Embed Size (px)

Citation preview

TEACHERS COLLEGE, COLUMBIA UNIVERSITY

Financial Statements

August 31, 2019 and 2018

(With Independent Auditors’ Report Thereon)

Independent Auditors’ Report

The Trustees Teachers College, Columbia University:

We have audited the accompanying financial statements of Teachers College, Columbia University, which comprise the balance sheets as of August 31, 2019 and 2018, and the related statements of activities and cash flows for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with U.S. generally accepted accounting principles; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Teachers College, Columbia University as of August 31, 2019 and 2018, and the changes in its net assets and its cash flows for the years then ended in accordance with U.S. generally accepted accounting principles.

KPMG LLP is a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

KPMG LLP345 Park AvenueNew York, NY 10154-0102

2

Emphasis of Matter

As discussed in note 2(n) to the financial statements, Teachers College, Columbia University adopted Accounting Standards Update 2016-14, Not-for-Profit Entities (Topic 958): Presentation of Financial Statements of Not for Profit Entities (ASU 2016-14), during the year ended August 31, 2019. Our opinion is not modified with respect to this matter.

December 4, 2019

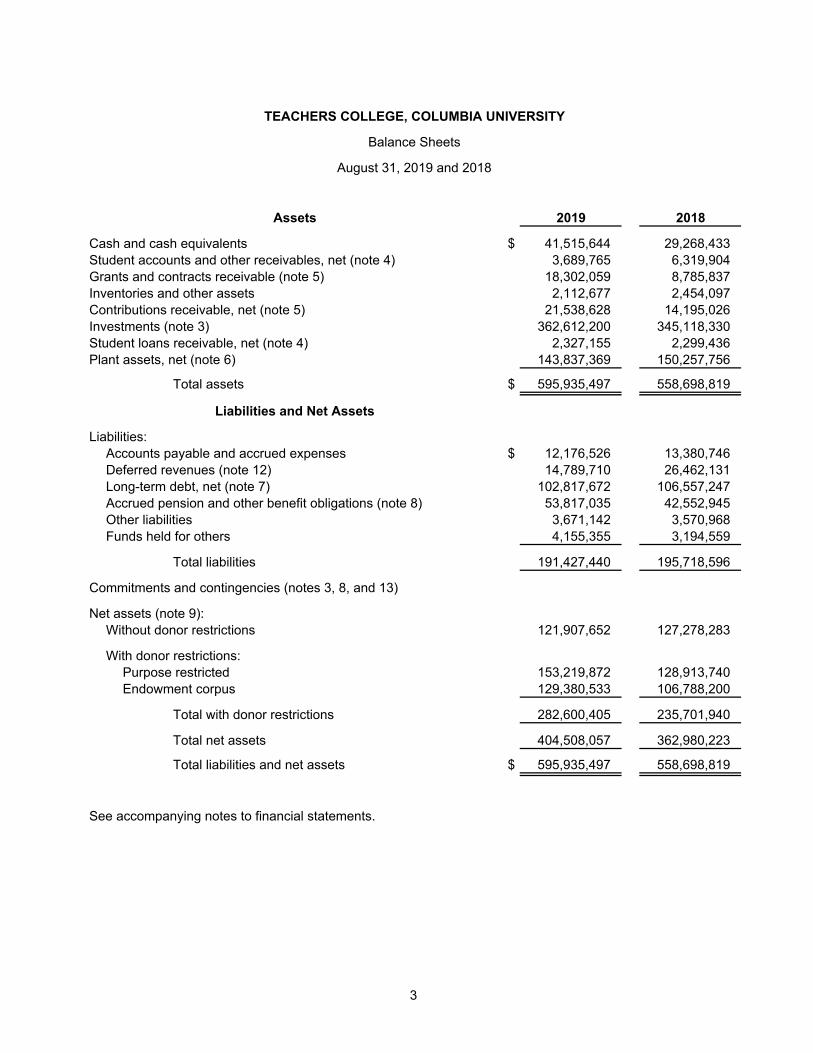

TEACHERS COLLEGE, COLUMBIA UNIVERSITY

Balance Sheets

August 31, 2019 and 2018

Assets 2019 2018

Cash and cash equivalents $ 41,515,644 29,268,433 Student accounts and other receivables, net (note 4) 3,689,765 6,319,904 Grants and contracts receivable (note 5) 18,302,059 8,785,837 Inventories and other assets 2,112,677 2,454,097 Contributions receivable, net (note 5) 21,538,628 14,195,026 Investments (note 3) 362,612,200 345,118,330 Student loans receivable, net (note 4) 2,327,155 2,299,436 Plant assets, net (note 6) 143,837,369 150,257,756

Total assets $ 595,935,497 558,698,819

Liabilities and Net Assets

Liabilities:Accounts payable and accrued expenses $ 12,176,526 13,380,746 Deferred revenues (note 12) 14,789,710 26,462,131 Long-term debt, net (note 7) 102,817,672 106,557,247 Accrued pension and other benefit obligations (note 8) 53,817,035 42,552,945 Other liabilities 3,671,142 3,570,968 Funds held for others 4,155,355 3,194,559

Total liabilities 191,427,440 195,718,596

Commitments and contingencies (notes 3, 8, and 13)

Net assets (note 9):Without donor restrictions 121,907,652 127,278,283

With donor restrictions:Purpose restricted 153,219,872 128,913,740 Endowment corpus 129,380,533 106,788,200

Total with donor restrictions 282,600,405 235,701,940

Total net assets 404,508,057 362,980,223

Total liabilities and net assets $ 595,935,497 558,698,819

See accompanying notes to financial statements.

