Embed Size (px)

Citation preview

1

Current Developments

American Bar Association Section of Taxation

Tax Accounting Committee 21 October 2011

Submitted by James Liechty, PricewaterhouseCoopers LLC, and Natalie Tucker, RSM McGladrey Sub-committee co-chairs for Tax Accounting Current Developments

The information contained herein is of general nature and based on authorities that are subject to change. Applicability to specific situations is to be determined through consultation with your tax advisor.

2

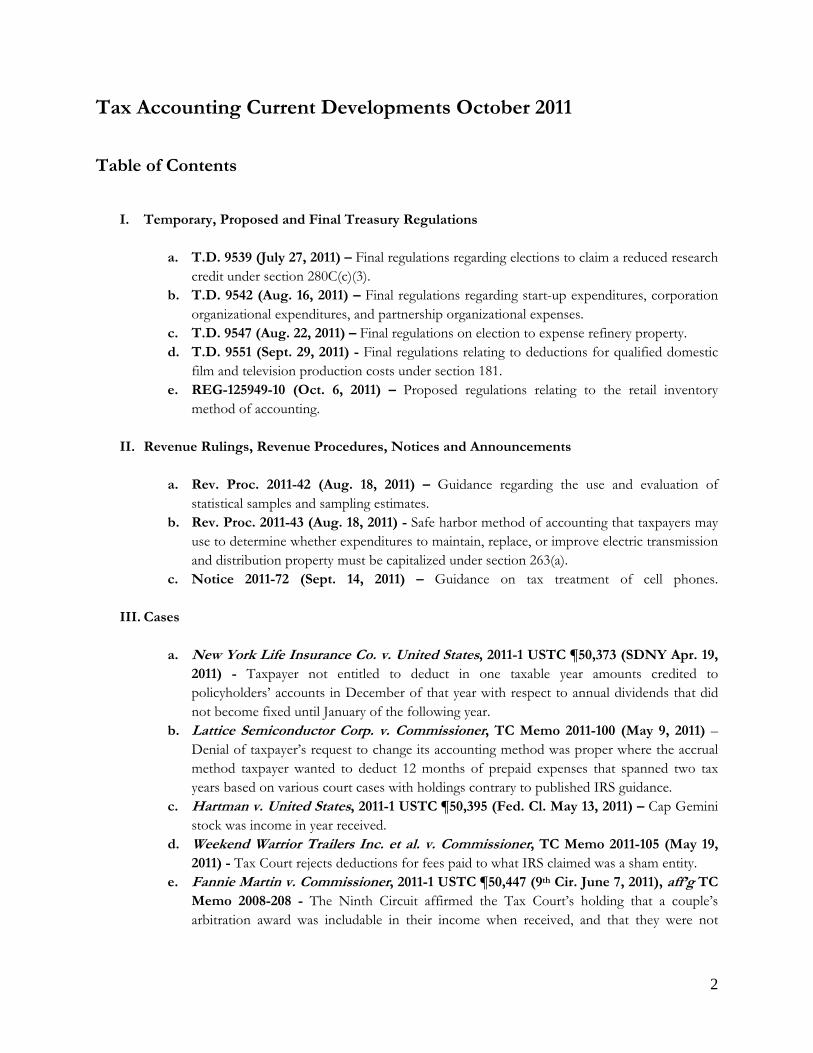

Tax Accounting Current Developments October 2011

Table of Contents

I. Temporary, Proposed and Final Treasury Regulations a. T.D. 9539 (July 27, 2011) – Final regulations regarding elections to claim a reduced research

credit under section 280C(c)(3). b. T.D. 9542 (Aug. 16, 2011) – Final regulations regarding start-up expenditures, corporation

organizational expenditures, and partnership organizational expenses. c. T.D. 9547 (Aug. 22, 2011) – Final regulations on election to expense refinery property. d. T.D. 9551 (Sept. 29, 2011) - Final regulations relating to deductions for qualified domestic

film and television production costs under section 181. e. REG-125949-10 (Oct. 6, 2011) – Proposed regulations relating to the retail inventory

method of accounting.

II. Revenue Rulings, Revenue Procedures, Notices and Announcements a. Rev. Proc. 2011-42 (Aug. 18, 2011) – Guidance regarding the use and evaluation of

statistical samples and sampling estimates. b. Rev. Proc. 2011-43 (Aug. 18, 2011) - Safe harbor method of accounting that taxpayers may

use to determine whether expenditures to maintain, replace, or improve electric transmission and distribution property must be capitalized under section 263(a).

c. Notice 2011-72 (Sept. 14, 2011) – Guidance on tax treatment of cell phones.

III. Cases a. New York Life Insurance Co. v. United States, 2011-1 USTC ¶50,373 (SDNY Apr. 19,

2011) - Taxpayer not entitled to deduct in one taxable year amounts credited to policyholders’ accounts in December of that year with respect to annual dividends that did not become fixed until January of the following year.

b. Lattice Semiconductor Corp. v. Commissioner, TC Memo 2011-100 (May 9, 2011) –Denial of taxpayer’s request to change its accounting method was proper where the accrual method taxpayer wanted to deduct 12 months of prepaid expenses that spanned two tax years based on various court cases with holdings contrary to published IRS guidance.

c. Hartman v. United States, 2011-1 USTC ¶50,395 (Fed. Cl. May 13, 2011) – Cap Gemini stock was income in year received.

d. Weekend Warrior Trailers Inc. et al. v. Commissioner, TC Memo 2011-105 (May 19, 2011) - Tax Court rejects deductions for fees paid to what IRS claimed was a sham entity.

e. Fannie Martin v. Commissioner, 2011-1 USTC ¶50,447 (9th Cir. June 7, 2011), aff’g TC Memo 2008-208 - The Ninth Circuit affirmed the Tax Court’s holding that a couple’s arbitration award was includable in their income when received, and that they were not

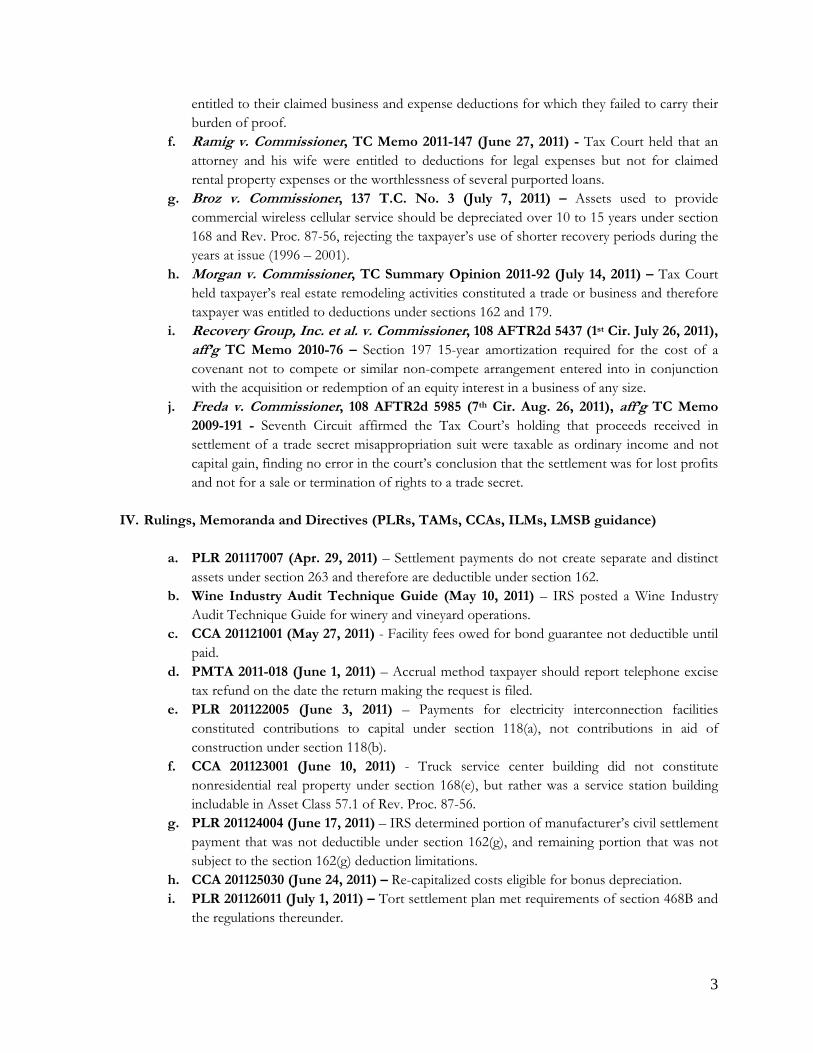

3

entitled to their claimed business and expense deductions for which they failed to carry their burden of proof.

