Embed Size (px)

Citation preview

TAX NEWS

VOL.XXXV SEPTEMBER-DECEMBER 2012 No.6

ANDHRA CHAMBER OF COMMERCE

(For Private Circulation)

C O N T E N T S

I - DIRECT TAXES

Income-Tax ( Ninth Amendment) Rules, 2012 – Substitution of Rule 40BA and Form No. 29CI

Income-Tax (Tenth Amendment) Rules, 2012

Income-Tax (Eleventh Amendment) Rules, 2012 - Insertion of Rules 31ACB, 37J, Form Nos. 26A & 27BA

Income Tax (Twelfth Amendment) Rules 2012

Income Tax (13th

Amendment) Rules, 2012

Income-Tax (Fourteenth Amendment) Rules, 2012

II - CENTRAL SALES TAX CST Act, 1956 – Loss of Blank or duly filled ,”C‟ declaration forms – pro-cedure prescribed for obtaining Duplicate forms under CST (R &T) Rules,1957 CST – Sale of Hosiery goods without "C" Form – scheme of refund of tax collected as special incentive ordered – revised orders (T.N.)

2

CST Act, 1956 – Cancellation process of „C‟ declaration forms and obtaining new „C‟ forms-procedure in CDSC application APVAT Act,2005 & CST Act, 1956 – Misuse of „C‟ Form by the Works contractors APVAT Act, 2005 & CST Act, 1956 – Misuse of „C‟ form

III - TAMIL NADU VALUE ADDED TAX

TNVAT Act, 2006 -- Introduction of Section 63-a -- filing of Form WW Tamil Nadu Value Added Tax Act, 2006 – Exemption from payment of value added tax on purchase of goods by Police Canteens in Tamil Nadu as well as subsequent sale to the serving and retired state police personnel and to the serving, retired and deceased uniformed personnel of fire and rescue services and prisons and their families Banks for availing of E-payment facility Creation of the large Tax payers‟ unit (LTU) at Chennai Tamil Nadu Value Added Tax Act, 2006 – Reduction of VAT on generating sets (gen-sets) used for producing Electricity from 14.5% to 5%

Tamil Nadu Value Added Tax Act, 2006 – Exemption from payment of Value Added Tax on the sale of Furnace oil for use in Gen-sets by the HT consumers for the period from 1.10.2012 to 31.5.2013

Tamil Nadu tax on Entry of Motor Vehicles into Local Areas Act, 1990 – Embassies/Consulates of 119 countries - Exemption from payment of Entry Tax

IV - ANDHRA PRADESH VALUE ADDED TAX

APVAT Act, 2005 – issue of notification under sub-rule (4) of rule 55 of APVAT rules,2005 – certain category of manufacturers are notified as ineligible to use the gate pass cum-invoice as waybill APVAT Act,2005- Audit and Assessments APVAT Act,2005- Audit and Assessments – issuing notices calling for books of accounts by the CTOs Tax deduction at source - Generation of VAT Form 501 A Online

TAX NEWS PUBLISHED BY

ANDHRA CHAMBER OF COMMERCE

CHENNAI OFFICE:

―Velagapudi Ramakrishna Building‖, 23, Third Cross Street, West C.I.T. Nagar, P.B. No.3368, Nanadanam Chennai-600 035 GRAMS: ―TELCHAMBER‖ PHONE: OFFICE: 24315277 Secy. (Per) 24315278 (Fax): 24315279 E.mail: [email protected] Web: www.andhrachamber.com

SECUNDERABAD OFFICE: “T.G. Venkatesan Bhavan”

60-2 & 603, Chenoy Trade Centre, VI Floor,

116, Park Lane, P.B.No.1716, Secunderabad-500 003 (A.P.)

GRAMS: “TELCHAMBER” PHONE:27840844

Jt. Secy. Per:040-27840767 Fax: 040-27840767

E.mail: [email protected]

VISAKHAPATNAM OFFICE: Door No. 43-19-30,

Venkataraju Nagar, Dondaparthy,

Near TSN Colony, Visakhapatnam-530 016 (A.P.)

GRAMS: “TELCHAMBER” PHONE:0891-2792220 Fax :0891-2792221

Email:[email protected]

(for Private Circulation only) (All correspondence relating to the publication may be addressed to CHENNAI office)

VOL.XXXV SEPTEMBER-DECEMBER, 2012 No.6

I - DIRECT TAXES INCOME-TAX ( NINTH AMENDMENT) RULES, 2012 – SUBSTITUTION OF RULE 40BA AND FORM NO. 29C: Vide Notification No. 34/2012 [F.No.142/22/2012-SO[TPL}-SO.1979(E) dated August 20, 2012 issued by the Central Board of Direct Taxes, Department of Revenue, Ministry of Finance, Government of India and published in the Gazette of India Extraordinary Part-II, Section 3, Sub-Section (ii).

In exercise of the powers conferred by section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax ( Ninth Amendment) Rules, 2012.

(2) They shall come into force on the 1st day of April, 2013.

2. In the Income-tax Rules, 1962,(hereafter referred to as the ―said rules‖), for rule 40BA, the following rule shall be substituted, namely:-

“Special provisions for payment of tax by certain persons other than a company. 40BA. The report of an accountant which is required to be furnished by the assessee under sub-section (3) of section 115JC, shall be in form No. 29C.‖.

4

3. In Appendix-II of the said rules, for Form No. 29C, the following form shall be substituted, namely:- Form NO. 29C – Report under Section 115JC of the Income-Tax Act, 1961 for computing adjusted total income and alternate mini-mum tax of the person other than a company.

P.S.: Form No. 29C which run to 2 pages, has not been reproduced in this issue. The full text of the notification is available in the office of the Chamber for perusal of members. Interested members may obtain a copy of same from the office of the Chamber on request by Email.

INCOME-TAX (TENTH AMENDMENT) RULES, 2012:

Vide Notification No. 36/2012 [F.No.133/5/2012-SO (TPL)/SO 2005(E) dated August 30, 2012 issued by the Central Board of Direct Taxes, Department of Revenue, Ministry of Finance, Government of India and published in the Gazette of India Extraordinary Part-II, Section 3 Sub-Section (ii).

In exercise of the powers conferred by sub-section (9) of section 92CC read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1). These rules may be called the Income-tax (10th Amendment) Rules, 2012.

(2). They shall come into force on the date of their publication in the official Gazette.

2. In the Income-tax Rules, 1962 (hereafter referred to as the principal rules), - (a) after rule 10E, the following rule shall be inserted, namely.- ―Advance Pricing Agreement Scheme

Meaning of expressions used in matters in respect of advance pricing agreement.

10F For the purposes of this rule and rules 10G to 10T,– (a) ‗agreement‘ means an advance pricing agreement entered into between the Board and the appli-cant, with the approval of the Central Government, as referred to in sub-section (1) of section 92CC of the Act;

Persons eligible to apply

10G Any person who –

(i) has undertaken an international transaction; or (ii) is contemplating to under-take an international transaction, shall be eligible to enter into an agreement under these rules.

5

Pre-filing Consultation

10H (1) Every person proposing to enter into an agreement under these rules shall, by an application in writing, make a request for a pre-filing consultation.; (2) The request for pre-filing consultation shall be made in Form No. 3 CEC to the Director General of Income Tax (International Taxation). ; (3) On receipt of the request in Form No. 3 CEC, the team shall hold pre-filing consultation with the person referred to in rule 10G.; (4) The competent authority in India or his representative shall be associated in pre-filing consultation involving bilateral or multilateral agreement. ; (5) The pre-filing consultation shall, among other things,- (i) determine the scope of the agreement; (ii) identify transfer pricing issues; (iii) determine the suitability of international transaction for the agreement; (iv) discuss broad terms of the agreement.

(6) The pre-filing consultation shall–

(i) not bind the Board or the person to enter into an agreement or initiate the agreement process; (ii) not be deemed to mean that the person has applied for entering into an agreement.

