Embed Size (px)

Citation preview

chair

Adrienne Woodyard DLA Piper (Canada) LLP

March 9, 2017

Tax Primer FOR LITIGATORS

*CLE17-0020801-a-puB*

DISCLAIMER: This work appears as part of The Law Society of Upper Canada’s initiatives in Continuing Professional Development (CPD). It provides information and various opinions to help legal professionals maintain and enhance their competence. It does not, however, represent or embody any official position of, or statement by, the Society, except where specifically indicated; nor does it attempt to set forth definitive practice standards or to provide legal advice. Precedents and other material contained herein should be used prudently, as nothing in the work relieves readers of their responsibility to assess the material in light of their own professional experience. No warranty is made with regards to this work. The Society can accept no responsibility for any errors or omissions, and expressly disclaims any such responsibility.

© 2017 All Rights Reserved

This compilation of collective works is copyrighted by The Law Society of Upper Canada. The individual documents remain the property of the original authors or their assignees.

The Law Society of Upper Canada 130 Queen Street West, Toronto, ON M5H 2N6Phone: 416-947-3315 or 1-800-668-7380 Ext. 3315Fax: 416-947-3991 E-mail: [email protected] www.lsuc.on.ca

Library and Archives Canada Cataloguing in Publication

Tax Primer for Litigators

ISBN 978-1-77094-811-3 (Hardcopy)ISBN 978-1-77094-812-0 (PDF)

1

Chair: Adrienne Woodyard, DLA Piper (Canada) LLP

March 9, 2017 9:00 a.m. to 12:00 p.m.

Total CPD Hours = 2 h + 30 m Substantive + 30 m Professionalism

The Law Society of Upper Canada Donald Lamont Learning Centre

130 Queen St. W. Toronto, ON

SKU: CLE17-0030301-A-REG

Agenda

9:00 a.m. – 9:05 a.m. Welcome and Opening Remarks

Adrienne Woodyard, DLA Piper (Canada) LLP

9:05 a.m. – 9:20 a.m. Intro: Key Tax Concepts for Litigators

Adrienne Woodyard, DLA Piper (Canada) LLP

Tax Primer FOR LITIGATORS

2

9:20 a.m. – 9:40 a.m. Achieving Tax-Efficient Settlements / Tax Treatment of Damage Awards

John Sorensen, Gowling WLG (Canada) LLP 9:40 a.m. – 10:00 a.m. GST/HST: What Lawyers Need to Know for Their Own

Practices D’Arcy Schieman, Osler Hoskin Harcourt LLP

10:00 a.m. – 10:20 a.m. CRA’s Collection Powers and Competing Claims: How

Parties’ Tax Debts Can Impact Lawyers, Trust Accounts and Amounts Held in Escrow/Holdback Funds

Timothy Fitzsimmons, Dentons Canada LLP 10:20 a.m. – 10:35 a.m. Coffee and Networking Break 10:35 a.m. – 10:55 a.m. Tax Implications of Debt Forgiveness and Seizure /

Repossession of Property Robert Kepes, Morris Kepes Winters LLP 10:55 a.m. – 11:15 a.m. When a Company Fails: Liability of Directors,

Shareholders and Transferees Leigh Somerville Taylor, Leigh Somerville Taylor

Professional Corporation 11:15 a.m. – 11:45 p.m. Professionalism Panel

Moderator- Adrienne Woodyard, DLA Piper (Canada) LLP

Panelists- Martha MacDonald, Torys LLP Pooja Mihailovich, Osler Hoskin Harcourt LLP

3

11:45 a.m. – 12:00 p.m. Go Ahead and Ask Us (Question and Answer Session) 12:00 p.m. Program Ends

1

March 9, 2017

SKU: CLE17-0030301-A-REG

Table of Contents

TAB 1 Tax Treatment of Damages and Settlement Amounts …………………………………………. 1 – 1 to 1 – 6

John Sorensen, Gowling WLG (Canada) LLP

TAB 2 GST/HST and Damage Payments: What Tax Litigators Need to Know ………………………….…………. 2 – 1 to 2 – 5

D’Arcy Schieman, Osler Hoskin Harcourt LLP Alan Kenigsberg, Osler Hoskin Harcourt LLP

TAB 3 CRA’s Collection Powers and Competing Claims: How Parties’ Tax Debts Can Impact Lawyers, Trust Accounts and Amounts Held in Escrow Holdback Funds ………………………………………………… 3 – 1 to 3 – 4

Timothy Fitzsimmons, Dentons Canada LLP

Tax Primer FOR LITIGATORS

2

TAB 4 Tax Implications of Debt Forgiveness & Seizure /

Repossession of Property ……………………………………… 4 – 1 to 4 - 10 Robert Kepes, Morris Kepes Winters LLP

Cindy Chiu, Morris Kepes Winters LLP Jennifer Leve, Morris Kepes Winters LLP

TAB 5 When a Company Fails: Liability of Directors, Shareholders and Transferees ………………………………. 5 – 1 to 5 – 31 Leigh Somerville Taylor, Leigh Somerville Taylor

Professional Corporation TAB 6 Professionalism Panel ………………………………………… 6 – 1 to 6 – 3

Martha MacDonald, Torys LLP Pooja Mihailovich, Osler Hoskin Harcourt LLP

Adrienne Woodyard, DLA Piper (Canada) LLP

TAB 1

Tax Treatment of Damages and Settlement Amounts

John Sorensen Gowling WLG (Canada) LLP

March 9, 2017

Tax Primer FOR LITIGATORS

TAX TREATMENT OF

DAMAGES AND

SETTLEMENT AMOUNTS

JOHN SORENSEN March 9, 2017 Damages and Settlement Payments Damages are money payable to a person as compensation for injury suffered Chamberlain v. The North American Accident Insurance Co., 1916 CanLII 334 (AB CA), at p. 301 In this presentation, I treat damages and settlement payments synonymously

• Income Tax Act (Canada) (“ITA”) does not set out code for taxation of damages: tax results are governed by general provisions and case law

• Tax treatment depends on characterization of amount • Receipt may be fully or partially taxed, or not taxed at all • A payment may be fully deductible or not • Tax treatment should be considered from outset of civil action: to assess tax, revenue

authority may rely on position taken in action by party

• Practice points • As a litigator, confirm in writing with your client that you are not providing tax

advice • Connect client with tax counsel or obtain instructions to retain counsel for advice

Overview

1. Employment Law 2. Personal Injury 3. Commercial Litigation

1 - 1

1. Employment Law & Dismissals

• Query whether worker was employee or contractor in business on her own account

• General principles: • was there an agreement; • control over the worker; • ownership of tools; • chance of profit; and • risk of loss

• Key concept in this area: retiring allowance • Taxable under ITA subpara. 56(1)(a)(ii)

• not including an amount received under an employee benefit plan, a retirement compensation arrangement or salary deferral arrangement

• Retiring allowance defined in ITA ss. 248(1): an amount received on or after retirement

from office or employment recognizing long service; or in respect of loss of office or employment, whether or not received as or on account of damages

• Not including pension/death benefit or counseling service to employee

• Inclusions: • Unpaid sick leave likely retiring allowance • Unpaid accumulated vacation time likely not

• Planning opportunities

• Retiring allowance taxed when received, so spreading payments over time could reduce tax at top marginal rate – may be bargaining chip in settlement

• Rollover to RRSP/RPP

• Transitional rules make this confusing, but employees with years of service before 1996 may transfer part of retiring allowance directly to an RRSP/RPP (“eligible portion”)

• Non-eligible piece can be transferred to if there is contribution room

• Consider also apportioning amongst heads of damage – amount may be partially: retiring allowance, tort damages, punitive

• T4A reporting and withholding to extent of any taxable amount (not transferred to RRSP/RPP)

• Withholding can waived if both payer and recipient agree and sign form • Speaking of tort damages and employment • Compensation for defamation or human rights violation likely not taxable • Challenge: will employer admit in settlement documents to bad acts?

1 - 2

• Further challenge: how to benchmark the defamation or human rights amount?

• Possible to use # of months of service • Using income as benchmark doesn’t necessarily make compensation “income”

• Apportionment of amounts determined by the CRA or Tax Court in accordance with their

“true character” • Apportionment must be reasonable and supported – fact driven exercise • Nonetheless, way pleadings or settlement/release documents are written may be

persuasive since drafting reflects parties’ intentions

• Characterization of Amounts • Ahmad case as example • Sued Ontario Hydro for breach of employment agreement • CRA called general damages retiring allowance • Tax Court said “no” – general damages were for Ontario Hydro ruining his career • Taxpayer stood his ground, lost his career and consequently self-respect and

dignity • General damages compensated for that

• Characterization of Amounts

• University dean who was passed over for teaching position for which qualified • Sued and received damages • CRA called it retiring allowance • Tax Court held it was for loss of future position and untethered from dean role

• Query also whether plaintiff was ever employed

• Schwartz SCC • Accepted corporate job and quit law practice • Company withdrew the offer and paid $400k for release • SCC held not ss. 248(1) retiring allowance

• ITA subpara. 56(1)(a)(ii) did not provide for tax on settlements for loss of intended

employment • General charging provision in s. 3 not applicable, because general provision trumped by

specific retiring allowance provision • Taxpayer never employed so no nexus between settlement and employment

• Legal fees incurred to obtain retiring allowance may be deductible (more specifically,

reimbursement of fees taxable under ITA ss. 56(1)(l.1) but deductible under ss. 60(o.1) • Any allocation of damages/settlement to reimbursement of legal fees must be

supportable, not fanciful • If you lose – see para. 8(1)(b) deduction

1 - 3

• Pre-judgment interest

• Tracks tax treatment of underlying amounts • Interest non-taxable to extent award not taxable

2. Personal Injury • General ITA rules and case law principles apply to deduction/inclusion • Special and general damages non-taxable • Special - typically out of pocket expenses (e.g. medical) or accrued and future lost

earnings • General – pain and suffering, loss of amenities of life, loss of earning capacity etc.

• Whether damages based on accrued or lost future earnings could be characterized as

employment income is a question of fact • But typically even if damages measured by lost income, should not be taxed • Again, accrued interest attributable to non-taxable aware would be non-taxable

• Cirella case (FCTD 1978)

• CRA determined compensation for loss of earnings was taxable • Court held that commercial case law not applicable – injured person not a

damaged business asset

• Forest case (FCA 2007) • Sued employer for damages for harassment ($100k “moral” damages and $100k

exemplary) for violating his fundamental rights including to honour, respect, dignity and reputation, by continuously harassing him

• Received $152k to abandon his suit

• CRA assessed based on retiring allowance • TCC agreed • FCA held that only $23k was in exchange for voluntarily leaving employment,

pursuant to employer’s policy so the rest was non-taxable

• Moral to the story – he lost at trial it seems because he argued that all of the settlement was for harassment and TCC judge could not agree

• Arguing apportionment would have been more advisable?

1 - 4

• Mathew (TCC 2012) • Allocation/characterization needs to be supportable • Don’t want a court to describe a settlement as “an attempt to camouflage

substantial amounts of income … received for work … as tax free damages for pain and suffering.”

