Embed Size (px)

Citation preview

Page 1 of 19

TARIFF DECISION FOR SASOL OIL (PTY) LTD’S SECUNDA

TO NATREF INTEGRATED (SNI) PIPELINE

10 MAY 2018

Page 2 of 19

TABLE OF CONTENTS

Introduction ...................................................................................................................... 6

Applicable Law ................................................................................................................ 6

The Methodology ............................................................................................................. 6

Decision-Making Process ................................................................................................ 7

Assessment of the Tariff Application ............................................................................... 7

Allowable Revenue (AR) .................................................................................................. 7

Regulatory Asset Base (RAB) ......................................................................................... 8

Property, Plant and Equipment (PPE) ............................................................................. 8

Net Working Capital ......................................................................................................... 9

Weighted Average Cost of Capital (WACC) .................................................................. 11

Cost of Equity ................................................................................................................ 11

Cost of Debt ................................................................................................................... 12

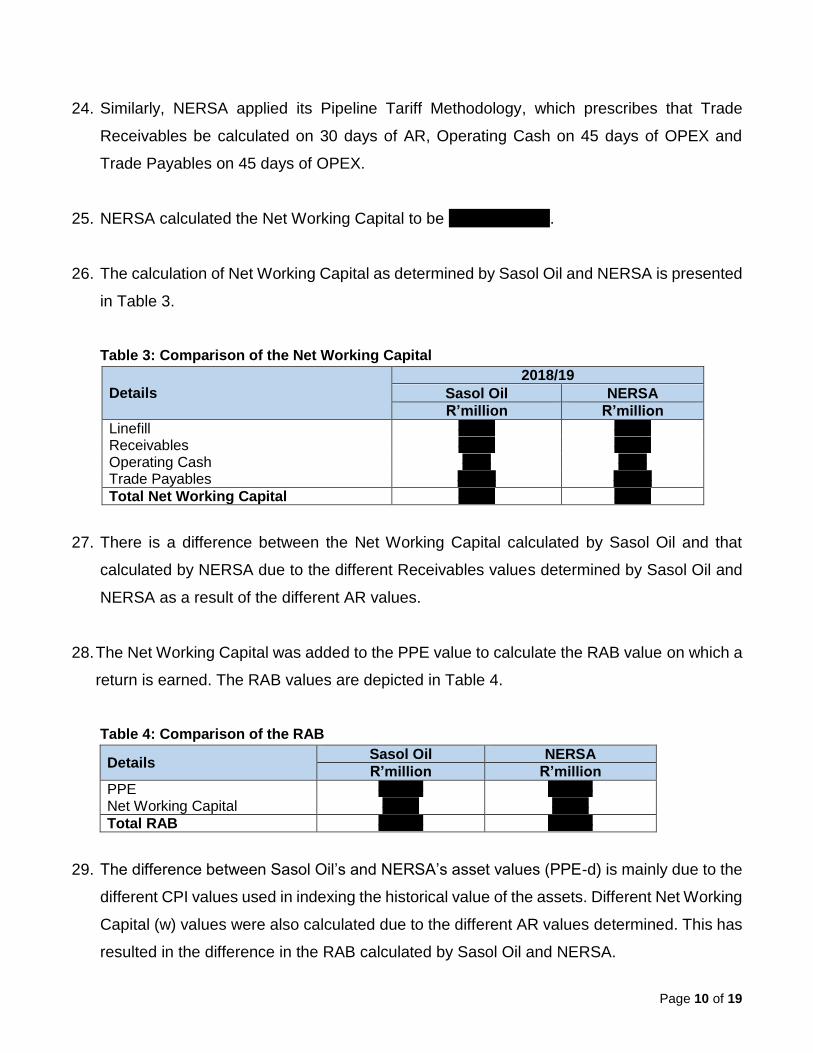

Debt-to-Equity Ratio ...................................................................................................... 12

Operation Expenditure (OPEX) ..................................................................................... 13

Land Rehabilitation ........................................................................................................ 15

Depreciation .................................................................................................................. 15

Clawback ....................................................................................................................... 15

Tax Expense .................................................................................................................. 16

Allowable Revenue (AR) ................................................................................................ 17

Volumes ......................................................................................................................... 18

Tariff Design .................................................................................................................. 18

Conclusion ..................................................................................................................... 19

Page 3 of 19

LIST OF TABLES

Table 1: Tariff set for the SNI pipeline ....................................................................................... 5

Table 2: Comparison of the PPE values .................................................................................... 9

Table 3: Comparison of the Net Working Capital ......................................................................10

Table 4: Comparison of the RAB ..............................................................................................10

Table 5: WACC Calculation ......................................................................................................13

Table 6: Operating Expenses ...................................................................................................13

Table 7: Detailed Breakdown of the OPEX costs .....................................................................14

Table 8: Clawback Calculation .................................................................................................16

Table 9: Tax Expense Calculation ............................................................................................17

Table 10: Comparison of the AR values ...................................................................................17

Table 11: Volumes Details ........................................................................................................18

Table 12: Comparison in tariffs .................................................................................................19

