Embed Size (px)

DESCRIPTION

computation of basic salary and txable income.

Citation preview

WELCOME TO THIS PRESENTATION

CLASS A PRESENTATION

ON INCOME FROM

SALARY

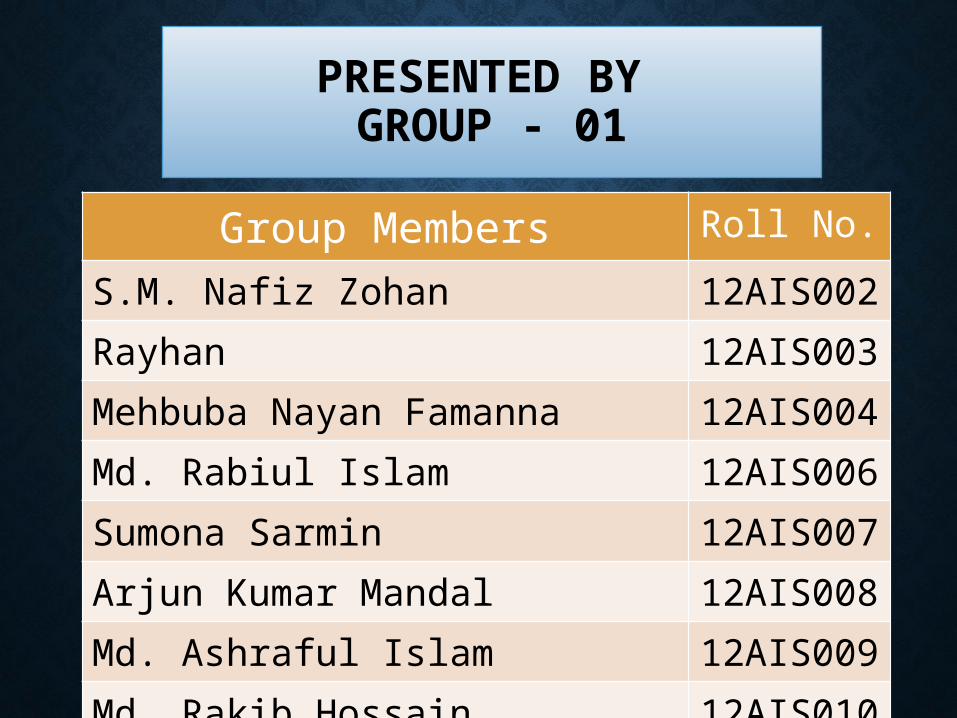

PRESENTED BY GROUP - 01

Group Members Roll No.

S.M. Nafiz Zohan 12AIS002Rayhan 12AIS003Mehbuba Nayan Famanna 12AIS004Md. Rabiul Islam 12AIS006Sumona Sarmin 12AIS007Arjun Kumar Mandal 12AIS008Md. Ashraful Islam 12AIS009Md. Rakib Hossain 12AIS010

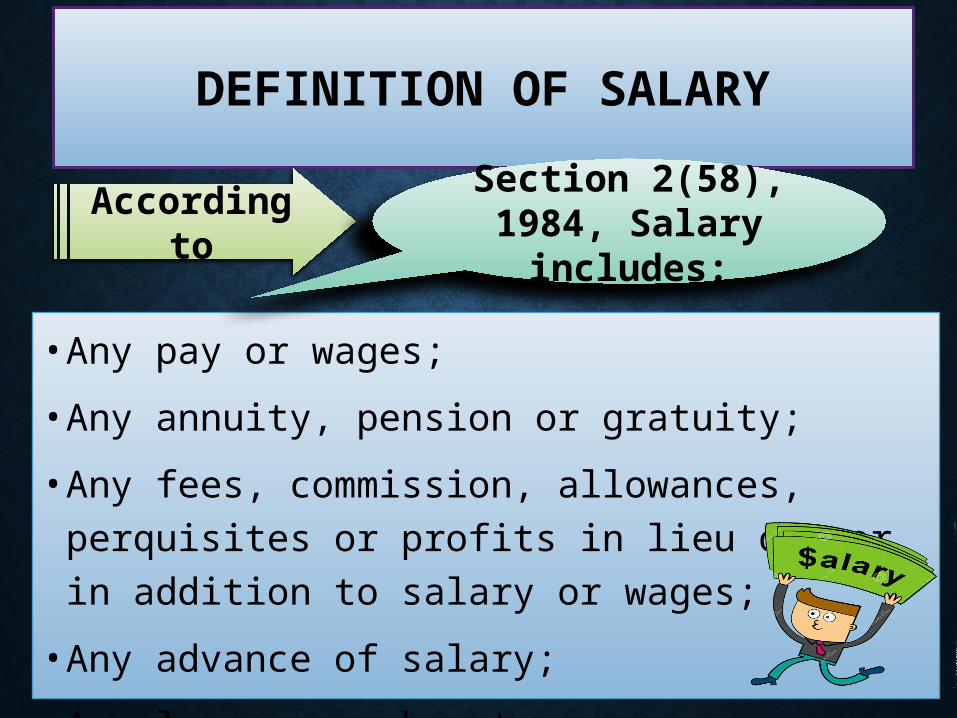

DEFINITION OF SALARY

• Any pay or wages;

• Any annuity, pension or gratuity;

• Any fees, commission, allowances, perquisites or profits

in lieu of, or in addition to salary or wages;

• Any advance of salary;

• Any leave encashment.

According toSection 2(58), 1984,

Salary includes:

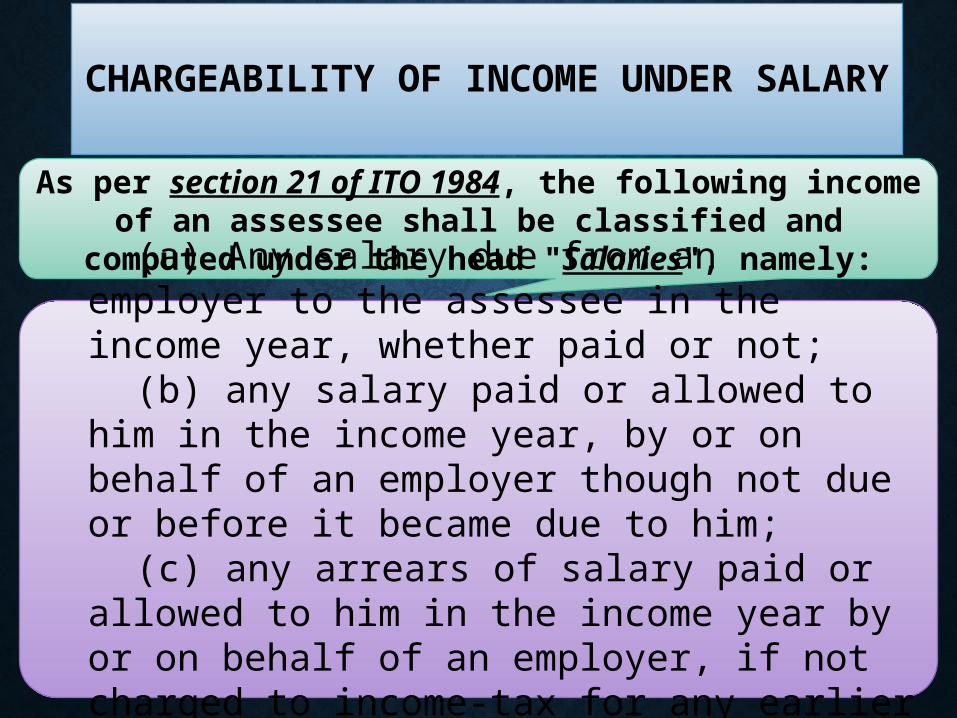

CHARGEABILITY OF INCOME UNDER SALARY

Where any amount of salary of an assessee is once included in his total income of an income year on the basis that it had become due or that it had been paid in advance in that year, that amount shall not again be included in his income of any other year.

As per section 21 of ITO 1984, the following income of an assessee shall be classified and computed under the head

"Salaries", namely:

(a) Any salary due from an employer to the assessee in the income year, whether paid or not;

(b) any salary paid or allowed to him in the income year, by or on behalf of an employer though not due or before it became due to him;

(c) any arrears of salary paid or allowed to him in the income year by or on behalf of an employer, if not charged to income-tax for any earlier income year.

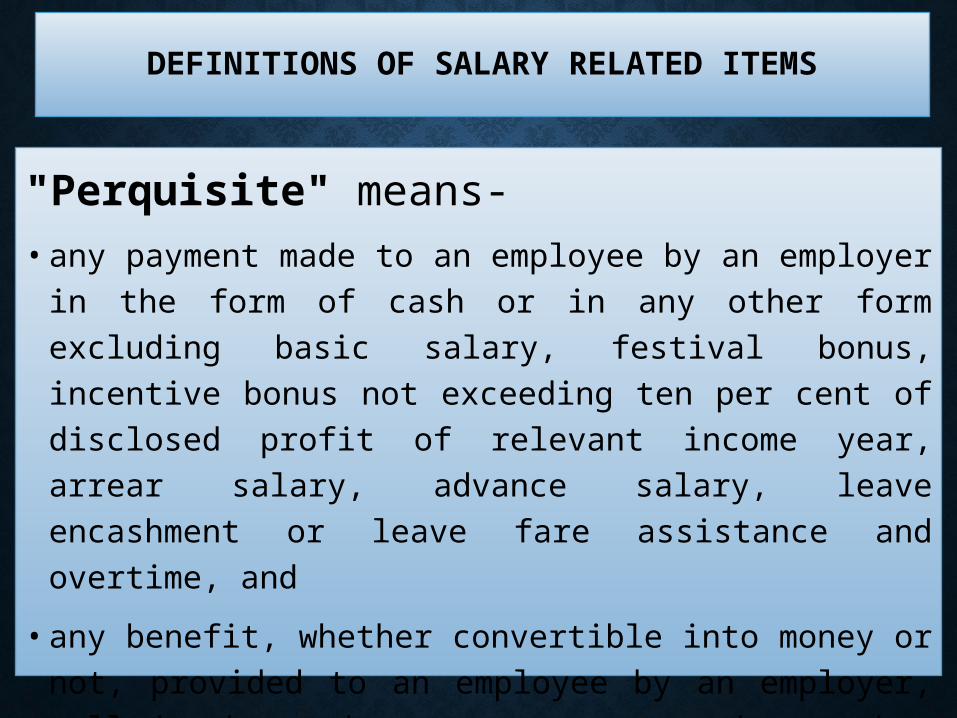

DEFINITIONS OF SALARY RELATED ITEMS

"Perquisite" means-

• any payment made to an employee by an employer in the form of

cash or in any other form excluding basic salary, festival bonus,

incentive bonus not exceeding ten per cent of disclosed profit of

relevant income year, arrear salary, advance salary, leave

encashment or leave fare assistance and overtime, and

• any benefit, whether convertible into money or not, provided to an

employee by an employer, called by whatever name, other than

contribution to a recognized provident fund, approved pension fund,

approved gratuity fund and approved superannuation fund.

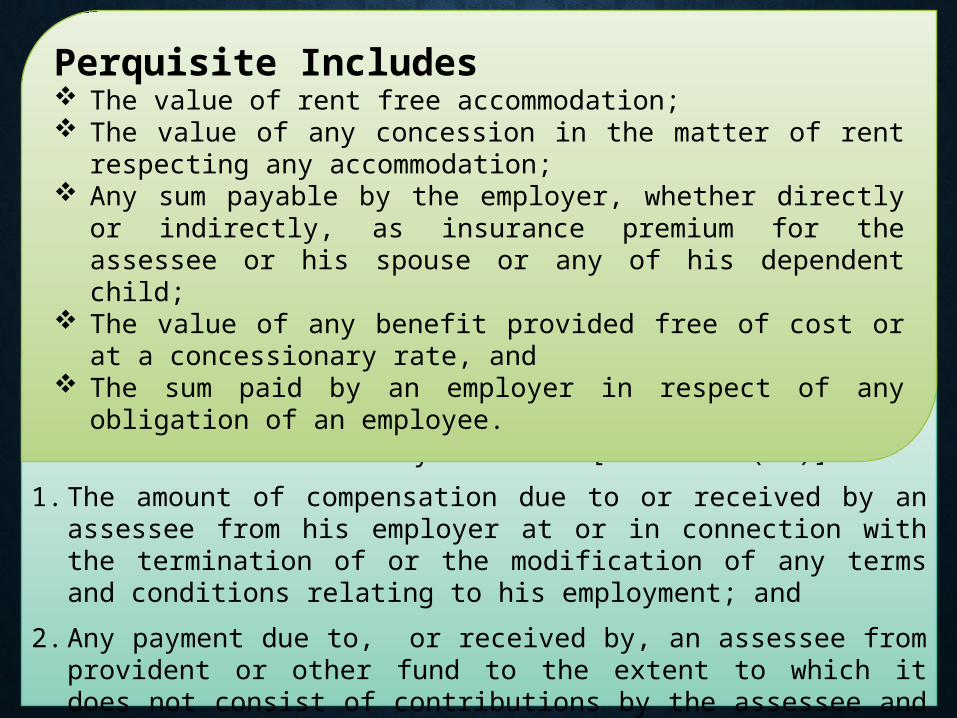

Profits in Lieu of SalaryProfits in lieu of salary includes [section 2(50)]:

1. The amount of compensation due to or received by an assessee from his employer at or in connection with the termination of or the modification of any terms and conditions relating to his employment; and

2. Any payment due to, or received by, an assessee from provident or other fund to the extent to which it does not consist of contributions by the assessee and the interest on such contributions.