3. Commercial Litigation Commercial Disputes - Recipient

• At high level/general rule: tax treatment of an amount tracks treatment of thing that was lost

• Compensation for lost income in commercial context typically taxed as income • Compensation for loss of, or damage to, capital property likely capital receipt • Surrogatum principle

• Can be confusing because again compensation for loss of an income producing asset

could be calculated using lost income as benchmark, but still be capital receipt • As very loose guideline, consider tree/fruit analogy

• Tree is capital asset producing fruit • Fruit is income

• Is compensation for loss of tree or production from tree (i.e. income) • As noted above, amounts in commercial context may be categorized as either:

• Paid for purpose of gaining or producing income (fully and currently deductible) • Paid on capital account (not deductible on a current basis but capital cost

allowance) • Eligible capital expenditure (deductible in accordance with specific ITA

provisions)

• In reality, capital gain treatment is most likely • Not surprisingly, punitive damages not taxable as not tethered to either capital asset or

lost income • Planning opportunity

• As with other types of damages, in commercial context consider allocation between heads of damage

• Important that pleadings / court order / settlement document be explicit

• As always, allocation needs to be reasonable and supportable • Consider also symmetry between how the payer and recipient would treat amount(s)

• Inconsistent treatment may be challenging to justify to CRA

1 - 5

• Pre and post judgment interest taxable • Unless interest connected with a non-taxable receipt

Commercial Disputes - Payer

• Payer’s perspective • Outlays may be fully deductible or capital expenditures • Key provisions s. 9 and paras. 18(1)(a) and (b) • Subsection 9(1) first queries whether claiming deduction was consistent with

“ordinary principles of commercial trading or well accepted principles of business”

Symes SCC 1993

• Beyond that general test: • 18(1)(a) limits deductibility of outlays except to extent made or incurred for

purpose of gaining or producing income from business or property • 18(1)(b) limits deductibility of outlays in respect of loss or replacement of capital,

obsolescence or depletion except as expressly provided for in ITA

• Payer’s perspective • Full deduction likely where damages paid as result of event incidental to normal

course of business or where connected with inherent risk of business • Where payment is capital in nature, deduction over time for capital cost

allowance

• Assets from which income derives: enduring benefit concept • Enduring benefit means more than benefit derived from a long-lived asset • Could also mean a benefit arising from an expenditure associated with breaking a long-

term lease or contract

• Payer’s perspective • Punitive damages likely deductible if incurred for purpose of earning income

from business or property • Query whether public policy would bar this

• McNeill (FCA) extended 65302 (SCC – deductibility of fines & penalties) • Breach of contract was intentional and damage deliberate, but bad acts were for

purpose of earning income from business, thus deductible • Still possible acts could be so repulsive that they could be disconnected from purpose of

earning income

1 - 6

TAB 2

GST/HST and Damage Payments: What Tax Litigators Need to Know

D’Arcy Schieman Alan Kenigsberg

Osler Hoskin Harcourt LLP

March 9, 2017

Tax Primer FOR LITIGATORS

GST/HST and Damage Payments: What Tax Litigators Need to Know

Presentation for the Law Society of Upper Canada: Tax Primer for Litigators

by Alan Kenigsberg and D’Arcy Schieman, Osler, Hoskin & Harcourt LLP

I. OVERVIEW OF GST/HST AND PROVINCIAL SALES TAXES

• The federal Goods and Services Tax (“GST”) is a value added tax that applies to most supplies of goods and services made in, or imported into, Canada, including most supplies of legal services. The current rate of GST is 5%.

• The provinces of Ontario, Prince Edward Island, Newfoundland, Nova Scotia and New Brunswick have harmonized their provincial sales taxes with the GST to form a single tax referred to as the Harmonized Sales Tax (“HST”). The HST is composed of the 5% federal GST plus an 8% or 10% provincial component, to equal a single rate of 13% in Ontario, and 15% in Prince Edward Island, Newfoundland, Nova Scotia and New Brunswick. The HST is imposed under the same act as the GST (the Excise Tax Act (“ETA”)), generally has the same rules as the GST, and uses the same GST registration number as is used for GST purposes.

• Most parties (with the exception of status Indians on a reserve, select provincial and territorial governments under certain circumstances, and recipients of zero-rated (taxable) supplies (described below)) must pay GST/HST on their purchases of taxable supplies made in Canada.

• GST registrants are generally required to collect GST or HST (depending on what province the supplies are considered to be made in) on their taxable supplies, and any GST and HST collected generally must be remitted by the GST registrant on their GST return for the period. There is only a single return which covers both the GST and HST.

• GST registrants who are engaged in commercial activities1 can generally claim input tax credits (in effect a refund) for GST/HST paid in the course of their commercial activities.

• Quebec has a 9.975% sales tax, the Quebec Sales Tax (“QST”), which generally applies in the same manner as the GST/HST, and generally follows the same rules. However, unlike the HST, there is a separate registration for QST, and any QST collected by the QST registrant must be remitted on a separate QST return.

• The provinces of Manitoba (8%), Saskatchewan (5%) and British Columbia (7%) have provincial sales taxes which apply in a different manner than the GST/HST, and generally only apply to most sales of tangible personal property and certain taxable services (which

1 As defined in the ETA – usually the registrant is engaged in a business which makes taxable supplies – i.e. the registrant is required to charge GST/HST on its supplies or its supplies are zero-rated (tax applies at the rate of 0%, as is the case for certain supplies of services to non-residents of Canada). Commercial activities is defined not to include exempt supplies such as many financial services.

2 - 1

generally include legal services provided in the province). Each province has its own separate registration requirements and its own filing requirements.

II. GST/HST ON DAMAGES FOR BREACH OF CONTRACT

a) Section 182 of the ETA and the Application of GST/HST to Payments for Damages

• Absent the deeming rule in section 182 of the ETA (discussed below), a damage payment would generally not be consideration for a supply, as it is compensatory or punitive in nature, and is not given in exchange for a supply of property or services by another party. Accordingly, it would generally not be subject to GST/HST, even if the payee agrees to release the payer from further liability. This applies regardless of whether the damage payment is made as a result of a court judgment or as a result of a settlement that was concluded in order to avoid a court judgment. Thus, absent the rule in section 182 of the ETA, most payments for damages would generally not be subject to GST/HST.

• Section 182 of the ETA provides that in cases where an amount is paid to a GST registered supplier as a consequence of the breach, modification or termination of an agreement for the making of a taxable supply (other than a zero-rated supply) by the supplier, the payment is deemed to include GST/HST. For example:

o Assume a GST/HST registered supplier enters into an agreement to sell widgets in Ontario to a purchaser for a price of $1,000 plus $130 of HST, the purchaser terminates the agreement, and the purchaser agrees to pay the supplier $500 as damages for the breach of the agreement. In these circumstances, section 182 of the ETA would apply, and the payment of the $500 would be deemed to be inclusive of tax. As such, the purchaser would be deemed to have paid $442.48 of consideration (100/113 * $500), and to have paid $57.52 of HST (13/113 * $500). The GST/HST registered supplier is deemed to have collected the $57.52 of HST, and must include this amount in its net tax calculation of the GST/HST it must remit to the CRA for the taxation period in which the payment is made.

• Since section 182 provides that, in certain circumstances, any payment made by the recipient of a supply to the supplier is deemed to be made inclusive of GST/HST, the amount of GST/HST included will depend on the particular province in which the supply is considered to be made. As such, the supplier would be deemed to have collected 5/105 of the amount if the supply in the example above was made in Alberta and only subject to GST, 13/113 of the amount if the supply was subject to HST in Ontario, or 15/115 of the amount received from the recipient if the supply was in one of the other HST provinces.

• If the deeming rule in section 182, described above, applies, the supplier would be required to remit the amount set out above regardless of whether the payment was made to the supplier in respect of a court ordered payment or an out-of-court settlement which was awarded as a consequence of the breach, modification or termination of an agreement for a taxable (but not zero-rated) supply. The rule could also apply where the recipient of the supply is required to pay or forfeit an amount to the registered supplier, or reduce or extinguish a debt or other obligation of the supplier. In these circumstances, the application of section 182 of the Excise Tax Act should be considered.

2 - 2

• It should be noted that the deeming rule in section 182 of the ETA does not apply in all circumstances. For example, it does not apply to payments made by the supplier to the recipient of the supply. Any time a damage payment is made, the parties should consider whether the payment is a taxable payment for a supply, is a non-taxable payment for damages, or whether section 182 deems the payment to be inclusive of tax.

• If careful attention is not taken to determine whether 182 applies, the total amount of the damage payment agreed to by the parties could be different than what the parties expect. Specifically, a party expecting to receive $100,000 as a damage payment may in fact only be receiving $88,495.58 (100/113 of $100,000) on its own account and may be required to remit the additional $11,504.42 received to the CRA as HST. For the same reason, a party expecting to make a damage payment of $100,000, may end up being entitled to an input tax credit of $11,504.42, such that they only effectively pay $88,495.58.

b) Technical Requirements for the Deeming Rule in Section 182 of the ETA

• For section 182 to apply, the following conditions must be satisfied:

(a) there must be an agreement (although it need not be in writing) for the making of a taxable supply (other than a zero-rated supply2) in Canada;

(c) the supplier is a GST registrant;

(d) the agreement is breached, modified or terminated;

(e) an amount is paid or forfeited to the GST/HST registered supplier by the purchaser otherwise than as consideration for the supply (if paid as consideration for a taxable supply, it would be taxable under the normal rules). Alternatively, a debt or other obligation of the supplier is reduced without payment;

(f) the amount paid or forfeited is not a late payment charge, as contemplated by section 161 of the ETA; and

(g) the amount paid or forfeited is neither for demurrage nor an inter-railway rolling stock penalty for failure to return rolling stock, as contemplated by section 162.1 of the ETA.

c) Circumstances under which Section 182 does not apply

• The CRA discusses in Policy Statement P-218R, “Tax Status of Damage Payments, Whether or not Within Section 182 of the Excise Tax Act” (August 9, 2007), situations in which section 182 does not apply. These situations include:

2 Zero-rated supplies are supplies where GST/HST is charged at a rate of 0%, such that no tax is actually payable. Zero-rated supplies include most supplies of services to non-residents of Canada, goods sold to a purchaser for export, etc. When a supply is intended to be zero-rated under Schedule VI, Part V, section 1 (a supply made to a purchaser who intends to export the property), the supply is arguably not zero-rated until after the supply takes place and property is subsequently exported. It is unclear that section 182 will apply if an agreement for such a supply is breached.

2 - 3

(a) where no prior agreement for the making of a supply existed between the parties;

(b) the original agreement was for the making of an exempt or zero-rated supply;

(c) the person making the payment is the supplier (since section 182 only applies to payments to the supplier, not to payments by the supplier);

(d) the supplier is not a GST/HST registrant;

(e) the payment is actual consideration for a supply; or

(f) the amount paid is otherwise than as a consequence of the breach, modification or termination of the agreement for the making of the supply.