Page 4 of 19

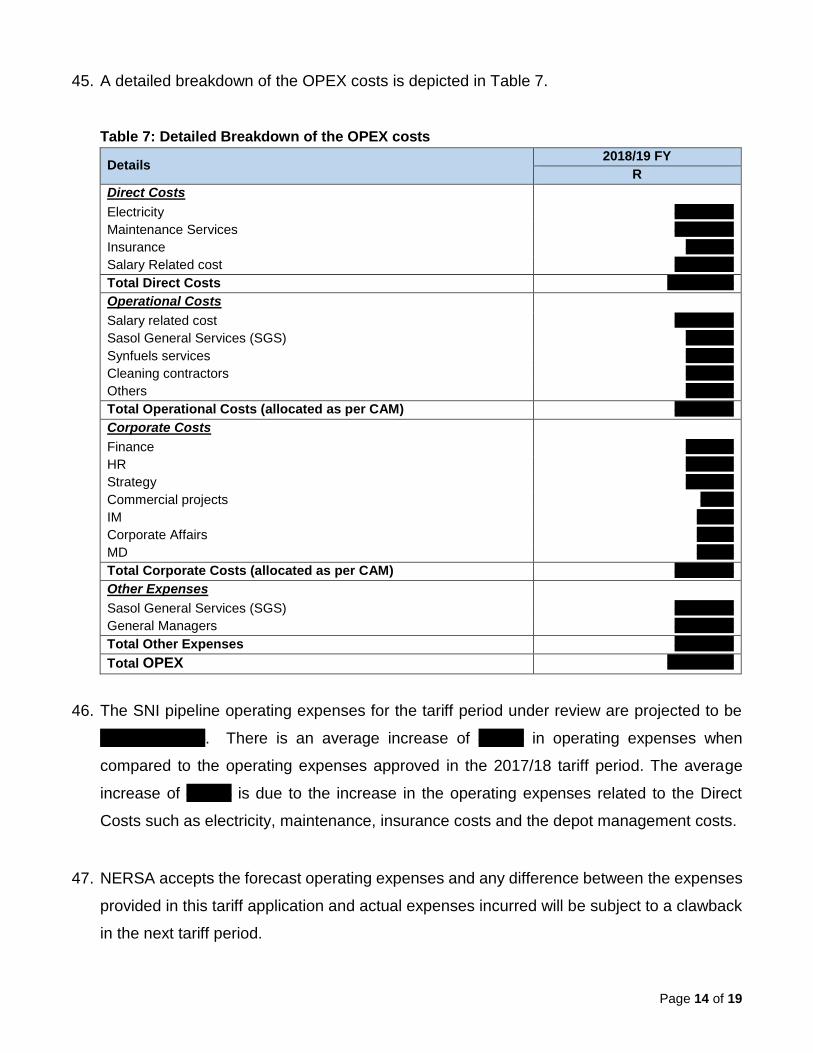

ABBREVIATIONS AND ACRONYMS

AR Allowable Revenue

BER Bureau of Economic Research

BFP Basic Fuel Price

CAM Cost Allocation Manual

CAPM Capital Asset Pricing Model

CPI Consumer Price Index

CPIf Consumer Price Index Forecast

Cpl Cents per litre

MRP Market Risk Premium

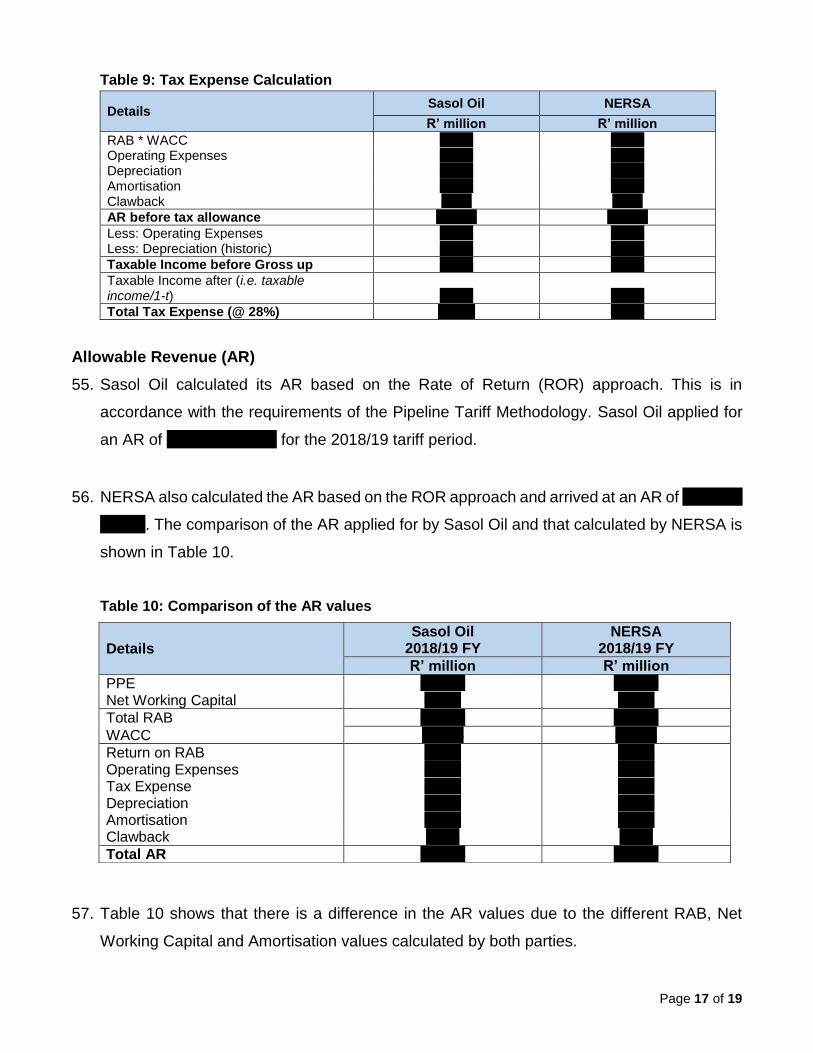

NERSA National Energy Regulator of South Africa

NRBTA Net Revenue Before Tax Allowance

PPE Property, Plant, Vehicles and Equipment

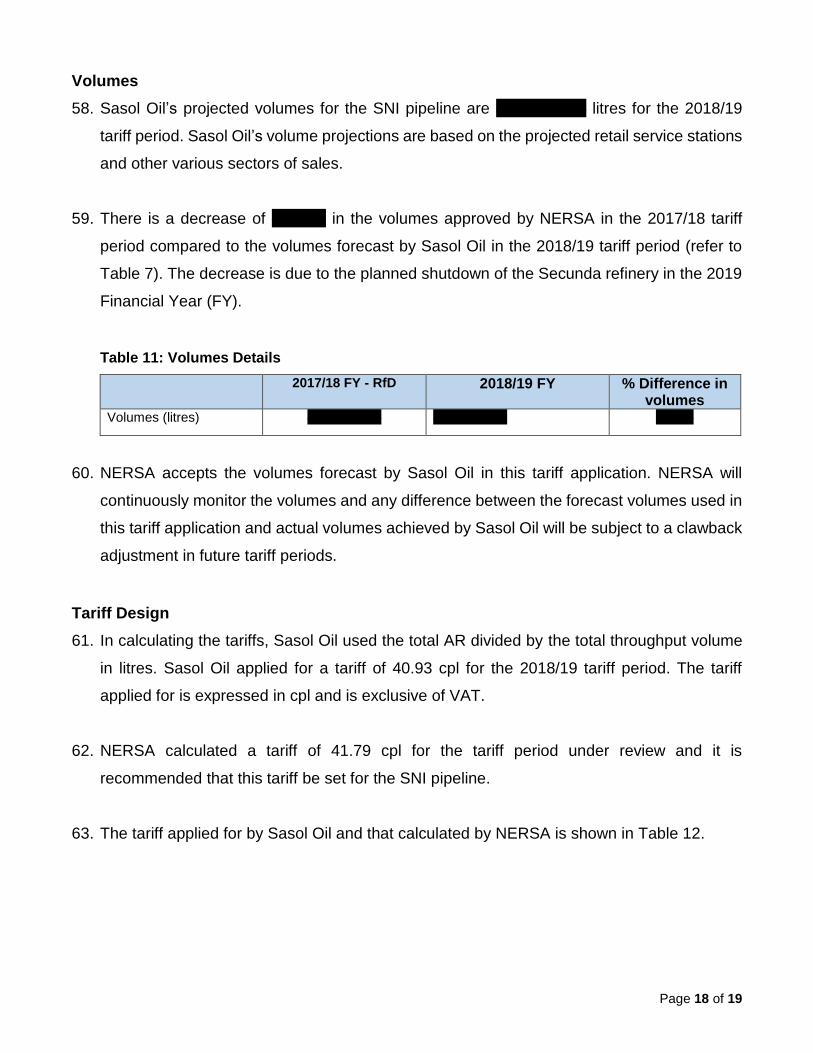

RAB Regulatory Asset Base

REC Regulator Executive Committee

RFR Regulatory Financial Reporting

Rf Risk Free Rate

RRM Regulatory Reporting Manuals

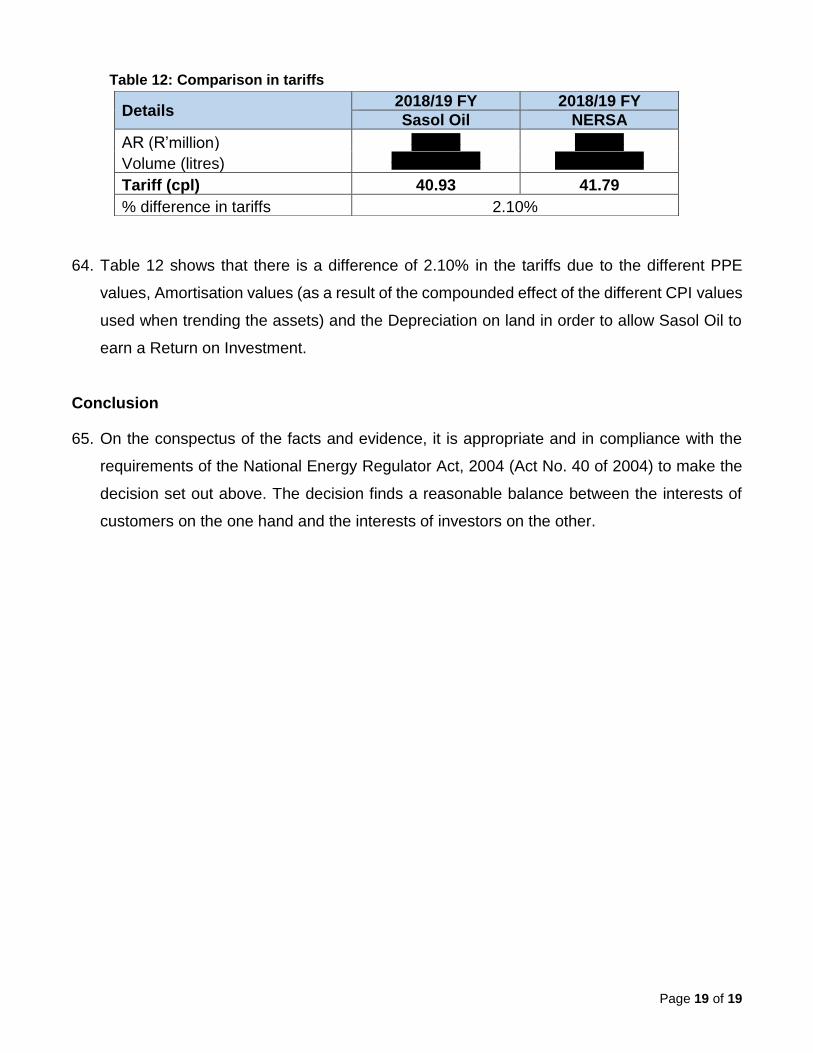

SNI Secunda to Natref Integrated Pipeline

SRAB Starting Regulatory Asset Base

TOC Trended Original Cost

VAT Value Added Tax

WACC Weighted Average Cost of Capital

Page 5 of 19

THE NATIONAL ENERGY REGULATOR OF SOUTH AFRICA

In the matter regarding

THE APPLICATION FOR SETTING A TARIFF FOR THE SECUNDA TO NATREF

INTEGRATED (SNI) PIPELINE FOR THE 2018/19 TARIFF YEAR

By

SASOL OIL (PTY) LTD

_______________________________________________________________________

THE DECISION

