Embed Size (px)

Citation preview

Please see Disclosures and Disclaimers at the end of this report. A division of Dundee Securities Ltd.

Dundee Capital Markets is a registered trademark of Dundee Corporation, used under license.

January 21, 2014

Josh Wolfson, CFA / (416) 350-5045 [email protected]

Jon French / (416) 350-3311 [email protected]

A Golden Glimmer Of Hope Emerging

DCM Precious Metals Coverage Universe Dundee is resuming coverage of the senior Canadian gold producers, Barrick (ABX-T; NEUTRAL rated; C$22.00 target), Goldcorp (G-T; NEUTRAL rated; $25.50 target), and Kinross (K-T; BUY rated; C$6.50 target). This complements DCM's existing coverage of the intermediate/junior producers, and developer group.

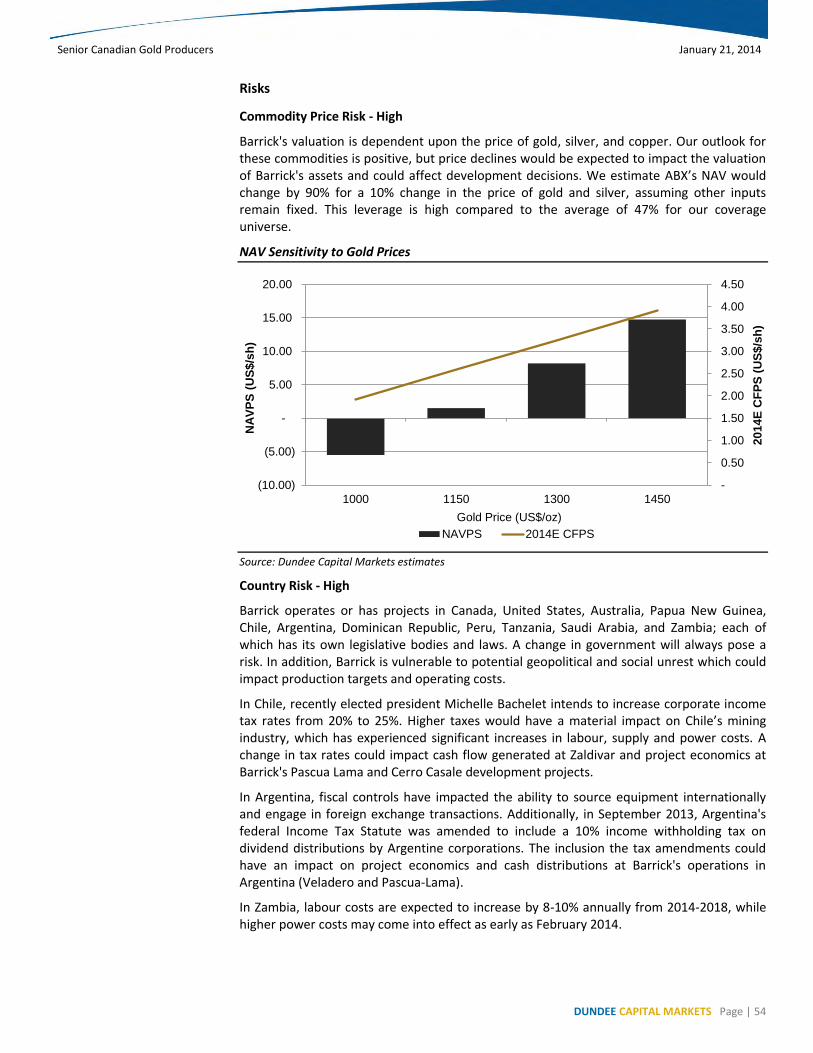

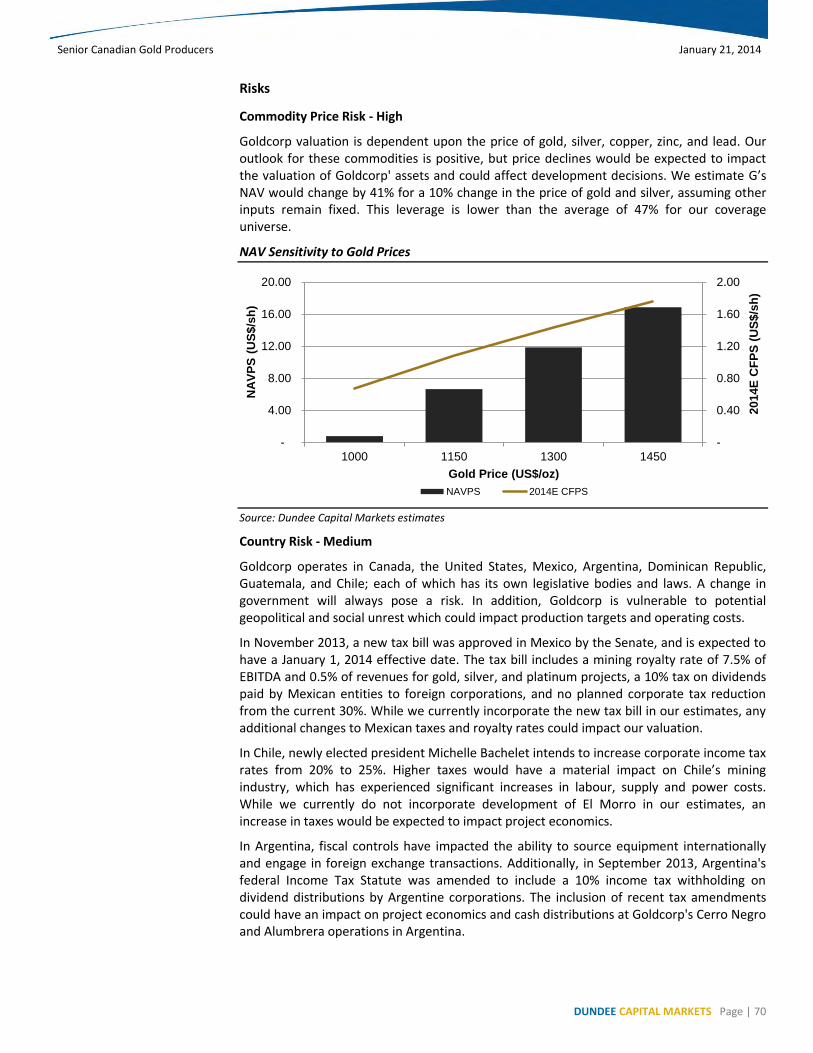

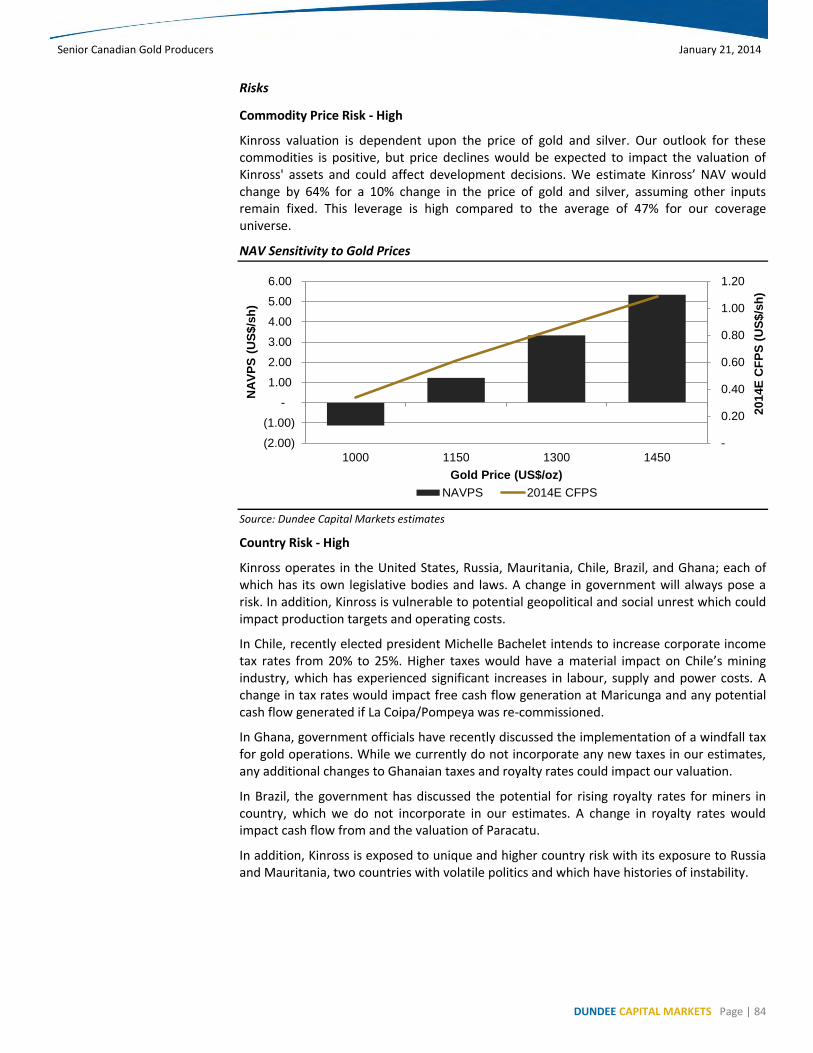

We remain positively biased on the long term prospects for gold prices. Our rationale is predicated upon a continuation of loose monetary policy and that demand for gold will remain strong from central banks and Asian markets. Key risks to our thesis include increasing real interest rates from policy tightening, a weak global economy, or the continuation of inventory sales due to interest in alternate investments or sales for liquidity purposes. Dundee gold price expectations incorporate $1,248/oz in 2014 and a long term gold forecasts of $1,325/oz.

Ultimately, we expect gold producers to benefit longer term from higher gold prices, although financial stress near term remains high and valuation is uninspiring to attract broader investment. Following the XAU gold index's devastating 48% decrease in 2013, we are issuing a neutral outlook for the gold mining industry, an improvement from our prior cautious view. Equity leverage to a potential increase in gold prices continues to hinge upon the ability for companies to contain operating and capital costs, and the maintenance or expansion of current elevated valuation levels. A renewed sector focus on margins, debt reduction, capital allocation, and risk management is encouraging. However, broadly we believe equity valuation has yet to adjust to the current pricing environment and equities incorporate an implied improvement in gold prices.

We recommend investors maintain a bias to producers with better quality operations, balance sheet strength, and trade at a reasonable valuation. Our forecasts are generally more conservative than consensus estimates and we anticipate downward consensus revisions to continue as gold price estimates are cut and financial models adapt to reflect a more realistic value of uneconomic assets. Generally, we believe the senior gold producers represent a weak risk-reward proposal for investors, and we see better risk-adjusted opportunities via intermediate and junior gold producers, and better reward via quality, funded developers, or lower risk gold exposure via the metal. For our new coverage, our preferred senior producer is Kinross, due to the company's successful turnaround efforts, but still heavily discounted relative valuation. We forecast the company will generate fair levels of near term free cash flow, while production estimates incorporate negligible development risk from new operations. The Dundee gold team also continues to recommend B2Gold, New Gold, and Randgold as preferred producer picks.

Company Ticker Rating

(1)

Risk Target

Price

Analyst

(2)

Senior Producers

Barrick Gold Corp. ABX N High $22.00 JW

Goldcorp Inc. G N High $25.50 JW

Kinross Gold Corp. K B High $6.50 JW

Intermediate Producers

Agnico-Eagle AEM N High $33.00 JW

Eldorado Gold Corp. ELD N High $7.50 JW

IAMGOLD Corp. IMG N High $4.50 JW

New Gold Inc. NGD B High $7.25 JW

Osisko Mining Corp OSK B High $7.00 JF

Randgold Resources GOLD B High US$90.00 JW

Yamana Gold Inc. YRI S High $10.00 JW

Junior Producers

Alamos Gold Inc. AGI B High $15.50 JW

AuRico Gold Inc. AUQ N High $5.00 JF

B2Gold Corp. BTO B High $3.50 JF

Dundee Precious Metals DPM NR N/A N/A JW

Kirkland Lake Gold KGI N High $3.50 JF

Perseus Mining Ltd. PRU N High $0.40 JW

Primero Mining P CN B High $6.50 JF

Timmins Gold Corp. TMM B High $2.25 JF

Developers/Explorecos

Belo Sun Mining BSX B Spec $0.75 JF

Continental Gold Ltd. CNL B Spec $5.50 JF

Torex Gold Resources TXG B Spec $2.00 JW

Silver

Coeur Mining CDM S High $8.50 CL

Endeavour Silver EDR N High $4.50 CL

First Majestic Silver FR B High $13.00 CL

Fortuna Silver Mines FVI B High $5.25 CL

Silver Standard SSO N Spec $10.00 CL

SilverCrest Mines SVL B High $2.25 CL

Tahoe Resources THO B Spec $20.00 CL

Pan American Silver PAAS N High $12.50 CL

Royalty

Franco Nevada FNV B Med. $51.00 CL

Silver Wheaton SLW B High $27.50 CL

(1) B - Buy, N - Neutral, S - Sell, NR- Not Rated. Refer to

disclosures for more information.(2) CL - Chris Lichtenheldt, JF - Joe Fazzini, JW -Josh Wolfson.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 2

Contents

A CHALLENGING BACKDROP FOR GOLD EQUITIES ................................................................................................................. 4

DRIVERS FOR FUTURE RETURNS BEGINNING TO ALIGN ......................................................................................................... 5

FULLY LOADED COSTS EXPECTED TO DECREASE FROM 2013 LEVELS..................................................................................... 7

INDUSTRY CHALLENGES REMAIN, THREATENING THE OUTLOOK .......................................................................................... 9

LONG-TERM GOLD PRICE OUTLOOK POSITIVE, INTERIM PROJECTIONS SUBDUED ............................................................. 12

A UNIQUE SECTOR WITH DISTINCTIVE CHARACTERISTICS ................................................................................................... 19

GOLD EQUITY OVERVIEW ...................................................................................................................................................... 20

Drivers for Industry Equity Returns ................................................................................................................................... 20

Gold Equity Investment Opportunities .............................................................................................................................. 20

VALUATION PHILOSOPHY INCORPORATES BOTH LONG AND SHORT TERM VIEWS ............................................................. 22

SENIOR COVERAGE RECOMMENDATIONS ............................................................................................................................ 23

Portfolio Asset Margins ..................................................................................................................................................... 25

Operations at Risk.............................................................................................................................................................. 26

Production and Delivery Risk ............................................................................................................................................. 28

Geopolitical Exposure ........................................................................................................................................................ 31

Credit Analysis ................................................................................................................................................................... 32

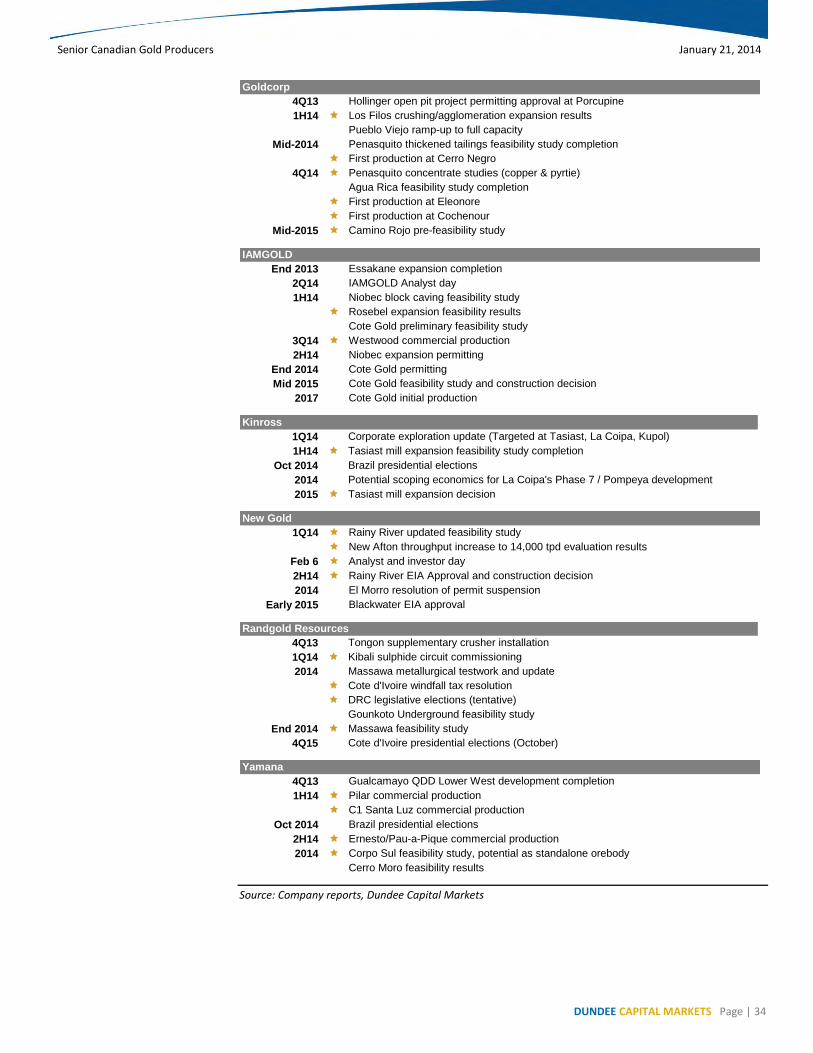

Upcoming Catalysts ........................................................................................................................................................... 33

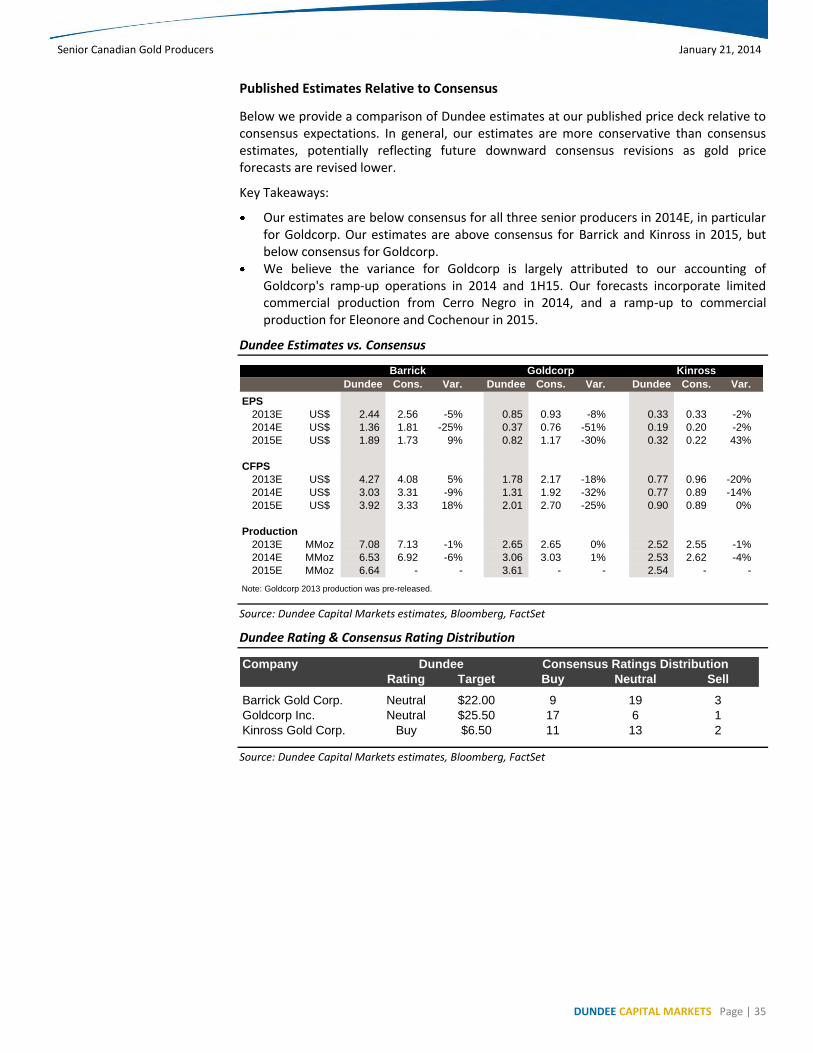

Published Estimates Relative to Consensus ...................................................................................................................... 35

Comparable Tables ............................................................................................................................................................ 36

BARRICK GOLD CORP. - BEARING THE WEIGHT OF DAYS GONE PAST; INITIATING WITH A NEUTRAL………….……………………37

Company Overview ........................................................................................................................................................... 40

Net Asset Valuation - At Spot Gold .................................................................................................................................... 41

Financial & Operating Forecasts - At Price Deck ............................................................................................................... 42

Key Assets .......................................................................................................................................................................... 44

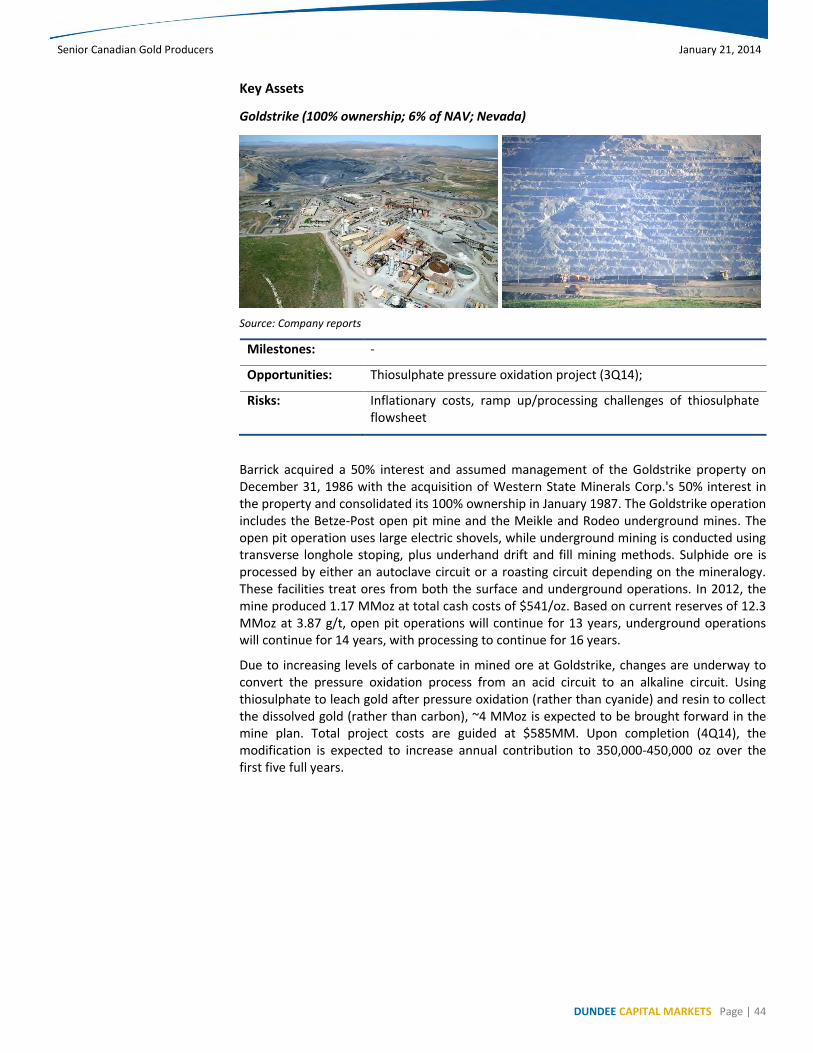

Goldstrike (100% ownership; 6% of NAV; Nevada)............................................................................................................. 44

