Embed Size (px)

Citation preview

TB Diagnostics: Global Market Analysis and Potential

Madhukar Pai, MD, PhD McGill University, Montreal, Canada [email protected] September 2012

2

Market analyses are important and necessary

• To support new product development

• To convince industries and investors about the need for investments in new TB tools

• To develop target product profiles (TPPs) that can guide product development and scale-up

• To inform donor/funder decisions

3

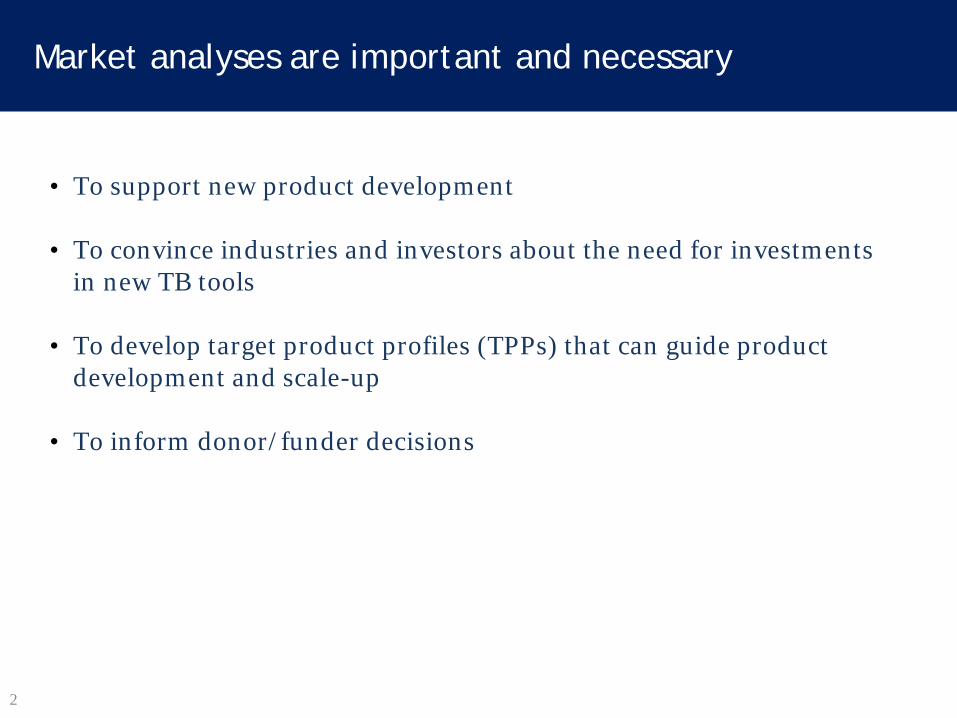

According to the World Health Organization, in 2010, there were ~9 million incident cases of TB Since ~7 - 10 people with TB symptoms need to be screened to detect one TB case, this means 60 - 90 million people get tested for active TB every year ~40% of this happens in India, China and South Africa In addition, there is testing for latent TB infection and MDR-TB

Source: WHO http://www.who.int/tb/publications/global_report/2011/gtbr11_full.pdf

Global TB burden: how many people are screened for TB ever year?

4

By FIND & TDR Published in 2006

Source: FIND http://www.finddiagnostics.org/export/sites/default/resource-centre/find_documentation/pdfs/tbdi_full.pdf

Only one global TB market analysis has been done to date

5

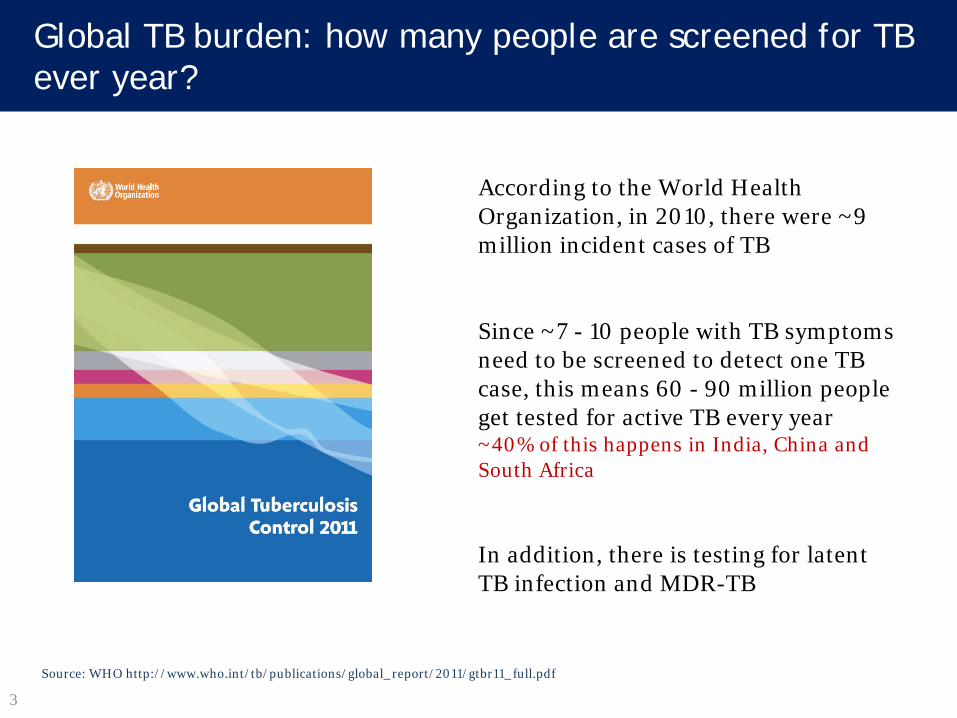

• Annually over US$ 1 billion is spent worldwide on TB diagnostics

• One third (US$ 326 million)

of this money is spent out side of the established market economies (EME),where 73% of TB diagnostic testing takes place

• In EME: latent TB testing (PPD) dominates

• In non-EMEs: active TB

dominates (smears and chest x-rays)

