Embed Size (px)

Citation preview

Berlin | Frankfurt a. M. | München

www.pplaw.com

Tax Aspects of cross-border M&A-transactions

IAP International

Associate

Programm

Munich, 2 July 2018

2

OVERVIEW

FIRST PART: CROSS-BORDER M&A: GENERAL STRUCTURES

SECOND PART: POST ACQUISITION STUCTURING

3

FIRST PART:

CROSS-BORDER M&A: GENERAL STRUCTURES

4

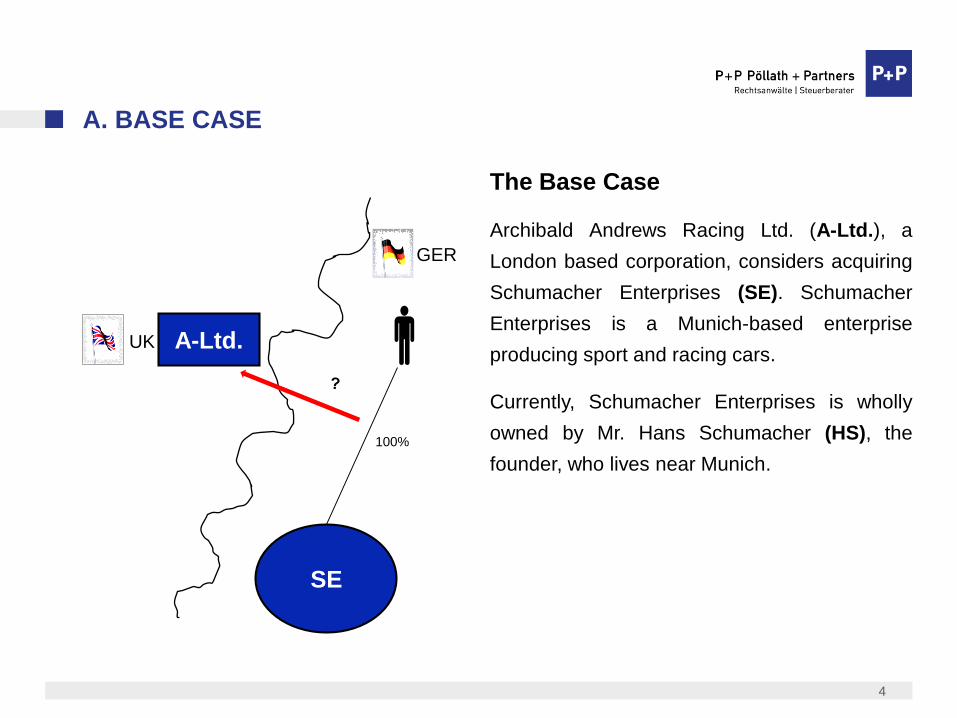

A. BASE CASE

The Base Case

Archibald Andrews Racing Ltd. (A-Ltd.), a

London based corporation, considers acquiring

Schumacher Enterprises (SE). Schumacher

Enterprises is a Munich-based enterprise

producing sport and racing cars.

Currently, Schumacher Enterprises is wholly

owned by Mr. Hans Schumacher (HS), the

founder, who lives near Munich.

A-Ltd.

GER

SE

100%

UK

5

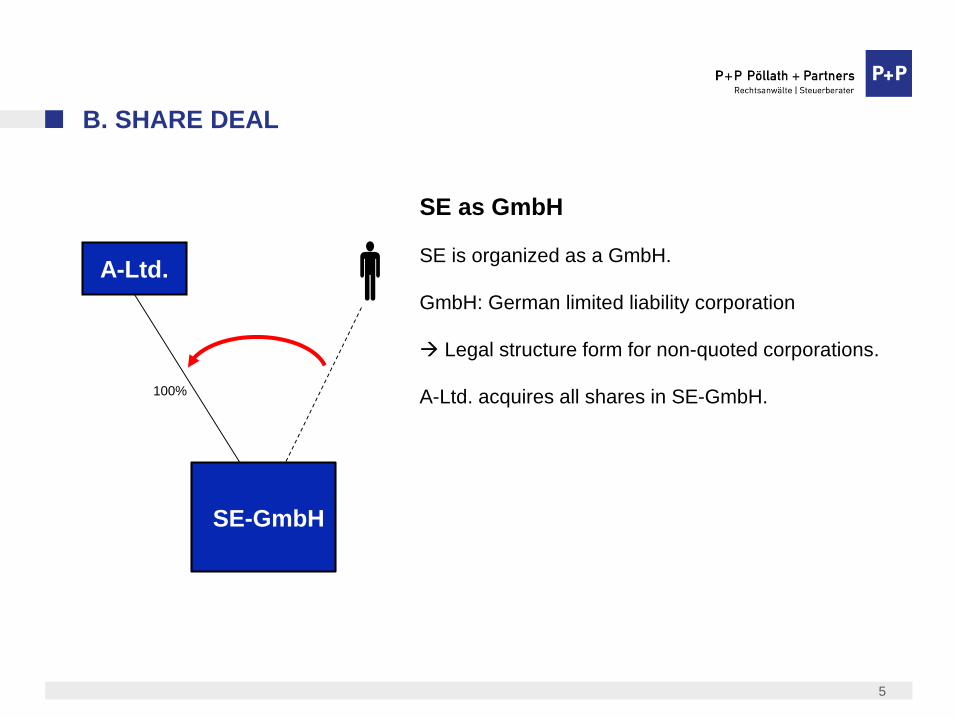

B. SHARE DEAL

SE as GmbH

SE is organized as a GmbH.

GmbH: German limited liability corporation

Legal structure form for non-quoted corporations.

A-Ltd. acquires all shares in SE-GmbH.

A-Ltd.

SE-GmbH

100%

6

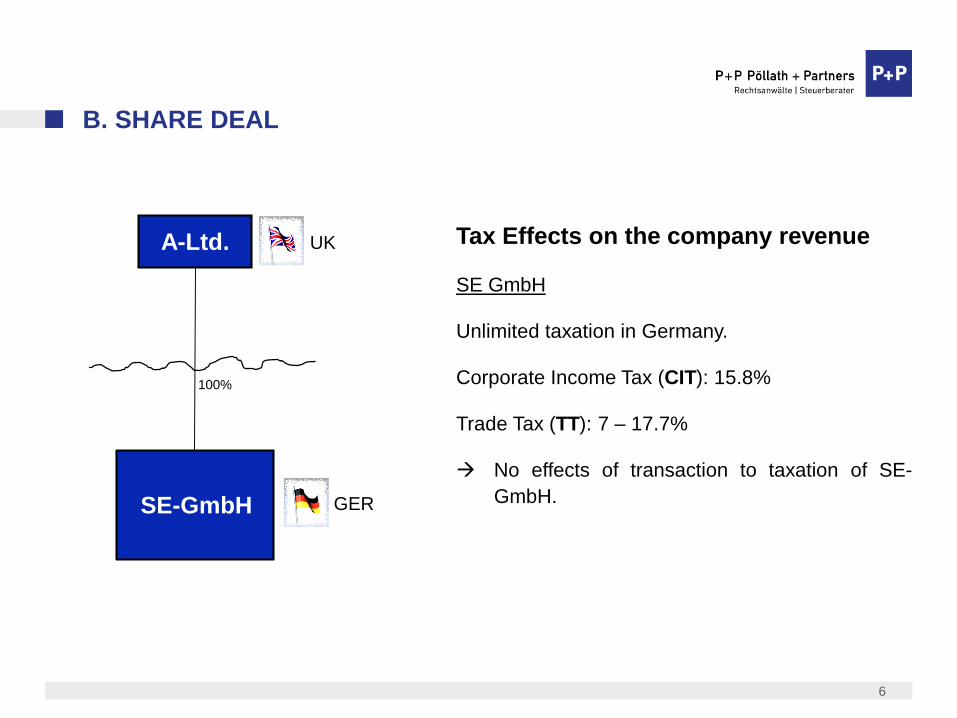

B. SHARE DEAL

Tax Effects on the company revenue

SE GmbH

Unlimited taxation in Germany.

Corporate Income Tax (CIT): 15.8%

Trade Tax (TT): 7 – 17.7%

No effects of transaction to taxation of SE-

GmbH.

A-Ltd.

GERSE-GmbH

100%

UK

7

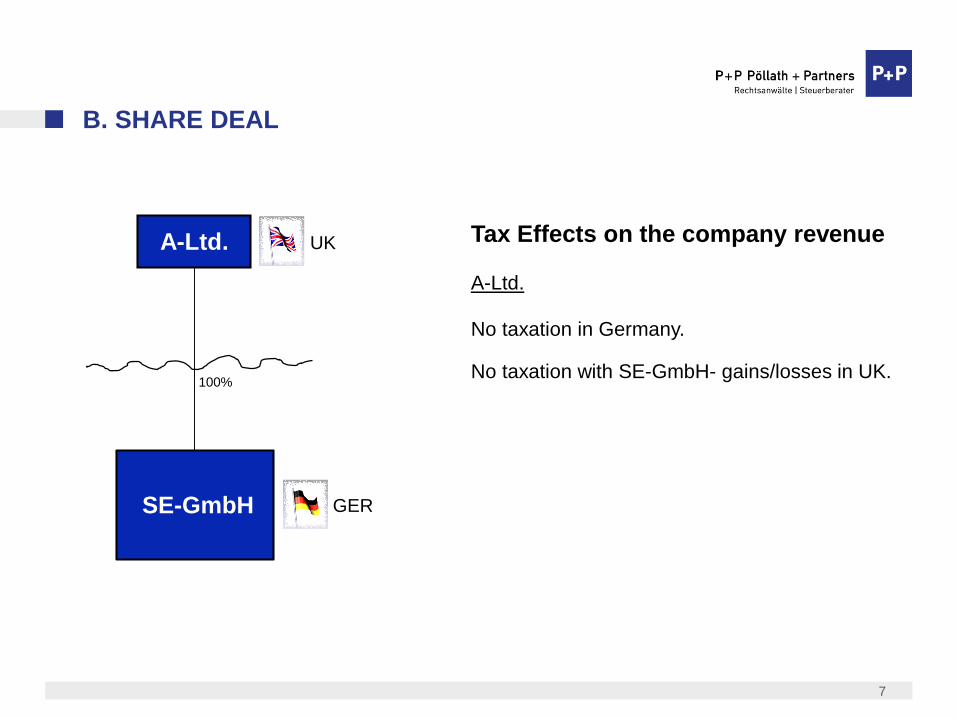

B. SHARE DEAL

Tax Effects on the company revenue

A-Ltd.

No taxation in Germany.

No taxation with SE-GmbH- gains/losses in UK.

A-Ltd.

