Embed Size (px)

Citation preview

Chemical Logistics Cooperation in Central and Eastern Europe

SWOT‐Analysis

Italy

Weaknesses

Strengths

Opportunities

Threats

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 2/36

TABLE OF CONTENT 1 STRUCTURE .......................................................................................................................................................................... 4

2 INTORDUCTION TO REGION / COUNTRY ...................................................................................................................................... 5

2.1 SHORT DESCRIPTION OF THE PIEDMONT REGION .................................................................................................................. 5

3 DESCRIPTION OF CHEMICAL INDUSTRY ........................................................................................................................................ 7

3.1 SHORT DESCRIPTION OF THE CHEMICAL INDUSTRY AS AN INTRODUCTION: ................................................................................... 7 3.2 CHEMICAL SALES .......................................................................................................................................................... 8 3.3 COMPANY STRUCTURE – SIZE OF ENTERPRISES AND EMPLOYEES .............................................................................................. 8 3.4 INTERNATIONAL TRADE .................................................................................................................................................. 9 3.5 REGIONAL STRUCTURE OF CHEMICAL INDUSTRY ................................................................................................................. 10

4 DESCRIPTION OF TRANSPORT INFRASTRUCTURE .......................................................................................................................... 13

4.1 INTRODUCTION .......................................................................................................................................................... 13 4.2 INTERMODAL TRANSPORT ............................................................................................................................................. 13

4.2.1 ACTUAL AND PLANNED FIGURES ........................................................................................................................... 13 4.2.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE .................................................................................................... 14 4.2.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS .................................................................................................... 14

4.3 ROAD TRANSPORT ...................................................................................................................................................... 15 4.3.1 ACTUAL AND PLANNED FIGURES ........................................................................................................................... 15 4.3.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE .................................................................................................... 16 4.3.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS .................................................................................................... 16

4.4 RAILWAY TRANSPORT .................................................................................................................................................. 17 4.4.1 ACTUAL AND PLANNED FIGURES ........................................................................................................................... 18 4.4.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE .................................................................................................... 18 4.4.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS .................................................................................................... 19

4.5 WATERWAY TRANSPORT .............................................................................................................................................. 19 4.6 PIPELINE TRANSPORT (NOT GAS PIPELINES) ....................................................................................................................... 19

4.6.1 ACTUAL AND PLANNED FIGURES ........................................................................................................................... 19 4.6.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE .................................................................................................... 20 4.6.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS .................................................................................................... 20

5 DESCRIPTION OF CHEMICAL LOGISTICS IN THE REGION / COUNTRY .................................................................................................. 21

5.1 RELEVANCE OF THE LOGISTICS SECTOR IN GENERAL FOR PIEDMONT REGION: ........................................................................... 21 5.2 MAJOR LOGISTIC COMPANIES ....................................................................................................................................... 21 5.3 PRODUCTS TRANSPORTED ............................................................................................................................................ 21

6 INTERNAL STRENGTHS OF CHEMICAL COMPANIES AND LOGISTIC PROVIDERS ..................................................................................... 23

6.1 STRENGTHS IN PROCUREMENT ....................................................................................................................................... 23 6.2 STRENGTHS IN WAREHOUSING OF RAW MATERIALS, SEMI‐FINISHED AND FINISHED PRODUCTS.................................................... 23 6.3 STRENGTHS IN PRODUCTION LOGISTICS ........................................................................................................................... 23 6.4 STRENGTHS IN DISTRIBUTION AND TRANSPORT .................................................................................................................. 24 6.5 STRENGTHS IN PLANNING AND CONTROLLING ................................................................................................................... 24 6.6 STRENGTHS IN ORDER PROCESSING ................................................................................................................................ 24 6.7 STRENGTHS IN INFORMATION LOGISTICS .......................................................................................................................... 24

7 INTERNAL WEAKNESSES OF CHEMICAL COMPANIES AND LOGISTIC PROVIDERS ................................................................................... 25

7.1 WEAKNESSES IN PROCUREMENT .................................................................................................................................... 25 7.2 WEAKNESSES IN WAREHOUSING OF RAW MATERIALS, SEMI‐FINISHED AND FINISHED PRODUCTS .................................................. 25 7.3 WEAKNESSES IN PRODUCTION LOGISTICS ......................................................................................................................... 25 7.4 WEAKNESSES IN DISTRIBUTION AND TRANSPORT ............................................................................................................... 25 7.5 WEAKNESSES IN PLANNING AND CONTROLLING ................................................................................................................. 26 7.6 WEAKNESSES IN ORDER PROCESSING ............................................................................................................................... 26 7.7 WEAKNESSES IN INFORMATION LOGISTICS ........................................................................................................................ 26

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 3/36

8 EXTERNAL OPPORTUNITIES AND CHANCES FOR CHEMICAL LOGISTICS IN CENTRAL AND EASTERN EUROPE ................................................... 27

8.1 ECONOMIC TRENDS ..................................................................................................................................................... 27 8.2 SOCIOCULTURAL TRENDS .............................................................................................................................................. 27 8.3 TECHNOLOGICAL TRENDS .............................................................................................................................................. 27 8.4 ENVIRONMENT AND ENERGY ......................................................................................................................................... 27 8.5 POLITICS AND INNOVATION ........................................................................................................................................... 27 8.6 TRANSPORT INFRASTRUCTURE ....................................................................................................................................... 28

8.6.1 RAILWAY ........................................................................................................................................................ 28 8.6.2 WATERWAY ..................................................................................................................................................... 28 8.6.3 ROAD ............................................................................................................................................................. 28 8.6.4 INTERMODAL ................................................................................................................................................... 28 8.6.5 PIPELINE ......................................................................................................................................................... 28

8.7 SAFETY AND SECURITY ................................................................................................................................................. 29 8.8 INDUSTRY SECTOR AND COMPETITION .............................................................................................................................. 29

9 EXTERNAL THREATS, PROBLEMS AND BARRIERS FOR CHEMICAL LOGISTICS IN CENTRAL AND EASTERN EUROPE .......................................... 30

9.1 ECONOMIC TRENDS ..................................................................................................................................................... 30 9.2 SOCIOCULTURAL TRENDS .............................................................................................................................................. 30 9.3 TECHNOLOGICAL TRENDS .............................................................................................................................................. 30 9.4 ENVIRONMENT AND ENERGY ......................................................................................................................................... 30 9.5 POLITICS AND INNOVATION ........................................................................................................................................... 30 9.6 TRANSPORT INFRASTRUCTURE ....................................................................................................................................... 31

9.6.1 RAILWAY ........................................................................................................................................................ 31 9.6.2 WATERWAY ..................................................................................................................................................... 31 9.6.3 ROAD ............................................................................................................................................................. 31 9.6.4 INTERMODAL ................................................................................................................................................... 31 9.6.5 PIPELINE ......................................................................................................................................................... 32

9.7 SAFETY AND SECURITY ................................................................................................................................................. 32 9.8 INDUSTRY SECTOR AND COMPETITION .............................................................................................................................. 32

10 NEEDS FOR FURTHER ACTIONS AND IMPROVEMENTS ‐ CONCLUSIONS ............................................................................................... 33

10.1 REQUESTS TO POLITICAL/INSTITUTIONAL BODIES ........................................................................................... 33 10.2 REQUESTS TO PRIVATE LOGISTIC OPERATORS .................................................................................................. 33 10.3 REQUESTS TO PUBLIC LOGISTIC OPERATORS (RAILWAYS) ................................................................................ 33 10.4 REQUESTS TO CHEMICAL COMPANIES ............................................................................................................. 34

11 LITERATURE ....................................................................................................................................................................... 35

11.1 LIST OF RELEVANT LITERATURE, STUDIES, SURVEYS, POLICY DOCUMENTS .............................................................................. 35 11.2 LIST OF EXPERTS IN RSM ......................................................................................................................................... 36

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 4/36

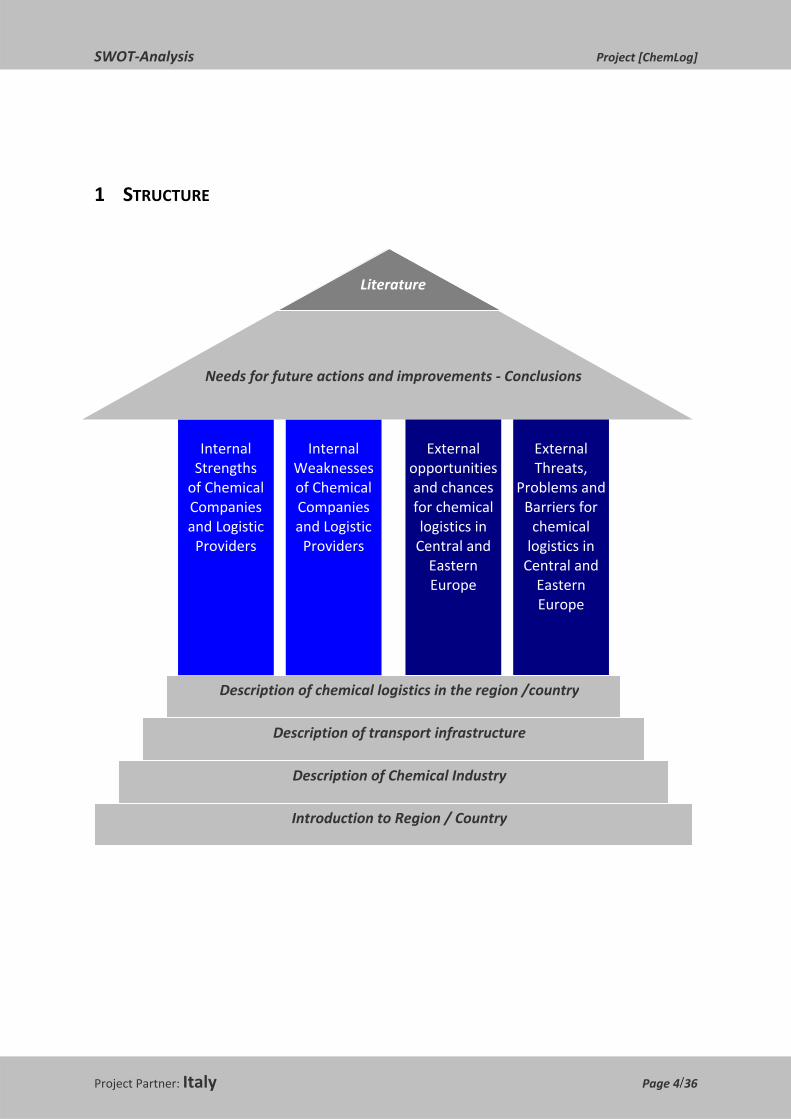

1 STRUCTURE

Introduction to Region / Country

Description of Chemical Industry

Description of transport infrastructure

Description of chemical logistics in the region /country

Internal Strengths of Chemical Companies and Logistic Providers

Internal Weaknesses of Chemical Companies and Logistic Providers

External opportunities and chances for chemical logistics in Central and Eastern Europe

External Threats,

Problems and Barriers for chemical logistics in Central and Eastern Europe

Needs for future actions and improvements ‐ Conclusions

Literature

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 5/36

2 INTRODUCTION TO REGION / COUNTRY

2.1 SHORT DESCRIPTION OF THE PIEDMONT REGION

Piedmont represents a hotbed of excellence over a landscape which is 38% plains, 33% hills and 29% mountainous terrain set to be the backdrop for the 2006 Olympic Winter Games.

