Embed Size (px)

Citation preview

1

Tax Sale Riches Introduction

Investing in Tax Liens and Tax Deeds the Easy Way

2

Copyright © 2013 Mike Warren

http://misuniversity.com

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, recording or otherwise, without the prior written permission of the author.

3

DISCLAIMER AND TERMS OF USE AGREEMENT The author and publisher of this Ebook and the accompanying materials have used their best efforts in preparing this Ebook. The author and publisher make no representation or warranties with respect to the accuracy, applicability, fitness, or completeness of the contents of this Ebook. The information contained in this Ebook is strictly for educational purposes. Therefore, if you wish to apply ideas contained in this Ebook, you are taking full responsibility for your actions.

EVERY EFFORT HAS BEEN MADE TO ACCURATELY REPRESENT THIS PRODUCT AND IT'S POTENTIAL. EVEN THOUGH THIS INDUSTRY IS ONE OF THE FEW WHERE ONE CAN WRITE THEIR OWN CHECK IN TERMS OF EARNINGS, THERE IS NO GUARANTEE THAT YOU WILL EARN ANY MONEY USING THE TECHNIQUES AND IDEAS IN THESE MATERIALS. EXAMPLES IN THESE MATERIALS ARE NOT TO BE INTERPRETED AS A PROMISE OR GUARANTEE OF EARNINGS. EARNING POTENTIAL IS ENTIRELYDEPENDENT ON THE PERSON USING OUR PRODUCT, IDEAS AND TECHNIQUES. WE DO NOT PURPORT THIS AS A “GET RICH SCHEME.”

ANY CLAIMS MADE OF ACTUAL EARNINGS OR EXAMPLES OF ACTUAL RESULTS CAN BE VERIFIED UPON REQUEST. YOUR LEVEL OF SUCCESS IN ATTAINING THE RESULTS CLAIMED IN OUR MATERIALS DEPENDS ON THE TIME YOU DEVOTE TO THE PROGRAM, IDEAS AND TECHNIQUES MENTIONED, YOUR FINANCES, KNOWLEDGE AND VARIOUS SKILLS. SINCE THESE FACTORS DIFFER ACCORDING TO INDIVIDUALS, WE CANNOT GUARANTEE YOUR SUCCESS OR INCOME LEVEL. NOR ARE WE RESPONSIBLE FOR ANY OF YOUR ACTIONS.

MATERIALS IN OUR PRODUCT AND OUR WEBSITE MAY CONTAIN INFORMATION THAT INCLUDES OR IS BASED UPON FORWARD-LOOKING STATEMENTS WITHIN THE MEANING OF THE SECURITIES LITIGATION REFORM ACT OF 1995. FORWARD- LOOKING STATEMENTS GIVE OUR EXPECTATIONS OR FORECASTS OF FUTURE EVENTS. YOU CAN IDENTIFY THESE STATEMENTS BY THE FACT THAT THEY DO NOT RELATE STRICTLY TO HISTORICAL OR CURRENT FACTS. THEY USE WORDS SUCH AS “ANTICIPATE,” “ESTIMATE,” “EXPECT,” “PROJECT,” “INTEND,” “PLAN,” “BELIEVE,” AND OTHER WORDS AND TERMS OF SIMILAR MEANING IN CONNECTION WITH A DESCRIPTION OF POTENTIAL EARNINGS OR FINANCIAL PERFORMANCE.

ANY AND ALL FORWARD LOOKING STATEMENTS HERE OR ON ANY OF OUR SALES MATERIAL ARE INTENDED TO EXPRESS OUR OPINION OF EARNINGS POTENTIAL. MANY FACTORS WILL BE IMPORTANT IN DETERMINING YOUR ACTUAL RESULTS AND NO GUARANTEES ARE MADE THAT YOU WILL ACHIEVE RESULTS SIMILAR TO OURS OR ANYBODY ELSES, IN FACT NO GUARANTEES ARE

4

MADE THAT YOU WILL ACHIEVE ANY RESULTS FROM OUR IDEAS AND TECHNIQUES IN OUR MATERIAL.

The author and publisher disclaim any warranties (express or implied), merchantability, or fitness for any particular purpose. The author and publisher shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental or other consequential damages arising directly or indirectly from any use of this material, which is provided “as is”, and without warranties.

As always, the advice of a competent legal, tax, accounting or other professional should be sought.

