Embed Size (px)

Citation preview

Tax Risk Management

Tony ElgoodTax PartnerUnited Kingdom

Ian ParoissienTax PartnerAustralia

Larry QuimbyTax PartnerUnited States

Larry Quimby, is a US based tax engagementpartner working with a number of our Philadelphiabased clients. He is currently the national lead foran initiative addressing the application of theSarbanes Oxley Act to the tax function.

For further information:[email protected]

Ian Paroissien is the leader of PwC’s GlobalCompliance Services for Australia and the AsiaPacific theatre. Ian advises many leadingcompanies on best practices and developmentsin tax management and compliance systems.

For further information:[email protected]

Tony Elgood is the author of The ‘Best Practice’tax function guide. He is based in the UK and ispart of PwC’s Global Compliance Services team.He works regularly with leading tax functions inhelping them set their strategies and managetheir tax functions.

For further information:[email protected]

Acknowledgments:We are very grateful for the help and comments given to us by a number of people during the preparation of this guide. Inparticular we would like to thank Pat Ellingsworth (head of group taxation at Royal Dutch/Shell) and Alan Davidson from thePricewaterhouseCoopers London office for their input. For more information on strategic thinking for a tax function see thePricewaterhouseCoopers ‘Best Practice’ tax function guide.

Tax Risk Management 1

Contents Page

1. Introduction 2

2. What is tax risk? 3

3. Why is tax risk management important and who to? 11

4. Where does managing tax risk fit into the overall tax strategy? 18

5. The risk management framework for tax 20

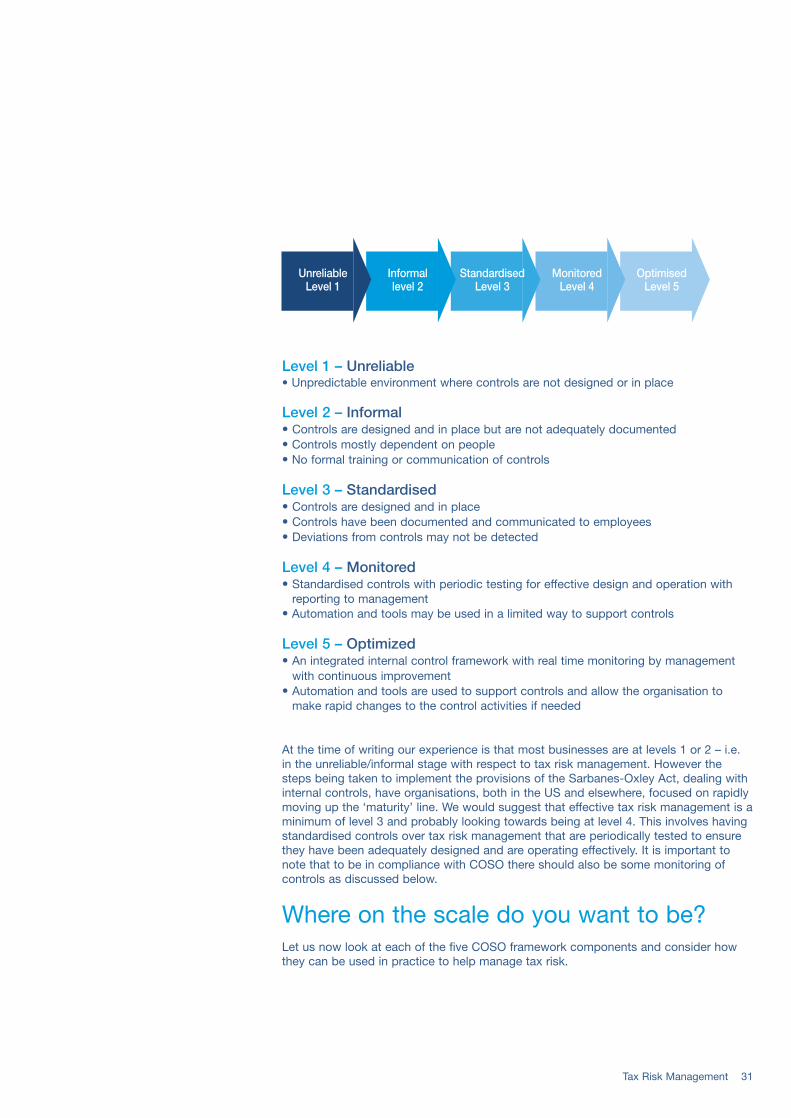

6. The tax risk management framework in practice 30

a. Risk control environment 32

b. Risk assessment 34

c. Control activities 41

d. Information and communication 46

e. Monitoring 47

7. Managing global tax risk 48

8. Summary 53

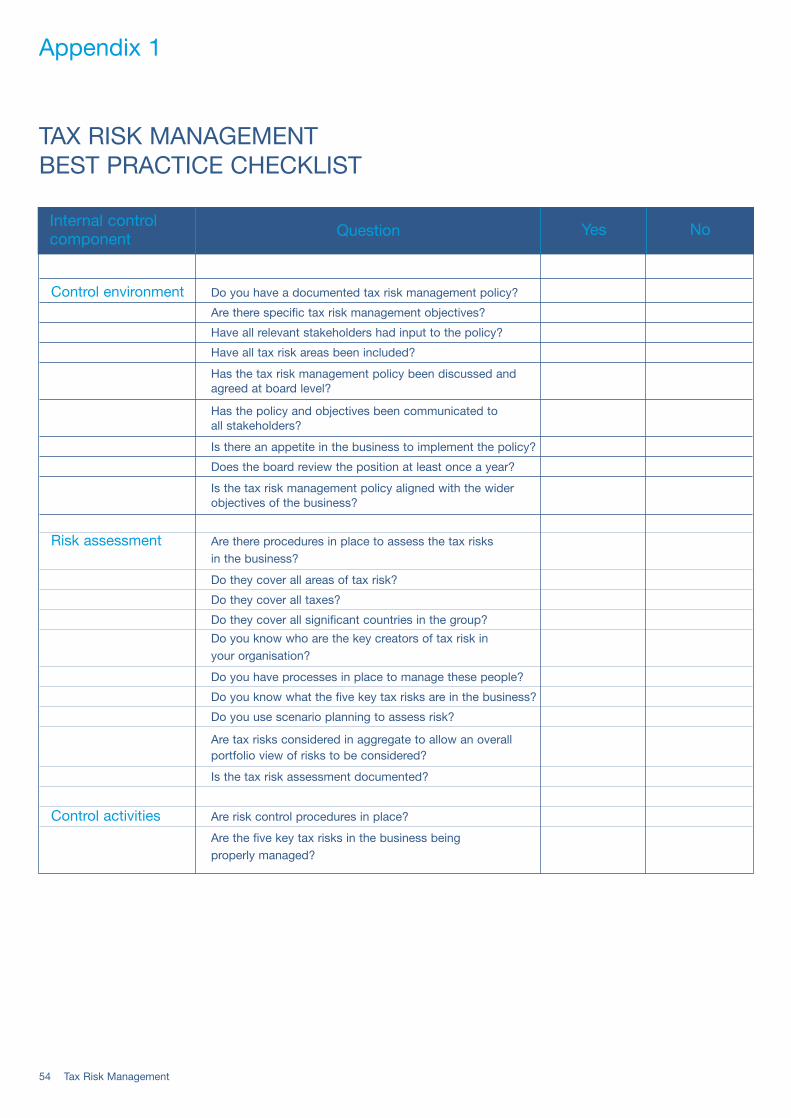

Appendix 1 Best practice checklist 54

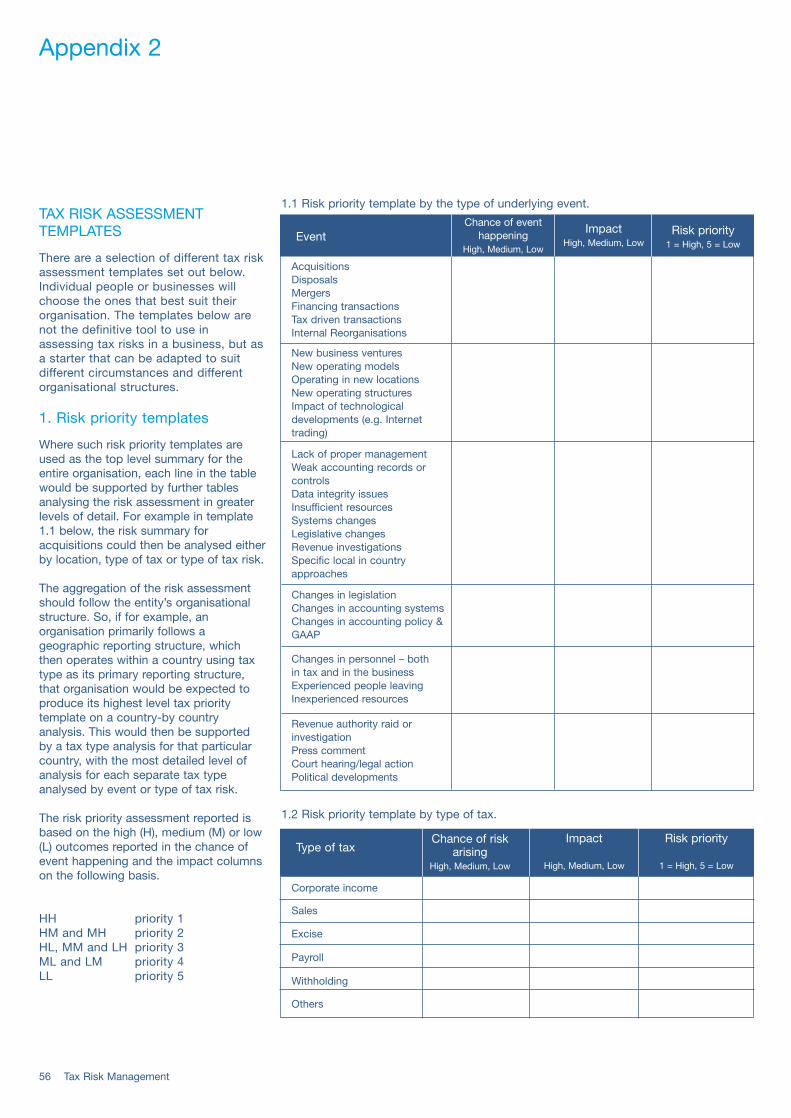

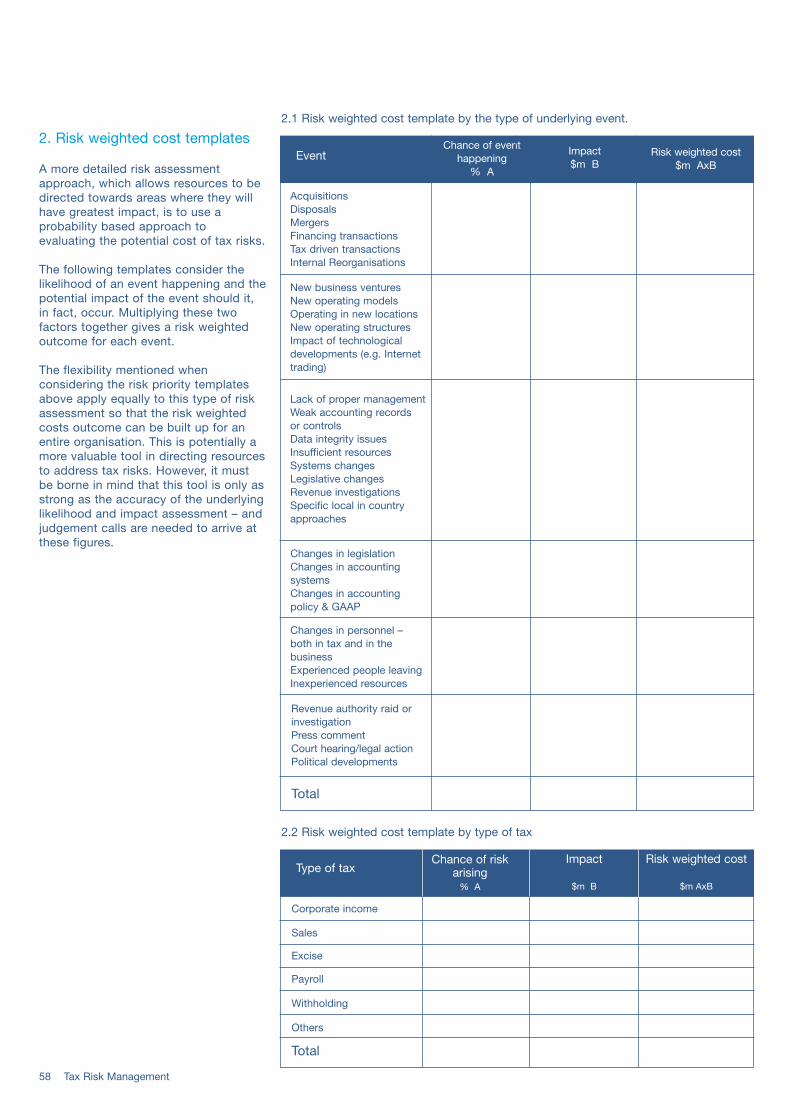

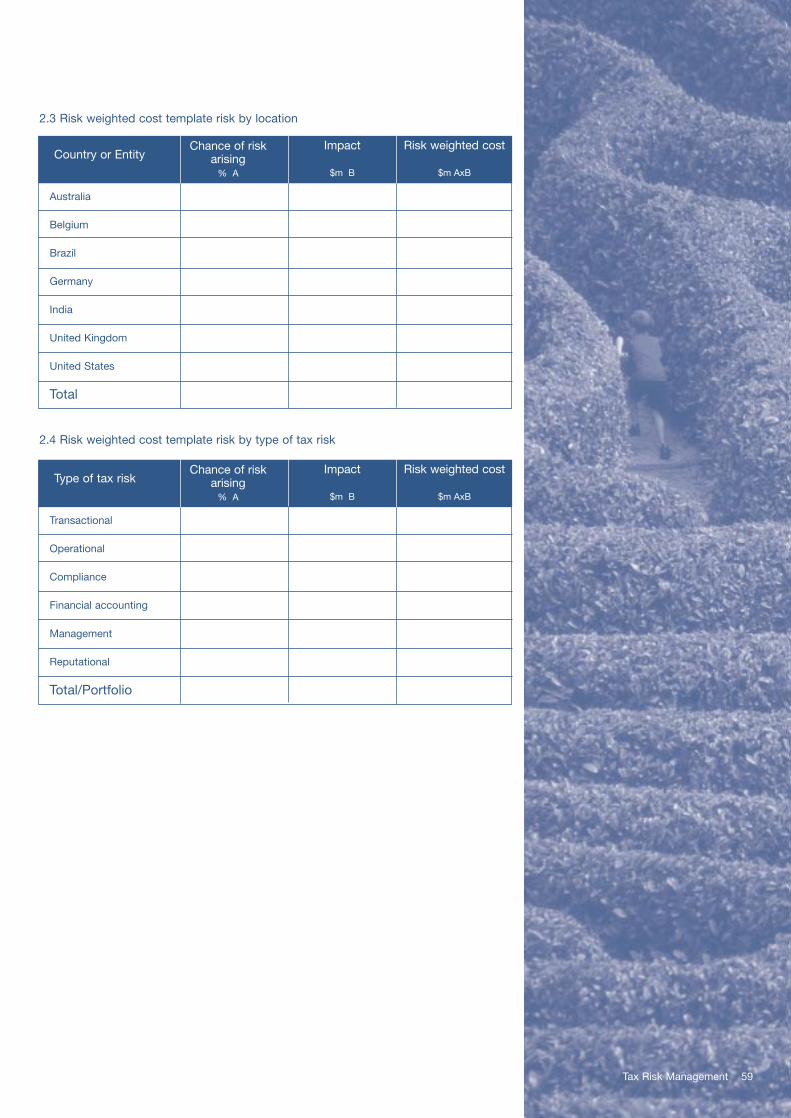

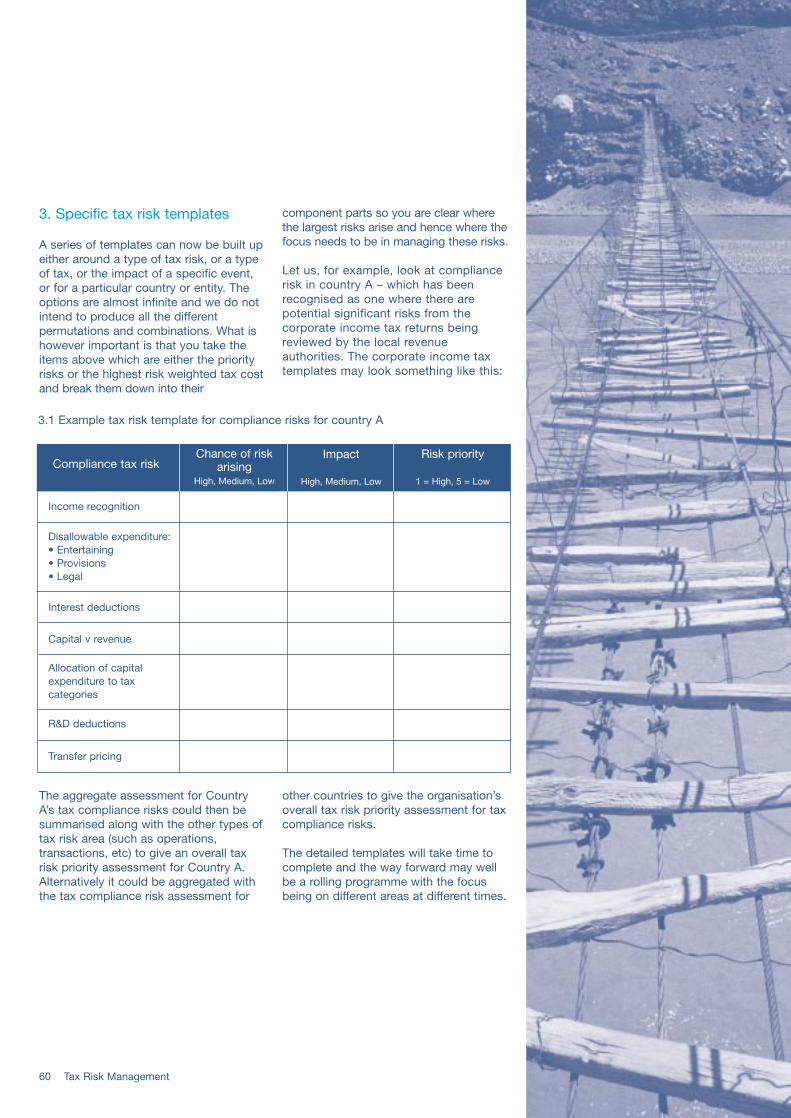

Appendix 2 Risk assessment templates 56

2 Tax Risk Management

1 INTRODUCTION

We have seen the Enron scandal in the US, and more recently the Parmalat scandal in Italy. The US hasresponded with the introduction of the Sarbanes-Oxley legislation, and with an ongoing increase inglobalisation, similar legislation and practices are springing up in a number of different countries. Insideorganisations there is an increasing awareness that risk management, and in particular, good internal controlprocedures is becoming more and more important.

Historically tax risk management and tax internal controls were a bit of a black art, not necessarilyunderstood even by those in the tax function, let alone those outside. Whilst recognising that the tax areahas its own unique profile, tax risk management is now increasingly being discussed inside both commercialorganisations and revenue authorities. Companies are starting to document their tax risk managementpolicies and to do this they are having to assess the different types of tax risk in their business. Someorganisations have also recently appointed internal tax risk managers.

The purpose of this guide is to pull together the current thinking on tax risk management. It is aimed notonly at tax directors and their teams, but also at CFOs, audit committees, chief risk officers and internalaudit functions. These stakeholders, including those sitting outside the tax function, need to be comfortablethat there is a tax risk management policy in their organisation, that tax, as one of the key costs in thebusiness, is being properly managed and that the inherent risks in the tax position of the organisation arebeing both understood and properly controlled.

Tax risk management has come a long way over the last couple of years and will continue to evolve. This isnot a manual about how to manage tax risk – different businesses will address their issues in different ways.What we have tried to do is to set out firstly the issues that need to be discussed when a company isdeciding on its policy and addressing its approach to tax risk management, secondly a framework formanaging the risks and finally some specific tools and techniques that can be used in doing so.

