Embed Size (px)

Citation preview

UK residential property ownership

Hayden Bailey, Partner

2 October 2015

© Boodle Hatfield LLP. All rights reserved.

The UK’s drive to encourage “de-enveloping”

OFFSHORE COMPANY

UK RESIDENTIAL PROPERTY

© Boodle Hatfield LLP. All rights reserved.

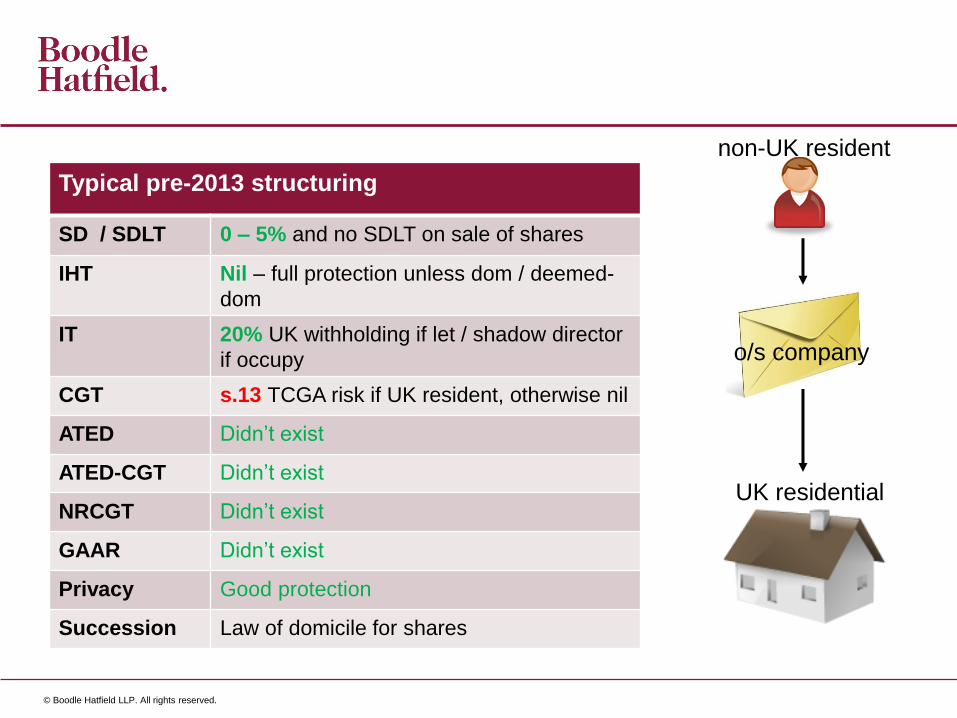

non-UK resident

Typical pre-2013 structuring

SD / SDLT 0 – 5% and no SDLT on sale of shares

IHT Nil – full protection unless dom / deemed-

dom

IT 20% UK withholding if let / shadow director

if occupy

CGT s.13 TCGA risk if UK resident, otherwise nil

ATED Didn’t exist

ATED-CGT Didn’t exist

NRCGT Didn’t exist

GAAR Didn’t exist

Privacy Good protection

Succession Law of domicile for shares

o/s company

UK residential

© Boodle Hatfield LLP. All rights reserved.

non-UK resident

o/s company

UK residential

Current and future position

SD / SDLT 12% - 15% - still no SDLT on sale of shares

IHT 40% - no protection from Apr 2017 and new

deductibility of debt rules (s.162A)

IT 20% UK withholding if let / shadow director if occupy

/ reduce by borrowing BEPS

CGT Less s.13 TCGA risk if UK resident (EU), otherwise

nil

ATED £218,200 per year + CPI (£20m+ houses) – N.B.

applies to UK companies too.

ATED-CGT 28% on gain since purchase or (if later) 1 April 2013

NRCGT 20% for gains after 5 April 2015

GAAR n/a but consider debt

Privacy Less - CRS / Beneficial ownership register

Succession Law of domicile for shares

© Boodle Hatfield LLP. All rights reserved.

NON-RESIDENT CAPITAL GAINS TAX

(“NRCGT”)

© Boodle Hatfield LLP. All rights reserved.

• NRCGT (Corporation Tax rate + indexation if seller is co) on gains on disposal

(including gifts) of an interest in UK resi property accruing post April 2015

• Rates depend upon entity being taxed (co, individual, trust)

• 3 computational methods (taxpayer’s choice):

• (a) Rebasing as at 5 April 2015 (automatic default);

• (b) No rebasing (use where the property has fallen in value); and

• (c) Straight line apportionment (useful where a property increases in value

disproportionately after 5 April 2015)

• No relief from the charge for letting the property (c.f. ATED)

• Compliance cost: “NRCGT” form on disposal even if no tax (30 days!)

• NRCGT losses only against gains of the same type (unless UK res)

• For trusts, NRCGT paid by trustees not added to stockpiled gains pool

© Boodle Hatfield LLP. All rights reserved.

HMRC FAQ’s 18 March 2015

Q20 I bought a UK residential property in 2001 whilst I was living abroad. I moved to the UK in December 2015 and sold the property at a gain in March 2018. Can I rebase to 5 April 2015?

• A20 No. UK residents are unaffected by the changes and will be subject to CGT in the normal way i.e. chargeable on the full gain less any reliefs due along with the CG annual exemption.

© Boodle Hatfield LLP. All rights reserved.