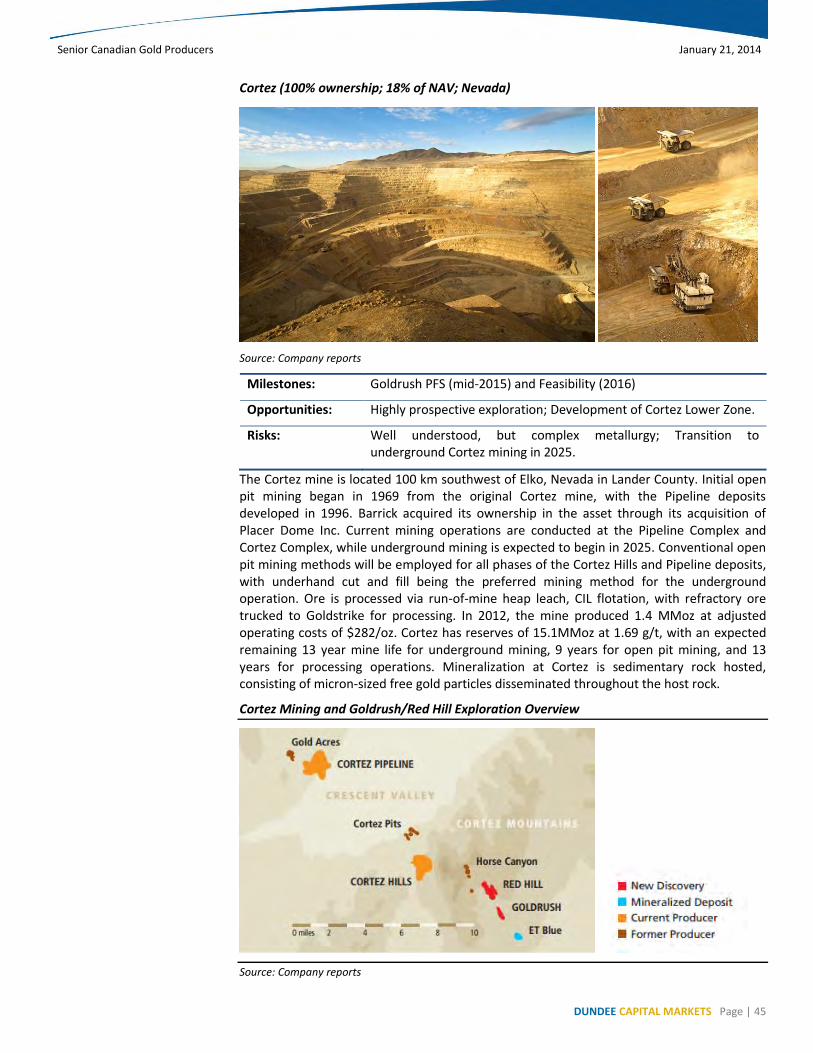

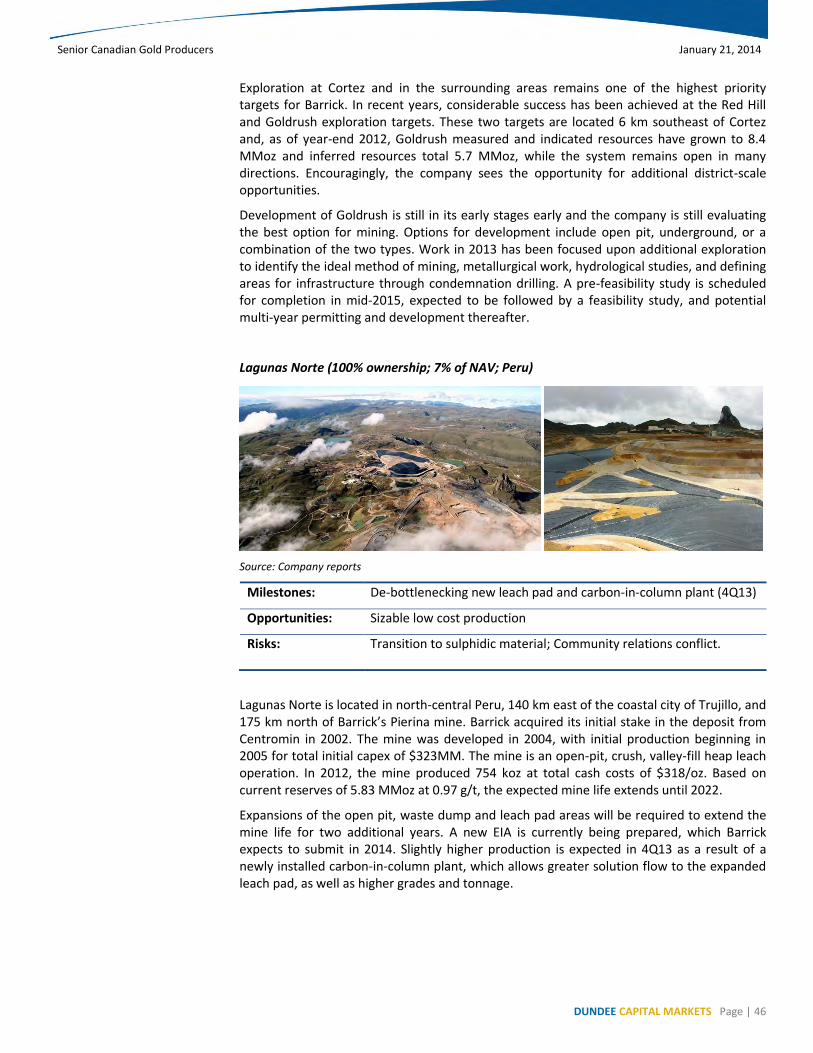

Cortez (100% ownership; 18% of NAV; Nevada) ................................................................................................................. 45

Lagunas Norte (100% ownership; 7% of NAV; Peru) .......................................................................................................... 46

Veladero (100% ownership; 11% of NAV; Argentina) ......................................................................................................... 47

Pueblo Viejo (60% ownership; 11% of NAV; Dominican Republic) ..................................................................................... 48

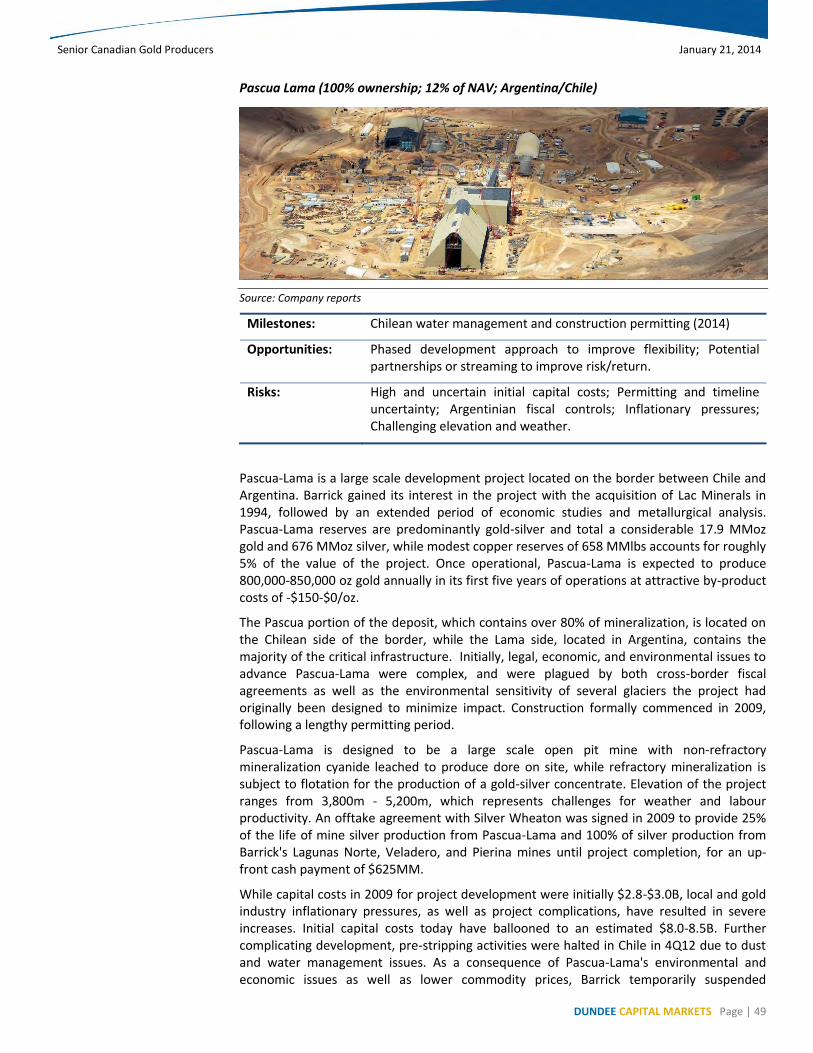

Pascua Lama (100% ownership; 12% of NAV; Argentina/Chile) ......................................................................................... 49

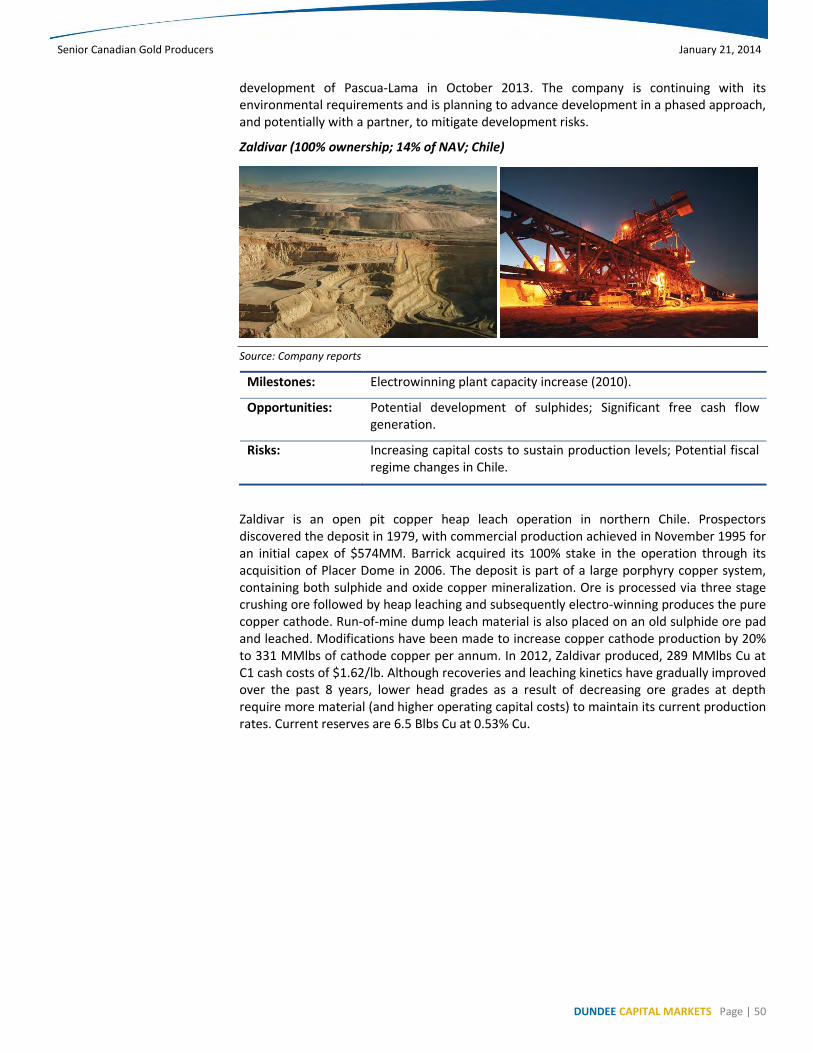

Zaldivar (100% ownership; 14% of NAV; Chile) .................................................................................................................. 50

Lumwana (100% ownership; 1% of NAV; Zambia) ............................................................................................................. 51

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 3

Other Operations ................................................................................................................................................................ 52

Risks ................................................................................................................................................................................... 54

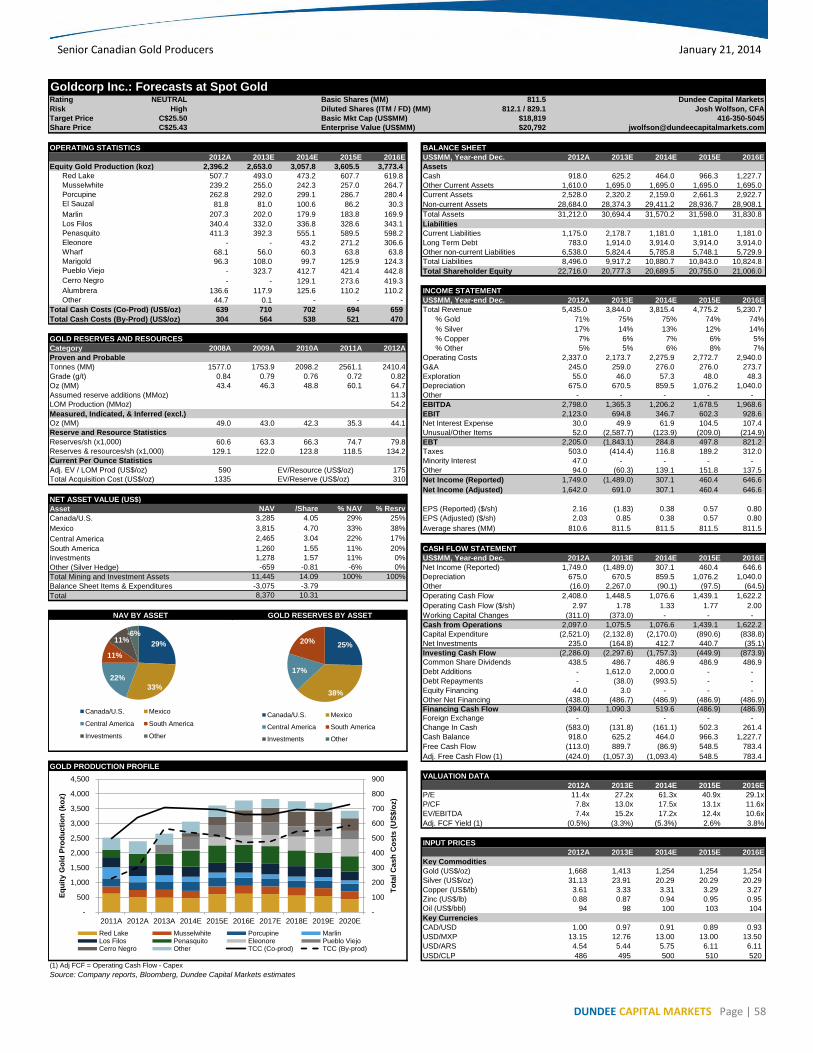

GOLDCORP INC. - ELEVATED DELIVERY RISK, TRANSITION YEAR AHEAD; INITIATING WITH A NEUTRAL…………..……………..56

Company Overview ........................................................................................................................................................... 59

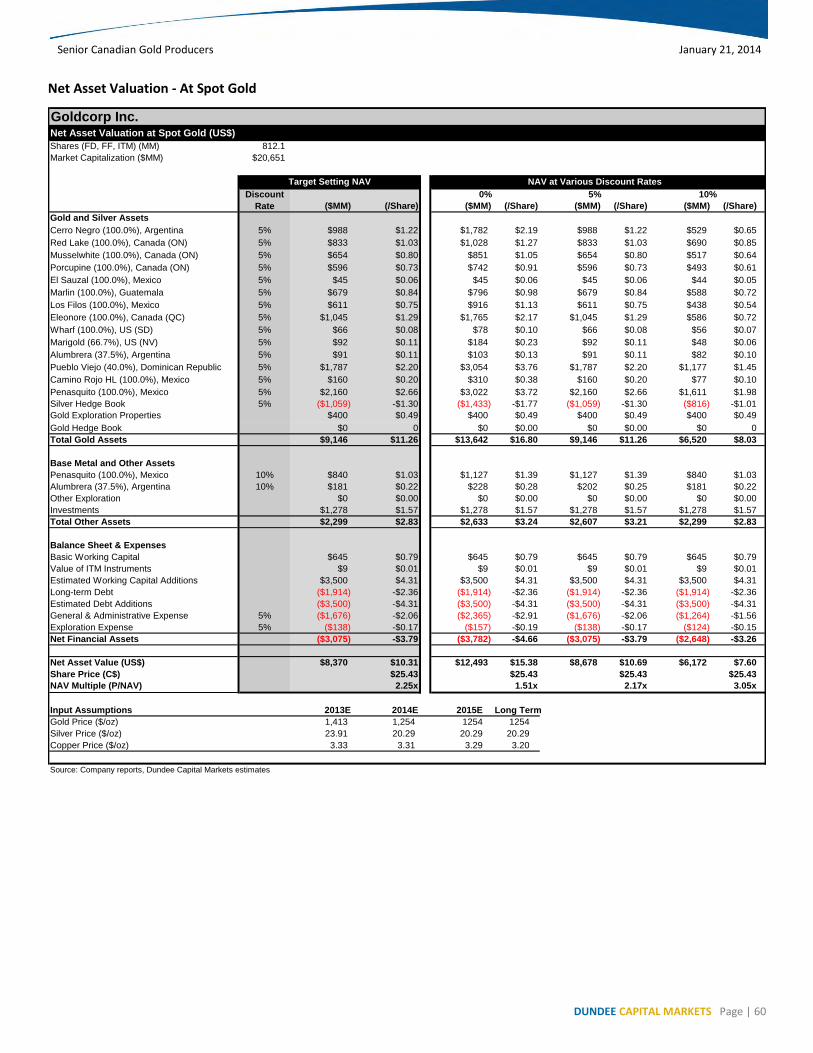

Net Asset Valuation - At Spot Gold .................................................................................................................................... 60

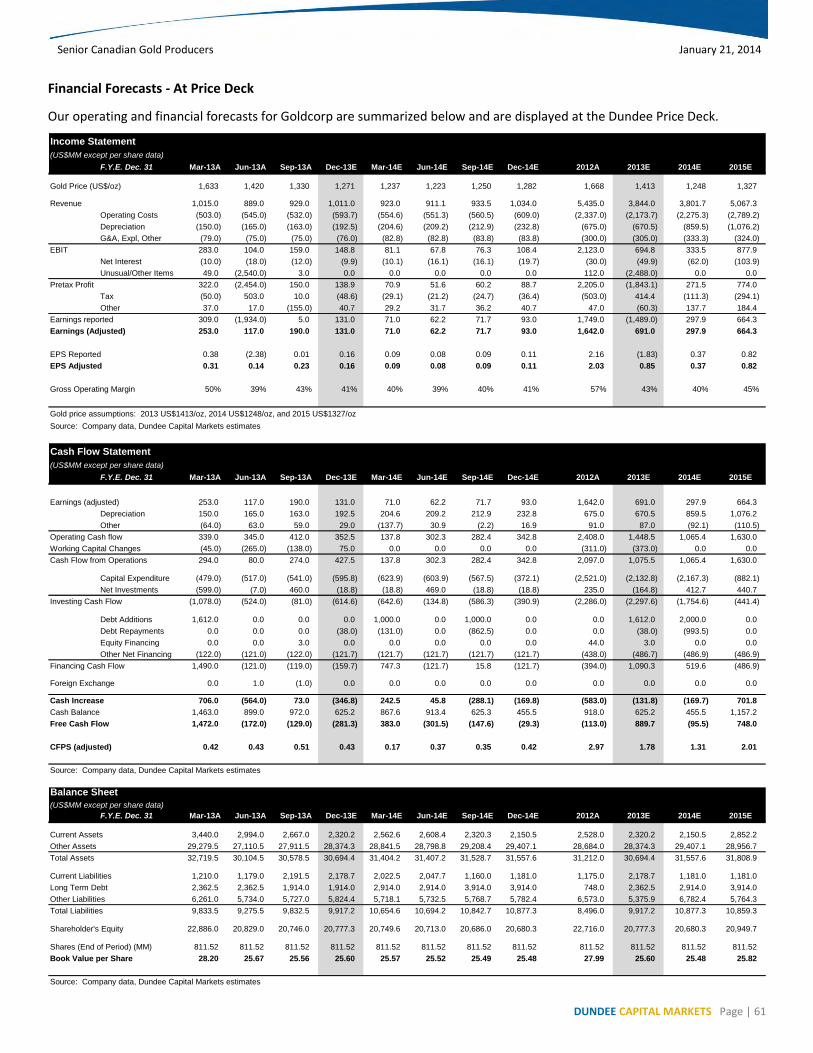

Financial Forecasts - At Price Deck .................................................................................................................................... 61