_______________________________________________________________________

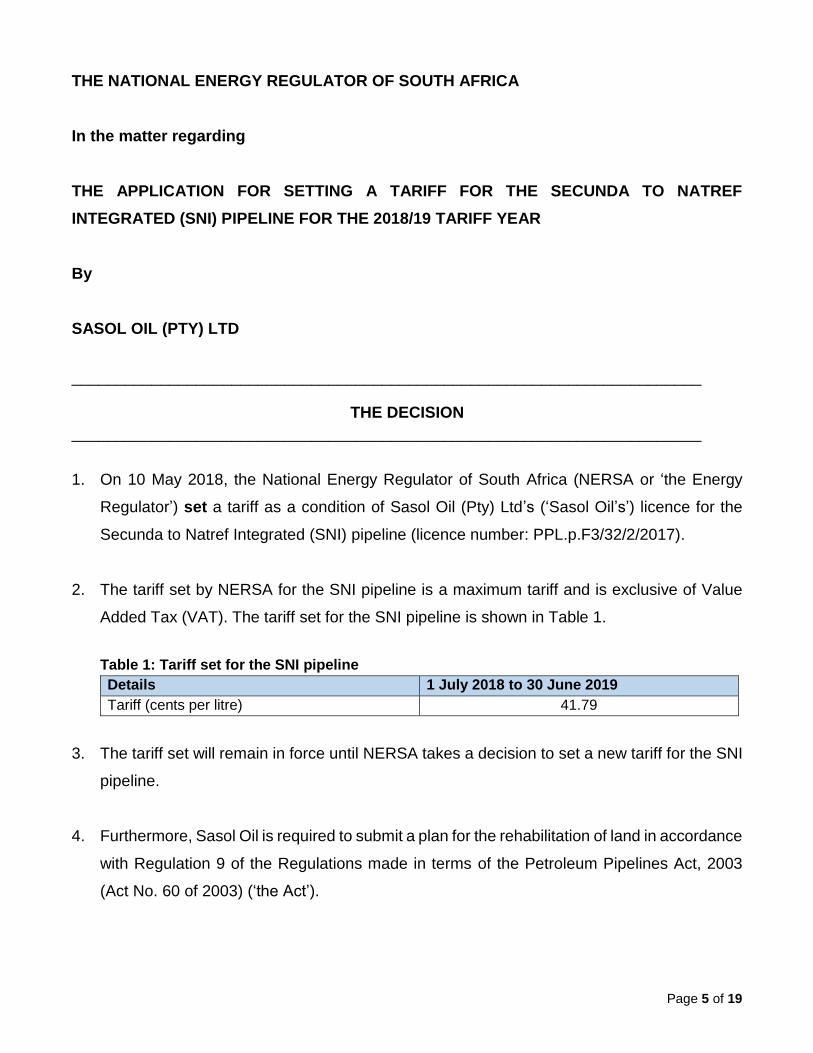

1. On 10 May 2018, the National Energy Regulator of South Africa (NERSA or ‘the Energy

Regulator’) set a tariff as a condition of Sasol Oil (Pty) Ltd’s (‘Sasol Oil’s’) licence for the

Secunda to Natref Integrated (SNI) pipeline (licence number: PPL.p.F3/32/2/2017).

2. The tariff set by NERSA for the SNI pipeline is a maximum tariff and is exclusive of Value

Added Tax (VAT). The tariff set for the SNI pipeline is shown in Table 1.

Table 1: Tariff set for the SNI pipeline

Details 1 July 2018 to 30 June 2019

Tariff (cents per litre) 41.79

3. The tariff set will remain in force until NERSA takes a decision to set a new tariff for the SNI

pipeline.

4. Furthermore, Sasol Oil is required to submit a plan for the rehabilitation of land in accordance

with Regulation 9 of the Regulations made in terms of the Petroleum Pipelines Act, 2003

(Act No. 60 of 2003) (‘the Act’).

Page 6 of 19

___________________________________________________________________________

REASONS FOR DECISION

___________________________________________________________________________

Introduction

1. On 27 January 2011, the National Energy Regulator of South Africa (NERSA or ‘the Energy

