Embed Size (px)

Citation preview

International Introduction Tax Issues for Foreigners at Aarhus University

Autumn 2013

SKAT, Markedsføring, Aarhus

International Introduction

Programme - topics

Ordinary tax system

Preliminary income assessment

Income tax return

Annual tax assessment notice

Tax on the internet - www.skat.dk

Side 2

International Introduction

New to Denmark

Side 3

International Introduction

International Citizen Service

International Citizen Service West Nordhavnsgade 4-6 8000 Aarhus C

Phone: +45 72 22 33 75 Mail: [email protected]

Opening hours: Thursday 1 p.m. – 5 p.m. and Friday 9 a.m. – 1 p.m.

Get off to a good start in Denmark – all the service you need in one place!

Side 4

International Introduction

Who pays tax in Denmark ?

• Any person living in Denmark must pay tax in Denmark - full tax liability.

• Any person working – but not living - in Denmark must pay some tax (on wages, salary etc.) – limited tax liability.

International Introduction

Side 5

International Introduction

Your tax status in Denmark

If you have been working at Aarhus University for more than six months, you will be subject to full tax liability.

You will be taxed on your global income.

A tax agreement to avoid double taxation between Denmark and your home country may regulate the tax to be paid.

International Introduction

Side 6

International Introduction

Your information to SKAT at arrival

You have to send this to SKAT:

Form no. 04.063 E

Copy of your letter of employment.

International Introduction

Side 7

International Introduction

Form no. 04.063 E

International Introduction

Side 8

International Introduction

You will receive a preliminary tax assessment from SKAT right away when getting a CPR-nummer (civil registration no.). Whenever you submit corrections to SKAT during the year about your current income you will receive a new preliminary tax assessment . In November you will automatically get an preliminary assessment for next year.

Check it! You must do this yourself.

Please inform SKAT of your global (foreign + Danish) income, i.e. interest from bank accounts, every year.

You can submit the information via E-tax (SKAT’s self-service facility – TastSelv) at www.skat.dk

Paying tax in Denmark – preliminarily

International Introduction

Side 9

International Introduction

Side 10

Paying tax in Denmark - tax assessment

The Danish tax year runs from 1 January to 31 December.

In March you will receive a tax assessment notice for the previous year.

The tax assessment notice contains information about your income and deductions etc. and taxes paid on income from the previous year and information from your employer, banks etc.

You can view your tax assessment notice for 2013 in your tax folder via E-tax (TastSelv) at www.skat.dk.

