Embed Size (px)

Citation preview

THE NEW JERSEY INITIATIVE:Building Management Capacity

in New Jersey Municipalities

TH

EN

EWJE

RSEY

INIT

IAT

IVE:

Bu

ildin

g Ma

na

gemen

t Ca

pacity in

New

Jersey Mu

nicipa

lities

THE NEW JERSEY INITIATIVE:Building Management Capacity

in New Jersey Municipalities

Maxwell School of Citizenship and Public AffairsSyracuse University, New York

Eagleton Institute of PoliticsRutgers, The State University of New Jersey

Funded by

The Pew Charitable Trusts

and

State of New Jersey Department of Community Affairs

2002

© 2002 by The Maxwell School of Citizenship and Public Affairs at Syracuse University.All rights reserved including the right of reproduction in whole or in part in any form.

Address inquiries to:The New Jersey InitiativeAlan K. Campbell Public Affairs Institute Maxwell School of Citizenship and Public Affairs Syracuse University306 Eggers HallSyracuse NY 13244-1090

315-443-9707315-443-9734 (Fax)www.campbellinstitute.org

ISBN 0-9723595-0-8

To all the dedicated public employees who serve in New Jersey’s 566 municipalities and state government.

iv

Dale JonesDirector

Managing for Results FacultyExpert

Dana Michael HarsellProject Manager

Managing for Results ResearchAssociate

Stuart BretschneiderInformation Technology

Management Faculty Expert

Sally Coleman SeldenHuman Resources

Management Faculty Expert

Yilin HouFinancial Management

Faculty Expert

Connie BawcumMax BohnstedtSuzette Denslow

Carol EbdonCapital Management Project

Consultants

Amy K. DonahuePublic Management

Consultant

Bethany WalawenderProject Finance and

Administration

Kelley ColemanOffice Coordinator

Willow JacobsonHuman Resources

Management ResearchAssociate

Ora-orn PoocharoenManaging for Results Research

Associate

New Jersey InitiativeProject Staff

Yonghong WuFinancial Management

Research Associate

Jessica CrawfordPublic Relations Coordinator

Human ResourcesManagement Senior Research

Assistant

Tiffany TannerPublication CoordinatorFinancial Management

Senior Research Assistant

Figen GungorProject Senior Research

Assistant

Chris FoltsProject ManagementResearch Assistant

Sharif NankoeProject ManagementResearch Assistant

Paula AcostaFinancial Management

Research Assistant

Kingsley ChukwuMelissa Mink

Human ResourcesManagement Research

Assistants

Alyssa ColonnaEditor

Kari ParsonsProject Consultant

Chris BronkWeb Site Designer

Dana CookeLogo Designer

Eagleton Institute of PoliticsRutgers, The State

University of New Jersey

Ingrid W. ReedAssociate Director

New Jersey Government Advisor

Jon EricksonProject Manager

Financial Management Advisor

Lucy BaruchProject Finance and Administration

Joanne PfeifferOffice Coordinator

Genikwa WilliamsProject Research Assistant

The Maxwell School of Citizenship and Public Affairs,

Syracuse University

v

Loretta BuckelewAssistant to the Deputy Director

Division of Local Government ServicesState of New Jersey

Henry A. ColemanDirector

Center for Government ServicesRutgers, The State University of New Jersey

Jon EricksonDirector

Master of Public Administration ProgramKean University

Michele Tuck-PonderPresident

Ponder Solutions

William A. WatsonExecutive Director

John S. Watson Institute for Public PolicyThomas Edison State College

John WeingartAssociate Director

Eagleton Institute of PoliticsRutgers, The State University of New Jersey

New Jersey InitiativeAdvisory Committee

vi

Funders

The New Jersey Initiative acknowledges with gratitude that the project is funded by grants from the following:

The Pew Charitable Trusts

State of New Jersey Department of Community Affairs

The opinions expressed in this report are those of the authors anddo not necessarily reflect the views of The Pew Charitable Trusts and

the State of New Jersey Department of Community Affairs. The New Jersey Initiative is solely responsible for the content of this report.

Table of Contents vii

Table of Contents

List of Tables and Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

List of Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xi

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xiii

Acknowledgments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xv

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xvii

1 Assessing Management Capacity in New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . .1The Government Performance Project: Foundation for the New Jersey Initiative . . . . . . . . . . .1The New Jersey Initiative . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4Management Capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7New Jersey Laws Governing Municipal Administration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13Backgrounds of Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

2 Financial Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33Financial Management Capacity and Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33Financial Management Environment for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . .34Criteria for Assessing Financial Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36Methodology and Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37Results: Financial Management in New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . .38Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .54Recommendations for New Jersey Municipalities and the State of New Jersey . . . . . . . . . . . .55

3 Capital Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61Capital Management Capacity and Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61Capital Management Environment for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . .63Criteria for Assessing Capital Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Methodology and Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65Results: Capital Management in New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . .66Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .70Recommendations for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .71Recommendations for the State of New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .72

4 Human Resources Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75Human Resources Management Capacity and Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75Human Resources Management Environment for New Jersey Municipalities . . . . . . . . . . . . .76Criteria for Assessing Human Resources Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .80Methodology and Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .80Results: Human Resources Management in New Jersey Municipalities . . . . . . . . . . . . . . . . . . .81Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .108Recommendations for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .109Recommendations for the State of New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .110

viii THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

5 Information Technology Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .113Information Technology Management Capacity and Systems . . . . . . . . . . . . . . . . . . . . . . . .113Information Technology Management Environment for New Jersey Municipalities . . . . . . .114Criteria for Assessing Information Technology Management . . . . . . . . . . . . . . . . . . . . . . . . .116Methodology and Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .117Results: Information Technology Management in New Jersey Municipalities . . . . . . . . . . . .118Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .127Recommendations for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .127Recommendations for the State of New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .128

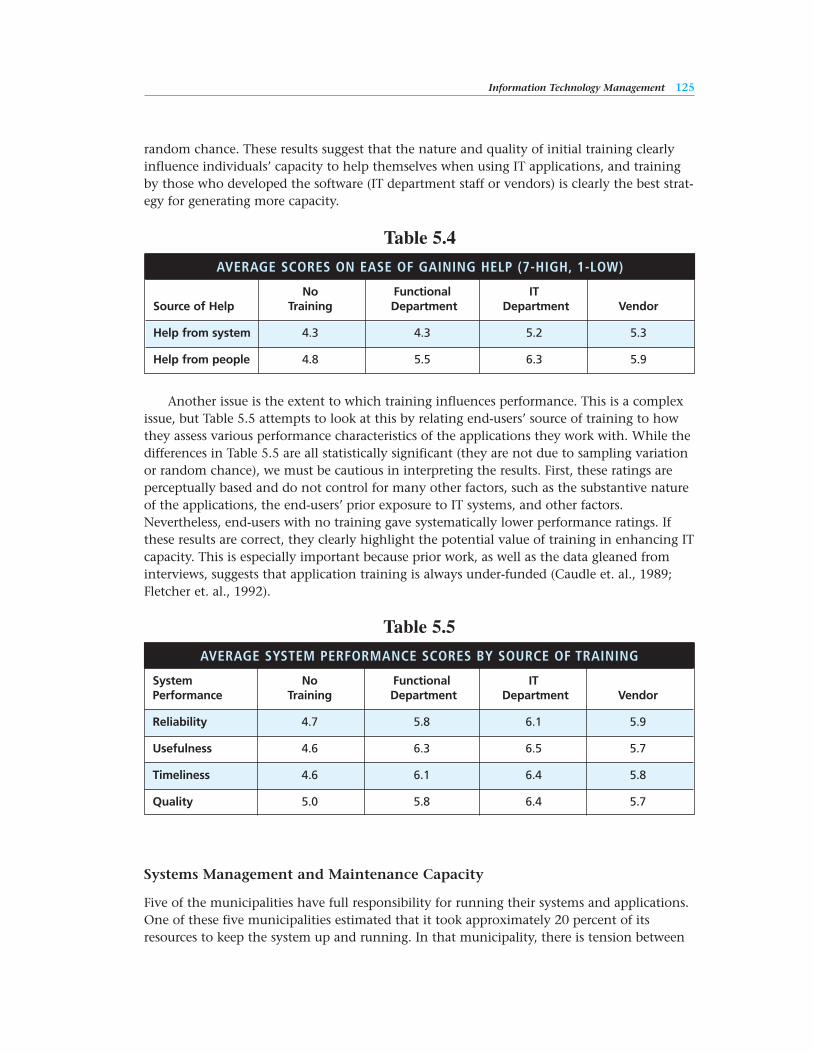

6 Managing for Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .131Managing for Results Capacity and Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .133Managing for Results Environment for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . .137Criteria for Assessing Managing for Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .137Methodology and Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .139Results: Managing for Results in New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . .139Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .146Recommendations for New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .147Recommendations for the State of New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .147Recommendations for New Jersey Municipalities and the State of New Jersey . . . . . . . . . . .148

7 Conclusion: Improving Management Capacity in New Jersey Municipalities . . . . . . . .151Collaborative Approach From Municipalities and the State . . . . . . . . . . . . . . . . . . . . . . . . . .151Vital Reforms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .152Bold Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .153

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .157

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .188

List of Tables and Figures ix

List of Tables and FiguresTables

1.1 History of the Government Performance Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2 Characteristics of Municipalities in the New Jersey Initiative. . . . . . . . . . . . . . . . . . . . . . . . . 5

