Embed Size (px)

Citation preview

Take Charge: Your Money. Your Life. Plan Now for 2013: Tax, Gift and Estate

Planning Tips

What to Do Before December 31, 2012

Brought to you by:

360 Degrees of Financial Literacy and

America's CPA Financial Planners

Personal Financial Planning Section 360 Degrees of Financial Literacy 2

Personal Financial Planning Section 360 Degrees of Financial Literacy

Let’s get this out of the way …

The general information contained in this web seminar

is provided by the American Institute of Certified

Public Accountants as a service to the public and our

members. It is not intended to serve as tax, legal or

any other professional advice applicable to any

particular person or matter.

3

Personal Financial Planning Section 360 Degrees of Financial Literacy

Lyle Benson, CPA/PFS

President, L.K. Benson & Co.

Ted Sarenski, CPA/PFS

President, Blue Ocean Strategic Capital, LLC

Scott Sprinkle, CPA/PFS

Partner, Sprinkle Financial Consultants, LLC

Introductions

4

Personal Financial Planning Section 360 Degrees of Financial Literacy

Agenda

Setting the stage

Proactive planning opportunities

Reviewing your tax return

Where to find help

5

Personal Financial Planning Section 360 Degrees of Financial Literacy

Setting the Stage

6

Personal Financial Planning Section 360 Degrees of Financial Literacy

2013 Tax Changes (if no action is taken)

Income Tax

• Bush tax cuts expire: increase in ordinary income, capital gains,

and qualified dividend rates

• 3.8% Medicare surtax on net investment income of high-income

individuals (MAGI > $200k single, $250k MFJ, $125k MFS)

• 0.9% increase in Medicare payroll tax for high earners

• Marriage penalty relief expires

Estate Tax

• $5 million exemption reverts back to $1 million

• Increase in estate tax rate from 35% to 55%

Gift Tax

• $5 million exemption reverts back to $1 million

7

Comparison of 2012 vs. 2013 Tax Rates

2012

2013 &

Beyond

10% 15%

15% 15%

25% 28%

28% 31%

33% 36%

35% 39.6%

2012

2013&

Beyond

0% 10%

15% 20%

(23.8% if

surtax

applies)

Ordinary Income Long-Term

Capital Gains

Personal Financial Planning Section 360 Degrees of Financial Literacy

Political Environment Uncertainty = Flexibility

Election Year

• Unlikely that we’ll have any certainty until last quarter

• Start planning now, gathering data, preparing projections, drafting

estate documents, etc.

What the proposals say

• Bush tax cuts – extended or eliminated?

• Tax rates – will we see increases or tax cuts?

• Dividends and capital gains – how will they be taxed?

• AMT – will it stay or go?

• Estate tax in limbo

Much remains to be seen. Don’t wait until after the election to

take action!

9

Personal Financial Planning Section 360 Degrees of Financial Literacy

Proactive Planning

Opportunities

10

Personal Financial Planning Section 360 Degrees of Financial Literacy

Income Acceleration and Planning Added dynamics of President’s proposal

• Requires min 30% effective rate for those with income over $1

million annually

Harvesting gains

• Last quarter of the year

• Not affected by 30-day wash sale rules

• Monitor elections for deemed sales

Comp and benefit issues

• Exercise stock options

• Pay bonuses before year-end

• Deferred compensation elections

(Don’t necessarily forego deferral accounts, particularly when there are

matching provisions. Educate your clients and consider the political landscape.)

Roth conversions

11

Personal Financial Planning Section 360 Degrees of Financial Literacy

Income Acceleration and Planning

Cash basis taxpayers

• Accelerate billings

Other income acceleration ideas

• Accrue bond interest in 2012 versus 2013

• Accelerate installment payments

Other planning

• Re-allocation of portfolio based on tax changes (qualified plan

versus non-qualified plans, etc.)

• AGI planning between 2012 and 2013 to effectively manage the

new 3.8 percent Medicare tax in 2013

12

Personal Financial Planning Section 360 Degrees of Financial Literacy

Itemized Deduction Planning

What will happen to itemized deductions?

• Flexibility is important.

