4Q15 vs. September 2015. However, we now turn more cautious on the raw milk price

outlook for 2016E, due to the declining feed cost, some of the large raw milk suppliers

could lower their ASPs to expand their sales volume, implying pricing pressure in the

industry. Moreover, despite the recent rebound in milk powder prices globally, the cost of

milk powder is still near its past-5-year low globally. This means imported milk powder

remains a cheap substitute for raw milk in 2016E. We assume a flat YoY raw milk ASP for

Modern Dairy and Huishan Dairy in 2016E.

Milk powder prices: imported prices (at China Customs) and the international spot price

China: raw milk price

Source: Global Dairy Trade, China Custom Source: Companies, Ministry of Agriculture

Palm oil and wheat/flour

Ong Keng Wee, a plantation analyst at Daiwa’s alliance partner in Malaysia, Affin Hwang,

forecasts an ASP for palm oil (in Malaysia) of MYR2,400/tonne for 2016E (+12% YoY),

supported by a decline in inventory and possible lower production in 2016E. We believe

the noodle players in China will be the key victims of the rising palm oil price in 2016E, as

we estimate that palm oil accounts for about 15% of their COGS.

Wheat is another major cost item for the instant-noodle makers (~15% of COGS), and we

expect the price of wheat to remain steady or increase slightly in 2016E, as the price the

government pays is likely to remain stable, which should give farmers the incentive to

produce wheat. Hence the noodle-makers are unlikely to make any cost saving when it

comes to the wheat input cost for noodles, in our view.

0

1,000

2,000

3,000

4,000

5,000

6,000

Apr-09 Feb-10 Dec-10 Oct-11 Aug-12 Jun-13 Apr-14 Feb-15 Dec-15

Import price Auction price

(USD/tonne)

3.0

3.5

4.0

4.5

5.0

5.5

Jan-13 Jun-13 Nov-13 Apr-14 Sep-14 Feb-15 Jul-15 Dec-15

National average CMD Huishan

CNY/kg

Downstream dairy

players likely to see cost

of milk rebound in 2016E

15

China Consumer Staples Sector: 26 January 2016

Palm oil prices: imported price of China (Tianjin port, LHS) China: wheat price

Source: Bloomberg Source: Bloomberg

Sugar

We expect the price of sugar to increase by 5-10% YoY in 2016 in China due to the tighter

supply. In December 2015, the Guangxi Provincial Government increased its guidance

price for sugar cane, from CNY400/tonne for the 2014/15 harvest to CNY440/tonne for the

2015/16 harvest due to a decrease in acreage, implying lower production costs for cane

sugar in China. On the international market, the price of sugar rose by 23% in 2H15 in

Brazil, the largest exporter of sugar in the world. According to a USDA report released in

November 2015, global sugar production for 2015/16 was forecast to decline by 3m

tonnes, at 172m, with declines in Brazil, India, the EU, and Ukraine more than offsetting

gains in Australia, Russia, and Turkey. The report projects consumption to reach a record

173m tonnes, pulling down the global inventory level by 4m tonnes to 40m tonnes in

November 2016E.

PET chips

According to data from Wind, the price of PET chips declined by 4% YoY in 4Q15 and 21%

YoY for 2015 on average due to the weak price of crude oil, which should be positive for

the gross margins of the beverage producers. However, as the PET chip price has almost

reached its past-10-year trough of some CNY5,800 (in 2008; currently: CNY6,000/tonne),

and given the strong USD, we don’t believe PET chip costs will decline by much in 2016E

in China (in CNY terms). This, together with rising sugar costs, implies to us that there is

limited room for the gross margins of the bottled-drink producers Tingyi and UPCH to

expand this year.