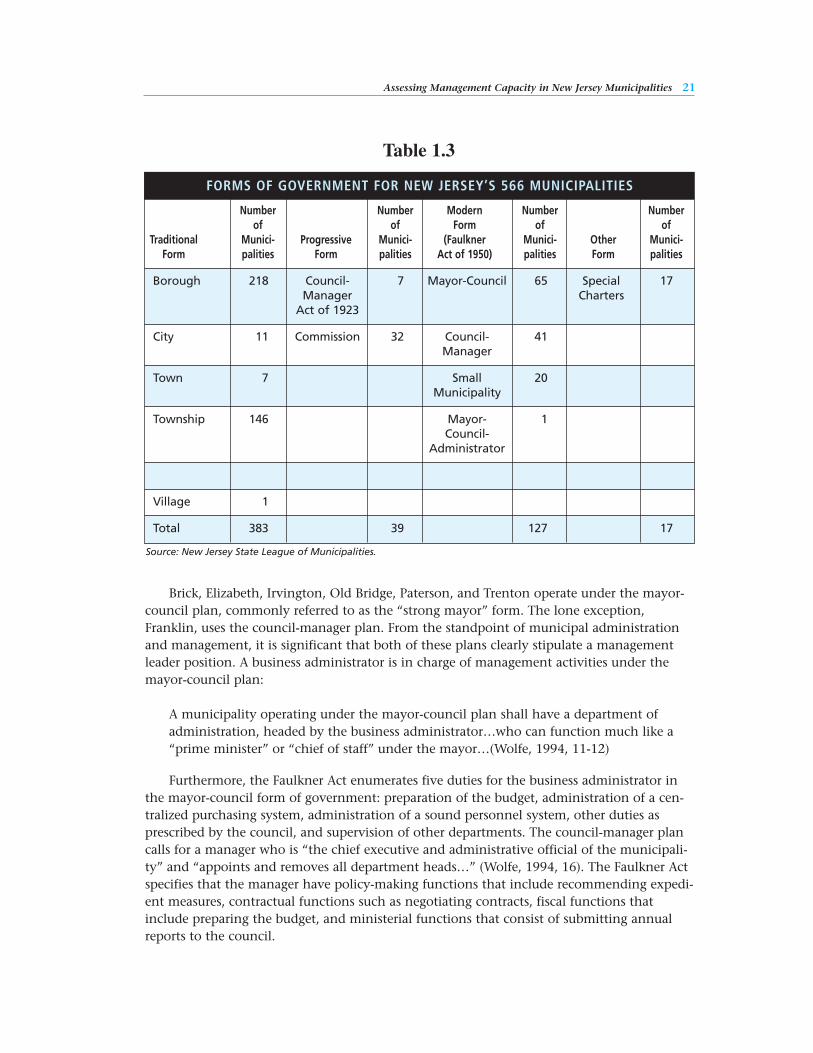

1.3 Forms of Government for New Jersey’s 566 Municipalities. . . . . . . . . . . . . . . . . . . . . . . . . . 21

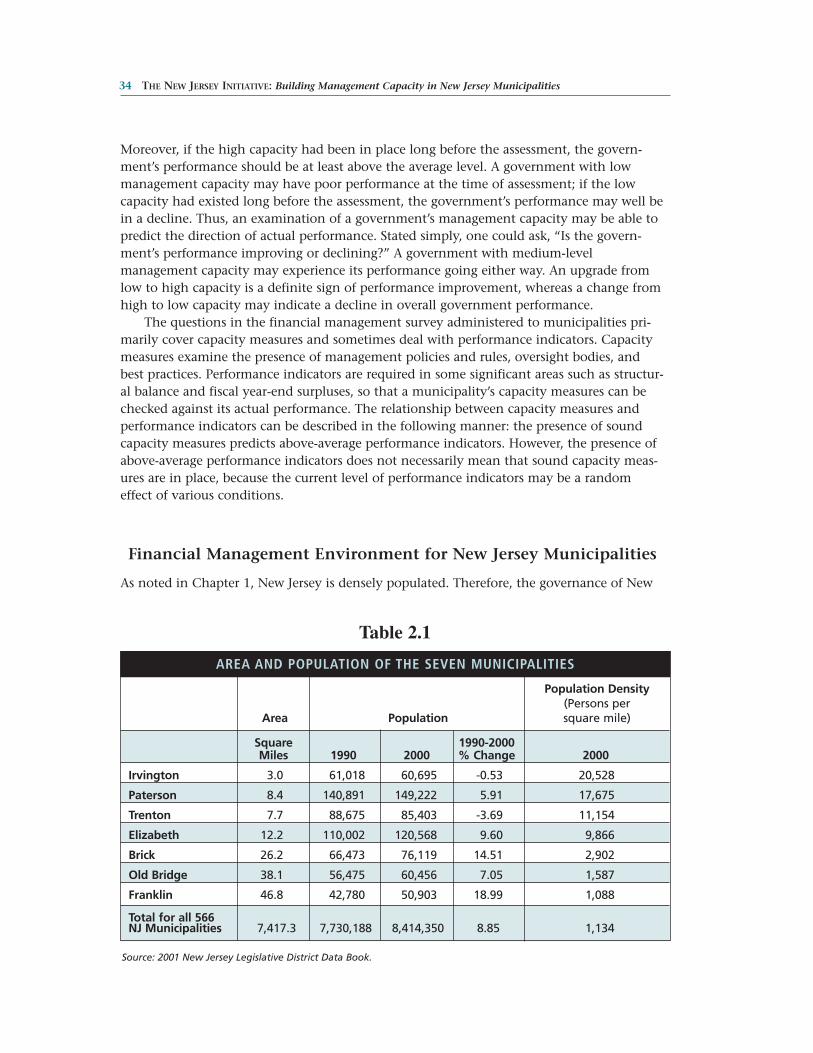

2.1 Area and Population of the Seven Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

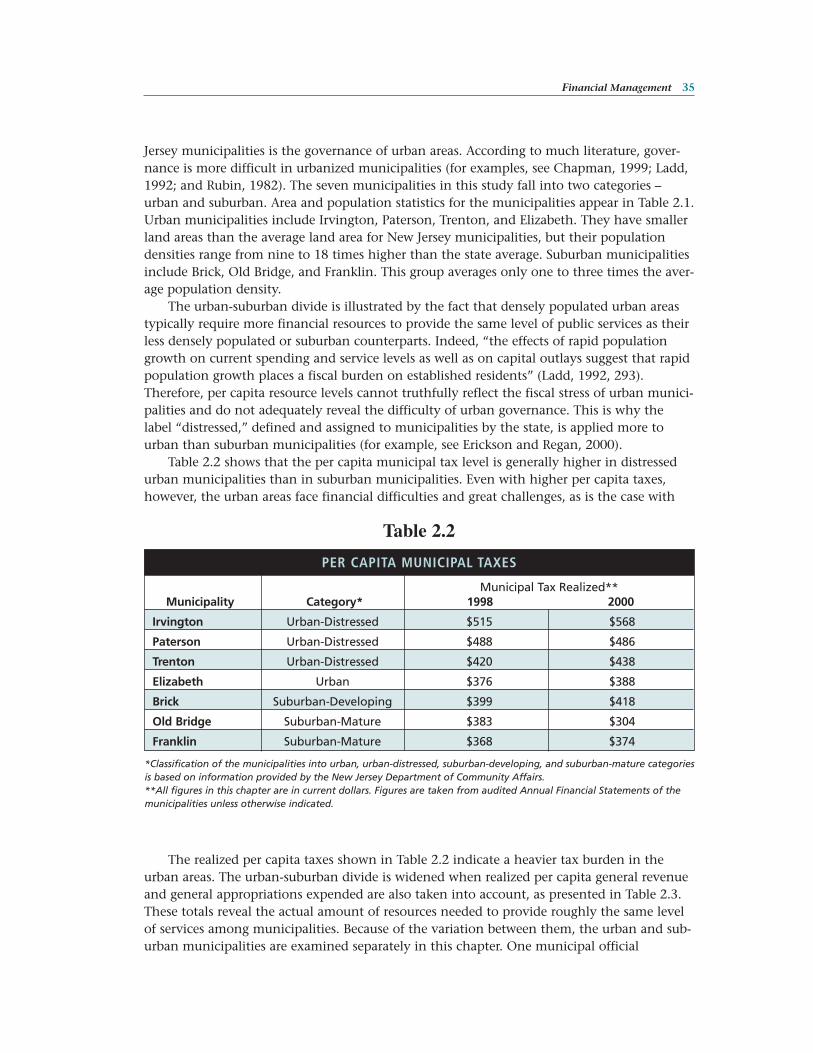

2.2 Per Capita Municipal Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

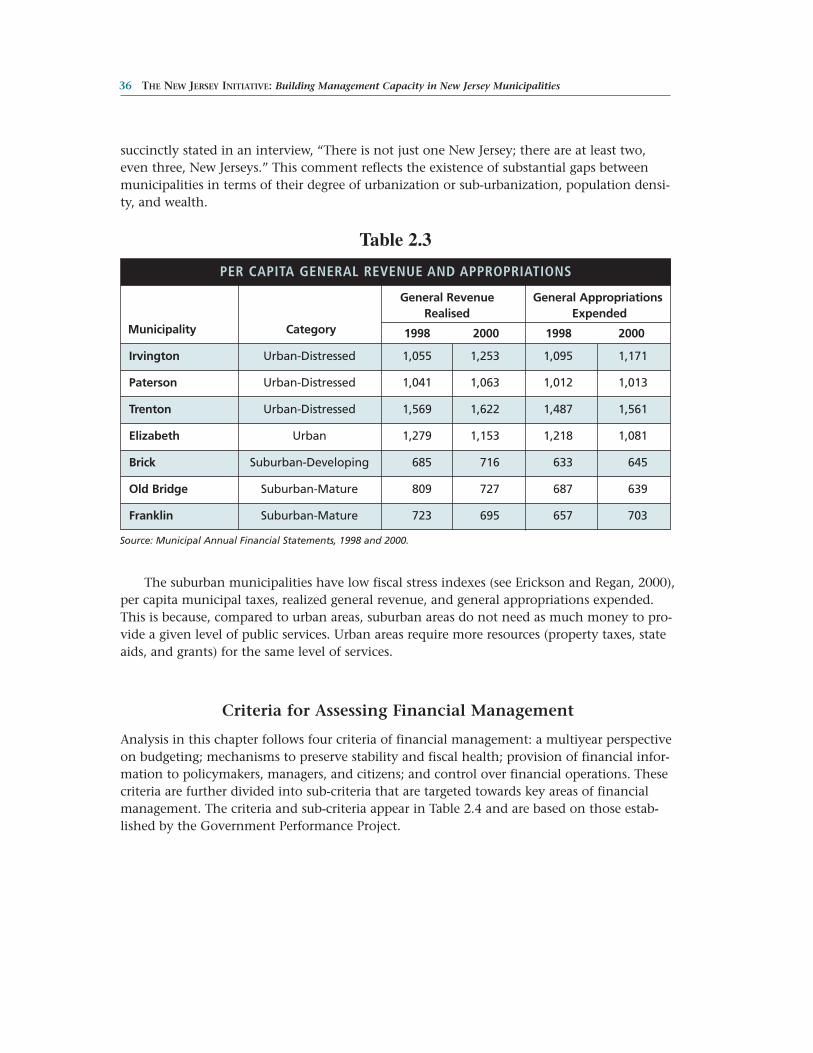

2.3 Per Capita General Revenue and Appropriations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

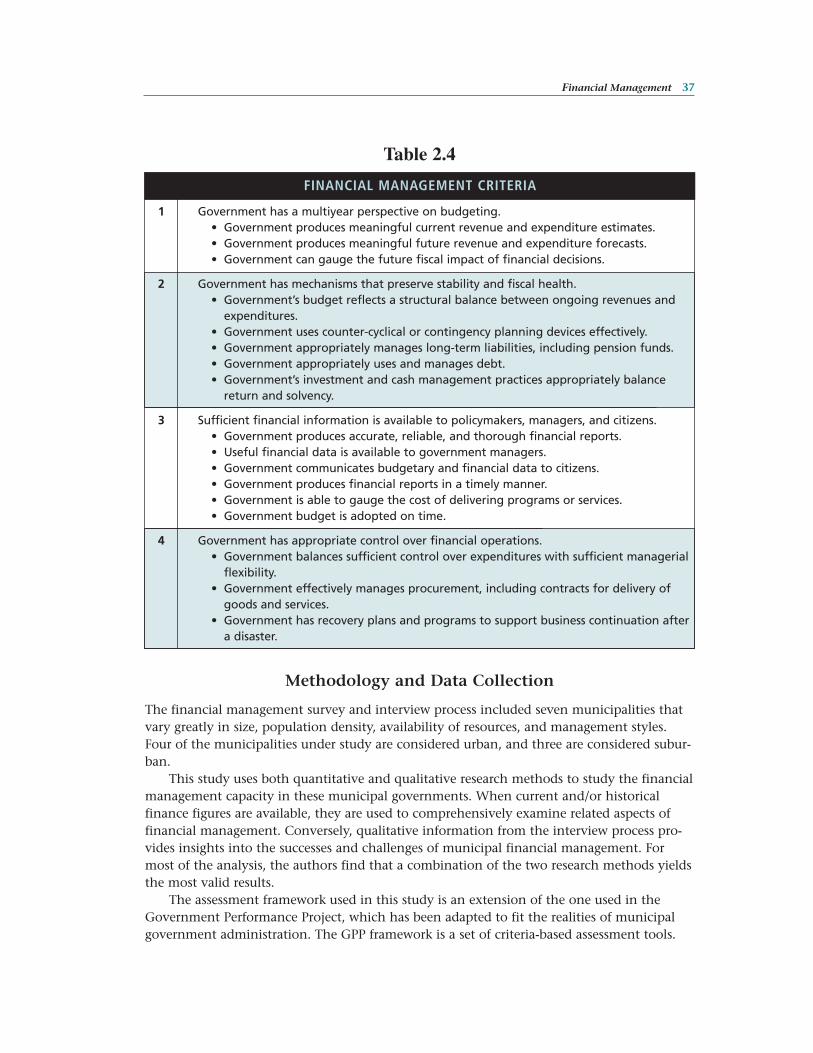

2.4 Financial Management Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

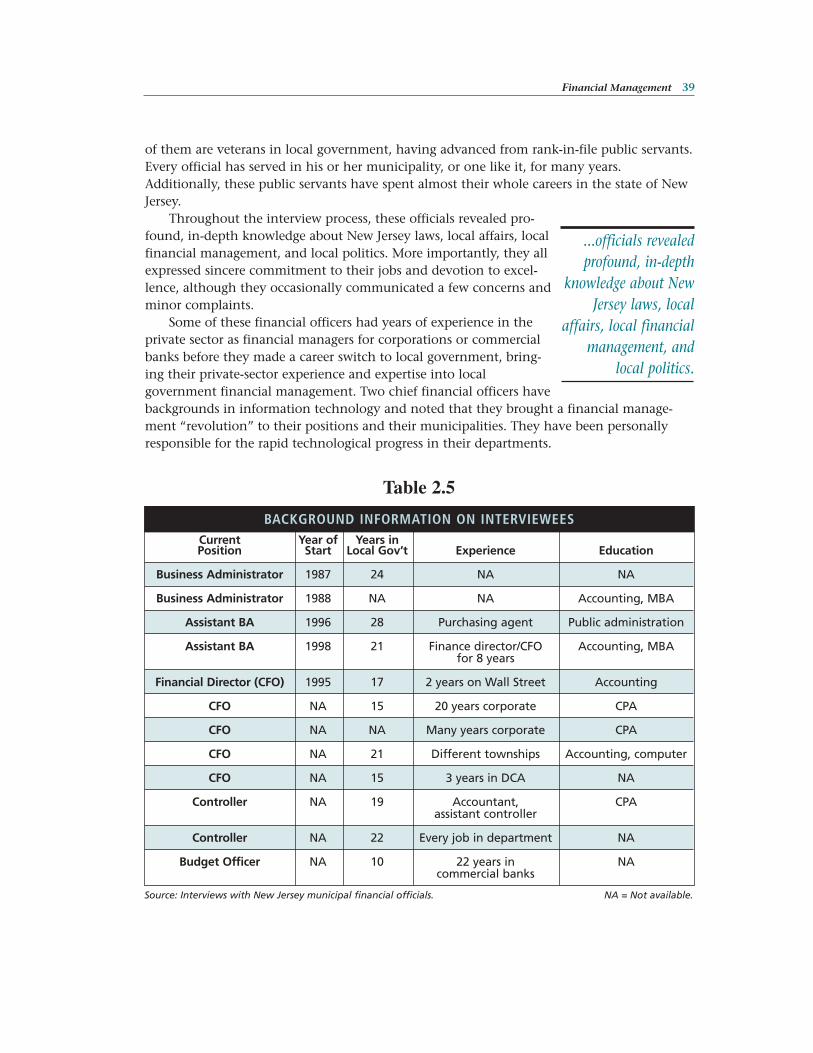

2.5 Background Information on Interviewees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

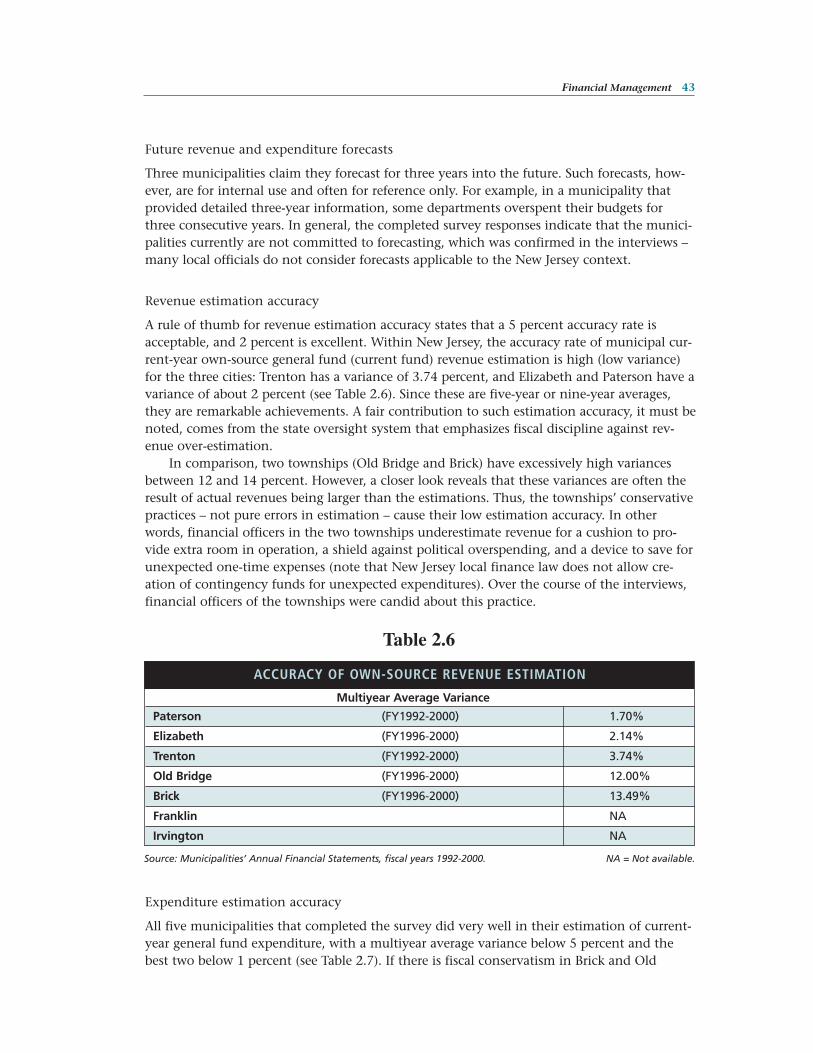

2.6 Accuracy of Own-Source Revenue Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

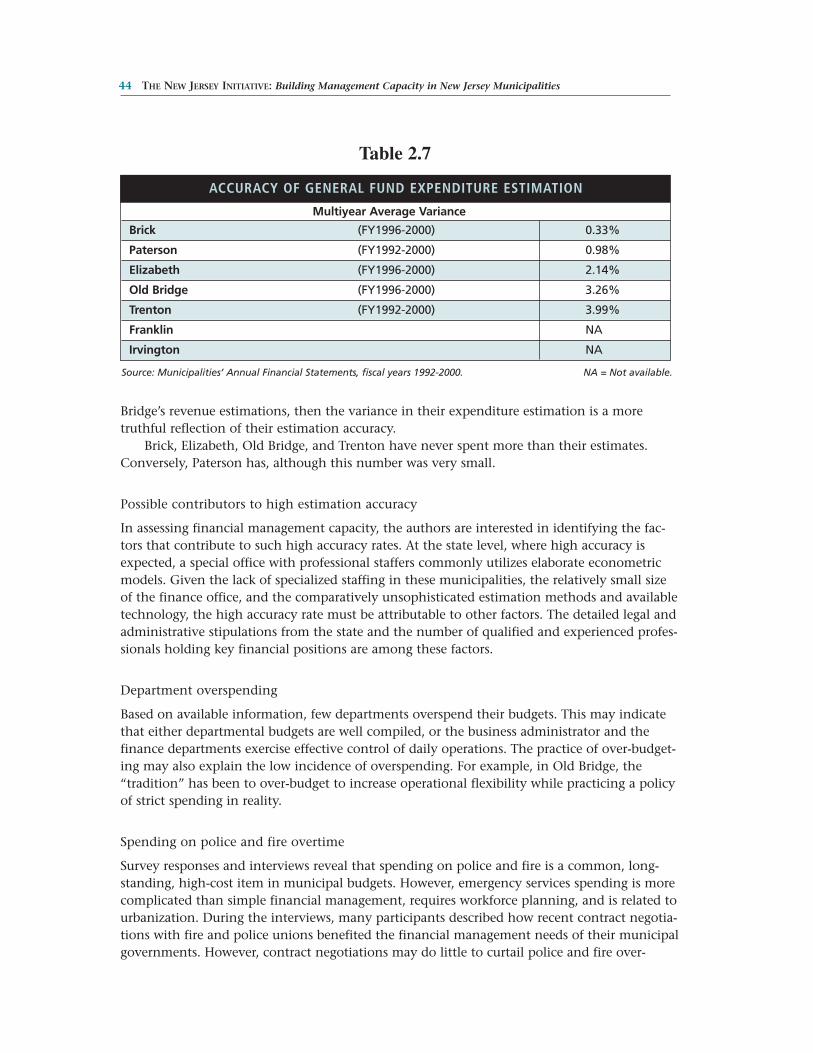

2.7 Accuracy of General Fund Expenditure Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

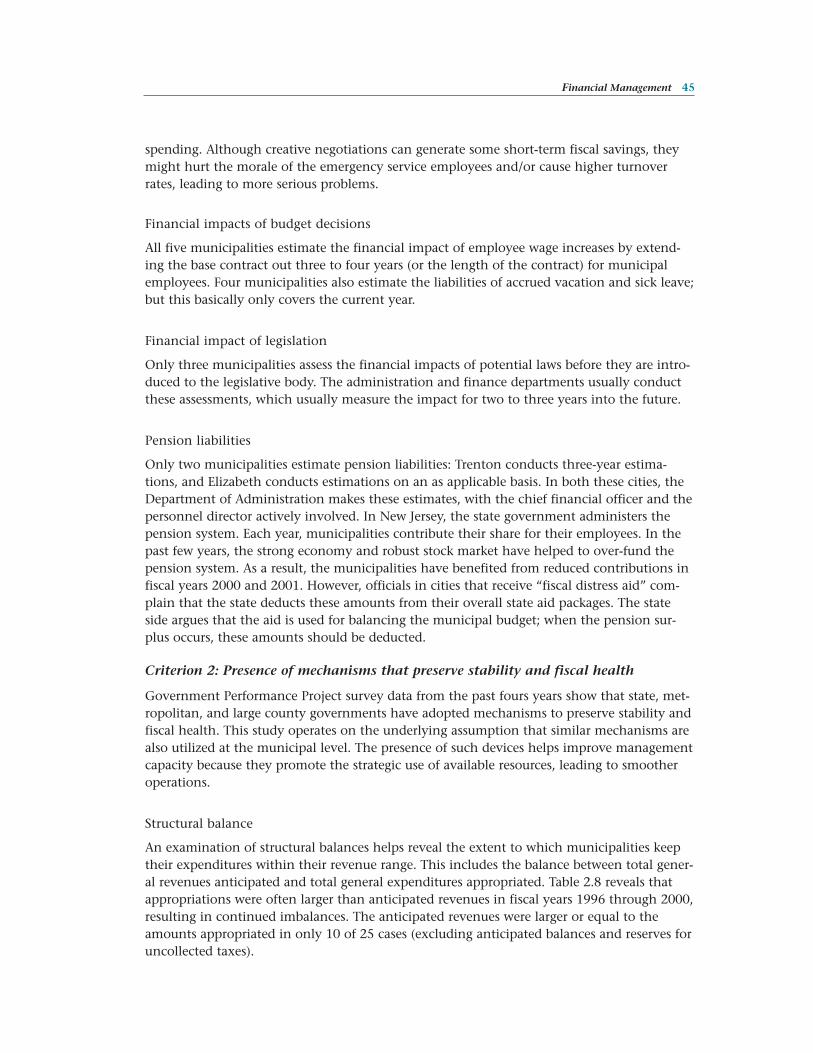

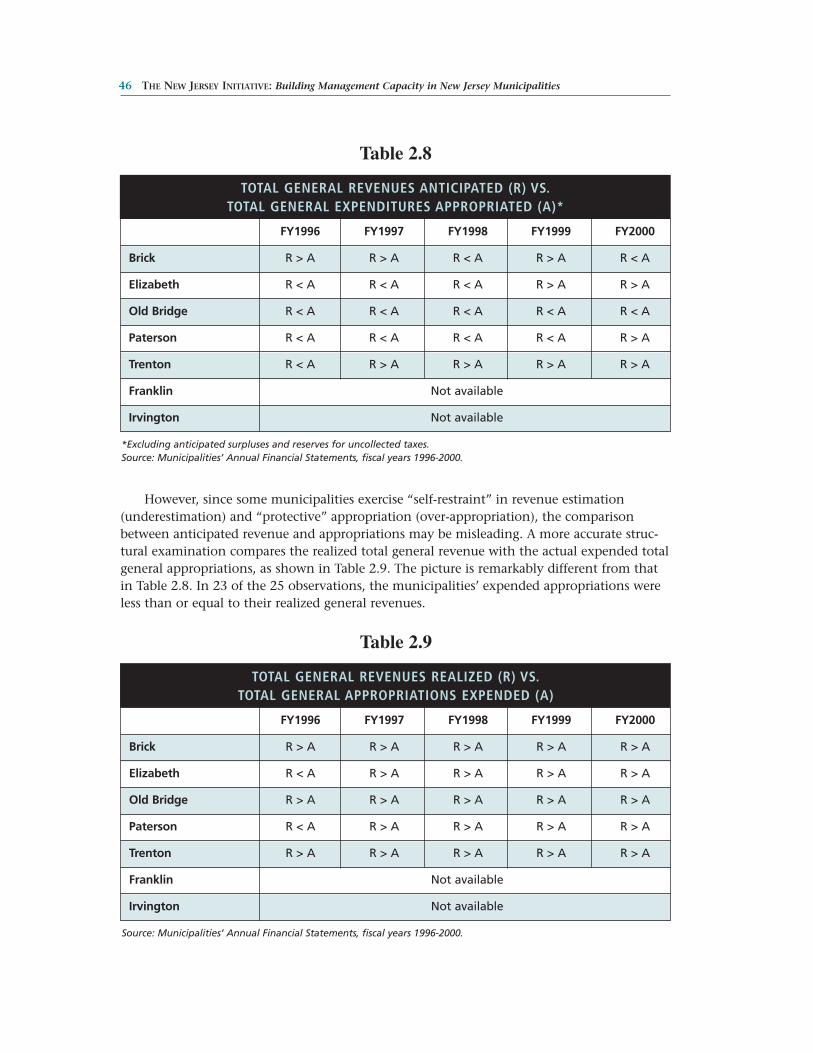

2.8 Total General Revenues Anticipated (R) vs. Total GeneralExpenditures Appropriated (A) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

2.9 Total General Revenues Realized (R) vs. Total General Appropriations Expended (A) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

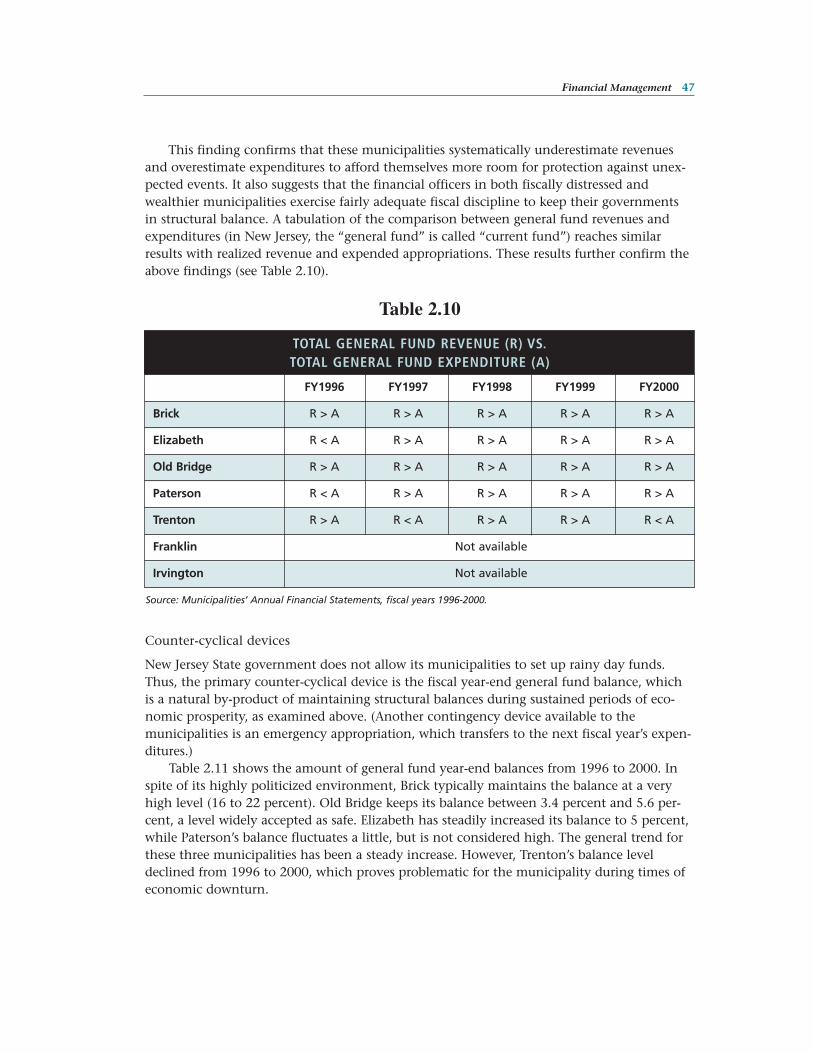

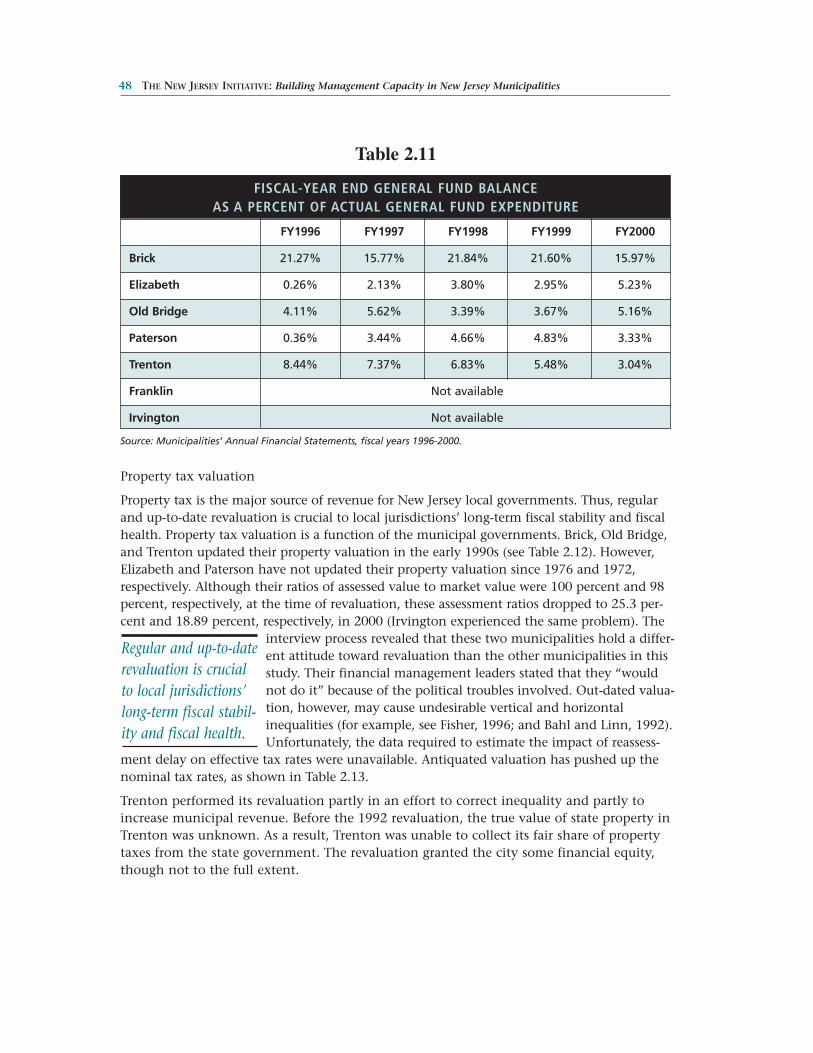

2.10 Total General Fund Revenue (R) vs. Total General Fund Expenditure (A) . . . . . . . . . . . . . . 47

2.11 Fiscal-Year End General Fund Balance as a Percent of Actual General Fund Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

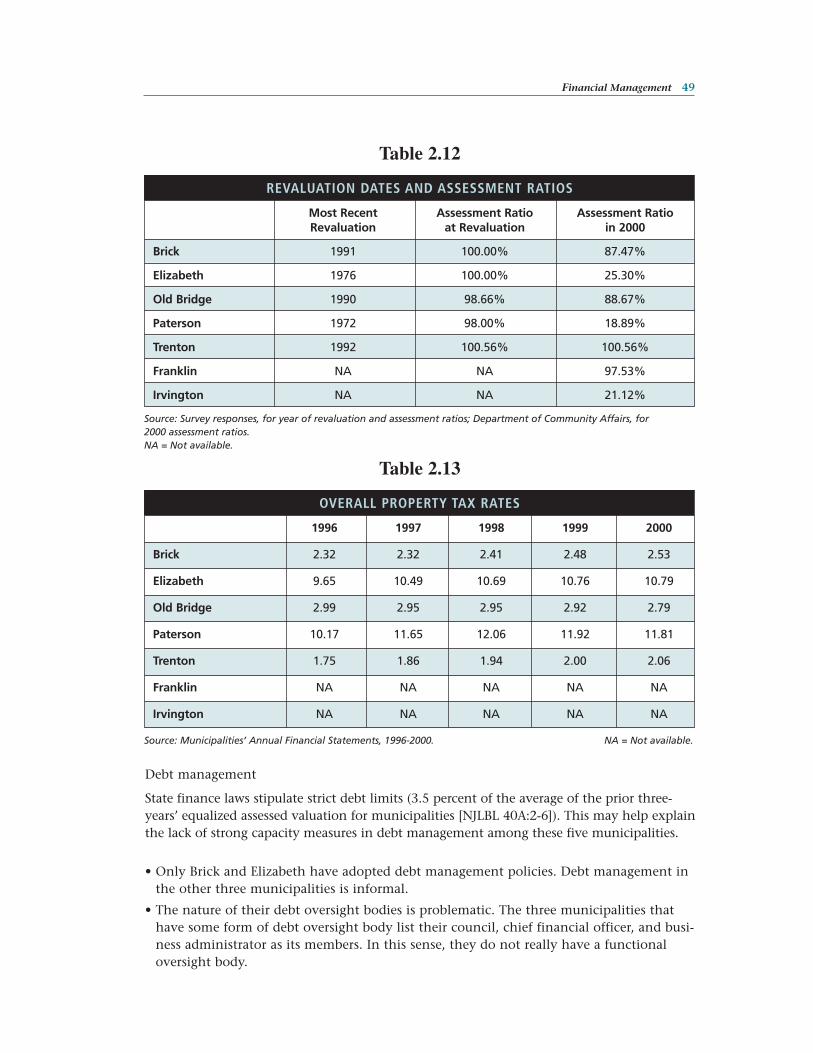

2.12 Revaluation Dates and Assessment Ratios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

2.13 Overall Property Tax Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

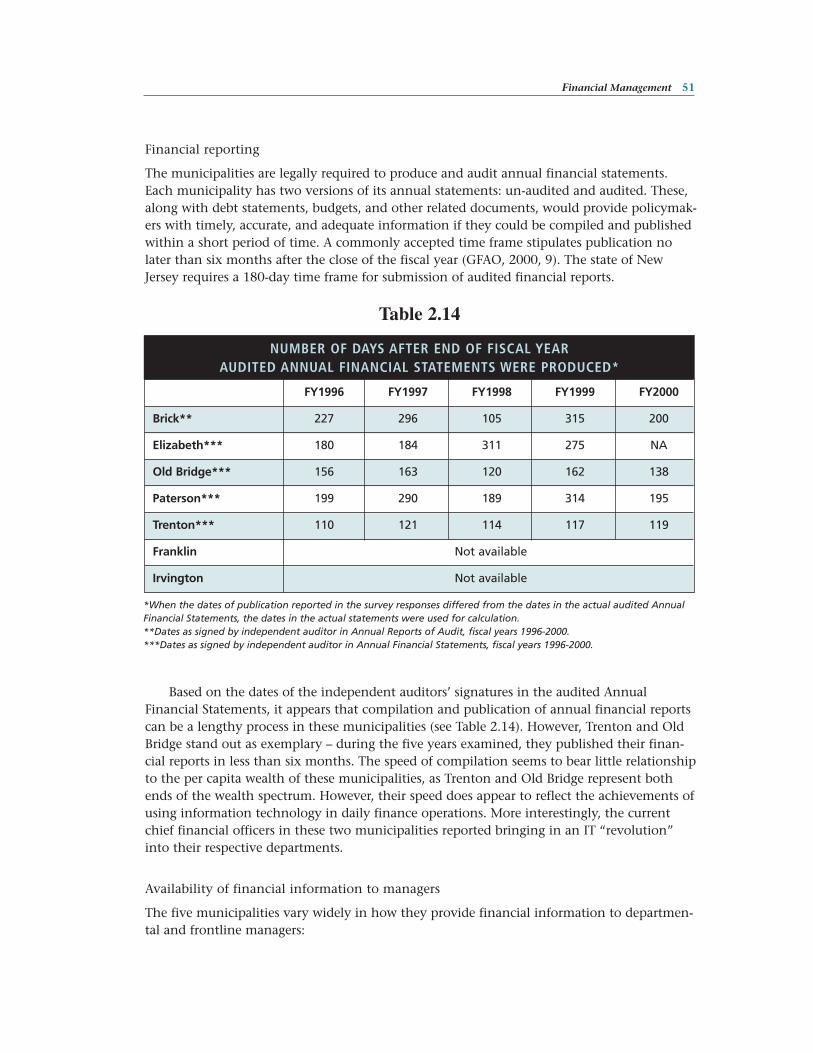

2.14 Number of Days after End of Fiscal Year Audited Annual Financial Statements Were Produced . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