PPR reforms from 6 April 2015

• To qualify, an individual now has to be resident in the

territory where the house is or meet the day count test

• Residence in the UK is determined by the Statutory

Residence Test (SRT)

• Not a one-off test at sale. For every period post April 2015

that the new rules are not met PPR will be lost (subject to

the final 18 months applying)

• Changes only apply from 2015/16. In determining relief for

periods prior to 6 April 2015, the new rules are ignored

© Boodle Hatfield LLP. All rights reserved.

PPR new day count test

• The day count test will be met if the individual or their spouse spends at

least 90 days in the property

• A day is treated as spent in the property if an individual:

(a) is present at the house at midnight, or

(b) (i) is present in the house for some period during the day, and

(ii) The next day has stayed overnight in the house.

• Not clear what “stayed overnight” means – difficulties of ‘midnight’

• Hard to qualify if non-res because 90+ days in UK generally = UK

resident under SRT. What if exactly 90 days? (c.f. SRT more than 90

nights)

© Boodle Hatfield LLP. All rights reserved.

PPR reform

• If property owned for part year (e.g. year of purchase or

sale) day count requirement reduced proportionately

• Where more than one property in the territory, the 90 day

test can be spread across both (or all of) those properties

• Your spouse occupies the UK property - so you qualify for

PPR and you may keep your non-UK resident status –

consider trust claims (s.225) where spouse not beneficiary.

• Evidential difficulties around occupation (record keeping)

• Use of elections – elect at time of disposal (no time limit)

© Boodle Hatfield LLP. All rights reserved.

HMRC FAQ’s 18 March 2015

• Q11 I lived in the property for 20 years before leaving the UK in 2010 and had met all the conditions for PRR up to that date. Does this mean if I sell the property by 5 October 2016 there will be no CGT liability?

• A11 Yes. If you can identify a time prior to 6 April 2015 that the property qualified for PRR then final period relief will be available i.e. the last 18 months of ownership will be eligible for relief.

© Boodle Hatfield LLP. All rights reserved.

ANNUAL TAX ON ENVELOPED DWELLINGS

(“ATED”)

© Boodle Hatfield LLP. All rights reserved.

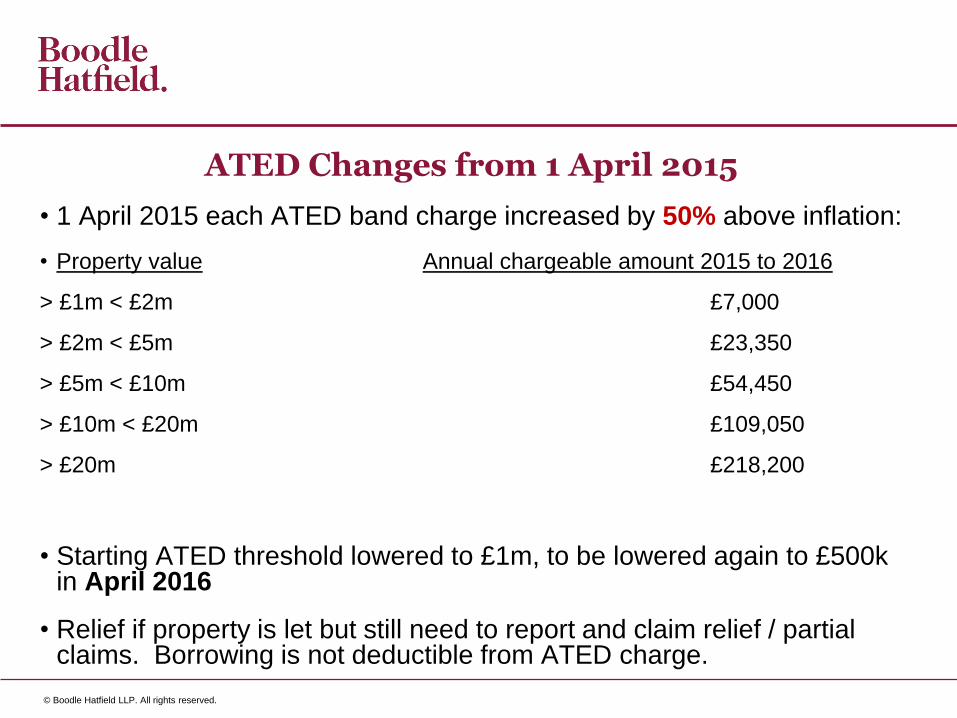

ATED Changes from 1 April 2015

• 1 April 2015 each ATED band charge increased by 50% above inflation:

• Property value Annual chargeable amount 2015 to 2016

> £1m < £2m £7,000

> £2m < £5m £23,350

> £5m < £10m £54,450

> £10m < £20m £109,050

> £20m £218,200

• Starting ATED threshold lowered to £1m, to be lowered again to £500k in April 2016

• Relief if property is let but still need to report and claim relief / partial claims. Borrowing is not deductible from ATED charge.

© Boodle Hatfield LLP. All rights reserved.

ATED-related CGT

• 28% rate with no indexation allowance

• Takes priority over NRCGT (which would be at 20% if company)

• UK and non-UK companies

• Reliefs against charge same as main ATED and similar to SDLT

• Valuation date at April 2012 – next valuation date April 2017

• Value threshold lowers to £500k from April 2016 = very low!

