Embed Size (px)

Citation preview

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 1 of 14

SYSTEMIC RISK and SHADOW BANKING

by the International Credit Insurance & Surety Association

(ICISA) 19th of March 2013

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 2 of 14

Contents

1 Introduction

2 Executive Summary 2 Systemic Risk 3 Shadow Banking 4 Appendices

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 3 of 14

1 INTRODUCTION 1.1 About ICISA The International Credit Insurance & Surety Association (ICISA) brings together the world's leading companies that provide trade credit insurance and/or surety bonds. Founded in 1928 as the first credit insurance association, the current members account for over 95% of the world's Trade Credit Insurance business. ICISA members insure risks on all five continents and in practically every country in the world. For an overview of members of ICISA see Appendix III. 1.2 How does Trade Credit Insurance work? Trade Credit Insurance insures manufacturers, traders and providers of services against the risk that their buyer does not pay (after bankruptcy or insolvency) or pays very late. Short-term credit insurance policies are generally one-year policies, and are tailor-made to the individual client’s needs, the type of company, nature of its business and the countries to which it exports. A credit insurance policy either insures all receivables or a selection of these, e.g. the top 10 buyers. These buyers can be based overseas but also in the same country as the seller. Risks are insured by means of a credit limit on each insured buyer, i.e. companies with whom the insured policyholder trades. A credit limit is an objective opinion from the underwriter of the financial condition of a company, not the reason for the financial position of that company. Credit insurance companies have sophisticated underwriting systems, allowing for thousands of credit limit decisions on a daily basis. Every credit limit is monitored and adjustments are made when trade increases or if the financial situation of the buyer justifies this. The Trade Credit Insurance policy pays out a percentage of the outstanding debt. This percentage usually ranges from 75% to 95% of the invoice amount, but may be higher or lower depending on the type of cover that was purchased. 1.3 Trade Credit Insurance is an insurance product, not a financial guarantee ICISA notes that the term “credit insurance” is sometimes also used for types of financial guarantees leading to confusion among stakeholders in the understanding of Trade Credit Insurance activity. Trade Credit Insurance cover is always a direct result of, and linked to, an underlying trade transaction. During the financial crisis of 2008 mono-liners in the US market came into focus, whose products were referred to as being “credit insurance“. However, their activities are totally different and should be seen as financial guarantee business, not as insurance, addressing the capital market with characteristics of non-traditional insurance activities. ICISA members are not in any way involved in this business and only provide traditional Trade Credit Insurance cover.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 4 of 14

2 EXECUTIVE SUMMARY The purpose of this document is to bring together the points of view which ICISA has shared over the years with regard to issues at hand i.e. Systemic Risk and Shadow Banking, albeit in the framework of Solvency II or Financial Stability. Solvency II and the financial crisis of 2008/2009 have brought these topics to the centre of attention, although discussions whether or not traditional insurance was to blame for this crisis are still on-going. The discussions during which these topics were addressed were based on different position papers from institutions varying from the International Association of Insurance Supervisors (IAIS), the Financial Stability Board (FSB) and the European Commission (EC). ICISA welcomes an open discussion on whether traditional Trade Credit Insurance companies are involved in so-called systemic risk and whether or not short term trade credit risk fall within the scope of Shadow Banking. One of the most important bases for these discussions is found in the questions posed by the EC in its paper “Consultation on a Possible Recovery and Resolution Framework for Financial Institutions other than Banks “. ICISA hopes to be give answers to the questions posed by the EC which are relevant to Trade Credit Insurance. ICISA believes its arguments are strong and convincing as Trade Credit Insurance is not part of any systemic risk, nor is it a shadow banking activity. Clarity is important in this context to allow ICISA members in the European Union to concentrate on their efforts to be Solvency II compliant within the time frame given by the EC. Their efforts are such that any deviation could risk being non-compliant on the implementation date (to be set by the EC). Trade Credit Insurance companies that are not compliant with Solvency II pose a much larger risk on the (in)availability of Trade Credit Insurance to potential clients than any discussion regarding the issues at hand. The arguments mentioned in this paper include opinions from organisations such as the Geneva Association, the CRO Forum and Insurance Europe regarding traditional Trade Credit Insurance and the issues at hand.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 5 of 14

