Embed Size (px)

Citation preview

© OECD/IEA 2017 - 1© OECD/IEA 2017

System Integration of Renewables

Séminaire CFE31 March 2017, Paris

Cédric Philibert

Renewable Energy Division

© OECD/IEA 2016

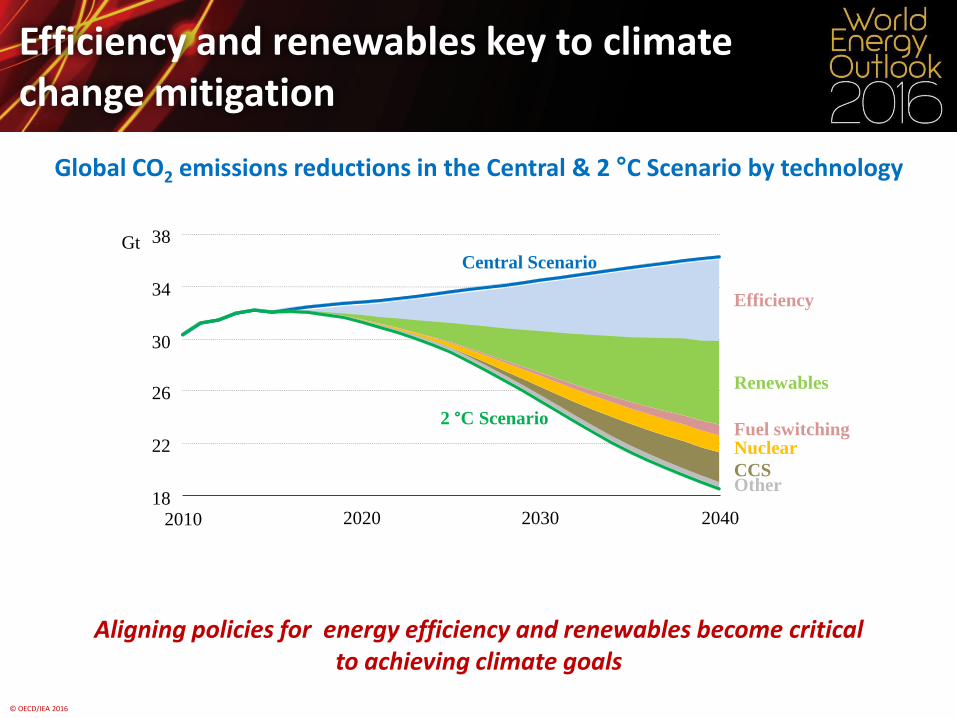

Efficiency and renewables key to climatechange mitigation

Global CO2 emissions reductions in the Central & 2 °C Scenario by technology

Aligning policies for energy efficiency and renewables become critical to achieving climate goals

Gt

18

22

26

30

34

38

2010 2020 2030 2040

Central Scenario

Efficiency

Renewables

CCS

NuclearFuel switching

Other

2 °C Scenario

© OECD/IEA 2016

1 000

2 000

3 000

4 000

TWh

1 500

3 000

4 500

6 000

TWh

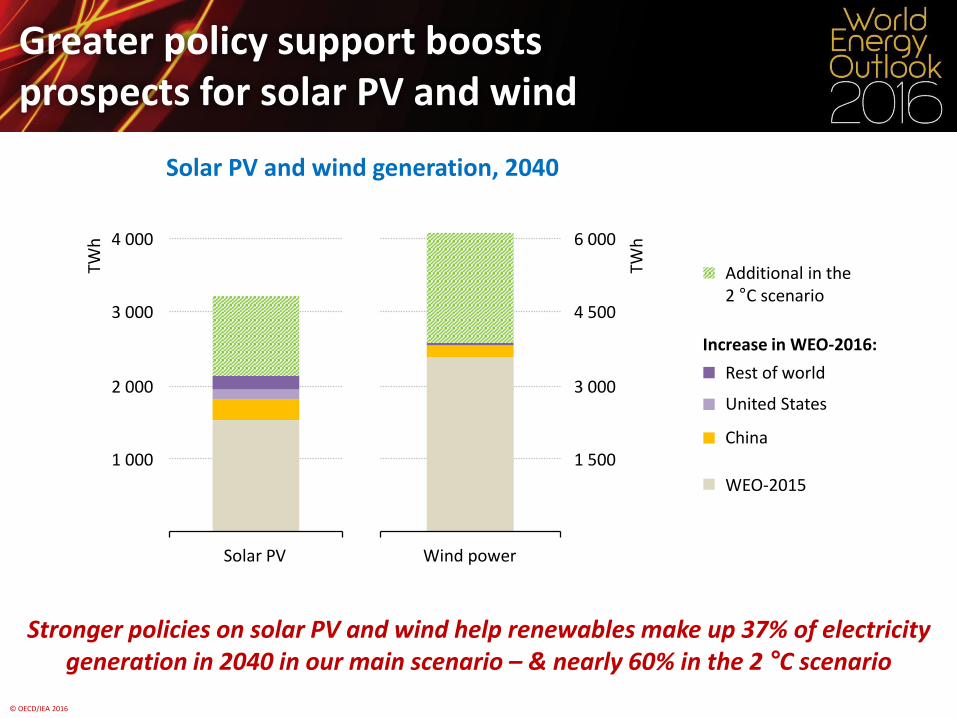

Greater policy support boostsprospects for solar PV and wind

Solar PV and wind generation, 2040

Stronger policies on solar PV and wind help renewables make up 37% of electricity generation in 2040 in our main scenario – & nearly 60% in the 2 °C scenario

Additional in the2 °C scenario

Rest of world

United States

China

WEO-2015

Increase in WEO-2016:

Solar PV Wind power

© OECD/IEA 2016

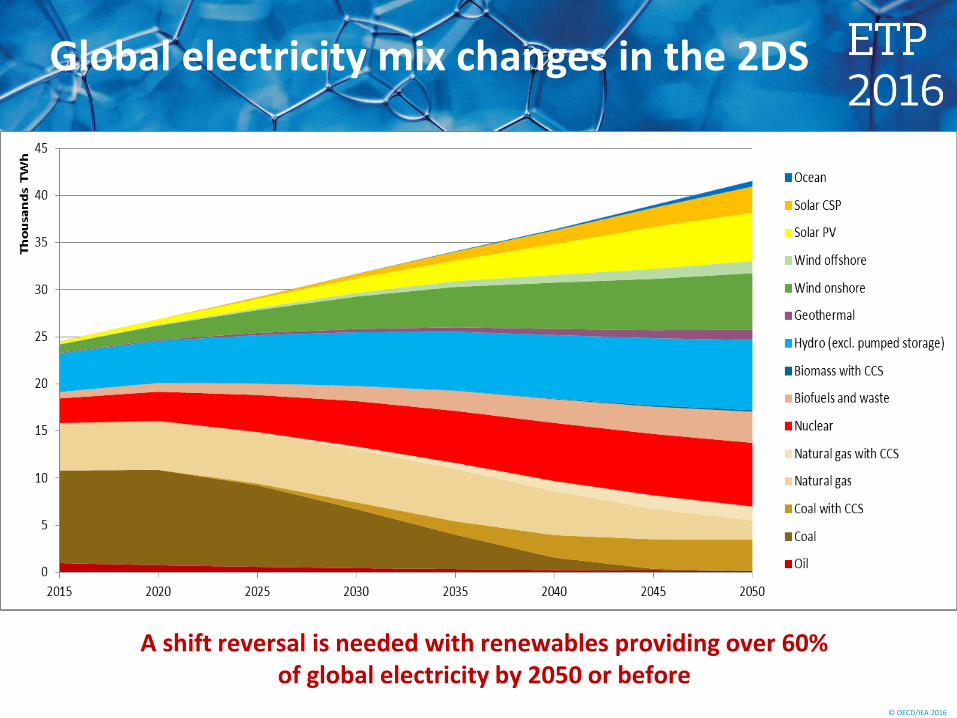

Global electricity mix changes in the 2DS

A shift reversal is needed with renewables providing over 60% of global electricity by 2050 or before