• Situations can arise where ATED-CGT, NRCGT and CGT apply!

© Boodle Hatfield LLP. All rights reserved.

STAMP DUTY LAND TAX

(“SDLT”)

© Boodle Hatfield LLP. All rights reserved.

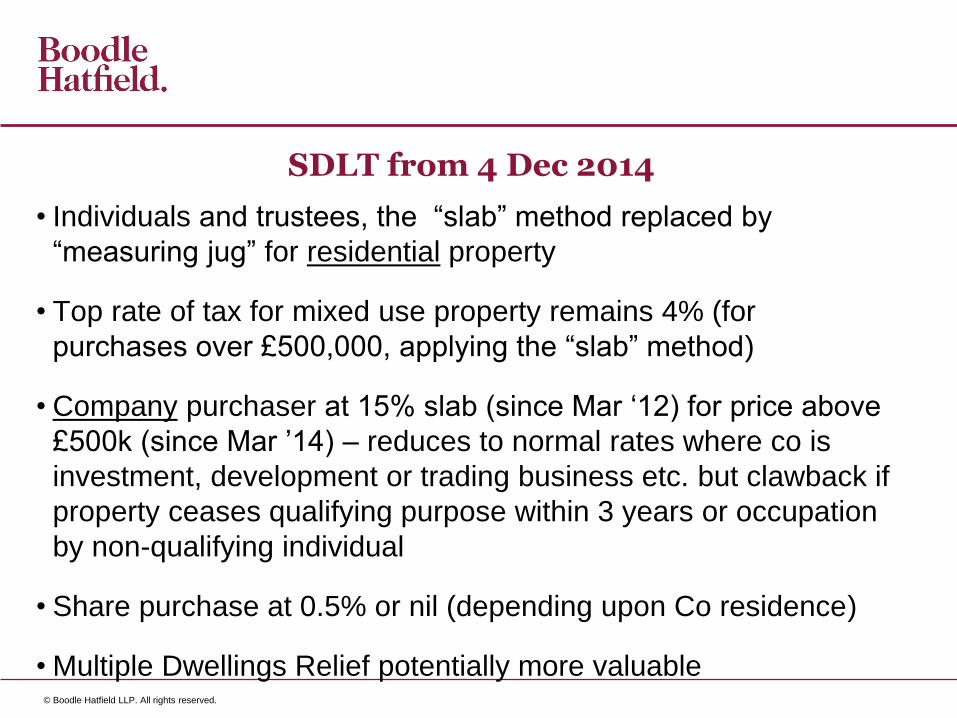

SDLT from 4 Dec 2014

• Individuals and trustees, the “slab” method replaced by

“measuring jug” for residential property

• Top rate of tax for mixed use property remains 4% (for

purchases over £500,000, applying the “slab” method)

• Company purchaser at 15% slab (since Mar ‘12) for price above

£500k (since Mar ’14) – reduces to normal rates where co is

investment, development or trading business etc. but clawback if

property ceases qualifying purpose within 3 years or occupation

by non-qualifying individual

• Share purchase at 0.5% or nil (depending upon Co residence)

• Multiple Dwellings Relief potentially more valuable

© Boodle Hatfield LLP. All rights reserved.

SDLT from 4 Dec 2014

Property purchase price SDLT rate

Up to £125,000 0%

The next £125,000 (the portion from £125,001 to £250,000) 2%

The next £675,000 (the portion from £250,001 to £925,000) 5%

The next £575,000 (the portion from £925,001 to £1.5 million) 10%

The remaining amount (the portion above £1.5 million) 12%

© Boodle Hatfield LLP. All rights reserved.

REVIEW EXISTING ARRANGEMENTS

© Boodle Hatfield LLP. All rights reserved.

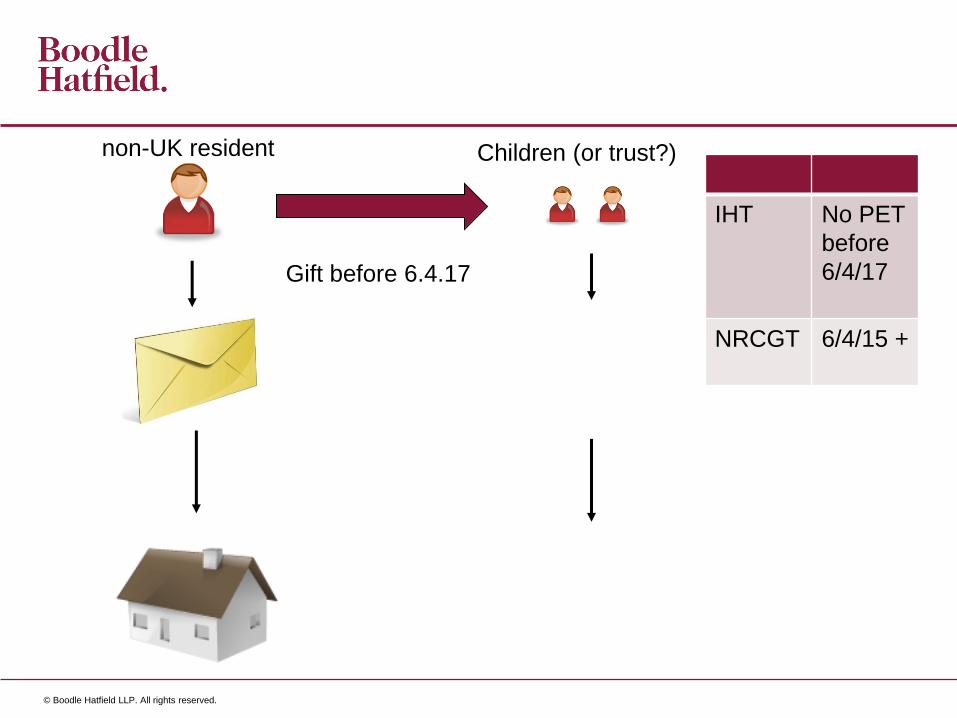

non-UK resident

IHT No PET

before

6/4/17

NRCGT 6/4/15 +

Children (or trust?)