3

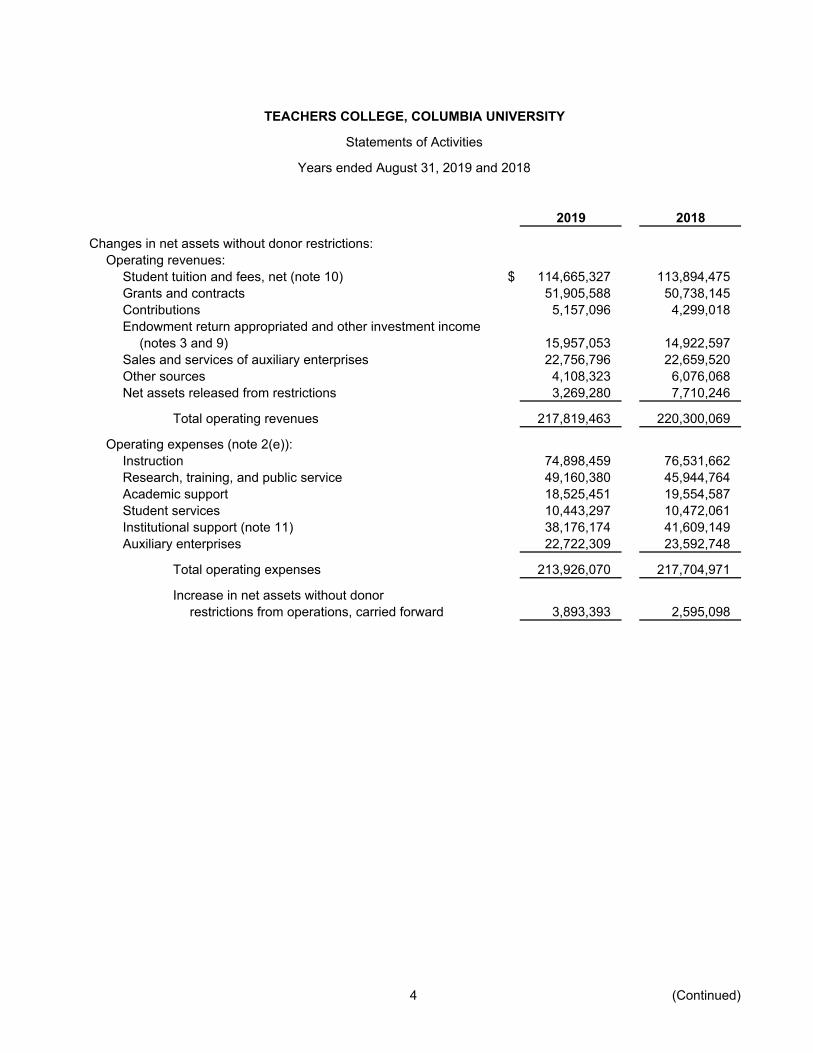

TEACHERS COLLEGE, COLUMBIA UNIVERSITY

Statements of Activities

Years ended August 31, 2019 and 2018

2019 2018

Changes in net assets without donor restrictions:Operating revenues:

Student tuition and fees, net (note 10) $ 114,665,327 113,894,475 Grants and contracts 51,905,588 50,738,145 Contributions 5,157,096 4,299,018 Endowment return appropriated and other investment income

(notes 3 and 9) 15,957,053 14,922,597 Sales and services of auxiliary enterprises 22,756,796 22,659,520 Other sources 4,108,323 6,076,068 Net assets released from restrictions 3,269,280 7,710,246

Total operating revenues 217,819,463 220,300,069

Operating expenses (note 2(e)):Instruction 74,898,459 76,531,662 Research, training, and public service 49,160,380 45,944,764 Academic support 18,525,451 19,554,587 Student services 10,443,297 10,472,061 Institutional support (note 11) 38,176,174 41,609,149 Auxiliary enterprises 22,722,309 23,592,748

Total operating expenses 213,926,070 217,704,971

Increase in net assets without donorrestrictions from operations, carried forward 3,893,393 2,595,098

4 (Continued)