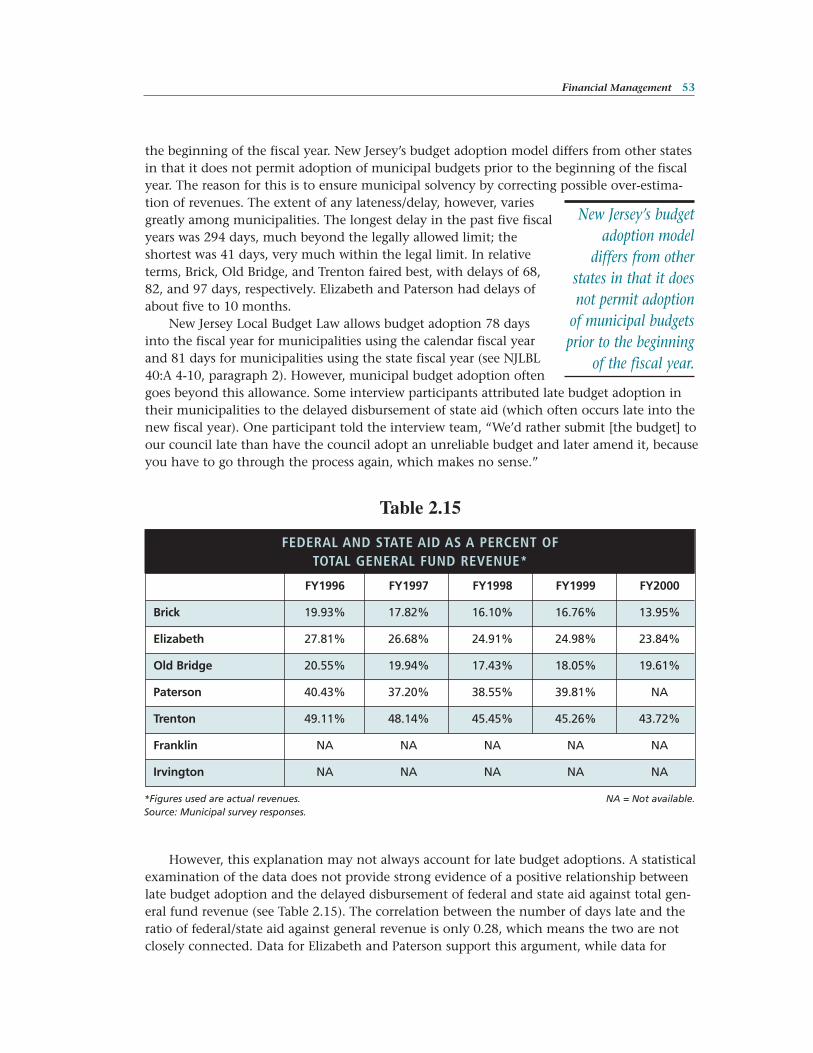

2.15 Federal and State Aid as a Percent of Total General Fund Revenue. . . . . . . . . . . . . . . . . . . . 53

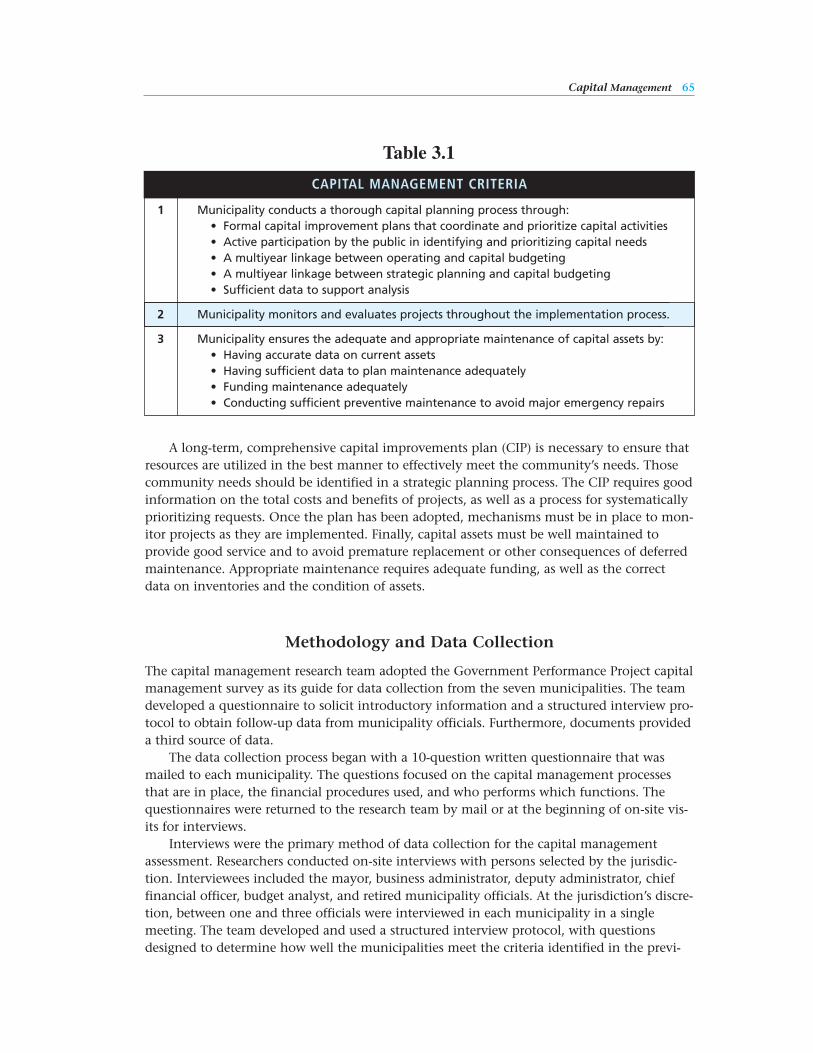

3.1 Capital Management Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

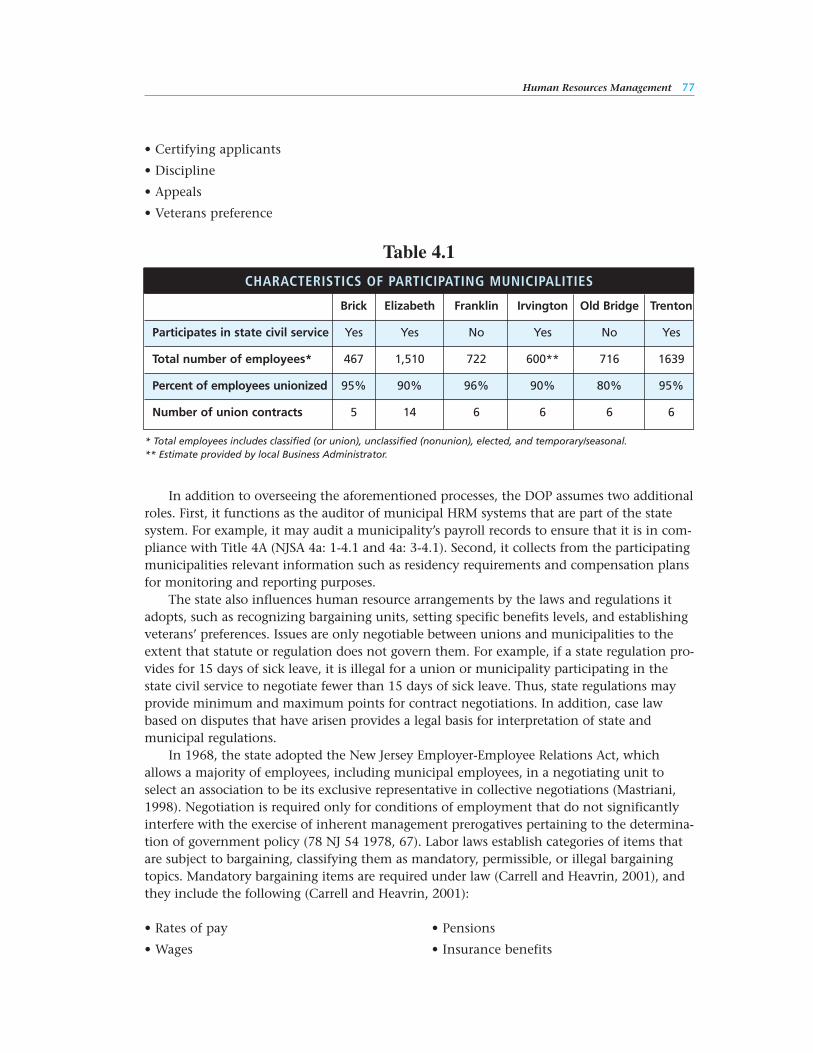

4.1 Characteristics of Participating Municipalities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

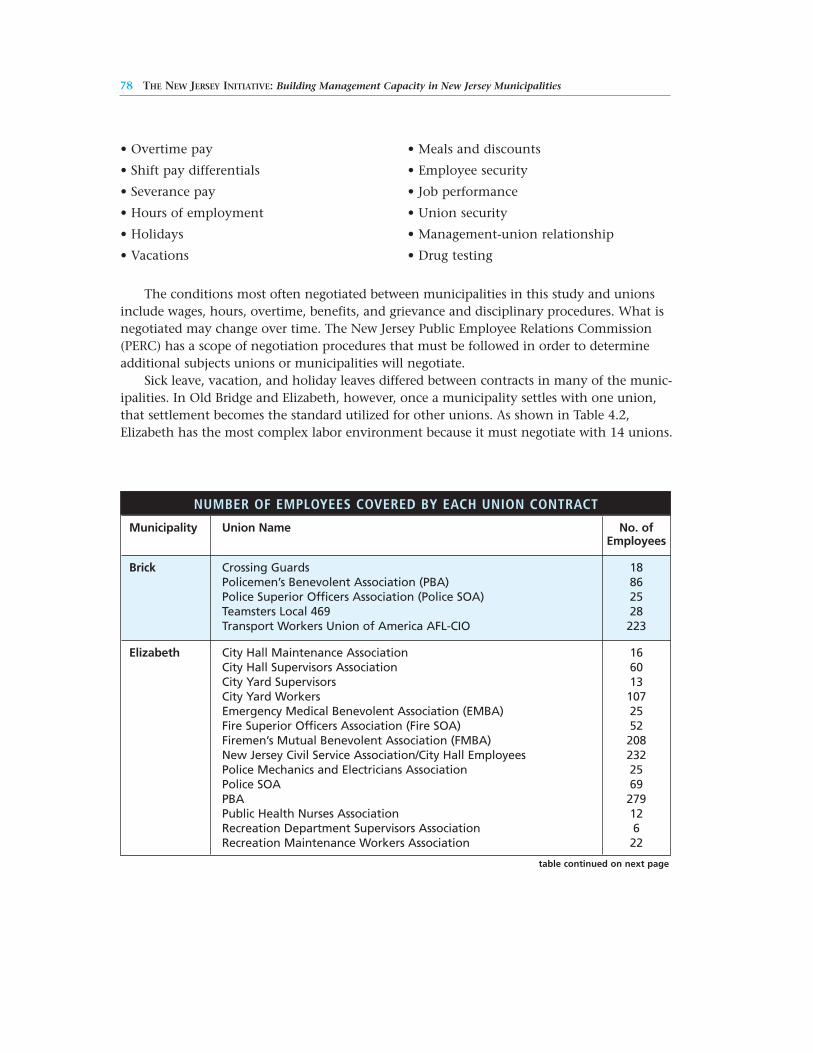

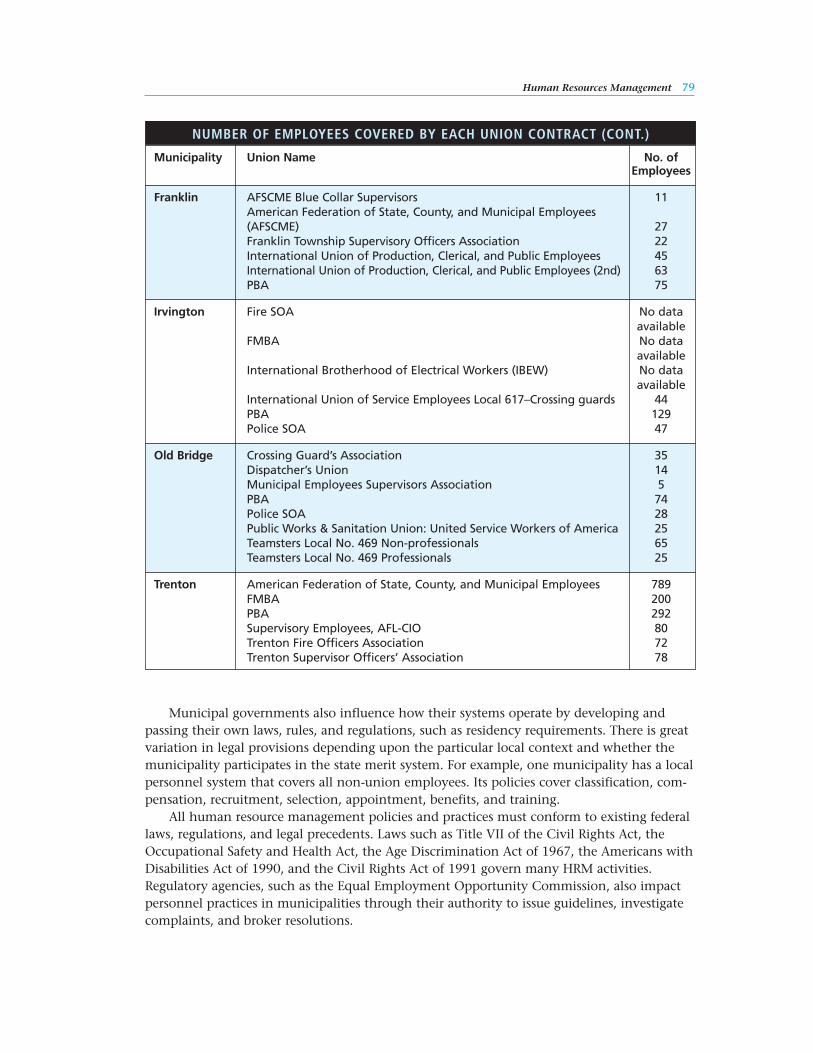

4.2 Number of Employees Covered by Each Union Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

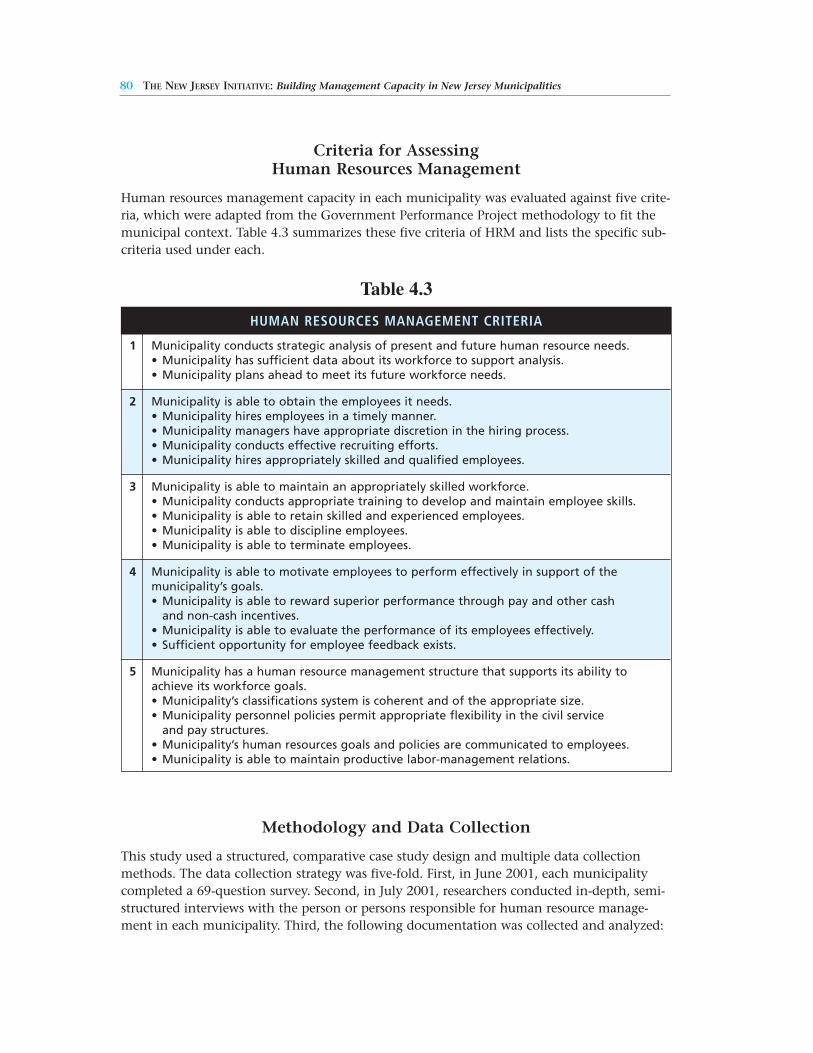

4.3 Human Resources Management Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

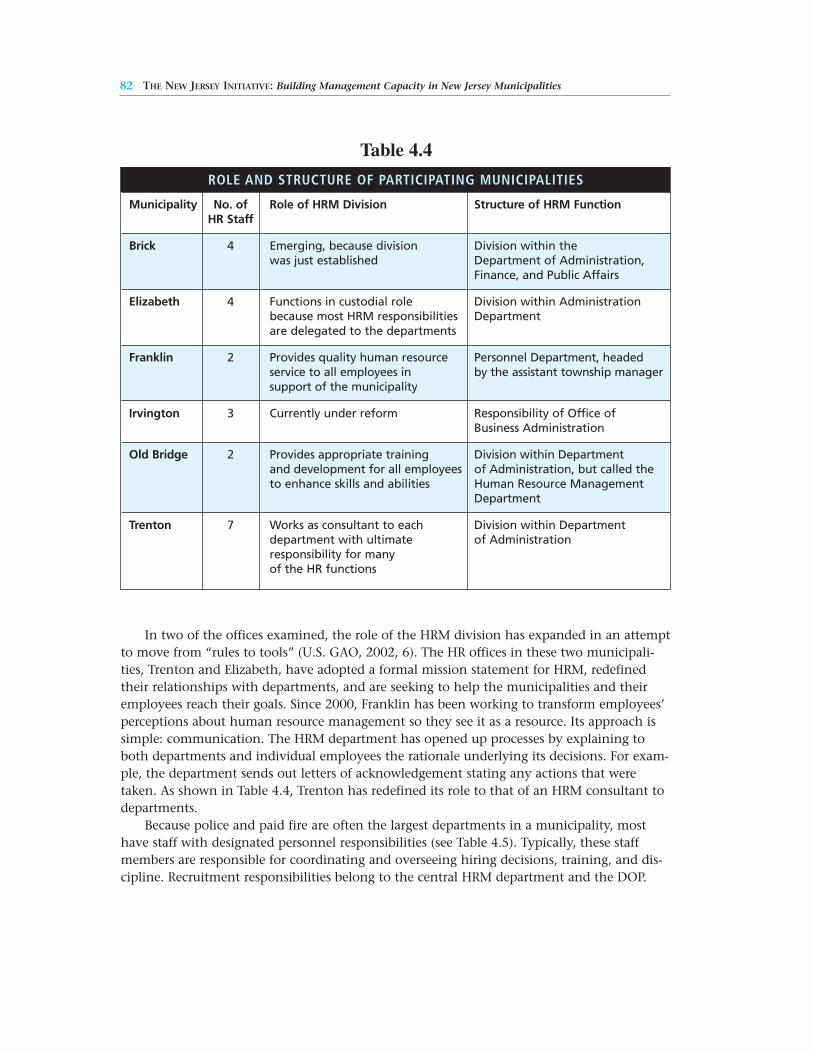

4.4 Role and Structure of Participating Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

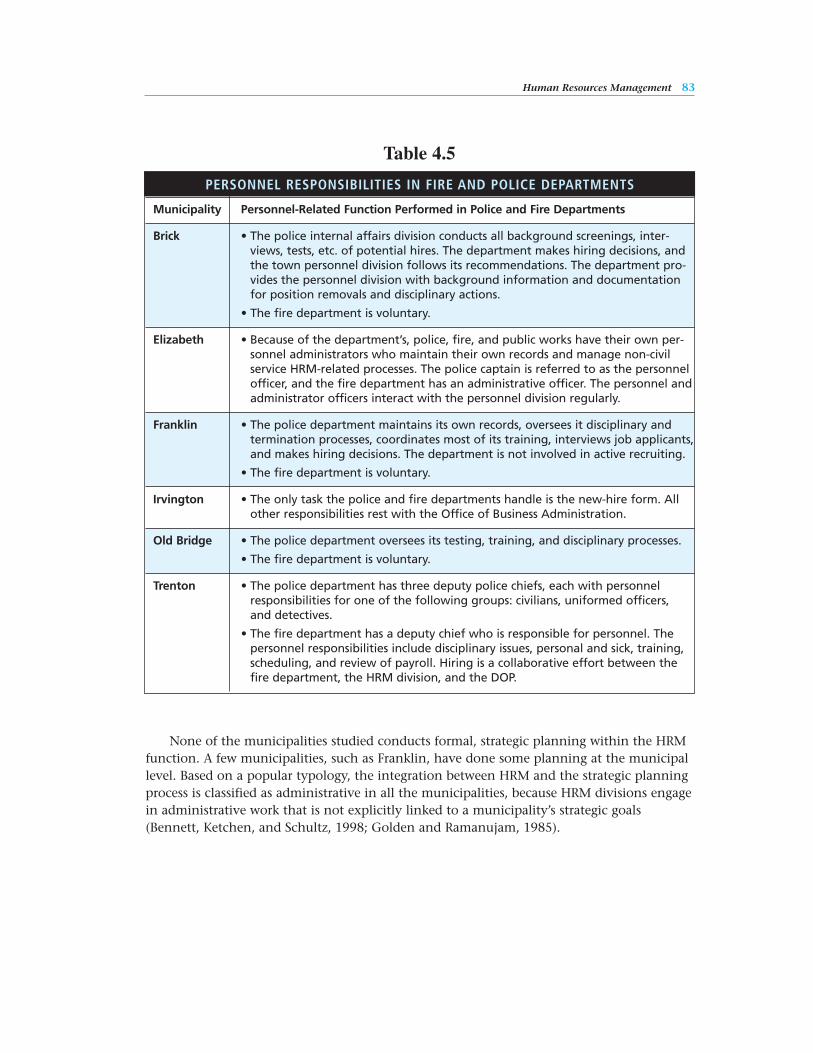

4.5 Personnel Responsibilities in Fire and Police Departments . . . . . . . . . . . . . . . . . . . . . . . . . . 83

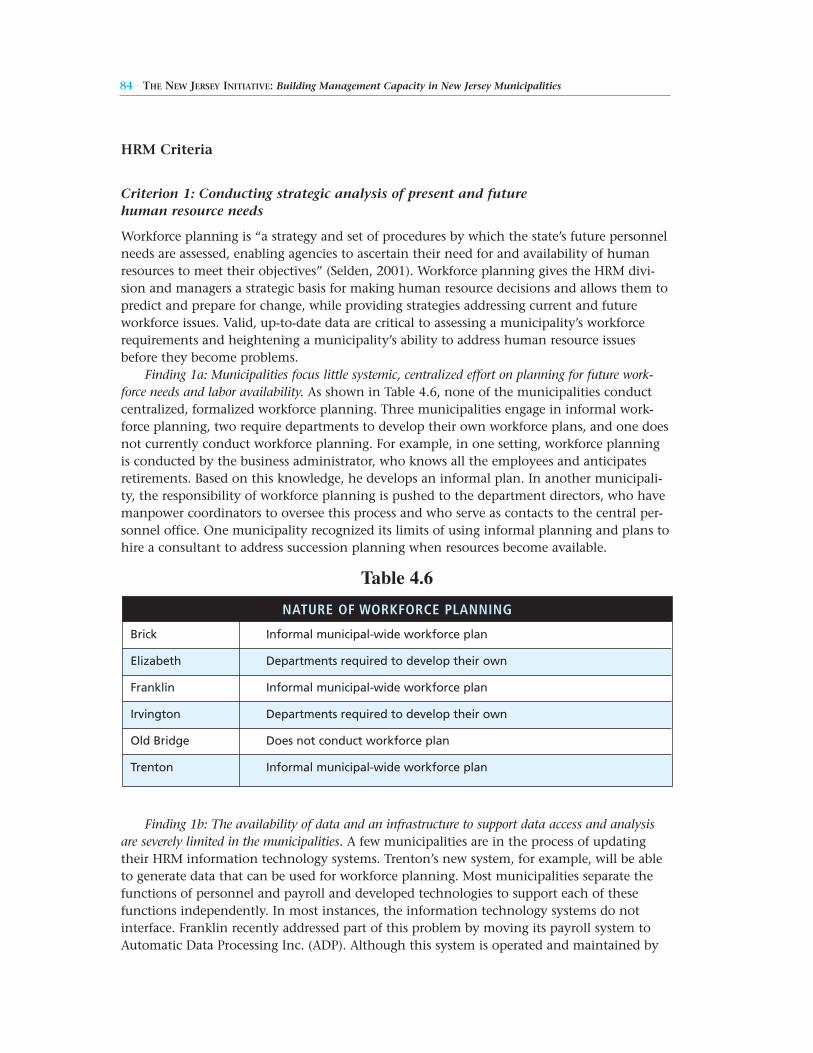

4.6 Nature of Workforce Planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

4.7 Testing and Use of Provisional and Temporary Employees . . . . . . . . . . . . . . . . . . . . . . . . . . 86