Gift before 6.4.17

© Boodle Hatfield LLP. All rights reserved.

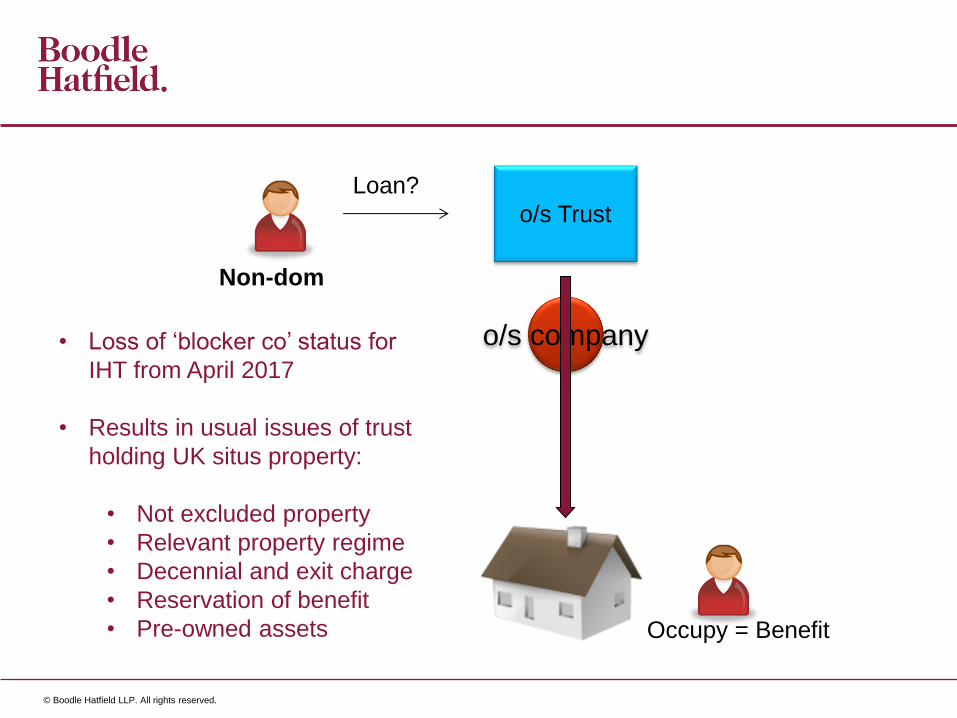

Non-dom

o/s Trust

Occupy = Benefit

o/s company

Loan?

• Loss of ‘blocker co’ status for

IHT from April 2017

• Results in usual issues of trust

holding UK situs property:

• Not excluded property

• Relevant property regime

• Decennial and exit charge

• Reservation of benefit

• Pre-owned assets

© Boodle Hatfield LLP. All rights reserved.

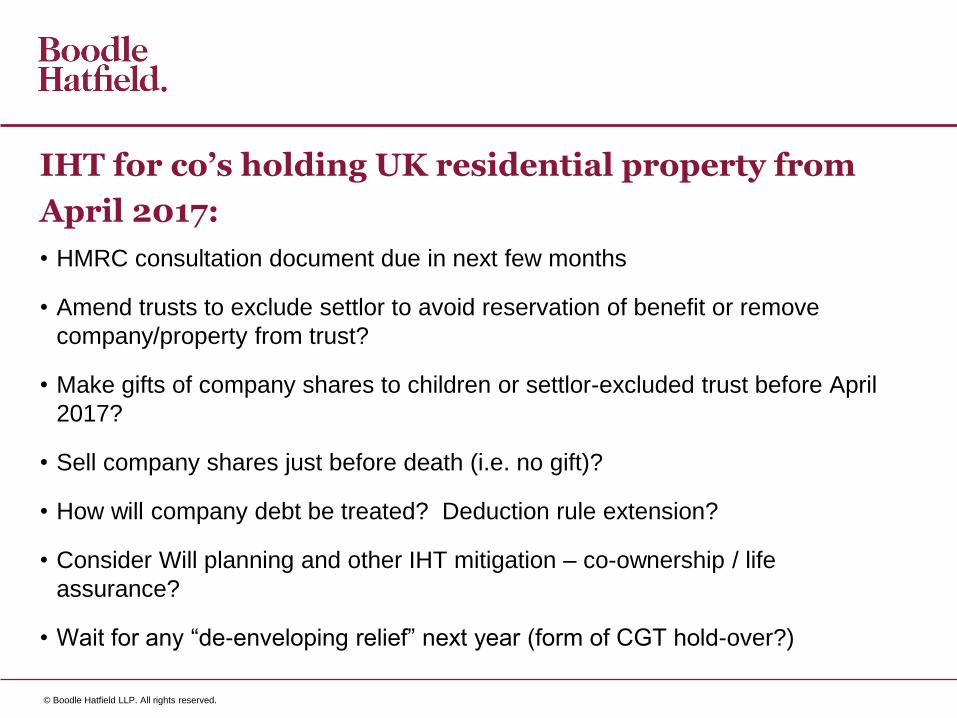

IHT for co’s holding UK residential property from

April 2017:

• HMRC consultation document due in next few months

• Amend trusts to exclude settlor to avoid reservation of benefit or remove

company/property from trust?

