Embed Size (px)

Citation preview

Systems Analysis and Design Fourth Edition

Introduction

A project is economically feasible if the future benefits outweigh the costs

The Systems Analyst’s Toolkit explains how to calculate a project’s costs and benefits

Cost-benefit analysis is performed whenConducting a preliminary investigationEvaluating a projectMaking recommendations to

management

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Cost classificationsCosts can be classified in several ways

Tangible and intangible costsDirect and indirect costsFixed and variable costsDevelopmental and operational costs

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Direct and indirect costsDirect costs are those that can be

associated with the development of a specific systemExamples: project team salaries, new

hardware or software needed for the system

Indirect costs, or overhead expenses, cannot be attributed to a particular systemExamples: network administrator’s salary,

copy machine rental costs

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Fixed and variable costsFixed costs are relatively constant and do

not depend on a level of activity or effortExamples: salaries, rental charges

Variable costs depend on the level of activityExamples: printer paper, supplies, telephone

line charges

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Developmental and operational costsDevelopment costs are incurred only

once, at the time the system is developedExamples: system development team

salaries, user training, hardware purchase

Operational costs are incurred after the system is implemented and continue while the system is in useExamples: system maintenance, ongoing

training, annual license fees

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Managing information systems costs and chargesManagement requires cost informationDirect costs can be associated with a specific

system, while indirect costs must be allocatedA chargeback method uses accounting entries to

allocate the indirect IS costsNo charge methodFixed charge methodVariable charge method based on resource useVariable charge method based on volumes

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Managing information systems costs and charges Chargeback methods

No charge methodTreats IS department indirect expenses as a

necessary cost of doing business, which benefits the entire company

The IS group is called a cost center because it generates no offsetting credits for services performed

User departments are not charged for indirect IS expenses

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Managing information systems costs and charges Chargeback methods

Fixed charge methodIndirect IS costs are divided among all other

departments in the form of a fixed monthly charge, using various formulas

In this method, the IS group is called a profit center because it is expected to break even or show a profit on the sale of services

User departments are charged with a fixed share of indirect IS expenses

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Managing information systems costs and charges Chargeback methods

Variable charge method based on resource use Resources might include CPU time, connect time to a

remote computer, communication lines or printers required

Costs can vary from month to monthIn this method, the IS group is called a profit centerUser departments are charged with indirect IS

expenses on the basis of resources used

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Managing information systems costs and charges Chargeback methods

Variable charge method based on volume Resources might include CPU time, connect time to

a remote computer, communication lines or printers required

Costs can vary from month to monthIn this method, the IS group is called a profit centerUser departments are charged with indirect IS

expenses on the basis of resources used

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Benefit classificationsBenefits can be classified into the same

categories as costsTangible and intangible benefitsDirect and indirect benefitsFixed and variable benefitsDevelopmental and operational benefits

Benefits also can be classified as positive benefits and cost-avoidance benefits

Systems Analysis and Design Fourth Edition

Describing Costs and Benefits

Positive and cost-avoidance benefitsPositive benefits are a direct result of the

new information systemExamples: increased revenues, improved

services, higher morale, better management

Cost-avoidance benefits refer to expenses that would be necessary if the new system is not installedExamples: handling work with current staff

instead of hiring, not having to replace hardware or software

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Cost-benefit analysis is the process of comparing anticipated costs to anticipated benefits

Cost-benefit analysis produces reliable information for making decisions

Common cost-benefit techniquesPayback analysisReturn on investment (ROI) analysisPresent value analysis

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Payback analysisPayback analysis is the process of

determining how long it takes for an information system, to pay for itself

Four step process1. Determine the system’s initial development

cost 2. Estimate annual benefits3. Determine annual operating costs4. Find the payback period by comparing total

costs to accumulated benefits

Click to see Figure 2-1 Click to see Figure 2-1 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Payback analysisWhen costs and benefits are plotted, the

economically useful life of the system is shown

Systems development costs are high at first, then drop

Systems operation costs remain low until increased maintenance is required toward the end of the system’s economically useful life

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Payback analysisWhen costs are plotted, the economically

useful life of the system is shownSystems development costs are high at

first, then dropOperational costs remain low at first, then

increase as more maintenance is required

Click to see Figure 2-2 Click to see Figure 2-2 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Payback analysisWhen costs are plotted, the economically

useful life of the system is shownSystems development costs are high at

first, then dropOperational costs remain low at first, then

increase as more maintenance is requiredBenefits usually increase rapidly when the

