Embed Size (px)

DESCRIPTION

Tapmi pratibimb april 2012

Citation preview

Pratibimb | April 2012 | 1

PRATIBIMB FINANCE | GENERAL MANAGEMENT | HUMAN RESOURCE | MARKETING | HEALTHCARE | OPERATIONS | SYSTEMS

The Reflection of Management

A Student’s Initiative

Each Art i san. An Entrepreneur – Need for Susta inable Impact . A Jaipur Rugs Special

By Ashish Agarwal FMS, Delhi

The People make it possible! By Simone Lobo

XIMR, Mumbai

Volume II, Issue X April 2012 A Monthly e-Magazine

This very stance of power and autonomy achieved by

these institutions is what Paul Volcker is adamant

about ending but then who is Paul Volcker and what

is he planning to do so? By Savio Fernandes

GIM, Goa Delving deeper into finer details of entire supply chain of the Healthcare industry, some glaring inefficiencies come to forefront… By Trisha Pandey

SJMSOM, Mumbai

TAPMI is now…

AACSB accredited!

Pratibimb | April 2012 | 2

T. A. Pai Management Institute (TAPMI) is a premier management institute situated in

Manipal and is well known for its academic rigor & faculty-student interaction. The

Institute has been recently ranked amongst top 1 per cent of B-schools in India & 4th in

the South Zone by The Week Magazine.

Founded by the visionary, Late Shri. T. A. Pai, TAPMI’s mission is to provide much

needed impetus to the task of building professional management capability in the

country. In the process, it has also played a role in strengthening the existing educational

and health infrastructure of Manipal.

We are committed to excellence in post graduate management education, research

and practice by nurturing and developing global wealth creators and leaders. We

shall continually benchmark ourselves against the best-in-class institutions. We shall

foster continuous learning and reflection, achievement-orientation, creative

interdependence, and respect for diversity with a holistic concern for ethics,

environment and society.

T. A. Pai Management Institute

Manipal, Karnataka

About TAPMI

Our Mission

Recent Updates AACSB( the Association to Advance Collegiate Schools of Business) Accreditation Standards are used as the basis to evaluate a business school’s mission, operations, faculty qualifications and contributions, programs, and other critical areas. AACSB accreditation ensures students and parents that the business school is providing a top-quality education. Additionally, AACSB accreditation provides global recognition. TAPMI is the second management institute in India to receive this meritorious accreditation.

Pratibimb | April 2012 | 3

TAPMI’s e-Magazine - is the conglomeration of the various

specializations in MBA (Marketing, Finance, HR, Systems and

Operations). It is primarily intended to provide insights into the

plethora of knowledge that relate to the various departments of

Management and to give an opportunity to the students of

TAPMI and the best brains across country to exhibit their

creative cells. The magazine also strives to bring expert inputs

from industries, thereby bringing the academia and industry

together.

Pratibimb the e-Magazine of TAPMI had its first issue in

December 2010. The issue comprised of an interview of denoted

writer Ms. Rashmi Bansal along with a series of articles by

students and industry experts like MadhuSudan Rao (AVP-Delivery, Mahindra Satyam) & Ed

Cohen who is a global leader and chief learning officer who led Booz Allen Hamilton & Satyam

Computer Services to the first rank globally for learning & development . It also included a

hugely successful and engrossing game for finance geeks called “Beat the Market” to bring out

the application based knowledge of students by providing them the platform where they were

expected to predict the stock prices of two selected stocks on a future date. The magazine is

primarily intended for the development of all around management knowledge by providing

unbiased critical insights into the modern developments.

TAPMI believes that learning is a continuous process and is not limited to the four walls of the

classroom. This viewpoint is further enhanced through Pratibimb wherein students manage

and contribute to create a refreshing learning environment outside the classrooms which

eventually leads to a holistic development process. The magazine provides a competitive

platform and opportunity to the students where they can compete with the best brains of the

country. The magazine also provides a platform for prominent industry stalwarts to

communicate their views and learning about and from the recent developments from their

respective fields of business which in turn helps to create a collaborative learning base for its

readers.

Pratibimb is committed in continuing this initiative by bringing in continuous improvement

in the magazine by including quality articles related to various management issues and

eventually creating a more engaging relationship with its readers by providing them a

platform to showcase their talent.

We invite all the best brains across country to be part of this initiative and help us take this to

the next level.

PRATIBIMB TAPMI’S MONTHLY e-MAGAZINE VOLUME 2, ISSUE X APRIL, 2012

Pratibimb | April 2012 | 4

It is always a pleasure to witness that certain efforts of the students are

sustained and carried forward; Pratibimb is one such. The oft-beaten

track, “We are here to learn,” ends up as a mere platitude when there are

no visible actions and documentation. Whereas there is no dearth of

actions at TAPMI, documentation is not something that many—other than

scholars—choose to engage in; it is normally viewed as uninteresting,

drab and a drudgery. TAPMIans have proved that they are equally

capable of actions and of documentation without losing the intellectual

flavour of it.

Scholarship is too important a phenomenon to be left to scholars alone,

especially in the field of management. As future practicing managers who

will be engaged in rigorous action in different fields of business, TAPMIans

have manifested both the penchant to produce research works and also

get their counterparts in other leading business schools to contribute their

thoughts to this endeavour. In this regard, TAPMIans have truly

demonstrated the evidence for creative interdependence, an important

aspect of TAPMI’s mission.

I sincerely appreciate the students and the faculty of TAPMI who have

made Pratibimb a possibility through their scholarly works, co-ordination

efforts and support. I wish the team the very best.

Dr. R. C. Natarajan.

DIR

EC

TO

R’S

ME

SS

AG

E

Pratibimb | April 2012 | 5

Editor’s corner

Dear Readers,

We would like to thank all the participants and readers for

their valuable contribution. By making this magazine

monthly, we aim to provide a platform that will give you more

opportunities to share knowledge and showcase your talent by

competing with the best minds in the country.

Our presence has also augmented due to the popularity of

social media. There has been a steady rise in our total

audience, including both readers and contributors, and more

number of posts have gone viral. The plethora of topics

published include learning from management gurus such as

Peter Drucker and Michael Porter, or management

innovation that helped leading brands define themselves

better. In fact we encourage our contributors to write about

any new upcoming events related to management. For all

these amazing contributions, apart from students of TAPMI

and other eminent b-schools in the country, we would also

like to thank Jaipur Rugs for their article in the current issue.

The articles have been selected by the Editorial Team. We

wish to thank all those who helped us in improving Pratibimb

through their feedbacks. We would like to take this

opportunity to extend our gratitude to all faculty and students

at TAPMI for their continual support, guidance, motivation

and inspiration that has helped us to take Pratibimb to the

next echelon.

To stay updated about the magazine, please like our page on

Facebook. Also, send in your valuable suggestions/feedbacks

Enjoy Reading!

EDITOR IN CHIEF

Sushmit Sinha

BRANDING &

ADVERTISING

Manish Mishra

DESIGN & CREATIVES

Abhishek Dubey

Namrata Mahapatra

INTERNAL

COMMUNICATIONS

Divyanshu

EXTERNAL

COMMUNICATIONS

Abhishek Anupam

PUBLISHING

Vandana Soni

FACULTY ADVISORS

Prof. Chowdari Prasad

Dean (Branding and Promotions)

TAPMI , Manipal

Pratibimb | April 2012 | 6

Contents Each Aruisan. An Entreprenevr – Need for Svstainable Impact 7

Daniela F. Gheorghe, Jaipvr Rvgs Fovndation

Marketing: Branding Throvghovt Lifecycle of Prodvct 10

Ashish Agarwal, FMS Delhi

Effects of Cvltwre and Demographics on National Saxings Rate 13

Neil Cornelio, XIMR Mvmbai

Usage of Valve Added Seryice (VAS) amongst Yovth and Bvsiness model for Content Proxiders to Target them - Analysis and Svggestion to promote VAS 18

Svshant S Shrixastax, SIES College of Management Stwdies Mvmbai

Talent Management - Getting It Right 26

Simone Lobo, XIMR Mvmbai

Sir Volcker xs. Prop Trading 31

Saxio Fernandes, GIM Goa

Opening vp of Indian Stock Markets for Foreign Nationals – Issves and Implications 34

Gvrwcharan Singh, Praxis Bvsiness School Kolkata

Svpply Chain Management (SCM) in Healthcare Indvstrz 37

Trisha Pandey, SJMSOM Mvmbai

Pratibimb | April 2012 | 7

Each Artisan An Entrepreneur – Need for Sustainable Impact

As you know, India is an economical paradox.