© OECD/IEA 2016

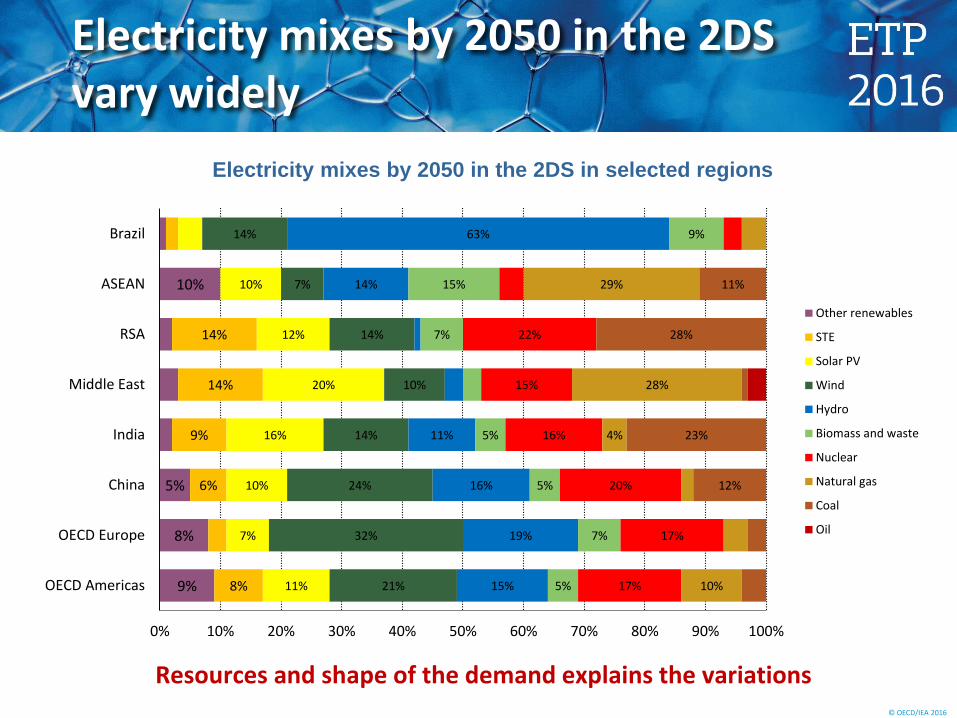

Electricity mixes by 2050 in the 2DS vary widely

Electricity mixes by 2050 in the 2DS in selected regions

9%

8%

5%

10%

8%

6%

9%

14%

14%

11%

7%

10%

16%

20%

12%

10%

21%

32%

24%

14%

10%

14%

7%

14%

15%

19%

16%

11%

14%

63%

5%

7%

5%

5%

7%

15%

9%

17%

17%

20%

16%

15%

22%

10%

4%

28%

29%

12%

23%

28%

11%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

OECD Americas

OECD Europe

China

India

Middle East

RSA

ASEAN

Brazil

Other renewables

STE

Solar PV

Wind

Hydro

Biomass and waste

Nuclear

Natural gas

Coal

Oil

Resources and shape of the demand explains the variations

© OECD/IEA 2017 - 6

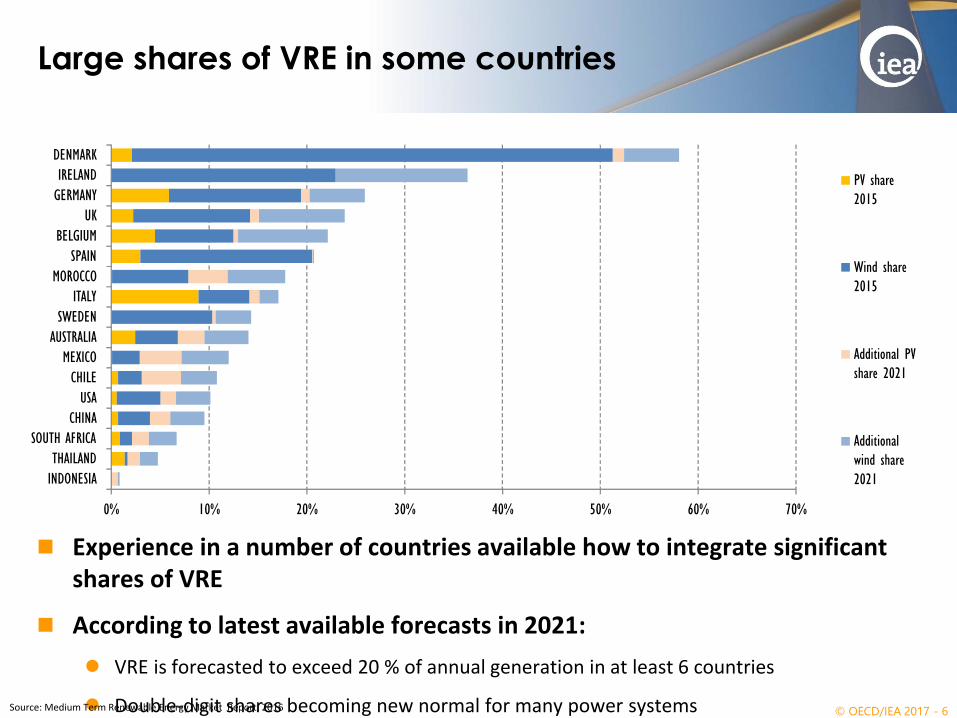

Large shares of VRE in some countries

Experience in a number of countries available how to integrate significant shares of VRE

According to latest available forecasts in 2021:

VRE is forecasted to exceed 20 % of annual generation in at least 6 countries

Double-digit shares becoming new normal for many power systemsSource: Medium Term Renewable Energy Market Report, 2016