The author and publisher do not warrant the performance, effectiveness or applicability of any sites listed or linked to in this Ebook.

All links are for information purposes only and are not warranted for content, accuracy or any other implied or explicit purpose.

This Ebook is © copyrighted by Mike Warren/misuniversity.com and is protected under the US Copyright Act of 1976 and all other applicable international, federal, state and local laws, with ALL rights reserved. No part of this may be copied, or changed in any format, sold, or used in any way other than what is outlined within this Ebook under any circumstances without express permission from Mike Warren/misuniversity.com

5

ContentsI. Introduction .................................................................................... 6

II. Tax Liens and Tax Deeds ................................................................. 4

III. Getting Involved in Tax Liens .......................................................... 6

IV. Getting Involved in Tax Deeds ......................................................... 7

V. Investing the Right Vehicles.............................................................. 8

VII. Right of Lien Holder..................................................................... 10

IX. Buy the Certificate ....................................................................... 12

X. Wrap ........................................................................................... 14

XI. How To Learn More ..................................................................... 16

Important Terms............................................................................... 17

6

I. Introduction

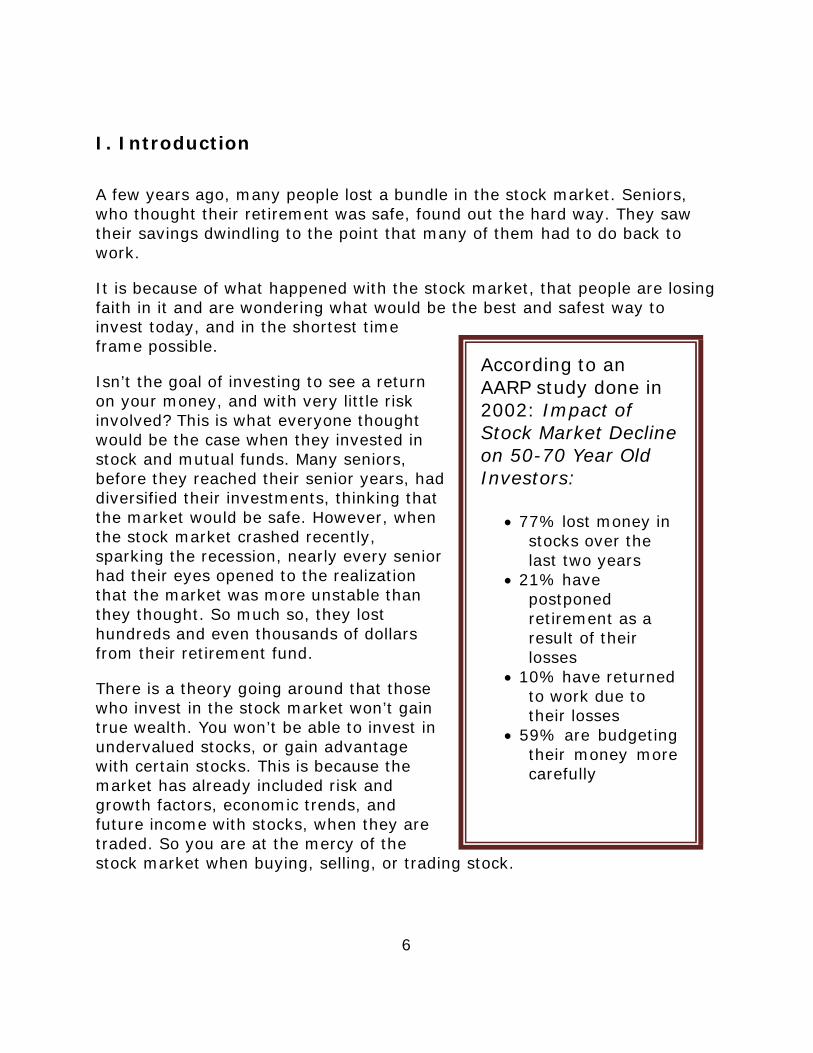

A few years ago, many people lost a bundle in the stock market. Seniors, who thought their retirement was safe, found out the hard way. They saw their savings dwindling to the point that many of them had to do back to work.

It is because of what happened with the stock market, that people are losing faith in it and are wondering what would be the best and safest way to invest today, and in the shortest time frame possible.

