Embed Size (px)

Citation preview

TableofContents

LittleBookBigProfitsSeriesTitlePageCopyrightPageForewordIntroduction

TheNewNormalDollarDowner

DiscoDays?GetReal

ChapterOne-CallingonCommodities

TradingPlacesYeah,But...WaitaMinuteRicochetABulgingMiddleADecadeofDecline

BondBluesTheHouseIsA-Rockin’WhatAmIMissing?

ChapterTwo-Gettin’Goin’

DumbLuckGoAlongtoGetAlongReadytoRockn’Roll?ManagingtheFutureCompanyMan

ChapterThree-Gusher

BigOilToErrIsHumanFromRussiawithLoveHaveWeReachedthe

Peak?HopeSpringsEternalShiftingSandsDeclineThatGreatSucking

SoundSecondComing?

Fill’ErUpNiceWheelsCrackShackSlickOperatorsPetrolProfits

ChapterFour-DrillingforDollars

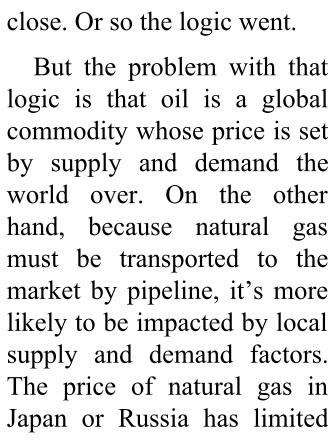

BeCarefulWhatYouWishForFromImportTerminals

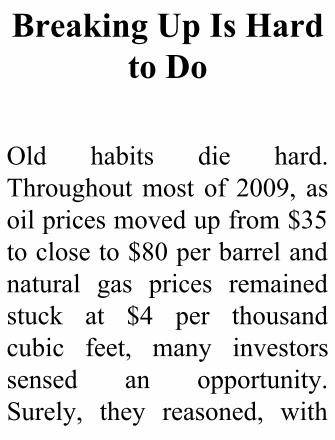

toAirportTerminalsWeatherBetsAPipelineofProfitsMethaneManGasGlutBreakingUpIsHardto

DoDrillingforDollars

ChapterFive-GoingforGold

AwashinDebtStartthePressesAGoldenEraTheGoldenRulesMoneyintheBankBaubles,Bangles,and

BlingBillionDollarBabyMyTwoCentsTheFamilySilverSilverLiningTheSilverScreenPlatinum:TheNewGold

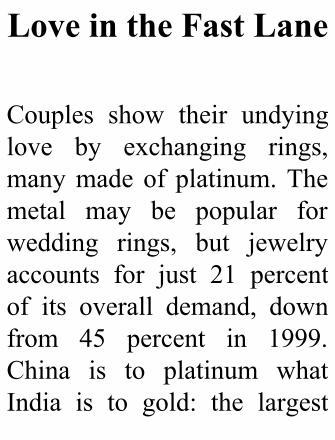

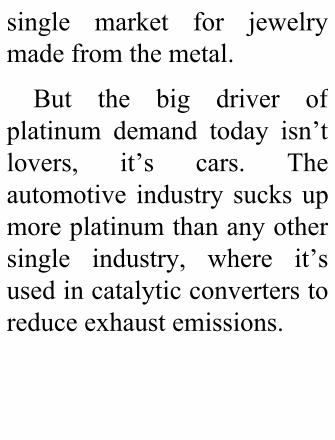

LoveintheFastLaneMetalMeddling?HammerandSickleBlingFling

ChapterSix-DiggingIt

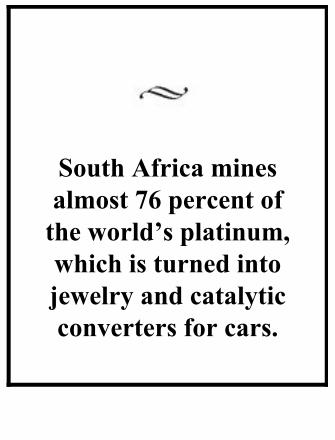

KerplunkHeavyMetalsMetalFatigueOutofAfricaThe800-PoundGorilla

LondonCallingSpringingaLeak?NukeRebootMetalMania

ChapterSeven-BettingtheFarm

FoodFightLandGrabGoingGreen?ThisLittlePiggyWent

toMarketNothingRunsLikea

DeereMoneyinManure?DustBunnyRoundup

ChapterEight-OrderingtheBreakfastSpecial

ReadyforaPerkUp?SugarHigh

FromGrovetoGlassDecadentDelightWhenPigsFlyAPlatefulofProfits

ChapterNine-GaininginGrains

FoodforThoughtSeedsofDoubtYouReapWhatYou

Sow

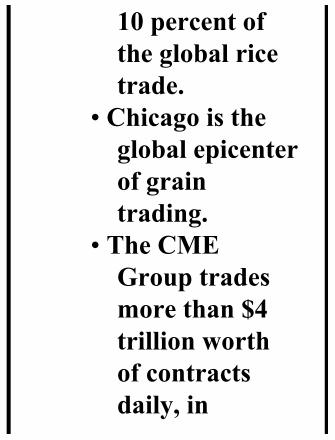

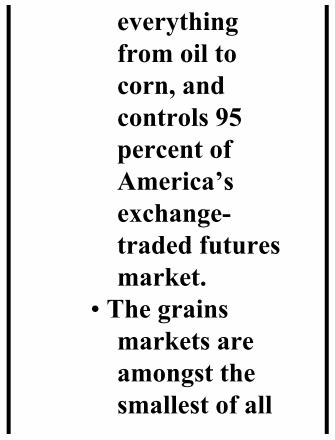

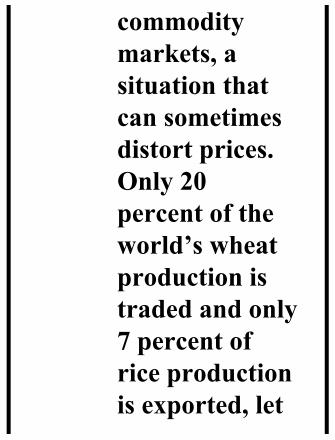

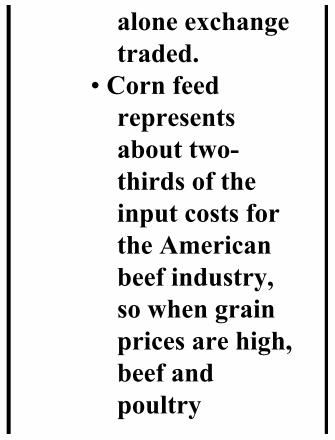

SweetHomeChicagoChicagoBullsGrainandBearItFoodChainWeatherReportPlowingforProfits

ChapterTen-BulkUp

CheapThrillsFireandBrimstoneGrowthinGirders

EntertheDragonLettheGoodTimesRollGristfortheMillRiskyBusinessSootandSuccessG’DayMateShipsAhoyForgettheFuture

ChapterEleven-CapitalizingonCommodities

MaxedOutBeltTighteningAsianAscensionBuyLow,SellHighBonanza

LittleBookBigProfitsSeries

IntheLittleBookBigProfitsseries, the brightest icons in

the financial world write ontopics that range from tried-and-trueinvestmentstrategiesto tomorrow’s new trends.Each book offers a uniqueperspective on investing,allowing the reader to pickandchoosefromtheverybestininvestmentadvicetoday.

Books in theLittleBookBigProfitsseriesinclude:

The Little Book That Beats

theMarketbyJoelGreenblatt

The Little Book of ValueInvesting by ChristopherBrowne

The Little Book of CommonSense Investing by John C.Bogle

The Little Book ThatMakesYouRichbyLouisNavellier

The Little Book That BuildsWealthbyPatDorsey

The Little Book That SavesYour Assets by David M.Darst

The Little Book of BullMoves in Bear Markets byPeterD.Schiff

The Little Book of MainStreet Money by JonathanClements

The Little Book of SafeMoneybyJasonZweig

The Little Book ofBehavioral Investing byJamesMontier

The Little Book of BigDividends by Charles B.Carlson

The Little Book of InvestingDo’sandDon’tsbyBenSteinandPhilDeMuth

The Little Book of BullMoves, Updated andExpandedbyPeterD.Schiff

The Little Book ofCommodity Investing byJohnStephenson

Copyright©2010byJohnStephenson.Allrightsreserved.

PublishedbyJohnWiley&Sons

Canada,Ltd.

Theviewsexpressedinthisbookare

thoseoftheauthoranddonotnecessarilyreflecttheviewsofFirstAssetInvestmentManagementInc.or

anyofitsaffiliates.

Allrightsreserved.Nopartofthisworkcoveredbythecopyrighthereinmaybe

reproducedorusedinanyformorbyanymeans—graphic,electronicormechanicalwithoutthepriorwrittenpermissionofthepublisher.Any

requestforphotocopying,recording,tapingorinformationstorageandretrievalsystemsofanypartofthis

bookshallbedirectedinwritingtoTheCanadianCopyrightLicensingAgency(AccessCopyright).ForanAccess

Copyrightlicense,visitwww.accesscopyright.caorcalltollfree

1-800-893-5777.

LimitofLiability/Disclaimerof

Warranty:Whilethepublisherandauthorhaveusedtheirbesteffortsin

preparingthisbook,theymakenorepresentationsorwarrantieswith

respecttotheaccuracyorcompletenessofthecontentsofthisbookandspecificallydisclaimanyimplied

warrantiesofmerchantabilityorfitnessforaparticularpurpose.Nowarrantymaybecreatedorextendedbysalesrepresentativesorwrittensales

materials.Theadviceandstrategiescontainedhereinmaynotbesuitableforyoursituation.Youshouldconsultwith

aprofessionalwhereappropriate.Neitherthepublishernorauthorshallbeliableforanylossofprofitoranyothercommercialdamages,includingbutnotlimitedtospecial,incidental,

consequential,orotherdamages.

Wileyalsopublishesitsbooksinavarietyofelectronicformats.Some

contentthatappearsinprintmaynotbeavailableinelectronicbooks.FormoreinformationaboutWileyproducts,visit

ourwebsiteatwww.wiley.com.

LibraryandArchivesCanadaCataloguinginPublication

Stephenson,John,1962-

Thelittlebookofcommodityinvesting

/JohnStephenson.ISBN978-0-470-67837-4

1.Commodityfutures.2.Commodityexchanges.3.Finance,Personal.I.