0% 10% 20% 30% 40% 50% 60% 70%

INDONESIA

THAILAND

SOUTH AFRICA

CHINA

USA

CHILE

MEXICO

AUSTRALIA

SWEDEN

ITALY

MOROCCO

SPAIN

BELGIUM

UK

GERMANY

IRELAND

DENMARK

PV share

2015

Wind share

2015

Additional PV

share 2021

Additional

wind share

2021

© OECD/IEA 2017 - 7

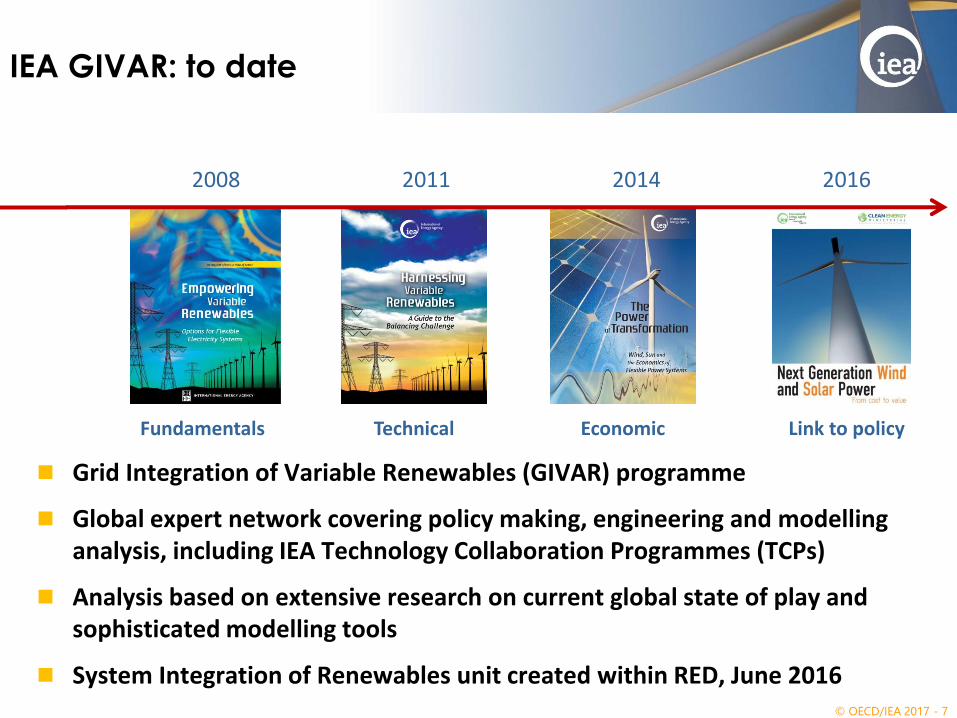

Grid Integration of Variable Renewables (GIVAR) programme

Global expert network covering policy making, engineering and modelling analysis, including IEA Technology Collaboration Programmes (TCPs)

Analysis based on extensive research on current global state of play and sophisticated modelling tools

System Integration of Renewables unit created within RED, June 2016

IEA GIVAR: to date

2008 2011 2014 2016

Fundamentals Technical Economic Link to policy

© OECD/IEA 2017 - 8

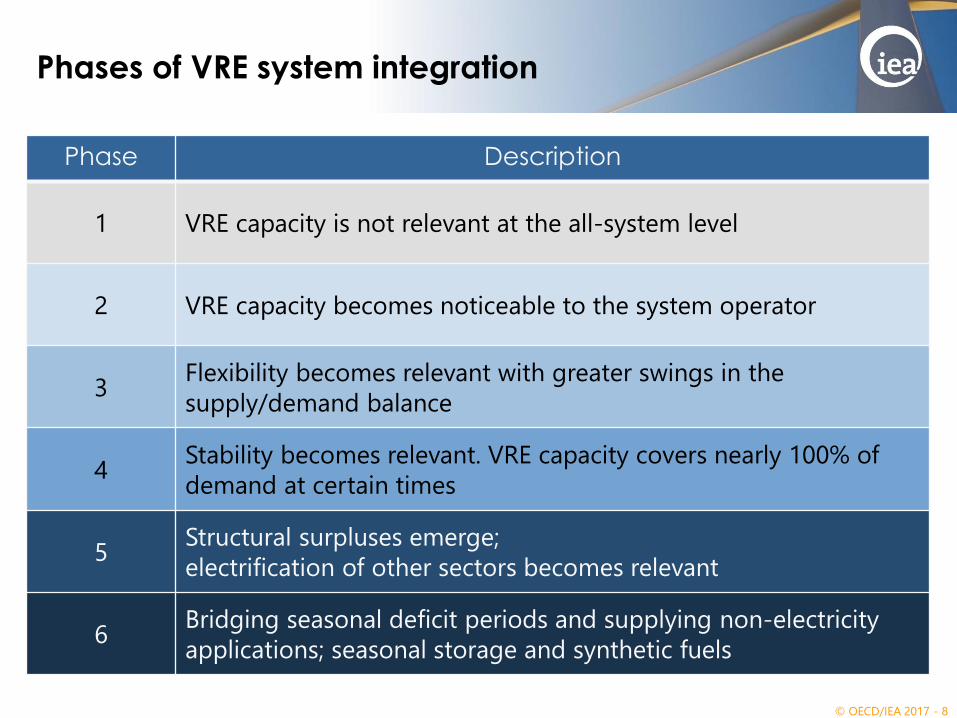

Phases of VRE system integration

Phase Description

1 VRE capacity is not relevant at the all-system level

2 VRE capacity becomes noticeable to the system operator

3Flexibility becomes relevant with greater swings in the

supply/demand balance

4Stability becomes relevant. VRE capacity covers nearly 100% of

demand at certain times

5Structural surpluses emerge;

electrification of other sectors becomes relevant

6Bridging seasonal deficit periods and supplying non-electricity

applications; seasonal storage and synthetic fuels

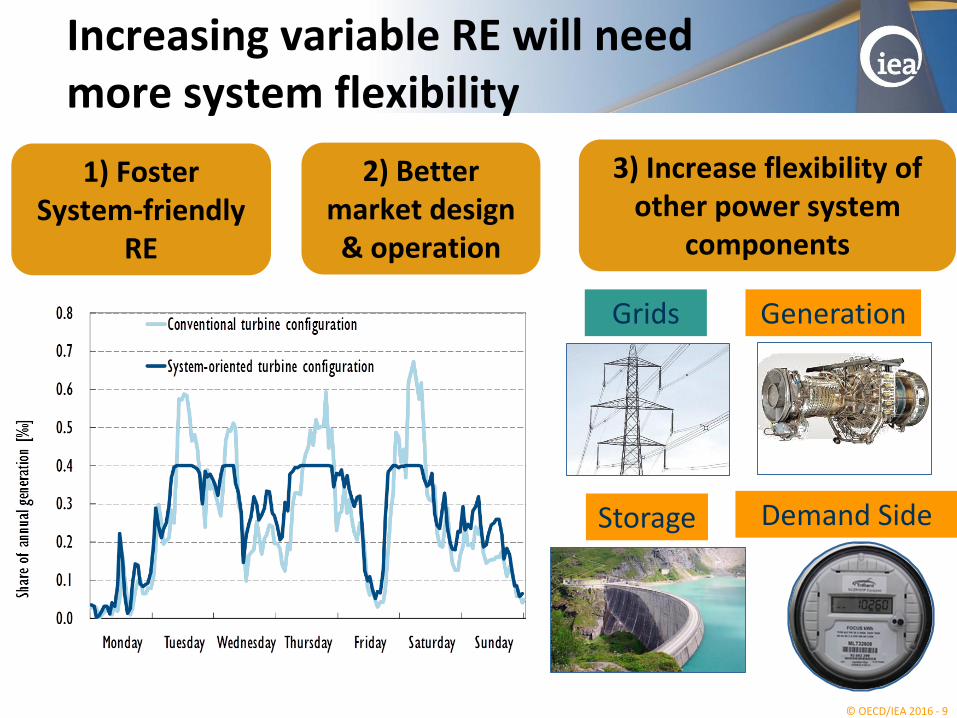

© OECD/IEA 2016 - 9

3) Increase flexibility of other power system

components

Grids Generation

Storage Demand Side

1) Foster System-friendly

RE

Increasing variable RE will need more system flexibility

2) Better market design & operation

© OECD/IEA 2017 - 10

Key point

New phase of wind and solar deployment:

Low-cost

Technologically mature

Requires new policies to achieve integration:

Focus on generation cost no longer enough

Policies need to consider system-wide impact

Case studies with specific recommendations:

Brazil, China, Indonesia,

Mexico, South Africa

Strong focus on country implementation

Next-generation wind and solar PV need ‘next-generation policies’ focusing

on system value and not just costs.

