Embed Size (px)

DESCRIPTION

This paper presents the results of the methodology used by experts of AL-Tax Center for calculation of Tax Freedom Day, 2015. The data used belong to the budget facts of 2014. An evaluation of this nature is going on for the third time in Albania and is being introduced in the way of tradition from the ALTax center in the economic and fiscal environment of Albania.The object of the presentation is the level of tax burden from one Albanian region to another, pointing to the need to have the ability to increase revenues through comparison with similar regions, in order to finance the costs for central and local investment. On the other hand, every citizen who is contributor to the government budget should be recognized that as is the burden that holds in relation to citizens in other regions of Albania and the Balkans.Calculating the tax burden is added value in the debate on fiscal transparency, enabling policy makers, businesses, researchers, analysts, media, and citizens to compare the distribution of the tax burden. Ranking fiscal burden allows to analyze business decisions and policies, as well as the allocation of public spending within the transparency of public finances context. This analysis, according to administrative zones serves to analyse who is the group or geographic area that is charged more, and on the other hand, a detailed analyse may guide the policy to see what the industry or area should have a different burden from that results.The object of comparing the data are incomes paid to the budget accounts by residents and non-residents. The Vocabulary used in this document refers to the terms of the law on tax procedures. Taxes and customs duties, which are included in this analysis, are the taxes administered by the central tax administration (including social security contributions), taxes and fees administered by local tax administrations, as well as customs, according to the point of custom where are moved the goods.Results of this study are based on income derived by residents under the residence principle where they belong, without excluding tax revenues from large taxpayers of the country (included under the address of residence), who meet around 50% of the total tax revenue for both levels of tax administration.The statistics for regions are also subject to analysis as data comparing the budgetary programs, the level of performance and different sources.

Citation preview

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 1

AL-Tax Center Fiscal Papers, No. 2015/03/02.1 www.al-tax.org [email protected] Date 26.03.2015 Tirana, Albania

Tax Freedom Day in 2015 in Albania Tax Freedom Day in Kosovo and other Balkan countries Tax burden in Albania, according to regions in fiscal year 2014. The comparison with Balkan countries

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 2

©AL-TAX Fiscal Papers March 2015

Prepared and distributed Gjokutaj

ALTax Center

Tax Freedom Day in 2015 in Albania Tax Freedom Day in Kosovo and other Balkan countries Tax burden in Albania, according to regions in fiscal year 2014. The comparison with Balkan countries

Abstract

AL-Tax Center (Albanian Taxation Association) present in this document for the third time in country about the

estimation of tax burden collected by central and local tax authorities, by 12 regions based on the highest rank

until to lowest rank of the ratio of tax burden. The tax burden is comparable with regional countries ratios and

biggest countries of the world.

The purpose of the presentation of estimation is to have the attention of lawmakers and media, as far as good

also to attire the attention of critics and scholars that perhaps could have opinions about this study or have

questions in regard of the methodology, or want to know better the sources of information, or have other

specific questions. The estimation and calculation used in this document are based on different sources,

internal and external ones.

Keywords: Tax burden, Albania, Balkan, taxes, VAT, direct taxes, region, Kosovo, 2014

This document is prepared by the AL-TAX, in a series of thematic collections, with the aim to became into a source of discussion for all concerned, or for use in tax policy function in the implementation of their practices. The copyright is © AL-TAX. Anyone who will use the data from this document requires copyright mark as reference materials to be used. The document is available to the website www.al-tax.org If you request and send questions to [email protected]

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 3

Terms and References

Tax Burden

The total amount collected of taxes, customs duties and social security, on the basis of

relevant tax revenues (taxes on capital, taxes on labor and taxes on consumption) by a

certain group of taxpayers, industry, region, and state., and comparable about what

pay groups, industries, regions, countries, etc.

Total Tax Rate

The total tax rate measures the amount of taxes and mandatory contributions payable

by businesses after calculating allowable deductions and exemptions as part of

commercial profit. Taxes at source (such as payroll taxes) or taxes collected by the tax

agent (such as VAT, sales tax) are excluded.

Income Taxes

A direct tax on income. Although the term is generally applied to a tax on individuals

(where it can be defined as personal income tax or individual income tax), it is also

used in some countries for a tax on legal entities, such as societies.

The tax generally applies on an annual basis, ie. on income derived on or associated

with, a particular fiscal year.

One can distinguish two main systems of income tax: a global tax system and a tax

system based brackets of incomes. However, the global tax systems, in view of

different theoretical definitions of income, most countries specify the positions that

constitute income for tax purposes. Tax rates on income can be implemented with

progressive scale where the tax rate increases with income or fixed rate. Can also be

placed an overpayment.

Most countries impose income tax on the total income of global scale of residents and

to income from sources within the country in case of non-residents. Some countries,

however, limit the income tax on domestic source income for residents as well as non-

residents under the principle of territory.

Tax on Labour This group includes taxes directly related to income generated from work. Such

incomes are tax on income from employment and social insurance contributions and

health.

Tax on Capital

The term used for statistical purposes by the United Nations to refer to 'capital

obligations (ie. Those taxes placed at irregular intervals and very rare on the values of

assets or net worth owned by institutional units) and taxes on transfers capital (ie.

taxes on the value of assets transferred between institutional units as a result of

inheritance, donations to inter vivos (ie. when the donor is alive) or other transfers

GDP Gross Domestic Product

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 4

CONTENT

Description page 5

I Tax Burden in Balkan page 7

II Tax Burden in Albania page 10

Regional tax ratio to GDP page 13

The calculation of tax burden for the regions page 14

The regions with the lowest tax burden page 15

The regions with the highest tax burden page 15

Index of Fiscal Freedom 2015 - Methodology page 16

Tax Freedom Day 2015 in Balkan page 16

Tax Freedom Day 2015 in Albania page 17

CONCLUSION page 18

ANNEXES page 19

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 5

Description

This paper presents the results of the methodology used by experts of AL-Tax Center for calculation of Tax

Freedom Day, 2015. The data used belong to the budget facts of 2014. An evaluation of this nature is going on

for the third time in Albania and is being introduced in the way of tradition from the ALTax center in the

economic and fiscal environment of Albania.

The object of the presentation is the level of tax burden from one Albanian region to another, pointing to the

need to have the ability to increase revenues through comparison with similar regions, in order to finance the

costs for central and local investment. On the other hand, every citizen who is contributor to the government

budget should be recognized that as is the burden that holds in relation to citizens in other regions of Albania

and the Balkans.

Calculating the tax burden is added value in the debate on fiscal transparency, enabling policy makers,

businesses, researchers, analysts, media, and citizens to compare the distribution of the tax burden. Ranking

fiscal burden allows to analyze business decisions and policies, as well as the allocation of public spending

within the transparency of public finances context. This analysis, according to administrative zones serves to

analyse who is the group or geographic area that is charged more, and on the other hand, a detailed analyse

may guide the policy to see what the industry or area should have a different burden from that results.

The object of comparing the data are incomes paid to the budget accounts by residents and non-residents. The

Vocabulary used in this document refers to the terms of the law on tax procedures. Taxes and customs duties,

which are included in this analysis, are the taxes administered by the central tax administration (including

social security contributions), taxes and fees administered by local tax administrations, as well as customs,

according to the point of custom where are moved the goods.