One thousand kilometres of motorways, two thousand of railways with high capacity lines, one international airport located in the suburb of Turin (two if we consider also Milano‐Malpensa) and other four on its borders: Piedmont lives and works at the "centre of the world", and this is something which goes beyond geographic location. Criss‐crossed by a dense network of fibre optic cable which is constantly being extended, Piedmont is also a leader in sectors where technology has overtaken geography.

The economic sectors keep in touch with the rest of the world through their own "neighbourhood" airport: Malpensa, the largest hub in southern Europe, located in Lombardy Region although the nearest town is Novara, in Piedmont Region.

Piedmont exports vehicles, machinery and industrial plant, textile products, electrical machinery, and food, followed by minerals, rubber and plastics.

This all means that Piedmont exports a lot of high technology, but above all solutions which aim to enhance the quality of life.

Tradition and innovation are the two key words to understand Piedmont as it looks to the future: a region that accepts challenges and ‐ thanks to its pro‐active approach and deep‐rooted know‐how ‐ is capable of creating a virtuous circuit always ready to put forward new ideas and new products.

The region is first and foremost a "factory of stability", that has shown how it can develop its own economy not only in car production but also around the engineering industry, textiles, chemicals, food, aerospace and IT: this leadership has over time built up its industrial credibility and acted as a launching pad for the development of financial and service industries. This is the reason behind a greatly diversified economy in constant contact with the international markets, thanks also to a highly integrated transport system.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 6/36

But this equilibrium must be dynamic: Piedmont is also the "factory of innovation". 1.3 billion Euros are invested every year in research and development (16% of all Italian investment). This means that Piedmont creates one twelfth of national wealth and one sixth of "innovative thinking". This innovation is seen in one hundred research and development laboratories, a network of Science Parks throughout the region linked with the industrial districts, three universities connected to the most important academic seats in the world.

In the era of communications, travel and "visibility" Piedmont has opted to become an "open laboratory". A "factory" without boundary walls, which will make a name for it globally and be picked out time and time again.

To conclude, Piedmont has:

o 3 Universities with chemistry‐related departments o 25 Private and Public Research Centres (excluding the departments of the universities)

with recognized specialization in chemistry‐related topics o 4 Scientific & Technological Parks o 2 incubators o 2 Business Innovation Centres

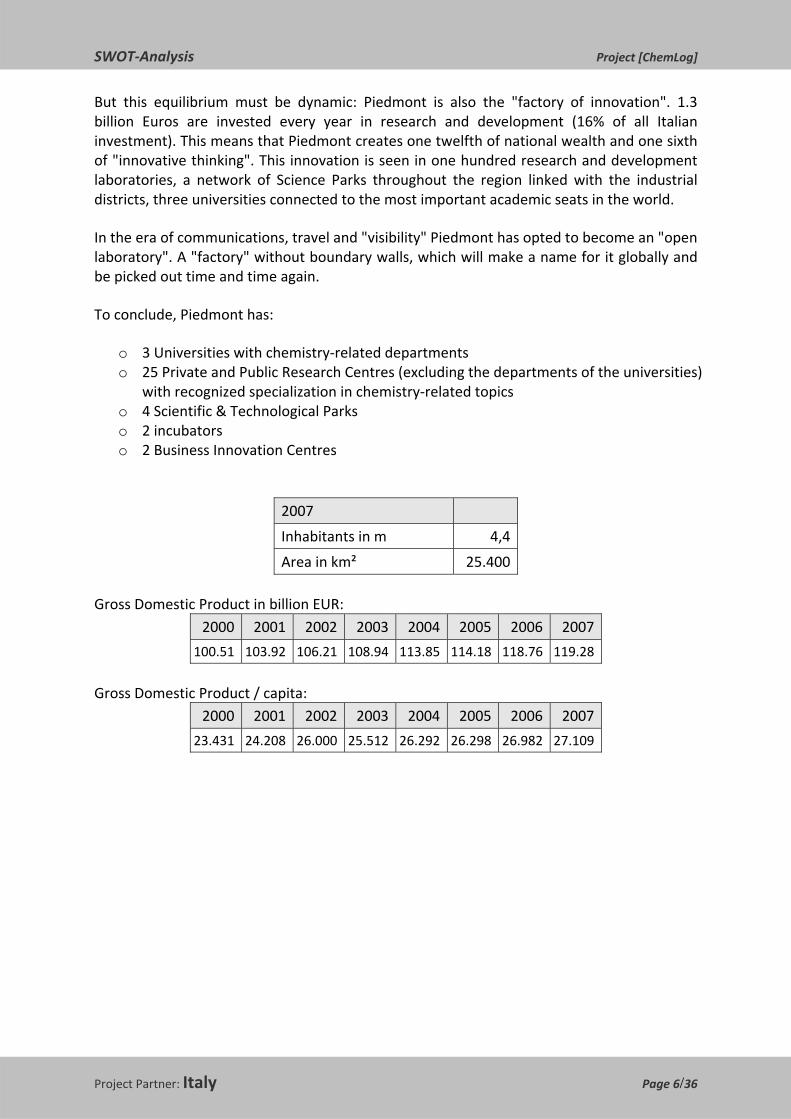

2007

Inhabitants in m 4,4

Area in km² 25.400 Gross Domestic Product in billion EUR:

2000 2001 2002 2003 2004 2005 2006 2007

100.51 103.92 106.21 108.94 113.85 114.18 118.76 119.28

Gross Domestic Product / capita:

2000 2001 2002 2003 2004 2005 2006 2007

23.431 24.208 26.000 25.512 26.292 26.298 26.982 27.109

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 7/36

3 DESCRIPTION OF CHEMICAL INDUSTRY

3.1 SHORT DESCRIPTION OF THE CHEMICAL INDUSTRY AS AN INTRODUCTION:

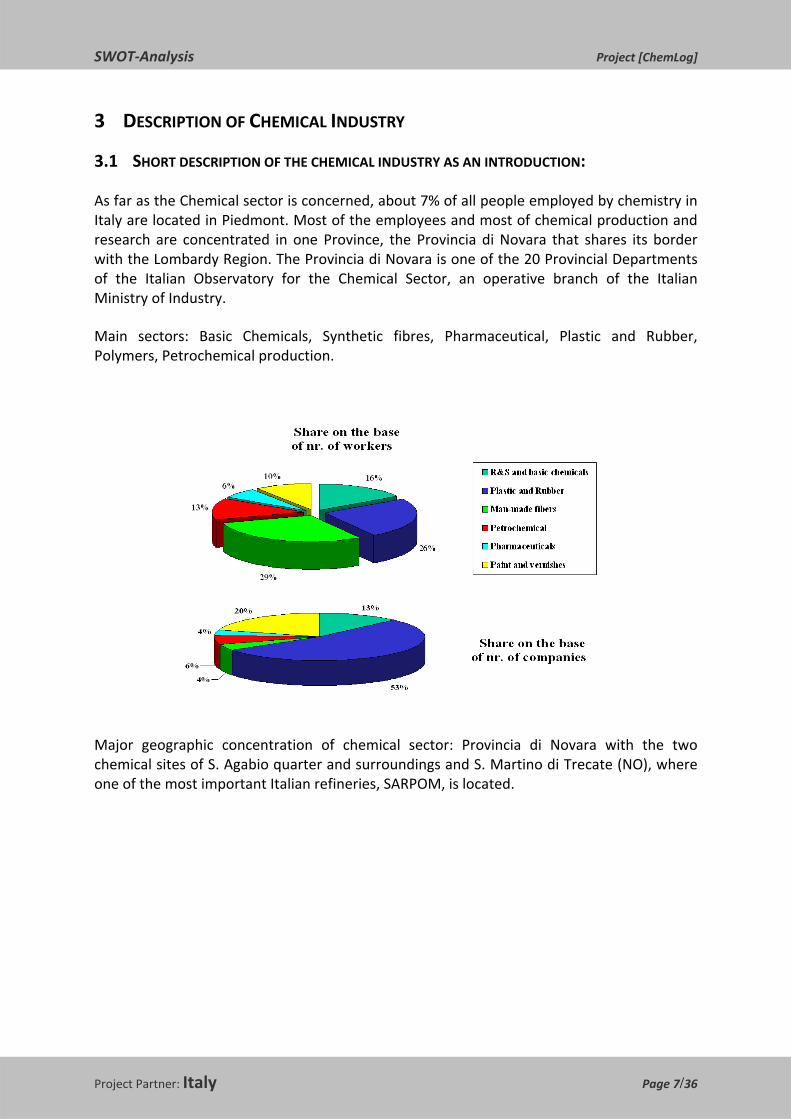

As far as the Chemical sector is concerned, about 7% of all people employed by chemistry in Italy are located in Piedmont. Most of the employees and most of chemical production and research are concentrated in one Province, the Provincia di Novara that shares its border with the Lombardy Region. The Provincia di Novara is one of the 20 Provincial Departments of the Italian Observatory for the Chemical Sector, an operative branch of the Italian Ministry of Industry.

Main sectors: Basic Chemicals, Synthetic fibres, Pharmaceutical, Plastic and Rubber, Polymers, Petrochemical production.