f. Ramig v. Commissioner, TC Memo 2011-147 (June 27, 2011) - Tax Court held that an attorney and his wife were entitled to deductions for legal expenses but not for claimed rental property expenses or the worthlessness of several purported loans.

g. Broz v. Commissioner, 137 T.C. No. 3 (July 7, 2011) – Assets used to provide commercial wireless cellular service should be depreciated over 10 to 15 years under section 168 and Rev. Proc. 87-56, rejecting the taxpayer’s use of shorter recovery periods during the years at issue (1996 – 2001).

h. Morgan v. Commissioner, TC Summary Opinion 2011-92 (July 14, 2011) – Tax Court held taxpayer’s real estate remodeling activities constituted a trade or business and therefore taxpayer was entitled to deductions under sections 162 and 179.

i. Recovery Group, Inc. et al. v. Commissioner, 108 AFTR2d 5437 (1st Cir. July 26, 2011), aff’g TC Memo 2010-76 – Section 197 15-year amortization required for the cost of a covenant not to compete or similar non-compete arrangement entered into in conjunction with the acquisition or redemption of an equity interest in a business of any size.

j. Freda v. Commissioner, 108 AFTR2d 5985 (7th Cir. Aug. 26, 2011), aff’g TC Memo 2009-191 - Seventh Circuit affirmed the Tax Court’s holding that proceeds received in settlement of a trade secret misappropriation suit were taxable as ordinary income and not capital gain, finding no error in the court’s conclusion that the settlement was for lost profits and not for a sale or termination of rights to a trade secret.

IV. Rulings, Memoranda and Directives (PLRs, TAMs, CCAs, ILMs, LMSB guidance) a. PLR 201117007 (Apr. 29, 2011) – Settlement payments do not create separate and distinct

assets under section 263 and therefore are deductible under section 162. b. Wine Industry Audit Technique Guide (May 10, 2011) – IRS posted a Wine Industry

Audit Technique Guide for winery and vineyard operations. c. CCA 201121001 (May 27, 2011) - Facility fees owed for bond guarantee not deductible until

paid. d. PMTA 2011-018 (June 1, 2011) – Accrual method taxpayer should report telephone excise

tax refund on the date the return making the request is filed. e. PLR 201122005 (June 3, 2011) – Payments for electricity interconnection facilities

constituted contributions to capital under section 118(a), not contributions in aid of construction under section 118(b).

f. CCA 201123001 (June 10, 2011) - Truck service center building did not constitute nonresidential real property under section 168(e), but rather was a service station building includable in Asset Class 57.1 of Rev. Proc. 87-56.

g. PLR 201124004 (June 17, 2011) – IRS determined portion of manufacturer’s civil settlement payment that was not deductible under section 162(g), and remaining portion that was not subject to the section 162(g) deduction limitations.

h. CCA 201125030 (June 24, 2011) – Re-capitalized costs eligible for bonus depreciation. i. PLR 201126011 (July 1, 2011) – Tort settlement plan met requirements of section 468B and

the regulations thereunder.

4

j. FAA 20112701F (July 8, 2011) – Bank Enterprise Award payment received from the U.S. Department of the Treasury Community Development Financial Institutions Fund is not excluded from Taxpayer’s income under section 118.

k. LB&I-04-0511-012 (July 28, 2011) – Directive on Examination of Success-Based Fees in Business Acquisitions.

l. CCA 201131010 (Aug. 5, 2011) – Tangible depreciable property used to circulate chilled water through a closed loop pipeline to heat exchangers in customers’ buildings to cool such buildings constitutes 7-year property under section 168(e)(3)(C)(v).

m. IRS drops Schedule M-3’s Supporting Attachment Requirement for R&D Costs (Aug. 4, 2011).

n. CCA 201132021 (Aug. 12, 2011) – Energy contract did not constitute a commodity for purposes of the section 475 mark-to-market rules.

o. PLR 201135022 (Sept. 2, 2011) - IRS revokes 2010 PLR on fringe benefits. p. CCA 201136022 (Sept. 9, 2011) - Commitment fee for construction financing must be

capitalized.

V. IRS 2011-2012 Priority Guidance Plan

5

I. Temporary, Proposed, and Final Treasury Regulations

a. T.D. 9539 (July 27, 2011) – Final regulations regarding elections to claim a reduced research credit under section 280C(c)(3).

In T.D. 9539, the IRS issued final regulations that simplify the IRC section 280C(c)(3) elections to claim a reduced research credit. In large part, these regulations adopt proposed regulations that were issued in 2009 (REG-130200-08) and requiring the election to be made on Form 6765, "Credit for Increasing Research Activities." Under those regulations, the election must be made on a Form 6765 that is filed with an original return by the due date for filing that return. The election is irrevocable for that tax year. In a change from the proposed regulations, the final regulations provide that each member of a controlled group may make a 280C(c)(3) election after the group credit is computed even if a member does not claim a credit. For consolidated groups, only a common parent may make the election on behalf of the members.

Section 280C(c)(1) provides that no deduction is allowed for that portion of the qualified research expenses or basic research expenses otherwise allowable that is equal to the section 41(a) credit. Similarly, section 280C(c)(2) provides that if the section 41(a)(1) credit exceeds the allowable deduction amount for qualified research expenses or basic research expenses, the amount chargeable to capital account for the taxable year for such expenses is reduced by that excess amount. However, neither of these sections apply if a section 280C(c)(3) election is made and the section 41(a) credit for that year is equal to the excess of the amount of credit determined under section 41(a) Without regard to section 280C(c)(3) over the product of the amount of credit determined under section 280C(c)(3)(B)(i) and the maximum rate of tax under section 11(b)(1). Under section 1.280C-4(a), these elections must be by claiming the reduced credit under section 41(a) on an original return for the taxable year. Elections become irrevocable for that taxable year once they are made.

Section 280C(c)(4) provides that section 280C(b)(3) applies for purposes of section 280C(c). Under section 280C(b)(3), in the case of a corporation that is a member of a controlled group of corporations Within the meaning of section 41(f)(5) or a trade or business under common control, Within the meaning of section 41(f)(1)(B) section 280C(b) is applied using rules similar to those found in section 41(f)(1)(A) and (f)(1)(B). Section 1.41-6(a)(1) provides that to determine group member’s research credit, a parent must: (a) compute the group credit in the manner described in section 1.41-6(b), and (b) allocate the group credit among the members of the group in the manner described under section 1.41-6(c). All members of the controlled group are required to use the same computation method (i.e. traditional or simplified).

The final regulations in T.D. 9539 simplify the section 280C(c)(3) election by requiring that it be made on Form 6765, "Credit for Increasing Research Activities." The form containing the election must be filed with an original return for the year on or before the due date (including extensions). These elections become irrevocable for that taxable year. The final regulations also provide that each member of a controlled group may make a 280C(c)(3) election after the group credit is computed and allocated under sections 1.41-6(b)(1) and 1.41-6(c). This rule was included because one of the commentators on the temporary regulations was concerned that the controlled group rules in the proposed regulations might cause administrative complexity if each member of a group had to file a separate Form 6765.

Generally, the proposed regulations provided that each member of a controlled group or a trade or business under common control could make the election. However, the final regulations add that only a common

6

parent Within the meaning of § 1.1502-77(a)(1)(i) of a consolidated group may make the election on behalf of the members. An attachment to a Form 6765 filed by a common parent that adequately identifies the members for which an election is made is sufficient to clearly indicate the intent to make the election for those members. Another commentator believed that some members of a controlled group may fail to make a timely election under section 280C(c)(3) because, at the time of filing the Form 6765 with the original return, no credit was reported by such members. The final regulations confirm that elections may be made whether or not a taxpayer claims any amount of credit on its original return by providing an example where no credit is claimed by a member.

b. T.D. 9542 (Aug. 16, 2011) – Final regulations regarding start-up expenditures, corporation organizational expenditures, and partnership organizational expenses.

Temporary regulations (T.D. 9411) issued in July 2008 under sections 195 (start-up expenditures), 248 (corporate organizational expenditures), and 709 (partnership organizational expenditures) expired on July 7, 2011. These regulations allowed taxpayers to deduct start-up expenditures in the year that an active trade or business begins, in an amount equal to the lesser of the expenses actually incurred or $5,000 (both reduced by any amount over $50,000, but not below zero). Any remainder is deductible ratably over 180 months, beginning with the month in which the active trade or business begins. The temporary regulations provide similar rules for organizational expenditures.