Results of this study are based on income derived by residents under the residence principle where they

belong, without excluding tax revenues from large taxpayers of the country (included under the address of

residence), who meet around 50% of the total tax revenue for both levels of tax administration.

The statistics for regions are also subject to analysis as data comparing the budgetary programs, the level of

performance and different sources.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 6

Presentation of data on domestic production, payment of taxes and fees are based on information contained

in the reports of Monetary Fund (Country Report), of which there are charts, analysis and projections for

macro data for recent years including the Last year 2014. For Albania, the data on regional domestic product

were obtained from the Institute of Statistics, while the macro data on collection of taxes and fees are

extracted by statistics and bulletin of Ministry of Economy and Ministry of Finance

The structure of this paper consists of two parts. The first part is the presentation of statistical data at the

international (Balkan) level. The second part is an analysis and interpretation of regional rankings under the tax

burden.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 7

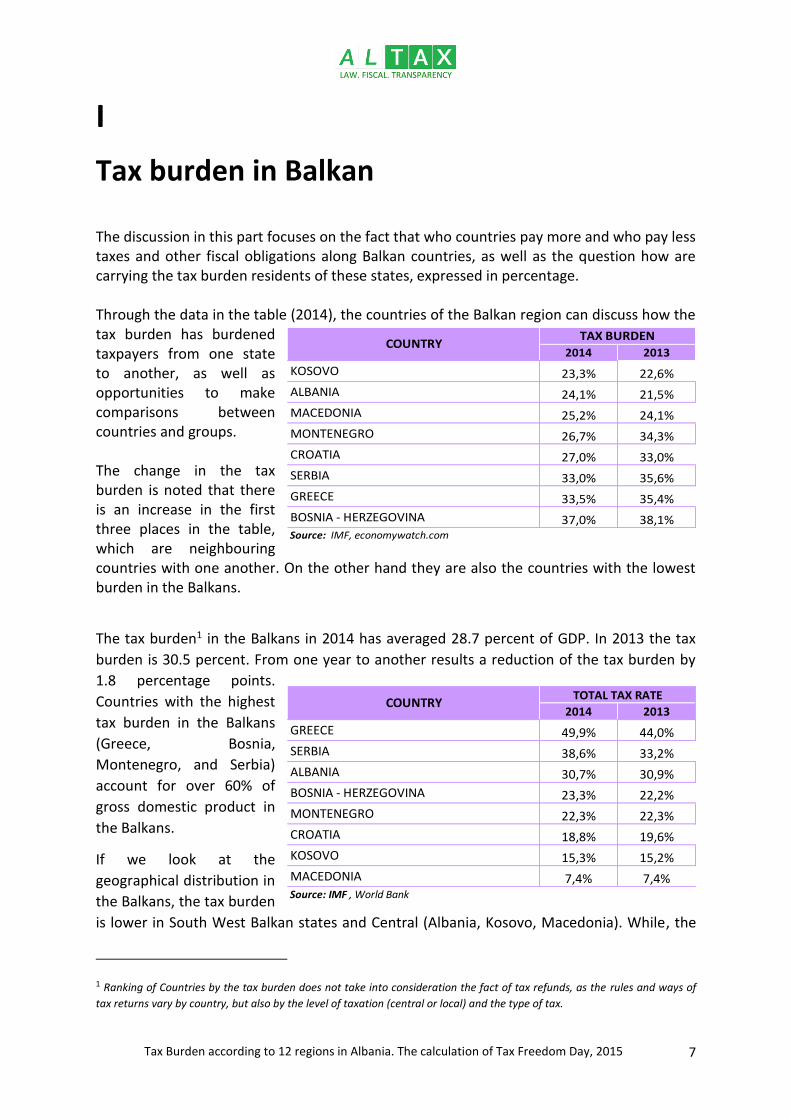

I

Tax burden in Balkan

The discussion in this part focuses on the fact that who countries pay more and who pay less taxes and other fiscal obligations along Balkan countries, as well as the question how are carrying the tax burden residents of these states, expressed in percentage. Through the data in the table (2014), the countries of the Balkan region can discuss how the tax burden has burdened taxpayers from one state to another, as well as opportunities to make comparisons between countries and groups. The change in the tax burden is noted that there is an increase in the first three places in the table, which are neighbouring countries with one another. On the other hand they are also the countries with the lowest burden in the Balkans.

The tax burden1 in the Balkans in 2014 has averaged 28.7 percent of GDP. In 2013 the tax

burden is 30.5 percent. From one year to another results a reduction of the tax burden by

1.8 percentage points.

Countries with the highest

tax burden in the Balkans

(Greece, Bosnia,

Montenegro, and Serbia)

account for over 60% of

gross domestic product in

the Balkans.

If we look at the

geographical distribution in

the Balkans, the tax burden

is lower in South West Balkan states and Central (Albania, Kosovo, Macedonia). While, the

1 Ranking of Countries by the tax burden does not take into consideration the fact of tax refunds, as the rules and ways of

tax returns vary by country, but also by the level of taxation (central or local) and the type of tax.

2014 2013

KOSOVO 23,3% 22,6%

ALBANIA 24,1% 21,5%

MACEDONIA 25,2% 24,1%

MONTENEGRO 26,7% 34,3%

CROATIA 27,0% 33,0%

SERBIA 33,0% 35,6%

GREECE 33,5% 35,4%

BOSNIA - HERZEGOVINA 37,0% 38,1%Source: IMF, economywatch.com

COUNTRYTAX BURDEN

2014 2013

GREECE 49,9% 44,0%

SERBIA 38,6% 33,2%

ALBANIA 30,7% 30,9%

BOSNIA - HERZEGOVINA 23,3% 22,2%

MONTENEGRO 22,3% 22,3%

CROATIA 18,8% 19,6%

KOSOVO 15,3% 15,2%

MACEDONIA 7,4% 7,4%Source: IMF , World Bank

COUNTRYTOTAL TAX RATE

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 8

tax burden is higher in Western Balkan countries (Bosnia-Herzegovina, Croatia) and the

north and south of the Balkans (Serbia, Greece).

In an analysis of the tax burden by calculating all tax rates together (total tax rate), the

higher tax burden can be found in Greece, Serbia and Albania. Lower burden hold

Macedonia, Kosovo, Montenegro, Croatia and Bosnia - Herzegovina. In calculating the tax

burden according to the tax rate does not include tax exemption schemes, as well as

temporary tax policies (within the fiscal year).

Ranking according to the tax burden of the Balkan countries there’s no the same tendency

with the total tax rate, which is presented in the table for 2013 and 2014. While the

horizontal comparison between themselves in terms of total tax rate is an average increase

in 2014 (25, 7%) compared with 2013 (24.3%) with 1.4 point percent, which reflects the

changes in the legislation of some Balkan countries regarding specific tax rates. In Greece it

is adopted the change of maximum rate of personal income tax to more 4 percent.

The same change to the maximum margin of personal income tax has passed also the

Croatia, but given the formulas for computing the total tax rate, the effect of changes will be

expected for the following year. As in other Balkan countries, changes occurred in tax rates

have given influences and smaller effects.

