Embed Size (px)

Citation preview

© The Chartered Institute of Management Accountants 2012 Page 1

Note: This report is far more comprehensive than would be expected from a candidate in exam conditions. It is more detailed for teaching purposes.

T4- Part B – Case Study

D plc House-Building case – November 2012

REPORT

To: Finance Director

From: Management Accountant

Date: November 2012

Review of issues facing D plc (D)

Contents

1.0 Introduction

2.0 Terms of reference

3.0 Prioritisation of the issues facing D

4.0 Discussion of the issues facing D

5.0 Ethical issues and recommendations on ethical issues

6.0 Recommendations

7.0 Conclusions

Appendices

Appendix 1 PEST analysis of UK Building Industry

Appendix 2 Five forces analysis of UK Building Industry

Appendix 3 SWOT analysis

Appendix 4 Stakeholder analysis for Trevill Planning Decision

Appendix 5 PEST analysis for Building Industry in Country Y

Appendix 6 Supporting calculations

Appendix 7 Part (b) Presentation on aspects of JV agreement

© The Chartered Institute of Management Accountants 2012 Page 2

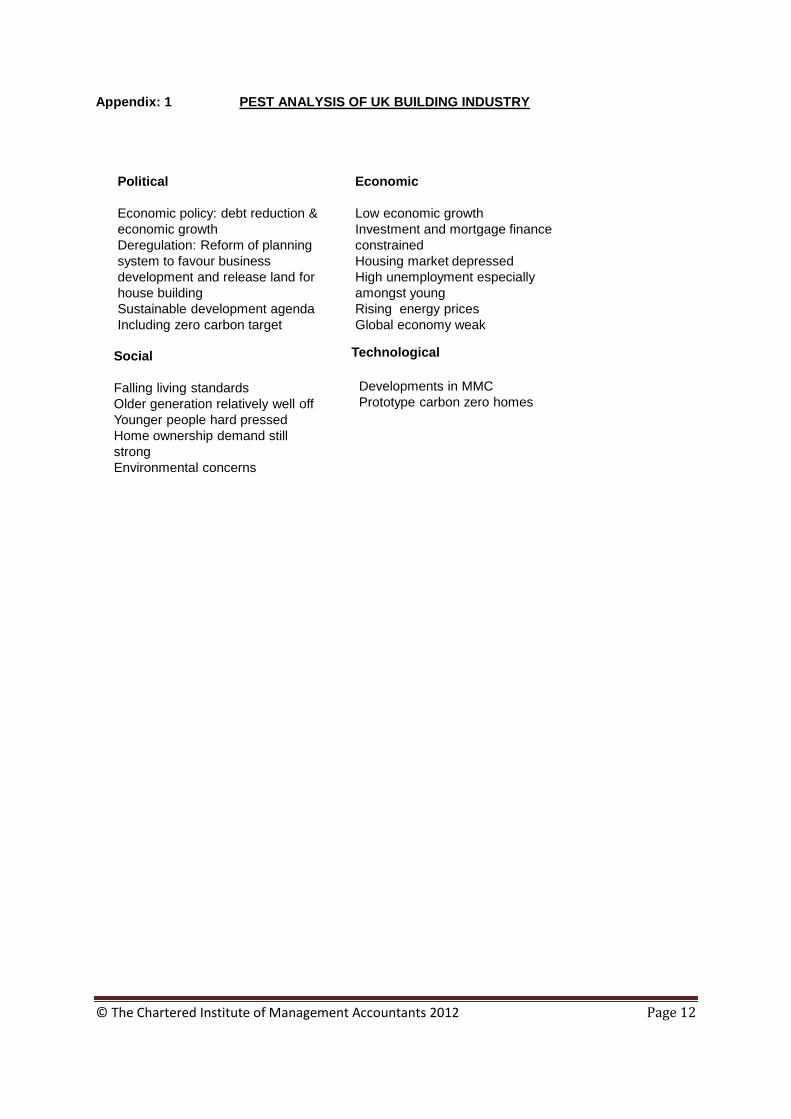

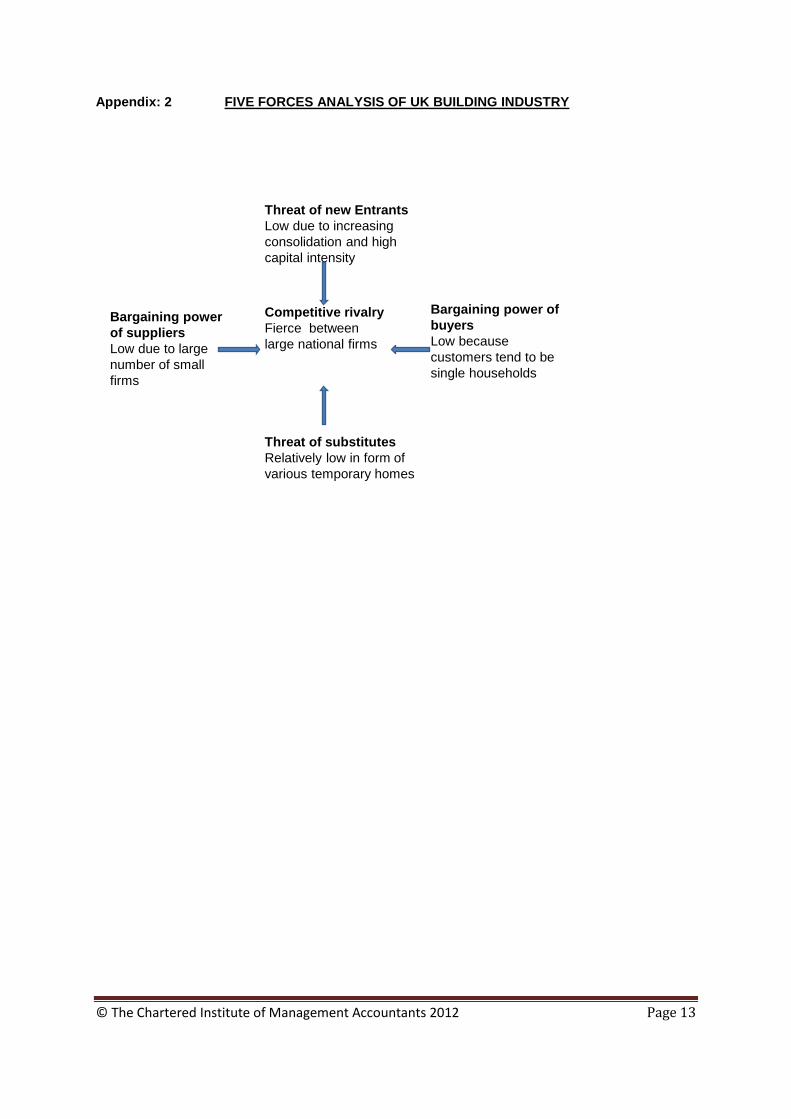

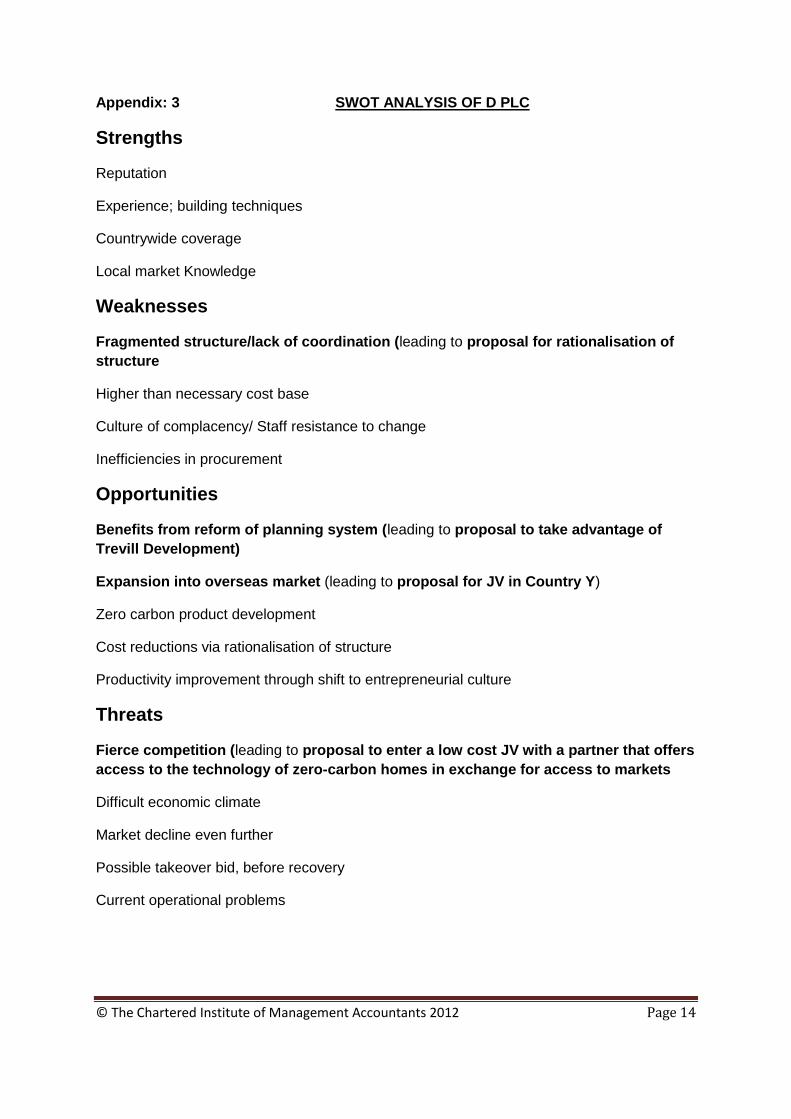

1.0 Introduction D plc (D) like other house-builders is facing difficult times. From a high of 200,700 new homes registered by the National House-Building Council (NHBC) in 2007, the numbers registered have fallen to around 115,000 in 2011 and independent reports suggest that the numbers will fall even further in 2012. The PEST analysis provided in Appendix 1 highlights the key issues facing the industry. The most important issue is the shortage of mortgage availability. This issue is compounded by high levels of unemployment, especially among the young. Porter’s Five Forces analysis of the building industry Appendix 2, suggests that while threats from new entrants, substitutes, and the bargaining power of buyers and suppliers is relatively low, the competitive pressure from its rivals is very high. This competitive pressure arises from the consolidation and increasing capital intensity that has developed in the UK building industry over the last two decades. The SWOT analysis of D in Appendix 3, however, suggests that while D faces a number of threats there still exist profitable opportunities including; an increase in available building land as a result of recent changes in the planning regime, potential expansion into overseas markets, product development opportunities arising from the government’s zero-carbon agenda and cost savings and productivity increases from a rationalisation of the organisation’s structure and systems. In order to exploit these opportunities however, D needs to manage the forces that act to constrain change as well as those that are driving change. The main restraining forces on change are the complacency of staff and the dysfunctional organisational structure, culture and systems. Managing these changes will be necessary to improve the performance of D in the future. The forecast fall in D’s house sales of over 10% per annum with an associated drop in forecast gross margin of over £37 million per year suggest the need for urgent action. This urgency has been increased by a number of recent developments such as the success of one of D’s key rivals, X Builders plc and the opportunity to participate in the Trevill new town development. The pressure on D to improve its performance has also made the exploitation of any market opportunity such as a joint venture with a building firm in Country Y difficult to ignore, see PEST analysis Appendix 5. Finally the long delayed rationalisation of D’s top heavy organisational structure and outdated systems could take significant costs out of running the business and at the same time contribute to its efficiency. The key issues are prioritised in section 3 of this report, and discussed and evaluated in section 4. Section 6 then summarises the main findings and makes recommendations. 2.0 Terms of reference

(a) I am the Management Accountant appointed to write a report to the Finance Director which prioritises analyses and evaluates the issues facing D and makes appropriate recommendations.

(b) I have also been asked to prepare a series of key points for the FD’s use in his forthcoming briefing on preparations for the drawing up of a foreign joint-venture agreement

© The Chartered Institute of Management Accountants 2012 Page 3

3.0 Prioritisation of the issues facing D As indicated in the case scenario, D faces on the one hand, very difficult economic conditions, a high cost base and a major competitive threat from the market leader, and on the other, two major opportunities: first the chance to obtain more building land and develop its substantial land bank more rapidly and secondly the chance to expand its operations into a growing market in South East Asia. 3.1 Top priority - Coping with the threat from the market leader The problem of how to respond to the threat by X Builders which has stolen a lead on the rest of the industry is a particularly difficult one. D’s delay in responding to structural and operational problems as well as a seeming reluctance to embrace new methods and materials means it has a lot of catching up to do. This cannot be done overnight and will involve the commitment of significant time and resources. The reason for making this the first priority is that the Company in meeting these challenges needs to meet the expectations of its institutional investors. This issue needs to be addressed as soon as possible, as it is a threat to its market position and profitability. 3.2 Second priority - Trevill development The development would appear to be a very desirable one if planning permission was to be granted. D needs to consider a number of stakeholders when considering the bidding process for the land, and this is further discussed in section 4 The potential opportunities available to D include opportunities in the domestic market arising from the change to the planning regime and secondly the opportunities for market expansion in South East Asia arising from the rapid process of urbanisation and economic growth. Of the two, the securing of a larger amount of building land in the UK appears to offer the best return for the resources expended because D has a substantial land bank and the knowledge and contacts to translate strategic and even newly available land into land with planning permission ready for development. The case of the Trevill development is likely to be just one development amongst others in the country at which D will have a chance to bid. The Trevill development together with any other UK developments should therefore be given second priority. 