Title.HG6046.S.63’28C2010-901888-5

CW

Foreword

PLANNINGFORTHEENDGAME. “May you live ininteresting times” wassupposedly an ancientChinese curse. Historiansreally only write about the

greatevents,usuallydisastersandwars,asthereisnotmuchofinterest inpeaceful,serenetimes. So, if the period youlive in is interesting, it isprobablynotserene;volatilityand the unknown become apartofthefabricoflife.

Unfortunately, as far asinvesting is concerned, welive invery interesting times.As I write this foreword, wehave just come through the

worst financial crisis andmost serious recession sincethe Great Depression. Itappears that the economiesare recovering in the UnitedStatesandAsia,buttherearerumblings that things mightnot be so good in theEurozone. Many of itseconomies are in recessions,ranging frommild to severe,and the credibility of thesovereign debt of the Club

Medcountriesisindoubt.

Indeed, just as we lurchedfrom one bubble to anotherover the past decade, we arerapidly approaching theburstingofthenextbubble—thatof sovereigndebt.Whileconsumersandbusinessesareretrenching and the world ofprivatedebtisinvolvedintheGreat Deleveraging,governments around theworld are running massive

deficits as they try tostimulate their economies inthe face of unemploymentand slack demand. But thereis a limit to the amount ofmoney they can borrow andto the interest rates theywillbeabletopay,astheturmoilinGreece and the rest of theMediterranean demonstrates.Even Japanwill find there isalimit.

And we are rapidly

approaching that limit. Asinvestors, we must nowcontemplate The End Game.What will the investmentclimate be when thedevelopedworld is forced todeleverage? For somecountries,itwillbedeflation.Forothers,itwillbeinflation.You can count on majorcurrency fluctuations.Recessions will come moreoften andbemorepersistent.

Unemployment will remainuncomfortably high. Interestrates?Expect themtobe lowuntilmarkets loseconfidenceintheabilityofagovernmenttorepayitsdebt.

As Reinhart and Rogoffwrote: “Highly indebtedgovernments, banks, orcorporations can seem to bemerrily rolling along for anextended period,when bang!—confidence collapses,

lendersdisappear,andacrisishits.”

Bangistherightword.Itisthenatureofhumanbeingstoassume that the current trendwill work out, that thingscan’treallybeasbadas theyseem.Comparehowthebondmarkets looked only a yearagowithhowtheylookedjusta few months before WorldWar I. Therewas no sign ofan impending war. Everyone

thought that cooler headswould prevail. In a similarvein, just prior to the recentcredit crisis, bond markets(andindeedallothermarkets)around the world were notsignalingthattheworstcreditcrisisin70yearswasabouttoemerge. And then overnight,so it seemed, the bankingmarkets collapsed. Bang,indeed.

Wecanlookbacknowand

seewherewemademistakesin the current crisis. Weactually believed that thistime was different, that wehad better financialinstruments, smarterregulators, and that we wereso,well,modern.Timesweredifferent. We knew how todeal with leverage.Borrowingagainstyourhomewas a good thing. Housingvalues would always go up,

andsoon.

Now, there are voicestelling us that things areheaded back to normal.Mainstream forecasts forGDP growth this year arequite robust, north of 4percentfortheyear,basedonevidence from pastrecoveries. However, theunderlying fundamentalsof abanking crisis are fardifferent from those of a

business-cycle recession. Ittypically takes years toworkoff excess leverage in abanking crisis, withunemployment often risingforfouryearsrunning.

So, John, this is all veryinteresting, but what does ithave to do with a book oncommodities?Everything.

Wehavejustgonethrougha lost decade for the stock

markets in the United Statesand much of the developedworld. What worked for somany years no longer does,yetmany investorspersistonputtingthebulkoftheirassetsinequities.TheenvironmentIhave described above is onein which equities and indexfunds (which are the mainway investors invest inequities) will struggle,offering nowhere near the

toutedlong-termaverages.

Indeed,ifyouwentbackto1966and invested in20-yearU.S.governmentbonds,yourbond portfolio would haveoutperformed the stockmarketoverthenext43yearsthrough the end of 2009.Stocks for the long run,indeed.

Whatthatsaystomeisthatinvestors should look for

ways to diversify theirportfolios away from thecurrent over-allocation tostocks. And one way to dothat is through commodityinvesting. But simply buyinga fund tied to somecommodity aggregate indexisn’t the answer. And that’swhere this book by JohnStephensonwillbesouseful.

To be a successfulcommodity investor takes

knowledge—as muchknowledge as (or even morethan) it takes to be asuccessful stock investor.While a pound of aluminum,iron, or nickel is the sameanywhere, the price canchange based upon demand.Thepriceofabushelofcornreflects not only the demandfor tortillas, but also thedemand for ethanol. Andeverything is complicated by

theworldeconomy,becauseagrowingAsiawillneedmoreenergy and food, even as thedeveloped world struggles tofindthatsamegrowth.Whichfactors will have moreinfluence?

Once you have made thedecision about pricedirection, there are manyways to invest incommodities. Stephensonhelps you work through the

pitfalls and advantages ofvariousfundsandstyles.

While I think thedeveloped world is in for aMuddle-Through Economy,there are so many ways thatindividual investors canprosper—even in a sidewaysworld. They need only tolook beyond the traditionalportfolioandexplore the restoftheinvestmentcornucopia.Volatilityandnimblenesswill

bringyouopportunity.

Arm yourself with thebasicknowledgethatisinthisbook,thendigdeepandlearnmore. And as my friendDennisGartmansays:

Good Luck and GoodTrading!

JohnMauldin

JohnMauldin (Dallas,TX)is the President of

Millennium WaveInvestments. One of theworld’smostreadinvestmentanalysts, his free weekly e-letter Thoughts from theFrontlineisreadbymorethana million people each weekand is reprintedonnumerousWeb sites. Mauldin is alsoauthor of the bestsellingbooks Bull’s Eye Investing(978-0-471-65543-5)andJustOne Thing (978-0-471-

73873-2).

Introduction

THE NEXT GREAT BULLMARKET HAS ARRIVEDand it’s not in real estate,bonds, or stocks, but incommodities. After thegreatest financial collapse in

more thanagenerationandadecadeofdeclinefortheS&P500stockindex,commoditiesstandalone as theonlygo-tosectorofthemarket.Bestyet,commodities are an indirectplayontheonlyregionoftheworld that is experiencingexplosiveeconomicgrowth—Asia.

Theheavily indebtedWestfaces years of sluggishgrowth and a dismal outlook

for job seekers. But forcommodities the story isdecidedly more upbeat,because commodities are thebasic raw materials ofurbanization andindustrialization. Today,hundreds of millions ofpeople are rising out ofextreme poverty and, for thefirst time in recordedhistory,becoming global consumers,a good news story for

commodities.

TheNewNormal

Consumers in the West hadenjoyed amore than 20-yearbonanza, one where realestatepricessteadilyclimbed,interest rates fell, andemployment prospects weregood.But today, in thewake

of the global financial crisisof 2008-2009, mostconsumersaredeeply indebtand so too are theirgovernments. Governmentsaroundtheworldhavepouredtrillions of dollars intostabilizing their nationaleconomies, yetunemployment rates remainhigh in the West andeconomic growth is tepid.Western economies are in

rehabaftera20-yearrunonadebt-fueledbender.Recoveryis likely to be painful andslowastheseeconomiesshedthe bad habits of racking uptoomuchdebtandsavingtoolittle.

Conversely, Asia’seconomy is rising and theprospectsforcommoditiesarerising along with it. ChinaandIndiawentintotheglobalfinancial crisis of 2008-2009

inmuchbettershapethantheWest.Theseemergingmarketeconomies had much lowerlevelsofnationaldebt,lotsofforeign currency reserves,and consumer sectors thatwere in their infancy. At thebeginningof2010,Chinahada total debt to GDP ratio of159percent,whiletheUnitedKingdom’s was an eye-popping 466 percent—anearlythreefolddifference.Is

it any wonder that Asia’sgrowth remains unrestrained,while Western growth issluggish?

The investmentopportunities of the futurewill increasingly come fromthe fast-growing economiesof Asia, not the stalwarts oftheWest.Andthat’sgoodforcommodities, the real stuffthat makes economicexpansionpossible.TheWest

hasgorgedon toomuchdebtfortoolong.Therepercussionofthisbingeingwillbeyearsof slower than normaleconomic growth as theeconomies of the West arerebuilt. Between 2000 and2009, U.S. stock marketreturns were negative andjoblessnessrosedramatically.

While economic growth intheWesthasbegun,it’sbeingdriven by the government

sector rather than bycorporations or consumers.The unemployment rateremains stubbornly high andconsumersaresittingontheirwallets, terrified of gettingwalloped again. Can thetraditional investmentmix ofstocks,bonds, and real estatereally be expected tooutperform in this low-growthenvironment?

Inalow-growthenvironment,canthetraditional

investmentmixofstocks,bonds,andrealestatereallybe

expectedtooutperform?

Nope. During the 1970s,commodities roared whilestocks and bonds wentnowhere.During thatdecade,America was strong, Europewas reemerging as an engineof global growth, and theeconomies of South Korea,Japan, and Taiwan were onthe move. This time around,four-fifths of the world’spopulation is emerging from

an economic funk—creatinghundreds of millions of newglobal consumers. Demandfor commodities continues tosurge. There are nosubstitutes for these criticalfeedstocksofindustrializationand urbanization, and supplyremains constrained. Apowerful rallying crywill beheard around the world asinvestorsclamortobepartofthe next great bull market—

not in stocks, bonds, or realestate, but rather, incommodities.

DollarDowner

Helping to propel the bullmarketincommoditieshigherareanAmericandollar that’ssagging under the weight ofpersonal and government

debt, which are in nosebleedterritory, and investors’ fearthat the Federal Reserve (theFed) will be forced to crankup the printing press to paydownthenation’sdebt.

Record low interest ratesand a national balance sheetthat looks positively sickly,with no immediate prospectsfor improvement, haveconspired to drive the dollarlower.Andthat’sbeenaboon

for commodities—which arepriced in U.S. dollars—asinvestorscorrectlyreasonthatthe value of tangible assetscannot be inflated away.Theworldmayonedaybeawashin American dollars, but theamount of copper incirculationisfinite.