• Section 182 also does not apply to certain contracts entered into in writing before 1991 (i.e., certain contracts pre-GST) where tax was not contemplated in the agreement.

• An award of judicial costs is not subject to section 182 even if the award purports to say “GST-inclusive” or “HST-inclusive,” as no supply of legal services is being made by the successful party to the unsuccessful party. An award that is “GST/HST-inclusive” in this context likely means that the losing party is required to reimburse the winning party for any unrecoverable GST/HST paid on legal fees by the party receiving the award.

• Where a payment for non-fulfillment of a provision is made pursuant to an indemnity clause in a contract, such as a provision specifically providing for liquidated damages, it is arguable that since the contract provides for payment, it is not made as consequence of the “breach, termination or modification” of the agreement3.

• Section 182 generally does not apply to payments for claims in tort rather than in contract. Such payments are normally not subject to GST, as there is no taxable supply.

d) Effect of Section 182

• If section 182 applies, paragraph 182(1)(a) provides that the purchaser is deemed to have paid consideration for the supply equal to 100/105 of the amount paid or forfeited in a GST province. In an HST province (with an HST rate of 13%), the purchaser is deemed to have paid consideration for the supply equal to 100/113 of the amount paid or forfeited.

• Paragraph 182(1)(b) then provides that the purchaser is deemed to have paid GST/HST on the amount paid or forfeited, and the supplier is deemed to have collected the same amount of tax. In effect, the total amount paid or forfeited is treated as “tax-included” for both parties.

• The purchaser may be able to claim an ITC if the original property or service would have been acquired for use in the course of the purchaser’s commercial activities.

3 The CRA agreed with this view in ruling letter HQR0000994 (October 8, 1998) but disagreed in letter HQR01294 (January 5, 1999).

2 - 4

e) Examples4

1. Aco and Bco enter into an agreement that Bco, a GST/HST registrant, was to make a taxable supply of custom software to Aco. Before the scheduled delivery date, Aco cancelled the order, but agreed to pay an amount to Bco to compensate for the cancellation. Is the payment subject to GST/HST under section 182?

o The payment is subject to GST/HST since all the requirements for the application of section 182 have been met. The payment is an amount other than for consideration for the supply under the agreement, and the payment is made as a consequence of the breach or termination of an agreement for the making of a taxable supply by a GST/HST registrant.

2. Cco and Dco enter into an agreement that Dco, a GST/HST registrant, would supply 1,000 widgets per month to Cco for a period of six months (for a total of 6,000 widgets). After 3 months and 3,000 widgets were delivered, Cco requests that the remaining portion of the order be modified to 1,500 widgets instead of 3,000. Cco agreed to pay Dco an additional amount as consideration for the modification. Is this payment for the modification subject to GST/HST under section 182?

o Yes as all the requirements have been met. The payment is an amount other than as consideration for the supply, it is made as a consequence of the modification of the agreement, and the payment is made to the GST/HST registered supplier.

3. Eco contracted with Fco whereby Fco would design and install a new software program by a certain date. Fco was unable to fulfil its obligations under the contract by the deadline, and Eco incurred additional expenses as a result of the non-delivery of the software by the date. Pursuant to negotiations, Eco agreed to release Fco from the contract in exchange for a settlement. Is the payment subject to GST/HST?

o The payment is not subject to GST/HST as it is in essence compensatory with respect to the additional expenses incurred by Eco, rather than consideration for a taxable supply. It is meant to restore Eco to the position it was in prior to the damage occurring.

o Further, subsection 182(1) does not apply as the payment is being made by the supplier and not to the supplier.

4. A truck owned by Gco causes damage to a property owned by Hco. Hco sues Gco for $100,000 for the damage caused by Gco’s truck. Gco agrees to settle the claim for a payment of $80,000. Is the payment subject to GST/HST?

o The payment is not subject to GST/HST as the payment is to compensate Gco for its losses. Further, section 182 does not apply as there was no agreement for a taxable supply between Gco and Hco.

4 Some of these examples are drawn from P-218R (which includes further examples and details).

2 - 5

TAB 3

CRA’s Collection Powers and Competing Claims: How Parties’ Tax Debts Can Impact

Lawyers, Trust Accounts and Amounts Held in Escrow/Holdback Funds

Timothy Fitzsimmons

Dentons Canada LLP

March 9, 2017

Tax Primer FOR LITIGATORS

CRA’s Collections Powers and Competing Claims: How Parties’ Tax Debts Can Impact Lawyers, Trust Accounts and Amounts Held in

Escrow/Holdback Funds Timothy Fitzsimmons Partner Tax Dispute Resolution and Tax Litigation CRA’s Collections Powers “Listen, and understand. The terminator is out there. It can’t be bargained with. It can’t be reasoned with. It doesn’t feel pity, or remorse, or fear. And it absolutely will not stop, ever …”

- Kyle Reese, The Terminator (1984) Background

• Assessments / Reassessments • Income tax, CPP contributions, EI premiums, GST/HST • Disputes –

• Notice of Objection • Notice of Appeal – Tax Court of Canada, Federal Court of Appeal, Supreme Court of

Canada Collections

• Collect from the tax debtor • Liens, garnishment, set-off, seizure of chattels

• If CRA can’t collect from tax debtor, collect from other persons … • Section 227.1 – Directors’ liability • Section 160 – Third party liability • Section 224 – Garnishment (“Requirement to Pay”)

Time limits

• Section 225.1 – 90 days after the mailing of a Notice of Assessment • … no delay for unremitted source deductions, and see jeopardy provisions …

• Section 222 – Ultimate 10-year limitation period

3 - 1

Compare Rule 60 of the Ontario Rules of Civil Procedure

Income Tax Act (Canada)

• Court proceedings – Section 223

• Set-off – Section 224.1

• Seizure of chattels – Section 225

• Security – Section 220

• Garnishment – Section 224

Section 224 – Garnishment / Requirement to Pay

Where the Minister …

• has knowledge or suspects

• that a person is or will be within one year

• liable to make a payment to a tax debtor …

the Minister may in writing require the person to pay

• forthwith or as and when the moneys become payable

• the moneys otherwise payable to the tax debtor … Section 224 - “Requirement to pay …”

• Subsections 224(1) and (1.1) contain the principal garnishment provisions under the Act. These provisions empower the Minister of National Revenue to collect unpaid taxes and other amounts owing under the Act by a person (the “tax debtor”) by serving a garnishment letter on any other person liable to make a payment to the tax debtor or on a financial institution or certain other persons intending to loan or advance moneys to the tax debtor. The garnishment letter requires these amounts to be paid to the Receiver General rather than to the tax debtor. • Department of Finance, Technical Notes, Section 224

• See also: • Canada Revenue Agency, “If you refuse to pay and to cooperate with the Canada

Revenue Agency” (2016-08-31) • Canada Revenue Agency, “Requirement to Pay: Questions and Answers” (2013-06-08)

Liable to pay …

• May apply to any payment

• No requirement for existence of debtor-creditor relationship

3 - 2

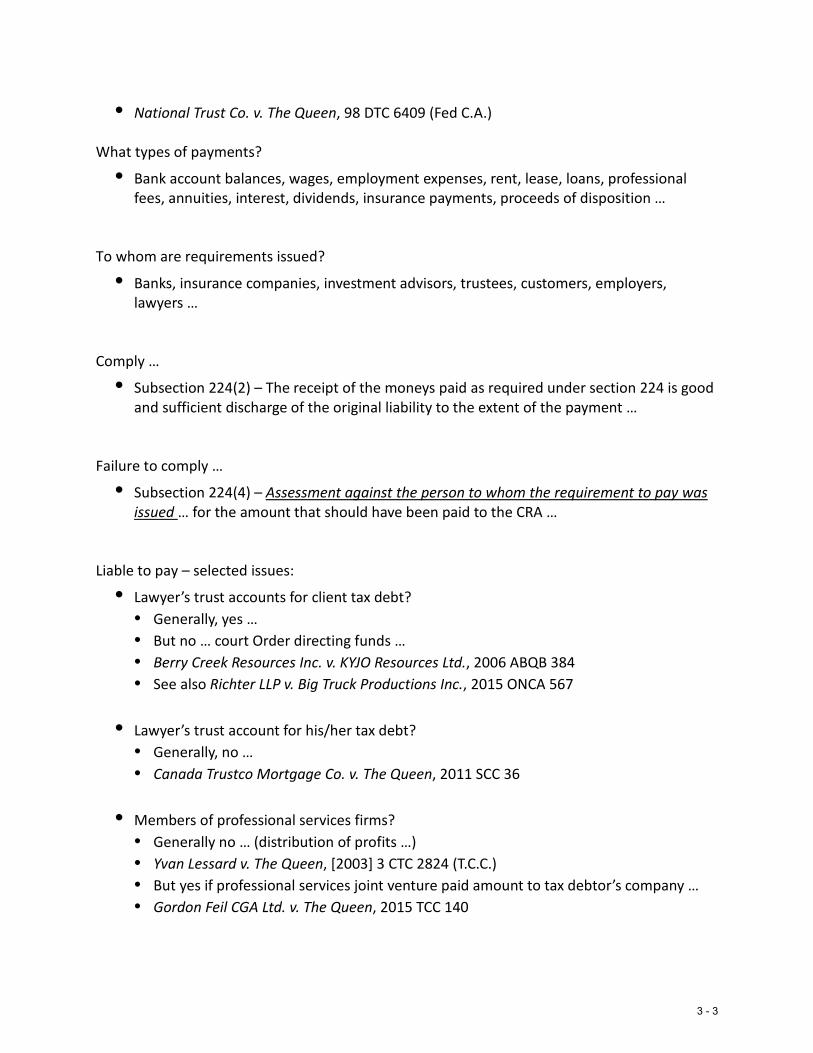

• National Trust Co. v. The Queen, 98 DTC 6409 (Fed C.A.)

What types of payments?

• Bank account balances, wages, employment expenses, rent, lease, loans, professional fees, annuities, interest, dividends, insurance payments, proceeds of disposition …

To whom are requirements issued?

• Banks, insurance companies, investment advisors, trustees, customers, employers, lawyers …

Comply …

• Subsection 224(2) – The receipt of the moneys paid as required under section 224 is good and sufficient discharge of the original liability to the extent of the payment …

Failure to comply …

• Subsection 224(4) – Assessment against the person to whom the requirement to pay was issued … for the amount that should have been paid to the CRA …

Liable to pay – selected issues:

• Lawyer’s trust accounts for client tax debt? • Generally, yes … • But no … court Order directing funds … • Berry Creek Resources Inc. v. KYJO Resources Ltd., 2006 ABQB 384 • See also Richter LLP v. Big Truck Productions Inc., 2015 ONCA 567

• Lawyer’s trust account for his/her tax debt? • Generally, no … • Canada Trustco Mortgage Co. v. The Queen, 2011 SCC 36

• Members of professional services firms? • Generally no … (distribution of profits …) • Yvan Lessard v. The Queen, [2003] 3 CTC 2824 (T.C.C.) • But yes if professional services joint venture paid amount to tax debtor’s company … • Gordon Feil CGA Ltd. v. The Queen, 2015 TCC 140

3 - 3

Liable to pay – selected issues:

• Amounts held by court clerk? • Generally, no … • HSBC Bank v. 410086 Alberta Ltd., 2010 ABQB 403

• Pending judgment in civil case? • Revenu Quebec entitled to attach notice to a civil lawsuit … • Location D’Autos Niveau Plus, [1998] G.S.T.C. 73 (F.C.T.D.)