Next Generation Wind and Solar Power

© OECD/IEA 2017 - 11

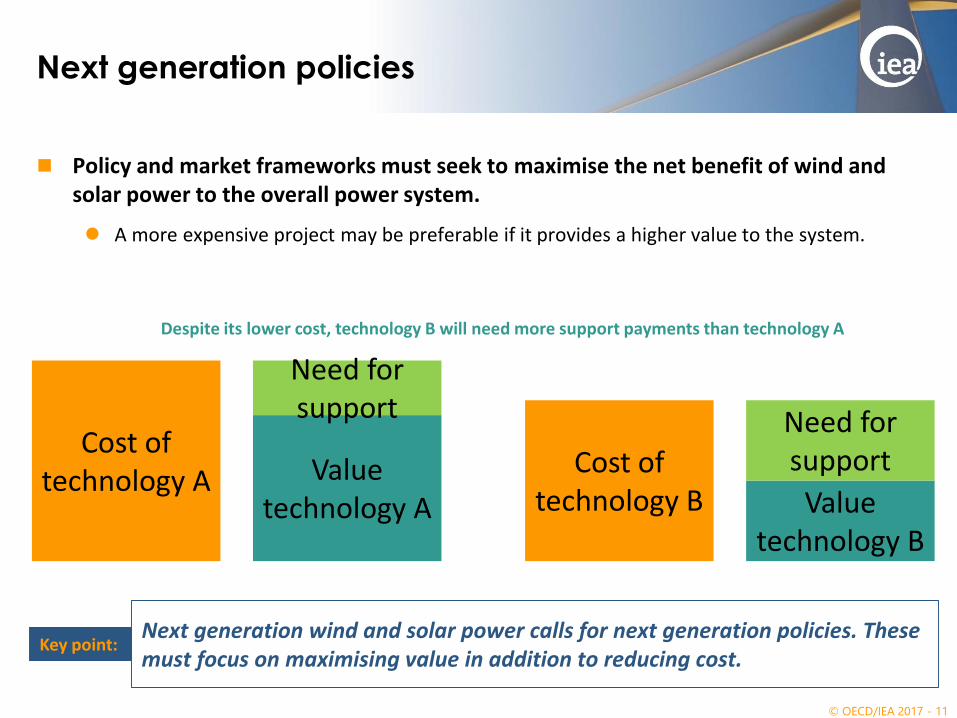

Key point:

Next generation policies

Policy and market frameworks must seek to maximise the net benefit of wind and solar power to the overall power system.

A more expensive project may be preferable if it provides a higher value to the system.

Next generation wind and solar power calls for next generation policies. These must focus on maximising value in addition to reducing cost.

Despite its lower cost, technology B will need more support payments than technology A

Cost of technology A

Cost of technology B

Value technology A Value

technology B

Need for support Need for

support

© OECD/IEA 2017 - 12

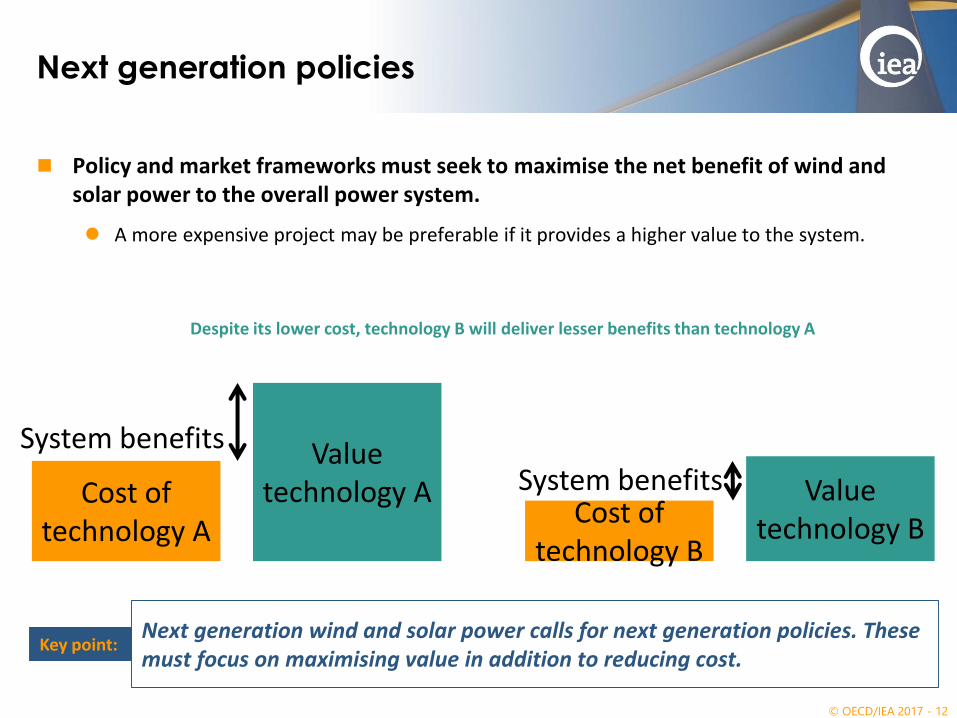

Key point:

Next generation policies

Policy and market frameworks must seek to maximise the net benefit of wind and solar power to the overall power system.

A more expensive project may be preferable if it provides a higher value to the system.

Next generation wind and solar power calls for next generation policies. These must focus on maximising value in addition to reducing cost.

Despite its lower cost, technology B will deliver lesser benefits than technology A

Cost of technology A

Cost of technology B

Value technology A Value

technology B

System benefits

System benefits

© OECD/IEA 2016 - 13

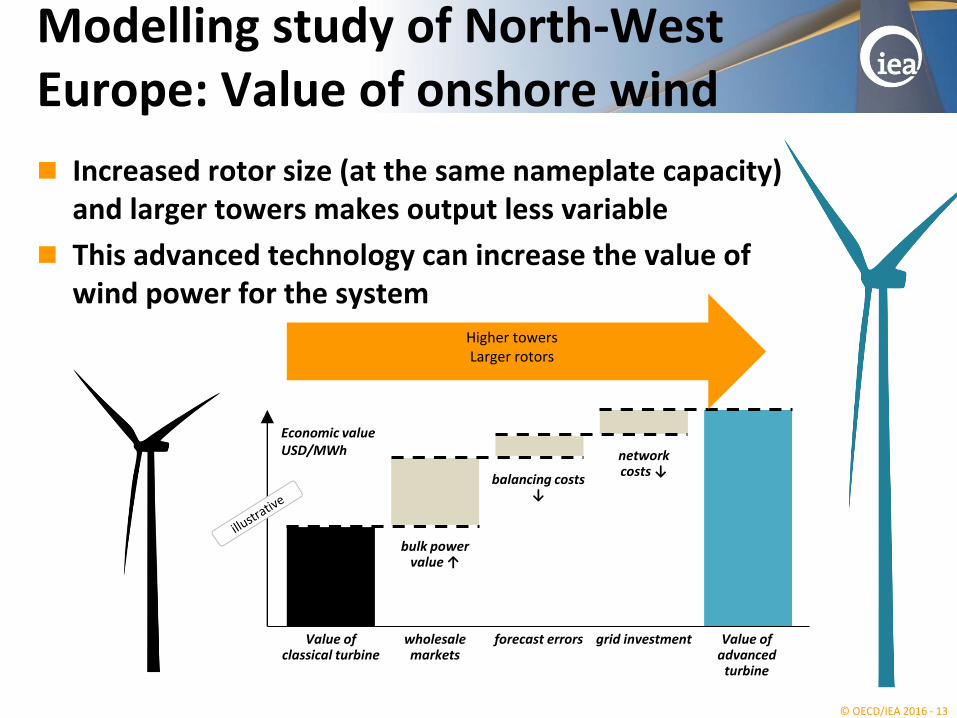

Modelling study of North-West Europe: Value of onshore wind

Increased rotor size (at the same nameplate capacity) and larger towers makes output less variable