To combat the recessionand get consumers spendingagain,UncleSamhasshotthelocks off his wallet—

spending money like adrunkensailoronshoreleave.And with trillions ofadditional dollars hitting thenation’s money supply,China,our largestcreditor, isworried. Already they’vepubliclyvoicedtheirconcernsoverthedirectionthedollaristaking and its potentialimpact on their foreigncurrency reserves. If Chinaever decides that holding

mostofitsreservesinrapidlydeclining U.S. dollars andreceivingapaltryinterestratein return is a bad deal—lookout.Were theBankofChinatoshift15or20percentofitsreserves into gold, or anyotherhardasset, instead—thedollarwouldimmediatelyfallsharplylower.

DiscoDays?

Discoandcommoditiesshareone thing in common: theyboth had their heyday in the1970s. During that decade,while the stock market andthe economy went nowhere,commodities were on fire—and so too was inflation.Millions of middle-classAmericanbabyboomerswereentering the workforce,starting families, and buyinghouses, cars, and appliances

—thestagewassetforalongbull run in commodities.Germany and Japan werereindustrializing after theSecond World War, and agrowing global middle classwas demanding houses, cars,and appliances—allcommoditydependent.Allofthis helpedmake commodityinvestingtheplacetobefrom1968to1982.

This demand for essential

goods helped drive inflationhigher. As basic rawmaterials, commodities aredirectly linked to thecomponents of inflation,making them ideal inflationhedges. Inflation erodes thevalue of a bond and stockportfolio, but not acommodity portfolio. Highlevels of inflation areassociated with boomingeconomies and surging

demand for commodities.Strong demand forcommodities translates intohigherpricesforthem,whichmore than offsets the effectsof inflation. As a result,commodities providepurchasing power protection.That’s important, becauseinvestorscareabouttheirreal—or inflation-adjusted—purchasingpower.

Commodities,asbasicraw

materials,aredirectlylinkedtothecomponentsofinflation,making

themidealinflationhedges.

Today,many of our banksare a mess, and both theconsumer and the Americangovernment face years ofpainful deleveraging as theytry to work off the excessesofadebt-fueledbender.Withgovernmentandconsumersindebt up to their eyeballs, theprospect of a slow-growingeconomy looks increasinglylikely. This economic

restraint will slowinvestment, profits, andpayments to investors in theform of dividends andinterest. As America, andmuch of the West, enters aslow-growth era, buying abasket of S&P 500 stockslooks increasingly like asucker’s bet. Commodities,fueled by the fast-growingeconomiesofAsia,shouldbethego-tosectoroverthenext

decade. Bell bottoms anddisco may never stage acomeback, but we may begoing back to an investmentclimate like the 1970s,whencommodities soared and justabouteverythingelsetanked.

Whilebell

bottomsanddiscomaynotbeyourthing,wemaybegoingbacktoan

investmentclimatelikethe1970s,whencommodities

soaredandjustabouteverythingelsetanked.

GetReal

There aremany things that Ienjoyaboutbeingaportfoliomanager,butImostenjoythetimeswhenIget to leavemyspreadsheetsbehindandheadoutoftheofficetoseetheoilfields, mines, shippingterminals, and natural gasplants that dot the landscape.Thefeelingisthesameeverytime I venture beyond my

computer screens: I alwaysmarvelatthesize,scope,andtechnical complexityof theseoperations and at the critical,yet unheralded, role theseassets provide in making theworldwork.

In spite of the crucial rolecommodityproducersplay inenablingtheglobaleconomy,most of us know almostnothingaboutthem;andwhatwe do know is often

jaundiced. In a world ofglitzy new product launchesand expensive marketingcampaigns, the world ofindustry seems woefully outof date. Yet we have justlived through an era whereWall Street and its world-class marketers badly misledtheinvestingpublicabouttheriches that lay ahead incutting edge technology andhighfinance.

Commodities can soarwhen stocks and bonds aregoing nowhere and inflationis running amok. In a worldof too much complexity andtoo few solutions, investorsare looking for somethingsimple, something tangible,where the accounting isn’tflawed and the path forwardis clear. As real things thatyou can hold and touch,things thatyouuseeveryday,

commodities seem to be thesolid store of value in thesetroubledtimes.

Best yet, armed with aknowledge of commoditiesyou will be better able tounderstand markets, wholeeconomies, and the world inwhichwe live.More than aninteresting niche area ofinvesting, commoditiesprovide uswith an importantwindow on the world of

investing and understandingthemtransformsusintobetterinvestors; not just bettercommodity investors, butbetterstock,bond,realestate,currency, and emergingmarketinvestors.

Mostinvestmentbooksarelong on theory but short onpractical no-nonsenseinformation and knowledgefrom which you can profit.This book is different. This

book is about companies,about whole industries, andaboutavaluechainthatspansthe globe and interconnectsthemarketsoftomorrowwiththe markets of today. Thisbook explains the worldaround us—how it works,whatmakesmarkets rise andfall,andhowyouasinvestorscan come out ahead of thepack.

The tried and true

investment path led manyinvestors to ruin in the2008-2009 market collapse. Whatworked before is unlikely towork again. The world haschanged and so too hasinvesting. Commodities zigwhen stocks and bonds zag,and thisoften-overlookedbutcrucial part of the investinglandscape is finally about togetitsdue.

Thisbookisyourblueprint

for navigating the world ofcommodities—the world oftomorrow. Itexamineswholeindustries, how they fittogether in thebiggerpuzzle,andwhatmakes them tick. Itexplores the worlds ofagriculture, mining, andenergy, as well as thecharacters and countriesbehind the production andconsumption of these criticalraw materials. You’ll learn

the various ways investorscan get commodity exposureandwhy thesebetsare likelyto be savvy rather thanfoolhardy.

Commodities are alreadypart of your daily routine—from the coffee that powersyou throughyourmorning tothe gas that fuels your car.And from the farmer’s fieldtothefoodonyourtable,theworld of commodities is

global and interlinked.Developments halfway roundthe world can have a bigimpact on the action in thetrading pits of Chicago andon your portfolio. In short,commodities are a vitallinchpin connecting marketsand providing powerfulsignalsabout thedirectionofthe world economy and thestockmarket.

And yet, they just don’t

figure as part of mostinvestment portfolios. Thisbookwill change that. Itwilldispel the myths aboutcommodities and make twobold claims—thatcommodities belong in everyportfolio and that you ignorecommodities at your owninvestmentperil.

The goal of this book issimple—to sweep away themystery surrounding

commodities and exposethem for what they are—thesinglebestassetclass for thenextdecade.

ChapterOne

CallingonCommodities

WhyCommodityInvestingIsaSavvyBet

A MASSIVE BULLMARKET INCOMMODITIES is about towash up on our shores,powerednotbythestagnatingWest, but by a surgingAsia.The big money of the nextdecade won’t be made inbonds or real estate, andcertainly not in the so-called

U.S.bluechipstocks—itwillbe made in commodities.Savvy investors know thatfollowing global growthwhereit’sgoing—asopposedto where it’s been—is thewinning bet. And aseconomicinfluencecontinuesto shift toward the East, thesmart money is investing inthe basic raw materials thatsupport economic growth—commodities.

A rapid reordering of theglobal economic peckingorder is underway. In 1987,one-third of the world’seconomic output came fromdeveloping economies andtwo-thirds came fromdevelopedeconomies.By theend of 2009, theircontributions were evenlysplit. By 2020, two-thirds oftheworld’seconomicactivitywill come from developing

economies, while the so-calledricheconomieswillberesponsibleforjustone-third.Thepaceofeconomicchangewe are witnessing is bothunparalleled andunprecedented.

By2020,two-thirdsof

theworld’seconomicactivitywillbecoming

fromdevelopingeconomies,whilethe

so-calledricheconomieswillberesponsibleforjust

one-third.

Commodities are realthings that we rely on everyday.Fromthetimewegetup

to the timewego tobed,weare surrounded bycommodities. The coffee wedrink and the sugar wesweeten it with arecommodities, so too are thesteel that holds our carstogether, the oil that makesthemrun,andthenaturalgasthatheatsourhomes.

Nothing aboutcommodities is bush-league;in2009,theproductionvalue

of seven of the mostimportant commodities wasnorth of $3.6 trillion. Thevalue of the commoditiestraded on theworld’s futuresexchanges dwarfs the dollarvolume of transactions onU.S. stock exchanges.Commodities and theexchanges that setpricesandmarry up buyers and sellersofthesecrucialrawmaterialsare so important to our way

of life that the world as weknow it just wouldn’t bepossiblewithoutthem.

Thevalueofcommoditiestradedontheworld’sfuturesexchangesdwarfsthedollarvolumeof

transactionsonU.S.stockexchanges.

Plenty of experts willespouse themerits of stocks,thebenefitsofbonds,andtheadvantagesofrealestate.Butwhen it comes tocommodities, there isn’tmuch of a fan club, despitecompelling evidence thatwhen stocks and bonds are

goingdown,commoditiesareusually going up. Wheninflation is heading higherand bonds and stocks areheading lower, commodityprices will be on fire.Commodities have beenproven to boost returns andchop risk in an investmentportfolio, but evensophisticated investors givethem short shrift. For mostinvestors, commodities just

don’tfigure.

TradingPlaces

Commodities trade oncommodityexchanges,wherethey are bought and sold forfuture delivery. The firstcommodity futures tradingcan be traced back to 17thcenturyJapan,wherefarmers

sold rice to local merchantswhostoredityear-round.Notcontent to just sit on theirinventory of rice, themerchants raised cash to payfortheircostsbyselling“ricetickets,” which were receiptsagainst the stored rice. Overtime, the rice tickets becameaccepted as a form ofcurrency and rules wereestablished to manage theirtrade.

Almost 200 years later, in1848, a group of Chicagobusinessmen formed theChicago Board of Trade(CBOT), a member-ownedorganization that offered acentralizedplacefortradingawiderangeofgoods.Withitsconvenient location betweenMidwestern producers andthe east coast market,Chicagowasanaturalhubforcashtradingincommodities.

As time went on, buyersandsellersnegotiateddirectlywithoneanothertosellcropsat an agreed upon price notonlyonthatday,butalsoonafuture date. These negotiatedtransactions, known as“forwardcontracts,”arestillafixture in the world ofcommodities. As trading inforward contracts increased,the CBOT decided that mostdetails could be standardized

tostreamlinethedeliveryandtrading of the contracts.Under thisnewsystem,priceand delivery date would betheonlyvariables.