3 - 4

TAB 4

Tax Implications of Debt Forgiveness and Seizure / Repossession of Property

Robert Kepes Cindy Chiu

Jennifer Leve Morris Kepes Winters LLP

March 9, 2017

Tax Primer FOR LITIGATORS

Tax Implications of Debt Forgiveness and Seizure/Repossession of Property

by Cindy Chiu, Robert Kepes, and Jennifer Leve1

Introduction

The purpose of this paper is to provide an overview of the tax rules regarding debt forgiveness

and the seizure or repossession of property.

Debt Forgiveness

The debt forgiveness rules are generally contained in section 80 of the Income Tax Act (“ITA”)2

and are intended to determine the tax consequences that arise on the settlement of certain debt

obligations owing to a debtor. The purpose of the debt forgiveness rules is to "claw back" tax

benefits or attributes (i.e. deductible expenses, adjusted cost base, etc.) that a taxpayer never

actually pays for, because the attributes are acquired with debt that is ultimately forgiven.3

In order for the debt forgiveness rules to apply, several requirements must be met:

the debt must be a “commercial debt obligation” issued by a debtor;

the commercial debt obligation must have been “settled or extinguished”; and

the settlement or extinguishment of the commercial debt obligation must result in a

“forgiven amount”.

When the above conditions are met, the forgiven amount will be applied to reduce losses of the

debtor through a series of ordering rules. Any remaining forgiven amount balance may then be

1 Morris Kepes Winters LLP.

2 All statutory references are to the provisions of the Income Tax Act (Canada) R.S.C. 1985, c. 1 (5th Supp.), as

amended (the “Act”) unless otherwise indicated. 3 This underlying policy concern was outlined in the 1966 Carter Commission Report. The current debt forgiveness

rules were introduced in 1994.

4 - 1

applied against other tax attributes of the debtor, and, if there is a further remaining forgiven

amount, a proportion of that remaining amount will be included in income.

What is a “commercial debt obligation”?

To be a commercial debt obligation, interest expense must have been deductible by the debtor

pursuant to a legal obligation to pay the interest, or, if interest was not payable, interest expense

would have been deductible if interest was payable. That is, it is irrelevant whether or not the

debt was interest bearing. What matters is whether the interest was or would have been tax

deductible.

Four elements in paragraph 20(1)(c) must be present before interest is deductible in a year: (1)

the interest must be paid in the year or be payable in the year; (2) the interest must be paid under

a legal obligation to pay interest on borrowed money; (3) the borrowed money must be used for

the purpose of earning non-exempt income from a business or property; and (4) the interest must

be reasonable.4

The requirement for interest deductibility effectively eliminates the application of the debt

forgiveness rules to personal loans.

When is a commercial debt obligation “settled”?

Paragraph 80(2)(a) of the Act provides that an obligation issued by a debtor will generally be

settled where the obligation is “settled or extinguished at that time”, which is not particularly

helpful guidance. The definition is circular, and the terms "settled" and "extinguished" are not

defined in the Act.

4 Collins (2010 FCA 12).

4 - 2

Some of the ways in which a debt obligation could be settled or extinguished include when the

debt obligation becomes statute-barred, by the payment of the amount owing to the creditor by

the debtor, or where the creditor and debtor deliberately agree to fix or vary their existing rights

or obligations; in other words, a novation of the debt obligation can settle or extinguish the

existing debt obligation. However, it is not necessary that a debt instrument be considered

“novated” from a legal perspective, as settlement or extinguishment of a debt obligation could

arise where the fundamental terms of the indebtedness are sufficiently materially altered.

The Canada Revenue Agency’s position is as follows:

For a debt or obligation to be “settled or extinguished” all liability

for payment must be terminated. Payment, cancellation, set-off,

substitution of debtors and release are examples of some possible

means of settlement. A debt or obligation is not settled when a

creditor abandons his right to enforce payment or becomes statute-

barred from enforcing his right to payment. However, a settlement

does occur where, by statute, the debtor's actual liability to pay is

extinguished after a specified period of time has elapsed.5

Paragraph 80(2)(a) provides two exceptions from the debt forgiveness rules: a settlement as a

result of a bequest or inheritance, and a settlement on the conversion of publicly-traded

convertible debt for shares of the corporate debtor.

Deemed settlement

In certain circumstances, the Act will deem the debt to be settled.

5 IT-293R, “Debtor's Gain on Settlement of Debt”, paragraph 6.

4 - 3

First, the amalgamation of a corporate debtor and creditor will result in a deemed settlement;

however the debtor is deemed to have paid an amount equal to the creditor’s cost amount of the

debt.6 Therefore, there should be no debt forgiveness as a result of the amalgamation.

Second, a debt owed to an unrelated creditor is deemed to be settled when it becomes statute

barred.

Third, a debt is deemed to be settled when it becomes “parked”. The debt parking rules are

beyond the scope of this paper, but they are designed to catch transactions that assist a debtor in

avoiding the debt forgiveness rules, typically so as to preserve the debtor’s loss carryforwards.

The creditor would sell the debt for less than its face amount to a shell company that was related

to the debtor. The shell company would never collect on the debt, and thus it had become

“parked”, but the debt would remain outstanding and not forgiven.

What is the “forgiven amount”?

Simply, a forgiven amount is the amount for which the debt was issued less the amount paid in

satisfaction of the debt. The forgiven amount is important as it is the amount used to reduce the

tax attributes of the debtor, and any unapplied forgiven amount is included in income. The

forgiven amount is expressed as a formula, A – B, where “A” is the lesser of the amount of

which the obligation was issued and the principal amount of the obligation. The forgiven

amount is reduced to the extent that the principal amount is less than the amount for which the

debt was issued. Amount “B” is the total of the amounts enumerated in item “B” of the

definition for “forgiven amount”. A description of all of these amounts is beyond the scope of

this paper; however, of particular relevance is paragraph (a) of amount “B” which is “the

6 The cost amount is generally the face amount of the debt that the creditor is entitled to receive.

4 - 4

amount, if any, paid at the time in satisfaction of the principal amount of the obligation.” This

means that in many cases, where a debt is settled and an amount (if any) is paid in satisfaction of

the principal amount of the debt which is less than the principal amount, a corresponding

forgiven amount will arise.

The application of the debt forgiveness rules

Once the requirements to fall within the ambit of the debt forgiveness rules are met, the forgiven

amount is applied to reduce to the tax attributes of the debtor in the following order:

1. Automatic application of the forgiven amount to prior year’s losses:

a. Non-capital losses

b. Farm losses

c. Restricted Farm Losses

d. Allowable business investment losses

e. Net capital losses

2. Discretionary application of any remaining forgiven amount among the following

accounts, in any order:

a. Undepreciated capital cost of depreciable property

b. Cumulative eligible capital

c. Resource expenditures

3. If the debtor applies any remaining forgiven amount to all the above tax attributes

(including those which are discretionary), the debtor may elect to apply any remaining

forgiven amount to the following accounts, in the following order:

4 - 5

a. Adjusted cost base of capital property (i.e. land and portfolio investments), but

excluding:

i. shares and debts of corporations of which the debtor owns more than 10%

or more of the corporation’s shares)

ii. interests in partnerships that are “related” to the debtor

b. Adjusted cost base of shares and debts of corporations of which the debtor does

own 10% or more of the corporation’s shares, but not including related

corporations

4. After maximum application to the above accounts, the debtor may apply any remaining

forgiven amount to current year capital losses in excess of capital gains.

5. After maximum application to the above accounts, the debtor may apply any remaining

forgiven amount to the adjusted cost base of shares and debts of related corporations and

interests in related partnerships, so long as the tax attributes of corporations that the

debtor corporation controls have been eliminated.

6. If any forgiven amount remains, and it has not been transferred to a related corporation,

50% of the amount is included in taxable income.

Relieving rules

Relief from income inclusion to a debtor under the debt forgiveness rules is available where the

debtor is a corporation or trust resident in Canada. In that case, the income inclusion may be

spread out over five years under a reserve mechanism.7 Where the debtor is an individual, other

than a trust resident in Canada, a reserve mechanism is available to limit income inclusion to

7 Sections 61.4 and 56.3 of the Act.

4 - 6

20% of the amount by which the individual’s income for the year exceeds $40,000.8 Where the

individual’s income is less than $40,000, the income inclusion can be deferred indefinitely. This

relief is also available in the year of death. Note that the relief available through the reserve

mechanism where the individual has made the maximum deductions possible to reduce his or her

tax attributes of assets other than debt and equity interests in related corporations and

partnerships.

Relief from the debt forgiveness rules are also available where income inclusion for a debtor

corporation may cause it to become insolvent.9 These rules operate to effectively allow an offset

against the income inclusion, but not a reserve, as the income must be included in current income

not at a later time.

Other than the relieving provisions discussed above, there are exclusions from the debt

forgiveness rules. Settlements arising on a bequest or inheritance, settlements involving the

issuance of distress preferred shares, settlements on the conversion of certain publicly-traded

convertible debts to shares, and statutory exclusions where other provisions of the Act override

the debt forgiveness rules, for example, section 79 which will be discussed below.10

Foreclosures and Repossessions

Sections 79 and 79.1 describe the tax implications to debtors and creditors when assets are

surrendered or seized as a result of a debtor’s failure to repay certain debt obligations, i.e.,

mortgages and other similar obligations and conditional sales agreements. A “surrender” or

“seizure” occurs where the beneficial ownership of the property is acquired or reacquired at that

8 Sections 61.2 and 56.2 of the Act.

9 Subsections 61.3(1) and 61.3(2).

10 An-depth discussion of these exceptions is beyond the scope of this paper.

4 - 7

time from the person by the other person and the acquisition or reacquisition of the property was

in consequence of the person’s failure to repay all or part of a debt obligation.11

The tax

implications to a debtor and creditor of a foreclosure or repossession are described below.

Section 79 – Consequences to a Debtor of a Surrender of Property

Where property (not including money or government debt) is surrendered by a debtor to a

creditor as a result of the debtor’s failure to pay all or part of a debt owed, the debtor is generally

deemed to have disposed of the property for proceeds equal to an amount determined by the

Act.12

Generally, proceeds of disposition will be the total of the unpaid principal amount and

unpaid accrued interest of the debt at that time, plus the amount of any unpaid principal and

accrued interest on debts owed to other creditors that are extinguished as a result of the transfer,

less any part of the debt that was included in the debtor’s income pursuant to other provisions of

the Act. If there are multiple properties being surrendered, the proceeds for each property are

determined as the proportion that the fair market value of the property is of the fair market value

of all the property.

