Embed Size (px)

Citation preview

TCI Investor Conference, New YorkMike Franczak – EVP Operations

17 June 2014

FO

R P

ER

SO

NA

L U

SE

ON

LY

Important notice

No Reliance on this document

This document was prepared by Aurizon Holdings Limited (ACN 146 335 622) (referred to as “Aurizon” which includes its related bodies corporate). Whilst Aurizon has

endeavoured to ensure the accuracy of the information contained in this document at the date of publication, it may contain information that has not been independently

verified. Aurizon makes no representation or warranty as to the accuracy, completeness or reliability of any of the information contained in this document.

Document is a summary only

This document contains information in a summary form only and does not purport to be complete and is qualified in its entirety by, and should be read in conjunction with, all

of the information which Aurizon files with the Australian Securities Exchange. Any information or opinions expressed in this document are subject to change without notice.

Aurizon is not under any obligation to update or keep current the information contained within this document. Information contained in this document may have changed

since its date of publication.

No investment advice

This document is not intended to be, and should not be considered to be, investment advice by Aurizon nor a recommendation to invest in Aurizon. The information provided

in this document has been prepared for general informational purposes only without taking into account the recipient’s investment objectives, financial circumstances,

taxation position or particular needs. Each recipient to whom this document is made available must make its own independent assessment of Aurizon after making such

investigations and taking such advice as it deems necessary. If the recipient is in any doubts about any of the information contained in this document, the recipient should

obtain independent professional advice.

No offer of securities

Nothing in this presentation should be construed as a recommendation of or an offer to sell or a solicitation of an offer to buy or sell securities in Aurizon in any jurisdiction

(including in the United States). This document is not a prospectus and it has not been reviewed or authorised by any regulatory authority in any jurisdiction. This document

does not constitute an advertisement, invitation or document which contains an invitation to the public in any jurisdiction to enter into or offer to enter into an agreement to

acquire, dispose of, subscribe for or underwrite securities in Aurizon.

Forward-looking statements

This document may include forward-looking statements which are not historical facts. Forward-looking statements are based on the current beliefs, assumptions,

expectations, estimates and projections of Aurizon. These statements are not guarantees or predictions of future performance, and involve both known and unknown risks,

uncertainties and other factors, many of which are beyond Aurizon’s control. As a result, actual results or developments may differ materially from those expressed in the

forward-looking statements contained in this document. Aurizon is not under any obligation to update these forward-looking statements to reflect events or circumstances

that arise after publication. Past performance is not an indication of future performance.

No liability

To the maximum extent permitted by law in each relevant jurisdiction, Aurizon and its directors, officers, employees, agents, contractors, advisers and any other person

associated with the preparation of this document, each expressly disclaims any liability, including without limitation any liability arising from fault or negligence, for any errors

or misstatements in, or omissions from, this document or any direct, indirect or consequential loss howsoever arising from the use or reliance upon the whole or any part of

this document or otherwise arising in connection with it.

2

3

FO

R P

ER

SO

NA

L U

SE

ON

LY

Aurizon is on the journey to World Class

Return on Invested Capital (ROIC)(2)Operating Ratio(1)

1) Operating Ratio = 1 – EBIT margin

2) ROIC = Underlying EBIT/(Net Working Capital + Net PP&E + AUC+ Gross Intangible Assets)

90.0

88.0

FY2010 FY2011

79.8

FY2013

83.4

FY2012

-1.4ppt

1H FY2014

78.4

8.6

8.0

6.7

4.4

2.0

1H FY2014

+0.6ppt

FY2013FY2012FY2011FY2010

4

Operating ratios below 70% are achievable for Aurizon, but it is a long term journey (often 10+ years)

All Class 1's have steadily improved returnson capital since 2004, moving towards 12% ROIC

1. Class 1 metrics based on calendar year data from December 1995 through to December 2012. Aurizon metrics based on financial year data from June 2011 through to December 2013.