Source: FIND/TDR, 2006

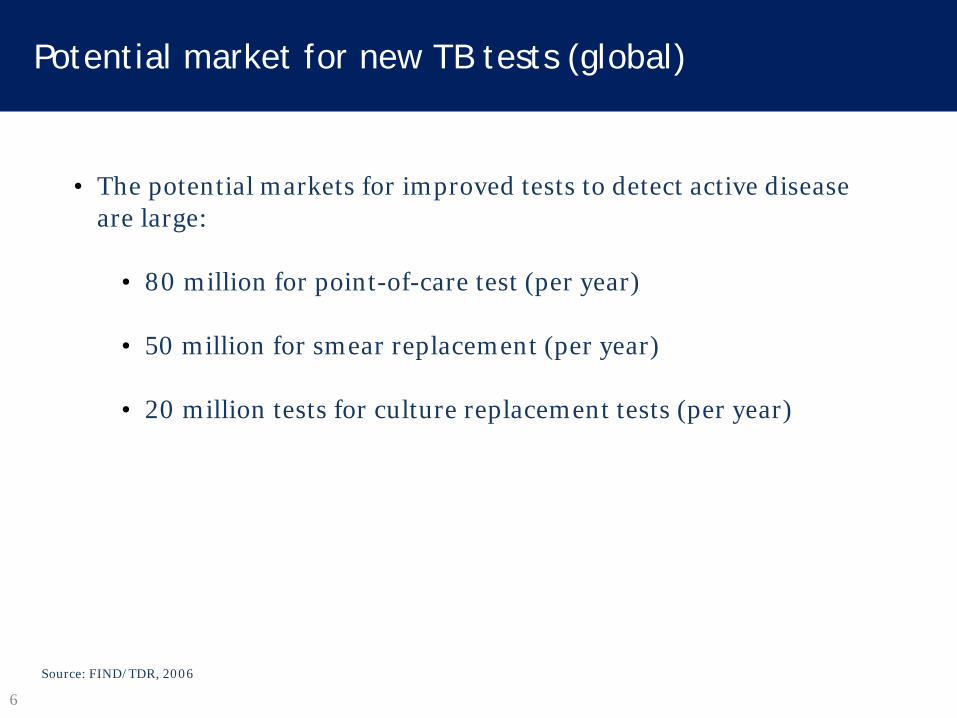

Findings from this analysis showed

6

• The potential markets for improved tests to detect active disease are large:

• 80 million for point-of-care test (per year) • 50 million for smear replacement (per year) • 20 million tests for culture replacement tests (per year)

Source: FIND/TDR, 2006

Potential market for new TB tests (global)

7

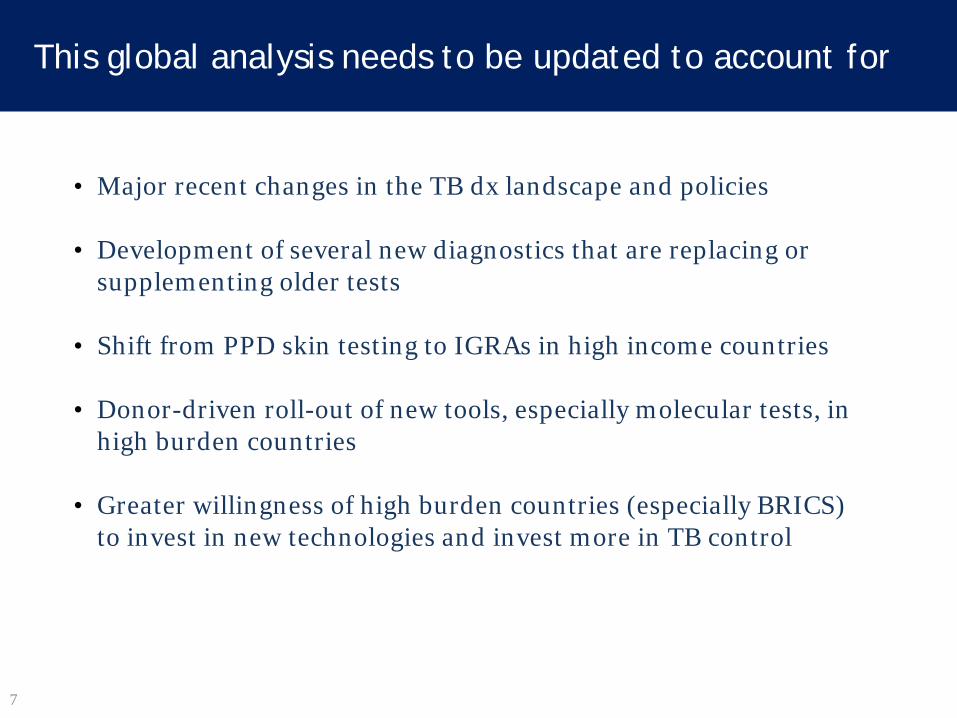

• Major recent changes in the TB dx landscape and policies

• Development of several new diagnostics that are replacing or supplementing older tests

• Shift from PPD skin testing to IGRAs in high income countries

• Donor-driven roll-out of new tools, especially molecular tests, in high burden countries

• Greater willingness of high burden countries (especially BRICS) to invest in new technologies and invest more in TB control

This global analysis needs to be updated to account for

8

The recently published UNITAID TB Dx landscape provides a good snapshot of this evolving landscape