GERSE-GmbH

100%

UK

8

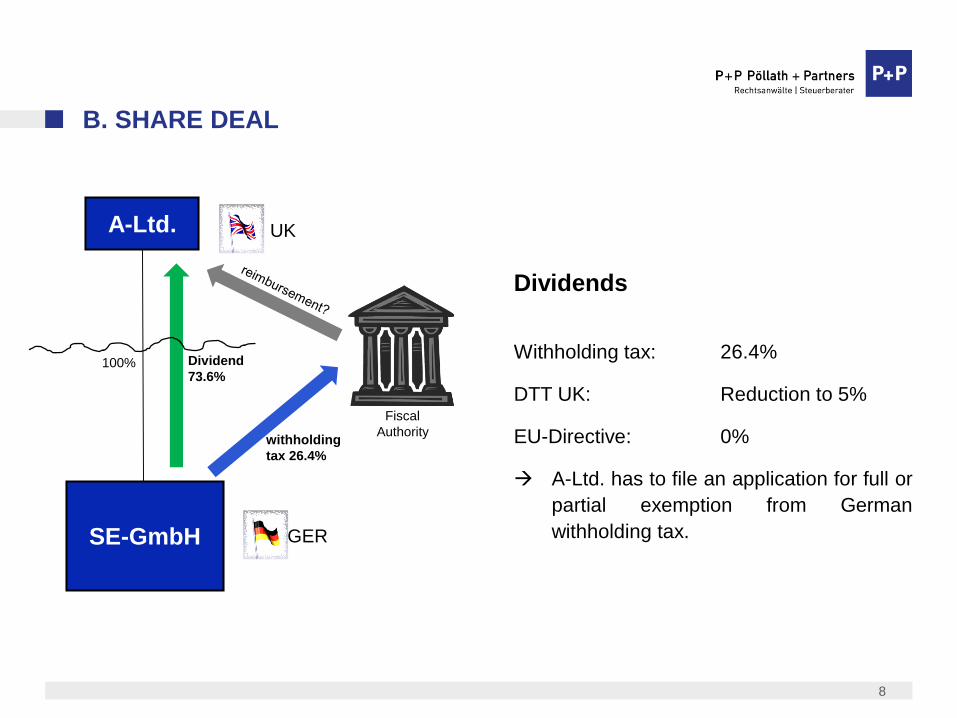

B. SHARE DEAL

Dividends

Withholding tax: 26.4%

DTT UK: Reduction to 5%

EU-Directive: 0%

A-Ltd. has to file an application for full or

partial exemption from German

withholding tax.

A-Ltd.

GERSE-GmbH

100% Dividend

73.6%

Fiscal

Authoritywithholding

tax 26.4%

UK

9

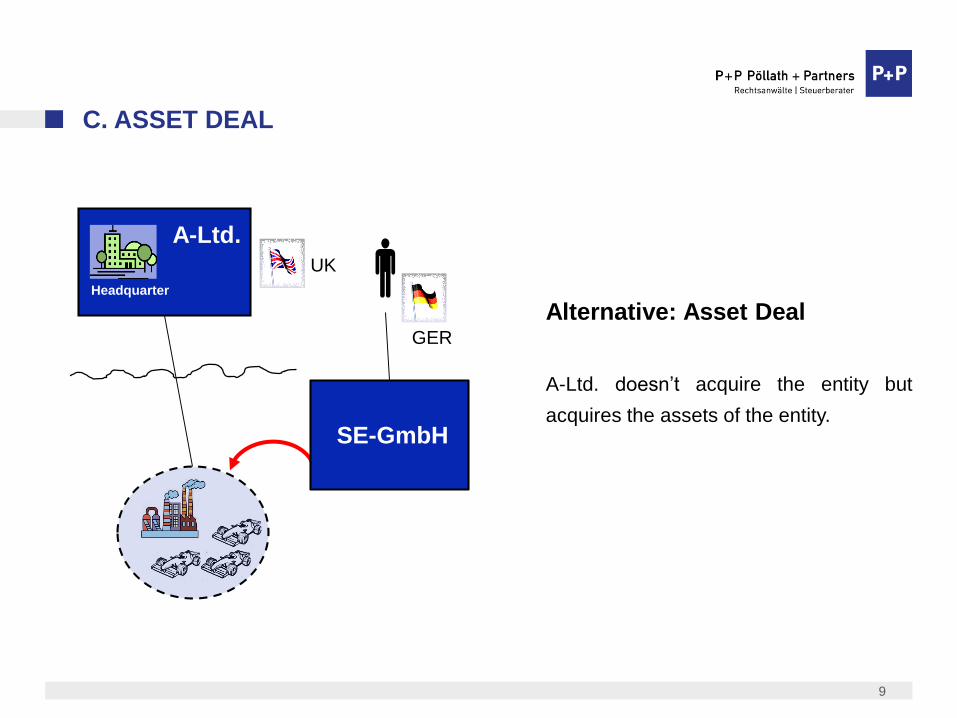

C. ASSET DEAL

Alternative: Asset Deal

A-Ltd. doesn’t acquire the entity but

acquires the assets of the entity.

GER

UK

A-Ltd.

Headquarter

SE-GmbH

10

C. ASSET DEAL

Tax Effects

Permanent establishment in Germany.

PE-income taxable in Germa-ny.

GER

UK

A-Ltd.

Headquarter

11

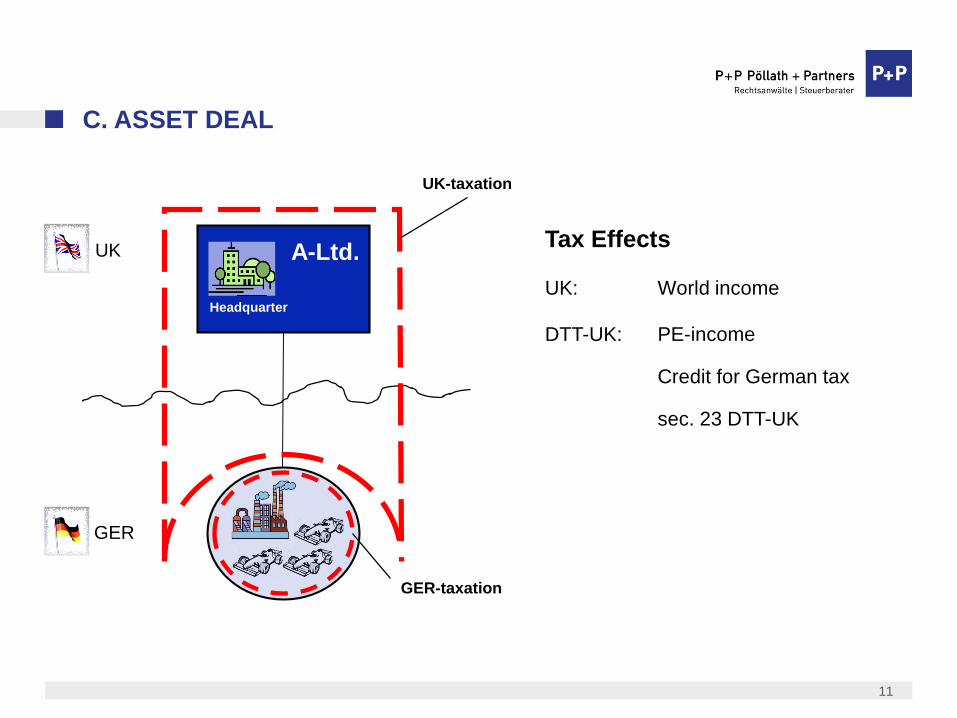

C. ASSET DEAL

Tax Effects

UK: World income

DTT-UK: PE-income

Credit for German tax

sec. 23 DTT-UK

GER

GER-taxation

UK-taxation

UK A-Ltd.

Headquarter

12

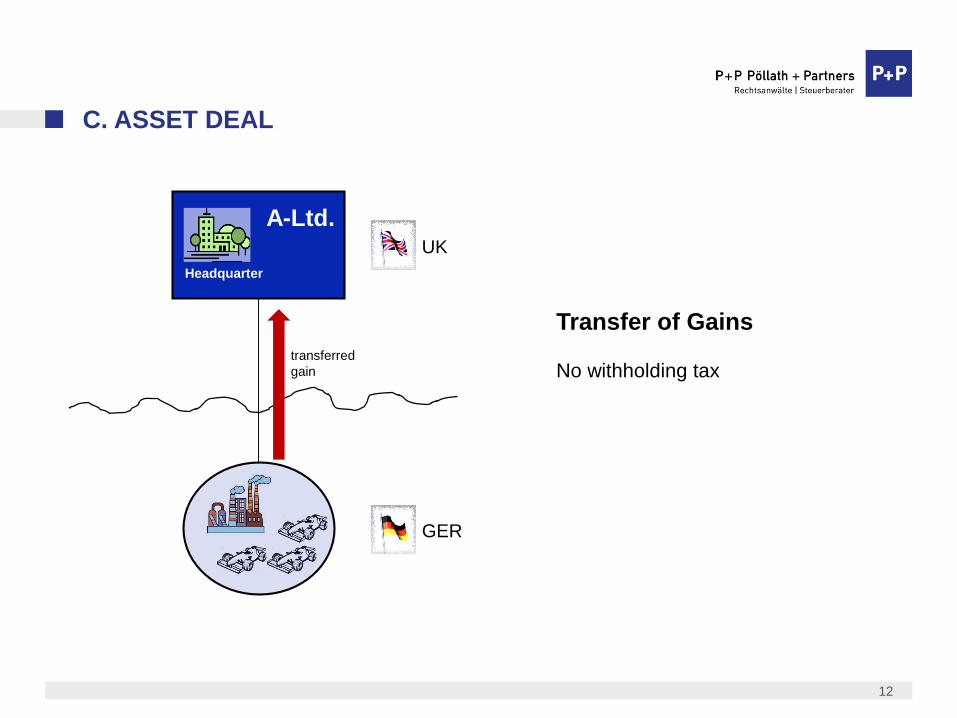

C. ASSET DEAL

Transfer of Gains

No withholding tax

GER

transferred

gain

UK

A-Ltd.

Headquarter

13

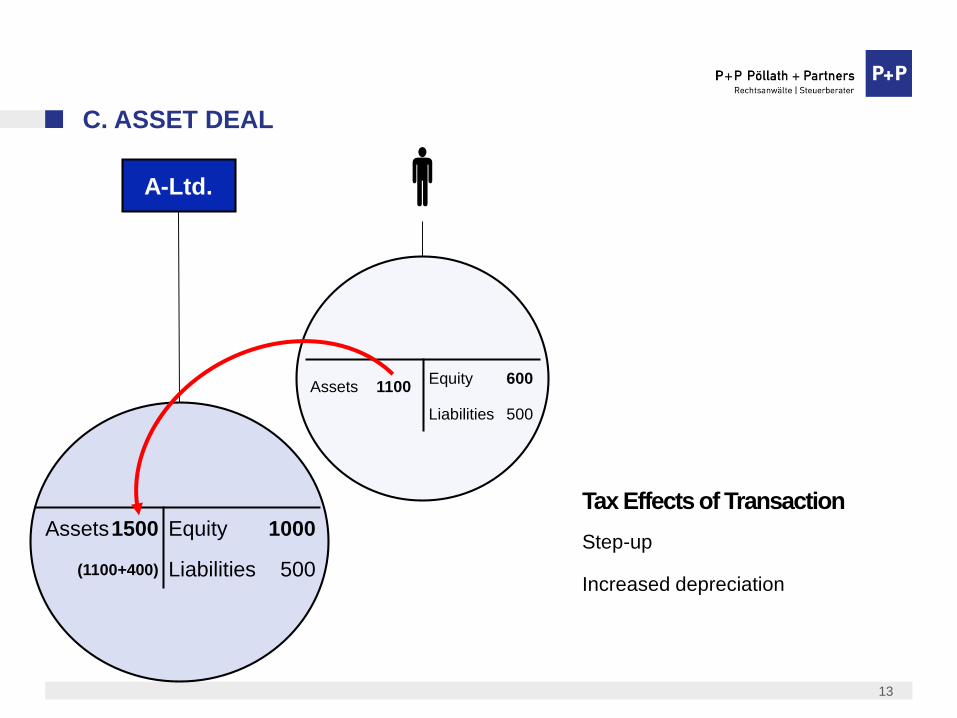

C. ASSET DEAL

A-Ltd.