Isn’t the goal of investing to see a return on your money, and with very little risk involved? This is what everyone thought would be the case when they invested in stock and mutual funds. Many seniors, before they reached their senior years, had diversified their investments, thinking that the market would be safe. However, when the stock market crashed recently, sparking the recession, nearly every senior had their eyes opened to the realization that the market was more unstable than they thought. So much so, they lost hundreds and even thousands of dollars from their retirement fund.

There is a theory going around that those who invest in the stock market won’t gain true wealth. You won’t be able to invest in undervalued stocks, or gain advantage with certain stocks. This is because the market has already included risk and growth factors, economic trends, and future income with stocks, when they are traded. So you are at the mercy of the

According to an AARP study done in 2002: Impact of Stock Market Decline on 50-70 Year Old Investors:

77% lost money in stocks over the last two years

21% have postponed retirement as a result of their losses

10% have returned to work due to their losses

59% are budgeting their money more carefully

stock market when buying, selling, or trading stock.

2

It is because of the way the stock market works that we have no control over certain events. However, there are so many people who didn’t fully understand the way the market worked, got involved with the idea that investing heavily would put them on the road to riches. At first they did make a good deal of money. But when the market crashed, they lost money as well.

Since the stock market is too risky and unstable, investors need a sure thing that they can put their money into that will guarantee them a bigger chance of return.

Some people like to go into real estate investing. But the idea of being a property manager scares off some investors. Buying one property may be okay, but when an investor buys more than one property, the idea of managing those properties becomes a stressful proposition.

To some investors, the idea of owning a lot of properties just caused them a lot of headaches. The amount of money invested in the properties was one thing, but when you take into account the addition of money for maintenance, property taxes, vacancies, and income taxes, just simply deterred many away from the idea.

The idea of collecting money from tenants, having to advertise for tenants, doing background checks to ensure good tenants, and dealing with bad tenants, just wasn’t my cup of tea.

There is a better way of investing that doesn’t have these hassles. Plus it is a part of a secret government program that guarantees you a high rate of

Difference in Investing:

Stockholders do own a part of the company. But their ownership is limited. They are risk takers and don’t make much on company dividends. And they are not secured creditors. Therefore, during bankruptcy, they are paid last.

Tax Lien Investors become secured creditors when they purchase the lien. In this position they can foreclosure on the property they hold a lien to.

3

return (rates of 16%, 36% even 50% per year on your money). This way is referred to as tax lien investing. If you play your cards right and do the right type of research, you can own property at and get a high rate of return on your invested funds. Or, if you rather, you can own the property at a deep discount. Here is another way of looking at this: you either get the rate of return (rates of 16%, 36% even 50% per year on your money) or you end up getting the property free and clear of all debt including mortgages and IRS tax liens.

If you are considering becoming a tax lien investor, you need to think about this point for a second. You can still make money investing in lease options, owner carried notes, and flipping. But the true safe way to make passive income is by way of property tax liens. The reason property tax liens are so safe is because they are secured to the property that the lien is tied to. And the reason they are lucrative is because you have first claim to the property. So if it were sold at foreclosure, you would get paid first before any other liens did. This means you can either get a nice sizable return on your investment, or you are given the rights to the property.

What I really love above tax lien investing is that you don’t need a lot of money. In fact, there have been cases of where tax liens were purchased for as little as $10, while on the other side of the spectrum, investors have paid

well over $100,000.

Property Tax Liens: A claim imposed by the federal government to liquidate a person's property until the tax and debt owed is fully paid.

Not all states issue tax lien certificates. Some states handle delinquent property taxes by offering actual properties or deeds, at their county tax sales. This means participants actually bid on properties rather than certificates. In states where deeds are offered, the property owner is generally three to five years overdue in paying his or her taxes. However, in many deed states there is a redemption period during which the property owner can redeem the deed and property from the owner who has previously taken title and possession of the property.

4

The great opportunity in tax lien certificates lies in purchasing them for your own investment portfolio. When purchasing them for yourself, you can take one of several different approaches:

First, you can use tax liens as a means of earning a guaranteed rate of

interest on your money. Second, you can use tax liens to acquire properties. With this strategy, you

seek to acquire attractive properties whenever possible, hold them a while, then sell them for a profit. By carefully selecting tax liens that are expected to go into foreclosure, you may earn many times your original investment this way.

Finally, you can use tax liens as leverage. For example, you can use them as collateral for obtaining a loan from a lending institution. Then, you use the loan to purchase more certificates. Or, you can assign the certificates to someone else as a down payment for other property or real estate in your area that you want to purchase.