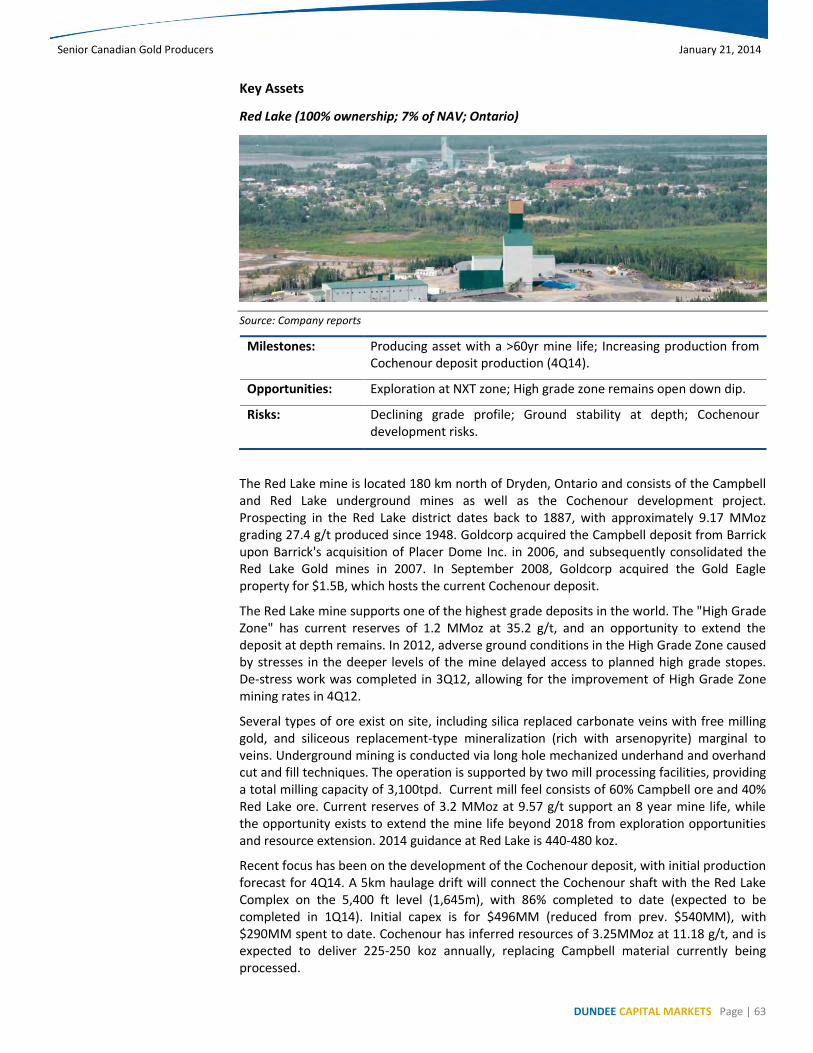

Key Assets .......................................................................................................................................................................... 63

Red Lake (100% ownership; 7% of NAV; Ontario) .............................................................................................................. 63

Pueblo Viejo (40% ownership; 16% of NAV; Dominican Republic) ..................................................................................... 64

Penasquito (100% ownership; 26% of NAV; Mexico) .......................................................................................................... 65

Cerro Negro (100% ownership; 9% of NAV; Argentina) .................................................................................................... 66

Eléonore (100% ownership; 9% of NAV; Quebec) ............................................................................................................... 67

Other Properties ................................................................................................................................................................. 68

Risks ................................................................................................................................................................................... 70

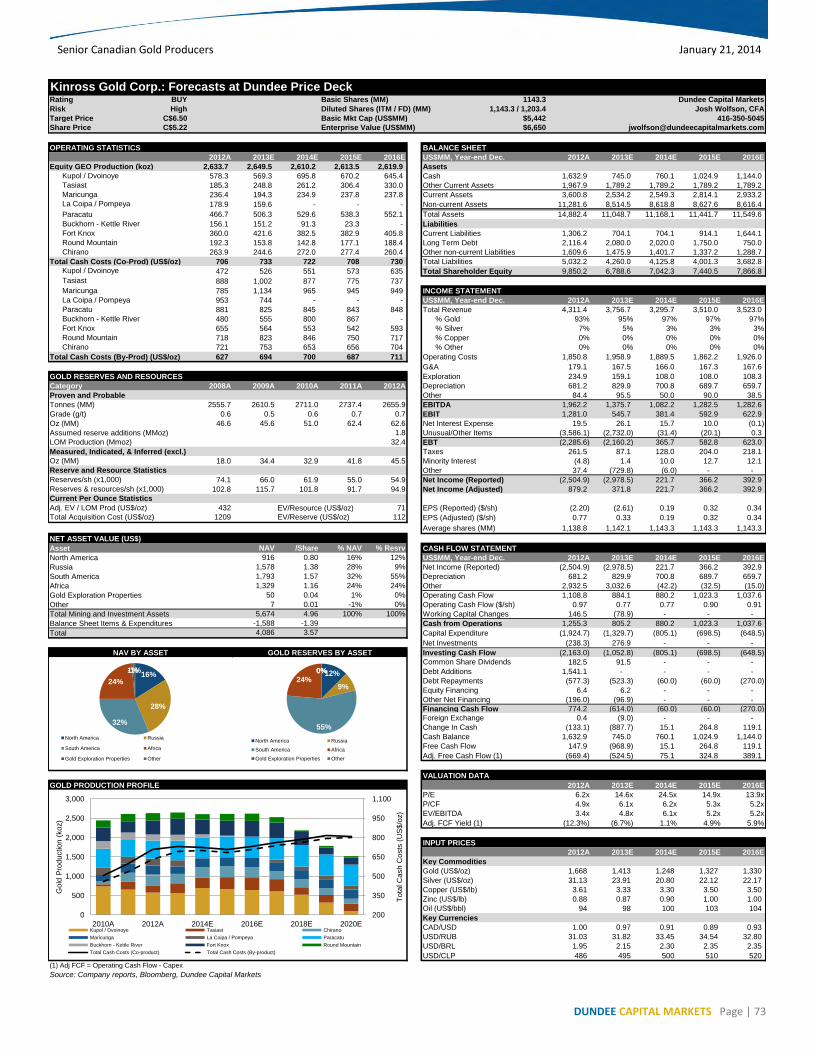

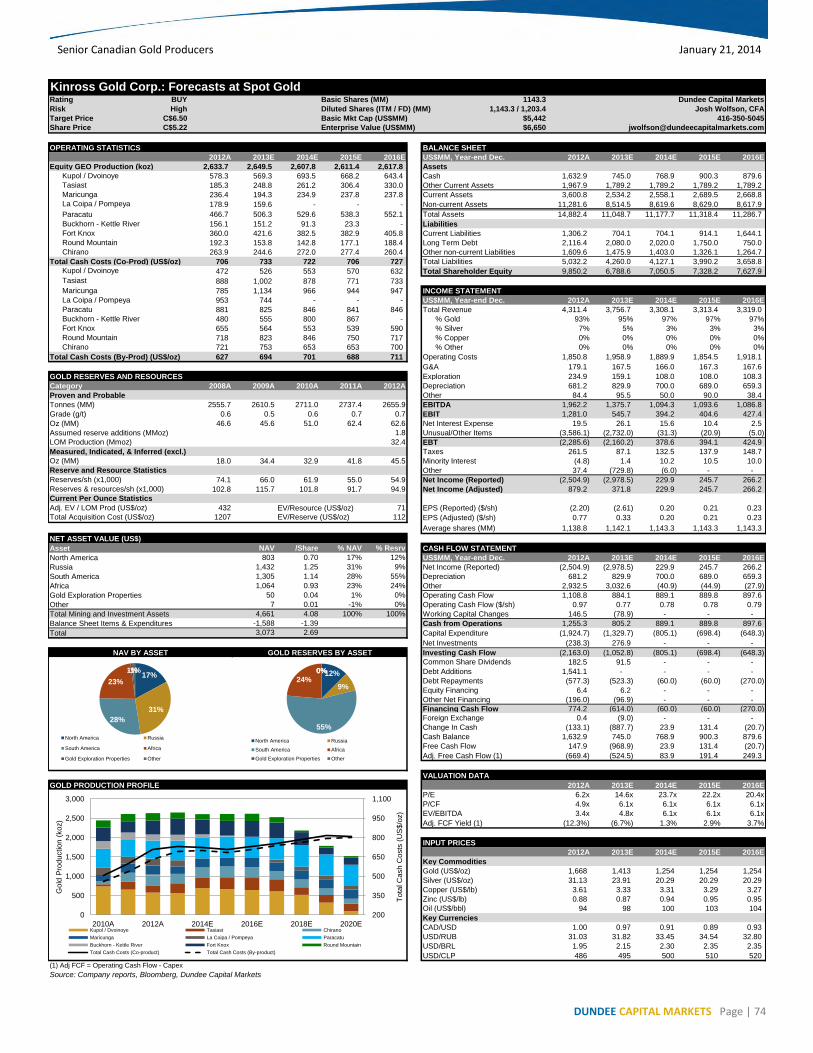

KINROSS GOLD CORP - IMPROVING CREDIBILITY AS TURNAROUND PROGRESSING; INITIATING WITH A BUY……………..….72

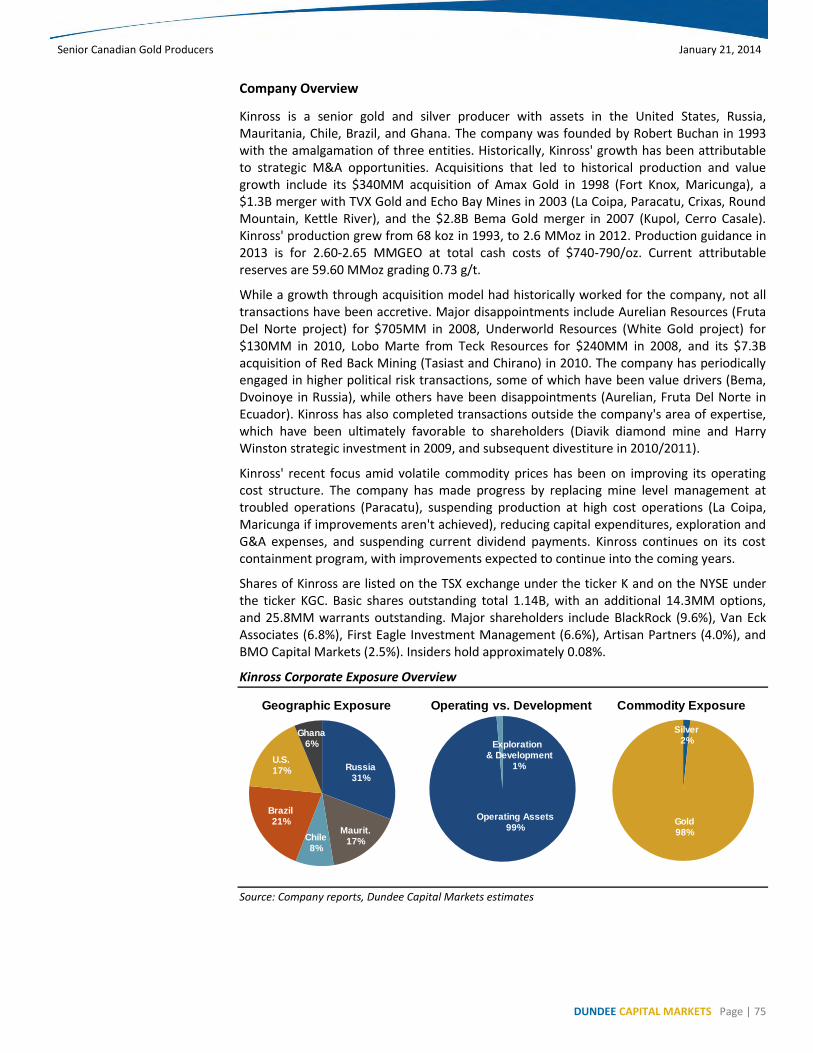

Company Overview ........................................................................................................................................................... 75

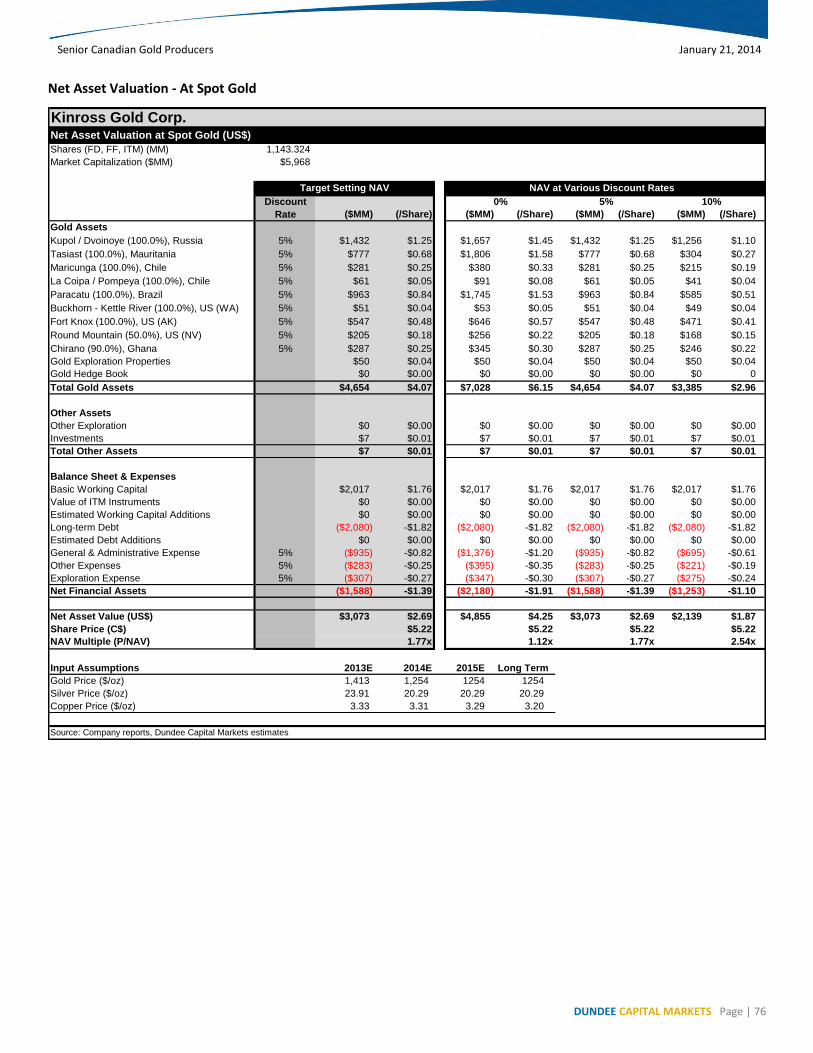

Net Asset Valuation - At Spot Gold .................................................................................................................................... 76

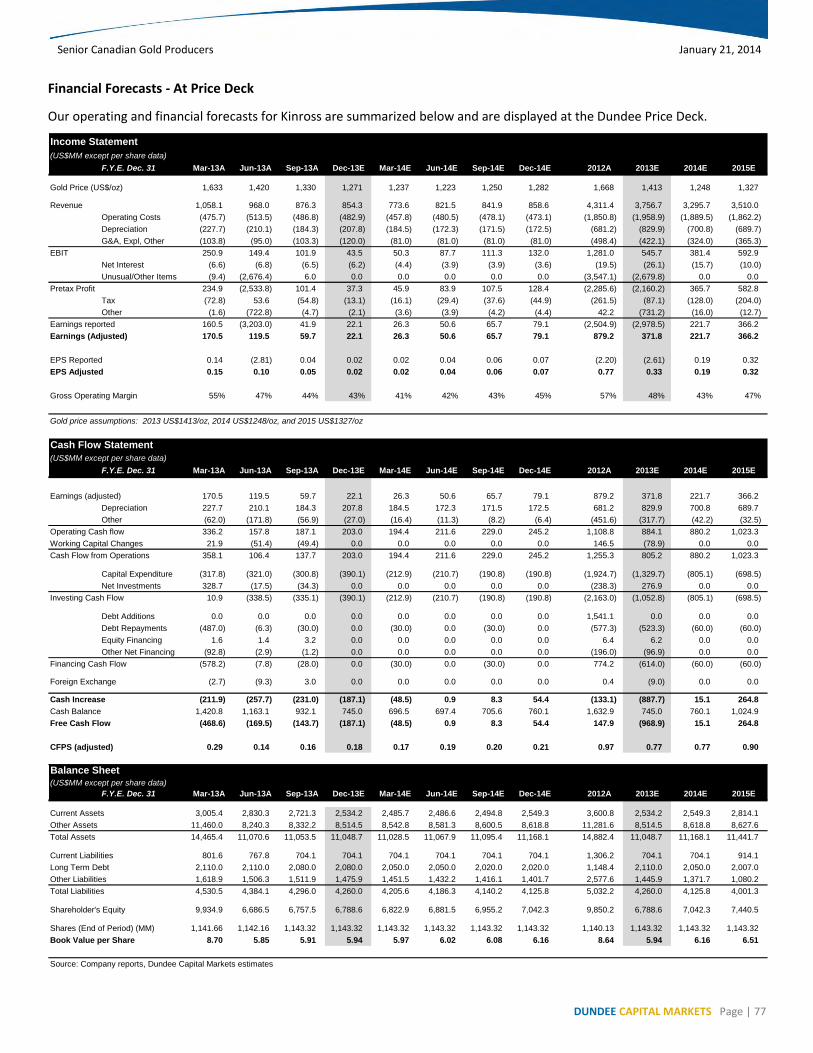

Financial Forecasts - At Price Deck .................................................................................................................................... 77

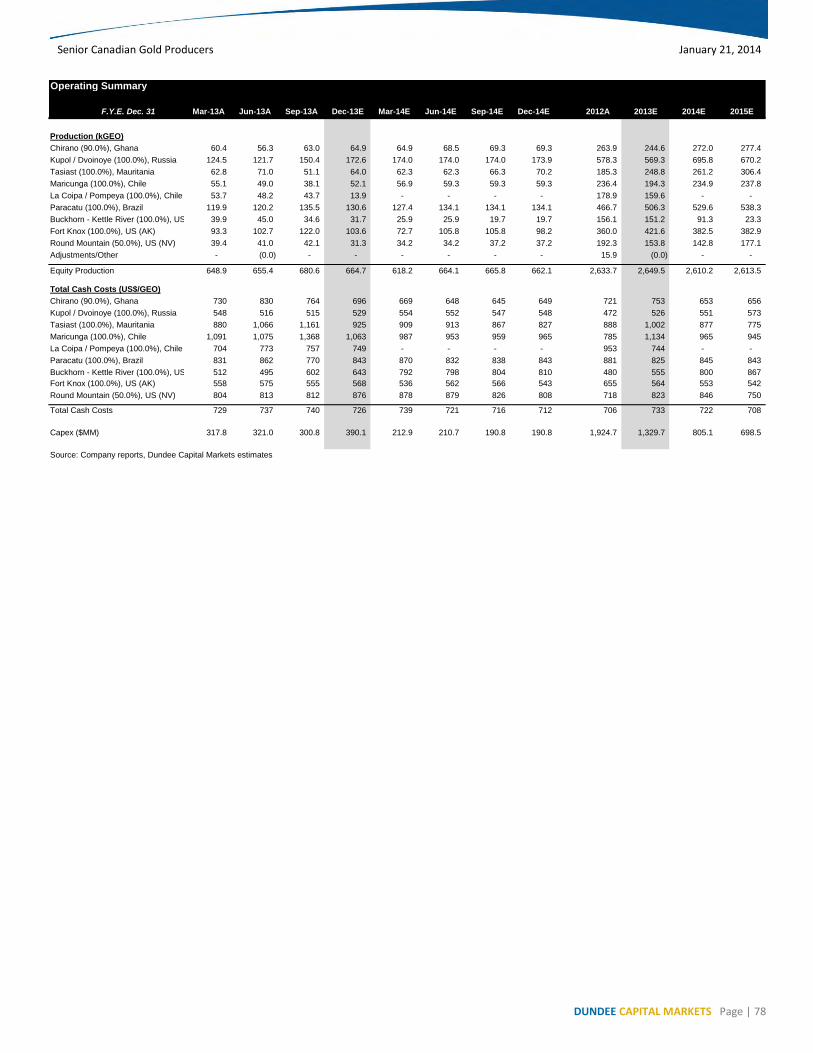

Key Assets .......................................................................................................................................................................... 79

Tasiast (100% ownership; 17% of NAV; Mauritania) .......................................................................................................... 79

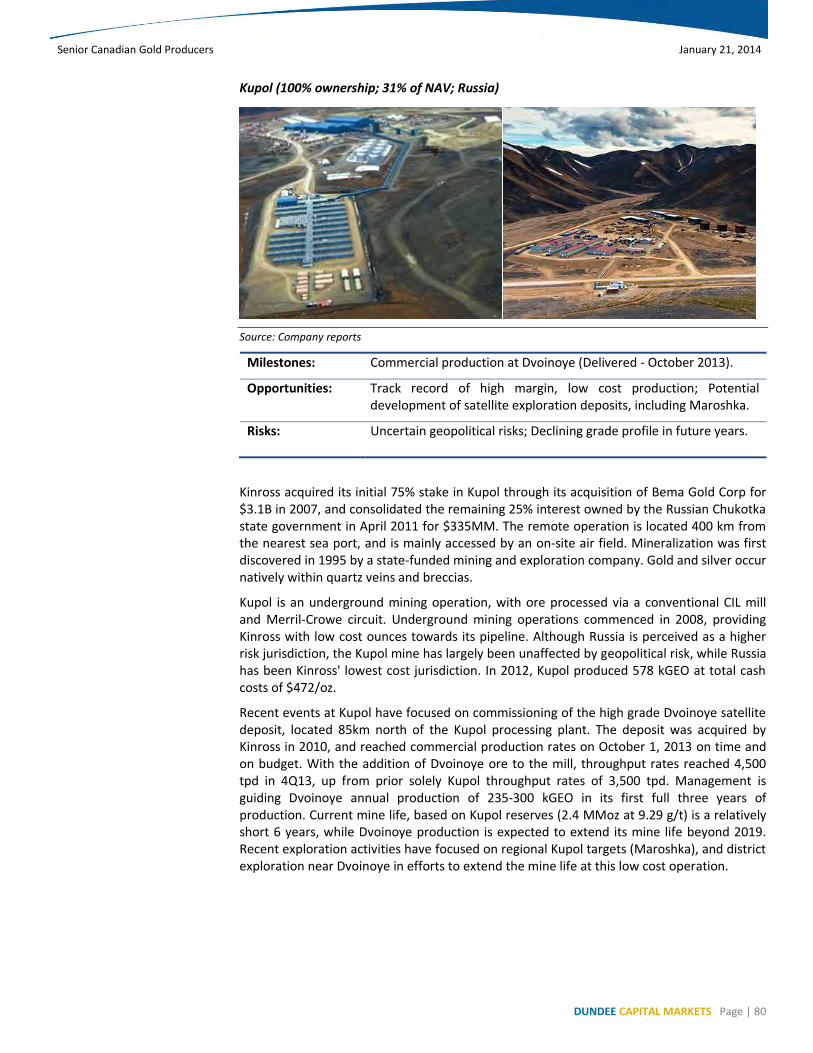

Kupol (100% ownership; 31% of NAV; Russia) .................................................................................................................... 80