• Make gifts of company shares to children or settlor-excluded trust before April

2017?

• Sell company shares just before death (i.e. no gift)?

• How will company debt be treated? Deduction rule extension?

• Consider Will planning and other IHT mitigation – co-ownership / life

assurance?

• Wait for any “de-enveloping relief” next year (form of CGT hold-over?)

© Boodle Hatfield LLP. All rights reserved.

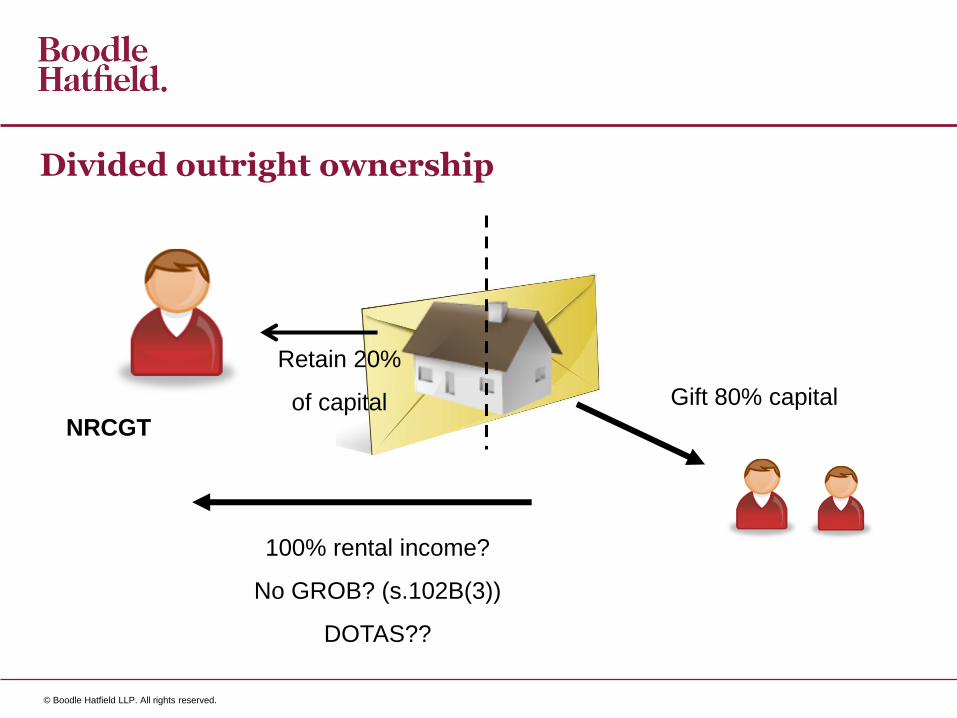

Divided outright ownership

Retain 20%

of capital Gift 80% capital

100% rental income?

No GROB? (s.102B(3))

DOTAS??

NRCGT

© Boodle Hatfield LLP. All rights reserved.

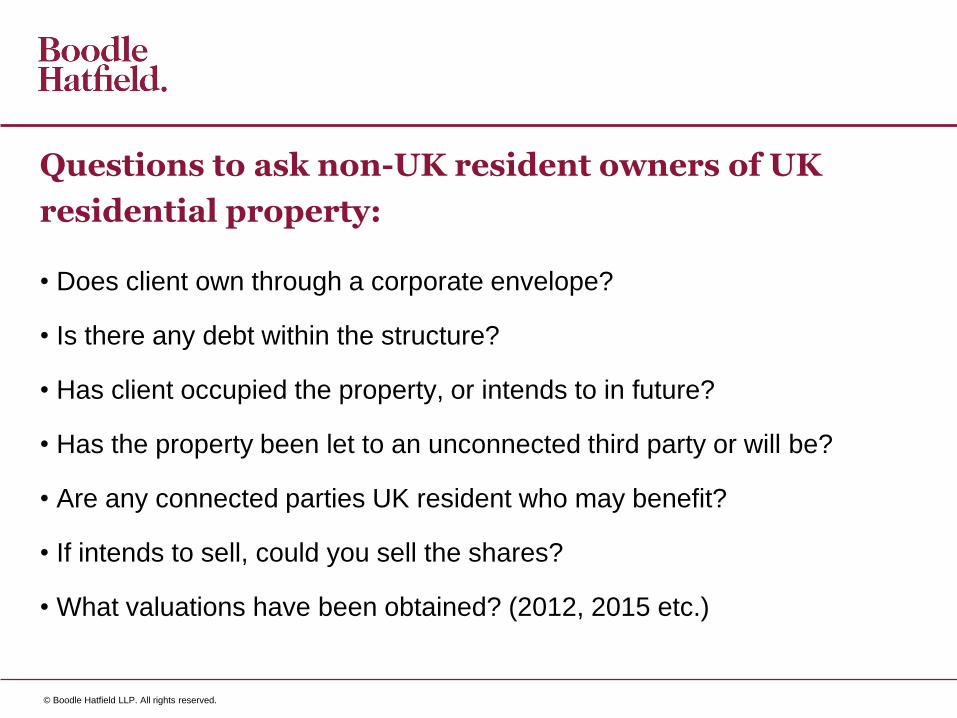

Questions to ask non-UK resident owners of UK

residential property:

• Does client own through a corporate envelope?