http://www.unitaid.eu/marketdynamics/tuberculosis-diagnostic-landscape

9

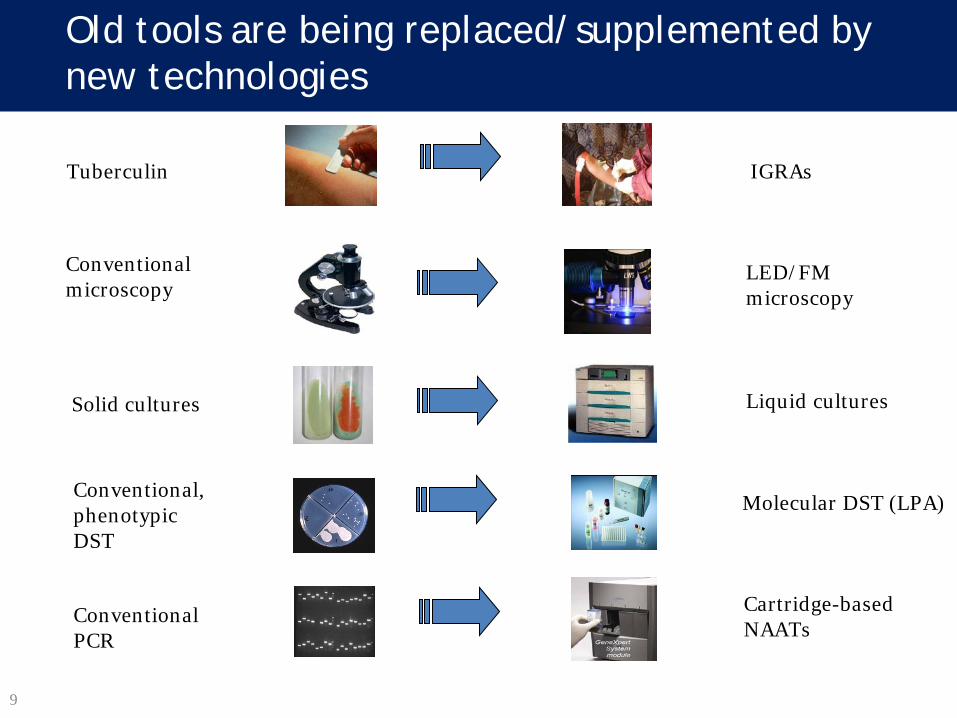

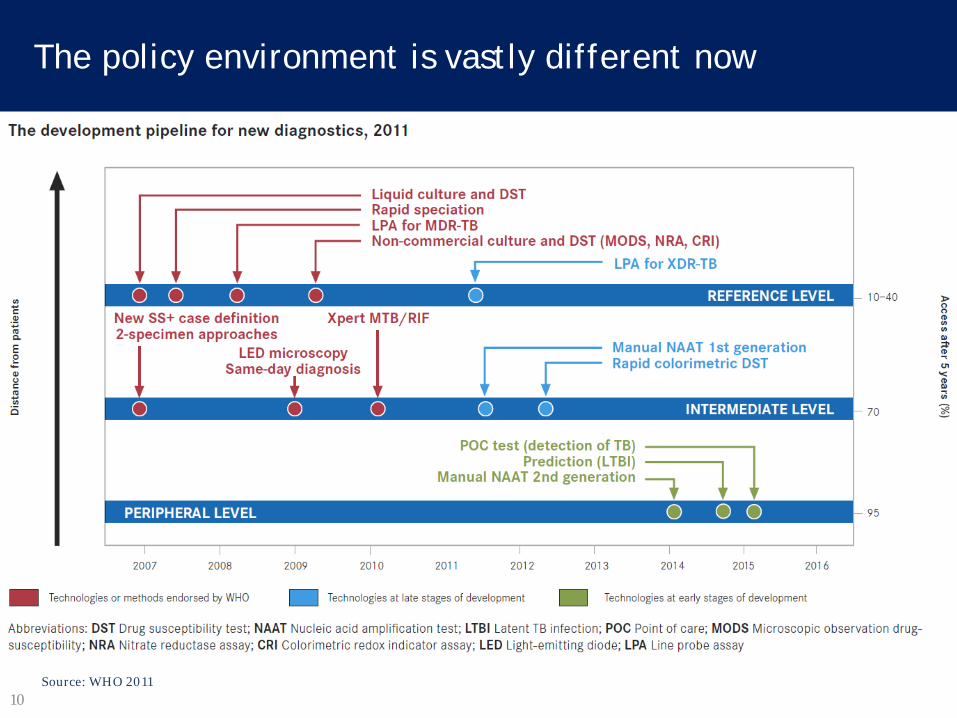

Old tools are being replaced/supplemented by new technologies

Tuberculin IGRAs

Conventional microscopy

LED/FM microscopy

Solid cultures Liquid cultures

Conventional PCR

Cartridge-based NAATs

Molecular DST (LPA) Conventional, phenotypic DST

10 Source: WHO 2011

The policy environment is vastly different now

11 Denkinger C et al. Clin Micro Infect 2011

In high-income countries, there is a growing shift from tuberculin skin testing to IGRAs, or TST + IGRA

T-SPOT.TB® [Oxford Immunotec, UK]

QuantiFERON-TB Gold® In Tube [Cellestis Ltd, Qiagen]

12

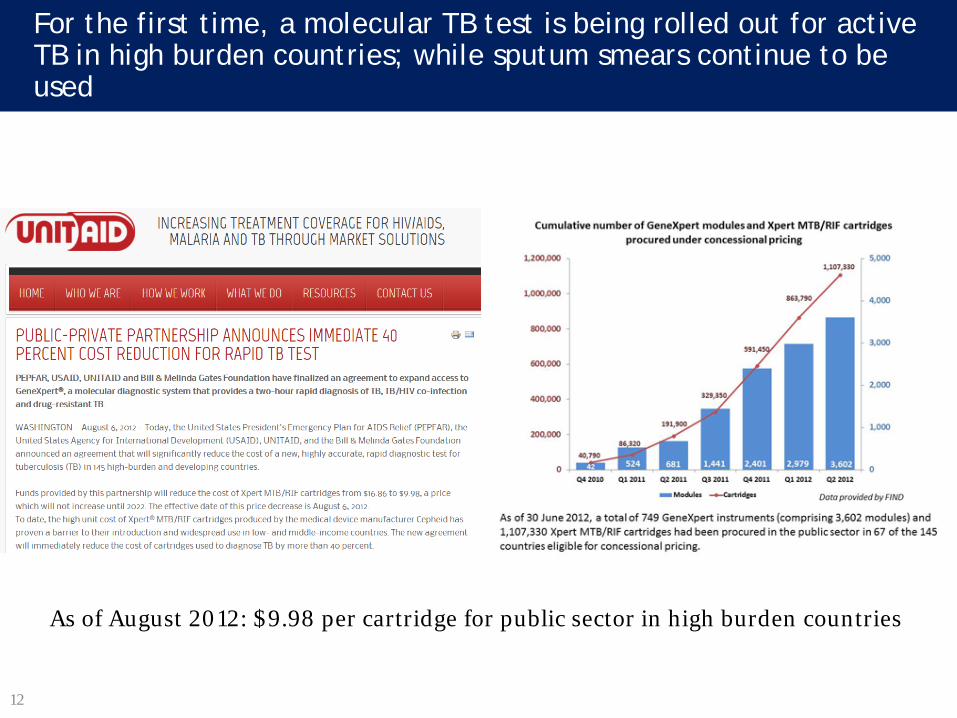

For the first time, a molecular TB test is being rolled out for active TB in high burden countries; while sputum smears continue to be used

As of August 2012: $9.98 per cartridge for public sector in high burden countries

13

Source: Pai NP, Pai M. Discovery Med 2012

After GeneXpert, several fast-followers are rapidly emerging, aiming at decentralized deployment