Major geographic concentration of chemical sector: Provincia di Novara with the two chemical sites of S. Agabio quarter and surroundings and S. Martino di Trecate (NO), where one of the most important Italian refineries, SARPOM, is located.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 8/36

3.2 CHEMICAL SALES Sales of chemical industry in Mio EUR: 2000 2001 2002 2003 2004 2005 2006 2007

Manufacture of basic chemicals*

Manufacture of pesticides and other agro‐chemical products

Manufacture of paints, varnishes and similar coatings, printing ink and mastics

Manufacture of pharmaceuticals, medicinal chemicals and botanical products**

Manufacture of soap and detergents, cleaning and polishing preparations, perfumes and toilet preparations

Manufacture of other chemical products***

Manufacture of man‐made fibres

Manufacture of chemicals and chemical products

5.227 4.765

Manufacture of rubber products****

Manufacture of plastic products*****

Manufacture of plastic and rubber products 4.281 4.577

Explanations: DF 23: 588 Mio (2004) and 882 Mio (2005) Share of chemical sales in processing industry

2000 2001 2002 2003 2004 2005 2006 2007

Manufacture of chemicals and chemical products

2,33 2,26

Manufacture of plastic and rubber product 1,91 2,17

3.3 COMPANY STRUCTURE – SIZE OF ENTERPRISES AND EMPLOYEES Number of enterprises 2000 2001 2002 2003 2004 2005 2006 2007

Manufacture of chemicals and chemical products

1121 1131 1137 1148 1101 1094 1121

1‐9 employees 583 588 591 597 573 569 583

10‐49 employees 292 294 296 298 286 284 291

50‐249 employees 179 181 182 184 176 175 179

250 ‐ … employees 67 38 68 69 66 66 68

Manufacture of plastic and rubber product 2074 2163 2190 2221 2276 2259 2241

1‐9 employees 1182 1233 1248 1266 1297 1288 1277

10‐49 employees 643 671 679 689 706 700 695

50‐249 employees 145 151 153 155 159 158 157

250 ‐ … employees 104 108 110 111 114 113 112

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 9/36

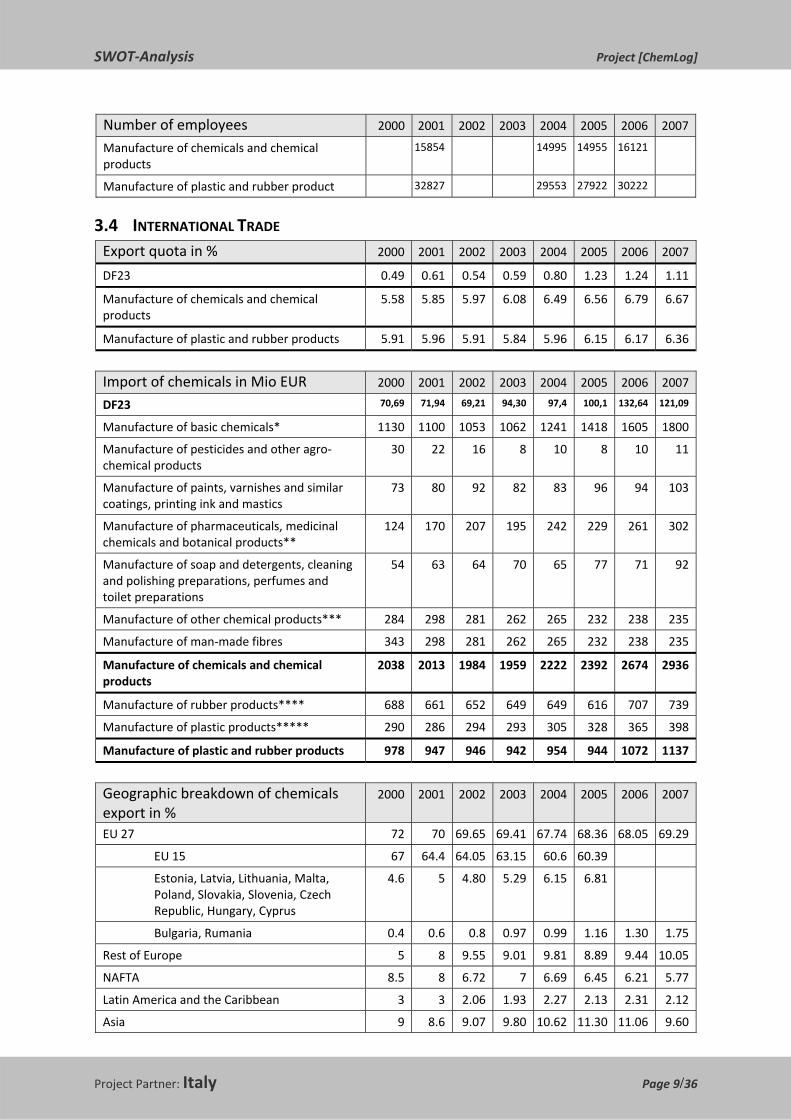

Number of employees 2000 2001 2002 2003 2004 2005 2006 2007

Manufacture of chemicals and chemical products

15854 14995 14955 16121

Manufacture of plastic and rubber product 32827 29553 27922 30222

3.4 INTERNATIONAL TRADE Export quota in % 2000 2001 2002 2003 2004 2005 2006 2007

DF23 0.49 0.61 0.54 0.59 0.80 1.23 1.24 1.11

Manufacture of chemicals and chemical products

5.58 5.85 5.97 6.08 6.49 6.56 6.79 6.67

Manufacture of plastic and rubber products 5.91 5.96 5.91 5.84 5.96 6.15 6.17 6.36

Import of chemicals in Mio EUR 2000 2001 2002 2003 2004 2005 2006 2007

DF23 70,69 71,94 69,21 94,30 97,4 100,1 132,64 121,09

Manufacture of basic chemicals* 1130 1100 1053 1062 1241 1418 1605 1800

Manufacture of pesticides and other agro‐chemical products

30 22 16 8 10 8 10 11

Manufacture of paints, varnishes and similar coatings, printing ink and mastics

73 80 92 82 83 96 94 103

Manufacture of pharmaceuticals, medicinal chemicals and botanical products**

124 170 207 195 242 229 261 302

Manufacture of soap and detergents, cleaning and polishing preparations, perfumes and toilet preparations

54 63 64 70 65 77 71 92

Manufacture of other chemical products*** 284 298 281 262 265 232 238 235

Manufacture of man‐made fibres 343 298 281 262 265 232 238 235

Manufacture of chemicals and chemical products

2038 2013 1984 1959 2222 2392 2674 2936

Manufacture of rubber products**** 688 661 652 649 649 616 707 739

Manufacture of plastic products***** 290 286 294 293 305 328 365 398

Manufacture of plastic and rubber products 978 947 946 942 954 944 1072 1137

Geographic breakdown of chemicals export in %

2000 2001 2002 2003 2004 2005 2006 2007

EU 27 72 70 69.65 69.41 67.74 68.36 68.05 69.29

EU 15 67 64.4 64.05 63.15 60.6 60.39

Estonia, Latvia, Lithuania, Malta, Poland, Slovakia, Slovenia, Czech Republic, Hungary, Cyprus

4.6 5 4.80 5.29 6.15 6.81

Bulgaria, Rumania 0.4 0.6 0.8 0.97 0.99 1.16 1.30 1.75

Rest of Europe 5 8 9.55 9.01 9.81 8.89 9.44 10.05

NAFTA 8.5 8 6.72 7 6.69 6.45 6.21 5.77

Latin America and the Caribbean 3 3 2.06 1.93 2.27 2.13 2.31 2.12

Asia 9 8.6 9.07 9.80 10.62 11.30 11.06 9.60

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 10/36

Africa 2 2 2.52 2.29 2.29 2.47 2.53 2.75

Australia / Oceania 0.5 0.4 0.43 0.56 0.58 0.40 0.40 0.42

Geographic breakdown of chemicals import in %

2000 2001 2002 2003 2004 2005 2006 2007

EU 27 81.89 80.20 79.03 80.30 79.83 80.44 80.48 80.40

EU 15 78.93 77.02 75.67 75.87 74.65 74.57

Estonia, Latvia, Lithuania, Malta, Poland, Slovakia, Slovenia, Czech Republic, Hungary, Cyprus

2.63 2.97 2.95 3.64 4.39 5.28

Bulgaria, Rumania 0.33 0.21 0.41 0.79 0.79 0.59 0.69 1.14

Rest of Europe 6.47 8.80 10.08 9.63 9.71 8.81 8.21 7.42

NAFTA 2.51 2.62 1.93 1.85 1.84 1.71 1.85 2.14

Latin America and the Caribbean 1 0.59 0.64 0.45 0.54 0.53 0.41 0.42

Asia 7.98 7.60 8.03 7.52 7.94 8.08 8.40 9.15

Africa 0.14 0.17 0.26 0.18 0.13 0.43 0.64 0.45

Australia / Oceania 0.01 0.02 0.03 0.01 0.01 0.01 0.01 0.02

3.5 REGIONAL STRUCTURE OF CHEMICAL INDUSTRY Major Companies and chemical sites Turnover 2007

in Mio EUR Location / chemical

site Number of employees

1. COLUMBIAN CARBON EUROPA SRL S. Martino di Trecate (NO)

2. ESSECO SPA4 S. Martino di Trecate (NO)

3. SUD CHEMIE MT SRL Novara

4. NOVAMONT SPA € 35 Novara 180

5. UNIVER ITALIANA SPA (Gruppo PPG Industries) Cavallirio (NO)

6. AKZO NOBEL CHEMICALS SPA € 28 Novara 65

7. COLORIFICIO I.CO.RI.P. SPA Oleggio (NO)

8. SICPA ITALIANA SPA S. Pietro Mosezzo (NO)

9. ISTITUTO BIOLOGICO CHEMIOTERAPICO SPA ‐ DIVISIONE UNIBIOS

Trecate (NO)

10. PROCOS SPA € 55 Cameri (NO) 230

11. DYNACREN SRL Castelletto T.(NO)

12. MIRATO NUOVA SPA5 Landiona (NO)

13. HB FULLER ITALIA SRL Borgolavezzaro (NO)

14. Vinavil S.p.A. (Gruppo MAPEI S.p.A.)1 €163 Villadossola (VB) 323*

15. ALCE SRL ‐ LABORATORIO MICROBIOLOGICO (Gruppo Mofin Alce)

Novara

16. IDROSOL S.p.A. (Gruppo F.A.R.) Novara

17. MEMC ELECTRONIC MATERIALS SPA2 €331 Novara 1250#

18. RADICI CHIMICA SPA € 200 Novara 320

19. KEMI S.p.A. S. Pietro Mosezzo (NO)

20. DONEGANI ANTICORROSIONE SRL Novara

21. ISAGRO RICERCA SRL €783 Novara 60

3

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 11/36

22. PRC TICINUM LAB SRL Novara

23. PROGE FARM SRL €4 Novara 13

24. SARPOM SPA (Esso Italiana Srl ‐ Gruppo EXXON CORPORATION)

S. Martino di Trecate (NO) 400

25. SIBA SRL Novara

26. Solvay Pharma S.p.A. Grugliasco (TO)

27. Powder Coatings (Gruppo PPG Industries) Felizzano (AL)

28. L’Oreal Italia S.p.A. Torino

29. UCB Pharma S.p.A. Pianezza (TO)

30. F.A.R. Fabbrica di Adesivi e Resine – Divisione Polioli

Vercelli

31. Rieter Automotive Fimit Spa Vicolungo (NO)

Leinì (TO)

Santhià (VC)