Under section 195(b)(3), for taxable years beginning in 2010, the $5,000 and $50,000 amounts for start-up expenditures were increased to $10,000 and $60,000, respectively. It is important to note that this increase is only for one taxable year (i.e., a taxable year beginning in 2010). For taxable years beginning in 2011, the thresholds revert back to $5,000 and $50,000, respectively.

Importantly, the temporary regulations provide that a taxpayer is not required to file a separate election statement to deduct start-up and organizational costs; rather, a taxpayer is deemed to make the election by deducting and amortizing such costs on its timely filed return for the year in which business begins. A taxpayer may forgo the deemed election by clearly electing to capitalize such costs on its return. As previously noted, the temporary regulations expired on July 7, 2011, but were recently finalized with certain modifications on Aug. 16, 2011, with the issuance of T.D. 9542.

As with the temporary regulations, the final regulations provide that taxpayers are not required to file a separate election statement to deduct start-up and organizational expenditures. Instead, a taxpayer is deemed to elect to deduct start-up and/or organizational expenditures by deducting such costs in accordance with the rules on its timely filed federal income tax return (including extensions) for the taxable year in which business begins. A taxpayer may forgo the deemed election by clearly electing to capitalize such costs on its timely filed federal income tax return (including extensions) for the taxable year in which business begins. The election to either expense and amortize or capitalize start-up and/or organizational expenditures is irrevocable, and applies to all start-up and/or organizational expenditures related to the taxpayer's active trade or business. The final regulations clarify the temporary regulations by defining what is meant by "clearly electing to capitalize" start-up and organizational costs. Specifically, the taxpayer must "affirmatively" elect to capitalize such costs on its timely filed federal income tax return for the year in which its business begins. Accordingly, a taxpayer who unintentionally fails to deduct or amortize start-up and organizational costs for the taxable year in which its business begins is not considered to have "clearly elected to capitalize" them.

7

The final regulations also continue to provide that a change in the characterization of an item as a start-up or organizational expenditure, or a change in the determination of the taxable year in which the business began its active trade or business, is generally treated as a change in method of accounting, requiring the filing of a Form 3115 and recognition of a section 481(a) adjustment.

The final regulations under sections 195, 248, and 709 apply to expenditures paid or incurred after Aug. 16, 2011, but, as with the temporary regulations, taxpayers may apply all the provisions of these regulations to start-up and/or organizational expenditures paid or incurred after Oct. 22, 2004, provided the period of limitations on assessment of tax has not expired for the year the election is deemed made.

c. T.D. 9547 (Aug. 22, 2011) – Final regulations on election to expense refinery property.

In TD 9547, the IRS issued final regulations on the section 179C election to expense 50 percent of qualified refinery property that reflect changes made by the Energy Improvement and Extension Act of 2008. The Act extended the placed-in service date for property to Jan. 1, 2014 and provided that either (a) the refinery construction must have been subject to a written binding construction contract entered into before Jan. 1, 2010, (b) the refinery must have been placed in service before Jan. 1, 2010, or (c) for self-constructed property, the construction of the refinery must have begun after June 14, 2005 and before Jan. 1, 2010. It also provided that, for property placed in service after Oct. 3, 2008, qualified refineries included those designed to process liquid fuel directly from shale or tar sands. Finally, it expanded the production capacity requirement to include property that enabled the refinery to process shale or tar sands. The regulations are automatically effective for tax years ending on or after Aug. 22, 2011, but may be applied to earlier years.

d. T.D. 9551 (Sept. 29, 2011) - Final regulations relating to deductions for qualified domestic film and television production costs under section 181.

In 2004, Congress enacted section 181 in an effort to keep and increase film and television production in the United States. Specifically, for a qualified film or television production commenced after Oct. 22, 2004 and before Jan. 1, 2008 (a pre-amendment production), section 181 permits the production owner to elect to deduct production costs in the taxable year paid or incurred (in lieu of capitalizing and depreciating the costs) if the aggregate production costs do not exceed $15 million ($20 million if a significant amount of the aggregate production costs are paid or incurred in certain designated areas for each qualifying production (the aggregate production costs limit). A film or television production is a qualified film or television production if 75 percent or more of the total compensation of the production is compensation for services performed in the United States by actors, directors, producers and other production personnel. For a television series, only the first 44 episodes qualify, and the production cost limit is determined on an episode-by-episode basis.[4] The election for any production must be made by the owner by the due date (including extensions) of the return for the tax year in which the production costs are first incurred, and is generally irrevocable once made.[5] If the production is owned by an entity, the election should be made at the entity level (e.g., by the common parent of a consolidated group, S corporation or partnership).

Proposed and temporary regulations under section 181 were issued in 2007. In 2008, Congress enhanced the benefits under section 181, providing that for productions which commenced after Dec. 31, 2007 and before Jan. 1, 2010, the first $15 million of costs for each qualified film and television production will qualify for a current deduction ($20 million if a significant amount of the production costs are incurred in designated areas), the “maximum production costs deduction limit.” Prior to this, productions that cost more than $15

8

million were entirely excluded from taking advantage of the deduction. In 2010, section 181 was extended for film and television productions commencing before Jan. 1, 2012.

Most recently, on Sept. 30, 2011, in T.D. 9551, the IRS released final regulations under section 181, adopting the proposed regulations as amended by the final regulations and removing the temporary regulations.

The final regulations use the term “pre-amendment production” to distinguish productions subject to the aggregate production costs limit (i.e., those for which production commenced after Oct. 22, 2004 and before Jan. 1, 2008) from productions subject to the maximum production costs deduction limit (i.e., those for which production commenced after Dec. 31, 2007 and before Jan. 1, 2012). Several provisions of the final regulations are designated as being only applicable to pre-amendment productions. The preamble notes that additional proposed and temporary regulations are expected to be issued to address post-amendment production costs (i.e., film and television productions commencing after Dec. 31, 2007).

These regulations are effective for qualified film and television productions for which principal photography or, for an animated production, in-between animation, commences on or after Sept. 29, 2011. The 2007 proposed and temporary regulations may still be applied to any qualified film or television production which commenced on or after Oct. 24, 2004 and before Feb. 9, 2007. In addition, the 2007 proposed and temporary regulations may also be applied to any other production commenced on or after Jan. 1, 2009 and before Sept. 29, 2011. Alternatively, the final regulations may be applied to such productions.

Final regulations on the deduction for qualified film and television production costs The final regulations define the term “aggregate production costs” as the total production costs paid or incurred “by any person, whether paid or incurred directly by an owner or indirectly on behalf of an owner.” As a result, an owner’s actual section 181 deduction may be less than the aggregate production costs. In addition, because aggregate production costs include payments made by third parties on behalf of the owner (e.g., participations and residuals paid by a film distributor), an owner will not be entitled to a section 181 deduction for any pre-amendment production costs if the aggregate production costs exceed $15 million (or, if applicable, $20 million), even if its directly incurred pre-amendment production costs are less than the aggregate production costs limit.

The final regulations also clarify that, with respect to participations and residuals, the term “production costs” should only include those amounts actually paid or incurred, “notwithstanding the treatment of participations and residuals permitted under the income forecast method in section 167(g)(7)(D)” (which allows a taxpayer to wait and include participations and residuals in depreciable basis when paid or incurred rather than based on the estimated income from the production under section 167(g)(7)(A)).

In determining whether the higher $20 million aggregate production cost limit may apply, a significant amount of production costs are incurred in a designated area if either (1) at least 20 percent of the first-unit principal photography occurred in the designated area or (2) at least 50 percent of the total days of principal photography occurred in a designated area. The final regulations favorably provide that, “[s]olely for purposes of determining whether a production qualifies for the higher aggregate production costs limit provided under this paragraph (b)(2), compensation (as defined in section 1.181-3(c)) to actors (as defined in section 1.181-3(f)(1)), directors, producers, and other production personnel (as defined in section 1.181-3(f)(2)) is allocated entirely to first-unit principal photography.”

9

In rejecting comments that the final regulations should exempt the section 181 deduction from the passive loss limitations of section 469 and the at-risk rules of section 465, Treasury and the IRS state in the preamble that “[b]ecause there is no specific statutory direction specifying that these limitations do not apply, the section 181 deduction continues to be subject to the passive loss and at-risk limitations.”

In the case of section 181 deductions being claimed by more than one owner, the final regulations retain the rule in the temporary regulations that each owner must provide a list of the names and taxpayer identification numbers of all owners claiming section 181 deductions related to the same production, if such owners are not members of an entity who are issued Schedule K-1s with respect to their interest in the production. The final regulations also clarify, however, that “whether or not multiple persons form a partnership with respect to the production will be determined in accordance with section 301.7701-3 of this chapter.”