Perquisite Includes The value of rent free accommodation; The value of any concession in the matter of rent respecting any

accommodation; Any sum payable by the employer, whether directly or indirectly, as

insurance premium for the assessee or his spouse or any of his dependent child;

The value of any benefit provided free of cost or at a concessionary rate, and The sum paid by an employer in respect of any obligation of an employee.

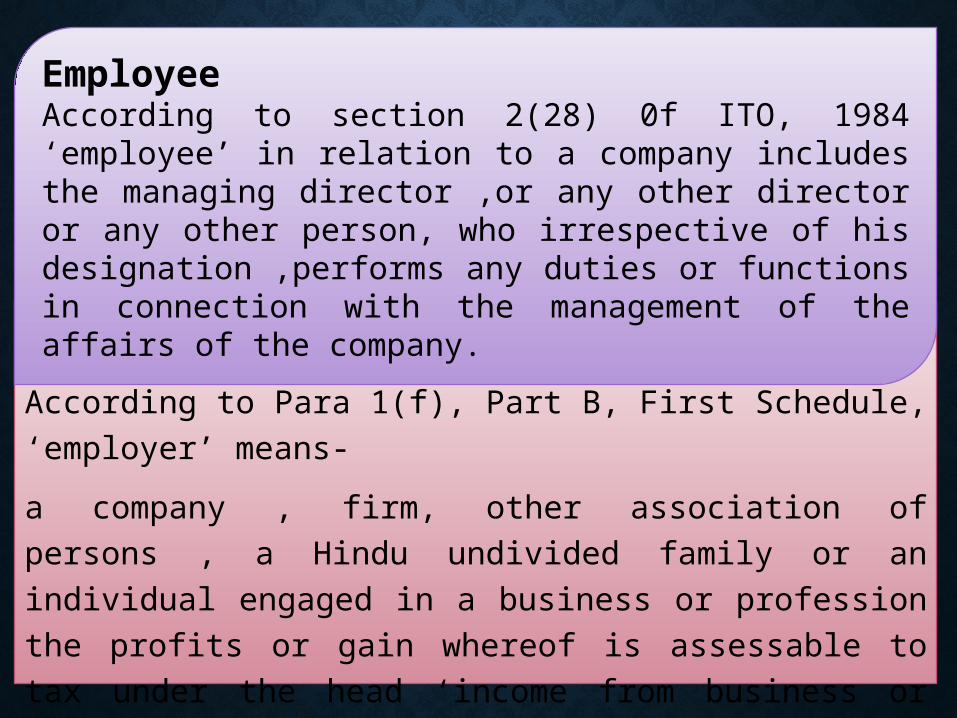

Employer

According to Para 1(f), Part B, First Schedule, ‘employer’ means-

a company , firm, other association of persons , a Hindu undivided

family or an individual engaged in a business or profession the profits

or gain whereof is assessable to tax under the head ‘income from

business or profession’ , maintaining a provident fund for the benefit

of his or its employees;

EmployeeAccording to section 2(28) 0f ITO, 1984 ‘employee’ in relation to a company includes the managing director ,or any other director or any other person, who irrespective of his designation ,performs any duties or functions in connection with the management of the affairs of the company.

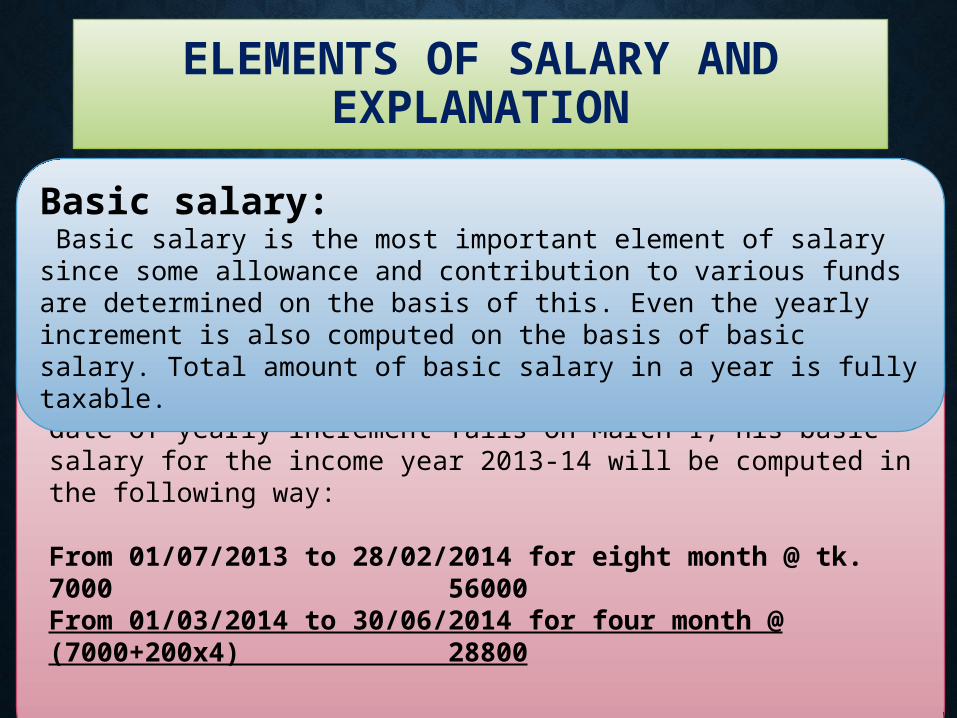

ELEMENTS OF SALARY AND EXPLANATION

Explanation: If Mr. X has withdrawn monthly salary of tk. 7000 on July 2013 in the scale of tk. 6000-200-10000 and his date of yearly increment falls on March 1; his basic salary for the income year 2013-14 will be computed in the following way:

From 01/07/2013 to 28/02/2014 for eight month @ tk. 7000 56000From 01/03/2014 to 30/06/2014 for four month @ (7000+200x4) 28800 84800

Basic salary: Basic salary is the most important element of salary since some allowance and contribution to various funds are determined on the basis of this. Even the yearly increment is also computed on the basis of basic salary. Total amount of basic salary in a year is fully taxable.

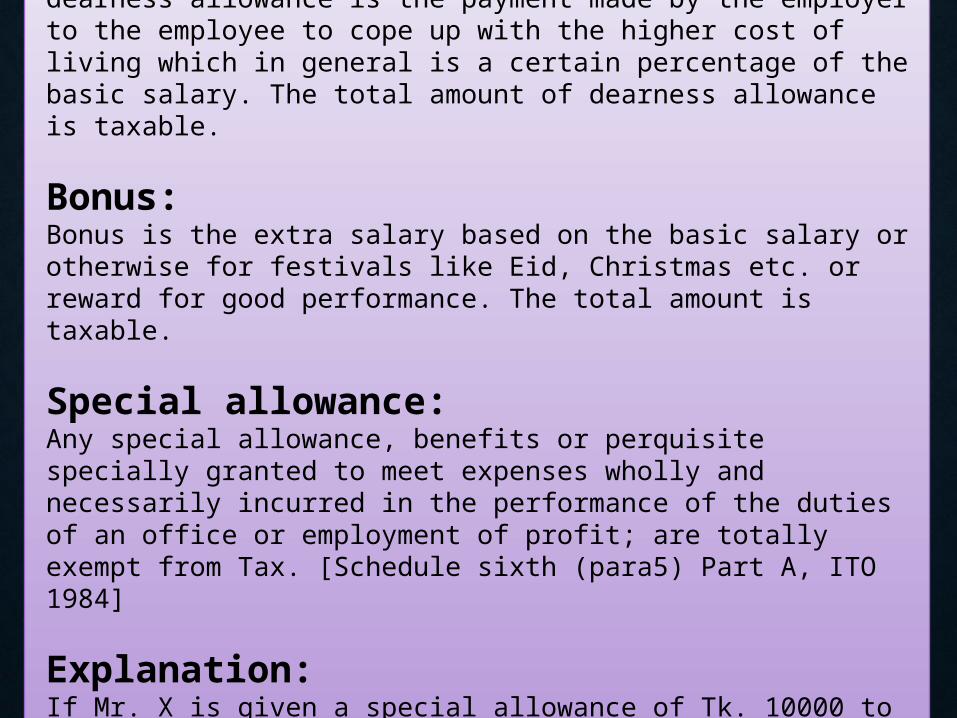

Dearness allowance:dearness allowance is the payment made by the employer to the employee to cope up with the higher cost of living which in general is a certain percentage of the basic salary. The total amount of dearness allowance is taxable.

Bonus:Bonus is the extra salary based on the basic salary or otherwise for festivals like Eid, Christmas etc. or reward for good performance. The total amount is taxable.

Special allowance: Any special allowance, benefits or perquisite specially granted to meet expenses wholly and necessarily incurred in the performance of the duties of an office or employment of profit; are totally exempt from Tax. [Schedule sixth (para5) Part A, ITO 1984]

Explanation: If Mr. X is given a special allowance of Tk. 10000 to meet some expenses wholly for official purpose and it will not be included under income from salary.

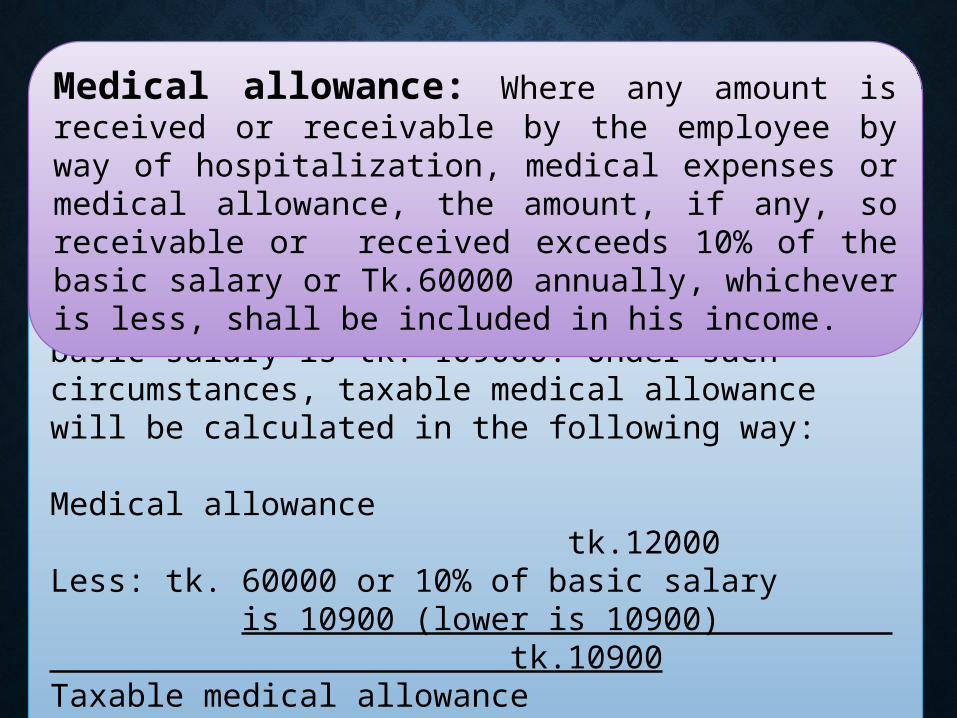

Explanation: If Mr. X is given Tk. 12000 as medical allowance in a year and his actual medical expenses is tk. 10000; His annual basic salary is tk. 109000. Under such circumstances, taxable medical allowance will be calculated in the following way:

Medical allowance tk.12000Less: tk. 60000 or 10% of basic salary is 10900 (lower is 10900) tk.10900Taxable medical allowance tk. 1100

Medical allowance: Where any amount is received or receivable by the employee by way of hospitalization, medical expenses or medical allowance, the amount, if any, so receivable or received exceeds 10% of the basic salary or Tk.60000 annually, whichever is less, shall be included in his income.

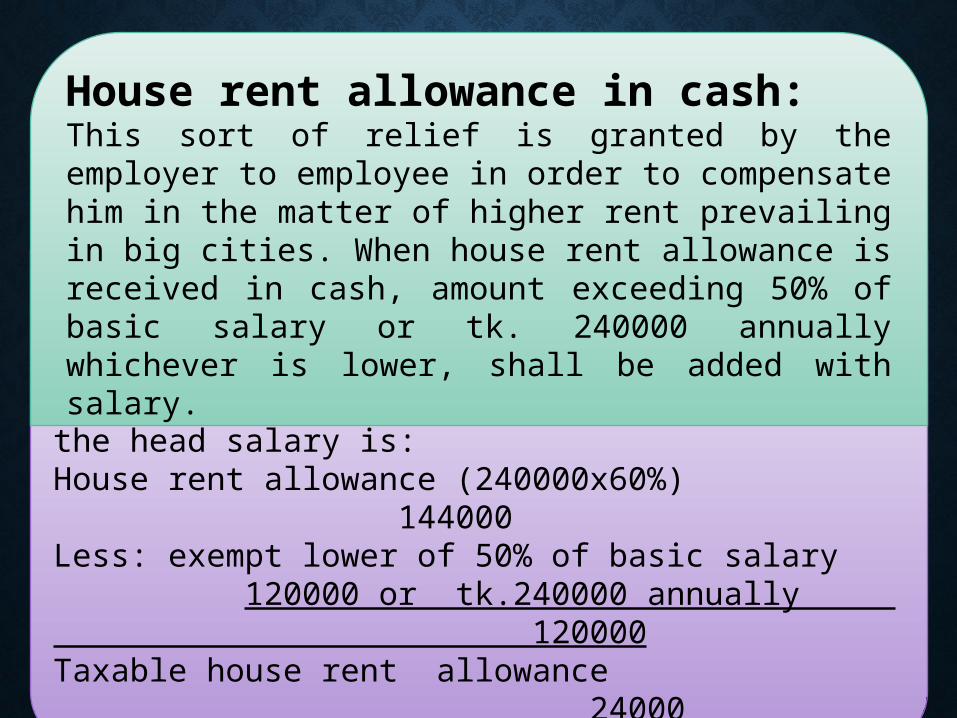

Explanation:Mr. X is paid monthly tk. 50000 as basic salary and is also given 60% of basic salary as house rent allowance. So the amount under the head salary is:House rent allowance (240000x60%) 144000Less: exempt lower of 50% of basic salary 120000 or tk.240000 annually 120000Taxable house rent allowance 24000

House rent allowance in cash:This sort of relief is granted by the employer to employee in order to compensate him in the matter of higher rent prevailing in big cities. When house rent allowance is received in cash, amount exceeding 50% of basic salary or tk. 240000 annually whichever is lower, shall be added with salary.