32. Mossi & Ghisolfi Group 1860 Tortona (AL) 1Plants of Milan, Ravenna and Villadossola (near Novara) 2MEMC SpA has two plants in Italy: Novara and Merano (BZ). In Novara was 832 in 2007. 3Isagro Italia S.p.A. 4Group Turnover 138,5 M Euro 5Group Turnover 129 M Euro

Explanations: 1. Manufacture and sale of carbon black. http://www.columbianchemicals.com/ 2. Esseco offers products that guarantee performance and safety in the field of sulfur chemistry and its derivates through certified processes, a constant structural innovation and attention to the needs of the market. http://www.esseco.com/ita/default.cfm 3. Production of catalysts for the industry. http://www.sued‐chemie‐mt.it/ 4. Producer of the Mater-Bi®, the first family of biopolymers that uses substances obtained from vegetables, like maize starch, whilst preserving the chemical structure generated by photosynthesis. http://www.materbi.com/ 5. Manufacturer of paints, varnishes and similar coatings http://www.univer.it/ 6. Production of thickeners. http://www.akzonobel.com/ 7. Production and packaging of water‐based paints and plastic wall coatings http://www.icorip.com/index_main.html 8. Leading global providers of security ink and solutions for the authentication of banknotes, value documents and products, as well as providers of integrated secure track and trace systems that monitor the journey of a product from manufacture to final point of sale. http://www.sicpa.com/58.asp 9. The chemical Unibios Division is dedicated to the production of chemical, biochemical and active ingredients for the pharmaceutical industry. The Unibios production is prevalently specialised in the manufacture of quinolones, antibacterial and antiviral drugs as well as enzymes. http://unibios.it 10. Pharmaceutical Fine Chemicals. http://www.procos.it 11. Production of patent registered medicines and generic medicines. http://www.dynacren.it/ 12. Production and distribution for "Beauty" products (i.e. cosmetics, soap and detergents, perfumes). http://www.mirato.it/home.php 13. Production of adhesives. http://www.hbfuller.com/ 14. VINAVIL, the most important Italian manufacturer of dispersion polymers and one of the largest in Europe. http://www.vinavil.it 15. ALCE srl LABORATORIO MICROBIOLOGICO is involved in the production of autochthonous natural starters, liquid and freeze‐dried lactic starters and blue moulds. http://www.mofinalce.it/ 16. Sodium hydrosuphite production. http://www.gruppofar.it/idrosol/ita/index.htm 17. MEMC is a global leader in the manufacture and sale of wafers and related intermediate products to the semiconductor and solar industries. http://www.memc.com/ 18. RadiciGroup's diversified businesses operate worldwide and are focused on Chemicals, Plastics, Synthetic Fibres and Textile Machinery. One of RadiciGroup's key strengths is the synergistic vertical integration of its polyamide chain. http://www.radicigroup.com/en/home/home.aspx

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 12/36

19. Kemi is a chemicals company which leads the way in the research and development of anti‐tack products, release agents and colour pastes for polyurethane. http://www.kemi.it/en/index.asp 20. Structural analysis, monitoring of corrosion and plant inspections. http://www.donegant.it/ 21. Research into new active principles; development of the product to permit its commercial registration; defence of the product to maintain its commercial usefulness. http://www.isagro.it 22. Analytical development and validation of methods relevant to the active pharmaceutical ingredients, to drug products and to pharmacokinetic studies. http://www.ticinumlab.com/ 23. Proge Fram S.r.l. supplies consultancy and services in the Research and Development (lactic acid bacteria), Analytical (microbiological analysis) and in the Regulatory Affairs field. http://www.progefarm.it/ 24. Production of about 7% of the oil derivatives used in Italy. It refines about 7.500.000 tons of crude oil per

year. http://www.esso.it/Italy‐Italian/PA/Operations/IT_Refining_Trecate.asp 25. Residual oil. http://www.sibabitumi.com/ 26. Pharmaceuticals. http://www.solvaypharmaceuticals.com/ 27. Powder coatings. http://corporateportal.ppg.com/ppg/ 28. Cosmetics and perfumes. http://www.loreal.it/_it/_it/index.aspx 29. Biopharma focused on severe diseases, allergy and epilepsy, antibody research. http://www.ucbpharma.com/ 30. Production of pure trimethylopropane (TMP). http://www.gruppofar.it/ 31. M&G Group is presently the world’s largest producer of PET for packaging applications and a technological

leader in the polyester market. http://www.gruppomg.com/ Data bases: http://www.italianbiotech.com http://www.guidamonaci.it/

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 13/36

4 DESCRIPTION OF TRANSPORT INFRASTRUCTURE

4.1 INTRODUCTION

The following description deepens a little bit extensions and characteristics of the main Piedmont intermodal hubs, the road and rail networks and gives some remarks about the future evolutions of the transport infrastructures.

4.2 INTERMODAL TRANSPORT

4.2.1 ACTUAL AND PLANNED FIGURES Goods traffic according to transport modes ‐ quantity Goods traffic in Mio tons 2000 2001 2002 2003 2004 2005 2006 2007

Total

Road 221 209 223 222 297 303

Railway 13 12 13 13 18 18

Inland waterway 0 0 0 0 0 0

Pipeline

Goods traffic – performance in 1000 tkm (quantity * km): Goods traffic in Mio tons 2000 2001 2002 2003 2004 2005 2006 2007

Total

Road

Railway

Inland waterway

Pipeline

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 14/36

Forecasts of the development of intermodal transport (quantities and terminals): According the section related the SWOT analysis, one of the weakness in distribution is the significant deficit in the railway connection to industrial sites. This prevents further shifts in traffic from road to rail.

4.2.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE

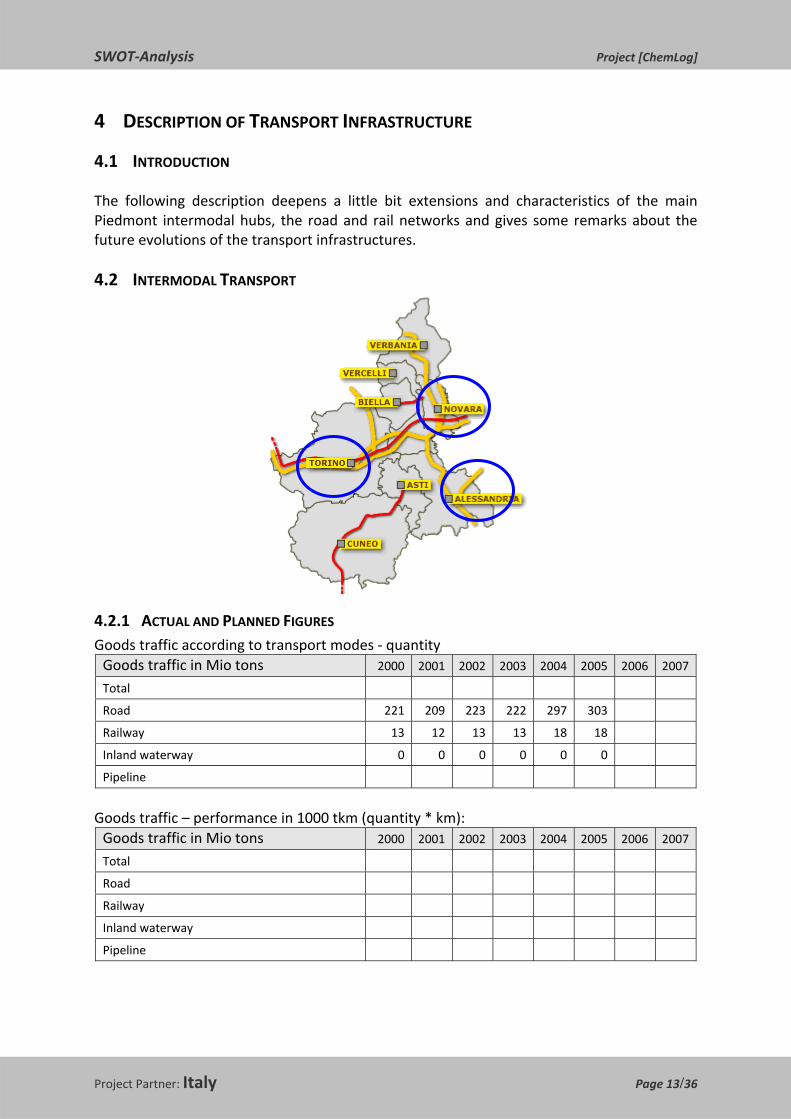

Piedmont (in Novara) is situated on the intersection of the European Corridor nr. 5, Lisboa‐Kiev, and the Axis 24, Genoa‐Rotterdam. This is the reason for the presence of three “Logistical poles”:

o Alessandria (Tortona, Rivalta Scrivia, Arquata Scrivia, Pozzolo Formigaro), where there are important Centres of Goods, appendix of Genoa Port. Now Alessandria is been developed as a main intermodal hub, particularly as interland hub of Genoa and Savona ports (3 years).

o Novara, where there is the C.I.M. Centro Interportuale Merci di Novara, important interport on the intersection of the European Corridor nr. 5, Lisboa‐Kiev, and the TEN 24, Genoa‐Rotterdam; near the Malpensa Hub, it can be the Landmark for the Central and Northern traffic of goods.

o Torino, where there is the S.I.TO. interport, located in one of the most populated and industrialized Italian areas, near to the French border.

4.2.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS Piedmont Region is currently defining the IV Regional Transport Plan, which reviews and redefines contents and strategically issues already presented in the previous 2004 Plan. The IV Plan will be focused on 2 fundamental requirements, which should be guaranteed:

o improving accessibility, both regional and interregional, by expanding and enlarging present regional facilities and by promoting the realization of major strategic projects;

o trying to reach a sustainable mobility. In order to satisfy these two main objectives and also to comply with the Regional Law number 336 “Rules and Guidelines for the integration of the transport systems and the development of regional logistics”, the IV Plan must include a territorial analysis, taking into account the merchandise flow, and define the foreseen logistic evolution.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 15/36

Most important scenarios of the logistic regional plan are: •the Novara logistic hub, which, thanks to its geographical position, will become in the next years a fundamental distribution centre of products coming from and going to the Mediterranean area and the Central/East Europe •The Orbassano (Turin) logistic pole, located on the Corridor 5 and central to the most densely populated area in Piedmont, with 2 main development lines:

- interconnection with high speed/high capacity lines, making so Orbassano a gateway to/from Europe

- “Logistic city “, oriented to become a regional distribution for the Turin metropolitan area, privileging the rail modality.