The preamble also clarifies that neither section 181 nor the final regulations impose (1) a time limit between when a production is set for production and the time expected for commencement of principal photography or (2) a minimum budget for production costs.

Productions for purposes of section 263A are generally productions for purposes of section 181 (e.g., motion picture films, video tapes, digital videos, etc.). The final regulations clarify that section 181 does not apply to productions acquired after “initial release or broadcast.” The final regulations define “initial release or broadcast” as the “first commercial exhibition or broadcast of a production to an audience,” but does not include “limited exhibition prior to commercial exhibition to general audiences if the limited exhibition is primarily for purposes of publicity, marketing to potential purchasers or distributors, determining the need for further production activity, or raising funds for the completion of production.” In the preamble to the final regulations, Treasury and the IRS note that the “object of this provision is to maximize the availability of the election under section 181 to advance the goal of the statute (to promote film and television production in the United States) while preventing the use of section 181 in situations that do not advance the goal of the statute, such as the purchase of an existing film library.”

e. REG-125949-10 (Oct. 6, 2011) – Proposed regulations relating to the retail inventory method of accounting.

On October 6, 2011 the IRS issued proposed regulations that clarify the computation of ending inventory values under the retail inventory method and provide a special rule for certain taxpayers that receive margin protection payments and similar vendor allowances. The proposed regulations restructure and restate the regulations under Treas. Reg. § 1.471-8.

Sales-based vendor allowances

Sales-based vendor allowances are a direct reduction of cost of goods sold, and do not impact the value of inventory on hand at year-end. The proposed regulations clarify the interaction of proposed Treas. Reg. § 1.471-3(e) with the retail inventory method by excluding from the numerator of the cost complement formula the amount of a sales-based vendor allowance, including any discount or rebate.

Cost complement and the retail LCM method

10

The retail inventory method determines an ending inventory value by maintaining proportionality between costs and selling prices. Under the retail inventory method, the value of ending inventory is determined by multiplying the retail selling price of inventory on hand at the end of the year by the cost complement. The cost complement is the ratio of costs to selling price, determined by the formula:

11

Value of beginning inventory + Cost of goods purchased during the tax year

Retail selling price of beginning inventory + Initial selling prices of goods purchased during the tax year

Under the retail lower of cost or market (LCM) method, a reduction in retail selling price reduces the value of ending inventory in the same ratio as the cost complement.

Under Treas. Reg. § 1.471-8, an anomaly in the retail LCM method formula has provided first-in, first-out (FIFO) taxpayers an opportunity to value ending inventory at an amount that is lower than what would otherwise be calculated for a FIFO taxpayer that values inventory at LCM. This distortion is caused when the taxpayer earns an allowance, discount, or price rebate for the permanent markdown of the retail selling price, such as a markdown allowance or margin protection payment. The allowance, discount, or price rebate earned decreases the cost of inventory in the numerator of the cost complement, and the markdown allowance or margin protection payment lowers the retail selling price of ending inventory, which is the multiplicand in the retail inventory method. The double reduction to the cost complement and the multiplicand for costs directly related to the inventory selling price creates the distortion. To eliminate the double reduction, the proposed regulations do not allow a retail LCM method taxpayer to reduce the numerator of the cost complement by the amount of an allowance, discount, or price rebate that is related to or intended to compensate for a permanent markdown of retail selling prices. Thus, in the case of markdown allowances and margin protection payments, the value of ending inventory as computed under the retail LCM method is reduced solely as a result of the reduction in retail selling price, avoiding an unwarranted additional reduction in inventory value for a single markdown allowance and more reasonably approximating LCM.

Although Treas. Reg. § 1.471-8 has allowed retail LCM method taxpayers to formulaically take an additional reduction in the cost of ending inventory, some taxpayers that took this approach have likely been disallowed the double reduction in exam.

The IRS provides for an alternative approach in the preamble to the proposed regulations. Under the alternative approach, the retail inventory method could achieve the same result by permitting taxpayers to reduce the numerator of the cost complement for all non-sales based allowances, discounts, or price rebates, including markdown allowances, but requiring a reduction of the denominator of the cost complement for all permanent markdowns related to markdown allowances. The IRS is seeking comments on whether the final regulations should provide this or other alternative retail LCM methods.

Temporary price adjustments

The proposed regulations also clarify that under the retail inventory method taxpayers do not adjust the cost complement or ending retail selling prices for temporary markdowns and markups. This has been a long-standing position of the IRS for which no authoritative guidance existed prior to the proposed regulations.

12

Comments on the proposed regulations and requests for a public hearing must be submitted to the IRS by January 5, 2012. The proposed regulations would apply for tax years beginning after the date they are published as final regulations.

II. Revenue Rulings, Revenue Procedures, Notices and Announcements

a. Rev. Proc. 2011-42 (Aug. 19, 2011) – Guidance regarding the use and evaluation of statistical samples and sampling estimates.

The IRS recently issued Rev. Proc. 2011-42 on the use and evaluation of statistical sampling procedures. In certain cases, the IRS has permitted the use of statistical sampling by taxpayers to support items on their income tax returns. See, for example, Rev. Proc. 2011-35 (safe harbor methodologies to determine basis in stock acquired in transfer basis transactions); Rev. Proc. 2004-29 (statistical sampling methodology taxpayer may use in establishing the amount of substantiated meal and entertainment expenses that are excepted from the 50% deduction disallowance under section 274(n)(1)); Rev. Proc. 2007-35 (when statistical sampling may be used for purposes of section 199 (income attributable to domestic production activities)); Rev. Proc. 2002-55 (permits external auditors of qualified intermediaries to use statistical sampling); and Rev. Proc. 72-36 (statistical sampling guidelines for determining the redemption rate of trading stamps). In lieu of and in addition to prior guidance, the IRS will use the criteria set forth in section 4 of Rev. Proc. 2011-42 to determine whether to accept a statistical sampling estimate as adequate substantiation for a return position. Statistical samples that fail to meet these criteria will be rejected. The guidance also includes three appendices: Appendix A - Sampling Plan Standards, Appendix B - Sampling Documentation Standards, and Appendix C - Technical Formulas. Application of the new guidance will be required for tax years ending on or after Aug. 19, 2011 and allowed, but not required, for tax years ending before that date (provided the applicable limitations period has not expired).

According to the guidance, the appropriateness of using a statistical sampling estimate as adequate substantiation for a return position is a facts-and-circumstances determination. The factors that the IRS will use in determining whether it is appropriate include (but are not limited to):

• The time required to analyze large volumes of data • The cost of analyzing data • The other books and records that may independently exist or have greater probative value

Statistical sampling estimates will not be considered appropriate if evidence is readily available from a more accurate source, or if the use of sampling does not conform to applicable accounting standards (such as GAAP). If sampling is appropriate, taxpayers must determine whether the final estimate is valid. An estimate will be considered valid if all of the following conditions are met:

• The taxpayer maintains proper documentation to support the statistical application, sample unit findings and all aspects of the sample plan.

• The estimate is based on a probability sample, in which sampling units have a known (non-zero) chance of selection using either a simple random sampling method or stratified random sampling method.

• The estimate is computed at the least advantageous 95 percent one-sided confidence limit, which is either the upper or lower limit that results in the least benefit to the taxpayer.

13

Although many methods exist to estimate population values from the sample data, only the following variable estimators will be considered by the IRS:

• The Mean (also known as the direct projection method) [The first variable used for the difference, ratio and regression estimators must be the variable used in the mean estimator.]

• The Difference (using "paired variables") [The second variable used for the difference, ratio, and regression estimators must be a variable that can be paired with the first variable and should be related to the first variable.]

• The (combined) Ratio (using a variable of interest and a "correlated" variable) • The (combined) Regression (using a variable of interest and a "correlated" variable)

Taxpayers that choose to use the ratio or regression methods must first demonstrate that the statistical bias inherent in those methods is negligible.

When creating a variable sampling plan, the final statistical sampling estimate with the smallest overall standard of error, as an absolute value, should be used to support a return position. Situations may exist in which only a single estimator may be appropriate for the variable sampling plan objective; in those specialized situations, the relevant estimator may be evaluated without consideration of other methods.

When using simple random samples, the confidence limits are determined using a Hypergeometric, Poisson, or Binomial distribution. If the proportion being estimated is between 30 and 70 percent, the normal distribution approximation may be used in lieu of one of the above distributions.