3 SYSTEMATIC RISK – TRADE CREDIT INSURANCE 3.1 Introduction The key identifying factors to determine whether or not an Institution can be regarded as a possible source of systemic risk are: size, inter-connectedness, substitutability and availability of the services rendered. The EC appears to follow the definition as set out in the IAIS paper “Insurance and Financial Stability” of November 2011. It mentions in its Consultation Paper (page 24, footnote 34) that the criteria to define a systemic insurer are being developed at international level within the framework of the IAIS. 3.2 Size In a recent article the Financial Times (Appendix IV) stated that: “IAIS will publish a list of systemically important Insurers in April based on the size of their non-traditional business and their centrality to the financial system” From this message ICISA deducts that Trade Credit Insurance, being a traditional business, is not on the list of systemic important Insurers thus they are not considered to be a source of systemic risk. 3.3 Classification of Trade Credit Insurance as traditional insurance activity ICISA is completely in line with the CRO Forum’s opinion on NTNI as expressed in its paper of January 2013 (NTNI from a CRO Forum perspective) the arguments below are based on this paper. The IAIS lists in its document “Insurance and Financial Stability” three main criteria of traditional insurance business which are all met by Trade Credit Insurance:

Trade Credit Insurance builds on the premise of insurability. The events, which lead to

a reimbursement of the policyholder are well defined in the contract (e.g. insolvency of the policyholder’s debtor), they are accidental, i.e. are not controlled by the policyholder, and the business is based on the law of large numbers (pooling risks from many different sectors and jurisdictions on a global basis is an essential element of the business);

Trade Credit Insurance is accounted for under IFRS, under US-GAAP and to the best

of our knowledge also under any other local GAAP system worldwide as insurance business, and not – as for example credit default swaps – as a derivative (i.e. a financial instrument). This clearly reflects that also accounting standard setters worldwide are of the view that Trade Credit Insurance is traditional insurance business which as a consequence is also accounted for as such;

The business builds on the notion of insurable interest. The insurable interest exists

for Trade Credit Insurance, as the policyholders are seeking protection against economic losses which they otherwise would have to bear.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 6 of 14

As explained above, the CRO Forum questions the distinction made by the IAIS between traditional and non-traditional (NT) insurance activities. ICISA shares this questioning. However, if a distinction is made, the above clearly demonstrates that Trade Credit Insurance has all the characteristics of traditional insurance business. 3.4 Substitutability It should be noted that currently only approximately 10% of all exports are covered by Trade Credit Insurance. This demonstrates that Trade Credit Insurance is not vital to the global economy, as the vast majority of trade is not on open account but rather settled on secured terms or without any insurance protection. In spite of the significant market share of the leading Trade Credit insurers there are alternatives should one of these companies go out of business. In each Member State of the European Union traders can choose between 6 and 11 different Trade Credit Insurance companies. New Trade Credit Insurers and reinsurers continue to enter the market. Policyholders can draw on a number of substitutes for Trade Credit Insurance, for example: Policyholders can retain the respective credit risk, i.e. replace Trade Credit Insurance by

self-insurance. It is worth noting in this context that the vast majority of customers that cancel their Trade Credit Insurance policy, switch to self-insurance, rather than buy credit protection from another Trade Credit Insurer;

Traders can switch from trading on open account to agreeing on pre-payment or cash-on-delivery payments;

Letters of Credit can be agreed as secured payment terms instead of open account

terms

Other services are available, allowing companies to mitigate their losses, e.g. credit management, as a prevention to avoid commercial relationships with potentially risky clients, or collection business in order to get as much money back as possible when a customer defaults;

Factoring is another substitute for Trade Credit Insurance protection. Any analysis of the substitutability of a particular Trade Credit insurer should therefore consider not only the Trade Credit Insurance market, but also the market for other financial services which provide customers with other types of risk protection.