We look forward to being part of the debate as this area of tax management continues to develop in the fastchanging commercial world in which we find ourselves.

In early 2002 we published a guide entitled the ‘Best Practice’tax function. In that guide there was one chapter (seven pages)on Tax Risk Management. Since that guide was published thecorporate world has changed dramatically and risk managementhas shot up the agenda of most organisations.

The decisions, activities and operationsundertaken by an organisation give rise tovarious areas of uncertainty – businessrisks. Some of these uncertainties will be inrespect of tax. These tax uncertainties maybe in relation to the application of tax lawand practice to particular facts, it may beuncertainty over the facts themselves or itmay be uncertainty as to how well systemsoperate to arrive at the tax results of thebusiness activities and operations. Theseuncertainties give rise to tax risk.

Managing tax risk is therefore aboutmanaging these uncertainties. Due to thevery nature of these uncertainties, there isoften no one right answer. Tax riskmanagement is about understanding wherethese risks arise and making judgementcalls as to how they are dealt with.

We have sought in this chapter to providean explanation of where we see the mainareas of tax uncertainty arising. This hasled us to define seven main areas of taxrisk. We have quite intentionally not triedto do any analysis by type of tax – sufficeit to say that we include all types of tax

under the umbrella of tax risk management,irrespective of whether they are taxesmanaged by the tax function or not. They all give rise to uncertainty and henceto tax risk.

For any type of risk, you not only need tounderstand what it is but you also need todecide how much risk you are willing andprepared to take. To our mind tax riskmanagement is not necessarily thereforeabout minimising risk. Businesses makeprofits by taking risks and a no-riskstrategy is probably neither cost effectivenor right for any business. By setting aframework scale (or a score out of 10),against where you either want to be or areprepared to be for each type of tax risk,you give yourself some criteria againstwhich to decide what actions need to betaken, what risks you are prepared to takeand how any particular type of tax risk is tobe managed. For each area of tax risk thischapter provides such a framework scale.

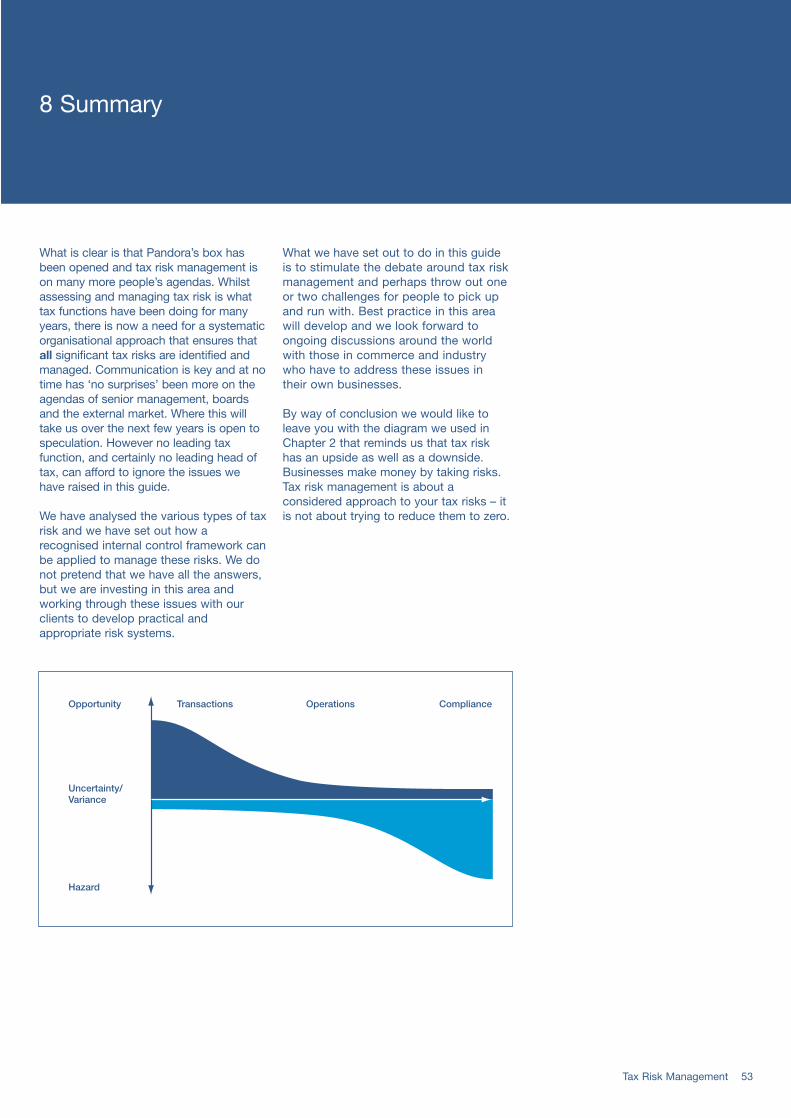

The tax risk spectrum below showswhere the major tax uncertainties canarise. It shows the upside opportunity

that can arise from business transactions,the downside hazard which can arisefrom the compliance process and the factthat the operational part of the businesscan give rise to both opportunities andhazards. Ensuring that the opportunitiesare maximised can be as important asmanaging the hazards.

A company’s policy on tax riskmanagement will therefore determine:• The value that can be achieved by

taking risks,• The costs that can be saved by

reducing risks, and• The resources needed to manage

both the upside opportunities andthe downside risks

Before we proceed, we should make itclear that we believe each business has aresponsibility and duty to pay theappropriate taxes on its businesstransactions. We also feel strongly that it isimportant for organisations to manage andplan their tax affairs. However we do notbelieve it is right for a business to play the‘tax audit lottery’ with the revenueauthorities. This chapter and, indeed, thewhole guide, are based on the fundamentalpremise that non disclosure to authoritiesis not an acceptable approach and that the‘risk of getting caught’ is therefore not aconsideration or risk to be ‘managed’.

Tax Risk Management 3

Opportunity Transactions Operations Compliance

Hazard

Uncertainty/Variance

The term tax risk means different things to different people andwe need to start with a common understanding of what it is weare talking about. Only then can we address how tax risk can be managed.