For stratified random samples, in which at least two strata are sampled, the confidence limits must be determined using the normal distribution approximation. If stratified random samples are not used, confidence limits will be determined using the Hypergeometric, Poisson, or Binomial distribution. One of the following two tests must be achieved for the use of the point estimate from an attribute sampling plan:

• A relative precision of 10 percent or less must be achieved on the point estimate (i.e., the estimated proportion, p) and on its complement (i.e., 1 - p); or

• A simple random sample size of at least 300 must be used to determine the point estimate, when the sample size of 300 excludes dummy and null sampling units.

b. Rev. Proc. 2011-43 (Aug. 18, 2011) - Safe harbor method of accounting that taxpayers may use

to determine whether expenditures to maintain, replace, or improve electric transmission and distribution property must be capitalized under section 263(a).

In Rev. Proc. 2011-43, the IRS provided a safe harbor method of accounting to determine whether expenditures to maintain, replace or improve electric transmission and distribution property must be capitalized under section 263(a). The safe harbor classifies transmission and distribution property as either linear property or nonlinear property. For linear property, the guidance defines the appropriate units of property and provides a simplified method of determining when the cost of replacing part of such a unit must be capitalized. For nonlinear property, the guidance provides definitions for the appropriate unit of property, but does not provide a simplified method for capitalization. The guidance also identifies expenditures that are per se treated as capital expenditures and provides several examples to illustrate the rules. Taxpayers seeking to change to the safe harbor must use the automatic change provisions in Rev. Proc. 2011-14 or its successor, and may use statistical sampling to determine the applicable section 481(a) adjustment. Taxpayers also may

14

extrapolate results to determine the section 481(a) adjustment. The revenue procedure is effective for tax years ending after Dec. 31, 2010.

Taxpayers that transmit and distribute electricity incur significant expenditures to maintain, replace and improve transmission and distribution property. Whether these expenditures are deductible as repairs under section 162 or must be capitalized as improvements under section 263(a) depends on whether the expenditures materially increase the value of the property or substantially prolong its useful life. Applying capitalization principles to electric transmission and distribution is difficult and leads to disagreements between taxpayers and the IRS about what constitutes a unit of property and whether the replacement of a particular item materially increases the value or substantially prolongs the useful life of such a unit of property. The guidance attempts to minimize these disputes by providing a safe harbor method to determine the amount of expenditures required to be capitalized. This method is available to a taxpayer that has a depreciable interest in electric transmission or distribution property used primarily to transport, deliver or sell electricity; and applies the safe harbor method to all of its electric transmission and distribution property.

Units of Property - For purposes of Rev. Proc. 2011-43, the "unit of linear property" is determined on a circuit-by-circuit basis. The following constitute a single unit of linear property:

• All conductor and any associated devices, whether overhead or underground, used to conduct electricity (not including customer service lines and substation property)

• All towers and poles and all structures and fittings mounted on towers and poles (not including the line transformers)

• All underground conduits • All boxes and vaults, and structures and fittings mounted in boxes or vaults (not including the line

transformers) • All the customer service drops (the conductor and any associated devices running from a utility pole

or underground box or vault to a customer's building or other premises) • All the street lighting • All the traffic and similar signal systems • All the smart grid property [As defined in section 168(i)(19)(B).] not located at a substation (including

access points, relays, and e-bridges, but excluding smart electric meters)

The following constitute a single unit of non linear property:

• Each transformer at a substation • All fencing, walls, enclosures, other structures surrounding each substation or supporting the

substation electrical devices (excluding enclosures or buildings suitable for occupation), and land improvements that are not properly capitalized to land

• Each set of installed storage battery property • All smart grid property located at each substation • All other electrical devices at each substation, such as fuses, breakers, other switches, regulators,

insulators, meters, and the pad on which the equipment is installed • Each line transformer • Each customer electric meter (including each smart electric meter) • All other property installed on each customer's premises

15

For each replacement of a portion of a unit of property, the taxpayer must determine whether more than 10 percent is replaced. If so, the cost of the replacement must be capitalized. The percentage replaced is determined based on the number of items (or other denominating factor) existing in a unit of property at the beginning of a taxable year as follows:

• For conductor and associated devices used to conduct electricity (not including customer service lines), the number of feet of conductor replaced is divided by the number of feet of conductor in the unit of property (for example, if 100 feet of conductor is replaced in a circuit that contains 2,000 feet of conductor, the percentage of the conductor replaced is 5 percent [100 / 2,000 = .05])

• For poles and towers, the number of poles and towers replaced is divided by the number of poles and towers in the unit of property

• For underground conduit, the number of feet of conduit replaced is divided by the number of feet of conduit in the unit of property

• For boxes and vaults, the number of boxes and vaults replaced is divided by the number of boxes and vaults in the unit of property

• For customer service drops, the number of customer service drops replaced is divided by the number of customer service drops in the unit of property

• For street lighting, the number of street lights replaced is divided by the number of street lights in the unit of property

• For traffic and similar signal systems, the number of traffic and similar signals replaced is divided by the number of traffic and similar signals in the unit of property

• For smart grid property (excluding smart electric meters), the historical cost of smart grid devices replaced is divided by the historical cost of the smart grid unit of property

In general, individual replacements within a circuit are not aggregated in determining the percentage of a unit of linear property replaced. Special rules also apply to multiple replacements that are initiated at the same time, such as using a blanket work order.

Per se capital expenditures - The following expenditures must be capitalized, notwithstanding any other provision of Rev. Proc 2011-43:

• The costs of replacing overhead conductor with underground conductor within a circuit, regardless of the percentage of conductor in the circuit that is replaced

• The costs of property necessary to add one or more new customers • The costs of property that materially increases rated capacity (a) in a unit of property or (b) to one or

more customers • The costs of property that extends an existing circuit

Taxpayers adopting the safe harbor method may use statistical sampling to determine its section 481(a) adjustment by following the sampling procedures provided in Rev. Proc. 2011-42. In addition, taxpayers may extrapolate results to determine their section 481(a) adjustment by following the relevant procedures provided in Appendix A of Rev. Proc. 2011-43. The guidance also provides the following instructions for switching to the safe harbor method described above:

• The scope limitations provided in the guidance do not apply to a company that changes to the safe harbor for its first or second taxable year ending after Dec. 30, 2010.

16

• A taxpayer must take the entire net section 481(a) adjustment into account (whether positive or negative) in computing taxable income in the year of change.

• The section 481(a) adjustment cannot include any amount attributable to property for which the taxpayer elected to apply the repair allowance under Treas. Reg. section 1.167(a)-11(d)(2) for any taxable year in which the election was made.

• A taxpayer changing its method of accounting under section 3.09 of the appendix must file a signed copy of its completed Form 3115 with the IRS in Ogden, UT, (Ogden copy) in lieu of filing the national office copy no earlier than the first day of the year of change and no later than the date the taxpayer files the original Form 3115 with its federal income tax return for the year of change.

• The designated automatic accounting method change number for this safe harbor is "160".

c. Notice 2011-72 (Sept. 14, 2011) – Guidance on tax treatment of cell phones.

The Small Business Jobs Act of 2010 (the Act) removed cell phones from the definition of listed property for taxable years beginning after Dec. 31, 2009.1 As a result, the additional substantiation requirements normally applicable to listed property no longer apply to cell phones for taxable years beginning after Dec. 31, 2009. However, this removal did not otherwise alter the requirement that an employer-provided cell phone is a fringe benefit, the value of which must be included in the employee's gross income unless an exclusion applies or the cell phone may be treated as an excludible fringe benefit

In Notice 2011-72, the IRS notes that many employers provide their employees with cell phones primarily for noncompensatory business reasons, further providing that the value of the business use of an employer-provided cell phone is excludable from an employee's income as a working condition fringe, to the extent that, if the employee paid for the use of the cell phone himself, such payment would be allowable as a deductible business expense.

Notice 2011-72 states that an employer will be considered to have provided an employee with a cell phone primarily for noncompensatory business purposes if there are substantial reasons relating to the employer's business (other than providing compensation to the employee) for providing a cell phone, and provides the following examples of possible substantial noncompensatory business reasons:

• an employer's need to contact an employee at all times for work-related emergencies • the employer's requirement that the employee be available to speak with clients at times when the

employee is away from the office • the employee's need to speak with clients located in other time zones at times outside of the

employee's normal work day

Alternatively, Notice 2011-72 states that substantial noncompensatory business reasons do not include cell phones provided:

• to promote employee morale or good will • to attract prospective employees • as a means of furnishing additional compensation to employees

In Notice 2011-72, the IRS favorably states that when an employer provides an employee with a cell phone primarily for noncompensatory business reasons, it will be nontaxable to the employee as a working condition

17

fringe benefit5 (the value of which is excludable from the employee's income), and recordkeeping of business use will not be required. In addition, the IRS will treat the value of any personal use of a cell phone provided by the employer primarily for noncompensatory business purposes as excludable from the employee's income as a de minimis fringe benefit.

