Embed Size (px)

Citation preview

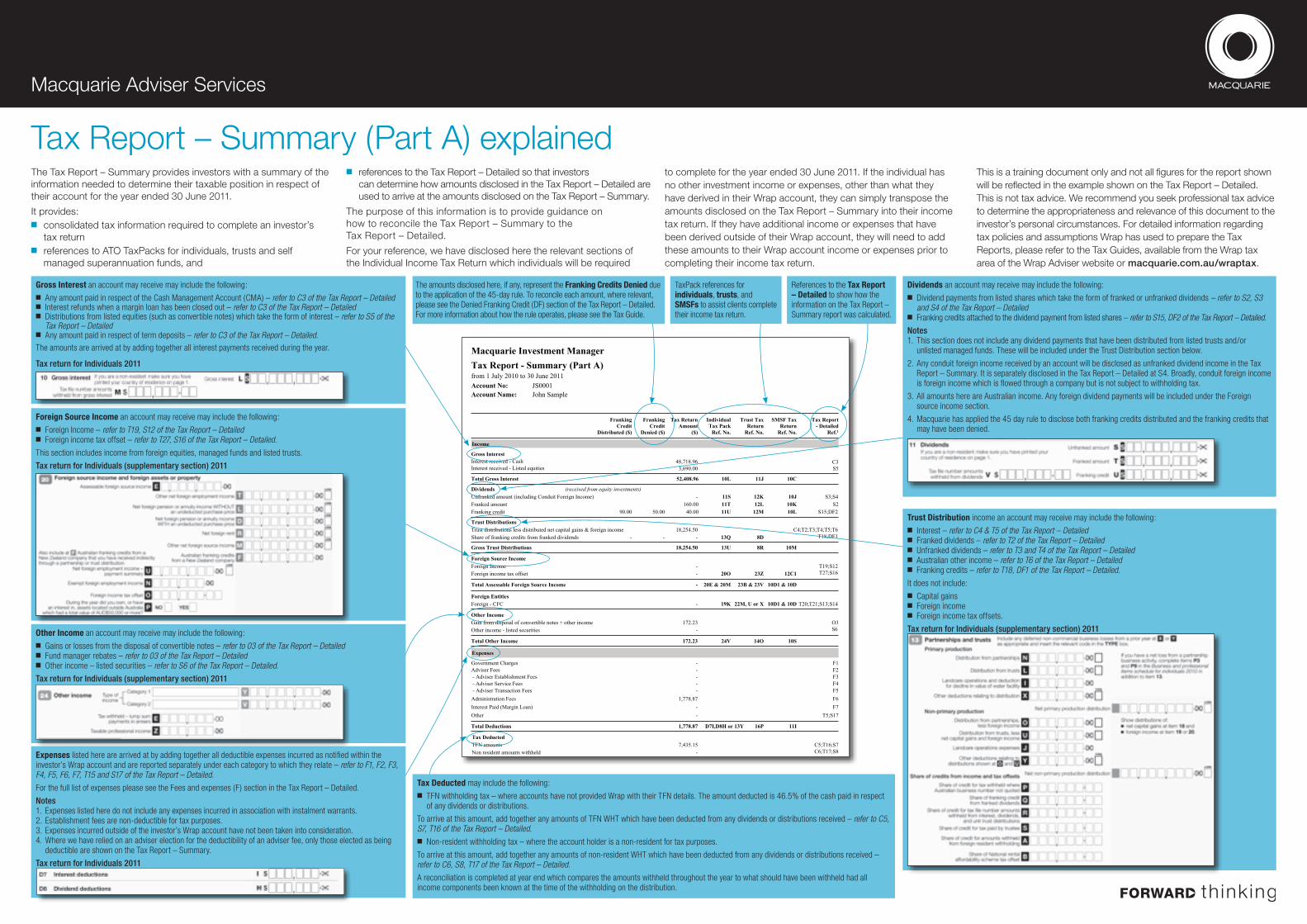

Tax Report – Summary (Part A) explainedThe Tax Report – Summary provides investors with a summary of the information needed to determine their taxable position in respect of their account for the year ended 30 June 2011.

It provides:■■ consolidated tax information required to complete an investor’s

tax return■■ references to ATO TaxPacks for individuals, trusts and self

managed superannuation funds, and

■■ references to the Tax Report – Detailed so that investors can determine how amounts disclosed in the Tax Report – Detailed are used to arrive at the amounts disclosed on the Tax Report – Summary.

The purpose of this information is to provide guidance on how to reconcile the Tax Report – Summary to the Tax Report – Detailed.

For your reference, we have disclosed here the relevant sections of the Individual Income Tax Return which individuals will be required

to complete for the year ended 30 June 2011. If the individual has no other investment income or expenses, other than what they have derived in their Wrap account, they can simply transpose the amounts disclosed on the Tax Report – Summary into their income tax return. If they have additional income or expenses that have been derived outside of their Wrap account, they will need to add these amounts to their Wrap account income or expenses prior to completing their income tax return.

This is a training document only and not all figures for the report shown will be reflected in the example shown on the Tax Report – Detailed. This is not tax advice. We recommend you seek professional tax advice to determine the appropriateness and relevance of this document to the investor’s personal circumstances. For detailed information regarding tax policies and assumptions Wrap has used to prepare the Tax Reports, please refer to the Tax Guides, available from the Wrap tax area of the Wrap Adviser website or macquarie.com.au/wraptax.

Macquarie Adviser Services

Macquarie Investment Manager

John Sample

Tax Report - Summary (Part A)

JS0001Account Name:Account No:from 1 July 2010 to 30 June 2011

Trust distributions less distributed net capital gains & foreign income

Income

FrankingCredit

Distributed ($)

FrankingCredit

Denied ($)

Tax ReturnAmount

($)

IndividualTax Pack

Ref. No.

Trust TaxReturn

Ref. No.

SMSF TaxReturn

Ref. No.

Tax Report- Detailed

Ref.1

Gross InterestInterest received - CashInterest received - Listed equities

Total Gross Interest 10L 11J 10C

C3S5

48,718.963,690.00

Unfranked amount (including Conduit Foreign Income)Franked amountFranking credit

11S 12K 10J11T 12L 10K11U 12M 10L

S3;S4S2

S15;DF2

T20;T21;S13;S14

-160.0040.0050.0090.00

(received from equity investments)Dividends

Share of franking credits from franked dividends

Gross Trust Distributions

13Q 8D

10M

C4;T2;T3;T4;T5;T6T18;DF1

T19;S12T27;S16

18,254.50- - -

Trust Distributions

18,254.50

Foreign Source IncomeForeign Income

Foreign - CFC

Foreign income tax offset

Total Assessable Foreign Source Income 20E & 20M 23B & 23V 10D1 & 10D

12C123Z20O-

-

-

-

Other Income

Other income - listed securities

Total Other Income 10S14O24V

O3S6

32.271emocni rehto + seton elbitrevnoc fo lasopsid morf niaG-

172.23

TFN amountsNon resident amounts withheld

7,435.15-

C5;T16;S7C6;T17;S8

1Refer to the Tax Report - Detailed provided with this Tax Report - Summary for details at a security level.