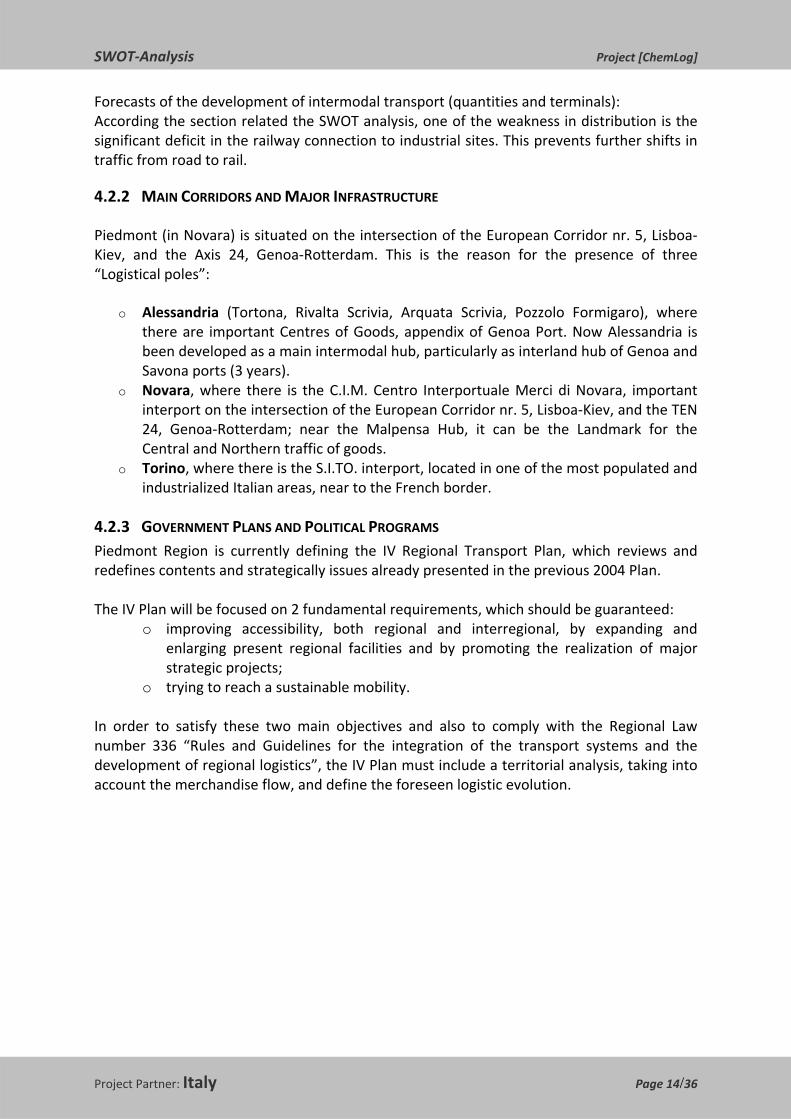

4.3 ROAD TRANSPORT

4.3.1 ACTUAL AND PLANNED FIGURES Actual and planned road network in km in operation in progress planned total

Highway 1000 ‐ ‐ 1000

State road 3000 ‐ ‐ 3000

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 16/36

Goods traffic in % according to traffic area ‐ road

2000 2001 2002 2003 2004 2005 2006 2007

Domestic traffic 97,92 97,47 97,30 97,49 97,55 97,40

Cross‐border entrance 1 1,20 1,34 1,20 1,10 1,23

Cross‐border dispatch 1,08 1,33 1,36 1,31 1,35 1,37

Transit ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

Other transportation abroad ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

Forecasts about development of road transport (quantities and terminals): In the medium period (3/5 years), without significant investments in rail infrastructures, the current trend to prefer road to rail will continue.

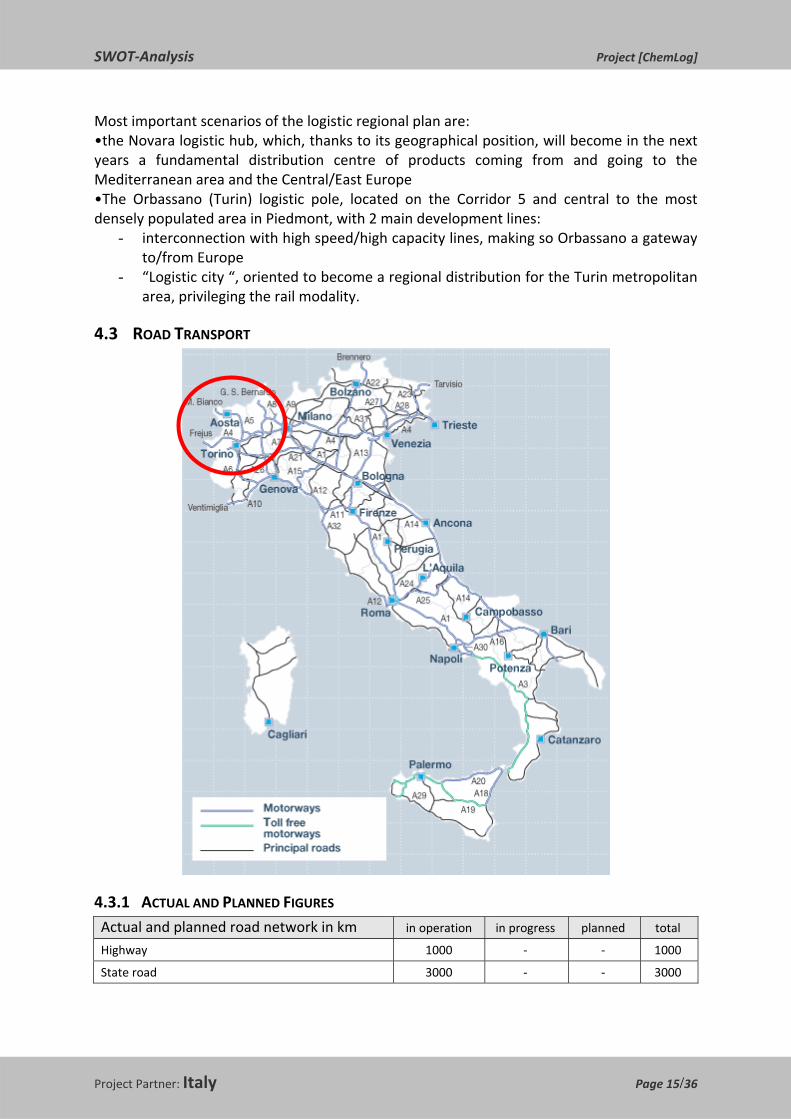

4.3.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE

Piedmont Highways Piedmont State Roads

4.3.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS A new transnational Region (Euro region) was created in July 2007, which encompasses 3 Italian Regions: Piedmont, Valle d’Aosta, Liguria, and 3 French Regions: Rhone‐ Alpes, Provence Alpes, Cote d’Azur.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 17/36

This “Euro region” covers an area with about 110.000 square Kilometres, with 16 m inhabitants, and its constitution is mainly aimed at reinforcing the already existing cross‐border cooperation in different fields, like:

o innovation o research and development o cross‐border traffic o accessibility o sustainable economic development

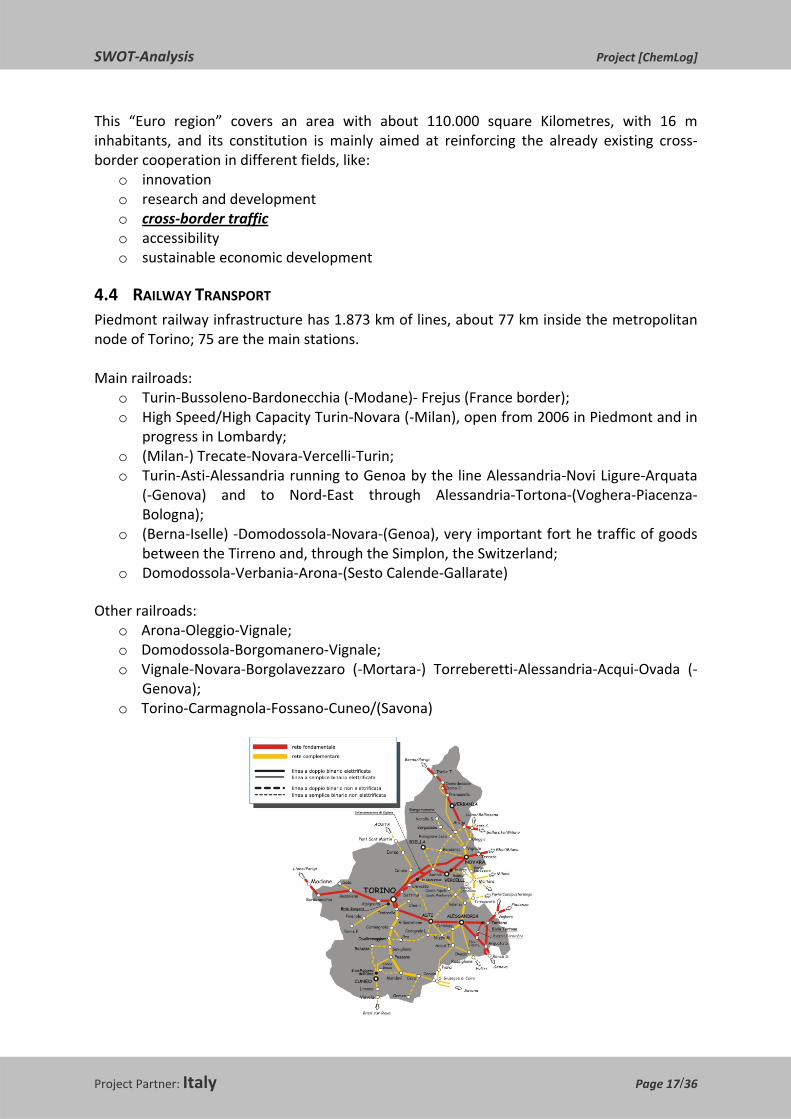

4.4 RAILWAY TRANSPORT Piedmont railway infrastructure has 1.873 km of lines, about 77 km inside the metropolitan node of Torino; 75 are the main stations. Main railroads:

o Turin‐Bussoleno‐Bardonecchia (‐Modane)‐ Frejus (France border); o High Speed/High Capacity Turin‐Novara (‐Milan), open from 2006 in Piedmont and in

progress in Lombardy; o (Milan‐) Trecate‐Novara‐Vercelli‐Turin; o Turin‐Asti‐Alessandria running to Genoa by the line Alessandria‐Novi Ligure‐Arquata

(‐Genova) and to Nord‐East through Alessandria‐Tortona‐(Voghera‐Piacenza‐Bologna);

o (Berna‐Iselle) ‐Domodossola‐Novara‐(Genoa), very important fort he traffic of goods between the Tirreno and, through the Simplon, the Switzerland;

o Domodossola‐Verbania‐Arona‐(Sesto Calende‐Gallarate) Other railroads:

o Arona‐Oleggio‐Vignale; o Domodossola‐Borgomanero‐Vignale; o Vignale‐Novara‐Borgolavezzaro (‐Mortara‐) Torreberetti‐Alessandria‐Acqui‐Ovada (‐

Genova); o Torino‐Carmagnola‐Fossano‐Cuneo/(Savona)

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 18/36

4.4.1 ACTUAL AND PLANNED FIGURES Actual and planned railway network in km in operation in progress planned total

Main railroads ‐ public 1873,3 80 20 1973,3

Standard gauge ‐ public

Narrow gauge – public

Private 122 ‐ ‐ 122

Total 1995,3 2095,3

Goods traffic in % according to traffic area ‐ railway

2000 2001 2002 2003 2004 2005 2006 2007

Domestic traffic

Cross‐border entrance

Cross‐border dispatch

Transit

Forecasts about development of railway transportation (quantities and terminals): See part two.