Before deciding whether to get involved in tax lien investing, I would like to present you with some details as to the difference between a tax lien and tax deed, as you will encounter both forms while you do your research.

II. Tax Liens and Tax Deeds

The first thing you need to know is what is a tax lien. Here is a definition of a tax lien: A claim imposed by a governmental body to liquidate a person's property until the tax and debt owed is fully paid.

When someone owns a piece of property and he fails to pay his property taxes, the government takes and uses their legal right to the money, and files a claim against the property owner. When this is done, the government imposes a lien on the property.

Tax liens can be imposed by the state, county, city or town, school district, or any government entity that is allowed by statutes to levy taxes.

When a lien is placed against a property, the government has a way of getting the back taxes. They do this by way of a tax sale. Sometimes this sale is referred to as a “tax lien sale,” “tax auction,” or “tax certificate sale.” To summarize, in a tax lien state the lien is an encumbrance right or enforcement right held by the county where the property is located. The lien grants the lien holder the right to receive interest penalty charges if the lien is not paid off by the delinquent property owner and it also give the lien

5

holder the right to foreclose on the tax lien and take full title to the property if the lien is not paid.

The best part of the tax lien is that the tax lien is in first position on the property ahead of the mortgage and any other debts.

Now you have an understanding of tax liens, now let’s turn our attention to tax deeds. What is a tax deed?

When property taxes have not been paid by the date due, they become delinquent. The local tax office sends a notice to the property owner of such delinquency and gives the owner time to pay the taxes owed. This time is known as the redemption period.

If the owner fails to pay the taxes owed by the due date, the tax office sends notice to the owner and a claim is filed, whereby the tax office becomes the new property owner. Then the tax office offers the property for sale at a public auction.

Tax deed sales are a great way to obtain property at a discounted price. The discounted price will depend on how much the property is worth and the taxes owed.

Currently, there are a number of states that deal in tax deeds. These states include Arkansas, Alaska, California, Florida, Idaho, Kansas, Maine, Michigan, Nevada, New Mexico, New York, North Carolina, North Dakota, Ohio, Oregon, Pennsylvania, South Dakota, Utah, Virginia, Washington, and Wisconsin.

The states that deal in tax liens include Florida, Nevada, New York, and Ohio.

Redemption Period: This is the time allotted to the property owner, where he can pay his debt, before a lien holder can foreclose. The redemption period varies from state to state. It could be six months to three years. The longer the redemption period is the more interest accrues for the lien holder. If the property owner does not pay the back taxes plus the penalty then you get the property free and clear regardless of the market value of the property.

Every state offers a tax sale. The tax sale could be a tax lien or a tax deed. If it is a tax lien sale, the owner has a chance to redeem his property. When

6

the sale is final with no ability of the owner to get the property back, this is known as a tax deed sale.

III. Getting Involved in Tax Liens

If you get involved in a tax lien sale, you will be buying the right of the taxing authority to receive interest, penalties, and costs. You also get to

obtain security in your investment should the homeowner redeem the property. If the homeowner doesn’t redeem the property in Foreclose: To

foreclose means that the lien gives the lien holder the right to claim the property as his own in final settlement of the original debt.

time, you, as tax lien holder, will receive the right to acquire the property. As a tax lien holder, any other liens, whether they are judgment liens, mortgage liens, trust deeds, or even private liens (contractor sues homeowner for nonpayment of work done), are wiped out if you foreclosure on the property and take possession of it.

Another factor about property tax liens is

that since they are much smaller than the market value of the property, the investment is very secure. Plus, when you actually purchase the lien, you are not assuming responsibility for any land liability, since you are not taking ownership in the property.

On the plus side, purchasing a tax lien can be lucrative for you. The rate of return can be as high as 50%.

Keep in mind that when you are the winning bidder at a tax lien auction, you are not winning the property. You are simply buying the taxing authorities rights, and are taking on the responsibility of paying all delinquent taxes including interests and penalties that have accrued at that time of sale. The law stipulates that common folks like you and me, from all across the world, have the right to come in and pay the delinquent taxes on behalf of the property owner or purchase the actual property as a way for the local government to collect overdue property tax revenues.

The amount you end up paying in your bid will include the amount of delinquent taxes, interest, penalty fees, legal costs, and administrative fees.

The actual tax sale may be held monthly, every six months, or once a year, depending on the city, town, or state.