The standardized contractsthe CBOT ushered in wereAmerica’s first futurescontracts.Allbids,offers,andtransactions were publishedby the exchange, whichincreased the transparencyand popularity of these

marketplaces. Withstandardizedcontracts, itwaseasy to trade commodities.Investors who wanted toprofit from a drought in theMidwestcouldeasilyuse theexchange to buy futurescontracts for wheat, and iftheir views changed, theycould sell their contracts justaseasily.Standardizationwasaboontotrading.

Commodityfuturesarestandardized

contractsthattradeoncommodityexchanges;priceandquantityaretheonlyvariables.

Other futures exchanges

quickly sprang up. TheChicago Butter and EggBoard,foundedin1898,laterbecame known as theChicago MercantileExchange. Kansas City, St.Louis, Memphis, and SanFrancisco all got into the actby forming their owncommodity exchanges; yettoday, Chicago still reignssupreme as the epicenter ofU.S. futures trading.

Globally, there are majorcommodity exchanges inmorethan20countries.

Yeah,But...

Commodities get a bad rap.Inspiteoftheirimportancetotheglobal economy, they areamong the mostmisunderstood of all asset

classes. Bonds, stocks, andreal estate all have plenty offollowers and universalagreement amongst expertsregarding their importancewithin a well-diversifiedportfolio.Butventureintotheworld of commodities, andyou’re into a fringe area ofinvesting whereunderstanding is limited andsuspicionsrundeep.

Inthe1983movieTrading

Places, Eddie Murphy andDanAykroydteamuptoturnthe tables on their formeremployers, Mortimer andRandolphDuke,byplacingawinning bet on commodities.In a single trading session,Louis Winthorpe III(Aykroyd) and Billy RayValentine (Murphy) becomefabulously wealthy whiledestroying the Dukesfinancially. To skeptics,

reversals of fortune like thatare all too common in theworld of commodityinvesting, where volatilityand complexity are the orderoftheday.

But peek behind thecurtain, and most of thecriticismsofcommoditiesjustdon’t hold water. Whilecommodities are morevolatile than bonds, theirvolatilityisaboutthesameas

that of stocks. Commoditieshave no funky accounting,scandalous behavior bymanagement, orincomprehensible off-balance-sheet items that canskewer your financesovernight. The problem withcommodities—if there is one—is the amount of leverageinvestorscanemploy.

Leverageisadouble-edgedsword. It can boost your

returns when prices areheadinghigherandtankyourinvestments when prices aresinking. “Leverage,” usingotherpeople’smoney,isquitecommon. For example,whenyoubuyahouseandtakeouta mortgage, you’re usingleverage. Both stocks andcommodities can be boughtonmargin,butbylawastockbuyer needs to pony up atleast 50 percent of the

purchaseprice.Incommodityinvesting, marginrequirements are skinnier—sometimes as little as 5percent.

Supposeyoudecidetobuycrudeoilcontractswhenoilistrading at $50 per barrelbecauseyouthinkit’smovinghigher. You open a futurestrading account, slap downthe minimum margin of$5,000 per contract and—

presto—you’re instantlycontrolling $50,000 worth ofcrude oil ($50 per barreltimes 1,000 barrels perfuturescontract).Ifoilmovesfrom $50 per barrel to $55per barrel, your position isworth$55,000($55perbarreltimes 1,000 barrels) andyou’ve doubled your moneyand are no doubt feelingpretty smart. But if oil goesfrom $50 to $45 per barrel,

you’ve lost your wholeinvestment. Still feeling sosmart?Idon’tthinkso.

WaitaMinute

TheYaleInternationalCenterfor Finance, in theirworkingpaper Facts and FantasiesAbout Commodity Futures,1concluded that an unlevered

basket of commodity futuresgave as much bang for thebuck as stocks.Not only didfuturesoffersimilarreturnstostocks, but they tended toperformwellwhenstocksandbondsweredoingpoorly.Byadding futures to a well-diversified portfolio, theresearchers found you couldchop risk while boostingreturns—a nifty trick.Because the value of

commodities is tied totangible assets, theyperformedwellininflationaryperiods,ortimeswhenpriceswere rising. Includingcommoditiesinyourportfoliocannotonlyhelpdiversifyit,but may also help youpreserve wealth wheninflation is gobbling away atthe value of your stocks andbonds.

Includingcommoditiesinyourportfoliocannotonlyhelpyoudiversifyit,butalsohelppreservewealthwheninflationis

gobblingawayatthevalueofyourstocks

andbonds.

In a separate study oncommodity returns, IbbotsonAssociates2foundthataddingcommoditiestoaninvestmentportfolio helped to reducerisk and increasediversification by generatingsuperior returns when theywere needed most. Theresearchersconcludedthatallportfolios could be improved

by the addition of a healthydollopofcommodities.

Ricochet

Shell-shocked investorswatched in horror as thecommodity markets tumbledwith the collapse of LehmanBrothers in September 2008.Executives at commodity-

producing companies nearlywent into cardiac arrest astheir share prices cratered,forcing them to slashexpenses just to keep theircompanies afloat—mineswere closed, oil fields werecapped, and steel millsslammedshut.

However, as the globaleconomy picks itself up offthe mat, the demand forcommodities—the stuff that

economic recoveries aremade of—will soar.Commodity production is atime- and capital-intensiveundertaking requiringextensive engineering,environmental, andpermitting procedures beforework can begin. Lead timesfor obtaining most majorpieces of equipment aremeasured in years, notmonths. In addition, a severe

shortage of well-qualifiedpeopleandinvestmentcapitalmeans new sources ofcommodity supply will be alongtimeincoming.Sluggishsupplyandvoraciousdemandhavesetthestageforournextbull market—one that won’tbe in North American realestateorbluechipstocks,butincommodities.

Sluggishsupplyandvoraciousdemandhavesetthestageforournextbullmarket—onethatwon’tbeinNorthAmericanrealestateorbluechipstocks,butincommodities.

ABulgingMiddle

An exploding global middleclass, fueled by global trade,is supplying the liquidhydrogen to the commodityrocket.Overthelast30years,hundreds of millions ofpeoplehavebeenliftedoutofextreme poverty andtransformed into globalconsumers. According to a

recent World Bank report,between1990and2002some1.2 billion people joined theranks of the developingworld’s middle class. Thesepeople are not rich byWestern standards, but arerich enough to leave asubsistence-level life behindand begin to spend. Moreremarkable, the report notedthat four-fifths of thisemerging middle class were

fromAsiaandhalfwerefromChina.

Others have predicted thatthe pace of thismiddle classexpansion will accelerate,likely reaching its zenitharound2018.GoldmanSachsestimates that by 2030 afurther two billion peoplecould join the global middleclass (defined as having ahousehold income in therange of $6,000-$30,000).

Wemay bemoan the declineoftheAmericanmiddleclass,yet researchers at Goldmanhave found that thedistribution of global incomeis becoming more, not less,equal,atrendthatislikelytocontinue. The surge of theworld’s middle class ishappening on anunprecedented scale.Affectingmorethanone-thirdoftheworld’spopulation,the

shift dwarfs the massivetransformation of the globaleconomythatoccurredduringthe19thcentury.

A mass migration isunderway through much ofAsia, as people leave thefieldsinsearchofbetterlivesinthecities.Withmillionsofnew factory workers hittingthe big cities, tremendousdemand is being created for

housing and other crucialinfrastructure. This demandwill underpin the boom incommodities as these newworkers and their familiesbegin to buy appliances,apartments,andcars.Thelastgreat bull market forcommodities lasted from1968to1982,whentheBabyBoom generation was on abuying spree. But this timeround, the scale of the

economic transformationwilleclipse anything we’ve seenbefore.

The key to understandingcommodities is tounderstandChina—a country that for 18of the last 20 centuries hashad the largest economy inthe world. China is alreadythe world’s largest consumerof iron ore, copper, zinc,aluminum,nickel,andcokingcoal. It’s also the second

largestconsumerofcrudeoiland the largest producer ofsteel—byacountrymile.Notonly is China growing at afurious clip, but so too areother emerging economiessuch as the Philippines,Vietnam, India, andMalaysia. Billions of people,all with aspirations like youand me, will demand thechance at a better life—andthat’s a good news story for

commodities.

Thekeytounderstanding

commoditiesistounderstandChina—acountrythatfor18ofthelast20centuries

hashadthelargesteconomyintheworld.

ADecadeofDecline

For investors in America’sbenchmark index, the S&P500, theperiod from2000 to2009 ranks as the worstdecadeinnearly200yearsof

American stock markethistory.Noteventhe10yearsencompassing the GreatDepressionwasasdismalforU.S. investors as the onewehave just witnessed. By thetime2009drewtoaclose,theS&P 500 index finished thedecade 24.1 percent belowwhere it had started—despitehaving two 50-percent-plusup moves. Investors wouldhavebeenbetteroffinvesting

inalmostanythingotherthanthe U.S. stock market.Stuffing theirmoney under amattress for safekeepingwould have been a savviermove than investing in theS&P500.

Forinvestorsin

America’sbenchmarkindex,theS&P500,theperiodfrom2000to2009ranksastheworstdecadeinnearly200yearsofAmericanstockmarkethistory.Stuffingyourmoneyunderamattressforsafekeepingwouldhavebeenasavvier

movethaninvestingintheS&P500.

The world witnessed aseismic shift in economicpowerduringthefirstdecadeof the 21st century. Thefastest growing economy intheAmericasisnolongertheUnited States, but rather,Brazil.Thosewhoinvestedinthe U.S. stock market at theheight of America’s powerarepoorerfortheexperience.

First they suffered throughthepoppingofthetechnologybubble and then the collapseof Wall Street. Globalinvestors fared somewhatbetter but, because U.S.stocks account for almostone-third of world marketcapitalization, they too gotcaught in the downdraft. Atthe start of the 21st century,America’s stock marketcapitalization was more than

$15.1 trillion, but by the endof the decade it stood closerto $13.7 trillion. Over thesame time period, the stockmarketcapitalizationsofbothBrazilandChinasoaredmorethan fivefold while India’sstock market increased morethaneightfold.AndChina,atthe start of 2010, is set toovertakeJapanastheworld’ssecond-largesteconomy.