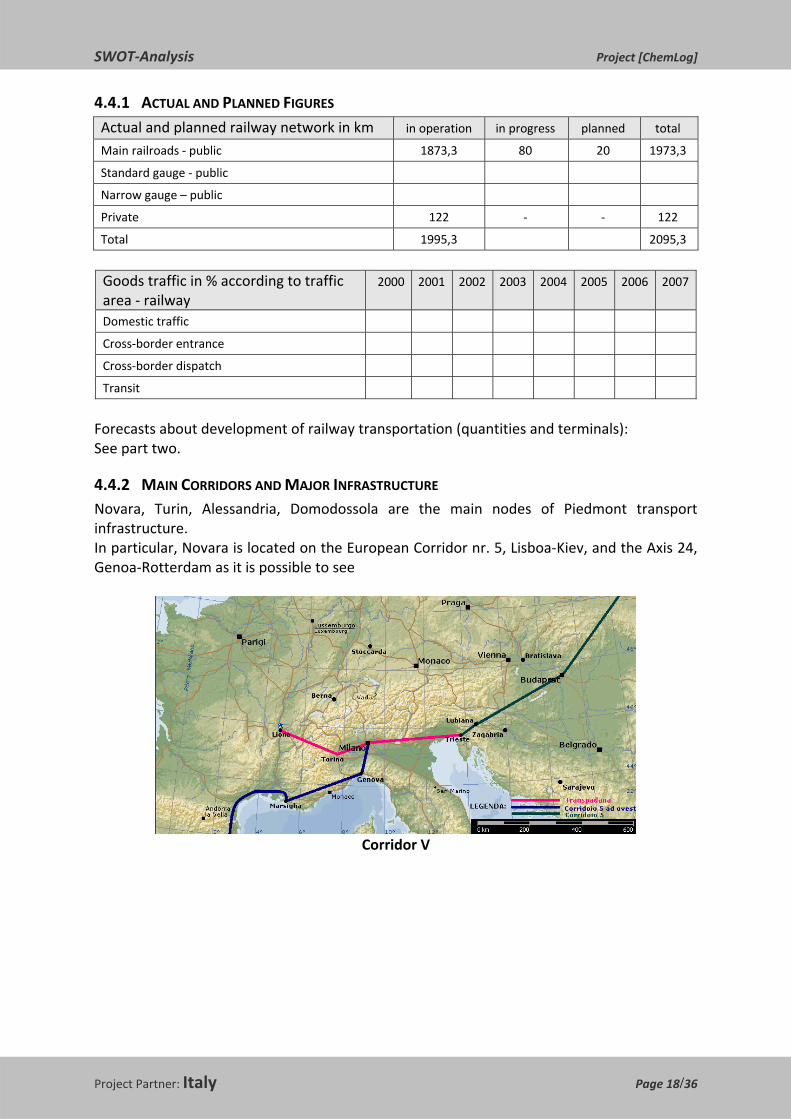

4.4.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE Novara, Turin, Alessandria, Domodossola are the main nodes of Piedmont transport infrastructure. In particular, Novara is located on the European Corridor nr. 5, Lisboa‐Kiev, and the Axis 24, Genoa‐Rotterdam as it is possible to see

Corridor V

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 19/36

Axis 24

4.4.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS Currently political attention is focused on passenger transportation; it is foreseen, however that, because of development of Alps transit development, political decision will be taken, in order to match the relevant railway traffic growth.

4.5 WATERWAY TRANSPORT There are no internal waterways in Piedmont.

4.6 PIPELINE TRANSPORT (NOT GAS PIPELINES)

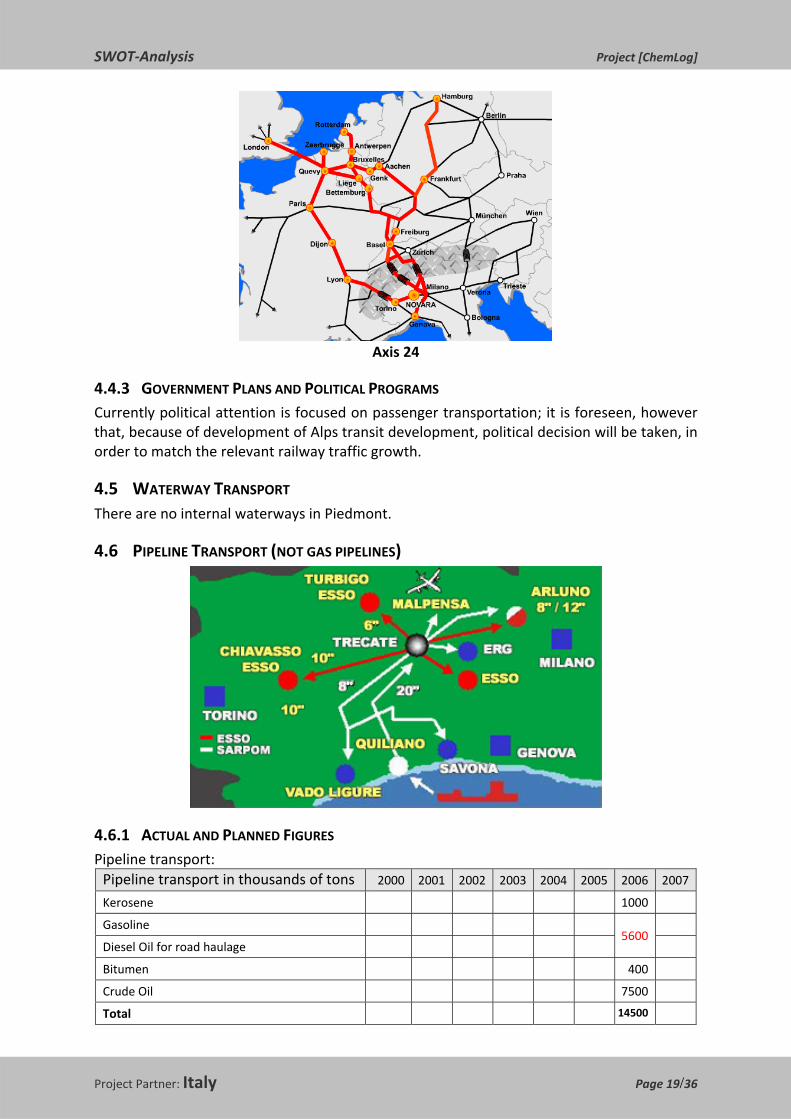

4.6.1 ACTUAL AND PLANNED FIGURES Pipeline transport: Pipeline transport in thousands of tons 2000 2001 2002 2003 2004 2005 2006 2007

Kerosene 1000

Gasoline 5600

Diesel Oil for road haulage

Bitumen 400

Crude Oil 7500

Total 14500

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 20/36

Explanations: Pipeline used for transporting Crude Oil (Quiliano‐Trecate) is about 150 km long. The other pipelines (10) are used for transporting chemical products‐ Globally the extension of the pipelines network centred in Piedmont is more than 700 km. Long. Forecasts about development of pipeline transport (quantities and terminals): No increase of the extension of pipelines is foreseen in the next 5 years. The percentage of different products transported through pipelines will probably change, with a growing share of lighter cuts.

4.6.2 MAIN CORRIDORS AND MAJOR INFRASTRUCTURE See chart; the control hub of the pipelines lies in S. Martino di Trecate, near Novara (15 km.). Note: the gas pipelines network in Piedmont is 2000 Km. long and the transported methane quantity is about 6 M m3 (2006).

4.6.3 GOVERNMENT PLANS AND POLITICAL PROGRAMS The development of pipeline network in Piedmont is currently only marginally considered at political level.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 21/36

5 DESCRIPTION OF CHEMICAL LOGISTICS IN THE REGION / COUNTRY

5.1 RELEVANCE OF THE LOGISTICS SECTOR IN GENERAL FOR PIEDMONT REGION: o number of logistics companies: 14.700 o gross added value of the sector: €7700 Mio o number of employees: 38.000

5.2 MAJOR LOGISTIC COMPANIES o Saima Avandero SpA o Gondrand SpA o Huktra Italia o Tts Multimodal Belgium o DHL Express o Cemat SpA o Norbert Dentressangle Italia o Satap SpA o Hupak SA o FNM SpA o Trenitalia Cargo SpA

5.3 PRODUCTS TRANSPORTED About the 75% of chemical products transported in Piedmont Region are crude oil and oil derivatives. Other main chemical products are Basic Chemicals, Synthetic fibres, Pharmaceutical, Plastic and Rubber, Polymers, Petrochemical production. Short description of chemical logistics in Piedmont region The current Piedmont situation for chemical logistics in very close to the National one: mainly road transportation, declining rail transportation, good usage of pipelines. As discussed in greater detail at the point 8.6.1, critical issues are related to railway services. Transported chemical goods – share of transportation modes Transported chemical goods – thousands of tons

2000 2001 2002 2003 2004 2005 2006 2007

Road 24280 25505 22896 24619 21572 24878

Railway 1839 1932 1735 1865 1634 1885

Intermodal 2575 2705 2428 2612 2288 2639

Pipeline 8094 8502 7632 8206 7191 8293

Total 36788 38644 34691 37302 32685 37695

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 22/36

RESULTS OF INDIVIDUAL INTERVIEWS WITH CHEMICAL COMPANIES AND LOGISTIC OPERATORS

THE FOLLOWING SECTION SUMMARIZES THE RESULTS OF INDIVIDUAL INTERVIEWS CONDUCTED WITH THE MOST SIGNIFICANT CHEMICAL INDUSTRIES AND LOGISTIC OPERATORS OF NOVARA PROVINCE, AS WELL AS INTERESTING HINTS /CONSIDERATIONS COLLECTED DURING THE FIRST STAKEHOLDERS’ MEETING HELD IN NOVARA ON MARCH,18 th ,2009 LIST OF INTERVIEWED COMPANIES/INSTITUTIONS

o ISAGRO RICERCA S.p.a. o AKZO NOBEL CHEMICALS S.p.a. o MAPEI S.p.a. – VINAVIL Division S.p.a. o MEMC S.p.a. o RADICI CHEMICALS S.p.a. o PROCOS S.p.a. o NOVAMONT S.p.a. o SARPOM S.p.a. o PROGE FARM S.r.l. o TICINUM LAB S.r.l. o HUPAC S.A. o HUKTRA Italia S.p.a. o C.I.M. S.p.a. o TRENITALIA S.p.a. o Assessorato allo sviluppo locale e politiche comunitarie – Prov. Novara o Assessorato all’urbanistica e piani territoriali – Prov. Novara o Assessorato attivita’ produttive – Trecate Municipality o A.I.N. (Novara Industrial Association) ‐ Novara o Eastern Piedmont University – Novara

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 23/36

6 INTERNAL STRENGTHS OF CHEMICAL COMPANIES AND LOGISTIC PROVIDERS

6.1 STRENGTHS IN PROCUREMENT Suppliers’ availability, reliability and flexibility The relationships with the suppliers are good; general policy is: at least 2 suppliers for products where availability is critical; for other products (commodities) the procurement is depending on price and lead time, sources can also be East Europe (e. g. Romania) or South/East Asia. Collaboration demand plan Some industries are production sites of multinational groups: in this case the procurement strategy is agreed upon with regional headquarters; others have different sites in different Italian regions: also here the demand planning is made on cooperative basis. Suppliers’ assessment For critical products it is very careful, with yearly revision on the basis of supply results/problems; other products, easily available, do not require special procurement attention.