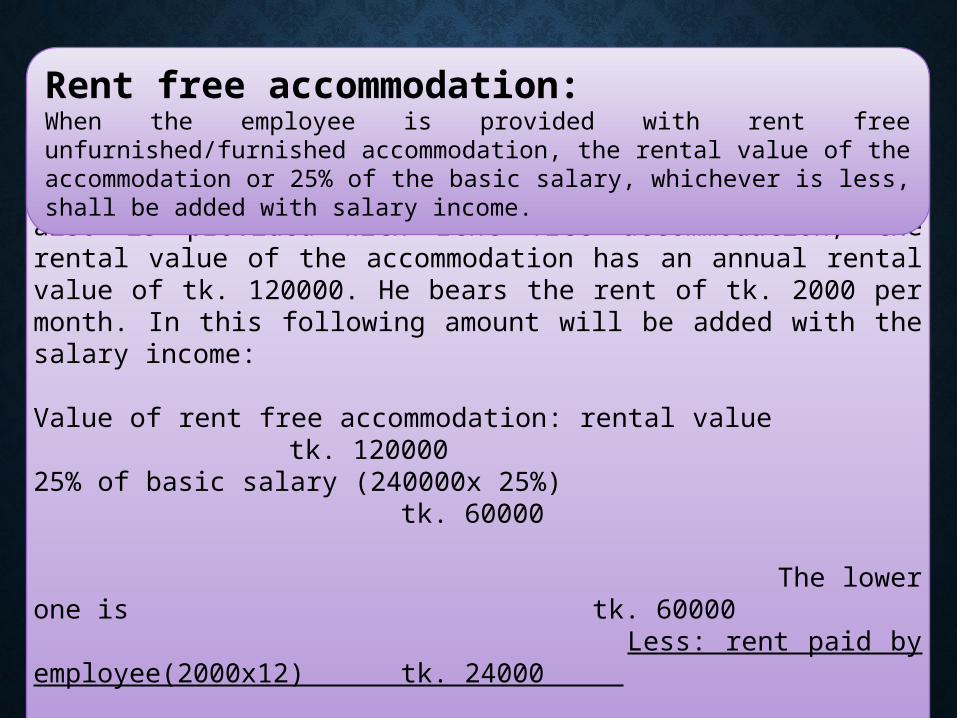

Explanation: Mr. X is paid monthly tk. 20000 as basic salary and is also is provided with rent free accommodation, the rental value of the accommodation has an annual rental value of tk. 120000. He bears the rent of tk. 2000 per month. In this following amount will be added with the salary income:

Value of rent free accommodation: rental value tk. 12000025% of basic salary (240000x 25%) tk. 60000 The lower one is tk. 60000 Less: rent paid by employee(2000x12) tk. 24000 Tk. 36000

Rent free accommodation: When the employee is provided with rent free unfurnished/furnished accommodation, the rental value of the accommodation or 25% of the basic salary, whichever is less, shall be added with salary income.

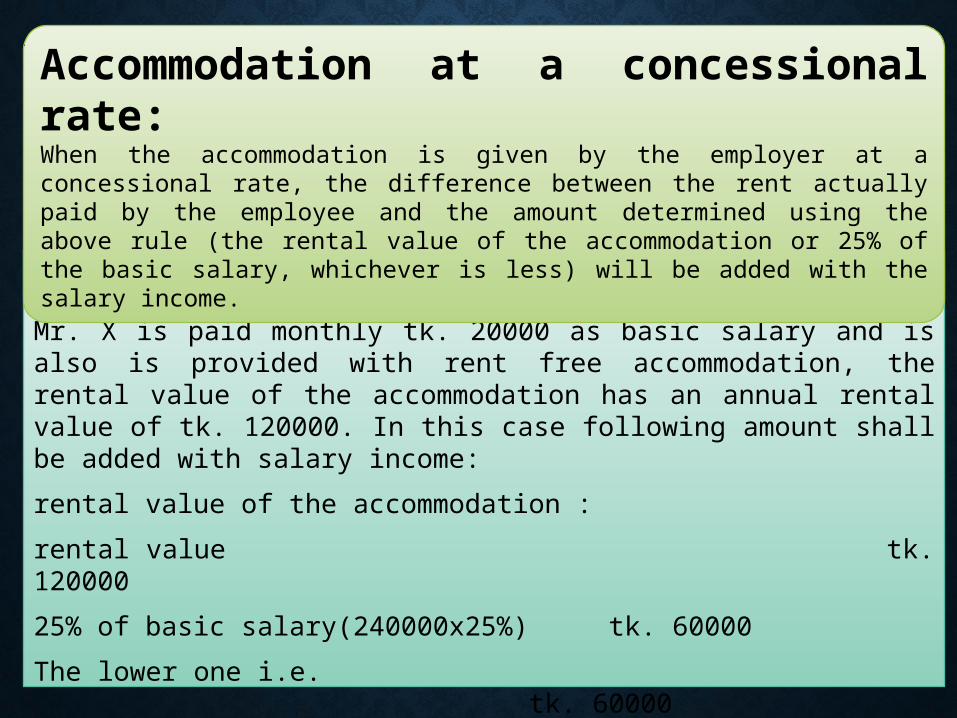

Explanation:Mr. X is paid monthly tk. 20000 as basic salary and is also is provided with rent free accommodation, the rental value of the accommodation has an annual rental value of tk. 120000. In this case following amount shall be added with salary income:

rental value of the accommodation :

rental value tk. 120000

25% of basic salary(240000x25%) tk. 60000

The lower one i.e. tk. 60000

Less: rent paid by employee(2000x12) tk. 24000

tk. 36000

Accommodation at a concessional rate: When the accommodation is given by the employer at a concessional rate, the difference between the rent actually paid by the employee and the amount determined using the above rule (the rental value of the accommodation or 25% of the basic salary, whichever is less) will be added with the salary income.

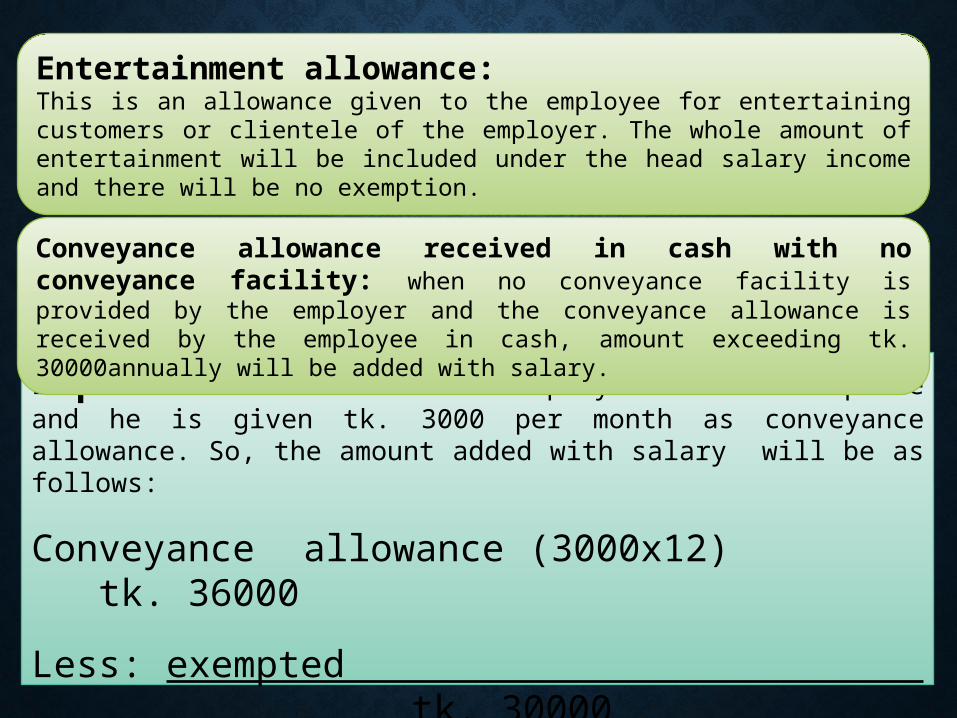

Explanation: Mr X in an employee of Grameen phone and he is given tk. 3000 per month as conveyance allowance. So, the amount added with salary will be as follows:

Conveyance allowance (3000x12) tk. 36000

Less: exempted tk. 30000

Tk. 6000

Entertainment allowance: This is an allowance given to the employee for entertaining customers or clientele of the employer. The whole amount of entertainment will be included under the head salary income and there will be no exemption.

Conveyance allowance received in cash with no conveyance facility: when no conveyance facility is provided by the employer and the conveyance allowance is received by the employee in cash, amount exceeding tk. 30000annually will be added with salary.

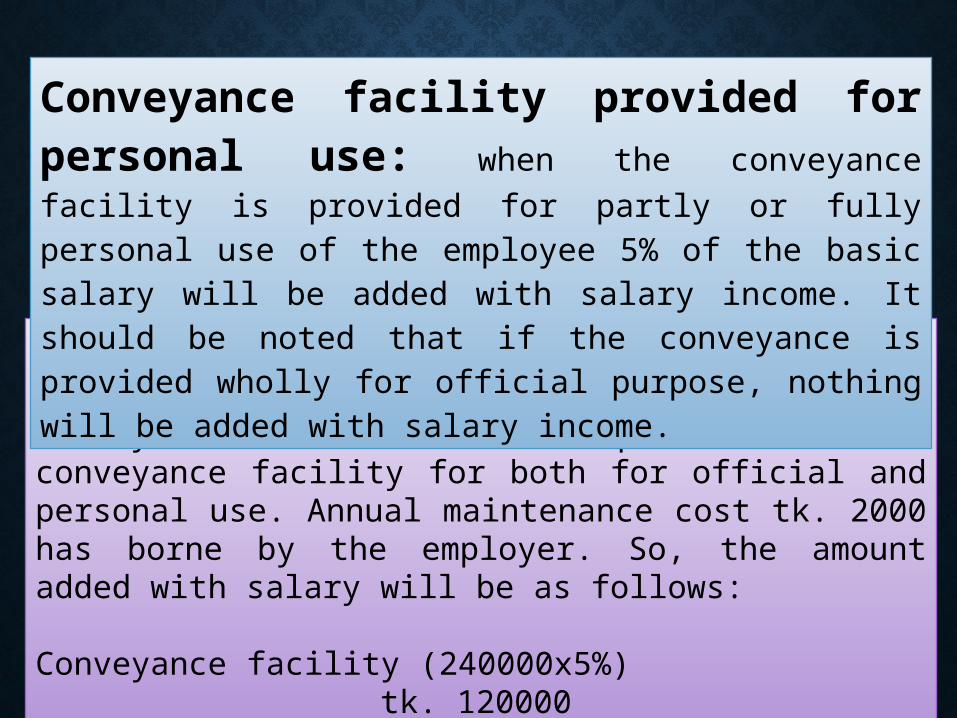

Explanation: Mr. X is paid monthly tk. 20000 as basic salary and has also been provide with a conveyance facility for both for official and personal use. Annual maintenance cost tk. 2000 has borne by the employer. So, the amount added with salary will be as follows:

Conveyance facility (240000x5%) tk. 120000

Conveyance facility provided for personal use: when the conveyance facility is provided for partly or fully personal use of the employee 5% of the basic salary will be added with salary income. It should be noted that if the conveyance is provided wholly for official purpose, nothing will be added with salary income.