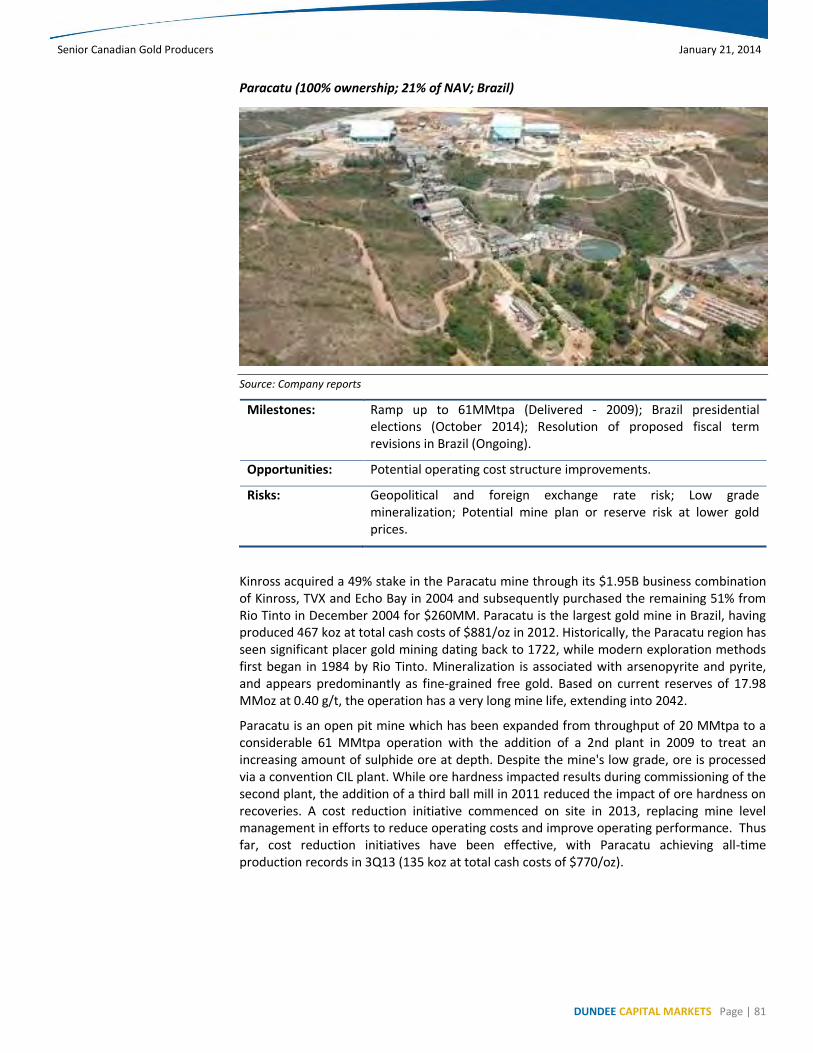

Paracatu (100% ownership; 21% of NAV; Brazil) ................................................................................................................ 81

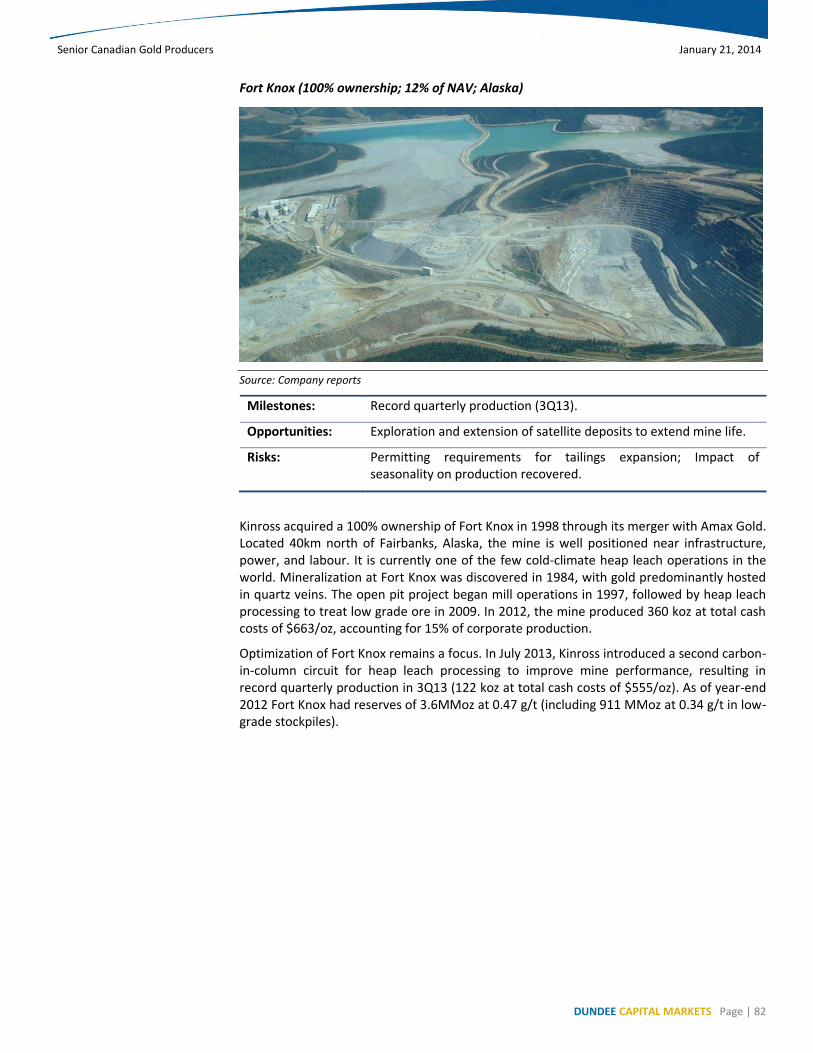

Fort Knox (100% ownership; 12% of NAV; Alaska) ............................................................................................................. 82

Other Operations ................................................................................................................................................................ 83

Risks ................................................................................................................................................................................... 84

QUARTERLY EPS & CFPS ESTIMATES……………..…………………………………………………………………………………………………………….…..86

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 4

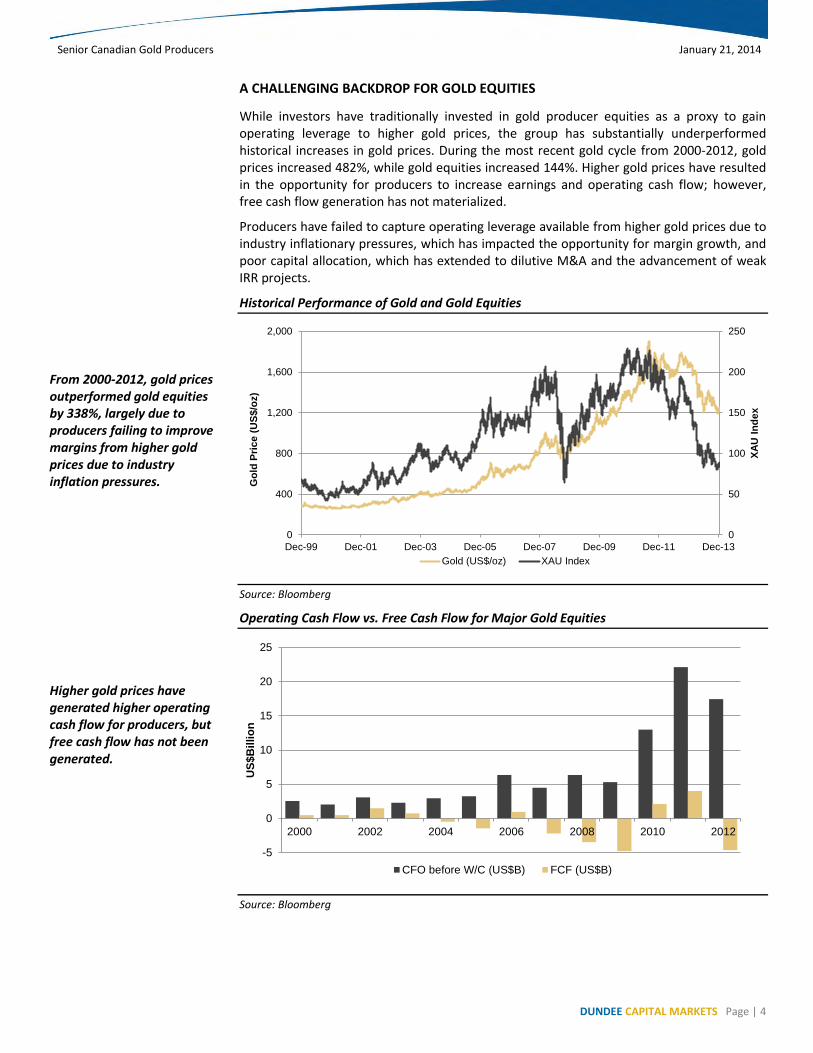

A CHALLENGING BACKDROP FOR GOLD EQUITIES

While investors have traditionally invested in gold producer equities as a proxy to gain operating leverage to higher gold prices, the group has substantially underperformed historical increases in gold prices. During the most recent gold cycle from 2000-2012, gold prices increased 482%, while gold equities increased 144%. Higher gold prices have resulted in the opportunity for producers to increase earnings and operating cash flow; however, free cash flow generation has not materialized.

Producers have failed to capture operating leverage available from higher gold prices due to industry inflationary pressures, which has impacted the opportunity for margin growth, and poor capital allocation, which has extended to dilutive M&A and the advancement of weak IRR projects.

Historical Performance of Gold and Gold Equities

Source: Bloomberg

Operating Cash Flow vs. Free Cash Flow for Major Gold Equities

Source: Bloomberg

0

50

100

150

200

250

0

400

800

1,200

1,600

2,000

Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13

XA

U I

nd

ex

Go

ld P

rice (

US

$/o

z)

Gold (US$/oz) XAU Index

-5

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012

US

$B

illio

n

CFO before W/C (US$B) FCF (US$B)

From 2000-2012, gold prices outperformed gold equities by 338%, largely due to producers failing to improve margins from higher gold prices due to industry inflation pressures.

Higher gold prices have generated higher operating cash flow for producers, but free cash flow has not been generated.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 5

DRIVERS FOR FUTURE RETURNS BEGINNING TO ALIGN

Dundee views the outlook for gold equities as improving based upon:

Increasing management emphasis on shareholder value creation, and, importantly, actions which are supportive of this direction.

Potential for higher margin reserves and production, at the expense of lower volumes and shorter mine lives.

Decreasing industry inflationary pressures, which have historically eroded the potential for margin growth.

Although past returns in the sector have been disappointing, encouraging signs of stability are beginning to materialize. Most importantly, value creation is now being measured in traditional investment metrics which would appeal to a broader investor base, including free cash flow and internal rate of return (at conservative gold prices). Although current valuation levels, in our view, are still not enticing to appeal to non-resource focused investors, we believe that potentially higher gold prices today would materialize in better returns for shareholders, unlike prior years.

While gold producer management teams have historically focused on shareholders, gold-specific industry metrics have traditionally focused on growth in resources and production. As a result of a deteriorating quality of the underlying drivers for these metrics, results have not translated to better financial results. Over the past decade, declining grades and rising operating as well as capital costs have resulted in stagnant margins, despite rising gold prices. Over this period, we estimate unit operating costs have increased by 156%, capital cost per unit of production output has increased 602%, while grade, representing the content of gold per unit of ore processed, has decreased by 44%.

Industry Processed Grades Have Decreased as Gold Prices Have Increased

Source: Company reports, Dundee Capital markets

-

2.5

5.0

7.5

10.0

2001 2003 2005 2007 2009 2011

Pro

cess

ed

Gra

de

(g

/t)

OP OP/UG UGOP = Open PitUG = Underground

We believe the outlook for gold equities is improving.

Declining processed grades have resulted in higher operating costs per ounce of production.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 6

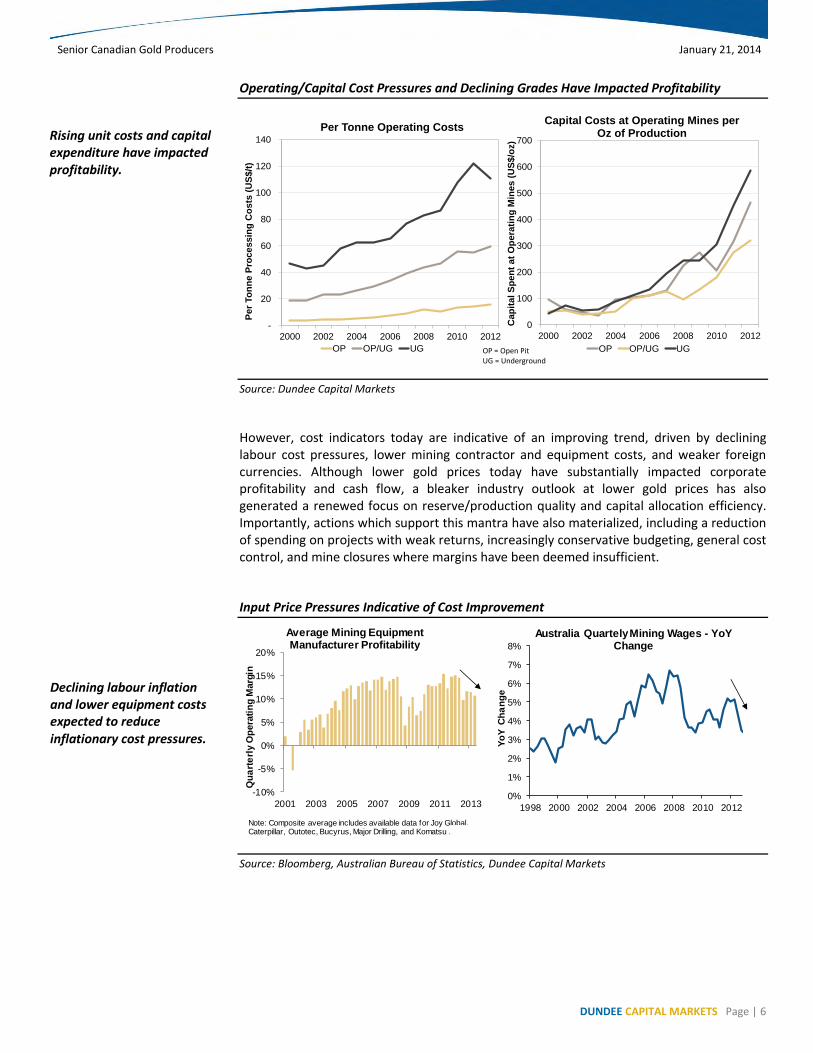

Operating/Capital Cost Pressures and Declining Grades Have Impacted Profitability

Source: Dundee Capital Markets

However, cost indicators today are indicative of an improving trend, driven by declining labour cost pressures, lower mining contractor and equipment costs, and weaker foreign currencies. Although lower gold prices today have substantially impacted corporate profitability and cash flow, a bleaker industry outlook at lower gold prices has also generated a renewed focus on reserve/production quality and capital allocation efficiency. Importantly, actions which support this mantra have also materialized, including a reduction of spending on projects with weak returns, increasingly conservative budgeting, general cost control, and mine closures where margins have been deemed insufficient.

Input Price Pressures Indicative of Cost Improvement

Source: Bloomberg, Australian Bureau of Statistics, Dundee Capital Markets

-

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012

Per

To

nn

e P

roce

ss

ing

Co

sts

(U

S$/t

)

Per Tonne Operating Costs

OP OP/UG UG

0

100

200

300

400

500

600

700

2000 2002 2004 2006 2008 2010 2012

Cap

ita

l S

pe

nt

at

Op

era

tin

g M

ine

s (

US

$/o

z)

Capital Costs at Operating Mines per Oz of Production

OP OP/UG UGOP = Open PitUG = Underground

0%

1%

2%

3%

4%

5%

6%

7%

8%

1998 2000 2002 2004 2006 2008 2010 2012

Yo

Y C

ha

ng

e

Australia Quartely Mining Wages - YoY Change

-10%

-5%

0%

5%

10%

15%

20%

2001 2003 2005 2007 2009 2011 2013

Qu

art

erl

y O

pera

tin

g M

arg

in

Average Mining Equipment Manufacturer Profitability

Note: Composite average includes available data for Joy Global, Caterpillar, Outotec, Bucyrus, Major Drilling, and Komatsu . Bucyrus

Declining labour inflation and lower equipment costs expected to reduce inflationary cost pressures.

Rising unit costs and capital expenditure have impacted profitability.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 7

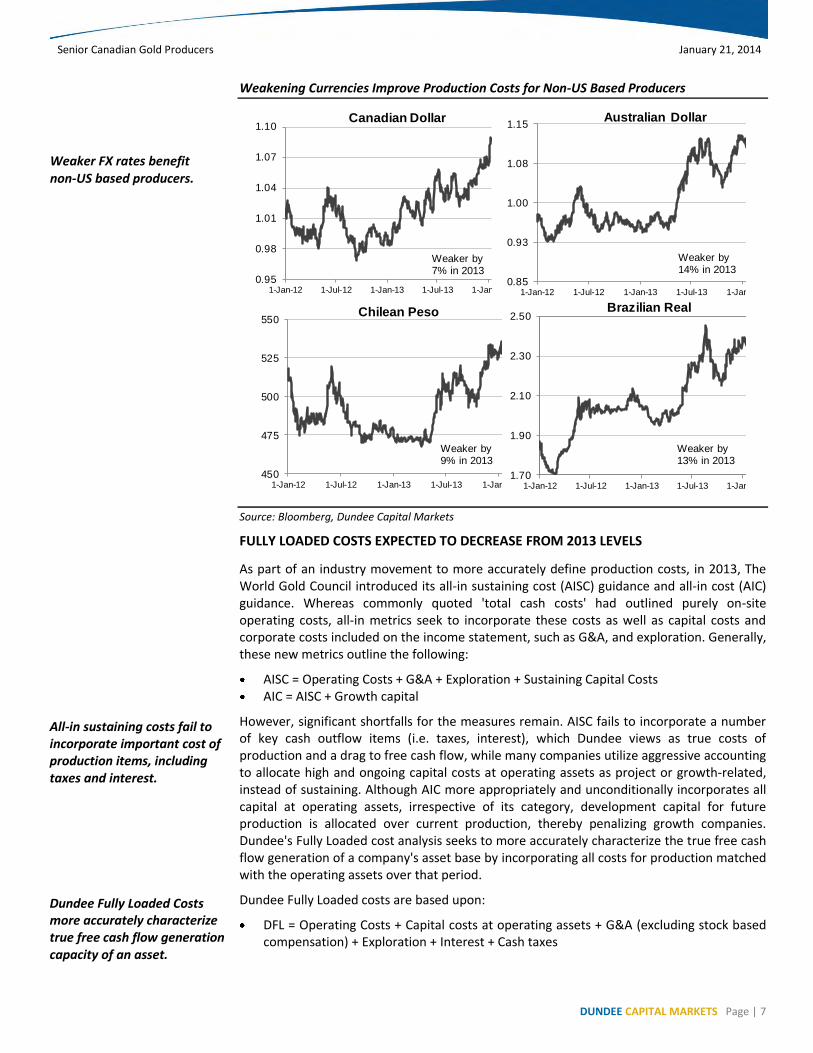

Weakening Currencies Improve Production Costs for Non-US Based Producers

Source: Bloomberg, Dundee Capital Markets

FULLY LOADED COSTS EXPECTED TO DECREASE FROM 2013 LEVELS

As part of an industry movement to more accurately define production costs, in 2013, The World Gold Council introduced its all-in sustaining cost (AISC) guidance and all-in cost (AIC) guidance. Whereas commonly quoted 'total cash costs' had outlined purely on-site operating costs, all-in metrics seek to incorporate these costs as well as capital costs and corporate costs included on the income statement, such as G&A, and exploration. Generally, these new metrics outline the following:

AISC = Operating Costs + G&A + Exploration + Sustaining Capital Costs AIC = AISC + Growth capital

However, significant shortfalls for the measures remain. AISC fails to incorporate a number of key cash outflow items (i.e. taxes, interest), which Dundee views as true costs of production and a drag to free cash flow, while many companies utilize aggressive accounting to allocate high and ongoing capital costs at operating assets as project or growth-related, instead of sustaining. Although AIC more appropriately and unconditionally incorporates all capital at operating assets, irrespective of its category, development capital for future production is allocated over current production, thereby penalizing growth companies. Dundee's Fully Loaded cost analysis seeks to more accurately characterize the true free cash flow generation of a company's asset base by incorporating all costs for production matched with the operating assets over that period.

Dundee Fully Loaded costs are based upon:

DFL = Operating Costs + Capital costs at operating assets + G&A (excluding stock based compensation) + Exploration + Interest + Cash taxes

Cad

-7%

CLP

-9%

0.95

0.98

1.01

1.04

1.07

1.10

1-Jan-12 1-Jul-12 1-Jan-13 1-Jul-13 1-Jan-14

Canadian Dollar

Weaker by 7% in 2013

0.85

0.93

1.00

1.08

1.15

1-Jan-12 1-Jul-12 1-Jan-13 1-Jul-13 1-Jan-14

Australian Dollar

Weaker by 14% in 2013

450

475

500

525

550

1-Jan-12 1-Jul-12 1-Jan-13 1-Jul-13 1-Jan-14

Chilean Peso

Weaker by 9% in 2013

1.70

1.90

2.10

2.30

2.50

1-Jan-12 1-Jul-12 1-Jan-13 1-Jul-13 1-Jan-14

Brazilian Real

Weaker by 13% in 2013

All-in sustaining costs fail to incorporate important cost of production items, including taxes and interest.

Dundee Fully Loaded Costs more accurately characterize true free cash flow generation capacity of an asset.

Weaker FX rates benefit non-US based producers.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 8

Undoubtedly, there is no one metric which will provide accurate insight for true production costs. Weaknesses for the Fully Loaded cost estimate include:

Excluding stock based compensation from costs, which is a true cost of production and dilutive to shareholders, but does not impact cash flow.

Incorporating cash taxes as a cost of production, which may be more irregular than tax expense and may understate costs where tax deferral is transient.