Worse yet,America enters

2010withoutaworld-leadingmajorindustry.Atthestartofthepastdecade,Americahadtwo industries that werevisible symbols of itseconomic preeminence: hightech and high finance. Bothindustries expanded rapidly,promising to enrich theiremployees, but instead theyimpoverished many. Topromote their industries toinvestors, they relied on the

notion that creativity waslimitless and so too wereprofits. After all, Americanfinance and technologyappeared to be reshaping theworld. America and itspublicly listed companiesbenefited from the globalperception that in all thingsthat mattered most, Americawas simply the biggest andthe best. But by the end of2000, the technology boom

thatmade somanypeople inCalifornia rich had quicklyturned to rot. In the process,SiliconValley becameDeathValley, sinking the state’seconomic hopes andprospects.

After the tech wreck of2000, Wall Street and theworld of high finance stoodalone as the engine for stockmarket growth. When theGlass-Steagall Act, which

separated investmentbankingactivities from commercialbanking, was repealed, WallStreet’s power and influencegrew dramatically. Itsdominance was reflected inits weight and overallimportance in the S&P 500stock index. By the end of2007, the financial servicessector accounted for 40percent of all S&P 500earnings—upsharplyfromits

historical contribution of 15percent.

BondBlues

In the investment game,bondsareoftencharacterizedas the steady performers,great for cranking out solidinvestment returns but not asfleetoffootassexystocks.In

spite of that reputation, overthe last 25 years bondinvestors have had it good—theyearnedgreat returnsandwere exposed to very littlerisk.Thegoldeneraforbondswas the 25 years followingthe 1968-1982 commoditybullmarket.

The 1970s, on the otherhand,wereagreatdecadeforcommodities but not muchelse. Inflation was rampant,

hitting13.3percentinAugustof 1979, and prompting adesperate President JimmyCarter to appoint PaulVolcker to the post ofchairman of the FederalReserve. Only by ratchetingup the benchmark federalfunds rate to a high of 20percent in July 1981 wasVolcker able to tame theinflationbeast.Intheensuingdecadesinterestrateswereon

a steady downward path,settingthestageforamassivebull market in bonds. Wheninterestratesarefalling,bondprices move higher,rewardinginvestorsbygivingthem both capital gains andinterest income. But can thepartycontinue?

No. With interest rates onU.S. government bonds atmulti-decade lows, there’snowhereforbondpricestogo

butdown.Rightnow,centralbanksintheWestarekeepinginterest rates artificially lowin an attempt to breathe newlife into their comatoseeconomies, but eventuallyrateswillhavetorisetostaveoff inflation. And wheninterestratesrise,bondsfall.

WithinterestratesonU.S.government

bondsatmulti-decadelows,there’snowhereforbondpricestogo

butdown.

TheHouseIsA-Rockin’

In2000,awaveofnew,moreaggressive lending practiceshadtakenrootintheU.S.realestate market, which, whencoupled with loose lendingstandardsandaneasy-moneyculture, helped propel U.S.house prices into thestratosphere. For the averageAmerican worker, long-conditioned to expect ever-rising levels of consumption,the rapid rise in residential

real estate prices offered asimple solution to thedilemmaofstagnantwages—theirhomes couldbeused toplugthegap.Ashousepriceswere rocketing ever higher,homeownersthrewcautiontothe wind and turned theirhomes into ATMs to fundtheir lifestyle—and nowonder, as realwage growthwas stagnant from 2000 to2007.

But economic disasterstruckas real estateprices intheU.S.havetumbledhard—down more than 30 percentfrom their 2006 peak. Sincethe credit bubble of 2008-2009 burst, average housepricesaredownmorethan50percent in some U.S. cities.While the American housingmarket has started tostabilize, it still facessignificant headwinds. A

stagnant economy, weak jobmarket, and a persistentlyhigh foreclosure rate are allmajorobstacles toovercome.Sincehousingaccountsfor20percentof theU.S.economy,animprovedoutlookwillbeakey pillar of any economicrecovery.

WhatAmIMissing?

Mostof theWest facesyearsof slow growth and sluggisheconomic prospects in thewake of the greatest marketmeltdown in a generation.The last decade has beenunkind to most investors.Stocks have tumbled badly,thebondrallyhasstalled,andreal estate has turned out tobeasucker’sbet.

But there is an alternativeto investing as you always

have; you can open yourmind to the world ofcommodities, to a worldwithouta legionof followersbut with plenty of upside.Driven by surging Asianmarkets, sluggish supply, asaggingU.S.dollar,andfew,if any, investmentalternatives, the next greatcommodity bull market isnow upon us. What are youwaitingfor?

HotCommodities

•Commoditiesarepartofoureverydaylivesandcrucialtomodernexistence.

•Commodityfuturesarestandardized

contractsthattradeoncommodityexchanges.Priceandquantityaretheonlyvariables.

•Whenstocksandbondsaregoingdownandinflationisheadinghigher,

commoditypricesmoveup.

•Therearelegionsoffollowersofstocks,bonds,andrealestate,butthereisn’tmuchofafanclubforcommodities.

•Chinaisthekeyto

understandingcommoditydemand.

•ForinvestorsintheS&P500,2000to2009ranksastheworstdecadeinnearly200yearsofAmericanstockmarkethistory.

•Withinterest

ratesonU.S.governmentbondsatmulti-decadelows,there’snowhereforbondpricestogobutdown.

•Commodityreturnsaresimilartothoseofequities,butcommodity

returnsarenotwellcorrelatedtothoseofstocksorbonds,makinganidealadditiontomostportfolios.

•Ifnotcommodities,thenwhat?

ChapterTwo

Gettin’Goin’

CompaniesorCommodities?

THEGLOBALECONOMICORDER is rapidly changing—creating tremendousopportunities for commodityinvestors. Demand forcommodities continues togrow despite the fact thatmuch of the world is stilllicking its wounds from theglobal economic collapse of2008-2009. Westerngovernments have tried topaper over the problem of

sluggish consumer demandby implementing stimulusprograms intended to jump-start infrastructure spending,for example, the Cash forClunkers rebate schemeaimed at the beleagueredAmerican car industry. Butdespite these efforts, thecollective credit cards of theU.S. and much of Europeremain completely maxedout.

The wheezing Westernrecovery aside, demand forcommodities remains strong.Commodities are a big deal,much bigger than mostpeople realize. Primarycommodities,suchasironoreand copper, account for 25percent of global trade.Supply has been sidelinedduring the global economiccollapse, creating a nearperfectstormforinvestors—a

situation that is likely to lastformanymore years.As thebasic feedstock for industrialand urban growth,commodities can be red hoteven when stocks and bondsare ice cold. And with theirdirect link to the drivers ofinflation, commodityinvestmentsareaheaven-senthedgeagainstrisingprices.

Commoditiesareabigdeal,muchbiggerthanmostpeoplerealize.Primary

commodities,suchasironoreandcopper,accountfor25percent

ofglobaltrade.

Despite these benefits,

commodities tend to begrossly underrepresented inmost investment portfolios.To be a total investor is toknow something aboutcommodities–especially witha commodity bull marketwashing up on our shores.Yet commodities are amystery to many investors:most haven’t a clue how tobegin.

DumbLuck

One way to get intocommodities is to luck out.You could find oil on yourproperty as happened in the1960s television show TheBeverly Hillbillies, or youcould stumble upon a majorgold discovery. You mighteven inherit the family farm.In any of these situations,

you’d be in the commoditybusiness, but if you haven’tyet struck oil on yourswampland, chances are youwon’t.

Even if you do get lucky,you’ll need plenty of helpdeveloping your find beforeyou can pull up stakes andmove to Beverly Hills.However, while it may looksimpleonTV,capitalizingona producing commodity

businessisanythingbuteasy.It is a highly sophisticatedand complex undertakingrequiring millions of dollarsand decades of experience—nottomentiongoodluckandexcellentjudgment.Owningafarm, mine, or oil field justisn’t a practical way to addcommodities to yourinvestmentlineup.

GoAlongtoGetAlong

Investors love index fundsand exchange traded funds(ETFs) because they mimicthe pricemovements of theirunderlying indices and giveinvestors an inexpensive andtransparent way to get directcommodity exposure. Thereareseveralmajor indicesand

plenty of exchange tradedfundstochoosefrom.

The granddaddy of allcommodity indices is theReuters/Jefferies CRB Index,which dates back to 1957.The index has gone through10revisionsovertheyearstohelpkeepitbothrelevantandreflective of the underlyingeconomic demand for thevarious commodities itrepresents. Most recently, in

1995, natural gas was addedto the index while lumber,pork bellies, unleadedgasoline, soybean oil, andsoybeanmealweredropped.

In 1992, investment bankGoldman Sachs created acommodity index knowntoday as the S&P GSCI.Another big player in thecommodity index game isUBS, which has two widelyfollowed indices: the Dow

Jones-UBSCommodityIndexand the UBS BloombergConstant MaturityCommodity Index (UBSBloombergCMCI),createdin1997. Jim Rogers, the WallStreet investment legend,created his own index in1998, called the RogersInternational CommodityIndex(RICI).

A problem for allcommodity indices is how to

weight their variouscomponents toprovidea truereflection of their overalleconomic importance. Moststock indices are constructedandweightedaccordingtothemarket capitalization of theircomponents. In commodities,however, the concept ofmarket capitalization (sharesoutstanding multiplied bystock price) just doesn’tapply. Commodities are held

in a variety of forms,including over-the-counterinvestments, offsettingfutures positions, andphysical producer stockpiles—the combination of whichmakes complete accountingimpossible and thecalculation of commoditymarket capitalization anelusivetarget.

Moststockindicesareconstructedand

weightedaccordingtothemarket

capitalization(sharesoutstandingmultipliedbystockprice)oftheir

components.Incommodities,theconceptofmarket

capitalizationjustdoesn’tapply.

Without the availability ofmarket capitalization figures,commodity index creatorshave been left to their owndevices, constructing andweighting the variouscomponents as they see fit.The result is awide rangeofmethodologies that can

dramatically skew theweights of the index and itsrelevance as a barometer forgauging activity levels incommodities.Somebasetheirweights on an assessment ofthe economic importance ofeachcommodity,whileothersbase them on a quantity ofproductionbasis.Subjectivityoften plays a major role inthis process, oil being a casein point. As the most

economically important andactively traded commodity,oil’simportancetotheglobaleconomy cannot beoverstated. In November2009, the target weights forenergyintheS&PGSCIwerea whopping 67.83 percent,yettheReuters/JefferiesCRBIndex set its energy targetweight at just 18 percent—adifference of nearly 50percent.