III. Cases

a. New York Life Insurance Co. v. United States, 2011-1 USTC ¶50,373 (Apr. 19, 2011) - Taxpayer not entitled to deduct in one taxable year amounts credited to policyholders’ accounts in December of that year with respect to annual dividends that did not become fixed until January of the following year.

In New York Life Insurance Co. v. United States, a U.S. district court has held that the taxpayer was not entitled to deduct in one taxable year amounts credited to policyholders’ accounts in December of that year with respect to annual dividends that did not become fixed until January of the following year.

Under New York law, the taxpayer was required to annually distribute a portion of its surplus earnings (“Annual Dividend”) to the owners of participating insurance policies and annuity contracts. The Annual Dividend became payable on the anniversary of the policy if it was still in force and all premiums due had been paid. In each of the years at issue, the taxpayer credited a policyholder’s account with the Annual Dividend on the later of (1) thirty days before the anniversary of the Policy; or (2) the date on which all premiums due had been received. However, the taxpayer did not actually pay the Annual Dividend until the policy anniversary date. For example, for policies with January anniversaries, the taxpayer credited the policyholder account in December of one year but did not pay the Annual Dividend until January of the following year.

In addition, New York law allows the taxpayer to distribute a portion of its surplus earnings as a one-time dividend to policyholders when a Policy terminates by death, maturity or surrender ("Termination Dividend”). If a policy terminated after the taxpayer credited the policyholder's account with the Annual Dividend, the policyholder received both an Annual Dividend and a Termination Dividend in the year in which the Policy terminated. Alternatively, if a Policy terminated before the taxpayer credited the policyholder's account with the Annual Dividend, the policyholder received only a Termination Dividend in that year. Finally, if a Policy did not terminate in a given year, the policyholder received only an Annual Dividend. Each December, the taxpayer estimated the minimum amount (i.e., the smaller of the two dividends), to be paid on each Policy in the following year.

The IRS challenged the timing of the taxpayer’s deductions for the Annual and Termination Dividends, asserting that they were not deductible until the year in which actually paid to policyholders. The court looked at the rules under section 461 and the regulations thereunder in determining when the taxpayer had a fixed and determinable liability for which economic performance had occurred. Citing United States v. General Dynamics, 481 US 239 (1987), the Court held that the taxpayer’s liability for Annual and Termination Dividends only arose if a Policy remained in force on its anniversary date (i.e., if the policy had not been terminated prior to that date, its liability was contingent). In rejecting the taxpayer’s argument that its liability to pay Annual Dividends became fixed when it credited the policyholder’s account for the dividend, the court noted that the taxpayer’s liability was not fixed until the anniversary date (the date fixed by the contract). Similarly, in rejecting the taxpayer’s assertion that it was entitled to deduct the smaller of the Annual or Termination Dividend, the court noted that as of December 31 of each tax year at issue the taxpayer did not

18

have a fixed liability to pay either the Annual or Termination Dividend in the following tax year (i.e., neither dividend was unconditionally due). Accordingly, because the all events test was not satisfied in this case, the Dividends were not deductible and the court did not consider whether such liabilities were determinable with reasonable accuracy or whether the recurring item exception applied.

b. Lattice Semiconductor Corp. v. Commissioner, TC Memo 2011-100 (May 9, 2011) –Denial of taxpayer’s request to change its accounting method was proper where the accrual method taxpayer wanted to deduct 12 months of prepaid expenses that spanned two tax years based on various court cases with holdings contrary to published IRS guidance.

In Lattice Semiconductor Corp. v. Commissioner, TC Memo 2011-100. the Tax Court held that the IRS’s denial of a taxpayer’s request to change its accounting method was proper where the accrual method taxpayer wanted to deduct 12 months of prepaid expenses that spanned two tax years based on various court cases with holdings contrary to published IRS guidance. Specifically, the taxpayer claimed a prepaid expense deduction for 2002 even though final regulations allowing such a change were not published until 2003. The Court rejected the taxpayer’s claim that the IRS ignored developing case law and abused its discretion because the cases relied upon by the taxpayer had narrow holdings that did not apply directly to the taxpayer.

Under the facts of the case, the accrual method taxpayer designed, developed, and marketed high-performance programmable logic devices and related software. The taxpayer regularly prepaid expenses for insurance, maintenance and service contracts. The benefits of these prepaid expenses generally did not exceed 12 months, but the contract periods sometimes spanned two tax years. Prior to 2002, the taxpayer capitalized such costs. In January 2002, the Treasury Department issued an Advance Notice of Proposed Rulemaking (ANPR) stating that it expected to propose a rule that would no longer require capitalization of 12-month prepaid expenses under section 263. In February 2002, the IRS issued an Industry Directive (ID) on guidelines for the application of the ANPR, which stated that the ANPR’s rule would likely be adopted despite the IRS’s contrary position. The ID cautioned that advance IRS consent was still required for accounting method changes.

In December 2002, Treasury published a Notice of Proposed Rulemaking (NPR), Prop. Treas. Reg. section 1.263(a)-4(f)(1). that again proposed to incorporate a 12-month rule so long as the useful life of any benefit did not exceed one year. The NPR advised taxpayers not to seek a method change in reliance upon the proposed rules until final regulations were published. Later that December, the taxpayer filed an advance consent method change request to deduct 12-month prepaid expenses spanning two taxable years based on the ANPR and U.S. Freightways Corp. v. Commissioner. 270 F.3d 1137 (7th Cir. 2001), rev’g. 113 T.C. 329 (1999). Prior to obtaining consent, the taxpayer claimed a deduction for such prepaid expenses on its 2002 consolidated Federal income tax return and calculated a net operating loss carryback from the 2002 deduction, which it applied to its 1999 and 2000 tax years and obtained refunds.

In January 2004, Treasury published final regulations that incorporated the rule that taxpayers were not required to capitalize 12-month prepaid expenses for amounts paid or incurred on or after Dec. 31, 2003. Treas. Reg. §1.263(a)-4(f), T.D. 9107. The IRS then released Rev. Proc. 2004-23, which provided automatic consent procedures for accounting method change requests to comply with the final regulations with the caveat that consent for such method changes would not be granted for a year of change prior to the effective date of the regulations. Accordingly, in May 2004, the IRS denied the taxpayer’s request to use the 12-month rule for prepaids and gave the taxpayer the option to either withdraw its application and receive a refund of the user fee, or to explain its reasons for not withdrawing its request. The taxpayer did neither. The IRS then

19

issued a letter formally denying petitioner's accounting method change in June 2005. The taxpayer submitted a response that included a discussion of Zaninovich v. Commissioner, 616 F.2d 429 (9th Cir. 1980), rev’g., 69 T.C. 605 (1978), to argue that the Ninth Circuit allowed taxpayers to use the 12-month rule for years prior to the issuance of the final regulations. The IRS issued a deficiency notice and the taxpayer timely filed a petition with the Tax Court.

Under section 446(e), a taxpayer must secure IRS consent before changing its accounting method for computing income. The Commissioner has wide discretion to grant or deny consent. See Capitol Fed. Sav. & Loan Ass'n & Sub. v. Commissioner, 96 T.C. 204, 213 (1991). The taxpayer must continue computing taxable income under its old accounting method if the Commissioner denies the taxpayer's request to change its accounting method. See United States v. Ekberg, 291 F.2d 913, 925 (8th Cir. 1961); Advertisers Exch., Inc. v. Commissioner, 25 T.C. 1086, 1092-1093 (1956), aff’d. 240 F.2d 958 (2d Cir. 1957). See also, section 9.17 of Rev. Proc. 2011-1. In addition, the Commissioner can require a taxpayer to abandon the new accounting method and to report taxable income using the old method if the taxpayer changes its accounting method without first obtaining consent. See, Advertisers Exch. at 1093; Sunoco, Inc. & Subs. v. Commissioner, T.C. Memo. 2004-29; section 2.06 of Rev. Proc. 2002-18. In Lattice Semiconductor, the taxpayer argued that despite these requirements, the IRS improperly denied its method change because it ignored developing case law and applied an automatic rejection policy in Rev. Proc. 2004-23. The IRS responded that the taxpayer was ineligible to deduct the relevant expenses before the regulations became final. The Tax Court agreed with the IRS.