Including discretionary exploration costs as costs of production, which also applies to AISC/AIC.

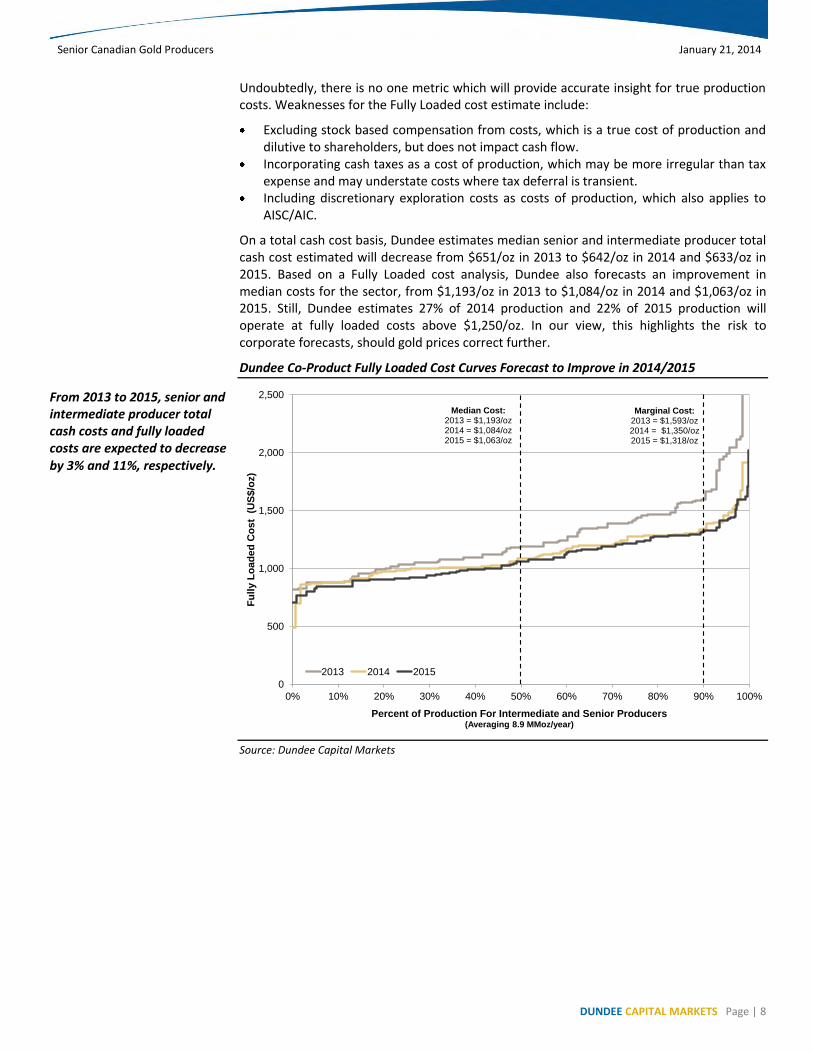

On a total cash cost basis, Dundee estimates median senior and intermediate producer total cash cost estimated will decrease from $651/oz in 2013 to $642/oz in 2014 and $633/oz in 2015. Based on a Fully Loaded cost analysis, Dundee also forecasts an improvement in median costs for the sector, from $1,193/oz in 2013 to $1,084/oz in 2014 and $1,063/oz in 2015. Still, Dundee estimates 27% of 2014 production and 22% of 2015 production will operate at fully loaded costs above $1,250/oz. In our view, this highlights the risk to corporate forecasts, should gold prices correct further.

Dundee Co-Product Fully Loaded Cost Curves Forecast to Improve in 2014/2015

Source: Dundee Capital Markets

0

500

1,000

1,500

2,000

2,500

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fu

lly L

oad

ed

Co

st

(U

S$/o

z)

Percent of Production For Intermediate and Senior Producers (Averaging 8.9 MMoz/year)

2013 2014 2015

Median Cost:2013 = $1,193/oz2014 = $1,084/oz2015 = $1,063/oz

Marginal Cost:2013 = $1,593/oz2014 = $1,350/oz2015 = $1,318/oz

From 2013 to 2015, senior and intermediate producer total cash costs and fully loaded costs are expected to decrease by 3% and 11%, respectively.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 9

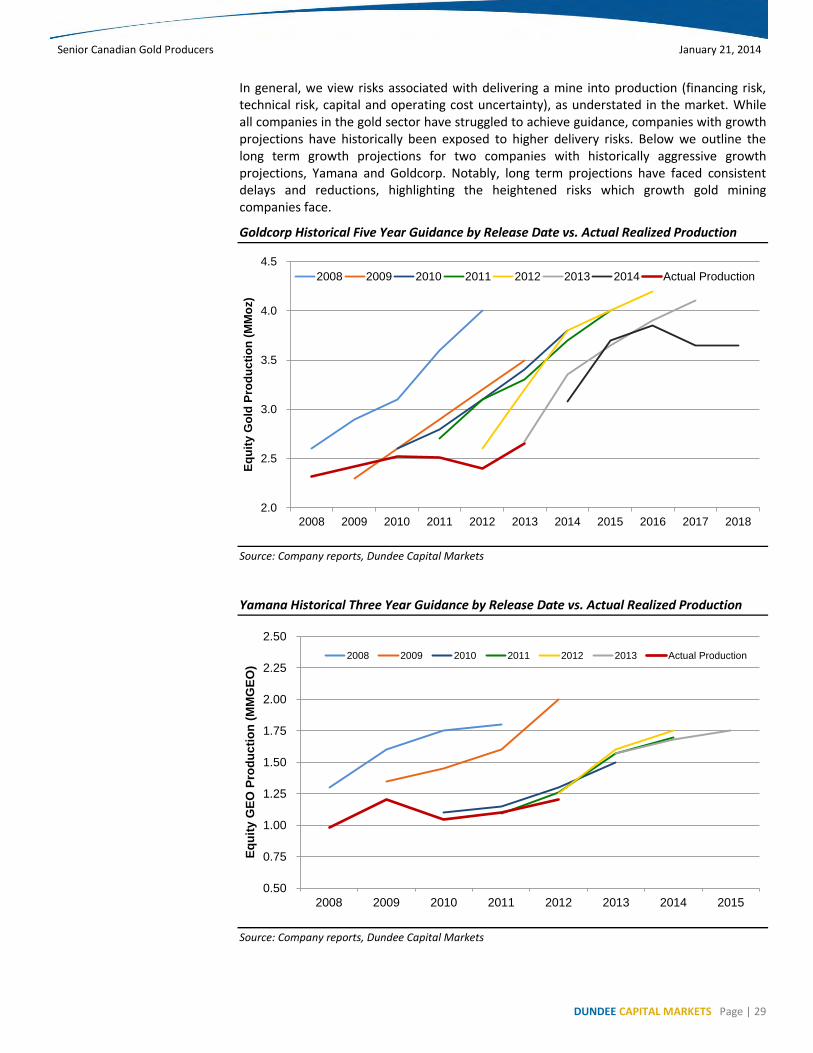

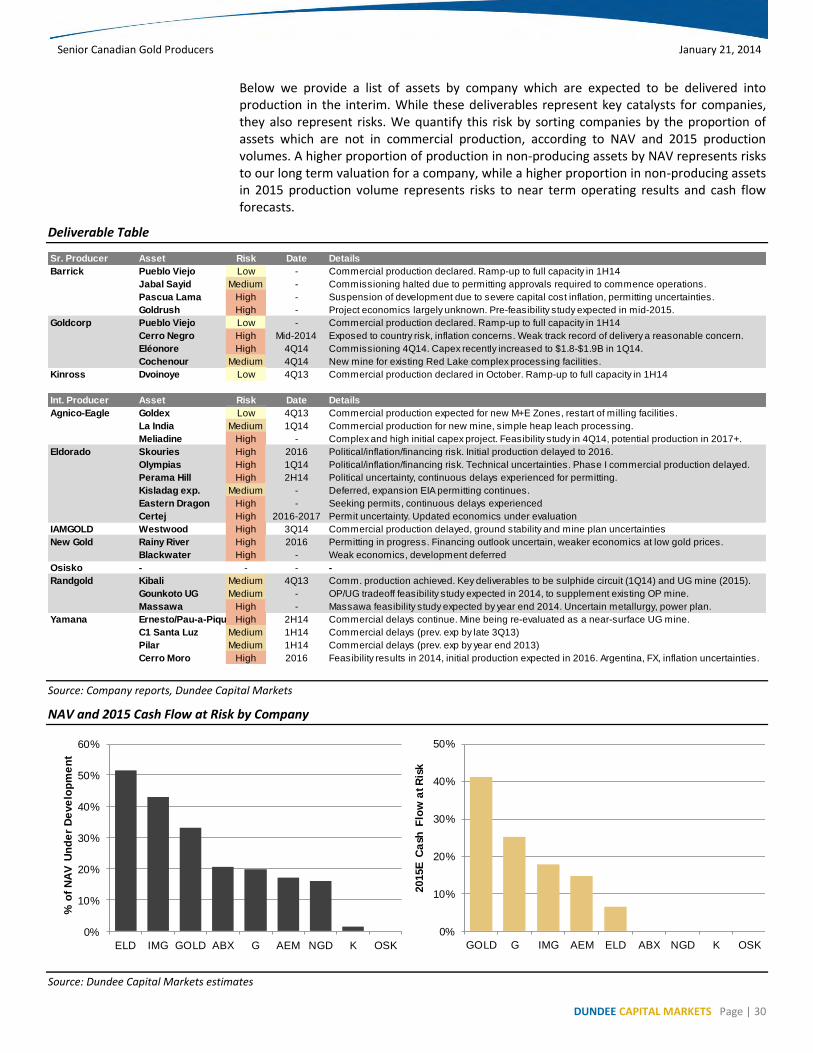

INDUSTRY CHALLENGES REMAIN, THREATENING THE OUTLOOK

Although we believe improving trends are materializing, sector risks remain elevated, including:

Weak industry free cash flow prospects at current gold prices, and uninspiring valuation levels to attract broader investment.

High sector debt levels, which reduces corporate financial flexibility. Potential downside risks, should gold price correct further.

Lower gold prices have impacted industry profitability and free cash flow, defined as operating cash flow, less capital expenditure. At our 2014 price deck, we estimate our senior and intermediate coverage universe will generate a free cash flow yield of 0.1%. Our senior and intermediate coverage universe would generate similar marginal free cash flow at current spot gold prices of $1,254/oz. To compete with the broader investment universe, which offered a free cash flow yield of 6.8% in 2013, we estimate gold prices would be required to average >$1,600/oz in 2014, compared to our forecast for $1,248/oz, and current spot gold prices of $1,254/oz.

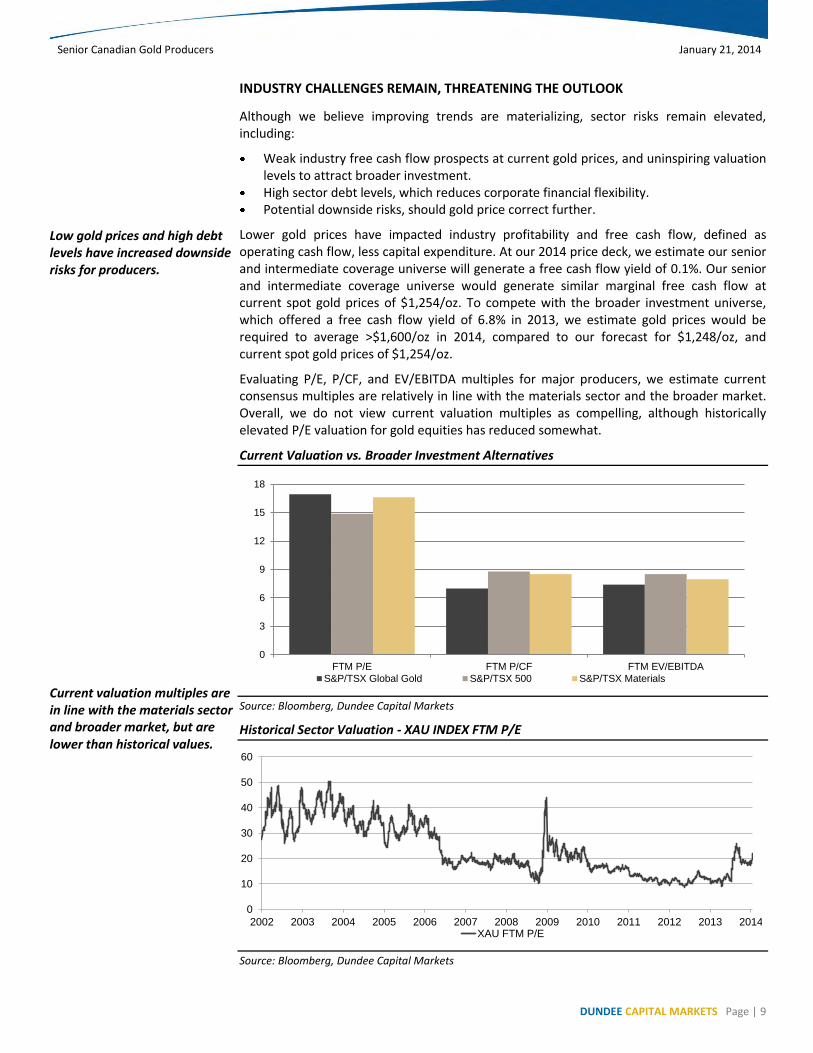

Evaluating P/E, P/CF, and EV/EBITDA multiples for major producers, we estimate current consensus multiples are relatively in line with the materials sector and the broader market. Overall, we do not view current valuation multiples as compelling, although historically elevated P/E valuation for gold equities has reduced somewhat.

Current Valuation vs. Broader Investment Alternatives

Source: Bloomberg, Dundee Capital Markets

Historical Sector Valuation - XAU INDEX FTM P/E

Source: Bloomberg, Dundee Capital Markets

0

3

6

9

12

15

18

FTM P/E FTM P/CF FTM EV/EBITDA

S&P/TSX Global Gold S&P/TSX 500 S&P/TSX Materials

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014XAU FTM P/E

Low gold prices and high debt levels have increased downside risks for producers.

Current valuation multiples are in line with the materials sector and broader market, but are lower than historical values.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 10

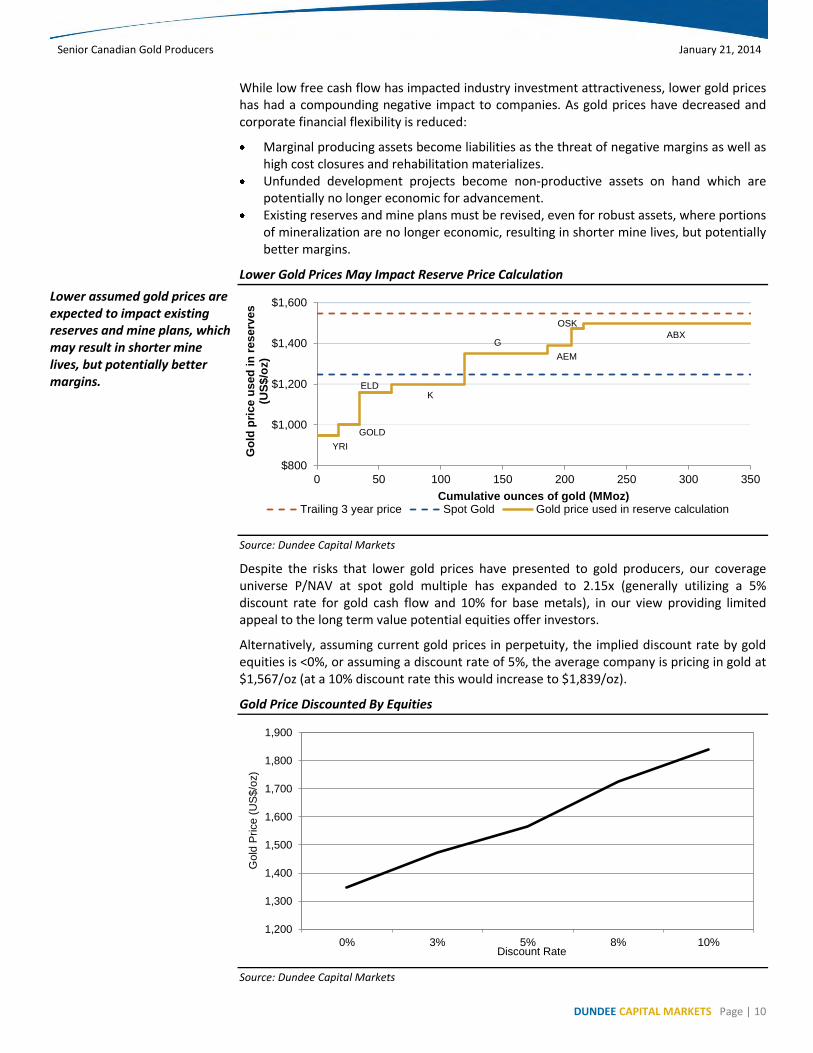

While low free cash flow has impacted industry investment attractiveness, lower gold prices has had a compounding negative impact to companies. As gold prices have decreased and corporate financial flexibility is reduced:

Marginal producing assets become liabilities as the threat of negative margins as well as high cost closures and rehabilitation materializes.

Unfunded development projects become non-productive assets on hand which are potentially no longer economic for advancement.

Existing reserves and mine plans must be revised, even for robust assets, where portions of mineralization are no longer economic, resulting in shorter mine lives, but potentially better margins.

Lower Gold Prices May Impact Reserve Price Calculation

Source: Dundee Capital Markets

Despite the risks that lower gold prices have presented to gold producers, our coverage universe P/NAV at spot gold multiple has expanded to 2.15x (generally utilizing a 5% discount rate for gold cash flow and 10% for base metals), in our view providing limited appeal to the long term value potential equities offer investors.

Alternatively, assuming current gold prices in perpetuity, the implied discount rate by gold equities is <0%, or assuming a discount rate of 5%, the average company is pricing in gold at $1,567/oz (at a 10% discount rate this would increase to $1,839/oz).

Gold Price Discounted By Equities

Source: Dundee Capital Markets

GOLD

ELD

YRI

K

G

AEM

OSK

$800

$1,000

$1,200

$1,400

$1,600

0 50 100 150 200 250 300 350

Go

ld p

rice u

sed

in

reserv

es

(US

$/o

z)

Cumulative ounces of gold (MMoz)Trailing 3 year price Spot Gold Gold price used in reserve calculation

ABX

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

0% 3% 5% 8% 10%

Go

ld P

rice

(U

S$

/oz)

Discount Rate

Lower assumed gold prices are expected to impact existing reserves and mine plans, which may result in shorter mine lives, but potentially better margins.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 11

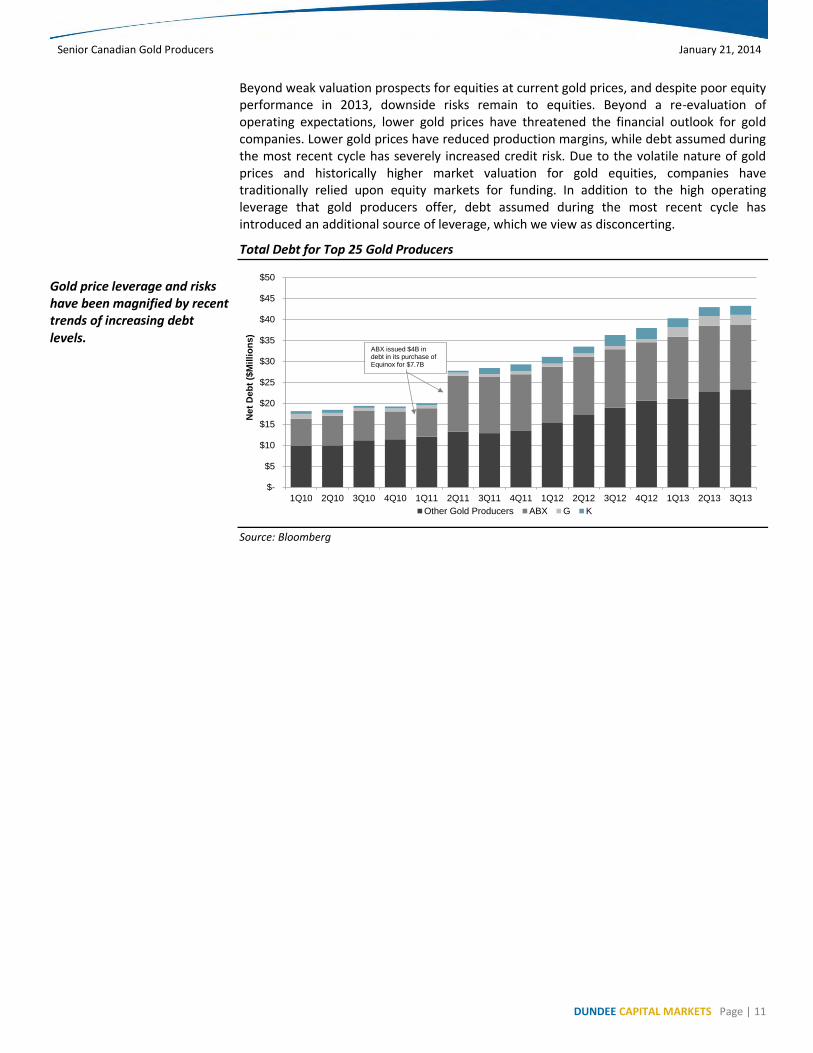

Beyond weak valuation prospects for equities at current gold prices, and despite poor equity performance in 2013, downside risks remain to equities. Beyond a re-evaluation of operating expectations, lower gold prices have threatened the financial outlook for gold companies. Lower gold prices have reduced production margins, while debt assumed during the most recent cycle has severely increased credit risk. Due to the volatile nature of gold prices and historically higher market valuation for gold equities, companies have traditionally relied upon equity markets for funding. In addition to the high operating leverage that gold producers offer, debt assumed during the most recent cycle has introduced an additional source of leverage, which we view as disconcerting.