On the surrender of the property, any gain or loss would be included in the debtor’s income and

taxed accordingly. However, this income is ignored for calculating certain entitlements and

obligations, including the old age credit threshold, GST/HST credit threshold, Canada Child

Benefit threshold, Working Income Tax Benefit threshold and the Old Age Security clawback

threshold.

11 Subsections 79(2) and 79.1(2).

12 Subsection 79(3).

4 - 8

The debt forgiveness rules do not apply to any portion of the principal amount that is included in

the deemed proceeds of disposition.13

If there is a subsequent payment by the debtor on a debt obligation where the property was

surrendered, it will be deemed to be a repayment of assistance and treated as a capital loss, where

the surrendered property was capital property, or an income deduction.14

Section 79.1 – Consequences to a Creditor of a Seizure of Property

Where property is seized by a creditor in consequence of the debtor’s failure to pay all or part of

a debt owed, the creditor is generally deemed to have acquired the property at a cost equal to the

total of the adjusted cost base of the debt plus certain expenses that the creditor incurred to

protects its interest, less certain reserves deducted in previous years.15

If there are multiple

properties being seized, the cost for each property is determined as the proportion that the fair

market value of the property is of the fair market value of all the property.

The creditor is also generally deemed to have disposed of the debt obligation for proceeds equal

to its adjusted cost base where the property is capital property, or to its cost amount for non-

capital property.16

As a result, the seizure by a creditor of property does not result in any

immediate tax consequences for a creditor.

13 Subsection 80(1) “forgiven amount” B(f).

14 Subsection 79)4).

15 Subsection 79.1(6).

16 Paragraphs 79.1(7)(a) and (b).

4 - 9

Where any portion of the debt remains outstanding after the seizure, the creditor shall be deemed

to have reacquired that portion immediately after that time at a cost equal to nil for capital

property and the cost amount for non-capital property.17

17 Paragraph 79.1(7)(c).

4 - 10

TAB 5

When a Company Fails: Liability of Directors, Shareholders

and Transferees

Leigh Somerville Taylor Leigh Somerville Taylor Professional Corporation

March 9, 2017

Tax Primer FOR LITIGATORS

When a Company Fails: Liability of Directors, Shareholders and Transferees Leigh Somerville Taylor, B.A. (Hons.), J.D., LL.M.(Tax) Leigh Somerville Taylor Professional Corporation