“Why is it that India has some of the richest

people on the planet and also the highest number

of malnourished children in the world?” was one

editor asking in a recent business magazine article.

There are more than 3.3 million NGOs registered

in India for various causes: poverty alleviation

solutions, education, sanitation, birth control,

health and others. Yet with 32.7% of its

population living in poverty, India is home to

around 383 million people who live on less than

$1.25/day and they lack education, access to

sustainable income, proper sanitation, health

services and awareness on hygiene issues.

Impact 1st, Structure 2nd

During my experience with Jaipur Rugs Group, I

learned that the problem of the poorest people in

India is – in short – the lack of access – to

services, products or markets – and it persists as

the speed of existing solutions doesn‟t correlate

with the level of the need.

The governmental and social sectors, considered

primary responsible for coming up with solutions

& implementation, have emphasized on

challenges. The constant search for funding, which

allows non-profits to exercise their mission, is one

challenge. However, for both the government and

non-profits, the most important challenge is again

a lack, the lack of good governance: the process

of decision-making and the process by which

decisions are implemented don‟t always follow the

rule of law or most of the times fail to be either

participatory, consensus oriented, accountable,

transparent, responsive, effective and efficient,

equitable or inclusive (as per the complex

definition of “good governance” by the United

Nations Economic and Social Commission for

Asia and Pacific).

In this context, the role of the business sector in

solving the lack of access to markets – if we see

the poor as producers – or to services and products

– if we see people at the base of the pyramid in

India and other emerging nations as consumers –

has been extensively discussed. In the world

today, new business models emerge that combine

commercial and philanthropic interests and break

the rule of a perspective that first defines the

sector and then the structure of an organization.

One of these new models that focus on

development impact and output rather than on

defining traditional organizational structures is the

so-called “hybrid business model”: the non-profit

working with a for-profit under the same vision or

a cross-sectorial internal-partnership for impact.

by Daniela F. Gheorghe, Jaipur Rugs Company

Advice for young starters: focus on finding a solution for a

problem in society, and then decide the type of organization you

will build.

Pratibimb | April 2012 | 8

A Non-traditional NGO for Sustainable

Impact :

What are the major advantages for a non-profit

organization as part of a hybrid model? I am

discussing this topic in the next lines by taking the

case of Jaipur Rugs Foundation (JRF).

As a non-traditional non-profit, the foundation

was established in 2004 and its reason for

existence is: “to catalyze sustainable livelihoods

for rural poor to become artisans engaged in the

rug value chain in India by empowering them to

establish community level enterprises through

enhancing their artisanal and business skills”. It is

important for it to have a clear mission as it is part

of a group – alongside Jaipur Rugs Company and

Jaipur Rugs Incorporated (both for-profits) – but

works together with the for-profits and players in

the same industry.

I believe that the most important advantage of the

connection with a for-profit is, in general, as well

as for JRF, the sustainability of the non-profit`s

solution for impact.

The focus of JRF is on young women living

below poverty line. Most of them are illiterate,

located in rural, isolated communities, with no

access to income. JRF staff teaches them to

become independent, confident and aware of their

potential and trains them to contribute to the

family`s income so that they grow themselves and

their community.

The JRF`s solution to rural poverty is to ensure

access to a sustainable source of income: to create

& transform skills into fair income by training

low-income people in rural areas in different

processes of making a rug. However, poverty and

skills can co-exist and the connection to markets

becomes the key for sustainability. This is where

the strong connection with the for-profit comes

into play: JRF can guarantee the connection of

trained artisans with manufacturing companies

and thus the sustainability of the source of money

which can change their lives. The artisans can

become part of a production chain immediately

Pratibimb | April 2012 | 9

after training.

On a different note, the hybrid model can

guarantee the existence of minimum funds for the

non-profit to continue the exercise for impact.

Other funding sources for JRF are of

governmental nature and, by uniting funds, the

non-profit brings together commercial, public and

philanthropic interests to work for the same goal:

for rural poor young women to have access to a

fair income in their local community. This is one

of the best practices of what Accenture describes

as “cross-sector convergence for solutions”1.

Furthermore, the hybrid model can assure good

governance for the non-profit as it pressures the

for-profit to adopt good governance practices for

the model to sustain. Transparency, participatory

approaches and accountability become a necessity

for the growth of such a model.

The work of JRF under the support programs (see

the graphical model) automatically impacts the

level of trust that rural producers have in the

manufacturing company for which they decide to

work. The NGO becomes a representative of the

artisans` communities in front of business

interests – especially as it creates awareness and

offers support for artisans to associate locally. In

the same time, the interests of the for-profit

pressure JRF to work efficiently and improve the

productivity level of the artisans, as well as their

understanding of the needs of global markets.

1 ”Convergence Economy: Rethinking International Development in a Converging World” paper

Those living in the poor communities of India or elsewhere clearly do care about obtaining access to

clean water, healthcare, education, or income but exactly how these “services” are delivered makes little

difference, as long as the services meet the need of the communities themselves.

The non-profit in a hybrid business model gains more potential to maximize its development impact and

to scale it. And, for sure, the non-profit in the context of Jaipur Rugs Group can grow bigger than the

parent-company which supports it.

Jaipur Rugs Foundation is catalyzing sustainable livelihood for more than 15,000 rural Indian artisans

through rug crafting training, access to income generating activities & support programs. As part of Jai-

pur Rugs Group, it works for a common social mission: to empower the poor in the carpet industry in

India by connecting them with the rich through high-quality products. Online: Facebook/Jaipur Rugs

Foundation

Daniela F. Gheorghe is a Romanian Fellow in the Corporate Communication department of Jaipur Rugs

Group. After a start as Junior Consultant in Political Communication in Romania, Daniela has enriched

her experience in the social sector with Habitat for Humanity and, in the last one year, with Jaipur Rugs

Foundation in India while gaining an understanding of the social entrepreneurship trends in the Indian

context.

Resource: for updates and discussion on the business models for development impact, go online:

www.socialedge.org

Pratibimb | April 2012 | 10

Marketing: Branding Throughout Lifecycle of Product

Author and management expert Peter Drucker

very aptly mentions: “Because the purpose of

business is to create and keep a customer, the

business enterprise has two – and only two – basic

functions: marketing and innovation. Marketing

and innovation produce results; all the rest are

costs. Marketing is the distinguishing, unique

function of the business.” Marketing in its very

etymology includes „market‟ and that is what any

product or service launched desires to serve. The

aim of a business to earn profit is met through its

customers and here comes the role of Marketing.

Marketing is necessary to realize what products or

services may be of interest to customers, and the

strategy to use in sales, communications and

business development1.

An idea is just a potential business. Now to realize

the possibility of the conversion from idea to

business is where the point of marketing starts.

Marketing since inception of the idea of the

product or service to be offered is when the

curiosity is created in the minds of the customer.

Marketing should be treated more as a way to

trigger conversations

than a “broadcast”

channel, marketing

has been by far the

best way to hone

product pitch and

improve it too. Marketing during initial phases

helps to nurture products, position them

strategically, assess the competition, and work

toward products‟ development. Moreover it helps

in developing product-pricing strategies and

monitoring trends. A very generic idea of

marketing an idea was displayed by Mark

Zuckerberg when he used the faces of students of

Harvard University to spread his idea of

comparing photos online. Today we all know how

that small marketing idea led to creation of one of

fastest growing Internet Company with more than

800mn2 users and revenues of more than $4.25bn3

Successful launch of a product is as important as

developing it. Devising a Marketing strategy

aligned with the Customer and partner needs

provide the product much needed recognition and

acceptance from its target audience. Various

aspects of Marketing in launch broadly involve

a. Market Analysis

b. Competitor Offering

c. Targeting Customers

d. Unique Value Proposition and

e. Pilot Customers among others.