TEACHERS COLLEGE, COLUMBIA UNIVERSITY

Statements of Activities

Years ended August 31, 2019 and 2018

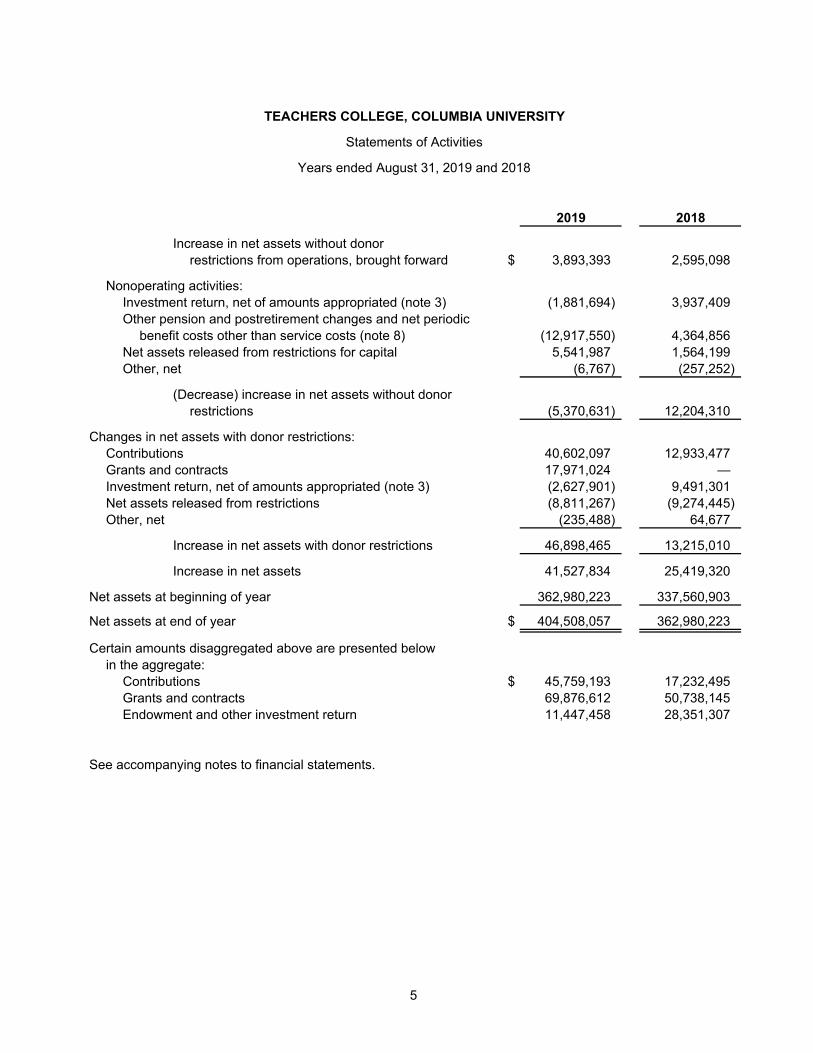

2019 2018

Increase in net assets without donorrestrictions from operations, brought forward $ 3,893,393 2,595,098

Nonoperating activities:Investment return, net of amounts appropriated (note 3) (1,881,694) 3,937,409 Other pension and postretirement changes and net periodic

benefit costs other than service costs (note 8) (12,917,550) 4,364,856 Net assets released from restrictions for capital 5,541,987 1,564,199 Other, net (6,767) (257,252)

(Decrease) increase in net assets without donorrestrictions (5,370,631) 12,204,310

Changes in net assets with donor restrictions:Contributions 40,602,097 12,933,477 Grants and contracts 17,971,024 — Investment return, net of amounts appropriated (note 3) (2,627,901) 9,491,301 Net assets released from restrictions (8,811,267) (9,274,445) Other, net (235,488) 64,677

Increase in net assets with donor restrictions 46,898,465 13,215,010

Increase in net assets 41,527,834 25,419,320

Net assets at beginning of year 362,980,223 337,560,903

Net assets at end of year $ 404,508,057 362,980,223

Certain amounts disaggregated above are presented belowin the aggregate:

Contributions $ 45,759,193 17,232,495 Grants and contracts 69,876,612 50,738,145 Endowment and other investment return 11,447,458 28,351,307

See accompanying notes to financial statements.