14

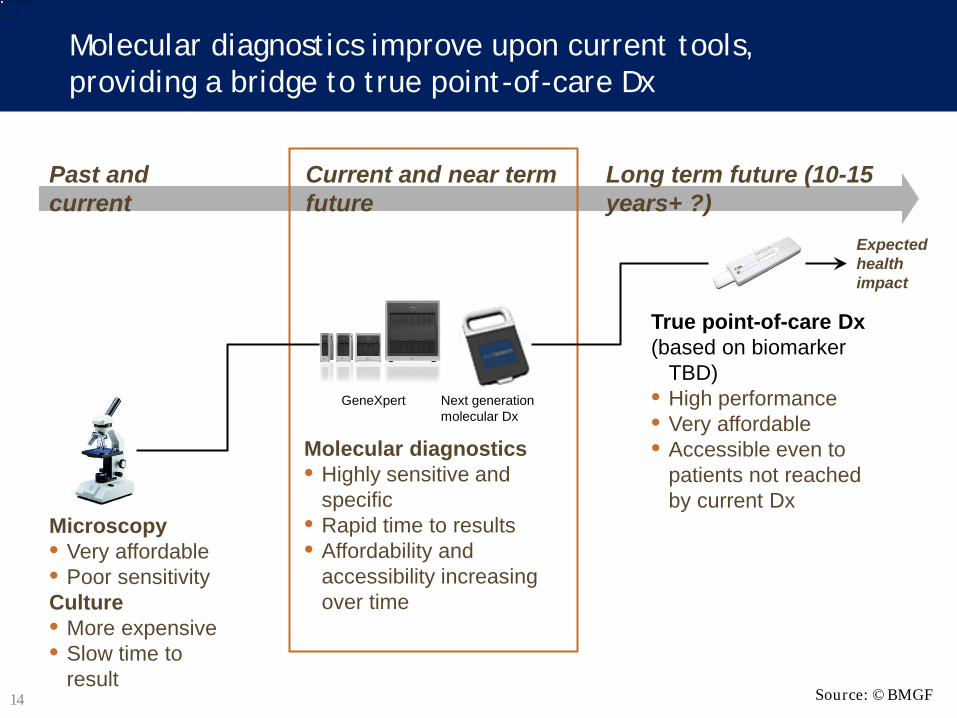

Molecular diagnostics improve upon current tools, providing a bridge to true point-of-care Dx

Past and current

Long term future (10-15 years+ ?)

Expected health impact

This image cannot currently be displayed.

Microscopy • Very affordable • Poor sensitivity Culture • More expensive • Slow time to

result

Molecular diagnostics • Highly sensitive and

specific • Rapid time to results • Affordability and

accessibility increasing over time

True point-of-care Dx (based on biomarker

TBD) • High performance • Very affordable • Accessible even to

patients not reached by current Dx

Current and near term future

Next generation molecular Dx

GeneXpert

Source: ©BMGF

15

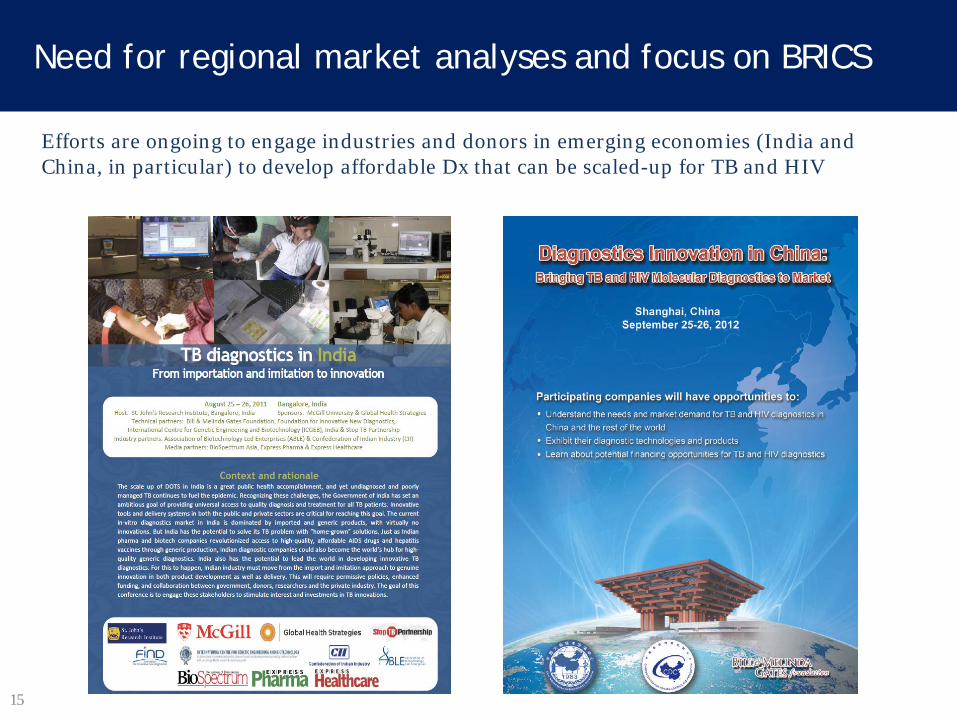

Efforts are ongoing to engage industries and donors in emerging economies (India and China, in particular) to develop affordable Dx that can be scaled-up for TB and HIV

Need for regional market analyses and focus on BRICS

TB Diagnostics in India: Market Analysis Revised - Version 2

Shekhar Menon, MBA [Indian Institute of Management, Bangalore] Minal Madhavankandi, MBA [Indian Institute of Management, Bangalore] Mansi Chitalia, MBA [Clinton Health Access Initiative, New Delhi] Madhukar Pai, MD, PhD* [McGill University, Montreal]

Full analysis is available at: http://tbevidence.org/resource-center/market-analyses/

17

Public sector (RNTCP) Private (non-RNTCP)

Refers to the testing facilities under the Revised National Tuberculosis Control Programme (RNTCP), the government tuberculosis programme

Includes all testing facilities in the private sector, government hospitals, medical colleges

TB diagnostics that are currently in use in India

• Active TB: • Sputum smear microscopy (direct

ZN staining) • Chest x-rays

• Drug resistant TB: • Line probe assays • Solid culture and DST • Liquid culture and DST

• Latent TB and pediatric TB: • Tuberculin skin test

• Active TB: • Sputum smear microscopy (direct

ZN and auramine staining) • Chest x-rays • Serological TB tests (ELISA and

rapid tests) • PCR (in-house or commercial) • QuantiFERON-TB Gold In Tube

• Drug resistant TB: • Line probe assays • Liquid culture and DST

• Latent TB: • Tuberculin skin test • QuantiFERON TB Gold In Tube

18

Estimation of number of patients with suspected pulmonary TB

Estimation of total pulmonary TB suspects (per year)