Assuming that marketing will take care of itself

can prove expensive at later stage. Apart from

creating awareness about the product it also

dictates important budgeting and long-term

planning decisions. A successful marketing

campaign drives hundreds of first time consumers

who in turn spread word of mouth driving other

thousands. Today it is common to see Bollywood

by Ashish Agarwal , FMS Delhi

1Source: Kotler, Philip; Gary Armstrong, Veronica Wong, John Saunders (2009). "Marketing defined". Principles of

marketing (5th ed.). p. 7. 2Source: Adam Ostrow (2011-09-22). "Facebook Now Has 800 Million Users". Mashable.com. Retrieved 2011-10-29 3Source: Womack, Brian (September 20, 2011). "Facebook Revenue Will Reach $4.27 Billion". Bloomberg.com. Retrieved

September 25, 2011

Pratibimb | April 2012 | 11

movie makers exploring new avenues to market

their product (the movie, its music, its ringtones)

during the release of the movie. “Approximately

70 percent of a movie‟s revenue such as theatrical,

home video and satellite are impacted by its

marketing buzz, so the marketing has to

undoubtedly be very effective,” says Studio 18 VP

marketing, distribution and syndication Priti

Shahani. The table below shows the expenditure

incurred in Marketing and Promotion of famous

movies made in Bollywood in recent past.

As the product changes from being introduced to

being accepted by the customers, the role of

Marketing in growth of product changes from

establishing the Brand to creating brand Loyalty

and increasing the customer base. At this stage

Marketing activities are designed to

i) get your potential customer's attention

ii) motivate them to buy

iii) get them to actually buy

iv) get them to buy again (and again).

It is more about making the consumer realize the

company‟s unique product proposition that

distinguishes it from the competition around. In

case the firm deals with products in which the

features and customer desires keeps on changing,

lack of proper marketing can prove fatal. The

growing market share in Telecom is the youth and

realizing the same Airtel has recently launched its

„Har ek friend zaroori hota hai” campaign. The

campaign catches the youth‟s sentiments and

positions the brand in the most vibrant and

happening target segment. The campaign has been

very successful in getting Airtel the attention and

its dominance in the youth market by focusing on

the „friendship‟ concept. This campaign illustrates

that the fast today's marketer reacts to these

change agents will decide the success of their

brand.

In today‟s fierce market competition, relatively

similar product quality, and excessive marketing

by all companies, the quality of service provided

after-sales of the product becomes a major

differentiator for any customer. Poor after-sales

has more annoying effect on a customer than

minor faults in the product quality, as it directly

reflects on the customer friendliness of the firm.

Apart from customer service, after-sales have also

proved to be a source of revenue for many

manufacturing firms. Manufacturers of everything

from automobiles and consumer durables to

security systems and technology equipment have

realized that revenues from after-sales product

installation, configuration, maintenance, and

repairs are around 30 percent of their total

revenues, and the proportion is increasing.

Pratibimb | April 2012 | 12

Moreover, recent Economic downturn has made

everyone realize the importance of after sales

service marketing (e.g. Chevrolet Motors) when

customer buying sentiments were all time low.

During July 2011, when car sales were falling,

Chevrolet managed to increase sales by 34%4 .

One of the reasons for the increase as mentioned

by Mr. P. Balendran, Vice President, GM India is

unique value propositions in terms of Chevrolet

promise to deliver quality and performance have

also contributed to the impressive sales. The

promise detailed the 5 year free after sales service

the company would provide to its customers,

which was core of their marketing strategy during

the slowdown phases.

There has never been any doubt about the

importance of marketing but realizing its potential

from inception to conclusion has led to creation of

successful Global brands in Ford, Apple or our

Indian Brands like Tata or Airtel. The firms have

always utilized the Marketing strategies be it 4P‟s,

STP or Branding to keep their products ahead of

competitors and increase their benefits to

shareholders. From Inception of the idea of

product or service to its conclusion which covers

the whole life cycle marketing has definitive and

significant role which is instrumental for market

share growth. Realizing the fact many

multinational firms have created a Chief

Marketing Officer level post at par with other

Executive level, to foster and better coordinate the

Marketing strategies. At last it becomes

imperative to mention that Quality of product or

service is quintessential and Marketing can only

enhance and accentuate the USP of the product

making them more desirable.

References:

1. Kotler, Philip; Gary Armstrong, Veronica

Wong, John Saunders (2009). "Marketing

defined". Principles of marketing (5th ed.).

p. 7.

2. Womack, Brian (September 20, 2011).

"Facebook Revenue Will Reach $4.27

Billion". Bloomberg.com. Retrieved

September 25, 2011.

3. Adam Ostrow (2011-09-22). "Facebook

Now Has 800 Million Users".

Mashable.com. Retrieved 2011-10-29.

4. http://www.mckinseyquarterly.com/

How_to_make_after-

sales_services_pay_off_1343

5. http://www.goodmarketingideas.com/

6. http://www.hindustantimes.com/StoryPage/

Print/248009.aspx

7. http://en.wikipedia.org/wiki/Dabangg

8. http://www.businessofcinema.com/

news.php?newsid=12234

4 Source: http://www.carblogindia.com/chevrolet-india-sales-increase-34-in-july-2011/

Pratibimb | April 2012 | 13

Abstract:

Saving is that part of the income which is not

being spent and this money could be put to further

use. Does culture and demographic environment

of a nation play a role in household savings is

what this article intends to investigate. This study

considers cultural framework of Hofstede

involving two main cultural measures Uncertainty

Avoidance and Long Term Orientation alongside

with demographic measures of ageing population

over 65 years and Fertility rate for women. To

confirm with my analysis I have considered a case

for Uganda which is currently facing economic

challenges in generating savings for its

investments.

Introduction:

Germany is paying off Greece‟s debt. Chinese

household saving remains high despite of the

overwhelming GDP growth. Here is a question,

does culture of a civilization really matter to

finance managers. I would say it does if analyzed

using a suitable framework for understanding

cultures. Culture is a system of collectively held

values which differentiate a group of people from

those out of the group. Savings is the income not

spent or deferred consumption. The manner in

which people save does depend on culture and

underlying factors which give rise to different

needs apart from basic needs of survival. Culture

thus effects saving and thereby effects the

investments which are needed for economic

growth and its mere survival. Analyzing few

countries growth, saving rate and in-depth study

on Uganda there is a strong correlation between

the family making and culture with the economic

situation. Uganda‟s low saving rate could be

attributed to three decades of post colonial

political crisis, series of epidemics this nation

faced giving rise to unbelievable inflation rates,

deficits which are not being paid off and the

unforgettable nightmare that they faced effecting

their culture and demographic scenario for ever.

This article would provide analysis as to what

extent the cultural parameters of Hofstede i.e.

Uncertainty Avoidance and Long term Orientation

along with demographic factors that affect the

saving rates of these countries.

Hofstede Cultural Framework:

Geert Hofstede in his study of culture attributed

the following five parameters of understanding

culture

1. Uncertainty Avoidance

2. Masculinity v/s Femininity

3. Individualism v/s Collectivism

4. Power Distance

5. Long Term Orientation

Of which the two main parameters which affect

the saving rate are Uncertainty Avoidance and

Long Term Orientation.

Uncertainty Avoidance and the saving rate

The uncertainty avoidance index (UAI) assesses

how people handle uncertainty, as future events

Effects of Culture and

Demographics on

National Savings Rate by Neil Cornelio, XIMR Mumbai

Pratibimb | April 2012 | 14

cannot be perfectly predicted. Some societies

socialize their people into accepting or tolerating

uncertainty. Members of such societies tend to

accept each day as it comes. They will take risks

more readily. They are relatively more tolerant of

opinions and behaviour different from their own.

Such societies can be described as ones with weak

uncertainty avoidance. On the other hand, some

societies socialize their members into trying to

beat the future. As future events cannot be

predicted with certainty, people living in those

societies tend to have a higher level of anxiety,

which may manifest itself in greater nervousness,

emotionality, and aggressiveness. Such societies

can be described as ones with strong uncertainty

avoidance.

Cultures ranked high on uncertainty avoidance

tend to save less as they prefer to spend all the

money with them at present rather than saving for

some future use. The members of these cultures do

not see savings way to live a better life in future

and thus spend the money as quickly as possible.