5

TEACHERS COLLEGE, COLUMBIA UNIVERSITY

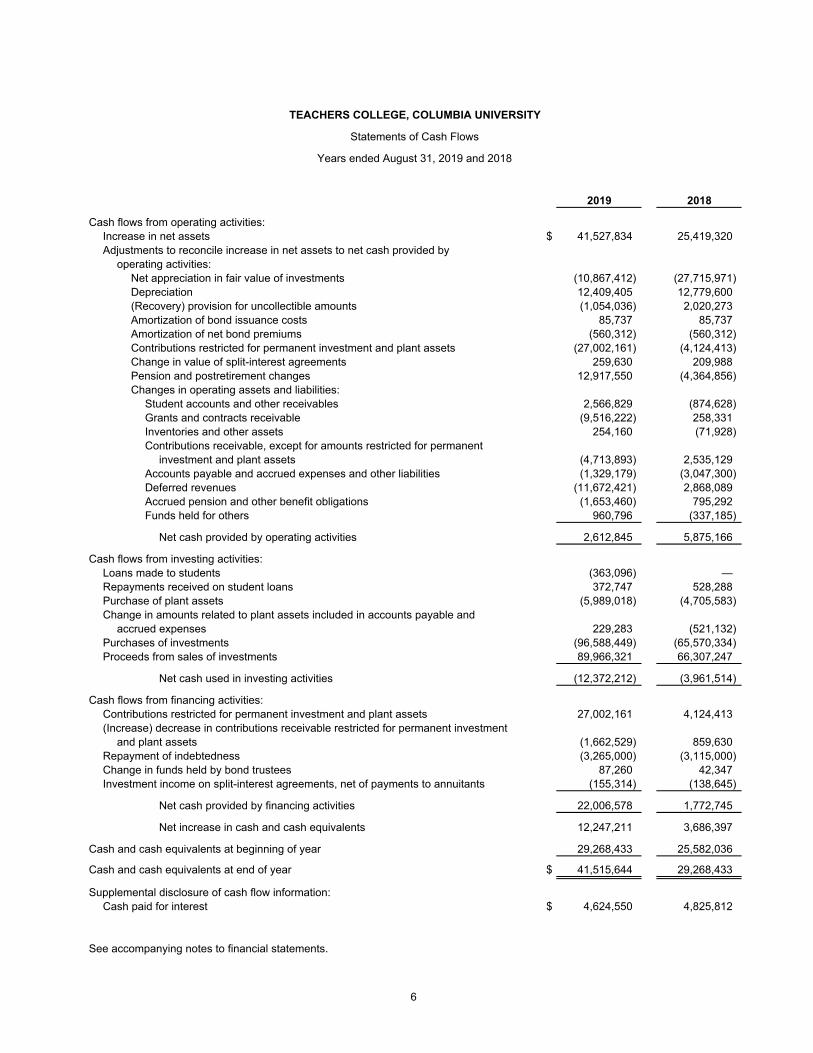

Statements of Cash Flows

Years ended August 31, 2019 and 2018

2019 2018

Cash flows from operating activities:Increase in net assets $ 41,527,834 25,419,320 Adjustments to reconcile increase in net assets to net cash provided by

operating activities:Net appreciation in fair value of investments (10,867,412) (27,715,971) Depreciation 12,409,405 12,779,600 (Recovery) provision for uncollectible amounts (1,054,036) 2,020,273 Amortization of bond issuance costs 85,737 85,737 Amortization of net bond premiums (560,312) (560,312) Contributions restricted for permanent investment and plant assets (27,002,161) (4,124,413) Change in value of split-interest agreements 259,630 209,988 Pension and postretirement changes 12,917,550 (4,364,856) Changes in operating assets and liabilities:

Student accounts and other receivables 2,566,829 (874,628) Grants and contracts receivable (9,516,222) 258,331 Inventories and other assets 254,160 (71,928) Contributions receivable, except for amounts restricted for permanent

investment and plant assets (4,713,893) 2,535,129 Accounts payable and accrued expenses and other liabilities (1,329,179) (3,047,300) Deferred revenues (11,672,421) 2,868,089 Accrued pension and other benefit obligations (1,653,460) 795,292 Funds held for others 960,796 (337,185)

Net cash provided by operating activities 2,612,845 5,875,166

Cash flows from investing activities:Loans made to students (363,096) — Repayments received on student loans 372,747 528,288 Purchase of plant assets (5,989,018) (4,705,583) Change in amounts related to plant assets included in accounts payable and

accrued expenses 229,283 (521,132) Purchases of investments (96,588,449) (65,570,334) Proceeds from sales of investments 89,966,321 66,307,247

Net cash used in investing activities (12,372,212) (3,961,514)

Cash flows from financing activities:Contributions restricted for permanent investment and plant assets 27,002,161 4,124,413 (Increase) decrease in contributions receivable restricted for permanent investment

and plant assets (1,662,529) 859,630 Repayment of indebtedness (3,265,000) (3,115,000) Change in funds held by bond trustees 87,260 42,347 Investment income on split-interest agreements, net of payments to annuitants (155,314) (138,645)

Net cash provided by financing activities 22,006,578 1,772,745

Net increase in cash and cash equivalents 12,247,211 3,686,397

Cash and cash equivalents at beginning of year 29,268,433 25,582,036

Cash and cash equivalents at end of year $ 41,515,644 29,268,433

Supplemental disclosure of cash flow information:Cash paid for interest $ 4,624,550 4,825,812

See accompanying notes to financial statements.

6

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

7 (Continued)

(1) Description of Business (a) Discussion of Operations

Teachers College, Columbia University (the College) is a graduate and professional school of education. The College engages in five basic activities: (1) research on critical issues of education; (2) instruction of future leaders-practitioners, policymakers, and academicians; (3) education of current leaders-teachers, principals, superintendents, board members, legislators, presidents, members of the media, and representatives of foundations and corporations; (4) development of the public discourse and national agenda for education; and (5) improvement of the practice of educational institutions via laboratories, models, and demonstration projects. The College was founded in 1887 and became affiliated with Columbia University in 1898. Under an arrangement with Columbia University, the faculty of the College was designated as faculty of Columbia University, but the College retained its legal and financial independence. The College remains a separate corporation.

(b) Tax Status The College is qualified as a not-for-profit organization under Section 501(c)(3) of the Internal Revenue Code, as amended. Accordingly, it is not subject to income taxes except to the extent it has taxable income from activities that are not related to its exempt purpose. The College recognizes the effect of income tax positions only if those positions are more likely than not of being sustained. No provision for income taxes was required for fiscal years 2019 or 2018.

(2) Summary of Significant Accounting Policies (a) Basis of Presentation

The accompanying financial statements have been prepared on the accrual basis of accounting in accordance with U.S. generally accepted accounting principles (GAAP). Net assets of the College and changes therein are classified and reported as follows:

Net Assets Without Donor Restrictions – Net assets that are not subject to donor-imposed restrictions, including those designated by the Board of Trustees of the College (the Board) to function as endowment.

Net Assets With Donor Restrictions – Net assets subject to donor-imposed restrictions that will be met by either actions of the College or the passage of time, and net assets subject to donor-imposed restrictions that stipulate that they be maintained permanently by the College, but permit the College to expend part or all of the income derived therefrom for general or donor-specified purposes.