3.3 Third priority - Rationalising the present structure Given the declining number of sales and its proportionally increasing overhead cost base, the third priority for D should be that of rationalising its organisational structure, improving its IT systems and trying to keep all other costs down while at the same time maintaining efforts to boost sales. This is an important issue because it impinges on the organisational effectiveness of the company and also provides the potential for cost savings. It is an on-going issue that will need careful management and planning. 3.4 Fourth priority- Completing a JV agreement with a building company in Country Y The preparations for entering the market in Country Y have been on-going for some time and there is every reason for D to press ahead. D is a large organisation and in the case in question the Sales Director has taken the initiative in championing the case and overseeing the feasibility study, choice of potential joint-venture partner and the many other preparations necessary for a joint-venture operation. Due care will be required in dealing with health and safety problems and the example of the use of bribes to secure contracts are associated potential problems of the proposed joint-venture and should be dealt with under the same umbrella.

© The Chartered Institute of Management Accountants 2012 Page 4

This would be a significant opportunity for D to enter a new market at a relatively low cost. In terms of Ansoff’s market matrix the investment in Country Y would be a market development opportunity. Given the resources of the D organisation it should be possible for a working group to continue with the preparations for the JV but not as a substitute for continuing to seek new development sites in the UK. 4.0 Discussion of issues

4.1 Zero carbon homes

The successful development by a competitor of the first full scale development of near carbon free houses underlines the relative weakness of D in the lack of use of modern methods of construction (MMC) and its failure to address the Government’s carbon free agenda. The success of X Builders in being awarded the House Builder of the year Award for outstanding quality for the second year running and becoming established as the country’s leading house builder is also a sign that D has not kept pace with the best in the industry.

The impact of these developments on D is difficult to determine in quantitative terms (potentially a loss of 6% of sales in 2013 and increasing) but there will be an effect on the general morale of the work force of D who will see they are losing ground to one of their main competitors. This cannot but have a detrimental effect on the productivity of D’s workforce unless action is taken to improve morale and motivation.

The required investment for the production of the zero carbon houses is relatively modest, when compared against the potential increasing sales loss for D. It involves new building techniques, new materials, and ventilation and heating systems together with new knowledge and skills that are not required in the traditional house-building process. It is also considered worthwhile in terms of potential construction cost saving for firms, in lower heating (or cooling) costs to the new home owners and in the reduced impact on the natural environment.

As far as this investment is concerned it will also be necessary to bear in mind potential related developments such as the enhanced opportunities for quicker and greater access to building land arising from the reform of the UK planning system and the opportunities available for profitable developments in the emerging economies.

In strategic terms, any venture into the production of carbon free homes is an instance of new product development for D and like any innovatory product carries a degree of risk. It does seem from the experience of X Builders that there is a demand for carbon free homes and the pressure is on from the Government for house builders to build carbon free homes. There is however, some evidence that the prospective British house buyer has fairly traditional tastes and so it will be necessary to produce houses that combine traditional features with the kind of materials, systems and technology that amounts to what the Government defines as ‘sustainable development’ and for which there would be a demand.

Given the lead established by X in Green Home construction and the Government’s commitment to a carbon free agenda D is under some pressure to begin its own production of houses that incorporate the materials, technology and systems that will help its houses meet government standards and consumers’ expectations and as a result D needs to respond to this challenge. It has already anticipated a fall in market share of 6% against the reduced forecast in 2013, (reduced margin of £19.1 million see Appendix 6.5) with further falls expected in future years.

To this end an investment of £21 million, with a payback of just over a year is well justified, enabling D to actively pursue the development of low energy efficient homes. Companies which have taken a lead in this market, appear to be at an advantage. Customers appear to be prepared to pay a premium for a future of lower energy bills, and a perception that their house is environmentally friendly, D cannot afford not to be a part of these developments.

© The Chartered Institute of Management Accountants 2012 Page 5

4.2 The Trevill Planning Application

The Trevill development needs to be considered as one of an increasing number of development opportunities that changes to the new planning system will bring forth.

As in any business venture, the opportunity to bid for extra projects is only worthy of consideration if the potential development can be undertaken profitably.

This development would appear to be a very desirable one if planning permission was to be granted.

It can be evaluated using Johnson, Scholes and Whittington’s framework as follows.