2. ROIC = Return on Invested Capital

3. ‘Rest of Class 1average’ comprises metrics for BNSF, UP, NS, KCS and CP

Source: Analysis of Class 1 Railroads (Association of American Railroads (AAR)) & Company reports

North American Class 1's have shown operating ratios <65% and ROICs >12% are achievable – Aurizon is on its way

0

4

8

12

16

ROIC (%)

13121110090807060504030201009998979695 14

Aurizon

Aurizon

Aurizon

CSX

CN

Rest of Class 1 average

60

70

80

90

100

Operating ratio (%)

1109 1008070605 12 1304030201009998979695 14

CN (leader in delivering gains)

Aurizon

CSX (largest shift of all Class 1s)

Rest of Class 1 average

5

FO

R P

ER

SO

NA

L U

SE

ON

LY

Transformation journey

IPO

Implementation of functional model to remove operating silos

Voluntary Redundancy (VR) program to reduce headcount

New holistic business model -Integrated Operating Plan (IOP)

Asset/fleet productivity + rationalisation

Crew efficiency Coordinated cross business

planning Improved contract

structures and service

Increasing value through sustainable, replicable and continuous improvement

Longer term outcome (post 75%) highly influenced by outcome of Enterprise Agreement (EA) negotiations

November 2010

December 2011

March 2012

July 2013

FutureMay 2014

Aurizon is evolving to an improved business model

6

FO

R P

ER

SO

NA

L U

SE

ON

LY

We focus on 5 core business principles

to drive value

Core design considerations guide our

work

What’s

changed?

Coordinated planning (where permitted) across functions and lines of business

Common KPIs / metrics to drive Enterprise outcomes

Continuous improvement focus with a replicable and adaptable model

Standardisation

Eliminate waste

Maximise train payloads

Balanced volumes

Multi-user; multi-cargo trains

Reliability based maintenance

Flexibility

Increase velocity

Energy efficient

Network planning –localised execution

Technology

Safe working practices Enterprise view

Asset focus / fungibility of assets

The IOP is underpinned by key business and operational principles….