National TB programme (RNTCP) – Pulmonary TB suspects1 7,550,522

Contribution of RNTCP to total pulmonary suspects 40%

Contribution of Non RNTCP (private sector) to total pulmonary suspects 60%

Non RNTCP – Estimated number of pulmonary TB suspects 11,325,783

Total pulmonary TB suspects 18,876,305

Source: 1. RNTCP report: TB India 2011;

Assumptions based on discussions with key stakeholders*

Note: *Key stakeholders include RNTCP, WHO, BMGF, CHAI, FIND, GHS, private laboratory service providers, diagnostics manufacturers

• We assumed the split of patients tested for pulmonary TB (pulmonary TB suspects) in RNTCP: Non-RNTCP sector to be 40: 60 based on discussions with various stakeholders*

• The split was applied to the pulmonary TB suspects in the RNTCP sector to calculate the number of pulmonary TB suspects in the Non-RNTCP sector

19

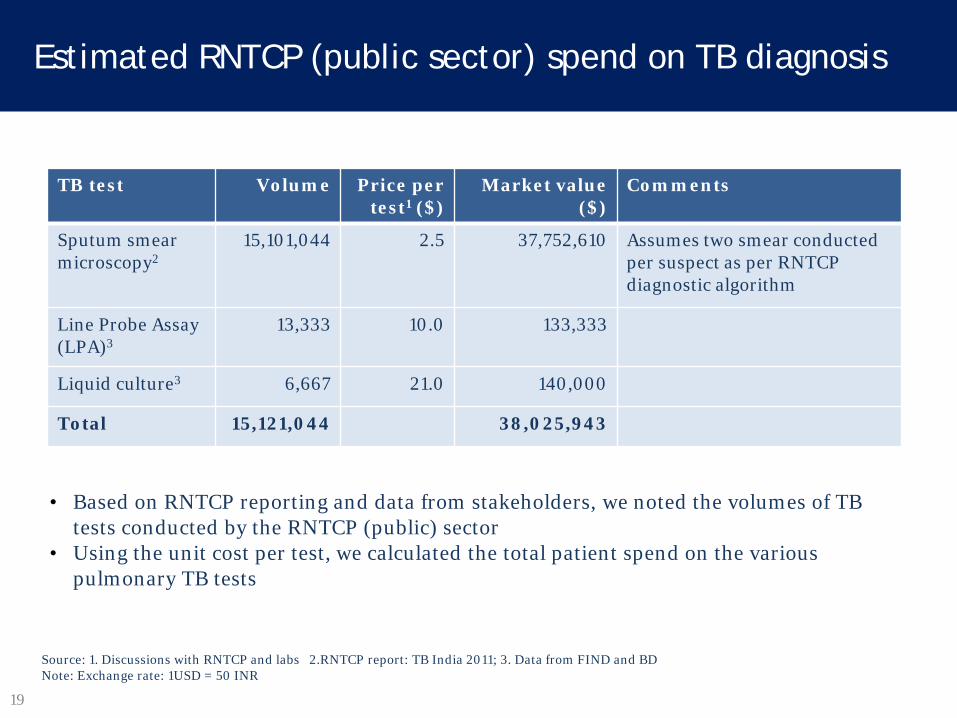

Estimated RNTCP (public sector) spend on TB diagnosis

Source: 1. Discussions with RNTCP and labs 2.RNTCP report: TB India 2011; 3. Data from FIND and BD Note: Exchange rate: 1USD = 50 INR

TB test Volume Price per test1 ($)

Market value ($)

Comments

Sputum smear microscopy2

15,101,044 2.5 37,752,610 Assumes two smear conducted per suspect as per RNTCP diagnostic algorithm

Line Probe Assay (LPA)3

13,333 10.0 133,333

Liquid culture3 6,667 21.0 140,000

Total 15,121,044 38,025,943

• Based on RNTCP reporting and data from stakeholders, we noted the volumes of TB tests conducted by the RNTCP (public) sector

• Using the unit cost per test, we calculated the total patient spend on the various pulmonary TB tests

20

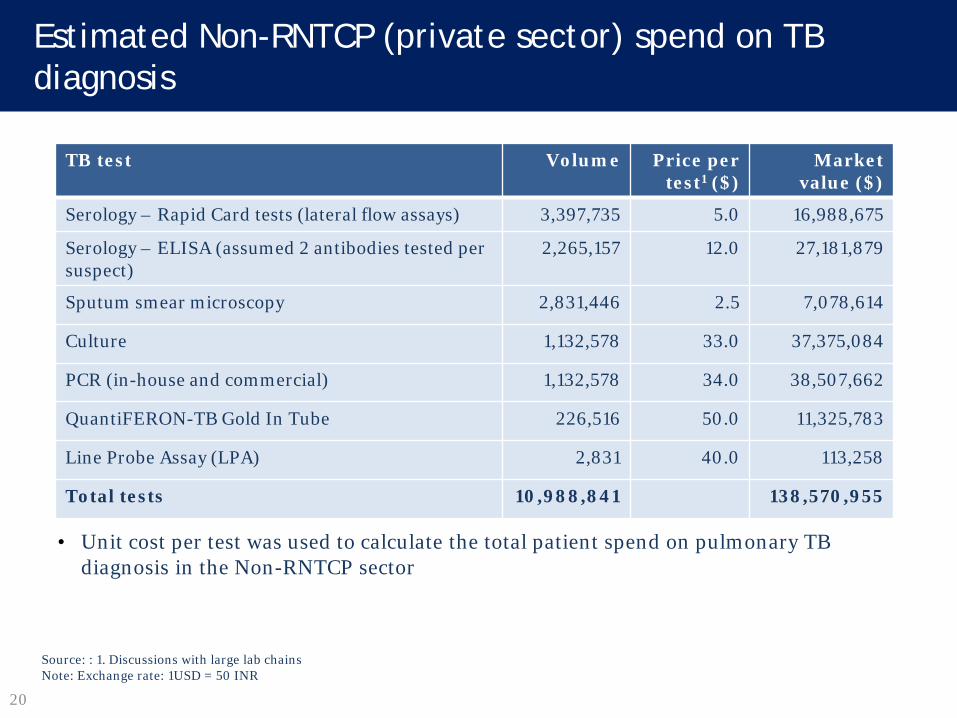

Estimated Non-RNTCP (private sector) spend on TB diagnosis

Source: : 1. Discussions with large lab chains Note: Exchange rate: 1USD = 50 INR

TB test Volume Price per test1 ($)

Market value ($)