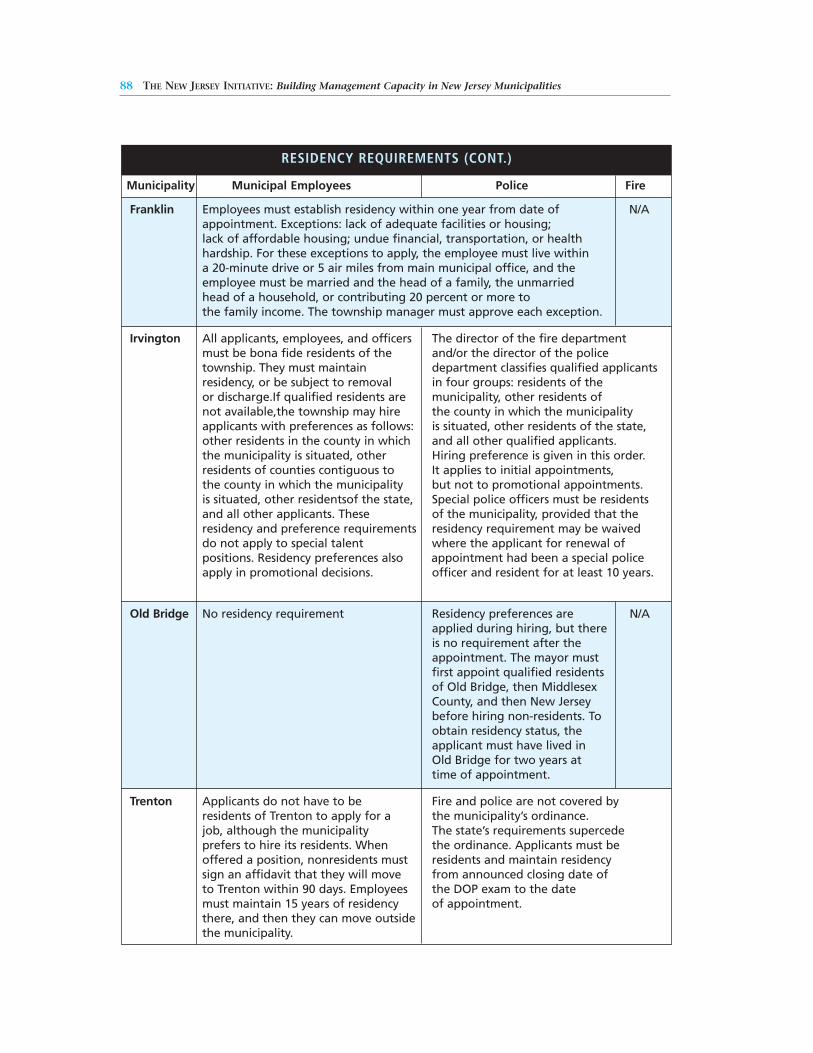

4.8 Residency Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

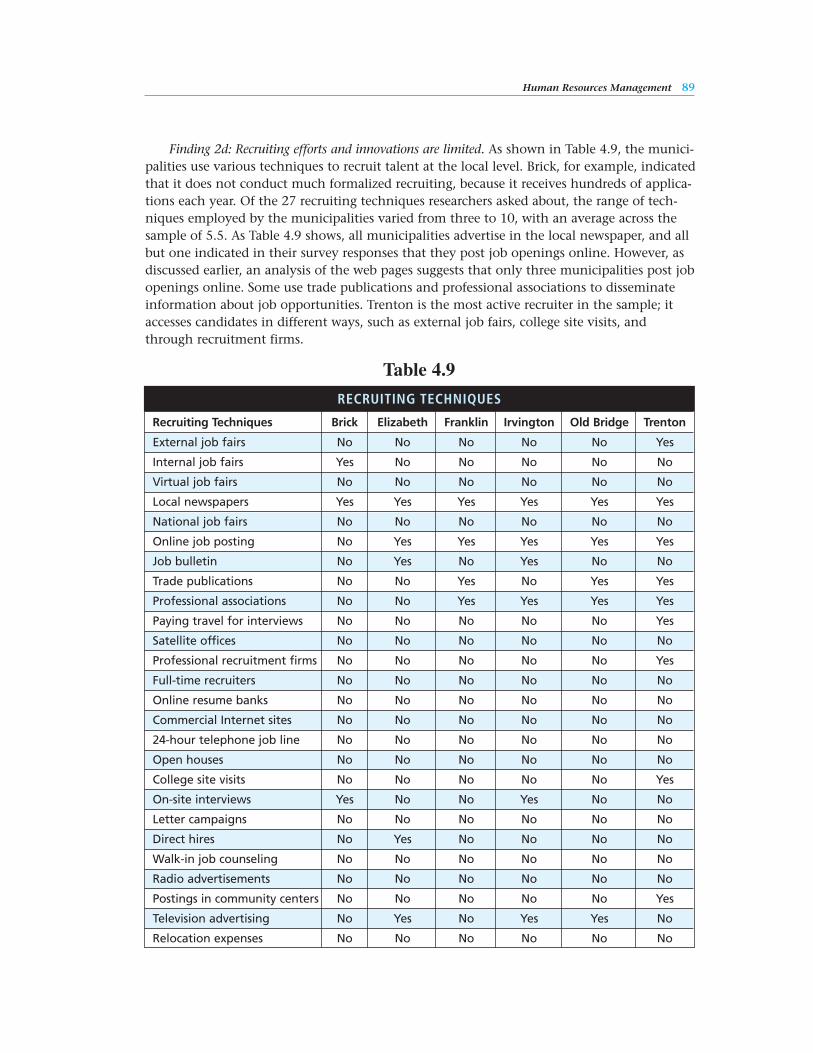

4.9 Recruiting Techniques. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

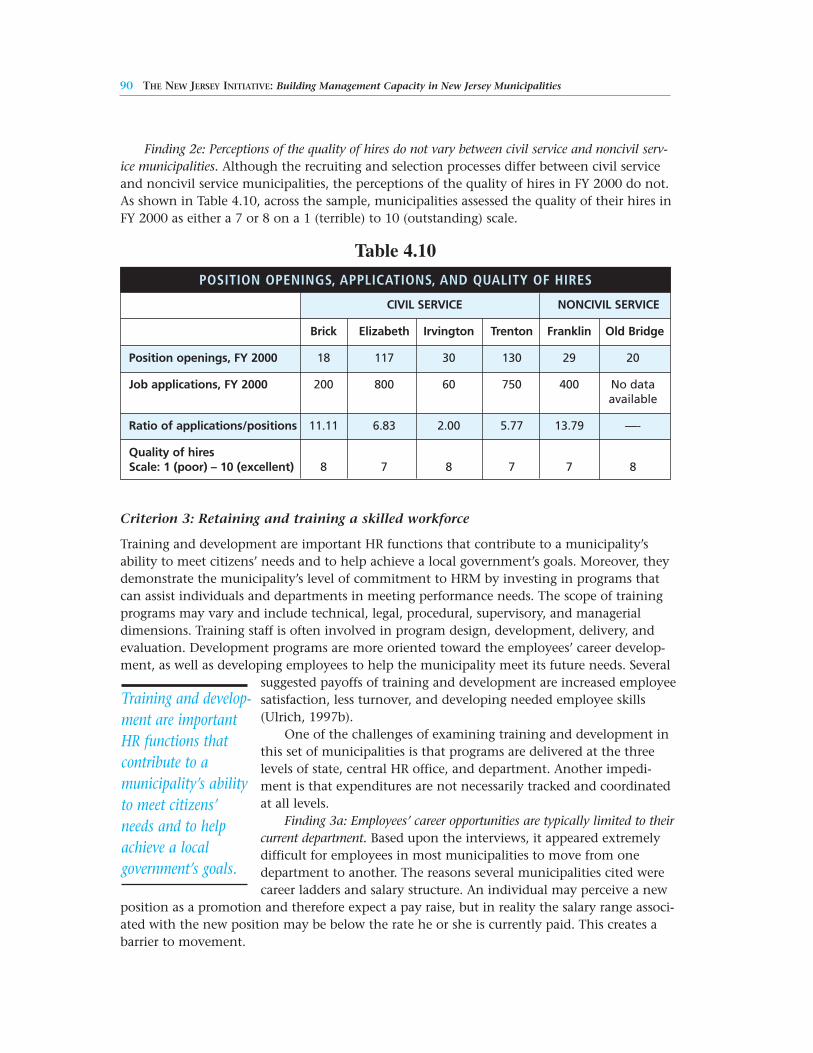

4.10 Position Openings, Applications, and Quality of Hires . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

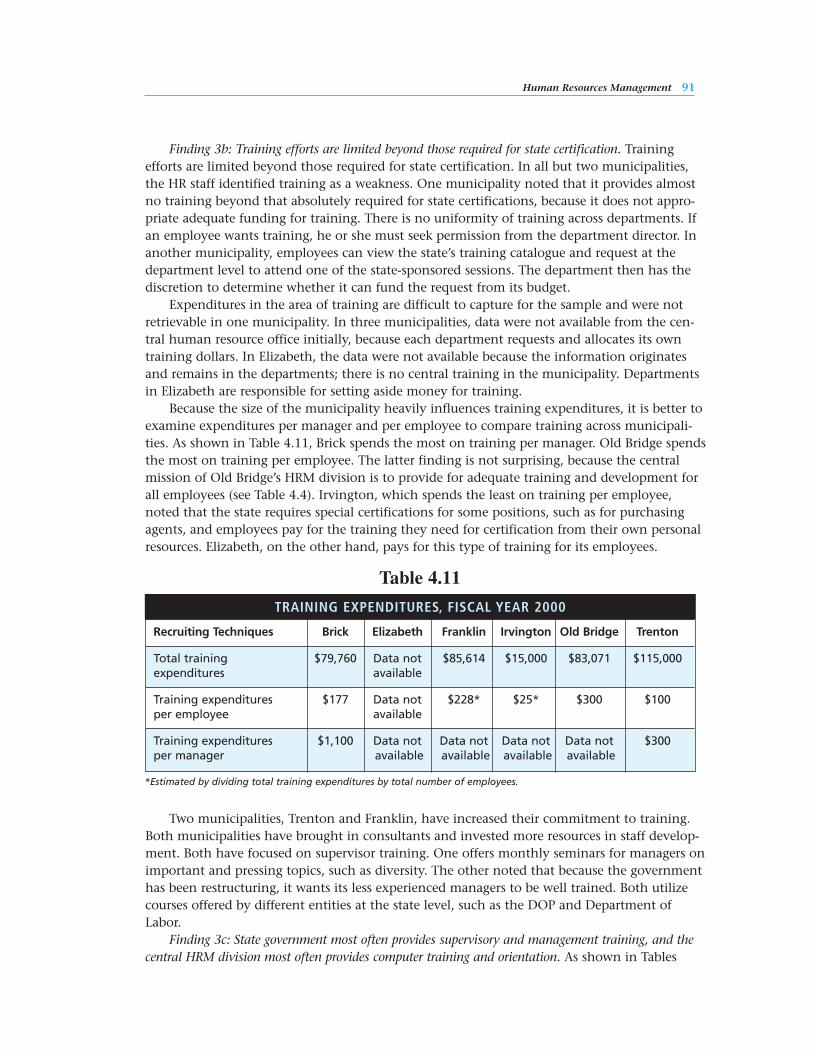

4.11 Training Expenditures, Fiscal Year 2000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

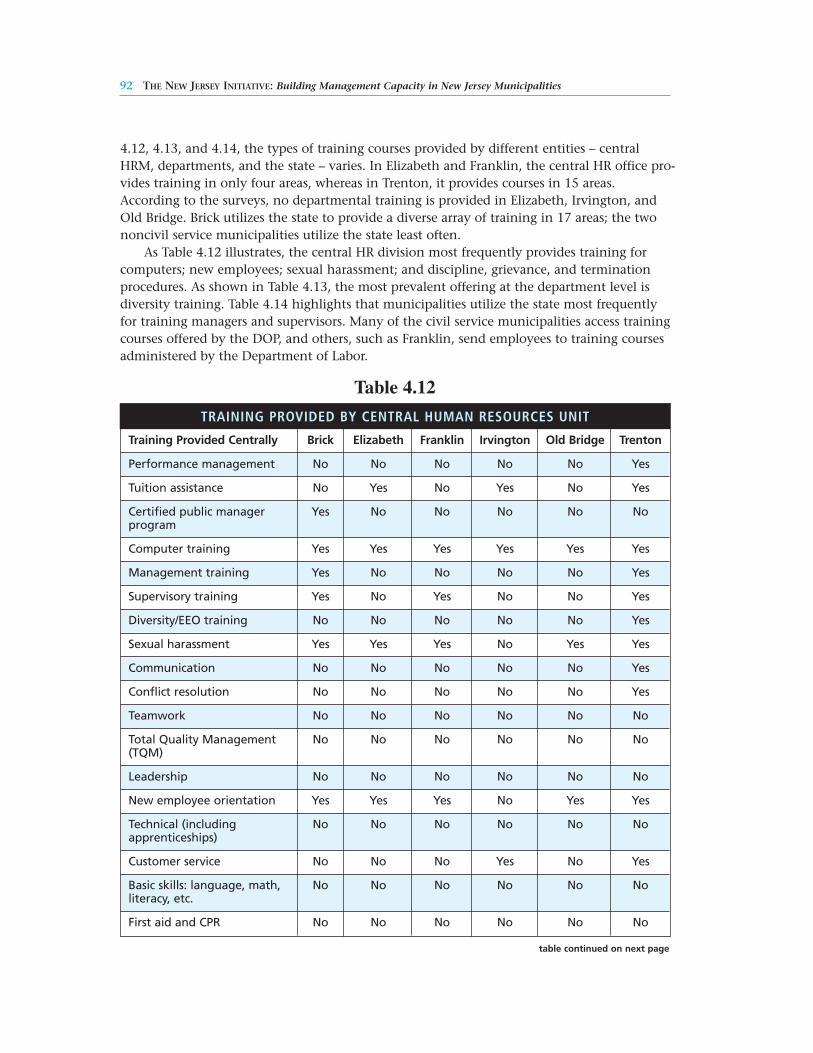

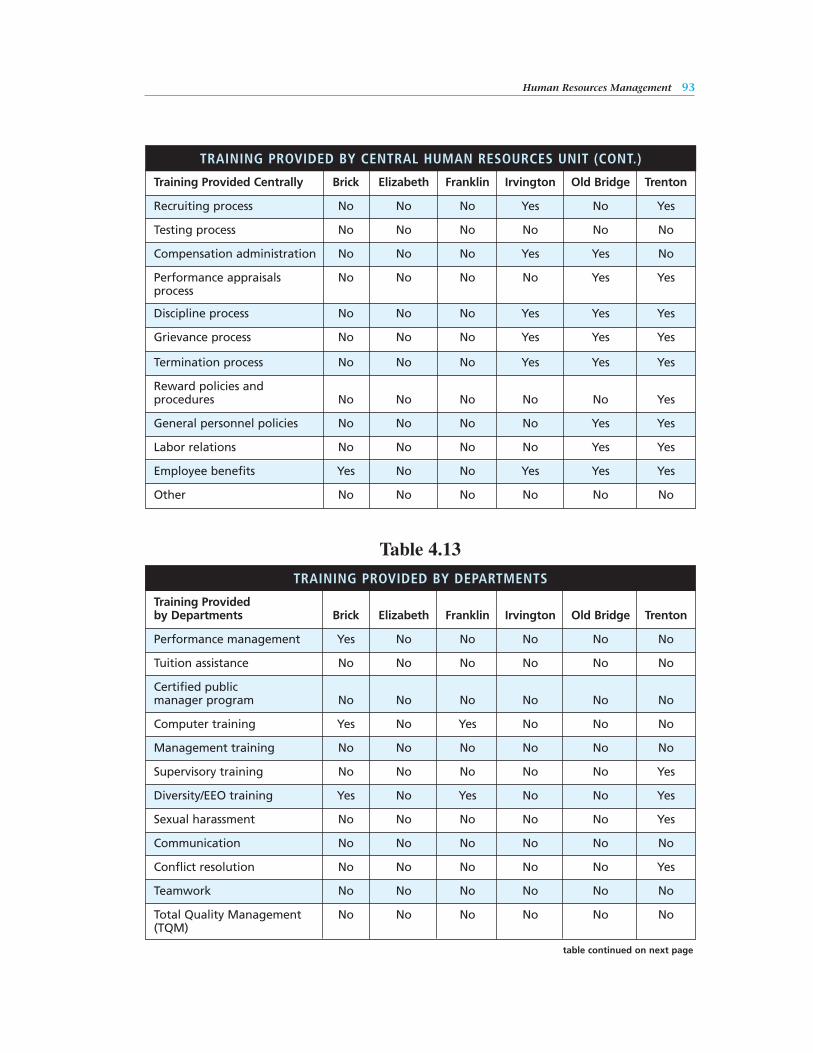

4.12 Training Provided by Central Human Resources Unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

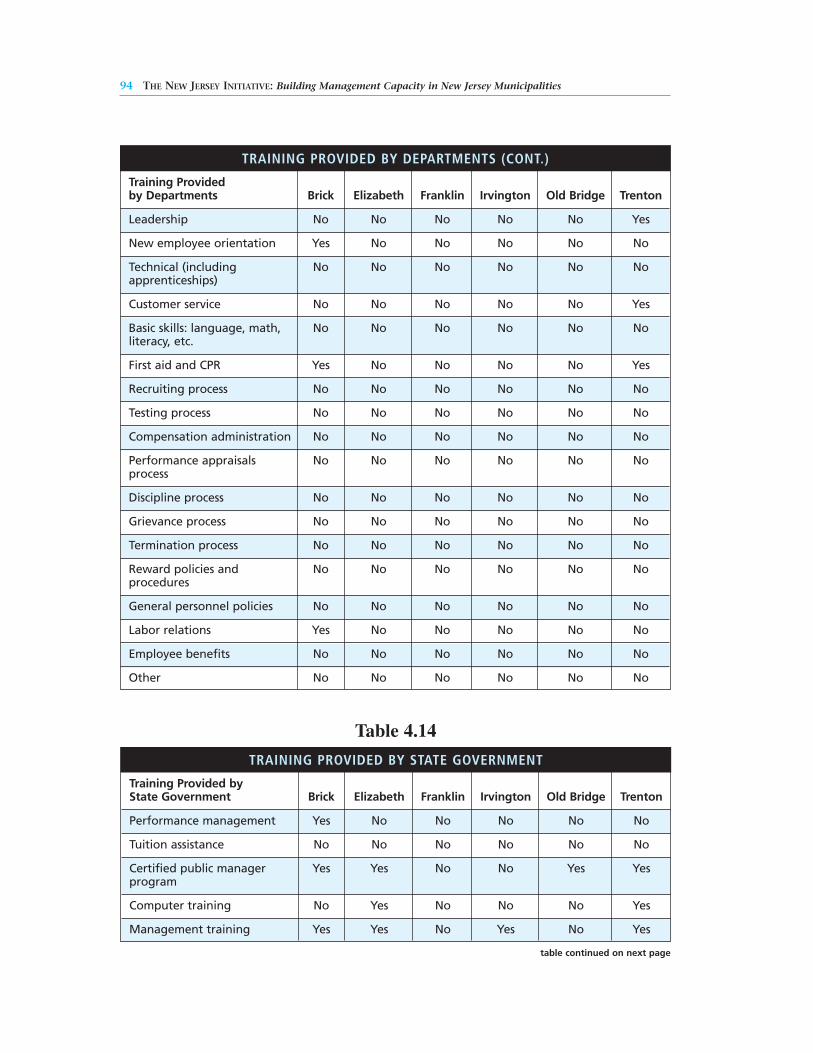

4.13 Training Provided by Departments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

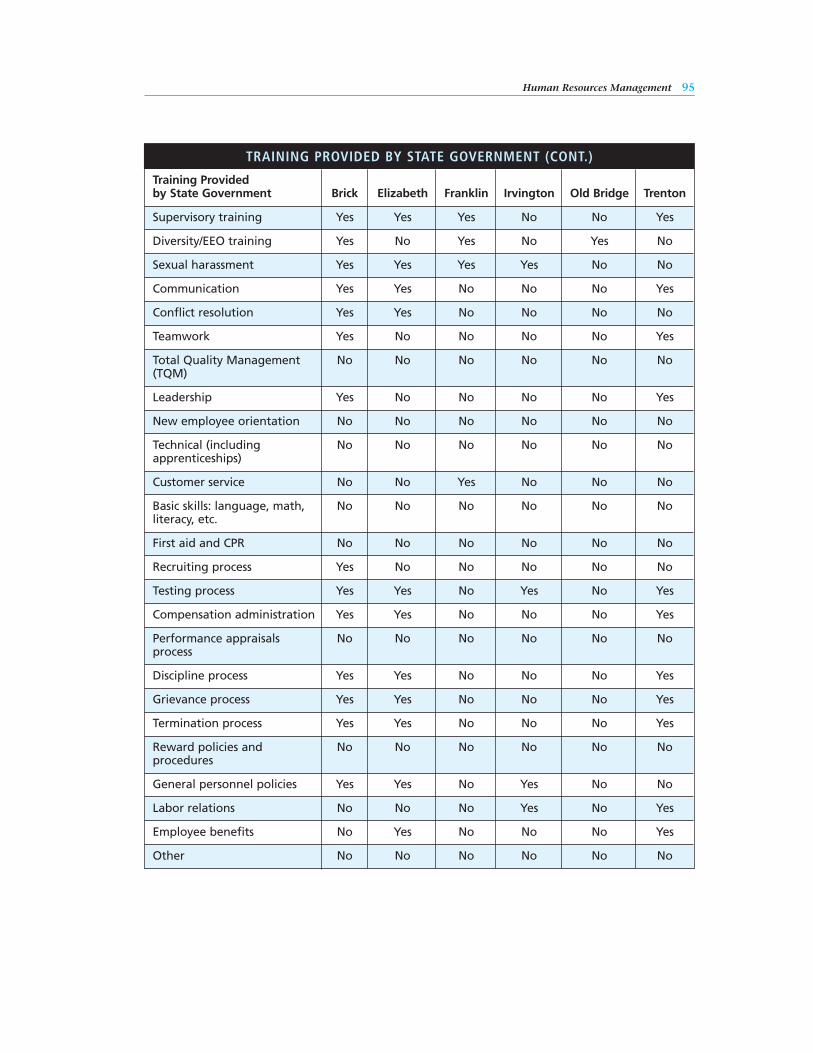

4.14 Training Provided by State Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

x THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

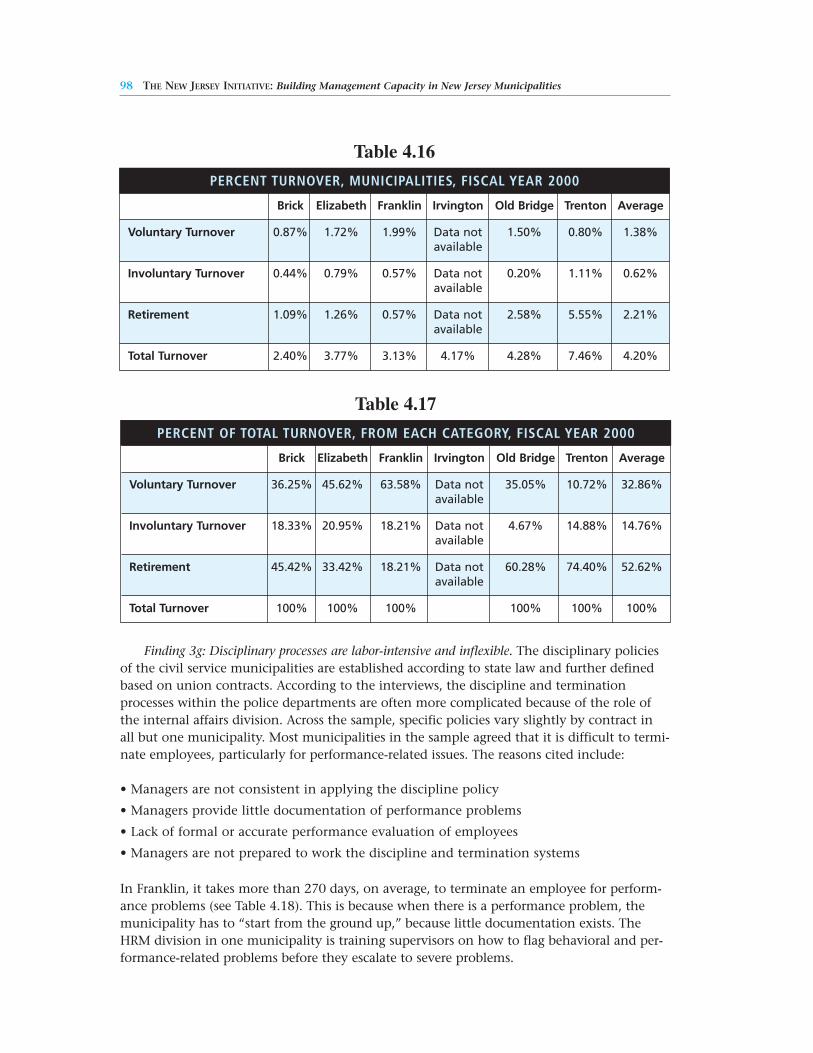

4.15 Tuition Reimbursement Based on Contracts and Educational Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.16 Percent Turnover, Municipalities, Fiscal Year 2000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