This advanced technology can increase the value of wind power for the system

Value ofclassical turbine

Economic valueUSD/MWh

Value of advanced

turbine

bulk power value ↑

networkcosts ↓

balancing costs ↓

wholesalemarkets

forecast errors grid investment

Higher towersLarger rotors

© OECD/IEA 2016 - 14

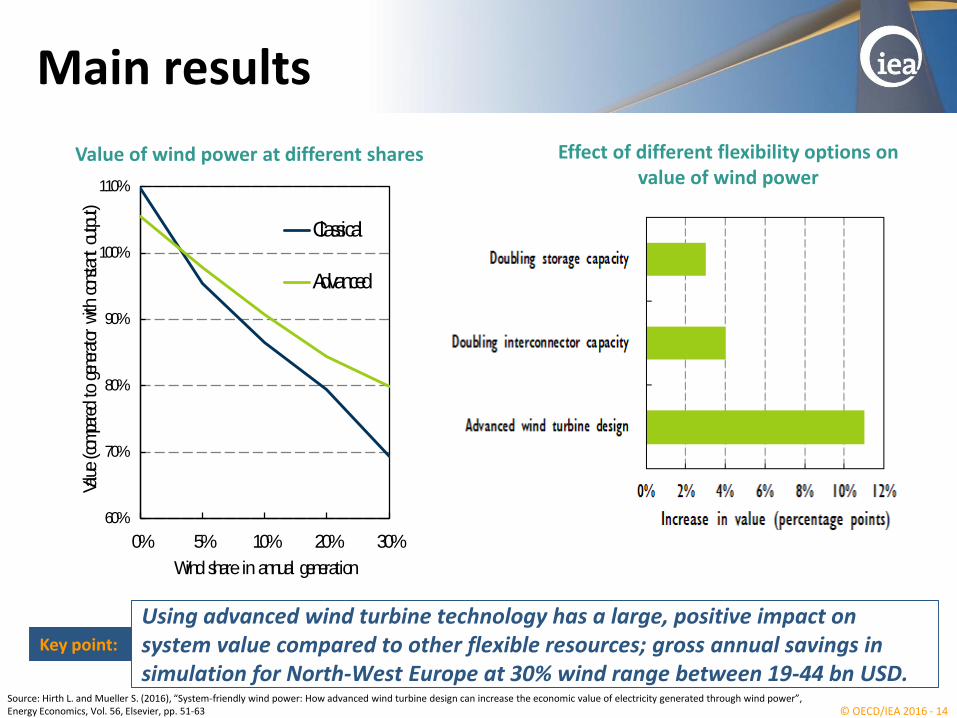

Key point:

Main results

Using advanced wind turbine technology has a large, positive impact on system value compared to other flexible resources; gross annual savings in simulation for North-West Europe at 30% wind range between 19-44 bn USD.

60%

70%

80%

90%

100%

110%

0% 5% 10% 20% 30%

Value

(com

pare

d to

gen

erat

or w

ith c

onstan

t ou

tput

)

Wind share in annual generation

Classical

Advanced

Value of wind power at different shares

Source: Hirth L. and Mueller S. (2016), “System-friendly wind power: How advanced wind turbine design can increase the economic value of electricity generated through wind power”, Energy Economics, Vol. 56, Elsevier, pp. 51-63

Effect of different flexibility options on value of wind power

© OECD/IEA 2017 - 15

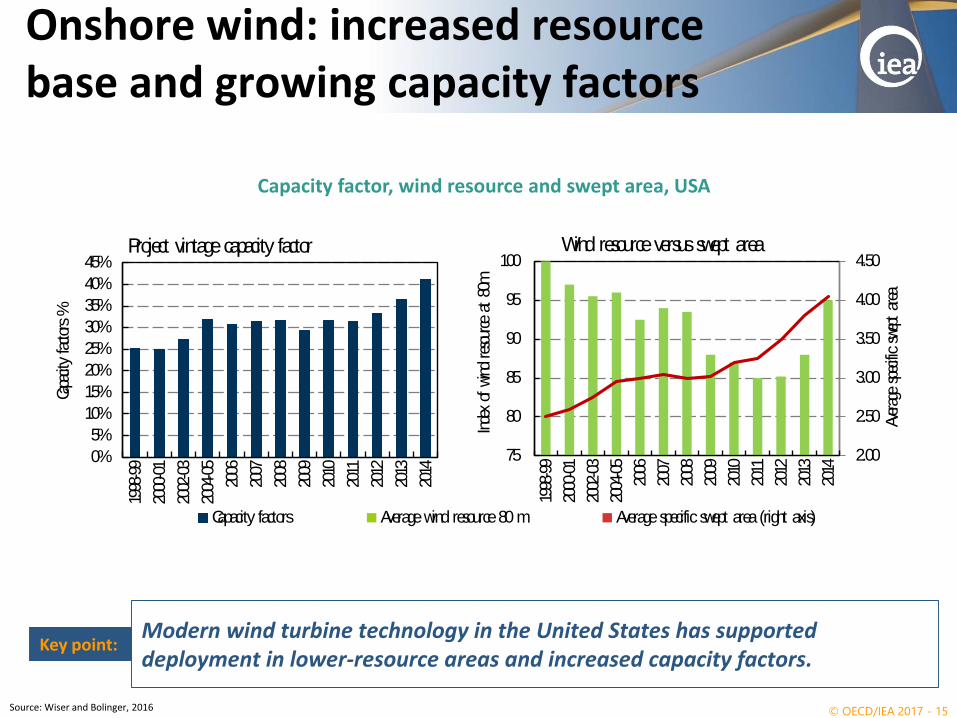

Key point:

Onshore wind: increased resource base and growing capacity factors

Modern wind turbine technology in the United States has supported deployment in lower-resource areas and increased capacity factors.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1998

-99

2000

-01

2002

-03

2004

-05

2006

2007

2008

2009

2010

2011

2012

2013

2014

Capa

city

factor

s %

Project vintage capacity factor

Capacity factors Average wind resource 80 m Average specific swept area (right axis)