P.S.: The full text of the Notification is available in income tax. Please click http://law.incometaxindia.gov.in/DIT/File_opener.aspx?page=NOTF&schT=&csId=6e3cf0a5-7f42-4222-88c8-b50a17284016&NtN=&yr=ALL&sec=&sch=&title=Taxmann - Direct Tax Laws to download the full notification .

INCOME-TAX (ELEVENTH AMENDMENT) RULES, 2012 - INSERTION OF RULES 31ACB, 37J, FORM NOS. 26A & 27BA:

Vide Notification No. 37/2012[F.No.142/18/2012-SO(TPL) dated September 12, 2012 issued by the Ministry of Finance, Government of India, New Delhi.

In exercise of the powers conferred by section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the fol-lowing rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (11th Amendment) Rules, 2012; (2) They shall come into force on the date of publication in the Official Gazette.

2. In the Income-tax Rules, 1962, (hereafter referred to as the "said rules"),- (a) after rule 31ACA, the following rule shall be inserted, namely:- "Form for furnishing certificate of accountant under the first proviso to sub-section (1) of section 201.

6

31ACB. The certificate from an accountant under first proviso to sub-section (1) of section 201 shall be furnished in Form No.26A";

(b) after rule 37-I, the following rule shall be inserted, namely:- "Form for furnishing certificate of accountant under first proviso to sub-section (6A) of section 206C

37J. The certificate from an accountant under first proviso to sub-section (6A) of section 206C shall be furnished in Form No. 27BA."

3. In Appendix-II to the said rules.- (a) after Form No. 26, the following form shall be inserted, namely.— "FORM No. 26A [See rule 31ACB] .

P.S.: Form No. 26A -- Form for furnishing accountant certificate under the first proviso to sub-section (1) of section 201 of the Income-tax Act, 1961; Annexure-A -- Certificate of accountant under first proviso to sub-section (1) of section 201 of the Income-tax Act, 1961 for certifying the furnishing of return of income, payment of tax etc. by the payee; FORM No. 27BA -- Form for furnishing accountant certificate under first proviso to sub-section (6A) of section 206C of the Income-tax Act, 1961; ANNEXURE A -- Certificate of accountant under first proviso to sub-section (6A) of section 206C of the Income-tax Act, 1961 for certifying the furnishing of return of income, payment of tax etc. by the buyer/licensee/lessee which run to 7 pages, have not been reproduced in this issue. The full text of the notification is available in the office of the Chamber for perusal of members. Interested members may obtain a copy of same from the office of the Chamber on request by Email. INCOME TAX (TWELFTH AMENDMENT) RULES 2012:

Vide Notification No. S.O. 2188 dated September 17, 2012 issued by the Ministry of Finance, Government of India, New Delhi.

In exercise of the powers conferred by section 90 and 90A read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1). These rules may be called the Income-tax (12th Amendment) Rules, 2012.; (2). They shall come into force on the 1st day of April, 2013.

2. In the Income-tax Rules, 1962 (hereafter referred to as the principal rules), - (a) after rule 21AA, the following rule shall be inserted, namely.- ―Certificate for claiming relief under an agreement referred to in section 90 and 90A. 21AB (1) The certificate referred to in sub-section (4) of section 90 and

7

sub-section (4) of section 90A to be obtained by an assessee, not being a resident in India, from the Government of the country or the specified territory shall contain the following particulars, namely:-

(i) Name of the assessee; (ii) Status (individual, company, firm etc.) of the assessee;

(iii) Nationality (in case of individual); (iv) Country or specified territory of incorporation or registration (in case of others); (v) Assessee‘s tax identification number in the country or specified territory of residence or in case no such number, then, a unique number on the basis of which the person is identified by the Government of the country or the specified territory; (vi) Residential status for the purposes of tax; (vii) Period for which the certificate is applicable; and (viii) Address of the applicant for the period for which the certificate is applicable;

(2) The certificate referred to in sub-rule (1) shall be duly verified by the Government of the country or the specified territory of which the assessee, referred to in sub-rule (1), claims to be a resident for the purposes of tax.

(3) An assessee, being a resident in India, shall, for obtaining a certificate of residence for the purposes of an agreement referred to in section 90 and section 90A, make an application in Form No. 10FA to the Assessing Officer.

(4) The Assessing Officer on receipt of an application referred to in sub-rule (3) and being satisfied in this behalf, shall issue a certificate of residence in respect of the assessee in Form No. 10FB.‖;

(b) in Appendix-II, after the Form No. 10F, the following Forms shall be inserted, namely:-

P.S.: FORM No. 10FA – Application for Certificate of residence for the purposes of an agreement under section 90 and 90A of the Income Tax Act, 1961; FORM No. 10FB -- Certificate of residence for the purposes of

section 90 and 90A which run to 3 pages, have not been reproduced in this issue. The full text of the notification is available in the office of the Chamber for perusal of members. Interested members may obtain a copy of same from the office of the Chamber on request by Email.

8

INCOME TAX (13TH

AMENDMENT) RULES, 2012:

Vide Notification No. S.O. 2261 dated September 20, 2012 issued by the Minis-try of Finance, Government of India, New Delhi.

In exercise of the powers conferred by section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Government hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (13th Amendment) Rules, 2012.; (2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Income-tax Rules, 1962, in rule 17C, after clause (vii), the following clause shall be inserted, namely:- ―(viii) investment in debt instruments issued by any infra-structure Finance Company registered with the Reserve Bank of India.‖ INCOME-TAX (FOURTEENTH AMENDMENT) RULES, 2012:

Vide Notification No. 42/2012 [F.NO.282/22/2012-IT (INV. V)], dated October 4, 2012, Ministry OF Finance, Government of India, New Delhi.

In exercise of the powers conferred by section 153A and 153C of the Income-tax Act, 1961 (43 of 1961) (hereinafter referred to as the Act), the Central Government hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (i) These rules may be called the Income-tax (14th Amendment) Rules, 2012.; (ii) They shall come into force from the 1st day of July, 2012.

2. In the Income-tax Rules, 1962, after rule 112E, the following rule shall be inserted, namely:

"Class or Classes of cases in which the Assessing Officer shall not be required to issue notice for assessment or reassessment of the total income for six assessment years immediately preceding the assessment year. 112F. The class or classes of cases in which the Assessing Officer shall not be required to issue notice for assessing or reassessing the total income for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made, shall be the cases-

(i) where, as a result of a search under sub-section (1) of section 132 of the Act or a requisition made under section 132A of the Act, a person is found to be in possession of any money, bullion, jewellery or other valuable articles or things, whether or not he is the actual owner of such money, bullion, jewellery etc.; and (ii) where, such search is conducted or such requisition is made in the territorial area of an assembly or parliamentary constituency in respect of which

9

a notification has been issued under section 30 read with section 56 of the Representation of the People Act, 1951 (43 of 1951), or where the assets so seized or requisitioned are connected in any manner to the ongoing election in an assembly or parliamentary constituency.

Provided that this rule shall not be applicable to cases where such search under section 132 or such requisition under section 132A has taken place after the hours of poll so notified;

Provided further that this rule shall not be applicable to cases where any assessment or reassessment has abated under the second proviso to section 153A and where any assessment or reassessment has abated under section 153C".

II - CENTRAL SALES TAX CST ACT, 1956 – LOSS OF BLANK OR DULY FILLED „C‟ DECLARATION FORMS – PROCEDURE PRESCRIBED FOR OBTAINING DUPLICATE FORMS UNDER CST (R &T) RULES,1957:

Vide CCT‘s Ref. Enft/ D2/50/2012 dated July 20, 2012 issued by the Commercial Taxes Department, Government of Andhra Pradesh.

Certain dealers are requesting department to guide them for obtaining duplicate „C‟ declaration forms in place of Original Blank or duly filled ―C‟ declaration forms lost by them either in the custody of the purchasing dealer or in transit to the selling dealer.