• Is there any debt within the structure?

• Has client occupied the property, or intends to in future?

• Has the property been let to an unconnected third party or will be?

• Are any connected parties UK resident who may benefit?

• If intends to sell, could you sell the shares?

• What valuations have been obtained? (2012, 2015 etc.)

© Boodle Hatfield LLP. All rights reserved.

If sell the shares:

•No ATED CGT

•No Non-res CGT

•No UK Corporation Tax

•No SDLT for buyer

•Buyer retains IT benefits

If company sells the property:

•Non-res CGT at 20% from 6 April ‘15

© Boodle Hatfield LLP. All rights reserved.

NEW PURCHASES

© Boodle Hatfield LLP. All rights reserved.

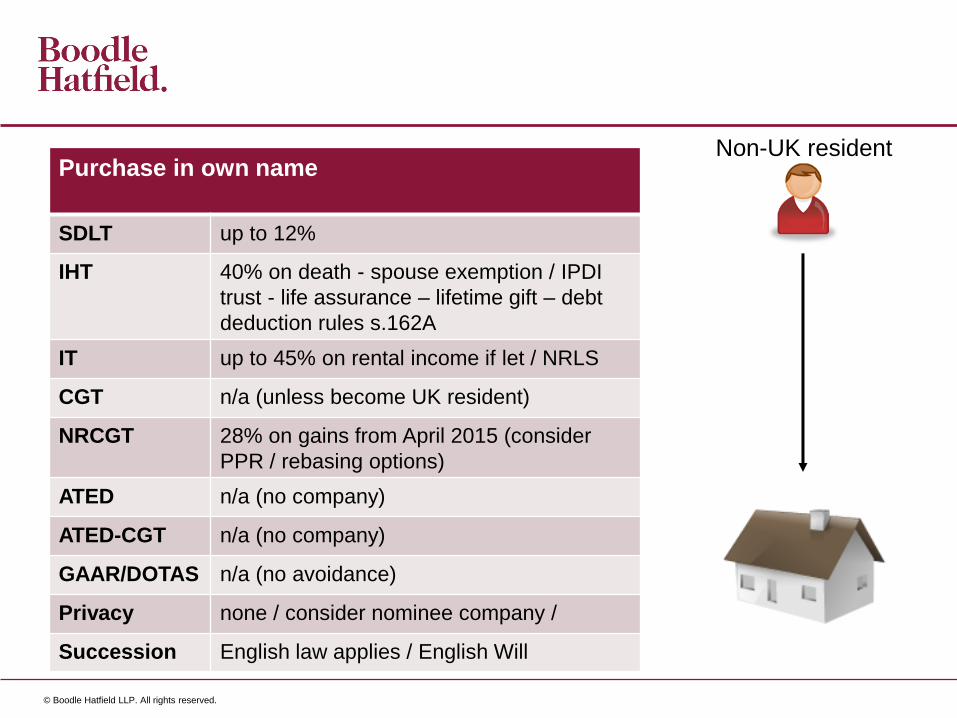

Non-UK resident Purchase in own name

SDLT up to 12%

IHT 40% on death - spouse exemption / IPDI

trust - life assurance – lifetime gift – debt

deduction rules s.162A

IT up to 45% on rental income if let / NRLS

CGT n/a (unless become UK resident)

NRCGT 28% on gains from April 2015 (consider

PPR / rebasing options)

ATED n/a (no company)

ATED-CGT n/a (no company)

GAAR/DOTAS n/a (no avoidance)

Privacy none / consider nominee company /

Succession English law applies / English Will

© Boodle Hatfield LLP. All rights reserved.

Non-dom

o/s Trust

Loan?

UK res ?