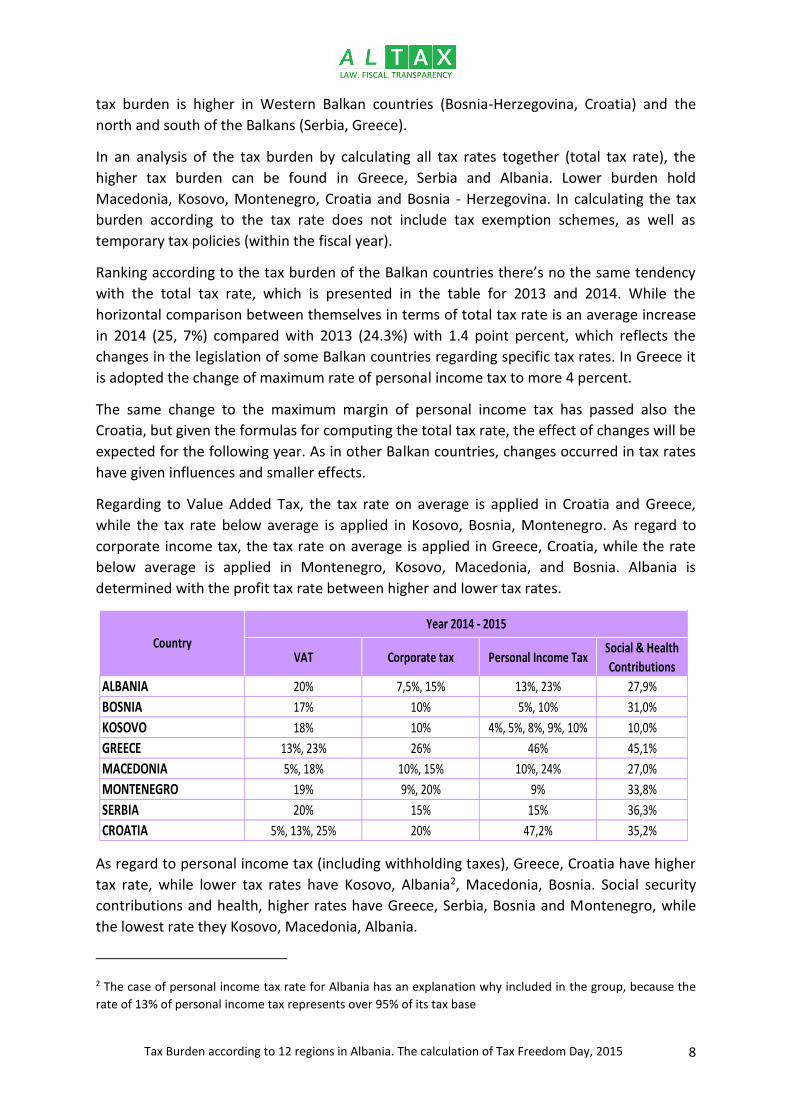

Regarding to Value Added Tax, the tax rate on average is applied in Croatia and Greece,

while the tax rate below average is applied in Kosovo, Bosnia, Montenegro. As regard to

corporate income tax, the tax rate on average is applied in Greece, Croatia, while the rate

below average is applied in Montenegro, Kosovo, Macedonia, and Bosnia. Albania is

determined with the profit tax rate between higher and lower tax rates.

VAT Corporate tax Personal Income TaxSocial & Health

Contributions

ALBANIA 20% 7,5%, 15% 13%, 23% 27,9%

BOSNIA 17% 10% 5%, 10% 31,0%

KOSOVO 18% 10% 4%, 5%, 8%, 9%, 10% 10,0%

GREECE 13%, 23% 26% 46% 45,1%

MACEDONIA 5%, 18% 10%, 15% 10%, 24% 27,0%

MONTENEGRO 19% 9%, 20% 9% 33,8%

SERBIA 20% 15% 15% 36,3%

CROATIA 5%, 13%, 25% 20% 47,2% 35,2%

Country

Year 2014 - 2015

As regard to personal income tax (including withholding taxes), Greece, Croatia have higher

tax rate, while lower tax rates have Kosovo, Albania2, Macedonia, Bosnia. Social security

contributions and health, higher rates have Greece, Serbia, Bosnia and Montenegro, while

the lowest rate they Kosovo, Macedonia, Albania.

2 The case of personal income tax rate for Albania has an explanation why included in the group, because the

rate of 13% of personal income tax represents over 95% of its tax base

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 9

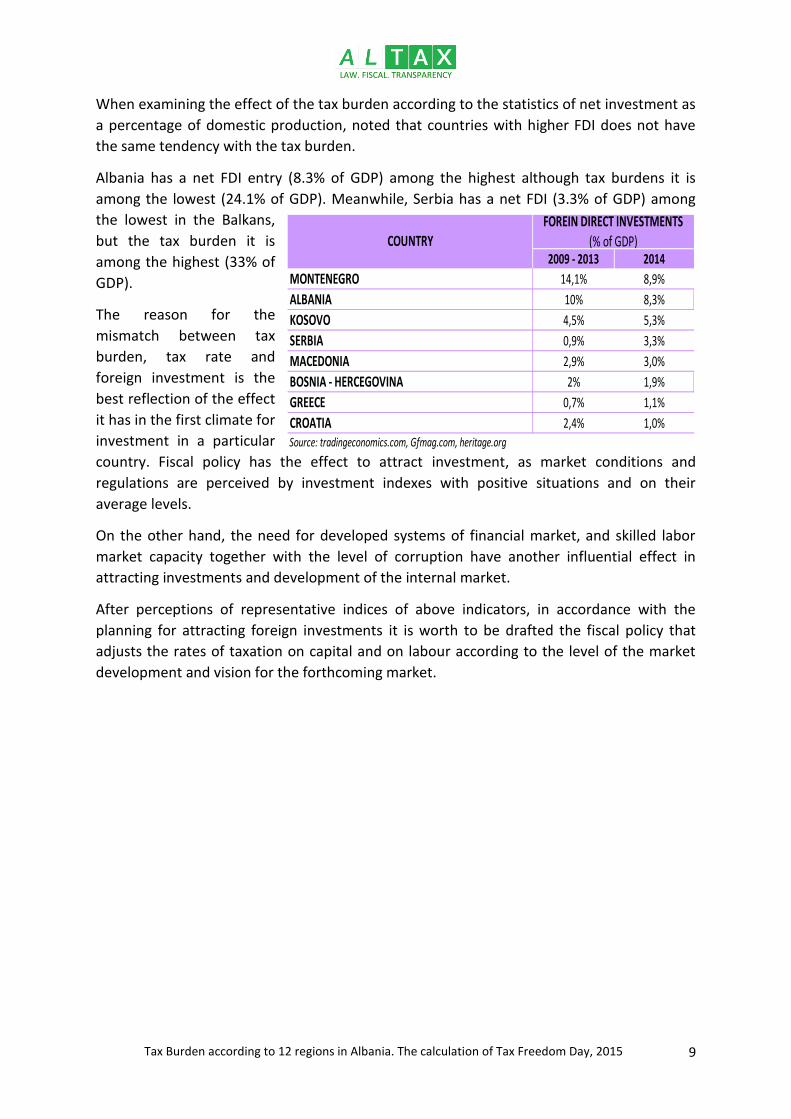

When examining the effect of the tax burden according to the statistics of net investment as

a percentage of domestic production, noted that countries with higher FDI does not have

the same tendency with the tax burden.