Where we have been advised that your adviser fees are deductible, we have relied on these instructions and have not considered whether the treatment is correct. Theinvestor should seek independent taxation advice to determine the deductibility or otherwise of these fees.

Expenses

Government Charges F1-Adviser Fees F2- - Adviser Establishment Fees F3- - Adviser Service Fees F4- - Adviser Transaction Fees F5-Administration Fees F61,778.87Interest Paid (Margin Loan) F7

T5;S17-

Other -

78.877,1snoitcudeD latoT D7I,D8H or 13Y 16P 11I

52,408.96

Total unallocated fees per Tax Report - Detailed (F section) are $18,756.47. The investor should seek independent taxation advice to determine thedeductibility or otherwise of these fees.

13U 8R

Tax Deducted

Foreign Entities10D1 & 10D19K 22M, U or X

1 2ofAccount: HH0435

Tax Deducted may include the following:■■ TFN withholding tax – where accounts have not provided Wrap with their TFN details. The amount deducted is 46.5% of the cash paid in respect

of any dividends or distributions.

To arrive at this amount, add together any amounts of TFN WHT which have been deducted from any dividends or distributions received – refer to C5, S7, T16 of the Tax Report – Detailed.■■ Non-resident withholding tax – where the account holder is a non-resident for tax purposes.

To arrive at this amount, add together any amounts of non-resident WHT which have been deducted from any dividends or distributions received – refer to C6, S8, T17 of the Tax Report – Detailed.

A reconciliation is completed at year end which compares the amounts withheld throughout the year to what should have been withheld had all income components been known at the time of the withholding on the distribution.

Gross Interest an account may receive may include the following:■■ Any amount paid in respect of the Cash Management Account (CMA) – refer to C3 of the Tax Report – Detailed■■ Interest refunds when a margin loan has been closed out – refer to C3 of the Tax Report – Detailed■■ Distributions from listed equities (such as convertible notes) which take the form of interest – refer to S5 of the

Tax Report – Detailed■■ Any amount paid in respect of term deposits – refer to C3 of the Tax Report – Detailed.

The amounts are arrived at by adding together all interest payments received during the year.

Tax return for Individuals 2011

The amounts disclosed here, if any, represent the Franking Credits Denied due to the application of the 45-day rule. To reconcile each amount, where relevant, please see the Denied Franking Credit (DF) section of the Tax Report – Detailed. For more information about how the rule operates, please see the Tax Guide.

TaxPack references for individuals, trusts, and SMSFs to assist clients complete their income tax return.

References to the Tax Report – Detailed to show how the information on the Tax Report – Summary report was calculated.

Trust Distribution income an account may receive may include the following:■■ Interest – refer to C4 & T5 of the Tax Report – Detailed■■ Franked dividends – refer to T2 of the Tax Report – Detailed ■■ Unfranked dividends – refer to T3 and T4 of the Tax Report – Detailed ■■ Australian other income – refer to T6 of the Tax Report – Detailed ■■ Franking credits – refer to T18, DF1 of the Tax Report – Detailed.

It does not include:■■ Capital gains■■ Foreign income■■ Foreign income tax offsets.

Tax return for Individuals (supplementary section) 2011

Dividends an account may receive may include the following:■■ Dividend payments from listed shares which take the form of franked or unfranked dividends – refer to S2, S3

and S4 of the Tax Report – Detailed■■ Franking credits attached to the dividend payment from listed shares – refer to S15, DF2 of the Tax Report – Detailed.

Notes1. This section does not include any dividend payments that have been distributed from listed trusts and/or

unlisted managed funds. These will be included under the Trust Distribution section below.

2. Any conduit foreign income received by an account will be disclosed as unfranked dividend income in the Tax Report – Summary. It is separately disclosed in the Tax Report – Detailed at S4. Broadly, conduit foreign income is foreign income which is flowed through a company but is not subject to withholding tax.

3. All amounts here are Australian income. Any foreign dividend payments will be included under the Foreign source income section.

4. Macquarie has applied the 45 day rule to disclose both franking credits distributed and the franking credits that may have been denied.

Tax return for Individuals 2011

Expenses listed here are arrived at by adding together all deductible expenses incurred as notified within the investor’s Wrap account and are reported separately under each category to which they relate – refer to F1, F2, F3, F4, F5, F6, F7, T15 and S17 of the Tax Report – Detailed.

For the full list of expenses please see the Fees and expenses (F) section in the Tax Report – Detailed.

Notes1. Expenses listed here do not include any expenses incurred in association with instalment warrants.2. Establishment fees are non-deductible for tax purposes.3. Expenses incurred outside of the investor’s Wrap account have not been taken into consideration.4. Where we have relied on an adviser election for the deductibility of an adviser fee, only those elected as being

deductible are shown on the Tax Report – Summary.

Tax return for Individuals 2011

Foreign Source Income an account may receive may include the following:■■ Foreign Income – refer to T19, S12 of the Tax Report – Detailed ■■ Foreign income tax offset – refer to T27, S16 of the Tax Report – Detailed.

This section includes income from foreign equities, managed funds and listed trusts.

Tax return for Individuals (supplementary section) 2011

Other Income an account may receive may include the following:■■ Gains or losses from the disposal of convertible notes – refer to 03 of the Tax Report – Detailed■■ Fund manager rebates – refer to 03 of the Tax Report – Detailed■■ Other income – listed securities – refer to S6 of the Tax Report – Detailed.

Tax return for Individuals (supplementary section) 2011

Freecall 1800 025 063

Fax Gateway 1800 025 175 Corporate Actions Fax Gateway 1800 281 476

Macquarie Wrap Solutions PO Box N498 Grosvenor Place NSW 1220

macquarie.com.au/wraptaxOTH7

211a

07/

11

This information is intended for the use of licensed financial advisers. It is general in nature and doesn’t take into account any individuals personal circumstances, financial needs or objectives, and we strongly recommend that individuals consult with their financial adviser and read the relevant Product Disclosure Statement before making a decision about a financial product or class of financial products. The information in this document is dated 30 June 2011 and is issued by Macquarie Investment Management Limited ABN 66 002 867 003 AFSL 237 492 RSEL L0001281 (MIML). This information is not to be treated as financial product advice, tax or legal advice.We have used all reasonable care in preparing this information, and we believe it is accurate at its date of publication. However we do not accept responsibility for any of the information in this application/document. Where information has been provided by third parties, we do not accept responsibility for errors or omissions by those third parties. This information is subject to change.MIML is not an authorised deposit taking institution for the purposes of the Banking Act (Cth) 1959, and other than as expressly set out in the applicable PDS or other offer document, MIML’s obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542. Macquarie Bank Limited does not guarantee or otherwise provide assurance in respect of the obligations of MIML.