Assets1500

(1100+400)

Equity 1000

Liabilities 500

Assets 1100Equity 600

Liabilities 500

Tax Effects of Transaction

Step-up

Increased depreciation

14

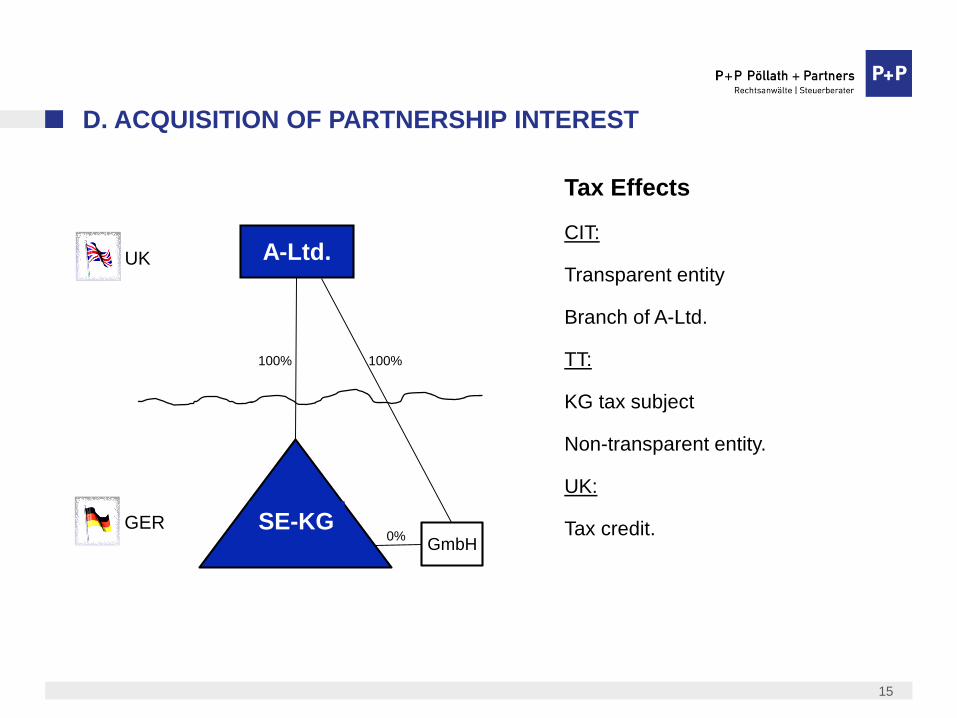

D. ACQUISITION OF PARTNERSHIP INTEREST

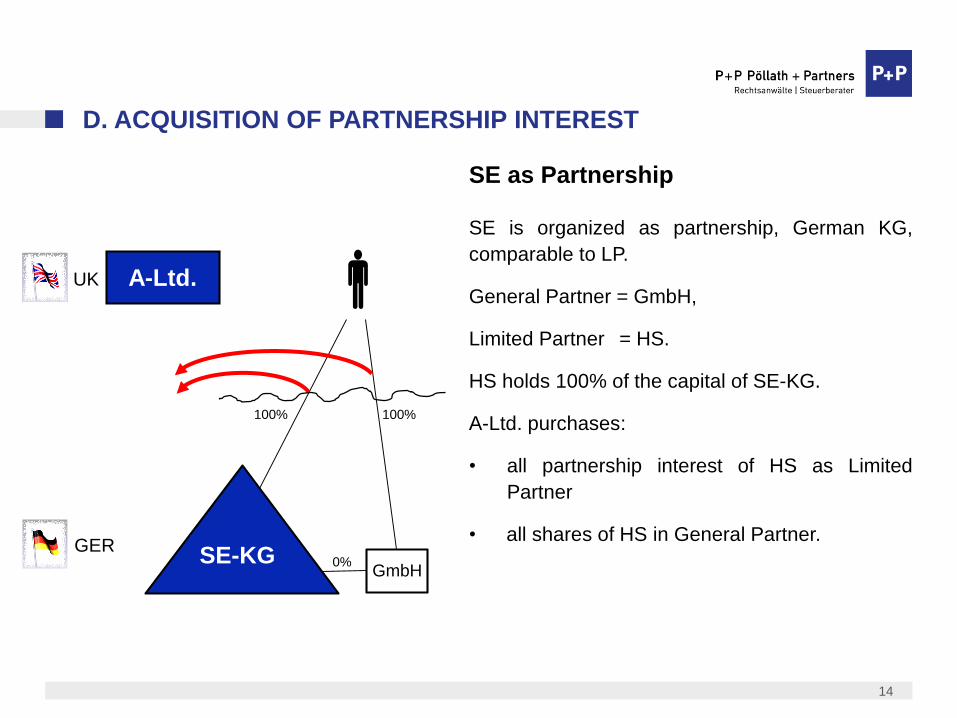

SE as Partnership

SE is organized as partnership, German KG,

comparable to LP.

General Partner = GmbH,

Limited Partner = HS.

HS holds 100% of the capital of SE-KG.

A-Ltd. purchases:

• all partnership interest of HS as Limited

Partner

• all shares of HS in General Partner.

A-Ltd.

GER

SE-KG

UK

0%

100%100%

GmbH

15

D. ACQUISITION OF PARTNERSHIP INTEREST

Tax Effects

CIT:

Transparent entity

Branch of A-Ltd.

TT:

KG tax subject

Non-transparent entity.

UK:

Tax credit.

A-Ltd.

GER SE-KG

UK

0%

100%100%

GmbH

16

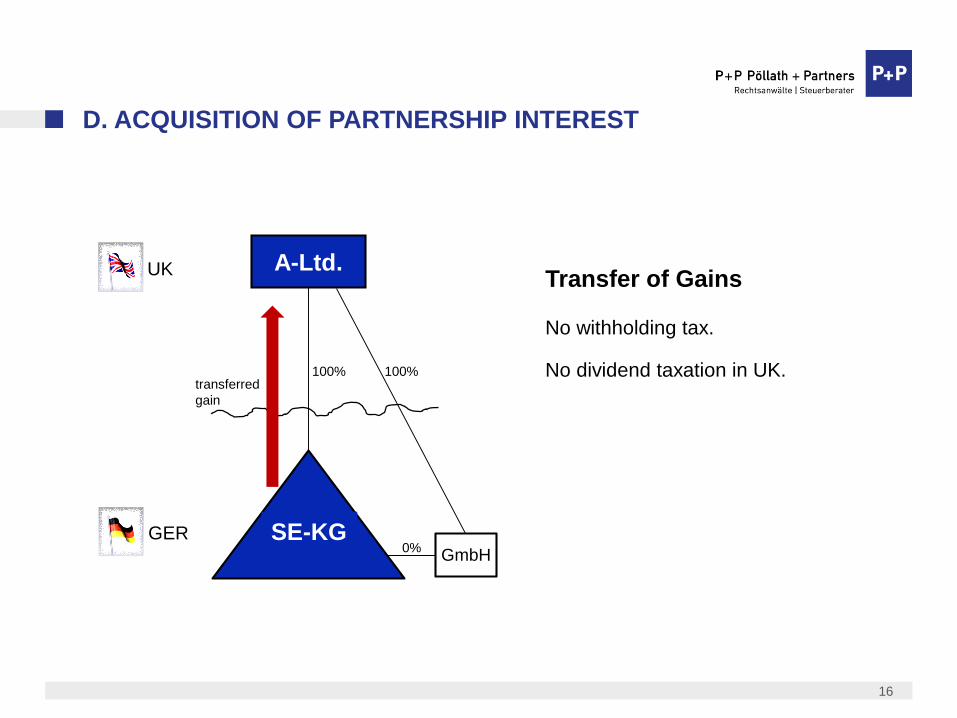

D. ACQUISITION OF PARTNERSHIP INTEREST

Transfer of Gains

No withholding tax.

No dividend taxation in UK.

A-Ltd.

GER SE-KG

UK

0%

100%100%transferred

gain

GmbH

17

D. ACQUISITION OF PARTNERSHIP INTEREST

A-Ltd.

GER

UK

100%

1100

Assets 1500

600

Equity 1000

Liabilities 500

Tax Effects of Trans-action

CIT

Step-up (like asset deal)

TT

Step-up

Trade Tax on gain of HS born by KG!

GmbH

18

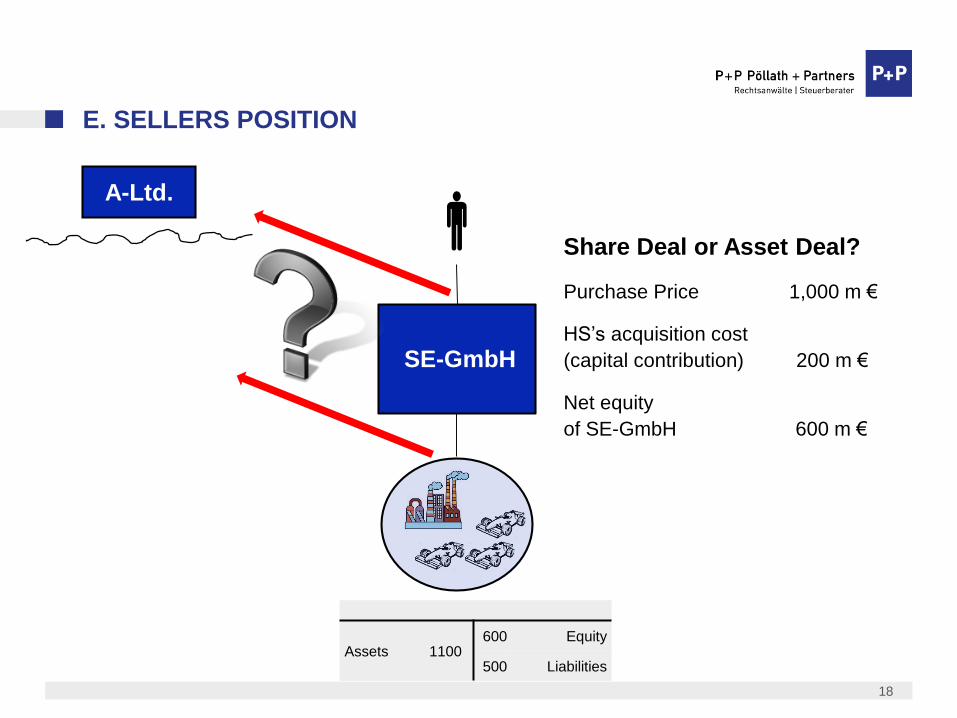

E. SELLERS POSITION

Assets 1100600 Equity

500 Liabilities

Share Deal or Asset Deal?

Purchase Price 1,000 m €

HS’s acquisition cost

(capital contribution) 200 m €

Net equity

of SE-GmbH 600 m €

A-Ltd.