Revenues and gains and losses on investments and other assets are reported as changes in net assets without donor restrictions unless limited by explicit donor-imposed restrictions or by law. Expirations of donor restrictions on net assets, that is, the donor-imposed stipulated purpose has been accomplished and/or the stipulated time period has elapsed, are reported as increases in net assets without donor restrictions if the purpose or time restrictions are met in the same reporting period that such assets are received; otherwise, they are reported as net assets released from restrictions. Expenses are reported as decreases in net assets without donor restrictions.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

8 (Continued)

(b) Cash Equivalents All highly liquid debt instruments with an original maturity of three months or less are considered to be cash equivalents, except for such assets that are part of the College’s investment portfolio managed by external investment managers for long-term purposes.

(c) Contributions Contributions, including unconditional promises to give, are reported initially at fair value as revenues in the period received or pledged. The College reports contributions of plant assets as increases in net assets without donor restrictions unless the donor places restrictions on their use. Contributions to be received after one year are discounted at a risk-adjusted rate. Amortization of the discount is recorded as additional contribution revenue in accordance with the donor-imposed restrictions, if any, on the contribution. An allowance is recorded for uncollectible contributions based on management’s judgment, past collection experience, and other relevant factors.

Conditional promises to give are not recognized until they become unconditional, that is, when the conditions on which they depend are met. At August 31, 2019, the College received conditional promises to give of approximately $4.3 million in the form of bequest intentions and agreements that are contingent upon the College meeting certain barriers or conditions not fulfilled as of year end.

(d) Grants and Contracts Grants, contracts, and similar agreements comprise federal and nonfederal (state, private foundation, etc.) contracts. The activity may represent a reciprocal transaction where commensurate value is exchanged or a nonreciprocal transaction where the resources provided are for the public at large, further support the funding organization’s mission or more directly benefit the College. Revenue from exchange transactions are recognized as performance obligations are satisfied, which may be as milestones are met or as related costs are incurred. Federal and certain nonfederal grants with specific restrictions on spending are classified as conditional transactions and the related revenue is recognized at the time expenditures are incurred. Unconditional revenue is recognized in full when a qualifying promise to give has been made and generally occurs when the agreement is executed.

At August 31, 2019, the College received conditional promises to give of approximately $14.2 million in the form of measureable performance related or other barriers that have not been reflected in the accompanying financial statements because the conditions on which they depend have not been met.

(e) Functional Expense Allocation The College’s primary functional programs are instruction and research. Other functional expenses are primarily incurred in support of the College’s core mission. Expenses for the operation and maintenance of facilities, depreciation and interest are first allocated to auxiliary enterprises based on square footage compared to total plant. The remainder is then allocated to other functional programs based on total headcount in each program.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

9 (Continued)

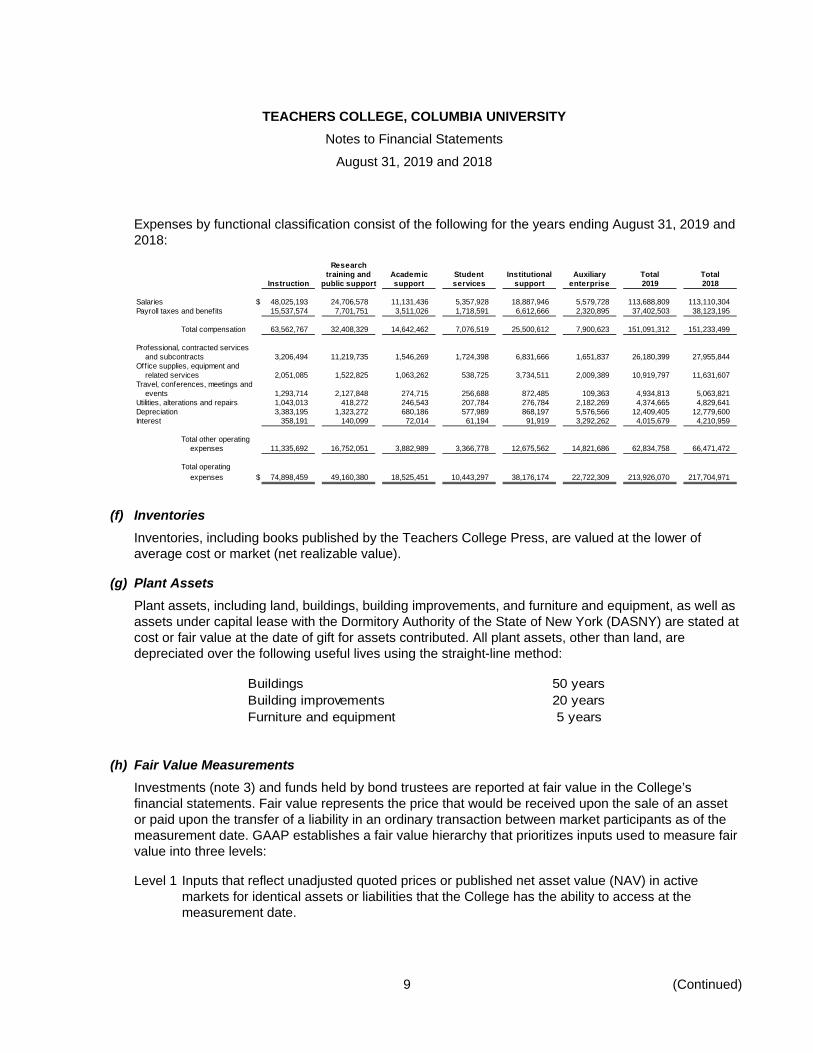

Expenses by functional classification consist of the following for the years ending August 31, 2019 and 2018:

Researchtraining and Academic Student Institutional Auxiliary Total Total

Instruction public support support services support enterprise 2019 2018

Salaries $ 48,025,193 24,706,578 11,131,436 5,357,928 18,887,946 5,579,728 113,688,809 113,110,304 Payroll taxes and benefits 15,537,574 7,701,751 3,511,026 1,718,591 6,612,666 2,320,895 37,402,503 38,123,195

Total compensation 63,562,767 32,408,329 14,642,462 7,076,519 25,500,612 7,900,623 151,091,312 151,233,499

Professional, contracted servicesand subcontracts 3,206,494 11,219,735 1,546,269 1,724,398 6,831,666 1,651,837 26,180,399 27,955,844

Office supplies, equipment andrelated services 2,051,085 1,522,825 1,063,262 538,725 3,734,511 2,009,389 10,919,797 11,631,607

Travel, conferences, meetings andevents 1,293,714 2,127,848 274,715 256,688 872,485 109,363 4,934,813 5,063,821

Utilities, alterations and repairs 1,043,013 418,272 246,543 207,784 276,784 2,182,269 4,374,665 4,829,641 Depreciation 3,383,195 1,323,272 680,186 577,989 868,197 5,576,566 12,409,405 12,779,600 Interest 358,191 140,099 72,014 61,194 91,919 3,292,262 4,015,679 4,210,959

Total other operatingexpenses 11,335,692 16,752,051 3,882,989 3,366,778 12,675,562 14,821,686 62,834,758 66,471,472

Total operatingexpenses $ 74,898,459 49,160,380 18,525,451 10,443,297 38,176,174 22,722,309 213,926,070 217,704,971

(f) Inventories Inventories, including books published by the Teachers College Press, are valued at the lower of average cost or market (net realizable value).

(g) Plant Assets Plant assets, including land, buildings, building improvements, and furniture and equipment, as well as assets under capital lease with the Dormitory Authority of the State of New York (DASNY) are stated at cost or fair value at the date of gift for assets contributed. All plant assets, other than land, are depreciated over the following useful lives using the straight-line method:

Buildings 50 yearsBuilding improvements 20 yearsFurniture and equipment 5 years

(h) Fair Value Measurements Investments (note 3) and funds held by bond trustees are reported at fair value in the College’s financial statements. Fair value represents the price that would be received upon the sale of an asset or paid upon the transfer of a liability in an ordinary transaction between market participants as of the measurement date. GAAP establishes a fair value hierarchy that prioritizes inputs used to measure fair value into three levels:

Level 1 Inputs that reflect unadjusted quoted prices or published net asset value (NAV) in active markets for identical assets or liabilities that the College has the ability to access at the measurement date.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

10 (Continued)

Level 2 Inputs other than quoted prices that are observable for the asset or liability either directly or indirectly, including inputs in markets that are not considered to be active.

Level 3 Inputs that are unobservable.

The College follows Accounting Standards Update (ASU) No. 2015-07, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent), which removes the requirements to categorize within the fair value hierarchy and to make certain disclosures for all investments where fair value is measured using the NAV per share practical expedient.

(i) Collections Collections at the College include works of art, literary works, historical treasures, and artifacts that are maintained in the College’s library and buildings. These collections are protected and preserved for public exhibition, education, research, and the furtherance of public service and, therefore, are not recognized as assets on the balance sheets. Costs associated with purchasing additions to and maintaining these collections are recorded as operating expenses in the period in which the items are acquired.

(j) U.S. Government Grants Refundable Funds provided by the U.S. government under the Federal Perkins and Nursing Faculty Loan programs are loaned to qualified students. These funds are ultimately refundable to the U.S. government and are presented in the accompanying balance sheets as a liability.

(k) Split-Interest Agreements In fiscal years 2019 and 2018, the College’s split-interest agreements with donors consist of charitable gift annuities, irrevocable charitable remainder trusts, perpetual trusts, and pooled life income funds.

Assets of charitable gift annuities and pooled life income funds are reported in investments in the accompanying balance sheets. Assets from charitable remainder trusts and perpetual trusts are reflected as contributions receivable in the accompanying balance sheets. Contributions are recognized at the date the trusts or pooled life income funds are established at the present value of the estimated future cash flows expected to be received by the College. The College’s interest in such split-interest gifts is adjusted annually for changes in the value of the assets, accretion of the discount, and other changes in the estimates of future benefits.

In addition, the College has the irrevocable right to receive income earned on two perpetual trusts. The College’s beneficial interest in the value of the trusts’ assets is classified as net assets with donor restrictions. Changes in the value of the College’s interest are recorded as changes in net assets with donor restrictions in the accompanying statements of activities.

(l) Operations The accompanying statements of activities distinguish between operating and nonoperating activities. Nonoperating activities represent changes in net assets without donor restrictions other than annual fund contributions, investment return on endowments in excess of or less than the amounts authorized for spending by the Board (note 9) on those funds, pension and postretirement changes and net

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

11 (Continued)

periodic benefit costs (other than service costs) (note 8), net assets released from restrictions for capital, and certain nonrecurring activities.