Macquarie Adviser Services

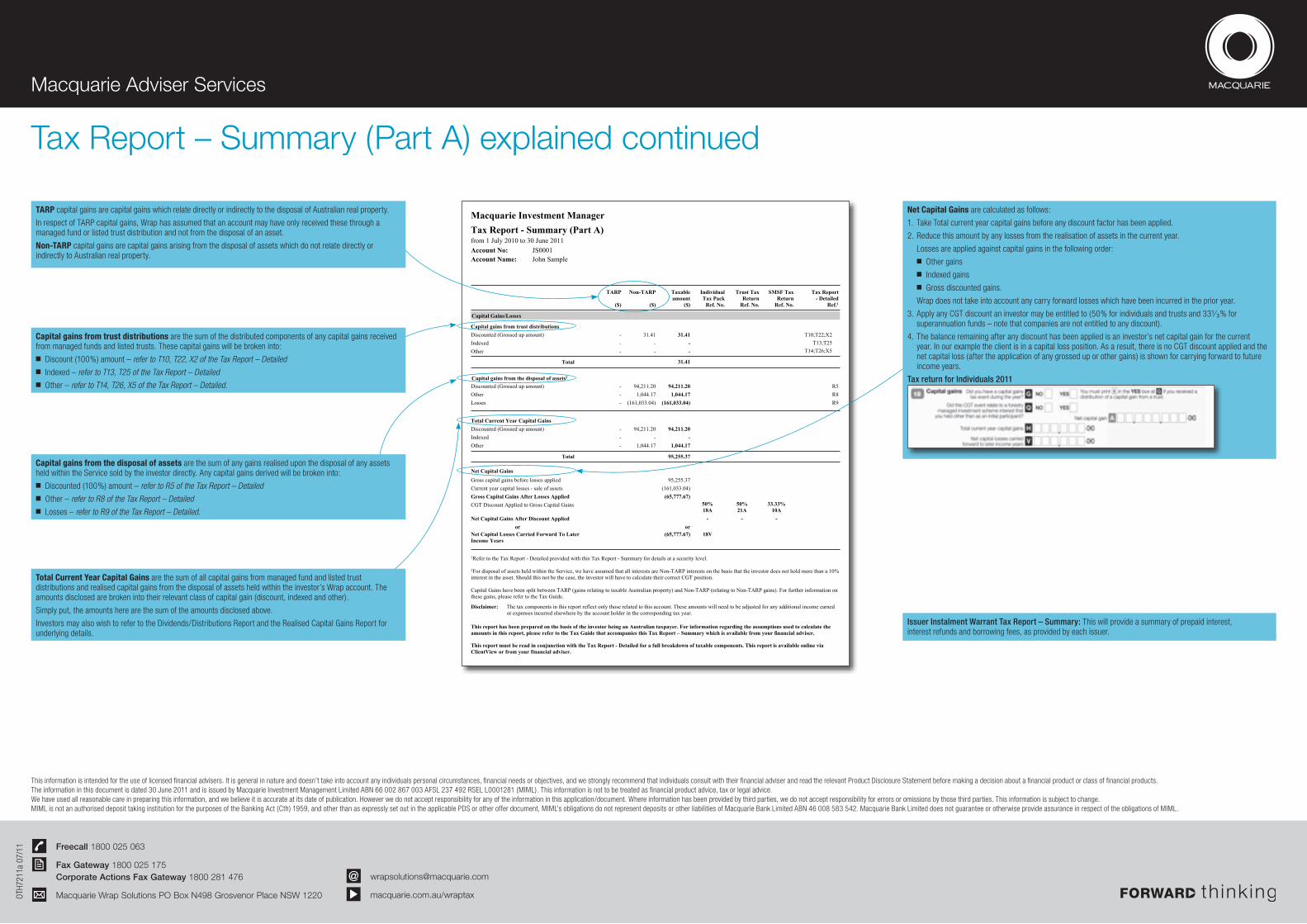

Issuer Instalment Warrant Tax Report – Summary: This will provide a summary of prepaid interest, interest refunds and borrowing fees, as provided by each issuer.

Tax Report – Summary (Part A) explained continued

Macquarie Investment Manager

John Sample

Tax Report - Summary (Part A)

JS0001Account Name:Account No:from 1 July 2010 to 30 June 2011

Capital Gains/Losses

TARP

($)

Non-TARP

($)

Taxableamount

($)

IndividualTax Pack

Ref. No.

Trust TaxReturn

Ref. No.

SMSF TaxReturn

Ref. No.

Capital gains from trust distributions31.41)tnuoma pu dessorG( detnuocsiD - 31.41

--dexednI --rehtO -

Total

-

)tnuoma pu dessorG( detnuocsiDOtherLosses

Capital gains from the disposal of assets2

R9

R5

T10;T22;X2T13;T25

T14;T26;X5

R81,044.17(161,033.04)

IndexedOther

Total

Total Current Year Capital GainsDiscounted (Grossed up amount) 94,211.20- 94,211.20

- - -1,044.17- 1,044.17

95,255.37

Net Capital GainsGross capital gains before losses appliedCurrent year capital losses - sale of assetsGross Capital Gains After Losses AppliedCGT Discount Applied to Gross Capital Gains

Net Capital Gains After Discount Applied

Net Capital Losses Carried Forward To LaterIncome Years

or

(161,033.04)

50%18A

50%21A

33.33%10A

or18V

95,255.37

(65,777.67)

- - -

(65,777.67)

Tax Report- Detailed

Ref.1

94,211.2094,211.201,044.17

(161,033.04)

---

31.41

1Refer to the Tax Report - Detailed provided with this Tax Report - Summary for details at a security level.

2For disposal of assets held within the Service, we have assumed that all interests are Non-TARP interests on the basis that the investor does not hold more than a 10%interest in the asset. Should this not be the case, the investor will have to calculate their correct CGT position.

Capital Gains have been split between TARP (gains relating to taxable Australian property) and Non-TARP (relating to Non-TARP gains). For further information onthese gains, please refer to the Tax Guide.

Disclaimer: The tax components in this report reflect only those related to this account. These amounts will need to be adjusted for any additional income earnedor expenses incurred elsewhere by the account holder in the corresponding tax year.

This report has been prepared on the basis of the investor being an Australian taxpayer. For information regarding the assumptions used to calculate theamounts in this report, please refer to the Tax Guide that accompanies this Tax Report – Summary which is available from your financial adviser.

This report must be read in conjunction with the Tax Report - Detailed for a full breakdown of taxable components. This report is available online viaClientView or from your financial adviser.