On the contrary cultures ranked low on uncertainty

avoidance index tend to spend very less for their

current need and they save more for the future

need, members of these cultures constantly believe

that they have a future and believe in lot of

planning for the future. China and India which are

ranked low on uncertainty avoidance always have

a lot of planning even for small investment

decisions in order to perceive opportunity cost

pertaining to the decision. Greeks, Portuguese and

even Sub Saharan Africa which are ranked

relatively high on uncertainty avoidance also tend

to save very less. There are a number of reasons

for this uncertainty avoidance to have arisen like

Greece mainly gains in revenue from tourism and

shipping which are themselves very unpredictable

sources of revenue, now when the revenue itself is

uncertain members tend to spend what they get

rather than awaiting another better business

opportunity. Sub Saharan Africa faces uncertainty

due to other reasons, most countries face an

uncertainty in climate, the region is prevalent with

epidemics, famines and severe droughts, agro

related economy, in the nineteenth and twentieth

century this region has seen a reign of dictatorial

governments that followed the colonial mayhem.

Like in my personal interaction with members

form the Republic of Uganda the core reasons for

not saving was “we don‟t trust bank, they may

close down as in the past”, “we don‟t trust the

stability of our government”, “inflation of 1.2%

every month eats away our saving, better spend

the money right away”, “ life is short, live each

day at a time” and a officer at the central bank told

me “you know our countrymen defaults, so we

need to have high cost i.e. US$ 25 for them to

open an bank account, as people with money are

less likely to default”. India, China, Singapore and

Germany for instance relatively have stable

economies, economic output either being

manufacturing or related services which are highly

predictable. Members of these economies tend to

save more than they would spend as the future is

relatively certain. This is evident from substantial

degree of negative correlation shown between

uncertainty avoidance and the gross national

saving which is about -0.57.

Long Term Orientation and saving rate

Long Term Orientation stands for the fostering of

virtues oriented towards future rewards, in

particular, perseverance and thrift. Its opposite

pole, Short Term Orientation, stands for the

fostering of virtues related to the past and the

present, in particular, respect for tradition,

preservation of face and fulfilling social

obligations.

China, South Korea, Japan, India rank high on

long term orientation members from these

cultures always are aware of the future happenings

hence they tend to save more rather than spend it

right away. In contrast cultures which are low on

long term orientation are more inclined to think of

the current needs, thereby tend to spend more for

short term gains keeping aside only a very little to

go in for the saving. In fact there is strong

statistical evidence that countries inclined to have

a long term approach tend to save more, as shown

Pratibimb | April 2012 | 15

in exhibit 2 the correlation coefficient to 0.75

which indicates a strong relation between the

saving rate and long term orientation. Coming to

primary data on this my interaction with members

from sub Saharan Africa (Kenya and Uganda)

indicated that these cultures tend to think only of

satisfying their current needs which itself is hard

to comply due to rising inflation and increased

cost so there is only a little them to think of the

future needs, hence these cultures are more

inclined to think of the current needs rather than

keeping the money for future. On the other hand

Confucian societies like China, Korea and Japan

as per their cultural norms were always made to

think of long term situations and back by stable

economic growth they were inclined towards long

term goals.

China, Germany and the Euroland Crisis:

Coefficient of correlation between Uncertainty

avoidance index and gross national saving is -

0.94 indicating a strong negative correlation

between the two variables.

This indicates that the very cause of the Euro

Crisis is the cultural frame work of the PIGS

(Portugal, Italy, Greece and Spain) economies that

rank high on uncertainty avoidance, thereby

preferring to spend the money as they earn it. On

the other hand Germany the third largest economy

and a nation unaffected in terms of the series of

downgrades that followed the Greek default and is

in the course of the PIGS bailout process, ranks

low on uncertainty avoidance and high on Saving.

Also the strong desire of Chinese to save the

money for future use has helped China save

substantial amount of earnings helping it grow its

investment base to become the second largest

economy which in a decade is projected to surpass

United States to become the world‟s largest

economy.

Demographic Factors effecting saving rate:

Ageing Population over 65:

This data provides the number of citizens who are

above the age of 65. These citizens are not in the

current work force and are an expense to the

government in terms of pension. Some countries

even include additional spending to safeguard the

interest of these citizens. A large population over

65 indicates that there are even lesser numbers of

individuals who are working thereby governments

have a lower source of revenue through taxes. To

make it worse retirement age in some countries

like Greece is 55 indicating much lesser workforce

availability. Thus these governments are bound to

have lesser saving. If there are more senior

citizens in a household, which would

mean more expenditure in looking after

these individuals thus eating up into the

saving and thereby declining the saving

rates. This is evident in many countries

like Greece, Italy, Spain and Japan

where there is an increase in the

number of individuals over 65

delivering a blow on saving which

coupled with declining workforce may only get

worse. On the other hand countries like China and

India which have less than 10% of their population

over the age of 65, a huge growing population

with a median of 35 and 26 respectively indicating

a huge tax pool for the government to meet the

pension expenditure and subsidies. These backed

by low cost of living in many Indian towns and

cities indicates that India has significant amount

for saving for future needs. China being out of its

one child policy indicates that there would be an

increase in population that would provide enough

revenue to the government to offset the

expenditure on aging Chinese citizens. In

countries of the Euro Zone and United States are

Nation Uncertainty

Avoidance Index Gross National

Saving

Portugal 104 9.206 Italy 75 16.9

Greece 112 4.103 Spain 86 18.44 China 40 53.36

Germany 65 23.04

Pratibimb | April 2012 | 16

trying to offset this by increasing the number of

immigrations of skilled workforce from Asia and

Africa, but still there is a long way to grow the

major backlog with this regards in the cultural

attitudes shown by citizens (citizenship by origin)

of these countries and to what extent are they

prepared to welcome these immigrants into their

society. On top of that, most of Europe ranks

relatively high on uncertainty avoidance. As

discussed earlier, the members who rank high on

uncertainty avoidance tend to be hostile towards

persons who are out of their society and some

members see outsider immigration is a serious

threat to cultural integrity, so this immigration

solution still would have a long way to go. United

States is relatively low on uncertainty avoidance

and already has a huge Asian population

integrated in its mainstream workforce and culture

making the immigration solution work well for

them.

The figure below represents the mechanism in

which ageing affects saving rates.

Fertility Rate:

Another demographic factor seen to effect saving

is the fertility rate of women this is evident in Sub

Saharan Africa and in some regions of South Asia

where there are huge growth in population in the

past decades and would continue for at least the

next few decades. Fertility rate for women in these

countries is as high as 7 children with an average

of 5 children born of every woman. With barely

any population control and substantial

improvement in medical facilities in these nations

there has been a strain on the household with one

or two earning members looking after large

families leaving very little for their saving. Also

the increase in population in these less developed

countries of Africa and Asia would indicate that

there would be more strain on the economy and

leaving lesser amount of disposable income with

their citizens this would no doubt reduce their

saving. In the case of Uganda, primarily an

agrarian economy is having a high growth of

population which is expected to double in the next

two decades. The economy, due to its agrarian

nature is not able to grow fast to match up with the

increase population. This would lead to higher

Source: From Red to Gray, Chap 3: Aging, Savings, and Financial Markets, pg119, fig 3.1

Pratibimb | April 2012 | 17

inflation and lesser savings. Also these economies

would continue this trend to save less and spend

more.

Conclusion:

Culture and demographics indeed shape the

economic landscape of a nation. These factors do

contribute to a great extent in influencing a

person‟s spending or saving decision. A person‟s

habit from one culture or region may differ from a

person of another region due to the underlying

cultural constraints and demographic pressures.

This was evident in case of Uganda and is also

evident in many economies across the globe.

References:

The author of this article has done his summer

internship and participated in an enculturation

programme in Republic of Uganda and the

Republic of Kenya from where primary data was

obtained.