The above clearly demonstrates that policyholders can easily replace Trade Credit Insurance products (no lack of substitutability) and that no Trade Credit Insurance company is vital to the proper functioning of the economy.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 7 of 14

Substitutability is also obtained through more capacity from reinsurers operating in the market as well as from those entering the market. 3.5 Conclusion Based on the above, the CRO Forum argues that Trade Credit Insurance does not qualify for as a non-traditional type of activity and does not pose any systemic risk. ICISA fully concurs. Moreover the Geneva Association states in its special report “Systemic Risk in Insurance (2010)” that: “...trade and credit insurance fail the test for systemic relevance of size, (lack of) substitutability and interconnectedness. Credit and surety insurance are relatively small markets, representing less than 1 per cent of global non-life insurance premiums. Despite their connection to the real economy and international trade via SMEs and exporters, credit insurers are not very connected to the financial system. They provide guarantees to a large number of small participants worldwide with limited financial interaction “ 4 SHADOW BANKING – TRADE CREDIT INSURANCE 4.1 Background According to the Green Paper Shadow Banking of 19.03.2012, COM (2012) 102 final, the major risk the EC wishes to identify is the occurrence of a systemic risk related to the disorderly failure of shadow bank entities which escape from the different control authorities. In its investigations the EC includes notably in the list of shadow banking entities insurance and reinsurance companies which issue or guarantee credit products. This Shadow Banking is in fact the intermediation of credit which works towards entities and activities which are not part of the regular banking system. Shadow Banking is based on 2 pillars:

A. Entities engaged in one of the following activities: 1) accepting funding with deposit-like characteristics 2) performing maturity and/or liquidity transformation 3) undergoing credit risk transfer 4) using direct or indirect financial leverage

B. These activities are important sources of funding of non-bank entities notably the securitisation, securities lending and repurchase transactions.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 8 of 14

4.2 Application to Trade Credit Insurance and Surety Business ICISA, whose members represents over 95% of Trade Credit Insurance business, informed in our letter of 23 April 2012 that Trade Credit Insurers do not fall under the criteria of shadow banking. Trade Credit insurers are governed by regulations under Solvency II (and by consequence subject to the controls of their respective national regulators). It is worth noting that the Green Paper also mentions securitization with regard to the insurance sector under the rules implementing the Solvency II Framework Directive (2009 Directive). This Framework Directive requires originators and sponsors of such products to meet risk retention requirements similar to those set out in banking legislation. Therefore it seems ineffectual to include insurance companies in a parallel regulation if Solvency II already deals with this matter. 4.3 Conclusion To sum up, credit insurers are not engaged in shadow banking, but if they were, the 2009 Solvency II Directive already rules this area.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 9 of 14