17-Jun-11 05:18PMAccount: HH0435 2 2of

Net Capital Gains are calculated as follows:

1. Take Total current year capital gains before any discount factor has been applied.

2. Reduce this amount by any losses from the realisation of assets in the current year.

Losses are applied against capital gains in the following order:■■ Other gains■■ Indexed gains■■ Gross discounted gains.

Wrap does not take into account any carry forward losses which have been incurred in the prior year.

3. Apply any CGT discount an investor may be entitled to (50% for individuals and trusts and 33¹⁄ ³% for superannuation funds – note that companies are not entitled to any discount).

4. The balance remaining after any discount has been applied is an investor’s net capital gain for the current year. In our example the client is in a capital loss position. As a result, there is no CGT discount applied and the net capital loss (after the application of any grossed up or other gains) is shown for carrying forward to future income years.

Tax return for Individuals 2011

Total Current Year Capital Gains are the sum of all capital gains from managed fund and listed trust distributions and realised capital gains from the disposal of assets held within the investor’s Wrap account. The amounts disclosed are broken into their relevant class of capital gain (discount, indexed and other).

Simply put, the amounts here are the sum of the amounts disclosed above.

Investors may also wish to refer to the Dividends/Distributions Report and the Realised Capital Gains Report for underlying details.

TARP capital gains are capital gains which relate directly or indirectly to the disposal of Australian real property.

In respect of TARP capital gains, Wrap has assumed that an account may have only received these through a managed fund or listed trust distribution and not from the disposal of an asset.

Non-TARP capital gains are capital gains arising from the disposal of assets which do not relate directly or indirectly to Australian real property.

Capital gains from trust distributions are the sum of the distributed components of any capital gains received from managed funds and listed trusts. These capital gains will be broken into:■■ Discount (100%) amount – refer to T10, T22, X2 of the Tax Report – Detailed■■ Indexed – refer to T13, T25 of the Tax Report – Detailed■■ Other – refer to T14, T26, X5 of the Tax Report – Detailed.

Capital gains from the disposal of assets are the sum of any gains realised upon the disposal of any assets held within the Service sold by the investor directly. Any capital gains derived will be broken into:■■ Discounted (100%) amount – refer to R5 of the Tax Report – Detailed ■■ Other – refer to R8 of the Tax Report – Detailed ■■ Losses – refer to R9 of the Tax Report – Detailed.

Macquarie Adviser Services

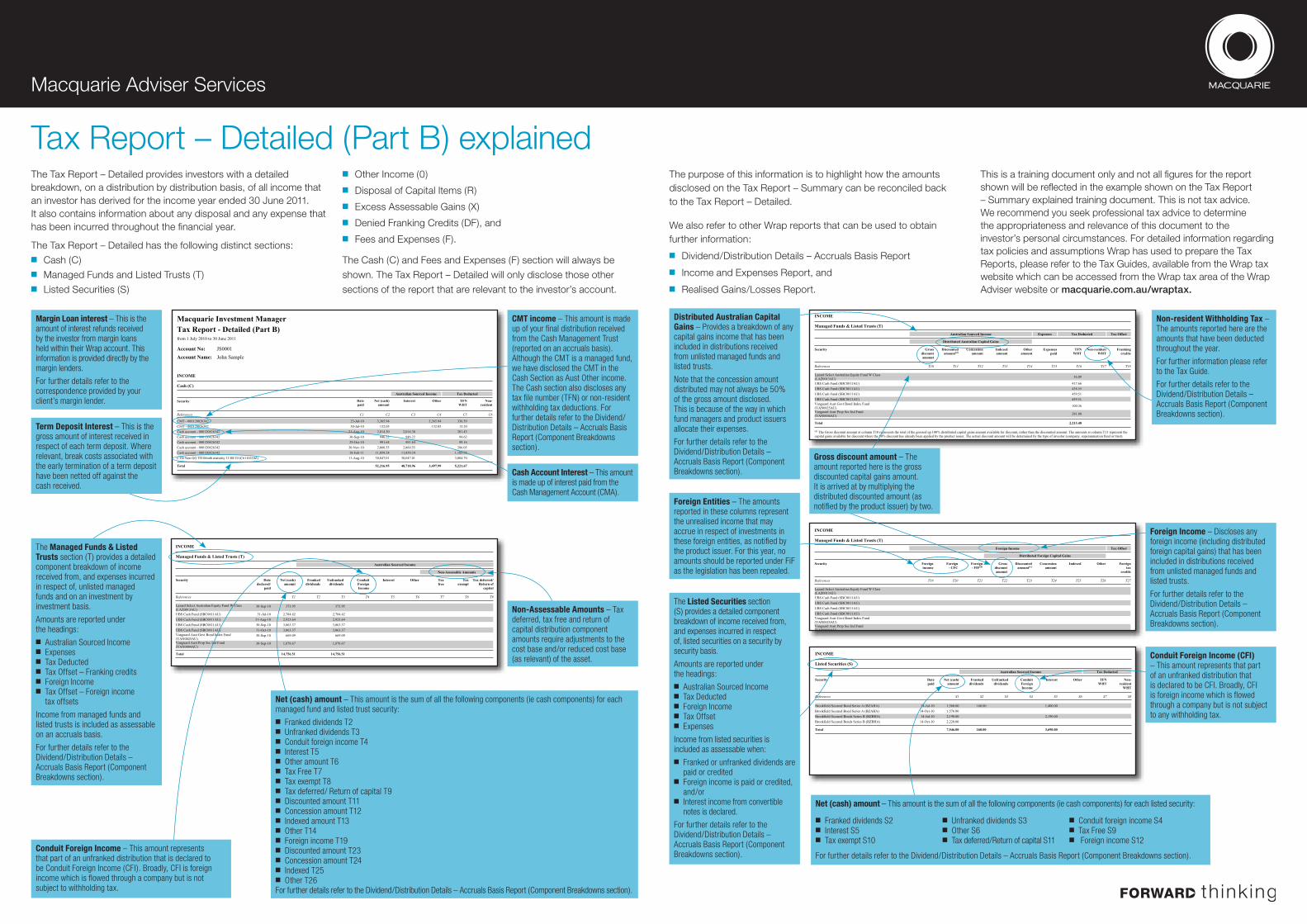

Tax Report – Detailed (Part B) explainedThe Tax Report – Detailed provides investors with a detailed breakdown, on a distribution by distribution basis, of all income that an investor has derived for the income year ended 30 June 2011. It also contains information about any disposal and any expense that has been incurred throughout the financial year.

The Tax Report – Detailed has the following distinct sections:■■ Cash (C)■■ Managed Funds and Listed Trusts (T)■■ Listed Securities (S)

■■ Other Income (0)

■■ Disposal of Capital Items (R)

■■ Excess Assessable Gains (X)

■■ Denied Franking Credits (DF), and

■■ Fees and Expenses (F).