system becomes operational, then level off

Click to see Figure 2-3 Click to see Figure 2-3 Package

Systems Analysis and Design Fourth Edition

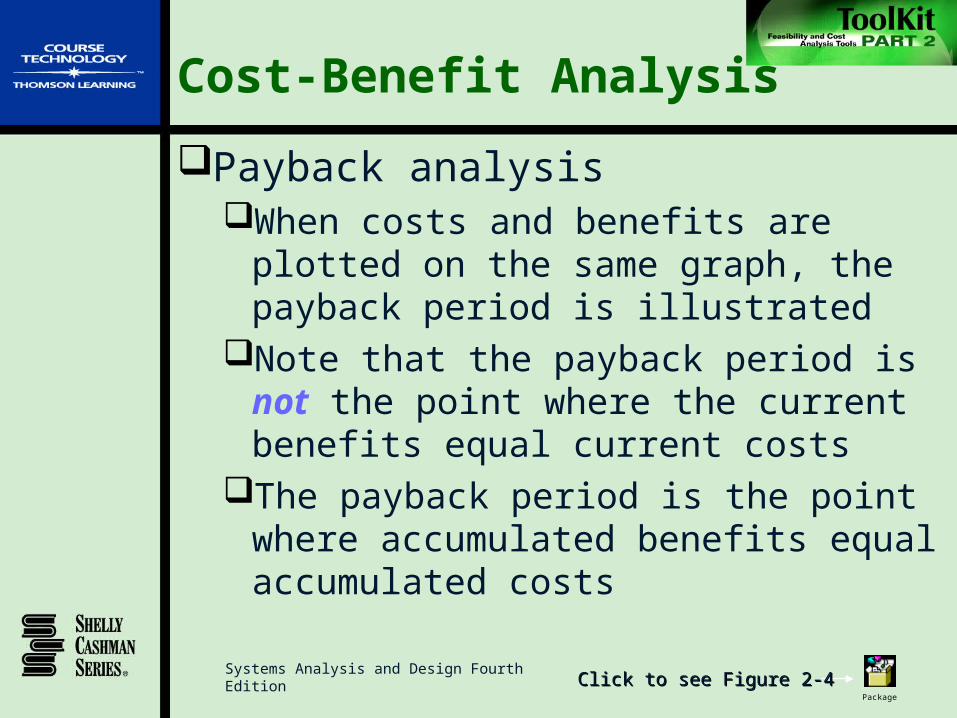

Cost-Benefit Analysis

Payback analysisWhen costs and benefits are plotted on

the same graph, the payback period is illustrated

Note that the payback period is not the point where the current benefits equal current costs

The payback period is the point where accumulated benefits equal accumulated costs

Click to see Figure 2-4 Click to see Figure 2-4 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Payback analysisPros and cons

Payback analysis emphasizes costs and benefits early in the system’s life and ignores those that occur later

Even though it has drawbacks, payback analysis is widely used

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Using a spreadsheet to compute payback analysisDesign the spreadsheet and label the

rows and columnsEnter the cost and benefit data for each

yearEnter the formulas to calculate

cumulative costs and benefits

Click to see Figure 2-6 Click to see Figure 2-6 Package

Click to see Figure 2-5 Click to see Figure 2-5 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Return on investment analysisROI is a percentage rate that measures

profitability by comparing a project’s total net benefits (the return) to its total costs (the investment)

ROI = (total benefits - total costs) / total costs

Projects can be ranked using ROI

Click to see Figure 2-7 Click to see Figure 2-7 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Return on investment analysisPros and cons

ROI does consider all costs and benefits during the system’s life, and is a more precise method than payback analysis

ROI only measures the overall rate of return for the total period, and annual rates can vary considerably

ROI ignores the timing of costs and benefits

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Using a spreadsheet to compute ROISet up the worksheet and enter cost and

benefit dataOverall cost and benefit totals are

requiredAdd a formula to calculate ROI, which is

total benefits minus total costs, divided by total costs

Click to see Figure 2-8 Click to see Figure 2-8 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Present value analysisThe time value of money is a concept that

adjusts future costs and benefits and expresses them in terms of current dollars

The timing of costs and benefits directly affects the desirability of a project Benefits that you receive now are more valuable

than those you receive in the future, because you gain the use of the money and can invest it

Costs that you incur now are more expensive than those you incur in the future, because you lose the use of the money immediately

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Present value analysisPresent value adjustment factors are based

on a specified interest rate called the discount rate

The discount rate is the return a company might expect on a risk-free investment, such as a bond

Each company determines its own acceptable rate of return for an information systems project

Adjustment factors are printed in tables called present value tables, which are readily available

Click to see Figure 2-9 Click to see Figure 2-9 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Present value analysis1. Use present value tables to time-adjust

valuesLocate the adjustment factor in the column

with the appropriate discount rate and the row for the appropriate number of years

Multiply this value times the costs and benefits to calculate the adjusted cost and benefit values

Click to see Figure 2-10 Click to see Figure 2-10 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Present value analysis1. Use present value tables to time-adjust

valuesLocate the adjustment factor in the column with

the appropriate discount rate and the row for the appropriate number of years

Multiply this value times the costs and benefits to calculate the adjusted cost and benefit values

2. Total the time-adjust costs and benefits3. The net present value (NPV) is total

benefits minus total costs

Click to see Figure 2-11 Click to see Figure 2-11 Package

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Present value analysisPros and cons

Present value analysis not only considers all costs and benefits, but adjusts the values based on timing

NPV results depend on future estimates, and are only as reliable as the forecasts themselves

Many companies use all three methods to evaluate projects

Systems Analysis and Design Fourth Edition

Cost-Benefit Analysis

Using a spreadsheet to calculate present valueSet up the worksheet and enter costs,

benefits, and present value adjustment factors

Provide cost and benefit totalsAdd formulas to multiply each cost and

benefit value times the appropriate adjustment factor

Add a formula to calculate net present value (NPV), which is total adjusted benefits minus total adjusted costs

Click to see Figure 2-12 Click to see Figure 2-12 Package

EndToolkit Part 2