Investors buy index fundsand index-linkedETFs underthe assumption that theywillmimic the price appreciationtheyexpectfortheunderlyingcommodities. Unfortunately,they are often disappointed.Not only do all commodityindices struggle to find anappropriate weighting ofcomponents,butmostalsodoa poor job of measuring thehere-and-now price

movements of commodities.Aninvestorwhoseesthatoilprices are up $2 per barrelmay justifiably assume thathis or her commodity indexfundisflyinghigh;andifthatinvestor is lucky, it will be.What all commodity indexfunds do is buy a basket offutures contracts, usuallynear-month contracts, whichshouldcloselytrackthepricein the here and now (also

known as the “spot price”)movement of the variouscommodities. Unfortunately,they often don’t. During thefirst 11 months of 2009, forinstance, the price of crudeoil surged some 73 percent,yet the S&P GSCI, with itsheavytargetweightingtooil,was a laggard—increasingjust46.88percent.

Commodityindexfundsshouldcloselytrackthespotpricemovementofthe

variouscommodities—butunfortunatelythey

oftendon’t.

ReadytoRockn’Roll?

Youcanmakealotofmoneyinfuturestradingifyouknowwhat you’re doing. And ifyoudon’t—well,let’sjustsayyou can lose your shirt in ahurry.Commodityfuturesarejust that: contracts for thefuture delivery of a givencommodity. While

commodity futures pricesoften resemble what’shappening in the here andnow, or the “spot market,”this isn’t always the case.Complicating matters furtheris the fact that most futurescontracts trade monthly andneed to be rolled forward—unless you want to takephysical delivery of thecommodity you just bought.And discovering you’re the

proud owner of a thousandbarrels of No. 2 heating oil,currently waiting for you atNew York Harbor, can surethrow a wrench in yourweekendplans.

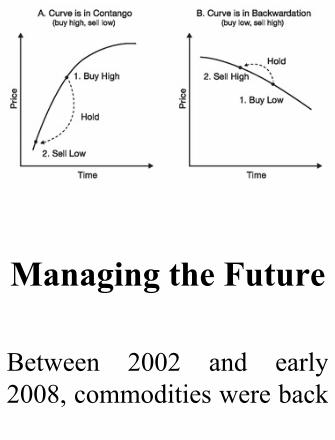

Depending on investors’expectations of commodityprices, the futures curve caneither be upward sloping(contango) or downwardsloping (backwardation). Thefuturescurveisnothingmore

than a compilation ofindividual futures contracts,so if investors expect oilpricestobegoinghigherovertime, then you should expectanupwardsloping(contango)futures curve. If, manymonths into the future, theprice of a commodity issignificantly higher than it istoday (contango), itmay payto hoard the physicalcommodity in the hope that

you can sell it later for aprofit. Oil traders andcompanies did just thatduring the 1970s when theyhired tankers to store crudeoil for months until theycouldsellitataprofit.

In commodity investing,the devil really is in thedetails, and the shape of thecommodity curve is noexception. We’ve alwaysheard that successful

investing is all about buyinglow and selling high, but ifyou’re buying futurescontracts when thecommodity curve is incontango, you’re doing justthe opposite. During the1980s and 1990s, the futurescurves formost commoditieswere downward sloping (inbackwardation), yetcommodity funds werepostingexcellentresultssince

theywereabletobuylowandsellhigh.

Duringthe1980sand1990s,thefuturescurvesformostcommoditieswere

downwardsloping,yetcommodityfundswere

postingexcellentresultssincetheywereabletobuylowand

sellhigh.

Figure2.1BuyingLowandSelling High—It’s theShape of the Curve thatCounts

ManagingtheFuture

Between 2002 and early2008,commoditieswereback

in vogue after a 20-yearhiatus, and commoditytradingadvisors(CTAs)weresuddenly in demand,movingtheirproductsfasterthanfreeice cream on the Fourth ofJuly. The idea behindmanaged commodity futuresis simple. A commoditytrading advisor manages apool of investments, takingcare of the pesky details likecontract rolling, and giving

youexposuretoawiderangeof products. Rather thanstudying the supply anddemand variables for thesoybeanmarket into the weehours of the morning, youhire an expert to makedecisionsforyou.

Of course, managingfutures contracts doesn’tcome cheap. There aretremendous benefits toobtaining professional

management,butwhile someCTAs are provenmoneymakers,manyaren’t—which means that yourreturns are going to be onlyas good as your advisor’sexpertise. Regardless ofwhom you choose, it’simportanttoknowthatyou’regiving up both investmentcontrol and transparencywhenyouuseaCTA.IfyourCTA decides to move

aggressively into frozenorange juice futures becausehe’s spending winters inFlorida, for example, youmayfindthatyouroncewell-diversified portfolio is nowjuiced-up on just a fewcommodities.

CompanyMan

So what’s a commodityinvestor to do? Commodityindices andETFsare easy tobuy, but as I’ve explained,mosthaveseriousissueswithweighting and tracking. Ifgetting direct exposure tocommodities by snapping upfarmland in Ohio or panningforgoldinNevadaseemsliketoo much work, you shouldconsiderbuyingthestocksofcommodity-producing

companies. A key benefit ofowning these is the leverageyou get to rising commodityprices.Aslongasthegaininthe price of the commoditythe company producesoutstripsanyincreaseintheircosts,you’re laughing.Whenbuying stock, you’re alsomaking an indirect bet onmanagement—so nail thecommodity and themanagement call, and you’re

sitting pretty.Best yet,manycommodity producers areroutinely able to build theirreserves over time as theyuncover more resources onthe lands they lease. Buyingcommodity-producingequitiesallowsyoutoprospernotonly in thehereandnowas commodity pricesimprove, but also in thefuture as rising prices allowadditional reserves to be

discovered. Chosenprudently, commodity-producing equities can be agiftthatkeepsongiving.

In my career I’ve tried itall,andIkeepcomingbacktoa well-chosen basket ofcommodity-producingcompanies. With futuresthere’s the “roll risk” tomanage, plus a wide varietyof new markets to study upon. Most commodity index

funds are far too dependenton the shape of the curve togiveyouthekindofexposureyou’re looking for. For mymoney the choice is clear,commodity producers are theway for most investors toprofit from a roaringcommoditybullmarket.

Akeybenefitofbuyingthestocksofcommodity-producing

companiesistheleverageyougettorisingcommodity

prices.

HotCommodities

•Owningyourownoilfield,mine,orfarmisonewaytogetdirectphysicalexposuretocommodities,butitjustisn’tpracticalformostpeople.

•Thepriceofagivenfutures

contractwillalwaysconvergetothe“spot,”orcashmarketpriceatexpiration,butalotcanhappenbetweenthedateswhenfuturescontractsbeginandexpire.

•Duringthe1980sand1990s,thefuturescurveformostcommoditieswasdownwardsloping(backwardation),yetcommodityfundswerepostingexcellentresults

sincetheywereabletobuylowandsellhigh.

•Moststockindicesareconstructedandweightedaccordingtothemarketcapitalizationoftheircomponents.Incommodities,

however,theconceptofmarketcapitalizationdoesn’tapply.

•Commodityindicesareoftenpoorbarometersforgaugingactivitylevelsincommodities.

•Commodity-

producingcompaniesofferleveragetorisingcommoditypricesandtheopportunitytobenefitfromreserveadditionsovertime.

ChapterThree

Gusher

InvestinginOil

NONATURALRESOURCEIS MORE FIERCELYPRIZEDorjealouslyguardedthan oil. Ancient Egyptiansused it forembalmingand tosupportthewallsofBabylon.Wars have been fought andempires created anddestroyed in the epicconquest for the power andwealth that surrounds oil.Since 1854, when thekerosene lamp was invented,

we’ve increased ourdependence on the preciousstuff and have sucked some650billion barrels of it fromthe ground. Access toabundant cheap oil makessuburbia and much of ourmodern world possible. Oilfuels our cars, planes, trains,and buses and is a criticalfeedstockfor theplasticsandcosmetics industries. Enoughoil to fill a trillion barrels

remainsintheground,butthecheap, easy-to-get stuff isalready gone. As the worldeconomybeginstogrowafterthe global recession, oilprices will once again beheadinghigher.Muchhigher.

BigOil

Everything about the oil

business is big. Oil is theworld’s first trillion-dollarindustry, it’s the mostactively traded commodity,and it’s the single largestcomponent of world trade.It’s also the commodity thatgenerates the most debate.Whether it’s America’sreliance on foreign imports,concernoveryourneighbor’scarbon footprint, or themassive profits Big Oil (as

theworld’slargestoilandgasmanufacturersarecollectivelyknown) seems to be makingwhen prices are movinghigher—everyone has anopinionaboutoil.

ToErrIsHuman

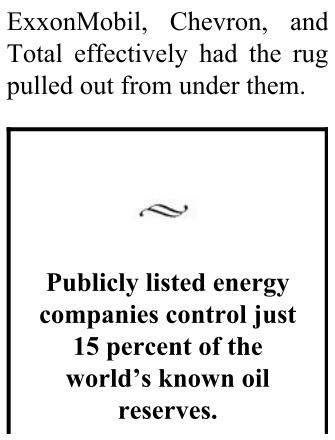

Yet in spite of oil’simportancetoourwayoflife,

publicly listed energycompanies control just 15percentoftheworld’sknownreserves. The rest arecontrolled by governmentsand their national oilcompanies,andmanyarelessthanfriendlytotheWest.Theposter boy for poor oilrelationsisVenezuela’sHugoChávez,theleft-leaning,anti-Americanleaderwhocametopowerin1999.InMay2007,

in his quest to makeVenezuela into a socialist-inspired state, Chávez tookdramatic action by strippingforeignoilcompaniesoftheirmajorityinterestsindomesticoil fields. Bymandating thatstate-controlled Petroleos deVenezuela (PDVSA) had tohave at least 60 percentownership in these new so-called “joint ventures,”companies such as

ExxonMobil, Chevron, andTotal effectively had the rugpulledoutfromunderthem.