SE-GmbH

19

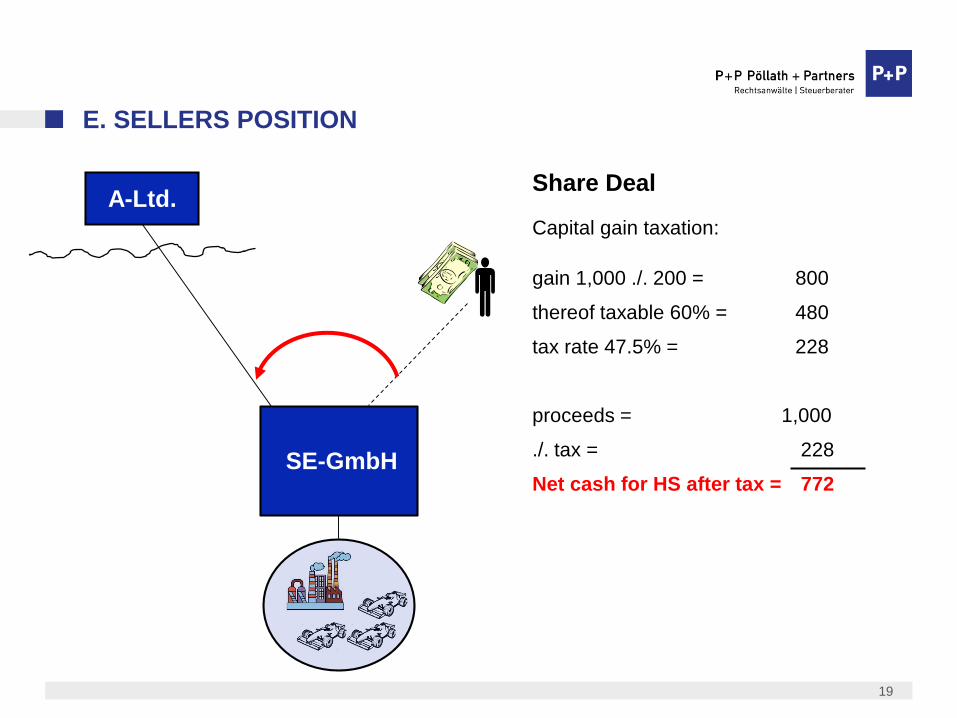

E. SELLERS POSITION

Share Deal

Capital gain taxation:

gain 1,000 ./. 200 = 800

thereof taxable 60% = 480

tax rate 47.5% = 228

proceeds = 1,000

./. tax = 228

Net cash for HS after tax = 772

SE-GmbH

A-Ltd.

20

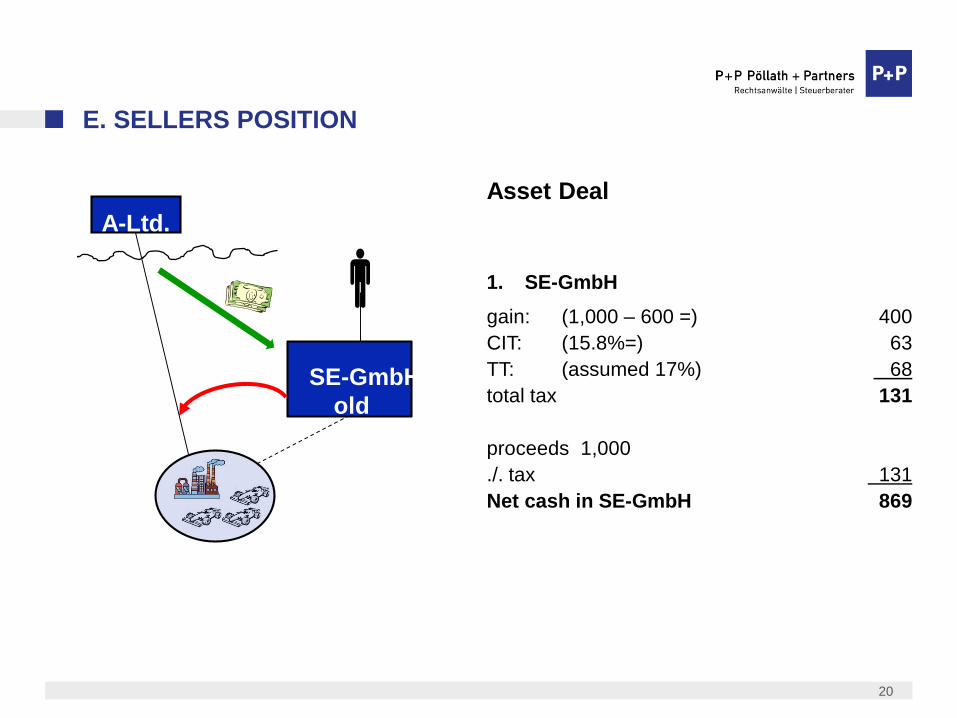

E. SELLERS POSITION

Asset Deal

1. SE-GmbH

gain: (1,000 – 600 =) 400

CIT: (15.8%=) 63

TT: (assumed 17%) 68

total tax 131

proceeds 1,000

./. tax 131

Net cash in SE-GmbH 869

SE-GmbH

old

A-Ltd.

21

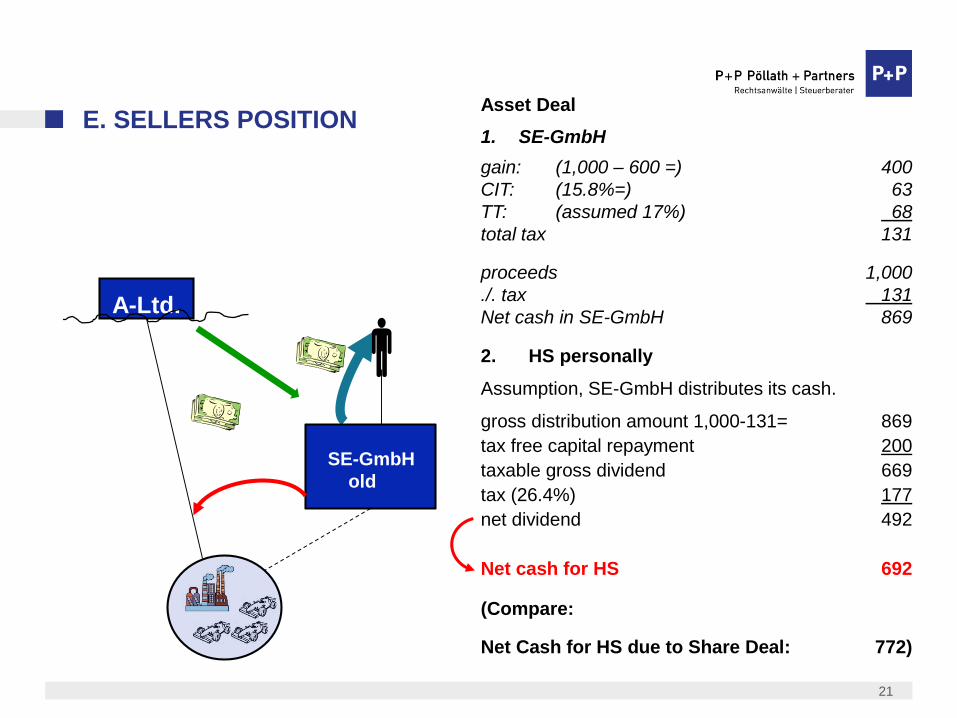

E. SELLERS POSITIONAsset Deal

1. SE-GmbH

gain: (1,000 – 600 =) 400

CIT: (15.8%=) 63

TT: (assumed 17%) 68

total tax 131

proceeds 1,000

./. tax 131

Net cash in SE-GmbH 869

2. HS personally

Assumption, SE-GmbH distributes its cash.

gross distribution amount 1,000-131= 869

tax free capital repayment 200

taxable gross dividend 669

tax (26.4%) 177

net dividend 492

Net cash for HS 692

(Compare:

Net Cash for HS due to Share Deal: 772)

SE-GmbH

old

A-Ltd.

22

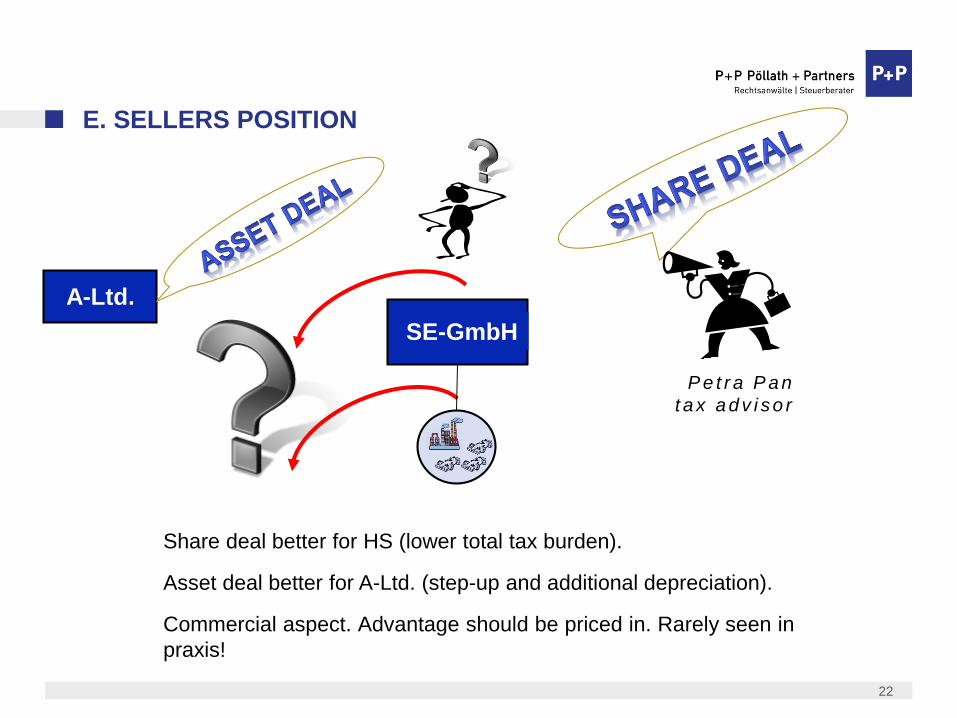

E. SELLERS POSITION

A-Ltd.

SE-GmbH

Share deal better for HS (lower total tax burden).

Asset deal better for A-Ltd. (step-up and additional depreciation).

Commercial aspect. Advantage should be priced in. Rarely seen in

praxis!