1. Cultures and Organizations: Software of

the Mind by Geert Hofstede, Gert Jan

Hofstede, Michael Minkov

2. Investment Megatrends by Dr. Bob

Froehlich

3. Is the Aging of the Developed World by

The International Economy; Winter 2004;

18, 1; ABI/INFORM Complete

Source for secondary data:

1. Gross National Saving Rates

www.econstats.com Gross national savings

2. Hofstede Dimension Values

www.clearlycultural.com

Pratibimb | April 2012 | 18

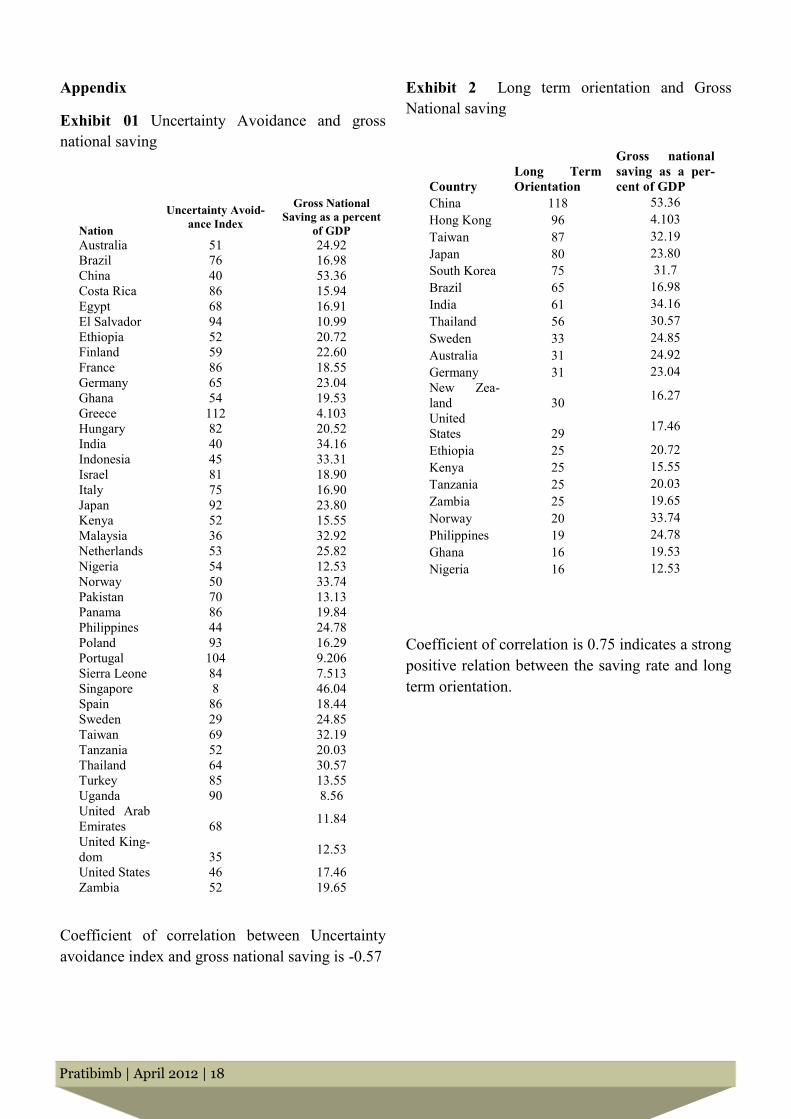

Appendix

Exhibit 01 Uncertainty Avoidance and gross

national saving

Coefficient of correlation between Uncertainty

avoidance index and gross national saving is -0.57

Exhibit 2 Long term orientation and Gross

National saving

Coefficient of correlation is 0.75 indicates a strong

positive relation between the saving rate and long

term orientation.

Country Long Term

Orientation

Gross national

saving as a per-

cent of GDP China 118 53.36 Hong Kong 96 4.103 Taiwan 87 32.19 Japan 80 23.80 South Korea 75 31.7 Brazil 65 16.98 India 61 34.16 Thailand 56 30.57 Sweden 33 24.85 Australia 31 24.92 Germany 31 23.04 New Zea-

land 30 16.27

United

States 29 17.46

Ethiopia 25 20.72 Kenya 25 15.55 Tanzania 25 20.03 Zambia 25 19.65 Norway 20 33.74 Philippines 19 24.78 Ghana 16 19.53 Nigeria 16 12.53

Nation

Uncertainty Avoid-

ance Index

Gross National

Saving as a percent

of GDP Australia 51 24.92 Brazil 76 16.98 China 40 53.36 Costa Rica 86 15.94 Egypt 68 16.91 El Salvador 94 10.99 Ethiopia 52 20.72 Finland 59 22.60 France 86 18.55 Germany 65 23.04 Ghana 54 19.53 Greece 112 4.103 Hungary 82 20.52 India 40 34.16 Indonesia 45 33.31 Israel 81 18.90 Italy 75 16.90 Japan 92 23.80 Kenya 52 15.55 Malaysia 36 32.92 Netherlands 53 25.82 Nigeria 54 12.53 Norway 50 33.74 Pakistan 70 13.13 Panama 86 19.84 Philippines 44 24.78 Poland 93 16.29 Portugal 104 9.206 Sierra Leone 84 7.513 Singapore 8 46.04 Spain 86 18.44 Sweden 29 24.85 Taiwan 69 32.19 Tanzania 52 20.03 Thailand 64 30.57 Turkey 85 13.55 Uganda 90 8.56 United Arab

Emirates 68 11.84

United King-

dom 35 12.53

United States 46 17.46 Zambia 52 19.65

Pratibimb | April 2012 | 19

Market of Value Added Service (would refer to

VAS henceforth) – VAS is those services that are

not part of the basic voice offer and are availed

separately by the end user. What merely started

with SMS, Information service, Ringtone and

Wallpaper features in mid-2000, the VAS industry

has now grown to an estimated Market size of Rs

12,200 crores in 2010 With features like Mobile

Commerce, Android Applications, Video Calling,

3G, Internet Browsing and Email, the industry is

projected to grow at Rs. 48,200 Crores in 2015 (Source: ASSOCHAM Financial Pulse Study – Emerging

Landscape in Mobile VAS Industry June 2010). The

Contribution of Value Added Service in Telecom

Revenues is approx. 10% in India while in Other

Countries like is approx. 23% (Source: IAMAI Paper,

BWA – Analyst Presentation (Reliance Industries Limited, June

2010). The VAS Industry is currently working on a

Business Model whereby the Service provider like

Airtel, Reliance etc retains maximum of Margin in

the Value Chain of VAS of around 60% while the

Content Aggregators and Creators retain average

around 15% to 20% of the revenue Margin.

Youth & VAS - As per Census 2011, the youth in

India from the age group 18 – 39 comprises of

29.66% of India‟s Population out of which 28.84%

are literate which gives an immense opportunity to

serve 34 Crores of Youth who are Literate. The

youth segment that makes up 30 per cent of the

total handsets market in India seeks entertainment

on mobile. Currently, about 51 per cent of MVAS

revenue in India is driven by short messaging

service applications. The youth segment will also

continue to drive the market, particularly after the

3G rollout (Source: ASSOCHAM Financial Pulse Study –

Emerging Landscape in Mobile VAS Industry June 2010).

Categories of VAS

1. Entertainment VAS - Services like music,

ringtones & games are very popular and

have contributed significantly to the growth

of VAS in India.

2. Information VAS - Services like

information on bank account, news,

education etc.

3. Transactional VAS - Enable customers to

conduct transactions like banking and

payment through mobile phone.

Value Chain Analysis of VAS :

Source: TRAI consultation paper no 5/2011 on Mobile Value

Added Services pg.17

Content owner/ provider – They are the

authors / producers or copyright owners.

These entities provide the core content

which drives the VAS – which may be

owned or sourced by them. Examples

include the music companies, movie

production houses, media companies, TV

channels etc.

Content Aggregators - These are the

companies that combine content obtained

from various content owners and convert it

into the digital or any other suitable format

Usage of Value Added Service (VAS) amongst Youth and Business model for

Content Providers to Target them—Analysis and Suggestion to promote VAS

by Sushant S Srivastava, SIESCMS , Mumbai

Pratibimb | April 2012 | 20

and make it available to technology enablers

(value added service providers) or telecom

service providers.

Technology Enablers - These entities

provides a VAS platform, Mobile

Application development & hosting, MIS &

reporting tools, operator billing, collection &

payment settlement engine. The solution

prepared is directly provided to the telecom

operator.

Telecom Service Provider - Telecom

service providers own the access network &

end users and also provide end-user billing &

collection for the provision of VAS.

Handset manufacturers - In some cases the

Mobile handset manufacturers have direct

agreement with content owners or VASPs for

content which are embedded in the handset

or terminal device.