(m) Accounting Estimates The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingencies at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Significant estimates made in the preparation of the financial statements include the valuation of investments and accrued postretirement pension and other benefit obligations, the allocation of functional expenses, and the net realizable value of receivables. Actual results could differ from those estimates.

(n) Authoritative Accounting Pronouncements The Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2016-14, Presentation of Financial Statements of Not-for-Profit Entities, which among other things, changes how not for profit entities report net asset classes, expenses, and liquidity in their financial statements. The College adopted the ASU for the year ending August 31, 2019 on a retrospective basis. Significant changes to the College’s financial statements under the new guidance include the reduction of net asset classifications to two categories based on the existence or absence of donor restrictions (with donor restrictions, previously reported as temporarily restricted net assets of $124,349,864 and permanently restricted net assets of $111,352,076, and without donor restrictions, previously reported as unrestricted net assets), the presentation of expenses by their functional and natural classification in one location and additional disclosure requirements including the Board designation of net assets and the liquidity and availability of the College’s financial assets to meet cash needs within one year of the balance sheet date.

The FASB issued ASU No. 2014-09, Revenue from Contracts with Customers, which includes criteria on how entities recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The College adopted the ASU during the year ending August 31, 2019 on a restrospective basis. There was no material impact to the College due to the adoption of the ASU.

The FASB issued ASU No. 2018-08, Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made, to clarify and improve the scope and the accounting guidance for contributions received and contributions made. The amendments in this ASU are intended to assist entities in (1) evaluating whether transactions should be accounted for as contributions (nonreciprocal transactions) within the scope of ASC Topic 958, Not-for-Profit Entities, or as exchange (reciprocal) transactions subject to other guidance and (2) determining whether a contribution is conditional. The College adopted the ASU during the year ending August 31, 2019. As a result of the adoption, for certain transactions evaluated and classified as unconditional contributions, the College recognized $18 million of net assets with donor restrictions during the fiscal year.

The FASB issued ASU No. 2017-07, Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, which requires companies to present the service cost component of net periodic benefit cost in the statement of activities line item where compensation costs are reported. The College adopted the ASU for the year ending August 31, 2019.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

12 (Continued)

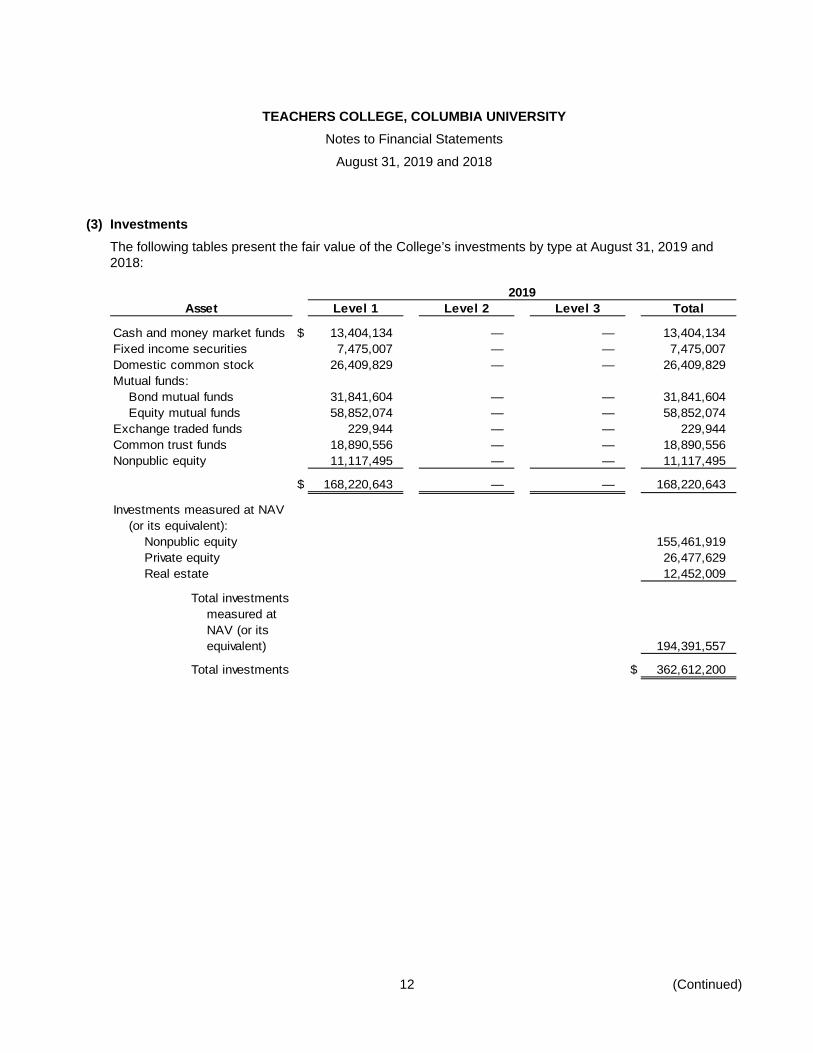

(3) Investments The following tables present the fair value of the College’s investments by type at August 31, 2019 and 2018:

2019Asset Level 1 Level 2 Level 3 Total

Cash and money market funds $ 13,404,134 — — 13,404,134 Fixed income securities 7,475,007 — — 7,475,007 Domestic common stock 26,409,829 — — 26,409,829 Mutual funds:

Bond mutual funds 31,841,604 — — 31,841,604 Equity mutual funds 58,852,074 — — 58,852,074