4.17 Percent of Total Turnover from Each Category, Fiscal Year 2000 . . . . . . . . . . . . . . . . . . . . . 98

4.18 Termination and Discipline . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

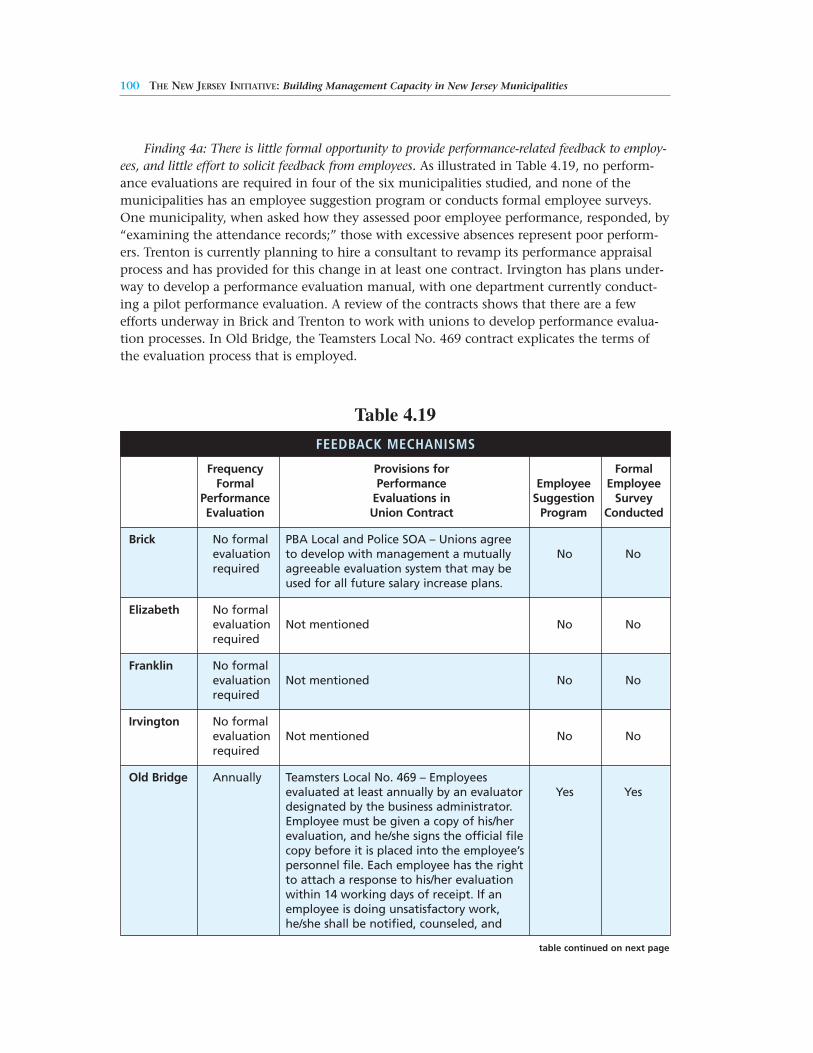

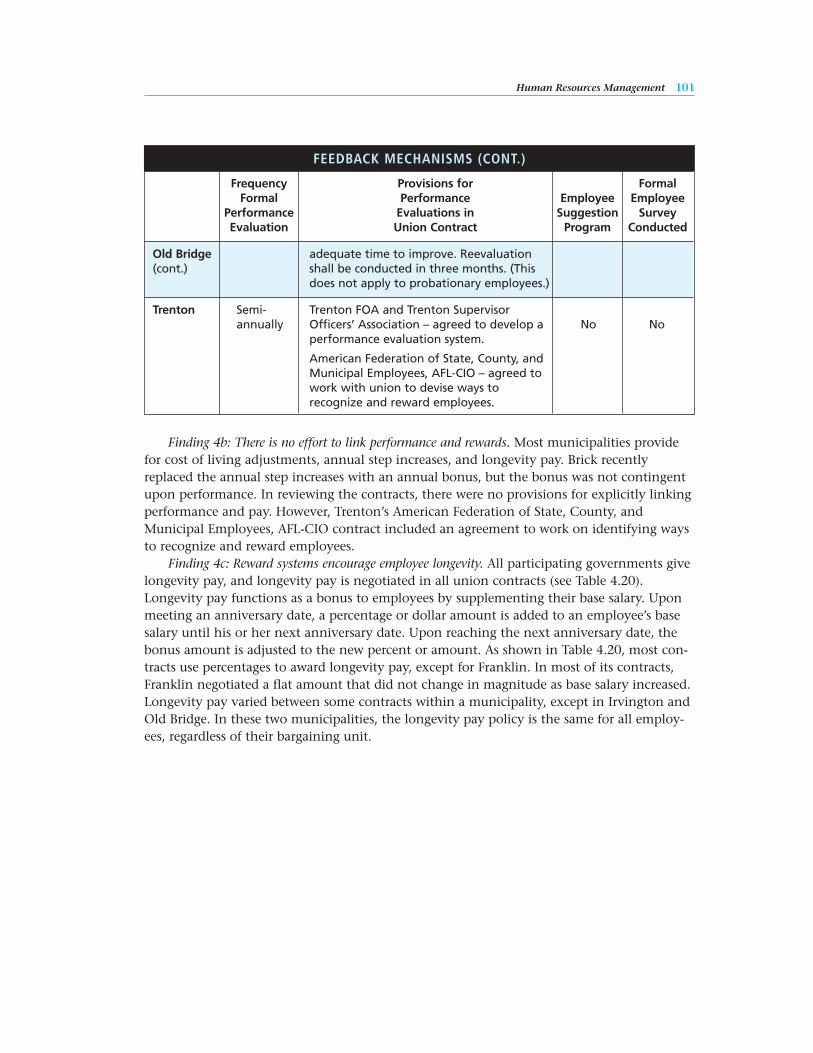

4.19 Feedback Mechanisms. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

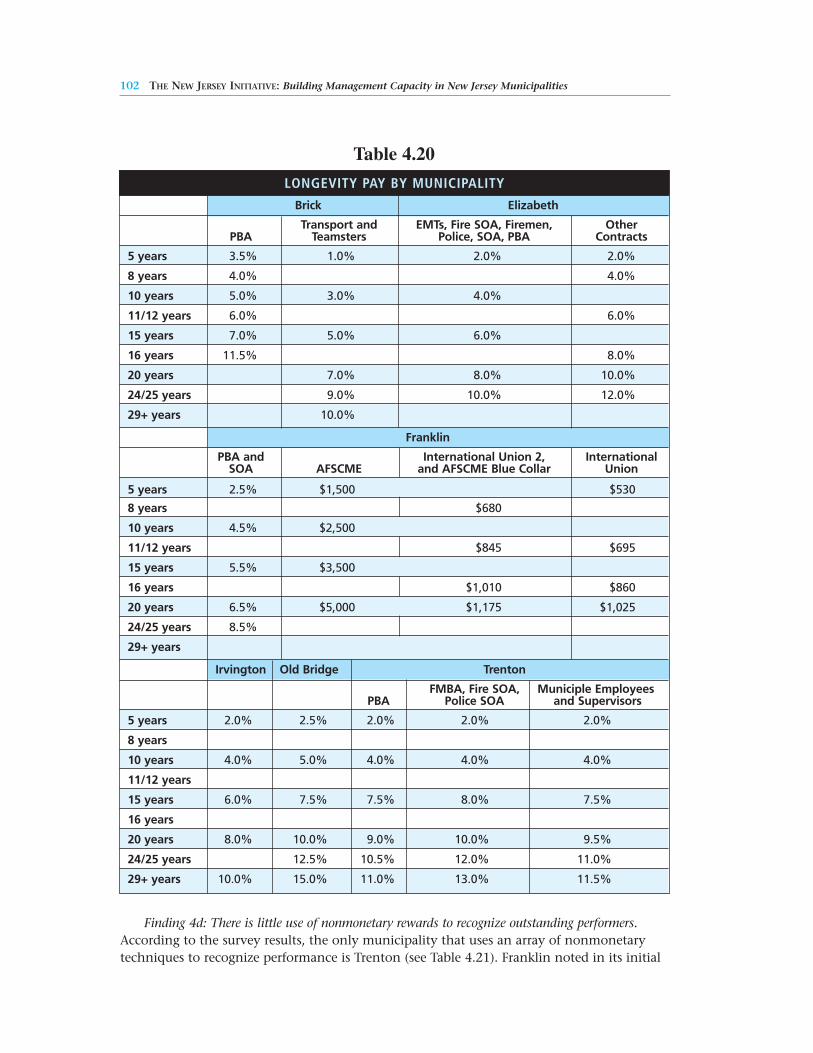

4.20 Longevity Pay by Municipality. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

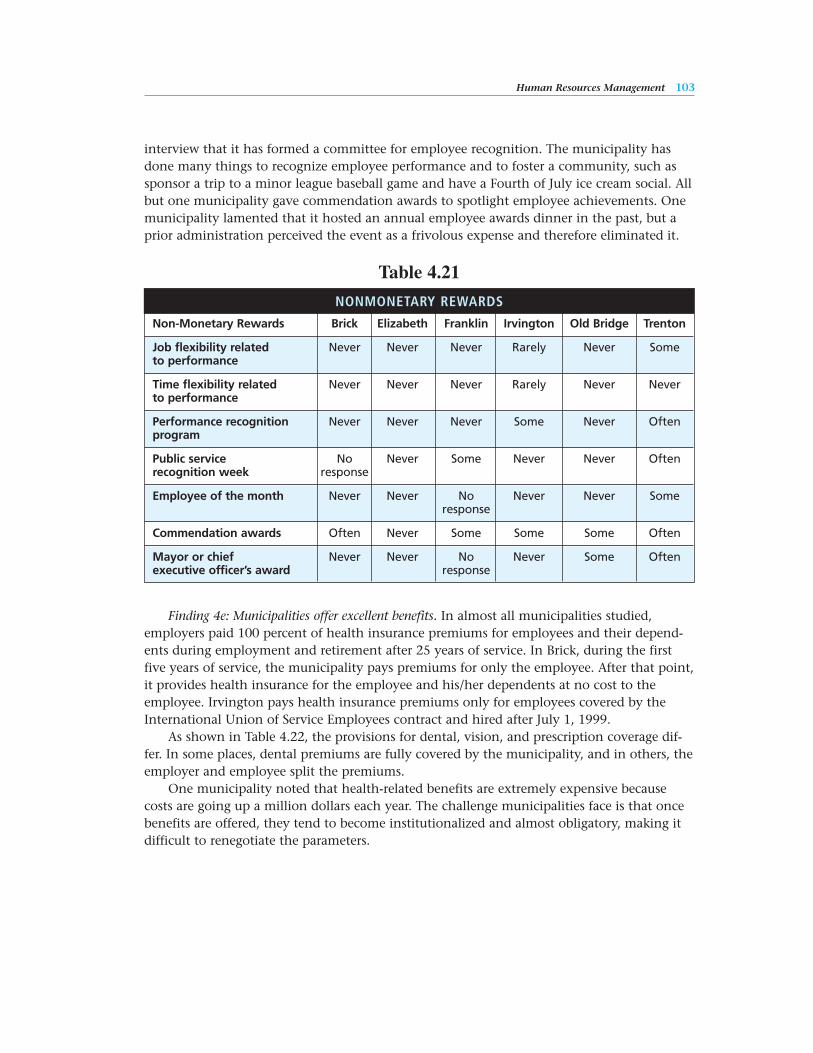

4.21 Nonmonetary Rewards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

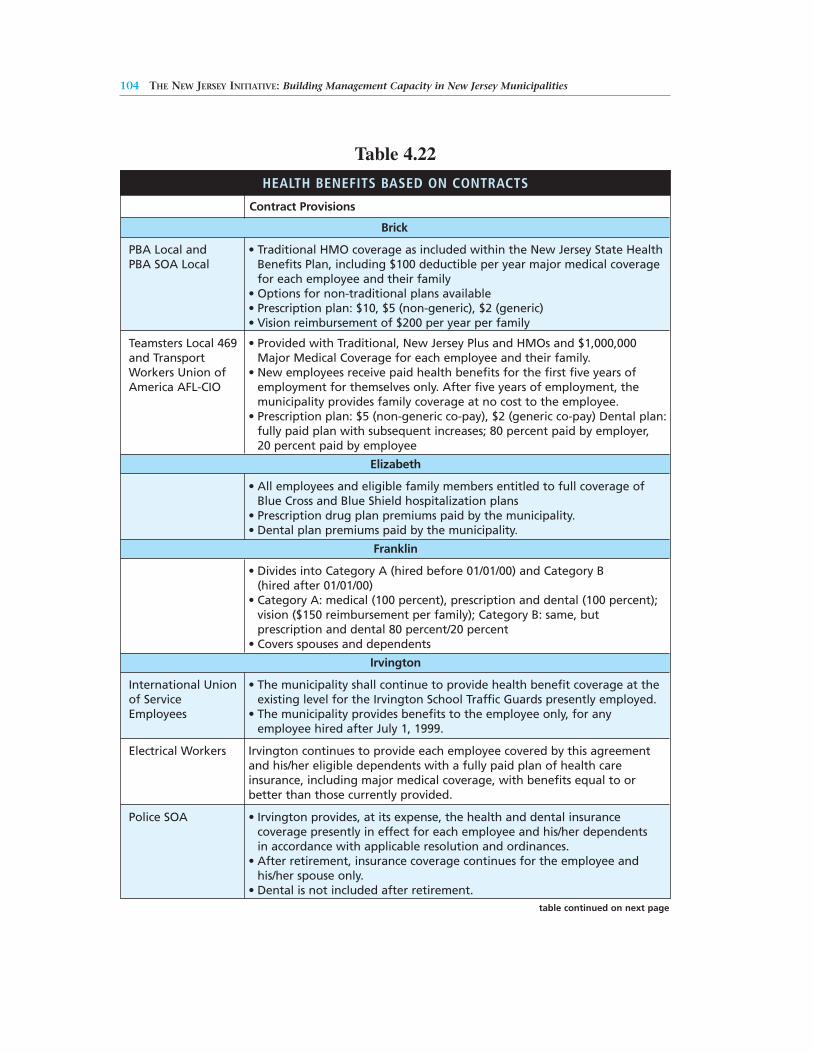

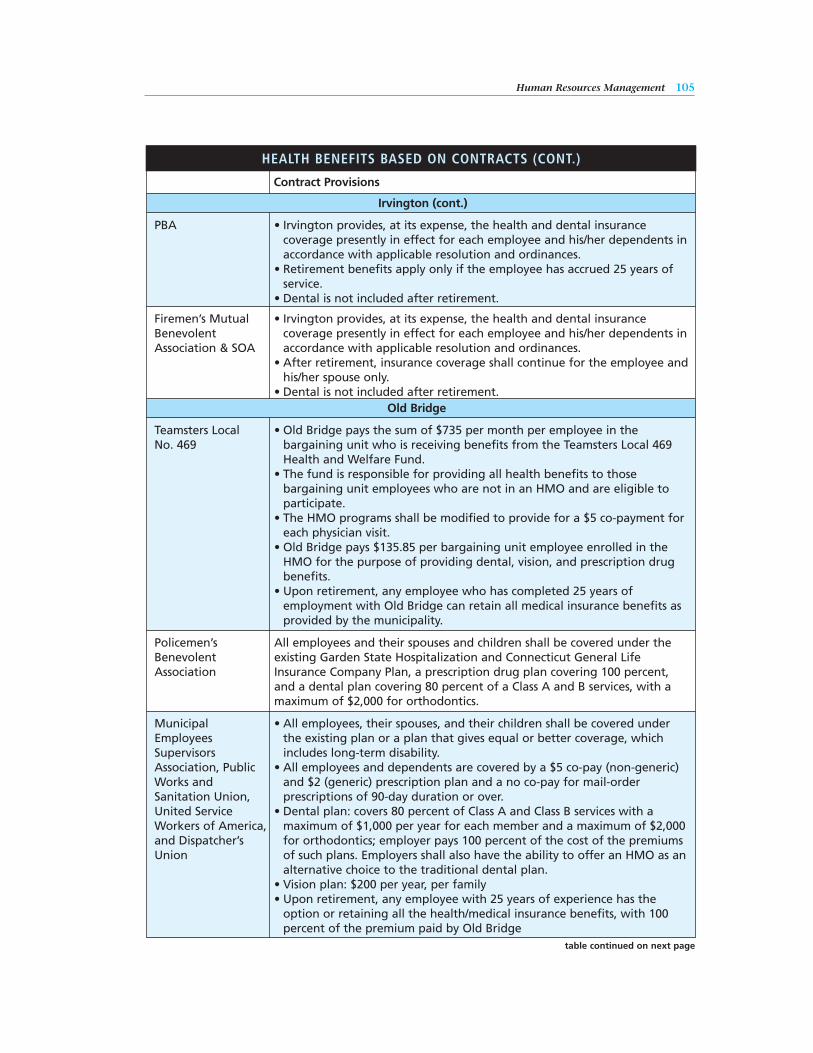

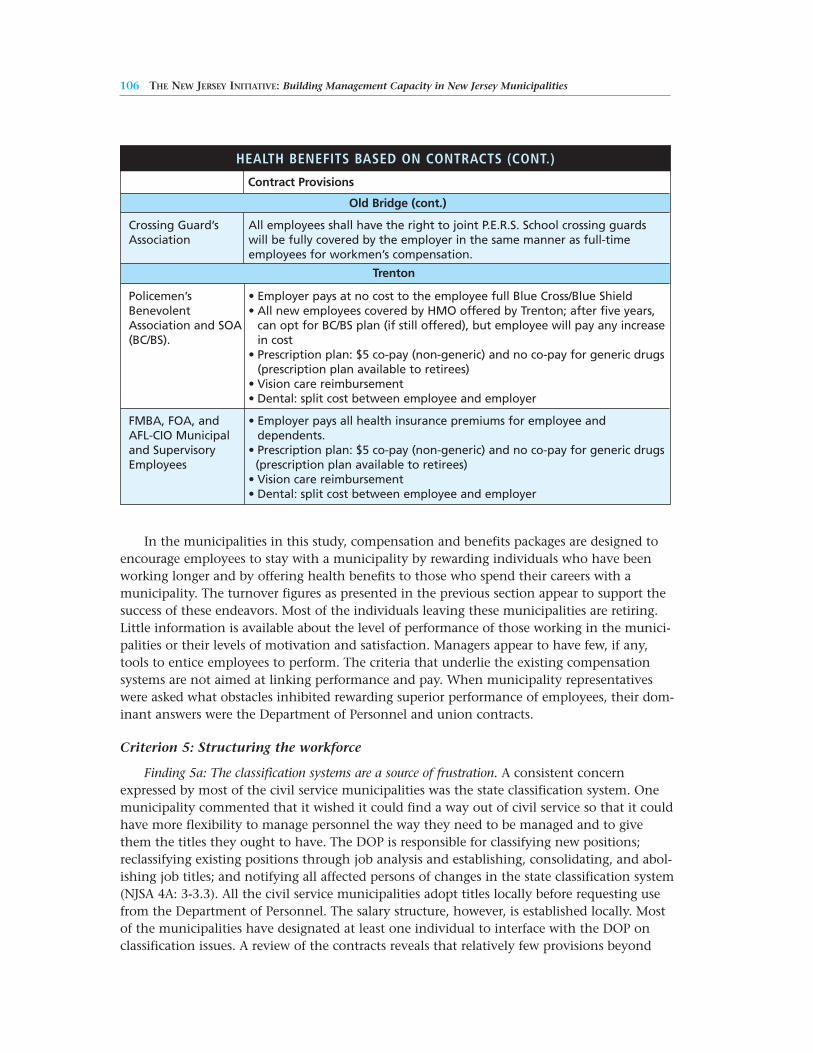

4.22 Health Benefits Based on Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

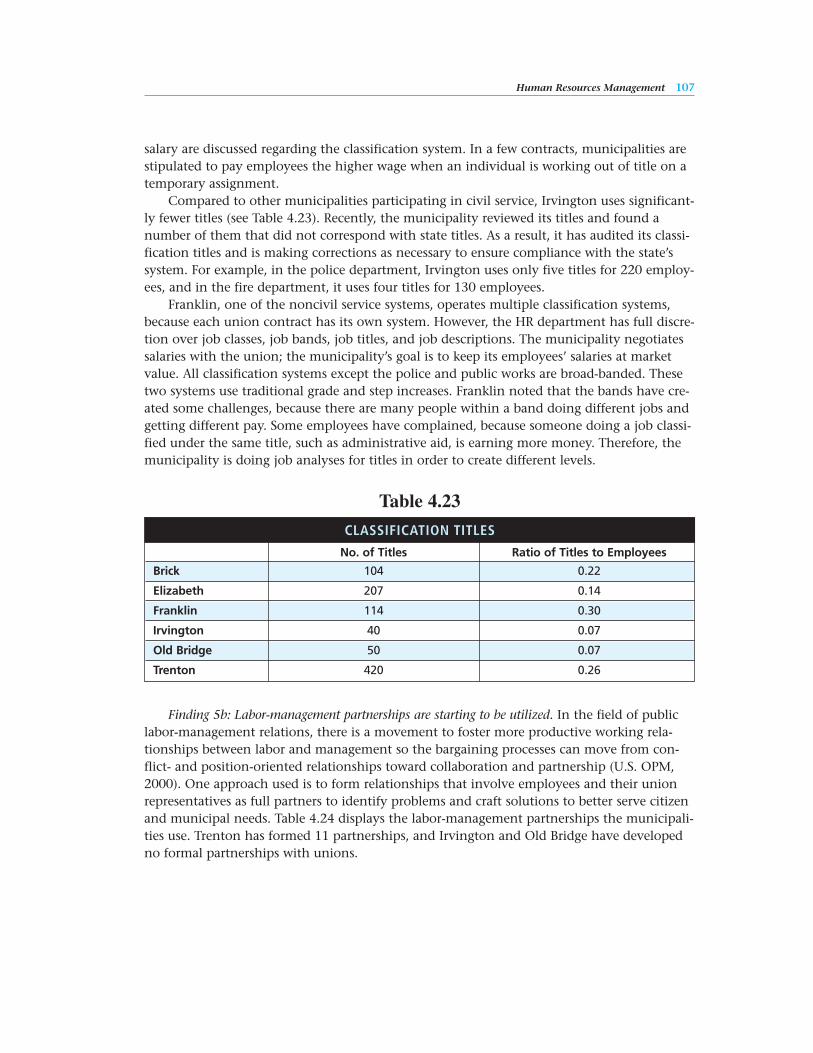

4.23 Classification Titles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

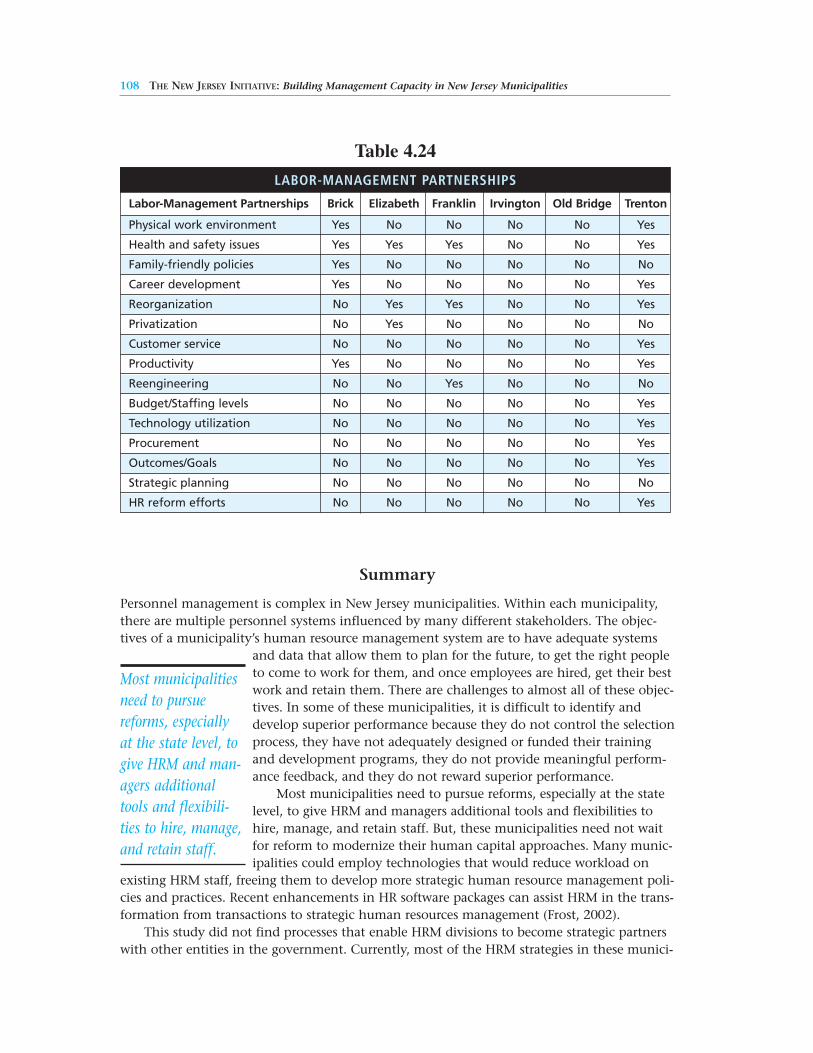

4.24 Labor-Management Partnerships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

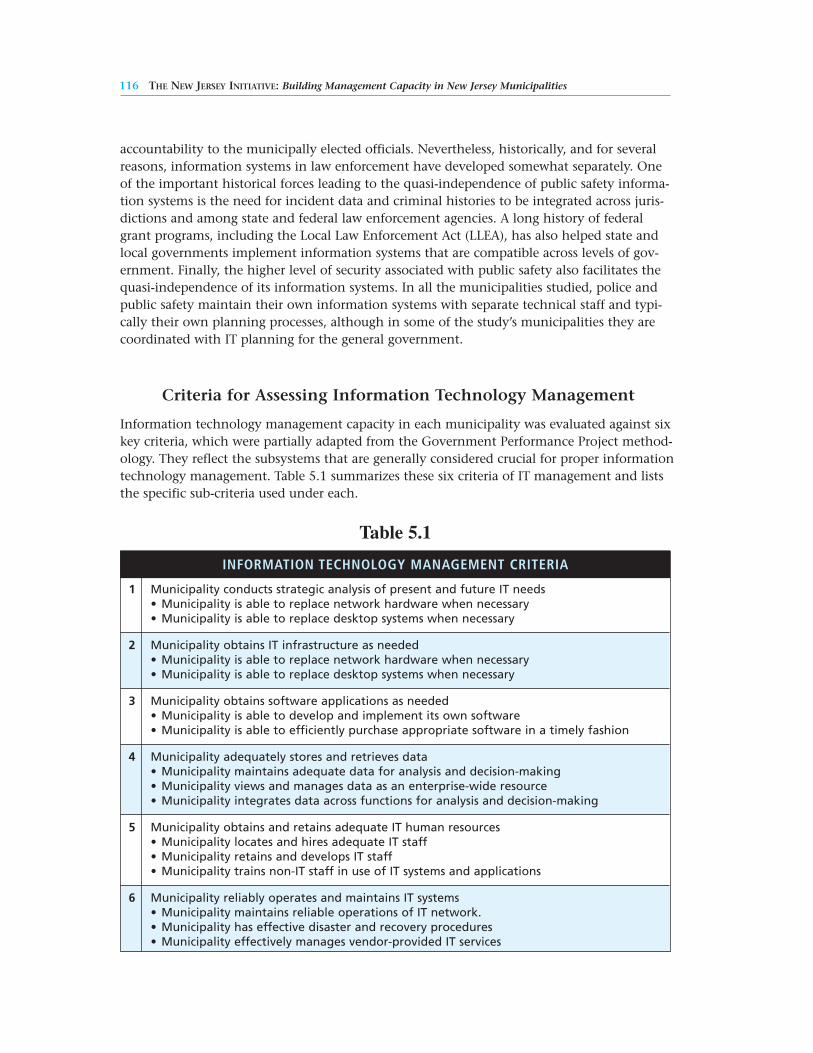

5.1 Information Technology Management Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

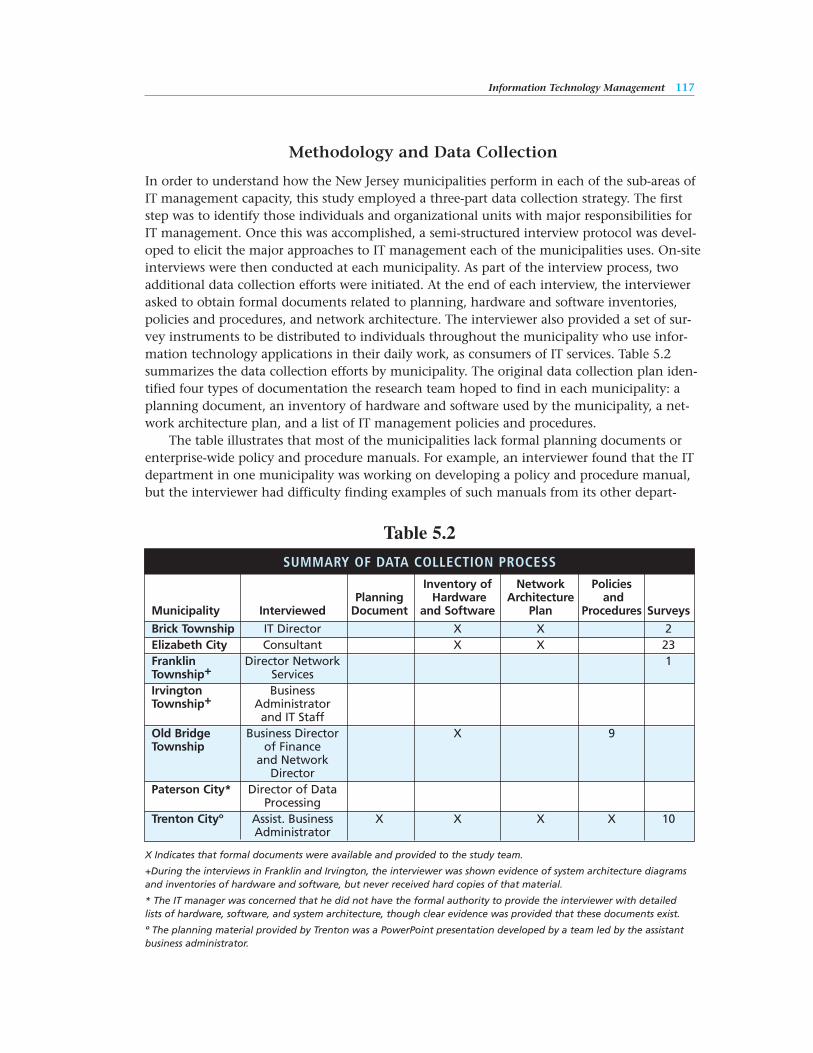

5.2 Summary of Data Collection Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

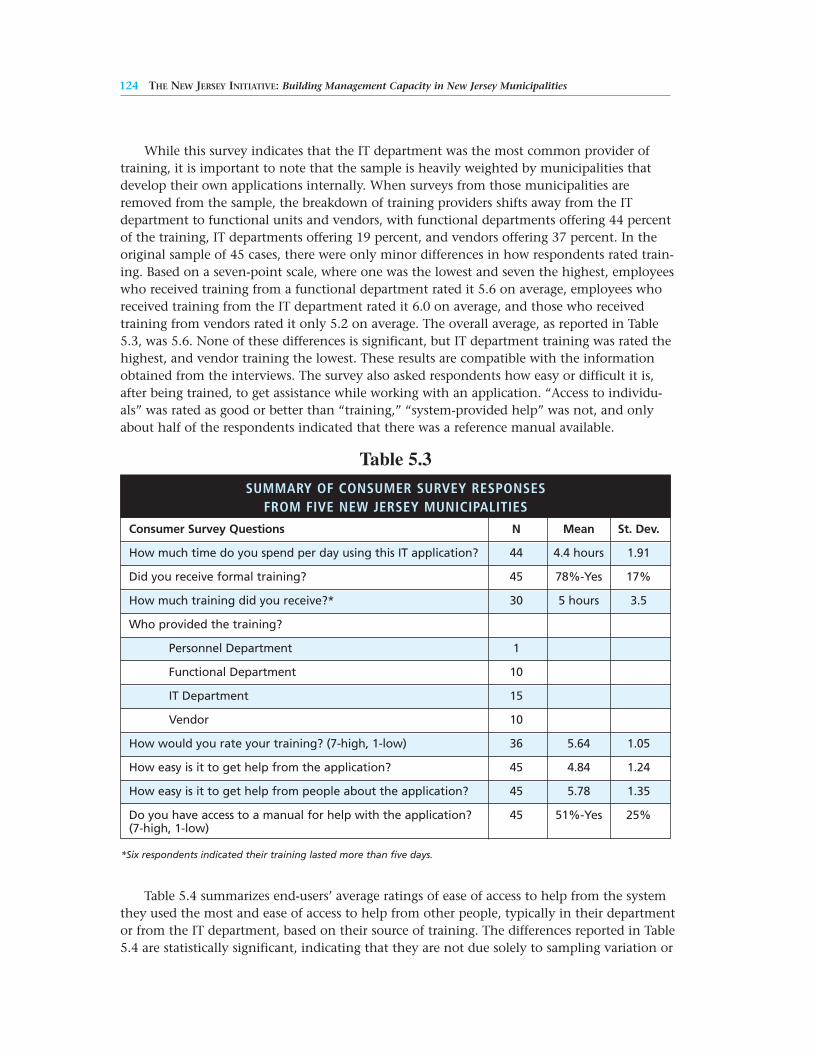

5.3 Summary of Consumer Survey Responses from Five New Jersey Municipalities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