Accelerate itemized deductions in 2012

• Set up donor advised funds and fund future year’s charitable

contributions in 2012

• Accelerate miscellaneous itemized deductions by prepaying

expenses to get above the 2% limit

Interest rates at historically low levels

• Look at the clients Form 1098 and mortgage statement

• Discuss their refinancing strategy

• Evaluate all of the client’s debt

Alternative minimum tax situation

• Consider prepaying real estate taxes and personal property

taxes

13

Personal Financial Planning Section 360 Degrees of Financial Literacy

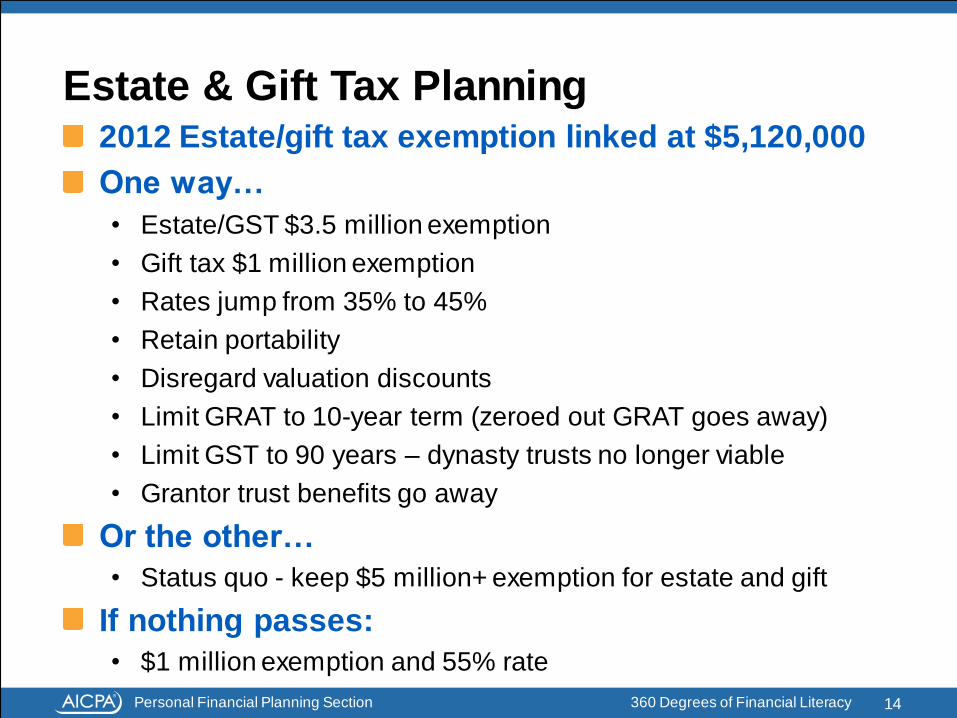

Estate & Gift Tax Planning 2012 Estate/gift tax exemption linked at $5,120,000

One way…

• Estate/GST $3.5 million exemption

• Gift tax $1 million exemption

• Rates jump from 35% to 45%

• Retain portability

• Disregard valuation discounts

• Limit GRAT to 10-year term (zeroed out GRAT goes away)

• Limit GST to 90 years – dynasty trusts no longer viable

• Grantor trust benefits go away

Or the other…

• Status quo - keep $5 million+ exemption for estate and gift

If nothing passes:

• $1 million exemption and 55% rate

14

Personal Financial Planning Section 360 Degrees of Financial Literacy

Estate & Gift Tax Planning

Who can benefit most from planning

• Elderly or ill, those who live in a state where state estate tax is

decoupled from fed, clients who have asset protection needs,

non-married same sex couples and wealthy

Impediment towards getting your clients to take

action

• Complexity (setting up trusts, etc.), cost of advisors, appraisals,

etc., disbelief that changes are going to take place, uncertainty

• Advisors need to help their clients understand the detriments to

not planning ahead and taking action when necessary (run

projections and show them the impact)

15

Personal Financial Planning Section 360 Degrees of Financial Literacy

Estate & Gift Tax Planning

Start now! Use up exemption in 2012

• Some techniques take months to implement (GRATs, IDGTs),

etc.)

• Need to start now to educate clients, draft documents, prepare

valuations, etc.

Income generation through CRUTs

Opportunities with low interest rates (GRAT)

Asset efficiency implications of gifting

Drafting to gift but not gift

16

Personal Financial Planning Section 360 Degrees of Financial Literacy

Estate & Gift Tax Planning Beware of large outright gifts

• They are not protected from creditors claims and the remainder

is not kept in the family

Reasons to gift now:

• Save estate tax (federal and state)

• Asset protection (if via trust)

• Grandfather for GST

• Grandfather for grantor trust changes

• Lock in discounts

• Remove appreciation from estate

Cash flow planning and running of projections is

essential before taking action (create plan to ensure

client is comfortable before triggering)