The Cash (C) and Fees and Expenses (F) section will always be

shown. The Tax Report – Detailed will only disclose those other

sections of the report that are relevant to the investor’s account.

INCOME

Australian Sourced Income

Distributed Australian Capital Gains

Tax OffsetTax DeductedExpenses

Managed Funds & Listed Trusts (T)

Security

T11 T12 T13 T14 T15 T16 T17 T18

Concessionamount

Indexedamount

Otheramount

TFNWHT

Non-residentWHT

Frankingcredits

Grossdiscountamount

T10

Expensespaid

References

Discountedamount(a)

Lazard Select Australian Equity Fund W Class(LAZ0013AU) 56.09

UBS Cash Fund (SBC0811AU) 417.66UBS Cash Fund (SBC0811AU) 438.55UBS Cash Fund (SBC0811AU) 459.51UBS Cash Fund (SBC0811AU) 459.51Vanguard Aust Govt Bond Index Fund(VAN0025AU) 100.36

Vanguard Aust Prop Sec Ind Fund(VAN0004AU) 281.80

Total 2,213.48

(a) The Gross discount amount at column T10 represents the total of the grossed up 100% distributed capital gains amount available for discount, rather than the discounted amount. The amounts at column T11 represent thecapital gains available for discount where the 50% discount has already been applied by the product issuer. The actual discount amount will be determined by the type of investor (company, superannuation fund or trust).

3 9ofAccount: HH0435

INCOME

Managed Funds & Listed Trusts (T)

Australian Sourced Income

Non-Assessable Amounts

Security Interest Other

T1 T2 T3 T5 T6 T7 T8

Datedeclared/

paid

Net (cash)amount

Frankeddividends

Unfrankeddividends

Taxfree

Taxexempt

References

Tax deferred/Return of

capital

T9

ConduitForeignIncome

T4

Lazard Select Australian Equity Fund W Class(LAZ0013AU)

30-Sep-10 373.95 373.95

UBS Cash Fund (SBC0811AU) 31-Jul-10 2,784.42 2,784.42UBS Cash Fund (SBC0811AU) 31-Aug-10 2,923.64 2,923.64UBS Cash Fund (SBC0811AU) 30-Sep-10 3,063.37 3,063.37UBS Cash Fund (SBC0811AU) 31-Oct-10 3,063.37 3,063.37Vanguard Aust Govt Bond Index Fund(VAN0025AU)

30-Sep-10 669.09 669.09

Vanguard Aust Prop Sec Ind Fund(VAN0004AU)

30-Sep-10 1,878.67 1,878.67

14,756.51 14,756.51Total

2 9ofAccount: HH0435

Macquarie Investment Manager

from 1 July 2010 to 30 June 2011

John Sample

Tax Report - Detailed (Part B)

JS0001 Account No:Account Name:

INCOME

Australian Sourced Income Tax Deducted

Cash (C)

Security Interest Other

References C1 C2 C3 C4 C5 C6

Datepaid

Net (cash)amount

Non-resident

TFNWHT

CMT - 000120826342 95.63349.563,349.563,301-luJ-32CMT - 000120826342 02.3150.23150.23101-luJ-03Cash account - 000120826342 34.10203.410,203.410,201-guA-13Cash account - 000120826342 26.4922.64922.64901-peS-03Cash account - 000120826342 61.9946.19946.19901-tcO-92Cash account - 000120826342 50.68255.068,255.068,201-voN-03Cash account - 000120826342 29.581,142.958,1142.958,1111-beF-81

07.400,310.740,0310.740,0301-guA-11)Z0120116C( 01/80/11 ytirutam htm60 DT GG noN DTC

52,216.95Total 48,718.96 3,497.99 5,221.67

1 9ofAccount: HH0435

CMT income – This amount is made up of your final distribution received from the Cash Management Trust (reported on an accruals basis). Although the CMT is a managed fund, we have disclosed the CMT in the Cash Section as Aust Other income. The Cash section also discloses any tax file number (TFN) or non-resident withholding tax deductions. For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

The Managed Funds & Listed Trusts section (T) provides a detailed component breakdown of income received from, and expenses incurred in respect of, unlisted managed funds and on an investment by investment basis.

Amounts are reported under the headings: ■■ Australian Sourced Income ■■ Expenses■■ Tax Deducted ■■ Tax Offset – Franking credits■■ Foreign Income ■■ Tax Offset – Foreign income

tax offsets

Income from managed funds and listed trusts is included as assessable on an accruals basis.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Non-Assessable Amounts – Tax deferred, tax free and return of capital distribution component amounts require adjustments to the cost base and/or reduced cost base (as relevant) of the asset.

Net (cash) amount – This amount is the sum of all the following components (ie cash components) for each managed fund and listed trust security:■■ Franked dividends T2■■ Unfranked dividends T3■■ Conduit foreign income T4■■ Interest T5■■ Other amount T6■■ Tax Free T7■■ Tax exempt T8■■ Tax deferred/ Return of capital T9■■ Discounted amount T11■■ Concession amount T12■■ Indexed amount T13■■ Other T14■■ Foreign income T19■■ Discounted amount T23■■ Concession amount T24■■ Indexed T25■■ Other T26

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Distributed Australian Capital Gains – Provides a breakdown of any capital gains income that has been included in distributions received from unlisted managed funds and listed trusts.

Note that the concession amount distributed may not always be 50% of the gross amount disclosed. This is because of the way in which fund managers and product issuers allocate their expenses.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Non-resident Withholding Tax – The amounts reported here are the amounts that have been deducted throughout the year.

For further information please refer to the Tax Guide.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Conduit Foreign Income – This amount represents that part of an unfranked distribution that is declared to be Conduit Foreign Income (CFI). Broadly, CFI is foreign income which is flowed through a company but is not subject to withholding tax.

INCOME

Foreign Income

Distributed Foreign Capital Gains

Tax Offset

Managed Funds & Listed Trusts (T)

Security

T19 T20 T21 T22 T23 T24 T25 T26

Foreigntax

credits

OtherIndexedConcessionamount

Discountedamount(c)

Foreign- FIF(d)

Foreign- CFC

Foreignincome

Grossdiscountamount

T27References

Lazard Select Australian Equity Fund W Class(LAZ0013AU)UBS Cash Fund (SBC0811AU)UBS Cash Fund (SBC0811AU)UBS Cash Fund (SBC0811AU)UBS Cash Fund (SBC0811AU)Vanguard Aust Govt Bond Index Fund(VAN0025AU)Vanguard Aust Prop Sec Ind Fund(VAN0004AU)

Total

(c) The Gross discount amount at column T22 represents the total of the grossed up 100% distributed capital gains amount available for discount, rather than the discounted amount. The amounts at column T23 represent thecapital gains available for discount where the 50% discount has already been applied by the product issuer. The actual discount amount will be determined by the type of investor (company, superannuation fund or trust).