China: PET-chip prices (vs. oil price) China: global sugar price

Source: Wind Source: Bloomberg

0

200

400

600

800

1000

1200

1400

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

M-09 M-10 J-11 N-11 A-12 J-13 A-14 F-15 N-15

"Malaysia" "Tianjin"

CNY/m tonnes USD/m tonnes

1,000

1,500

2,000

2,500

3,000

3,500

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Apr

-15

Aug

-15

Dec

-15

Flour Wheat

CNY/m tonnes

0

20

40

60

80

100

120

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Jun-

15

Sep

-15

PET (CNY/mt, LHS) Brent oil (USD/barrel, RHS)

CNY/m tonnes USD/Barrel

0

1

2

3

4

5

6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-08 Apr-09 Jul-10 Oct-11 Jan-13 Apr-14 Jul-15

Nanning Brazil

CNY/m tonnes USD/lb

In 2016E, we expect the

price of sugar to reverse

its downtrend since 2013

16

China Consumer Staples Sector: 26 January 2016

Wood pulp – (short and long-fibre)

Mercer Int. (Not rated), a global pulp supplier of wood pulp, and Hawkins Wright, a global

research firm on forest, pulp and paper industry, offer the following insight into the global

supply outlook:

Softwood (northern bleached softwood kraft pulp [NBSK]): global capacity is expected

to grow by 0.7m tpa in 2016E (<4% of total demand, based on our estimates), and

according to Mercer, such growth is consistent with growth in demand. Wright forecasts

softwood pulp demand to increase by 0.127m tpa over 2014-18, versus 0.19m tpa rises

per year in capacity.

Hardwood (bleached hardwood kraft pulp [BHKP]): global capacity growth should be

fast for 2016, at c. 3% on our estimates, but should match demand growth. Hawkins Wright

forecasts hardwood pulp capacity to rise by 1.5m tpa over 2016E, versus demand growth

of 1.38m tpa in 2015E.

Based on Bloomberg data, BHKP and NBSK pulp averaged USD803/tonne and

USD832/tonne for 2H15, up 5% and down 5% YoY, respectively. We estimate normal wood

pulp inventory for tissue producers is currently at about 4-6 months (including raw

materials being shipped to China); and over 60% of the pulp used for tissue paper is

NBSK. Hence, we expect pulp costs in 1H16 to be flat or decline slightly for wood pulp

users in USD terms. However, if we take CNY depreciation into consideration (-4.5%

against USD in 2015 per Bloomberg), wood pulp costs would remain flat YoY in terms of

CNY in 1H16E, and risk rising in 2H16E.

Wood pulp prices

Source: Bloomberg

Rice, corn and other grains (sourced in China)

We believe prices of domestically sourced grains (corn, wheat, rice) will stop increasing or

reverse their uptrends seen over the past 6 years as a result of changes to policies that

used to support grain prices through government purchasing. For grains that are

domestically produced and sourced in China (ie, corn, rice), prices have gone up slowly

since 2009, supported by favourable policies. We believe the prices of major crops in

China are supported by government incentives encouraging farmers to produce more. The

China government has already cut its guaranteed purchase price for corn for the 2015/16

harvest period by c.11% YoY due to the high reserves level in the country. The government

has also stated, that while it will continue to purchase wheat and rice in 2016, it hasn’t

decided whether to continue to purchase corn or not.

Government purchase price of major grains in China (CNY/50kg

2015 2014 2013 2012 2011 2010

Corn 100 111-113 111-113 105-107 n.a.

Wheat 118 118 112 102 93 86

Early rice 135 135 132 120 102 93

Later rice 138 138 135 125 107 97

Hard rice 155 155 150 140 126 103

Source: Ministry of Agriculture

300

400

500

600

700

800

900

1,000

1,100

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

NBSK BHKP

USD/tonne

Lower USD pulp costs

offset by CNY

depreciation vs. USD

17

China Consumer Staples Sector: 26 January 2016

We estimate that grain prices in China are about 20% higher than international prices at

present (except soybean, whose imports accounted for over 60% of the consumption in the

past 5 years) due to supportive government policies. We expect this gap to continue to

trigger imports of grains into China or a reduction in domestic grain prices, in particular for

corn. As shown below, international corn and wheat prices trended up in 4Q15, by 1% and

13% QoQ on average, based on Bloomberg data, respectively.

Corn price in the US spot market Corn price in China price

Source: Bloomberg Source: Bloomberg

Hogs and pork

Hog inventory as of November 2015 was 388m heads in China, according to the Ministry

of Agriculture (down 1% MoM, but down 10% YoY). The number of reproductive sows in

China declined to 38.3m heads in November 2015 (-12% YoY), implying that supply is

continuing to tighten. We expect pork prices to rise by less than 5% YoY on average in

2016E, due to the low base in 1H15 followed by a slight tightening of supply in 2H15-2016.