Page

I. Who is liable? 2

II. Directors 2

a. General Rule 2

b. Two-Year limitation period 3

i. De Facto Directors 4

c. Preconditions 8

d. Due diligence defence 9

e. Practice 15

III. Shareholders 16

a. General Rule 16

b. Preconditions 18

c. No due diligence defence 19

d. No limitation period 19

e. Dividends are transfers of property 21

f. Defences 21

g. Practice 26

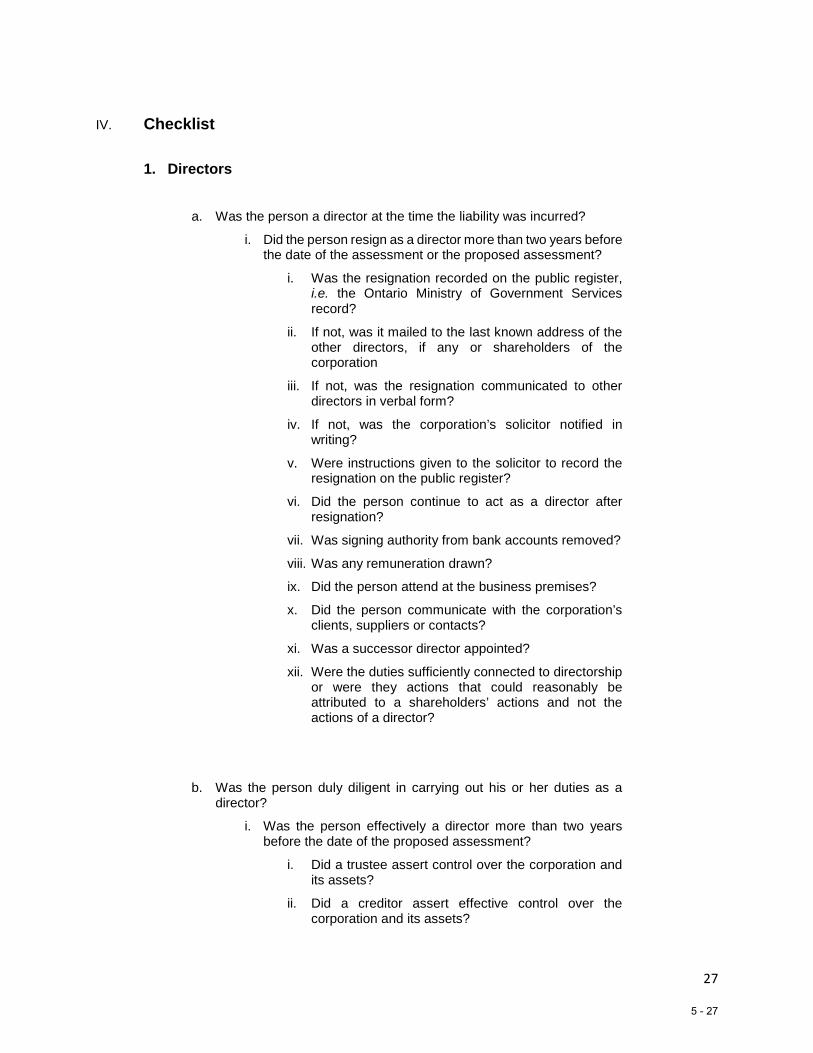

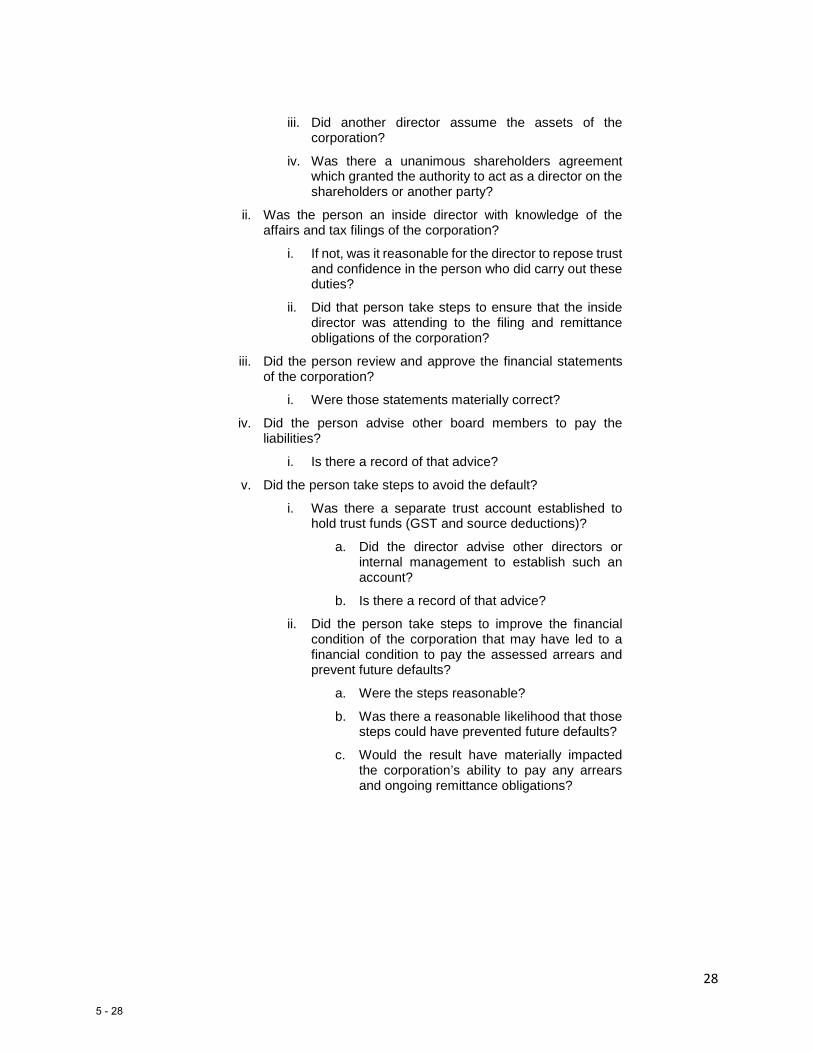

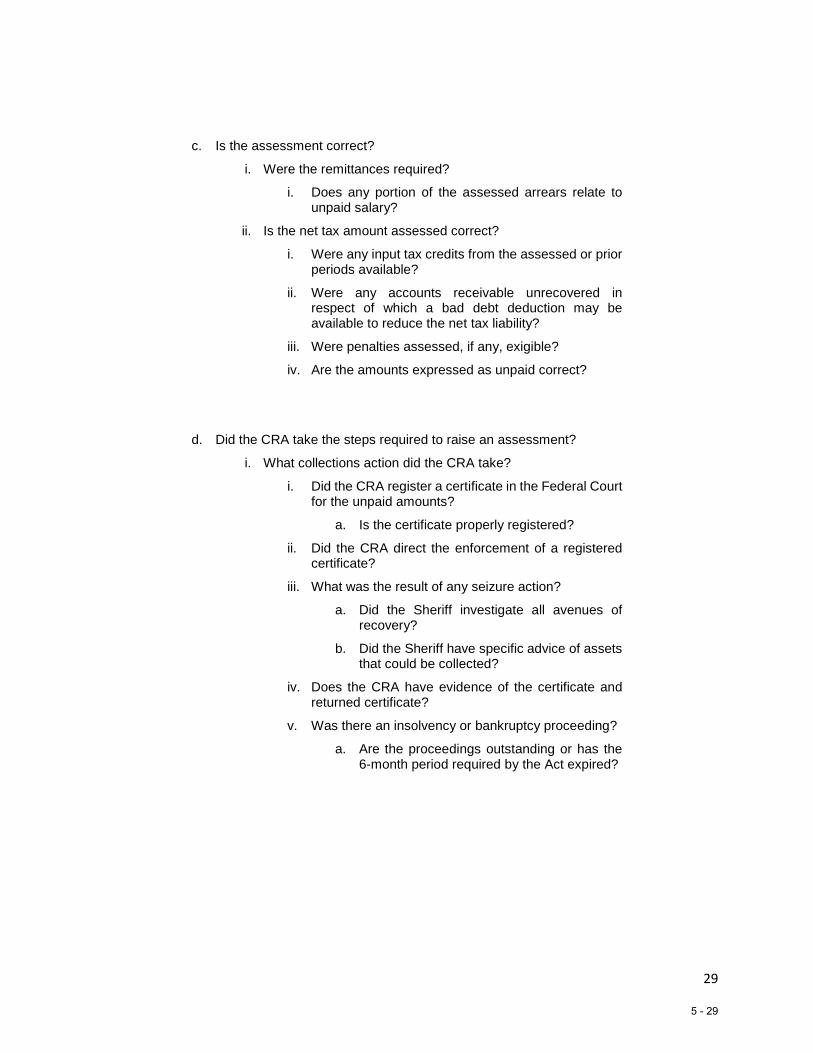

IV. Checklist 27

a. Directors 27

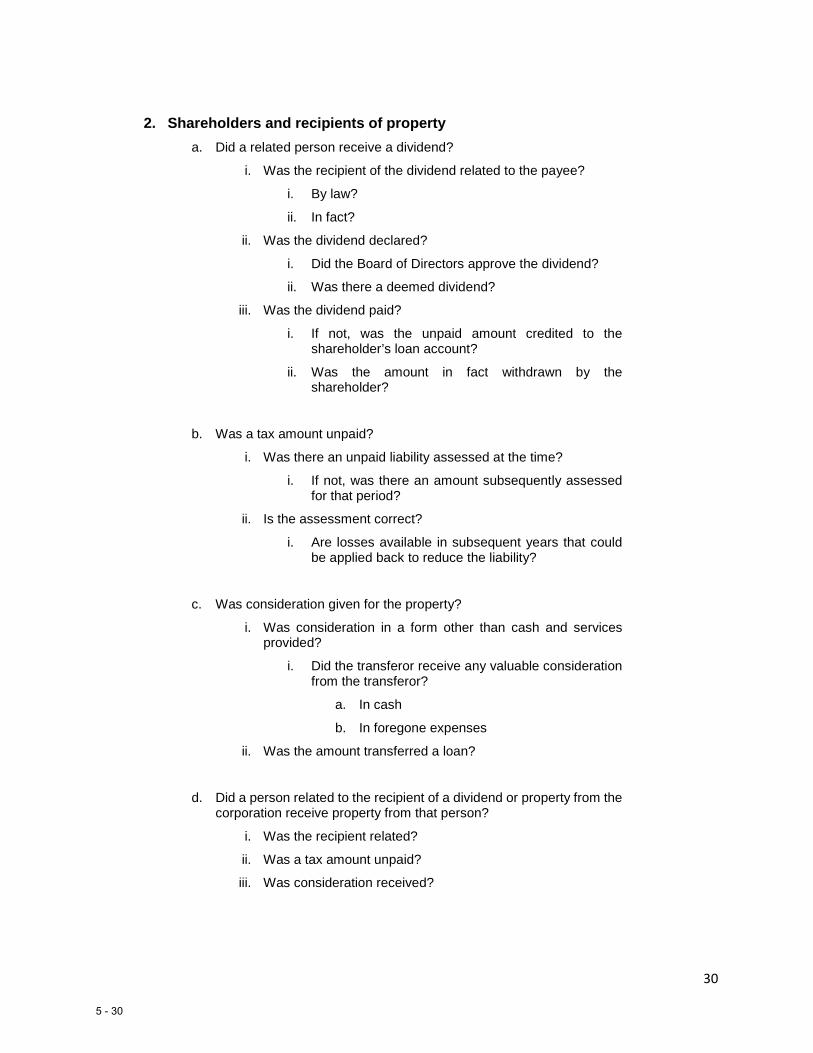

b. Shareholders 30

V. Appendix 31

5 - 1

2

I. Who is liable?

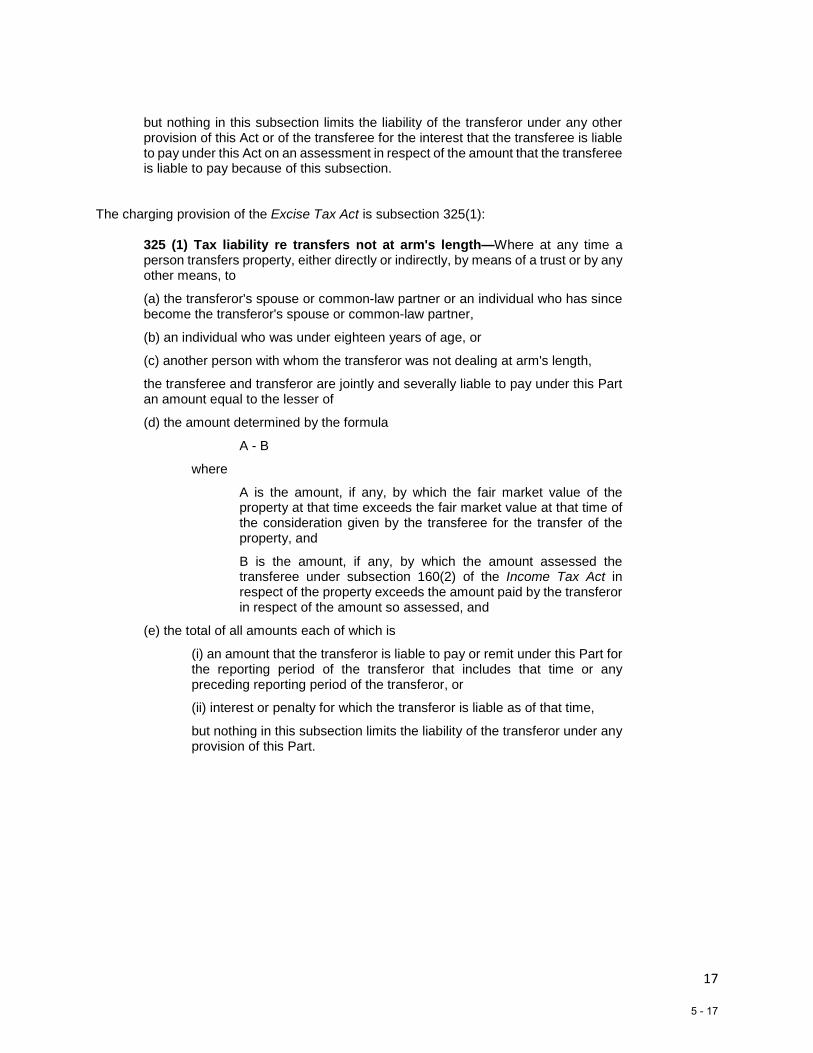

When a company fails, the Minister of National Revenue’s power to collect unpaid taxes does not end with the assets and undertakings of the company. The Income Tax Act, R.S.C., c. 1 (5th Supp.) (the “Income Tax Act”) and Excise Tax Act, R.S.C. 1985, c.E-15 (the “Excise Tax Act”) grant broad powers to raise derivative assessments against directors of a company and recipients of property from the corporation. II. Directors

a. General rule A director is jointly, severally and solidarily liable with a corporation for the unpaid GST and payroll remittance liabilities of a corporation. The charging provision of subsection 323(1) of the Excise Tax Act is:

323 (1) Liability of directors— If a corporation fails to remit an amount of net tax as required under subsection 228(2) or (2.3) or to pay an amount as required under section 230.1 that was paid to, or was applied to the liability of, the corporation as a net tax refund, the directors of the corporation at the time the corporation was required to remit or pay, as the case may be, the amount are jointly and severally, or solidarily, liable, together with the corporation, to pay the amount and any interest on, or penalties relating to, the amount.

The liabilities are the liabilities that should have been remitted, whether or not they comprise unpaid tax or improperly claimed input tax credits. The charging provision of subsection 227.1(1) of the Income Tax Act is:

227.1(1) Liability of directors for failure to deduct—Where a corporation has failed to deduct or withhold an amount as required by subsection 135(3) or 135.1(7) or section 153 or 215, has failed to remit such an amount or has failed to pay an amount of tax for a taxation year as required under Part VII or VIII, the directors of the corporation at the time the corporation was required to deduct, withhold, remit or pay the amount are jointly and severally, or solidarily, liable, together with the corporation, to pay that amount and any interest or penalties relating to it.

The liabilities are the liabilities that should have been withheld and remitted, whether or not they in fact were withheld and include deficiencies in employee payroll deductions pursuant to section 153 of the Income Tax Act and non-resident withholding tax pursuant to section 215 of the Income Tax Act, among other withholding obligations.1

1 Including amounts required to be withhold from payments respecting patronage dividends (pursuant to subsection 135(3)) and tax-deferred patronage dividends (pursuant to subsection 135.1(7).

5 - 2

3

A director may also be assessed for the CPP and EI obligations pursuant to the Canada Pension Plan2 and Employment Insurance Act.3 The amount exigible includes the amount of interest assessed on a deficient assessment and the interest that may have accumulated after assessment.4

b. Two-year limitation period The Canada Revenue Agency (“CRA”) may raise an assessment against a director only where the assessment was raised within two years of the date the person last ceased to be a director. The limitations are contained within section 323 of the Excise Tax Act and 227.1 of the Income Tax Act:

Excise Tax Act, 323(5) Time limit—An assessment under subsection (4) of any amount payable by a person who is a director of a corporation shall not be made more than two years after the person last ceased to be a director of the corporation. Income Tax Act, 227.1(4) Limitation period No action or proceedings to recover any amount payable by a director of a corporation under subsection (1) shall be commenced more than two years after the director last ceased to be a director of that corporation.

What it means to “last cease to be a director” is a topic of much dispute. When did the director really lose power to cause the corporation to pay its liabilities when due, if at all?

2 Canada Pension Plan, R.S.C., 1985, section 21.1:

21.1 (1) If an employer who fails to deduct or remit an amount as and when required under subsection 21(1) is a corporation, the persons who were the directors of the corporation at the time when the failure occurred are jointly and severally or solidarily liable, together with the corporation, to pay to Her Majesty that amount and any interest or penalties relating to it.

3 Employment Insurance Act, S.C. 1996, c. 23, section 83:

83 (1) If an employer who fails to deduct or remit an amount as and when required under subsection 82(1) is a corporation, the persons who were the directors of the corporation at the time when the failure occurred are jointly and severally, or solidarily, liable, together with the corporation, to pay Her Majesty that amount and any related interest or penalties.

4 See, e.g. Zen v. Her Majesty the Queen, [2010] 6 C.T.C. 28 (FCA).

5 - 3

4

De facto directors

The fiscal courts have consistently held that a director for the purposes of the director’s liability provisions can include both de jure and de facto directors. In Wheeliker v. Her Majesty the Queen, [1999] 3 F.C. 173 (sub nom. Canada v. Corsano) the Federal Court of Appeal held that the name is not determinative:

7 The ITA does not define “director” either for the purposes of the ITA as a whole or for the purposes of section 227.1. As this Court held in Kalef, it is therefore appropriate to look to the Corporation's incorporating legislation for guidance as to who is a “director” for the purposes of section 227.1. Under paragraph 2(1)(f) of the Act,

“director” includes any person occupying the position of director by whatever name called; [emphasis added]

I agree with the conclusion of the Tax Court judge that the words “occupying the position of director by whatever name called” brings within the definition a director irrespective of how this position may be designated. This is consistent with the approach of the Chancery Division in Lo-Line Electric Motors Ltd., Re where the Court interpreted the identical definition under the U.K. Companies Act, 1985. According to the Court:

...the words “by whatever named called” show that the subsection is dealing with nomenclature; for example where the company's articles provide that the conduct of the company is committed to “governors” or “managers.”