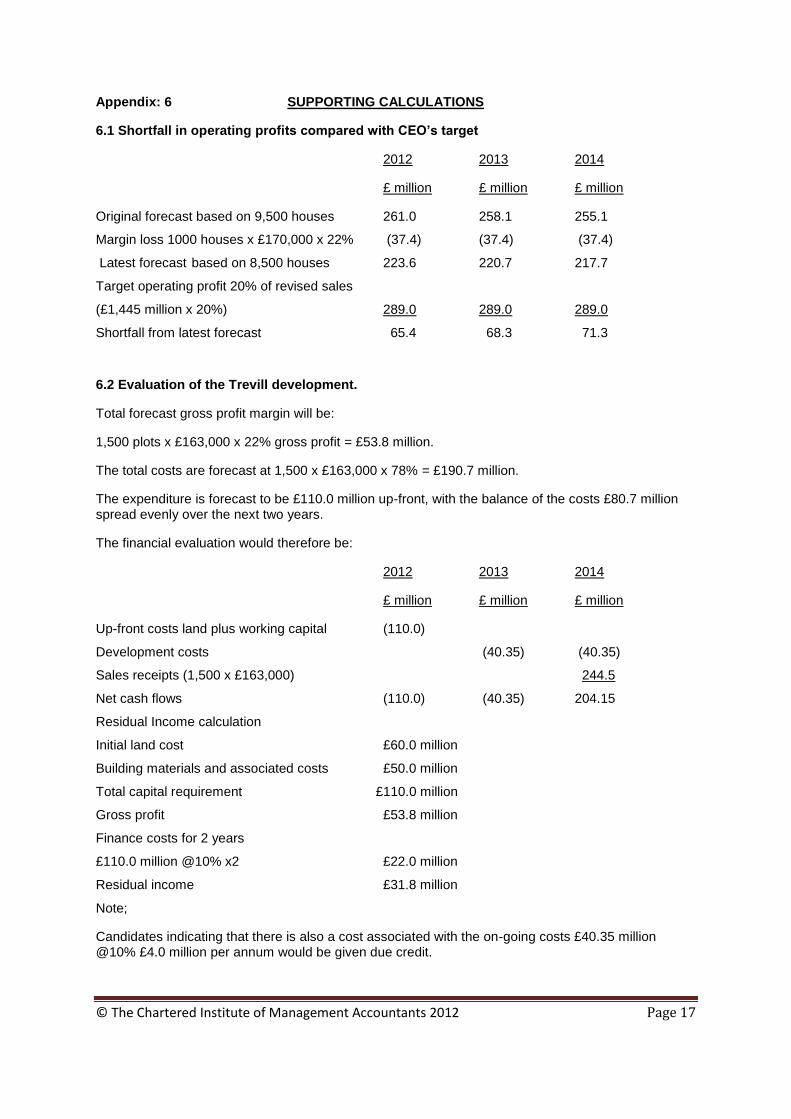

The development would be suitable for D to undertake. It builds on D’s core strengths i.e. house building in the UK, and with the forecast drop in activity of 1,000 homes to 8,500 homes built, D has the capacity to manage this 1,500 home development. It is acceptable because as can be seen from Appendix 6.2 cash flows and profitability, are favourable over the development period. In terms of feasibility, the FD is confident of obtaining finance and treating this as a stand-alone project. In the event that this is not possible the existing cash position will still enable the project to go ahead, but care will be needed in managing the overall cash position. The likely implications for D’s stakeholders if the Company progresses with the Trevill development will in general be positive in that it means substantial additional business with all that this implies for future earnings. For employees this will mean more secure employment, for shareholders potential dividends, for creditors the assurance of loan repayments, for suppliers extra business and for customers the opportunity to purchase a new house in a small country town with good local services.

There are however, some minor risks. D will wish to be seen as a good corporate citizen. A successful media campaign by protestors like 3VAG and national environmental interest groups that manages to label Trevill as, ‘a blight’ on the UK countryside could have some impact on D’s reputation as a socially responsible company that cares about the communities for which it builds houses and the environment which it claims to try to protect.

It will be important for D therefore to make clear in its marketing campaign that its particular development in Trevill will be designed to fit sympathetically into a small country town and that its houses will meet the carbon neutral standards set by the government and local planning authority while at the same time exhibiting the traditional appearance of the British country house.

It is also relevant to note that the planning system, although reformed, still involves a political process and will be the outcome of a contested fight between vested interest groups.

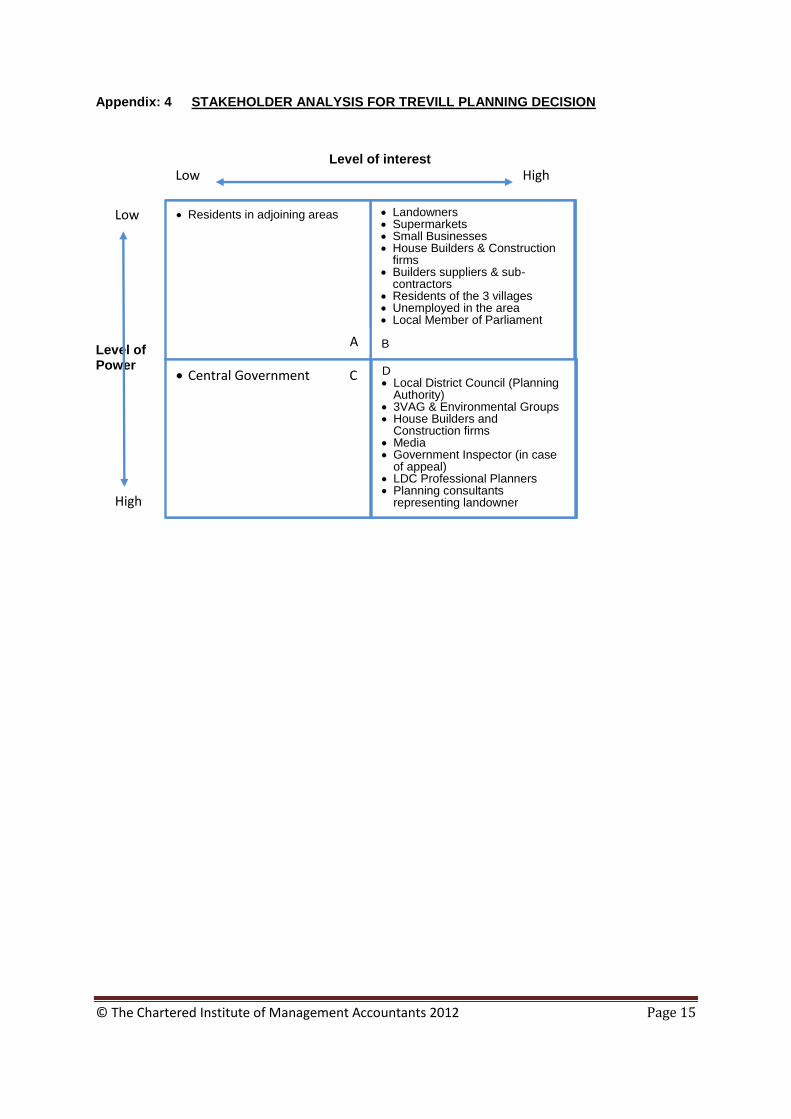

In attempting to predict the outcome it is useful to consider the power and interests of the stakeholders involved using one of the matrices that have been developed for this purpose.

The Mendelow stakeholder matrix is a widely used model in the field of strategic management and will be employed here. The framework can be found in Appendix 4 below and has been used to identify the power and interests of each stakeholder group.

What becomes apparent from this mapping exercise is that some stakeholders such as residents living in other parts of the country, as in ‘A’ will have limited interest in the outcome of the planning decision since it does not immediately affect them, that said however, other such residents living beyond the Trevill district may have a high interest because of their wish to see the British countryside protected. In both cases however, their power to affect the outcome of the planning decision will vary according to whether or not they become active members of a campaigning group either for or against the development.

Stakeholders classified in ‘B’ of the matrix will generally have high interest either because, as in the case of businesses and the unemployed, the building of the new town would be to their benefit or

© The Chartered Institute of Management Accountants 2012 Page 6

because in the case of village residents a decision to build might be regarded as detrimental to the rural environment in which they live.

In ‘C’ Central Government will have considerable power but limited interest in the sense that this will be just one local planning decision amongst many hundreds or thousands of others. That said, the Government might well become interested if the national media were to highlight the Trevill application as a test case of its recently reformed planning legislation.

Stakeholders in ‘D’ would generally have high interest, because the decision could have a significant impact on their business, political, professional and/or environmental interests and concerns. These groupings would also have considerable power to influence the planning decision because of their power of expertise, legal power, persuasive power and political power respectively.

It is highly likely that D and all the other house building companies would make written representation to the District Council Planning authority to cast the best possible light on a decision in favour of the proposed development and that 3VAG and other environmental action groups would themselves be represented by professional specialists in the planning field.