Albania has a net FDI entry (8.3% of GDP) among the highest although tax burdens it is

among the lowest (24.1% of GDP). Meanwhile, Serbia has a net FDI (3.3% of GDP) among

the lowest in the Balkans,

but the tax burden it is

among the highest (33% of

GDP).

The reason for the

mismatch between tax

burden, tax rate and

foreign investment is the

best reflection of the effect

it has in the first climate for

investment in a particular

country. Fiscal policy has the effect to attract investment, as market conditions and

regulations are perceived by investment indexes with positive situations and on their

average levels.

On the other hand, the need for developed systems of financial market, and skilled labor

market capacity together with the level of corruption have another influential effect in

attracting investments and development of the internal market.

After perceptions of representative indices of above indicators, in accordance with the

planning for attracting foreign investments it is worth to be drafted the fiscal policy that

adjusts the rates of taxation on capital and on labour according to the level of the market

development and vision for the forthcoming market.

2009 - 2013 2014

MONTENEGRO 14,1% 8,9%

ALBANIA 10% 8,3%

KOSOVO 4,5% 5,3%

SERBIA 0,9% 3,3%

MACEDONIA 2,9% 3,0%

BOSNIA - HERCEGOVINA 2% 1,9%

GREECE 0,7% 1,1%

CROATIA 2,4% 1,0%

Source: tradingeconomics.com, Gfmag.com, heritage.org

COUNTRYFOREIN DIRECT INVESTMENTS

(% of GDP)

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 10

II

Tax burden in Albania To answer the question of which geographical area under the respective region pays more taxes in the budget (expressed as a percentage of the taxes and fees paid to GDP) will advance to clarify firstly the effects of factors that make the evaluation of possible. When we consider the influencing factors, the measurement of the tax burden is not a measure of the size of government or the public administration (its composition), but on the other hand is not the measurement of all the obligations that carries a taxpayer as an evaluation of incomes he performs within a year (i.e. fee for non-fiscal institutions).

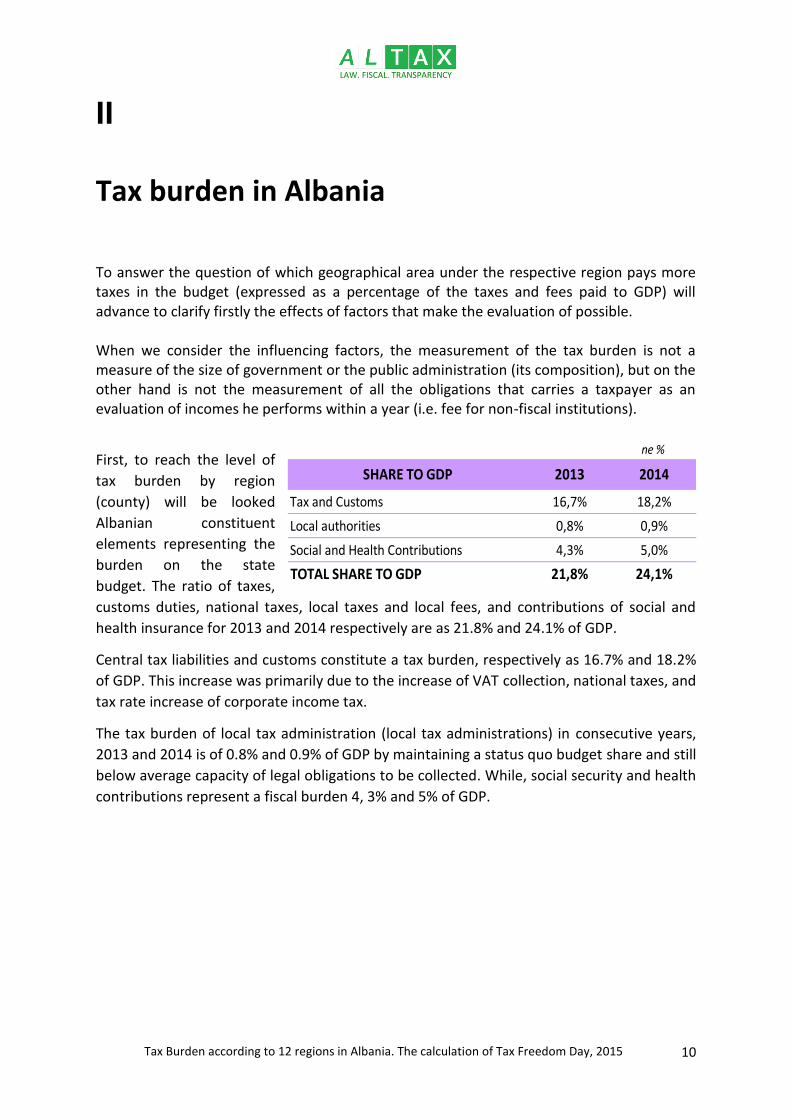

First, to reach the level of

tax burden by region

(county) will be looked

Albanian constituent

elements representing the

burden on the state

budget. The ratio of taxes,

customs duties, national taxes, local taxes and local fees, and contributions of social and

health insurance for 2013 and 2014 respectively are as 21.8% and 24.1% of GDP.

Central tax liabilities and customs constitute a tax burden, respectively as 16.7% and 18.2%

of GDP. This increase was primarily due to the increase of VAT collection, national taxes, and

tax rate increase of corporate income tax.

The tax burden of local tax administration (local tax administrations) in consecutive years,

2013 and 2014 is of 0.8% and 0.9% of GDP by maintaining a status quo budget share and still

below average capacity of legal obligations to be collected. While, social security and health

contributions represent a fiscal burden 4, 3% and 5% of GDP.