Explanation: Mr. X is paid monthly tk. 20000 as basic salary and

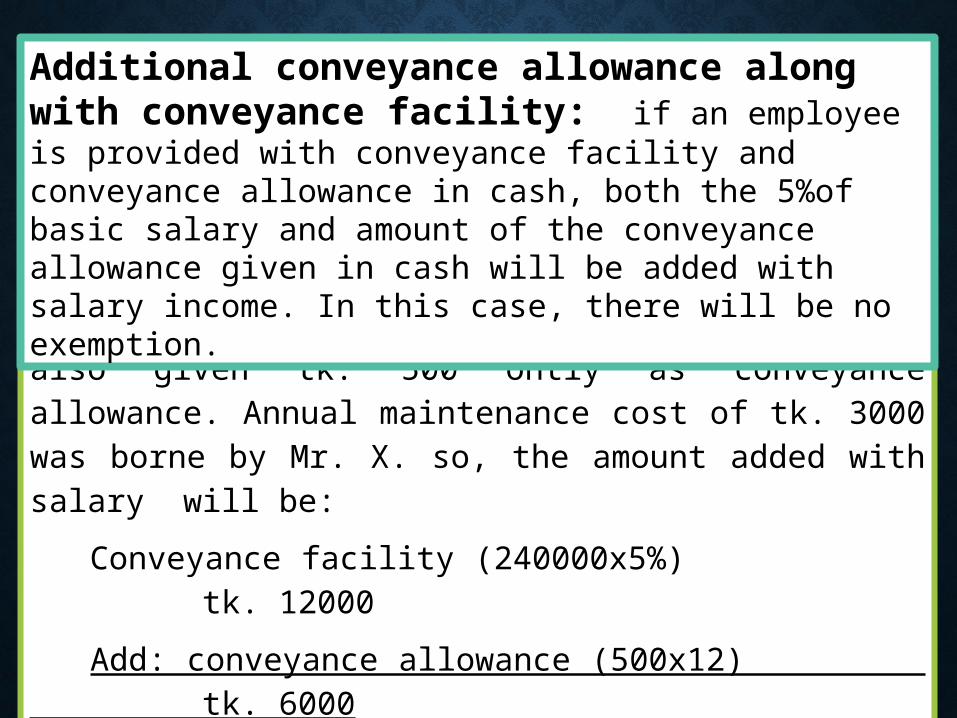

he has also been provided with a conveyance facility for both personal and official use. In addition to this he is also given tk. 500 ontly as conveyance allowance. Annual maintenance cost of tk. 3000 was borne by Mr. X. so, the amount added with salary will be:

Conveyance facility (240000x5%) tk. 12000

Add: conveyance allowance (500x12) tk. 6000

Tk. 18000

Additional conveyance allowance along with conveyance facility: if an employee is provided with conveyance facility and conveyance allowance in cash, both the 5%of basic salary and amount of the conveyance allowance given in cash will be added with salary income. In this case, there will be no exemption.

Explanation: Mr. X is paid monthly tk. 20000 as basic salary

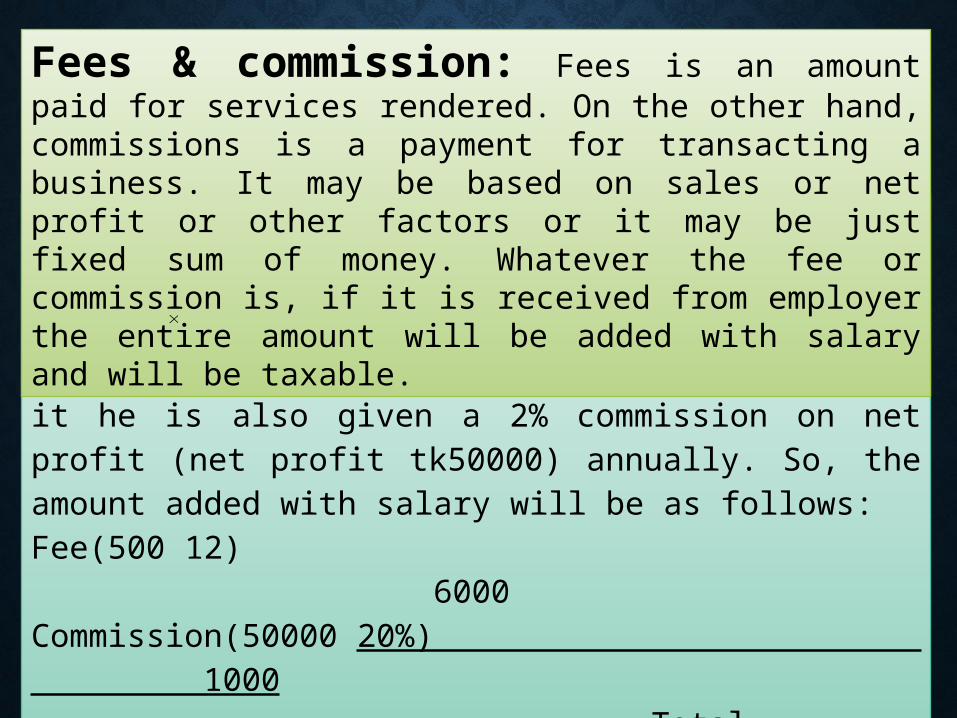

and he has also been provided with a monthly fee of tk. 500 for a special task conducted by him. In addition to it he is also given a 2% commission on net profit (net profit tk50000) annually. So, the amount added with salary will be as follows: Fee(500 12) 6000Commission(50000 20%) 1000 Total 7000

Fees & commission: Fees is an amount paid for services rendered. On the other hand, commissions is a payment for transacting a business. It may be based on sales or net profit or other factors or it may be just fixed sum of money. Whatever the fee or commission is, if it is received from employer the entire amount will be added with salary and will be taxable.

Outstanding salary: The outstanding salary of a particular income year will be added with the salary income in that income year. But if it is received in the next year then it will be excluded from the salary income of the next year since tax has already been paid on that amount.

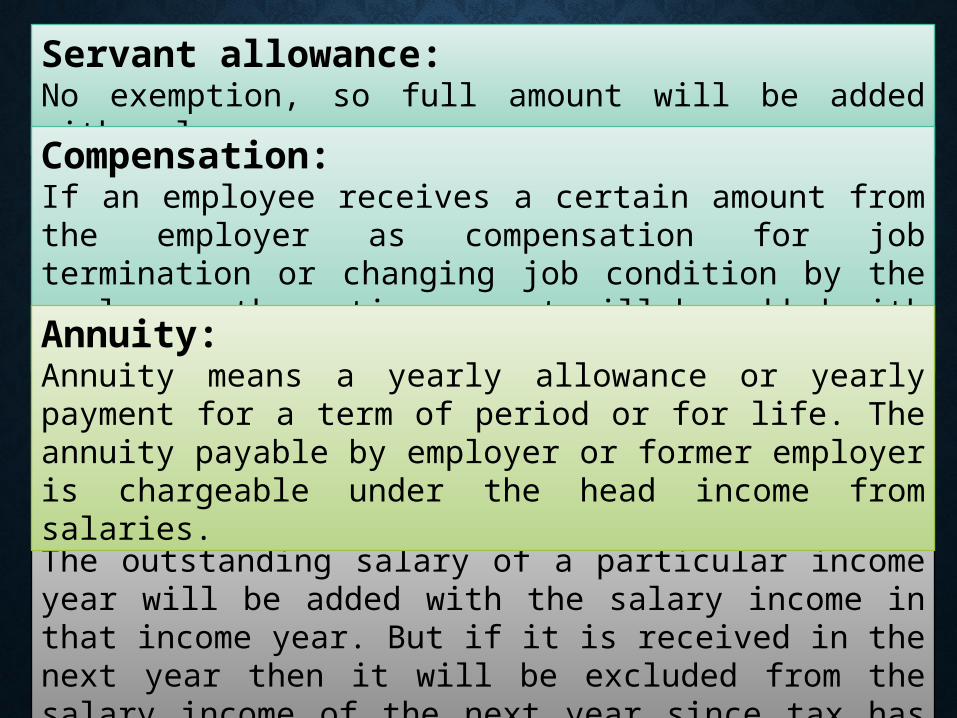

Servant allowance: No exemption, so full amount will be added with salary.

Compensation: If an employee receives a certain amount from the employer as compensation for job termination or changing job condition by the employer, the entire amount will be added with salary.

Annuity: Annuity means a yearly allowance or yearly payment for a term of period or for life. The annuity payable by employer or former employer is chargeable under the head income from salaries.

Gratuity: Gratuity is paid in reorganization of past services.

Generally it is paid at the time of leaving job. Gratuity is fully exempt

from tax and hence not included as a part of salary income.

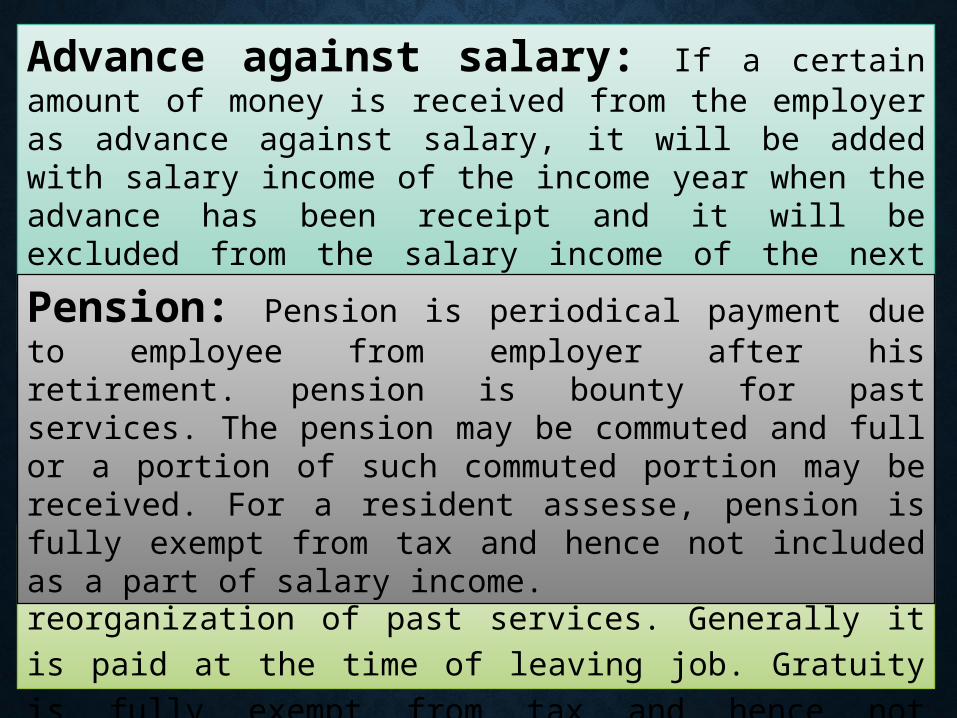

Advance against salary: If a certain amount of money is received from the employer as advance against salary, it will be added with salary income of the income year when the advance has been receipt and it will be excluded from the salary income of the next year since tax has already been paid on that amount.

Pension: Pension is periodical payment due to employee from employer after his retirement. pension is bounty for past services. The pension may be commuted and full or a portion of such commuted portion may be received. For a resident assesse, pension is fully exempt from tax and hence not included as a part of salary income.

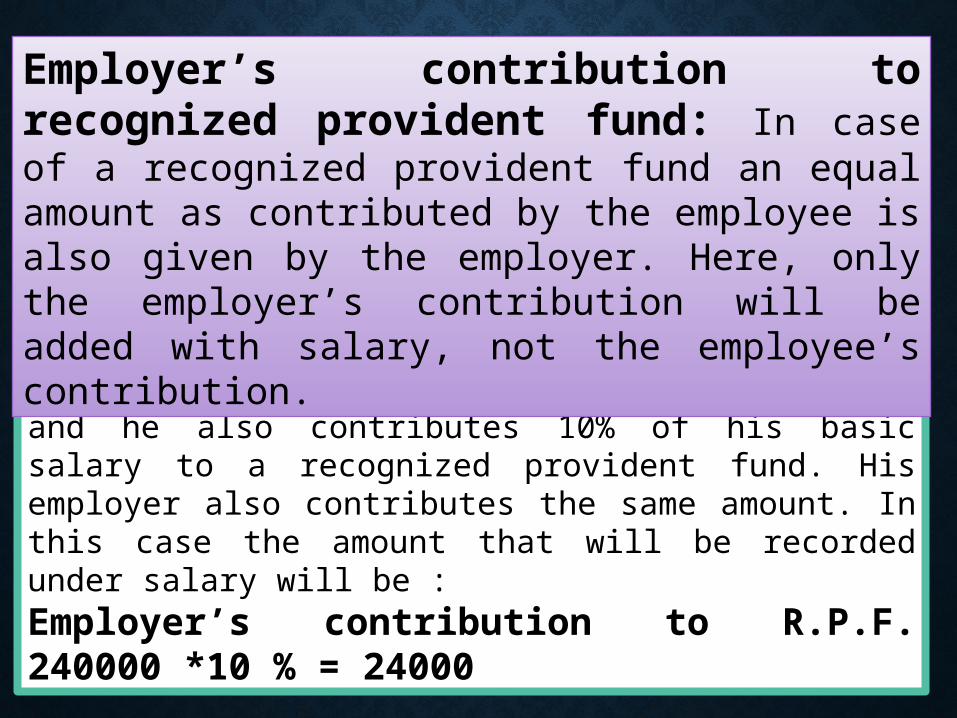

Example: Mr.X is paid monthly tk 20000 as basic salary and he also contributes 10% of his basic salary to a recognized provident fund. His employer also contributes the same amount. In this case the amount that will be recorded under salary will be : Employer’s contribution to R.P.F. 240000 *10 % = 24000

Employer’s contribution to recognized provident fund: In case of a recognized provident fund an equal amount as contributed by the employee is also given by the employer. Here, only the employer’s contribution will be added with salary, not the employee’s contribution.