The outcome of such an application is difficult to predict and depends to a considerable extent on the action mounted by the protest groups, the role of the media, the skills of professional lobbyists on each side and the alignment of political interests within the Local District Council. D and other building companies will be watching the manoeuvring of the main stakeholder groupings to get the earliest possible information so that they can put their plans into action.

If a successful planning application were submitted a financial analysis of the Trevill project indicates that it will generate additional margin of £53.8m, and have residual income of £31.8m (See Appendix 6.2)

4.3 Company structure, change and reorganisation

The existing structure of D is a result of the growth of the Company over many years as D acquired companies H, R, and S.

The companies are still operating in their original trading styles, and there is some justification for this with regard to sales and marketing, as they have all established a reasonable reputation, (present problems excepted), for building good quality houses to the various differing budgets.

However this has led to a somewhat unwieldy organisation structure. As the company expanded, it was found that because of distances involved, control on a regional basis was required to ensure the effective implementation of strategies and control of quality and costs.

The FD is acutely aware that the current structure is the cause of conflicts between companies at the local level, and that the flow of information through the organisation is both poor and in some cases inaccurate, because of the number of people involved and the considerable duplication of functions. In the ‘good’ times this has been allowed to continue as the cost of major reorganisation didn’t seem to merit the potential problems and cost savings of such a move. The current structure was established before the availability of more modern data processing and transfer techniques and with these now available at reasonable costs he is convinced that it is time to reorganise.

From a financial point of view centralising the administration functions appears to be good value. The investment would cost around £75 million, but the savings of around 40% of the operating expenses is significant for D. The potential savings would be £38.9 million in 2013 (i.e.40% of £97.2 million) and £40 million in 2014 (i.e. 40% of £100.2 million). This equates to a saving equivalent to the contribution on more than 1000 house sales (1000 x £170,000 x 22% = £37.4 million) and is urgently required.

Although the full financial benefit would only be achieved after two years, the one-off investment cost is recovered inside a two year period and is of benefit on an on-going basis. In reality it may be that these exact savings are not achieved in the time period, re-organisation sometimes poses more difficulties than planned for.

© The Chartered Institute of Management Accountants 2012 Page 7

There are also some management implications of rationalising the organisation structure. Some staff will be made redundant, and other staff moved to the centre. The management of change is not an easy thing for organisations to undertake, and this process needs to be carefully thought through, with due care given to redundancy issues and staff.

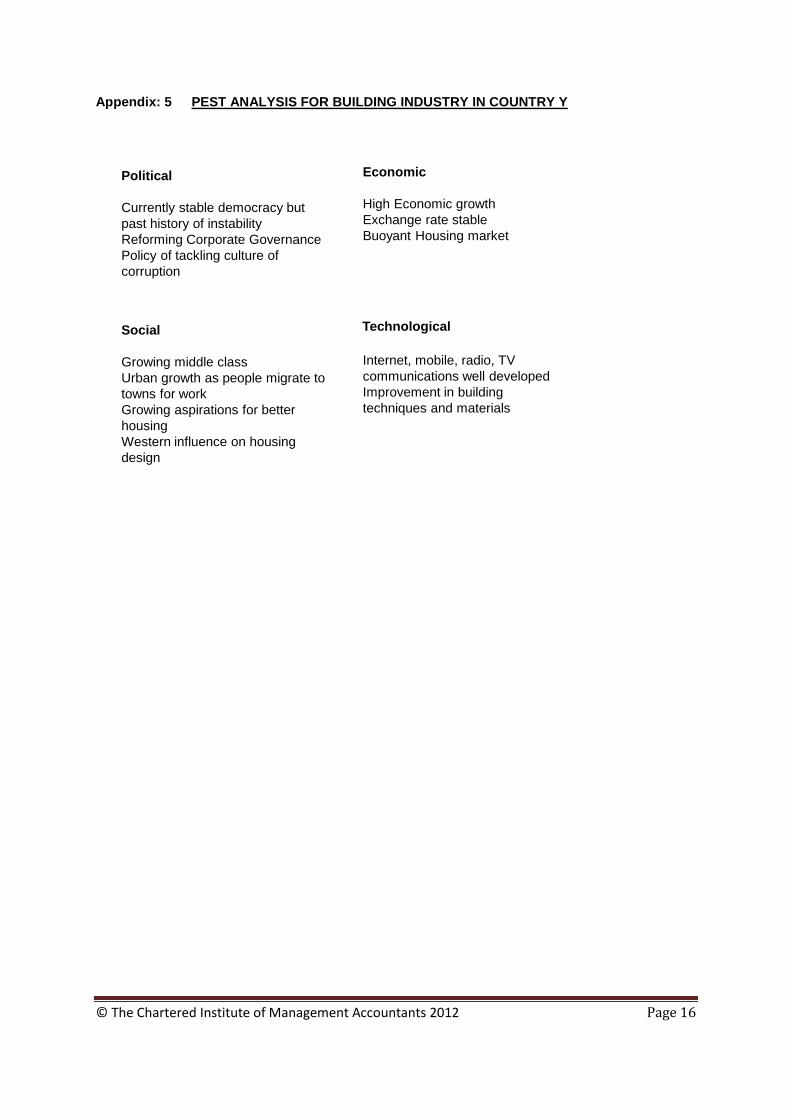

4.4 Proposed joint-venture in Country Y

This would be a significant opportunity for D to enter a new market at a relatively low cost.

The opportunities and threats of investing in country Y are considered below:

Opportunities

Country Y has enjoyed recent rapid economic growth of about 7% per annum.

Although this may inevitably slow because of the current world-wide economic conditions, Y does offer D the opportunity to get into a growing economy at a relatively early stage of development.

For D this would represent a major opportunity to diversify away from its current core market i.e. the UK. This would help mitigate the tough competition in the UK, and would also provide D with a learning experience for perhaps developing other markets abroad in the future.

D’s Sales Director already has good contacts in Y’s house building industry and this would be a good opportunity for D on which to capitalize.

There appears to be a demand in Y from increasingly affluent house purchasers for more western-style buildings, which would be an opportunity for D to build upon its strengths.

Working with either company L or S would reduce the risk for D because of the joint-venture partners’ local knowledge.

However an investment in Country Y is not without its potential problems.

Threats

The political stability of Country Y is only recent, and the Country has been the subject of armed conflict in the past.

Some groups are still very much opposed to the present government.

Corporate governance and the legal system in Y are weak, with much corruption.

Large family groups typically exert a significant influence over companies, which can lead to abuse of power. For example Fellowes, the US stationery company, had to get courts to liquidate its joint venture in China after a power struggle within the Chinese partner company.

Cultural differences between the UK and Y will typically impact on business relationships.

Country Y is subject to frequent earthquakes and typhoons.

An investment in Country Y would leave D exposed to foreign exchange risks.

© The Chartered Institute of Management Accountants 2012 Page 8

5.0 Ethical issues

5.1 Newspaper allegations in Country Y

The reason why this has an ethical aspect is that, certainly in Western countries, managers and professionals are expected to observe the highest standards of conduct, and to comply with some fundamental ethical principles and in particular those of integrity (i.e. being honest in business relationships), and also of professional behaviour.

As a responsible company therefore D would not wish to be seen associating with a company that it knows has won a contract through bribery. However D also needs to recognise that there is a cultural difference between Country Y and the UK, and that corruption appears to be reasonably commonplace in Y.

However from a business perspective Company L would be an attractive proposition and whichever company D should choose for a joint venture in Country Y, it would presumably be exposed to a similar risk.

It is recommended therefore that this issue in itself should not prevent company D from working with Company L.

However it is further recommended that D, should it form a joint venture with L, gets L to agree that all contracts awarded to subcontractors in the joint venture should be honest and as a result of open and competitive tenders, and that major contracts awarded are ratified by D.

The rationale is that D would wish to ensure that it has done all that it can to ensure honest business relations and that would not be construed by an outsider to be dishonest.

5.2 Health and safety issues with company S

The reason why this is considered to be an ethical issue is that all companies have an absolute obligation to provide a safe working environment for their workforce, and to ensure that their products (construction work in this case) provide no risks to the community at large.

In the case of Company S there appear to be two major failures in working practices. If D should decide to form a joint venture with S, it lends itself to accusations of putting profits before safety concerns by knowingly working with a company which appears to have lower standards than expected.

S may argue that the deaths and injuries to workers is a subcontractor issue, possibly one of poor supervision. However S has an absolute responsibility to ensure that safe working practices are followed.

In the partial collapse of the building, S should have expertise in these constructions since Country Y is in a known typhoon belt. If other buildings in the area have also been affected by the typhoon, then it may just be an exceptional and one-off situation. If not, then the quality of S’s building work would be of concern, but even so S needs to learn for future projects.

It would appear that Company S would wish to benefit from D’s experience to bring it up to the highest standards of health and safety processes. So therefore from an ethical perspective it could be argued that D would be helping both Company S and related stakeholders (and in particular their workforce,

customers and the local communities) by forming a joint-venture with S.