As per the Rule 10 of CST (AP) Rules „Every registered dealer and every dealer liable to pay tax under the Act shall maintain a register in Form 12 (CST IV/ XIII) showing a true and correct account of declaration in Form ―C‟/Form ―F‟‟ received from the notified authority . If any form is lost, destroyed or stolen he shall report the same to the said authority immediately and shall make appropriate entries in the remarks column of the register concerned.

The purchasing dealer in the State of A.P. who lost a blank or duly completed ―C‟ declaration form while in his custody or in transit to the selling dealer shall furnish an indemnity bond in Form ‗G‘ to the CTO concern as prescribed under sub-rule 2 of Rule 12 of CST(R & T) Rules 1957. If more than one „C‟ declaration form is lost the purchasing dealer may furnish one such indemnity bond to cover all the forms of declarations so lost as per the proviso under sub-rule 2 of Rule 12 of CST (R & T) Rules 1957.

On receipt of such indemnity bond, CTO concern after satisfying himself, can issue duplicate C Form by writing boldly ―Duplicate C Form‖ on it.

The issuing authorities concerned may please take necessary action accordingly in such cases.

10

CENTRAL SALES TAX – SALE OF HOSIERY GOODS WITHOUT "C" FORM – SCHEME OF REFUND OF TAX COLLECTED AS SPECIAL INCENTIVE ORDERED – REVISED ORDERS (T.N.):

Vide G.O. (Ms) No.132 dated October 11, 2012 issued by the Commercial Taxes and Registration (C1) Department, Government of Tamil Nadu.

ORDER:

In the Government Order first read above, a scheme of Special Industrial Incentive has been introduced on the sale of Hosiery goods whereby tax at the rate of 10% should be collected from the dealers on inter-State sales of hosiery goods, if made without C Form and 90% of the tax collected will be refunded as a specific industrial incentive so that the effective rate will be 1%, subject to the following conditions:-

a) the dealers who make inter-State sale of hosiery goods and file ‗C‘ form declarations shall be assessed at the reduced rate of 1% as per the Government Notification No. II(1)/CTRE/84(a-2)/96, dated 5.8.1996.

b) the dealers who make inter-State sale of hosiery goods but could not file ‗C‘ form declarations shall be assessed at 10% as per the mandatory provisions of filing of ‗C‘ forms under the Central Sales Tax Act, 1956 effective from 13.5.2002.

c) to give effect to the notified reduced rate of 1% to the dealers who are assessed at 10% referred to in clause (b) above, the difference between the amount of tax assessed at 10% and the amount of tax at reduced rate of 1% shall be given refund.

d) the refund of 90% of the tax paid shall be treated as specific industrial incentive to the dealers referred to above.

2. Consequent to the amendment to Section 8 of the Central Sales Tax Act, 1956 with effect from 1.4.2007, inter-State sales of hosiery goods without ‗C‘ form declaration are liable to Central Sales Tax at 4% being the rate applicable to the sale of hosiery goods inside the State under Tamil Nadu Value Added Tax Act, 2006. Accordingly, the scheme of repayment of Central Sales Tax on hosiery goods as specific industrial incentive was modified and the rate of tax for inter-State sale of hosiery goods without ‗C‘ form was revised from 10% to 4% in the Government Order second read above.

3. In the Government Order third read above, the rate of tax in respect of commodities specified in Part B to the First Schedule of the Tamil Nadu Value Added Tax Act, 2006 has been increased from 4% to 5% with effect from 12.7.2011.

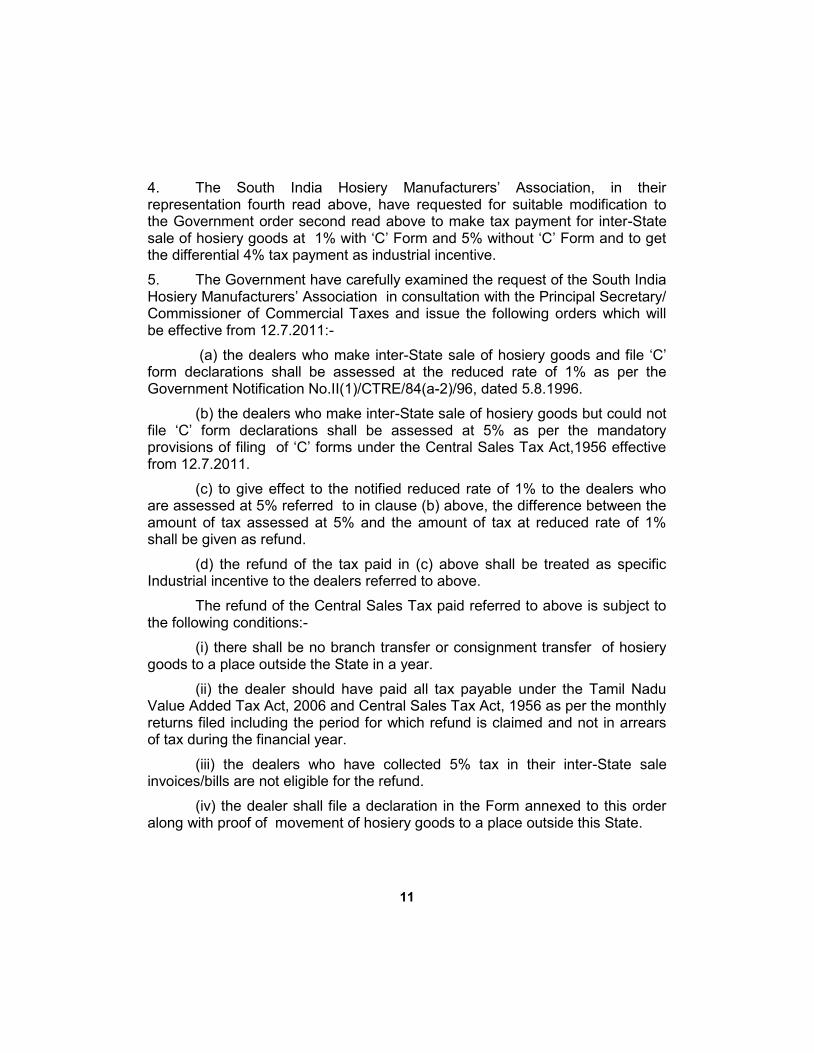

11

4. The South India Hosiery Manufacturers‘ Association, in their representation fourth read above, have requested for suitable modification to the Government order second read above to make tax payment for inter-State sale of hosiery goods at 1% with ‗C‘ Form and 5% without ‗C‘ Form and to get the differential 4% tax payment as industrial incentive.

5. The Government have carefully examined the request of the South India Hosiery Manufacturers‘ Association in consultation with the Principal Secretary/Commissioner of Commercial Taxes and issue the following orders which will be effective from 12.7.2011:-

(a) the dealers who make inter-State sale of hosiery goods and file ‗C‘ form declarations shall be assessed at the reduced rate of 1% as per the Government Notification No.II(1)/CTRE/84(a-2)/96, dated 5.8.1996.

(b) the dealers who make inter-State sale of hosiery goods but could not file ‗C‘ form declarations shall be assessed at 5% as per the mandatory provisions of filing of ‗C‘ forms under the Central Sales Tax Act,1956 effective from 12.7.2011.

(c) to give effect to the notified reduced rate of 1% to the dealers who are assessed at 5% referred to in clause (b) above, the difference between the amount of tax assessed at 5% and the amount of tax at reduced rate of 1% shall be given as refund.

(d) the refund of the tax paid in (c) above shall be treated as specific Industrial incentive to the dealers referred to above.

The refund of the Central Sales Tax paid referred to above is subject to the following conditions:-

(i) there shall be no branch transfer or consignment transfer of hosiery goods to a place outside the State in a year.

(ii) the dealer should have paid all tax payable under the Tamil Nadu Value Added Tax Act, 2006 and Central Sales Tax Act, 1956 as per the monthly returns filed including the period for which refund is claimed and not in arrears of tax during the financial year.

(iii) the dealers who have collected 5% tax in their inter-State sale invoices/bills are not eligible for the refund.