However, as of December 2015, the hog-corn cost ratio was already 8.6x, per the Ministry

of Agriculture, near the high-end of the guidance range for hog raisers (6x-9x) as indicated

by the government. If such a ratio rose above 9x the government may have to sell pork

reserves to stabilise prices. Moreover, with the recent decline in corn costs (a major feed

for hogs), we see limited upside for hog costs in 2016E. Hence we see limited upside to

our hog and pork price forecast for in 2016.

China: pork and hog prices Hog-corn cost ratio

Source: Wind, Bloomberg Source: CEIC

0

100

200

300

400

500

600

700

800

900

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

USD/5000 bushel

1,000

1,500

2,000

2,500

3,000

Jan-

09

May

-09

Oct

-09

Mar

-10

Aug

-10

Jan-

11

Jun-

11

Nov

-11

Mar

-12

Aug

-12

Jan-

13

Jun-

13

Nov

-13

Apr

-14

Sep

-14

Jan-

15

Jun-

15

Nov

-15

Heilongjiang Jilin Shandong

(CNY/m tonnes)

5

10

15

20

25

30

J-08 J-08 D-08 J-09 D-09 J-10 D-10 J-11 D-11 J-12 D-12 J-13 D-13 J-14 N-14M-15N-15

Pork wholesale price Hog cost

CNY/kg

2013 Ave.6.22

2014Ave, 5.50

2015Ave, 6.55

4

5

6

7

8

9

10

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

Sep

-12

Jan-

13

May

-13

Sep

-13

Jan-

14

May

-14

Sep

-14

Jan-

15

May

-15

Sep

-15

(x)

We expect grain prices

to stay flat or decline in

China in 2016E due to

policy changes

Any increase in the cost

of hogs and pork in

2016E will be lower than

we previously expected

18

China Consumer Staples Sector: 26 January 2016

Impact of CNY depreciation – mainly on the debt side

Debt and financial costs – the key factor. Before 2014, most staples companies enjoyed

low interest rates and the benefits of CNY appreciation against foreign currencies by using

foreign debt (mainly USD or HKD). However, with the CNY starting to depreciate against

the USD in 1H15, most companies reported forex losses for that period. Most of them did

not use derivatives to hedge against currency rate changes. To lessen the impact of CNY

depreciation, some companies have already started replacing USD/HKD-debt with CNY-

debt wherever possible:

In this report, we are revising down our 2016-17 EPS forecasts for 6 of the 12 companies

we cover in the staples sector as a result of FX losses. We see companies with higher net

gearing being slower to cut their USD/HKD debt to reduce FX losses, since they may not

have sufficient resources to pay down their USD-debt quickly.

(1) Companies with net cash: Want Want and Hengan have the highest exposure to

USD/HKD denominated debt (99-100%) among our coverage universe. They are in a

net cash position, which enables them to pay down debt quickly if necessary.

(2) Companies with net debt may have to raise CNY debt locally before settling their

USD debt. Among the big caps, we expect Mengniu to work on replacing its non-CNY

debt previously raised for acquisitions by leveraging on its relationship with COFCO

Group (as an SOE) to secure more local debt in CNY and reduce its exposure to CNY.

Also, for Tingyi, the debt borrowers (bond issuers) are Hong Kong entities (functional

currency is HKD), so there is no mark-to-market loss for USD debt incurred by its

Hong Kong entity. Translation losses on balance sheet items are debited to equity

reserves, instead of the P&L. For Tingyi, we believe the FX loss in 2015 was due

mainly to its EUR-denominated debt (for the purchase of machines), which is non-

recurring in 2016E. Hence for both, we believe the impact of CNY depreciation in

2016-17E will not be higher than it likely was in 2015E. Vinda faces the biggest impact

from further CNY depreciation due to its high gearing. However, we believe this factor

has been priced in its recent share-price correction.

(3) Some companies like Modern Dairy and Fufeng reported slight positive FX gains in

1H15, which we believe was due to non-CNY cash and other assets they have (eg,

receivables). Going forward, we expect the impact of FX to be even smaller as they

raise CNY-debt and reduce USD-denominated loans.

