Embed Size (px)

Citation preview

CONFIDENTIAL

y o u r t r u s t e d v a l u e a d v i s e r

Taxation by valuation – landholder duty issues and cases

Presented by Michael Churchill

July 2016

Contents

Introduction

What’s in the box?

Taxation by valuation!

The ingredients of an acquisition

The basic financial relationship

What are the assets?

What are the liabilities?

Everything needs to be valued!

If its not land, it’s not dutiable

What is mining and exploration information?

How is information valued?

The legacy of accountants

Page 1

Cases regarding information

Cases regarding portfolio value

Cases regarding top-down approach

Cases regarding goodwill

Conclusion

Introduction

• Ambrose Bierce’s Devils Dictionary (1911) defines litigation as “a machine which you go into as a pig and come out a sausage” and a litigant as “a person about to give up his skin for the hope of retaining their bones”!

• Today we are going to consider :

– The reason why the stamp duty world has been a feast of litigation relating to valuation issues

– The nature of those issues

– The current position arising from the deliberations of the

courts around Australia

• In particular, we will consider some critical valuation issues impacting the amount of landholder duty payable on the acquisition of entities in Australia including:

– ‘Top-down’ v ‘bottom-up’ valuation approaches

– Mining and exploration information

– Portfolio value

– Goodwill

Page 2

What’s in the box?

• Landholder duty seeks to levy duty on the dutiable value of assets within an entity that has been acquired

• The acquirer pays the duty as though the underlying land assets have been directly acquired

• The critical issue is the dutiable value of the land assets

• The acquirer typically does not have particular regard to the value of the underlying assets but rather assesses its bid or purchase price based on the likely future cashflows (or profits) likely to emerge from the assets operating together as a coherent whole

• The Duties Acts however, require the purchaser to consider the

individual values of the assets within the entity.

• The ‘bottom-up’ approach is preferred by the revenue offices whereby the values of those assets which satisfy the definition of land within each of the respective Acts is assessed on a direct, stand-alone basis

• As we will see later in the presentation, the courts have

favoured the ‘top-down’ approach which requires that all of the assets (and liabilities) that are presented by virtue of controlling the equity in the entity are expressly considered and reconciled with the purchase price paid for the entity

• Thus begins the tug of war…

Page 3

Taxation by valuation!

• Really? There is no objective basis for the assessment of landholder duty?

• As there has been no price set or consideration paid in the typical share acquisition, a dilemma arises as to how duty is to be assessed as it must clearly be based on an assessment of market value undertaken by the taxpayer and (frequently) challenged by the revenue office!

Page 4

The ingredients of an acquisition

• Most large business acquisitions will be executed by acquisition of the shares in an entity rather than a sale and purchase of assets

• The entity acquired will typically hold a wide range of assets – only some of which are dutiable:

– Working capital items such as receivables, work in progress, stock, run of mine ore (in mining operations), cash, foreign exchange, and commodity swaps and options

– Non current assets such as plant, leasehold and freehold land, licenses over land, easements, franchise agreements, concessions, mining and exploration information, copyright, trademarks, customer contracts

• The assets within the entity will be funded by a mix of operating liabilities, interest-bearing debt and equity or quasi-equity instruments

• The net value of all assets and liabilities represent the purchase price

• Just like the family-size supreme pizza that was purchased

for $17.50, the sum of the individual components that make up the price cannot be either more or less than the purchase price – that is the effect of the bargain that was struck between purchaser and vendor

• However, unlike the pizza, a company usually comes with debts that mean that the purchase of an entity (by

acquiring 100% of the shares) for $100 might reflect assets of (say) $300 and liabilities of $200 (equals $100)

Page 5

The basic financial relationship

Equity (value of shares)

Debt

Assets (including enterprise value) = +

What are the assets?

Tangible assets (including land)

Assets (enterprise value) = +

Financial assets and working capital items

Identifiable intangible assets

+

Goodwill

+

What are the liabilities?