(iv) the dealer shall file a declaration in the Form annexed to this order along with proof of movement of hosiery goods to a place outside this State.

12

It is further ordered that the assessing authority shall make the refund to the dealers immediately, who satisfy the above conditions on receipt of the claim with the documents prescribed above after confirming the realization of the tax at 5% paid by them.

6. This order issues with the concurrence of the Finance Department vide its U.O.No.41466/Revenue/2012, dated 13.8.2012.

ANNEXURE

FORM OF DECLARATION TO BE FURNISHED BY HOSIERY DEALERS FOR CLAIM OF REFUND OF TAX PAID UNDER CENTRAL SALES TAX ACT, 1956.

Note: This should be submitted along with monthly returns in Form I.

CST ACT, 1956 – CANCELLATION PROCESS OF „C‟ DECLARATION FORMS AND OBTAINING NEW „C‟ FORMS-PROCEDURE IN CDSC APPLICATION:

Vide Circular No. IST/D1/OUT/544/2012 dated August, 24, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh.

The following procedure is designed to streamline the procedure of cancellation of ‗C‘ declaration forms and obtaining new forms through CDSC.

1. Serial No. :

2. Seller Invoice No. :

3. Name and address of the purchasing dealer with name of the State

4. Place to which the goods have been dis-patched with name of the State

5. Mode of dispatch of goods with R.R.No., LR or Way Bill No. and date etc.

6. Quantity and description of goods sold

7. Sale price (net) :

8. Sales Tax collected, if any :

9. Proof of payment of tax :

10. Remarks :

13

a) Action to the done by the dealer for Cancellation of issued forms: The dealer has to submit a requisition online to the concerned Commercial Tax Officer, by selecting the option ‗Form cancellation request‘ from ‗Transactions‘ menu and enter the details of the forms to be cancelled, along with reasons for cancellation. The dealer will produce the original forms, which are to be cancelled, to the concerned Commercial Tax Officerwith necessary documents for verification and with the reasons for cancellation.

b) Action to the done by the Commercial Tax Officer/ Assistant Commissioner (CT) LTU for Cancellation of issued forms : The Commercial Tax Officer/ Assistant Commissioner (CT) LTU concerned has to verify the reasons for cancellation based on the documentary evidence produced by the dealer and retain the original forms by making an entry ‗Cancelled‘ on all the three copies i.e. original, duplicate and triplicate of the form and to be filed in the office record. The Commercial Tax Officer/Assistant Commissioner (CT) LTU has to then login to CDSC applications, using his user id and password and select ‗Form Cancellation Requests‘ option from the ‗Transactions‘ menu and can Approve the same with his remarks.

The dealer in turn can view the status of his request made to the Commercial Tax Officer/Assistant Commissioner (CT) LTU by logging into CDSC application and selecting ‗Status of Cancellation Request‘ from the ‗Reports‘ menu. The dealer can view the status and after it is approved dealer can make a fresh request for the fresh C Form, in place of cancelled forms.

The circular instructions issued shall be strictly adhered to, while cancelling ‗C‘ forms.

APVAT ACT,2005 & CST ACT, 1956 – MIS – USE OF „C‟ FORM BY THE WORKS CONTRACTORS:

Ref: CCT‘s Ref. Enft. No. B3/17/AC – III/2007 – 08, Dt.03.01.2008.

The attention of all the Deputy Commissioner(CT)/Assessing Authorities in the state is invited to the reference cited, wherein, certain instructions were issued with regard to the Issue of ‗C‘ Forms to the work contractors informing that, the transactions of the execution of works contractors cannot be treated as manufacturing or processing of the goods; and therefore the goods like plant & machinery, earth moving equipments and their spare parts , scarf folding material etc cannot be treated as ―goods‖ used in the manufacture or processing of the goods for sale‖ and hence the works contractors are not entitled to Issue C – Forms against the purchase of such goods.

Further it was informed that, if there is any Contractor who manufactures goods, which he incorporates them at the time of execution of works contract he shall be treated as a manufacturer and he will be eligible to purchase goods to

14

the extent they are used in the manufacturer of such goods that are incorporated. For example the Works Contractors may undertake the job of conversion of boulders into metals through crushers and they may require machinery and spare parts and they shall be treated as manufacturers, who will be eligible to issue C-Forms, to such a limited extent and requested all the Deputy Commissioners(CT) in the state to delete the ineligible goods or material from the Reg-istration Certificates issued to works contractors under CST Act, wherever incorporated and to take steps to examine all the cases of works contractors resorting to misuse of C – Form by purchasing the ineligible goods against C Forms in violation of Sec.8(3) of CST Act,1956, and to take appropriate action in terms of Sec.10 A of the CST Act.

But , it came to notice that, some of the works contractors are still issuing ‗C‘ Form for the purchase of Machinery which are used in the execution of works contracts, in contravention of the provisions of Sec.8(3) of CST Act read with Sec.8(1) of CST Act. The purpose for which goods can be purchased against Form – C, as mentioned in clause (b) of Sec 8(3) of CST Act are as follows:

(i) goods intended for resale: (ii) goods used in the manufacture or processing of goods for sale (iii) goods used in the tele communications network (iv) goods used in the mining (v) goods used in the generation or distribution of electricity or any other form

of power containers or materials intended for being used for packing of the goods for sale, as specified in the certificate of registration under CST Act (container or any other material, specified in the RC of material used for packing of the goods, specified in the RC).

In view of the above, the Deputy Commissioner(CT) in the state are once again informed that „C‟ Form can be issued and used by the dealer only when goods are purchased for specific purposed indicated in CST Act, 1956 as above and mere entry of goods in Registration Certificate should not entitle the dealer to get ‗C‘ Form from the Department.

Therefore, all the Deputy Commissioners(CT) in the state are requested to instruct the Commercial Tax Officers in their jurisdiction not to issue – C-Forms to the works contractors for purchase of any material or goods, which are neither incorporated in the execution of works contract nor used any of the purposes, as enumerated in Clause (b) of Sec 8(3) of CST Act, and to take the penal action under Sec 10 A of CST Act against those works contractors who issue C – Forms in contravention of the legal provisions. APVAT ACT,2005 & CST ACT, 1956 – MIS – USE OF „C‟ FORM:

Vide Circular CCT‘s Ref. No. A(II)(2)/2012 dated September 6, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh. `