Total Debt for Top 25 Gold Producers

Source: Bloomberg

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Net

Deb

t ($

Mil

lio

ns)

Other Gold Producers ABX G K

ABX issued $4B in debt in its purchase of Equinox for $7.7B

Gold price leverage and risks have been magnified by recent trends of increasing debt levels.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 12

LONG-TERM GOLD PRICE OUTLOOK POSITIVE, INTERIM PROJECTIONS SUBDUED

Dundee forecasts currently incorporate a long term supportive outlook for gold prices, but suggest no near-term recovery from current price levels. Dundee forecasts incorporate gold prices averaging $1,248/oz in 2014, $1,327/oz in 2015, and a long term gold price assumption of $1,325/oz. Our near term forecasts are in line with the current spot gold price of $1,254/oz, while our long term forecast is $1,325/oz.

Dundee's near-term gold price assumptions are calculated based on a probability weighted estimate of three different gold price scenarios:

Scenario A - Assumes the U.S. dollar will rise significantly over the next six quarters, the official sector is a net seller of gold, mine output rises at a lower rate, and hedging is expected to recommence.

Scenario B - Assumes the U.S. dollar will rise marginally over the next six quarters, the official sector is a net buyer of gold, mine output rises at a moderate rate, and hedging is expected to recommence (although more moderately than Scenario A).

Scenario C - Assumes the U.S. dollar will weaken over the next six quarters, the official sector is a net buyer of gold, mine output rises at a higher rate, and no hedging is expected.

Dundee Gold Probability Weighted Price Forecasts and Scenario Analysis

Source: Dundee Capital Markets

Dundee is of the view that the current selling pressure for gold represents a mid-cycle correction for the metal and that the long term outlook remains positive for gold. This is based upon:

Loose monetary policy continuing to support the current deleveraging cycle and that policy tightening will not occur quickly.

Ongoing investment in gold continuing from central bank demand (excessive FX reserves, diversification) and consumer demand (Asian market deregulation).

Investor and central bank holdings in gold being low relative to historical quantities.

Largely, these bullish factors are similar factors which contributed to the most recent bull cycle. Risks to our thesis are:

Real interest rates rise, a consequence of declining monetary easing and potential global liquidity contraction, which may result in a strengthening US dollar.

The global economy remains sluggish, commodity demand is weak, and a trend of disinflation is in place.

Gold inventories are sold for liquidity purposes or sold as other investments are preferred by investors.

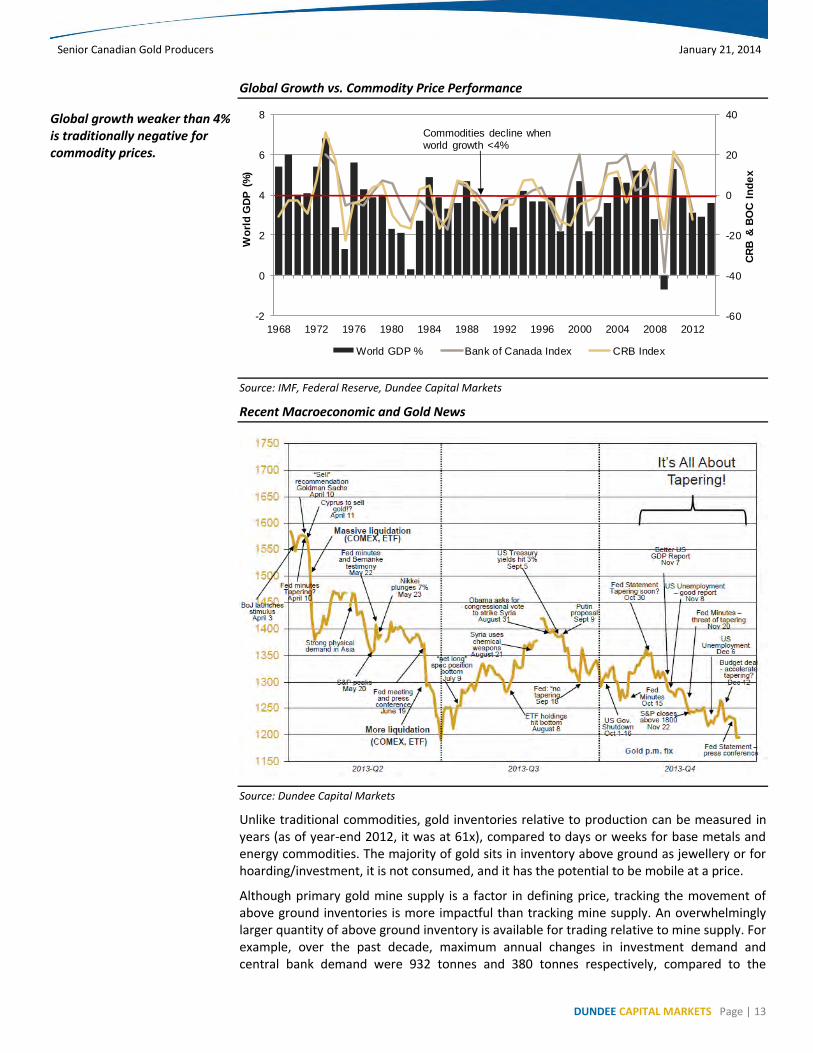

Dundee views the outlook for the broader commodity space to be challenging, given low, but improving, prospects for global growth. Historically, global growth levels below 4% have been poor for commodity price performance. Dundee views 1H14 as a period of weaker growth and sees risks to commodity prices over this time frame.

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Scenario A $1,123 $1,091 $1,060 $1,029 $1,009 $990

B $1,289 $1,279 $1,311 $1,341 $1,388 $1,399

C $1,385 $1,403 $1,490 $1,572 $1,688 $1,756

Probability A 40% 40% 35% 30% 30% 30%

B 45% 45% 50% 55% 55% 55%

C 15% 15% 15% 15% 15% 15%

Probability-Weighted $1,237 $1,223 $1,250 $1,282 $1,319 $1,330

Dundee forecasts a 2014 gold price of $1,248/oz.

Dundee sees central bank and investment demand, as well as ongoing loose monetary policy, as supportive for gold prices.

Rising real interest rates, slower global growth, and alternative investment preferences are risks for gold.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 13

Global Growth vs. Commodity Price Performance

Source: IMF, Federal Reserve, Dundee Capital Markets

Recent Macroeconomic and Gold News

Source: Dundee Capital Markets

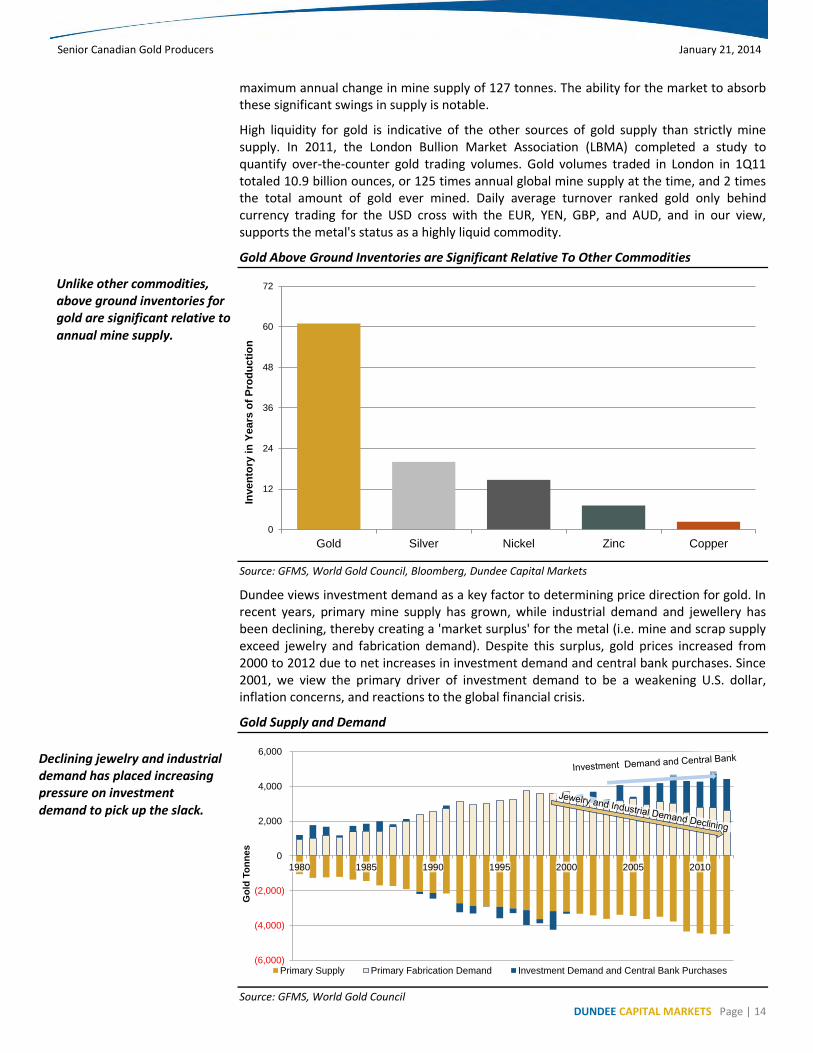

Unlike traditional commodities, gold inventories relative to production can be measured in years (as of year-end 2012, it was at 61x), compared to days or weeks for base metals and energy commodities. The majority of gold sits in inventory above ground as jewellery or for hoarding/investment, it is not consumed, and it has the potential to be mobile at a price.

Although primary gold mine supply is a factor in defining price, tracking the movement of above ground inventories is more impactful than tracking mine supply. An overwhelmingly larger quantity of above ground inventory is available for trading relative to mine supply. For example, over the past decade, maximum annual changes in investment demand and central bank demand were 932 tonnes and 380 tonnes respectively, compared to the

-60

-40

-20

0

20

40

-2

0

2

4

6

8

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012

CR

B &

BO

C I

nd

ex

Wo

rld

GD

P (

%)

World GDP % Bank of Canada Index CRB Index

Commodities decline when world growth <4%

Global growth weaker than 4% is traditionally negative for commodity prices.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 14

maximum annual change in mine supply of 127 tonnes. The ability for the market to absorb these significant swings in supply is notable.

High liquidity for gold is indicative of the other sources of gold supply than strictly mine supply. In 2011, the London Bullion Market Association (LBMA) completed a study to quantify over-the-counter gold trading volumes. Gold volumes traded in London in 1Q11 totaled 10.9 billion ounces, or 125 times annual global mine supply at the time, and 2 times the total amount of gold ever mined. Daily average turnover ranked gold only behind currency trading for the USD cross with the EUR, YEN, GBP, and AUD, and in our view, supports the metal's status as a highly liquid commodity.

Gold Above Ground Inventories are Significant Relative To Other Commodities

Source: GFMS, World Gold Council, Bloomberg, Dundee Capital Markets

Dundee views investment demand as a key factor to determining price direction for gold. In recent years, primary mine supply has grown, while industrial demand and jewellery has been declining, thereby creating a 'market surplus' for the metal (i.e. mine and scrap supply exceed jewelry and fabrication demand). Despite this surplus, gold prices increased from 2000 to 2012 due to net increases in investment demand and central bank purchases. Since 2001, we view the primary driver of investment demand to be a weakening U.S. dollar, inflation concerns, and reactions to the global financial crisis.

Gold Supply and Demand

Source: GFMS, World Gold Council

0

12

24

36

48

60

72

Gold Silver Nickel Zinc Copper

Inve

nto

ry i

n Y

ea

rs o

f P

rod

uc

tio

n

(6,000)

(4,000)

(2,000)

0

2,000

4,000

6,000

1980 1985 1990 1995 2000 2005 2010

Go

ld T

on

ne

s

Primary Supply Primary Fabrication Demand Investment Demand and Central Bank Purchases

Unlike other commodities, above ground inventories for gold are significant relative to annual mine supply.

Declining jewelry and industrial demand has placed increasing pressure on investment demand to pick up the slack.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 15

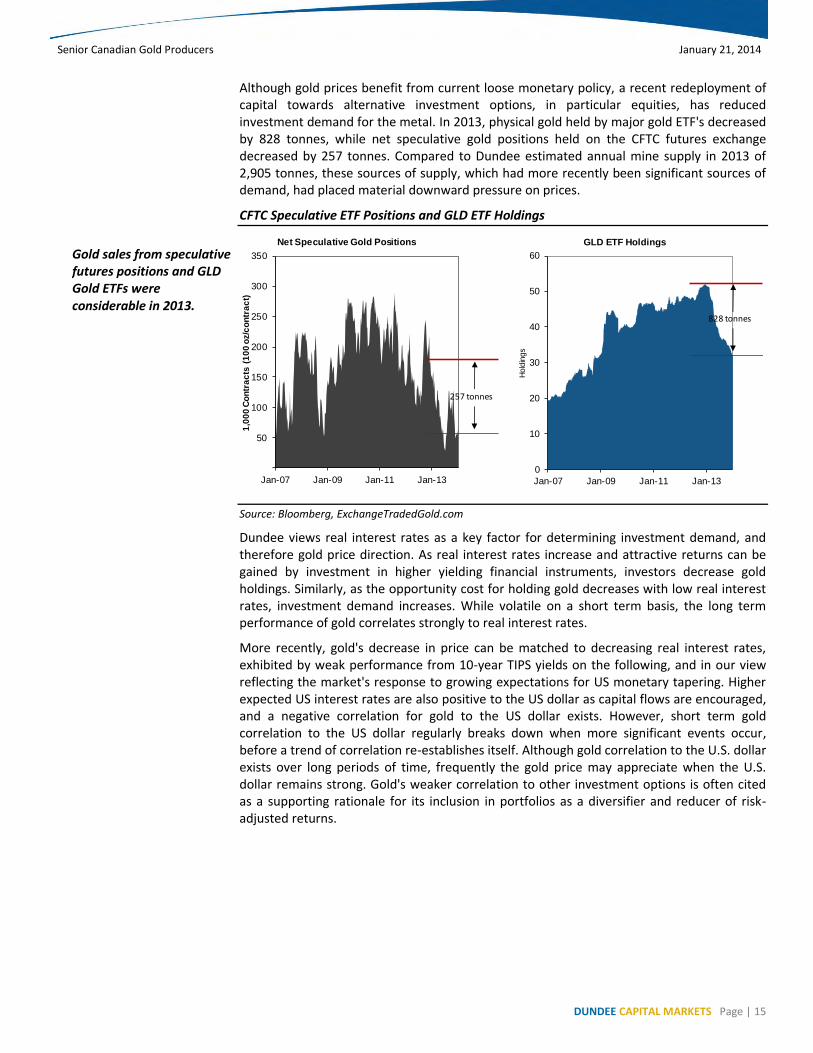

Although gold prices benefit from current loose monetary policy, a recent redeployment of capital towards alternative investment options, in particular equities, has reduced investment demand for the metal. In 2013, physical gold held by major gold ETF's decreased by 828 tonnes, while net speculative gold positions held on the CFTC futures exchange decreased by 257 tonnes. Compared to Dundee estimated annual mine supply in 2013 of 2,905 tonnes, these sources of supply, which had more recently been significant sources of demand, had placed material downward pressure on prices.

CFTC Speculative ETF Positions and GLD ETF Holdings

Source: Bloomberg, ExchangeTradedGold.com

Dundee views real interest rates as a key factor for determining investment demand, and therefore gold price direction. As real interest rates increase and attractive returns can be gained by investment in higher yielding financial instruments, investors decrease gold holdings. Similarly, as the opportunity cost for holding gold decreases with low real interest rates, investment demand increases. While volatile on a short term basis, the long term performance of gold correlates strongly to real interest rates.

More recently, gold's decrease in price can be matched to decreasing real interest rates, exhibited by weak performance from 10-year TIPS yields on the following, and in our view reflecting the market's response to growing expectations for US monetary tapering. Higher expected US interest rates are also positive to the US dollar as capital flows are encouraged, and a negative correlation for gold to the US dollar exists. However, short term gold correlation to the US dollar regularly breaks down when more significant events occur, before a trend of correlation re-establishes itself. Although gold correlation to the U.S. dollar exists over long periods of time, frequently the gold price may appreciate when the U.S. dollar remains strong. Gold's weaker correlation to other investment options is often cited as a supporting rationale for its inclusion in portfolios as a diversifier and reducer of risk-adjusted returns.

50

100

150

200

250

300

350

Jan-07 Jan-09 Jan-11 Jan-13

1,0

00

Co

ntr

ac

ts (

10

0 o

z/c

on

tra

ct)

Net Speculative Gold Positions

257 tonnes

0

10

20

30

40

50

60

Jan-07 Jan-09 Jan-11 Jan-13

Hold

ings

GLD ETF Holdings

828 tonnes

Gold sales from speculative futures positions and GLD Gold ETFs were considerable in 2013.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 16

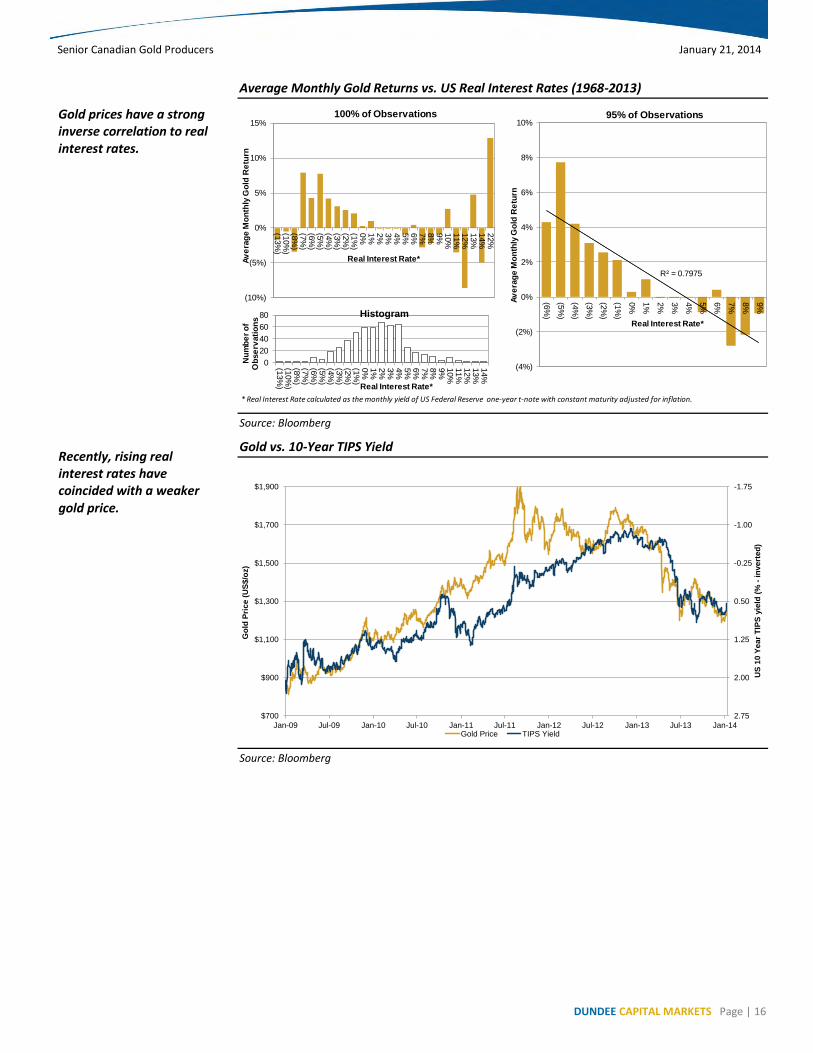

Average Monthly Gold Returns vs. US Real Interest Rates (1968-2013)

Source: Bloomberg

Gold vs. 10-Year TIPS Yield

Source: Bloomberg

* Real Interest Rate calculated as the monthly yield of US Federal Reserve one-year t-note with constant maturity adjusted for inflation.

(10%)

(5%)

0%

5%

10%

15%

(13%

)(1

0%

)(8

%)

(7%

)(6

%)

(5%

)(4

%)

(3%

)(2

%)

(1%

)0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

22%

Av

era

ge

Mo

nth

ly G

old

Re

turn

Real Interest Rate*

100% of Observations

0

20

40

60

80

(13%

)(1

0%

)(8

%)

(7%

)(6

%)

(5%

)(4

%)

(3%

)(2

%)

(1%

)0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

Nu

mb

er

of

Ob

se

rvati

on

s

Real Interest Rate*

Histogram

R² = 0.7975

(4%)

(2%)

0%

2%

4%

6%

8%

10%

(6%

)

(5%

)

(4%

)

(3%

)

(2%

)

(1%

)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Av

era

ge

Mo

nth

ly G

old

Re

turn

Real Interest Rate*

95% of Observations

-1.75

-1.00

-0.25

0.50

1.25

2.00

2.75$700

$900

$1,100

$1,300

$1,500

$1,700

$1,900

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

US

10 Y

ear

TIP

S y

ield

(%

-in

ve

rte

d)

Go

ld P

ric

e (

US

$/o

z)

Gold Price TIPS Yield

Gold prices have a strong inverse correlation to real interest rates.