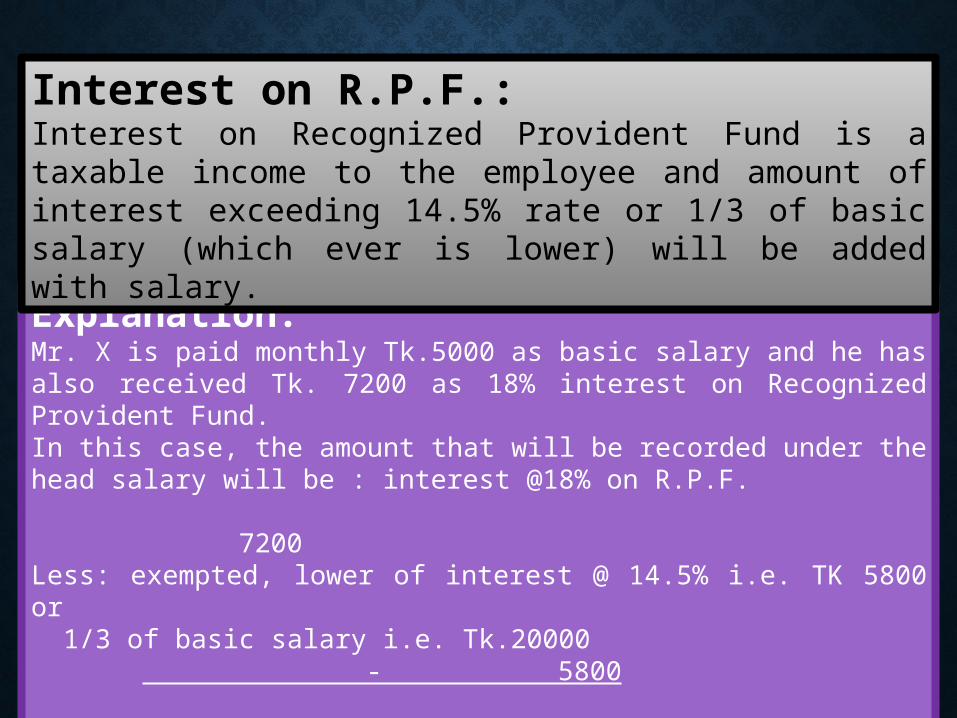

Explanation: Mr. X is paid monthly Tk.5000 as basic salary and he has also received Tk. 7200 as 18% interest on Recognized Provident Fund.In this case, the amount that will be recorded under the head salary will be : interest @18% on R.P.F. 7200Less: exempted, lower of interest @ 14.5% i.e. TK 5800 or 1/3 of basic salary i.e. Tk.20000 - 5800 1400Calculation of 14.5% interest = (interest actual rate of interest) 14.5% =(7200 8 ) 14.5% = 5800

Interest on R.P.F.: Interest on Recognized Provident Fund is a taxable income to the employee and amount of interest exceeding 14.5% rate or 1/3 of basic salary (which ever is lower) will be added with salary.

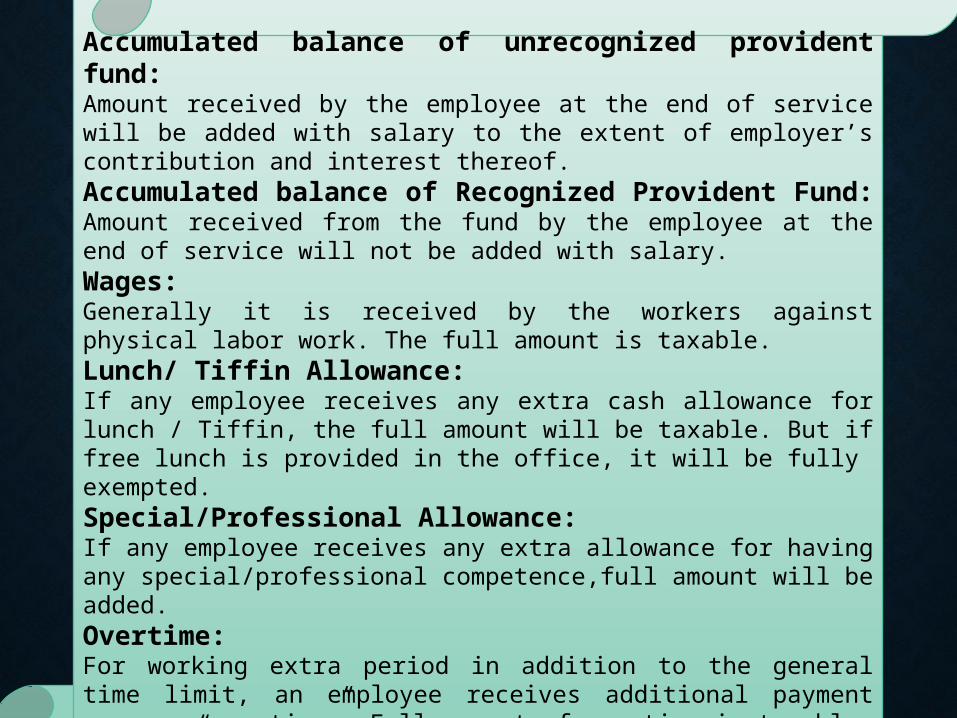

Accumulated balance of unrecognized provident fund: Amount received by the employee at the end of service will be added with salary to the extent of employer’s contribution and interest thereof.Accumulated balance of Recognized Provident Fund: Amount received from the fund by the employee at the end of service will not be added with salary.Wages: Generally it is received by the workers against physical labor work. The full amount is taxable.Lunch/ Tiffin Allowance: If any employee receives any extra cash allowance for lunch / Tiffin, the full amount will be taxable. But if free lunch is provided in the office, it will be fully exempted.Special/Professional Allowance: If any employee receives any extra allowance for having any special/professional competence,full amount will be added.Overtime: For working extra period in addition to the general time limit, an employee receives additional payment name as “overtime”. Full amount of overtime is taxable.

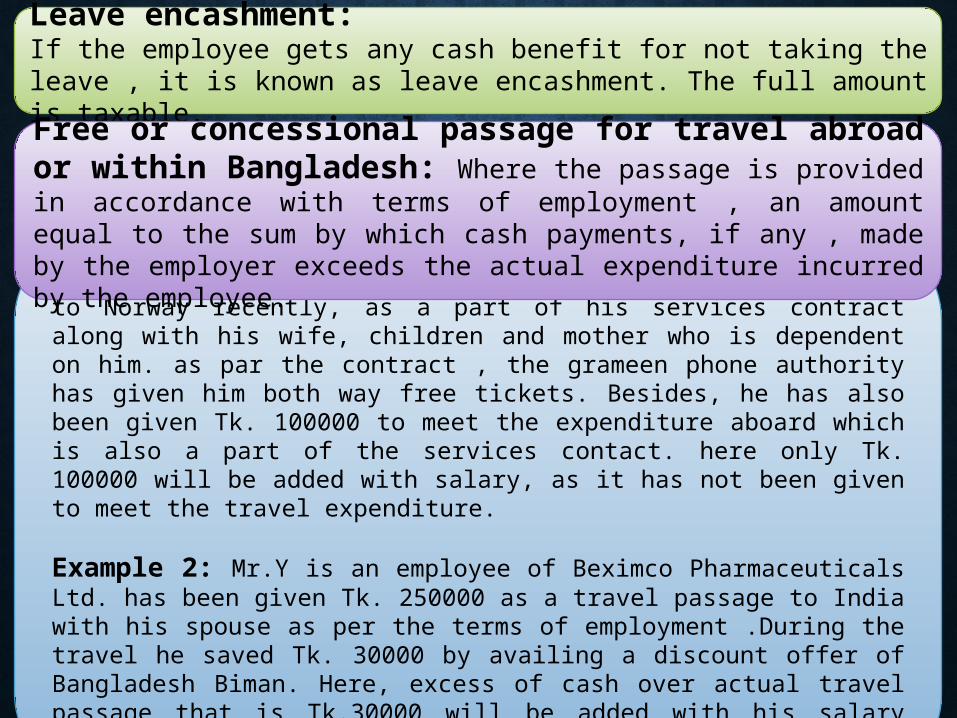

Example: Mr. X an employee of the Grameen Phone traveled to Norway recently, as a part of his services contract along with his wife, children and mother who is dependent on him. as par the contract , the grameen phone authority has given him both way free tickets. Besides, he has also been given Tk. 100000 to meet the expenditure aboard which is also a part of the services contact. here only Tk. 100000 will be added with salary, as it has not been given to meet the travel expenditure.

Example 2: Mr.Y is an employee of Beximco Pharmaceuticals Ltd. has been given Tk. 250000 as a travel passage to India with his spouse as per the terms of employment .During the travel he saved Tk. 30000 by availing a discount offer of Bangladesh Biman. Here, excess of cash over actual travel passage that is Tk.30000 will be added with his salary income.

Leave encashment: If the employee gets any cash benefit for not taking the leave , it is known as leave encashment. The full amount is taxable.

Free or concessional passage for travel abroad or within Bangladesh: Where the passage is provided in accordance with terms of employment , an amount equal to the sum by which cash payments, if any , made by the employer exceeds the actual expenditure incurred by the employee.

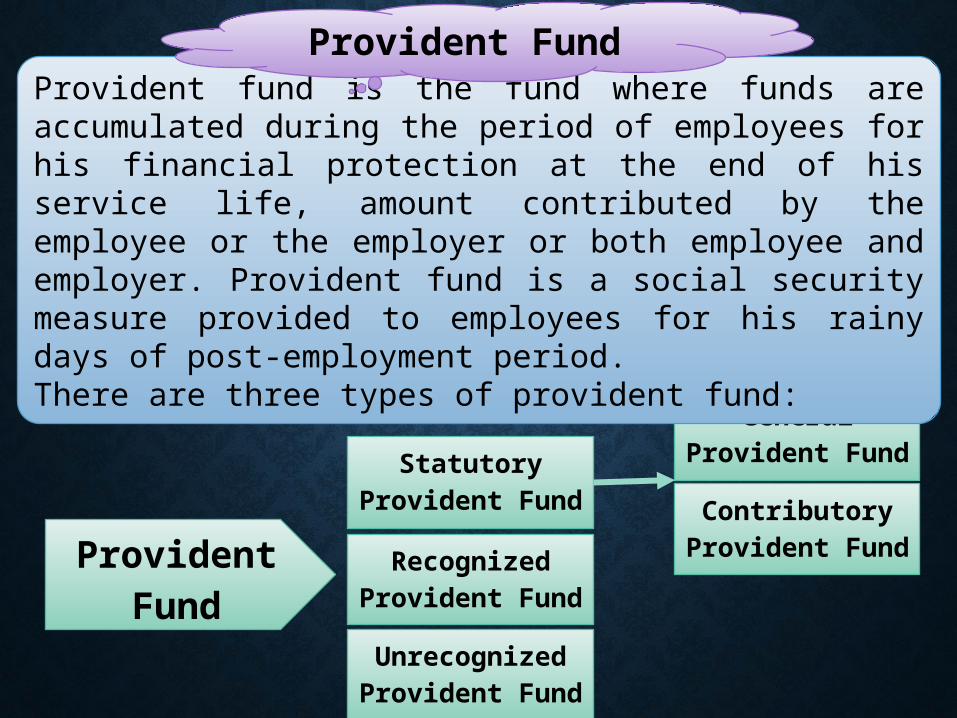

Provident Fund

Recognized Provident Fund

General Provident FundStatutory

Provident Fund

Unrecognized Provident Fund

Contributory Provident Fund

Provident fund is the fund where funds are accumulated during the period of employees for his financial protection at the end of his service life, amount contributed by the employee or the employer or both employee and employer. Provident fund is a social security measure provided to employees for his rainy days of post-employment period. There are three types of provident fund:

Provident Fund

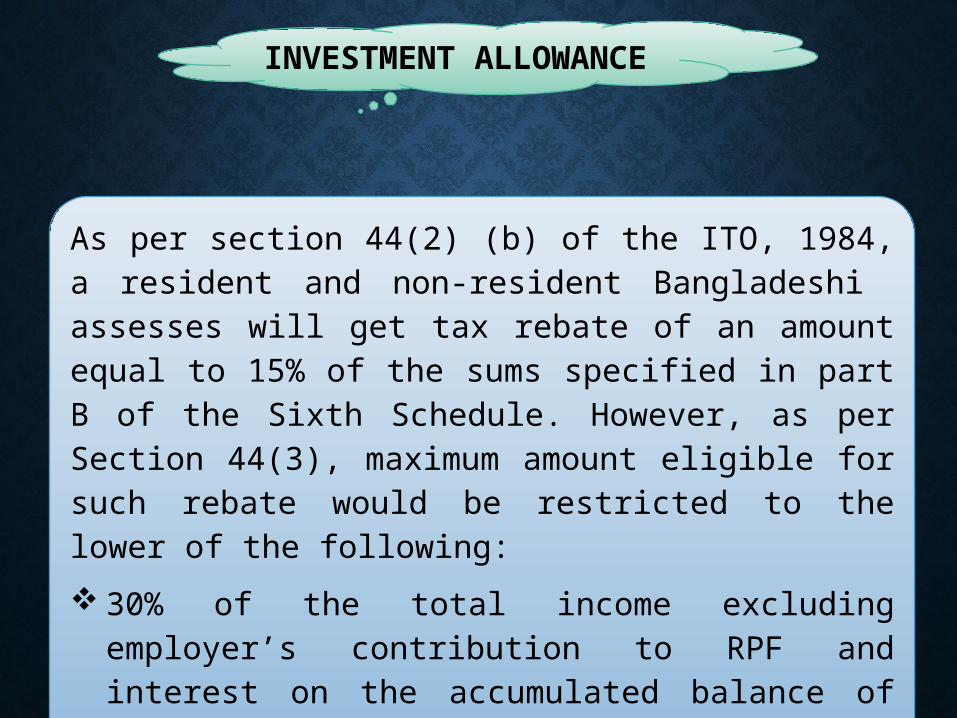

INVESTMENT ALLOWANCE

As per section 44(2) (b) of the ITO, 1984, a resident and non-resident Bangladeshi assesses will get tax rebate of an amount equal to 15% of the sums specified in part B of the Sixth Schedule. However, as per Section 44(3), maximum amount eligible for such rebate would be restricted to the lower of the following:

30% of the total income excluding employer’s contribution to RPF and interest on the accumulated balance of RPF and any income u/s 82C, or

TK. 1,50,00,000.