2 WHAT IS TAX RISK?

4 Tax Risk Management

Specific risk areas

Transactional risk

This concerns the risks and exposuresassociated with specific transactionsundertaken by a company. In anytransaction there may be uncertainty as to how the relevant tax law will applyand uncertainty arising from specificjudgement calls – particularly in the morecomplex areas.

The more unusual and less routine aparticular transaction is, then generally, the greater the tax risks associated withthe transaction are likely to be. One-off,non-routine transactions, such asacquisitions/disposals of businesses orparts of a business, or significantrestructuring projects and reorganisations,will generally bear greater tax risks than theroutine every day business such as sellingproducts and services. In addition there arelikely to be well-designed procedures andsystems in place for the processing ofroutine transactions, which would usuallynot apply to non-routine, one-off

transactions. From a tax point of view thehighest risk transactions are often thosethat are happening specifically for taxpurposes e.g. a tax driven reorganisation.

In any transaction there will be viewstaken during the process as to what isacceptable and what is not – risks willundoubtedly be taken. This is in the verynature of the way transactions andnegotiations are carried out. Some partsof a transaction may be carried out toachieve a particular tax result (for exampleto preserve tax losses). The steps takento achieve the hoped for tax result may below risk or they may be more aggressivewith more chance of being challenged bya revenue authority.

Major transactions have for some timebeen a key focus for tax authorities butthe signs are that this is increasing. InAustralia for example, the Commissionerof Taxation has just written to the boardsof all public companies indicating that aspart of their governance responsibilitiesthey should be signing-off that the tax

risks have been properly assessed and areappropriate. In doing so the Commissionerhas provided boards with 10 questions or criteria against which to judge this. (For more details on the AustralianCommissioner’s position see Chapter 3.)The appropriateness of this and the issuesit raises are a major discussion point inthemselves but it does highlight thegrowing profile and importance of tax riskmanagement in this area.

Additionally tax risks can arise fromfailures, such as:

• The tax department is not involved inthe transaction or are brought in onlyat the last minute;

• There is no organisational agreedframework against which to judgeacceptable risk; and/or

• There is a failure to properly documentand implement a transaction.

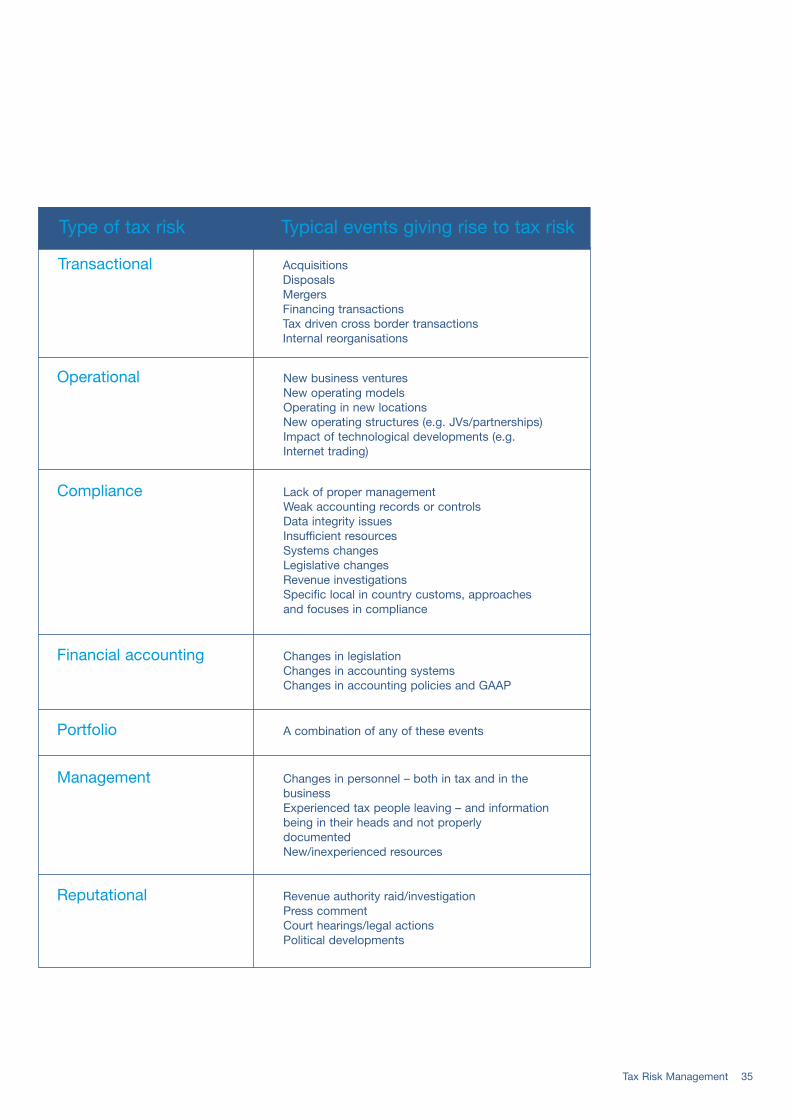

Types of Tax RiskIn our view there are seven broad categories of risk associatedwith taxes, four that are specific risk areas and three that arerather broader and more generic.

These are:

Specific risk areas1 Transactional risk2 Operational risk3 Compliance risk4 Financial accounting risk

Generic risk areas

5 Portfolio risk6 Management risk, and7 Reputational risk

Tax Risk Management 5

In our view this last point often carries the greatest risk in the transactional area. Failureto implement and document properly what has been planned and agreed is in ourexperience the cause of more tax authority challenges in this area than any other. Wherethe tax result depends on a particular sequence of events, board meeting or wording in a documentation there is often the risk that the ‘i’s are not dotted and the ‘t’s are notcrossed – and all the best planning falls down due to inadequate implementation andmonitoring over the life of the issue to ensure nothing is done to prejudice the tax result.Revenue authorities are increasingly asking to see the full documentation relating to aparticular transaction to test out whether the implementation has achieved the result thecompany is claiming.

The question then arises as to how much tax risk are you prepared to take in particulartransactions and how much risk are you actually taking over the correct implementationof the transactions? What is your profile in relation to transactional risk?

It is important in considering this scale to indicate where you want to end up as distinctfrom the inherent risk in the transaction or planning idea. Risks identified can in manycases be managed, such that a risk initially identified as above an acceptable level maybe capable of being brought within it by a tax ruling or some other approach. Thisrecognises that risks can be managed so that the potential upside benefit is not lost.

Operational risk

Operational risk concerns the underlying risks of applying the tax laws, regulations anddecisions to the routine every day business operations of a company. Different typesof operation will have different levels of tax risk associated with them. For example,compare normal third party product sales with intra-group cross-border products sales;there are greater tax risks associated with connected party cross-border transactions(primarily transfer pricing issues). With increasing globalisation of trade there is an ever increasing risk of operational people inadvertently creating a taxable presence in a country in which they are operating. These are just two examples of tax risks that can occur from the normal ongoing business of a company.

In our experience the closer the tax function is to the business operations the betterthese types of risks are managed. Communication between the various parties is key.The standing of the tax function in the organisation will be an important point here; if the people are well respected, then they are more likely to be contacted at theappropriate time. Where are you today on the operational risk scale – and where wouldyou like to be?

Low Medium High

0ConservativeNo riskProud of the tax we pay

10Aggressive

Minimum amount possible

5

Low Medium High

0

Tax heavily involved in operationsFormal sign off procedures in place

10

Tax seldom consultedNo formal procedures

5

6 Tax Risk Management

Compliance risk

Compliance risk concerns the risksassociated with meeting an organisation’stax compliance obligations. (As we notedearlier, we do not believe risk of discoveryby tax authorities is a factor. One mustassume full disclosure and that theauthorities are aware of and will reviewyour activities.) From a tax perspectivecompliance risk would primarily relate tothe preparation, completion and review ofan organisation’s tax returns (of whatevertype and not only corporate tax returns)and the risks within those processes.

Compliance risk addresses the risksimplicit in the systems, processes andprocedures adopted by a company toprepare and submit its tax returns and inresponding to any enquiries/issues raisedin the process of reaching an agreedposition with the authorities.

What we are talking about here is:

• the integrity of the underlying accountingsystems and information,

• the processes of extracting tax sensitiveinformation from the accounting system,

• ensuring the tax compliance analysisprocesses are based on up to dateknowledge of the latest tax law andpractice, and

• the proper and efficient use oftechnology in the processes.

There are clearly cost implications in whereyou position yourself on the scale belowand there will be a trade off between costsspent and risks taken. To achieve no errorsin any tax return will undoubtedly be costprohibitive. Alternatively, are you overengineering the process and could youreduce the cost with little or no impact onyour risk position? What is your attitude totax penalties? Where do you want to be onthe scale above – and what changes needto happen in the way you operate to getyou there?

Tax compliance risk also includes therisks arising from agreement of taxreturns and from enquiries on, or theaudit of, submitted tax returns by fiscalauthorities. In a number of countries thefinal agreement of a tax return oftenends in a ‘horse trade’ between thetaxpayer and the relevant revenueauthority; it may make sense to have anumber of aggressive positions in thereturn so that there is something to giveas part of any negotiations.

Additionally, and we will come back to thispoint later on, how many of the group’stax returns is the tax function activelyinvolved with? What about payroll taxreturns, indirect tax returns, and customsand duty returns? If it is not the taxfunction, who is managing the risksassociated with these returns?

There is also an interaction betweencompliance risk and reputational risk (seebelow). How do the revenue authoritiesrate you on a risk scale? Do they see youas an aggressive tax planning group andhave ‘marked your card’ as one wherethey have to do a lot of work – or are youseen as a more conservative group wherethey have little to go for?

Financial accounting risk

The Sarbanes-Oxley Act of 2002 hasbrought the risks in the financialaccounting area into sharper focus. A particular challenge for many taxdepartments is the requirement inSarbanes-Oxley Section 404 requiringdocumented and tested internal controlsover financial reporting.

At this point one should note that in mostjurisdictions the figures included in the tax accounts, at the time the financialstatements are issued, are ‘estimates’. In fact, deferred tax accounting generallycalls for the estimation of future taxes tobe paid under tax regimes on transactionsthat are recorded in the accounts in thecurrent year. Avoiding negative prior yearadjustments to the tax accounts hasalways been high on most tax directors’agendas. We have lost count of thenumber of times we have been told by taxdirectors that what the CFO and board arelooking for is ‘no surprises’. This hasprobably led tax directors to be more riskaverse than they might have been (and tomiss upside opportunities?) Thisconservative view as to what should beprovided for in the accounts may lead to a debate with the auditors as to whether a provision is justified or is perhaps atouch over prudent.

As well as looking at the processes inarriving at the accounts figures, and theinternal controls around these processes,the following questions need to be asked:

• How much uncertainty is there in theinterpretation or application of the taxlaw(s) used to compute the taxfigures?

• What is the quality of the data receivedfrom or used in the transactional,operational and compliance areas?

• Are there issues or questions as to theapplication of the tax law to the data?

• What provisions are needed to coverthese uncertainties and what level ofmateriality is acceptable?

Low Medium High

0

Zero tolerance – no error rate

10

Large acceptable error rate

5

Tax Risk Management 7

It will be interesting to see howcompanies apply Section 404 to the taxaccounts. The ‘spirit’ of the law wouldsuggest that better information and moretimely consideration of risk will evolve.Some have suggested a mechanical‘check the box approach’ to the adoptionof the requirements of Section 404. Webelieve that the mechanical approachmay cause a number of tax functions tofocus too heavily on the processes inarriving at the tax figures in the financialaccounts – at the expense of theprocesses of managing the other tax risksconsidered in this chapter. These othertax risks are potentially the ones thathave been less well managed and arewhere there are both larger opportunitiesand greater risks.

Clearly it is not only the statutory financialaccounts where financial accounting riskarises. Tax figures appear in cash flowplanning, forecasting, and in managinginvestor expectations of the future.

Generic risk areas

You could argue that the four specific taxrisks set out above are the only ones thatreally exist, and the risks we set outbelow are more about managing theserisks than risks themselves. However webelieve them to be sufficiently importantto be treated as separate risks in theirown right and to be reviewed as part ofthe tax risk management process. If youdisagree with us then some of the toolsintroduced later in this guide will needadapting to show four risk areas, notseven. However whichever way we go onthis point, the general principles of taxrisk management will not change. Thethree areas of tax risk that we are callingthe generic tax risks are explained below.

Portfolio risk

Portfolio risk concerns the overallaggregate level of risk when looking attransactional, operational and compliancerisks as a whole and considers theinteraction of these three different specificrisk areas. This is of particular concern tothose organisations that are involved in anumber of transactions, whether tax drivenor business driven. One might argue thatthe financial reporting is the measure ofthe portfolio risk and well it might be.However, we believe that a consciousconsideration of the aggregation of thethree risks should be considered.

Each particular transaction may be belowthe ‘risk threshold’, but when combinedtogether with positions taken with variousrevenue authorities the cumulative riskprofile becomes unacceptable.

What would be the impact if all the areasof tax risk went wrong at the same time?What would be the financial implicationsand what would be the resourcingimplications to deal with the issues?