While acknowledging that the Ninth Circuit had reversed the Zaninovich case to hold that 12-month rental payments were fully deductible in the year of payment, the Tax Court distinguished Zaninovich as applicable only to cash basis taxpayers. The case had no application to accrual basis taxpayers such as the taxpayer here. The Tax Court also noted that U.S. Freightways, which adopted the 12-month rule for accrual method taxpayers, was not binding on the IRS, the Tax Court, or taxpayers outside the Seventh Circuit. Accordingly, the court dismissed the taxpayer’s claim that Zaninovich and U.S. Freightways indicated that the Ninth Circuit would have adopted a 12-month rule for accrual method taxpayers without enactment of the final regulations. Accordingly, the Tax Court held that the IRS National Office did not abuse its discretion in rejecting the taxpayer’s accounting method change request. Because this holding settled the matter, the Court did not examine the automatic rejection policy issue.

The Tax Court found that the taxpayer’s only option in this case was to wait for the final regulations and their implementation as described in Rev. Proc. 2004-23. Because the regulations promulgating the 12-month rule were effective for amounts prepaid on or after Dec. 31, 2003 and the taxpayer had sought to deduct expenses for 2002, the court found that the IRS was justified in denying the taxpayer’s request for a method change.

c. Hartman v. United States, 2011-1 USTC ¶50,395 (Fed. Cl. May 13, 2011) – Cap Gemini stock was income in year received.

In Hartman v. United States, the Court of Federal Claims denied a couple’s request for a partial tax refund based on their claim that the husband, a former Ernst & Young LLP partner, did not receive all the Cap Gemini stock they reported on their 2000 income tax return, holding that he constructively received all the shares in 2000 and properly reported the gain.

Under the facts of the case, Cap Gemini bought Ernst & Young's information-technology consulting business in 2000. Consulting partners of Ernst & Young received shares of Cap Gemini stock in exchange for

20

their partnership interests. Cap Gemini transferred 25% of the shares to the partners in 2000. The remaining 75% of the shares were held by Merrill Lynch in individual accounts for each partner. These shares could not be sold for up to five years, and were subject to forfeiture if a partner quit, was fired for cause or "poor performance," or went into competition with Cap Gemini.

On their 2000 federal income tax return, the taxpayers, who used the cash method of accounting and “prepared [the tax return] in accordance with the letters and instructions” provided by Cap Gemini and Ernst & Young, reported a long-term capital gain. Mr. Hartman left Cap Gemini in 2002, was initially allocated 55,000 shares, and likely forfeited 10,543 shares. The taxpayers reported the forfeiture of Cap Gemini stock on their 2002 federal income tax return as a restoration of amounts held under a claim of right pursuant to section 1341. They included a statement with their return indicating that Mr. Hartman had returned 10,560 shares to Cap Gemini and that they had originally reported the receipt of these shares on their 2000 return. They claimed that because they over-reported the number of shares Mr. Hartman received in 2000, they were entitled to a credit. Because the IRS had not granted their refund request, they filed suit.

The taxpayers asserted that Mr. Hartman did not actually or constructively receive all of his shares of Cap Gemini stock in 2000, and therefore should not be taxed in 2000 on all of the shares allocated to him in the transaction. The IRS contended that the taxpayers were attempting to recharacterize the terms of the transaction to obtain preferred taxation, asserting that under the Danielson rule, they were prohibited from recharacterizing the transaction and should therefore be taxed in 2000 on all of the Cap Gemini stock received in the transaction.

In comparing the instant case to two federal appellate court decisions on suits brought by other former consulting partners (see United States v. Fletcher, 562 F.3d 839 (7th Cir. 2009), and United States v. Fort, 2011 WL 1466419 (11th Cir. Apr. 19, 2011)), the court noted that it saw “no reason to depart from the well-reasoned analyses and conclusions of the Seventh and Eleventh Circuits.” The court determined that Mr. Hartman, like the former consulting partners in Fletcher and Fort, had a significant amount of control over his receipt and disposition of Cap Gemini stock. In addition, while some of the shares were held in the restricted account, Mr. Hartman could vote on and receive dividends from them. Thus, the court held that Mr. Hartman constructively received all of the shares for tax purposes in 2000 (i.e., when they were issued to him by Cap Gemini). As a result, the court further held that the taxpayers were not entitled to a refund because they properly reported gain from the receipt of such stock on their 2000 federal income tax return.

d. Weekend Warrior Trailers Inc. et al. v. Commissioner, TC Memo 2011-105 (May 19, 2011) - Tax Court rejects deductions for fees paid to what IRS claimed was a sham entity.

In Weekend Warrior Trailers Inc. et al. v. Commissioner, the court disallowed the taxpayer’s deductions for depreciation and management fees which lacked substantiation, economic substance and economic purpose.

Management fees

Under the facts of the case, the taxpayer’s sole shareholder was also the sole shareholder of its management services company. During the years at issue, the taxpayer deducted amounts paid to its management services company for management and employee leasing fees. The IRS challenged such deductions on the basis that there was no business purpose for the transactions and the management services company was formed for the primary purpose of obtaining tax benefits. See, e.g., Moline Props., Inc. v. Commissioner, 319 U.S. 436 (1943).

21

In addition, the taxpayer was not able to provide any credible evidence that the management services company resulted in any meaningful changes in business operations or achieved cost savings or efficiencies.

While holding that the management services company carried on sufficient business activity to be recognized as a corporation for Federal income tax purposes (based on its bank accounts, employees, tax returns, etc.), the court agreed with the IRS that the management fees were not necessary or reasonable, and therefore were not deductible under section 162. The court determined that the fees were not reasonable or necessary based on the fact that no invoices were ever issued to the taxpayer for the services provided, the lack of job descriptions and clear employee responsibilities, and the lack of evidence supporting what services were provided under the management agreement. Thus, the taxpayer failed to meet its burden of proof.

Depreciation

The taxpayer also purchased and claimed depreciation deductions (including bonus depreciation under section 168(k)) for a used airplane for which mileage logs describing or listing any business purpose for flights were not maintained. The IRS determined that the taxpayer used the airplane 14% for business during 2002 and 40% during 2003 – 2004, and therefore disallowed depreciation deductions related to any personal use. In addition, the IRS disallowed the bonus depreciation that was claimed since the airplane was not original use property. In agreeing with the IRS, the court determined that the taxpayer failed to establish business use of the airplane and substantiation requirements. In addition, the court noted that even if the taxpayer had met the section 274(d) requirements with respect to the airplane, it was not entitled to claim bonus depreciation under section 168(k) because the airplane did not satisfy the original use requirement. The court also upheld the IRS’s disallowance of the taxpayer’s deductions related to repairs and maintenance of the airplane, insurance, pilot fees, etc., due to lack of substantiation.

In addition, the taxpayer purchased and claimed depreciation deductions for a boat for which contemporaneous logs regarding business use were not maintained. The IRS fully disallowed the taxpayer’s depreciation deductions for the boat due to the taxpayer’s failure to meet the substantiation requirements of section 274(d). The court agreed that the taxpayer did not satisfy the adequate records requirement of section 274(d) and therefore the taxpayer was not able to support that the boat was used for business purposes.

e. Fannie Martin v. Commissioner, 2011-1 USTC ¶50,447 (9th Cir. June 7, 2011), aff’g TC Memo 2008-208 - The Ninth Circuit affirmed the Tax Court’s holding that a couple’s arbitration award was includable in their income when received, and that they were not entitled to their claimed business and expense deductions for which they failed to carry their burden of proof.

Under the facts of Fannie Martin v. Commissioner, the taxpayers were the beneficiaries of an arbitration award that the IRS determined was includable in their income when received. The Tax Court ruled in favor of the IRS, holding that under the cash method of accounting, the taxpayers were required to recognize their award as income in the year the award was received. In noting that the taxpayers failed to carry their burden of proof with respect to their business deductions, the Court also ruled that their claimed business expenses were not proper or substantiated, and upheld the IRS’s determination of deficiencies and penalties.

f. Ramig v. Commissioner, TC Memo 2011-147 (June 27, 2011) - Tax Court held that an attorney and his wife were entitled to deductions for legal expenses but not for claimed rental property expenses or the worthlessness of several purported loans.

22

Under the facts of Ramig v. Commissioner, the taxpayer formed a startup company to which he made seven purported loans. The taxpayer paid some of his company’s operating expenses and claimed that such amounts were loans to the company that would be repaid. Shortly before the company shut down, the company was sued but prevailed in the suit and claimed deductions for the related legal fees. The taxpayer also claimed bad debt deductions under section 166 for the unpaid principal of the loans and business expenses paid on the company’s behalf.