5.4 Average Scores on Ease of Gaining Help (7-high, 1-low). . . . . . . . . . . . . . . . . . . . . . . . . . . 125

5.5 Average System Performance Scores by Source of Training . . . . . . . . . . . . . . . . . . . . . . . . . 125

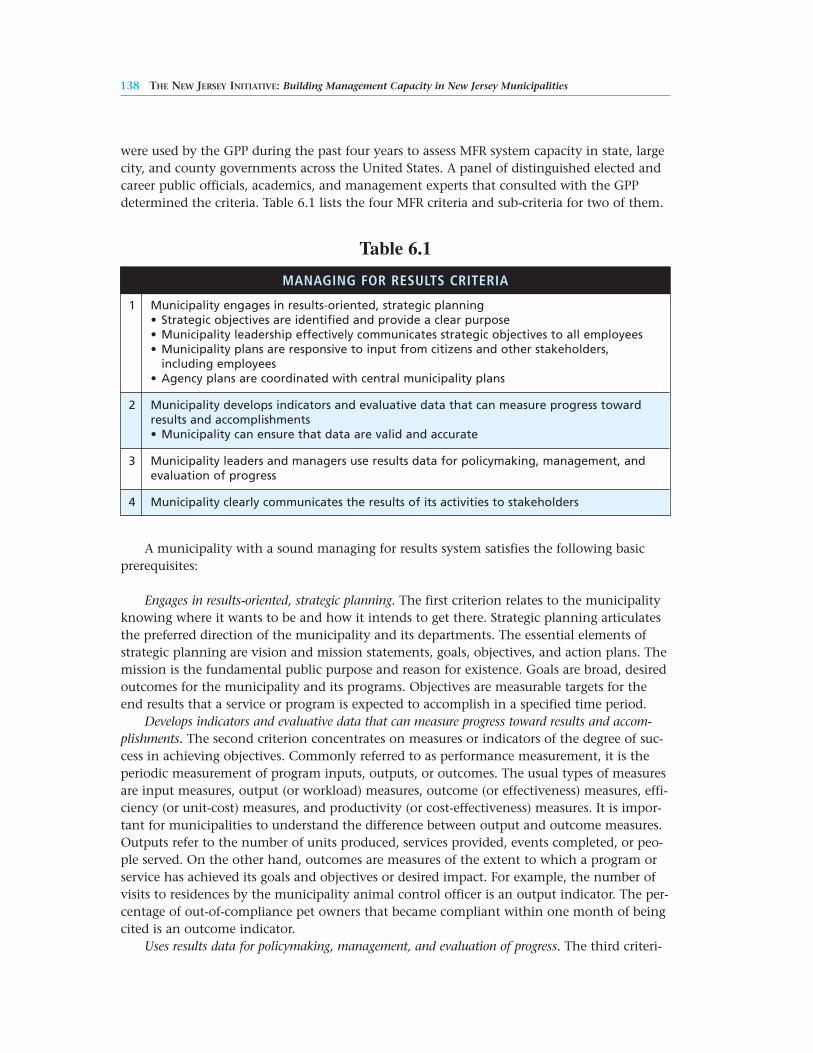

6.1 Managing for Results Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

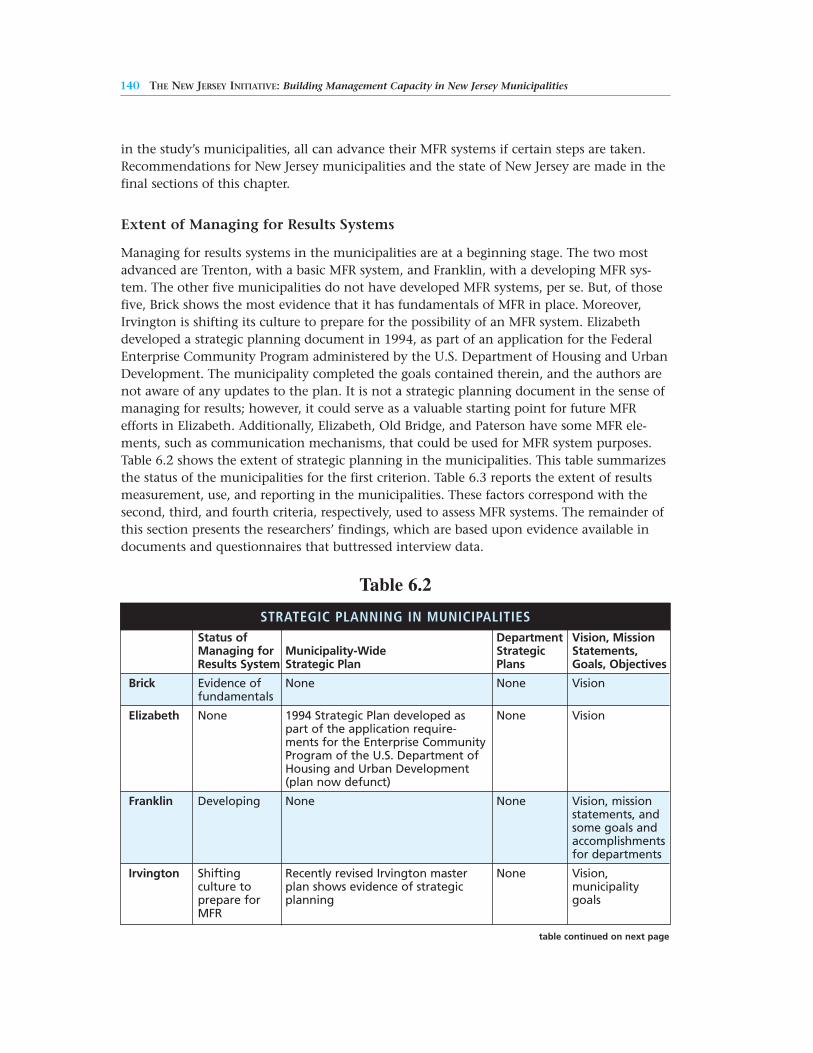

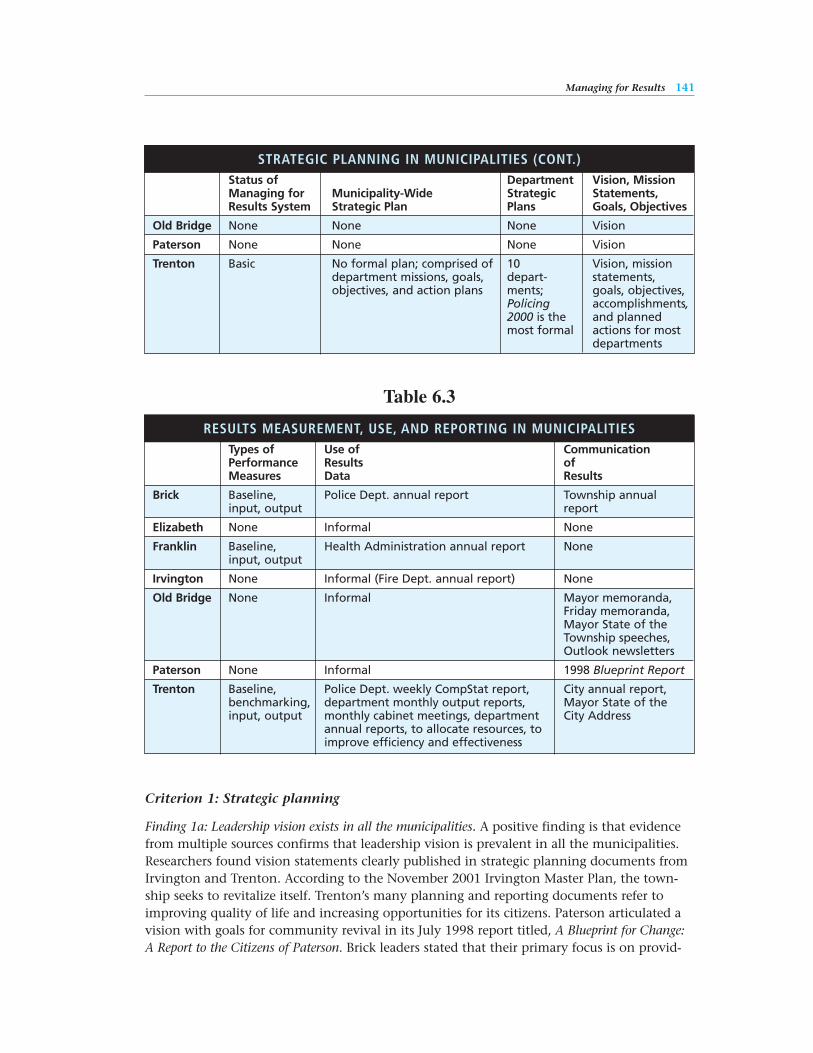

6.2 Strategic Planning in Municipalities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

6.3 Results Measurement, Use, and Reporting in Municipalities . . . . . . . . . . . . . . . . . . . . . . . 141

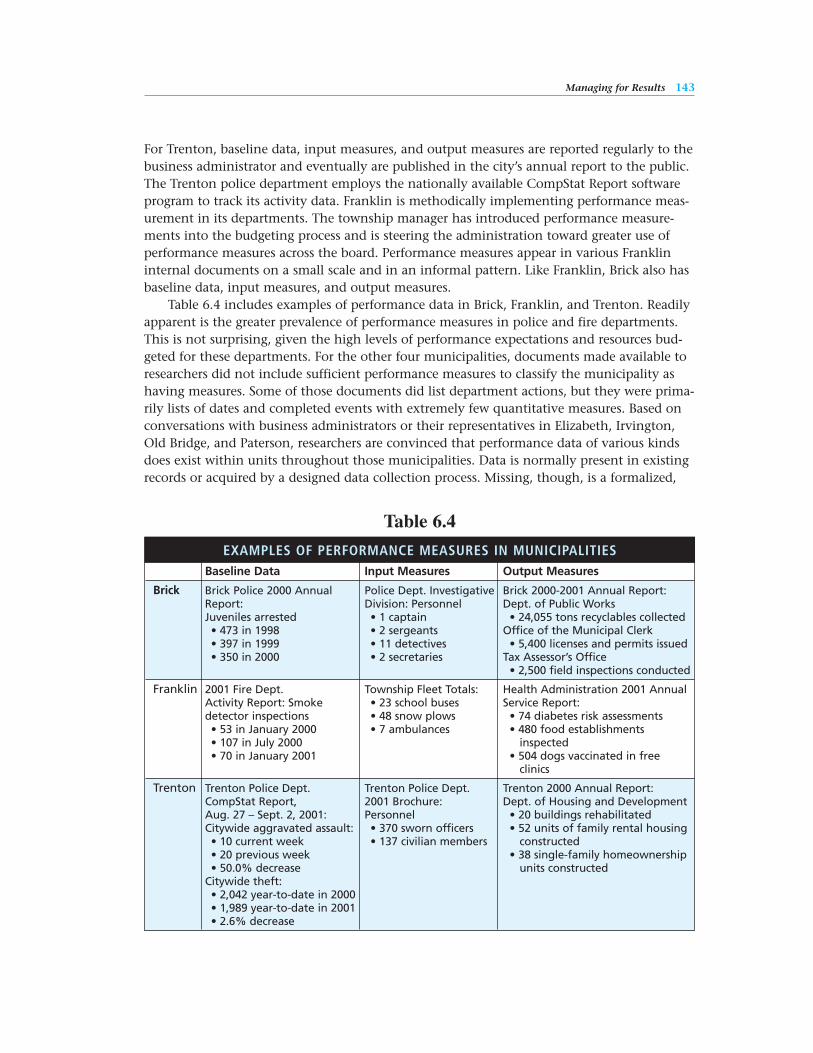

6.4 Examples of Performance Measures in Municipalities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

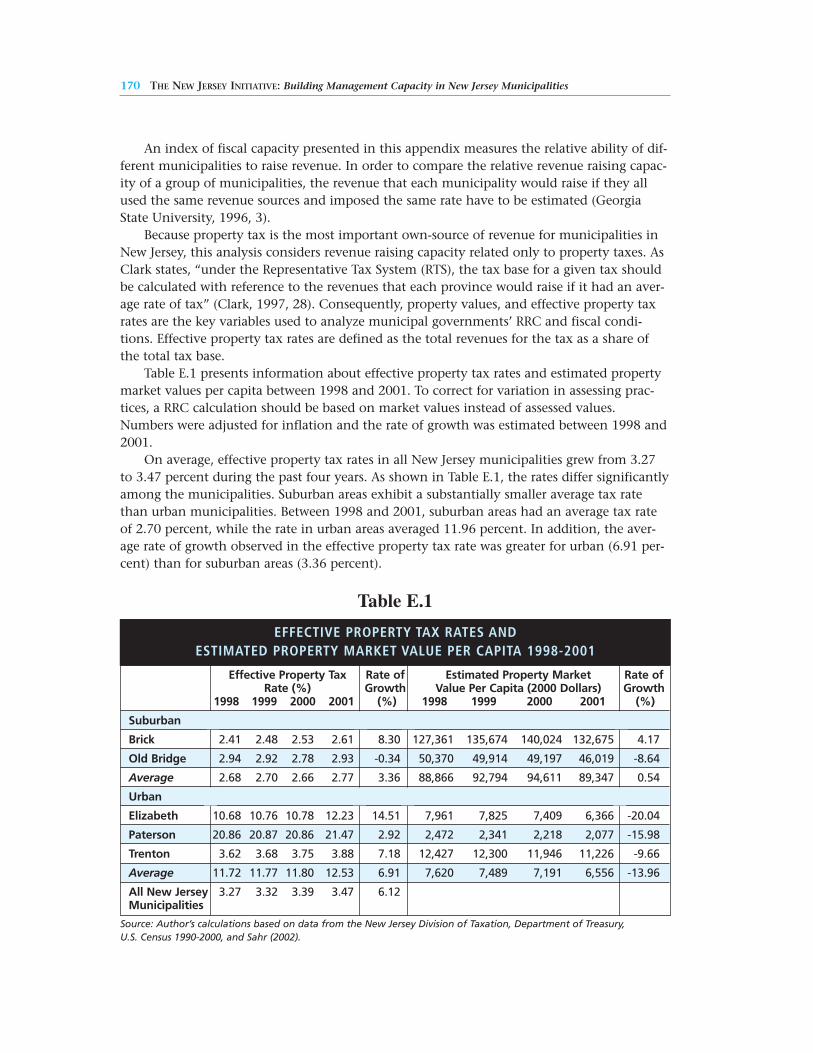

E.1 Effective Property Tax Rates and Estimated Property Market Value Per Capita 1998-2001 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

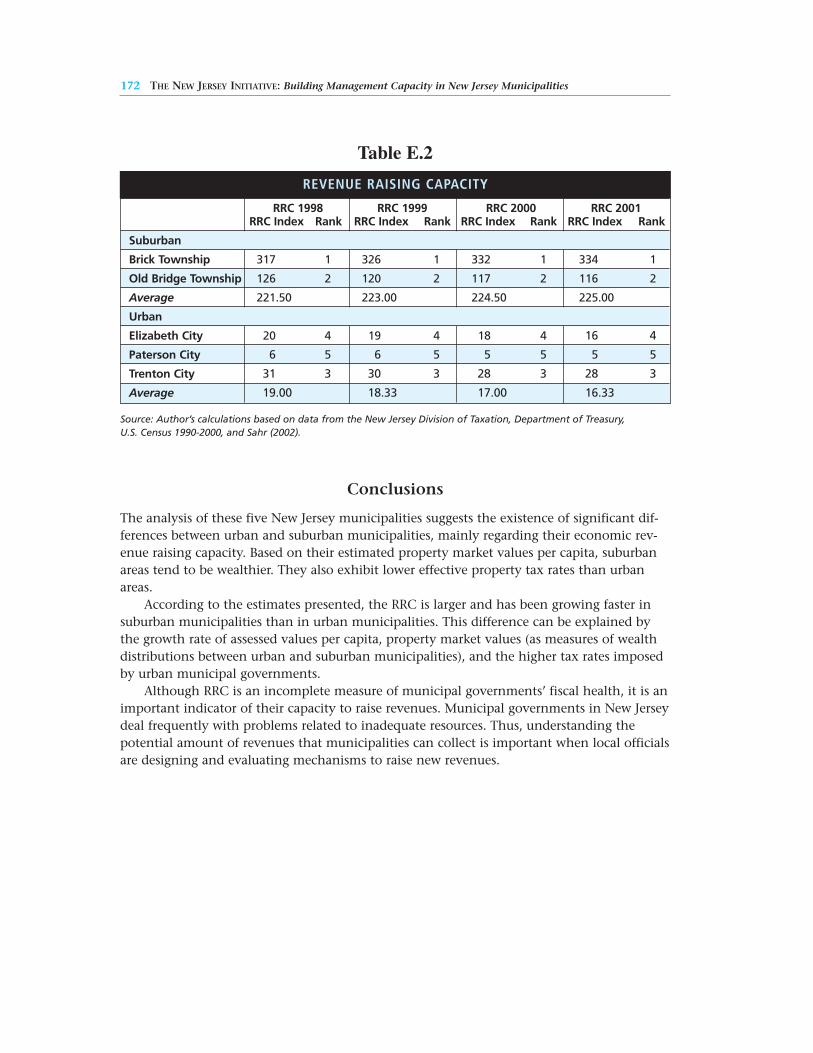

E.2 Revenue Raising Capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

Figure

1.1 A Schematic of Government Management Capacity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

List of Appendices xi

List of Appendices

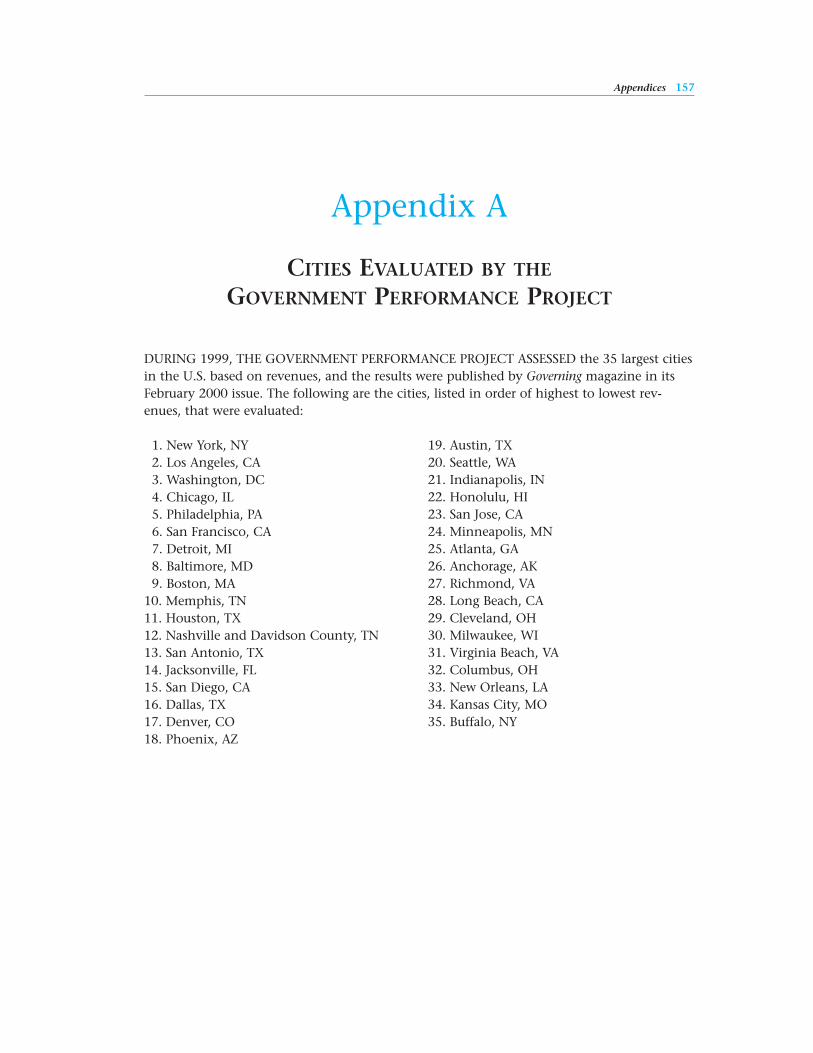

A Cities Evaluated by the Government Performance Project . . . . . . . . . . . . . . . . . . . . . . . . . 157

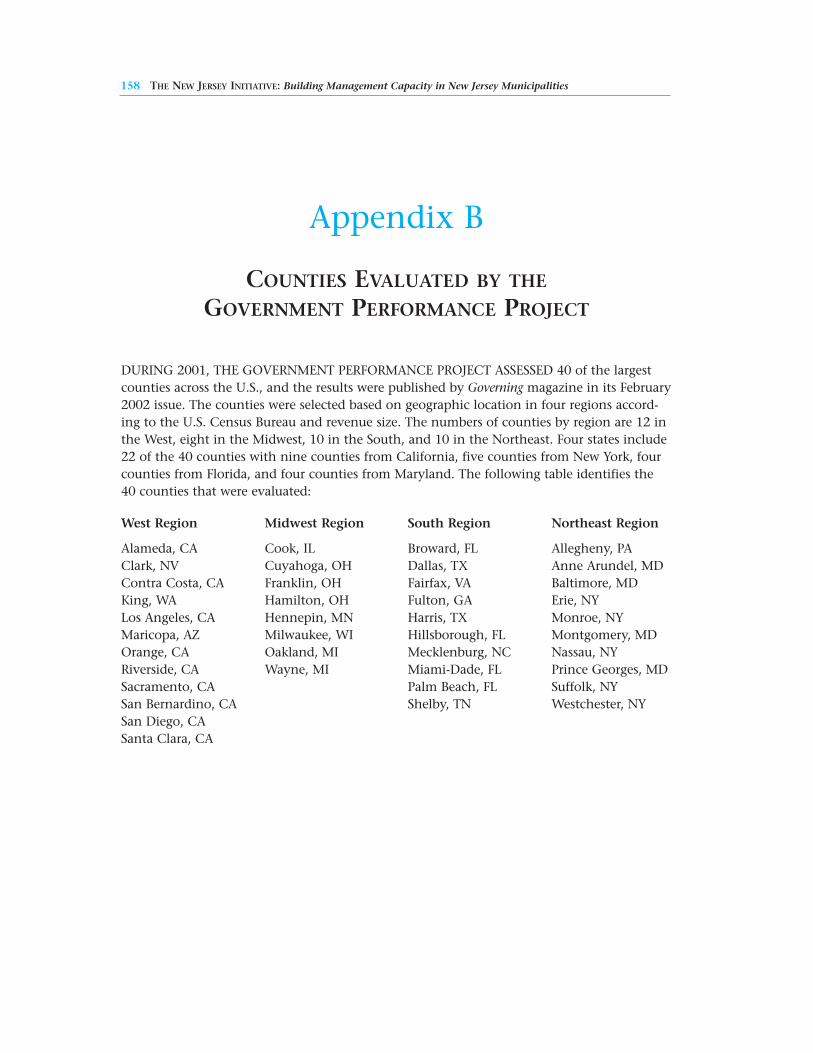

B Counties Evaluated by the Government Performance Project . . . . . . . . . . . . . . . . . . . . . . 158

C Profile of New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

D Contracting and Procurement Practices in New Jersey Municipalities . . . . . . . . . . . . . . . . 161

E Revenue Raising Capacity in New Jersey Municipalities . . . . . . . . . . . . . . . . . . . . . . . . . . 169

F New Jersey Department of Community Affairs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

G The Maxwell School of Citizenship and Public Affairs at Syracuse University. . . . . . . . . . 175

H Alan K. Campbell Public Affairs Institute at Syracuse University . . . . . . . . . . . . . . . . . . . . 177

I Eagleton Institute of Politics at Rutgers, The State University of New Jersey . . . . . . . . . . . 178

J Biographies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Foreword xiii

Foreword

The New Jersey Initiative is an unprecedented learning opportunity for all municipalitiesin New Jersey, and especially for the seven municipalities participating directly in the proj-ect. The New Jersey Initiative generates analyses of five important management systemareas: financial management, capital management, human resources management, infor-mation technology management, and managing for results. In doing so, the New JerseyInitiative creates a tremendous opportunity for municipalities to more systematicallyexamine their own management systems and how they are integrated, learn from eachother, and consider how their allocation of resources to the various systems translates intooverall effectiveness and performance potential.

The New Jersey Initiative was conducted by a strong partnership between two highlyreputable academic institutions: the Alan K. Campbell Public Affairs Institute of the MaxwellSchool of Citizenship and Public Affairs at Syracuse University and the Eagleton Institute ofPolitics at Rutgers, The State University of New Jersey. We are proud of how Maxwell andEagleton pooled their resources to unite as a team to produce high quality research that isobjective, valid, constructive, and useful for government leaders, practitioner managers, citi-zens, and scholars. The Maxwell School contributed the research expertise from its nationallyrecognized faculty and the Eagleton Institute contributed its expertise on New Jersey politicsand government. Together, Maxwell and Eagleton formed a dedicated team to help NewJersey municipalities understand and improve their management capacity in order toachieve greater government performance.

During 2001 and 2002, researchers worked closely with seven New Jersey municipalitiesthat participated in the study: Brick Township, Elizabeth City, Franklin Township, IrvingtonTownship, Old Bridge Township, Paterson City, and Trenton City. Our research teamsobtained data from the municipalities through surveys and questionnaires, public docu-ments, and interviews of professional managers. We were impressed with the genuine dedi-cation and commitment from the men and women who are in public service in the munici-palities. On a sadder note, we extend our condolences to Paterson City on the loss of itsdirector of human resources who unfortunately passed away during the project. Committedto serving the citizenry in their communities, the public managers we engaged constantlyseek ways to achieve greater efficiency and effectiveness, be more innovative, and improvemanagement as they face an environment full of challenges.

The New Jersey Initiative follows a distinguished predecessor. Our effort is a logicalextension of the path-breaking work of the Government Performance Project, which untilnow focused on large city and county governments and state governments. We are gratifiedthat we applied the Government Performance Project model to smaller municipal-level gov-ernments. The New Jersey Initiative is new territory and our knowledge about governmentmanagement capacity expanded as a result of our journey through the Garden State.