6.2 STRENGTHS IN WAREHOUSING OF RAW MATERIALS, SEMI‐FINISHED AND FINISHED PRODUCTS

Safety stock level / inventory level Companies are generally satisfied with their stock management: no stock‐outs were mentioned, and both inventory levels and costs are under control. Warehouse infrastructures are adequate, as far as capacity and safety are concerned. Inventory strategy – outsourcing of warehousing Almost all companies visited have their own warehouse; some also use consignment stocks c/o their suppliers, if they are close to them. While outsourcing of warehousing is almost zero, total outsourcing is the strategy of Agro companies, in order to avoid costs and commitment needed by Seveso II regulations. SARPOM refinery is a story by itself: they manage a huge tank park autonomously, where both crude oil and intermediate products are stocked. This park is managed with the help of specific software.

6.3 STRENGTHS IN PRODUCTION LOGISTICS Complexity of production processes Production management inside the refinery is performed following ESSO know‐how (ESSO owns 75% of the refinery). Referring to medium‐large chemical companies operating in East Piedmont, processes are relatively stable and well known: almost all take advantage of an installed ERP/MRP package. Many small companies are mainly dedicated to research activity: their production is practically negligible (some tons/year).

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 24/36

6.4 STRENGTHS IN DISTRIBUTION AND TRANSPORT Distribution and transport are globally considered effective by companies, there are, however, some shadows, but they originate mainly not inside the industries but from logistic operators, especially railways and intermodal centres. Distance to customers / mode of transport For high value added products (pharma products, electronic basic materials), transportation to far customers is performed by air, from Milan Malpensa airport. The large majority of Italian/European destinations are reached via road transport; much less used is rail. Internal waterways do not exist in Piedmont; frequently destinations in Sicily and always in Sardinia are reached by sea, from Liguria harbours. Pipelines constitute by far the main transport mode for the refinery: it handles 7/8 m tons crude oil per year; oil is unloaded near Genoa and then stocked in a coastal tank park; from here it is sent to the refinery tank park through a 20”pipeline (150 km). 80% of the refinery output will be sent to 9 peripheral sites, always via pipelines (~ 300 km); the remaining 20% is shipped to final customers either by train or by road: good system of connections with both trunk roads and railway is a big asset for refinery. Outsourcing of transport Nearly 100% of the goods transport is outsourced to specialized operators. Communication & Coordination with logistic service providers Communication channels between chemical companies and logistic service providers are good, with the only remarkable exception of State Railways, with which the relationships are only fair, according to many local companies and need to be improved from the railway side.

6.5 STRENGTHS IN PLANNING AND CONTROLLING By interviewed people operational planning and controlling were considered not deserving of any particular attention: neither specific strengths nor weaknesses were mentioned.

6.6 STRENGTHS IN ORDER PROCESSING Order processing is generally supported by a software application that makes easier the operations; also here no particular mention was made by company representatives.

6.7 STRENGTHS IN INFORMATION LOGISTICS Medium/large companies take advantage of ERP/MRP packages in the main activity areas; EDI is largely used both by logistic companies and intermodal terminals.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 25/36

7 INTERNAL WEAKNESSES OF CHEMICAL COMPANIES AND LOGISTIC PROVIDERS General remarks:

o The dimension of most companies is small: 1‐49 employees o More than 50 % of the products are technologically obsolete, prone to competition

from emerging countries

7.1 WEAKNESSES IN PROCUREMENT This issue is rather considered as a strong point.

7.2 WEAKNESSES IN WAREHOUSING OF RAW MATERIALS, SEMI‐FINISHED AND FINISHED PRODUCTS

In Piedmont there is a shortage of company structures fully compliant with Seveso II norm. This shortage, meaning external storage and longer in and out travels, is causing increasing logistic costs. A general claim exists for bigger stock areas and intermodal hubs: the current situation c/o C.I.M. Novara, where storage and handling capacities are limited and are perceived as being critical.

7.3 WEAKNESSES IN PRODUCTION LOGISTICS Also this issue is considered by most companies as a strong point rather than as a weakness.

7.4 WEAKNESSES IN DISTRIBUTION AND TRANSPORT Delivery times The delivery time of merchandise loaded on single wagons, not on wagon blocks, is, to a certain extent, unstable. Tracking and tracing Sometimes, single wagons remain parked in intermediate stations for a long time, because they are “lost“ by the railway tracking system. Mode of transport There is lack of railway sidings not only for production companies, but also for distribution hubs: this makes modal transfer impossible. Novara suffers heavily from the single track connection between the shunting station in Borghetto and the very close intermodal hub (C.I.M.). Consolidated shipment on selected destinations All the air shipments, leaving from Malpensa, must be transported through Milan, because there, all the logistic operators consolidate the packages to be air shipped; this implies a double transport (forward and almost backward: Novara is much closer to Malpensa than Milan), with the likely delay of 1 day.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 26/36

Transport costs In the current economic downturn, customers order fewer quantities; in order to keep the agreed delivery times, a payload optimization is often unattainable: trucks are sent away without being fully loaded, with increased transport costs.

7.5 WEAKNESSES IN PLANNING AND CONTROLLING See point 5.5.

7.6 WEAKNESSES IN ORDER PROCESSING See point 5.6..

7.7 WEAKNESSES IN INFORMATION LOGISTICS This issue is considered not a weakness but a strong point.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 27/36

8 EXTERNAL OPPORTUNITIES AND CHANCES FOR CHEMICAL LOGISTICS IN

CENTRAL AND EASTERN EUROPE

8.1 ECONOMIC TRENDS o Piedmont is the second most important industrial region in Italy o Novara lies in the centre of the Italian industrial triangle (Milan, Turin, Genoa) o Novara is the most important chemical district in Piedmont (43% of C23+C24+C25

classes) and borders Lombardy, the heart of Italian chemical industry and second chemical region in Europe, after Nordrheinland‐Westfalen.

8.2 SOCIOCULTURAL TRENDS Educational standards

o two of the most famous Italian chemical research centres were established in Novara. o Piedmont hosts 2 University centres: Turin (its Study University was founded in 1404

and its Polytechnic founded in 1859), and the University of Eastern Piedmont, with two locations: Novara and Alessandria that hosts the chemical faculty.

8.3 TECHNOLOGICAL TRENDS All the interviewed companies agreed that the road traffic should be reduced in favour of railway use, but, as later mentioned in point 8.6, too many obstacles limit this option.

8.4 ENVIRONMENT AND ENERGY There is a trend in intercompany collaboration for the realization of cogeneration plants, where the global cost for electricity + steam is significantly reduced, compared to the traditionally separate production units. This is also a way to reduce CO2 emissions and, in general, environment pollution.

8.5 POLITICS AND INNOVATION RFI (the state‐owned railway company), TAV (the state‐owned high speed train company ), FNM (the private rail company), Piedmont Region, Novara Province and Municipality have designed (2002) a joint project for a new overall layout of Novara rail and road node, taking not only local short term needs into account, but also the foreseen development of the future cargo traffic flows.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 28/36

8.6 TRANSPORT INFRASTRUCTURE Novara lies at the intersection of 2 main European corridors: LISBON‐KIEV (C5) and ROTTERDAM‐GENOA (C 24).

8.6.1 RAILWAY Piedmont is the second Italian region with the largest railway extension and Novara is the hinge of rail traffic to/from France and Switzerland. Novara is one of two main Piedmont shunting stations A new cargo rail axis is being built between Novara and Vignale: this will allow traffic to/from Domodossola (Simplon) and to/from Luino (Gotthard). Besides Trenitalia (the state railway company), Novara is connected with Milan by a private railway company (F.N.M.), which operates on its own rail tracks.

8.6.2 WATERWAY There are no inland waterways in Piedmont.

8.6.3 ROAD Piedmont is the Italian region with largest motorway extension (800 km out of slightly more than 6500 km); Novara has direct access to 2 main Italian motorways:

• A4 ( Turin‐ Venice: East‐West ), and • A26 ( Gravellona T. – Genoa/Voltri: North‐South ).

8.6.4 INTERMODAL There are two main hubs in East Piedmont: Novara C.I.M., with its convenient geographic location, and Alessandria, which is now being completely rebuilt, to become the hinterland main hub for Genoa and Savona in 3 years Also Novara C.I.M. will undergo a major revamping (installation of new rail tracks more than 1000 m. long, to allow parking space for block trains). Strict cooperation between these two intermodal centres is foreseen, just to be prepared to serve the future traffic increase from North Europe, after the completion of Alp transit project.

8.6.5 PIPELINE Piedmont pipeline network has an extension of about 600 km , connecting 11 sites, all located in Northern Italy. The strategic node, controlling almost all the pipelines , is the SARPOM refinery in Trecate, 10 Km west of Novara.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 29/36

8.7 SAFETY AND SECURITY S.E.T. (Servizio Emergenza Trasporti) S.E.T. was constituted by Federchimica (the Italian federation of chemical companies) in 1998, to provide technical/operational support to the Public Authorities (mainly Fire Brigades), when managing emergency situations during the transport of chemical products. S.E.T. interventions are coordinated by the National Response Centre located near Venice, which in turn is in touch with more than 40 companies, mainly chemical industries, but also other entities with chemical competence, operating in the different Italian regions. Piedmont hosts 3 S.E.T. companies; one of these is located in Novara Province.