(d) Please note that for the 2010/2011 tax year, there is currently no enacted legislation regarding FIF income. We expect that for the 2011/2012 income year, the Foreign Accumulation Fund legislation will apply and will beenacted. Macquarie has left this FIF section in the 2010/2011 tax report but we expect this to be blank for the current year. If you have any questions regarding how this legislative change may impact you, we recommend youseek independent taxation advice.

4 9ofAccount: HH0435

Foreign Income – Discloses any foreign income (including distributed foreign capital gains) that has been included in distributions received from unlisted managed funds and listed trusts.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

INCOME

Listed Securities (S)

etaDytiruceSpaid

Net (cash)amount

Frankeddividends

Unfrankeddividends

InterestConduitForeignIncome

Other TFNWHT

Non-resident

WHT

References S1 S2 S3 S4 S5 S6 S7 S8

Australian Sourced Income Tax Deducted

00.004,100.065,101-luJ-41)AHAZB( A seireS dnoB deruceS dleifkoorB00.675,101-tcO-41)AHAZB( A seireS dnoB deruceS dleifkoorB

00.091,200.091,201-luJ-41)AHBZB( B seireS sdnoB deruceS dleifkoorB00.022,201-tcO-41)AHBZB( B seireS sdnoB deruceS dleifkoorB

Total 00.096,300.645 00.061

00.061

,7

5 9ofAccount: HH0435

Net (cash) amount – This amount is the sum of all the following components (ie cash components) for each listed security:

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Foreign Entities – The amounts reported in these columns represent the unrealised income that may accrue in respect of investments in these foreign entities, as notified by the product issuer. For this year, no amounts should be reported under FiF as the legislation has been repealed.

Conduit Foreign Income (CFI) – This amount represents that part of an unfranked distribution that is declared to be CFI. Broadly, CFI is foreign income which is flowed through a company but is not subject to any withholding tax.

The Listed Securities section (S) provides a detailed component breakdown of income received from, and expenses incurred in respect of, listed securities on a security by security basis.

Amounts are reported under the headings:■■ Australian Sourced Income ■■ Tax Deducted■■ Foreign Income■■ Tax Offset■■ Expenses

Income from listed securities is included as assessable when: ■■ Franked or unfranked dividends are

paid or credited■■ Foreign income is paid or credited,

and/or ■■ Interest income from convertible

notes is declared.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Margin Loan interest – This is the amount of interest refunds received by the investor from margin loans held within their Wrap account. This information is provided directly by the margin lenders.

For further details refer to the correspondence provided by your client’s margin lender.

■■ Franked dividends S2■■ Interest S5 ■■ Tax exempt S10

■■ Unfranked dividends S3■■ Other S6 ■■ Tax deferred/Return of capital S11

■■ Conduit foreign income S4■■ Tax Free S9■■ Foreign income S12

Gross discount amount – The amount reported here is the gross discounted capital gains amount. It is arrived at by multiplying the distributed discounted amount (as notified by the product issuer) by two.

Term Deposit Interest – This is the gross amount of interest received in respect of each term deposit. Where relevant, break costs associated with the early termination of a term deposit have been netted off against the cash received.

The purpose of this information is to highlight how the amounts disclosed on the Tax Report – Summary can be reconciled back to the Tax Report – Detailed.

We also refer to other Wrap reports that can be used to obtain further information:

■■ Dividend/Distribution Details – Accruals Basis Report

■■ Income and Expenses Report, and

■■ Realised Gains/Losses Report.

This is a training document only and not all figures for the report shown will be reflected in the example shown on the Tax Report – Summary explained training document. This is not tax advice. We recommend you seek professional tax advice to determine the appropriateness and relevance of this document to the investor’s personal circumstances. For detailed information regarding tax policies and assumptions Wrap has used to prepare the Tax Reports, please refer to the Tax Guides, available from the Wrap tax website which can be accessed from the Wrap tax area of the Wrap Adviser website or macquarie.com.au/wraptax.

Cash Account Interest – This amount is made up of interest paid from the Cash Management Account (CMA).

OTH7

211b

07/

11

This information is intended for the use of licensed financial advisers. It is general in nature and doesn’t take into account any individuals personal circumstances, financial needs or objectives, and we strongly recommend that individuals consult with their financial adviser and read the relevant Product Disclosure Statement before making a decision about a financial product or class of financial products. The information in this document is dated 30 June 2011 and is issued by Macquarie Investment Management Limited ABN 66 002 867 003 AFSL 237 492 RSEL L0001281 (MIML). This information is not to be treated as financial product advice, tax or legal advice.We have used all reasonable care in preparing this information, and we believe it is accurate at its date of publication. However we do not accept responsibility for any of the information in this application/document. Where information has been provided by third parties, we do not accept responsibility for errors or omissions by those third parties. This information is subject to change.MIML is not an authorised deposit taking institution for the purposes of the Banking Act (Cth) 1959, and other than as expressly set out in the applicable PDS or other offer document, MIML’s obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542. Macquarie Bank Limited does not guarantee or otherwise provide assurance in respect of the obligations of MIML.

OTHER INCOME (O)

UnitsSecurity Netproceeds

Assessableincome/loss

Purchasecost

Sale date/maturity

Purchasedate

O1 O2 O3

Event

References

Fund Manager Rebate 172.23

Total 172.23

8 9ofAccount: HH0435

DISPOSAL OF CAPITAL ITEMS - COST BASE/PROCEEDS INFORMATION (R)

UnitsSecurity Capitallosses

Net saleproceeds

Indexedadjusted

cost

Adjustedcostbase

Saledate

Purchasedate

R1 R2 R3 R9

Discounted331/3%(b)

Discounted50%(a)

R6 R7References

Proceedsless cost

R4

Other

R8

Grossdiscountamount

R5

9,673 01-Sep-03 22-Nov-10 129,248.88 0.00 190,937.57 0.0030,844.35 41,125.79 00.096.886,1696.886,16

....... ....... ....... ....... ....... ....... ....... ....... ....... ....... ....... .......

Dimensional Australian Value Trust(DFA0101AU)......

132,481 02-Oct-09 22-Nov-10 82,782.85 0.00 77,793.02 (4,989.83)0.00 0.00 00.000.0)38.989,4(Vanguard Aust Prop Sec Ind Fund(VAN0004AU)

Total 2,380,614.52 (161,033.04)47,089.91 62,786.53 1,044.1794,179.79(65,809.08)

(a)This amount represents the taxable capital gains after a 50% discount has been applied.

(b)This amount represents the taxable capital gains after a 331/3% discount has been applied. The number included is the 662/3% amount.