15

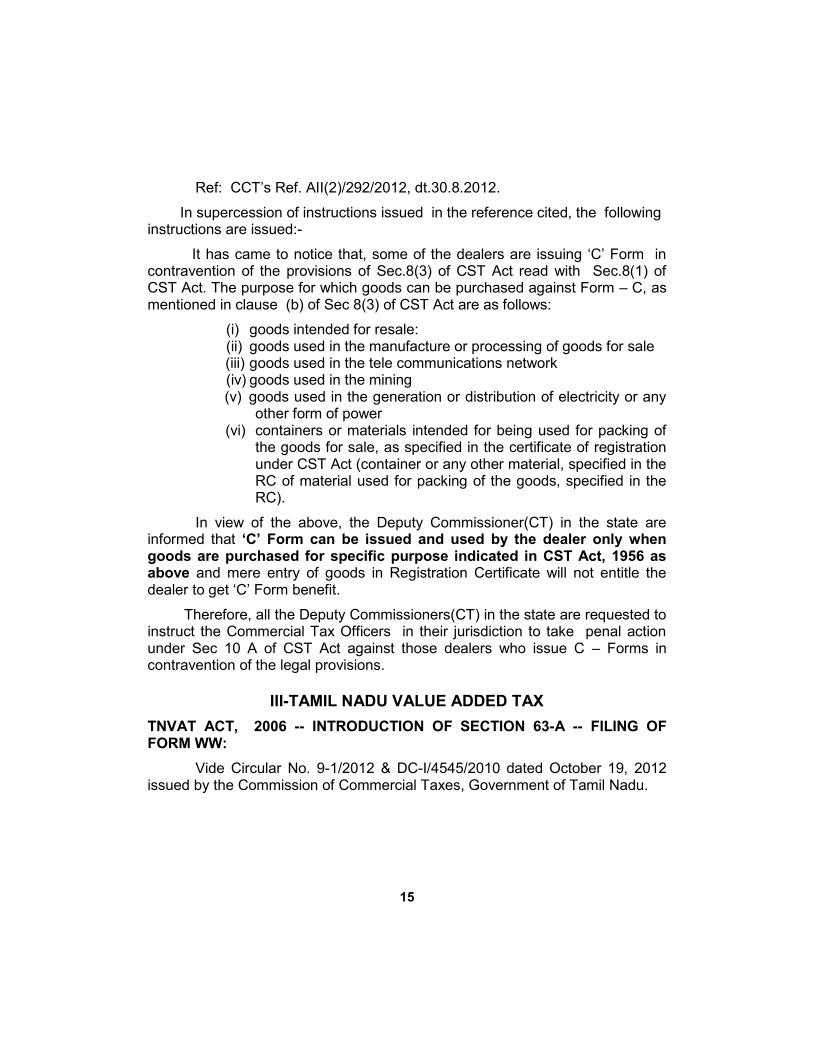

Ref: CCT‘s Ref. AII(2)/292/2012, dt.30.8.2012.

In supercession of instructions issued in the reference cited, the following instructions are issued:-

It has came to notice that, some of the dealers are issuing ‗C‘ Form in contravention of the provisions of Sec.8(3) of CST Act read with Sec.8(1) of CST Act. The purpose for which goods can be purchased against Form – C, as mentioned in clause (b) of Sec 8(3) of CST Act are as follows:

(i) goods intended for resale: (ii) goods used in the manufacture or processing of goods for sale (iii) goods used in the tele communications network (iv) goods used in the mining (v) goods used in the generation or distribution of electricity or any

other form of power (vi) containers or materials intended for being used for packing of

the goods for sale, as specified in the certificate of registration under CST Act (container or any other material, specified in the RC of material used for packing of the goods, specified in the RC).

In view of the above, the Deputy Commissioner(CT) in the state are informed that „C‟ Form can be issued and used by the dealer only when goods are purchased for specific purpose indicated in CST Act, 1956 as above and mere entry of goods in Registration Certificate will not entitle the dealer to get ‗C‘ Form benefit.

Therefore, all the Deputy Commissioners(CT) in the state are requested to instruct the Commercial Tax Officers in their jurisdiction to take penal action under Sec 10 A of CST Act against those dealers who issue C – Forms in contravention of the legal provisions.

III-TAMIL NADU VALUE ADDED TAX

TNVAT ACT, 2006 -- INTRODUCTION OF SECTION 63-A -- FILING OF FORM WW:

Vide Circular No. 9-1/2012 & DC-I/4545/2010 dated October 19, 2012 issued by the Commission of Commercial Taxes, Government of Tamil Nadu.

16

Kind attention is invited to the Circular cited.

In the said circular it was informed that the submission of Audit Report in Form ―WW‖ is applicable from the financial year 2011-12.

However, in partial modification of the said Circular, it is brought to the notice of all the Officers that, submission of Audit Report in Form ―WW‖ is applicable only from the financial year 2012-13 onwards.

TAMIL NADU VALUE ADDED TAX ACT, 2006 – EXEMPTION FROM PAYMENT OF VALUE ADDED TAX ON PURCHASE OF GOODS BY POLICE CANTEENS IN TAMIL NADU AS WELL AS SUBSEQUENT SALE TO THE SERVING AND RETIRED STATE POLICE PERSONNEL AND TO THE SERVING, RETIRED AND DECEASED UNIFORMED PERSONNEL OF FIRE AND RESCUE SERVICES AND PRISONS AND THEIR FAMILIES:

Vide G.O. Ms. No.121 dated September 11, 2012 issued by the Commercial Taxes and Registration (B2) Department, Government of Tamil Nadu.

In exercise of the powers conferred by sub-sections (1), (2) and (3) of section 30 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 32 of 2006), and in supersession of the Commercial Taxes and Registration Department Notification No.II(2)/CTR/90(k-3)/2011, published at pages 2-3 of Part II-Section 2 of the Tamil Nadu Government Gazette, Extraordinary, dated the 1st March 2011, the Governor of Tamil Nadu hereby makes an exemption in respect of tax payable under the said Act by any dealer on the sale of any goods (other than petrol, diesel, cement, liquor and alcoholic beverages) to the State police canteens established in the State at (i) RC, Avadi, Chennai (ii) Tamil Nadu Special Police I Battalion Trichy and (iii) Tamil Nadu Special Police VI Battalion Madurai and canteens to be established in the State on the lines of Central police canteen network for the serving and retired Tamil Nadu State police personnel and serving, retired and deceased Uniformed Services personnel of Fire and Rescue Services and Prisons Department and their fami-lies, subject to the following conditions, namely:-

(a) That the dealer obtains and produces before the Assessing Authority a Certificate duly filled and signed by the purchaser in the Form appended below; and (b) That the State police canteen files the annual return before the Assessing Authority as required under sub-rule (7) of rule 7 of the Tamil Nadu Value Added Tax Rules, 2007.

17

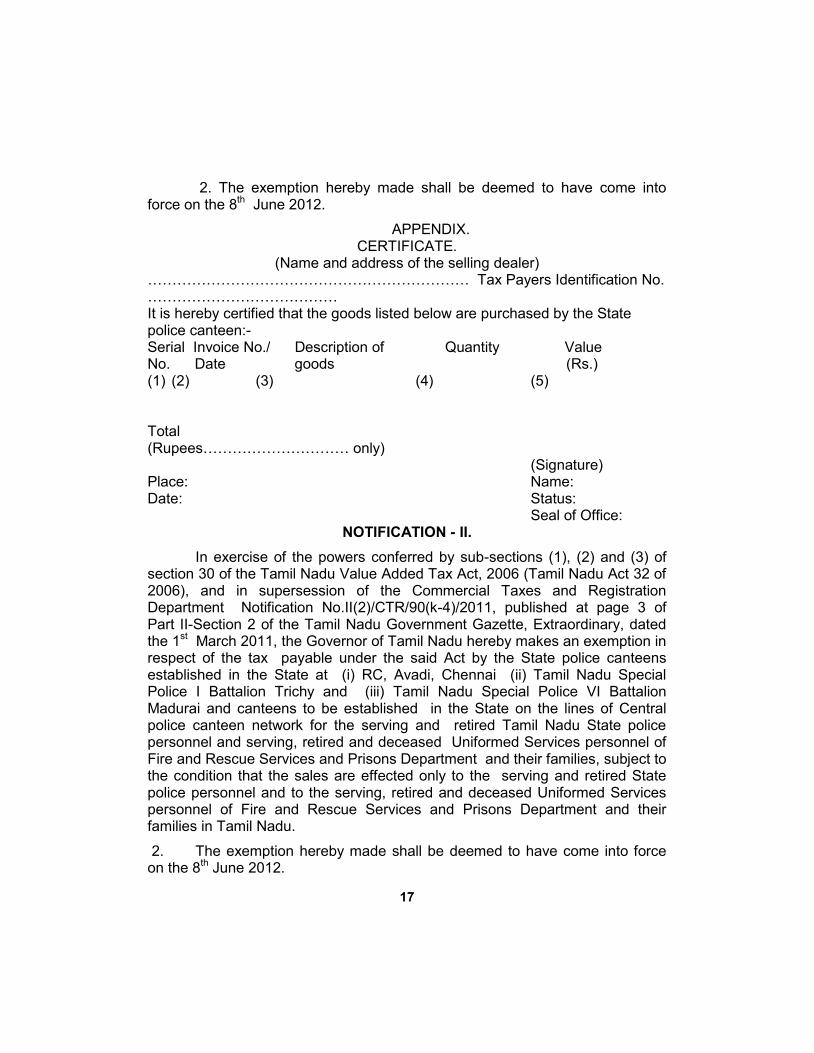

2. The exemption hereby made shall be deemed to have come into force on the 8th June 2012.

APPENDIX. CERTIFICATE.