2.00

2.50

3.00

3.50

4.00

4.50

75

80

85

90

95

100

1998

-99

2000

-01

2002

-03

2004

-05

2006

2007

2008

2009

2010

2011

2012

2013

2014

Aver

age

spec

ific

swep

t ar

ea

Inde

x of w

ind

reso

urce

at

80m

Wind resource versus swept area

Capacity factor, wind resource and swept area, USA

Source: Wiser and Bolinger, 2016

© OECD/IEA 2017 - 16

PSP: >90% of current on-grid storage

Pumped-hydro plants the reference solution

140 GW in service, 50 GW in development

PSP developed from existing hydro plants

“off-stream” or “pumped-back” schemes

Small energy volumes but large power capacities

Daily/weekly storage does not require large areas

© OECD/IEA, 2011

Source: Inage 2009. © OECD/IEA 2012

© OECD/IEA 2017 - 17

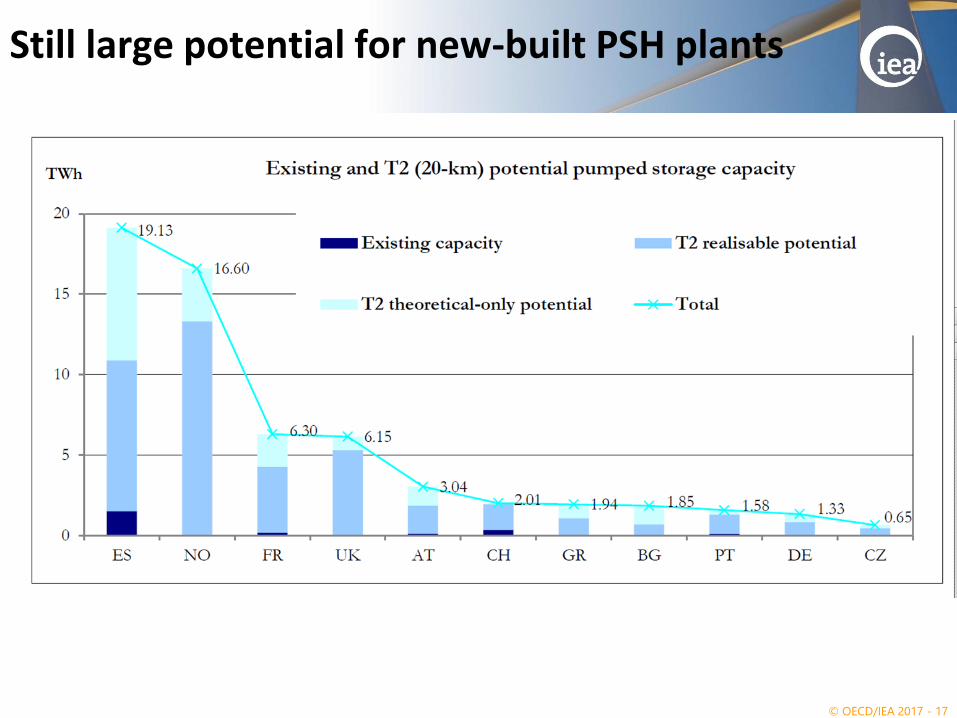

Still large potential for new-built PSH plants

© OECD/IEA 2017 - 18

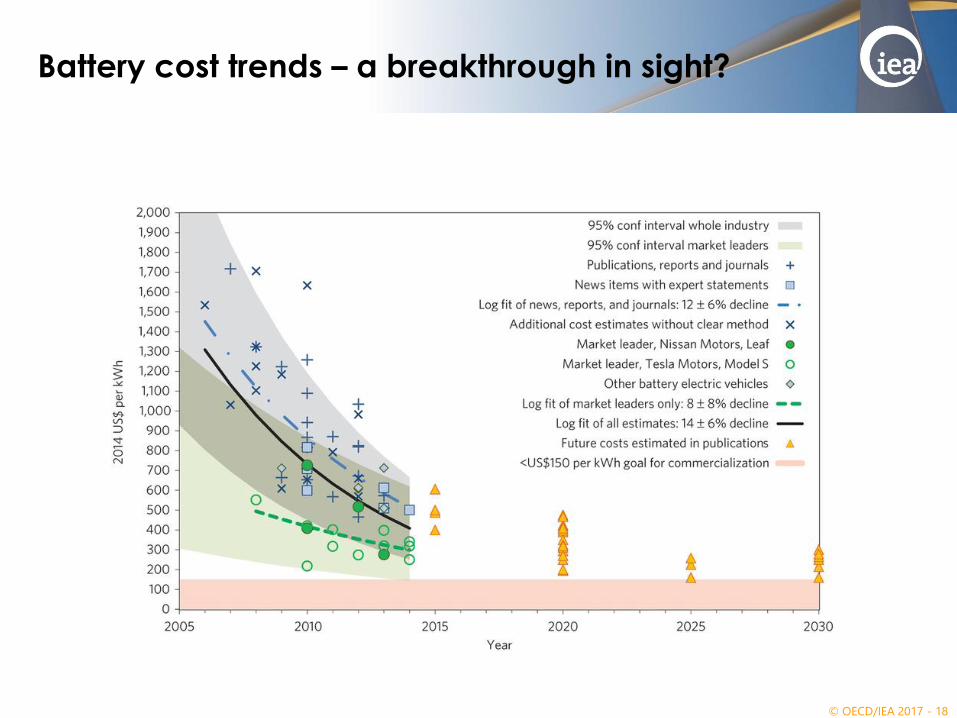

Battery cost trends – a breakthrough in sight?