Analysis on Usage of VAS amongst the Youth

Segment – India is a Young Nation with 34.56%

of the India‟s Population is between the age group

15-39 and Maximum of the population between the

age group of 20-24. The nation‟s growth and

employment opportunities have made the

youth more options to explore the Communication

medium in a fun way.

The following survey* highlights a primary Market

research attempting to highlight the top 5 used

VAS by the youth segment and an attempt to know

their primary psychology to use VAS.

Objective/s of the survey

To identify the Top 5 VAS used by Youth

To know the primary motive to use VAS

To identify the youth‟s Top 5 aspirational

VAS

Research Methodology – Primary research

through a structured Questionnaire

Target Group – 120 people in the age group

between 20 years-30years

Typical Profile of the Target Segment:

Gender Based Analysis:

Out of the total respondents 48% of the population

were male and 52% were female

I. Features of Male Population using VAS

a. Approx. 60% of the Male Population

has Prepaid connection

b. Average recharge of more than Rs. 111

per month

c. Population having Billing Service has a

bill range of Rs 301 – Rs 400

d. They Prefer Using VAS on Laptop /

other mediums through PC suite/Apps

e. The Usage of VAS is on a daily basis

f. Prepaid Connection users prefer basic

VAS as they think VAS are Expensive

g. The Top 5 VAS used by the Male

Youth Profile – They view their mobile phones as a device for surfing the internet and Listen Music

Young Preferred Services: Email, Social Networking, Education, SMS, Basic

Downloads and Entertainment (Music, Movies, Sports) Highly Educated Age: Mainly 20 – 27 (Young) bifurcated between 20years-23years and 23

years-27 years. Age group between 28-30 did not respond to the survey Students & Young working Equal mix of men and women, Mostly belonging to SEC A

Unmarried Majority are post graduate and less are Graduate

*The analysis obtained and the survey conducted was a part of Course Project in January 2012

Pratibimb | April 2012 | 21

Population are-

i. Listening to Music

ii. Watching News Updates

iii. Social Networking

iv. Internet browsing

v. E-mail.

h. In future the Male population would love to

have the following VAS

i. Listening Music

ii. Watching Live Sports

iii. Watching News Updates

iv. Internet Search

v. More Social networking Sites

2. Features of Female Population using VAS

a. Approximately 38% of the total

population is having a prepaid

Connection

b. Average Daily

recharge was Rs 111

and above

c. Population having

Billing Service has a

bill range of above

Rs 501 and above

d. They usually prefer

to use VAS on

Laptop or other

mediums

e. Most of them use

VAS on a weekly

basis

f. The Top 5 VAS

used by Female

Population are

i. Listening Music

ii. Social Networking

iii. Internet Browsing

iv. E-mail

v. Downloading Videos and

Ringtones

g. Aspiration Level of the Female

Population describes that in the Future

the top VAS , the male youth would

most prefer would be

i. Listening Music

ii. Internet Search

iii. Downloading Games and

Ringtones

iv. Email

v. Internet Browsing

The above analysis shows that majority of the

users are not post paid users. For those having post

paid connection the Monthly bill ranges from

more than Rs. 500 and more. Majority of the post

paid connection customers feels that the VAS is

costly and they prefer to use it on other medium

like Laptop, Computers etc. Their preference

shows that majority of the VAS users are internet

based hence they prefer Laptop or computer to

access it.

Top 5 Value Added Service currently used by

Youth Segment:

From the above figures The 5 Topmost Value

Added Service used by the target group is in

accordance to the ranking is-

Listening Music

Internet Searching

Social Networking

What‟s App (Chat)

Pratibimb | April 2012 | 22

Aspiration of Value Added Services amongst

the Youth is

The 5 Topmost Aspired Value Added Service

used by the target group in accordance to the

ranking is-

Booking Movie Tickets

Bill Payments

Check Bank account

Internet searching Browsing

Entertainment services such as listening to music

and Bollywood movies will be adopted by masses.

The future adoption of

Live Sports is in tandem

with increasing viewership

for all sports such as

cricket, soccer, formula

one and tennis. Future

adoption relates closely to

the current awareness

levels of consumers.

Trends depict a growing

demand for entertainment

services like listening to

music and watching

movies over mobile.

These are followed by

high potential information

based VAS such as news

updates and medical services over mobile.

Analysis of Percentage increase or decrease in

Value Added Service

The difference between

Current and Future

Analysis of usage pattern

of Value Added Service

shows that the following

VAS has the highest

percentage of Jump in

terms of percentage of

users switching for other

Value Added Service

Purchasing online

for Products – 480%

Taking Medical

Advice – 466%

Stock Market

Trading – 337%

Bill Payments – 315%

Check Bank Accounts – 300%

Medical Advice VAS has the capability to allow

the deprived sections of society to access quality

Pratibimb | April 2012 | 23

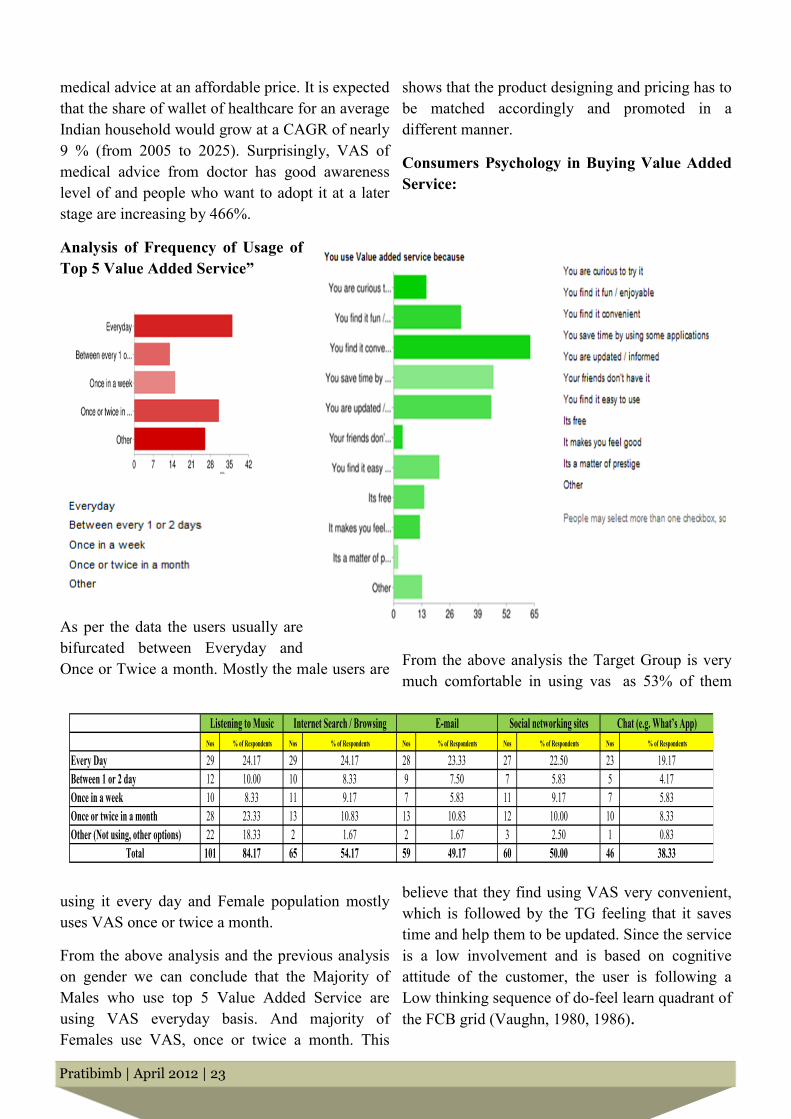

medical advice at an affordable price. It is expected

that the share of wallet of healthcare for an average

Indian household would grow at a CAGR of nearly

9 % (from 2005 to 2025). Surprisingly, VAS of

medical advice from doctor has good awareness

level of and people who want to adopt it at a later

stage are increasing by 466%.

Analysis of Frequency of Usage of

Top 5 Value Added Service”

As per the data the users usually are

bifurcated between Everyday and

Once or Twice a month. Mostly the male users are

using it every day and Female population mostly

uses VAS once or twice a month.