P e t r a P a n

t a x a d v i s o r

23

SECOND PART:

POST ACQUISITION STRUCTURING

24

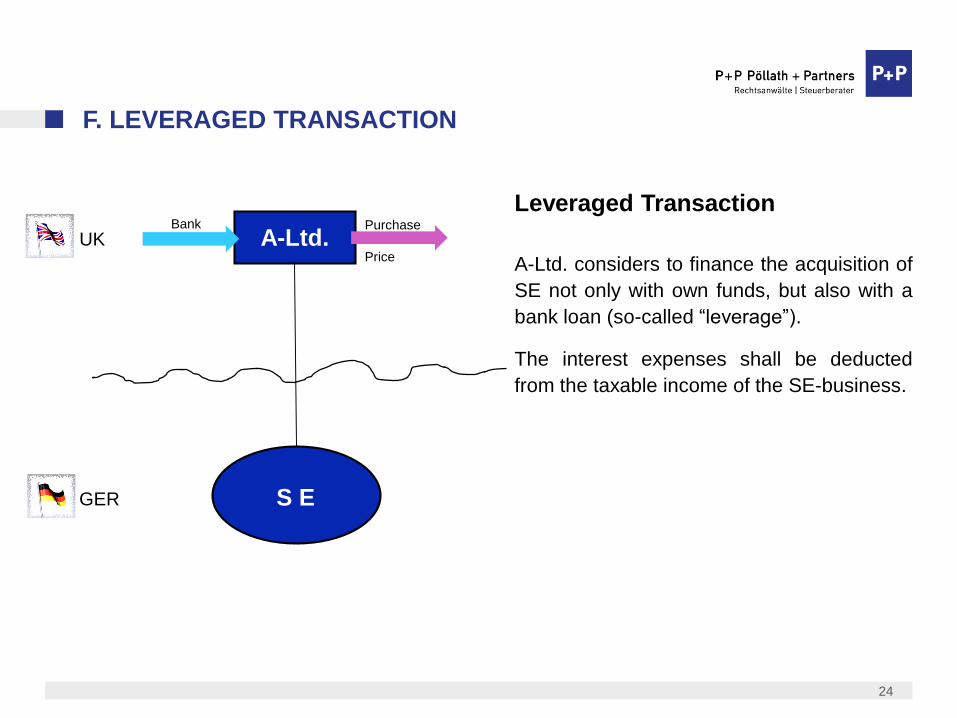

F. LEVERAGED TRANSACTION

Leveraged Transaction

A-Ltd. considers to finance the acquisition of

SE not only with own funds, but also with a

bank loan (so-called “leverage”).

The interest expenses shall be deducted

from the taxable income of the SE-business.

A-Ltd.

GER

UK

S E

Bank Purchase

Price

25

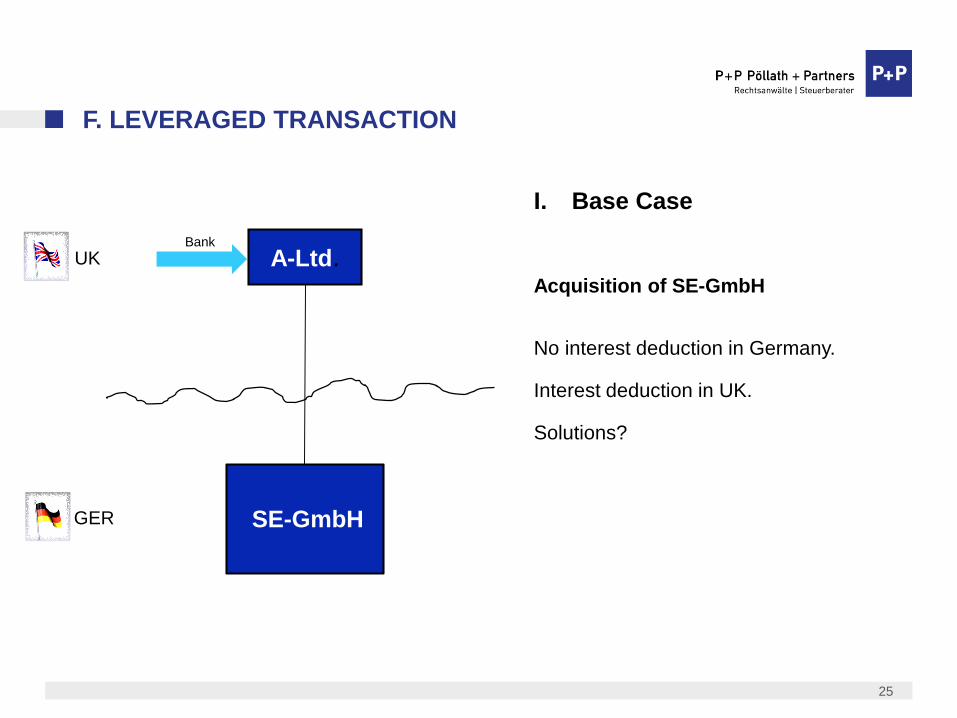

F. LEVERAGED TRANSACTION

I. Base Case

Acquisition of SE-GmbH

No interest deduction in Germany.

Interest deduction in UK.

Solutions?

A-Ltd.

GER

UKBank

SE-GmbH

26

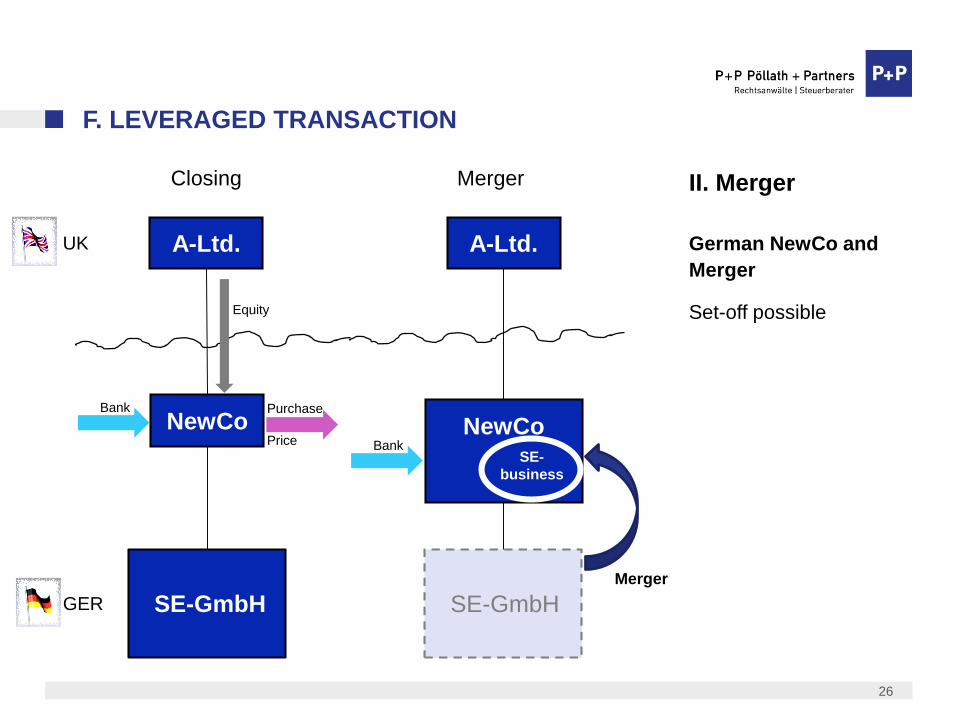

F. LEVERAGED TRANSACTION

GER

UK A-Ltd.

Bank

SE-GmbH

NewCoPurchase

Price

Equity

Closing

A-Ltd.

Bank

SE-GmbH

Merger

Merger

NewCoSE-

business

II. Merger

German NewCo and

Merger

Set-off possible

27

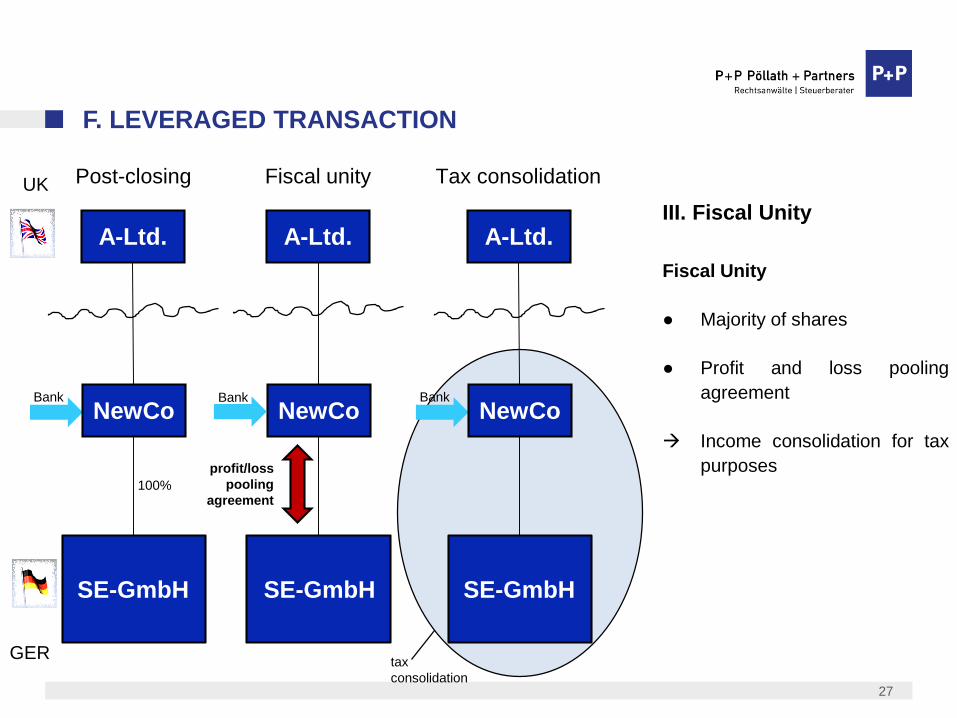

F. LEVERAGED TRANSACTION

III. Fiscal Unity

Fiscal Unity

● Majority of shares

● Profit and loss pooling

agreement

Income consolidation for tax

purposes

A-Ltd.

Bank

SE-GmbH

NewCo

100%

Post-closing

A-Ltd.

SE-GmbH

NewCoBank

Fiscal unity

profit/loss

pooling

agreement

A-Ltd.

Bank

SE-GmbH

NewCo

Tax consolidation

tax

consolidation

UK

GER

28

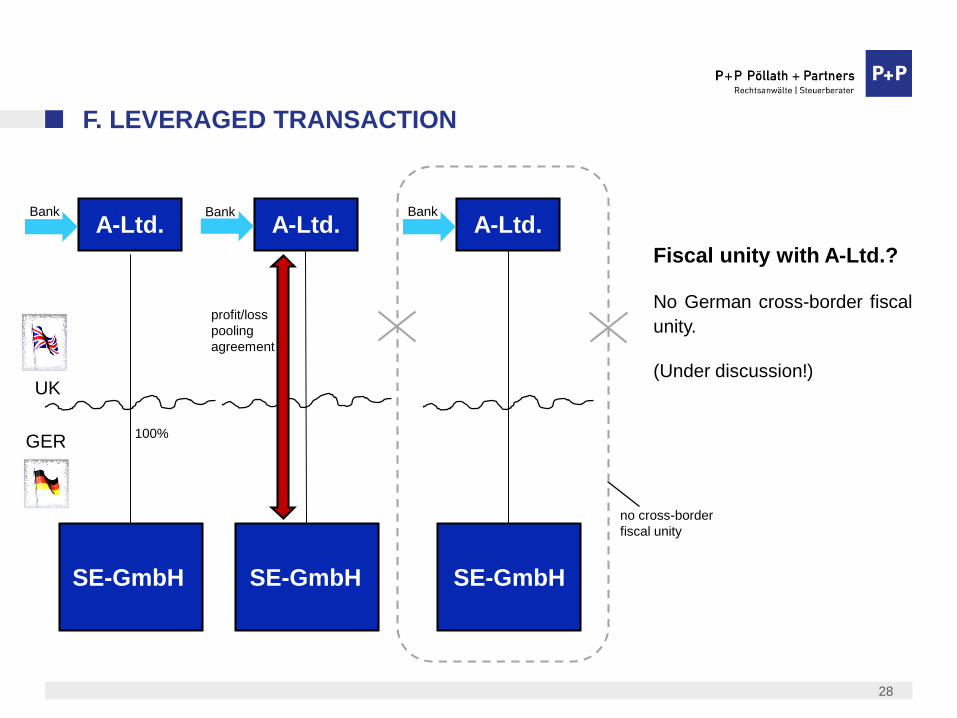

F. LEVERAGED TRANSACTION

Fiscal unity with A-Ltd.?