Provisions for tax, deferred tax and dividends

Debt = +

Creditors, leave provisions and operating liabilities

Short-term interest-bearing liabilities (o/d, leasing)

+

Long-term interest bearing liabilities (bonds, term debt)

+

Everything needs to be valued!

Tangible assets (including land)

+

Financial assets and working capital items

Identifiable intangible assets

+

Goodwill

+

• Market valuation required – in current use and with careful

consideration of the separability of the underlying assets from key

intangibles such as rights to operate the business in its current form

• Market valuation required – in current use and with careful

consideration of the separability of the identifiable intangibles from

the tangible assets – an iterative process

• A residual calculation – after all other sources of cashflows have

been identified and provided we are satisfied that there is indeed

an “attractive force of custom” then goodwill “falls out”

• Being short-term in nature, there is typically little valuation work

required – often the balance sheet with a few adjustments for

recoverability of debtors and market value of stock is all that is

required

If it’s not land, it’s not dutiable

• Taxpayers will prefer an outcome where there is a lower

value of land assets. Some of the assets which create

value but are not land include:

– Goodwill (including the portfolio value which arises

from multiple assets working together)

– Trademarks and other identifiable, customer-related

intellectual property

– Franchise agreements, concession deeds and

intellectual property licenses

– Distribution agreements

– Power purchase agreements, transmission

agreements

– Future income tax benefits

– Relocatable equipment (e.g. power generation

facilities – see Origin v WA Commissioner)

– Mining and exploration information (except in WA)

Page 10

If you can't explain it to

a six year old, you don't

understand it yourself.

What is mining and exploration information?

Page 11

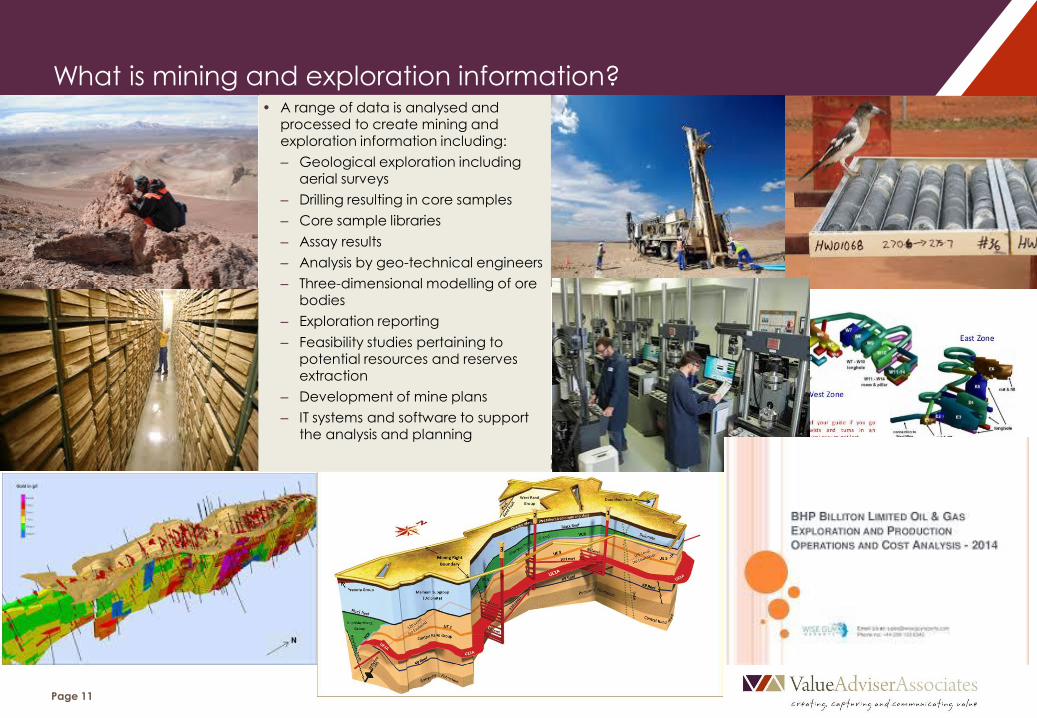

• A range of data is analysed and processed to create mining and exploration information including:

– Geological exploration including aerial surveys

– Drilling resulting in core samples

– Core sample libraries

– Assay results

– Analysis by geo-technical engineers

– Three-dimensional modelling of ore bodies

– Exploration reporting

– Feasibility studies pertaining to potential resources and reserves extraction

– Development of mine plans

– IT systems and software to support the analysis and planning

How is information valued?

• As there is no observable market in information and no directly-attributable cashflow, the IVSC guidelines recommend that a replacement cost methodology be employed

• The more sophisticated approach is ‘deprival’ value which takes into account:

– The current cost of replacing the asset taking into account

– Obsolescence

– Redundancy

– Opportunity costs associated with the time necessary to replace the asset

– Resulting in an optimal, notionally-depreciated replacement cost

• Same methodology is employed in valuing regulatory asset base of utilities such as water, wastewater, transmission, distribution assets which earn revenue from a (regulated) price and ensures a return on capital invested, a return of the capital invested and an allowance for the operational and administrative cost of deploying the asset

• The cases have focussed on:

– Whether information is a separate asset from the tenements to which it relates

– The appropriate methodology by which it should be valued

– Whether an opportunity cost should be allowed

– The possibility that a hypothetical market would see competitive tension in the buyer and seller view of price and

value

Page 12

The legacy of accountants

• We don’t know what it is … so lets call it goodwill!

• The doctrine of conservatism calls for the acquisition price to only ascribe so much of the mineral tenement value to that asset that is supported by current JORC resource and reserve estimates.

• No allowance is made in the accounting allocation for the inevitable fact that the acquirer has taken a probabilistic view on the likelihood that further geological discovery and validation work will result in the ore body expanding beyond its current

resource/reserve estimation

Page 13

Cases regarding information

• The existence of information as an asset separate from the tenements to which it relates was established in Nischu in 1990

• At a Commonwealth tax level, the deductibility of mining and exploration information has enjoyed particular attention having been introduced into tax legislation as an incentive to encourage exploration and development of the nation’s

mineral wealth in the 1970’s

• The Gillard government – in its last budget – announced removal of the ‘immediately deductible’ rule but the ITAA retains the write-off over the life of mining operations

• Information has gained recent attention as a consequence of the TARP (Div 855) legislation which operates in a way very similar to the (old) land-rich legislation. RCF has been a turning point in the valuation discussion. The punch-line from Edmonds’ judgment appears to the right

• Commissioner of Taxation v Resource Capital Fund III LP [2014] FCAFC 37; Resource Capital Fund III LP v Commissioner of Taxation [2013] FCA 363

• Placer Dome Inc. (now an amalgamated entity named Barrick

Gold Corporation) v Commissioner of State Revenue [2015] WASAT 141

• AP Energy Investments Limited and Commissioner of Taxation [2013] AATA 626

• Alacer Gold Corp And Hill 51 Pty Ltd (Formerly Alacer Gold Pty Ltd) And Commissioner Of State Revenue [2016] Wasat 31

• Nischu Pty Ltd v Commissioner of State Taxation (WA) (1990) 90 ATC 4391

Page 14

…(information) value is ascertained by dividing

the notional “bargaining zone” equally. In this way, the hypothetical price of the mining information, as the determinant of its market value, is arrived at as a mid point between the maximum that the hypothetical purchaser, as the owner of the mining tenements, might pay

to acquire the information (being the amount of outlay and the value of loss of cashflow suffered to re-create it) and the maximum the hypothetical vendor of the information could realise from any other disposal of the information (Edmonds, J, RCF 2013)

Cases regarding portfolio value

• Multiple assets working together will often create additional value by virtue of characteristics such as:

– Diversification benefits

– Economies of scale of operation

– Greater market capture by providing customers with georgaphic alternatives

– Brand awareness and prominence

– Exposure to economic factors which may be (partially) negatively correlated between alternative sites

• Where those assets are land-like or satisfy the definition of land it has been proposed that the portfolio benefit should accrue to the value of the land

• Regis makes it clear that the value over and above the market value of the individual asset (such as a nursing home, car parking facilities, petrol station etc) operating as part of a network or portfolio of similar assets is goodwill

• Regis Aged Care Pty Ltd v Commissioner of State Revenue [2015] VSC 279

Page 15

Cases regarding top-down approach

• The courts have favoured a ‘top-down’ approach to the allocation of a purchase price to underlying assets

• As mentioned earlier, the task of the taxpayer is to assess and assign the market value of all the assets acquired via the acquisition of an entity such that the value of dutiable land assets can be determined – in circumstances where there has

been no transaction in the underlying assets and therefore no price determined for those assets

• The price paid for the company is (typically) struck on arms-length principles and via a contest involving more than one party. It therefore represents the most reliable starting point, recognising that the allocation process involves assessments that are somewhat ‘malleable’

• The valuation should ensure that there is an explicit reconciliation between the values of all underlying assets and the purchase price paid for the entity. Whilst not an entirely ‘foolproof’ process, it is more reliable than merely rushing to assess the value of land without reference to the purchase price. In many ways, the top-down and bottom-up approach should achieve the same outcome

• Alacer Gold Corp And Hill 51 Pty Ltd (Formerly Alacer Gold Pty Ltd) And Commissioner Of State Revenue [2016] Wasat 31

• Placer Dome Inc. (now an amalgamated entity named Barrick Gold Corporation) v Commissioner of State Revenue [2015] WASAT 141

Page 16

Cases regarding goodwill

• We have long argued that there is no goodwill in mining operations

• The legal definition of goodwill (the attractive force of custom) makes it clear that the business must possess an attractive force by which revenue and profits are generated

• Homogenous products (e.g. gold and many other commodities) are sold by reference to a chemical composition specification

• Profitability varies according to cost, not by reference to the price at which the product is sold

• Goodwill is often recorded in acquisitions due to a failure in the accounting rules. If the accounting rules mimicked the

approach taken by the acquirers (who ultimately must justify any purchase to the capital markets which make the acquisition possible) then the ‘goodwill’ would be ascribed to the mineral tenements (ore bodies)

• Commissioner of Territory Revenue v Alcan (NT) Alumina Pty Ltd (2008) 156 NTR 1

• Regis Aged Care Pty Ltd v Commissioner of State Revenue [2015] VSC 279

• Origin Energy Power Limited And Commissioner Of State Revenue [2007] Wasat 302

• Placer Dome Inc. (now an amalgamated entity named Barrick Gold Corporation) v Commissioner of State Revenue [2015]

WASAT 141

Page 17

Conclusion

Page 18

• So long as landholder duty is a form of taxation by valuation, there will be a tension between the revenue offices and taxpayers as to the ‘true’ value of land

• The tug of war continues and many issues which are dealt with in the judgments (and therefore create precedents) relate to specific or idiosyncratic issues which must be distinguished on the facts in each case

• The winners:

– Top-down approach

– Portfolio value is goodwill

– (Optimised) replacement cost for valuing information

– No goodwill in mining operations

• The losers:

– Bottom-up approach

– Aspects of the information valuation equation (opportunity cost)

• Jury still out:

– Separability of mining and exploration information and therefore whether it can be excluded from dutiable assets

• A short, shameless promotion for Cambodia Kids Can – an organisation supported by VAA which provides accommodation and education to 40 at-risk girls in Prey Van, Cambodia. All and any contributions gratefully received!

• www.cambodiakidscan.com

Melbourne | Sydney | Adelaide | Hobart | Perth

© 2016 Value Adviser Associates Pty Ltd

www.vaassociates.com.au

Freecall 1800 912226