Have you given each key tax risk in yourorganisation a percentage chance ofgoing wrong and aggregated the result?Have you considered the worst-casescenario and the impact of this on theprofit and loss account and the balancesheet? Is this acceptable?

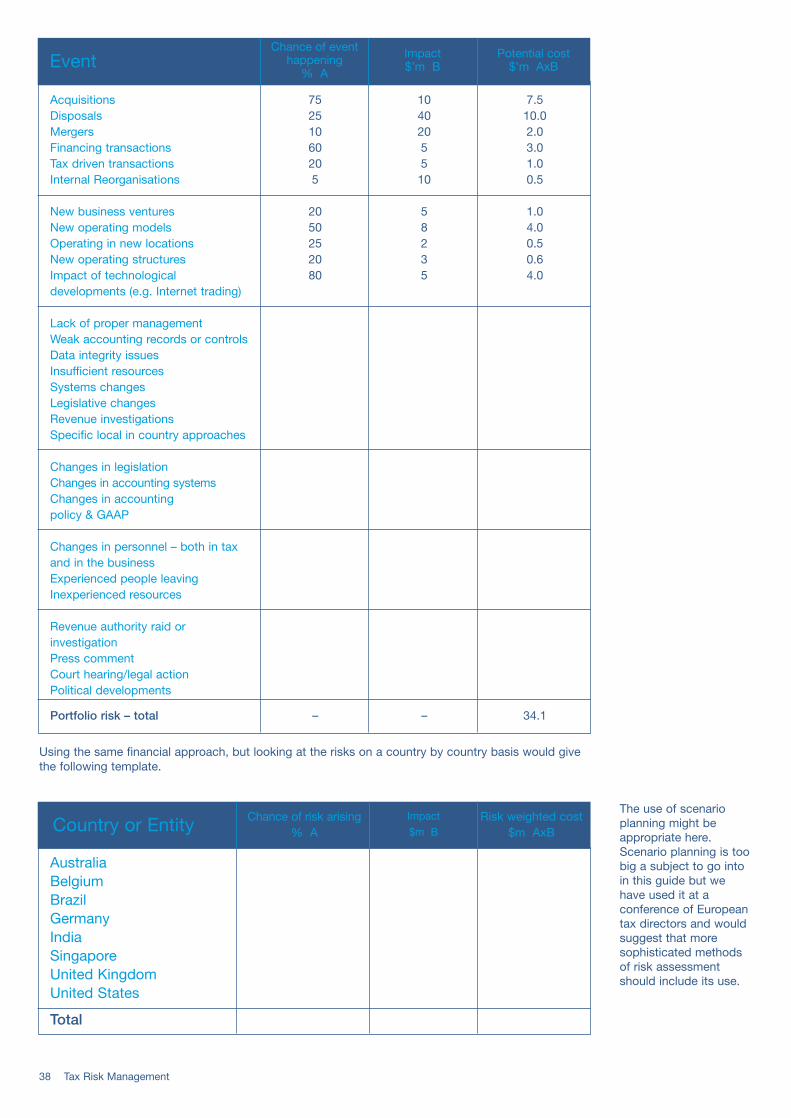

We look later, in Chapter 6 andAppendix 2, at how you might measureportfolio risk by considering both theimpact and the probability of particularrisks actually happening.

Low Medium High

0

Good internal controlsHigh degree of certainty

10

Unquantified riskLow degree of certainty

5

Low Medium High

0

Low aggregate risk

10

High aggregate risk

5

8 Tax Risk Management

Management risk

The second generic area of tax risk is oneof not properly managing the various risksset out above. In our experience, few taxfunctions actually have a documented taxrisk management policy, though we arestarting to see tax risk managers beingappointed. Risk management issomething that historically has notspecifically been on the agenda for manytax functions. While some of the risksabove will have been managed, wesuspect few people will claim that all theirtax risks have been managed in asystematic way. Even where it has, a lotof the information about tax issues iscarried around in people’s heads and ifthese people leave the organisation thenthe information leaves with them.

In this new world, with tax risk managementbecoming increasingly important, it is clearthat organisations need to put some timeand resources behind this issue. They alsoneed to ensure that those charged withmanaging tax risks have the skills and theability to do so. ‘Under-managing’ theseissues, either through a lack of skill,resource or time can lead to unexpected‘surprises’ or possibly worse, missedopportunities. Tax risk management willneed to become a higher managementpriority for many organisations.

Reputational risk

We have collected a file of press cuttingsrelating to the tax affairs of companies –and this file is becoming increasinglybulky. How will your CEO or the boardreact to seeing your tax affairs splashedall over the front page of a nationalnewspaper (or even on the inside pages)?

Reputational risk concerns the widerimpact on the organisation that mightarise from an organisation’s actions ifthey become a matter of publicknowledge. By their very nature suchrisks will impact wider business interests.For example, consider the impact on acompany if, as a result of pursuing a tax

issue through a public arena such as the courts, information about the company’s activities or practices result in changes tothe perception of the company by itscustomers, suppliers, or employees.

Consider also the impact of being seento pursue considerably more aggressivetax planning and ideas than the norm –does this matter to you?

Low Medium High

0Tax risk management taken seriouslyHigh on management agendaResources available to do this

10Lack of risk management skills

Lack of budget/resourcesQuality resources not available

5

Low Medium High

0

Not important

10

Very important

5

Tax Risk Management 9

More than one tax strategy we have seen have included policiessuch as “We will not undertake any tax planning transactionwhich would reflect adversely on the group if details of it were to be published in the business pages of [Daily Newspaper Title].”

By way of an example, in the US it isproposed that failure to disclose certain‘listed transactions’ under the ReportableTransaction Regulations will result in afine. For an SEC listed company, the factthat a fine has been levied may have tobe disclosed in the published accounts.The potential disclosure of the failure toreport properly certain transactions to theInland Revenue Service could however be more concerning than the fine itself.

For MNCs (multi national corporations)this issue may also go to the heart ofgood corporate citizenship, particularly inforeign jurisdictions where reputational risksmay be more important in some countriesthat at home. It is also where culturaldifferences and policy clashes can occur.Identifying and managing issues such asthe impact of aggressive tax planning,reputational issues just from major taxauthority challenges, and policy andpractices around corruption, are allelements of reputational tax risk management.

This leads on to the question of tax ‘ethics’and whether companies have an obligationto pay their ‘fair share’ of tax – whateverthat might mean. There is a debate takingplace in many countries around this point –and whether companies should pay the taxthat is in accordance with the letter of thelaw, the spirit of the law or both (if that ispossible). To be seen to be doing anythingdifferent can impact on a company’s widerreputation. Is transparency of your taxposition an important part of managingyour reputational risk?

External risks

The comments so far have focused onthe risks that are manageable inside anorganisation. There will also be risks thatare external and by their very nature areunmanageable – but are very real andequally important nevertheless. Examplesunder this heading are a change oflegislation, an unexpected court decisionon a particular point, or even a change of government. The rest of this guidefocuses on those risks that a businesshas some control over – but perhapsportfolio risk should be deemed toinclude this extra layer of external risk.

Use of the scale frameworks

In our discussions so far, there is anassumption that there is one point on thescale for each of the different types of risk.However we recognise that thisassumption may not be valid when youlook across the spectrum of different taxesand different countries. For example youmay well decide that the compliance riskyou are prepared to take for one particulartax in country A is very different from thatfor another type of tax in country B.

You may wish to put the different taxesand countries at different points on thescales. This leads us to a threedimensional matrix, covering the types of risk, the types of tax and the differentcountries in which you operate.

Co

rpo

rate incom

e taxesS

ales taxesE

xcise duties

Payro

ll taxesW

ithhold

ing taxes

Austra

lia

Belgium

Brazil

Germ

any

India

Singap

ore

United

King

dom

United

Sta

tes

Transactional risk

Operational risk

Compliance risk

Financial accounting risk

Portfolio risk

Management risk

Reputational risk

It is likely that the mere exercise ofcompiling the information and consideringthe areas of tax risk that we have discussedin this chapter will significantly enhance acompany’s management of tax risks.

10 Tax Risk Management

Other activities

In our experience tax functions often havea wider remit than just tax. Tax and treasuryare sometimes the same department; taxfunctions are often responsible for thepreparation of statutory accounts as theyare the people who need them most – toenable them to file the tax returns.

The purpose of this guide is to focus ontax risk management and we have notsought to stray into the other activities thatmay be carried out by the tax function.That is not to say that the risks in theseareas do not need managing.

SummaryWe have set out the seven areas of tax risk, together with a scale of one to ten for each one. By reviewing allseven scales, it should be possible to produce one overall scale summarising your organisation’s attitude to taxrisk management. You should be able to consider where you want to be on the scale – and where you are today. This will give you a template to consider further what actions you need to take going forward.

Low Medium High

0

ConservativeLow appetite for risk

10

AggressiveRisk taker

5

Where are you today – and, more importantly, are you where you want to be?

Very few organisations will be positioned at eitherend of this scale. The organisations on the left hand side might be the ones who:• Are inherently cautious• Spend more time managing risk• Are more concerned about compliance risk• Are concerned about their reputation

The organisations that position themselves on theright hand side of the scale:• Are more aggressive• Accept that they will have more compliance risks• Have a higher materiality level• Are less concerned about upsetting revenue

authorities• Spend less time managing tax risk

We look in more detail in Chapter 4 as to how tax risk management fits into the bigger picture both in terms of managingtax and managing risk in the organisation as a whole. However before doing so can you answer the question belowspecifically in terms of tax risk management.

Tax Risk Management 11

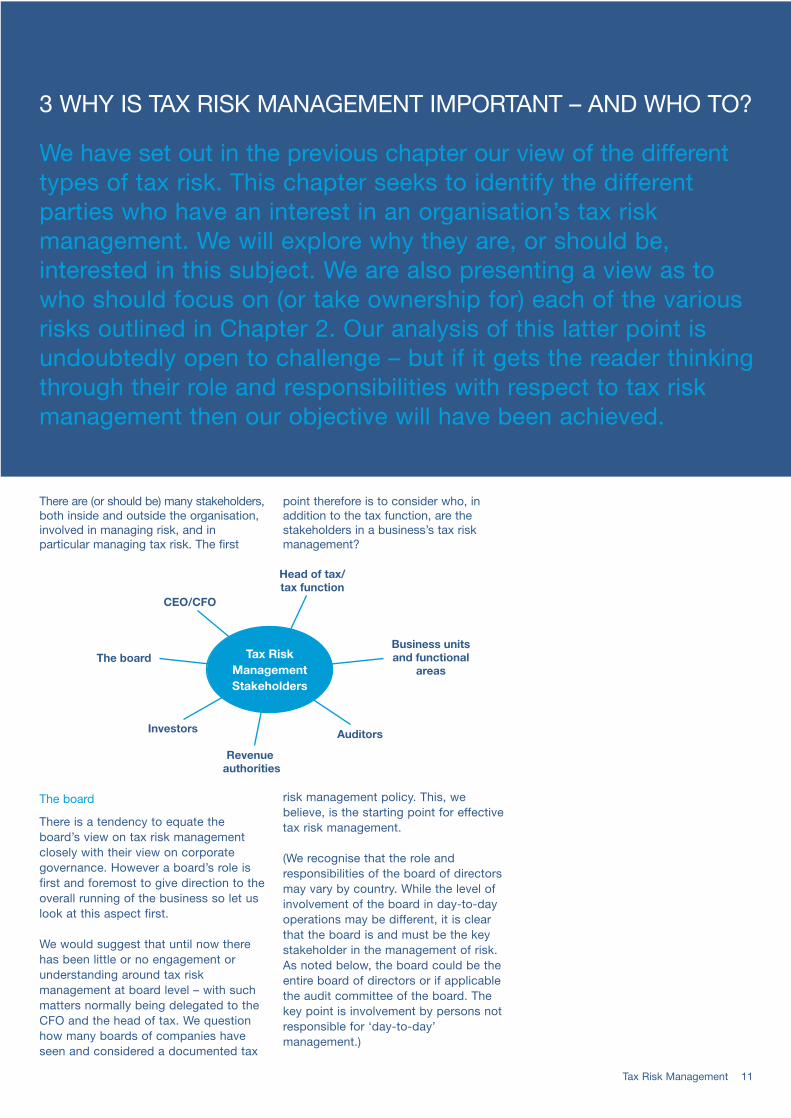

There are (or should be) many stakeholders,both inside and outside the organisation,involved in managing risk, and inparticular managing tax risk. The first

point therefore is to consider who, inaddition to the tax function, are thestakeholders in a business’s tax riskmanagement?

Head of tax/tax function

CEO/CFO

The boardBusiness unitsand functional

areas

Auditors

Revenue authorities

Investors

Tax RiskManagementStakeholders

3 WHY IS TAX RISK MANAGEMENT IMPORTANT – AND WHO TO?

We have set out in the previous chapter our view of the differenttypes of tax risk. This chapter seeks to identify the differentparties who have an interest in an organisation’s tax riskmanagement. We will explore why they are, or should be,interested in this subject. We are also presenting a view as towho should focus on (or take ownership for) each of the variousrisks outlined in Chapter 2. Our analysis of this latter point isundoubtedly open to challenge – but if it gets the reader thinkingthrough their role and responsibilities with respect to tax riskmanagement then our objective will have been achieved.