The results of the New Jersey Initiative are being made widely available in New Jersey tocitizens, elected officials, municipality managers, state government officials, academic insti-

xiv THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

tutions, and research centers. We are confident that the New Jersey Initiative can helpadvance the improvement of management systems in all 566 New Jersey municipalities, aswell as in municipalities across the nation. Ultimately, better public sector management sys-tems will lead to stronger government performance.

Dale JonesDirectorSyracuse, New York

Ingrid W. ReedAssociate DirectorNew Brunswick, New Jersey

Acknowledgments xv

Acknowledgments

The New Jersey Initiative is indebted to many people who contributed from its genesis toits completion. All deserve much credit and thanks for making the New Jersey Initiativepossible.

The idea to conduct an assessment of New Jersey municipalities originated with stategovernment leaders. Former New Jersey Governor Christine Todd Whitman and Jane Kenny,former New Jersey Commissioner of Community Affairs, requested the GovernmentPerformance Project at The Maxwell School of Syracuse University consider evaluating NewJersey municipalities. Their aim was to find ways for the state to help its municipalities. Theproject thanks The Pew Charitable Trusts and the state of New Jersey for their generousgrants that funded the project. Marc Pfeiffer, Deputy Director of the Division of LocalGovernment Services for the New Jersey Department of Community Affairs, and LorettaBuckelew, Assistant to the Deputy Director, were invaluable in helping the project get startedand providing important documents while giving researchers the freedom they needed toconduct objective evaluations.

Most importantly, our sincerest thanks go to the seven municipalities that volunteeredto participate in the New Jersey Initiative: Brick Township, Elizabeth City, FranklinTownship, Irvington Township, Old Bridge Township, Paterson City, and Trenton City. Thisresearch project could not have been completed without their cooperation. We greatlyappreciate the mayors for granting the project access to their municipalities. Additionally, wethank the dedicated staff of leaders, administrators, and employees at all levels within themunicipalities for giving their valuable time to work with us. Moreover, we thank them forbeing candid in interviews and imparting their experiences and views to researchers.

A special thank you goes to members of the New Jersey Advisory Committee. Theirextensive practical government experience, policy research experience, familiarity with NewJersey state and local governments, and knowledge of politics in New Jersey were a tremen-dous asset to the project. We extend our gratitude to them for taking time away from theirown important endeavors to provide professional guidance: Loretta Buckelew; HenryColeman, Director of the Center for Government Services, Rutgers University; Jon Erickson,Director of the Master of Public Administration Program, Kean University; Michele Tuck-Ponder, President of Ponder Solutions; Bill Watson, Executive Director of the John S. WatsonInstitute for Public Policy, Thomas Edison State College; and John Weingart, AssociateDirector of the Eagleton Institute of Politics, Rutgers University.

Next, we are extremely appreciative and thankful for assistance from the New JerseyState Library in Trenton, local libraries in the seven municipalities, and historical societiesthroughout the state. The reference staffs of each were always more than helpful and a pleas-ure to work with. Also, we acknowledge the Newark Star-Ledger for supplying the project withdetailed census data for New Jersey.

Central to the New Jersey Initiative were the project’s many scholars, consultants,research associates, and research assistants. Organized into five research teams, they were theheart of the project. Faculty experts were Stu Bretschneider, Yilin Hou, Dale Jones, and SallyColeman Selden. Project consultants were Connie Bawcum, Max Bohnstedt, SuzetteDenslow, Amy Donahue, Carol Ebdon, and Kari Parsons. Research associates were Dana Michael Harsell, Willow Jacobson, Ora-orn Poocharoen, and Yonghong Wu. Senior

xvi THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

research assistants were Jessica Crawford, Figen Gungor, and Tiffany Tanner and researchassistants were Paula Acosta, Kingsley Chukwu, Chris Folts, Melissa Mink, Sharif Nankoe,and Genikwa Williams. We extend our heartfelt thanks and appreciation to each for theirextensive contributions. Recognition goes to Figen Gungor for her assistance in the finalstage of the project.

Additionally, we thank the staffs at the Alan K. Campbell Public Affairs Institute of TheMaxwell School at Syracuse University and the Eagleton Institute of Politics at RutgersUniversity for their wonderful assistance to the project. Bethany Walawender and KelleyColeman at the Campbell Institute provided fantastic support. Likewise, Lucy Baruch andJoanne Pfeiffer at the Eagleton Institute gave terrific help. Alyssa Colonna served as the edi-tor for manuscript preparation, and we are thankful for her heroic service, which enableddeadlines to be met. Chris Bronk designed and maintained a high quality web site for theproject and Dana Cooke designed our project logo.

The Syracuse University Publications Office kept us on track to ensure the manuscriptwas properly prepared. We are especially thankful to Susan Hoxie who was a superb publica-tions coordinator and guided us through the process with her meticulous oversight. Also,our thanks go to Amy McVey and Joye Morrisseau for their skillful work as the publicationdesigners.

Finally, we express very special gratitude to our two project managers. Dana MichaelHarsell was the perfect project manager for The Maxwell School. We relied on his strongorganization and planning abilities, diplomatic skills, and good judgment to navigate usthrough the year, especially during the final stages. Jon Erickson was an excellent projectmanager for the Eagleton Institute. We depended on his extensive knowledge of New Jerseygovernment and politics and pivotal role as liaison to the municipalities. We thank them fortheir highly regarded advice and for being there every time we needed them.

Dale JonesDirector

Ingrid W. ReedAssociate Director

Executive Summary xvii

Executive Summary

Governments at all levels in the United States are engaged in long-term efforts to improveperformance and provision of services. Citizens, elected officials, the media, and govern-ment leaders and managers expect excellence from government and support reform effortsto achieve it. Indeed, government reinvention and reengineering activities were common-place in the 1990s for federal, state, and local levels of government. The overarching goalin most government reform efforts then and now is to enhance government performance.

The New Jersey Initiative is an innovative research effort in the state of New Jerseyinvolving seven municipalities invited to participate in a pilot project that examines munici-pal management. The study was conducted by Syracuse University’s Maxwell School ofCitizenship and Public Affairs and Rutgers University’s Eagleton Institute of Politics during2001 and 2002 with funding from The Pew Charitable Trusts and the state of New JerseyDepartment of Community Affairs. The municipalities that participated in the project areBrick Township, Elizabeth City, Franklin Township, Irvington Township, Old BridgeTownship, Paterson City, and Trenton City.

The purpose of the New Jersey Initiative is to increase understanding of the capacity ofmanagement systems that best enable municipal governments to perform well and meet theneeds of citizens. Based on the premise that more extensive management capacity precedesbetter management performance, the New Jersey Initiative assessed management capacity inthe following five areas that are critical to delivering improved services at lower costs andachieving high performance in government:

• Financial management

• Capital management

• Human resources management

• Information technology management

• Managing for results

The 1993 National Commission on the State and Local Public Service stated, “Yet a grow-ing consensus has emerged among both citizens and public officials that state and local gov-ernments need to improve their capacity and performance if we are to meet the challenges ofour rapidly changing economic and social systems.” Thus, the New Jersey Initiative is animportant effort to identify how New Jersey municipalities can improve their managementcapacity to result in better performing government and delivery of services to their citizens.

The five management areas represent elaborate systems for each municipality.Furthermore, the complex environment in which they operate creates management chal-lenges. Today, municipal managers in New Jersey contend with pressures associated withkeeping taxes under control; managing fiscal affairs tightly; maintaining physical infrastruc-tures; hiring, training, and retaining personnel; investing in information technology; andplanning for the future. At the same time, they are complying with rules and regulations;responding to security and safety issues related to the aftermath of 9-11 terrorist attacks; deal-ing with citizen inputs and complaints; working in a political environment; and responding

xviii THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

to state policies and requirements. This report shines a light on those complexities. Giventhe nature of the challenges and constraints these municipalities face, researchers notedimpressive strengths in their governance activities.

It is important to clarify that this study is about municipal management, not municipalpolitics. We acknowledge the significance of political factors and recognize they must be con-sidered, but they were not the focus of this study. It is true that municipal management inNew Jersey is often affected by politics, as is the case for all government entities.Nevertheless, the New Jersey Initiative was chartered specifically to evaluate the managementcapacity of municipalities.

Researchers found both strengths and weaknesses in each of the management areas.Comprehensive criteria-based analyses of financial management, capital management,human resources management, information technology management, and managing forresults are contained in separate chapters of the report. Throughout the process of conduct-ing the study, researchers all too often witnessed an on-going tension driven by state finan-cial management and civil service legal requirements. To some extent, an “us versus them”condition exists which does not always give rise to good governance. This may be partly areflection of the state’s higher level of oversight of those municipalities in the DistressedCities Program. Another contributing factor may be that the higher performing municipali-ties feel frustrated by the “one size fits all” oversight approach. Therefore, the report’s chap-ters include recommendations for each of the management areas, for the state as well as themunicipalities, aimed at improving management capacity in municipalities.

Overall, improving management capacity in the seven municipalities in the study, alongwith other New Jersey municipalities with similar characteristics and conditions, requires astronger collaborative approach from municipalities and the state, recognition of vitalreforms, and bold actions. A major conclusion of the study is that success in improving man-agement capacity will depend on mutually reinforcing actions and greater cooperation byboth municipalities and the state.

The New Jersey Initiative concludes that municipalities can increase management capaci-ty in two important ways. First, they can take advantage of any existing leeway, such as thatmade possible by the New Jersey Optional Municipal Charter Law, known as the FaulknerAct, to grant business administrators broad powers and authority to operate and managemunicipal affairs. Second, municipal leaders can create an environment that recognizes thevalue of and rewards management initiative, innovative actions, implementation of bestpractices from other locales, and prudent risk-taking.

For the state level, the project also recommends new approaches to bring improvementto municipal management capacity. First, if the state modifies its oversight relationship withmunicipalities, it may experience positive results. The current approach emphasizes imposingthe state’s view of appropriate performance and regulating to prevent wrongful behavior bymunicipal officials. Although firm state oversight is well intended and does prevent unwant-ed behavior, it comes with the price of frustrating local government managers. For thosemunicipalities where good performance warrants it, shifting to an approach that gives greaterprominence to independent capacity building and trust might lead to higher performinggovernment. Second, the state should work closely with municipalities to find ways to pro-vide regulatory relief where appropriate, generate flexibility for management decision-mak-ing, and furnish management tools to local governments.

Executive Summary ixx

The New Jersey Initiative concludes that vital reforms are necessary in the following four areas:

Vital Reform Area #1: State regulatory and procedural restraints impede local governmentmanagement innovation.

Vital Reform Area #2: In its regulatory management oversight role, the state does not sufficiently differentiate among municipalities in terms of their characteristics and performance.

Vital Reform Area #3: Municipalities lack formalized, centralized, and long-term management planning activities.

Vital Reform Area #4: Municipalities do not sufficiently exercise the management prerogatives that are available to them.

In order to build management capacity in New Jersey municipalities, the following boldactions correspond with and are recommended to address the vital reform areas:

Bold Action #1: The state should reduce burdensome and costly restrictions on municipalmanagement activities where appropriate; allow more flexibility and discretion formunicipal managers; enhance state mechanisms for providing technical, financial, andother kinds of assistance to municipalities; and create incentives for entrepreneurial man-agement behavior by municipal managers.

Bold Action #2: The state should further its efforts to classify municipalities in multiplecategories, apply different strategies to assist the various categories, and customize regula-tory treatment to fit the specific needs and circumstances of different municipalities.

Bold Action #3: Municipal councils and mayors should delegate greater authority to busi-ness administrators so they can bolster strategic planning; strengthen their managementsystems; formalize and centralize management oversight activities; and where it is best todo so, integrate management systems across departments.

Bold Action #4: Municipalities should be more innovative in applying management prac-tices, take reasonable risks when implementing new management practices, and ask forguidance and assistance when needed from the state.

Professional managers for the state of New Jersey and its 566 municipalities are consid-ered to be highly qualified. They have a reputation for managing programs well and success-fully serving the citizenry despite many challenges. The New Jersey Initiative focuses on howmunicipalities and the state can reach a higher level of performance by improving manage-ment capacity in municipalities. The report presents its findings in a constructive manner.The New Jersey Initiative observes that if the state and its municipalities work together andmake the recommended changes, they will build municipal management capacity andstrengthen excellence in governance for New Jersey.

1

ASSESSING MANAGEMENT CAPACITY

IN NEW JERSEY MUNICIPALITIES

The Government Performance Project: Foundation for the New Jersey Initiative

THE NEW JERSEY INITIATIVE PROJECT WAS INSPIRED BY the Government PerformanceProject (GPP). The purpose of the New Jersey Initiative is to provide an in-depth analysis oflocal government management capacity. The project results provide valuable feedback andrecommendations to municipalities in New Jersey as well as the state government. In orderto understand the New Jersey Initiative, one must first understand the GPP.

The Government Performance Project is believed to be the most comprehensive exami-nation of the effectiveness of core government management activities ever conducted. Thecentral purpose of the GPP is to improve understanding of public sector management and,thereby, assist in strengthening government performance. Since 1996, with grants from ThePew Charitable Trusts, the Maxwell School of Citizenship and Public Affairs at SyracuseUniversity, in partnership with Governing magazine, has analyzed the management capacityof state, city, and county governments across the United States. The national level, multiyearproject is administered by the Alan K. Campbell Public Affairs Institute at The MaxwellSchool. Governing is a nationwide publication that concentrates on state and local govern-ments and annually publishes the results of the GPP in a special February issue. The projectassesses the effectiveness of management systems in five key areas. Additionally, the projectexamines how well those management systems are integrated. The GPP does not focus pri-marily on performance; it analyzes management capacity, which is the foundation for highperformance. Management capacity is further discussed later in this chapter in a sectiontitled “Management Capacity.” An important objective of the project is to communicate itsfindings to governments at all levels as well as to the public. Additional details about theGPP are available on the project’s web site at www.maxwell.syr.edu/gpp.

Government Performance Project Goals

The overarching purpose of the Government Performance Project is to improve the under-standing of government management on the state, city, and county levels, first by facilitatinga better intellectual understanding of the dimensions of management in government, andsecond, by holding government entities publicly accountable for the quality of managementin their jurisdictions. The five specific goals of the GPP are as follows:

• To recognize innovations and improvements in government management practices

• To generate a dialogue and facilitate a learning process among governments

2 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

• To create a clearinghouse of information related to government management

• To inform the public about factors which contribute to effective management in thepublic sector

• To enhance citizen understanding of government management issues and practices

Government Performance Project Management Areas and Criteria

The Government Performance Project conducts criteria-based assessments in five centralareas of government management: financial management, capital management, humanresources management, information technology management, and managing for results. Inthe first two years of the project, senior advisory panels consisting of respected public admin-istration scholars and practitioners agreed upon the management areas and developed theircriteria. Each of the five management system areas has a set of criteria on which their assess-ments are based. After the pilot year, the criteria were refined based on direct feedback fromgovernments that were evaluated. Other than fine-tuning some of the wording for the crite-ria, the criteria have remained the same during the four years of evaluations conducted since1998. The criteria are listed and discussed in Chapters 2 through 6, which address the find-ings for each of the management areas, respectively.

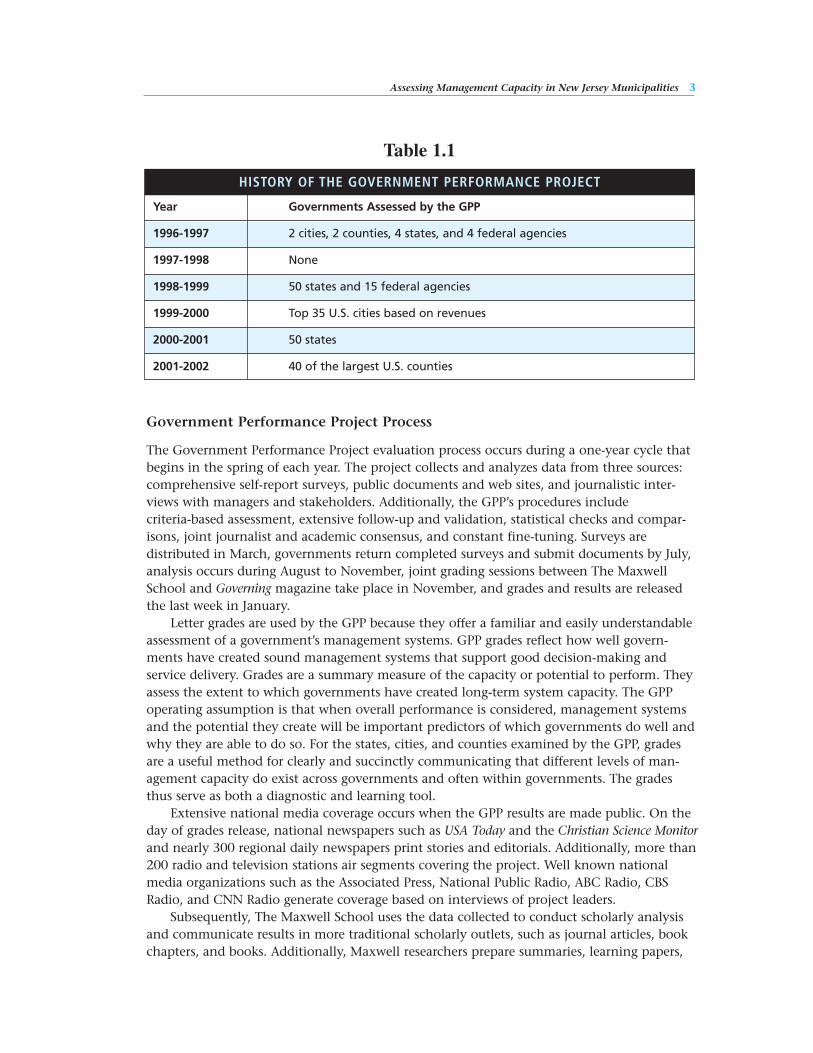

Government Performance Project History

Table 1.1 summarizes the history of the Government Performance Project. During the 1996to 1997 pilot year, the GPP conducted studies in two cities, two counties, four states, andfour federal agencies. Pilots were chosen through a process that emphasized diversity in func-tion, size, and location among the federal agencies. During this phase, The Maxwell Schooldeveloped a methodology that was used and improved upon throughout the duration of theproject. The pilot year ended in the fall of 1997. During the late 1997 to early 1998 period,researchers refined their procedures and prepared for subsequent years. In 1998, the projectstudied and graded government management systems in all 50 states and 15 federal agencies.The state results were published in the February 1999 issue of Governing and the federalresults were published in the February 1999 issue of Government Executive magazine, whichtargets the federal government. In 1999, the GPP assessed the management capacity of thetop 35 U.S. cities based on revenues and five federal agencies. Appendix A contains a list ofthe cities. The city findings were published in the February 2000 issue of Governing and thefederal results were published in the March 2000 issue of Government Executive. As of January2000, federal agency evaluations are being conducted by George Washington University. In2000, the GPP reevaluated the 50 states and the results were published in the February 2001issue of Governing. During 2001, the GPP assessed 40 of the largest counties in the U.S. andthe findings appeared in the February 2002 issue of Governing. Appendix B identifies thecounties by regions.

Assessing Management Capacity in New Jersey Municipalities 3

Government Performance Project Process

The Government Performance Project evaluation process occurs during a one-year cycle thatbegins in the spring of each year. The project collects and analyzes data from three sources:comprehensive self-report surveys, public documents and web sites, and journalistic inter-views with managers and stakeholders. Additionally, the GPP’s procedures includecriteria-based assessment, extensive follow-up and validation, statistical checks and compar-isons, joint journalist and academic consensus, and constant fine-tuning. Surveys aredistributed in March, governments return completed surveys and submit documents by July,analysis occurs during August to November, joint grading sessions between The MaxwellSchool and Governing magazine take place in November, and grades and results are releasedthe last week in January.

Letter grades are used by the GPP because they offer a familiar and easily understandableassessment of a government’s management systems. GPP grades reflect how well govern-ments have created sound management systems that support good decision-making andservice delivery. Grades are a summary measure of the capacity or potential to perform. Theyassess the extent to which governments have created long-term system capacity. The GPPoperating assumption is that when overall performance is considered, management systemsand the potential they create will be important predictors of which governments do well andwhy they are able to do so. For the states, cities, and counties examined by the GPP, gradesare a useful method for clearly and succinctly communicating that different levels of man-agement capacity do exist across governments and often within governments. The gradesthus serve as both a diagnostic and learning tool.

Extensive national media coverage occurs when the GPP results are made public. On theday of grades release, national newspapers such as USA Today and the Christian Science Monitorand nearly 300 regional daily newspapers print stories and editorials. Additionally, more than200 radio and television stations air segments covering the project. Well known nationalmedia organizations such as the Associated Press, National Public Radio, ABC Radio, CBSRadio, and CNN Radio generate coverage based on interviews of project leaders.

Subsequently, The Maxwell School uses the data collected to conduct scholarly analysisand communicate results in more traditional scholarly outlets, such as journal articles, bookchapters, and books. Additionally, Maxwell researchers prepare summaries, learning papers,

Table 1.1

HISTORY OF THE GOVERNMENT PERFORMANCE PROJECT

Year Governments Assessed by the GPP

1996-1997 2 cities, 2 counties, 4 states, and 4 federal agencies

1997-1998 None

1998-1999 50 states and 15 federal agencies

1999-2000 Top 35 U.S. cities based on revenues

2000-2001 50 states

2001-2002 40 of the largest U.S. counties

4 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

and innovation papers to report various aspects of GPP findings. Furthermore, the CampbellPublic Affairs Institute at The Maxwell School continues to build an information and docu-ment library.

The New Jersey Initiative

The New Jersey Initiative (NJI) is a pilot project designed to work closely with a select groupof New Jersey municipalities to analyze their management capacities. The purpose of the proj-ect is to increase understanding of the capacity of management systems that best enablemunicipal governments to perform well and meet the needs of citizens. In March 2001, theNJI was established through a new grant from The Pew Charitable Trusts with additional

financial support from the New Jersey Department of CommunityAffairs. The NJI is conducted jointly by The Maxwell School’s(Appendix G) Alan K. Campbell Public Affairs Institute (Appendix H)and the Eagleton Institute of Politics at Rutgers, The State Universityof New Jersey (Appendix I). The goal of the NJI is to apply theGovernment Performance Project model and its methodologies toseven urban and suburban municipalities. The NJI analyzes the man-agement capacity of the same five management system areas as theGPP – financial management, capital management, human resourcesmanagement, information technology management, and managingfor results.

The 1993 National Commission on the State and Local PublicService stated, “Yet a growing consensus has emerged among both citizens and public officialsthat state and local governments need to improve their capacity and performance if we are tomeet the challenges of our rapidly changing economic and social systems.” Thus, the NewJersey Initiative is an important effort to identify how New Jersey municipalities can improvetheir management capacity to result in better performing government and delivery of servicesto their citizens.

Researchers interacted much more closely with the New Jersey municipalities than theydid with governments across the nation in the GPP. In the summer and fall of 2001, researchteams obtained data from municipalities through surveys and questionnaires, public docu-ments, and interviews of professional managers. The original surveys were developed for theGPP and improved upon to make them appropriate for New Jersey municipalities. During thewinter months, the researchers analyzed the data and diagnosed the municipalities. Finally, inthe spring of 2002, they authored the final report. In order to keep the municipalitiesinformed and to respond to their concerns, the project conducted three seminars during theyear. Attendees were usually business administrators, assistant business administrators, orchief financial officers. The first event was an introductory seminar to learn about the project,the second was an interim seminar to engage in discussions about the research process, andthe third was a learning seminar to receive the final report and review its findings and recom-mendations. For the NJI, rather than using grades as for the GPP, the final report identifiesareas demonstrating strengths, as well as those in need of improvements, in order to providea foundation for enhancing the performance of government in the seven municipalities andothers with similar characteristics and conditions.

The comprehensive approach of the NJI reflects the complexity of government and the

The purpose of theproject is to increaseunderstanding of thecapacity of manage-ment systems thatbest enable municipalgovernments to per-form well and meetthe needs of citizens.

Assessing Management Capacity in New Jersey Municipalities 5

political environment in which public management occurs. The NJI collaborative researcheffort is designed to assist both elected and appointed government officials in improving thecapacity of municipalities to serve their communities. More broadly, the NJI provides anopportunity for other municipalities, other levels of government, educational institutions,and non-profit organizations to learn about management systems, how they might beimproved, and how they can better meet the needs of those in leadership positions.

At the start of the project, a strong consensus was established between The MaxwellSchool and the Eagleton Institute that letter grades not be used for the New Jersey Initiative.In doing so, Maxwell School researchers were able to provide a more in-depth diagnosis ofmanagement capacity in the seven NJI municipalities since fewer governments are evaluatedthan in the national-level Government Performance Project. The final report provides con-structive feedback to the municipalities through a deeper explanation of managementcapacity in the management system areas than is possible with the use of grades. Morespecifically, Chapters 2 through 6 contain rich descriptions of the strengths and weaknessesof management systems in the municipalities and recommendations for improving thesemanagement systems.