© OECD/IEA 2017 - 19

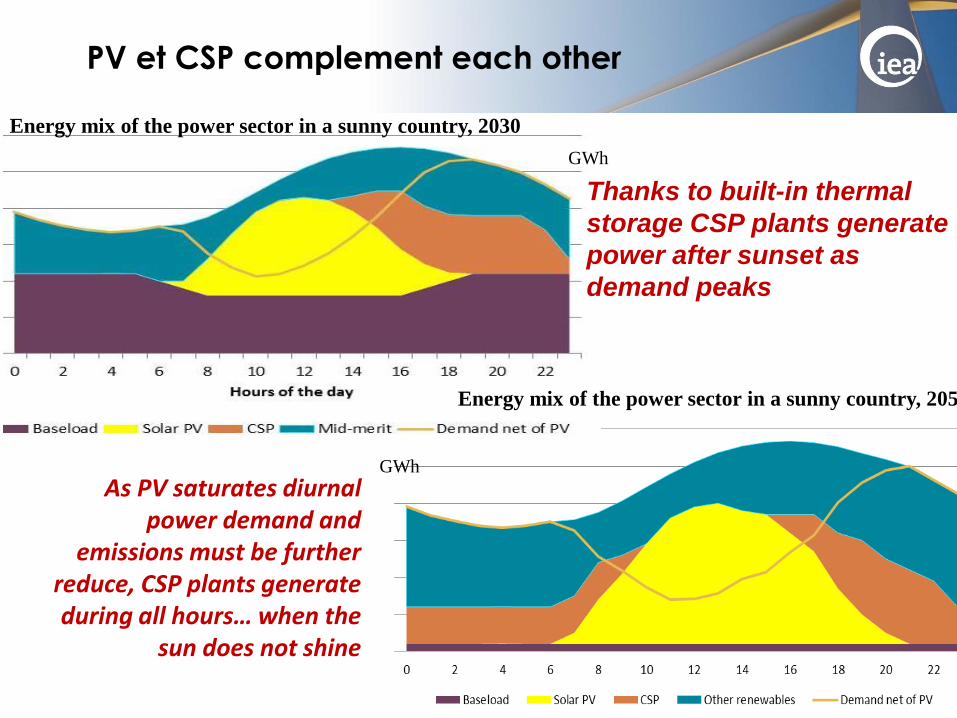

PV et CSP complement each other

©

As PV saturates diurnal power demand and

emissions must be further reduce, CSP plants generate during all hours… when the

sun does not shine

Thanks to built-in thermal

storage CSP plants generate

power after sunset as

demand peaks

Energy mix of the power sector in a sunny country, 2030

GWh

GWh

Energy mix of the power sector in a sunny country, 2050

© OECD/IEA 2017 - 20

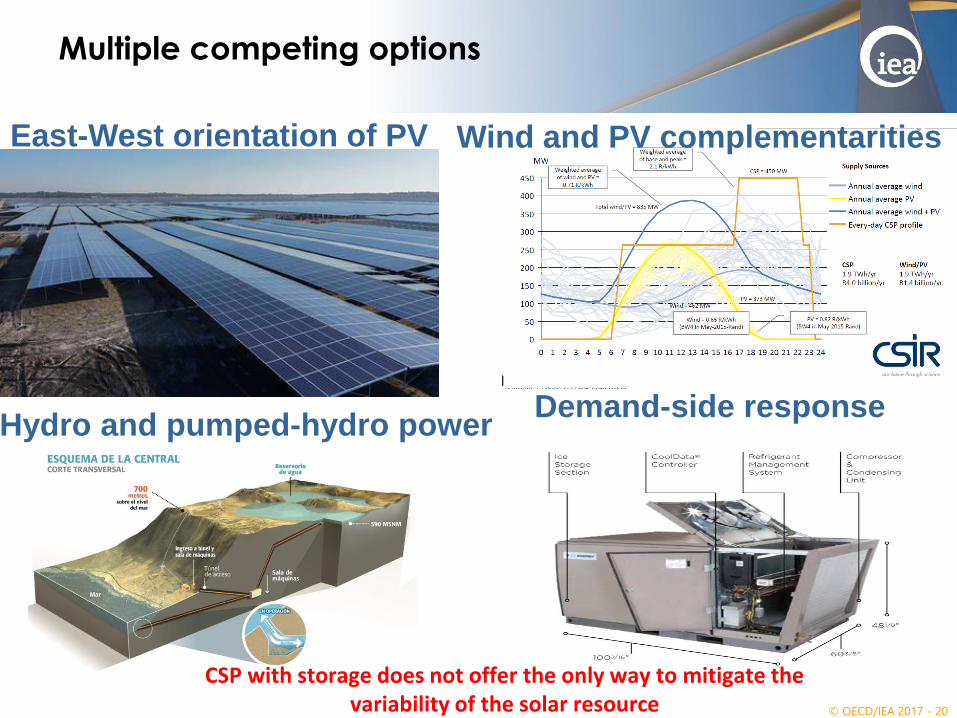

Multiple competing options

Wind and PV complementarities

Hydro and pumped-hydro powerDemand-side response

CSP with storage does not offer the only way to mitigate the variability of the solar resource

East-West orientation of PV

© OECD/IEA 2016

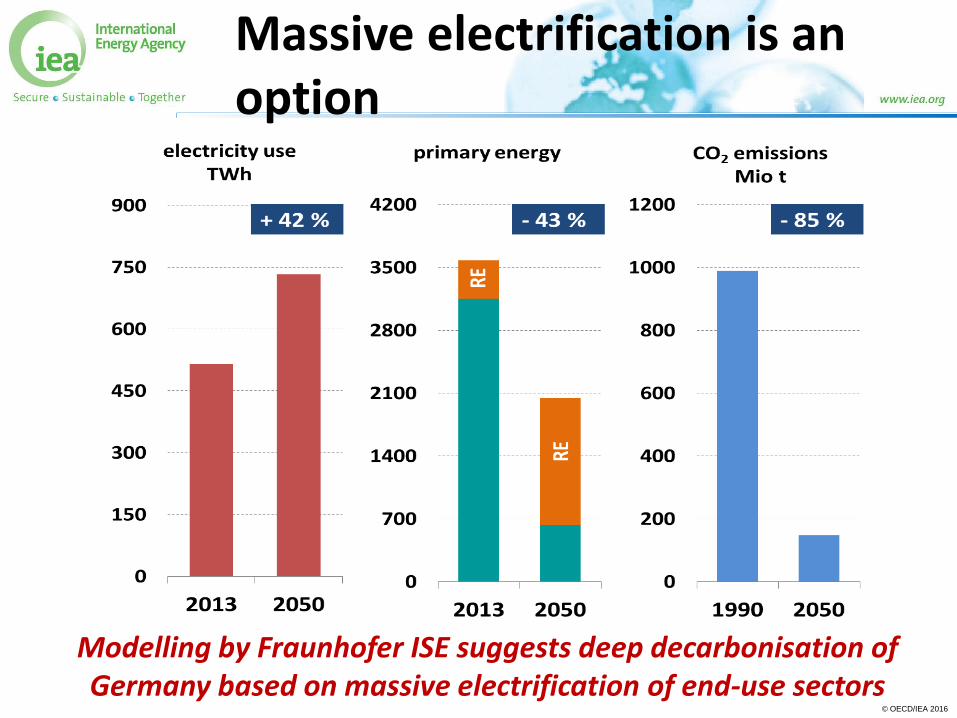

Massive electrification is an option

Modelling by Fraunhofer ISE suggests deep decarbonisation of Germany based on massive electrification of end-use sectors

© OECD/IEA 2016

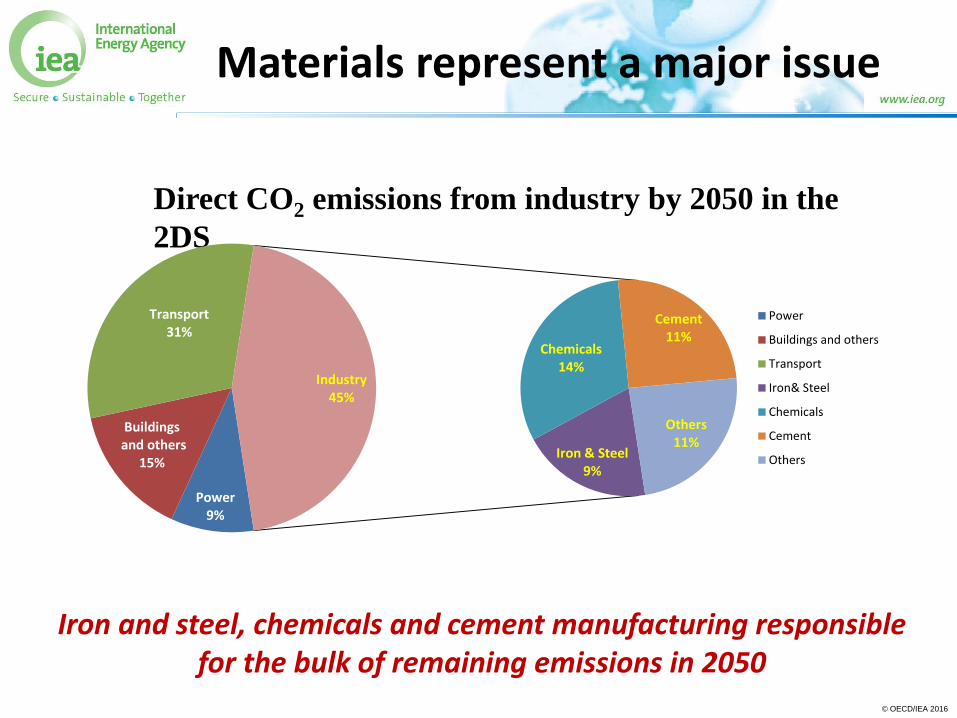

Materials represent a major issue

36%

20%

29%

30% 31%Iron and steel, chemicals and cement manufacturing responsiblefor the bulk of remaining emissions in 2050