It may be that Country Y has a similar organisation to the UK’s NAHB (National Association of House Builders) which works with members to support cost effective building codes and practices. If so, then D could use its experience in the UK to help facilitate this process.

In conclusion, from a business perspective, D risks damaging its reputation for health and safety.

However from an ethical perspective it is recommended that D could still form a joint-venture with Company S.

© The Chartered Institute of Management Accountants 2012 Page 9

The rationale for this recommendation is that D would be acting responsibly in trying to improve working practices in the country, and encouraging companies in Country Y to move towards high western standards for health and safety.

6.0 Recommendations

6.1 Zero carbon homes

6.1.1 Recommendation

D ensures that it has the facilities and abilities to produce an increasing proportion of its houses as ‘green’ zero-carbon homes in line with market expectations, thus protecting its established market position.

The investment of £21 million is approved and the co-ordination of the required marketing and manufacturing are put in place as soon as possible to protect the future market base of the company.

6.1.2 Justification

If D is to remain in the premier league of house builders it needs to remain competitive and up-to-date with its product offering. If not, it risks jeopardising its market position, and losing out to other more forward thinking competitors.

6.1.3 Actions to be taken

The project should be initiated with co-ordination between design, procurement, and operations to ensure that the required ‘green’ product specifications can be achieved in the short timescale required.

Some of the existing planned build should be upgraded to the new specification with immediate effect, and effective marketing should be commenced based on the design specifications produced and the ‘show’ houses built. This to apply to all companies in all regions.

Marketing literature should emphasise the ‘green’ credentials and long term energy saving benefits of the technological investments. Regional ‘open days’ need to be arranged to encourage potential customers to visit new build properties to see for themselves the benefits of the new energy saving technology.

One advantage for D of being a late comer to the new technology rather than being a first mover is that a prototype near carbon free house has already been constructed by a competitor and so other house builders like D can copy the model. The downside of being late into the market is that the competitor X Builders will have already established a significant market share with what is a new product that fits with the demands of the times.

6.2 Trevill

6.2.1 Recommendation

The investment should be undertaken as it has a positive residual income, and positive opportunities for further investment. A planning application should be made, and considerations of stakeholder reactions and methods of dealing with these should be undertaken, as discussed above.

6.2.2 Justification

This course of action will produce a positive residual income, and may lead to the development in the future of more plots. The company regards this as a prestige project, and association with Trevill will hold it in good stead for future developments.

© The Chartered Institute of Management Accountants 2012 Page 10

6.2.3 Actions to be taken

Ensure planning applications are correctly applied for and all procedures rigidly adhered to. Ensure financing is available and in place. Ensure stakeholder reactions are monitored/dealt with appropriately. Ensure that the bid is submitted in accordance with the procedures and requirements of the bidding process.

6.3 Reorganisation of structure.

6.3.1 Recommendation

Select a change in structure which is more centralised and communicate this to the stakeholders. The rationale is potential cost savings, survival of the business, and the ability to manage the company efficiently going forward in a cost effective manner.

Following on from this decision, the staff will need to be briefed, with appropriate justification. Implementation teams will need to be formed, project managers and teams organised, with all the associated project management procedures in place.

6.3.2Justification

Perhaps the most savings could be achieved by rationalising at the original company level, H,R,S, as this accounts for the bulk of the overheads (50%), however it may be that certain sales and marketing elements may need to be retained. Some savings may be made at regional level; it would seem that a reasonable estimate of 40% savings can be achieved.

So for an investment of £75 million savings of 40% x £97.2million £38.9 million (2013) and 40% x £100.2 million £40 million seem well worth it, paying back the investment in just under 2yrs. This would more than offset, but should not be considered a substitute for, the loss of current sales volumes. An added benefit is that this will continue into the future and provide a sound administrative and cost base to assist the future development of the company.

6.3.3 Actions to be taken

A review of the current structure is required with a detailed look at costs associated with each Company and existing and desired information flows around D Company. This may be a role for outside consultants.

When this is complete and presented to the Board, there will inevitably be a choice of options with regard to structures and information systems.

Implementation plans will need to be drawn up, with time scales and deadlines, and it must be ensured that existing functions will carry on while new ones are put in place.

Information regarding the new structure will need to be shared with staff, and those who will be adversely affected assisted accordingly. Meetings will need to be arranged throughout the company to keep the staff informed.

6.4 Joint-venture

6.4.1 Recommendation Enter a joint-venture with S, as it is more resilient, potentially providing a faster return, will give quick improvement to Company results, and is a greener option. It is necessary to ensure the agreement is very strictly worded and agreed terms are adhered to, with potential get-out clauses and agreed procedures for dispute resolution.

© The Chartered Institute of Management Accountants 2012 Page 11

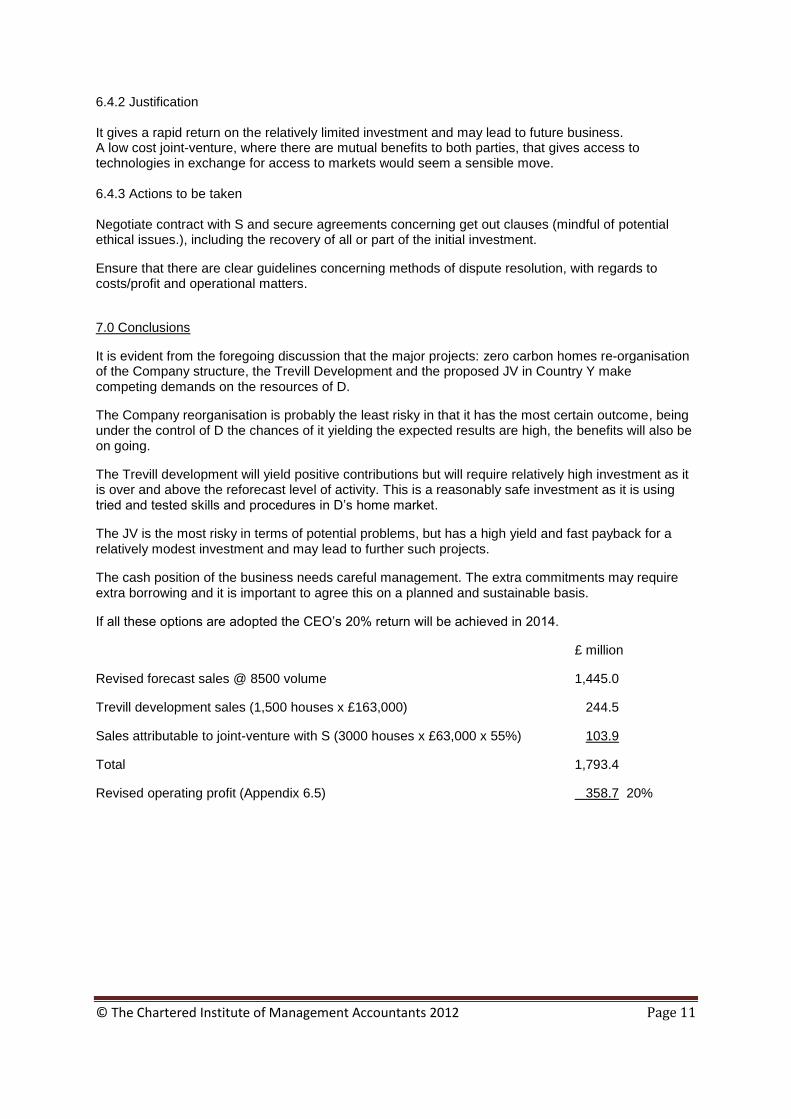

6.4.2 Justification It gives a rapid return on the relatively limited investment and may lead to future business. A low cost joint-venture, where there are mutual benefits to both parties, that gives access to technologies in exchange for access to markets would seem a sensible move. 6.4.3 Actions to be taken Negotiate contract with S and secure agreements concerning get out clauses (mindful of potential ethical issues.), including the recovery of all or part of the initial investment.

Ensure that there are clear guidelines concerning methods of dispute resolution, with regards to costs/profit and operational matters.

7.0 Conclusions

It is evident from the foregoing discussion that the major projects: zero carbon homes re-organisation of the Company structure, the Trevill Development and the proposed JV in Country Y make competing demands on the resources of D.

The Company reorganisation is probably the least risky in that it has the most certain outcome, being under the control of D the chances of it yielding the expected results are high, the benefits will also be on going.

The Trevill development will yield positive contributions but will require relatively high investment as it is over and above the reforecast level of activity. This is a reasonably safe investment as it is using tried and tested skills and procedures in D’s home market.

The JV is the most risky in terms of potential problems, but has a high yield and fast payback for a relatively modest investment and may lead to further such projects.

The cash position of the business needs careful management. The extra commitments may require extra borrowing and it is important to agree this on a planned and sustainable basis.

If all these options are adopted the CEO’s 20% return will be achieved in 2014.