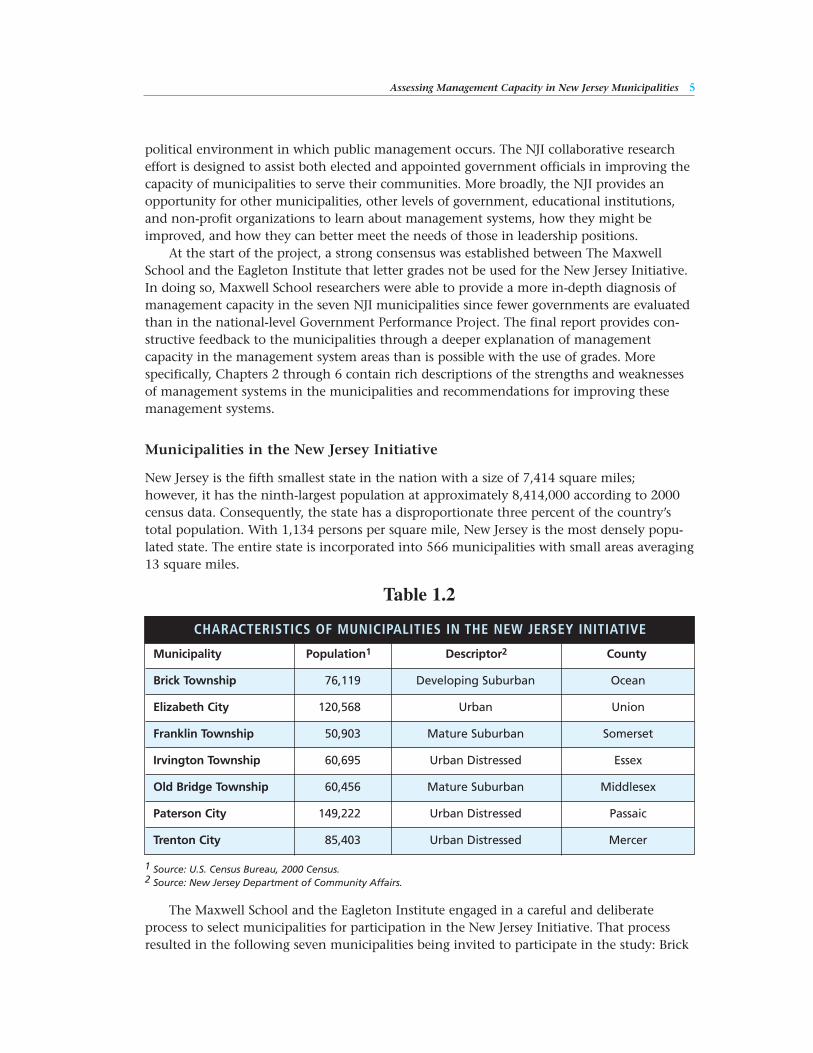

Municipalities in the New Jersey Initiative

New Jersey is the fifth smallest state in the nation with a size of 7,414 square miles; however, it has the ninth-largest population at approximately 8,414,000 according to 2000census data. Consequently, the state has a disproportionate three percent of the country’stotal population. With 1,134 persons per square mile, New Jersey is the most densely popu-lated state. The entire state is incorporated into 566 municipalities with small areas averaging13 square miles.

The Maxwell School and the Eagleton Institute engaged in a careful and deliberateprocess to select municipalities for participation in the New Jersey Initiative. That processresulted in the following seven municipalities being invited to participate in the study: Brick

1 Source: U.S. Census Bureau, 2000 Census. 2 Source: New Jersey Department of Community Affairs.

Table 1.2

CHARACTERISTICS OF MUNICIPALITIES IN THE NEW JERSEY INITIATIVE

Municipality Population1 Descriptor2 County

Brick Township 76,119 Developing Suburban Ocean

Elizabeth City 120,568 Urban Union

Franklin Township 50,903 Mature Suburban Somerset

Irvington Township 60,695 Urban Distressed Essex

Old Bridge Township 60,456 Mature Suburban Middlesex

Paterson City 149,222 Urban Distressed Passaic

Trenton City 85,403 Urban Distressed Mercer

6 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

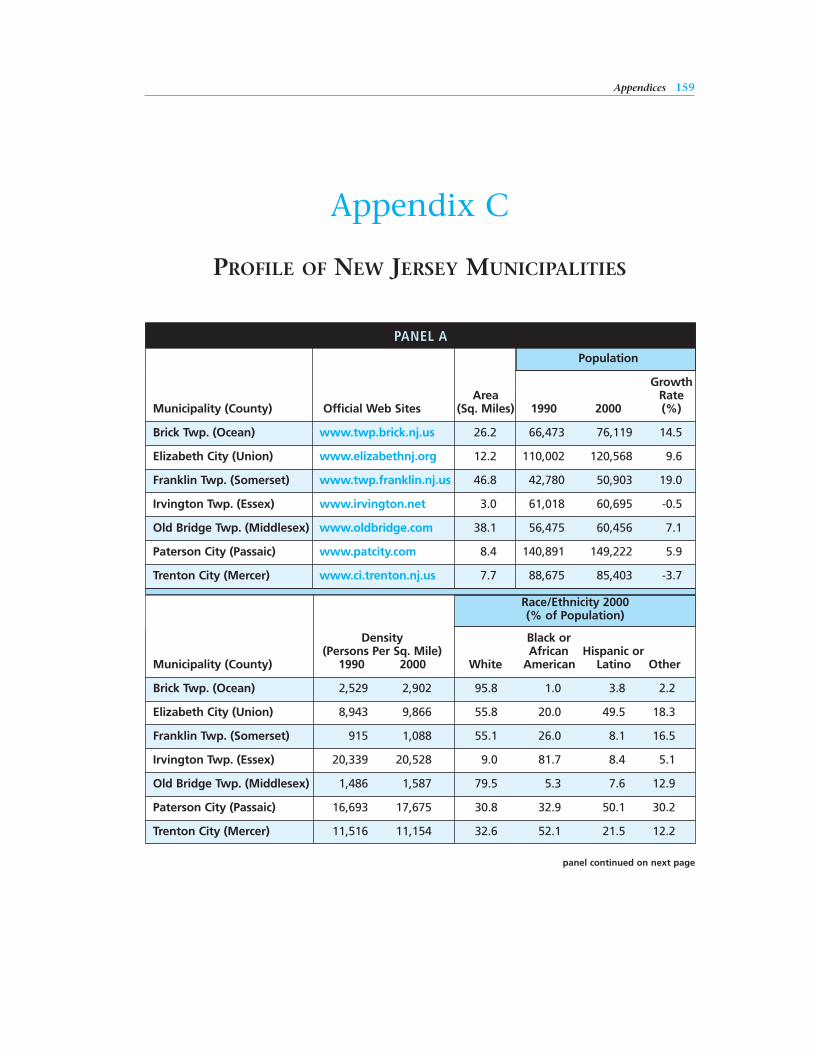

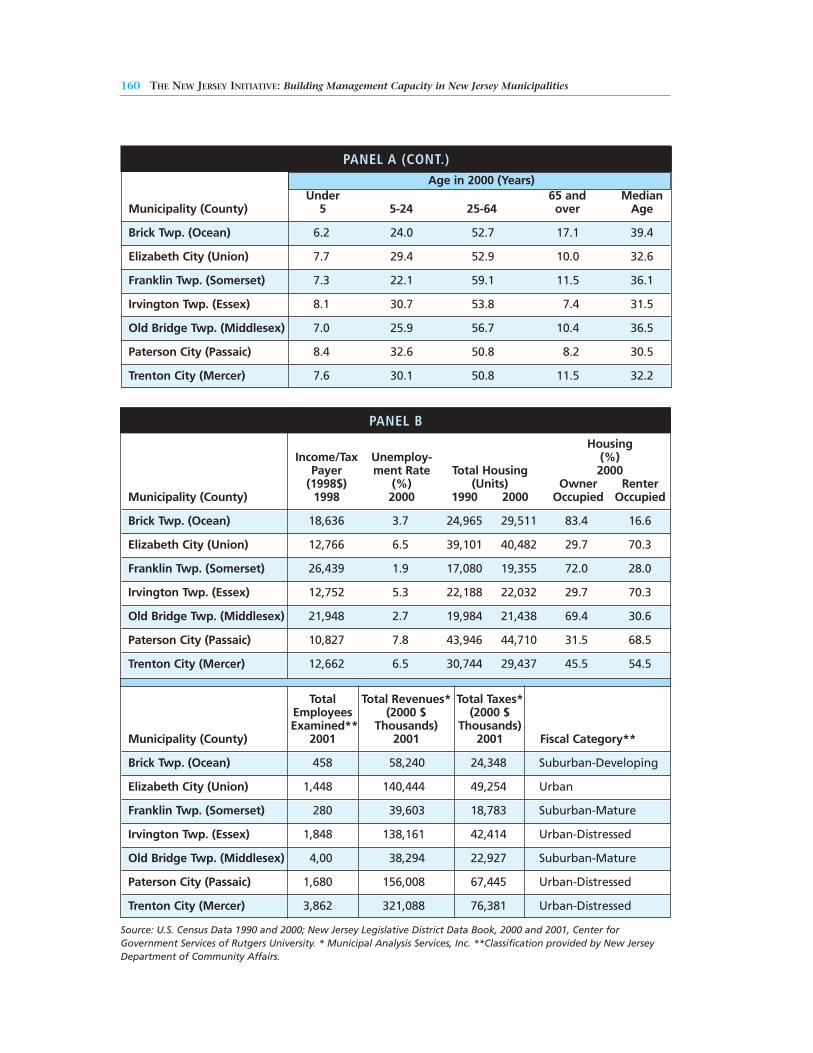

Township, Elizabeth City, Franklin Township, Irvington Township, Old Bridge Township,Paterson City, and Trenton City. Each of the municipalities voluntarily accepted the invita-tion and cooperated with the project during the evaluation process. Table 1.2 containsgeneral characteristics of the municipalities. The municipalities are among the 25 largest inpopulation relative to all municipalities in New Jersey. Their populations range from approxi-mately 50,000 in Franklin Township to 150,000 in Paterson City, according to 2000 censusdata. Moreover, three of the municipalities are suburban and four are urban. Furthermore,three of the four urban municipalities are categorized as fiscally distressed according to theNew Jersey Department of Community Affairs. Thus, the project included a variety of citiesand townships in the study. More details about the municipalities appear in Appendix C.

Criteria for Invitation to Participate

As a starting point, the New Jersey Department of Community Affairs recommended that theNJI focus primarily on urban cities and include several fiscally distressed cities. The MaxwellSchool, the Eagleton Institute, and the New Jersey Initiative Advisory Committee agreed thata broad set of factors should be considered to ensure some variation among the final set ofmunicipalities. Characteristics identified as important variables included urban or suburbanlocation, county, population, racial demographics, and degree of fiscal stress. Approximately25 municipalities were considered in the final pool of possible municipalities. The final sevenmunicipalities were recommended to receive an invitation to participate based on a balanceof factors to ensure some commonalities and variation among them.

Benefits to New Jersey Municipalities

The municipalities that participated in the New Jersey Initiative gained the opportunity tolearn about and improve their own management systems. But much more than that, theirparticipation will enable municipalities all over New Jersey to benefit from the results of theevaluations contained in this report. The Government Performance Project and the NewJersey Initiative are two of the most comprehensive surveys ever conducted of core govern-ment management systems. The NJI is derived from the GPP, which is a successful, widelyknown, highly regarded, and credible national research project. Municipalities that partici-pated in the NJI took advantage of an opportunity to be a part of cutting-edge publicmanagement research.

Governments today find that they are often held to specific performance standards suchas the number of potholes filled per week. Also, governments are often judged by whether ornot expenditures match revenues without regard to need, sources of funds, or the adequacyof resources to support management systems. The GPP and NJI focus on the capacity of gov-ernments to perform. Without systems in place and those systems coordinated, governmentscannot meet the demands placed on them, however worthy they may be. Like the GPP, theNJI seeks to raise the importance of understanding management systems and enhancing thecapacity of governments to perform.

New Jersey municipalities, like all levels of governments across the nation, are expectedto improve their performance. Most of the reform emphasis has been on measures of per-formance and not on capacity to perform. Common sense tells us, however, that unlesscapacity is present, measurement of results can be a futile and dispiriting exercise. The NJIexamines capacity by analyzing the extent to which government has the right resources in

Assessing Management Capacity in New Jersey Municipalities 7

the right place at the right time, whether it has and can use the right information at theright time, and whether the management systems that support both the visions and strate-gies of leaders are present. Government management capacity is the platform forgovernment performance. Without capacity in place, high performance is not likely to occur.With it in place, both performance and its effective measurement become more likely. TheNJI helps participating municipalities learn more about their management system capacities,know where and how to improve management systems, and, hence, increase performance.

Furthermore, the NJI can help all of the state’s municipalities understand what consti-tutes good management systems. One of the NJI’s objectives is to draw out lessons abouteffective management systems and to understand how, and in what contexts, good manage-ment matters to strong performance. Consequently, the NJI facilitates the sharing ofinformation and a learning process among New Jersey municipalities.

Management Capacity

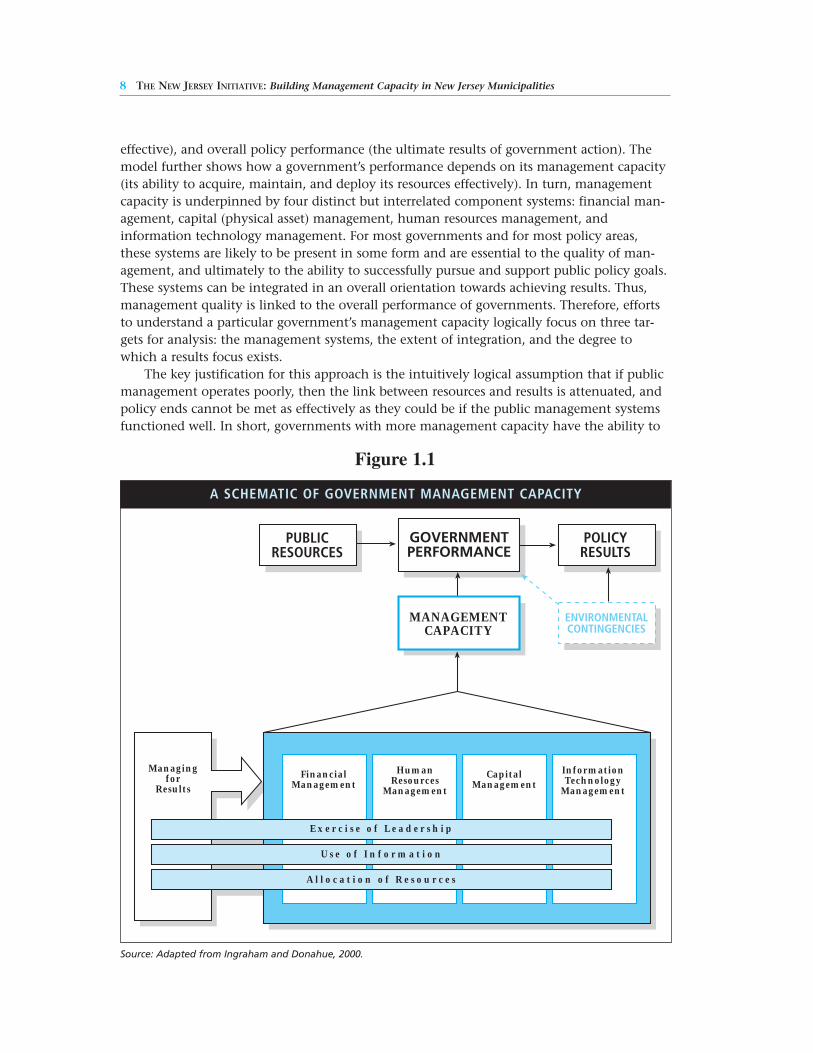

This section presents the conceptual framework that describes the key relationships inherentin government performance and forms the analytical basis for the New Jersey Initiative. Thisframework is presented in two parts. First, we discuss the relationship between managementand performance. Then, we define management capacity and describe three key dimensionsof capacity that affect a government’s ability to be effective: the major management systemscommonly present in governments, the mechanisms by which these systems are integrated,and the role of a focus on results. Much of the discussion presented here is derived fromscholarship associated with the Government Performance Project.

Management and Performance

Discussions of performance and reform are integral to contemporary debates about the con-tinuing role of government in society. Thus, rigorous analysis of and prescriptions toimprove government performance must be cognizant of the complex issue of how to assessand improve government management. As governments movetoward greater emphasis on results, they and their constituents havebegun to pursue this very objective throughout the United States andelsewhere, as evidenced by the focus and nature of many modernreform initiatives. The idea that reforms should target managementis sensible because the systems created within and across governmentorganizations to manage resources, and to translate them into publicservices, are substantially influenced by public managers. At the sametime, many critical environmental influences on performance (suchas politics and elections; legislative mandates; economic, social, andphysical conditions; the media; and citizen views about policy prob-lems) are mostly beyond the control of public organizations andtheir managers. Nonetheless, to understand how to improve publicperformance, the quality of public management must receive primeattention.

The model shown in Figure 1.1 represents the linkage between public resources, govern-ment management performance (the degree to which a public entity’s administration is

Therefore, efforts tounderstand a particu-

lar government’smanagement capacity

logically focus on threetargets for analysis:

the management systems, the extent of

integration, and thedegree to which a

results focus exists.

effective), and overall policy performance (the ultimate results of government action). Themodel further shows how a government’s performance depends on its management capacity(its ability to acquire, maintain, and deploy its resources effectively). In turn, managementcapacity is underpinned by four distinct but interrelated component systems: financial man-agement, capital (physical asset) management, human resources management, andinformation technology management. For most governments and for most policy areas,these systems are likely to be present in some form and are essential to the quality of man-agement, and ultimately to the ability to successfully pursue and support public policy goals.These systems can be integrated in an overall orientation towards achieving results. Thus,management quality is linked to the overall performance of governments. Therefore, effortsto understand a particular government’s management capacity logically focus on three tar-gets for analysis: the management systems, the extent of integration, and the degree towhich a results focus exists.

The key justification for this approach is the intuitively logical assumption that if publicmanagement operates poorly, then the link between resources and results is attenuated, andpolicy ends cannot be met as effectively as they could be if the public management systemsfunctioned well. In short, governments with more management capacity have the ability to

Source: Adapted from Ingraham and Donahue, 2000.

Figure 1.1

A SCHEMATIC OF GOVERNMENT MANAGEMENT CAPACITY

8 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

FinancialManagement

HumanResources

Management

CapitalManagement

InformationTechnology

Management

Managingfor

Results

Exerc i se of Leadership

Use of Infor mat ion

Al locat ion of Resources

PUBLICRESOURCES

POLICYRESULTS

GOVERNMENTPERFORMANCE

MANAGEMENTCAPACITY

ENVIRONMENTALCONTINGENCIES

Assessing Management Capacity in New Jersey Municipalities 9

perform better than governments with less management capacity, all else equal. Whether gov-ernments with more capacity actually perform better than governments with less capacity (inother words, whether their ability to perform is translated into the desired results) depends onthe influence of other determinants, such as the political environment or economic condi-tions. Because assessing capacity ultimately allows us to understand the potential to achievepolicy outcomes that is created by the configuration and operation of a government’s man-agement systems, it gets at the heart of government effectiveness; public organizationalstructures and managerial behavior are drivers of policy outcomes that public administratorscontrol to a large extent.

In short, management performance supports policy performance. And capacity supportsperformance – all else equal, if public organizations have good managers and good manage-ment systems, they are more likely to be effective performers. It is important, though, not toconstrue management capacity as demonstrated performance. It is, rather, a platform for per-formance – a measure of positive or negative potential. The capacity to perform is the targetof our analysis.

Management Capacity Defined

By “capacity” we mean government’s intrinsic ability to marshal, develop, direct, and controlits human, physical, and information capital to support the discharge of its policy directions.That is, management capacity concerns the extent to which a government has the rightresources in the right place at the right time. A government’s management capacity residesboth in its people – public managers – and in what we refer to as “management systems”:administrative structures and processes created to address a government’s financial, humanresources, capital, and information technology needs. Capacity is also intertemporal, that is, itdepends on the extent to which a government can maintain a reliable and appropriately con-figured resource base over time, success at which necessitates functions such as strategicplanning, performance measurement, and performance monitoring. In addition, capacityencompasses both a public entity’s intrinsic administrative ability (i.e., its innate potential toperform), and its ability to carry out its administrative functions under existing environmen-tal conditions, such as resource constraints and political imperatives. Finally, capacity is notsimply structural; rather, it depends on the quality of a government’s management systemsand the extent to which they are mutually enabling in support of meeting the government’soverall administrative needs.

Components of management capacity

As we have stated, a government’s management capacity fundamentally depends on threecomponents, each of which we will now describe briefly:

1. The configuration, tasks, procedures, and work processes of a government’s manage-ment systems that embody its intrinsic administrative activities

2. The ways in which these management systems are interrelated and orchestrated to forma coherent and cohesive totality

3. The existence of a formal managing for results system that lends a substantial frame-work to organizational learning processes

10 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

Management systems

For most governments and for most policy areas, four broad core systems are likely to bepresent. The characteristics of the systems that underpin government management are sum-marized next:

Financial management. Government financial management systems distribute and man-age money for public purposes through processes such as procurement, accounting, cashmanagement, and reporting. Financial management includes both budget allocation andbudget execution systems. A financial management system that supports performance mustdetermine the appropriate level of resources, allocate those resources according to strategicpriorities, and spend money effectively and accountably. Key components of the effectivenessof the financial management system include the ability to engage in accurate revenue andexpenditure forecasting, a long-term focus, the practice of planning for contingencies, aware-ness of the linkage between cost and performance, appropriate flexibility, and controls thatguard against waste, fraud, and abuse.

Capital management. Capital management involves planning for, developing, maintain-ing, and disposing of long-lived resources. This area is particularly salient for state and localgovernments, where capital spending and stock management demands are typically morefrequent than in federal agencies, although many federal agencies have large capital responsi-bilities. Key components of the effectiveness of the capital management system includeactive engagement in long-range planning and prioritization of projects, adequate budgetaryresources for infrastructure maintenance and repair, and attention to the relationshipbetween the capital and the operating budgets.

Human resources management. Government activities are typically highly labor-intensiveand, thus, personnel systems, concerned with recruiting, testing, hiring, retaining, motivat-ing, training, and terminating public employees, are a key element of public institutions. Keycomponents of the effectiveness of the human resources management system include the useof coherent rules and procedures, efforts at workforce planning, timely hiring, sufficient pro-fessional development programs, and meaningful reward structures and disciplinary actions.Because increased flexibilities in the human resources management process have been a con-sistent focus of administrative reform, it is also important to consider where in the systemand for whom such flexibility occurs.

Information technology management. The quality and availability of information is crucialto the ability of managers and policymakers to make decisions and carry out the key func-tions of resource acquisition and policy implementation. Managing information technologyincludes the design, acquisition, maintenance, and use of technological systems to collect,analyze, and communicate data. Especially in public institutions responsible for executingcomplicated programs and interfacing with large, diverse constituencies, information tech-nology performs both primary and integrative functions. It not only responds to informationdemands particular to specific programs, but also supports the information needs of theother management systems. Key components of the effectiveness of the information technol-ogy management system include the timeliness, accuracy, reliability, usefulness, andcost-effectiveness of data and the ability of all personnel to use the information systems.

Integration

Good management depends not only on the good performance of each of these systems

Assessing Management Capacity in New Jersey Municipalities 11

independently, but particularly on the extent to which these management systems operateaccording to consistent objectives, are mutually supporting, and are well coordinated.Management systems in combination, not isolation, create effective management capacity.Thus, within the context of government management, the relationships among the manage-ment systems and their contribution to management effectiveness are influenced by thedegree of integration. In our model, integration is the extent to which the management sys-tems are orchestrated as part of a unified, cohesive whole with shared values, common goals,aligned objectives, and mutually-enabling tasks. Integration is primarily accomplishedthrough three key activities: the exercise of leadership, the use of information, and the strate-gic allocation of resources.

Leadership. Leadership essentially refers to the ability of senior executive, appointed, andcareer officials to make decisions; to provide guidance and direction; to develop the institu-tion’s mission, vision, and values and communicate them to all its members; and tocoordinate the behavior of all organizational components and systems to behave in a man-ner consistent with the institutional and broader public values in order to achieve the statedmission and ultimately to realize policymakers’ intent. The extent to which coherence acrossmanagement systems and the capacity to move constructively toward public goals and objec-tives is achieved depends on leadership at both the political and executive levels. Politicalleadership provides a critical set of directions, resources, and supports for system creation,configuration, and maintenance. Political leadership generally does not, however, interactspecifically or consistently with the management systems. Leadership of these systems is theresponsibility of a different set of leaders: those located within the organizations.

Use of information. The freedom, consistency, and speed with which managers causeinformation to flow throughout a government, the attention that managers give data, andthe willingness of managers to share knowledge converge to facilitate or thwart the overallintegration of the management systems. While the information technology management sys-tem, a mechanism concerned with the collection and availability of timely and accurate data,supports the transmission and use of information, it is the interaction of government man-agers with information that can enable the management systems to operate in concert.

Allocation of resources. The decisions managers make about how resources will be garneredand distributed across a government and the activities that facilitate this decision-makingprocess influence the extent to which the management systems are configured to be mutual-ly supporting. The classic example of such activity is the budget process, whereby managersnegotiate over how money will be allocated, which fundamentally communicates the collec-tive perception of the government’s goals and priorities. Another example is the location ofcapable human capital throughout the government. While such processes as recruiting andhiring personnel are the purview of the human resources management system, the place-ment of people at key points of intersection among the management systems affects thedegree of cohesion in the system as a whole.

Results focus

Another factor that affects how the management systems influence management capacity isthe degree to which a formalized system of managing for results is present and in use by thegovernment. This system is itself formally developed as a management system by some gov-ernments and can have an important impact on the quality of the other systems. Managingfor results is the dominant mechanism by which leaders identify, collect, and use the infor-

12 THE NEW JERSEY INITIATIVE: Building Management Capacity in New Jersey Municipalities

mation necessary to evaluate the institution’s performance in pursuit of key objectives tomake decisions and direct institutional actions. Managing for results comprises a set of toolsthrough which organizational learning processes are formalized. It is thus a key tool for lead-ers seeking to improve the ability of the other systems to support the overall institutionalmanagement capacity and ultimately to contribute positively to successful policy outcomes.

By our definition, governments that are managed for results focus continually on discov-ering the most effective ways of achieving their objectives, employing these techniques acrossall management systems, and monitoring agency activity in light of these objectives. Such aresults orientation rests on three vital components. The first is the ability to identify clearobjectives. The second is a means to assess progress toward those objectives according toaccepted criteria or standards, a mechanism often referred to as performance measurement.The third is an established habit of monitoring performance on an ongoing basis. Thus, man-agement capacity is driven not only by the characteristics and degree of integration of themanagement systems, but also by broader mechanisms for tracking activities and perform-ance relative to overall objectives.

Environmental contingencies

It is important to recognize that a variety of environmental factors affect all components inthe government performance system. Local conditions can have a dramatic impact on thecharacter of programs, their outcomes, and policy performance. These factors embody abroad array of influences, including properties of the larger context within which the govern-ment operates and properties of the government’s jurisdiction, such as socioeconomicconditions, demographic characteristics, and the physical environment. It is easy to see thatenvironmental factors might affect public management systems. Human resources manage-ment, for example, will be influenced by demographic factors such as the size andqualifications of the available labor pool. Capital management likely would be affected by theweather.

It is also important to acknowledge that politics and the political environment play animportant part in policy content, management effectiveness, and policy performance. Thepolitical environment plays a crucial role in determining how good performance is defined.The clarity – or lack thereof – of public goals and objectives is directly connected to the poli-tics of organizational mission and support. The capacity of the organization to marshalresources to attain its goals and objectives is directly related to levels of external political sup-port and understanding. In short, management activities and systems do not exist as ends inthemselves, but as one part of the complex performance equation for public organizations. Atthe same time, management matters in ways that are central to public performance.

Value of the Model