ne %

SHARE TO GDP 2013 2014

Tax and Customs 16,7% 18,2%

Local authorities 0,8% 0,9%

Social and Health Contributions 4,3% 5,0%

TOTAL SHARE TO GDP 21,8% 24,1%

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 11

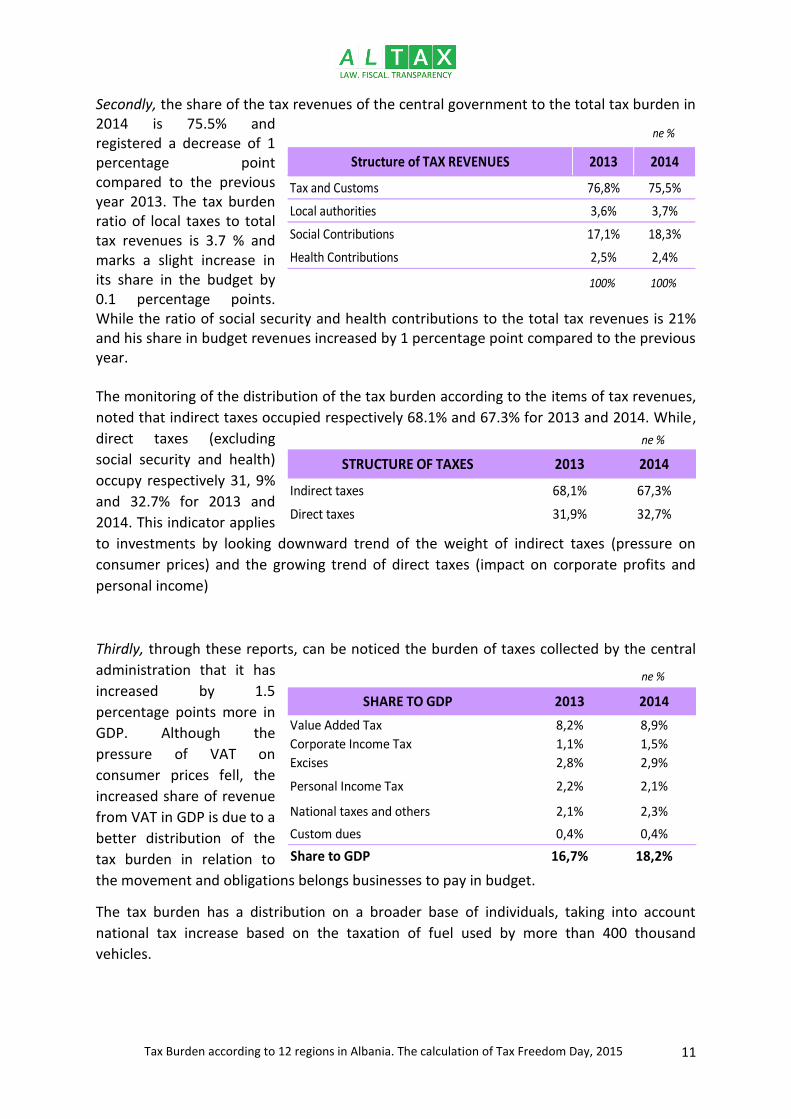

Secondly, the share of the tax revenues of the central government to the total tax burden in 2014 is 75.5% and registered a decrease of 1 percentage point compared to the previous year 2013. The tax burden ratio of local taxes to total tax revenues is 3.7 % and marks a slight increase in its share in the budget by 0.1 percentage points. While the ratio of social security and health contributions to the total tax revenues is 21% and his share in budget revenues increased by 1 percentage point compared to the previous year. The monitoring of the distribution of the tax burden according to the items of tax revenues,

noted that indirect taxes occupied respectively 68.1% and 67.3% for 2013 and 2014. While,

direct taxes (excluding

social security and health)

occupy respectively 31, 9%

and 32.7% for 2013 and

2014. This indicator applies

to investments by looking downward trend of the weight of indirect taxes (pressure on

consumer prices) and the growing trend of direct taxes (impact on corporate profits and

personal income)

Thirdly, through these reports, can be noticed the burden of taxes collected by the central

administration that it has

increased by 1.5

percentage points more in

GDP. Although the

pressure of VAT on

consumer prices fell, the

increased share of revenue

from VAT in GDP is due to a

better distribution of the

tax burden in relation to

the movement and obligations belongs businesses to pay in budget.

The tax burden has a distribution on a broader base of individuals, taking into account

national tax increase based on the taxation of fuel used by more than 400 thousand

vehicles.

ne %

Structure of TAX REVENUES 2013 2014

Tax and Customs 76,8% 75,5%

Local authorities 3,6% 3,7%

Social Contributions 17,1% 18,3%

Health Contributions 2,5% 2,4%

100% 100%

ne %

STRUCTURE OF TAXES 2013 2014

Indirect taxes 68,1% 67,3%

Direct taxes 31,9% 32,7%

ne %

SHARE TO GDP 2013 2014

Value Added Tax 8,2% 8,9%

Corporate Income Tax 1,1% 1,5%

Excises 2,8% 2,9%

Personal Income Tax 2,2% 2,1%

National taxes and others 2,1% 2,3%

Custom dues 0,4% 0,4%

Share to GDP 16,7% 18,2%

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 12

While the trend of decline (- 0.1 percentage points) of the burden of tax on the value of

labour (personal income tax) and the tendency of growth (0.4 percentage points) of the

burden of tax on capital (income tax) are two flows that coincide with the tendency of the

economy and the current Albanian government program.

In 2014, it was approved the big change of the previous fiscal policy, which operated under

the principle of the flat tax for a period of more than 4 years of taxation of individuals with

low and medium wages.

The new policy was oriented by increasing fiscal pressure on capital accumulation

coordinated with the tendency of the shifting of the tax burden mostly on savings of rich

individuals, as well as on the capital of companies, differentiating from this burden small

business.

From the calculation of the distribution of the tax burden by month of the year has an equal

proportion distribution. Each month the tax burden is on the average level of 8% of the total

tax burden. Lower the tax burden is in February while the highest is in December.

Detailed data for each item in the state budget revenues are in ANNEX.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 13

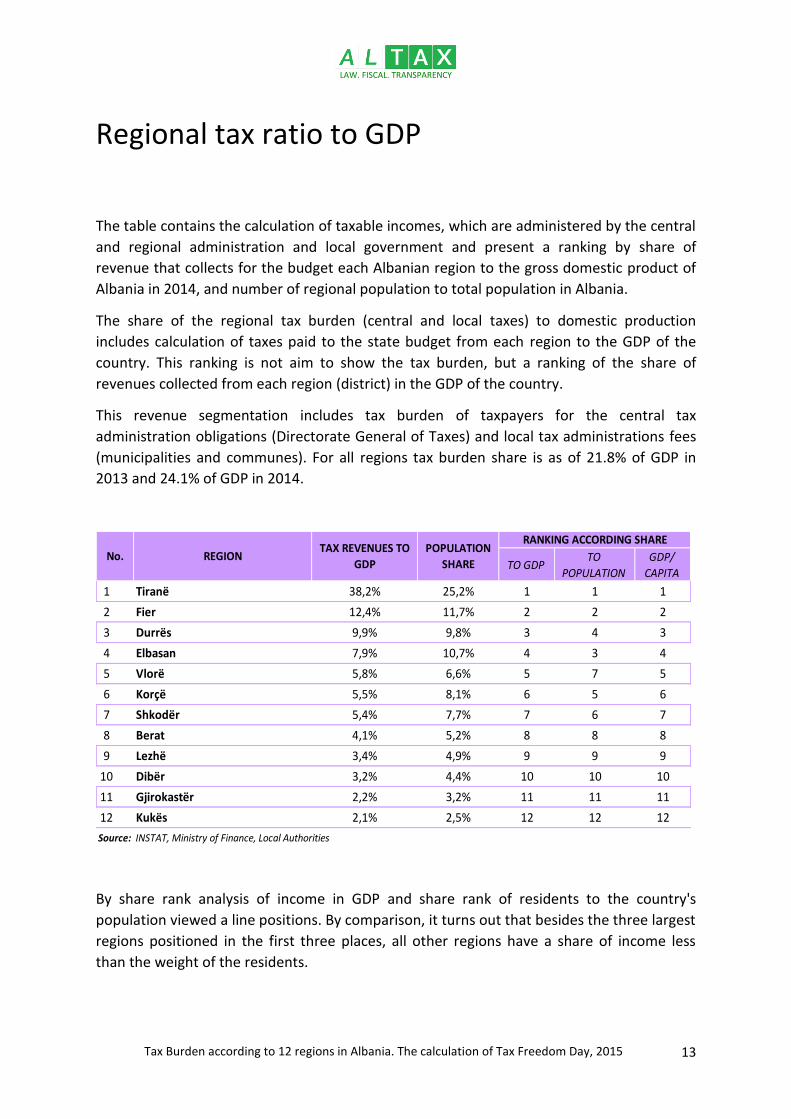

Regional tax ratio to GDP

The table contains the calculation of taxable incomes, which are administered by the central

and regional administration and local government and present a ranking by share of

revenue that collects for the budget each Albanian region to the gross domestic product of

Albania in 2014, and number of regional population to total population in Albania.