The board

There is a tendency to equate theboard’s view on tax risk managementclosely with their view on corporategovernance. However a board’s role isfirst and foremost to give direction to theoverall running of the business so let uslook at this aspect first.

We would suggest that until now therehas been little or no engagement orunderstanding around tax riskmanagement at board level – with suchmatters normally being delegated to theCFO and the head of tax. We questionhow many boards of companies haveseen and considered a documented tax

risk management policy. This, webelieve, is the starting point for effectivetax risk management.

(We recognise that the role andresponsibilities of the board of directorsmay vary by country. While the level ofinvolvement of the board in day-to-dayoperations may be different, it is clearthat the board is and must be the keystakeholder in the management of risk.As noted below, the board could be theentire board of directors or if applicablethe audit committee of the board. Thekey point is involvement by persons notresponsible for ‘day-to-day’management.)

The templates in Chapter 2 might beused as a starting point for engaging theboard in the debate as to what is thegroup’s tax risk management policy. Havethey properly considered both thebenefits and the costs of the variousapproaches to tax risk management –how aggressive or conservative do theywant the group to be? How does this fit in with the risk management policy for thegroup as a whole? How does this fit inwith the group’s overall tax strategy?

Historically, we have found that, whenasked, boards may have perceived thatthe tax function was one where there was‘low risk’. In fact, the board may haveperceived (and expected) the company tobe taking a more aggressive approach totax risk management than the tax functionwas actually adopting. The process ofdiscussing a tax strategy with the boardis, in our recent experience, changing andadding direction to and support for whatthe tax function is expected to do.Whatever the view of the board, gettingthe tax strategy in front of them is goodfor the profile of the tax function.

Perhaps the two key tax risks the boardshould focus on are portfolio risk andreputational risk. The board should have ageneral understanding of the organisations‘risk profile’. The portfolio risk addressesthis ‘profile’ for tax. Of equal or possibly of greater importance is a view onreputational risk. It is important that theboard understands the impact onreputation that the organisation’s taxpositions (or lack thereof) may have withinthe business community or the communityat large. A consistent position, along withboard support for the resources needed to manage reputational risk, are key tosuccessfully addressing this area.

A documented tax risk policy that isembraced by the board is also crucial forgood corporate governance. The boardnot only sets the tax risk/rewardphilosophy of the business, it also setsthe tax risk management framework andthe whole ethos as to how risk isassessed, how management controlsoperate within the business and how they are monitored.

The rules, regulations and commentarygenerated by Sarbanes-Oxley have beendriving most of the current thinking in thisarea, even where a group is not SEClisted. The Sarbanes-Oxley rules requiredetailed documentation of the design andoperational effectiveness of internalcontrols to be in place – anddocumentation of tax risk managementpolicies and controls is not something wehave seen in many organisations. Bestpractice would suggest that whatever thetax function (or others) produces in thisarea should be acknowledged andembraced by the board.

In some countries revenue authoritieshave also been driving thinking in thisarea. In Australia for example, theCommissioner of Taxation has written to public company boards stating, “It isimportant that the board identify thetaxation risks associated with theirorganisation’s operations, which risks areacceptable and appropriate, and whichare not, and put in place a process for the management of those risks.”

The view expressed was that in respect of major transactions and arrangementsit was not sufficient for boards to relysimply on tax functions and externaladvice but should focus beyond taxoutcomes to questions of probability,level of aggressiveness, likely tax officeresponse and the implications ofalternative outcomes.

12 Tax Risk Management

Tax Risk Management 13

This of course raises a whole series ofissues and questions to be addressed.These range from whether these are theright questions and whether this is in factthe right level to be asking these questions.(Should it be the audit committee, CEO,CFO or the tax director?) Issues range from the capacity of the board to makeappropriate judgements to content and tax office access to board papers. In ourview many of the matters raised in thesequestions can be dealt with by appropriatepolicies that the board has signed off on,and controls to ensure those policies areadhered to.

Just how far the board should go is anopen question, the discussion on whichhas only just begun. We would say that, inthis new world of greater governance andresponsibility of boards, greaterinvolvement than we currently have seendoes seem appropriate. In this regard,involvement in ensuring there is anappropriate risk management frameworkand policy in place, that it fits in with theorganisation’s overall attitude to riskmanagement and that a process forensuring that this is functioning asintended, would be an important placeto start.

The CEO and CFO

Historically it has been the CFO whorepresents tax at board level and to whommost heads of tax report. However we areseeing pressure in some countries forCEOs to become more actively engagedin the tax area – whether because of theneed to sign off on accounts or fromexternal pressures (e.g. the above debatebeing initiated at CEO level by theAustralian Tax Office). We have thereforecombined these two positions in terms of stakeholder consideration – whilstrecognising that more of the responsibilityfor tax risk management will likely fall onthe shoulders of the CFO than the CEO.

The points discussed above concerningthe board’s involvement in tax riskmanagement obviously apply to the CEOand CFO as members of the board.However their interest in tax riskmanagement will go further. The CEO andCFO, having had high level input into thestrategy design, should be using it as aframework for participating in significanttax related decisions both on thetransactional side and possibly also on the operational side.

They clearly have an interest in thefigures in the accounts and hence infinancial accounting risk. They may even be personally at risk if majorrestatements or prior year adjustmentsarise in the accounts.

They are also responsible for monitoringhow tax risk is being managed and howthe tax department is performing (taxmanagement risk). We come back to thepoint that in today’s environment it isimportant that the leadership view of thetax function’s risk profile is consistent withpractice. Where there is a disconnectthere can be surprises for the CEO andCFO from adjustments to the accounts ormissed tax savings, and frustrations onthe part of the tax function wheninformation provided or resourcesallocated are not sufficient to achieve therisk management targets established.

Virtuouscircle

Tax riskshigh on

managementagenda

Tax riskidentified and

communicated

Appropriatetax resource

1. What level of confidence do you havein the correctness of your advice?

2. How likely is it that the tax office willtake a different view of the applicationof the law and assess the companyaccordingly?

3. If the Australian Tax Office takes adifferent view and the matter proceedsto litigation, what is the risk of theFederal Court or the High Court decidingthe matter in favour of the tax office?

4. What is the potential downside if thecompany is unsuccessful in litigationwith the tax office?

5. If there is a dispute, what is the likelihoodof the tax office being prepared to settlethe dispute and, if so, on what terms?

6. How likely is it that the tax office willidentify the tax issues that arise fromthe proposed course of action? Alliedwith that, to what extent will embarkingon the proposed course of actionincrease the tax risk profile of thecompany and increase the possibilityof audit scrutiny?

7. In light of the potential risk, would itbe desirable to approach the taxoffice for guidance in the form of aprivate binding ruling

8. Where a position has been taken on atax issue, would it be desirable, in theinterests of appropriately managing anyrisk, to be up front with the tax office inidentifying the issues before or whenlodging the tax return and endeavouringto constructively handle anydisagreements which may ensue?

9. Is the advice based on the actualtransaction or on an expectation ofhow the transaction will beimplemented?

10. Are you satisfied that the factual basisfor your opinion to the board has beenproperly checked?

In this context the AustralianCommissioner posed 10questions boards should beasking in this area:

14 Tax Risk Management

The head of tax and his/her team

Obviously the tax function is responsiblefor managing the majority of tax outcomes,and the actions and activities that createtax risk. It is also the first point of contactin tax risk management. What therefore arethe head of tax’s objectives in relation totax risk management? Do they buy in tothe concept that tax risk can be managed?How do their objectives on riskmanagement fit in with those set out bythe chief risk officer? What framework isused to measure risk and does the taxfunction participate in developing thescores? Is the head of tax trying to make aname for themselves by taking risk – or dothey come from the ‘no surprises’ schoolwhere tax risk management is aboutavoiding potentially contentious oraggressive positions? How secure do theyfeel in their jobs? Will they now be signingoff, to the CEO or CFO, that the tax figuresin the accounts are acceptable – and if thegroup is SEC listed, also on the internalcontrols over tax?

Whilst the board will agree the strategy, inpractice it is the head of tax who will setthe whole tone on tax risk managementfor the rest of the organisation – whetherit is the tax team doing the tax returns orthe advice and support provided tooperational and other teams doing theirjobs. It is therefore vitally important thatthe head of tax, CEO and CFO, and theboard are in agreement on the group’s taxrisk management policy.

The one area where we see some gaps iswith MNC’s foreign subsidiaries. In manycases tax is the responsibility of the localCFO in the foreign subsidiary with indirectline responsibility to the head of tax. Inthese circumstances there is a real risk thattax risk management is falling between thecracks and it is important that clearresponsibilities are established. This pointis explored in more detail in a later chapter.

The head of tax will, or should, beinvolved in all areas of tax riskmanagement. However they will usuallyhave prime responsibility for the

management risk – ensuring that the rightpeople are in place to manage tax,ensuring these people have the rightskills, and ensuring that the appropriateprocesses and procedures are in place.

But however good the tax riskmanagement policy of an organisation isand however much leadership anddiscussion there is at board level, thehead of tax and his/her team will deliverwhat they are being measured on. Thisbegs the question as to what are theymeasured on – and what are theconsequences for them personally if,having taken a risk, revenue authoritiestake different positions or imposearbitrary adjustments.

We would encourage those settingobjectives for tax functions to build taxrisk management into such objectives –and to identify acceptable levels of risk(whatever that might be for thatorganisation) in order to add value to thebusiness. Once risks have been taken, taxfunctions will need support if things gowrong – and praise when things go well.We will look at how tax risk managementcan be monitored in a later chapter.

Business units and functional areas

The interest in the management of taxrisks by the other business units andfunctional areas of the organisation willvary based on the broader managementand risk profile of the organisation. For example, the level of interest bymanagement of a business unit will beclosely aligned with whether the unit ismeasured on a pre-tax or after-tax basis.The business unit’s accountability forinformation provided to the tax function (orresponsibility for transaction taxes withinthe unit) will also drive the level of interest.In a similar manner the legal departmentwill need to understand where thebusiness sits on transactional risk. Thetreasury department will want to knowwhat tax is payable – and what tax mightbe payable if some of the risks taken doactually crystallise. This may include bothtransactional risk and compliance risk. The

business planning team may well bedealing with forecasting, both of taxcharges in the accounts and cash goingout of the business.

The finance department will nearly alwaysplay a key role because it is impacted bytax in many ways. Its own responsibilitiescan vary from managing expectationsaround the effective tax rate throughprocessing the results of operationalactivities to full responsibility for tax inforeign jurisdictions. The financedepartment is nearly always involved in theimplementation of significant transactionsand will also often be involved in producingdetailed information for the tax returns –how much detail does it need to go into,what level of materiality is appropriate fordifferent tax returns? In all these areas itwill need to understand the full range ofthe tax risk profile of the business.

To do their job properly internal auditorswill need to understand the group’sposition on tax risk. This is applicable toany role they may have in monitoringcontrols or in reviewing the tax function.Historically we believe that internalauditors may have found reviewing the taxfunction as one of those items that goes inthe ‘too specialised’ basket. Perhaps thiswill have to change. Indeed where internalaudit functions undertake broader reviewsof the tax function, which we have seen in a small number of cases, they can help raise the profile of the tax function by highlighting where the tax function isadding value to the business.

Moving away from the functional areas ofa business to the operational people wecome to people who are responsible formaking decisions with potentiallysignificant tax implications. This is theoperational tax risk area, and the questionarises as to whether operational peopleunderstand what risks they are taking,when they need to consult, when they canact without consulting – and whathappens when something goes wrong? Inbusinesses that are measured on a profitbefore tax basis, operational people will

Tax Risk Management 15

often be more focused on sales taxes and payroll taxes and will often ignorecorporate income taxes. This in itself is a risk – tax management risk.

This brief list skims the surface of themany potential interactions between taxand the different areas of yourorganisation – which other functionalareas are making decisions that have atax impact and hence carry tax risk? Ifthese people are to take responsibility forthe tax impact of their actions they needto understand both where the risk areasare and how they are expected to managetheir tax risks. You need to be able toanswer the question below.

Who are the tax riskmanagement internalstakeholders in yourbusiness?

External auditors and other externaladvisors

Let us now consider the stakeholdersoutside your organisation. The externalauditors clearly have an interest in agroup’s tax risk policy. They need tounderstand both the policy and whererisks are being taken so they can plantheir audit of the financial accounts. Wewould suggest the auditors have aninterest in all seven of the areas of tax risk.

One of the effects of the currentcorporate governance concerns is thatsome groups are not using the taxdepartments of their auditors as muchas they used to for tax planning advice.Where the auditors are not the taxadvisors to the company, they will haveless familiarity with the client’s taxaffairs. This is likely to be particularlysignificant where the group has, forexample, made large acquisitions ordisposals, undertaken new financingarrangements, implemented a groupreorganisation, or implemented taxmitigation strategies. As a result the

auditors will require more time and effortto understand where the risks lie andthe implications for them in reachingtheir opinion on the financial statements– with corresponding additional costsfor the group concerned.