Exposure and impact of FX exchange rate changes on net profit

USD/HKD debt as %

of total

USD/HKD debt as %

of book equity

HKD/USD cash as % of equity

net HKD/USD debt as % of equity

Report. currency

FX loss (m reporting

currency)

as % of pre-FX

net profit COGS %

contribution in USD

2014 2014 2014 2014

1H15 2015E 2016E 1H15 2015E 2016E

Tsingtao Brewery c.0% n.a. n.a. n.a. CNY 3.0 negligible -0.3 negligible <10%

Fufeng 40% 26% 2% 24% CNY 5.5 negligible 1.1 negligible <10%

UPCH 41% 19% 3% 17% CNY 1.7 negligible 0.2 negligible <10%

Modern Dairy 41% 36% 5% 31% CNY 2.9 negligible 0.6 negligible <20%

Mengniu 85% 39% 7% 32% CNY -22.0 -50 -50 -1.6 -1.9 -1.9 <10%

Tingyi 87% 84% 4% 80% USD -49.2* -49 -50 -11* -12 -11 <10%

Vinda 91% 82% 2% 80% HKD -30.0 -280 -300 -8 -37 -32 c.50%

WH Group 97% 75% n.a. n.a. USD n.a. n.a. n.a. n.a. n.a. n.a. <50%.

Want Want 99% 68% 2% 66% USD -0.9 -2 -5 -0.3 -0.3 -0.7 <20%

Hengan 100% 85% 11% 74% HKD -139.0 -270 -240 -7 -6 -5 >30%

Huishan Dairy 12% 7% 5% 2% CNY -124.6 negligible -13.8 negligible <10%

Source: Company, Daiwa estimates for 2015-16E Note: * for nine months ended Sep-15; # including impact from FX change in non USD/HKD currency exchange rate against CNY, 1due to its US operation

Revenue: CNY depreciation mainly weighs on companies that report in USD or HKD. Of

the 6 companies we cover that report in USD or HKD, WH Group should be least

impacted, as we estimate that over 50% of its revenue came from the US in 2015. We also

estimate that about 25% of Vinda’s revenue comes from outside China (Hong Kong and

ASEAN countries) after its acquisition of SCA’s pan-Asian hygiene products business in

1Q16.

CNY depreciation

against USD weighed

more on financial costs

than raw materials

19

China Consumer Staples Sector: 26 January 2016

Cost of production: Except wood pulp, soybean and milk powder, most raw materials

used by staples companies in China are locally sourced. As such, a depreciating CNY is

negative for the gross margins of users. But as discussed before, wood pulp prices have

been trending down since 4Q15 on an abundant global supply, which we believe could

help offset the pressure of a depreciating CNY. For milk powder, we also believe a

weakening NZD against USD could help mitigate the pressure of increasing milk powder

costs, as New Zealand accounts for more than 50% of the milk powder imported into China

(in fact, the NZD has depreciated from NZD1:CNY4.8 a year ago to NZD1:CNY4.2 in

January 2016).

20

China Consumer Staples Sector: 26 January 2016

Valuations and recommendations

Rerating opportunity for selected stocks

The China Consumer Staples sector has been derated since 2013 on the back of slowing

revenue and earnings momentum. In 2015, the MSCI China Staples Index fell by 17.1%,

vs. declines of 14.6% in the MSCI China and 8.2% in the HSI. Our coverage universe of

downstream staples companies is trading currently at a 16x 2016E PER on a market-cap

weighted average, based on our forecasts, and most are trading below their past-5-year

12-month-forward PER bands.

MSCI China Staples and MSCI China Indices (2015)

The staples stocks have

underperformed the

MSCI China for the past 2

years

Source: Bloomberg

China players already trading at discounts to international peers

The China Consumer Staples stocks are currently trading at PER discounts to their

international downstream peers. Based on the Bloomberg consensus forecasts, the China

Consumer Staples stocks under our coverage are trading at 16x 2016E PER on average,

vs. 21x for the main US and Europe F&B players. As a result of our now less favourable

outlook for net-profit growth in 2016 in China due to a high base, macro headwinds, and

CNY depreciation, we see little potential for a PER rerating of the Chinese players towards

international peers’ valuations at this juncture. But at the same time, given that growth in

nominal GDP and personal income in China eclipses the growth rates for most developed

countries, as evidenced by the China players’ prospect of faster EPS growth in 2016E vs.

their international peers, we also see limited room for a further derating.