7

If after you purchase the tax lien, and the property owner decides to come

forward and pay what is owed, he has to pay you, the lien holder, not only all that you paid at the auction, but also interest that has accrued as well. This interest could be anywhere from 16% to 50%.

This means you get all the money you spent at the auction, plus the interest penalty charge. This amount of money can be large, depending on length of delinquency and amount of taxes owed.

Tax liens are relatively safe. The interest is mandated by the State Legislature and assured by the county government.

They provide good leverage. When you buy a certificate, you automatically become the senior lien-holder on the property. (In some counties, your lien may be co-equal with that of other taxing agencies, and in a very few states, an IRS lien may be superior to a property tax lien.) You can control thousands of dollars worth of property simply by paying the back taxes that are due.

They offer a high yield. You can earn up to 50 percent interest plus any penalties that have accumulated, depending on the state in which the property is located.

No negotiations are required. You and the property owner never come face-to-face to negotiate. The state and county handle the transaction.

Tax benefits. The money you earn investing in tax lien certificates could be tax- exempt or tax-deferred if you buy the certificates through a retirement fund or an IRA. Also, if you buy tax lien certificates as a business, you may be able to deduct typical business expenses on your income tax return.

IV. Getting Involved in Tax Deeds

As a real estate investor, if you are going to get involved in buying a tax deed, your goal is to buy the properties for as little as you can. Once you obtain the property, you can turn it around and sell the property at a high price. This is how you make a profit from the property.

Keep in mind that when you bid on a property, if you do end up being the winning bidder, you will end up owning the property.

There are two types of tax deed sales to be aware of:

8

1. The taxing authority sells the property for a starting bid that includes

the taxes owed, penalties, interests, and costs.

2. The taxing authority sells the property for a minimum bid that is a percentage of the market value of the property.

If the property is being sold because the back taxes were not paid, the starting bid will be the total of taxes owed plus penalties, interests, and other costs. However, if the taxing authority foreclosed on the property already and owns the property, the minimum bid will be based on a percentage of market value.

It would be to your advantage, before getting involved in tax deeds or tax liens, to get professional help, especially if you are new to tax liens and deeds. If you make the wrong move, it could cost you.

A key to success, and we have heard this from our students all around the world, is professional guidance. Having someone who has already been there and know the ins and outs of what to expect, what to watch out for and how to avoid all the landmines, and even how to do the entire business virtually (meaning you can invest in tax liens from anywhere in the world using your computer), made the difference between failure and success.

V. Investing the Right Vehicles

Your biggest concern before going to the auction sale is to know the property you are going to bid on. If you end up winning the bid, you will own the property. As such, you should spend a good deal of time researching the properties so you know what you are getting.

You may not be a financial wizard, but think about this fact. It doesn’t take rocket science to figure that if you put $3000 into a retirement account at 1.5% interest a year, at 25 years of age, by the time you reach 65, you will have accumulated $121,800.

However, if you were to buy into tax liens at 20% interest compounded yearly, and you bought one tax lien at age 25, which resulted in $3000 in your pocket, by the time you retired at age 65, your investment would be well over one million dollars.

9

Do you see the difference? And what is even better is that the money you

make from your tax lien sales can be put into your retirement account so you don’t pay taxes on it. The IRS allows you to invest in tax liens using your retirement accounts.

The effect of compounding interest of 20% each year as compared to simple interest at the rate of 1.5% each year is an enormous difference. You will see that for yourself when you get involved in tax liens.

Albert Einstein – “The most powerful force in the universe is compound interest”

What would be even better for you is if you were able to foreclose on each property you had a tax lien on. Then you turned around and sold that property for a large amount. You just made a huge profit from that home.

Let’s look at an example. You bought a tax lien for $50. You held on to it for a year. You found out at the last minute the owner of the property died. No one in the family paid the back taxes. The day for redemption came and went. You have been told you can now claim the property. So you place the property in foreclosure. The property becomes yours. You then sell it for $50,000. You just made $49,950 profit.

Here is another example. Let’s say you go to an auction that sells tax deeds. You learn the property has already been foreclosed on and the city is selling the property for $25,000. You are the winning bidder. You end up paying the money. You did a lot of research and found the property was worth $250,000. The property was in excellent shape. The homeowner just lost his job and could no longer pay the taxes.

You take the property and sell it for $220,000. Since you paid $25,000 for the deed, you just made $195,000 profit. Do you see how lucrative buying tax deeds and tax liens can be?