Regulator’) issued a licence with conditions to Sasol Oil (Pty) Ltd (‘Sasol Oil’) for the operation

of a pipeline from the Sasol Oil (Pty) Ltd coal-to-liquids refinery at Secunda to the Natref

crude oil refinery at Sasolburg.

2. On 30 November 2017, Sasol Oil submitted a tariff application for the Secunda to Natref

Integrated (SNI) pipeline. The tariff application is for the period 1 July 2018 to 30 June 2019.

3. Sasol Oil applied for a tariff of 40.93 cents per litre (cpl) for the period 1 July 2018 to 30 June

2019. The tariff applied for is a maximum tariff and is exclusive of Value Added Tax (VAT).

4. The tariff applied for by Sasol Oil is based on the total Allowable Revenue (AR) divided by

the total volume in litres.

5. A detailed analysis of the tariff application is provided in the following paragraphs.

Applicable Law

6. The legal basis for NERSA to set tariffs for petroleum pipelines is derived from the National

Energy Regulator Act, 2004 (Act No. 40 of 2004) (‘the NERSA Act’), read with the Petroleum

Pipelines Act, 2003 (Act No. 60 of 2003) (‘the Act’)1.

The Methodology

7. NERSA is required by section 28(2)(a)(i) of the Act to set tariffs based on a systematic

methodology applicable on a consistent and comparable basis. Sasol Oil used the Tariff