£ million

Revised forecast sales @ 8500 volume 1,445.0

Trevill development sales (1,500 houses x £163,000) 244.5

Sales attributable to joint-venture with S (3000 houses x £63,000 x 55%) 103.9

Total 1,793.4

Revised operating profit (Appendix 6.5) 358.7 20%

© The Chartered Institute of Management Accountants 2012 Page 12

Appendix: 1 PEST ANALYSIS OF UK BUILDING INDUSTRY

Political

Economic policy: debt reduction &

economic growth

Deregulation: Reform of planning

system to favour business

development and release land for

house building

Sustainable development agenda

Including zero carbon target

Economic

Low economic growth

Investment and mortgage finance

constrained

Housing market depressed

High unemployment especially

amongst young

Rising energy prices

Global economy weak

Social

Falling living standards

Older generation relatively well off

Younger people hard pressed

Home ownership demand still

strong

Environmental concerns

Technological

Developments in MMC

Prototype carbon zero homes

© The Chartered Institute of Management Accountants 2012 Page 13

Appendix: 2 FIVE FORCES ANALYSIS OF UK BUILDING INDUSTRY

Threat of new Entrants

Low due to increasing

consolidation and high

capital intensity

Bargaining power

of suppliers

Low due to large

number of small

firms

Competitive rivalry

Fierce between

large national firms

Bargaining power of

buyers

Low because

customers tend to be

single households

Threat of substitutes

Relatively low in form of

various temporary homes

Porter’s Five Forces analysis of UK House Building Industry

© The Chartered Institute of Management Accountants 2012 Page 14

Appendix: 3 SWOT ANALYSIS OF D PLC

Strengths

Reputation

Experience; building techniques

Countrywide coverage

Local market Knowledge

Weaknesses

Fragmented structure/lack of coordination (leading to proposal for rationalisation of

structure

Higher than necessary cost base

Culture of complacency/ Staff resistance to change

Inefficiencies in procurement

Opportunities

Benefits from reform of planning system (leading to proposal to take advantage of

Trevill Development)

Expansion into overseas market (leading to proposal for JV in Country Y)

Zero carbon product development

Cost reductions via rationalisation of structure

Productivity improvement through shift to entrepreneurial culture

Threats

Fierce competition (leading to proposal to enter a low cost JV with a partner that offers

access to the technology of zero-carbon homes in exchange for access to markets

Difficult economic climate

Market decline even further

Possible takeover bid, before recovery

Current operational problems

© The Chartered Institute of Management Accountants 2012 Page 15

Appendix: 4 STAKEHOLDER ANALYSIS FOR TREVILL PLANNING DECISION

Level of interest

Level of Power

Landowners Supermarkets Small Businesses House Builders & Construction

firms Builders suppliers & sub-

contractors Residents of the 3 villages Unemployed in the area Local Member of Parliament

Residents in adjoining areas

Central Government D Local District Council (Planning

Authority) 3VAG & Environmental Groups House Builders and

Construction firms Media Government Inspector (in case

of appeal) LDC Professional Planners Planning consultants

representing landowner

A

Landowners Supermarkets Small Businesses House Builders & Construction

firms Builders suppliers & sub-

contractors Residents of the 3 villages Unemployed in the area Local Member of Parliament

Residents in adjoining areas

Central Government D Local District Council (Planning

Authority) 3VAG & Environmental Groups House Builders and

Construction firms Media Government Inspector (in case

of appeal) LDC Professional Planners Planning consultants

representing landowner

A

Landowners Supermarkets Small Businesses House Builders & Construction

firms Builders suppliers & sub-

contractors Residents of the 3 villages Unemployed in the area Local Member of Parliament B

Residents in adjoining areas

Central Government C D Local District Council (Planning

Authority) 3VAG & Environmental Groups House Builders and

Construction firms Media Government Inspector (in case

of appeal) LDC Professional Planners Planning consultants

representing landowner

A

Low High

Low

High

© The Chartered Institute of Management Accountants 2012 Page 16

Appendix: 5 PEST ANALYSIS FOR BUILDING INDUSTRY IN COUNTRY Y

Political

Currently stable democracy but

past history of instability

Reforming Corporate Governance

Policy of tackling culture of

corruption

Economic

High Economic growth

Exchange rate stable

Buoyant Housing market

Social

Growing middle class

Urban growth as people migrate to

towns for work

Growing aspirations for better

housing

Western influence on housing

design

Technological

Internet, mobile, radio, TV

communications well developed

Improvement in building

techniques and materials

© The Chartered Institute of Management Accountants 2012 Page 17

Appendix: 6 SUPPORTING CALCULATIONS

6.1 Shortfall in operating profits compared with CEO’s target

2012 2013 2014

£ million £ million £ million

Original forecast based on 9,500 houses 261.0 258.1 255.1

Margin loss 1000 houses x £170,000 x 22% (37.4) (37.4) (37.4)

Latest forecast based on 8,500 houses 223.6 220.7 217.7

Target operating profit 20% of revised sales

(£1,445 million x 20%) 289.0 289.0 289.0

Shortfall from latest forecast 65.4 68.3 71.3

6.2 Evaluation of the Trevill development.

Total forecast gross profit margin will be:

1,500 plots x £163,000 x 22% gross profit = £53.8 million.

The total costs are forecast at 1,500 x £163,000 x 78% = £190.7 million.

The expenditure is forecast to be £110.0 million up-front, with the balance of the costs £80.7 million spread evenly over the next two years.

The financial evaluation would therefore be:

2012 2013 2014

£ million £ million £ million

Up-front costs land plus working capital (110.0)

Development costs (40.35) (40.35)

Sales receipts (1,500 x £163,000) 244.5

Net cash flows (110.0) (40.35) 204.15

Residual Income calculation

Initial land cost £60.0 million

Building materials and associated costs £50.0 million

Total capital requirement £110.0 million

Gross profit £53.8 million

Finance costs for 2 years

£110.0 million @10% x2 £22.0 million

Residual income £31.8 million

Note;

Candidates indicating that there is also a cost associated with the on-going costs £40.35 million @10% £4.0 million per annum would be given due credit.

© The Chartered Institute of Management Accountants 2012 Page 18

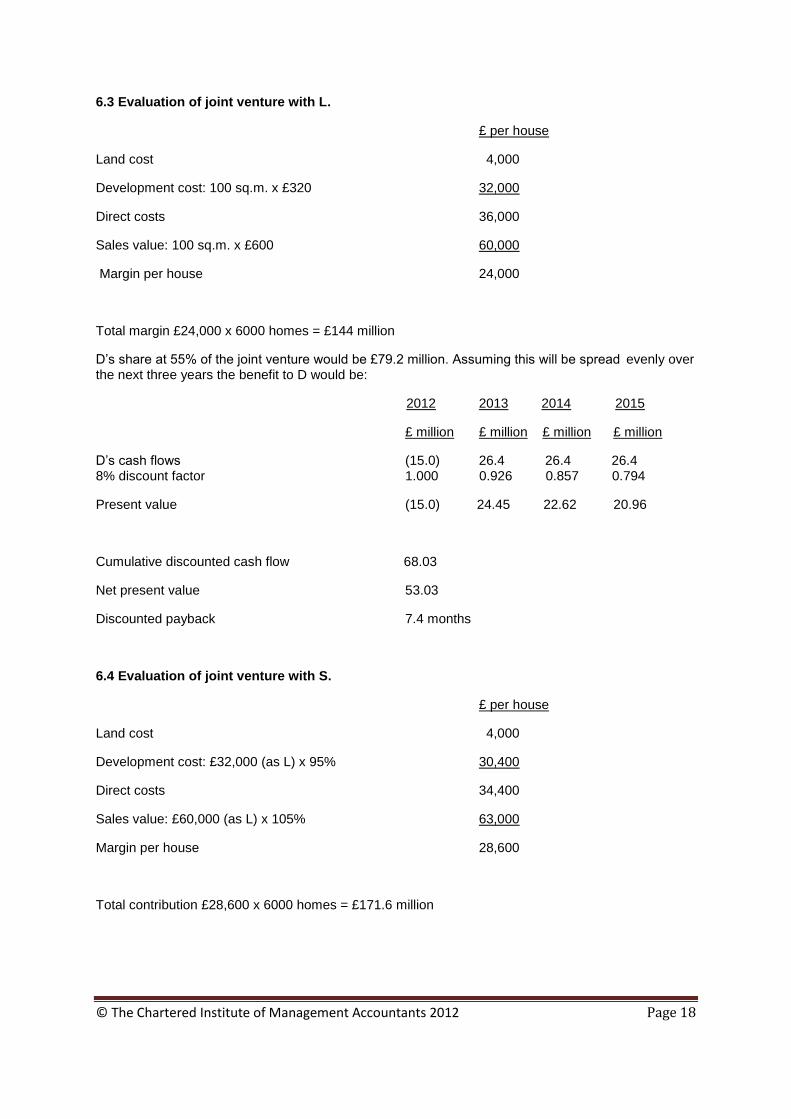

6.3 Evaluation of joint venture with L.

£ per house

Land cost 4,000

Development cost: 100 sq.m. x £320 32,000

Direct costs 36,000

Sales value: 100 sq.m. x £600 60,000

Margin per house 24,000

Total margin £24,000 x 6000 homes = £144 million

D’s share at 55% of the joint venture would be £79.2 million. Assuming this will be spread evenly over the next three years the benefit to D would be:

2012 2013 2014 2015

£ million £ million £ million £ million

D’s cash flows (15.0) 26.4 26.4 26.4 8% discount factor 1.000 0.926 0.857 0.794

Present value (15.0) 24.45 22.62 20.96

Cumulative discounted cash flow 68.03

Net present value 53.03

Discounted payback 7.4 months

6.4 Evaluation of joint venture with S.

£ per house

Land cost 4,000

Development cost: £32,000 (as L) x 95% 30,400

Direct costs 34,400

Sales value: £60,000 (as L) x 105% 63,000

Margin per house 28,600

Total contribution £28,600 x 6000 homes = £171.6 million

© The Chartered Institute of Management Accountants 2012 Page 19

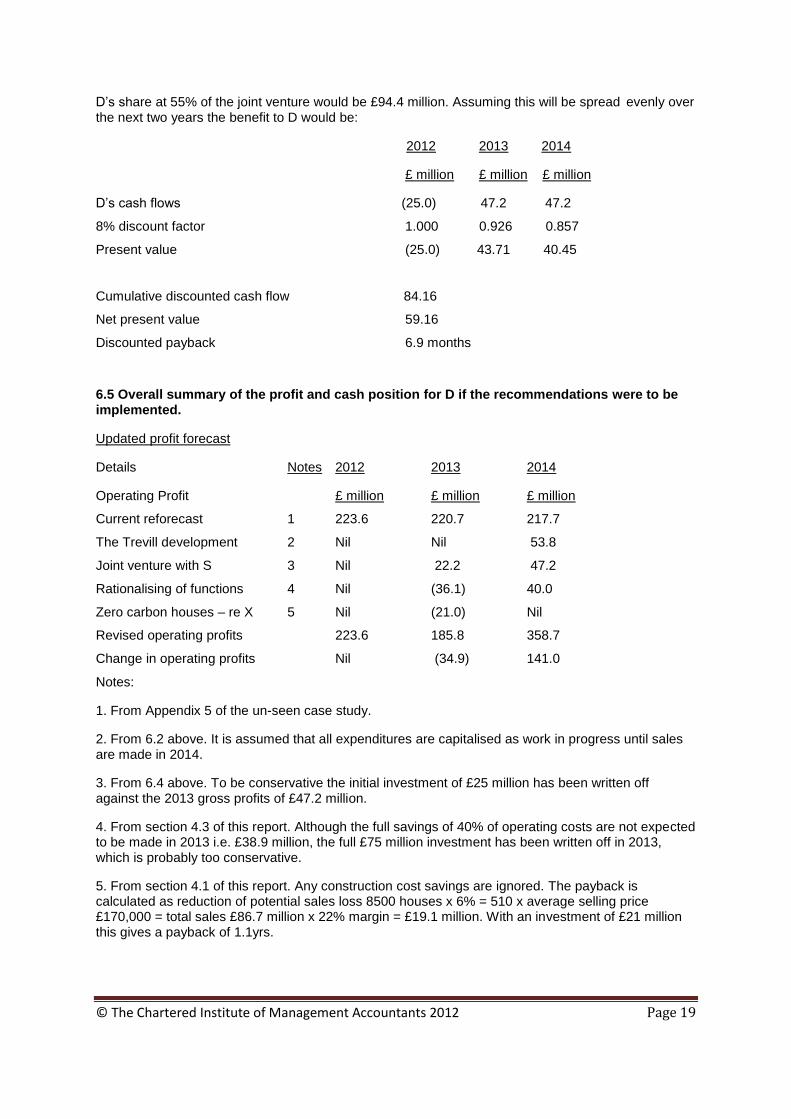

D’s share at 55% of the joint venture would be £94.4 million. Assuming this will be spread evenly over the next two years the benefit to D would be:

2012 2013 2014

£ million £ million £ million

D’s cash flows (25.0) 47.2 47.2

8% discount factor 1.000 0.926 0.857

Present value (25.0) 43.71 40.45

Cumulative discounted cash flow 84.16

Net present value 59.16

Discounted payback 6.9 months

6.5 Overall summary of the profit and cash position for D if the recommendations were to be implemented.

Updated profit forecast

Details Notes 2012 2013 2014

Operating Profit £ million £ million £ million

Current reforecast 1 223.6 220.7 217.7

The Trevill development 2 Nil Nil 53.8

Joint venture with S 3 Nil 22.2 47.2

Rationalising of functions 4 Nil (36.1) 40.0

Zero carbon houses – re X 5 Nil (21.0) Nil

Revised operating profits 223.6 185.8 358.7

Change in operating profits Nil (34.9) 141.0

Notes:

1. From Appendix 5 of the un-seen case study.

2. From 6.2 above. It is assumed that all expenditures are capitalised as work in progress until sales are made in 2014.

3. From 6.4 above. To be conservative the initial investment of £25 million has been written off against the 2013 gross profits of £47.2 million.

4. From section 4.3 of this report. Although the full savings of 40% of operating costs are not expected to be made in 2013 i.e. £38.9 million, the full £75 million investment has been written off in 2013, which is probably too conservative.

5. From section 4.1 of this report. Any construction cost savings are ignored. The payback is calculated as reduction of potential sales loss 8500 houses x 6% = 510 x average selling price £170,000 = total sales £86.7 million x 22% margin = £19.1 million. With an investment of £21 million this gives a payback of 1.1yrs.

© The Chartered Institute of Management Accountants 2012 Page 20

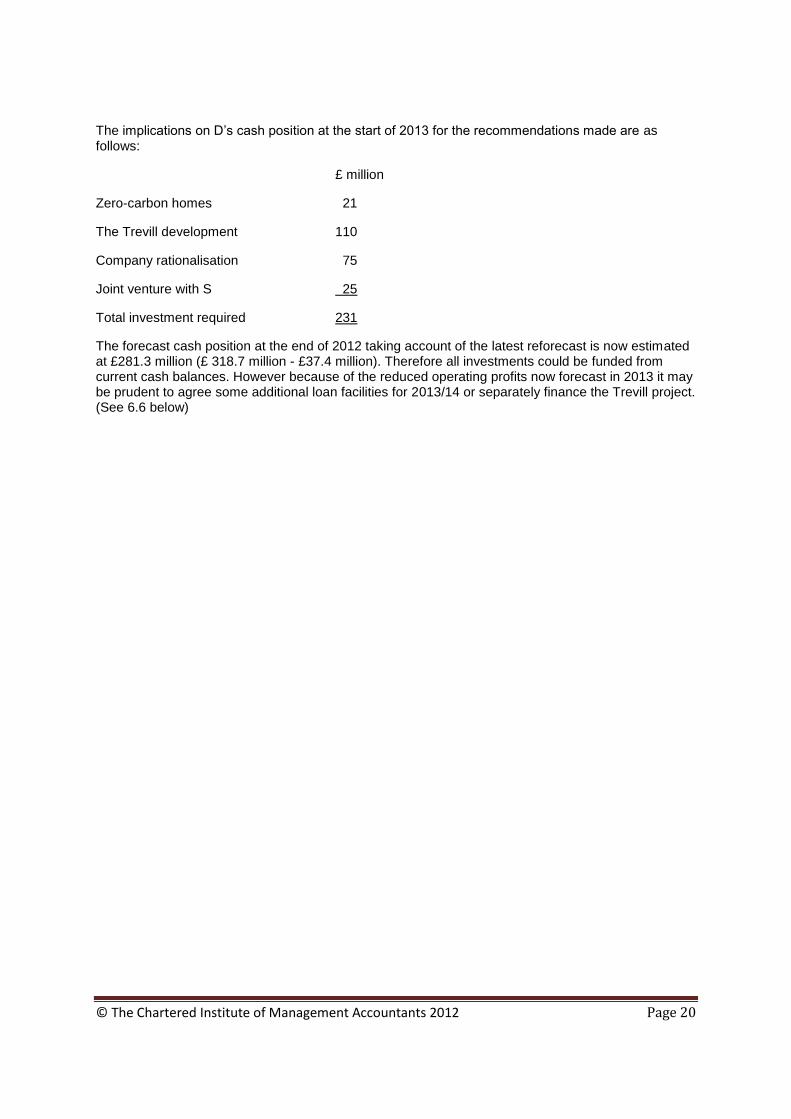

The implications on D’s cash position at the start of 2013 for the recommendations made are as follows:

£ million

Zero-carbon homes 21

The Trevill development 110

Company rationalisation 75

Joint venture with S 25

Total investment required 231

The forecast cash position at the end of 2012 taking account of the latest reforecast is now estimated at £281.3 million (£ 318.7 million - £37.4 million). Therefore all investments could be funded from current cash balances. However because of the reduced operating profits now forecast in 2013 it may be prudent to agree some additional loan facilities for 2013/14 or separately finance the Trevill project. (See 6.6 below)