(Name and address of the selling dealer) ………………………………………………………… Tax Payers Identification No.………………………………… It is hereby certified that the goods listed below are purchased by the State police canteen:- Serial Invoice No./ Description of Quantity Value No. Date goods (Rs.) (1) (2) (3) (4) (5) Total (Rupees………………………… only) (Signature) Place: Name: Date: Status: Seal of Office:

NOTIFICATION - II.

In exercise of the powers conferred by sub-sections (1), (2) and (3) of section 30 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 32 of 2006), and in supersession of the Commercial Taxes and Registration Department Notification No.II(2)/CTR/90(k-4)/2011, published at page 3 of Part II-Section 2 of the Tamil Nadu Government Gazette, Extraordinary, dated the 1st March 2011, the Governor of Tamil Nadu hereby makes an exemption in respect of the tax payable under the said Act by the State police canteens established in the State at (i) RC, Avadi, Chennai (ii) Tamil Nadu Special Police I Battalion Trichy and (iii) Tamil Nadu Special Police VI Battalion Madurai and canteens to be established in the State on the lines of Central police canteen network for the serving and retired Tamil Nadu State police personnel and serving, retired and deceased Uniformed Services personnel of Fire and Rescue Services and Prisons Department and their families, subject to the condition that the sales are effected only to the serving and retired State police personnel and to the serving, retired and deceased Uniformed Services personnel of Fire and Rescue Services and Prisons Department and their families in Tamil Nadu.

2. The exemption hereby made shall be deemed to have come into force on the 8th June 2012.

18

BANKS FOR AVAILING OF E-PAYMENT FACILITY:

Vide G.O. (Ms) No. 124 dated September 13, 2012 issued by the Commercial Taxes and Registration (F1) Department, Government of Tamil Nadu.

ORDER

In the Government Order first read above, the Government have issued orders to authorise the following thirteen Public Sector/Private Sector Banks to undertake e-payment of Commercial Taxes so that dealers get convenience of more banks for availing of e-payment facility, subject to the accreditation of Re-serve Bank of India:-

1. Vijaya Bank 2. IDBI Bank 3. Corporation Bank 4. United Bank of India 5. UCO Bank 6. Union Bank of India 7. Punjab National Bank 8. HDFC Bank 9. AXIS Bank 10. ICICI Bank 11. Federal Bank 12. Catholic Syrian Bank 13. City Union Bank

2. Based on the willingness given by the Public Sector/Private Sector Banks to take part in e-payment project of Commercial Taxes, the Commissioner of Commercial Taxes in his letter second read above has requested the Government to authorize 6 more Public Sector/ Private Sector banks viz., Karur Vysya Bank Ltd, YES Bank Ltd, State Bank of Patiala, Bank of Maharastra, Tamil Nadu Mercantile Bank Ltd and Oriental Bank of Commerce which are not accredited by Reserve Bank of India to take part in e-payment project of Commercial Taxes Department.

3. The Government have examined the proposal of the Commissioner of Commercial Taxes and decided to authorize the following six Public Sector/Private Sector banks to undertake e-payment of Commercial Taxes so that dealers get convenience of more banks for availing of e-payment facility, subject to the accreditation of Reserve Bank of India:-

19

Sl.No. Name of the Bank

1. Karur Vysya Bank Ltd. 2. YES Bank Ltd. 3. State Bank of Patiala 4. Bank of Maharastra 5. Tamil Nadu Mercantile Bank Ltd. 6. Oriental Bank of Commerce

4. This order issues with the concurrence of Finance Department vide its U.O.No.38982/Finance (Revenue)/2012, dated 21.08.2012.

CREATION OF THE LARGE TAY PAYERS‟ UNIT (LTU) AT CHENNAI:

Vide G.O. (Ms) No. 122 dated September 11, 2012 issued by the Commercial Taxes and Registration (A2) Department, Government of Tamil Nadu.

ORDER:

In the Government Order first read above, orders were issued for the creation of the Large Tax Payers‘ Unit (LTU) at Chennai after merging the existing four Fast Track Assessment Circles in Chennai with the staff sanctioned to these circles and sanction was also accorded for the creation of certain additional posts. In the Government Order third read above, among others, orders were issued that the Commissioner of Commercial Taxes shall take necessary action to transfer all the Large Tax Payers having taxable turnover of Rs.200 Crores and above within the State to the Large Tax Payer‘s Unit at Chennai.

2. The Commissioner of Commercial Taxes in his letter fifth read above has reported that all the dealers with the taxable turnover of Rs.200 crore were identified for transferring to Large Tax Payers' Unit at Chennai and the total number of dealers comes to 166 (for Chennai area alone) as against the original number of 97 which were attached to the erstwhile Fast Track Assessment Circles. He has added that increase in the number of dealers in the Large Tax Payers' Unit without proportionate increase in staff would lead to deterioration in service levels in the LTU, which would in turn nullify the intention of its formation. He has therefore requested the Government that he may be permitted to transfer the top 100 tax paying dealers (large tax payers) in Chennai to LTU to begin with. The Fast Track Assessment Circle - I & II in Coimbatore would be brought to the LTU in Chennai in future and requested that necessary amendment may be issued to the Government Order third read above.

20

3. The Government have carefully examined the request of the Commissioner of Commercial Taxes and have decided to accept it. Accordingly, the following amendment is issued to the Government Order third read above with retrospective effect from 29.10.2010.

AMENDMENT

For the existing paragraph 5 in G.O Ms. No.186, Commercial Taxes and Registration Department, dated 29.10.2010, the following paragraph shall be substituted:-

―5. The Government have carefully examined the above proposal of the Commissioner of Commercial Taxes and decided to accept it on the following lines and order accordingly:

(i) the Commissioner of Commercial Taxes shall take necessary action to transfer the top 100 large tax payers in Chennai to the Large Tax Payers‘ Unit at Chennai to begin. Thereafter the large tax payers in the Fast Track Assessment Circle-I&II in Coimbatore shall be brought to the Large Tax Payers‘ Unit in Chennai in future.

(ii) one new post of Assistant Commissioner is created for the office of the Large Tax Payers‘ Unit at Chennai.

(iii) the incumbent of the post sanctioned in para 5 (ii) above is eligible to draw pay and allowances as per orders in force.‖

4. The Government also ratify the action of the Commissioner of Commercial Taxes in having transferred the 100 Large Tax Payers in Chennai area alone to the Large Tax Payers Unit pending issue of orders by Government.

5. This orders issues with the concurrence of the Finance Department vide its U.O.No.41806/Revenue/2012, dated 17.8.2012.

TAMIL NADU VALUE ADDED TAX ACT, 2006 – REDUCTION OF VAT ON GENERATING SETS (GEN-SETS) USED FOR PRODUCING ELECTRICITY FROM 14.5% TO 5%:

Vide G.O. Ms. No. 154 dated December 8, 2012 issued by the Commer-cial Taxes and Registration (B2) Department, Government of Tamil Nadu.

In exercise of the powers conferred by sub-sections (1) and (2) of sec-tion 30 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 32 of 2006), the Governor of Tamil Nadu hereby makes a reduction in rate from 14.5% to 5% in respect of tax payable under the said Act by any dealer on the sale of Generating sets (Gen-sets) used for producing electricity.