Why invest in the stock market that has proven to be very risky, when you can put your money into something that really presents low risk. When you buy a tax lien, you are purchasing a ‘safety net.” This is something the stock market doesn’t provide.

VI. Doing Proper Research

10

The key to making money with tax liens and even with tax deeds is by doing proper research. This is extremely important. Why? You don’t want to go to an auction, pay $20,000 for a deed to a property and find the house is about to fall apart. That wouldn’t be good for you. But if you did your research and found the property is really solid with no major problems, and the neighborhood is really decent, you may choose to invest in this property.

How do you find properties that are in good shape and are worth investing in? You need to know the location of the property you want to purchase. When you know that you can take the next steps to obtain the lists of properties for that state or county.

You can get the list by the following means:

1. Contact the county you are interested in. Each county usually has a

website.

2. If you live nearby, go to the tax office and pick up a list. If you don’t live near the tax office, contact them and ask for the list to be mailed to you. You may have to pay for shipping and handling.

3. Check the local papers. Most county offices are required by state law

to post the auction date and all liens available.

4. Purchase the list from a listing service. While this option is costly, it is the quickest and most efficient way to purchase lists for several counties at once.

Tax liens are different. You can’t see the property ahead of time. But you can learn about the property and where it is. Then you can research the property and find out if there are any other liens on the property that may survive foreclosure. Normally, there are no other liens that survive foreclosure, but there are exceptions.

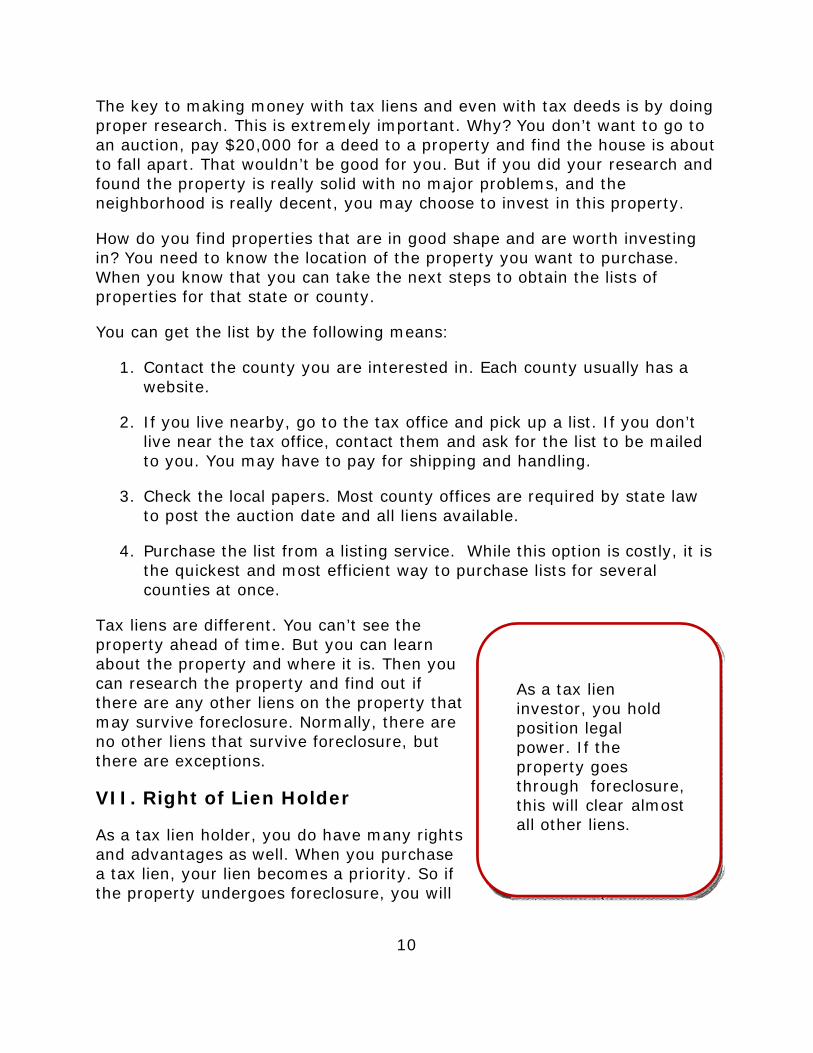

VII. Right of Lien Holder

As a tax lien holder, you do have many rights and advantages as well. When you purchase a tax lien, your lien becomes a priority. So if the property undergoes foreclosure, you will

As a tax lien investor, you hold position legal power. If the property goes through foreclosure, this will clear almost all other liens.