1 Available at www.nersa.org.za

Page 7 of 19

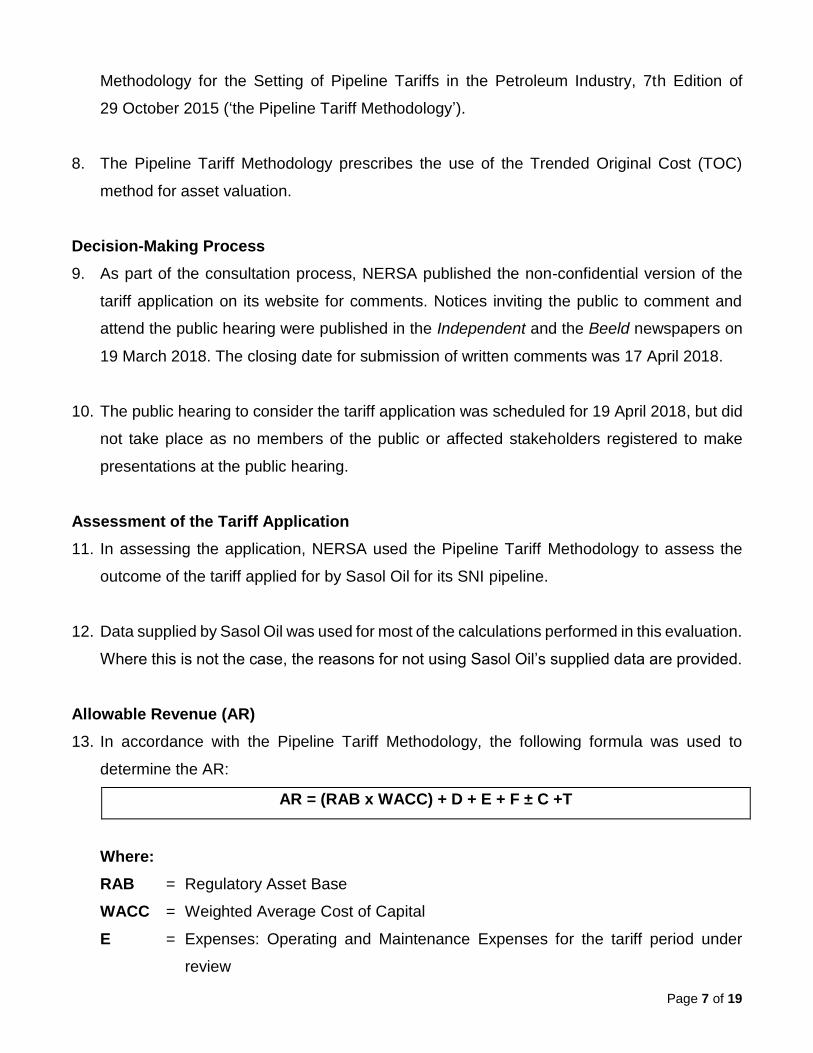

Methodology for the Setting of Pipeline Tariffs in the Petroleum Industry, 7th Edition of

29 October 2015 (‘the Pipeline Tariff Methodology’).

8. The Pipeline Tariff Methodology prescribes the use of the Trended Original Cost (TOC)

method for asset valuation.

Decision-Making Process

9. As part of the consultation process, NERSA published the non-confidential version of the

tariff application on its website for comments. Notices inviting the public to comment and

attend the public hearing were published in the Independent and the Beeld newspapers on

19 March 2018. The closing date for submission of written comments was 17 April 2018.

10. The public hearing to consider the tariff application was scheduled for 19 April 2018, but did

not take place as no members of the public or affected stakeholders registered to make

presentations at the public hearing.

Assessment of the Tariff Application

11. In assessing the application, NERSA used the Pipeline Tariff Methodology to assess the

outcome of the tariff applied for by Sasol Oil for its SNI pipeline.

12. Data supplied by Sasol Oil was used for most of the calculations performed in this evaluation.

Where this is not the case, the reasons for not using Sasol Oil’s supplied data are provided.

Allowable Revenue (AR)

13. In accordance with the Pipeline Tariff Methodology, the following formula was used to

determine the AR:

AR = (RAB x WACC) + D + E + F ± C +T

Where:

RAB = Regulatory Asset Base

WACC = Weighted Average Cost of Capital

E = Expenses: Operating and Maintenance Expenses for the tariff period under

review

Page 8 of 19

D = Depreciation Expense for the tariff period under review

F = Approved Revenue addition to meet debt obligations for the tariff period under

review

C = Clawback Adjustment: to correct for differences between actual and forecasts in

formula elements from a preceding tariff period in relation to the actual estimates

for that tariff period

T = Tax: estimated Tax Expense for the tariff period under review.

14. The elements of the AR are discussed in more detail in the paragraphs below.

Regulatory Asset Base (RAB)

15. According to the Pipeline Tariff Methodology, the RAB is to be determined by applying the

following formula:

RAB = (PPE - d) + w

Where:

PPE = Original cost and inflation write-up of operating assets (Property, Plant, Vehicles

and Equipment)

d = Accumulated Depreciation and Accumulated Amortisation of inflation write-up

for the period up to the commencement of the tariff period under review

w = Net Working Capital

Property, Plant and Equipment (PPE)

16. Sasol Oil calculated the Property, Plant and Equipment (PPE) value using the TOC method.

The TOC method requires that the original cost of assets be adjusted annually using the

Consumer Price Index (CPI) over the economic useful life of the assets. Sasol Oil applied

the TOC method correctly when calculating the PPE value and arrived at the PPE value of

R880.18 million.

17. NERSA accepted the use of the TOC method to calculate the PPE value on which a return

is to be earned. The original cost of the assets were trended using the CPI from the year in

which the assets were brought into use, until the tariff period under review. NERSA calculated

the PPE value to be R858.88 million.