This leads on to the point as to the board’sand the audit committee’s view of usingtheir audit firm for tax work. Differentbusinesses have taken different views here.Our view is that the audit firm is generallythe best placed provider of both taxplanning and tax compliance services.There is a strong linkage between acompany’s accounts and its tax affairs thathas led to the audit firm generally alsoproviding tax services to its audit clients.The audit firm will have a deepunderstanding of the company’s businessand therefore generally be best placed toprovide related tax services. Additionally,the tax charge will generally be a materialcomponent of the company’s profit and lossaccount and therefore needs to be carefullyconsidered by the auditor. This process ismade easier where the audit firm providestax services on an ongoing basis; with itsdeep involvement with the company thisleads to a better quality audit. It thereforefollows that we believe that the company’smanagement of its tax risk is improved bythe involvement of its auditors in theprovision of tax services as opposed to theprovision of such services by others.

In addition to issuing an opinion on thefinancial statements, there are specificrequirements for auditor attestation ofinternal control procedures over financialreporting for SEC registered clients (asrequired by Section 404 of Sarbanes-OxleyAct of 2002). As with the necessity toconsider the impact of the tax accounts onthe financial statements, the internal controlsapplicable to the tax accounts will need tobe considered in the attestation on acompany’s internal controls over financialreporting. These requirements will first apply,broadly, for accounting periods ending on orafter 15 November 2004 for US registrantsand 15 July 2005 for non-US registrants.The Public Company Accounting OversightBoard (PCAOB) rules, which govern theaudits of internal controls over financialreporting, will also have a significant impacton both auditors and registrants.

External advisors, who may or may not beyour auditors, need to understand yourappetite for tax risk. This will help them todeliver more appropriate advice and filterout unsuitable ideas they might be thinkingof bringing to you. They will also need tounderstand the accounting implications ofwhat they are advising on – this is perhapsmore of an issue for lawyers thanaccountants, but still a point to beconsidered if the advisor is not the auditor.

The understanding of the corporateappetite for risk is particularly importantfor tax advisors in foreign jurisdictionswhere tax in these jurisdictions is often theresponsibility of the finance functions. Inthese circumstances local risks and issuesneed to be understood and tax riskpolicies adapted to local circumstances. In some cases policies that do not have tobe enunciated at home may need to beoverseas, to ensure that different culturalcircumstances and local practices do notinadvertently breach corporate policy.

16 Tax Risk Management

Revenue and other regulatory authorities

Tax authorities are taking an increasinglysophisticated approach to tax riskmanagement. If they can be clear wherethe tax risks are in any organisation theywill know where to focus their resources.

The Australian Tax Office has, for example,published a list of seven criteria they usewhen assessing an organisation’s tax riskprofile and listed the six key areas they aregoing to focus on. The seven criteria forrisk assessment are:

• Business and transactions

• Globalisation

• Attitude

• Systems of compliance

• Perceptions of stakeholders

• Materiality

• Application of the law

For each category they rate the business,and from this they can build up a pictureof the organisation they are looking at.With this analysis they are focusing on thefollowing questions to decide howdetailed a review they need to do.

• Whether the group’s financial or taxperformance varies substantially fromindustry norms?

• Are there significant variations in theamounts or patterns of tax payments?

• Are there unexplained variationsbetween economic performance,productivity and tax performance?

• Are there unexplained losses, loweffective tax rates, and cases wherepart or all of the group consistentlypays low tax?

• Is there a history of aggressive taxplanning?

• Are there weaknesses in the group’sstructure, processes and approachesto tax compliance?

Additionally a number of revenueauthorities are keen to discuss a group’srisk assessment with that organisationand discuss with them which areas willcome under particular scrutiny this year ornext. The US authorities have moved to avery specific series of regulations requiringspecific identification and disclosure oftransactions that they (the authorities) viewas giving an indication of aggressive orinappropriate tax positions. The UK InlandRevenue instigated a specific initiativeentitled ‘Spend to Save’ that particularlyfocused on where their resources shouldbest be concentrated to achieve maximumrevenue raising benefit. They have nowannounced a crackdown on tax avoidanceby introducing a package of measurestargeted at perceived loopholes, in additionto specific anti-avoidance legislation.

The issue here is not to be undulyinfluenced by either aggressive or dormantrevenue activity but rather to build therevenue authorities’ approach andinformation requirements into your riskassessment, strategy and policies. We areaware of some businesses that haveshared their tax strategy with taxauthorities in order to help demonstrate‘lower risks’ than may have otherwise havebeen perceived; however this is not acommon approach.

As well as revenue authorities there are anumber of other regulatory authorities indifferent industries (e.g. financial services)and countries (e.g. in the US, the SEC)that will be interested in the tax risk profileof a business. We have not attempted tolist these out – but are you aware of whichother authorities are looking at yourfigures and possibly also your riskmanagement systems?

Investors and analysts

One of the prime sources of informationfor investors and analysts is the accountsand other quarterly/half yearlystatements. The element of uncertainty in the financial accounts is therefore ofinterest to them – and as such they areinterested in financial accounting tax risk.To the extent that the tax charge tends to fluctuate they will wish to understandwhy this is so and how it might fluctuatein the future. Portfolio tax risk may alsobe of interest to them – is there a highportfolio of tax risk that could causesignificant fluctuations in the tax figuresor is there a small portfolio of risk and asteady tax charge is to be expected?

There seems to be an increasing focus on cash tax as opposed to theaccounting tax charge – the commentsabove are equally relevant to cash tax asthey are to the accounting charge. Finallyreputational tax risk is somethinginvestors will be interested in – what isthe effect on the share price if, forexample, a major revenue investigationbecomes public knowledge?

Tax Risk Management 17

Documentation and communication

A theme that has been running throughthe above discussion is the width ofimpact that taxes and tax riskmanagement has in the organisation andtherefore the importance of documentingpolicies and disseminating them throughan appropriate communication strategy.Word of mouth and informalcommunications are unlikely to beappropriate for such a wide range ofdifferent stakeholders. We will explore thisin more detail in later chapters.

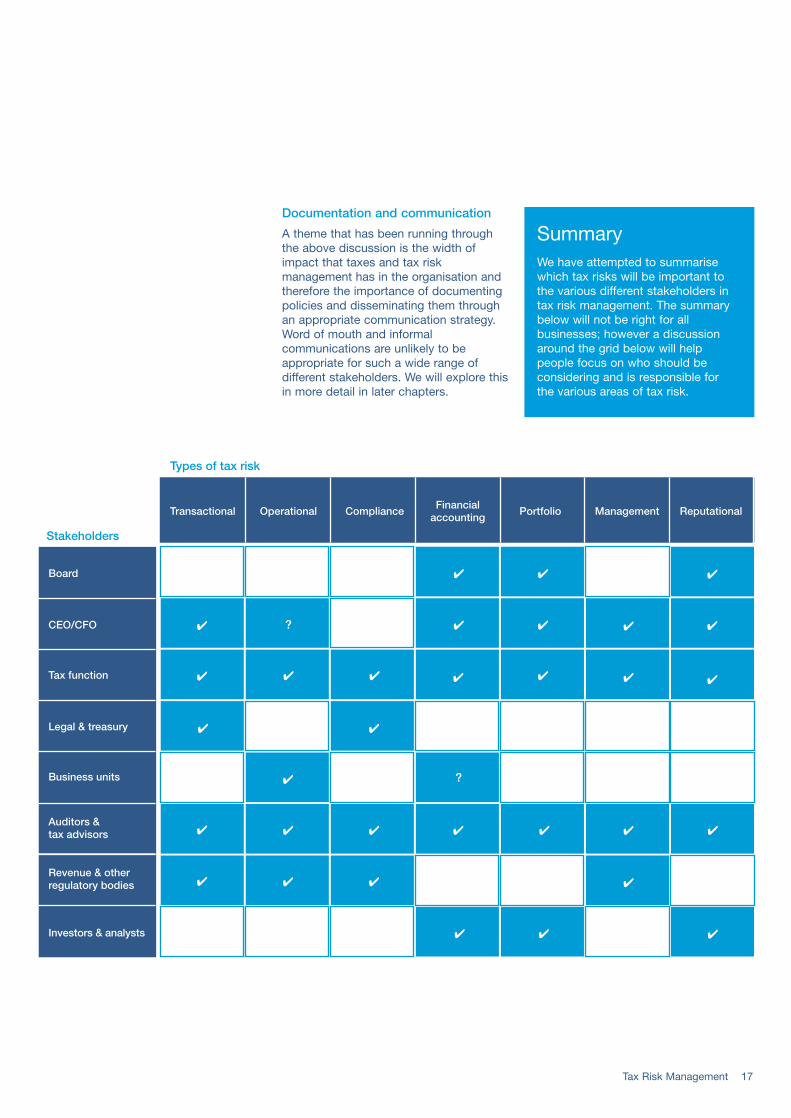

Types of tax risk

Stakeholders

Transactional Operational ComplianceFinancial

accountingPortfolio Management Reputational

Board

CEO/CFO

Tax function

Legal & treasury

Business units

Auditors & tax advisors

Revenue & other regulatory bodies

Investors & analysts

✔

✔

✔

?

✔

✔

✔ ✔ ✔ ✔

✔

✔

✔

✔

✔

✔

✔ ✔

?

✔ ✔

✔ ✔

✔✔

✔✔ ✔✔ ✔ ✔

✔ ✔

✔

SummaryWe have attempted to summarisewhich tax risks will be important tothe various different stakeholders intax risk management. The summarybelow will not be right for allbusinesses; however a discussionaround the grid below will helppeople focus on who should beconsidering and is responsible for the various areas of tax risk.

18 Tax Risk Management

However we can consider how tax riskmanagement fits within an overall taxstrategy. Indeed it is the overall taxstrategy that should drive the approach totax risk management – and not the otherway around.

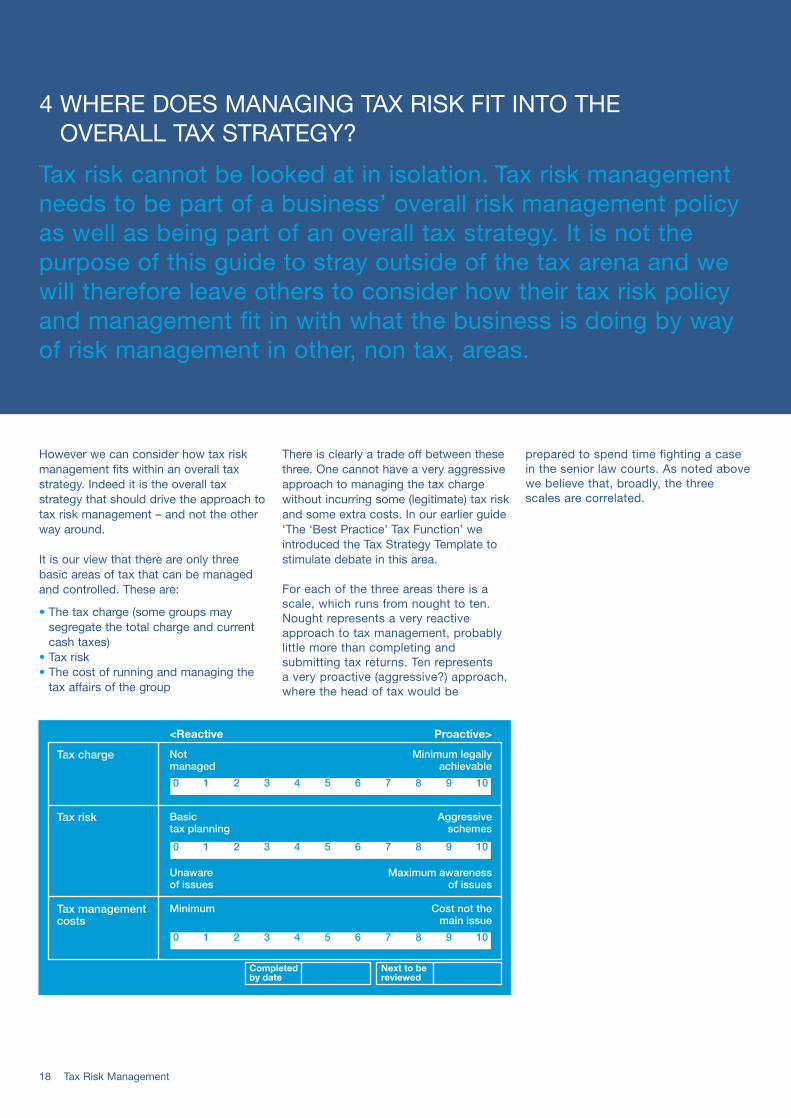

It is our view that there are only threebasic areas of tax that can be managedand controlled. These are:

• The tax charge (some groups maysegregate the total charge and currentcash taxes)

• Tax risk• The cost of running and managing the

tax affairs of the group

There is clearly a trade off between thesethree. One cannot have a very aggressiveapproach to managing the tax chargewithout incurring some (legitimate) tax riskand some extra costs. In our earlier guide‘The ‘Best Practice’ Tax Function’ weintroduced the Tax Strategy Template tostimulate debate in this area.

For each of the three areas there is ascale, which runs from nought to ten.Nought represents a very reactiveapproach to tax management, probablylittle more than completing andsubmitting tax returns. Ten represents a very proactive (aggressive?) approach,where the head of tax would be

prepared to spend time fighting a casein the senior law courts. As noted abovewe believe that, broadly, the threescales are correlated.