Publiclylistedenergycompaniescontroljust

15percentoftheworld’sknownoil

reserves.

But lately, with oil pricesplunging from theirpreviously lofty peaks,Chávez is humming adifferent tune. Once againhe’s soliciting bids from bigWestern oil companies—including many of thosewhose agreements hetrampledon in 2007.Chávezneeds Western money and

know-how tounlockhis vastreserves, yet he still holdsmost of the cards becauseWestern oil companies aredesperate to find large-scaleprojects in which to invest.As a result, once-spurnedWestern companies are stillwilling to take their chanceson Venezuela. Talk aboutdesperation!

Oil revenues account forabout 93 percent of

Venezuela’s export revenue.And with the unpaid billsstarting tostackupforsocialwelfare programs such ashealth care and highereducation, embracingWestern oil companies maybe Chávez’s best option forbalancingthebooks.Thedealmay be bad and the slice ofthepiemaybeshrinking,butVenezuela—unlike other oil-rich countries where the

national companies have astranglehold on production—is at least willing to letmultinational companiesparticipate in the drilling.Saudi Arabia, the world’slargest producer of crudeoil,and Mexico have barredAmerican and other foreignbusinesses from participatingin thesearchforoil formorethanhalfacentury.

FromRussiawithLove

InRussia,theworld’ssecondlargest producer of oil,muscle-flexing is the norm.For years, the Kremlin hasmoved aggressively toreclaim ownership ofRussia’s oil and gas industryfrom private firms. At onetime, Yukos was Russia’s

largest private oil and gascompany,worthanestimated$40 billion. But a personalrivalry with Vladimir Putincost Yukos founder MikhailKhodorkovsky, one of thenotorious so-called Russianoligarchs, both his companyand his freedom. For years,theKremlinandtheoligarchshad maintained an informal,mutually beneficialarrangement: the oligarchs

would stay out of politics inexchange for the Kremlinkeeping its nose out of thedubious circumstances underwhichthisgangoffabulouslywealthy businessmen gainedcontrolofformerstateassets.By Putin’s second term asRussia’s president, however,Khodorkovskyhadsouredonthe arrangement and startedfunding opposition parties intheDuma.ForPutin,thiswas

intolerable. On October 25,2003, Khodorkovsky, thewealthiest man in Russia atthe time, was arrested andchargedwith fraud. Six dayslater,theRussiangovernmentfroze trading in the sharesofYukosandbroughtchargesofincome tax evasion againstthe firm. In May 2005,Khodorkovsky was foundguiltyof fraudandsentencedto nine years in prison.With

this criminal prosecution andthe drawn-out dismantling ofthecompany, anunequivocalmessagehadbeensent:don’tcrosstheKremlin.

In 2003, BP, one of theworld’s largest energycompanies, acquired a 50percent stake in one ofRussia’s largest oilcompanies, TNK. The jointventure, calledTNK-BP, hadPresident Putin’s personal

blessing. But the happymarriage didn’t last long.Faster than you could say“oligarch,” BP and the fourRussian billionaires whoshared control of Russia’sthirdlargestoilcompanyhada falling out. The Russianpartners took objection toTNK-BP’s American chiefexecutive, Robert Dudley,accusing him of favoringBPand running the jointventure

likeasubsidiary.

In adealhammeredout inSeptember2008,BPcededtoall the Russian partners’demands. BP agreed todismiss Robert Dudley andappoint a Russian-speakingchief executive agreeable toits four major Russianshareholders. BP also agreedto create three additionalindependent seats on theboard of directors. While it

must have been a bitter pillfor BP to swallow, it helpedthe company preserve itsownershipinterestinthejointventure,andwithit,accesstothelargeoilfieldsofSiberia.Atatimewhenoilcompaniesare struggling to find newreserves,adealthatpermittedBPtopreserveaquarterofitsworldwide production wasoneithadtomake.

Whilepoliticalriskmaybe

part of the game forinternational oil and gascompanies, itdoesn’thave tobe a gamble that individualinvestors take. For mymoney, I prefer to bet oncompanieswhoseonlyriskisgeological rather thanpolitical. Investing can betrickyenoughwithouthavingto consult theminutes of thelast UN meeting to try andfigure out which way the

politicalwindisblowing.

HaveWeReachedthePeak?

No debate is morecontentiousintheworldofoilthan the debate overwhetheror not the world has passedthe peak of maximum oilproduction. The theory now

knownas“peakoil”wasfirstadvanced by Dr. M. KingHubbert, a geophysicist whoworked for Shell OilCompanyfrom1943to1964.During his career, Hubbertmade many significantcontributions to the field ofgeophysics, but his mostfamous theory was that therateofoilproductionforanygivengeography—beitanoilfield,anation,ortheplanet—

wouldalwaysresembleabellcurve. As time went by,production would increaseuntil it hit its maximum or“peak” production, afterwhich production wouldforeverfall.

Hubbertfirstpresentedthistheory, later dubbed the“Hubbert Curve,” at a 1956meeting of the AmericanPetroleum Institute in SanAntonio,Texas.Hepredicted

that the United States wouldsee oil production peaksomewhere between the late1960s and the early 1970sand thereafter enter anirrevocable decline in thelower 48 states. At the time,hewasderidedbycolleagueswho pointed out that allpredictions made about oilcapacity over the past halfcentury had proven false. Sowhen U.S. petroleum

productionpeakedin1970,asHubbert had accuratelypredicted 14 years earlier,you can guess who had thelastlaugh.

WhenU.S.petroleumproductionpeakedin1970,asHubberthad

accuratelypredicted14yearsearlier,youcanguesswhohadthe

lastlaugh.

According to theInternational EnergyAgency’s(IEA)reportWorldEnergy Outlook 2008,production from currentlyproducing fields was set tostart declining in 2009. The

shortfall between the amountof oil that the Paris-basedIEA figures the planet willneed and what is currentlybeing produced will have tocome from yet-to-be-discovered oil fields, fieldsalreadydiscoveredbutnotyetin production, natural gasliquids (NGLs), andnonconventionalsourcessuchasCanada’s oil sands.NGLsare liquids such as propane,

butane, and pentane, whichare often found in oilreservoirs. While NGLs canbe used in many chemicalprocesses, such as themanufacturing of plastics,theyaren’tmuchgoodasfuelfor your car. Over the nextfewdecades,withtheworld’sexisting oil fields tired andtheir production in decline,theoilindustryclearlyfacesamonumental task: finding

vast, economically viablenewreservestoexploit.

HopeSpringsEternal

Already, many of our mostpromisingsupplybasinshaverolled over and started todecline. The North Sea iscaseinpoint.Itstwomassiveoil fields, theForties and the

Brent, were discovered in1970 and 1971 respectively.The Forties field hit its peakproductionof523,000barrelsper day in 1980, while theBrent hit its maximum of440,000 barrels per day in1985. In an effort to keepproducing as much aspossible for as long aspossible, exploration andproduction companiesinjected massive amounts of

waterintothereservoirsinanattempttosweepoilfromtheedges to the center, where itcould be brought to thesurface and collected moreeasily. By 2000, however,production from the NorthSeahaddroppedlikeastone,aggressive water floodinghavingultimatelyexacerbateditsdecline.

The last major oil field tocomeintoproductionwasthe

giant Cantarell field inMexico, which wasdiscovered in 1975. Withpeakproductionofmorethantwomillionbarrelsaday,thiswastrulyaGoliathofafield.To keep the good timesrolling and boost productionlevels, Pemex, Mexico’snational oil company,initiated an enhanced oilrecovery program in 1998.Despite spending more than

$10 billion on the effort,Cantarell’sproductionstarteddroppingquicklyin2003.

ShiftingSands

In 2007, when I visited themammoth Syncrude projectnearFortMcMurray,Alberta,in the heart of Canada’s oilsands, I felt as if I was

standingonthesurfaceofthemoon. The earth had beenscarred andwas riddledwithpockmarks; years of surfacemining had altered thelandscape forever. In thedistance, I could see a smallyellow dump truck. As itclosedthenearly30-mile(48kilometer)distancetowhereIwas standing, it becameapparent that this was noordinary dump truck. Rather,

it was a massive Caterpillar797 haul truck boasting apayloadof400shorttonsandstanding more than 50 feet(15meters)high.

Projects such asSyncrude’s arewhat the IEAhopes will become thecornerstone of future oilsupply growth. Canada’s oilsands reserves are massive,rankedaclosesecondbehindSaudi Arabia. However,

getting all that gooey, sandyoil out of the ground and tomarket is no easy task. Itrequires either an enormoussurfacemining operation, or,when the resource is buriedtoo far below the earth’ssurface, a highly energy-intensive operation involvingtheinjectionofsteamintothereservoir to get the tar-likeresource flowing. Once theoil is recovered, sand and

impurities need to beremovedandtheoilupgradedbefore it can be sent bypipeline to refineriesthroughout North America.While the oil sands are atremendous resource,removing oil from sand isn’tcheap.

Decline

To hold oil production at2008 levels, the global oilindustry needs to find morethan four million barrels perday—an amount equal toIran’s total 2008 production—each and every year. In2008, the average oil fieldsaw production declines ofaround 9.7 percent. Byspending more than $250billion annually on waterflooding and other enhanced

oil recovery techniques, theoil industrywas able to slowthe rate of decline to 5.1percentperyear.

Toholdoilproductionat2008levels,theglobaloilindustryneedstofindmore

thanfourmillionbarrelsperdayofproduction—an

amountequaltoIran’s2008production—eachandeveryyear.

To find the huge new oilfields they require,exploration companies needto be drilling plenty of newexploration wells.

Unfortunately, energyinvestmenthasslumpedsince2008, as the effects of theglobalfinancialcrisismadeitharder for energy companiesto secure the necessaryfinancing. According to theIEA, global explorationspending plunged by over$90 billion, more than 19percent, in 2009—the firstsuch drop in more than adecade.

While exploration effortsremainmuted, oil demand isforecast to soar asconsumption in China andIndia increases. The IEApredicts that between nowand2030,fully93percentoftheincreaseinoverallenergydemand will be driven bynon-OECD3 countries, withChina and India aloneaccounting for 53 percent offuturedemand.Notonlymust

new oil fields be found tomake up for dwindlingproduction from existingfields, but the IEA alsoestimates that at least 20million barrels per day ofadditional production willneed to be found over thenext20years.Goodluck!