Page 9 of 19

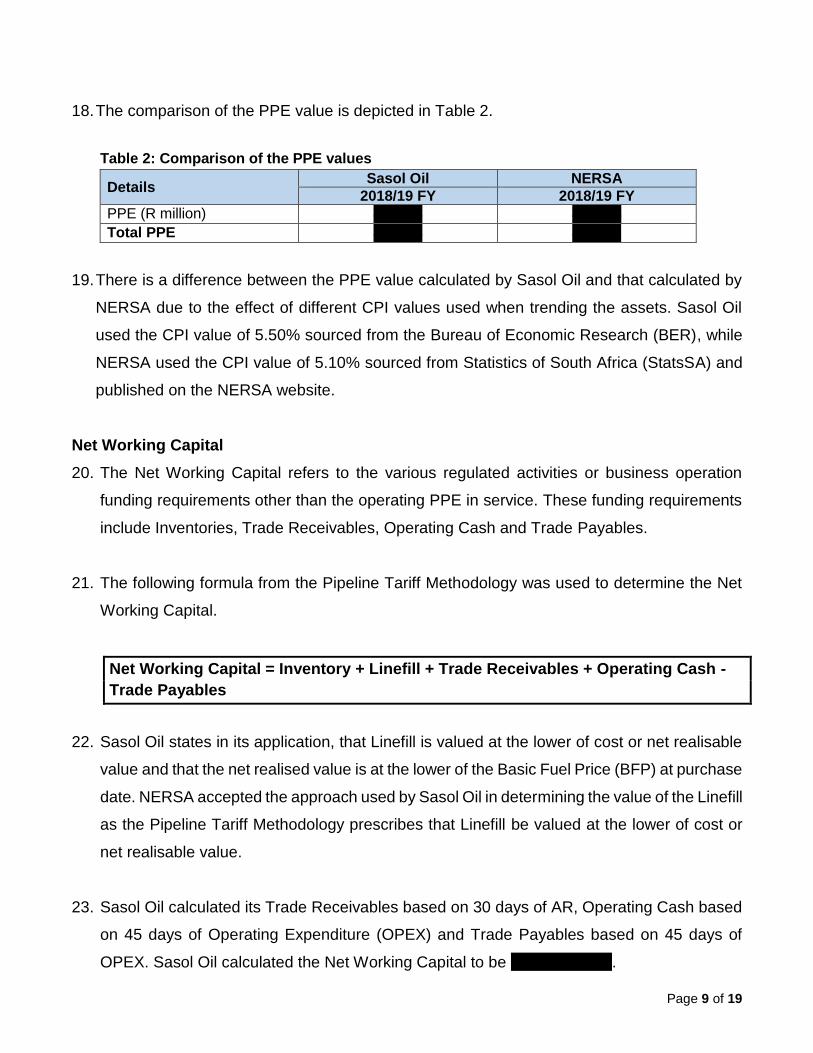

18. The comparison of the PPE value is depicted in Table 2.

Table 2: Comparison of the PPE values

Details Sasol Oil NERSA

2018/19 FY 2018/19 FY

PPE (R million) 880.18 858.88 Total PPE 880.18 858.88

19. There is a difference between the PPE value calculated by Sasol Oil and that calculated by

NERSA due to the effect of different CPI values used when trending the assets. Sasol Oil

used the CPI value of 5.50% sourced from the Bureau of Economic Research (BER), while

NERSA used the CPI value of 5.10% sourced from Statistics of South Africa (StatsSA) and

published on the NERSA website.

Net Working Capital

20. The Net Working Capital refers to the various regulated activities or business operation

funding requirements other than the operating PPE in service. These funding requirements

include Inventories, Trade Receivables, Operating Cash and Trade Payables.

21. The following formula from the Pipeline Tariff Methodology was used to determine the Net

Working Capital.

Net Working Capital = Inventory + Linefill + Trade Receivables + Operating Cash -

Trade Payables

22. Sasol Oil states in its application, that Linefill is valued at the lower of cost or net realisable

value and that the net realised value is at the lower of the Basic Fuel Price (BFP) at purchase

date. NERSA accepted the approach used by Sasol Oil in determining the value of the Linefill

as the Pipeline Tariff Methodology prescribes that Linefill be valued at the lower of cost or

net realisable value.

23. Sasol Oil calculated its Trade Receivables based on 30 days of AR, Operating Cash based

on 45 days of Operating Expenditure (OPEX) and Trade Payables based on 45 days of

OPEX. Sasol Oil calculated the Net Working Capital to be R61.23 million.

Page 10 of 19

24. Similarly, NERSA applied its Pipeline Tariff Methodology, which prescribes that Trade

Receivables be calculated on 30 days of AR, Operating Cash on 45 days of OPEX and

Trade Payables on 45 days of OPEX.

25. NERSA calculated the Net Working Capital to be R61.48 million.

26. The calculation of Net Working Capital as determined by Sasol Oil and NERSA is presented

in Table 3.

Table 3: Comparison of the Net Working Capital

Details 2018/19

Sasol Oil NERSA

R’million R’million

Linefill 49.55 49.55 Receivables 11.68 11.93 Operating Cash 2.24 2.24 Trade Payables (2.24) (2.24)

Total Net Working Capital 61.23 61.48

27. There is a difference between the Net Working Capital calculated by Sasol Oil and that

calculated by NERSA due to the different Receivables values determined by Sasol Oil and

NERSA as a result of the different AR values.

28. The Net Working Capital was added to the PPE value to calculate the RAB value on which a

return is earned. The RAB values are depicted in Table 4.

Table 4: Comparison of the RAB

Details Sasol Oil NERSA

R’million R’million

PPE 880.18 858.88 Net Working Capital 61.23 61.48

Total RAB 941.41 920.36

29. The difference between Sasol Oil’s and NERSA’s asset values (PPE-d) is mainly due to the

different CPI values used in indexing the historical value of the assets. Different Net Working

Capital (w) values were also calculated due to the different AR values determined. This has

resulted in the difference in the RAB calculated by Sasol Oil and NERSA.

Page 11 of 19

Weighted Average Cost of Capital (WACC)

30. Section 5 of the Pipeline Tariff Methodology stipulates that the Weighted Average Cost of

Capital (WACC) must be calculated using the following formula:

Where:

Eq = Shareholders Equity

Dt = Interest Bearing Debt

Ke = Post-tax, real Cost of Equity derived from the Capital Asset Pricing Model

(CAPM)

Kd = Post-tax, real2 Cost of Debt

31. Sasol Oil used the Pipeline Tariff Methodology to calculate the WACC and the components

of WACC such as the Cost of Equity and Cost of Debt. In calculating the WACC, the following

components of WACC were analysed:

a) Cost of Equity;

b) Cost of Debt; and

c) Debt-to-Equity Ratio.

Cost of Equity

32. Sasol Oil calculated the Cost of Equity in terms of the requirements of the Pipeline Tariff

Methodology. The Pipeline Tariff Methodology prescribes that the Cost of Equity be

calculated using the CAPM3.

33. The Pipeline Tariff Methodology further prescribes that the economic data used to calculate

the Cost of Equity be that of 12 months prior to the commencement of the tariff period under

review. In this regard, Sasol Oil used the economic data of May 2017 (13 months prior to

the commencement of the tariff period) instead of the economic date of June 2017 (12

months prior to the commencement of the period). This therefore results in different WACC

values between Sasol Oil and NERSA.

2 First convert from pre- to post-tax and then from nominal to real.

3 The cost of equity can also be determined by applying any other appropriate model as per the provisions of Regulation 4(5) of the Regulations in terms of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003).

Kd*

EqDt

DtKe*

EqDt

Eq WACC

Page 12 of 19

34. The Cost of Equity applied for by Sasol Oil is 8.27% and NERSA calculated a Cost of Equity

of 8.03%. The difference in the Cost of Equity is due to different economic data used by

Sasol Oil and NERSA.

