Embed Size (px)

Citation preview

TAX IMPLICATIONS OF OWNING RENTAL REAL ESTATE

Jonathan L. Nichols, CPA

Huey and Associates, P.C.

January 11, 20117

To help make the presentation as directed and useful as possible, please feel free to email questions to [email protected] or jot your questions down here and bring them along for the Q&A session

1. ____________________________________

2. ____________________________________

3. ____________________________________

4. ____________________________________

5. ____________________________________

2

WHAT’S ON YOUR MIND?

3

BENEFITS OF LONG TERM RENTALS

NET INCOME TAXED AT ORDINARY TAX RATES

INCOME (CASH, IN-KIND OR SERVICES)

LESS EXPENSES (INTEREST, TAXES, INSURANCE)

LESS DEPRECIATION

=TAXABLE INCOME/(LOSS)

FILED ON SCHEDULE E OF FORM 1040

MANY TIMES A PROPERTY WILL BE CASH-FLOW POSITIVE BUT SHOW A NET LOSS FOR TAX PURPOSES…WHY?

THE MAGIC OF DEPRECIATION

4

HOW IS RENTAL INCOME TAXED?

Any costs paid by a tenant on your behalf are considered income to you. However, these costs are also deductible as rental expenses.

Any property or service you receive in lieu of money is considered income. This income is based on the fair market value of the property or services received.

Security deposits are not income if they are to be refunded at the end of a lease period. However, any funds withheld from a deposit are income in the year they are retained.

5

WHAT INCOME IS TAXABLE?

Commissions or property management fees,

Advertising costs,

Cleaning, maintenance, supplies and repair costs,

Homeowners insurance and HOA dues,

Real estate taxes, mortgage interest and insurance,

Home operating expenses, such as utilities, landscaping, garbage, and so forth

Mileage ($.565/mile) and Travel (primary purpose)

Depreciation

Legal expenses concerning rental property

Tax return preparation for rental forms

6

WHAT CAN BE DEDUCTED?

REPAIRS Expenditures made that do not add to the value or extend the life

of your property but rather keeps the property in good condition is a repair and immediately deductible.

IMPROVEMENTS Expenditures that result in betterment, restoration or adaptation

of a unit of property.

7

REPAIRS AND IMPROVEMENTS

8

IMPROVEMENTS

DEFINITION – Deduction for the cost of the building spread over a period of time specified by Congress Building – 27.5 years Land – Not depreciable Personal Property (Furniture, Fixtures, Land improvements) 5,7,15 years

Begins when property becomes “Rent Ready” Depreciate lesser of FMV or Cost basis If home vacant, be sure to document how you are actively seeking a

tenant

Depreciation Recapture 25% Recapture (Real Property) Ordinary Income Recapture (Personal Property)

9

MAGIC OF DEPRECIATION

Primary Residence Cost (including purchase costs)- $506,235 FMV of property when placed in service - $400,000 Land included in Cost (20%)

Check your Real estate tax home assessment

Lesser of Cost or FMV - $400,000 Land included in Cost (20%) – $80,000 Building to be Depreciated - $320,000

$320,000/27.5 = $11,636 The first $11,636 of rental income is offset by depreciation