The share of the regional tax burden (central and local taxes) to domestic production

includes calculation of taxes paid to the state budget from each region to the GDP of the

country. This ranking is not aim to show the tax burden, but a ranking of the share of

revenues collected from each region (district) in the GDP of the country.

This revenue segmentation includes tax burden of taxpayers for the central tax

administration obligations (Directorate General of Taxes) and local tax administrations fees

(municipalities and communes). For all regions tax burden share is as of 21.8% of GDP in

2013 and 24.1% of GDP in 2014.

TO GDPTO

POPULATION

GDP/

CAPITA

1 Tiranë 38,2% 25,2% 1 1 1

2 Fier 12,4% 11,7% 2 2 2

3 Durrës 9,9% 9,8% 3 4 3

4 Elbasan 7,9% 10,7% 4 3 4

5 Vlorë 5,8% 6,6% 5 7 5

6 Korçë 5,5% 8,1% 6 5 6

7 Shkodër 5,4% 7,7% 7 6 7

8 Berat 4,1% 5,2% 8 8 8

9 Lezhë 3,4% 4,9% 9 9 9

10 Dibër 3,2% 4,4% 10 10 10

11 Gjirokastër 2,2% 3,2% 11 11 11

12 Kukës 2,1% 2,5% 12 12 12

Source: INSTAT, Ministry of Finance, Local Authorities

No. REGIONTAX REVENUES TO

GDP

POPULATION

SHARE

RANKING ACCORDING SHARE

By share rank analysis of income in GDP and share rank of residents to the country's

population viewed a line positions. By comparison, it turns out that besides the three largest

regions positioned in the first three places, all other regions have a share of income less

than the weight of the residents.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 14

This discrepancy is explained, with the centralization of consume and industry in these

regions. On the other hand, a better tax administration can justify narrowing the differences

between the consumption and distribution of the population and businesses in the region.

The specific share of regions of the country, has specifications that include the number of taxpayers who bear the tax burden, industrial characteristics, gender composition, population structure, education, natural resources underground and above ground, the individual assets inherited and assets created in these two decades, as well as elements of the environment and investment in public and private funds, including regional development plans. These reports orient the distribution of segmentation of taxpayers, according to the size that they fit (micro, small, medium, or large). The data reports show that the tax burden on regions is held at the quantitative level from the base of resident taxpayers who fall into the categories of micro businesses (self) and small business than the base of resident taxpayers who fall into the categories of medium and large businesses.

A contributing factor is related to the distribution of goods and services for consumption, which have a tendency to consumed out of area in which are created or produced to the export or in areas with population density. Significant example is the case of areas where are extracted the minerals. Shifting of goods for export or in areas with dense urban populations at the same time makes the shift of the burden from one region to another one. On the other hand, the tax burden that keeps the non-residents, although there is a specific share not more than 4% of the total tax burden has an impact in areas where they are located and generate income within the country.

The calculation of tax burden for the regions Calculation The tax burden for the regions of the country is based on data distributed on a regional basis under the administrative and territorial division. The statistics are taken from INSTAT newsletter, and other data published by tax administrations, customs and local authorities, crossed with data publications from Monetary Fund, World Bank, as well as studies conducted in Albania from local projects, which have served as a reference for calculating the tax burden and other comparative indicators. For the calculation of the regional domestic product for 2014 are estimated by experts’ based in the edition of the Statistical Institute and regional trends of domestic production structure in the 5 years prior to the mean. For the calculation of customs duties are calculated receipts of customs houses and allocation according goods and points of entry crossed with the consumption of the regional population and activities there.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 15

While taxes paid by larger companies are calculated as a tax burden that belongs Tirana and their location in some of the regions where they have their business locations in major cities of Durres, Elbasan, Fier, Korce, Shkodra and Gjirokastra. After determining the taxes paid by regions has become domestic product ratio by respective region resulting in reports submitted to analysis. In this calculation error of calculation goes up to 3%.

The regions with the lowest tax burden

From the ratio of taxes paid in

2014 with regional domestic

product in 2014, shows that the

tax burden is lower in Kukes region

with 11.1%. In second place is the

region of Elbasan with 11.6%. In

third place is the region of Berat

with 13.3%.

The 6 regions and municipalities

with the lowest tax burden are in a

geographical spread in the south west, central, northeast, north and west.

The regions with the highest tax burden

From the ratio of taxes paid in

2014 with regional domestic

product in 2014, shows that the

tax burden is higher in Tirana

region with 29.3%. After this

region the second region with high

burden is Durres region with a tax

burden of 29% and Gjirokastra

region with 27.6%.

The 6 regions and municipalities

with the lowest tax burden are in a geographical spread in central, south and southeast of

Albania.

Tiranë 29,3%

Durrës 29,0%

Gjirokastër 27,6%

Elbasan 24,7%

Korçë 23,5%

Vlorë 22,8%

ALBANIAN REGIONSREGIONAL TAX

BURDEN, 2014

Kukës 11,1%

Dibër 11,6%

Berat 13,3%

Lezhë 15,8%

Shkodër 17,1%

Fier 18,2%

ALBANIAN REGIONSREGIONAL TAX

BURDEN, 2014

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 16

Index of Fiscal Freedom 2015 Methodology Tax Freedom Day is calculated based on the ratio of tax revenue for the fiscal year with gross domestic product. Tax revenues include all types of taxes, customs duties, as well as health and social security.

Total tax revenue is calculated as a percentage of GDP. The resulting report is multiplied by

the number of days of the year (365). The resulting number is counted as day to months

starting from 1 January. The calculation of days finishes in that day of the month in which

the number fit with proper day.

In the day that counting of days of the year stop is considered as the Tax Freedom Day. The

meaning of this day is that the taxpayers of the country to this day have closed accounts of

paying taxes and from this day the following year they work for themselves, without having

any state tax liability.