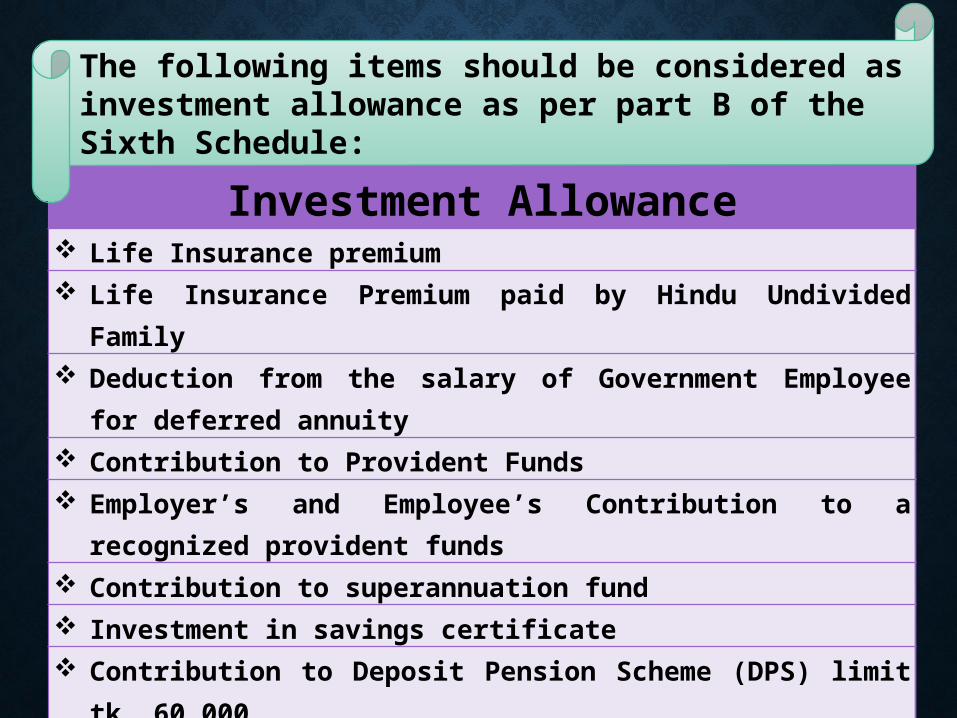

Investment Allowance Life Insurance premium Life Insurance Premium paid by Hindu Undivided Family Deduction from the salary of Government Employee for deferred

annuity

Contribution to Provident Funds Employer’s and Employee’s Contribution to a recognized provident

funds

Contribution to superannuation fund Investment in savings certificate Contribution to Deposit Pension Scheme (DPS) limit tk. 60,000 Donation to charitable Hospital Donation to Organizations set up for the welfare of retarded people

The following items should be considered as investment allowance as per part B of the Sixth Schedule:

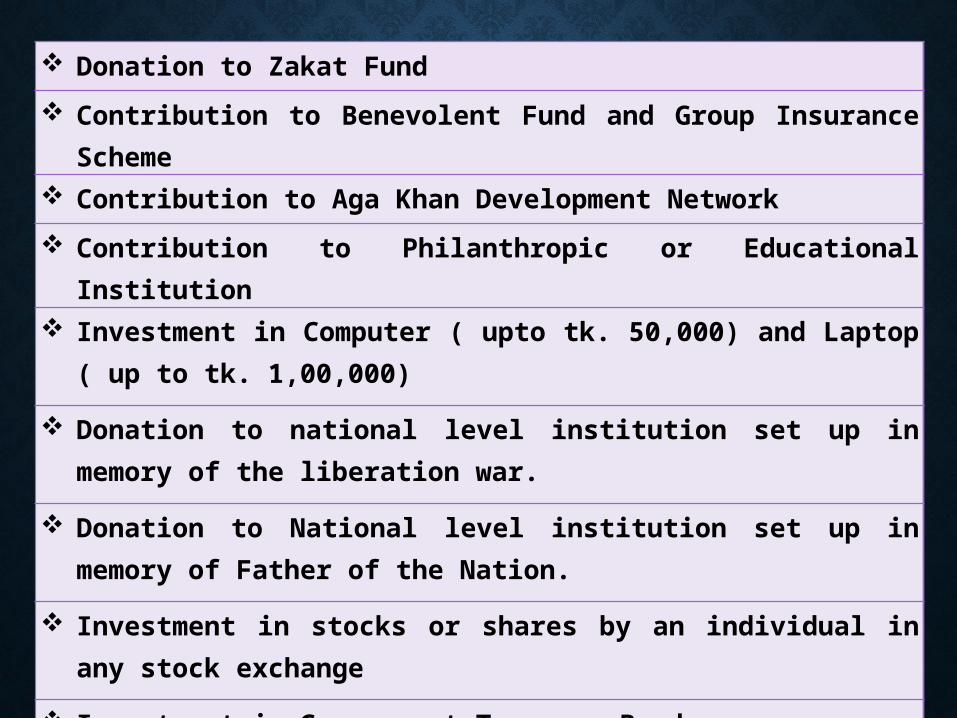

Donation to Zakat Fund

Contribution to Benevolent Fund and Group Insurance Scheme

Contribution to Aga Khan Development Network

Contribution to Philanthropic or Educational Institution

Investment in Computer ( upto tk. 50,000) and Laptop ( up to tk. 1,00,000)

Donation to national level institution set up in memory of the liberation war.

Donation to National level institution set up in memory of Father of the Nation.

Investment in stocks or shares by an individual in any stock exchange

Investment in Government Treasure Bond

PROBLEM RELATED TO

INCOME SALARY & SOLUTION

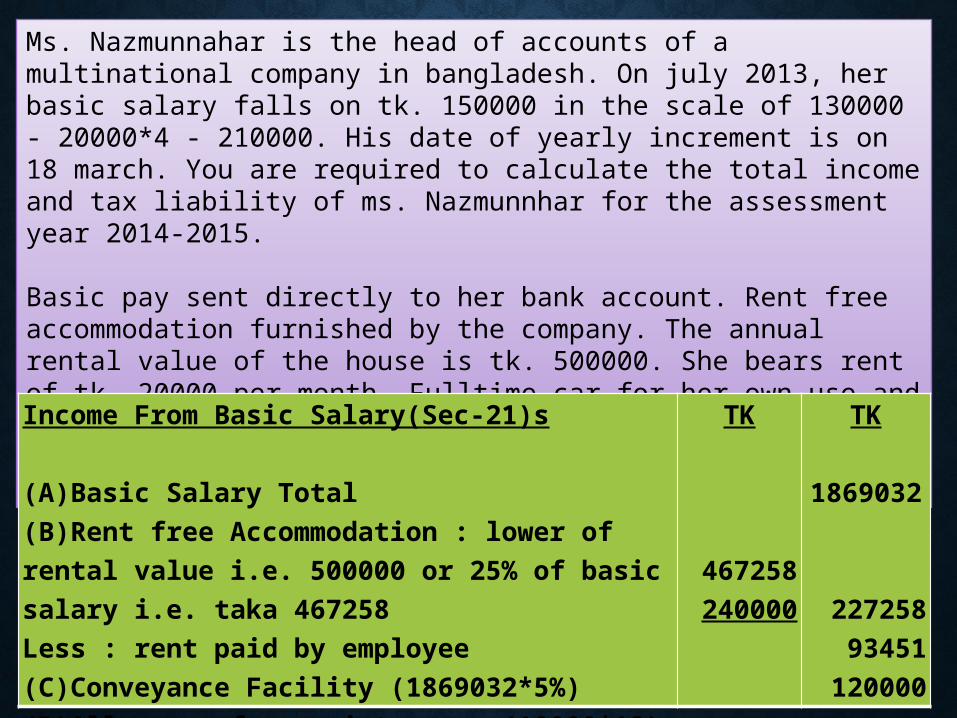

Ms. Nazmunnahar is the head of accounts of a multinational company in bangladesh. On july 2013, her basic salary falls on tk. 150000 in the scale of 130000 - 20000*4 - 210000. His date of yearly increment is on 18 march. You are required to calculate the total income and tax liability of ms. Nazmunnhar for the assessment year 2014-2015.

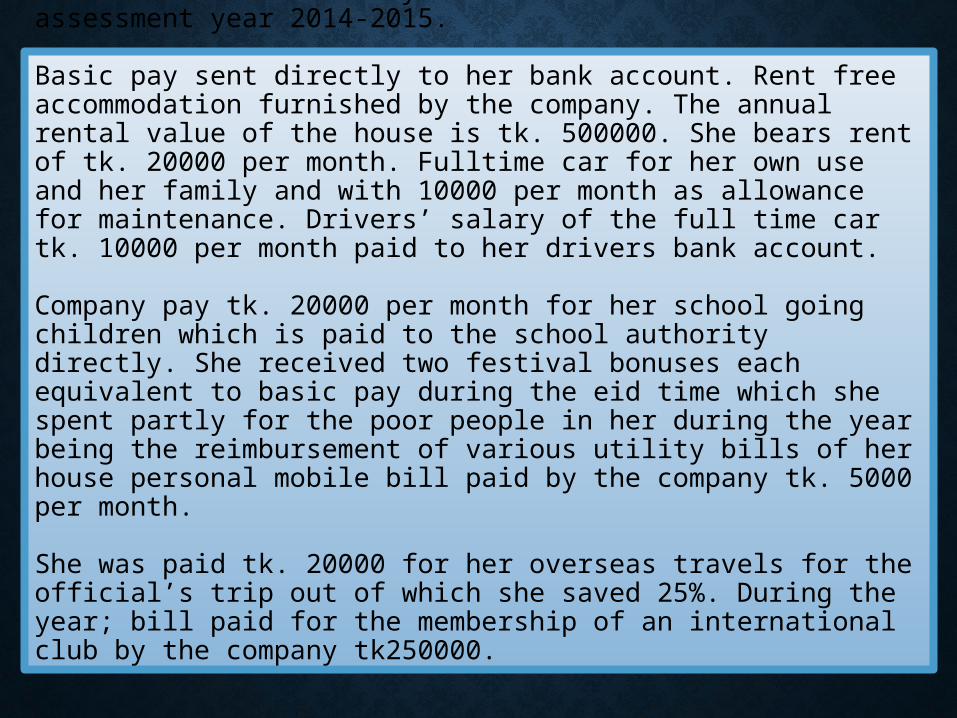

Basic pay sent directly to her bank account. Rent free accommodation furnished by the company. The annual rental value of the house is tk. 500000. She bears rent of tk. 20000 per month. Fulltime car for her own use and her family and with 10000 per month as allowance for maintenance. Drivers’ salary of the full time car tk. 10000 per month paid to her drivers bank account.

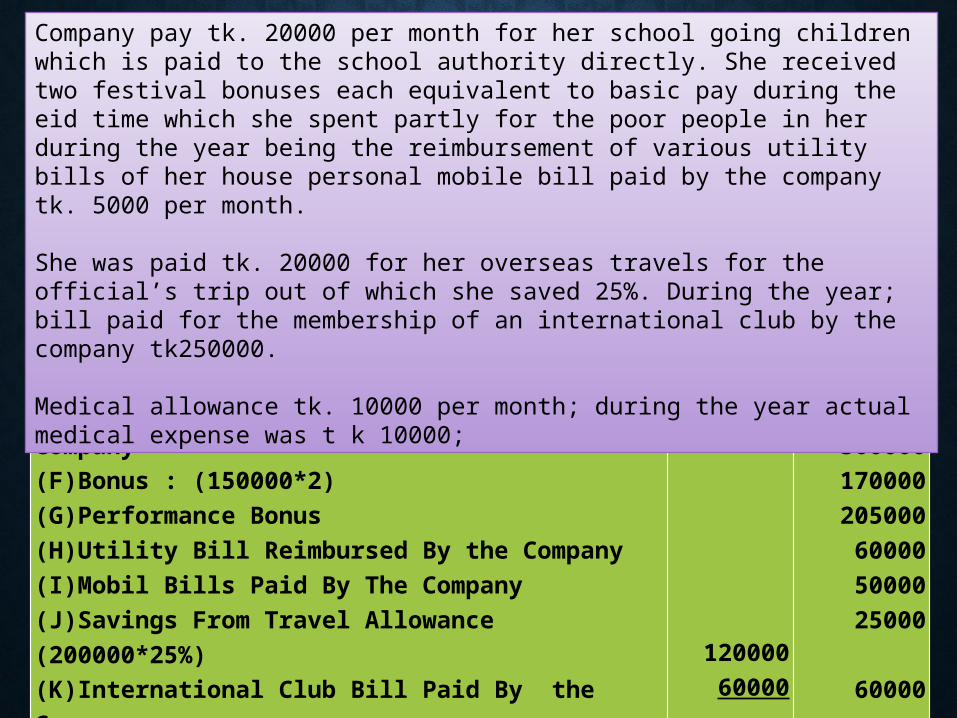

Company pay tk. 20000 per month for her school going children which is paid to the school authority directly. She received two festival bonuses each equivalent to basic pay during the eid time which she spent partly for the poor people in her during the year being the reimbursement of various utility bills of her house personal mobile bill paid by the company tk. 5000 per month.