10

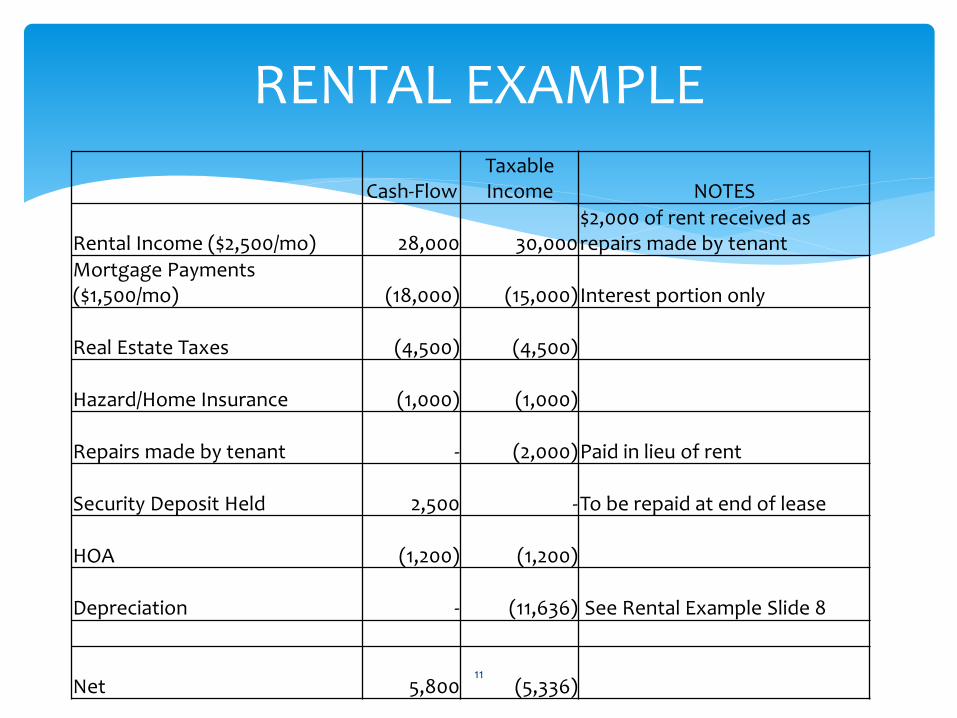

DEPRECIATION EXAMPLE

Cash-Flow Taxable Income NOTES

Rental Income ($2,500/mo)

28,000

30,000 $2,000 of rent received as repairs made by tenant

Mortgage Payments ($1,500/mo)

(18,000)

(15,000) Interest portion only

Real Estate Taxes

(4,500)

(4,500)

Hazard/Home Insurance

(1,000)

(1,000)

Repairs made by tenant

-

(2,000) Paid in lieu of rent

Security Deposit Held

2,500

- To be repaid at end of lease

HOA

(1,200)

(1,200)

Depreciation

-

(11,636) See Rental Example Slide 8

Net

5,800

(5,336) 11

RENTAL EXAMPLE

Losses from Rental Real Estate are Passive

Passive losses can only offset Passive Income

Passive income is income earned in which you do not materially participate (excluding investment income)

Unused losses are carried forward until Passive income is created or the property is sold

Active Participant Exception

Active in management in property

$25,000 of losses deductible against income per year

Phase-out AGI between $100K-$150K ($.50 on the dollar over $100K) 12

USING REAL ESTATE LOSSES

Taxpayer AGI (w/o rental activity) $ 140,000

AGI in excess of $100,000 base $ 40,000

Reduction in available loss (50%) $ 20,000

Maximum Active Participation Loss $ 25,000

Reduction in available loss $ 20,000

Maximum deductible loss $ 5,000

Maximum deductible loss $ 5,000

Current Year Taxable Loss $ (5,336)

Excess loss carryover $ (336) 13

ACTIVE PARTICIPATION EXAMPLE

Two tests More than 750 hours in qualified real estate activities

> 5% owner

Per activity

Election to group activities

Time spent in real estate is greater than time spent in ALL OTHER income producing activities combined

Real Estate Professional Exception Must materially participate in order to treat losses as non-passive

(§469(c)(7))

May need to aggregate activities

Either taxpayer or spouse can meet requirements

14

REAL ESTATE PROFESSIONAL

Create Passive Income Income from rental real estate Gain from the sale of rental real estate Income from other passive activities

LP interest in an active business Any other investment in active business in which you do not

materially participate (Real estate development)

Sale of property Unused passive losses not lost – carry forward to future years Passive losses released when property is sold (watch