17

Personal Financial Planning Section 360 Degrees of Financial Literacy

Reviewing Your Tax

Return

18

Personal Financial Planning Section 360 Degrees of Financial Literacy

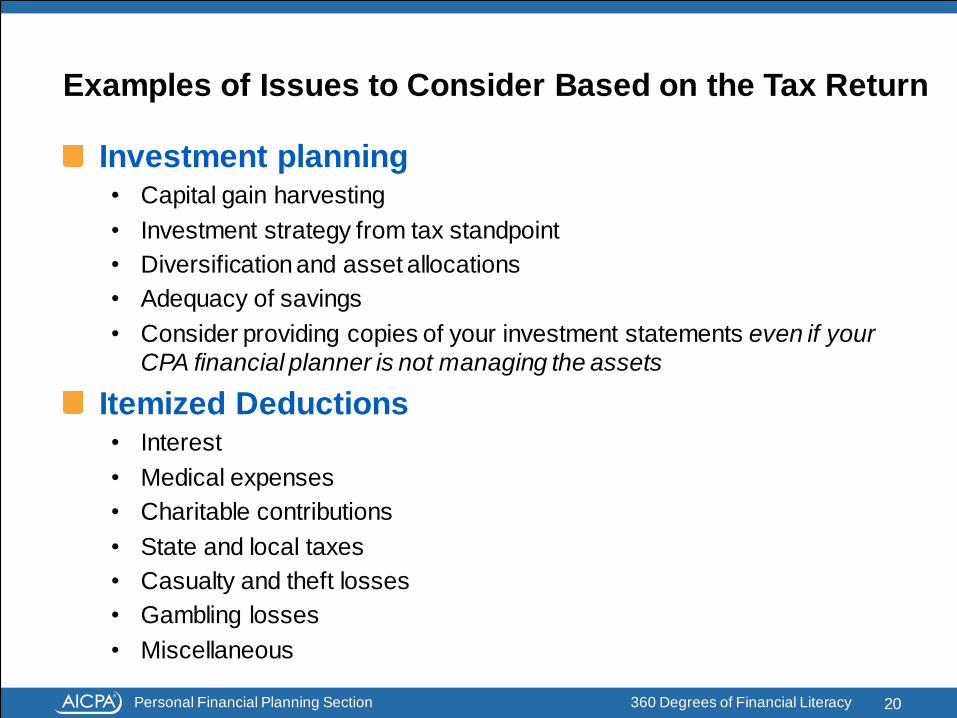

Examples of Issues to Consider Based on the Tax Return

Your age can be great starting point for discussions

with your CPA financial planner or CPA/PFS!

Baby Boomers

• When to collect Social Security (spousal considerations)

• Medicare and healthcare considerations

• Safe withdrawal rates

• Required minimum distributions

• Roth conversion planning

• Long-term care insurance (start these conversations with clients

even in their 40s!)

Younger clients

• Retirement planning (comp & benefit planning)

• Education planning for children

19

Personal Financial Planning Section 360 Degrees of Financial Literacy

Investment planning • Capital gain harvesting

• Investment strategy from tax standpoint

• Diversification and asset allocations

• Adequacy of savings

• Consider providing copies of your investment statements even if your

CPA financial planner is not managing the assets

Itemized Deductions • Interest

• Medical expenses

• Charitable contributions

• State and local taxes

• Casualty and theft losses

• Gambling losses

• Miscellaneous

20

Examples of Issues to Consider Based on the Tax Return

Personal Financial Planning Section 360 Degrees of Financial Literacy

Use this checklist to

identify financial planning

opportunities as you

analyze your tax return.

Download this checklist at

www.360financialliteracy.org

along with other

resources

Tax Return for PFP Checklist

21

Personal Financial Planning Section 360 Degrees of Financial Literacy

Where to find help

22

Personal Financial Planning Section 360 Degrees of Financial Literacy

How to Choose the Right CPA Financial Planner

Choosing the right financial planner may be one of the

more important decisions you make in your lifetime.

Ideally, you will be creating a trusted relationship that

works for the long term. Selecting a planner is like

choosing a CFO, a confidant, a friend, a teacher, a

psychiatrist and counselor all rolled into one. Here are

some tips to help you make this important decision:

• Educate yourself

• Ask about qualifications

• Inquire and investigate

• Connect

• Choose a CPA/PFS or CPA financial planner

23

www.findacpapfs.org

Personal Financial Planning Section 360 Degrees of Financial Literacy

Questions

24

Personal Financial Planning Section 360 Degrees of Financial Literacy

Resources

Additional resources are available online at

www.360financialliteracy.org. Among them:

• Ask the Money Doctor

• Checklists to use with your own return

• Today’s PowerPoint presentation

• Archived recording of today’s webinar

• Tips on choosing a financial advisor

www.findacpapfs.org

25

![Take Charge of Your Money when you leave your job LFD0405-0574 [Presenter's Name] [Presenter's Title] [Presenter's Firm Information] [Date of Presentation]](https://img.pdfslide.net/doc/110x75/56649e845503460f94b85de9/take-charge-of-your-money-when-you-leave-your-job-lfd0405-0574-presenters.jpg)