Direct CO2 emissions from industry by 2050 in the

2DS

Power9%

Buildingsand others

15%

Transport31%

Iron & Steel9%

Chemicals14%

Cement11%

Others11%

Industry45%

Power

Buildings and others

Transport

Iron& Steel

Chemicals

Cement

Others

© OECD/IEA 2016

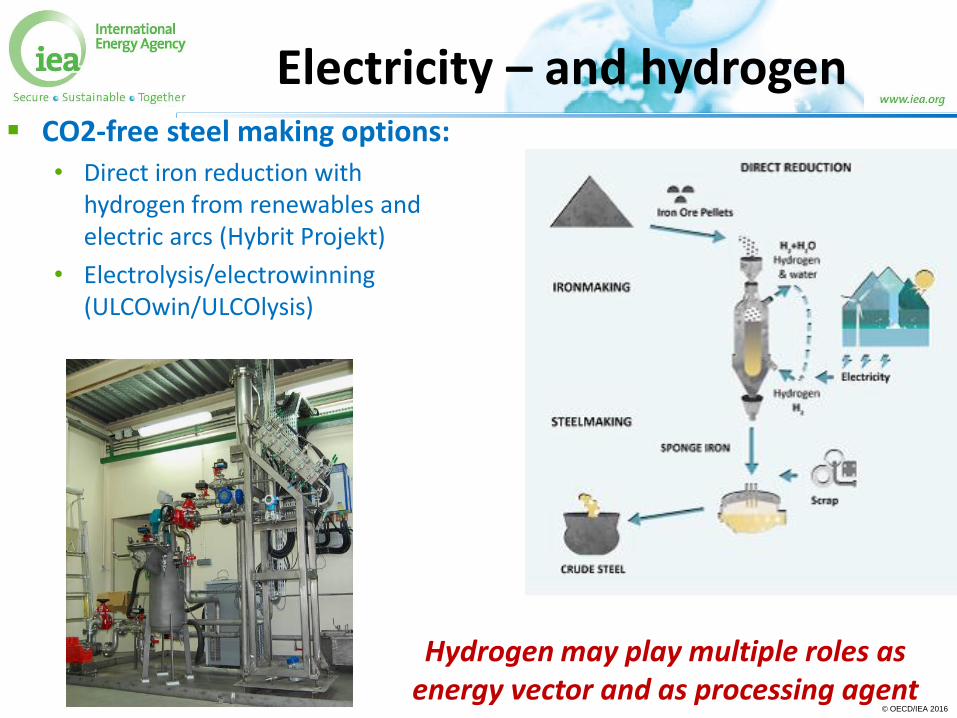

Electricity – and hydrogen CO2-free steel making options:

• Direct iron reduction withhydrogen from renewables and electric arcs (Hybrit Projekt)

• Electrolysis/electrowinning(ULCOwin/ULCOlysis)

Hydrogen may play multiple roles as energy vector and as processing agent

© OECD/IEA 2016

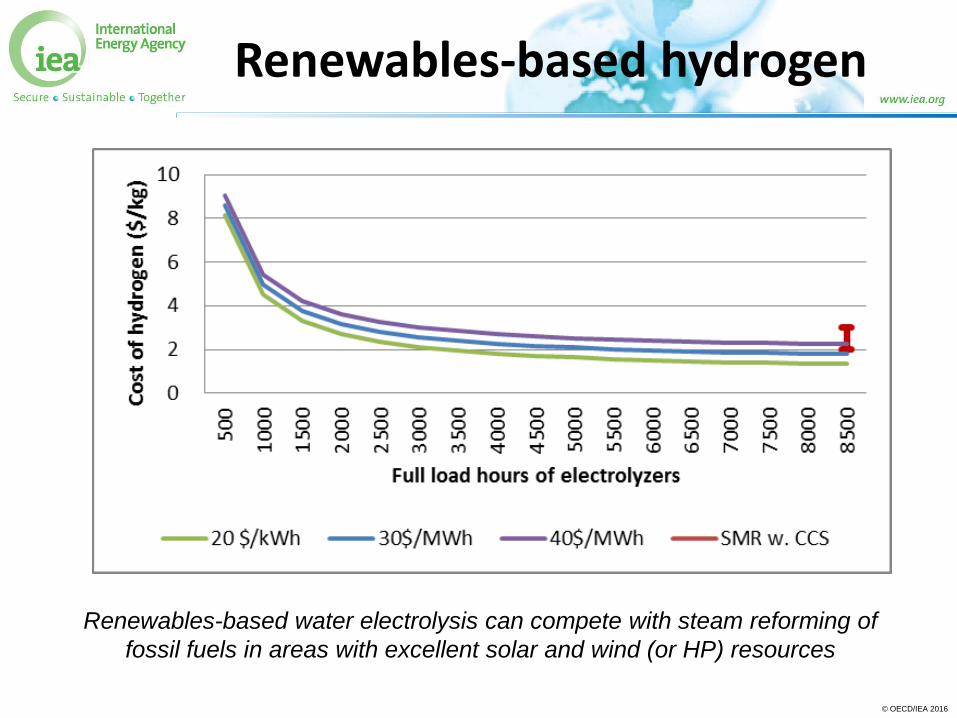

Renewables-based hydrogen

Renewables-based water electrolysis can compete with steam reforming of

fossil fuels in areas with excellent solar and wind (or HP) resources

© OECD/IEA 2016

© OECD/IEA 2016

Ammonia, the other hydrogen

60 Mt H2 is produced annually for industrialuses; half is for ammonia, input to fertilizers

Current hydrogen production is 95% from NG or coal; manufacturing 1 t H2 emits 10 t CO2!

Clean hydrogen requires CCS or renewables-based electrolysis

Clean ammonia, however, could serve as an energy carrier and store, and be directed to some end-use applications, e.g. balancingpower plants

© OECD/IEA 2016

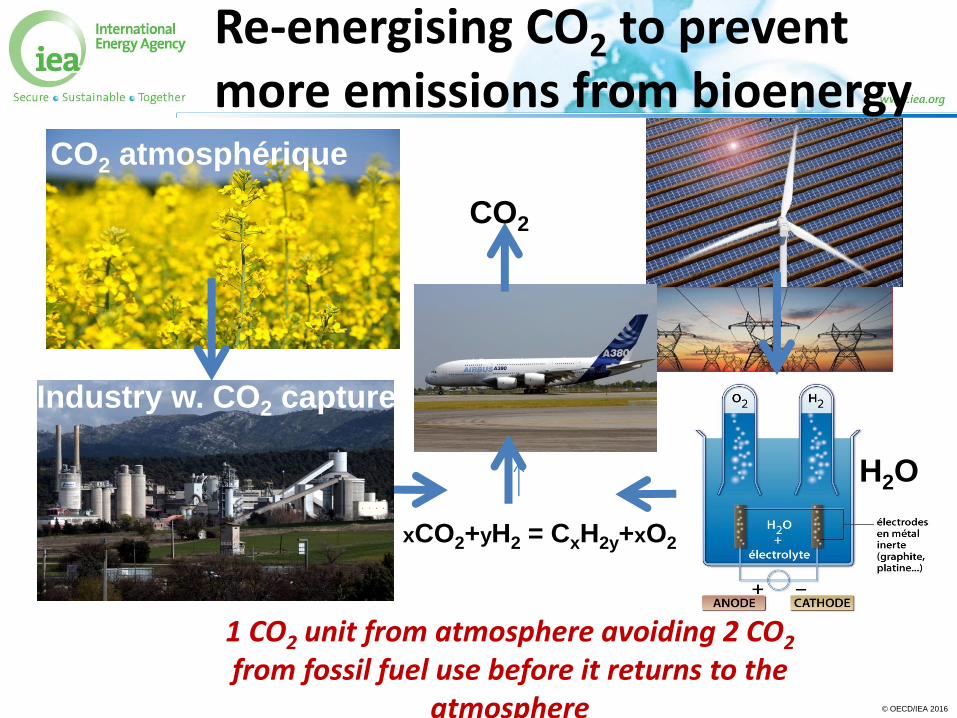

1 CO2 unit from atmosphere avoiding 2 CO2

from fossil fuel use before it returns to the atmosphere

CO2 atmosphérique

xCO2+yH2 = CxH2y+xO2

Industry w. CO2 capture

CO2

H2O

Re-energising CO2 to preventmore emissions from bioenergy