11

get paid first. Plus, by holding a first position tax lien, the foreclosure will clear almost all other liens from the title.

Plus, you get to claim legal right to the property. This legal right only happens to you when you go into foreclosure. Before that time, your only obligation is to own the tax lien certificate. And when you own just the tax lien certificate, you don’t have any responsibility or liability toward the property. This is the same in all states except for one. Only one state gives the tax lien investor actual possession of the property when the tax lien is purchased.

Another advantage of the tax lien holder is regarding payment of tax lien. As a tax lien holder, you don’t have to get involved in the collection process. Many states or counties will not only handle receipt of the taxes for you, but if you decide to pursue a foreclosure of the property, they will handle this for you as well. The bottom line is you don’t have to worry about having contact

with the owner or delinquent tax payer.

With every tax sale there are usually tax liens left over after the auction, since not all are sold. When investing, make sure the lien has a value of no more than 10% of the property. Also, make sure you know the property ahead of time.

If the property owner has up to three years to redeem his property, and at the end of the second year he hasn’t paid for the second year taxes either, the tax lien holder has the legal right to have those taxes added to the bill. This way, if the taxpayer were to come forward and agree to pay all back taxes, he would have to pay for two years taxes, plus interest, plus, penalties, plus, the interest the tax lien holder requests. What this means is you have first right of refusal on future tax bills from the delinquent homeowner. This means get additional tax liens without hardly lifting a finger. VIII. Sales Opportunities

As a tax lien investor, there are so many opportunities for you to buy tax liens and make money with them. In some cases, more than 20,000 tax liens have been auctioned off in the past. This number can fluctuate, but the idea is that when you attend a tax sale, bring plenty of money, or make arrangements ahead of time for financing, because you may just end up purchasing a lot of fantastic deals.

12

I remember one tax investor went to a tax sale and ended up spending about $20,000 dollars. He bought about 20 tax liens that day. A year later, he ended up foreclosing on five of them, and ended up making a good deal of money on the interest for 10 of them. He really cleaned up nicely.

And what is even more interesting is that even after the auction sale is over, there are a ton of properties that didn’t get sold. One investor realized this, so he contacted the tax office, and bought a few of those tax liens through the mail. Some states refer to buying tax liens in the mail as buying them “over the counter.” Imagine doing the entire business over the internet or through the mail. It does not get any better or safer than having the government guarantee your profit.

IX. Buy the Certificate

You can buy tax liens a number of ways, depending on your state's particular rules. Below are the most common ways to purchase them.

A u c t ion

The first way is to attend an auction, where they are first offered to the public. Some states hold auctions once a year; others hold them every month. These times are well advertised in local and regional newspapers.

The bidding procedure for the auction varies depending on the state. Below are the most common ways to bid for certificates.

1. Bidding down interest rates

This involves bidding the interest rate down. This form of bidding starts at the maximum percentage amount and then is bid down to a point where the lowest bidder successfully obtains the bid. Some bids are taken down to 0 percent on property that has little chance of the taxes being paid but has a high potential market value.

2 . B i d d i n g d o w n p e r c e n t o w n e r s h i p

This involves bidding down the percent ownership in the property the investor is willing to accept if the property is not redeemed. The bidding always starts at 100 percent, but the percentage may be lowered through successive bids of 95, 90, 80, 70, 50 percent, etc. It is not uncommon for investors to accept a 25 or 30 percent ownership in a property they might

13

receive. In recent years, many investors have bid down to 1 percent, or a very small fraction of 1 percent, ownership in the hopes the property owner will redeem and pay a high rate of interest. (Caution: The ITV ratio will increase quite rapidly with this form of bidding.)

3. Bidding up premiums

This involves bidding the price of the certificate up. If you bid up the price, you pay more for the property, but you earn a higher interest rate. The premiums over and above the tax levy and interest may not be recoverable. However, premiums are usually very small percentage increments above the lien amount. If the interest rate on the certificate is high enough, it is a worthwhile investment. (Caution: The ITV ratio will increase quite rapidly with this form of bidding.)

4. Lottery

This involves the buyer being allowed to purchase liens in an order determined through either a round-robin or random drawing process. Although many counties allow this technique, it is illegal in most states because it denies the property owner the advantage of competitive bidding prescribed by state law.