No German cross-border fiscal

unity.

(Under discussion!)

A-Ltd.Bank

SE-GmbH

100%

A-Ltd.

SE-GmbH

Bank

A-Ltd.Bank

SE-GmbH

no cross-border

fiscal unity

profit/loss

pooling

agreement

UK

GER

29

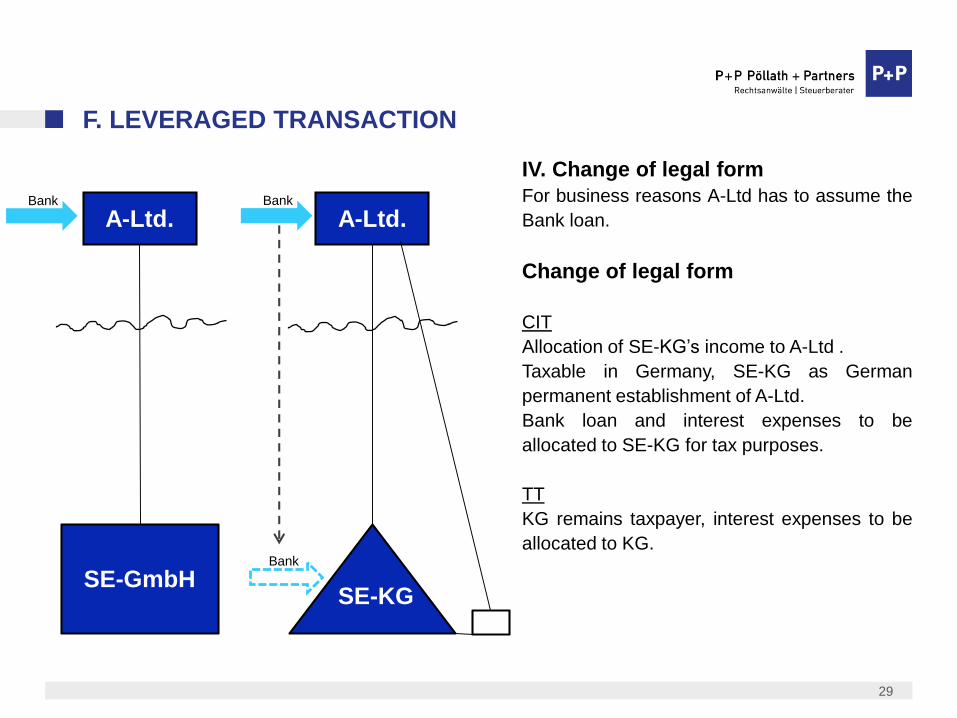

F. LEVERAGED TRANSACTION

IV. Change of legal form

For business reasons A-Ltd has to assume the

Bank loan.

Change of legal form

CIT

Allocation of SE-KG’s income to A-Ltd .

Taxable in Germany, SE-KG as German

permanent establishment of A-Ltd.

Bank loan and interest expenses to be

allocated to SE-KG for tax purposes.

TT

KG remains taxpayer, interest expenses to be

allocated to KG.

A-Ltd.

SE-GmbH

A-Ltd.

Bank

SE-KG

Bank Bank

30

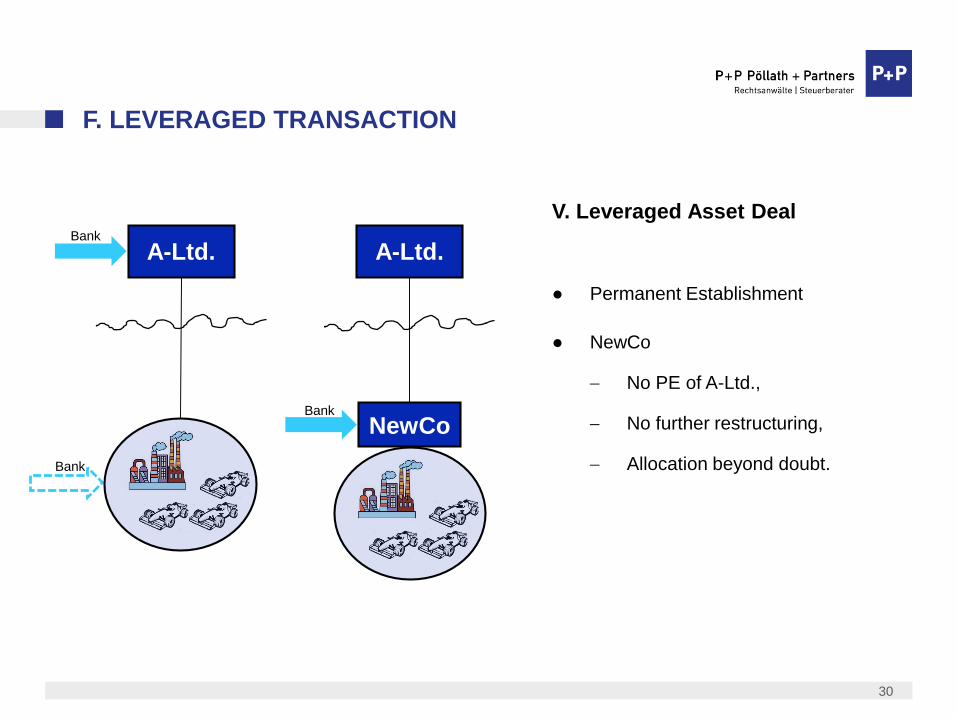

F. LEVERAGED TRANSACTION

V. Leveraged Asset Deal

● Permanent Establishment

● NewCo

No PE of A-Ltd.,

No further restructuring,

Allocation beyond doubt.

A-Ltd.

Bank

NewCo

A-Ltd.

Bank

Bank

31

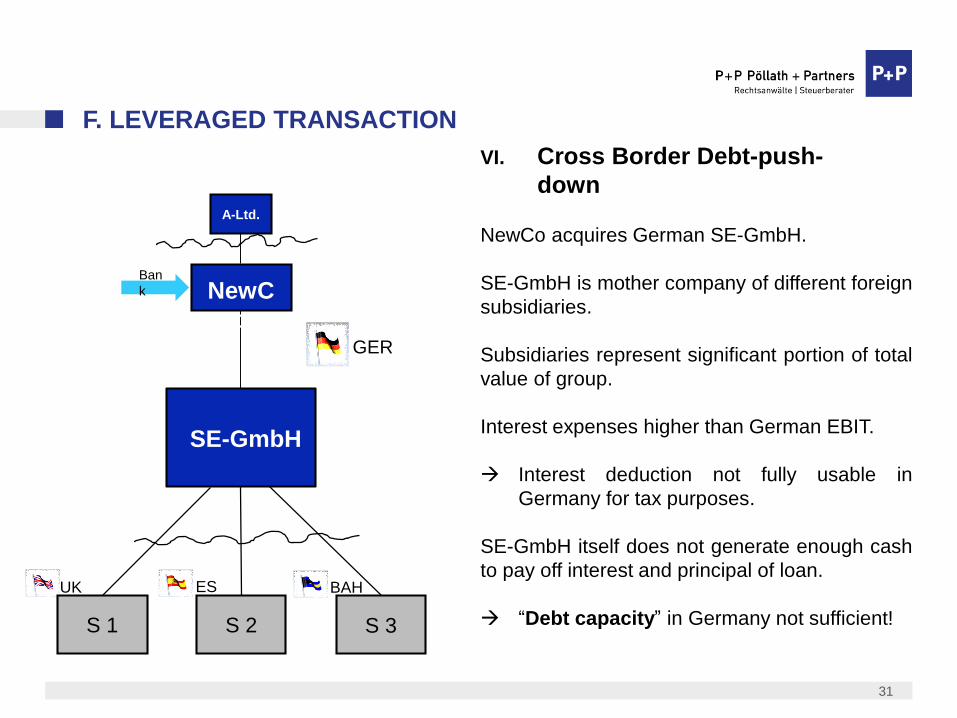

F. LEVERAGED TRANSACTION

VI. Cross Border Debt-push-

down

NewCo acquires German SE-GmbH.

SE-GmbH is mother company of different foreign

subsidiaries.

Subsidiaries represent significant portion of total

value of group.

Interest expenses higher than German EBIT.

Interest deduction not fully usable in

Germany for tax purposes.

SE-GmbH itself does not generate enough cash

to pay off interest and principal of loan.

“Debt capacity” in Germany not sufficient!

NewC

o

Ban

k

SE-GmbH

GER

ES

PBAHUK

S 1 S 2 S 3

A-Ltd.

32

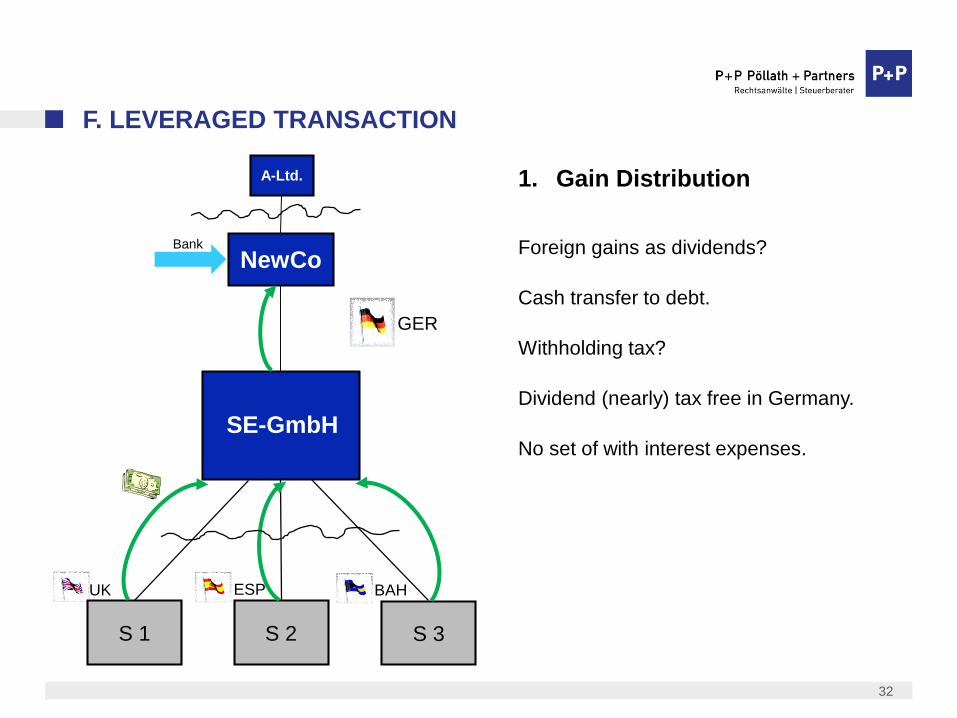

F. LEVERAGED TRANSACTION

1. Gain Distribution

Foreign gains as dividends?