Davids’ premium to Goliaths justified, in our view

The Davids we highlighted in this report (Vinda, UPCH, etc) are trading at premiums to

their peers (Hengan, Tingyi) in terms of PER. We believe these premiums are justified by

the Davids’ higher prospective EPS growth in 2016-17E, on our forecasts, and their long-

term revenue growth potential. The key rerating catalysts we see are: 1) M&A within the

same industry/segment or strategic investments in new businesses, 2) successful new

product launches, and 3) share buybacks or debt reductions.

The only exception is Modern Dairy, which is trading currently at a 7.1x 2016E PER, a

significant discount to its peers Mengniu (15x) and Huishan (FY17E PER of 34x, March

year end). We believe this discount is due to investors’ concerns about flat raw milk ASPs

in 2016E. Nevertheless, we expect Modern Dairy shares to be rerated on the back of an

increasing revenue and earnings contribution from its downstream operation, and gross-

margin improvement from lower feed costs.

50

55

60

65

70

75

80

85

90

800

900

1,000

1,100

1,200

1,300

1,400

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

MSCI China Staples MSCI China

MSCI China Staples MSCI China

21

China Consumer Staples Sector: 26 January 2016

China Staples Sector: valuation comparison (as of 25 Jan 2016)

Market cap

Share price

(HKD)

PER (X) EPS growth YoY (%) EV/EBITDA Sales growth YoY

(%) EBIT margin

(%) ROE

Company Ticker Rating (USDm) 2014 2015E 2016E 2017E 2014 15E 16E 17E 15E 16E 2014 15E 16E 2014 15E 16E 15E

Food and beverage players

Want Want China 151 HK Buy 8,174 4.96 13.7 15.4 12.7 11.5 -10 -11 21 10 9.1 7.4 -1 -6 6 20.6 20.9 23.5 27.1

Tingyi 322 HK Hold 6,512 9.07 16.4 17.6 16.9 15.4 1 -7 4 10 7.5 6.7 -6 -9 1 7.2 8.1 8.7 12.0

WH Group 288 HK Outperform 8,247 4.40 8.5 13.6 10.2 9.1 48 -37 34 12 6.6 5.7 98 -1 6 8.1 6.4 6.9 11.3

Mengniu Dairy 2319 HK Hold 5,516 11.08 14.8 13.5 14.7 13.2 32 9 -8 11 8.8 9.1 15 -2 4 5.1 6.4 5.7 11.5

Tsingtao Brewery 168 HK Underperform 4,988 28.80 15.5 19.3 20.4 19.2 13 -20 -6 6 8.5 8.9 3 -3 -4 6.6 6.3 6.0 10.3

China Resources Beer 291 HK Hold 3,818 12.30 n.a. 34.1 23.2 18.5 -chg +chg 47 25 5.8 12.8 16 -79 4 1.1 7.9 8.6 2.7

Uni-President China 220 HK Buy 2,880 5.20 129.1 21.6 18.9 17.0 -74 499 14 11 8.0 7.1 -3 5 8 0.9 4.4 5.2 7.5

Market cap. Weighted average

20.4 17.8 15.6 13.9 9 24 15 12 7.8 7.9 23 -11 4 8.7 9.6 10.3 13.4

Dairy farm operators

Modern Dairy 1117 HK Buy 985 1.45 7.2 9.4 7.1 5.0 108 -23 31 41 5.5 6.4 53 -1 8 27.2 27.5 25.8 8.3

Huishan Dairy # 6863 HK Sell 5,095 2.95 43.0 43.5 34.4 29.6 -43 1 31 16 28.0 24.3 11 14 24 32.0 29.4 27.1 5.8

Market cap. Weighted average

37.2 38.0 29.9 25.6 -19 -3 31 20 24.3 21.4 18 12 21 31.2 29.1 26.9 6.2

Personal healthcare

Hengan Int 1044 HK Hold 10,621 67.75 21.2 19.4 18.4 18.2 8 9 5 1 11.7 11.3 12 2 -1 24.1 25.1 25.7 23.5

Vinda Int 3331 HK Outperform 1,664 13.00 21.9 27.2 22.8 15.0 9 -19 19 52 11.9 10.9 17 18 31 10.5 10.5 10.1 8.9