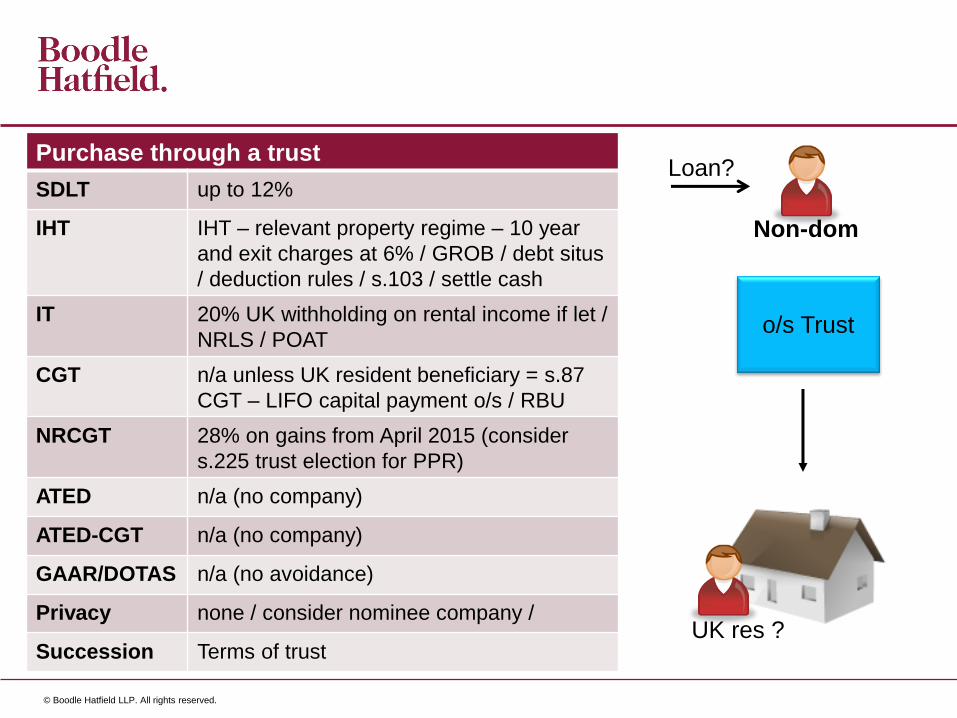

Purchase through a trust

SDLT up to 12%

IHT IHT – relevant property regime – 10 year

and exit charges at 6% / GROB / debt situs

/ deduction rules / s.103 / settle cash

IT 20% UK withholding on rental income if let /

NRLS / POAT

CGT n/a unless UK resident beneficiary = s.87

CGT – LIFO capital payment o/s / RBU

NRCGT 28% on gains from April 2015 (consider

s.225 trust election for PPR)

ATED n/a (no company)

ATED-CGT n/a (no company)

GAAR/DOTAS n/a (no avoidance)

Privacy none / consider nominee company /

Succession Terms of trust

© Boodle Hatfield LLP. All rights reserved.

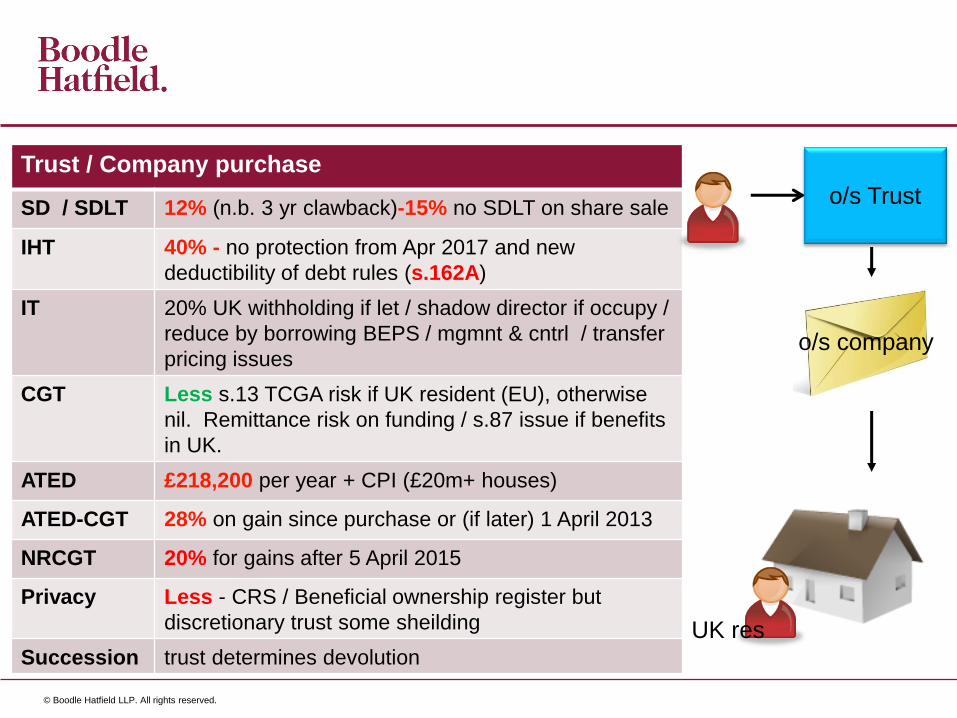

Trust / Company purchase

SD / SDLT 12% (n.b. 3 yr clawback)-15% no SDLT on share sale

IHT 40% - no protection from Apr 2017 and new

deductibility of debt rules (s.162A)

IT 20% UK withholding if let / shadow director if occupy /

reduce by borrowing BEPS / mgmnt & cntrl / transfer

pricing issues

CGT Less s.13 TCGA risk if UK resident (EU), otherwise

nil. Remittance risk on funding / s.87 issue if benefits

in UK.

ATED £218,200 per year + CPI (£20m+ houses)

ATED-CGT 28% on gain since purchase or (if later) 1 April 2013

NRCGT 20% for gains after 5 April 2015

Privacy Less - CRS / Beneficial ownership register but

discretionary trust some sheilding

Succession trust determines devolution

o/s Trust

UK res

o/s company

© Boodle Hatfield LLP. All rights reserved.

OWNER OCCUPIER

© Boodle Hatfield LLP. All rights reserved.