Cash transfer to debt.

Withholding tax?

Dividend (nearly) tax free in Germany.

No set of with interest expenses.

NewCoBank

SE-GmbH

GER

ESP BAHUK

S 1 S 2 S 3

A-Ltd.

33

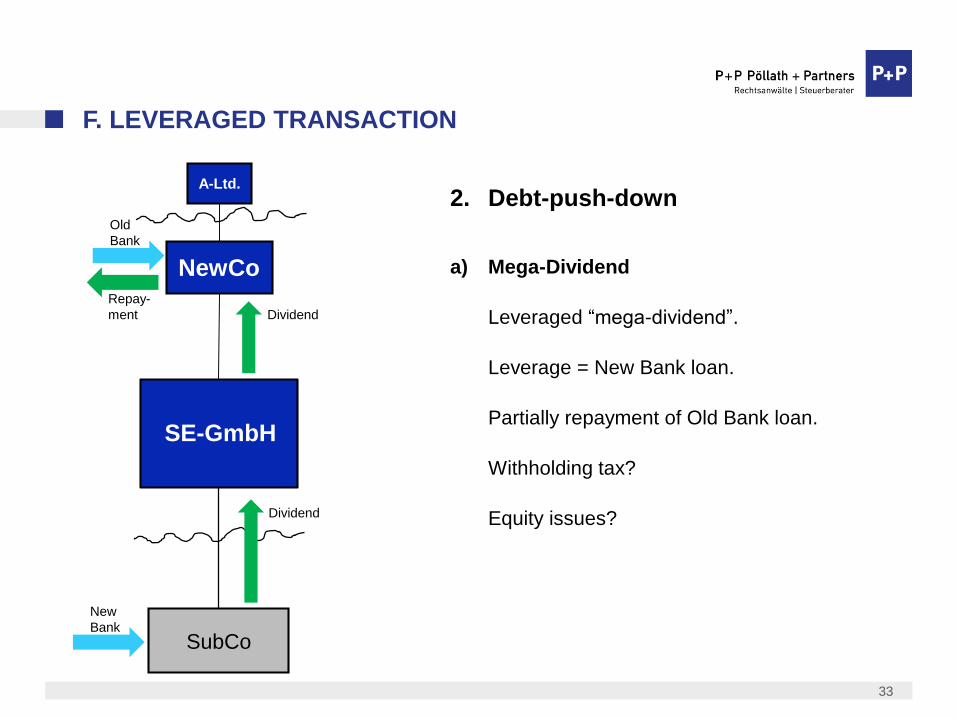

F. LEVERAGED TRANSACTION

2. Debt-push-down

a) Mega-Dividend

Leveraged “mega-dividend”.

Leverage = New Bank loan.

Partially repayment of Old Bank loan.

Withholding tax?

Equity issues?

NewCo

Old

Bank

SE-GmbH

SubCo

New

Bank

Repay-

ment Dividend

Dividend

A-Ltd.

34

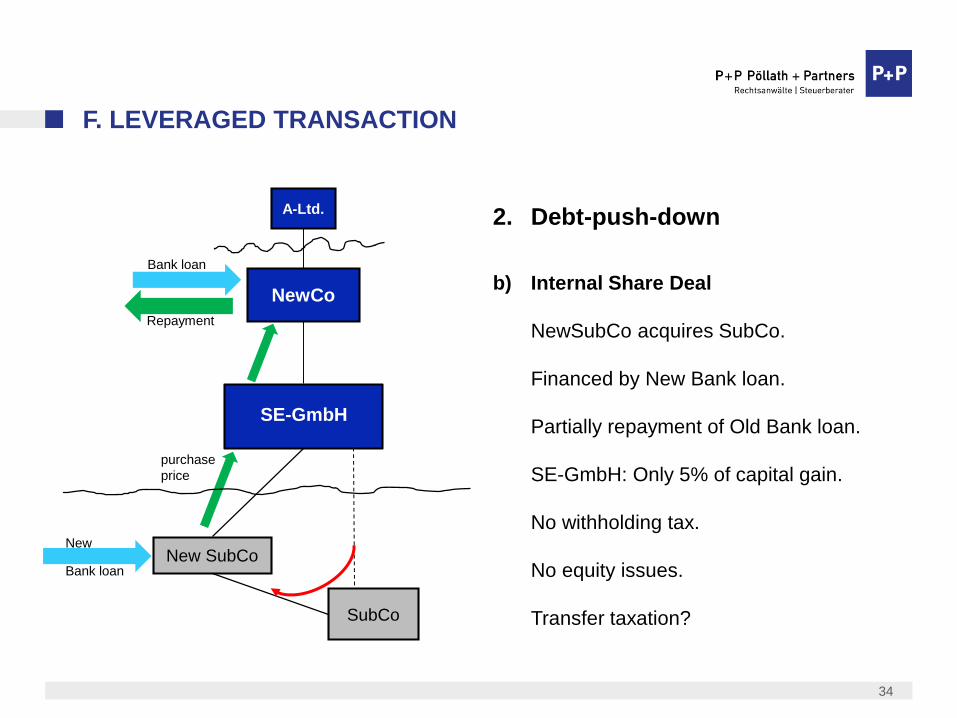

F. LEVERAGED TRANSACTION

2. Debt-push-down

b) Internal Share Deal

NewSubCo acquires SubCo.

Financed by New Bank loan.

Partially repayment of Old Bank loan.

SE-GmbH: Only 5% of capital gain.

No withholding tax.

No equity issues.

Transfer taxation?

NewCo

Bank loan

SE-GmbH

New SubCo

Repayment

SubCo

New

Bank loan

purchase

price

A-Ltd.

35

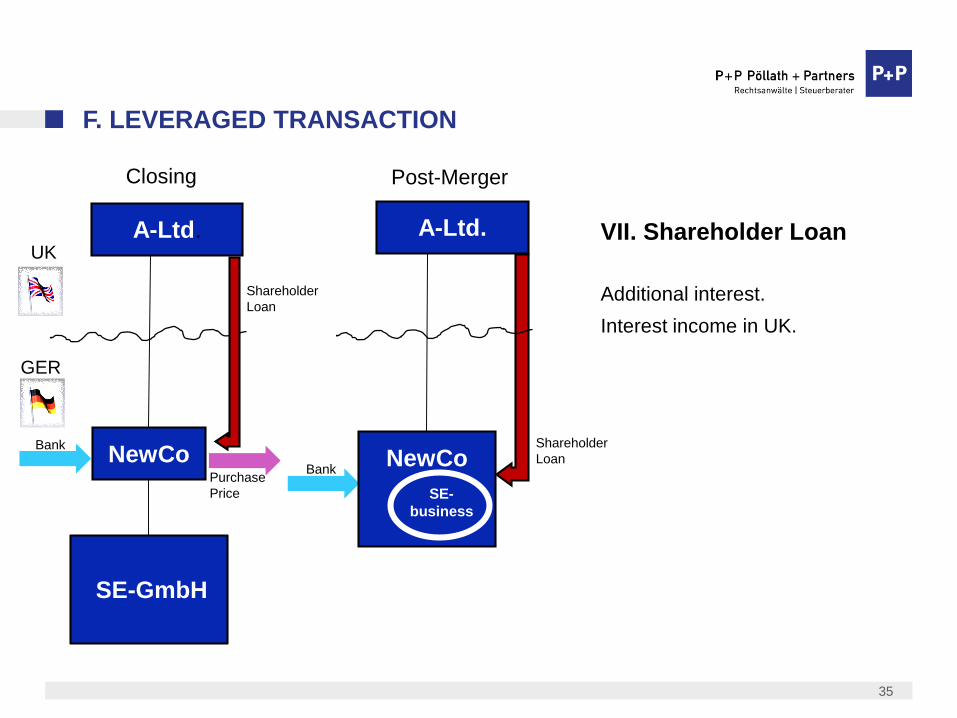

F. LEVERAGED TRANSACTION

VII. Shareholder Loan

Additional interest.

Interest income in UK.

Bank

SE-GmbH

NewCoPurchase

Price

A-Ltd.

Shareholder

Loan

BankNewCo

A-Ltd.

Shareholder

Loan

SE-

business

Closing Post-Merger

GER

UK

36

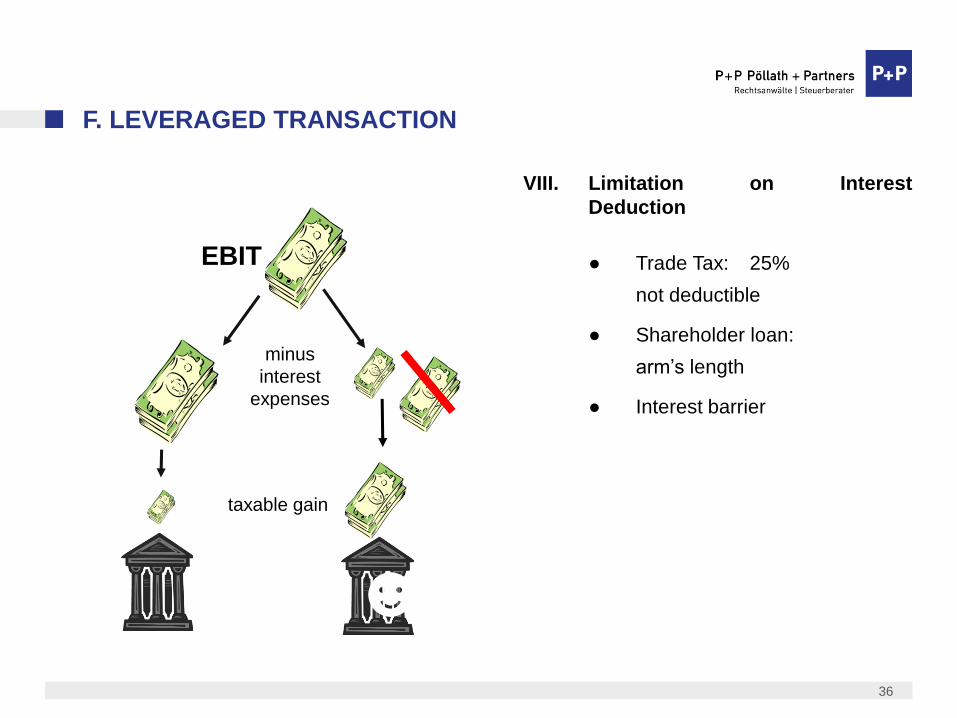

F. LEVERAGED TRANSACTION

VIII. Limitation on Interest

Deduction

● Trade Tax: 25%

not deductible

● Shareholder loan:

arm’s length

● Interest barrier

☻

EBIT

minus

interest

expenses

taxable gain

37

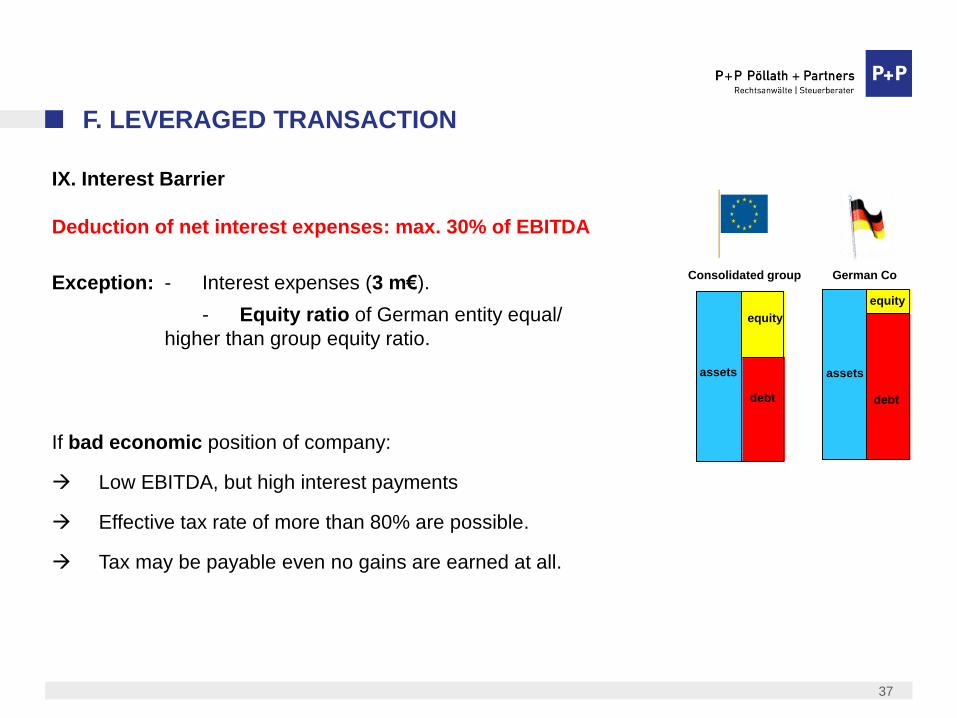

F. LEVERAGED TRANSACTION

IX. Interest Barrier

Deduction of net interest expenses: max. 30% of EBITDA

Exception: - Interest expenses (3 m€).

- Equity ratio of German entity equal/

higher than group equity ratio.

If bad economic position of company:

Low EBITDA, but high interest payments

Effective tax rate of more than 80% are possible.

Tax may be payable even no gains are earned at all.

Consolidated group German Co

equity

equity

assets

debt debt

assets

38

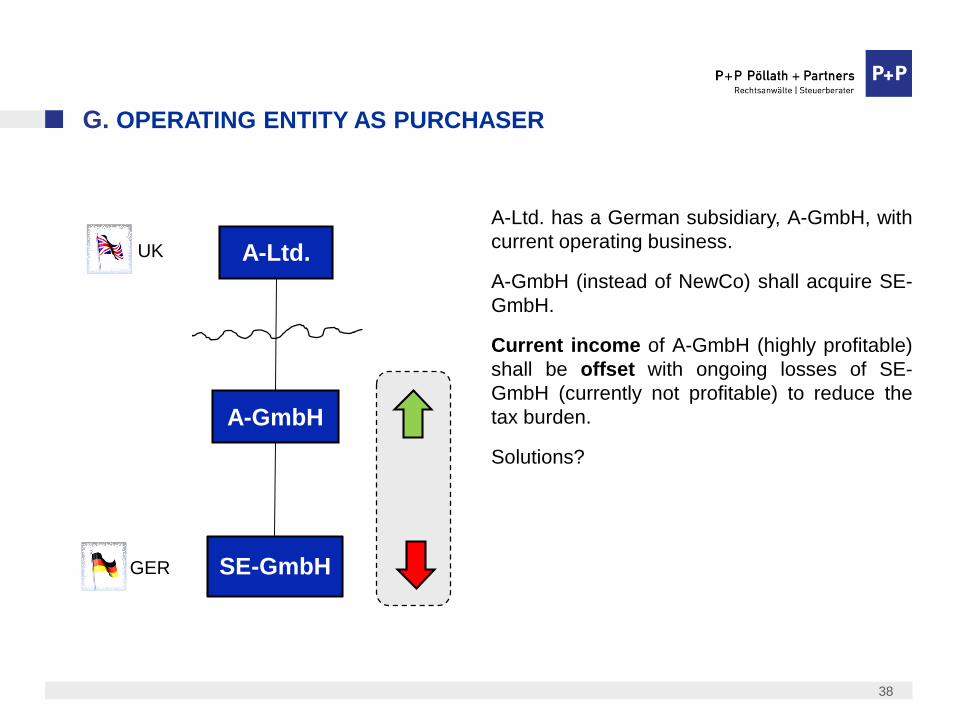

G. OPERATING ENTITY AS PURCHASER

A-Ltd. has a German subsidiary, A-GmbH, with

current operating business.

A-GmbH (instead of NewCo) shall acquire SE-

GmbH.

Current income of A-GmbH (highly profitable)

shall be offset with ongoing losses of SE-

GmbH (currently not profitable) to reduce the

tax burden.

Solutions?

SE-GmbH

A-GmbH

A-Ltd.

GER

UK

39

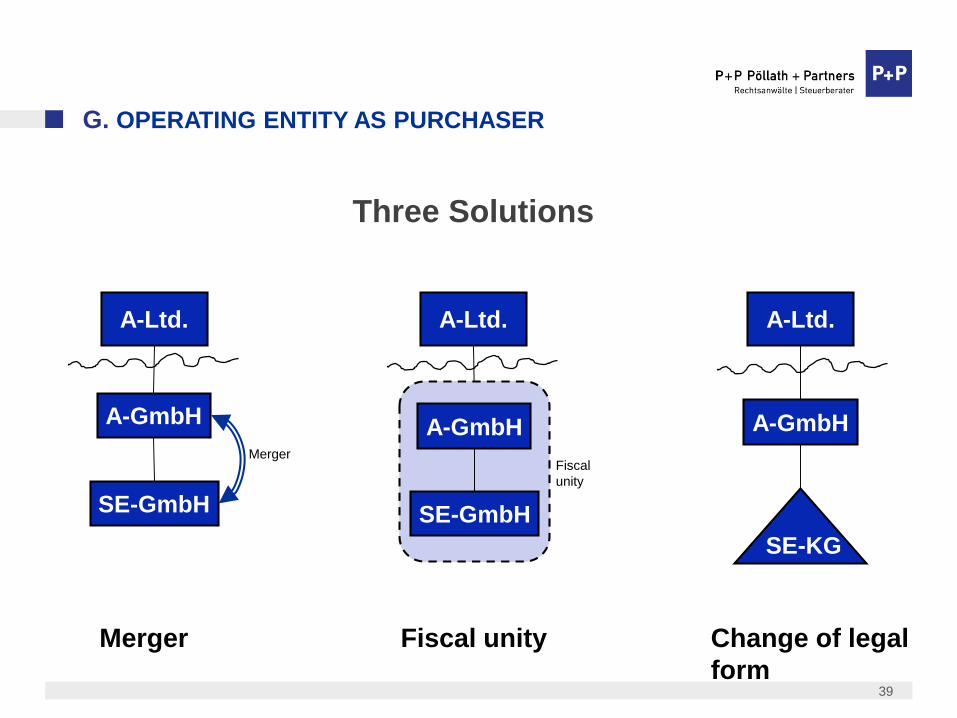

G. OPERATING ENTITY AS PURCHASER

Three Solutions

Merger Fiscal unity

A-Ltd.

SE-GmbH

A-GmbH

Merger

A-Ltd.

SE-GmbH

A-GmbH

Fiscal

unity

A-Ltd.

A-GmbH

SE-KG

Change of legal

form

40

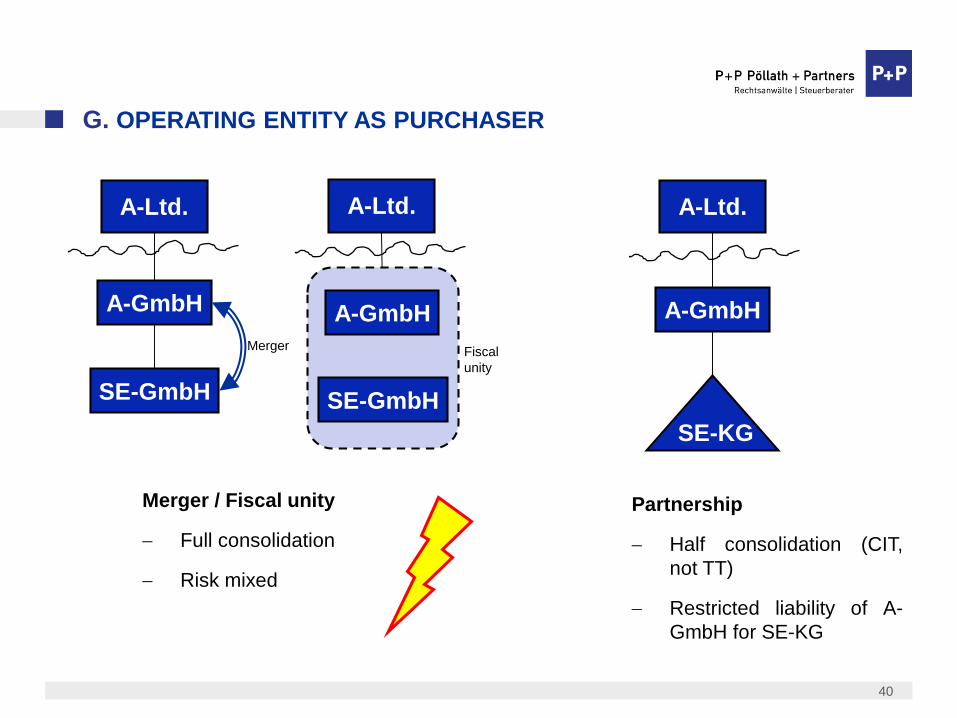

G. OPERATING ENTITY AS PURCHASER

A-Ltd.

SE-GmbH

A-GmbH

Merger

Merger / Fiscal unity

Full consolidation

Risk mixed

A-Ltd.

SE-GmbH

A-GmbH

Fiscal

unity

A-Ltd.

A-GmbH

SE-KG

Partnership

Half consolidation (CIT,

not TT)

Restricted liability of A-

GmbH for SE-KG

41

H. ACQUISITION STRUCTURING

Resume

Acquisition structuring:

tailor-made,

not boiler plate.

Dr. Nico Fischer

CV

Studied law in Passau, Regensburg und Lausanne (Switzerland)

Admitted to bar in 2005

Joined P+P Pöllath + Partners in 2005

Other Activities

Co-Author of the formbook „Recht & Steuern, Teil Unternehmenskauf“

Regular publications as guest author in „Handelsblatt Steuerboard (tax board)“

Associate Lecturer of University of Muenster/ JurGrad for the Master‘s Courese for Tax Sciences/Tax Law

Attorney-at-law

Partner

P+P Pöllath + Partners München

Tel.: +49 (89) 24 240 470

Specialization:

Domestic and International Taw Law

General Tax Planning and Tax Structuring

Tax Structuring with focus on Private Equity

42