0.002,446,423.60

7 9ofAccount: HH0435

INCOME

Listed Securities (S)

Foreign Income Tax Offset

Security

51S31S21S

Foreigntax

credits

Foreign- CFC

Foreignincome

S16

Frankingcredits

References

Non-Assessable Amounts

Taxfree

Taxexempt

Tax deferred/Return of

capital

S9 S10 S11

Foreign- FIF(b)

S14

Expenses

Expensespaid

S17

Brookfield Secured Bond Series A (BZAHA)Brookfield Secured Bond Series A (BZAHA)Brookfield Secured Bonds Series B (BZBHA)Brookfield Secured Bonds Series B (BZBHA)

Total

(b) Please note that for the 2010/2011 tax year, there is currently no enacted legislation regarding FIF income. We expect that for the 2011/2012 income year, the Foreign Accumulation Fund legislation will apply and will beenacted. Macquarie has left this FIF section in the 2010/2011 tax report but we expect this to be blank for the current year. If you have any questions regarding how this legislative change may impact you, we recommend youseek independent taxation advice.

6 9ofAccount: HH0435

90.00

90.00

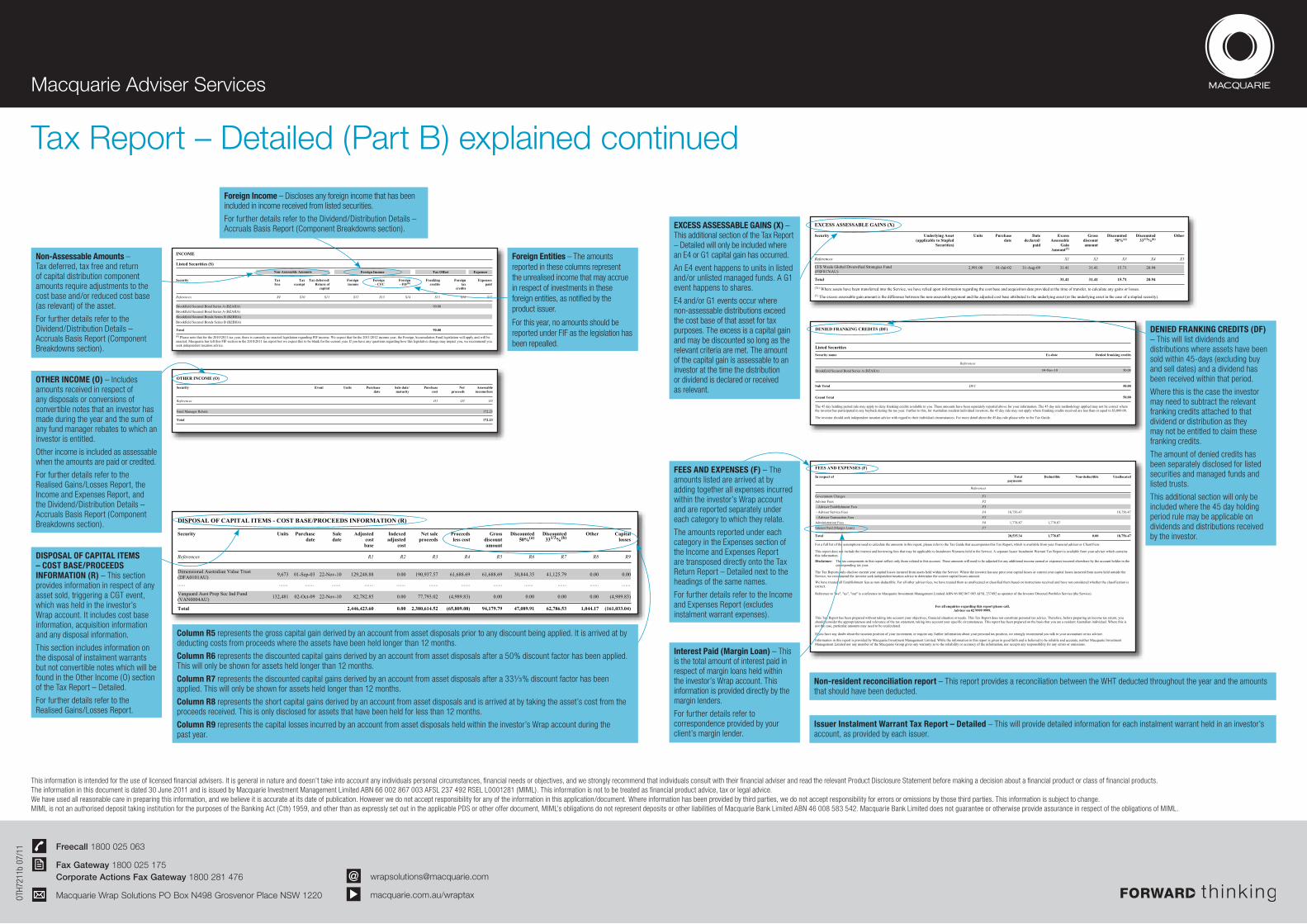

Tax Report – Detailed (Part B) explained continued

EXCESS ASSESSABLE GAINS (X)

UnitsSecurity Datedeclared/

paid

Purchasedate

Underlying Asset(applicable to Stapled

Securities)

X1

ExcessAssessable

GainAmount(1)

Grossdiscountamount

X2

Discounted50%(a)

X3

Discounted331/3%(b)

X4

Other

X5References

2,991.00CFS Wsale Global Diversified Strategies Fund(FSF0176AU)

01-Jul-02 31-Aug-09 31.41 31.41 15.71 20.94

Total 31.41 31.41 15.71 20.94

(Tr) Where assets have been transferred into the Service, we have relied upon information regarding the cost base and acquisition date provided at the time of transfer, to calculate any gains or losses.

As the total non-assessable distributions have exceeded the cost base of the asset, all relevant future non-assessable distributions attributed to this underlying asset may trigger a capital gain.

(1) The excess assessable gain amount is the difference between the non-assessable payment and the adjusted cost base attributed to the underlying asset (or the underlying asset in the case of a stapled security).

(a) This amount represents the taxable capital gains after a 50% discount has been applied.(b) This amount represents the taxable capital gains after a 331/3% discount has been applied. The number included is the 662/3% amount.

23-Jun-11 08:02PMAccount: M05188 10 10ofTAX_125

Foreign Income – Discloses any foreign income that has been included in income received from listed securities.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section). EXCESS ASSESSABLE GAINS (X) –

This additional section of the Tax Report – Detailed will only be included where an E4 or G1 capital gain has occurred.

An E4 event happens to units in listed and/or unlisted managed funds. A G1 event happens to shares.

E4 and/or G1 events occur where non-assessable distributions exceed the cost base of that asset for tax purposes. The excess is a capital gain and may be discounted so long as the relevant criteria are met. The amount of the capital gain is assessable to an investor at the time the distribution or dividend is declared or received as relevant.