Serology – Rapid Card tests (lateral flow assays) 3,397,735 5.0 16,988,675

Serology – ELISA (assumed 2 antibodies tested per suspect)

2,265,157 12.0 27,181,879

Sputum smear microscopy 2,831,446 2.5 7,078,614

Culture 1,132,578 33.0 37,375,084

PCR (in-house and commercial) 1,132,578 34.0 38,507,662

QuantiFERON-TB Gold In Tube 226,516 50.0 11,325,783

Line Probe Assay (LPA) 2,831 40.0 113,258

Total tests 10,988,841 138,570,955

• Unit cost per test was used to calculate the total patient spend on pulmonary TB diagnosis in the Non-RNTCP sector

21

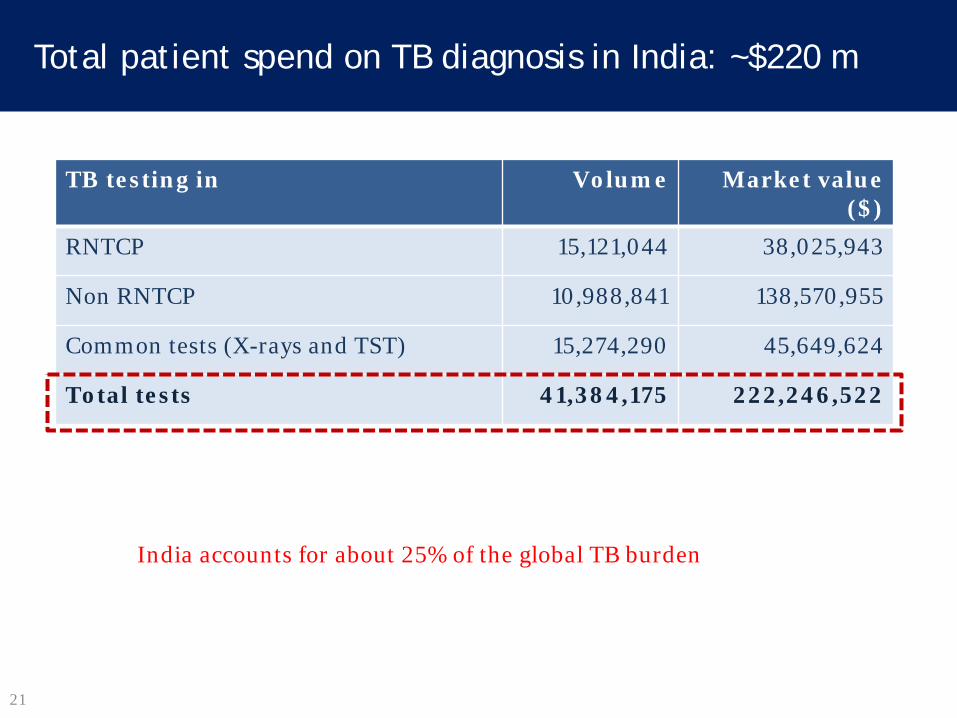

Total patient spend on TB diagnosis in India: ~$220 m

TB testing in Volume Market value ($)

RNTCP 15,121,044 38,025,943

Non RNTCP 10,988,841 138,570,955

Common tests (X-rays and TST) 15,274,290 45,649,624

Total tests 41,384,175 222,246,522

India accounts for about 25% of the global TB burden

22

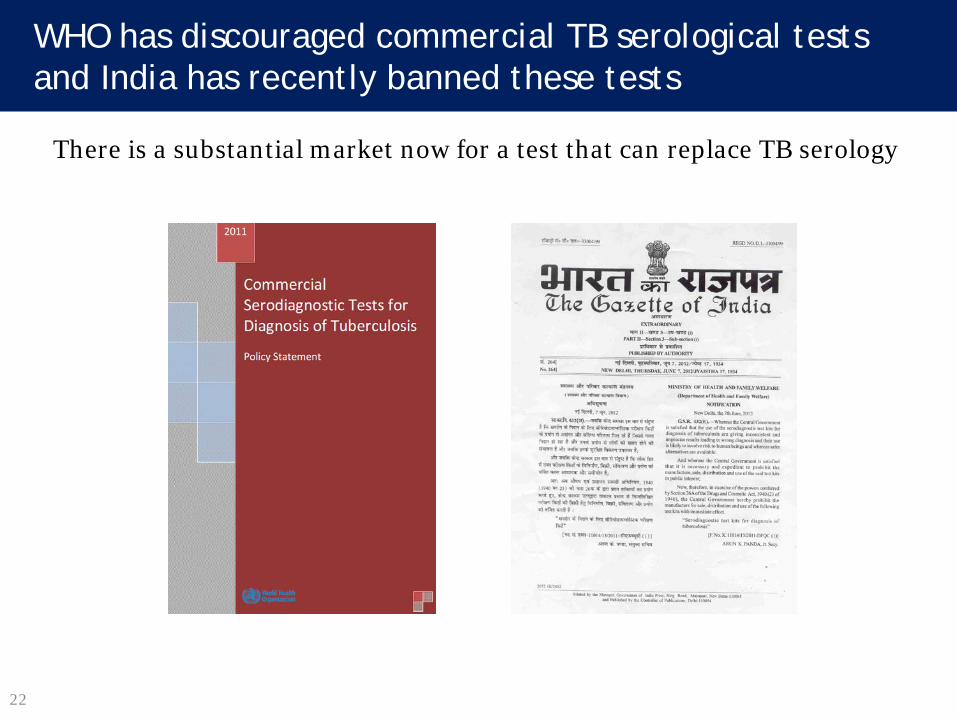

WHO has discouraged commercial TB serological tests and India has recently banned these tests