International Introduction

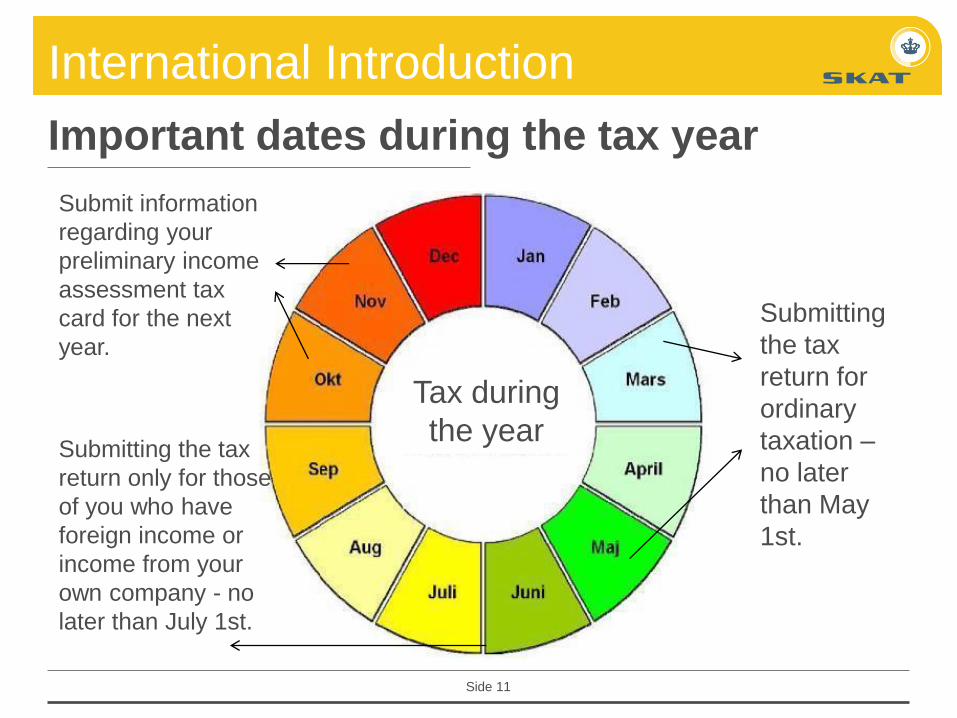

Important dates during the tax year

Tax during

the year

Submitting

the tax

return for

ordinary

taxation –

no later

than May

1st.

Submit information

regarding your

preliminary income

assessment tax

card for the next

year.

Submitting the tax

return only for those

of you who have

foreign income or

income from your

own company - no

later than July 1st.

Side 11

International Introduction

As an ordinary taxpayer in Denmark you have to inform SKAT of your foreign income or foreign property – every year.

Danish income like salary, interest, etc. is automatically put on your

tax assessment notice.

You can apply for tax deductions like any other Danish taxpayer.

Paying tax in Denmark

Side 12

International Introduction

Employees taxed in Denmark on salary are allowed certain tax deductions/allowances:

• You are allowed to earn DKK 43,000 before your start paying tax (this is known as your personal allowance (personfradrag)

• Special employment allowance up to DKK 22,300

• Deduction for transport between home and work - if more than 24 km a day – no matter whether you have got any expenses or not

• Interest payments - both Danish and foreign

• Pension scheme contributions - made by you

• Contributions to unemployment fund and trade union membership

• Deduction for meals and accommodation expenses, under certain conditions, during travelling.

Tax deductions/allowances in Denmark

International Introduction

Side 13

International Introduction

Deduction for transport

Transport between home and work :

Rates for 2013: Rates for 2014:

0 - 24 km No deduction No deduction 25 - 120 km DKK 2.13 per km (do not know yet) 121 km - DKK 1.07 per km (do not know yet)

International Introduction

Side 14

International Introduction

Tax and pensions schemes

You can take your foreign pension scheme with you to Denmark and get a tax deduction.

For more information, you need to contact SKAT, who must approve your pension scheme.

You must submit form no. 07.055E for SKAT’s approval.

Side 15

International Introduction

If sent out by their employer employees may apply for the following tax deductions during the travel:

- up to a maximum of DKK 25,000.

The deduction for food is only allowed for the first 12 months.

The deduction for accommodation can be allowed for up to 24 months.

Please note that you have to meet certain conditions in order to get the deductions.

Deduction for food and accommodation expenses

International Introduction

Food: DKK 455 per day (24 hours)

Accommodation: DKK 195 per day (24 hours)

Side 16

International Introduction

Forskudsopgørelse – Preliminary income assessment – tax card

1 Your salary after deduction of labour market contributions (AM-bidrag)

2 Total provisional tax calculated for the year

3 Total preliminary labour market contributions calculated at the rate of 8%

4 The tax per cent that will be deducted from your salary

5 Your monthly tax-free amount

1

2

3

4 5

Side 17

International Introduction

Calculation Your salary

Monthly salary after deduction

of pension contributions DKK 33,971 DKK 33,971

Labour market contributions at 8% DKK -2,718 DKK -2,718

Salary after deduction of labour market contributions DKK 31,253

Deductions as stated on your tax card DKK -8,232

Salary to be taxed at the rate of 37% DKK 23,021

Tax deducted (A-skat) at the rate of 37% DKK -8,518 DKK -8,518

You will receive DKK 22,735

Monthly salary and tax deduction

International Introduction

Side 18

International Introduction

You will probably receive a tax assessment notice from SKAT automatically

CHECK IT – You are obliged to do so!

If it is incorrect, please submit the right information to SKAT.

The self-service site at www.skat.dk opens in March.

Tax assessment notice

International Introduction

Side 19

International Introduction

Tax information card (Oplysningskort)

International Introduction

Side 20

International Introduction

Side 21

If you have had :

• income from your own business (are self-employed)

• foreign income from employment or securities abroad

• income from rental property

- then you have to submit an income tax return for 2013.