Market cap. Weighted average

21.3 20.5 19.0 17.7 8 5 7 8 11.8 11.2 13 4 4 22.3 23.2 23.6 21.5

Others

Fufeng 546 HK Hold 707 2.61 6.9 8.7 8.4 7.8 15 -21 4 8 4.6 4.4 -1 4 9 9.9 7.6 6.4 9.0

Source: Bloomberg, Daiwa forecasts Note: #FY15-18E numbers for Huishan are used as the company year-end is on 31 March;

International Staples Sector: valuation comparison (as of 22 January 2016)

Bloomberg Mkt.Cap. Price PER (x) EPS Growth EV/EBITDA x Revenue YoY % EBIT margin

Name Code LCY USDm

14 15E 16E 17E 14 15E 16E 17E 15E 16E 2014 15E 16E 15E 16E 16E

US major F&B players

Kraft-Heinz KHC US USD 90,269 74.39 55.5 34.2 25.1 20.6 n.a. 62 36 22 18.3 16.3 n.a. -6 -1 15.1 19.9 23.7

Coca Cola KO US USD 182,918 42.06 26.0 21.1 20.5 19.1 -16 23 3 7 17.0 16.5 -2 -4 0 21.1 23.0 23.6

Pepsi PEP US USD 139,639 95.85 22.2 21.0 19.9 18.5 -1 6 5 8 12.9 12.5 0 -5 1 14.4 15.9 16.2

General Mills GIS US USD 32,830 55.33 27.4 19.3 18.1 17.0 -30 42 7 7 12.2 11.9 -2 -5 1 11.8 16.6 17.0

Mondelez MDLz US USD 66,109 41.6 32.2 23.4 20.8 18.7 -1 38 13 11 16.3 15.2 -3 -17 0 9.5 15.9 15.0

Kellogg K US USD 25,378 71.61 40.7 20.5 19.5 18.3 -65 99 5 6 13.6 13.2 -1 -7 -1 7.0 14.1 14.7

Nestle NSRGY US USD 226,472 71.03 n.a. 21.1 20.0 18.8 45 n.a. 5 7 n.a. n.a. -1 -1 3 11.9 15.8 16.3

Market cap. weighted average

22.2 22.7 20.7 18.9 6 22 9 9 11.0 10.4 -1 -5 1 14.5 18.0 18.8

Global Dairy companies

Fonterra FCG NZ NZD 7,641 5.86 n.a. 13.6 12.2 11.3 190 n.a. 12 8 9.2 8.5 -15 6 13 4.3 7.1 n.a.

Danone BN FP EUR 55,794 59.61 31.7 20.6 19.3 17.7 -22 54 7 9 12.4 11.8 -1 6 3 10.2 12.7 13.3

Mead Johnson MJN US USD 13,831 70.16 19.8 20.7 20.0 18.6 5 -5 5 8 13.5 13.5 5 -8 -2 22.4 23.7 23.9

ABBOTT ABT US USD 59,714 40.03 26.7 18.6 17.2 15.3 -11 44 10 11 12.3 11.5 3 1 5 12.8 18.4 19.6

Market cap. weighted average

26.5 19.4 18.1 16.4 -3 40 8 10 12.3 11.6 1 3 4 12.2 16.0 16.4

International hog processors

TYSON FOODS-A TSN US USD 20,276 51.22 17.0 14.3 13.0 11.6 21 19 10 11 8.3 7.9 10 -4 2 5.2 6.2 6.5

SANDERSON FARMS SAFM US USD 1,750 77.54 8.1 14.4 13.3 15.9 -12 -43 8 -16 5.6 5.4 1 -3 9 12.0 7.2 5.2

PILGRIM'S PRIDE PPC US USD 5,526 21.66 7.9 7.9 10.8 12.3 30 1 -27 -12 4.8 6.3 2 -5 -1 14.0 13.7 9.9

HORMEL FOODS CRP HRL US USD 20,076 75.98 29.2 26.0 24.3 22.3 14 12 7 9 15.1 14.2 -1 4 4 11.5 12.3 12.8

INDUS BACHOC-B BACHOCOB MM MXN 2,164 66.55 10.2 9.4 12.1 11.5 93 9 -22 5 4.6 5.7 5 10 3 12.8 12.1 9.5

JBS JBSS3 BZ BRL 7,425 10.64 15.1 5.6 6.7 5.7 119 170 -15 17 5.2 4.2 30 37 26 6.5 6.4 6.2

Market cap. weighted average

19.6 16.5 15.9 14.8 35 33 1 8 9.7 9.3 8 5 6 9.0 9.3 9.1

Japanese player

ITOHAM FOODS INC 2284 JP JPY 1,304 625 11.5 20.9 19.7 17.6 143 -45 6 9 14.1 11.0 4 31 17 0.8 n.a. n.a.