The Court determined that the taxpayer was entitled to deduct the legal fees based on the fact that the taxpayer was an employee of the company, and the legal expenses related to a claim that arose from the taxpayer’s performance of duties as the president and general manager of the company. However, the Court determined that the taxpayer was not entitled to its claimed bad debt deductions. In making its determination that the advances did not constitute a bona fide debt, the Court looked at the following factors: (i) the labels on the documents evidencing the (supposed) indebtedness, (ii) the presence or absence of a maturity date, (iii) the source of payment, (iv) the right of the (supposed) lender to enforce payment, (v) the lender’s right to participate in management, (vi) the lender’s right to collect compared to the regular corporate creditors, (vii) the parties’ intent, (viii) the adequacy of the (supposed) borrower’s capitalization, (ix) whether stockholders’ advances to the corporation are in the same proportion as their equity ownership in the corporation, (x) the payment of interest out of only “dividend money”, and (xi) the borrower’s ability to obtain loans from outside lenders. The Court determined that the advances constituted equity based on the following the factors: (i) the taxpayer was unable to present evidence that the company could have borrowed money from outside lenders, (ii) the taxpayer only expected repayment if the company raised more capital, (iii) the company consistently operated at a loss and the taxpayer did not demand timely repayment, (iv) the taxpayer had no evidence to support that the company ever paid interest or that he ever requested the payment of interest, and (v) the taxpayer never tried to enforce the notes and some of the notes were unsigned. Accordingly, because the taxpayer and his company did not have a bona fide debtor-creditor relationship, the Court held that the taxpayer was not entitled to deductions under section 166 for its “advances” to the company.

g. Broz v. Commissioner, 137 T.C. No. 3 (July 7, 2011) – Assets used to provide commercial wireless cellular service should be depreciated over 10 to 15 years under section 168 and Rev. Proc. 87-56, rejecting the taxpayer’s use of shorter recovery periods during the years at issue (1996 – 2001).

In Broz v. Commissioner, the Tax Court held that assets used to provide commercial wireless cellular service should be depreciated over 10 to 15 years under section 168 and Rev. Proc. 87-56, rejecting the taxpayer's use of shorter recovery periods during the years at issue (1996 – 2001).

Under the facts of the case, RFB Cellular Inc. (RFB) depreciated cell towers, antennas, equipment shelters, and land improvements as seven-year property under asset class 48.32, Telegraph, Ocean Cable, and Satellite Communications – High Frequency Radio and Microwave Systems. It depreciated other assets as five- and seven-year property under asset class 48.121, Computer-based Telephone Central Office Switching Equipment. The IRS determined that such assets should have been depreciated over 10 to 15 years, under asset classes 48.12 (Telephone Central Office Equipment) and 48.14 (Telephone Distribution Plant), and proposed deficiencies of more than $16 million for the years at issue (1996 – 2001). Based on the plain language of section 168 and Rev. Proc. 87-56, the Court agreed with the IRS, and held that the assets constituted 10- to 15-year depreciable property for the years at issue.

23

Specifically, RFB provided wireless cellular service through its cellular network that consisted of three basic components: (1) the base station, which includes towers, antennas and related electronic equipment; (2) transmission facilities between the base station and the switch; and (3) the switch. RFB claimed depreciation deductions for this equipment during the years at issue by classifying the equipment into the following three categories:

• Antenna support structures – included costs for towers, antennas, equipment shelters and related land improvements, which were depreciated over seven years under asset class 48.32.

• Cell site equipment – included a wide variety of equipment, including the switch and the base station, which were depreciated over five to seven years under asset class 48.121.

• Leased digital equipment – included costs for concrete, excavating, steel, fencing and construction, which were depreciated over five years under asset class 48.121.

Under exam, the IRS issued a deficiency notice, disallowing the depreciation deductions and asserting that the antenna structures should have been depreciated over 15 years under asset class 48.14, Telephone Distribution Plant 2, the cell site equipment and the leased digital equipment (other than the switch) should have been depreciated over 10 years under asset class 48.12, Telephone Central Office Equipment,3 but that RFB had properly classified the switch.

Section 167 allows a reasonable depreciation deduction for the exhaustion, wear and tear, and obsolescence of property used in a trade or business. This deduction is based on the adjusted basis of the property, as determined under section 1011. Depreciation deductions are based on the Modified Accelerated Cost Recovery System. The Treasury Secretary has the authority to prescribe class lives for each class of property. These class lives can be found in a series of revenue procedures. The revenue procedure in effect for the years at issue is Rev. Proc. 87-56, which establishes two categories of depreciable assets: (1) asset classes 00.11 through 00.4, which consist of specific assets used in all business activities (asset categories), and (2) asset classes 01.1 through 80.0, which consist of assets used in specific business activities (activity categories) based on broadly defined industry classifications. The same item of depreciable property may be described in both an asset category and an activity category, in which case the item is classified in the asset category, unless specifically excluded from the asset category or specifically included in the activity category (the "priority rule").4 Rev. Proc. 87-56 includes Telephone Communications as an activity, and includes assets identified in asset classes 48.11 through 48.14 that are used to provide commercial and contract telephone services. The various classes of telephone equipment are defined by reference to the FCC's Uniform System of Accounts for Class A and Class B Telephone Companies (USOA).

As previously noted, RFB depreciated a broad range of wireless cellular equipment as "antenna supporting structures" over seven years under asset class 48.32, the Telegraph, Ocean Cable, and Satellite Communications (TOCSC) activity category, which the IRS contended should be depreciated over 15 years under asset class 48.14. The Tax Court agreed with the IRS, holding that asset class 48.32 did not apply; the TOCSC activity category involves "domestic and international radio-telegraph, wire-telegraph, ocean-cable … [or] satellite communications services." It found that the antenna support structures were more appropriately categorized in the Telephone Communications activity category. RFB disputed this classification on the grounds that the activity category is too broad to apply to the wireless equipment at issue, and that wireless network assets are more advanced than landline telephone assets. It also asserted that wireless assets have a useful life that is "demonstrably shorter" than that of landline equipment. The Tax Court noted that RFB could not depreciate its equipment "under a class life simply because they believe it better approximates the

24

equipment's useful life." Rather, the Tax Court stated that deductions are a "matter of legislative grace," and taxpayers are "entitled to deduct only the amounts prescribed by Congress." Further, the Tax Court noted that the plain language of Rev. Proc. 87-56 is "unambiguous" - assets in the Telephone Communications activity category are used to provide commercial and contract telephonic services (which RFB provided during the years at issue). Based on this reasoning, the Tax Court concluded that the relevant asset class for the antenna support structures was asset class 48.14, with a 15-year recovery period.

RFB characterized a wide variety of cell site equipment, including the base station and the switch, under asset class 48.12 with a five-year recovery period. The IRS conceded that RFB properly classified the switch under this asset class; however, the IRS asserted that the remaining cell site equipment, including the base station, should be classified as telephone central office equipment under asset class 48.12. RFB argued that the base station should be included in asset class 48.121 because it had some of the same equipment and could perform some of the same functions as the switch. Asset classes 48.121 and 48.12 apply to telephone central office switching equipment. The main difference between the two asset classes is that asset class 48.121 "includes equipment whose functions are those of a computer or peripheral equipment." Under section 168(i)(2)(B), the term "computer" refers to a programmable electronically activated device that (1) is capable of accepting information, applying prescribed processes to the information, and supplying the results of these processes with or without human intervention, and (2) consists of a central processing unit containing extensive storage. "Related peripheral equipment" includes any equipment designed to be placed under the control of the central processing unit of a computer. In rejecting RFB's argument that the remaining cell site equipment qualified as computer equipment because it contained computerized parts, the Tax Court noted that under RFB's analysis "virtually every asset in today's increasingly computerized world would be labeled a computer." Thus, even though the remaining cell site equipment included some computerized parts, it did not constitute a computer. The Tax Court also noted that the key component of the base station and other cell site equipment was the radio, which did not employ computer processing and had functioned for many years without computerized parts. Further, the Tax Court noted that, even though the base station contained some of the same software as the switch (which was properly classified as a computer), the base station did not have the computer system or storage capacity to keep billing records. Based on this reasoning, the Tax Court found that the remaining cell site equipment, including the base station, should have been depreciated under asset class 48.12 over a 10-year recovery period. The Tax Court applied the same classification methods to various pieces of equipment that were leased by RFB.

Since the years at issue in Broz were prior to the IRS's recent guidance on wireless class lives in Rev. Proc. 2011-22, the Tax Court noted that "the Internal Revenue Service has since provided updated class life guidance for the ever-changing cellular service industry. Rev. Proc. 2011-22, 2011-18 I.R.B. 737, applies for years after the years at issue."