There is a substantial market now for a test that can replace TB serology

23

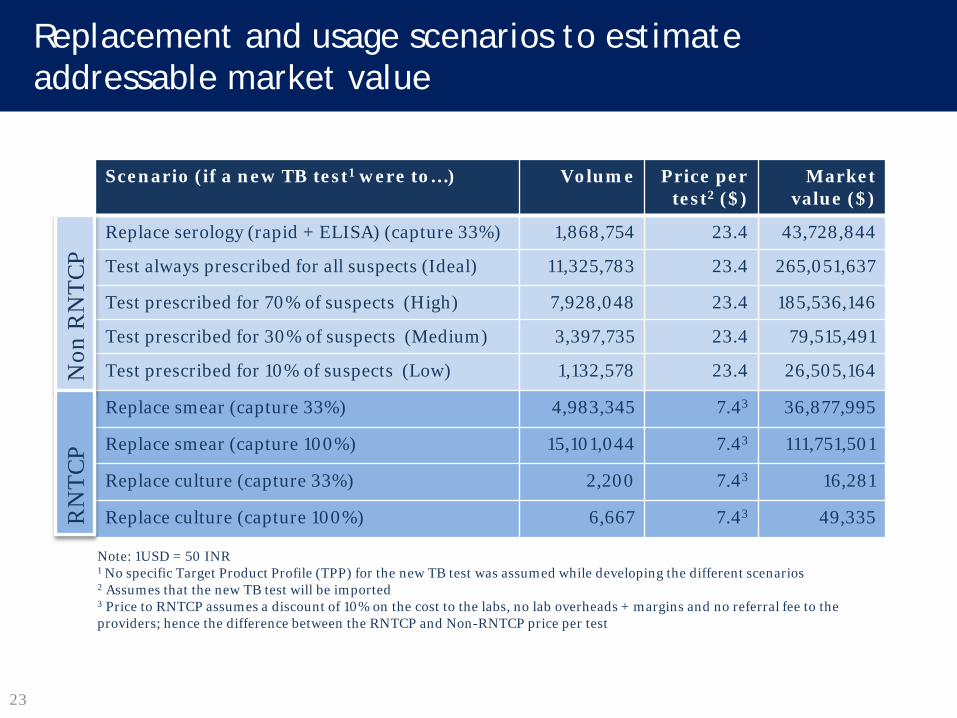

Replacement and usage scenarios to estimate addressable market value

Note: 1USD = 50 INR 1 No specific Target Product Profile (TPP) for the new TB test was assumed while developing the different scenarios 2 Assumes that the new TB test will be imported 3 Price to RNTCP assumes a discount of 10% on the cost to the labs, no lab overheads + margins and no referral fee to the providers; hence the difference between the RNTCP and Non-RNTCP price per test

Scenario (if a new TB test1 were to…) Volume Price per test2 ($)

Market value ($)

Replace serology (rapid + ELISA) (capture 33%) 1,868,754 23.4 43,728,844

Test always prescribed for all suspects (Ideal) 11,325,783 23.4 265,051,637

Test prescribed for 70% of suspects (High) 7,928,048 23.4 185,536,146

Test prescribed for 30% of suspects (Medium) 3,397,735 23.4 79,515,491

Test prescribed for 10% of suspects (Low) 1,132,578 23.4 26,505,164

Replace smear (capture 33%) 4,983,345 7.43 36,877,995

Replace smear (capture 100%) 15,101,044 7.43 111,751,501

Replace culture (capture 33%) 2,200 7.43 16,281

Replace culture (capture 100%) 6,667 7.43 49,335

Non

RN

TCP

RN

TCP

24

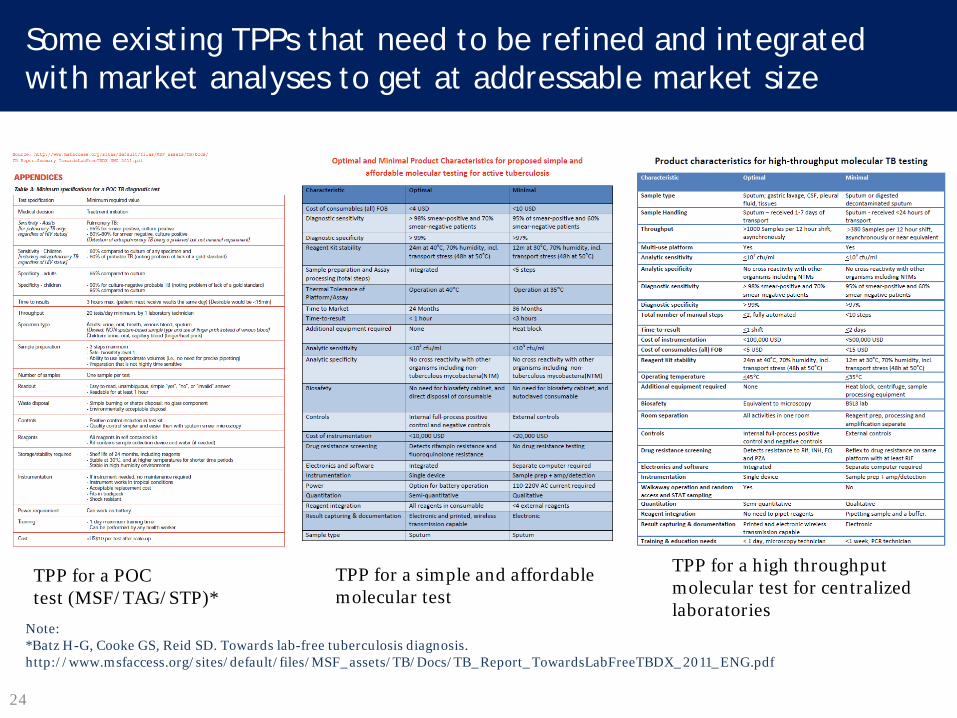

Some existing TPPs that need to be refined and integrated with market analyses to get at addressable market size

TPP for a POC test (MSF/TAG/STP)*

TPP for a simple and affordable molecular test

TPP for a high throughput molecular test for centralized laboratories

Note: *Batz H-G, Cooke GS, Reid SD. Towards lab-free tuberculosis diagnosis. http://www.msfaccess.org/sites/default/files/MSF_assets/TB/Docs/TB_Report_TowardsLabFreeTBDX_2011_ENG.pdf