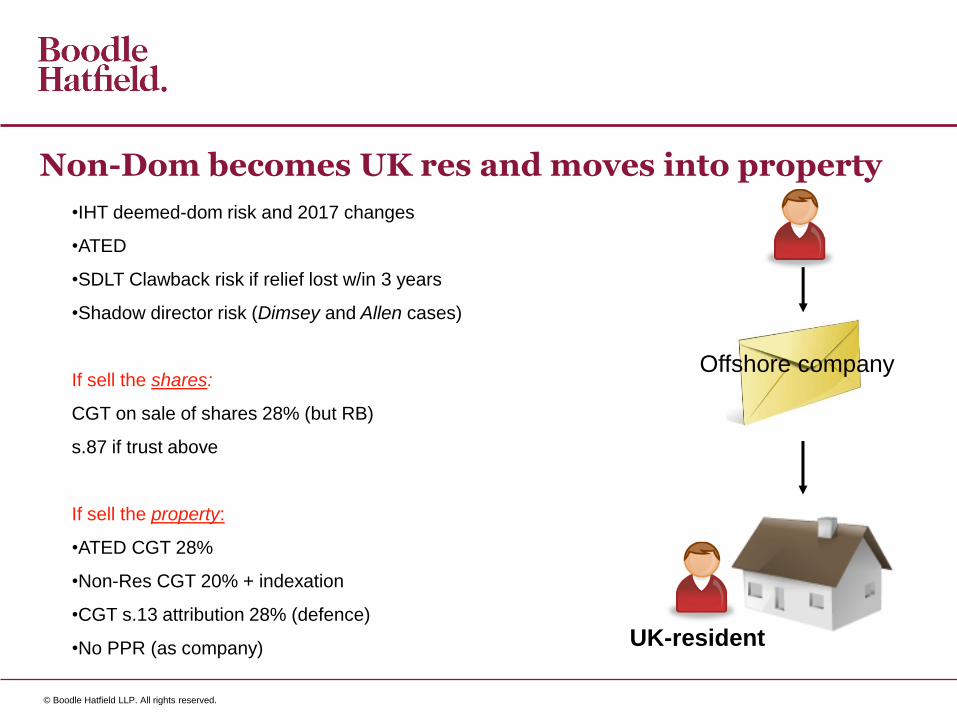

Non-Dom becomes UK res and moves into property

•IHT deemed-dom risk and 2017 changes

•ATED

•SDLT Clawback risk if relief lost w/in 3 years

•Shadow director risk (Dimsey and Allen cases)

If sell the shares:

CGT on sale of shares 28% (but RB)

s.87 if trust above

If sell the property:

•ATED CGT 28%

•Non-Res CGT 20% + indexation

•CGT s.13 attribution 28% (defence)

•No PPR (as company) UK-resident

Offshore company

© Boodle Hatfield LLP. All rights reserved.

COMMERCIAL / AGRICULTURAL

© Boodle Hatfield LLP. All rights reserved.

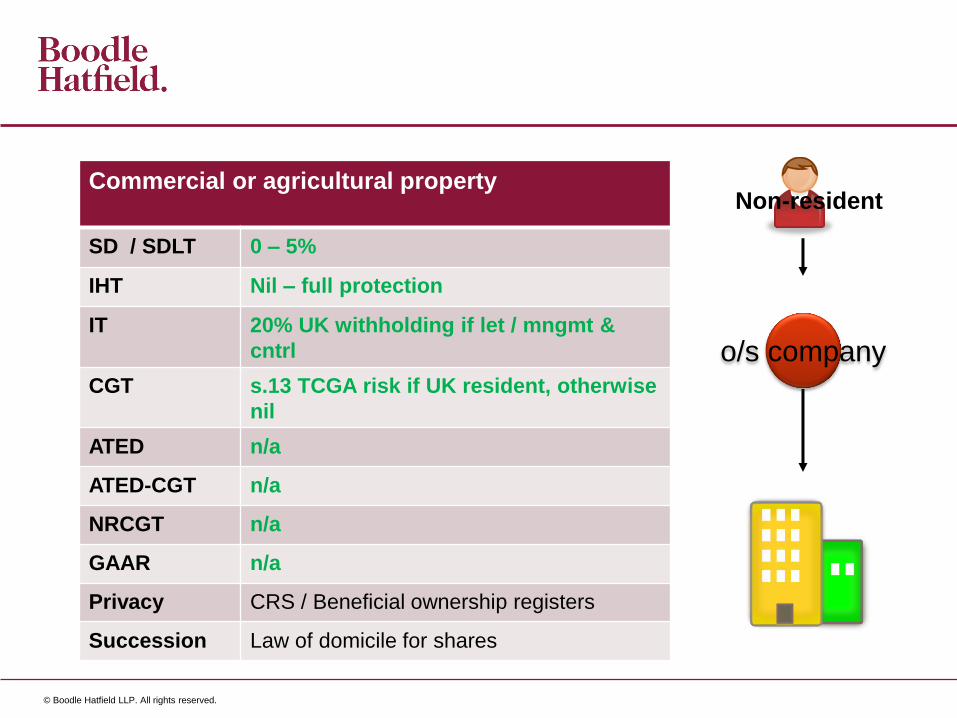

Non-resident Commercial or agricultural property

SD / SDLT 0 – 5%

IHT Nil – full protection

IT 20% UK withholding if let / mngmt &

cntrl

CGT s.13 TCGA risk if UK resident, otherwise

nil

ATED n/a

ATED-CGT n/a

NRCGT n/a

GAAR n/a

Privacy CRS / Beneficial ownership registers

Succession Law of domicile for shares

o/s company

Hayden Bailey, Partner

13 May 2015