21

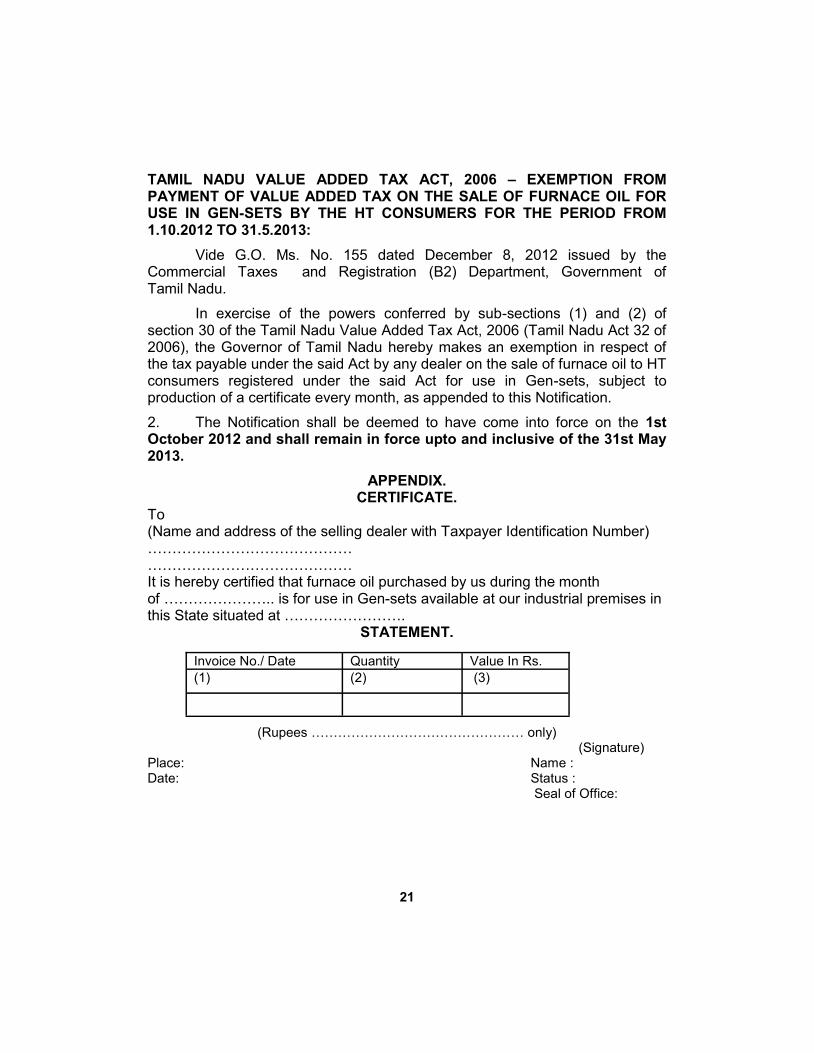

TAMIL NADU VALUE ADDED TAX ACT, 2006 – EXEMPTION FROM PAYMENT OF VALUE ADDED TAX ON THE SALE OF FURNACE OIL FOR USE IN GEN-SETS BY THE HT CONSUMERS FOR THE PERIOD FROM 1.10.2012 TO 31.5.2013:

Vide G.O. Ms. No. 155 dated December 8, 2012 issued by the Commercial Taxes and Registration (B2) Department, Government of Tamil Nadu.

In exercise of the powers conferred by sub-sections (1) and (2) of section 30 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 32 of 2006), the Governor of Tamil Nadu hereby makes an exemption in respect of the tax payable under the said Act by any dealer on the sale of furnace oil to HT consumers registered under the said Act for use in Gen-sets, subject to production of a certificate every month, as appended to this Notification.

2. The Notification shall be deemed to have come into force on the 1st October 2012 and shall remain in force upto and inclusive of the 31st May 2013.

APPENDIX. CERTIFICATE.

To (Name and address of the selling dealer with Taxpayer Identification Number) …………………………………… …………………………………… It is hereby certified that furnace oil purchased by us during the month of ………………….. is for use in Gen-sets available at our industrial premises in this State situated at …………………….

STATEMENT.

(Rupees ………………………………………… only) (Signature)

Place: Name : Date: Status : Seal of Office:

Invoice No./ Date Quantity Value In Rs.

(1) (2) (3)

22

TAMIL NADU TAX ON ENTRY OF MOTOR VEHICLES INTO LOCAL AREAS ACT, 1990 – EMBASSIES/CONSULATES OF 119 COUNTRIES - EXEMPTION FROM PAYMENT OF ENTRY TAX:

Vide G.O. Ms. No. 153 dated December 8, 2012 issued by the Commercial Taxes and Registration (B2) Department, Government of Tamil Nadu.

In exercise of the powers conferred by section 12 of the Tamil Nadu Tax on Entry of Motor Vehicles into Local Areas Act, 1990 (Tamil Nadu Act 13 of 1990), the Governor of Tamil Nadu, having considered it necessary to do so in the public interest, hereby exempts any importer from payment of the whole of the tax payable under the said Act in respect of entry of cars and two wheelers into any local area for sale thereon to Embassies or Consulates and its diplomatic officers of the countries specified in the Annexure hereto for their official and personal use under reciprocal arrangements with India.

2. The Notification shall come into force with effect on and from the 8th December, 2012.

IV - ANDHRA PRADESH VALUE ADDED TAX

APVAT ACT, 2005 – ISSUE OF NOTIFICATION UNDER SUB-RULE (4) OF RULE 55 OF APVAT RULES,2005 – CERTAIN CATEGORY OF MANUFACTURERS ARE NOTIFIED AS INELIGIBLE TO USE THE GATE PASS CUM-INVOICE AS WAYBILL:

Vide CCT‘s JC (CT) Enft. Ref. No. D2/723/05 dated July 16, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh

In exercise of the powers conferred under sub-rule (4) of Rule 55 of AP VAT Rules, 2005, the Commissioner of Commercial Taxes, Andhra Pradesh is hereby notifies the following category of manufacturers as ineligible to use the gate pass cum invoice as waybill. These Manufactures shall make out way bills on Form 600.

1) Cement and Cement Products 2) Plastic Furniture 3) Paper of all kinds 4) Sugar Excluding Khandasari Sugar 5) Laminated Sheets of All Kinds 6) Plywood and Particle Board of all kinds 7) Package drinking water 8) Electrical Fans of all kinds 9) Electrical Domestic wires

10) Iron and Steel

23

Further informed that sub-rule (4) of Rule 55 is not applicable to the Manufacturers who are exempted from Excise levy.

This notification will come into force with effect from 10-08-2012.

APVAT ACT,2005- AUDIT AND ASSESSMENTS:

Vide Circular CCT‘s Ref: No. BV(3)/37/2010 dated August 27, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh.

Ref: (1) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 29.5.2006; (2) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 19.6.2006; (3) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 8.9.2006; (4) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 16.9.2006; (5) CCT‘s Ref. No. B II (2)/ 122/ 2006-1, dt. 4.10.2006; (6) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 31.5.2007; (7) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 13.6.2007; (8) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 22.9.2007; (9) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 5.10.2007; (10) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 25.10.2007; (11) CCT‘s Ref. No. BV I (3)/ 120/ 2008, dt. 16.4.2008; (12) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 30.10.2008; (13) CCT‘s Ref. No. BV (3)/ 60/ 2009, dt. 11.5.2009; (14) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 29.3.2010.; (15) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 5.9.2011.; (16) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 21.5.2012.; (17)CCT‘s Ref.No.AII(1)/267/2012, dt.20.7.2012.

The attention of all the Deputy Commissioners(CT) and Enforcement Wing is invited to the ref.2nd cited, wherein, it was already instructed to issue authorization of Audit in Form ADM 1B and Notification of Advisory/Audit visit to VAT dealers in Form VAT 304 through VATIS only. But, it is noticed that in some cases these guidelines are not followed strictly and audit is being authorized outside VATIS without generating ADM 1B and Form VAT 304 through the software. Therefore, the following instructions are issued:-

1) Effective from 1.9.2012, all the Deputy Commissioners concerned and Additional Commissioner/Joint Commissioner, Enforcement shall issue ―Audit authorizations‖ in Form ADM-1B with Unique No. through VATIS only. Any authorization (ADM 1B) issued outside VATIS or without unique No. shall not be a valid authorization for audit/assessment. Any officer conducting audit/assessment without valid authorization shall be liable for disciplinary action.

2) Jumbling system shall be used to allot dealers to audit officers for audit/assessment.