OTHER INCOME (O) – Includes amounts received in respect of any disposals or conversions of convertible notes that an investor has made during the year and the sum of any fund manager rebates to which an investor is entitled.

Other income is included as assessable when the amounts are paid or credited.

For further details refer to the Realised Gains/Losses Report, the Income and Expenses Report, and the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Column R5 represents the gross capital gain derived by an account from asset disposals prior to any discount being applied. It is arrived at by deducting costs from proceeds where the assets have been held longer than 12 months.

Column R6 represents the discounted capital gains derived by an account from asset disposals after a 50% discount factor has been applied. This will only be shown for assets held longer than 12 months.

Column R7 represents the discounted capital gains derived by an account from asset disposals after a 33¹⁄ ³% discount factor has been applied. This will only be shown for assets held longer than 12 months.

Column R8 represents the short capital gains derived by an account from asset disposals and is arrived at by taking the asset’s cost from the proceeds received. This is only disclosed for assets that have been held for less than 12 months.

Column R9 represents the capital losses incurred by an account from asset disposals held within the investor’s Wrap account during the past year.

DISPOSAL OF CAPITAL ITEMS – COST BASE/PROCEEDS INFORMATION (R) – This section provides information in respect of any asset sold, triggering a CGT event, which was held in the investor’s Wrap account. It includes cost base information, acquisition information and any disposal information.

This section includes information on the disposal of instalment warrants but not convertible notes which will be found in the Other Income (O) section of the Tax Report – Detailed.

For further details refer to the Realised Gains/Losses Report.

DENIED FRANKING CREDITS (DF)

Security name stiderc gniknarf deineDetad-xE

Listed Securities

References

Brookfield Secured Bond Series A (BZAHA) 50.0004-Nov-10

Sub Total DF2 50.00

Grand Total

The 45 day holding period rule may apply to deny franking credits available to you. These amounts have been separately reported above for your information. The 45 day rule methodology applied may not be correct wherethe investor has participated in any buyback during the tax year. Further to this, for Australian resident individual investors, the 45 day rule may not apply where franking credits received are less than or equal to $5,000.00.

The investor should seek independent taxation advice with regard to their individual circumstances. For more detail about the 45 day rule please refer to the Tax Guide.

50.00

10 11ofAccount: V02531

FEES AND EXPENSES (F)

In respect of

References

Deductible Non-deductible UnallocatedTotalpayments

Government Charges F1Adviser Fees F2 - Adviser Establishment Fees F3 - Adviser Service Fees F4 18,756.4718,756.47 - Adviser Transaction Fees F5Administration Fees F6 1,778.871,778.87Interest Paid (Margin Loan) F7

Total 20,535.34 1,778.87 0.00 18,756.47

For a full list of the assumptions used to calculate the amounts in this report, please refer to the Tax Guide that accompanies this Tax Report, which is available from your financial adviser or ClientView.

This Tax Report has been prepared without taking into account your objectives, financial situation or needs. This Tax Report does not constitute personal tax advice. Therefore, before preparing an income tax return, youshould consider the appropriateness and relevance of the tax statement, taking into account your specific circumstances. This report has been prepared on the basis that you are a resident Australian individual. Where this isnot the case, particular amounts may need to be recalculated.

If you have any doubt about the taxation position of your investment, or require any further information about your personal tax position, we strongly recommend you talk to your accountant or tax adviser.

For all enquiries regarding this report please call,Adviser on 02 9999 9999.

This report does not include the interest and borrowing fees that may be applicable to Instalment Warrants held in the Service. A separate Issuer Instalment Warrant Tax Report is available from your adviser which containsthis information.

The Tax Reports only disclose current year capital losses incurred from assets held within the Service. Where the investor has any prior year capital losses or current year capital losses incurred from assets held outside theService, we recommend the investor seek independent taxation advice to determine the correct capital losses amount.

We have treated all Establishment fees as non-deductible. For all other adviser fees, we have treated them as unallocated or classified them based on instructions received and have not considered whether the classification iscorrect.

Reference to "we", "us", "our" is a reference to Macquarie Investment Management Limited ABN 66 002 867 003 AFSL 237492 as operator of the Investor Directed Portfolio Service (the Service).

The tax components in this report reflect only those related to this account. These amounts will need to be adjusted for any additional income earned or expenses incurred elsewhere by the account holder in thecorresponding tax year.

Disclaimer:

Information in this report is provided by Macquarie Investment Management Limited. While the information in this report is given in good faith and is believed to be reliable and accurate, neither Macquarie InvestmentManagement Limited nor any member of the Macquarie Group gives any warranty as to the reliability or accuracy of the information, nor accepts any responsibility for any errors or omissions.

17-Jun-11 05:18PMAccount: HH0435 9 9ofTAX_125

Interest Paid (Margin Loan) – This is the total amount of interest paid in respect of margin loans held within the investor’s Wrap account. This information is provided directly by the margin lenders.

For further details refer to correspondence provided by your client’s margin lender.

DENIED FRANKING CREDITS (DF) – This will list dividends and distributions where assets have been sold within 45-days (excluding buy and sell dates) and a dividend has been received within that period.

Where this is the case the investor may need to subtract the relevant franking credits attached to that dividend or distribution as they may not be entitled to claim these franking credits.

The amount of denied credits has been separately disclosed for listed securities and managed funds and listed trusts.

This additional section will only be included where the 45 day holding period rule may be applicable on dividends and distributions received by the investor.

FEES AND EXPENSES (F) – The amounts listed are arrived at by adding together all expenses incurred within the investor’s Wrap account and are reported separately under each category to which they relate.

The amounts reported under each category in the Expenses section of the Income and Expenses Report are transposed directly onto the Tax Return Report – Detailed next to the headings of the same names.

For further details refer to the Income and Expenses Report (excludes instalment warrant expenses).

Non-Assessable Amounts – Tax deferred, tax free and return of capital distribution component amounts require adjustments to the cost base and/or reduced cost base (as relevant) of the asset.

For further details refer to the Dividend/Distribution Details – Accruals Basis Report (Component Breakdowns section).

Foreign Entities – The amounts reported in these columns represent the unrealised income that may accrue in respect of investments in these foreign entities, as notified by the product issuer.

For this year, no amounts should be reported under FIF as the legislation has been repealled.

Macquarie Adviser Services

Freecall 1800 025 063

Fax Gateway 1800 025 175 Corporate Actions Fax Gateway 1800 281 476

Macquarie Wrap Solutions PO Box N498 Grosvenor Place NSW 1220

macquarie.com.au/wraptax

Issuer Instalment Warrant Tax Report – Detailed – This will provide detailed information for each instalment warrant held in an investor’s account, as provided by each issuer.

Non-resident reconciliation report – This report provides a reconciliation between the WHT deducted throughout the year and the amounts that should have been deducted.