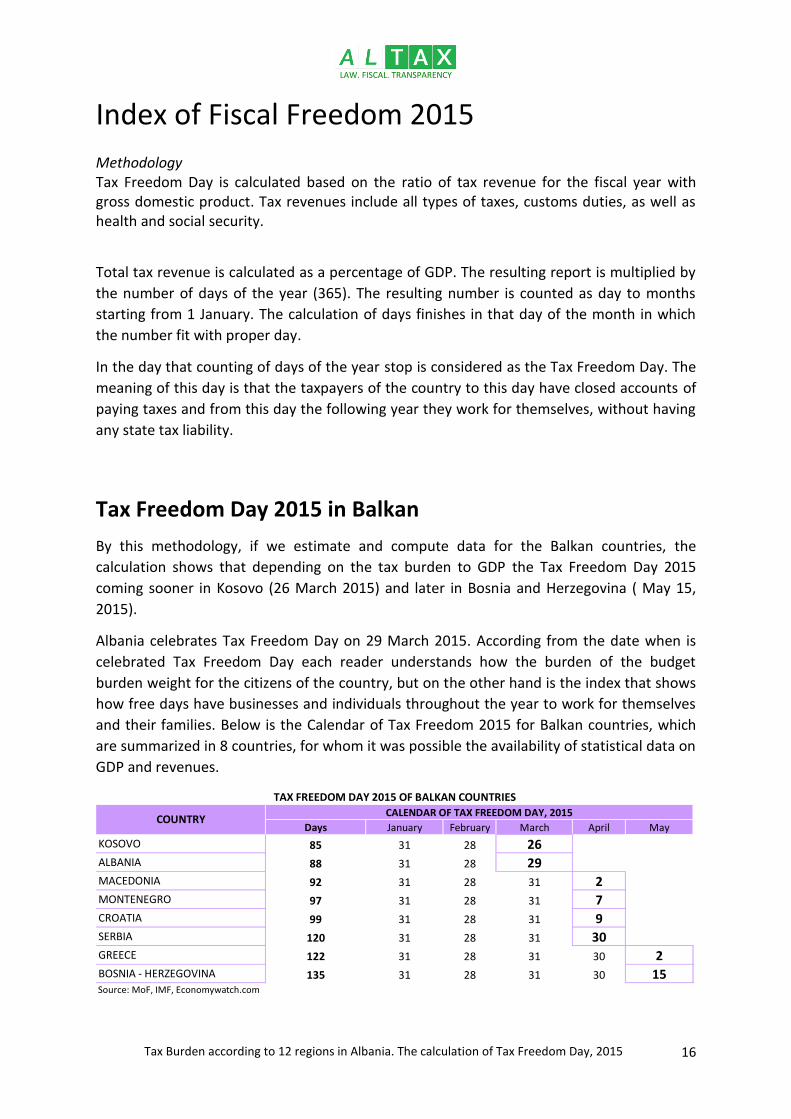

Tax Freedom Day 2015 in Balkan

By this methodology, if we estimate and compute data for the Balkan countries, the

calculation shows that depending on the tax burden to GDP the Tax Freedom Day 2015

coming sooner in Kosovo (26 March 2015) and later in Bosnia and Herzegovina ( May 15,

2015).

Albania celebrates Tax Freedom Day on 29 March 2015. According from the date when is

celebrated Tax Freedom Day each reader understands how the burden of the budget

burden weight for the citizens of the country, but on the other hand is the index that shows

how free days have businesses and individuals throughout the year to work for themselves

and their families. Below is the Calendar of Tax Freedom 2015 for Balkan countries, which

are summarized in 8 countries, for whom it was possible the availability of statistical data on

GDP and revenues.

Days January February March April May

KOSOVO 85 31 28 26ALBANIA 88 31 28 29MACEDONIA 92 31 28 31 2MONTENEGRO 97 31 28 31 7CROATIA 99 31 28 31 9SERBIA 120 31 28 31 30GREECE 122 31 28 31 30 2BOSNIA - HERZEGOVINA 135 31 28 31 30 15Source: MoF, IMF, Economywatch.com

COUNTRYCALENDAR OF TAX FREEDOM DAY, 2015

TAX FREEDOM DAY 2015 OF BALKAN COUNTRIES

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 17

Tax Freedom Day 2015 in Albania

Tax Freedom Day, as in the Balkans also in Albania is the index of individual and business

facilitation of the burden of taxes and fees. Tax Freedom Day for the year 2015 is the 29th

day of March.

The date clarifies the Albanians that they have to work for their state budget until to the

end of the third ten days of the third month of the year. Thereafter, work and their profits

do not go to the account of the state, but in their account. But, according to the tax burden

of each region, also by calendar year calculation results that Tax Freedom in Albanian cities

comes in different dates this year.

Days January February March April

1 Kukës 40 31 9

2 Dibër 43 31 12

3 Berat 49 31 18

4 Lezhë 58 31 27

5 Shkodër 62 31 28 3

6 Fier 66 31 28 7

7 Vlorë 83 31 28 24

8 Korçë 86 31 28 27

9 Elbasan 90 31 28 31

10 Gjirokastër 101 31 28 31 11

11 Durrës 106 31 28 31 16

12 Tiranë 107 31 28 31 17Source: INSTAT, Ministry of Finance, Local Authorities

TAX FREEDOM DAY 2015, OF ALBANIAN REGIONS

No. REGIONSCALENDAR OF TAX FREEDOM DAY, 2015

Tax Freedom comes first in the Kukes region. Residents of the area celebrate this day in the

first days of February 2015. Following them are the inhabitants of the regions of Diber,

Berat and Lezha, who celebrate Freedom Day in February 2015.

Residents of the Tirana region are the last to close the 4-month period of fiscal freedom

celebration. Data belonging them to celebrate is 17 April 2015.

As a general date, Tax Freedom Day for the entire country in 2015 will be celebrated on 29

March.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 18

Conclusion

In conclusion, we can say that the weight that keeps Albania (2% of GDP in the Balkans), or weight that keeps Kosovo (1.1% of GDP in the Balkans) belong to the countries by the last posts in the Balkans. But even though the tax burden in Albania is among the lowest in the Balkan region has a growing burden in 2014 compared with 2013. This fact is explained, as by the growth of certain tax rates, as well as to increase of processes of fiscal management. This fact is expressed to Index of Tax Freedom Day in Albania in 2015 that did not come earlier than in any other Balkan countries, as proved in the past year. Looking at net FDI, Albania is the first country in the Balkans for their share in relation to

GDP for the period 2014 showing that the effect of the tax burden and low rates is not the

primary influential in attracting investment.

Net FDI indicator tells us that if successfully will be harmonized tax rates with the increase of

management capacity and strengthening regulatory capacity and reducing corruption, then

will result in an effect that will give incentive and increase to foreign investment flows into

the country. This conclusion should apply to Albania, Kosovo and each of the other Balkan

countries.

Distributed tax burden through different regions if faced with the resources and capacities

available and if in more rational way will be textured with the impact of the role of

government programs in the distribution of investment and provision of conditions for

investors where the burden is not encouraging, then would help each city, to think more

deeply opportunities and ways to integrate within the model of economic growth of the

country.

Albania suffers a loss of tax revenue accrued to 1 billion Euros a year from tax evasion and

avoidance. But also another blow suffers effectiveness and fairness in the distribution of the

tax burden on taxpayers. Tax evasion affects us all, even though they may be sourced

internally or comes imported from abroad.