Cost of Debt

35. The Pipeline Tariff Methodology prescribes that a nominal pre-tax Cost of Debt be converted

into the real post-tax Cost of Debt by using the CPI value and Corporate Tax Rate. In order

to determine the real post-tax Cost of Debt, Sasol Oil used the CPI of 5.50% (sourced from

BER) and the Corporate Tax Rate of 28%. Sasol Oil applied for the real post-tax Cost of

Debt of 1.09%.

36. Similarly, NERSA used the Pipeline Tariff Methodology to calculate the real post-tax Cost of

Debt. NERSA used the CPI of 5.50% (sourced from StatsSA and published by NERSA on

its website) and the Corporate Tax Rate of 28% to calculate the real post-tax Cost of Debt.

NERSA calculated the real post-tax Cost of Debt to be 1.42%.

37. There is a slight difference between the real post-tax Cost of Debt applied for by Sasol Oil

and that calculated by NERSA due to the different CPI values used by both parties.

Debt-to-Equity Ratio

38. The Pipeline Tariff Methodology prescribes a minimum Debt of 30% for funding petroleum

infrastructure. Sasol Oil followed the requirements of the Pipeline Tariff Methodology and

applied for a Debt-to-Equity ratio of 30:70.

39. NERSA accepts the use of the minimum Debt-to-Equity ratio of 30:70 in determining the

WACC value, as it is considered reasonable for the efficient operation of petroleum

infrastructure.

40. When using the weighted average of the Cost of Equity (Equity Ratio multiply by Cost of

Equity) and the Cost of Debt (Debt Ratio multiply by Cost of Debt), Sasol Oil arrived at a real

WACC of 6.12%.

Page 13 of 19

41. NERSA also used the Pipeline Tariff Methodology and calculated a WACC of 6.05%. The

comparison of the WACC values calculated by Sasol Oil and NERSA is shown in Table 5.

Table 5: WACC Calculation

Details Sasol Oil NERSA

Risk Free Rate (before-tax real) 4.68% 4.70% Market Risk Premium (real) 4.55% 4.21% Beta 0.79 0.79 Cost of Equity (post-tax real) 8.27% 8.03%

Cost of Debt (pre-tax) 9.15% 9.15% Corporate Tax Rate 28% 28% Nominal Cost of Debt 6.59% 6.59% CPI forecast 5.50% 5.10% Cost of Debt (post-tax real) 1.09% 1.42%

Capital Structure: Debt Ratio 30% 30% Equity Ratio 70% 70%

WACC 6.12% 6.05%

Operation Expenditure (OPEX)

42. Regulation 5(2) read with regulation 4(2) (a) of the Regulations provides that the tariffs

approved by NERSA must enable an efficient licensee to recover the reasonable operational

and maintenance expenses of the storage facility in the year in which they are incurred.

43. Sasol Oil has an approved Cost Allocation Manual (CAM). Corporate costs and group

services costs are allocated in accordance with the approved CAM.

44. Table 6 provides a comparison between the operating expenses approved for the 2017/18

tariff period and that applied for in the 2018/19 tariff period.

Table 6: Operating Expenses

Details 2017/18 RfD 2018/19 FY % Difference

R’million R’million

Direct Cost Centre 11 657 026 12 712 333 9,05%

Shared services cost 1 130 400 1 074 605 -4,94%

General Managers Cost 1 071 987 1 097 281 2,36%

Corporate division expenses 1 131 811 1 152 758 1,85%

Depot management cost 3 203 523 3 731 172 16,47%

Total OPEX 18 194 747 19 768 149 8,65%

Page 14 of 19

45. A detailed breakdown of the OPEX costs is depicted in Table 7.

Table 7: Detailed Breakdown of the OPEX costs

Details 2018/19 FY

R

Direct Costs

Electricity 6 214 242

Maintenance Services 4 160 331

Insurance 671 145

Salary Related cost 1 666 615

Total Direct Costs 12 712 333

Operational Costs

Salary related cost 2 528 797

Sasol General Services (SGS) 496 148

Synfuels services 216 496

Cleaning contractors 174 551

Others 315 180

Total Operational Costs (allocated as per CAM) 3 731 172

Corporate Costs

Finance 728 261

HR 187 403

Strategy 132 461

Commercial projects 4 261

IM 19076

Corporate Affairs 61582

MD 19714

Total Corporate Costs (allocated as per CAM) 1 152 758

Other Expenses

Sasol General Services (SGS) 1 074 605

General Managers 1 097 281

Total Other Expenses 2 171 886

Total OPEX 19 768 149

46. The SNI pipeline operating expenses for the tariff period under review are projected to be

R19.77 million. There is an average increase of 8.65% in operating expenses when

compared to the operating expenses approved in the 2017/18 tariff period. The average

increase of 8.65% is due to the increase in the operating expenses related to the Direct

Costs such as electricity, maintenance, insurance costs and the depot management costs.

47. NERSA accepts the forecast operating expenses and any difference between the expenses

provided in this tariff application and actual expenses incurred will be subject to a clawback

in the next tariff period.

Page 15 of 19

Land Rehabilitation 48. No provision for Land Rehabilitation costs has been submitted by Sasol Oil in this tariff

application. Additional information was requested from Sasol Oil to ensure compliance with

Regulation 9 of the Regulations, made in terms of the Act. At a meeting held on 20 April

2018, Sasol Oil indicated that it cannot include the Land Rehabilitation cost in the AR, as

Sasol Oil will not be able to recover the cost through tariffs since Sasol Oil does not have

third-party access at its SNI pipeline. Sasol Oil further stated that it makes provision in its

financial statements in case there is a need to rehabilitate its facility.

Depreciation 49. Sasol Oil depreciated its assets (excluding land) on a straight-line basis and the Depreciation

calculated by Sasol Oil is R31.39 million. NERSA in its evaluation also depreciated the

assets (including land) on a straight-line basis and calculated the Depreciation to be R34.32

million. There is a difference between the Depreciation values calculated by Sasol Oil and

that calculated by NERSA due to NERSA accounting for the Depreciation on land in order

to allow Sasol Oil to earn a Return on Investment (ROI).

Clawback 50. Sasol Oil calculated a clawback value of R4.73 million. The clawback determined consists

of the volume adjustment, where the difference between the forecast volumes and actual

audited volumes for the 2016/17 tariff period was taken into consideration, as well as an AR

adjustment between the set AR and the actual audited costs in the 2016/17 tariff period

(refer to Table 8).