Recently, rising real interest rates have coincided with a weaker gold price.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 17

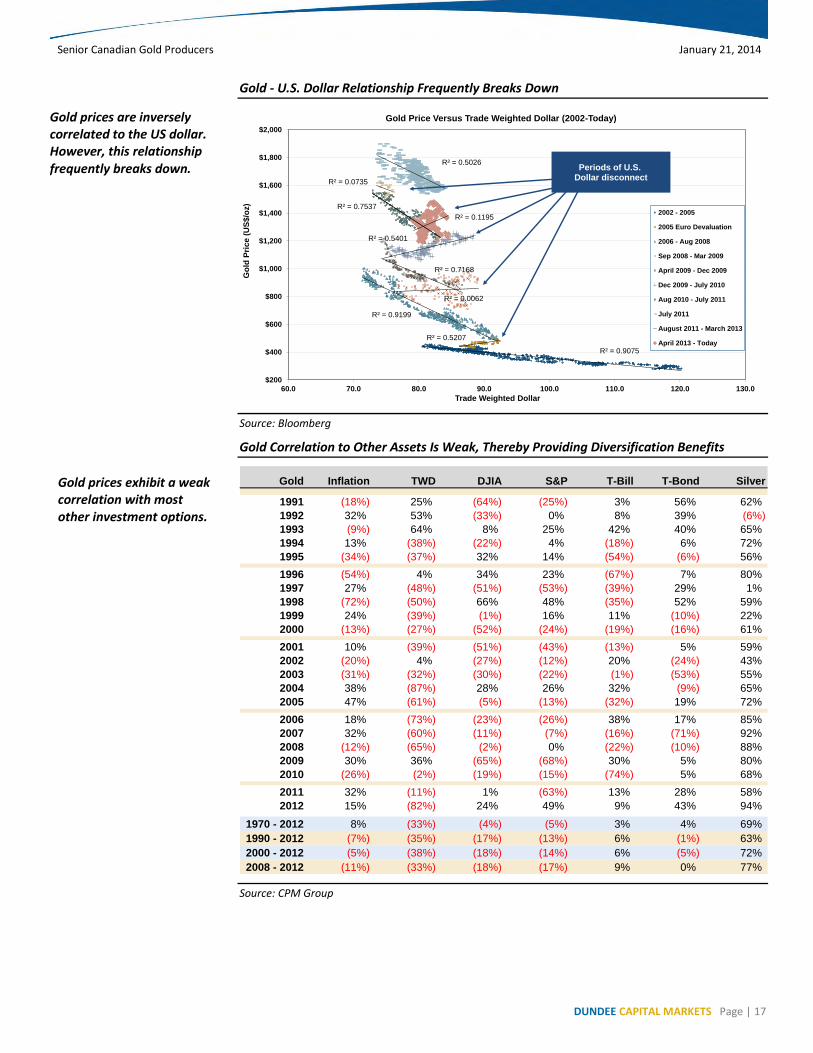

Gold - U.S. Dollar Relationship Frequently Breaks Down

Source: Bloomberg

Gold Correlation to Other Assets Is Weak, Thereby Providing Diversification Benefits

Source: CPM Group

R² = 0.9075

R² = 0.5207

R² = 0.9199

R² = 0.0062

R² = 0.7168

R² = 0.5401

R² = 0.7537

R² = 0.0735

R² = 0.5026

R² = 0.1195

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

60.0 70.0 80.0 90.0 100.0 110.0 120.0 130.0

Go

ld P

rice (

US

$/o

z)

Trade Weighted Dollar

Gold Price Versus Trade Weighted Dollar (2002-Today)

2002 - 2005

2005 Euro Devaluation

2006 - Aug 2008

Sep 2008 - Mar 2009

April 2009 - Dec 2009

Dec 2009 - July 2010

Aug 2010 - July 2011

July 2011

August 2011 - March 2013

April 2013 - Today

Periods of U.S. Dollar disconnect

Gold Inflation TWD DJIA S&P T-Bill T-Bond Silver

1991 (18%) 25% (64%) (25%) 3% 56% 62%

1992 32% 53% (33%) 0% 8% 39% (6%)

1993 (9%) 64% 8% 25% 42% 40% 65%

1994 13% (38%) (22%) 4% (18%) 6% 72%

1995 (34%) (37%) 32% 14% (54%) (6%) 56%

1996 (54%) 4% 34% 23% (67%) 7% 80%

1997 27% (48%) (51%) (53%) (39%) 29% 1%

1998 (72%) (50%) 66% 48% (35%) 52% 59%

1999 24% (39%) (1%) 16% 11% (10%) 22%

2000 (13%) (27%) (52%) (24%) (19%) (16%) 61%

2001 10% (39%) (51%) (43%) (13%) 5% 59%

2002 (20%) 4% (27%) (12%) 20% (24%) 43%

2003 (31%) (32%) (30%) (22%) (1%) (53%) 55%

2004 38% (87%) 28% 26% 32% (9%) 65%

2005 47% (61%) (5%) (13%) (32%) 19% 72%

2006 18% (73%) (23%) (26%) 38% 17% 85%

2007 32% (60%) (11%) (7%) (16%) (71%) 92%

2008 (12%) (65%) (2%) 0% (22%) (10%) 88%

2009 30% 36% (65%) (68%) 30% 5% 80%

2010 (26%) (2%) (19%) (15%) (74%) 5% 68%

2011 32% (11%) 1% (63%) 13% 28% 58%

2012 15% (82%) 24% 49% 9% 43% 94%

1970 - 2012 8% (33%) (4%) (5%) 3% 4% 69%

1990 - 2012 (7%) (35%) (17%) (13%) 6% (1%) 63%

2000 - 2012 (5%) (38%) (18%) (14%) 6% (5%) 72%

2008 - 2012 (11%) (33%) (18%) (17%) 9% 0% 77%

Gold prices are inversely correlated to the US dollar. However, this relationship frequently breaks down.

Gold prices exhibit a weak correlation with most other investment options.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 18

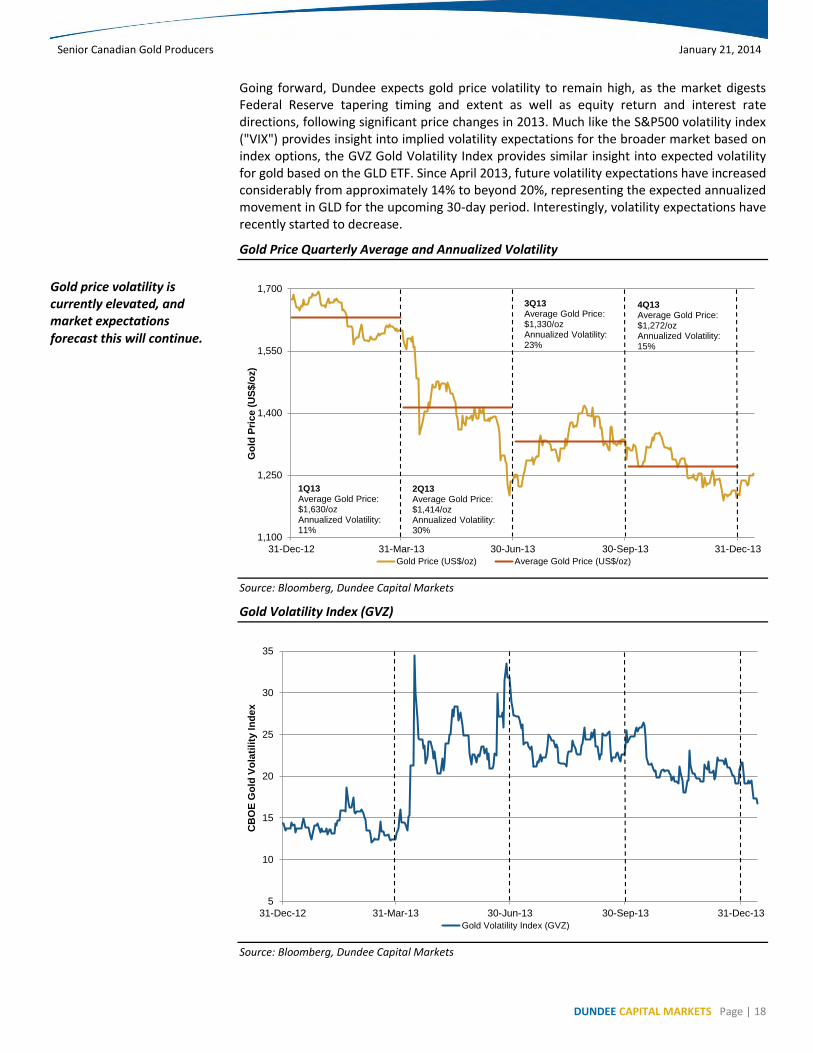

Going forward, Dundee expects gold price volatility to remain high, as the market digests Federal Reserve tapering timing and extent as well as equity return and interest rate directions, following significant price changes in 2013. Much like the S&P500 volatility index ("VIX") provides insight into implied volatility expectations for the broader market based on index options, the GVZ Gold Volatility Index provides similar insight into expected volatility for gold based on the GLD ETF. Since April 2013, future volatility expectations have increased considerably from approximately 14% to beyond 20%, representing the expected annualized movement in GLD for the upcoming 30-day period. Interestingly, volatility expectations have recently started to decrease.

Gold Price Quarterly Average and Annualized Volatility

Source: Bloomberg, Dundee Capital Markets

Gold Volatility Index (GVZ)

Source: Bloomberg, Dundee Capital Markets

1,100

1,250

1,400

1,550

1,700

31-Dec-12 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13

Go

ld P

rice (

US

$/o

z)

Gold Price (US$/oz) Average Gold Price (US$/oz)

1Q13Average Gold Price: $1,630/ozAnnualized Volatility:11%

2Q13Average Gold Price: $1,414/ozAnnualized Volatility:30%

3Q13Average Gold Price: $1,330/ozAnnualized Volatility:23%

4Q13Average Gold Price: $1,272/ozAnnualized Volatility:15%

5

10

15

20

25

30

35

31-Dec-12 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13

CB

OE

Go

ld V

ola

tili

ty In

de

x

Gold Volatility Index (GVZ)

Gold price volatility is currently elevated, and market expectations forecast this will continue.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 19

A UNIQUE SECTOR WITH DISTINCTIVE CHARACTERISTICS

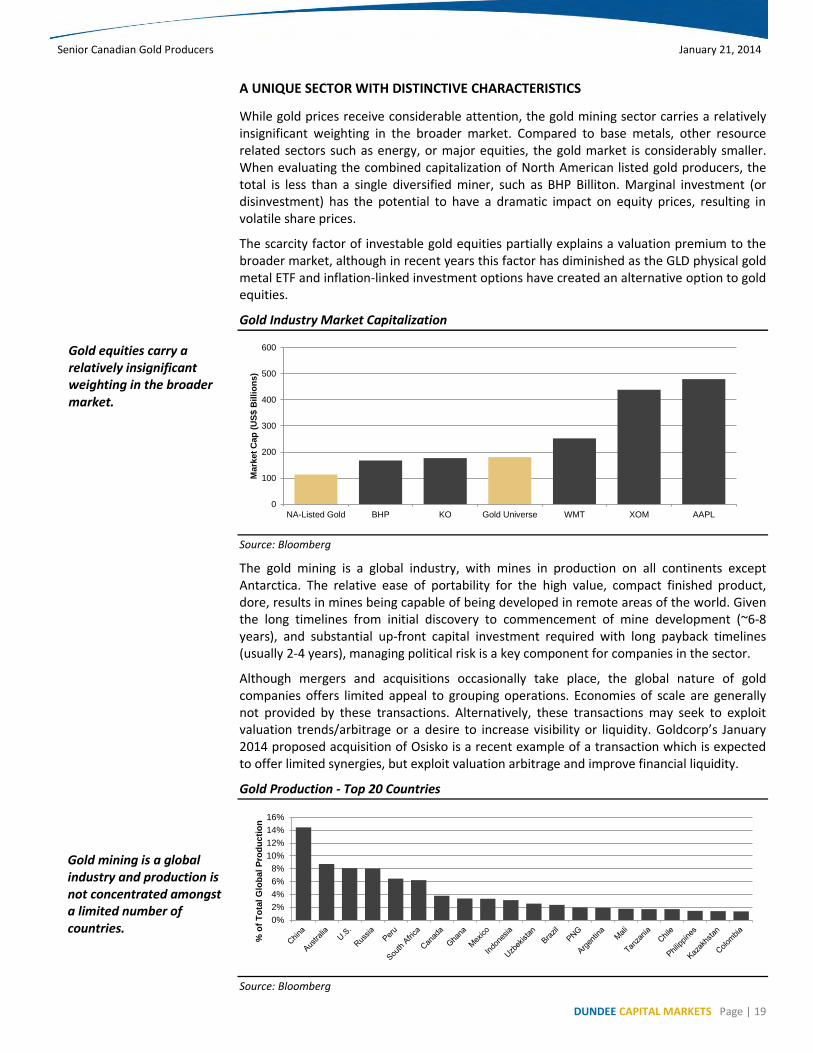

While gold prices receive considerable attention, the gold mining sector carries a relatively insignificant weighting in the broader market. Compared to base metals, other resource related sectors such as energy, or major equities, the gold market is considerably smaller. When evaluating the combined capitalization of North American listed gold producers, the total is less than a single diversified miner, such as BHP Billiton. Marginal investment (or disinvestment) has the potential to have a dramatic impact on equity prices, resulting in volatile share prices.

The scarcity factor of investable gold equities partially explains a valuation premium to the broader market, although in recent years this factor has diminished as the GLD physical gold metal ETF and inflation-linked investment options have created an alternative option to gold equities.

Gold Industry Market Capitalization

Source: Bloomberg

The gold mining is a global industry, with mines in production on all continents except Antarctica. The relative ease of portability for the high value, compact finished product, dore, results in mines being capable of being developed in remote areas of the world. Given the long timelines from initial discovery to commencement of mine development (~6-8 years), and substantial up-front capital investment required with long payback timelines (usually 2-4 years), managing political risk is a key component for companies in the sector.

Although mergers and acquisitions occasionally take place, the global nature of gold companies offers limited appeal to grouping operations. Economies of scale are generally not provided by these transactions. Alternatively, these transactions may seek to exploit valuation trends/arbitrage or a desire to increase visibility or liquidity. Goldcorp’s January 2014 proposed acquisition of Osisko is a recent example of a transaction which is expected to offer limited synergies, but exploit valuation arbitrage and improve financial liquidity.

Gold Production - Top 20 Countries

Source: Bloomberg

0

100

200

300

400

500

600

NA-Listed Gold BHP KO Gold Universe WMT XOM AAPL

Mark

et

Cap

(U

S$ B

illi

on

s)

0%

2%

4%

6%

8%

10%

12%

14%

16%

% o

f T

ota

l G

lob

al

Pro

du

cti

on

Gold equities carry a relatively insignificant weighting in the broader market.

Gold mining is a global industry and production is not concentrated amongst a limited number of countries.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 20

GOLD EQUITY OVERVIEW

Drivers for Industry Equity Returns

Dundee projects the following key drivers will define gold producer equity returns:

Gold price direction. Changes in the gold price have a direct impact on producer profitability and equity returns. However, Dundee believes only a select group of companies have the capacity to generate value for shareholders at current gold prices and recommends investment selectivity amongst producers. Dundee maintains a positive long term perspective on gold prices, but forecasts no material price recovery near term.

Free cash flow generation. Following a prolonged period of lackluster cash generation for gold producers, despite rising earnings and cash flow, we expect actual cash generation from operations will become the most relevant metric for determining short term operating performance. Under this outlook, current performance is expected to be weighted more heavily than growth. Dundee expects growth capital allocation to be increasingly scrutinized against the potential for margin impairment, incremental financial risk assumed, and the potential for higher technical risk.

Execution capacity. Gold intermediate and senior producers under coverage over a five year period from 2008-2012 missed production guidance 33% of the time and missed cost guidance 50% of the time. While gold investors are familiar with the uncertainties and risks of mining, an important part of attracting new capital will be successful execution and the achievement of both short and long term targets. Should management, who have the greatest access to information, be incapable of providing accurate projections, Dundee expects attracting new capital to the sector will continue to be a challenge.

Cost containment and margin control. Over a five year period from 2008 - 2012, we estimate unit operating costs increased 28%, while capital costs at operating mines increased 109%, compared to the gold price change of 100% over the same period. Excessive historical inflationary pressures and poor cost management has previously impacted the potential for expanding margins from higher gold prices. Dundee expects those companies which can control costs and exercise discipline, thereby demonstrating margin expansion from a potential increase in gold prices, to be rewarded by investors.

Management of financial risk. High gold prices had historically provided a motivation for increasing industry capital expenditure, the assumption of debt, and distribution of dividends, although declining gold prices has impacted aggressive management decisions. Current lower gold prices and high sector financial leverage have greatly increased financial risk, should gold prices stay at current levels or decrease further. Dundee views low financial leverage to be key for producers to ensure financial health, given high gold price volatility. The ability for producers to maintain low leverage is an important measure to reducing downside risk.

Gold Equity Investment Opportunities

In our evaluation of gold producers, we have separated gold companies according to four categories, with our broad perspective of each group below. Our evaluation of the sector is predominantly focused upon producers, with particular emphasis on the senior group. We consider:

Seniors producers as companies with current output or a pipeline to production of >2.0 MMoz. Seniors typically have a higher number of operating assets which are diversified across a greater number of jurisdictions. Corporate strategy, production profiles, and capital allocation are key attributes for consideration. Historically the seniors are the strongest financially positioned, however rising debt levels have severely limited senior producer flexibility. These companies have undergone the greatest changes in

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 21

management and strategy to accommodate the current gold price environment, as these changes are required to generate a material impact to the bottom line. Despite a weaker track record of the group, valuation of the seniors is highest. Dundee views this group as providing weaker risk-returns than the more financially flexible intermediate group, although having greater trading liquidity and access to capital is a distinguishable figure.

Intermediate and junior producers as companies with <2.0 MMoz. Intermediate and junior producers may have one or more operating assets, although production and reserves are typically concentrated in fewer mines. Risk management, financing, and capital allocation are key attributes for consideration. Dundee views operating flexibility and financial leverage as challenges for this group; however, the spectrum of these risks range considerably by company. Many intermediate and junior producers have also implemented operating and strategy changes, and given fewer operating and corporate risks, the net impact is more significant than for the senior producers. Dundee views both equity valuation dispersion and the risk spectrum as widest amongst this group, thereby providing the highest opportunity for investment return differentials amongst individual equity selection.

Advanced developers are companies nearing or currently engaged in mine construction. Advanced developers are exposed to higher risks, but have the potential to yield greater returns with project advancement, production, or acquisition. Financing risk, market liquidity, and achievement of development targets remain very high risks for developers, with more severe consequences in the current market environment should challenges be experienced. Dundee views the reward opportunity as highest amongst the advanced developer group for longer time horizon investors, although investment options are limited and risks are quite elevated.

Explorers are companies with projects or properties being advanced to resource definition or a construction decision. Explorers are typically exposed to the highest uncertainties and may face considerable political, financial, and technical risk. However, the group also has the potential to demonstrate the greatest amount of value creation through the advancement of a project from discovery to resource delineation to initial production. Financing risk and market illiquidity is highest amongst this group. Dundee views increasingly conservative producer strategies as having diminished the appetite for acquisition of earlier stage exploration companies. An increasing trend of explorer earn-in agreements with producers provides the ability for exploration projects to progress, while it is funded by financially supportive producers. While investment opportunities are broad, Dundee recommends risk-tolerant investors select only companies with assets which have the highest probability for economic development (i.e. above average grades, proven processing technique), with an experienced management team in place, focused on minimizing risks, and maximizing available capital.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 22

VALUATION PHILOSOPHY INCORPORATES BOTH LONG AND SHORT TERM VIEWS

When evaluating target price valuation for producer mining equities, Dundee evaluates both long and short term performance, contrasted below:

Short term - i.e. P/CF, P/E, EV/EBITDA, FCF/EV

Readily available financial data, easily comparable across sectors. Better representation of current performance and fewer assumptions required. No consideration for upcoming changes in operations, risk, reserve life. Can favor short term results, understate near term risks to targets.

Long term - i.e. P/NAV

All cash flows are accounted for, weighted according to time value of money. Accounts for project uniqueness, anticipated changes in operations. Many variables and assumptions required, can be manipulated. Highly sensitive to both discount rate and commodity price assumptions.

Dundee believes that it is key for investors to recognize that a mine is a finite resource, and operating changes are inherently part of a mine plan (i.e. grade, metallurgy, processing), while capital investment is irregular. Below we illustrate annual changes for an operating mine, where near term metrics would fail to capture changes beyond a 1-2 year outlook.

Annual Changes Experienced at Barrick's Cortez Mine

Source: Company reports, Dundee Capital Markets

NAV most appropriately captures all available information and future expectations. However, substantial changes in the gold price have amplified assumption uncertainties, including the definition of what economic reserves are and the economics of long term mine plans where margins are weak. Similarly, short term earnings, cash flow, and free cash flow, while historically indicative of operating performance, has been impacted by increasing accounting variance for the capitalization of costs, rising financial leverage, and inflated growth capital expenditure. In our view, traditional metrics have been weakened by this variance and are not an accurate comparable across companies.

For the analysis of NAV, Dundee applies a discount rate of 5% for gold cash flow and 10% for non-gold cash flow. Both discount rates are traditionally applied by investors. Although we view investor required returns as higher, observed equity cost of capital is low. For short term performance, Dundee evaluates operating cash flow as well an operating cash flow estimate which deducts non-growth capital expenditure, typically defined more strictly as capital allocated to non-producing assets, to create an equally comparable figure across our coverage universe.

Dundee mine level estimates generally incorporate modest operating cost inflation over a 3 year period and ongoing high sustaining capital costs, while reserve additions and resource conversion is incorporated to reflect a realistic outlook, evaluated on an individual asset basis. Exploration projects which offer low returns or have limited prospects of being financed are attributed a nominal value.

$0

$200

$400

$600

$800

$1,000

$1,200

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13E

20

14E

20

15E

All

-In

Sit

e C

os

t (

US

$/o

z)

Go

ld P

rod

uc

tio

n (

MM

oz)

Gold Production (Left axis) All-In Site Cost (Right axis)

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 23

SENIOR COVERAGE RECOMMENDATIONS

We evaluate our resumption of senior gold equity coverage within the context of our existing intermediate producer group coverage. Our perspectives are based upon a three factor analysis of risk, return, and quality. Our risk and quality analysis generates the multiples which we apply to determine target prices, while we weigh this in the context of our three return factors.

Return - i.e. Share price performance. This incorporates:

Upcoming catalysts. Long term potential shareholder returns via P/NAV. Short term potential shareholder returns via operating cash flow, adjusted for

non-growth capital.

Risk - i.e. Potential downside. This incorporates:

Financial indebtedness and scheduled repayments. Geopolitical exposure and associated production/fiscal term uncertainties. Achievement of guidance and growth-related uncertainties.

Quality - i.e. Flexibility. This incorporates:

Portfolio asset margins. Outlook sensitivity, assuming current gold prices are sustained or decrease. Management strategy and growth pipeline.

Our recommendations and price targets are as follows:

Senior and Intermediate Producer Ratings and Recommendations

Source: Dundee Capital Markets

Barrick

We are initiating coverage of Barrick with a NEUTRAL rating and C$22.00 price target. Barrick is expected to generate sizable near term free cash flow relative to its peers. While we forecast no near term funding risks for the company, longer term the company’s substantial debt load is expected to consume these cash flows, reduce operating flexibility, and increasing downside risks should gold price correct further. Barrick features a core of world class assets, which account for a material portion of the company’s valuation, and are generally located in better jurisdictions. Development risk is above average for Barrick, and although the company’s projects are of higher quality (Pascua Lama, Goldrush), timelines and capital requirements remain highly uncertain. Both growth prospects and upcoming catalysts for Barrick are limited, and declining production is expected beyond 2016, in particular should Pascua Lama be delayed beyond 2017.