Some businesses find themselves in an unequal competition with other businesses that find

ways and means to avoid taxes that they are entitled to pay based in the law.

It is the tax burden that should attire the attention of the whole society, whether public

sector, but the private sector also should be prompted to change the approach seeking a

more equitable distribution, where everyone should feel contributor and beneficiary from

taxes paid to government.

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 19

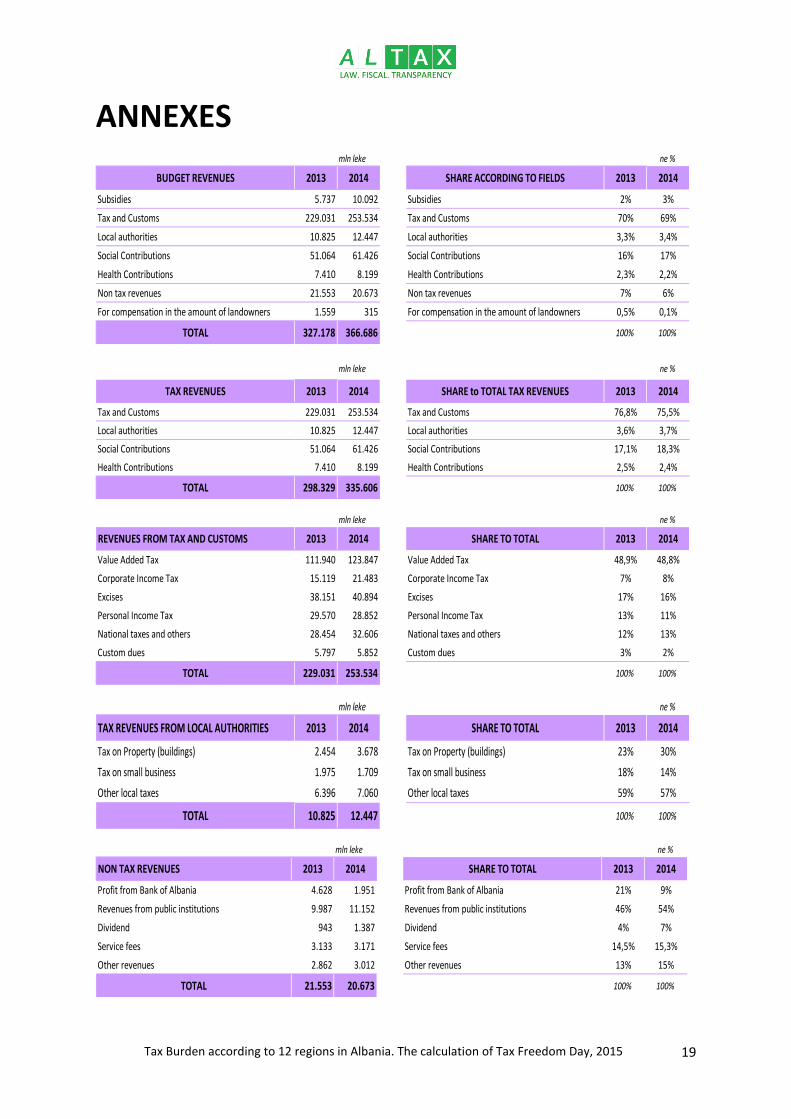

ANNEXES mln leke ne %

BUDGET REVENUES 2013 2014 SHARE ACCORDING TO FIELDS 2013 2014

Subsidies 5.737 10.092 Subsidies 2% 3%

Tax and Customs 229.031 253.534 Tax and Customs 70% 69%

Local authorities 10.825 12.447 Local authorities 3,3% 3,4%

Social Contributions 51.064 61.426 Social Contributions 16% 17%

Health Contributions 7.410 8.199 Health Contributions 2,3% 2,2%

Non tax revenues 21.553 20.673 Non tax revenues 7% 6%

For compensation in the amount of landowners 1.559 315 For compensation in the amount of landowners 0,5% 0,1%

TOTAL 327.178 366.686 100% 100%

mln leke ne %

TAX REVENUES 2013 2014 SHARE to TOTAL TAX REVENUES 2013 2014

Tax and Customs 229.031 253.534 Tax and Customs 76,8% 75,5%

Local authorities 10.825 12.447 Local authorities 3,6% 3,7%

Social Contributions 51.064 61.426 Social Contributions 17,1% 18,3%

Health Contributions 7.410 8.199 Health Contributions 2,5% 2,4%

TOTAL 298.329 335.606 100% 100%

mln leke ne %

REVENUES FROM TAX AND CUSTOMS 2013 2014 SHARE TO TOTAL 2013 2014

Value Added Tax 111.940 123.847 Value Added Tax 48,9% 48,8%

Corporate Income Tax 15.119 21.483 Corporate Income Tax 7% 8%

Excises 38.151 40.894 Excises 17% 16%

Personal Income Tax 29.570 28.852 Personal Income Tax 13% 11%

National taxes and others 28.454 32.606 National taxes and others 12% 13%

Custom dues 5.797 5.852 Custom dues 3% 2%

TOTAL 229.031 253.534 100% 100%

mln leke ne %

TAX REVENUES FROM LOCAL AUTHORITIES 2013 2014 SHARE TO TOTAL 2013 2014

Tax on Property (buildings) 2.454 3.678 Tax on Property (buildings) 23% 30%

Tax on small business 1.975 1.709 Tax on small business 18% 14%

Other local taxes 6.396 7.060 Other local taxes 59% 57%

TOTAL 10.825 12.447 100% 100%

mln leke ne %

NON TAX REVENUES 2013 2014 SHARE TO TOTAL 2013 2014

Profit from Bank of Albania 4.628 1.951 Profit from Bank of Albania 21% 9%

Revenues from public institutions 9.987 11.152 Revenues from public institutions 46% 54%

Dividend 943 1.387 Dividend 4% 7%

Service fees 3.133 3.171 Service fees 14,5% 15,3%

Other revenues 2.862 3.012 Other revenues 13% 15%

TOTAL 21.553 20.673 100% 100%

LAW. FISCAL. TRANSPARENCY

Tax Burden according to 12 regions in Albania. The calculation of Tax Freedom Day, 2015 20

REFERENCES Ministria e Financave, Statistika Fiskale Janar - Dhjetor 2014

Ministria e Financave, Buletini Fiskal (ne tremujore)

Ministria e Financave te Republikës se Kosovës, Treguesit makro dhe buxhetore 2014

INSTAT, PBB sipas rajoneve statistikore viti 2012

Tax card 2014 in Kosovo, Kpmg.com.al

Taxes at a glance 2014, pwc.com

Paying taxes 2014, pwc.com

Economywatch.com

Tradingeconomics.com

IMF, Country Reports 2014

James Rogers & Cécile Philippe, the Tax Burden of Typical Workers in the EU 28, 2014 Edition

Taxation trends in the European Union, 92/2014 - 16 June 2014

Index of Tax Freedom Report, 2015, Heritage.org

Global Magazine Editions, 2015

![[Albania] New Albania I.pdf](https://img.pdfslide.net/doc/110x75/544cfeb4b1af9f710c8b499e/albania-new-albania-ipdf.jpg)