24

3) Guidelines issued from time to time for selection of dealers and allocation to Audit officers for audit/assessment shall be followed. 4) Audit visit notice to dealers in Form VAT 304 shall also be generated through VATIS only. 5) As per High Court Judgment, initially ‗Authorization for Audit‘ (Inspection) shall alone be issued. After receipt and verification of audit report, and if required, authorization for assessment (ADM 1B) should be issued separately, whether to the same Audit officer or to different audit officer.

6) The audit officer on authorization from the competent authority, shall issue ―Notice of assessment‖ inviting objections, and thereafter after considering reply from dealer if any, ―Assessment Order‖ shall be issued.

7) Penalty proceedings if any shall be issued separately after issue of Assessment order.

8) The result of the Audit/Assessment finalized shall be entered in VA-TIS.

9) The details of Penalty, if any, shall also be entered in VATIS.

10) Performance of Audit/Assessment shall be reviewed through VATIS Reports. 11) Step by step help is available on VATIS Home Page for the guid-ance of field staff.

The above procedure shall be followed even in the case of audits/assesment authorized by the officers of Enforcement Wing, O/o Commissioner of Commercial Taxes.

The above instructions shall be followed w.e.f. 1.9.2012 without fail.

APVAT ACT,2005- AUDIT AND ASSESSMENTS – ISSUING NOTICES CALLING FOR BOOKS OF ACCOUNTS BY THE CTOS:

Vide CCT‘s Ref. No. BV(3)/37/2010 dated August 30, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh.

Ref: (1) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 29.5.2006; (2) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 19.6.2006; (3) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 8.9.2006; (4) CCT‘s Ref. No. B II (2)/ 122/ 2006, dt. 16.9.2006; (5) CCT‘s Ref. No. B II (2)/ 122/ 2006-1, dt. 4.10.2006; (6) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 31.5.2007; (7) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 13.6.2007; (8) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 22.9.2007; (9) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 5.10.2007; (10) CCT‘s Ref. No. BV I (3)/ 120/ 2007, dt. 25.10.2007; (11) CCT‘s Ref. No. BV I (3)/ 120/ 2008, dt. 16.4.2008; (12) CCT‘s Ref. No. BV I

25

(3)/ 120/ 2007, dt. 30.10.2008; (13) CCT‘s Ref. No. BV (3)/ 60/ 2009, dt. 11.5.2009; (14) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 29.3.2010.; (15) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 5.9.2011.; (16) CCT‘s Ref. No. BV (3)/ 37/ 2010, dt. 21.5.2012.; (17) CCT‘s Ref.No.AII(1)/267/2012, dt.20.7.2012; (18) CCT‘s Ref.No.BV(3)/37/2010, dt.27.8.20012; (19)E-Mail dt.27.8.2012 from CTO-II, Anantapur Circle.

It is brought to the notice of the Commissioner (CT) that Circle CTOs are issuing notices to the dealers under section 21(4) of the AP VAT Act calling for books of Accounts. For example:-

1. V&E cases. 2. AG paras and internal Audit paras. 3. For the purpose of cross verification reports received from other circles. 4. In cases where the returns are not filed continuously and also when taxes are

not paid continuously. 5. To disallow ineligible input tax credit under Rule 20. 6. For extracts received from the check posts and other investigating agencies. 7. To verify whether the checked waybills received from DC‘s are accounted for

in the books of accounts of the dealers. 8. Input tax verification in case of Iron ore dealers particularly in light of CBI in-

vestigation on Iron ore dealers. 9. In case of big manufacturing units, to call for the IT Returns if not submitted to

the CT dept and to make cross verification of the same with our returns. 10. In cases where output tax/input tax ratio is very small or negligible. 11. In cases where there is continuous input tax credt for 3-4 years. 12. Refund claims. 13. When a firm is closed, in order to verify whether VAT is paid on the closing

stock and to prevent leakage of Govt Revenue. 14. And any other case forwarded by the DC to take further action.

All the Assistant Commissioners (CT) and Commercial Tax Officers are informed that such calling for the records of the dealers and doing assessment after scrutiny of such records of dealers will amount to inspection/audit without authorization which is not in the spirit of VAT Act and rules and goes against the provisions of Rule 59 of APVAT Rules, 2005.

Therefore, all the Commercial Tax Officers of the Circles and Assistant Commissioners (CT)(LTU) are directed to confine themselves to scrutiny of returns with any information already available with them (obtained/ received from any source) and then take necessary action to take up Audit/Assessment if required, by seeking authorization from the Deputy Commissioner for Audit/Assessment. If any of the officers act in contravention of the above instructions it will be viewed seriously besides taking disciplinary action for violation of instructions.

26

TAX DEDUCTION AT SOURCE - GENERATION OF VAT FORM 501 A ONLINE:

Vide Circular CCT‘s Ref: No.A(ii)/291/2012 dated August 27, 2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh.

As per the rule 17 of APVAT Rules, the contractor dealer will obtain VAT

Form 501 A with unique ID from the CTO or AC concerned and supply the same to the contractee. The contractee in turn will complete the VAT Form 501 A, Sign and furnish the same to the contractor dealer within 15 days after end of the month in which the VAT deduction is made. The contractor dealer shall submit such signed VAT Form 501 A in original in CTO/AC office to claim credit for TDS.

Now a facility has been created to generate the VAT Form 501 A Online

from the Departmental Website with unique number. The contractor dealers are directed to generate the VAT Form 501 A with Unique ID from the Departmental Website at www.apct.gov.in by entering basic details and handover the same to the contractee for entering the Challan No., Challan Date and for signature of the contractee. On receipt of signed VAT Form 501 A from Contractee, Contractor dealer will update details like Challan Number, Challan Date, TDS proposed to be transferred to Sub Contractor on the website. Dealer will Sign VAT Form 501 and then hand over the same in CTO/AC office for getting credit of TDS. Detailed step by step help also has been provided on VAT 501 A Form web page.

With effect from September 1, 2012, the Department will accept ONLY

those VAT Form 501 A which are generated Online through above mentioned procedure.

It is also brought to the notice of the contractor dealers that they will be able to enter only those VAT Form 501 A in eReturn which have unique ID and generated through above procedure. Hence all the contractor dealers are re-quested to generate VAT Form 501 A with Unique ID by following above proce-dure. It is again reiterated that eReturn software will not accept VAT Form 501 A which does not have Unique ID, Challan No. and Challan date.

TAX DEDUCTION AT SOURCE – GENERATION OF VAT FORM 501 A ONLINE:

Vide circular CCT‘s Ref. No. A II(2 )/291 /2012 dated September 17,2012 issued by the Commissioner of Commercial Taxes, Government of Andhra Pradesh.

Ref:- CCT‘s Ref. No. A II(2 )/291 /2012, dt. 27.08.2012 (CC No-20).

The attention of all the Commercial Tax Officers and Asst. Commissioners (LTU) in the State is invited to the ref. cited, wherein it was directed that all the Works contractors have to generate the VAT Form 501A with Unique ID from the Departmental Website w.e.f.1.9.2012. Further it was also informed that eReturn software will not accept VAT Form 501 A which does not have Unique ID, Challan No./Book Adjustment No. and Date. Therefore, all the Commercial Tax Officers and Asst. Commissioners (LTU) in the State are instructed to accept and enter VAT Form 501A in Payment module with effect from 01-09-2012 only if it has Challan Number/Book Adjustment and Date. It means Form 501 A must contain proof of payment of TDS to CT Department. If any Contractor produces VAT Form 501A without Challan Number/Book Adjustment No. and Date, it should be returned to the Contractor for furnishing these details and it shall not be entered in Payment module.

_______________

Edited, Published and Printed by Shri P. Nandagopal, Secretary on behalf of Andhra Chamber of Commerce at „Velagapudi Ramakrishna Bldg., 23, Third Cross Street, West C.I.T. Nagar, P.B. No. 3368, Nandanam, Chennai-600 035 (Phones: 24315277/ 24315278/ 24315279)