7

FO

R P

ER

SO

NA

L U

SE

ON

LY

… and is being rolled out across all key national corridors

Aurizon’s operations footprint

NorthernTerritory

New South Wales

South Australia

Western Australia

Victoria

Queensland

Tasmania

Cairns

Townsville

Mackay

Rockhampton

BRISBANE

NewcastleSYDNEY

CANBERRA

MELBOURNE

HOBART

ADELAIDE

Alice Springs

Mt Isa

DARWIN

Port Hedland

Geraldton

Esperance

Kalgoorlie

Port AugustaPERTH

Aurizon operations

Do not operate

Hunter Valley Coal

South West Corridor

Coal North Corridor

North West Corridor

North Coast Line

Western Australian Corridors

Coal South Corridor

Interstate Intermodal

8

FO

R P

ER

SO

NA

L U

SE

ON

LY

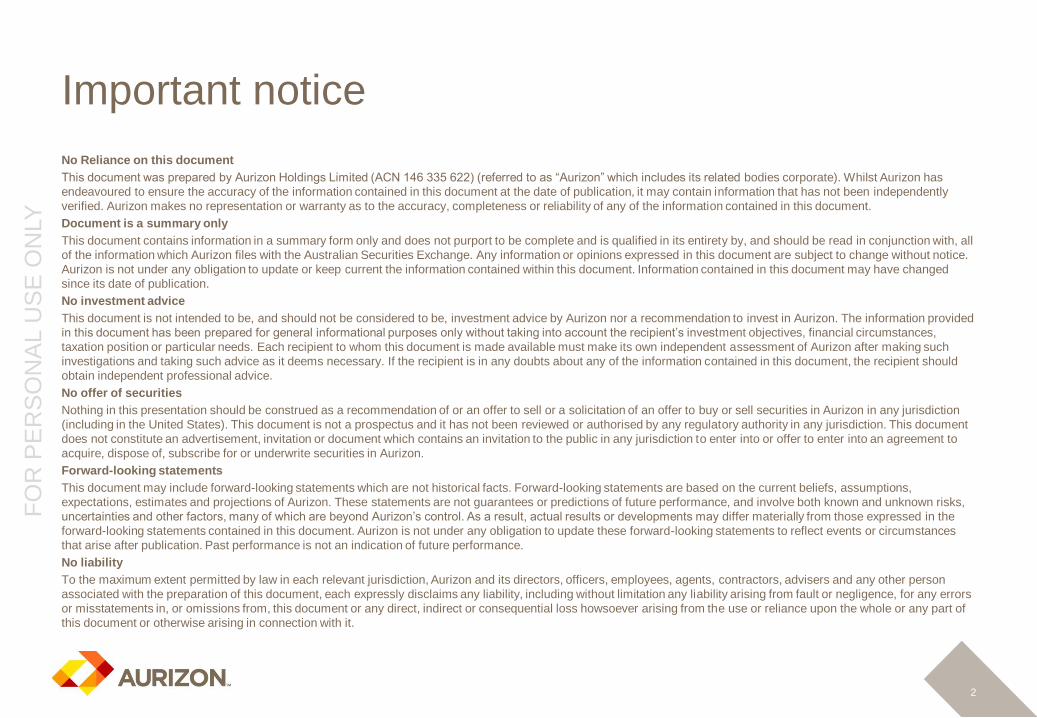

Redesign Activities

18 Nov 2013IOP workshop kick-off

New operating plan

Exit non-core business (TOMA)

Below rail engagement (QR)

Customer engagement

Community engagement

Government engagement

Additional growth volume opportunities

Rationalisation of fuelling and maintenance footprint

Redesign consideration

This approach is being replicated across the entire business

Principles Impact

Close down depotsCrew training

Rollingstock maintenance changes

Forward looking

12 May 2014Full new design implementation completion

Safety risk assessments (End of Train device)

NOSC consolidation

Network access negotiation

Energy efficient Fuel efficiency gains from loco cascade, reduced fuelling points

Standardisation Reduction of loco classes, e.g. Clyde

Multi-user trainsImproved asset utilisation through consolidation of services, e.g. Bowen Coke

Maximise trainpayloads

Increased payload in multiple services, e.g. Glencore

Increase velocityQuicker cycles through reduction of number of crew changes, e.g. Charters Towers

Eliminate wasteElimination of dwell no longer required from a cycle, e.g. Hughenden stops

Balanced volumes Right sized asset based on volume requirement, e.g. IPL

Reduction of property (admin)