Company Ticker Price

17-Jan-14

Rating

(1)

Risk Target

Price

Return to

Target

Target Setting

NAV Multiple

Target Setting

CFPS Multiple

Analyst

(2)

Senior Producers

Barrick Gold Corp. ABX C$20.61 N High $22.00 7% 1.3x 12x JW

Goldcorp Inc. G C$25.43 N High $25.50 0% 1.6x 16x JW

Kinross Gold Corp. K C$5.22 B High $6.50 25% 1.1x 10x JW

Intermediate Producers

Agnico-Eagle AEM C$32.21 N High $33.00 8% 1.5x 13x JW

Eldorado Gold Corp. ELD C$7.32 N High $7.50 13% 1.3x 13x JW

IAMGOLD Corp. IMG C$4.45 N High $4.50 9% 0.9x 6x JW

New Gold Inc. NGD C$6.38 B High $7.25 17% 1.4x 15x JW

Osisko Mining Corp OSK C$6.47 B High $7.00 12% 1.3x - JF

Randgold Resources GOLD US$65.32 B High US$90.00 43% 1.6x 16x JW

Yamana Gold Inc. YRI C$10.54 S High $10.00 -3% 1.3x 13x JW

(1) B - Buy, N - Neutral, S - Sell, NR- Not Rated. Refer to disclosures for more information.

(2) JF - Joe Fazzini, JW -Josh Wolfson.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 24

What would make us more constructive: Should Barrick successfully reduce its debt load (i.e. strategic partnerships, better cash flow), or the company’s valuation contract meaningfully, we would seek to be more positive.

Barrick valuation at spot gold:

3.06x P/NAV, above peers at 2.15x.

6.2x / 5.4x 2014E / 2015E P/CF, below peers at 9.3x / 8.2x.

3.1% / 3.0% 2014E / 2015E FCF Yield, above peers at 0.1% / 2.1%.

Goldcorp

We are initiating coverage of Goldcorp with a NEUTRAL rating and C$25.50 price target. We believe Goldcorp’s premium NAV and cash flow valuation already reflects its catalyst and growth outlook, while delivery risks remain. Goldcorp is scheduled to deliver three growth projects in 2014 (Cerro Negro, Cochenour, Eléonore), and it is currently engaged in a hostile proposal to acquire Osisko. Should Goldcorp achieve its growth targets, future free cash flow will grow meaningfully, although near term delivery risk is very high for the company in 2H14. Financial risk is also elevated, although we currently anticipate the company has flexibility to manage these risks with the monetization of its equity portfolio, draw down of its line of credit, and debt refinancing. Goldcorp maintains a higher quality asset base, which is located in better quality jurisdictions. The company also has several potential longer term growth projects.

What would make us more constructive: Should Goldcorp successfully deliver its growth projects or its valuation more appropriately reflect the risks associated with its assets, we would seek to be more positive.

Goldcorp valuation at spot gold:

2.25x P/NAV, above peers at 2.15x.

17.5x / 13.1x 2014E / 2015E P/CF, above its peers at 9.3x / 8.2x.

(5.3)% / 2.6% 2014E / 2015E FCF Yield, mixed compared to peers at 0.1% / 2.1%.

Kinross

We are initiating on Kinross with a BUY rating and C$6.50 price target. In recent quarters, Kinross has improved its credibility by executing on its targets and reducing its costs. In our view, the market has yet to recognize these efforts and shares trade at a significant discount to its senior producer peers. Although Kinross on average operates higher cost operations, which are located in higher risk jurisdictions, the company is expected to generate fair free cash flow over the interim and we see limited delivery risk to our expectations, given nominal ramp-up requirements. While the company has little delivery risk, it also has no growth pipeline, and we expect the company’s production base to decline beyond 2016. We believe material financial flexibility and good near term free cash flow provides the company with better flexibility than its peers.

Kinross valuation at spot gold:

1.77x P/NAV, below peers at 2.15x.

6.1x / 6.1x 2014E / 2015E P/CF, below peers at 9.3x / 8.2x.

1.3% / 2.9% 2014E / 2015E FCF Yield, above peers at 0.1% / 2.1%.

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 25

Portfolio Asset Margins

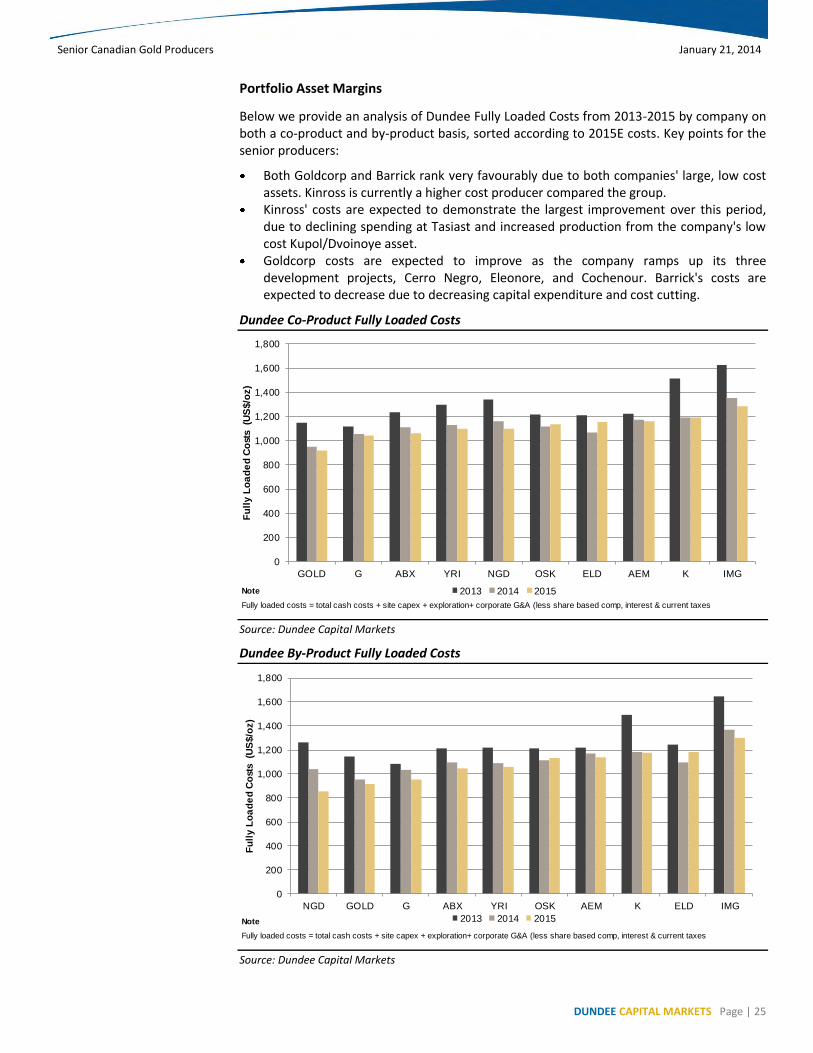

Below we provide an analysis of Dundee Fully Loaded Costs from 2013-2015 by company on both a co-product and by-product basis, sorted according to 2015E costs. Key points for the senior producers:

Both Goldcorp and Barrick rank very favourably due to both companies' large, low cost assets. Kinross is currently a higher cost producer compared the group.

Kinross' costs are expected to demonstrate the largest improvement over this period, due to declining spending at Tasiast and increased production from the company's low cost Kupol/Dvoinoye asset.

Goldcorp costs are expected to improve as the company ramps up its three development projects, Cerro Negro, Eleonore, and Cochenour. Barrick's costs are expected to decrease due to decreasing capital expenditure and cost cutting.

Dundee Co-Product Fully Loaded Costs

Source: Dundee Capital Markets

Dundee By-Product Fully Loaded Costs

Source: Dundee Capital Markets

Note

Fully loaded costs = total cash costs + site capex + exploration+ corporate G&A (less share based comp, interest & current taxes

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

GOLD G ABX YRI NGD OSK ELD AEM K IMG

Fu

lly L

oa

de

d C

ost

s (U

S$/o

z)

2013 2014 2015

Note

Fully loaded costs = total cash costs + site capex + exploration+ corporate G&A (less share based comp, interest & current taxes

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

NGD GOLD G ABX YRI OSK AEM K ELD IMG

Fu

lly L

oa

de

d C

ost

s (U

S$/o

z)

Fully Loaded Costs (By-Product)

2013 2014 2015

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 26

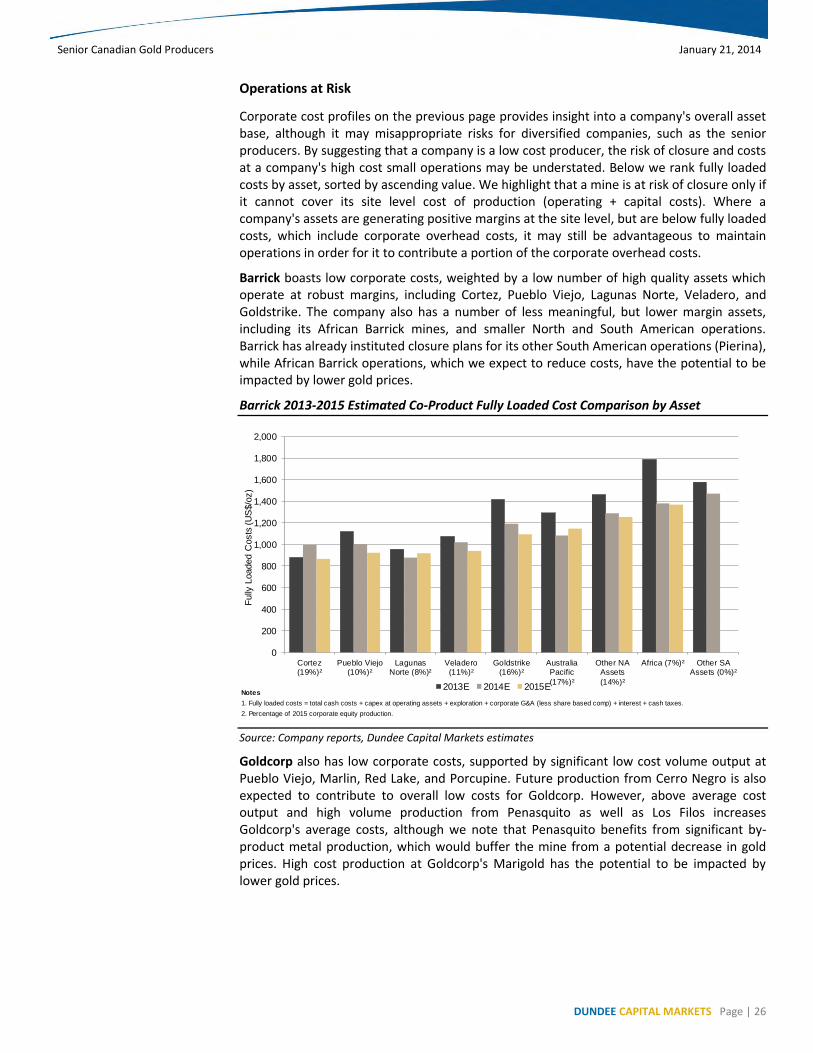

Operations at Risk

Corporate cost profiles on the previous page provides insight into a company's overall asset base, although it may misappropriate risks for diversified companies, such as the senior producers. By suggesting that a company is a low cost producer, the risk of closure and costs at a company's high cost small operations may be understated. Below we rank fully loaded costs by asset, sorted by ascending value. We highlight that a mine is at risk of closure only if it cannot cover its site level cost of production (operating + capital costs). Where a company's assets are generating positive margins at the site level, but are below fully loaded costs, which include corporate overhead costs, it may still be advantageous to maintain operations in order for it to contribute a portion of the corporate overhead costs.

Barrick boasts low corporate costs, weighted by a low number of high quality assets which operate at robust margins, including Cortez, Pueblo Viejo, Lagunas Norte, Veladero, and Goldstrike. The company also has a number of less meaningful, but lower margin assets, including its African Barrick mines, and smaller North and South American operations. Barrick has already instituted closure plans for its other South American operations (Pierina), while African Barrick operations, which we expect to reduce costs, have the potential to be impacted by lower gold prices.

Barrick 2013-2015 Estimated Co-Product Fully Loaded Cost Comparison by Asset

Source: Company reports, Dundee Capital Markets estimates

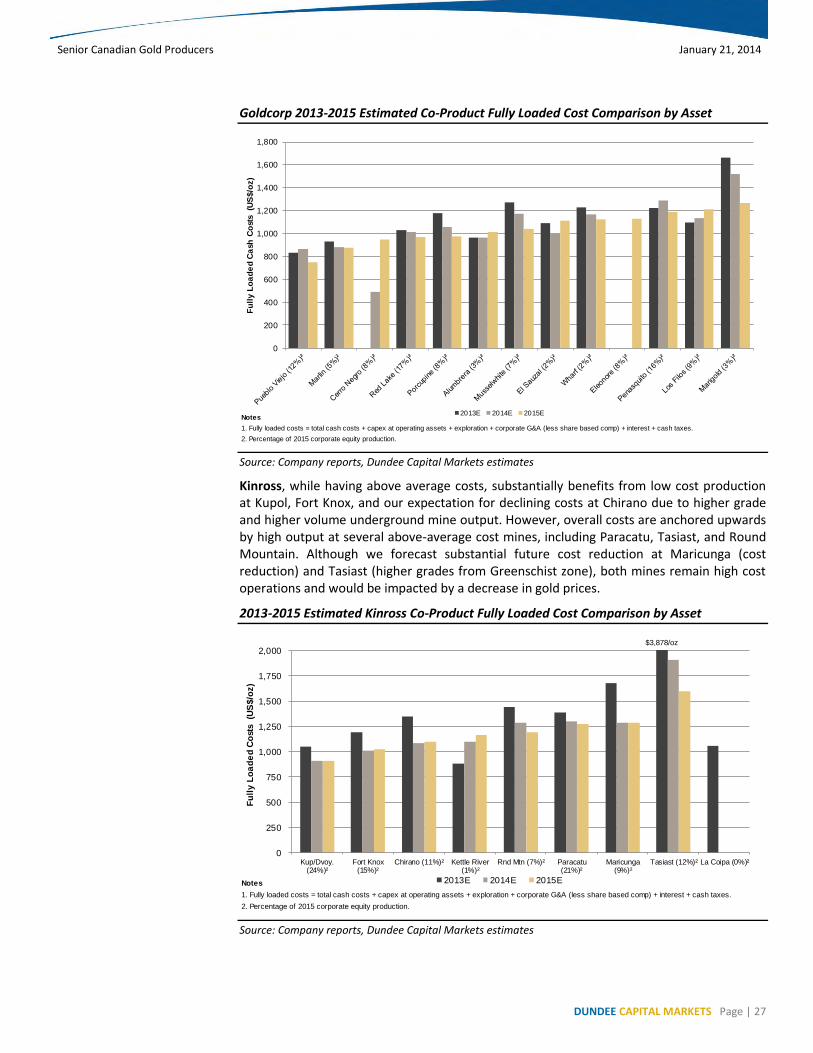

Goldcorp also has low corporate costs, supported by significant low cost volume output at Pueblo Viejo, Marlin, Red Lake, and Porcupine. Future production from Cerro Negro is also expected to contribute to overall low costs for Goldcorp. However, above average cost output and high volume production from Penasquito as well as Los Filos increases Goldcorp's average costs, although we note that Penasquito benefits from significant by-product metal production, which would buffer the mine from a potential decrease in gold prices. High cost production at Goldcorp's Marigold has the potential to be impacted by lower gold prices.

Notes

1. Fully loaded costs = total cash costs + capex at operating assets + exploration + corporate G&A (less share based comp) + interest + cash taxes.

2. Percentage of 2015 corporate equity production.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Cortez(19%)²

Pueblo Viejo(10%)²

LagunasNorte (8%)²

Veladero(11%)²

Goldstrike(16%)²

AustraliaPacific

(17%)²

Other NAAssets

(14%)²

Africa (7%)² Other SAAssets (0%)²

Fully

Loaded C

osts

(U

S$/o

z)

2013E 2014E 2015E

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 27

Goldcorp 2013-2015 Estimated Co-Product Fully Loaded Cost Comparison by Asset

Source: Company reports, Dundee Capital Markets estimates

Kinross, while having above average costs, substantially benefits from low cost production at Kupol, Fort Knox, and our expectation for declining costs at Chirano due to higher grade and higher volume underground mine output. However, overall costs are anchored upwards by high output at several above-average cost mines, including Paracatu, Tasiast, and Round Mountain. Although we forecast substantial future cost reduction at Maricunga (cost reduction) and Tasiast (higher grades from Greenschist zone), both mines remain high cost operations and would be impacted by a decrease in gold prices.

2013-2015 Estimated Kinross Co-Product Fully Loaded Cost Comparison by Asset

Source: Company reports, Dundee Capital Markets estimates

Notes

1. Fully loaded costs = total cash costs + capex at operating assets + exploration + corporate G&A (less share based comp) + interest + cash taxes.

2. Percentage of 2015 corporate equity production.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Fu

lly L

oa

de

d C

ash

Co

sts

(US

$/o

z)

2013E 2014E 2015E

Notes

1. Fully loaded costs = total cash costs + capex at operating assets + exploration + corporate G&A (less share based comp) + interest + cash taxes.

2. Percentage of 2015 corporate equity production.

0

250

500

750

1,000

1,250

1,500

1,750

2,000

Kup/Dvoy.(24%)²

Fort Knox(15%)²

Chirano (11%)² Kettle River(1%)²

Rnd Mtn (7%)² Paracatu(21%)²

Maricunga(9%)²

Tasiast (12%)² La Coipa (0%)²

Fu

lly L

oa

de

d C

ost

s (U

S$/o

z)

2013E 2014E 2015E

$3,878/oz

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 28

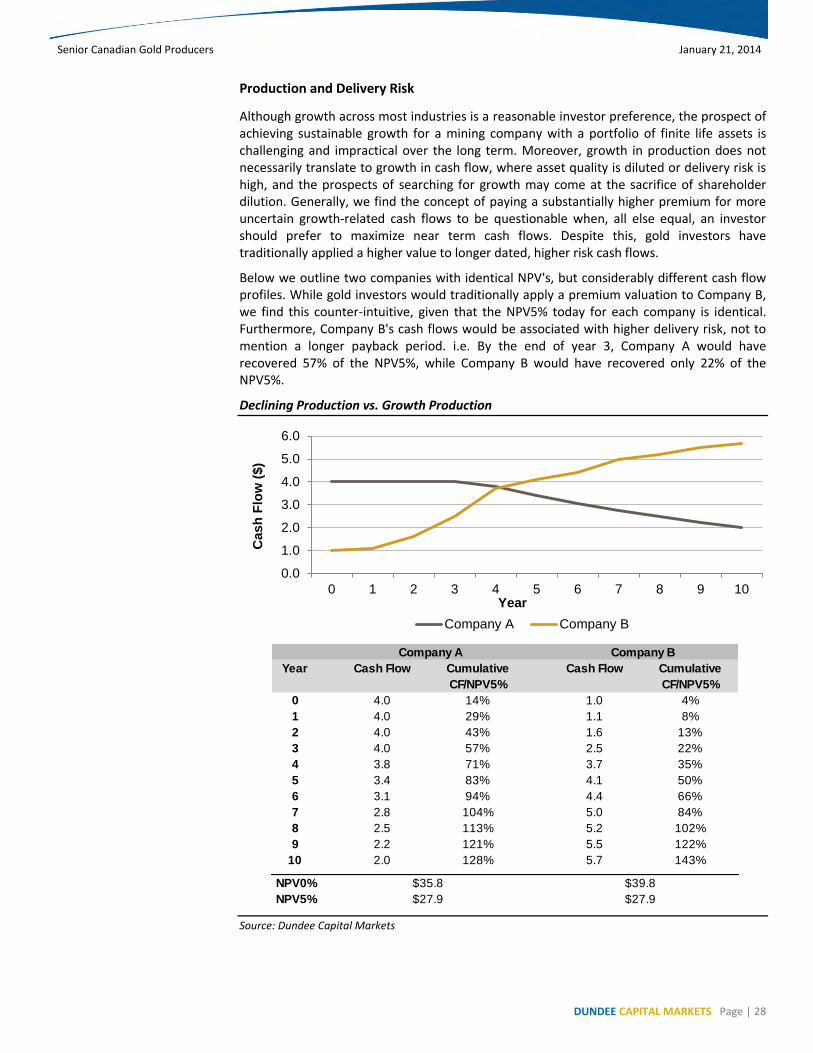

Production and Delivery Risk

Although growth across most industries is a reasonable investor preference, the prospect of achieving sustainable growth for a mining company with a portfolio of finite life assets is challenging and impractical over the long term. Moreover, growth in production does not necessarily translate to growth in cash flow, where asset quality is diluted or delivery risk is high, and the prospects of searching for growth may come at the sacrifice of shareholder dilution. Generally, we find the concept of paying a substantially higher premium for more uncertain growth-related cash flows to be questionable when, all else equal, an investor should prefer to maximize near term cash flows. Despite this, gold investors have traditionally applied a higher value to longer dated, higher risk cash flows.

Below we outline two companies with identical NPV's, but considerably different cash flow profiles. While gold investors would traditionally apply a premium valuation to Company B, we find this counter-intuitive, given that the NPV5% today for each company is identical. Furthermore, Company B's cash flows would be associated with higher delivery risk, not to mention a longer payback period. i.e. By the end of year 3, Company A would have recovered 57% of the NPV5%, while Company B would have recovered only 22% of the NPV5%.

Declining Production vs. Growth Production

Source: Dundee Capital Markets

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0 1 2 3 4 5 6 7 8 9 10

Cash

Flo

w (

$)

Year

Company A Company B

Company A Company B

Year Cash Flow Cumulative

CF/NPV5%

Cash Flow Cumulative

CF/NPV5%

0 4.0 14% 1.0 4%

1 4.0 29% 1.1 8%

2 4.0 43% 1.6 13%

3 4.0 57% 2.5 22%

4 3.8 71% 3.7 35%

5 3.4 83% 4.1 50%

6 3.1 94% 4.4 66%

7 2.8 104% 5.0 84%

8 2.5 113% 5.2 102%

9 2.2 121% 5.5 122%

10 2.0 128% 5.7 143%

NPV0% $35.8 $39.8

NPV5% $27.9 $27.9

Senior Canadian Gold Producers January 21, 2014

DUNDEE CAPITAL MARKETS Page | 29