8.8 INDUSTRY SECTOR AND COMPETITION Big international players are now working towards a vertical integration of the supply chain that involves suppliers and customers. This process is slow and not completely transparent to local people, but will surely affect in deep the future strategy of the local subsidiaries. The other local companies suffer because of their small dimension; economies of scale are now being investigated, especially regarding logistic service suppliers ( activity fields are generally too different to allow real synergies ).

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 30/36

9 EXTERNAL THREATS, PROBLEMS AND BARRIERS FOR CHEMICAL LOGISTICS IN

CENTRAL AND EASTERN EUROPE

9.1 ECONOMIC TRENDS The IMF’s chief economist said 2009 would be the world economy’s worst year since end of II W.W. In January 2009 the IMF reduced its forecast of global G.D.P. growth to 0.5% from the 2.2% predicted last November. U.S. economy will shrink by 1.6%, European Union by 2% and Japan by 2.6%. •The economic slump will unavoidably delay/cancel investments already planned. In Italy, for the first time in 9 years, unemployment is rising again.

9.2 SOCIOCULTURAL TRENDS As consequence of rising unemployment an increase in conflicts between social parties is considered probable, eventually resulting in strikes and reduction of productivity.

9.3 TECHNOLOGICAL TRENDS Public acceptance of both road and rail new infrastructures is not guaranteed; the history of transalpine tunnel needed for the high speed train between Lyon and Turin is an enlightening example

9.4 ENVIRONMENT AND ENERGY The rail transport of dangerous goods, the most safe transport mode, is declining in favour of higher road utilization. Road traffic growth has a negative environmental impact; territorial plans are badly needed to achieve a balance between logistic development and environmental sustainability.

9.5 POLITICS AND INNOVATION There is no priority assignment to transport infrastructure development and relevant investments. Traffic transfer from road to rail cannot happen if the public railways operator destinates the lion’s share of investments to develop passenger traffic.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 31/36

Transregional integration of territorial development plans is difficult and slow. The bill for traffic congestion, especially in the big cities, is increasingly high: the Italian Automobile Club estimates (February 2009) that in 4 cities: Rome, Milan, Turin and Genoa wasted time in queues and gas emissions will cost 40 billions euro.

9.6 TRANSPORT INFRASTRUCTURE

9.6.1 RAILWAY There is a growing shortage of side tracks connecting the industrial sites: in spite of that, track dismantling goes on, compelling industries to choose road. The “rolling motorway” to/from Switzerland through the Simplon tunnel is accessible for trucks only from Novara: there is no other more northern access. Arcaic labour regulations and tasks definition reduce the productivity level of railway workers. Too often it happens that the industrial counterpart is seen by railway operator not as a customer to satisfy, but instead as a source of random interference.

9.6.2 WATERWAY There are no inland waterways in Piedmont.

9.6.3 ROAD Extraurban roads need interventions in order to enhance safety and discourage town crossing: there is a painful deficit in the availability of modern effective suburban road rings. Queues and congestion characterize motorway toll exits; solutions for the problem are already known, tested and implemented abroad. Sometimes investments for road improvements to make the traffic smoother are blocked by municipal rivalries or by misdirected opposition of so called “greens“.

9.6.4 INTERMODAL There is a lack of coordination and control by Authorities/Institutions, when new distribution centres are built: the inspiring strategy should be H&S (Hub & Spike), with a hierarchy of structures: big hubs, far from urban centres, where chemical products, especially the dangerous goods, can be safely stocked and managed; intermediate ones, smaller but closer to human settlements; finally, distribution facilities supplying the consumer directly. Instead, today many distribution hubs are located without considering how close they are to urban centres.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 32/36

Sometimes big hubs, otherwise efficient, lack adequate storage and handling capacity, especially for dangerous goods. In some harbours, rail tracks do not reach the docks, making intermodality difficult.

9.6.5 PIPELINE For Piedmont the current pipelines development is considered an asset.

9.7 SAFETY AND SECURITY All major chemical companies participate to Responsible Care Programs.

9.8 INDUSTRY SECTOR AND COMPETITION See point 7.8

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 33/36

10 NEEDS FOR FURTHER ACTIONS AND IMPROVEMENTS ‐ CONCLUSIONS What are the articulated needs of chemical enterprises and logistic providers for future action to improve framework conditions for chemical logistics in Central and Eastern Europe?

10.1 REQUESTS TO POLITICAL/INSTITUTIONAL BODIES o Political acceptance of and priority assignment to the investments required for

transport infrastructure. o Speed‐up planning/implementation of cross‐border traffic projects, especially for the

European corridors. o Define at a national/regional level a master plan related to the territorial use for

logistic purposes, privileging the H & S strategy. o Promote an international harmonization of the traffic governing rules, using ChemLog

project as resonance box. o Oblige new distribution hubs to be connected to the rail network through adequate

sidetracks.

10.2 REQUESTS TO PRIVATE LOGISTIC OPERATORS o Suggest development priorities in the transport and distribution field. To

political/institutional bodies. o Provide all intermodal centres with the necessary infrastructures to promote and

sustain intermodality. o Implement the H & S strategy when building new distribution centres, preventing

dangerous goods from being too close to human concentrations. o Actively support harbour interconnection with hinterland logistic infrastructures.

10.3 REQUESTS TO PUBLIC LOGISTIC OPERATORS (RAILWAYS) o Speed‐up the transition from bureaucratic/monopolistic culture and mentality to a

market driven habit (customer satisfaction is the real objective) o Attention and investments may not only be dedicated to passenger traffic, but also to

cargo transport. o Consider the big transalpine projects as a unique opportunity to encourage transition

from road to rail. o Reverse the current trend of eliminating secondary rail trunks and side tracks

connections, using them, instead to increase rail flexibility and capillarity, and consequently rail use.

o •Promote, at right audience levels, the message that rail is much safer and environmentally friendly than road.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 34/36

10.4 REQUESTS TO CHEMICAL COMPANIES o Initiate and strengthen all cooperation/synergy forms with different partners

(suppliers, customers,..), to reach a win‐win relationship. o Promote the creation of chemical clusters, in order to exchange know‐how and best

practices, and, therefore, matching market demands better. o Push for a ‘’ meeting table “, where industries, logistic operators and institutions can

directly talk to each other and agree upon investment priorities, development plans, territorial strategies.

o Promote alliances/cooperation/synergy among medium/small size industries, in order to increase international market access/penetration and to facilitate scale economy.

o Take advantage of the innovative landscape offered in Piedmont and, particularly, in Novara province by many research centres and small companies dedicated to R&D activity

o Support the growth of a sustainable chemical industry, actively participating to Responsible Care programs and sharing its philosophy.

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 35/36

11 LITERATURE

11.1 LIST OF RELEVANT LITERATURE, STUDIES, SURVEYS, POLICY DOCUMENTS www.istat.it www.coeweb.istat.it www.regione.piemonte.it/trasporti/rete/index.htm www.trail.pie.camcom.it www.rfi.it www.piemonteincifre.it www.italianbiotech.com www.guidamonaci.it/ L'industria chimica in Italia ‐ Rapporto 2007/2008 ‐ Federchimica Servizio Emergenza Trasporti ‐ Anno 2007 ‐ Federchimica Il trasporto merci pericolose in Piemonte ‐ A. Robotto, 12 novembre 2008 Emissione dei gas serra dai trasporti ‐ Eurostat/Apat Statistiche relative all'import export italiano ‐ Ministero del Commercio Internazionale, 2007 Trasporto merci nel settore italo‐francese dell'arco alpino ‐ Ministero delle Infrastrutture e dei Trasporti, 2005 Osservazioni e proposte su traffici marittimi e Mediterraneo ‐ Commissione Politiche Settoriali V, 1999 PON Trasporti 2000‐2006, Ministero delle Infrastrutture e dei Trasporti 14^ Rapporto Annuale Responsible Care 2008 ‐ Federchimica 3^ Rapporto S.E.T. – Anno 2007 ‐ Federchimica Il settore chimico in Italia – Alcuni elementi di analisi – Osservatorio per il settore chimico – Ministero per le Attivita’ Produttive, 2005 Il settore chimico in Italia – Osservazioni e proposte – CNEL, 2004 Il mercato dei servizi logistici e dei trasporti nell’Europa Comunitaria – M.Distinto, 2003 La politica dei trasporti nell’Unione Europea – La logistica ei container – G.Frego, Universita’ A.Avogadro , Novara, 2004 11.1.1.1 Panel congiunturale Federchimica – 2005 Norme e indirizzi per l’integrazione dei sistemi di trasporto e per lo sviluppo della logistica regionale – Regione Piemonte, 2008 Il futuro di Novara – Confronto per lo sviluppo di un territorio – Camera di Commercio di Novara, 2005 Il territorio – Fondazione Novara Sviluppo, 2005 Quadro analitico conoscitivo – Il contesto regionale/interregionale – Provincia di Novara, 2003 Il C.I.M. – Centro Interportuale merci di Novara,1999

SWOT‐Analysis Project [ChemLog]

Project Partner: Italy Page 36/36

11.2 LIST OF EXPERTS IN RSM Name Organisation Function Giovanni Pieri Provincia di Novara Consultant Antonio Santoro CISL Novara Secretariat Furio Bombardi Trenitalia Cargo Pricing Responsible Adriana Borrini Akzo Nobel Chemicals Supply Chain Responsible Carlo Meregaglia Mapei/Vinavil Logistics Responsible Fausto Giustetto Novara, Verbano Cusio

Ossola, Vercelli SME Association

Credit and Financing Responsible

Giovanni Antonio Dell’Aquila Politecnico di Torino Researcher Luca Terribile Hupac S.A. Business Development Luigi Panza Università del Piemonte

Orientale Chemical Faculty Representative

Gionanni Rossitti Associazione Industriali Novara

AIN Representative

Paola Borgini Huktra Italia Customer Service Giancarlo Rosina Comune di Trecate Town Councillor Lorenzo Volonté Comune di Trecate Town Councillor Roberto Vittorio Unione Italiana del Lavoro ‐

Novara Responsible

Federica Mastroianni Novamont SpA Special Projects Umberto Ruggerone CIM SpA Development Responsible Rossano Denetto Confartigianato Imprese

Novara VCO Transport Department Officer – ADR Consultant

Barbara Tosi Provincia di Novara Project Assistano ChemLog Marcello Miani Provincia di Novara Consultant – SWOT Analysis

Expert Valeria Galli Provincia di Novara Province Councillor Bruno Lattanzi Provincia di Novara Province Councillor Silvano Brustia Provincia di Novara Local Development and

European Policies Officer Antonella Tacca Provincia di Novara Local Development and

European Policies Office Maria Cristina Pavesi Provincia di Novara Local Development and

European Policies Office