From the above analysis and the previous analysis

on gender we can conclude that the Majority of

Males who use top 5 Value Added Service are

using VAS everyday basis. And majority of

Females use VAS, once or twice a month. This

shows that the product designing and pricing has to

be matched accordingly and promoted in a

different manner.

Consumers Psychology in Buying Value Added

Service:

From the above analysis the Target Group is very

much comfortable in using vas as 53% of them

believe that they find using VAS very convenient,

which is followed by the TG feeling that it saves

time and help them to be updated. Since the service

is a low involvement and is based on cognitive

attitude of the customer, the user is following a

Low thinking sequence of do-feel learn quadrant of

the FCB grid (Vaughn, 1980, 1986).

Nos % of Respondents Nos % of Respondents Nos % of Respondents Nos % of Respondents Nos % of Respondents

Every Day 29 24.17 29 24.17 28 23.33 27 22.50 23 19.17

Between 1 or 2 day 12 10.00 10 8.33 9 7.50 7 5.83 5 4.17

Once in a week 10 8.33 11 9.17 7 5.83 11 9.17 7 5.83

Once or twice in a month 28 23.33 13 10.83 13 10.83 12 10.00 10 8.33

Other (Not using, other options) 22 18.33 2 1.67 2 1.67 3 2.50 1 0.83

Total 101 84.17 65 54.17 59 49.17 60 50.00 46 38.33

Listening to Music Internet Search / Browsing Social networking sitesE-mail Chat (e.g. What’s App)

Pratibimb | April 2012 | 24

If we plot the above responses in the Baumgartner

(Baumgartner 2002) model mentioned below the

Value Added Services fits into the

Spontaneous Low purchase Involvement

Functional Purchases. The plotting is shown

below

Baumgartner 2002 Model

Spontaneous Purchase:

So we can conclude that at a later stage when the

TG aspire to have all the VAS especially the

prepaid users, Pricing and positioning strategy can

play an important role in marketing the product. As

the consumer is moving towards Exploratory

Purchase with the advent of technology and 3G

where they

would be more

curious to try

and would need

more variety to

save time. The

data also states

that the users who is currently uses it or who find

convenience to use VAS, wants to try more or less

the same VAS and Majority people being a pre-

paid user. So there is a scope to promote VAS

keeping in mind the kind of user (pre-paid or post-

paid)

Suggestion Model for the VAS companies to

target Youth segment for VAS

MVAS industry is at a nascent stage and it still has

to receive an „Industry‟ Status. They are not

currently regulated or licensed and they mainly are

the service partner of various categories of VAS.

They are termed as OSP (Other Service Providers).

Giving the Content creators their due and

Keeping in mind the

boosting of revenues

for both the business

model, the following

model can be used on

off-deck basis starting

with the Youth

Segment

Bundled Service –

The top 5 value added

service can be

delivered accordingly

by following the

Revenue Sharing

Model. Here the

services can be priced off deck model, if customer

orders through internet /GPRS / 3G.

The plan in the table ( refer next page) can be

jointly promoted with the Service provider on

contractual basis with different Value Added

Service provider. This kind of agreement will give

boost in Competition and different VAS partners

Pratibimb | April 2012 | 25

for different type of Content.

The offering of these services could also be

customized as the charges levied overall on the

user will be less as the competition amongst the

content will eventually decrease the cost of the

application provided by the VAS providers.

The positioning of these services could be on the

basis of convenient service and Rates where the

promotion would be mainly Above the Line

focusing on TV ads, College Promotion and BPO‟s

where the target group is maximum in number and

would be given at half the price for the Closed

User Group Customers

Conclusion:

As per PWC report Students will comprise around

28% of the estimated mobile subscribers‟ base in

2015. Students are expected to be the highest

consumers of most VAS services based on future

adoption levels. This can generate additional

revenue of Rs. 1411 crores in 2015. The total

revenue from information services is expected to

reach 7,953 Crores by 2015.

So a combination of Top VAS used by the Youth

segment and bundling at a competitive pricing will

make the youth feel more attracted towards using it

and the Gender specific usage pattern can be

addressed through effective promotion through

Above the Line Marketing strategy and keeping in

mind that they are low involvement products. The

internet usage of these consumers need to

analyze which will provide the company to market

on the Social Media space and other online portals.

Bibliography

PWC. Connect with Consumers Value Added

Services: The next wave. PWC, March 2011

TRAI Consultation paper on Mobile Value

Added Service, 21st July 2011

Deloitte, ASSOCHAM Mobile Value Added

Services (MVAS) - A vehicle to usher in

inclusive growth and bridge the digital divide

January 2011

PWC, CII-MITSOT report Beyond voice and

Text Teletech 2011, January 2011

Ernst and Young, FICCI report Enabling the

next wave of telecom growth in India -

Industry inputs for National Telecom Policy,

2011

IAMAI report, Towards a liberal Mobile

Value Added Services Regime Approach

paper submitted by the Internet and Mobile

Association of India to the Ministry of

Communications and Information

Technology, March 2007

Reference Books

Naresh Malhotra book on „Review of

Marketing Research‟ Volume 6

Off deck Content Revenue %* Off deck Content Revenue Price* What Customer Pay for

top 5 VAS

Rs 150 + per month for 1GB and 25 Mb free, post

that 10 paisa / 10kb Content Owners 25% Rs. 37.50 Per user

Content Creator 15% Rs. 22.50 Per user

Content Aggregators 30% Rs. 60.00 Per user

Service Provider 35% Rs. 52.50 Per user

(+) Cost of SMS Rs. 3/ SMS (If ordered through SMS)

(+) Taxes as per GST „12

In Off-deck content, the VAS Provider sells content directly to subscribers. The content can be provided either through the operators' por-

tal or through their short code.

Pratibimb | April 2012 | 26

Talent Management

– Getting It Right by Simone Lobo, XIMR Mumbai

Financial capital earns no gain without human

capital. Even the 4 Ps of marketing i.e. Product,

Price, Promotion and Place, require a 5th i.e.

People. The corporate landscape today is witness

to hits and misses through M&A‟s and crashes

and burns with the economic crises the world over.

Uncertainties lurk within organizations and the

environment around. In the haziness of the abstract

scenario in the business world, silhouettes of

people stand out. They come alive and quieten the

din. It is people that take life-altering decisions,

help restore organization health and put pieces of

the puzzle back together.

People are priority:

People are an organization‟s corner-stone on

which its foundation firmly stands. A

breakthrough innovation, a cutting-edge product, a

world-class leader – people make it possible. And

behind every successful corporation are its people.

Business intelligence and competitor analysis are

enhanced by technology but enabled by people.

Values are disseminated by top management and

imbibed by new entrants of a company – again an

exchange through people. At every step of

organizational life – hand-holding, enculturation,

learning and development, career growth,

employee engagement – people initiate and

facilitate.

The changing face of HR:

Enter Human Resources, and the task at hand

seems daunting. Laying to rest misconceptions of a

„9-5‟ job and „fun‟ work life, HR is here to deliver

and demonstrate its impact on bottom-line results.

HR today has come full circle, with shareholders

now concerned not only about annual report

figures but also what‟s happening on the shop

floor.

The key to carrying the baton of organizational

success forward is innovative practices in talent

management. It is essential today to ensure that

new recruits are a cultural fit and uphold the

strongly held organizational values. The founders

of successful organizations leave behind a legacy

that is entrusted in the care of generations to come.

A striking example of an organization that is

known for its exemplary values is the Tata‟s.

HR strategies make tangible results visible. A

good induction programme, valuable training and

positive re-enforcements like career growth

opportunities go a long way in setting a positive

trend with the promise of a future in the company.

Providing a safe work environment and fair

compensation are other important areas. Through

leadership coaching and mentoring, employees are

given the encouragement to initiate, freedom to

create and empowerment to inspire. HR helps

make the voice of employees heard through the

Voice of Customer (VOC) report. It is the pulse of

an organization and is adopted by many businesses

today.

With regard to employee engagement and welfare,

many aspects need to be considered e.g. work-life

balance, trust and respect, job security etc. Open

communication is the need of the hour.

Management by walking around, open-door policy

and town-hall with the CEO are some of the

practices followed in organizations today. It helps

connect with and understand the needs of an

Pratibimb | April 2012 | 27

organization‟s internal customers – its employees.