For Big Oil, a perfectstorm of slumping globalsupplies, voracious demand,and increasingly hostile host

governments have made itdifficult to grow its “reservebase”—that is, the inventoryfrom which oil companiesproduce their supply eachyear. For the large majorproducers, the lack of accessto quality projects and thehigh cost of finding andbooking reserves have lefttheminadifficultposition.In2008,theaveragereservelife(reserves/current annual

production)forthesixlargestpublicly listedoilcompanies,or “super majors,” was just12.2years.Atcurrentratesofproduction, and in theabsence of new discoveries,the super majors will be outofoilreservesinlessthan15years.

Atcurrentratesofproduction,andwithoutnew

discoveries,thesupermajorswillbeoutofoilreservesinlessthan15years.

ThatGreatSuckingSound

Big Oil has found itselftrappedbetweenarockandahard place. Shareholders aredemanding increases in bothproduction and reserves, yetWestern oil companies areoften stymied in their questfor new oil. Increasingly,companies are investingbillions in cutting-edgetechnologies to unlock moreof the oil that lies trappedbelowtheearth’ssurface.But

despitemajoradvancesintheindustryoverthelastcentury,a shocking two-thirds of alloilstillgetsleftintheground.

Despitemajoradvancesintheoil

industryoverthelastcentury,ashocking

two-thirdsofalloilstillgetsleftinthe

ground.

If international oilcompanies can raise therecovery ratesonexistingoilfields from a paltry 35percent to closer to 50percent, the world’srecoverable oil reserveswould soar.TheOil andGas

Journal, a leading industrymagazine,estimatesthatwithcurrent recovery rates, theworldhas1.34trillionbarrelsofrecoverableoilreserves.Ata 50 percent recovery rate,thatnumber could zoom to astaggering2.5trillionbarrels!Sofar,however,thedreamofrecovering vast new amountsof trapped oil has provedelusive.

Energy companies are

constantly looking for newways to unlock more oil.Water flooding is often usedin aging reservoirs, whiletechniques such as nitrogeninjectionareused to thinandmobilizeoilinmuchthesameway that detergent cuts thegrease on dinner plates. Yetinspiteofalloftheseefforts,global recovery rates remainalarminglylow.

SecondComing?

Whilenewoilfieldsarebeingdiscovered all the time, theyare increasingly in remote,inhospitable parts of theworld.Thelatestthingstosethearts racing are themassivediscoveries in Brazil, some180 miles from the coast ofRio de Janeiro in the SantosOilBasin. In all, threemajor

newfields—theTupi,Jupiter,and Sugar Loaf—have beenfound, comprising the largestoildiscoveriessince2000.Bysome estimates, the threefields could contain asmanyas 80 billion barrels of oil,enough to launch Brazil intothe big leagues of oil-producing and oil-exportingnations.

But there’s a catch. Thefields lie in ultra deepwater,

more than 2.5 miles belowthe seabed. And a biggerproblem is that these fieldsarelocatedintheocean’spre-salt layer, which makesdrilling for oil extremelydifficult and expensive. TheTupifieldalonecouldcostinexcess of $600 billion todevelop. Collectively, themajor fields in the SantosBasin will cost in excess of$1.5 trillion tobring into full

production—aheftypricetag.

Fill’ErUp

Demand for oil is alsoexpected to grow in the verysame part of the world thatwe’llbelookingtoforfutureoilsupplies: theMiddleEast.Outside of Asia, the MiddleEast is showing the fastest

rate of increase in demand,accounting for roughly 10percent of the incrementalglobal energy demandforecastedbytheIEA.

One reason for thisincreased demand is heavysubsidization at MiddleEasterngaspumps.Whilewestart togrumbleprettyloudlywhen the cost of topping upour tanks hits $4 per gallon,many of our pals in Saudi

Arabia are paying amere 45cents per gallon. And whileit’s cheap to drive in theMiddle East, operating a cabin Caracas, Venezuela, hasgot tobethebestdealgoing.Gasoline prices in Chávez’sSoviet-styled state clocked inat a jaw-dropping 17 centsper gallon in 2008. Oilsubsidies are a big dealthroughout most of the oil-producing world. According

to the IEA, the 20 largestnon-OECD energy-consumingcountriesspentanestimated $150 billion onsubsidies in 2007. Anafternoon spin is a lot morefun when someone else isfootingthebill!

NiceWheels

In theU.S., vehicle sales fell18 percent during 2008. InChina, however, theycontinuedtoclimbdespitetheworldwide recession. In thelastdecadealone,carsalesinChina have surged fivefold,leaving foreignmanufacturers, such asGeneral Motors Corp. andVolkswagen AG, and theirChinese partners scramblingto produce enough cars to

meetthedemand.InFebruaryof 2009, the manufacturers’hardworkpaidoff,asthesaleof vehicles in Chinasurpassed those of the U.S.forthefirsttime.

In August of 2009, Chinaachieved yet anothereconomic milestone when itbecame the largest carmanufacturing nation on theplanet,despite the fact that itdid not export a single car.

India’sTataMotors,ownerofthe Jaguar and Range Roverbrands,hasbegun toproducean entry-level car called theNano, which retails for just$2,000. With a sticker pricethat low, more drivers arebound tobehitting the roadsinIndiaandChina,whichcanonly mean one thing: highergasoline prices for NorthAmericans.

CrackShack

Refinersareakeycomponentof the oil and gas business,and yet they often get shortshrift. In the business, thejoke is that refiners are the“commodities’ commodity.”Refinery guys were alwaysthe ones wearing thechocolate brown suits andthick-soled loafers at the oil

and gas conferences. Thebusiness, while complex andindispensible, just isn’t allthat sexy or profitable.Whether they’re stand-aloneindependents or part ofintegrated oil and gascompanies, refiners are pricetakers.Theirprofitability liesin the razor-thin marginsbetween what they get forsellingrefinedproducts,suchas gasoline, diesel, and fuel

oil, and the costs of buyingthecrudeoilfromproducers.

Today, with crude priceshighandgasolinestoragefull,American refineries aregettingsqueezedonallsides.Adding to theirmisery is thefact that thecrudeoil they’rereceiving is increasinglybothsour (high in sulfur content)and heavy (doesn’t floweasily).MostrefineriesintheU.S.weredevelopedinanera

whenthelight,sweetblendofcrude oil (the type that theWTI contract is based on)was the norm. But today, asthe oil fields have aged andproductionisstartingtogetalittle long in the tooth, light,sweetcrudeoilmakesupjust15percentoftheglobalcrudeslate. And that means costlyretrofits (in the billions ofdollars per refinery) torearrangethevariouspotsand

pans necessary to handle theheavier sour grades of crudethat have become soprevalent.

With America awash ingasoline and refineriesworking at just 80 percentcapacityutilization, the stockmarkethassoldoffthesharesof the independent refiningcompanies. Refiners maketheir highest margin sellinglighter, more valuable

productssuchasgasoline.Toproduce gasoline from crudeoil, the oil molecules firstneed to be “cracked” indevicessuchashydrocrackersor fluid catalytic crackers.The profit margin thatrefiners make in the processis thus known as the “crackspread.” Today, the crackspread has collapsed from ahigh of $31.98 per barrel onDecember 31, 1998, to

around $7 per barrel—a lossofmorethan70percent.

Theprofitmarginthatrefinersmakein

upgradingcrudeoiltoproductssuchas

gasolineisknownasthecrackspread.

SlickOperators

Onceuponatime,billionsofdollars were chasing Internetstocks, but today the hotmoneyisflowingintooilandcommodity funds.Unlike theInternet investment fad, thisbullmarketisunderpinnedby

some pretty solidfundamentals: namely,sagging supply and soaringdemand.Andthat’smakingalot of people in London andNewYorkrich.

As a critical feedstock forthe modern economy, oil isquite simply themost visibleand important of all thetraded commodities. This isreflected on the trading floorat NYMEX, where oil is

traded alongside natural gas,coffee,andcopperbybrokerswhobuyandsellcontractstodeliver these goods for acertain price at a future date.Unlike the modern,computerized tradingplatforms such asNASDAQ,the NYMEX is an open-outcry system where,dependingonthecommodity,floor traders meet inpreassigned circular pits to

match buy and sell ordersfromthemarketplace.WhenIvisited the floor, it was amaze of activity, with phonecables everywhere, runnersgoing every which way, andtraders shouting at the topoftheirlungs.Butnopitwasasphysically large, boisterous,oraction-packedasthecrudeoil pit, where floor traderswere executing client ordersfromaroundtheworld.

Far away from thetestosterone-fueled tradingfloor of the NYMEX sit thereally slick operators in theworld of oil trading: thecommodity traders employedby hedge funds andinvestment banks. Here, anunexpected calm reigns asbillions of dollars arewagered on the spreadbetween light, sweet crude,and heavy crude oil prices.

Trades are executed in theblink of an eye by a bankofcomputers reacting to presettrading algorithms or bytraderswithadvanceddegreesin mathematics. Ascommodity prices movehigher, the demand fortrading talent has increaseddramatically.Today,adecentmid-level trader who knowsthe energy complexwell caneasilyearnbetween$1and$3

million per year—a levelonce reserved for the toptraders.

Nowadays, oil tradersaren’t just buying contractsfor the future delivery of oil,they’re also charteringsupertankers to store thecrudeinthehopeofresellingit for a profit months later.And in what’s been dubbedthe “trade of the year,”companies such as Citigroup

and Morgan Stanley havebeensnappingupthisfloatingstorage at deeply discountedrates. In 2008, when rentalrates plunged 78 percent,somesavvytraderssecured7percent of the global fleet oflargecrudecarriers.

PetrolProfits

As the global economybegins to grow again, oilprices will head higher.Strong demand, sluggishsupply, and technical andoperational challenges willcontinue to plague theindustry, making higher oilprices a foregoneconclusion.Investors looking to profitfrom the coming bullmarketin petroleum need look nofurther than the stocks of

well-run oil and gascompanies engaged inexploration and productionactivities. Companies withlong-lived oil reserves incountries with low politicalrisk should be the go-tonames for investors lookingtopumpuptheirprofits.

Companieswithlong-livedoilreservesincountrieswithlow

politicalriskshouldbethego-tonamesforinvestorslookingto

pumpuptheirprofits.