© 2012 Bill & Melinda Gates Foundation | 25

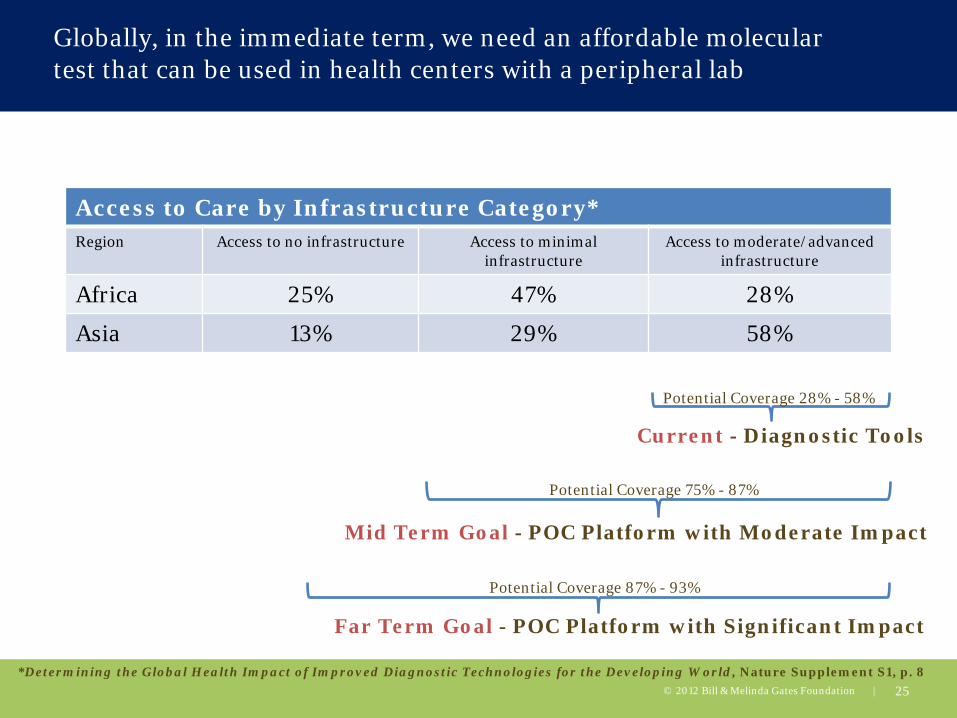

Access to Care by Infrastructure Category* Region Access to no infrastructure Access to minimal

infrastructure Access to moderate/advanced

infrastructure

Africa 25% 47% 28%

Asia 13% 29% 58%

*Determining the Global Health Impact of Improved Diagnostic Technologies for the Developing World, Nature Supplement S1, p. 8

Current - Diagnostic Tools

Mid Term Goal - POC Platform with Moderate Impact

Far Term Goal - POC Platform with Significant Impact

Potential Coverage 28% - 58%

Potential Coverage 75% - 87%

Potential Coverage 87% - 93%

Globally, in the immediate term, we need an affordable molecular test that can be used in health centers with a peripheral lab

26

In the longer term, we need a simple POC test that can be deployed in the community and health posts

Pai NP, Vadnais C, Denkinger C, Engel N, et al. (2012) Point-of-Care Testing for Infectious Diseases: Diversity, Complexity, and Barriers in Low- And Middle-Income Countries. PLoS Med 9(9): e1001306. doi:10.1371/journal.pmed.1001306 http://www.plosmedicine.org/article/info:doi/10.1371/journal.pmed.1001306

27

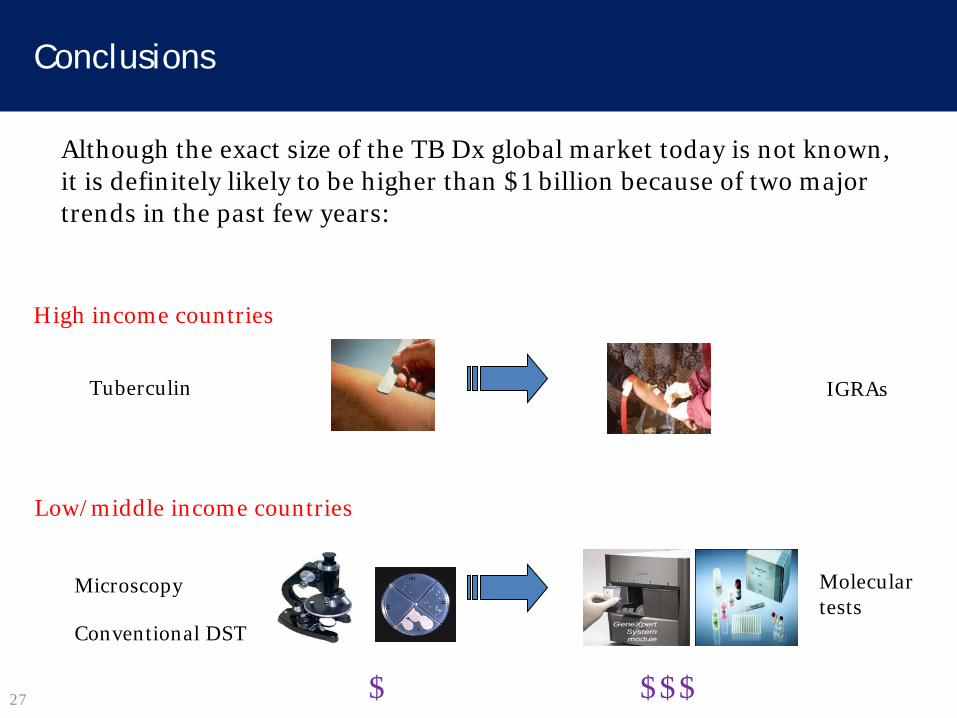

Conclusions

Although the exact size of the TB Dx global market today is not known, it is definitely likely to be higher than $1 billion because of two major trends in the past few years:

Tuberculin IGRAs

High income countries

Low/middle income countries

Microscopy Conventional DST

Molecular tests

$ $$$

28

Conclusions

However, since current versions of IGRAs and molecular tests are expensive and challenging to scale-up, there is an opportunity for companies to develop:

▫ More affordable IGRAs or next-generation assays for latent TB

infection that are more predictive for future disease

▫ More affordable molecular tests or next-generation assays for active TB and MDR-TB

▫ Truly innovative, simple technologies for POC use in decentralized settings

29

Chinese companies are already making progress along these lines

For example:

• TB-IGRAs by ▫ Beijing Wantai ▫ Haikou VTI Biological Institute ▫ Zhengzhou Biocell Biotechnology

• TB molecular assays by: ▫ Ustar Biotechnologies ▫ CapitalBio

• These products need to be internationally validated for policy recommendations and global uptake/adoption ▫ Regulatory approvals are required but not sufficient for policy and global scale-up

30

Which are the biggest markets for TB diagnostics? 30

For latent TB dx

For active TB dx

Canada: Health Canada USA: FDA >20 million tests for LTBI in North America

REGULATORY AGENCY & VOLUMES

India: Drug Controller General of India China: SFDA Brazil: ANVISA South Africa: Medicines Control Council 30 – 40 million tests for active TB in these countries

31

What evidence is needed for global policy? What are the challenges for global scale-up?

31

J Infect Dis 2012

Int J Tuberc Lung Dis 2012

32

Thank you!

• No financial/industry conflicts

• I serve as a consultant to the Bill & Melinda Gates Foundation

• I receive grant support from the Bill & Melinda Gates Foundation & Grand Challenges Canada