aggregation) Gain on sale of passive activity is passive

15

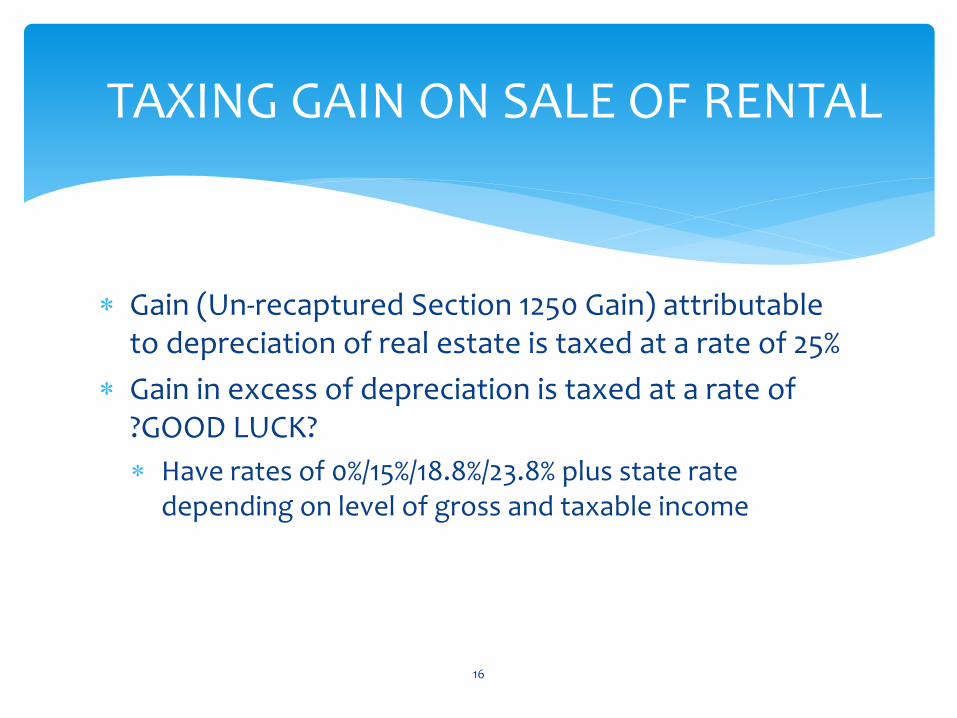

USING PASSIVE LOSSES

Gain (Un-recaptured Section 1250 Gain) attributable to depreciation of real estate is taxed at a rate of 25%

Gain in excess of depreciation is taxed at a rate of ?GOOD LUCK?

Have rates of 0%/15%/18.8%/23.8% plus state rate depending on level of gross and taxable income

16

TAXING GAIN ON SALE OF RENTAL

Home Sale Exclusion – “Two of Five Rule”

Taxpayer Relief Act of 1997

Owned and Used a property as your Primary Residence for 24 months of the previous 60 months from date of sale

Exclude $250K single, $500K joint

Generally eligible once every two years

Loss on sale of primary residence is not deductible

17

PRIMARY RESIDENCE GAIN EXCLUSION

Reduced Exclusion for “Unforeseen Circumstances”

Health

Change in employment

Divorce

Man-made disasters

Depreciation Recapture periods after May 6, 1997

Nonqualified Use of property after 12/31/2008

Military Exception (2 of 15 rule)

Extends 5 year rule by 10 years

See article enclosed in materials

18

EXCEPTIONS TO “2 OF 5”

Adjusted Cost Basis for Rental Property The formula for calculating your cost basis on rental property is as follows: Purchase price + Purchase costs (title & escrow fees, real estate agent commissions, etc.) + Improvements (replacing the roof, new furnace, etc.) + Selling costs (title & escrow fees, real estate agent commissions, etc.) - Accumulated depreciation (as reported on your tax forms) = Cost Basis And then calculating your gain or loss would be: Selling price - Cost Basis = Gain or Loss

19

CALCULATING GAIN/(LOSS) ON SALE OF RENTAL PROPERTY

ASSUMPTIONS

Sales Price $600,000

Sales costs (8%) - $48,000

Improvements made to sell home - $5,000

Selling home from slide 10

Home used as primary residence 2 of previous 5 years

20

EXAMPLE – SELLING YOUR RENTAL PROPERTY

STEP ONE: Compute Cost Basis

21

SELLING YOUR RENTAL PROPERTY

Purchase Price 500,000.00

Purchase Costs 6,235.00

Improvements 5,000.00

Selling Costs 48,000.00

Accum Depreciation (11,636.00)

COST BASIS 547,599.00

STEP TWO – Compute Gain

STEP THREE – Compute Taxable Gain

Watch Nonqualified Use

22

SELLING YOUR RENTAL PROPERTY

Selling Price $ 600,000.00

Cost Basis $ (547,599.00)

GAIN ON SALE $ 52,401.00

GAIN ON SALE 52,401.00

Depreciation Recapture (25%) 11,636.00

Gain excluded 2 of 5 rule 40,765.00

Very complicate piece of legislation

Meant to trap Vacation Home buyers

Any use of a property (not as a primary residence) beginning January 1, 2009 will limit the amount of the gain that can be excluded by the home sale exclusion Portion of gain not eligible to be excluded is the gain from

sale multiplied by the ratio of years used for nonqualified uses over total years of ownership

Exception in place for nonqualified use after a home has been used as a primary residence

23

NONQUALIFIED USE

Starting in 2013, net rental activity is included in calculation of Medicare Surtax

AGI > $200K/$250K

Added benefit or additional tax?

Watch sale of investment home

24

MEDICARE SURTAX

Renting Foreign Property US has world-wide taxation view Depreciation 40 years vs. 27.5 Watch Foreign Bank Disclosures – FIN 114, Form 8938

Buying and owning a home and residency (BE CONSISTENT) Homestead Tuition 469(j) election State income tax Home sale exclusion

Real Estate Professional and grouping Maximize benefit of deductions in first year (when does rental start?)

Start-up costs

Passive Loss Harvesting Maximize depreciation

Cost Segregation

Plan for Active Participation

25

PLANNING CONSIDERATIONS

SCHEDULE E INSTRUCTIONS https://www.irs.gov/pub/irs-dft/i1040se--dft.pdf

IRS PUBLICATION 527 http://www.irs.gov/pub/irs-pdf/p527.pdf

EMAIL [email protected]

26

RESOURCES