She was paid tk. 20000 for her overseas travels for the official’s trip out of which she saved 25%. During the year; bill paid for the membership of an international club by the company tk250000.

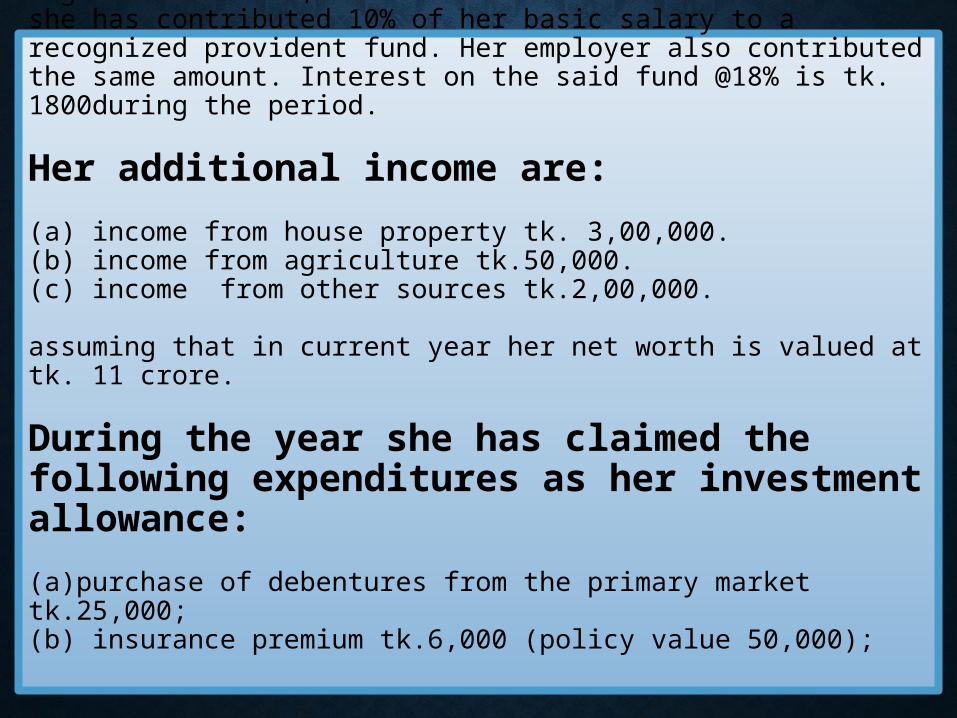

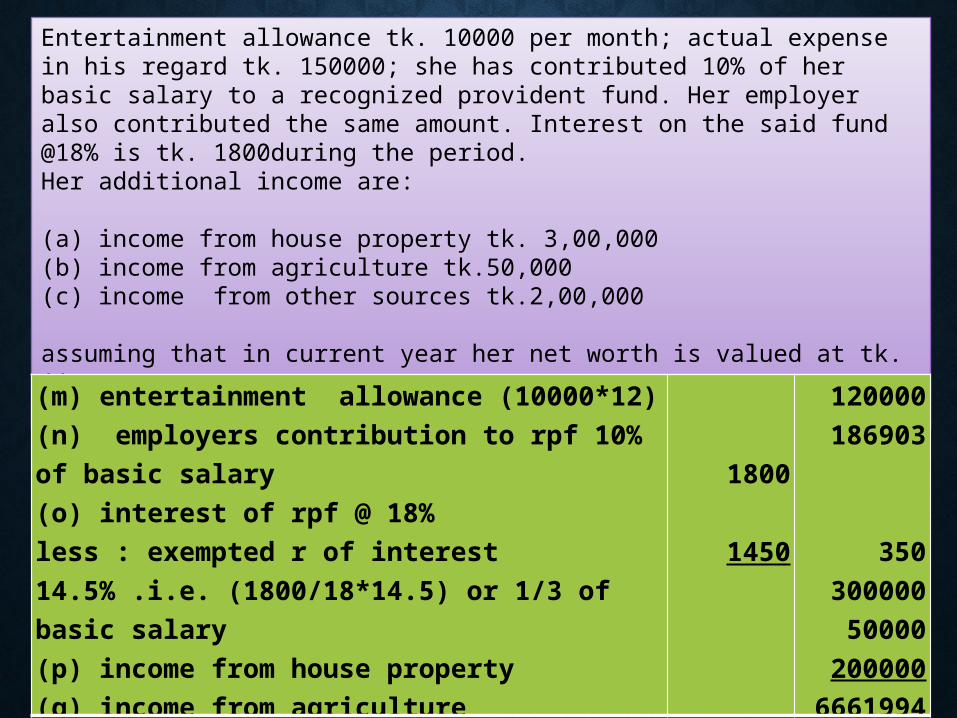

Medical allowance tk. 10000 per month; during the year actual medical expense was t k 10000; entertainment allowance tk. 10000 per month; actual expense in his regard tk. 150000; she has contributed 10% of her basic salary to a recognized provident fund. Her employer also contributed the same amount. Interest on the said fund @18% is tk. 1800during the period.

Her additional income are:

(a) income from house property tk. 3,00,000.(b) income from agriculture tk.50,000.(c) income from other sources tk.2,00,000.

assuming that in current year her net worth is valued at tk. 11 crore.

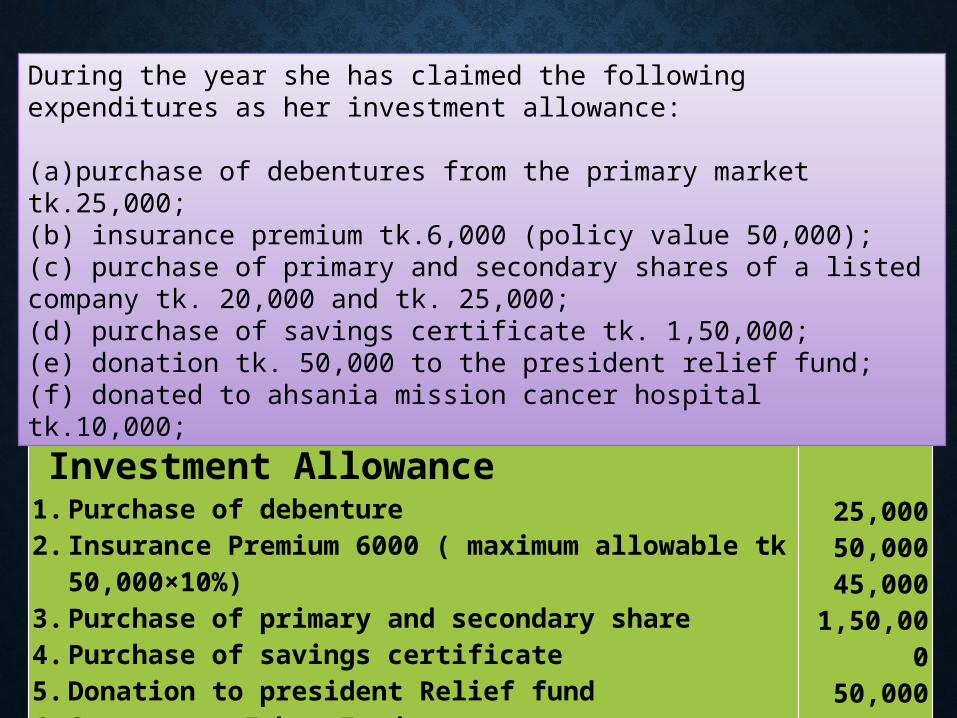

During the year she has claimed the following expenditures as her investment allowance:

(a)purchase of debentures from the primary market tk.25,000;(b) insurance premium tk.6,000 (policy value 50,000);

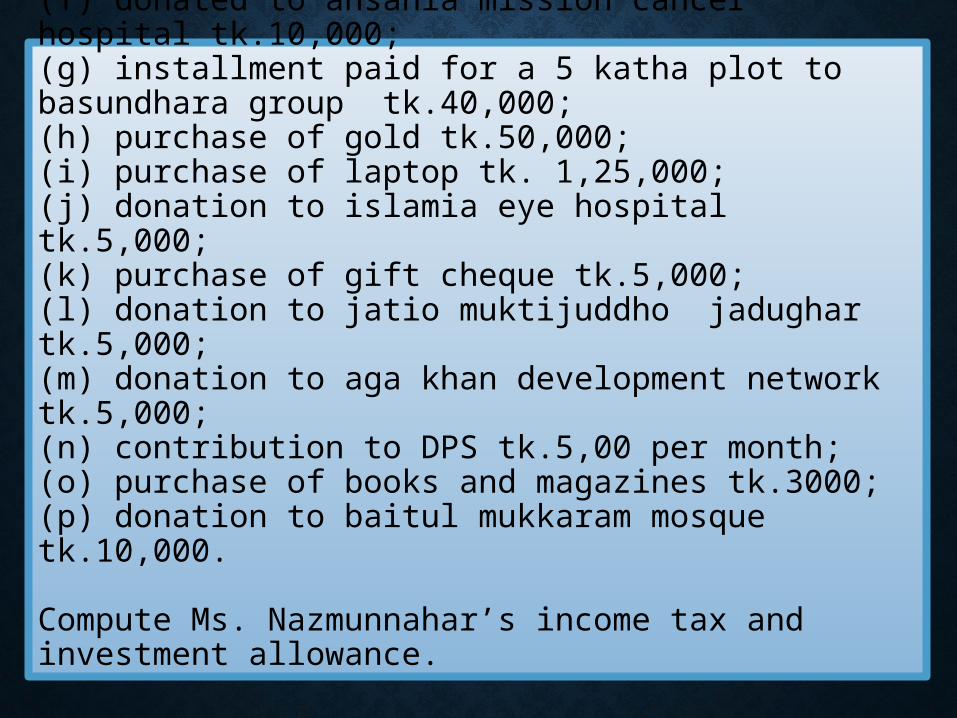

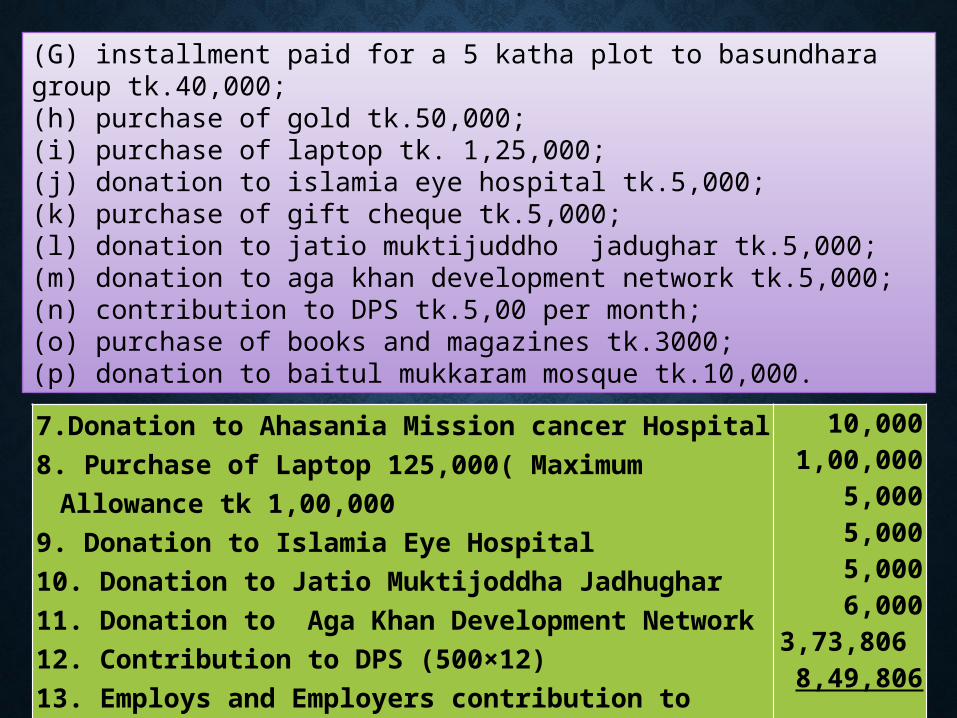

(c) purchase of primary and secondary shares of a listed company tk. 20,000 and tk. 25,000;(d) purchase of savings certificate tk. 1,50,000;(e) donation tk. 50,000 to the president relief fund;(f) donated to ahsania mission cancer hospital tk.10,000;(g) installment paid for a 5 katha plot to basundhara group tk.40,000;(h) purchase of gold tk.50,000;(i) purchase of laptop tk. 1,25,000;(j) donation to islamia eye hospital tk.5,000;(k) purchase of gift cheque tk.5,000;(l) donation to jatio muktijuddho jadughar tk.5,000;(m) donation to aga khan development network tk.5,000;(n) contribution to DPS tk.5,00 per month;(o) purchase of books and magazines tk.3000;(p) donation to baitul mukkaram mosque tk.10,000.

Compute Ms. Nazmunnahar’s income tax and investment allowance.

Ms. Nazmunnahar is the head of accounts of a multinational company in bangladesh. On july 2013, her basic salary falls on tk. 150000 in the scale of 130000 - 20000*4 - 210000. His date of yearly increment is on 18 march. You are required to calculate the total income and tax liability of ms. Nazmunnhar for the assessment year 2014-2015.