5. Rotational bidding (or “round robin” bidding)

In this form of bidding, bidders draw numbers at random, or numbers are issued based on a "first come — first serve" basis determining their rotational position. Position number one gets first refusal on a lien. If he or she does not want the property, then position number two is solicited. The lien paper goes down the list until someone in the rotation wants that particular lien paper. The process starts all over again with the second and subsequent liens.

6. Random Lottery

14

With this form of bidding, the sale is handled through random drawings.

If you attend a tax lien certificate auction, get a feel for the process at first. Wait until you feel confident about the process before you bid. Be careful not to get caught up in the excitement of the auction. Instead, prepare for the auction and know precisely which properties you want to bid on and what price you want to pay.

7. Tax Collector’s Office

The second way to buy tax liens is to wait until after an auction has been held and visit the appropriate county office to inquire about certificates that were not sold. (You can do this on any working day.) If you decide to buy a certificate, the county Tax Collector simply hands the certificate to you, and you keep it in your possession just like you would any other receipt.

8. Purchase from Another Investor

The third way to buy certificates is to purchase them from another tax lien investor. Buying tax liens may tie up an investor's money for one, two, or three years. If the investor changes his or her mind and needs cash right away, you can negotiate to buy those certificates at a discount.

X. Wrap

There can be some risks involved when investing in tax liens. However, if you do your research, you can minimize this risk. And with investing in tax liens, you have no invested interest in the property, at least until you take it over by foreclosure (remember the county does this for you), if that should happen.

If you play your cards right, you can actually take advantage of tax liens that have redemption periods that have expired. By acquiring these properties, you can make a profit off of them quickly.

If you are looking to get a nice return on your investment, investing in tax liens is the way to go. If you like to acquire property that you can use or

15

sell, tax deeds are the way to go. It depends on your strategy and which direction you wish to pursue.

As a tax lien investor, you will profit from the tax lien no matter what happens to the property. And if you use your head, you will gain even more, by going after property that is less likely to be redeemed like vacant lots or homes that don’t have a mortgages attached. However, homes with people living in them and that do have mortgages does have value as well.

Don’t let anyone fool you. Investing in tax liens or tax deeds are a better investment choice than going after unstable stock options that Wall Street sells.

It’s better than a lot of real estate strategies.

It is a virtual business.

It can be done by mail.

You have first lien position on the property for the ultimate protection.

And best of all your return is guaranteed by the government.

Stick with a sure thing and you will find you will gain financially in the near future and long-term as well. Tax lien investing is a strategy that will last a lifetime and has consistent and predictable results. Avoid the stress of other investment vehicles and focus on tax liens. You will be forever grateful that you did.

I have taught thousands of people from all across the world including (but certainly not limited to):

United States

Canada

Mexico

United Kingdom

Australia

Singapore

16

Dubai

Ireland

New Zealand XI. How To Learn More

If you liked this report and would like to get 90 minutes of video training on tax liens and deeds including case studies then please sign up for one of our free training webinars. Make sure to bring about 10 sheets of blank paper to take a lot of notes. I will show you how to earn 16%, 18%, 25%$ even 50% per year. I will even show you how to get started for as little as $10.

Visit our website at http://misuniversity.com/

17

Important Terms Assessment The amount of value the county or municipality places on real property.

Auction A selling process whereby the seller offers goods to buyers in an open market. The successful buyer is the one who offers the greatest amount for the goods being sold.

Collateral The property asset that guarantees payment of a tax lien.

Constant A value computed by the county, expressed as a percentage, when multiplied by the market value of the property results in the assessment value of the property.

Deed An official record of true ownership of real property. A deed is recorded with the county in which the property is located.

Early redemption The satisfaction of a tax lien prior to its maturity (usually one year).

Foreclosure An action taken by a tax lien holder against a property that has delinquent taxes to liquidate the property in order to satisfy the lien. This action is usually based on a specific time formula set by the county or state.

Senior lien Establishes top priority for a tax lien to be paid in the event the property is foreclosed or disposed of in a bankruptcy proceeding. May, in some cases, take priority over federal tax liens.

Tax Collector's Office The local county government department responsible for tax assessment, revenue collection, lien auctions, and county foreclosure proceedings. Tax liens that are not disposed in auction may be obtained directly from this county office.

Tax Lien A delinquent notice issued by a county or municipality to owners of real property who have not paid their tax bills within a proscribed time limit.

Title See deed.