A shareholder may have the power to act as a director under a unanimous shareholders’ agreement expanding the scope of the liability or attributing the liability to a different party. The CRA has argued that continuing to communicate with the CRA regarding the tax debt or attendance to payment arrangements thereon is sufficient activity to comprise de facto directorship.5 The Federal Court of Appeal has confirmed that a de facto directorship endures at least as long as that person manages or supervises the management of the business and affairs of the corporation.” In Bremner v. Her Majesty the Queen, 2009 FCA 146, the Federal Court of Appeal considered and confirmed the actions of the person assessed as follows:

5 Consider, Walsh v. Her Majesty the Queen, 2009 TCC 557:

42 The Respondent's alternative position is that, even if the Appellant's resignation was effective, he remained a de facto director of JSL and as such, is liable for the company's unremitted source deductions. While acknowledging that there had not been much for the Appellant to do once the company ceased operations, counsel for the Respondent argued that the little he had done warranted a finding that he remained in control of JSL. Counsel relied, in particular, on the Appellant's having forwarded JSL cheques and correspondence to Mr. Raper and having authorized him to carry on discussions with CRA officials. Counsel submitted that the Appellant's actions went beyond mere holding out, as in Hartrell v. R.; here, the Appellant actually maintained control of JSL at all times relevant to this appeal.

5 - 4

5

5 The Tax Court Judge accepted the appellant's admission that he was a deemed director of the Corporation from the time of his wife's resignation as a director of the Corporation but did not agree with the appellant's argument that he ceased to be a director of the Corporation in September of 2000. Instead, the Tax Court Judge found that the appellant's engagement in the management of the Corporation continued until at least April 10, 2001, the date of a letter that the appellant wrote to the Canada Customs and Revenue Agency (the “CCRA”), as it was then known, in response to a letter it wrote. In his letter to the CCRA, the appellant requested that future correspondence from the CCRA should be sent to him, and not to his wife. 6 The Tax Court Judge found that in corresponding with the CCRA, the appellant demonstrated that he was still managing the actions of the Corporation, however minimal those actions may have been. 7 In our view, this finding is unassailable and is sufficient to dispose of the appeal, since it establishes that the two year limitation period for the assessment would not expire before April of 2003, a date subsequent to October 1, 2002, the date of the assessment. 8 While no authority was provided to the Court with respect to the interpretation of subsection 115(4) of the BCA, the language of that provision supports the conclusion that the directorship of a person that arises by virtue of that provision must be considered to endure at least as long as that person manages or supervises the management of the business and affairs of the corporation in question. 9 The Tax Court Judge found that by virtue of his having written the April 10, 2001 letter to the CCRA, the appellant engaged in the management of the business and affairs of the Corporation on that date. This factual finding was open to the Tax Court Judge and in making this finding, we are not persuaded that he committed a palpable and overriding error. While the appellant contends that this letter was written on behalf of his wife, this contention is not supported by the record. In fact, in testimony given in the Tax Court of Canada, the appellant stated that he was a director of the Corporation when he wrote that letter. It follows that the appellant was a deemed director of the Corporation on April 10, 2001, and consequently, the two year limitation period in subsection 323(5) of the ETA does not protect the appellant from liability under the assessment.

Individuals who act as directors may be held liable as directors, even if they have filed notice of their resignation with the appropriate authority. Regard should be had to the service requirements of the governing Business Corporations Act. If no successor director is appointed, a person may continue to act as a director notwithstanding a formal resignation. Consider section 115(4) of the Business Corporations Act (Ontario), which holds

115(4) Deemed Directors—Where all of the directors have resigned or have been removed by the shareholders without replacement, any person who manages or supervises the management of the business and affairs of the corporation shall be deemed to be a director for the purposes of this Act. 1994, c. 27, s. 71 (12).

5 - 5

6

In Goicoechia v. Her Majesty the Queen, 2010 TCC 539, the Tax Court affirmed the application of subsection 115(4) in the context of a sole shareholder of a corporation:

20 Even if the Appellant were considered to have resigned as director on May 3, 2004, the fact would remain, nevertheless, that he was the person who managed the affairs of the Corporation after May 3, 2004. At that point in time, the Corporation had no officer and no director, and the Appellant as sole shareholder was the only person who could appoint a new director. No one else could manage or administer the affairs of the Corporation. Subsection 115(4) of the OBCA contemplates the situation where all of the directors of a corporation have resigned or have been removed and deems the person who manages or supervises the management of the business to be the director of the corporation.

On the other end of the scale, a director may have effectively resigned even if the requirements of the governing Business Corporations Act were not met. In Perricelli v. Her Majesty the Queen, [2002] G.S.T.C. 71, the Court held that announcement to fellow directors may be sufficient:

23 I am satisfied Mr. Perricelli resigned in the summer of 1990. He did so when the three directors and shareholders were all together. It is a matter of whether this resignation was effective in accordance with the laws of Ontario. Did any one of the three men utter the words: “Notice of this meeting is waived?” Unlikely. Did Mr. Cuthbert and Mr. Lishman say: “We accept Mr. Perricelli's resignation and hereby elect the two of us as ongoing directors?” Again, unlikely. But did all three leave the meeting with an understanding that Mr. Perricelli would no longer serve in his capacity as director? Absolutely.

5 - 6

7

A person may allege that he or she was never validly appointed as a director, such as a case where a spouse is appointed without knowledge or consent and does not act as a director. Neither directors6 nor provisional directors7 may be found liable as a director where no consent to act as director has been given by the person. In Lau v. Her Majesty the Queen, 2003 G.T.C. 527, the Tax Court confirmed that an assessment based on records purporting to appoint a spouse who had not consented to act and had not acted would not be sustained: “To hold Agatha liable as a director when she was not one, in law or in fact, based on the slapdash work of the law firm, would be unconscionable.” In Danso-Coffey v. Her Majesty the Queen, in Right of Ontario, 2010 ONCA 171 a relative who had not consented to act as a director of her brother’s company but nonetheless took steps to file a notice of change sought and obtained a declaration in the Ontario Superior Court that she was not a director, which was upheld at the Ontario Court of Appeal:

36 I turn now to the application judge's declaration that Ms. Danso-Coffey was never a director. I would uphold that declaration. The Minister accepted that the RSTA is not relevant to the respondent's request for a declaration that she was never a director of the company. This position can only be based on an implicit acknowledgment that the Superior Court did have jurisdiction to make that declaration pursuant to s. 97 of the Courts of Justice Act and that the declaration is not “any matter arising under this Act” pursuant to s. 29.1(5) of the RSTA. At para. 56 of its factum, the Ministry states:

Ontario submits that if it is determined that a matter is outside of the RSTA regime, then none of the provisions of the statute, including s. 29.1, has any application, whether the provision is read retroactively or prospectively.

37 On the basis of the unchallenged evidence concerning the respondent's lack of involvement with the corporation and in the light of the position taken by the Minister, I see no reason to interfere with the application judge's declaration that the respondent was never a director of the company.

6 See, e.g. DeWitt v. Minister of National Revenue, [1990] 1 C.T.C. 2098. 7 See, e.g. Hay v. Her Majesty the Queen, 2004 TCC 51:

33 In my view, subsection 106(9) CBCA, like subsections 100(5) and (6) ABCA, does not apply to provisional directors because their appointment does not take place “at [a] meeting”. I believe that subsection 106(9) only envisages directors elected or appointed at such a meeting. The appointment of provisional directors results from the designation made by the incorporator in Form 6 when it is filed with the Director. No meeting is required in that process. Indeed, the CBCA contemplates that the first meeting will occur after the certificate of incorporation has been issued by the Director. Under subsection 106(2) CBCA, the provisional director “holds office from the issue of the certificate of incorporation until the first meeting of shareholders”. Directors can be elected at that meeting pursuant to subsection 106(3) CBCA or appointed at a meeting of directors pursuant to subsection 106(8) CBCA. 34 However, it cannot be inferred from the wording of subsection 106(9) CBCA that the legislator intended provisional directors to be appointed directors without their consent. In the common law, it has been recognized that a director must consent either explicitly or implicitly in order to be considered a director.

5 - 7

8

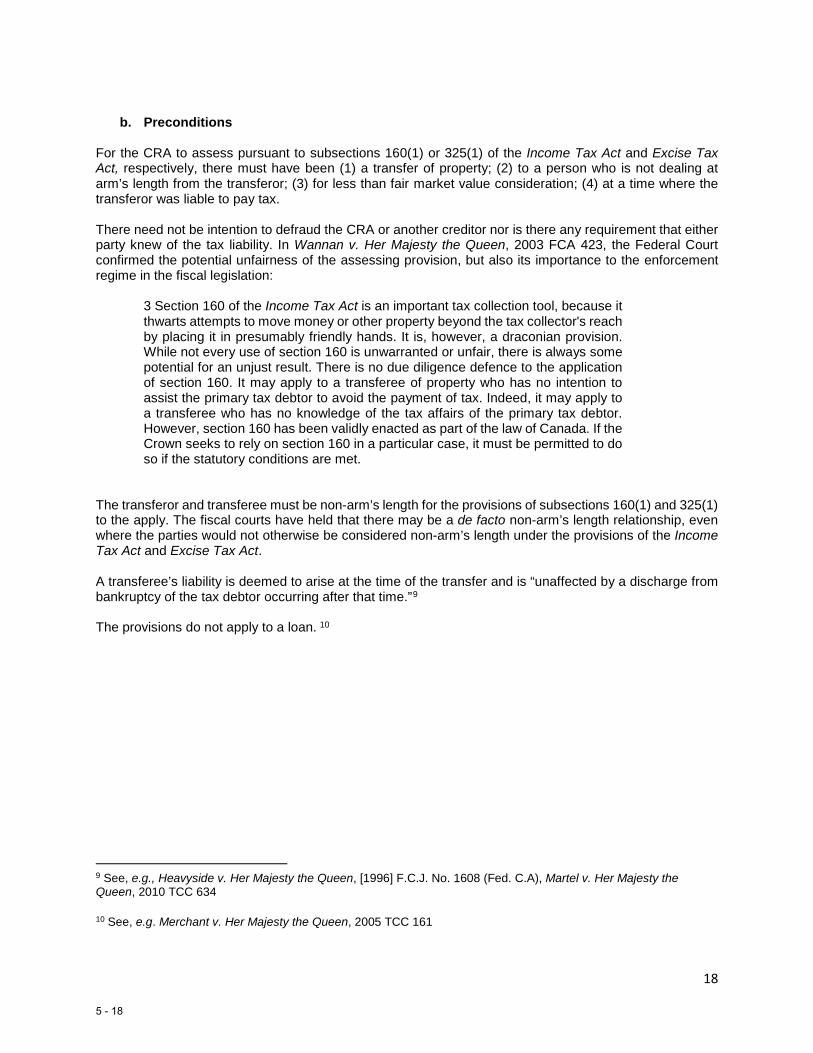

c. Preconditions

The CRA must meet the preconditions before raising a proper assessment of a director. Under the Excise Tax Act, no assessment can be raised unless, pursuant to subsection 323(2)

(a) a certificate for the amount of the corporation’s liability referred to in that subsection has been registered in the Federal Court under section 316 and execution for that amount has been returned unsatisfied in whole or in part;

(b) the corporation has commenced liquidation or dissolution proceedings or has been dissolved and a claim for the amount of the corporation’s liability referred to in subsection (1) has been proved within six months after the earlier of the date of commencement of the proceedings and the date of dissolution; or

(c) the corporation has made an assignment or a bankruptcy order has been made against it under the Bankruptcy and Insolvency Act and a claim for the amount of the corporation’s liability referred to in subsection (1) has been proved within six months after the date of the assignment or bankruptcy order.