© The Chartered Institute of Management Accountants 2012 Page 21

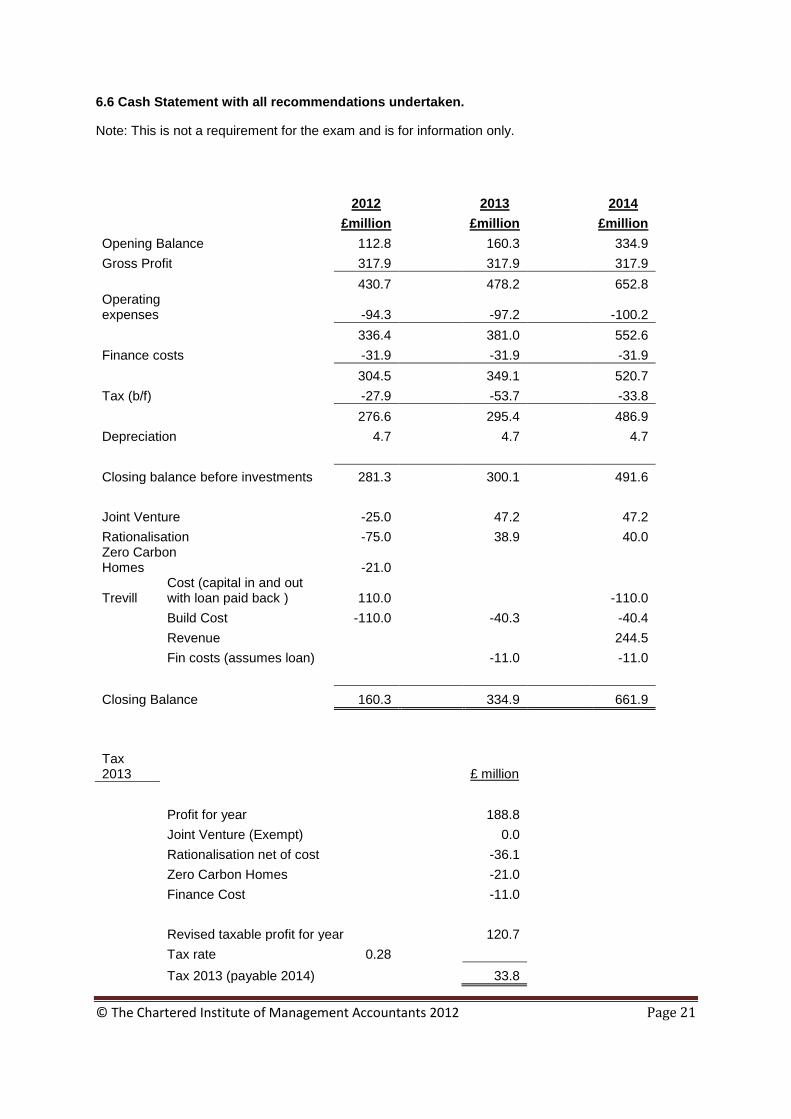

6.6 Cash Statement with all recommendations undertaken.

Note: This is not a requirement for the exam and is for information only.

2012

2013

2014

£million

£million

£million

Opening Balance

112.8

160.3

334.9

Gross Profit

317.9

317.9

317.9

430.7 478.2 652.8

Operating expenses

-94.3

-97.2

-100.2

336.4 381.0 552.6

Finance costs

-31.9

-31.9

-31.9

304.5 349.1 520.7

Tax (b/f)

-27.9

-53.7

-33.8

276.6 295.4 486.9

Depreciation

4.7

4.7

4.7

Closing balance before investments 281.3 300.1 491.6

Joint Venture

-25.0

47.2

47.2

Rationalisation

-75.0

38.9

40.0 Zero Carbon Homes

-21.0

Trevill

Cost (capital in and out with loan paid back ) 110.0

-110.0

Build Cost -110.0

-40.3

-40.4

Revenue

244.5

Fin costs (assumes loan)

-11.0

-11.0

Closing Balance

160.3 334.9 661.9

Tax 2013

£ million

Profit for year

188.8

Joint Venture (Exempt)

0.0

Rationalisation net of cost

-36.1

Zero Carbon Homes

-21.0

Finance Cost

-11.0

Revised taxable profit for year

120.7

Tax rate

0.28

Tax 2013 (payable 2014)

33.8

© The Chartered Institute of Management Accountants 2012 Page 22

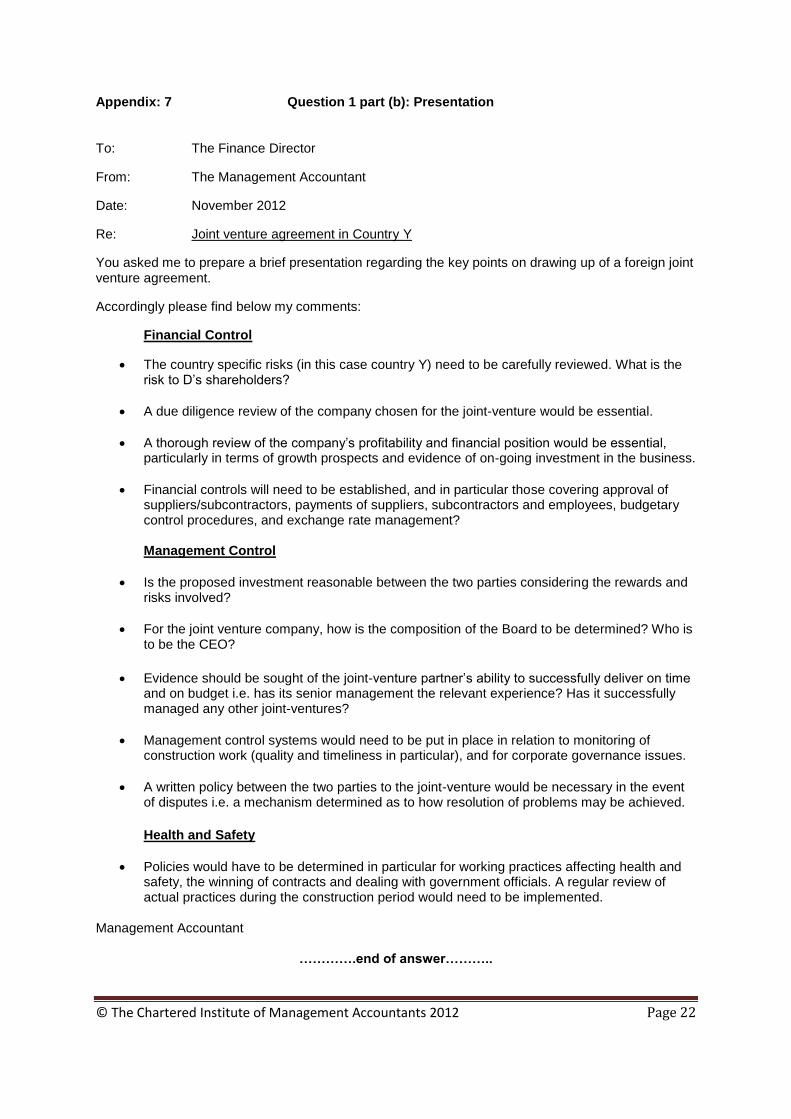

Appendix: 7 Question 1 part (b): Presentation

To: The Finance Director

From: The Management Accountant

Date: November 2012

Re: Joint venture agreement in Country Y

You asked me to prepare a brief presentation regarding the key points on drawing up of a foreign joint venture agreement.

Accordingly please find below my comments:

Financial Control

The country specific risks (in this case country Y) need to be carefully reviewed. What is the risk to D’s shareholders?

A due diligence review of the company chosen for the joint-venture would be essential.

A thorough review of the company’s profitability and financial position would be essential, particularly in terms of growth prospects and evidence of on-going investment in the business.

Financial controls will need to be established, and in particular those covering approval of suppliers/subcontractors, payments of suppliers, subcontractors and employees, budgetary control procedures, and exchange rate management? Management Control

Is the proposed investment reasonable between the two parties considering the rewards and risks involved?

For the joint venture company, how is the composition of the Board to be determined? Who is to be the CEO?

Evidence should be sought of the joint-venture partner’s ability to successfully deliver on time and on budget i.e. has its senior management the relevant experience? Has it successfully managed any other joint-ventures?

Management control systems would need to be put in place in relation to monitoring of construction work (quality and timeliness in particular), and for corporate governance issues.

A written policy between the two parties to the joint-venture would be necessary in the event of disputes i.e. a mechanism determined as to how resolution of problems may be achieved.

Health and Safety

Policies would have to be determined in particular for working practices affecting health and safety, the winning of contracts and dealing with government officials. A regular review of actual practices during the construction period would need to be implemented.

Management Accountant

………….end of answer………..