The protocol followed by many effective HR

practitioners is

never to

compromise on

quality. A concern

of highest regard is

to follow Standard

Operating

Procedures (SOPs)

and relevant laws

applicable from

time to time.

Motivation does matter:

The common thread that binds employees to the

company and prevents them from switching

loyalties is motivation. If we look at Frederick

Herzberg‟s two-factor theory, it talks about

motivators and hygiene factors. Motivators are the

intrinsic factors that motivate an individual e.g.

higher responsibility, recognition etc. Whereas,

hygiene factors are the extrinsic factors that don‟t

motivate if present but their absence leads to

demotivation e.g. salary and other benefits.

Taking this forward, we will look at innovative

practices being followed by organizations

presently to attract and retain talent.

With the veil of economic uncertainty imminent

today and looming large, monetary gains like

increments have taken a back-seat. This has led

many companies to turn to newer approaches of

preventing people from changing jobs.

The employee lifeline:

“This year, a healthy employee will be the sign of

a wealthy one”. Current examples of organizations

that “have started betting on health and medical

benefits to rein in as many as possible from

shifting loyalties” are Wipro, Tesco, Philips and

Intel. “They are also looking at attracting talent

with a revamped medical benefits

package.” (Sengupta, 2012). This is evident

through the illustration below.

Source: http://

articles.economictimes.indiatimes.com/2012-02-

17/news/31071292_1_medical-insurance-medical-

benefits-high-premium

In times of inflation, altered lifestyles, the onset of

new illnesses and subsequently burgeoning

medical expenses, the above seems to be an

excellent proposition. Although it falls within the

gamut of medical benefits in the construct of

compensation, it is a welcome step towards

employee attraction and retention. A stride in this

direction could take companies a long way.

Whether packages such as these help the

companies in actual talent management remains to

be seen. It is for employees to recognize the access

to such benefits and appreciate them as

instruments of employer care. “Whatever be the

reason, healthcare is no longer a hygiene factor for

companies – it is now a conscious retention

tool.” (Sengupta, 2012)

The fitness test – internal seems the best:

Most employees have access to information on

Internal Job Postings (IJPs) through the company

intranet. While external consultants help gain

access to a pool of qualified talent fit for the job,

“some organizations are adopting innovative ways

of filling job postings through internal head-

hunting of premium talent. This serves two

Pratibimb | April 2012 | 28

purposes. One, the organization gets the best

candidate for the job posting while enabling it to

retain key employees and, two, employees get a

better posting, for which they would have

otherwise looked outside the group.” (Singh,

2012)

Examples of companies with such initiatives are

many. Different companies have different criteria

that need to be met before an internal candidate is

considered for a role. The process adopted by each

company also differs. “In the 20,000-strong Essar

Group, 200 people have so far benefitted from the

HR initiative. There is a seven member team

which identifies high-potential talent within the

organization and, like any other external head-

hunter; it reaches out to such employees to offer

them a host of opportunities within the group. The

understanding is that the employee should have

completed a minimum of two years in the previous

role.” (Singh, 2012)

Candidate fitness to the role is of prime

importance. Persuasion also helps employees

consider jobs available internally, that they may

have previously not contemplated. At times, there

are separate people from the recruitment team

assigned to handle requirements of such a nature,

on an on-going or project basis. “Santrupt Misra,

CEO, carbon black business & director, group

HR, Aditya Birla Group, describes his group's

initiative in this direction as an internal talent

management process which works as a virtual

head-hunting team. „There are many examples

where people have been actively influenced and

persuaded to look at a role that they would

otherwise have not thought about‟, he

said.” (Singh, 2012)

Today, it is not very easy to acquire the right

people for the right job at the right time.

Competition is fierce and with companies offering

swanky roles and lucrative packages, the potential

candidate is sometimes driven in the opposite

direction. Time is of the essence especially when it

has a direct impact on business and bottom-line

results. “Marc Effron, president, The Talent

Strategy Group, believes that internal headhunting

is the right approach in a talent-scarce world.

„You should check what's in your own cupboard

before taking a trip to the market. Internal head-

hunting is advantageous in three ways. Firstly,

internal candidates are far more likely to succeed,

since they've already been vetted for cultural fit

and performance. Two, it sends a powerful

message to the organization's employees that there

will be opportunities to grow and develop. And,

three, absence of such opportunities is proven to

decrease employee engagement and increase

turnover of a company's high-potential leaders.

However, the only area of caution is to realize that

internal talent might not be the best fit for every

opportunity‟, said Effron.” (Singh, 2012)

HR innovation vis-à-vis employee inclination:

Apart from verifying employee fitness for an

available position internally, it is important to

check employee readiness for such an opportunity.

While in-house head-hunting presents a platform

for employees to traverse organizational

businesses and offers a great deal of exposure and

learning, there exists a fine line between employee

fitness for a suitable role and their readiness to

take up the same. Having said this, the efforts

taken up by organizations in this direction are

truly commendable and open doors to endless

possibilities. Such innovative avenues should be

respected. Think talent management – think avant-

garde – seems to be the mantra today for planning

and executing talent management programmes

effectively.

Recruitment etiquette:

Recruiters today need to be well-informed. Apart

from role clarity, it is important to ensure that

compensation parity exists among team members.

This is crucial and must be done with the help of

benchmarking and other tools. HR needs to be

aware of headcount as per budgeted manpower

plans. There also needs to be robust interviewing

Pratibimb | April 2012 | 29

mechanisms in place e.g. resume screening,

personal interviews, group discussions, case study/

article writing, testing etc. It is essential to have a

candidate pipeline and it is extremely vital for HR

to connect with potential candidates on a regular

basis, so that time is uncompromised. A clear

understanding of the career growth prospects for a

given role under consideration must be charted out

in detail. Candidates today are keen to know their

future role within the company.

When considering a candidate for a given profile,

his/her resume serves as a yardstick that enables

decision-making. While past laurels do not

guarantee a successful future with the company,

they serve as a guide nonetheless. “A person‟s past

job performance is the surest guide to future

performance. The right education + the right

experience + a compatible personality = a good

fit.” (Luecke, 2002). Today, reference or

background checks play an important role in the

recruitment process. With many reported frauds,

certifying credentials of new entrants helps ensure

that the necessary checks and balances are in

place. This also lowers the risk that companies are

otherwise faced with when they encounter a

situation of this nature.

Employment errors:

There are certain hiring mistakes that companies

often commit. Falling prey to the pressures

around, they are then trapped with employees who

are either high maintenance or lack diversity. To

understand this further we consider 2 aspects –

“desperately seeking the hottest prospects and

hiring in your own image.” (Luecke, 2002). Such

decisions can prove to be ill-suited to the role

requirement in the first place. “Winning the hottest

prospects may cost your firm more than it can

comfortably afford. Their educational or

professional background may be more than what

the job in question actually requires. They may be

so confident of their desirability that they won‟t

bring a healthy dose of appreciation and gratitude

to their new job at your firm – and they‟ll always

have one eye out for the bigger, better

deal.” (Luecke, 2002)

The second aspect focuses on the importance of

workforce diversity. It is a concept that many

organizations today are fast embracing. “Another

all-too-common mistake is to hire people just like

you. Many managers assume that they can build

strong teams by gathering people who all have the

same strengths and personalities – those defined

by the managers themselves. But diversity in

personality, work styles and decision-making

approaches creates richness in a team‟s culture,

increases the group‟s chances of generating

creative ideas and solutions and lets members

complement one another‟s strengths and make up

for one another‟s weaknesses.” (Luecke, 2002)

Personalized attention:

Today, companies offer various opportunities,

with part-time, contractual and temporary

employment on the rise. HR is then faced with an

uphill task of managing such employees.

“Retention is especially challenging when the

workforce is highly diverse. One-size-fits-all

strategies for keeping good people simply don‟t

work any longer. Companies can best improve

their retention rates by crafting creative,

specialized strategies for each major segment of

the workforce.” While a contingent workforce

presents an organization with advantages like

flexibility in work timings and affordability, they

have a down-side that cannot be ignored. The

challenges include a high turnover witnessed

among such employees, a lesser degree of loyalty

towards the company and a demand for similar

benefits accrued by a company‟s regular

employees. (Luecke, 2002)

The happiness quotient:

If the business environment today is a battle field,

employees are its arsenal. They breathe life into an