Basic pay sent directly to her bank account. Rent free accommodation furnished by the company. The annual rental value of the house is tk. 500000. She bears rent of tk. 20000 per month. Fulltime car for her own use and her family and with 10000 per month as allowance for maintenance. Drivers’ salary of the full time car tk. 10000 per month paid to her drivers bank account.

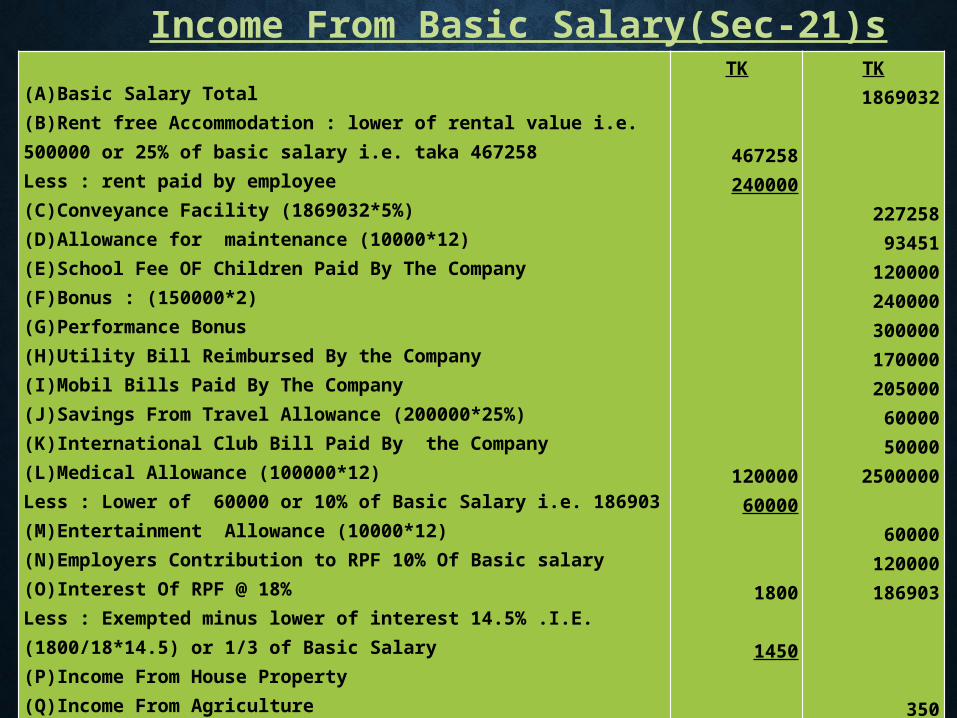

Income From Basic Salary(Sec-21)s (A)Basic Salary Total(B)Rent free Accommodation : lower of rental value i.e. 500000 or 25% of basic salary i.e. taka 467258Less : rent paid by employee(C)Conveyance Facility (1869032*5%)(D)Allowance for maintenance (10000*12)

TK

467258240000

TK

1869032

227258

93451120000

(E)School Fee OF Children Paid By The Company(F)Bonus : (150000*2)(G)Performance Bonus(H)Utility Bill Reimbursed By the Company(I)Mobil Bills Paid By The Company(J)Savings From Travel Allowance (200000*25%)(K)International Club Bill Paid By the Company(L)Medical Allowance (100000*12)Less : Lower of 60000 or 10% of Basic Salary i.e. 186903

12000060000

240000300000170000205000 600005000025000

60000

Company pay tk. 20000 per month for her school going children which is paid to the school authority directly. She received two festival bonuses each equivalent to basic pay during the eid time which she spent partly for the poor people in her during the year being the reimbursement of various utility bills of her house personal mobile bill paid by the company tk. 5000 per month.

She was paid tk. 20000 for her overseas travels for the official’s trip out of which she saved 25%. During the year; bill paid for the membership of an international club by the company tk250000.

Medical allowance tk. 10000 per month; during the year actual medical expense was t k 10000;

Entertainment allowance tk. 10000 per month; actual expense in his regard tk. 150000; she has contributed 10% of her basic salary to a recognized provident fund. Her employer also contributed the same amount. Interest on the said fund @18% is tk. 1800during the period. Her additional income are:

(a) income from house property tk. 3,00,000(b) income from agriculture tk.50,000(c) income from other sources tk.2,00,000

assuming that in current year her net worth is valued at tk. 11 crore.

(m) entertainment allowance (10000*12)(n) employers contribution to rpf 10% of basic salary(o) interest of rpf @ 18%less : exempted r of interest 14.5% .i.e. (1800/18*14.5) or 1/3 of basic salary(p) income from house property (q) income from agriculture(r) income from other sources

1800

1450

120000186903

350300000

50000200000

6661994

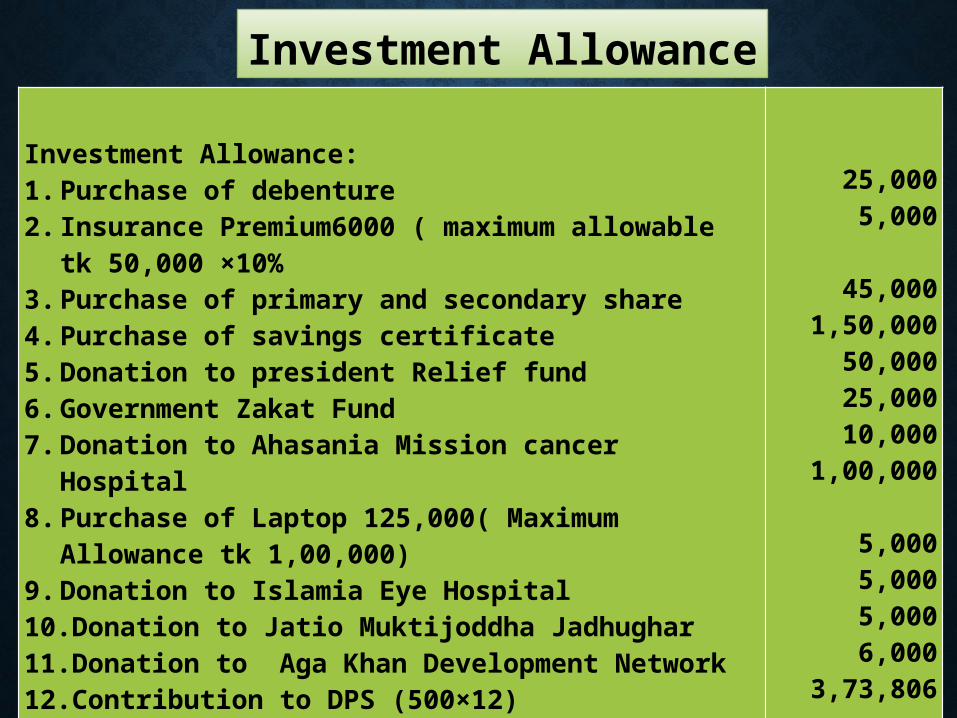

Investment Allowance1. Purchase of debenture2. Insurance Premium 6000 ( maximum allowable tk

50,000×10%)3. Purchase of primary and secondary share4. Purchase of savings certificate5. Donation to president Relief fund6. Government Zakat Fund

25,000 50,00045,000

1,50,00050,00025,000

During the year she has claimed the following expenditures as her investment allowance:

(a)purchase of debentures from the primary market tk.25,000;(b) insurance premium tk.6,000 (policy value 50,000);(c) purchase of primary and secondary shares of a listed company tk. 20,000 and tk. 25,000;(d) purchase of savings certificate tk. 1,50,000;(e) donation tk. 50,000 to the president relief fund;(f) donated to ahsania mission cancer hospital tk.10,000;

(G) installment paid for a 5 katha plot to basundhara group tk.40,000;(h) purchase of gold tk.50,000;(i) purchase of laptop tk. 1,25,000;(j) donation to islamia eye hospital tk.5,000;(k) purchase of gift cheque tk.5,000;(l) donation to jatio muktijuddho jadughar tk.5,000;(m) donation to aga khan development network tk.5,000;(n) contribution to DPS tk.5,00 per month;(o) purchase of books and magazines tk.3000;(p) donation to baitul mukkaram mosque tk.10,000.

7. Donation to Ahasania Mission cancer Hospital8. Purchase of Laptop 125,000( Maximum Allowance tk

1,00,0009. Donation to Islamia Eye Hospital10. Donation to Jatio Muktijoddha Jadhughar11. Donation to Aga Khan Development Network12. Contribution to DPS (500×12)13. Employs and Employers contribution to R.P.F (186,903×2)

Total=

10,0001,00,000

5,0005,0005,0006,000

3,73,806 8,49,806

(A)Basic Salary Total(B)Rent free Accommodation : lower of rental value i.e. 500000 or 25% of basic salary i.e. taka 467258Less : rent paid by employee(C)Conveyance Facility (1869032*5%)(D)Allowance for maintenance (10000*12)(E)School Fee OF Children Paid By The Company(F)Bonus : (150000*2)(G)Performance Bonus(H)Utility Bill Reimbursed By the Company(I)Mobil Bills Paid By The Company(J)Savings From Travel Allowance (200000*25%)(K)International Club Bill Paid By the Company(L)Medical Allowance (100000*12)Less : Lower of 60000 or 10% of Basic Salary i.e. 186903 (M)Entertainment Allowance (10000*12)(N)Employers Contribution to RPF 10% Of Basic salary(O)Interest Of RPF @ 18%Less : Exempted minus lower of interest 14.5% .I.E. (1800/18*14.5) or 1/3 of Basic Salary(P)Income From House Property (Q)Income From Agriculture(R)Income from Other Sources

TK

467258240000

12000060000

1800

1450

TK 1869032

227258

93451120000240000300000170000

205000 6000050000

2500000

60000120000186903

350

30000050000

2000006661994

Income From Basic Salary(Sec-21)s

Investment Allowance:1. Purchase of debenture2. Insurance Premium6000 ( maximum allowable tk 50,000

×10%3. Purchase of primary and secondary share4. Purchase of savings certificate5. Donation to president Relief fund6. Government Zakat Fund7. Donation to Ahasania Mission cancer Hospital8. Purchase of Laptop 125,000( Maximum Allowance tk

1,00,000)9. Donation to Islamia Eye Hospital10.Donation to Jatio Muktijoddha Jadhughar11. Donation to Aga Khan Development Network12.Contribution to DPS (500×12)13.Employs and Employers contribution to R.P.F (186,903×2)

25,0005,000

45,000

1,50,00050,00025,00010,000

1,00,000

5,0005,0005,0006,000

3,73,806

Total= 8,49,806

Investment Allowance

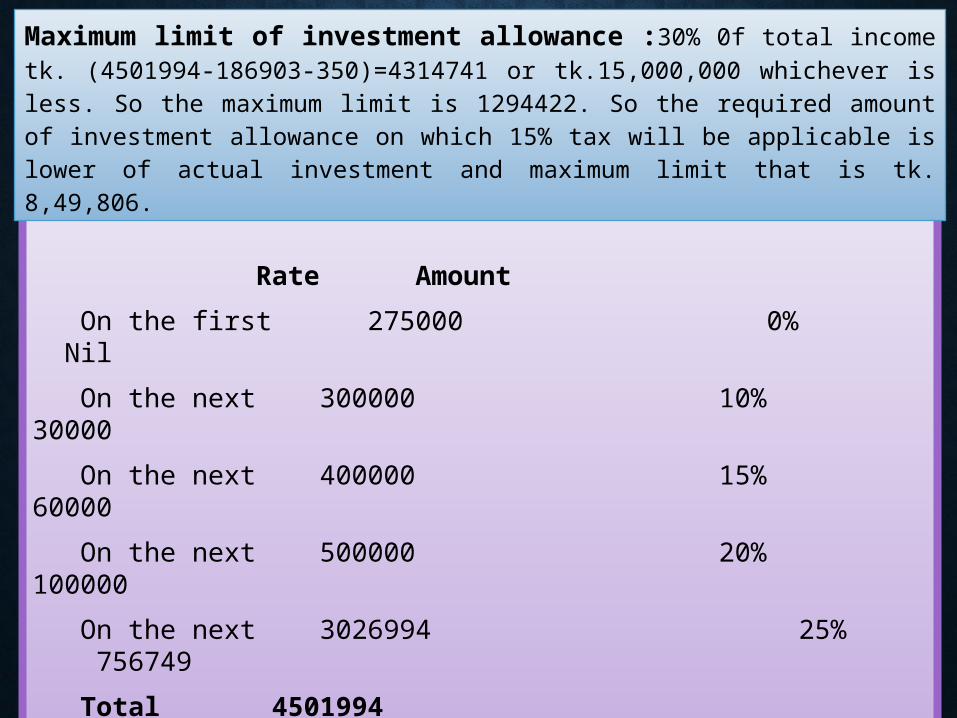

Tax Liability

Rate Amount

On the first 275000 0% Nil

On the next 300000 10% 30000

On the next 400000 15% 60000

On the next 500000 20% 100000

On the next 3026994 25% 756749

Total 4501994 946749

Less: Investment tax credit 127471

819278

Add: Surcharge (819278*15%) 122892 Net tax liability 942170

Maximum limit of investment allowance :30% 0f total income tk. (4501994-186903-

350)=4314741 or tk.15,000,000 whichever is less. So the maximum limit is 1294422. So the required amount of investment allowance on which 15% tax will be applicable is lower of actual investment and maximum limit that is tk. 8,49,806.

THANKS TO ALL