Under the Income Tax Act, no assessment can be raised unless, pursuant to subsection 227.1(2):

(a) a certificate for the amount of the corporation's liability referred to in that subsection has been registered in the Federal Court under section 223 and execution for that amount has been returned unsatisfied in whole or in part;

(b) the corporation has commenced liquidation or dissolution proceedings or has been dissolved and a claim for the amount of the corporation's liability referred to in that subsection has been proved within six months after the earlier of the date of commencement of the proceedings and the date of dissolution; or (c) the corporation has made an assignment or a bankruptcy order has been made against it under the Bankruptcy and Insolvency Act and a claim for the amount of the corporation's liability referred to in that subsection has been proved within six months after the date of the assignment or bankruptcy order.

The Federal Court of Canada makes available to the public a list of proceedings, which include proceedings in which Excise Tax Act and Income Tax Act certificates are registered.8

8 As of the date of writing, the Proceedings Queries index can be accessed at http://cas-cdc-www02.cas-satj.gc.ca/IndexingQueries/infp_queries_e.php.

5 - 8

9

There is no precondition that the corporation be assessed for the liability before a director is. In Siow v. Her Majesty the Queen, 2011 TCC 301, the Tax Court confirmed that liability is not contingent on an assessment and that the legislation would be rendered meaningless to import a restriction not required by law:

40 The Respondent argues that the liability of a director does not flow from any underlying assessment but from the operation of the Act itself, namely section 323 which is reproduced again for convenience below. I must agree with the Respondent's submission.

323. (1) Liability of directors—If a corporation fails to remit an amount of net tax as required under subsection 228(2) or (2.3) or to pay an amount as required under section 230.1 that was paid to, or was applied to the liability of, the corporation as a net tax refund, the directors of the corporation at the time the corporation was required to remit or pay, as the case may be, the amount are jointly and severally, or solidarily, liable, together with the corporation, to pay the amount and any interest on, or penalties relating to, the amount. [Emphasis added]

41 The clear wording of the above provision crystallizes a director's liability to pay the net tax not remitted by the Corporation “at the time the corporation was required to remit or pay, as the case may be, the amount...”. 42 The provision makes no reference to any requirement for assessment or that the amount must be related to an assessed amount. The “amount” referenced is clearly the “amount of net tax as required under subsection 228(2)”, applicable here, which subsection requires a registrant to remit net tax. There is no ambiguity in the textual wording of subsection 323(1). 43 Moreover, I am in agreement with the Respondent that the same “amount” is referenced in paragraph 323(2) (a), requiring a certificate setting out the “amount” instead of an “assessed amount” for purposes of registering a certificate in Federal Court under section 316 and the requirement that an execution for “that amount” be returned unsatisfied in whole or in part; referenced also in subsection 323(6) which defines the amount recoverable from a director as the “amount” remaining unsatisfied after execution. 44 This interpretation is confirmed by subsection 299(2) of the Act which reads as follows: 299 (2) Liability not affected—Liability under this Part to pay or remit any

tax, penalty, interest or other amount is not affected by an incorrect or incomplete assessment or by the fact that no assessment has been made.

45 Clearly, the liability under this Part, (which includes all of Part IX of the Act under which all of the above provisions fall), to pay any tax or other amount is not affected by the fact no assessment has been made.

5 - 9

10

The Federal Court of Appeal in Barrett v. Her Majesty the Queen, 2012 FCA 33 held that the CRA need not even take reasonable steps to find assets of a corporate debtor prior to seeking enforcement:

24 The text of the Act only requires that the corporate liability be registered in the Federal Court under section 316 of the Act and that execution be returned unsatisfied. Nothing in the text of the provision imposes any requirement on the Minister to take reasonable steps to search for the assets of the corporate debtor prior to instructing the sheriff with respect to execution.

…

28 Nothing in the Federal Courts Act or Rules expressly imposes any obligation upon a judgment creditor to make reasonable efforts to search for assets of a judgment debtor before instructing a sheriff with respect to the collection of the debt. 29 The Federal Courts Rules as to writs of execution are complemented by the provincial laws of execution. Subsection 56(3) of the Federal Courts Act provides that writs of execution issued by the Federal Court bind property in the same manner as provincial writs, and are to be executed as nearly as possible in the same manner as similar writs issued by the superior court of the province in which the writ is to be executed. Rule 448 also requires a sheriff when seizing assets to follow the laws applicable to the execution of similar writs issued by a superior court of the province in which the property was seized.

30 In the present case, the Federal Court writ was to be executed in Ontario. Nothing in the Courts of Justice Act, R.S.O. 1990, c. C-43, the Execution Act, R.S.O. 1990, c. E-24 or the Rules of Civil Procedure of Ontario expressly requires a judgment creditor to make reasonable efforts to search for assets.

In Turner v. Her Majesty the Queen, 2006 TCC 130, the Court held that an “execution has been returned unsatisfied” means only compliance with the Federal Court Rules and need not include an endorsement of “nulla bona.” The Court rejected submissions made by an assessed director that there may have been receivables that could be collected by a Sheriff in satisfaction of a writ:

27 Counsel for the Appellant pointed out that, according to the evidence, Arden's financial difficulties of 1995, 1996 and 1997 were caused by its inability to collect receivables which included GST. Two arguments seem to be based on this. First that the uncollected GST might be set off against the GST debt. Second, the receivables might have been found and attached by execution. The first argument fails because the validity of the assessments underlying the amounts certified to the Federal Court was not put in issue. The second argument is untenable because there was no evidence that any of the receivables remained in existence in 2003 and, moreover, it is inconsistent with the admission that Arden had no assets.

5 - 10

11

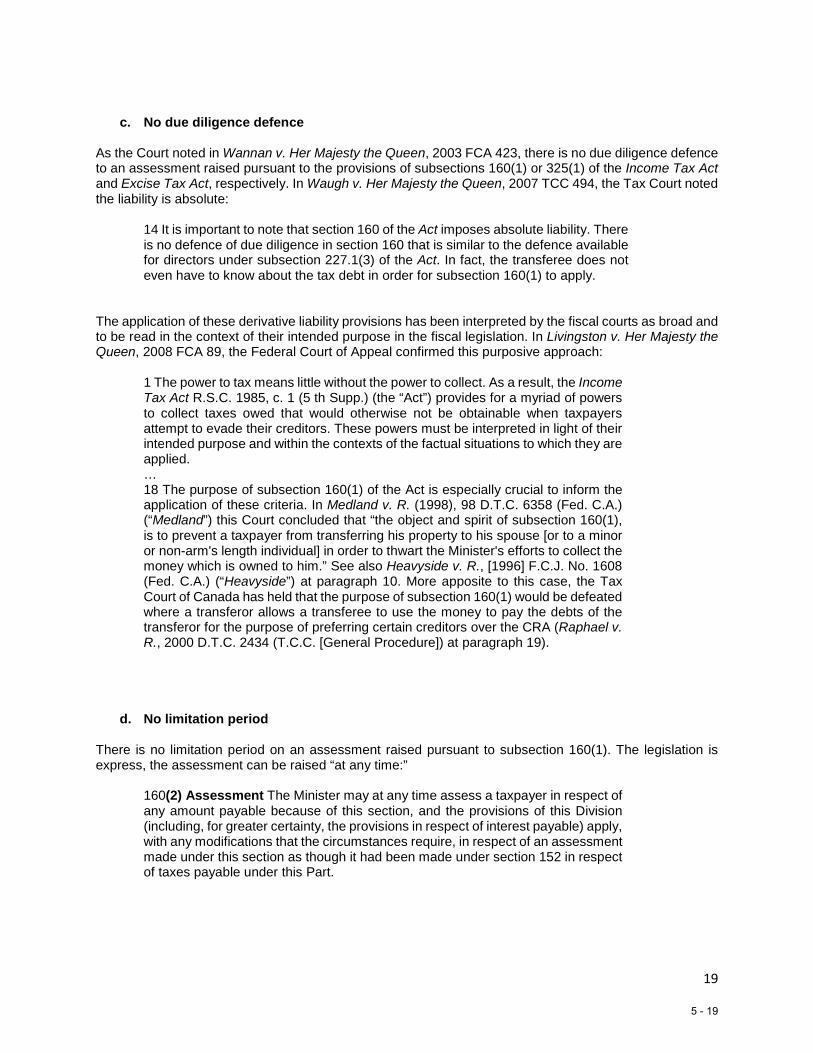

d. Due diligence defence Under each of the Income Tax Act and Excise Tax Act, a person may not be liable for the corporation’s debts if he or she was duly diligent in the performance of his or her duties as directors:

Income Tax Act, 227.1 (3) Idem [due diligence defence] A director is not liable for a failure under subsection (1) where the director exercised the degree of care, diligence and skill to prevent the failure that a reasonably prudent person would have exercised in comparable circumstances.

Excise Tax Act, 323(3) Diligence—A director of a corporation is not liable for a failure under subsection (1) where the director exercised the degree of care, diligence and skill to prevent the failure that a reasonably prudent person would have exercised in comparable circumstances.

The test is an objective test and the case authorities readily distinguishable on factual analyses. As the Court in Worrell v. Her Majesty the Queen, [2000] G.S.T.C. 91 noted, the desire to avoid mischief is clear, the application less so:

23 In the absence of a developed analytical framework, cases are readily distinguishable on their facts, even when those facts, including the facts in the instant appeal, conform to a recurring general pattern. Inevitably, but without express advertence, some decisions exhibit a relatively strict approach to subsection 227.1(3), while others, including the decision under appeal here, adopt a view more favourable to the director. 24 Nonetheless, amid this wilderness of single instances some general guidance on section 227.1 is available, most notably from this Court in Soper v. R. (1997), [1998] 1 F.C. 124 (Fed. C.A.). First, writing for the majority in Soper, supra, Robertson J.A. (at paragraph [11]) put subsection 227.1(3) into context by explaining its rationale:

Non-remittance of taxes withheld on behalf of a third party was likewise not uncommon during the recession. Faced with a choice between remitting such amounts to the Crown or drawing such amounts to pay key creditors whose goods or services were necessary to the continued operation of the business, corporate directors often followed the latter course. Such patent abuse and mismanagement on the part of directors constituted the “mischief” at which section 227.1 was directed....

5 - 11

12