Tax risk cannot be looked at in isolation. Tax risk managementneeds to be part of a business’ overall risk management policyas well as being part of an overall tax strategy. It is not thepurpose of this guide to stray outside of the tax arena and wewill therefore leave others to consider how their tax risk policyand management fit in with what the business is doing by wayof risk management in other, non tax, areas.

Tax charge

Tax risk

Tax management costs

Notmanaged

<Reactive Proactive>

Basictax planning

Unaware of issues

Minimum

Minimum legallyachievable

Aggressiveschemes

Maximum awarenessof issues

Cost not themain issue

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 9 10

Next to bereviewed

Completedby date

4 WHERE DOES MANAGING TAX RISK FIT INTO THE OVERALL TAX STRATEGY?

Tax Risk Management 19

To get an overall view of someone’sapproach to their tax strategy, andbecause of the correlation noted above,we ask people to draw a vertical linedown the template giving a singleoverall ‘score’ between nought and ten.The more conservative and reactivegroups would have a lower score thanthose who manage their tax moreaggressively and proactively – and areprepared to take greater tax risks.

This is an overview tool. It’s not meant tobe a ‘scientifically perfect’ model of a taxfunction’s strategy. It’s a tool that helpsclarify opinions as to overall approachand start discussions that draws outsome of the underlying issues.

The overall score above should bearsome correlation to the summary scorearrived at in the last section of thesecond chapter of this guide. (This wasthe scale that summarised yourorganisation’s overall attitude to tax riskmanagement.) If the two scores are notclose together one of them needsrevisiting. As both scales are part ofyour overall group tax strategy, in termsof best practice, both should be agreedwith the board and getting the twoscores the same should be achievable.

Tax charge

Tax risk

Tax management costs

Notmanaged

<Reactive Proactive>

Basictax planning

Unaware of issues

Minimum

Minimum legallyachievable

Aggressiveschemes

Maximum awarenessof issues

Cost not themain issue

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 9 10

Next to bereviewed

Completedby date

20 Tax Risk Management

The COSO Internal ControlIntegrated Framework

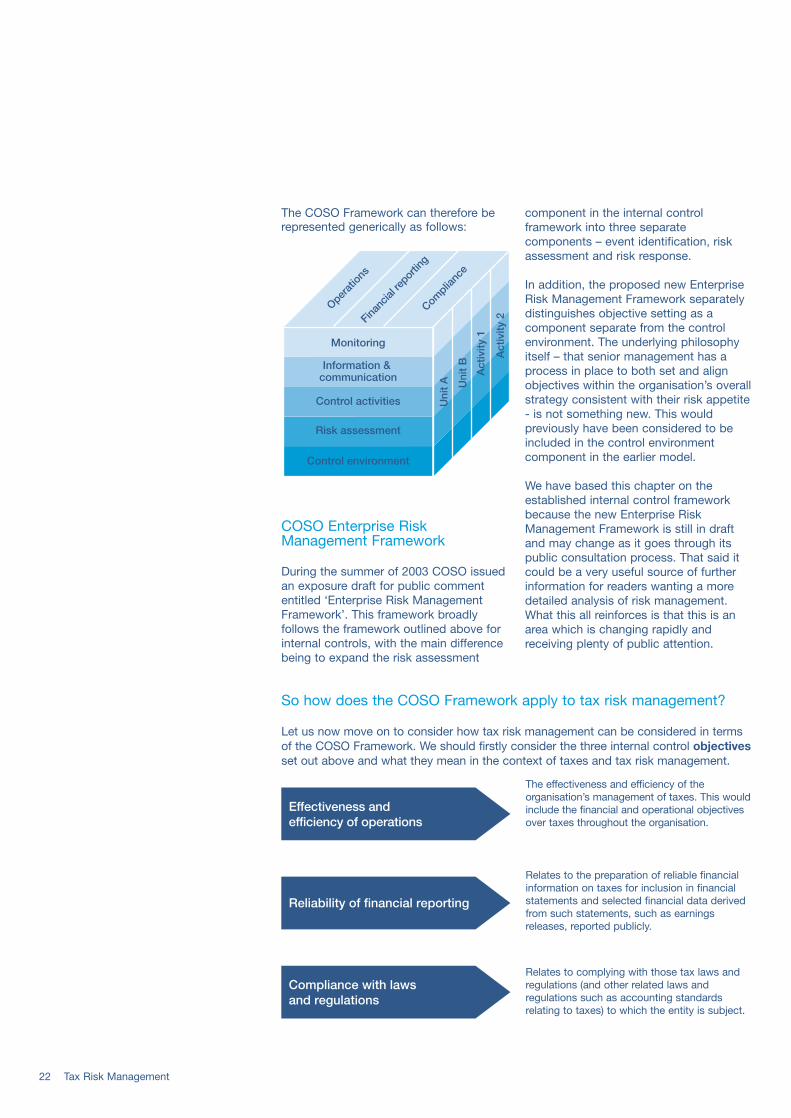

In the early 1990s the Committee ofSponsoring Organisations of theTreadway Commission (COSO), set up in the US, called for a study to developa framework for internal control and in1992 the Internal Control – IntegratedFramework was published. Today themost widely recognised internationalstandard for an integrated framework ofinternal control is the COSO Framework.We have sought in this chapter firstly to explain how the COSO Frameworkoperates and more importantly how itmight be used to manage tax risk.

What is internal control?

The COSO Framework defines internalcontrol as:

“A process, effected by an entity’s boardof directors, management and otherpersonnel, designed to provide reasonableassurance regarding the achievement ofobjectives in the following categories:

• Effectiveness and efficiency ofoperations;

• Reliability of financial reporting; and

• Compliance with applicable laws andregulations.”

The commentary around the COSOFramework explains that whilst internalcontrol is a process that will change anddevelop over time, the effectiveness ofan organisation’s internal control is astatement of the condition of thatprocess at one or more points in time.The purpose of internal control is to helpan organisation achieve its performanceand profitability objectives, andsafeguard assets. It can also help toensure reliable financial reporting,compliance with laws and regulationsand therefore avoid damage to itsreputation and other consequences. As the COSO Framework is the leadingmodel for internal control, and is beingused on a global basis, it seems anappropriate model to consider for tax riskmanagement.

The early chapters of this guide have focused on what is tax riskand who should be interested in it. We have looked, at a highlevel, at how a tax risk policy fits into the overall strategy of abusiness. It is time to look in a bit more detail as to how tax riskcan actually be managed and what processes might be put inplace to achieve this – and introduce an internal controlframework for tax risk management. This chapter focuses ondesigning a systematic approach to tax risk management, andthe following chapter then looks at how to make the systematicapproach work in practice.

5 THE RISK MANAGEMENT CONTROL FRAMEWORK FOR TAX

INTERNAL CONTROLINTEGRATEDFRAMEWORK

COMMITTEE OFSPONSORINGORGANISATIONS OFTHE TREADWAYCOMMISSION

Tax Risk Management 21

Components of internal control

The current COSO Framework sets outfive interrelated components in anintegrated system of internal control thatapplies to organisations of all types andsizes – and hence should equally applyto tax risk management. The fivecomponents are:

• Control environment

• Risk assessment

• Control activities

• Information and communication

• Monitoring

Let us look at these in a generic sensebefore going on to look at them specificallyin terms of tax risk management.

Control environment

The control environment is the overalltone of an organisation – the culture andatmosphere of the organisation in whichpeople conduct their activities and carryout their responsibilities, and theseriousness with which risk andcompliance with controls and processesis taken. The control environment isbased on the individual attributes andattitudes of the senior management ofthe organisation – and will reflect theirintegrity, ethical values, competence andauthority. The control environment is afoundation for all the other componentsof internal control and is the nature of theplatform on which the whole organisationis built. If risk management is notimportant in an organisation and peopledo not take processes and controlsseriously then introducing specific riskpolicies, procedures and controls in anarea like tax, may have little chance ofbeing effective.

Risk assessment

This is the awareness and response of anorganisation to the risks that it faces.Processes and procedures will need to beestablished to identify, evaluate andmanage those risks. Risk objectives mustbe set that are integrated with the rest ofthe organisation.

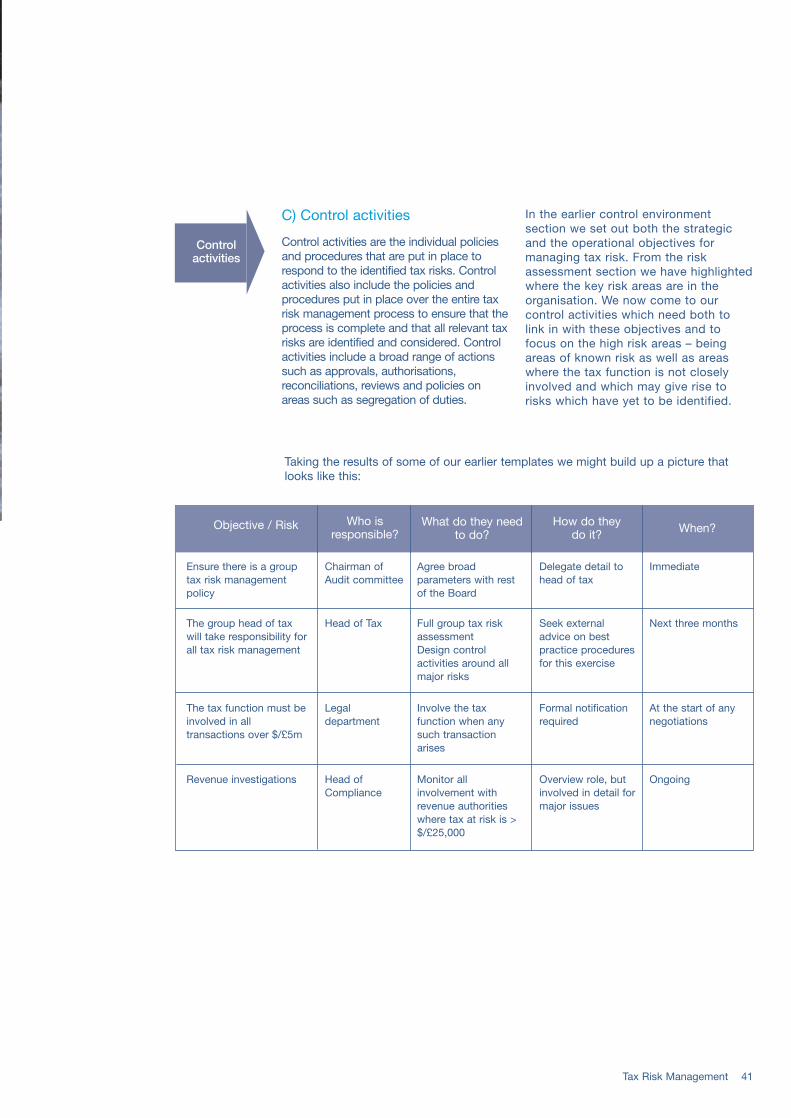

Control activities

Control activities are the policies andprocedures that are designed andoperate in order to manage and addressthe risks to the achievement of anorganisation’s objectives. These controlactivities need to be effective in theiroperation in order to manage and mitigatethe risks consistent with the overallobjectives of the organisation.

Information and communication

Information and communication systemsare required to support the other fourcomponents in order to ensure thepeople in an organisation understand,capture, exchange and record theinformation needed to manage andcontrol risk in an organisation.Information and communication is alsoneeded to assess how the organisationis performing and whether its goals andobjectives are being achieved.

Monitoring

The entire process, but particularlycontrols and processes, must bemonitored to assess their effectivenessand to identify where modifications orremedial actions are necessary. Monitoringallows early identification of deficienciesso that the internal control system can beresponsive to changing conditions bothwithin and from outside the organisation.

Each of these components can and willimpact and influence each of the othercomponents. The extent to which anorganisation implements these componentswill vary from business to business and willbe influenced by many different factors.However, these five components should beidentifiable in any integrated system ofinternal control for tax risk managementand should be embedded throughout theorganisation in order to be effective.

There is a direct relationship betweenthese five components and the threecategories of objective set out earlier inthe definition of internal control. The fivecomponents are what an organisationneeds to have in place and be operatingeffectively, in order to achieve each of thethree objectives throughout all activitiesand business units in the organisation.

22 Tax Risk Management

The COSO Framework can therefore berepresented generically as follows:

COSO Enterprise RiskManagement Framework

During the summer of 2003 COSO issuedan exposure draft for public commententitled ‘Enterprise Risk ManagementFramework’. This framework broadlyfollows the framework outlined above forinternal controls, with the main differencebeing to expand the risk assessment

component in the internal controlframework into three separatecomponents – event identification, riskassessment and risk response.

In addition, the proposed new EnterpriseRisk Management Framework separatelydistinguishes objective setting as acomponent separate from the controlenvironment. The underlying philosophyitself – that senior management has aprocess in place to both set and alignobjectives within the organisation’s overallstrategy consistent with their risk appetite- is not something new. This wouldpreviously have been considered to beincluded in the control environmentcomponent in the earlier model.

We have based this chapter on theestablished internal control frameworkbecause the new Enterprise RiskManagement Framework is still in draftand may change as it goes through itspublic consultation process. That said itcould be a very useful source of furtherinformation for readers wanting a moredetailed analysis of risk management.What this all reinforces is that this is anarea which is changing rapidly andreceiving plenty of public attention.