Page 16 of 19

Table 8: Clawback Calculation

Details Sasol Oil NERSA

Projected 2016/17 Volumes (litres) a 376 582 000 a 376 582 000 Actual 2016/17 Volumes b 386 926 000 b 386 926 000 Difference (litres) c = a - b -10 344 000 c = a - b -10 344 000 Tariff Set by ER (c/l) d 42.13 d 42.13

Volumes Adjustment Giveback e = c x d 4 357 927 e = c x d 4 357 927

Details 2016/17

RFD 2016/17 Actual Clawback

2016/17 RfD

2016/17 Actual Clawback

AR Calculation RAB 927.33 914.35 -12.98 927.33 914.35 -12.98 WACC 5.74% 5.79% 0.05% 5.74% 5.79% 0.05%

RAB X WACC 53.23 52.93 -0.29 53.23 52.93 -0.29 Depreciation 31.58 31.39 -0.19 31.58 31.39 -0.19 Operating expense 17.08 15.89 -1.19 17.08 15.89 -1.19 Amortisation 7.01 8.03 1.02 7.01 8.03 1.02

AR before Tax Expense 108.90 108.25 -0.65 108.90 108.25 -0.65 Tax Expense 23.43 23.71 0.28 23.43 23.71 0.28 Clawback 26.32 26.32 26.32 26.32

Total AR adjustment 158.64 158.28 -0.36 158.64 158.28 -0.36

Total Clawback in favour of Sasol Oil (R’million)

-4 726 483

-4 726 483

Tax Expense

51. The Tax Expense has been calculated according to the notional taxation method as

prescribed by the Pipeline Tariff Methodology. The Pipeline Tariff Methodology allows the

use of the notional tax method when calculating the Tax Expense to be included in the AR.

52. Sasol Oil calculated the Tax Expense to be R25.47 million.

53. Similarly, NERSA used the notional tax method to calculate the Tax Expense. NERSA

calculated the Tax Expense to be R25.49 million.

54. There is a slight difference between the Tax Expense applied for by Sasol Oil and that

calculated by NERSA due to the different AR values (refer to Table 9).

Page 17 of 19

Table 9: Tax Expense Calculation

Details Sasol Oil NERSA

R’ million R’ million

RAB * WACC 57.61 55.66 Operating Expenses 19.77 19.77 Depreciation 31.39 34.32 Amortisation 12.62 14.61 Clawback -4.72 -4.73

AR before tax allowance 116.66 119.63

Less: Operating Expenses 19.77 19.77 Less: Depreciation (historic) 31.39 34.32

Taxable Income before Gross up 65.50 66.54

Taxable Income after (i.e. taxable income/1-t) 90.98 91.03

Total Tax Expense (@ 28%) 25.47 25.49

Allowable Revenue (AR)

55. Sasol Oil calculated its AR based on the Rate of Return (ROR) approach. This is in

accordance with the requirements of the Pipeline Tariff Methodology. Sasol Oil applied for

an AR of R142.14 million for the 2018/19 tariff period.

56. NERSA also calculated the AR based on the ROR approach and arrived at an AR of R145.12

million. The comparison of the AR applied for by Sasol Oil and that calculated by NERSA is

shown in Table 10.

Table 10: Comparison of the AR values

57. Table 10 shows that there is a difference in the AR values due to the different RAB, Net

Working Capital and Amortisation values calculated by both parties.

Details Sasol Oil

2018/19 FY NERSA

2018/19 FY

R’ million R’ million

PPE 880.18 858.88 Net Working Capital 61.23 61.48

Total RAB 941.41 920.36

WACC 6.12% 6.05%

Return on RAB 57.61 55.66 Operating Expenses 19.77 19.77 Tax Expense 25.47 25.49 Depreciation 31.39 34.32 Amortisation 12.62 14.61 Clawback -4.73 -4.73

Total AR 142.14 145.12

Page 18 of 19

Volumes

58. Sasol Oil’s projected volumes for the SNI pipeline are 347 281 376 litres for the 2018/19

tariff period. Sasol Oil’s volume projections are based on the projected retail service stations

and other various sectors of sales.

59. There is a decrease of 17.88% in the volumes approved by NERSA in the 2017/18 tariff

period compared to the volumes forecast by Sasol Oil in the 2018/19 tariff period (refer to

Table 7). The decrease is due to the planned shutdown of the Secunda refinery in the 2019

Financial Year (FY).

Table 11: Volumes Details

2017/18 FY - RfD 2018/19 FY % Difference in volumes

Volumes (litres) 422 900 000 347 281 376 -17.88

60. NERSA accepts the volumes forecast by Sasol Oil in this tariff application. NERSA will

continuously monitor the volumes and any difference between the forecast volumes used in

this tariff application and actual volumes achieved by Sasol Oil will be subject to a clawback

adjustment in future tariff periods.

Tariff Design

61. In calculating the tariffs, Sasol Oil used the total AR divided by the total throughput volume

in litres. Sasol Oil applied for a tariff of 40.93 cpl for the 2018/19 tariff period. The tariff

applied for is expressed in cpl and is exclusive of VAT.

62. NERSA calculated a tariff of 41.79 cpl for the tariff period under review and it is

recommended that this tariff be set for the SNI pipeline.

63. The tariff applied for by Sasol Oil and that calculated by NERSA is shown in Table 12.

Page 19 of 19

Table 12: Comparison in tariffs

64. Table 12 shows that there is a difference of 2.10% in the tariffs due to the different PPE

values, Amortisation values (as a result of the compounded effect of the different CPI values

used when trending the assets) and the Depreciation on land in order to allow Sasol Oil to

earn a Return on Investment.

Conclusion

65. On the conspectus of the facts and evidence, it is appropriate and in compliance with the

requirements of the National Energy Regulator Act, 2004 (Act No. 40 of 2004) to make the

decision set out above. The decision finds a reasonable balance between the interests of

customers on the one hand and the interests of investors on the other.

Details 2018/19 FY 2018/19 FY

Sasol Oil NERSA

AR (R’million) 142.14 145.12

Volume (litres) 347 281 376 347 281 376

Tariff (cpl) 40.93 41.79

% difference in tariffs 2.10%