NH FOODS LTD 2282 JP JPY 3,719 2,163 14.2 15.5 14.5 13.4 25 -8 5 8 8.5 8.0 8 4 2 4.0 3.5 3.8

Market cap. weighted average

13.5 16.9 15.9 14.5 57 -18 6 8 10.0 8.8 7 11 6 3.1 2.6 2.8

International personal hygiene products

9

PROCTER & GAMBLE PG US USD 210,464 77.36 30.9 20.6 18.3 16.8 -22 50 13 12 13.3 12.7 -5 -13 3 15.5 21.5 22.3

KIMBERLY-CLARK KMB US USD 45,999 126.72 31.1 22.0 20.6 19.1 -22 42 7 9 13.4 12.8 1 -6 2 12.8 17.3 17.9

Sven ska Cellulosa AB SCAB SS SEK 20,083 244.4 26.0 19.9 18.3 17.2 19 30 9 24 11.3 10.3 12 11 4 9.9 11.2 11.6

KAO CORP 4452 JP JPY 24,610 5,793 37.0 30.5 24.8 22.7 24 21 23 8 11.8 11.0 7 5 4 9.5 10.8 11.9

UNICHARM CORP 8113 JP JPY 11,285 2,156.50 33.6 35.6 27.2 24.2 -18 -5 29 8 12.7 11.5 21 25 9 11.2 10.3 10.8

Market cap. weighted average

31.2 22.1 19.5 17.9 -15 43 13 9 13.1 12.4 -1 -8 3 14.1 19 19.8

Source: Bloomberg

22

China Consumer Staples Sector: 26 January 2016

The Davids

Uni-President China (220 HK, HKD5.20): New products shine - upgrading to Buy (1)

In this report, we are upgrading our rating for UPCH to Buy (1), from Underperform (4), as

we expect its revenue growth to resume (5-8% YoY in 2015-17E, after a 4% decline in

2014) on likely market-share gains in the noodle segment and an increasing revenue

contribution from high-end beverage products. We believe UPCH can realise revenue

growth more easily than its biggest competitor, Tingyi, by improving its market-penetration

rate and focusing on high-value items. As a result of doing so, we expect its operating

margin to expand by 0.7pp and 0.3pp in 2016-17E to 5.2% and 5.5%, respectively, on our

forecasts, after a jump of 3.4pp in 2015E. UPCH’s share price is down by 27% from its 52-

week peak and is now trading at 19x 2016E PER, below its past-3-year average 12-month-

forward PER of 26x, which see as a good entry point. We have a new 12-month target

price of HKD6.20 (from HKD7.00), which is based on a 2016E PER of 22.6x (UPCH’s

average forward PER since its IPO in 2007).

UPCH: financial summary UPCH: share price and past-7-year PER band chart

2013 2014 2015E 2016E 2017E

Revenue (CNY m)

23,329 22,488 23,642 25,524 26,783

YoY (%)

9 -4 5 8 5

Our forecast vs. consensus (%) n.a. n.a. 5 5 8

Net profit (CNY m)

446 127 844 1,004 1,114

Net profit growth (%)

-48 -72 566 19 11

EPS (CNY)

0.12 0.03 0.20 0.23 0.26

EPS growth YoY (%)

-48 -74 511 19 11

Operating margin

2.0% 0.9% 4.4% 5.2% 5.5%

ROE

5.6% 1.3% 7.5% 8.3% 8.6%

Source: Company, Daiwa forecasts Source: Bloomberg

Vinda (3331 HK, HKD13.0): An emerging Asian play - reiterating Outperform (2)

We reiterate our Outperform (2) rating on Vinda. We argue that the stock should be rerated

on: 1) its transformation from a pure China tissue-paper manufacturer to a regional