You can download a tax return for foreign income on www.skat.dk,

Form no. 04.012.

Please note there are different forms – depending on whether you have

had foreign income or not.

Tax return for the tax assessment

International Introduction

Income from abroad – form no. 04.012 E

If you have any income from abroad while staying in Denmark, and you are subject to full tax liability in Denmark, you also have to submit form no. 04.012 E - The tax return for foreign income.

Side 22

International Introduction

Property abroad – form no. 04.053 EN

You also have to submit the form 04.053 if you own a property abroad

Side 23

International Introduction

E-tax (TastSelv) on the internet

International Introduction

Side 24

International Introduction

Side 25

International Introduction

Tastselv – how to check your tax information

International Introduction

Side 26

International Introduction

Side 27

International Introduction

In the tax folder you will find:

• Your preliminary income assessment and tax assessment notice in PDF format. The latest will always be the "current“, but you can also view the previous one as well as other records.

• Information reported to SKAT by your employers, banks, pension funds, etc.

• Current salary and e-tax card; you can see information about your payslips and which employer uses your tax card.

• A "log" which is a summary of the entries you or SKAT have made in E-tax.

• Information about your property.

Side 28

International Introduction

Side 29

Advantages of using E-tax (TastSelv)

If you have any changes to your tax assessment notice, you can use E-tax at skat.dk.

There you can

• view your new tax assessment notice right away – and print it if you like.

• click on the text for each box to see detailed information about your income, deductions etc.

• print any of your tax assessment notices from the tax folder. The version you print yourself is identical to the one SKAT sends you and is valid in exactly the same way.

International Introduction

Side 30

Overpaid tax (NemKonto)

If you have paid too much tax, you will (nearly at the same time as you receive your tax assessment notice in March) get a tax refund transferred to your Nem-konto.

You will get a tax-free interest of 0.5% of the amount.

The tax refund will be paid to your NemKonto in March.

International Introduction

Overpaid tax (foreign banks)

If your tax assessment notice states that you have paid too much tax, and if you do not have a Danish NemKonto, please inform SKAT of your IBAN number and SWIFT/BIC code as well as your Danish civil registration number (CPR) by e-mail.

Please note that it may take up to 90 days before the tax refund is credited your foreign account.

Side 31

International Introduction

Side 32

Overpaid tax

Payment of overpaid tax if you have left Denmark:

SKAT calculates your tax and makes a tax assessment notice for you on the basis of the information SKAT has received about your income. But SKAT very often does not have information about the date you left Denmark, and therefore the tax calculation is carried out on the assumption that you are tax liable for the entire year.

In many cases this assessment is incorrect, and SKAT therefore retains any overpaid tax until you have informed us about when you left Denmark for good.

International Introduction

Side 33

Underpaid tax

Pay the rest of your tax in time and save money!

• Until 1 July you must pay a day-to-day interest of 2.7%.

• After 1 July, you must pay an interest of 4.7%.

International Introduction

Side 34

Day-to-day interest (underpaid tax)

Example of calculation of interest (before 1 July):

Thomas Jensen has paid too little tax: DKK15,000.

At the end of March, he chooses to pay the tax on 31 March.

He must pay interest for 91 days (from 1 January to 1 April) as follows:

DKK 15,000 x 2.7% x 91 days = DKK 100.97 (DKK 101)

365 days

Total payment DKK 15,101.00

International Introduction

Side 35

Underpaid tax

If your tax assessment notice shows that you have paid too little tax and you wish to pay the rest from a foreign bank account, you need an IBAN number (International Bank Account Number) and a SWIFT/BIC code in order to pay SKAT:

IBAN number: DK94 3000 0007540531 SWIFT/BIC code: DABADKKK

You must write your Danish civil registration number (CPR) and which year the payment concerns.

International Introduction

Leaving Denmark?

Please remember to

• inform SKAT about your residence and other relevant information about your stay abroad when leaving Denmark

• fill in form no. 04.029E and send it to SKAT. If you are moving abroad (including to Greenland or the Faroe Islands), your tax liability has to be determined.

Side 36

International Introduction

Any questions?

Thank you for your attention!

Side 37