Act

ivity

2

Act

ivity

1

Uni

t B

Uni

t A

Operat

ions

Finan

cial r

epor

ting

Complia

nce

Monitoring

Information & communication

Control activities

Risk assessment

Control environment

So how does the COSO Framework apply to tax risk management?

Let us now move on to consider how tax risk management can be considered in termsof the COSO Framework. We should firstly consider the three internal control objectivesset out above and what they mean in the context of taxes and tax risk management.

Effectiveness and efficiency of operations

Compliance with laws and regulations

Reliability of financial reporting

The effectiveness and efficiency of theorganisation’s management of taxes. This wouldinclude the financial and operational objectivesover taxes throughout the organisation.

Relates to the preparation of reliable financialinformation on taxes for inclusion in financialstatements and selected financial data derivedfrom such statements, such as earningsreleases, reported publicly.

Relates to complying with those tax laws andregulations (and other related laws andregulations such as accounting standardsrelating to taxes) to which the entity is subject.

Tax Risk Management 23

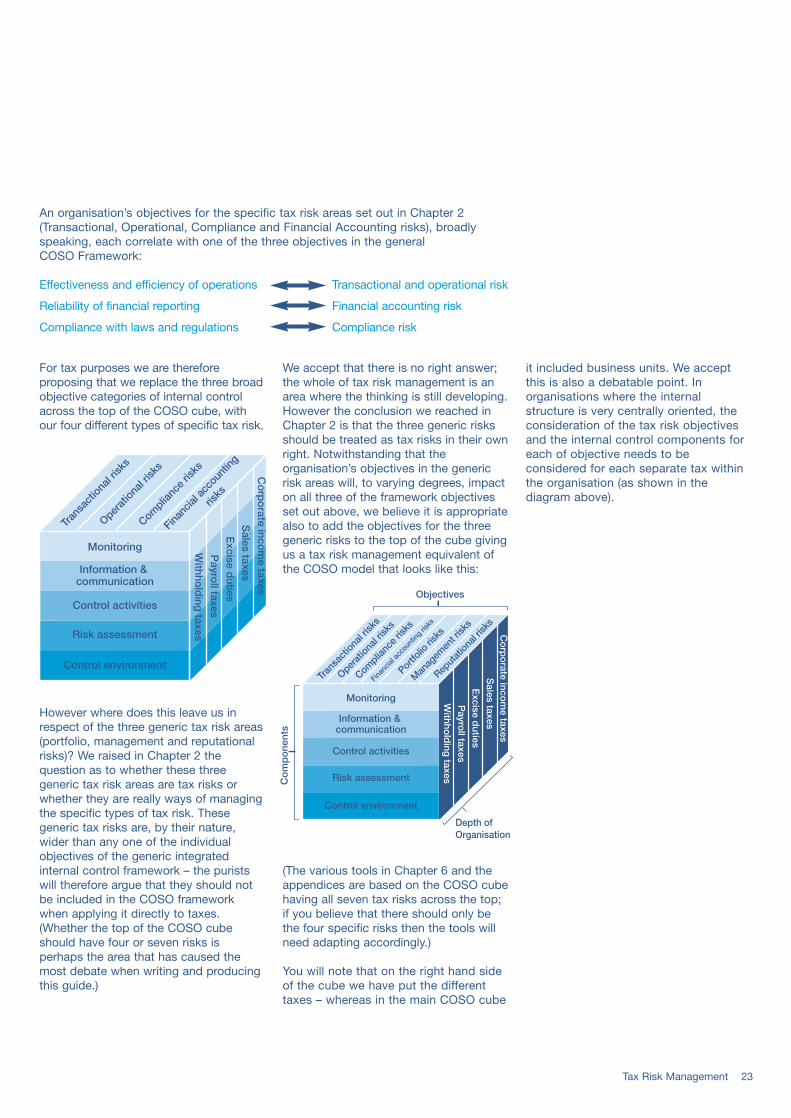

For tax purposes we are thereforeproposing that we replace the three broadobjective categories of internal controlacross the top of the COSO cube, withour four different types of specific tax risk.

However where does this leave us inrespect of the three generic tax risk areas(portfolio, management and reputationalrisks)? We raised in Chapter 2 thequestion as to whether these threegeneric tax risk areas are tax risks orwhether they are really ways of managingthe specific types of tax risk. Thesegeneric tax risks are, by their nature,wider than any one of the individualobjectives of the generic integratedinternal control framework – the puristswill therefore argue that they should notbe included in the COSO frameworkwhen applying it directly to taxes.(Whether the top of the COSO cubeshould have four or seven risks isperhaps the area that has caused themost debate when writing and producingthis guide.)

We accept that there is no right answer; the whole of tax risk management is anarea where the thinking is still developing.However the conclusion we reached inChapter 2 is that the three generic risksshould be treated as tax risks in their ownright. Notwithstanding that theorganisation’s objectives in the genericrisk areas will, to varying degrees, impacton all three of the framework objectivesset out above, we believe it is appropriatealso to add the objectives for the threegeneric risks to the top of the cube givingus a tax risk management equivalent ofthe COSO model that looks like this:

(The various tools in Chapter 6 and theappendices are based on the COSO cubehaving all seven tax risks across the top;if you believe that there should only bethe four specific risks then the tools willneed adapting accordingly.)

You will note that on the right hand sideof the cube we have put the differenttaxes – whereas in the main COSO cube

it included business units. We acceptthis is also a debatable point. Inorganisations where the internalstructure is very centrally oriented, theconsideration of the tax risk objectivesand the internal control components foreach of objective needs to beconsidered for each separate tax withinthe organisation (as shown in thediagram above).

Withho

lding

taxes

Payro

ll taxes

Excise d

uties

Sales taxes

Co

rpo

rate incom

e taxesTr

ansa

ctio

nal r

isks

Operat

iona

l risk

s

Complia

nce

risks

Finan

cial a

ccou

nting

r

isks

Monitoring

Information & communication

Control activities

Risk assessment

Control environmentTr

ansa

ctio

nal r

isks

Operat

iona

l risk

s

Complia

nce

risks

Finan

cial a

ccou

nting

risk

s

Portfo

lio ri

sks

Man

agem

ent r

isks

Reput

ation

al ris

ks

Monitoring

Objectives

Co

mp

one

nts

Information & communication

Control activities

Risk assessment

Control environment

Withho

lding

taxes

Payro

ll taxes

Excise d

uties

Sales taxes

Co

rpo

rate incom

e taxes

Depth ofOrganisation

Effectiveness and efficiency of operations Transactional and operational risk

Reliability of financial reporting Financial accounting risk

Compliance with laws and regulations Compliance risk

An organisation’s objectives for the specific tax risk areas set out in Chapter 2(Transactional, Operational, Compliance and Financial Accounting risks), broadlyspeaking, each correlate with one of the three objectives in the general COSO Framework:

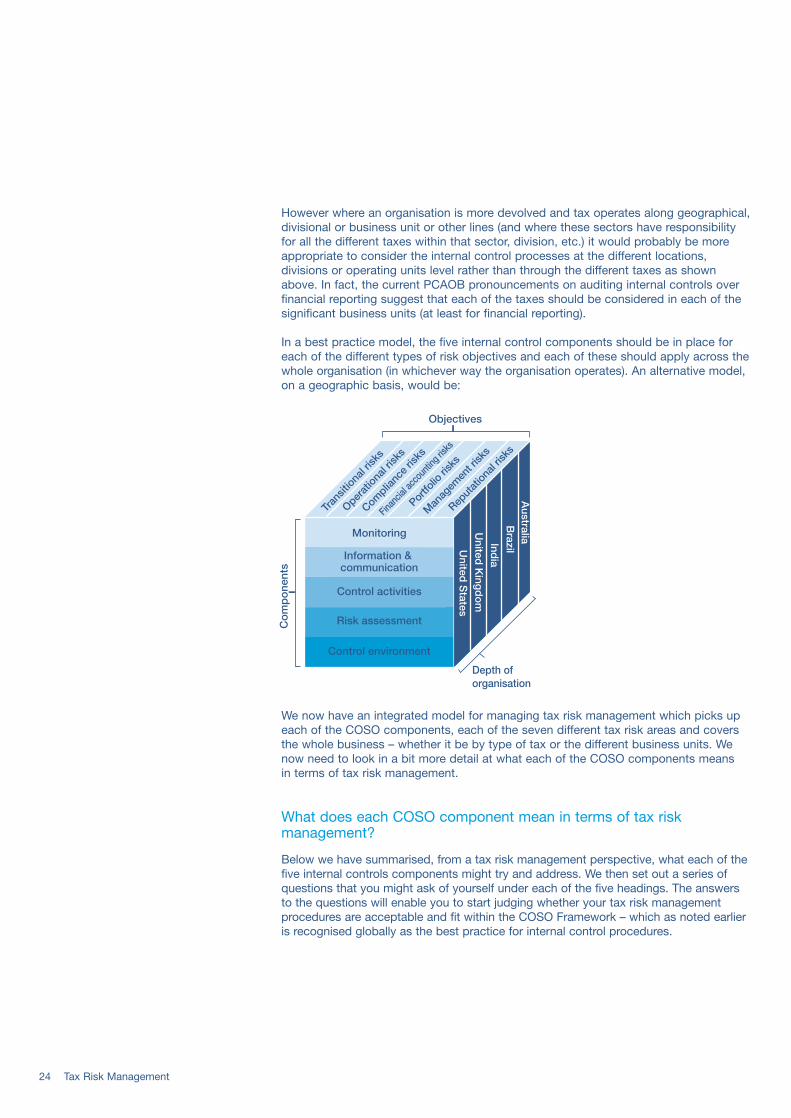

However where an organisation is more devolved and tax operates along geographical,divisional or business unit or other lines (and where these sectors have responsibilityfor all the different taxes within that sector, division, etc.) it would probably be moreappropriate to consider the internal control processes at the different locations,divisions or operating units level rather than through the different taxes as shownabove. In fact, the current PCAOB pronouncements on auditing internal controls overfinancial reporting suggest that each of the taxes should be considered in each of thesignificant business units (at least for financial reporting).

In a best practice model, the five internal control components should be in place foreach of the different types of risk objectives and each of these should apply across thewhole organisation (in whichever way the organisation operates). An alternative model,on a geographic basis, would be:

We now have an integrated model for managing tax risk management which picks upeach of the COSO components, each of the seven different tax risk areas and coversthe whole business – whether it be by type of tax or the different business units. Wenow need to look in a bit more detail at what each of the COSO components means in terms of tax risk management.

What does each COSO component mean in terms of tax riskmanagement?

Below we have summarised, from a tax risk management perspective, what each of thefive internal controls components might try and address. We then set out a series ofquestions that you might ask of yourself under each of the five headings. The answersto the questions will enable you to start judging whether your tax risk managementprocedures are acceptable and fit within the COSO Framework – which as noted earlieris recognised globally as the best practice for internal control procedures.

24 Tax Risk Management

Tran

sitio

nal r

isks

Operat

iona

l risk

s

Complia

nce

risks

Finan

cial a

ccou

nting

risks

Portfo

lio ri

sks

Man

agem

ent r

isks

Reput

ation

al ris

ks

Monitoring

Objectives

Co

mp

one

nts

Information & communication

Control activities

Risk assessment

Control environment

United

States

United

King

do

m

India

Brazil

Australia

Depth oforganisation

Tax Risk Management 25

1 Control environment

This is the attitude and culture of the board and senior management towards tax riskand their overall strategy and objectives for tax risk. This will include their commitmentto tax risk management, the degree to which tax risk policies are set and communicatedand the level of accountability for achieving and monitoring the performance of thosepolicies. This also includes consideration of the compensation ‘driver’ for the taxfunction and their overall position within the organisation.

The types of questions that need considering under this heading are:

• What influence does tax risk have when the organisation’s overall strategy andobjectives are being established?- Is tax risk considered side-by-side with other business risks in evaluating proposals

and making decisions about achieving the organisation’s goals?

• What is the organisation’s tax risk appetite/tolerance - where on the tax risk spectrumis it and where does it want to be? - What is the organisation’s approach, management style and attitude to tax risk –

what is its risk culture?

• How does the board of directors manage tax risk?- Is there a written and agreed tax risk policy and methodology?- How are the board’s strategy and objectives with regard to tax risk and tax risk

management delegated, communicated and embedded with the people throughoutthe organisation?

- Is the board’s policy understood throughout the organisation?- How do senior management ensure their policies and objectives are met – how do

they assess to whom responsibility is delegated and that responsibility is passed tosufficiently competent and experienced personnel?

• How do senior management assess whether the organisation is in compliance withtheir strategy and objectives on tax risk management?- Is information on tax risk management and measurement of achievement against

objectives gathered and regularly reviewed by senior management? - How do senior management respond to new tax risks and weaknesses or

deficiencies over tax risk management? - Do senior management demonstrate their commitment to their tax risk management

philosophy and strategy in their everyday activities?

• How do the compensation policies and organisation structure of the tax departmentsupport or conflict with the fundamental goals of the organisation?

Controlenvironment

26 Tax Risk Management

2 Risk assessment