Future operation

efficiency gain

Future design of yard requirement

EA implication

Example of how this works through in a corridor

4000 class locomotive cascade from CQCN

North West corridor IOP redesign example

9

FO

R P

ER

SO

NA

L U

SE

ON

LY

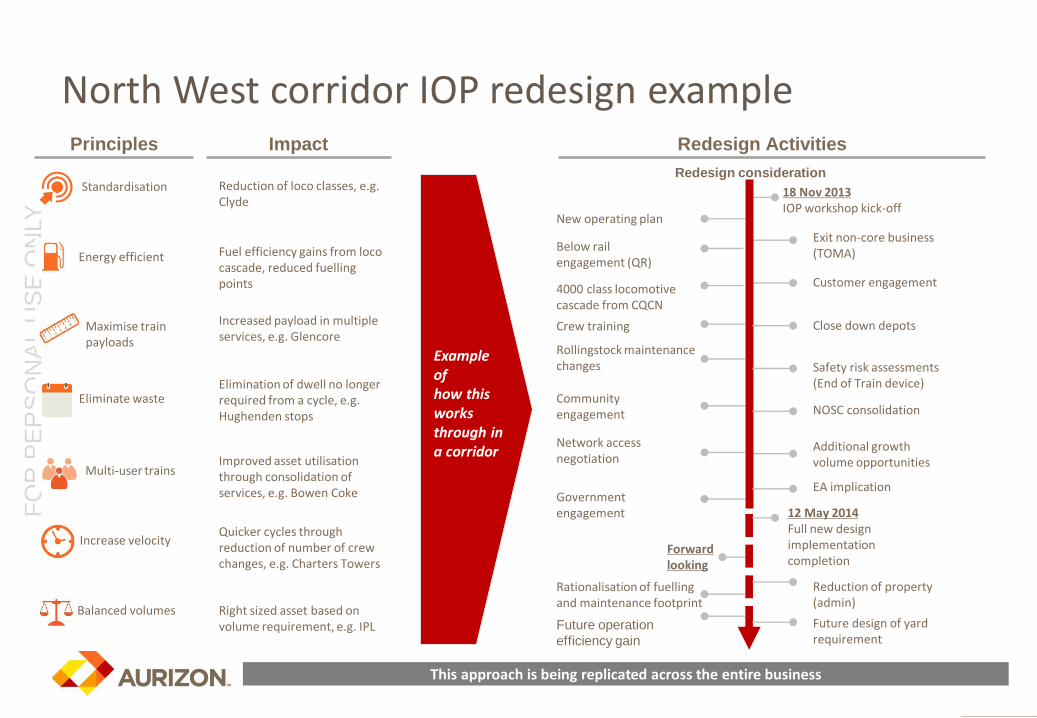

The IOP is helping drive a smaller, more productive, standardised fleet

1. All figures are subject to market changes2. Expect procurement of new rollingstock to support growth options and asset replacements. We do not expect

anything material before FY2016. Will update market on requirements and capital cost closer to the time3. Assumes total volumes CAGR of 3%-5% p.a. over 5 years

59

30

[-49%]

FY18FY13

[+30%]

FY18FY13

829

[77]

FY13 fleet Not Required Estimated

FY18 fleet(1)

[598]

[-28%]

[308]

Estimated

New(2)

Loco

mo

tive

s

297

185

[-38%]

FY13 FY18 FY13

[+15%]

FY18

18,546

FY13 fleet

[5,185]

Estimated

New(2)

[2,931]

Not Required

[16,292]

Estimated

FY18 fleet(1)

[-12%]

Wag

on

s

Active Fleet Classes

Productivity(NTKs/Active fleet) 5 Year Fleet Plan3

[ ] Approximate figures

Reduced (RSM) footprint

Standardised maintenance practices

Reduced materials, inventory and carrying costs

Ease of training

Younger, more fuel efficient fleet

Reduce maintenance and depreciation expense

• Significant reduction in classes across Aurizon’s rollingstock

• Large planned productivity improvements across Aurizon’s rollingstock

Ou

tco

me

Benefits

[ ]

[ ]

10

FO

R P

ER

SO

NA

L U

SE

ON

LY

Technology is helping Aurizon re-engineer its work to drive leading edge improvements in safety, efficiency and capacity

• Fewer equipment failures

• Moving from interval to condition based maintenance

• Reduced dwell time in yards

• Improved asset reliability and productivity

• Improved labour productivity (finders become fixers)

11

FO

R P

ER

SO

NA

L U

SE

ON

LY

Operations transformation programs delivering a strong 1H FY2014 performance

1. The NTK/Employee metric for the half year is annualised for operational purposes and uses monthly average FTE2. Monthly average3. CQCN = Central Queensland Coal Network4. Operations costs base includes Coal, Iron Ore and Freight costs (unless otherwise noted) but excludes Access, Electricity and

Intermodal road solutions costs

Metric1H

FY20141H

FY20131H

Variance2H

FY2013

Pro

du

ctio

n

Net tonne kilometres (bn) 38.2 33.5 14.0% 33.5

Tonnes (m) 149.4 133.8 11.7% 133.9

Peo

ple

1 Full time equivalents2 5,464 5,807 5.9% 5,520

NTK/Employee (FTE)1,2 14.00 11.56 21.1% 12.17

Flee

t2 NTK/Active loco2 9.63 7.91 21.7% 8.16

NTK/Active wagon2 0.41 0.34 20.6% 0.35

Pro

du

ctiv

ity

& e

ffic

ien

cy

Average Payload Coal (tonnes)2 7,921 7,651 3.5% 7,769

Turnaround time - CQCN3 (hrs)2 25.14 26.73 5.9% 27.69

Fuel consumption (l/dGTK) 3.51 3.64 3.6% 3.58

Operating expenses (c/NTK)4 have improved by ~14%

12

FO

R P

ER

SO

NA

L U

SE

ON

LY

Operational transformation of Aurizon is well underway….

Aurizon has demonstrated a track record of improvement and transformation

Aurizon is poised to deliver future value

1

2

Key Takeaways

TCI Investor Conference, New YorkMike Franczak – EVP Operations

17 June 2014