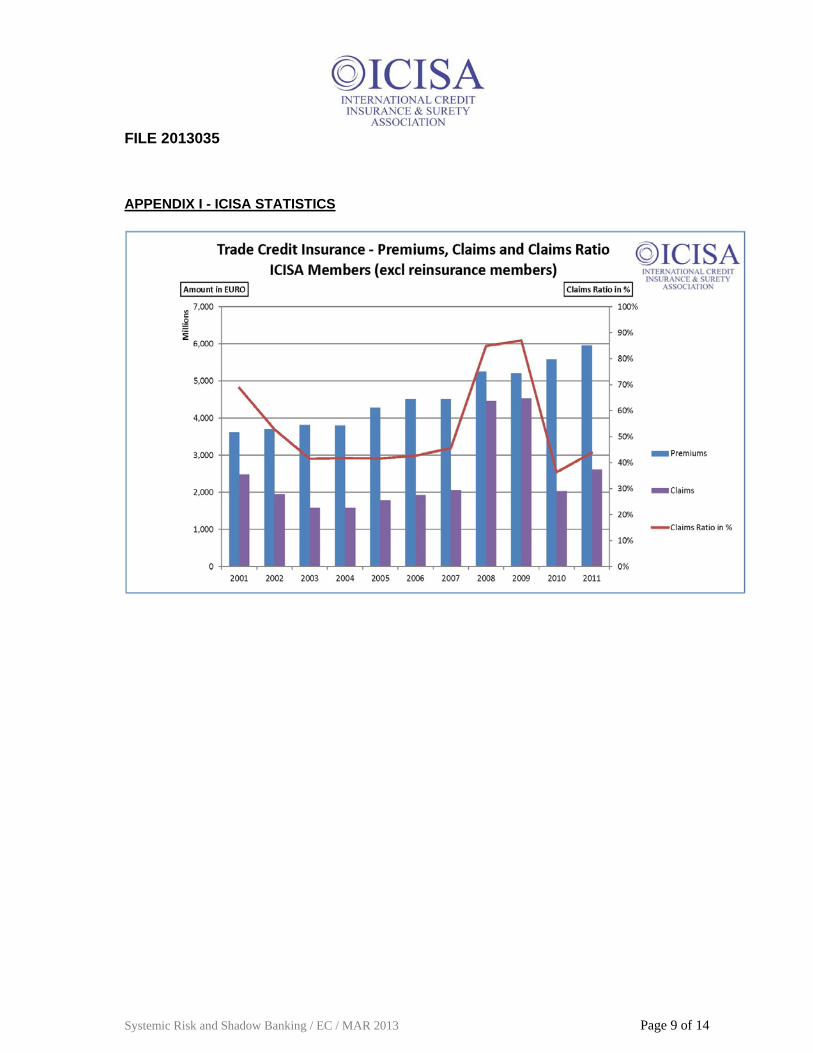

APPENDIX I - ICISA STATISTICS

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 10 of 14

APPENDIX II - ICISA OUTLOOK 2013 (ICISA press release of 6 February 2013) increased demand for trade credit insurance and surety expected to continue new growth markets are recognised and offer new opportunities 15% of global trade is credit insured high retention rates confirm customer satisfaction in the product competition is increasing concern about deteriorating risk environment concern about the uncertainty regarding Solvency II implementation ICISA celebrates 85 years of supporting trade Demand for trade credit insurance and surety bonds is on the rise, as a result of increasing trade flows, mostly from high-growth markets, in an overall ongoing deteriorating risk environment. Capacity is expected to remain ample, while conditions for trade credit insurance may harden in some markets. Major resources and skilled underwriting are needed to meet the demand for surety bonds in the on-going poor conditions of the construction and transportation areas. Concern is raised about availability of adequate trade finance. For the EU clarity about Solvency II implementation is welcomed. Developments in 2012 and current state of the markets During 2012 members of ICISA experienced a deteriorating risk environment, resulting in increased claims activity. Jim Davidson, President of ICISA, states that “in spite of a negative outlook for 2012, largely related to lack of adequate bank financing, and a deteriorating risk environment, the risk appetite of the trade credit insurance members remained more or less stable. Premium rates remain under a downward pressure in a market environment with increased competition”. Robert Nijhout, Executive Director of ICISA, adds that “market conditions in general remained relatively soft during 2012 although this is not the case for all countries (e.g. Spain and Portugal). Construction and transport sectors continued to be weak. Reinsurance capacity has increased, also thanks to new players entering the market. The reinsurance market for trade credit continued to be soft. There is concern about the on-going tight credit conditions in Europe and the risk of overheating in Brazil. In general ICISA members continue to be concerned about the reserved attitude of banks, but are pleased with the increased level of interest for trade credit insurance and surety during the past year”. Davidson underlines that “trade credit insurance is an important trade enhancer, insuring 15% of global trade. The reported high retention rate confirms customer satisfaction in the product”. Trade credit insurance outlook 2013 The trade credit insurance members expect a mixed picture; some markets are expected to harden while others will soften during 2013. Growth is expected from Asia and Latin America, the same regions as in 2012. Andreas Tesch, Vice-President of ICISA, explains that “especially in continental Europe, the UK, Australia and New Zealand markets are expected to harden. As a result overall average

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 11 of 14

premium rates are expected to show an upward trend with stricter policy conditions. The USA and Asia market conditions are expected to soften over 2013. The political instability in MENA and the volatility in Southern Europe and parts of Africa and South America cause concerns for 2013”. The economic slowdown in Europe and the on-going financing constraints of banks are other external factors negatively influencing the 2013 outlook for trade credit insurance. Tesch states that “the Euro zone needs to find solutions for some on-going negative developments which hamper the trustworthiness of the entire Euro area. A more positive outlook can be reached when the sovereign debt issue combined with the political indecision regarding e.g. the Solvency II regime are solved. The possible fall-out of e.g. the UK and the further deterioration of the economic situation in Spain and Portugal are affecting the Euro area as a whole and prevent a structural economic recovery”. Nijhout reports that ICISA members “continue to expect growth for the sector in Latin America, especially in Brazil, and the Far East with key growth markets China, India, Vietnam and Myanmar. Africa, especially Angola and Mozambique, shows strong demand. Also the USA, the Gulf region and countries such as Russia and the Ukraine are expected to show notable demand in 2013.” Surety market outlook 2013 Surety members report on-going difficult conditions in the construction and transport sectors. This results in a further deterioration of the risk quality. And although the market overall will remain soft, this is expected to harden in some countries. “Members express their great concern about the on-going effects of the economic downturn. This downturn in combination with a lack of public spending, mainly as a result of the sovereign debt crisis in the EU and the USA, leads to higher claims activities in the construction and transport sectors. Unfortunately no improvement is expected in these regions during 2013”, Nijhout states. He is however more positive regarding the outlook for areas such as Latin America, African countries such as Mozambique, Ghana and Angola and the fast-growing economies in the Far East. “Concerns remain about the Euro zone area and the USA” according to Nijhout. “Demand will continue to rise in countries that were already successful in 2012. These also include countries bordering the EU, and countries in the Euro area, such as Germany”. ICISA: supporting trade since 1928 During 2013 ICISA will celebrate that it was founded 85 years ago. As the association marks this milestone, it is adding regional focus to its current committee structure, which is based more on risk categories and products. Last year saw the introduction of a new Asia platform, dedicated to the needs of ICISA members operating in the Asian region. For 2013 the association will further address the particular needs of ICISA members in North America. “Demand in North America for our products continues to rise. We hope to build on our positive experience in Asia by giving special focus and support to ICISA members operating in this region.” says Jim Davidson.

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 12 of 14

APPENDIX III - ICISA MEMBERS 2013 - 50 members

Group Members (Worldwide operations) ATRADIUS COFACE EULER HERMES Members ACE SURETY USA AFIANZADORA Argentina ALLIANZ SE Germany ASKRINDO Indonesia ASPEN RE Switzerland AXA ASSURCREDIT France AXA-WINTERTHUR Switzerland AXIS RE Switzerland CATLIN RE Switzerland CESCE Spain CGIC South Africa CHINA I&G China CLAL Israel COSEC Portugal DUCROIRE|DELCREDERE Belgium ECICS Singapore ENDURANCE RE Switzerland FIANZAS ATLAS Mexico FIANZAS MONTERREY Mexico GARANT Austria GCNA Canada GROUPAMA ASSURANCE CREDIT France HANNOVER RE Germany HCC INTERNATIONAL United Kingdom ICIC Israel LOMBARD INSURANCE COMPANY South Africa MAPFRE Spain MITSUI SUMITOMO Japan MUNICH RE Germany NATIONALE BORG Netherlands NOVAE GROUP PLC United Kingdom PARTNER RE Switzerland PICC China PRISMA Austria R+V RE Germany QBE Australia SACE BT Italy SCOR GLOBAL P&C SE France SGI Korea SID - FIRST CREDIT Slovenia SOMPO JAPAN Japan SWISS RE Switzerland TOKIO MARINE & NICHIDO FIRE Japan TRYG GARANTI Denmark ZURICH INSURANCE PLC Germany

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 13 of 14

ZURICH SURETY United Kingdom ZURICH SURETY, CREDIT AND POL. RISK USA

FILE 2013035

Systemic Risk and Shadow Banking / EC / MAR 2013 Page 14 of 14

APPENDIX IV - Financial Times - Article of 18 March 2013