Exchange traded funds 229,944 — — 229,944 Common trust funds 18,890,556 — — 18,890,556 Nonpublic equity 11,117,495 — — 11,117,495

$ 168,220,643 — — 168,220,643

Investments measured at NAV(or its equivalent):

Nonpublic equity 155,461,919 Private equity 26,477,629 Real estate 12,452,009

Total investmentsmeasured atNAV (or itsequivalent) 194,391,557

Total investments $ 362,612,200

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

13 (Continued)

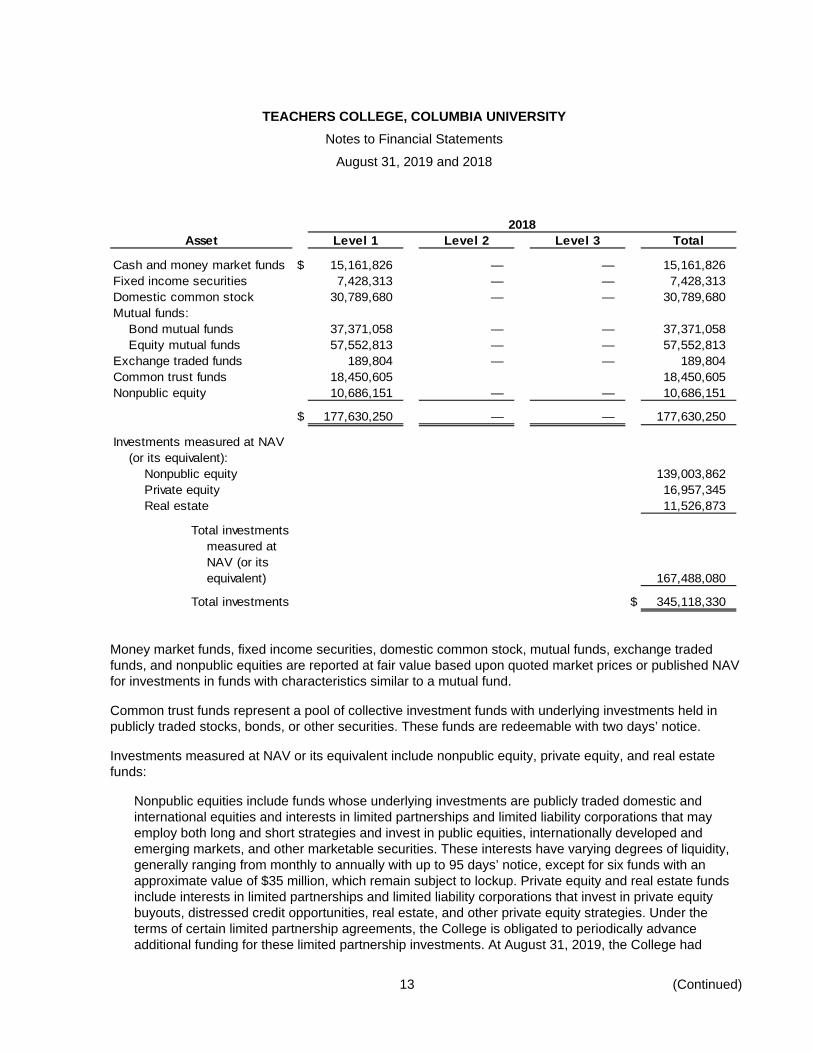

2018Asset Level 1 Level 2 Level 3 Total

Cash and money market funds $ 15,161,826 — — 15,161,826 Fixed income securities 7,428,313 — — 7,428,313 Domestic common stock 30,789,680 — — 30,789,680 Mutual funds:

Bond mutual funds 37,371,058 — — 37,371,058 Equity mutual funds 57,552,813 — — 57,552,813

Exchange traded funds 189,804 — — 189,804 Common trust funds 18,450,605 18,450,605 Nonpublic equity 10,686,151 — — 10,686,151

$ 177,630,250 — — 177,630,250

Investments measured at NAV(or its equivalent):

Nonpublic equity 139,003,862 Private equity 16,957,345 Real estate 11,526,873

Total investmentsmeasured atNAV (or itsequivalent) 167,488,080

Total investments $ 345,118,330

Money market funds, fixed income securities, domestic common stock, mutual funds, exchange traded funds, and nonpublic equities are reported at fair value based upon quoted market prices or published NAV for investments in funds with characteristics similar to a mutual fund.

Common trust funds represent a pool of collective investment funds with underlying investments held in publicly traded stocks, bonds, or other securities. These funds are redeemable with two days’ notice.

Investments measured at NAV or its equivalent include nonpublic equity, private equity, and real estate funds:

Nonpublic equities include funds whose underlying investments are publicly traded domestic and international equities and interests in limited partnerships and limited liability corporations that may employ both long and short strategies and invest in public equities, internationally developed and emerging markets, and other marketable securities. These interests have varying degrees of liquidity, generally ranging from monthly to annually with up to 95 days’ notice, except for six funds with an approximate value of $35 million, which remain subject to lockup. Private equity and real estate funds include interests in limited partnerships and limited liability corporations that invest in private equity buyouts, distressed credit opportunities, real estate, and other private equity strategies. Under the terms of certain limited partnership agreements, the College is obligated to periodically advance additional funding for these limited partnership investments. At August 31, 2019, the College had

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

14 (Continued)

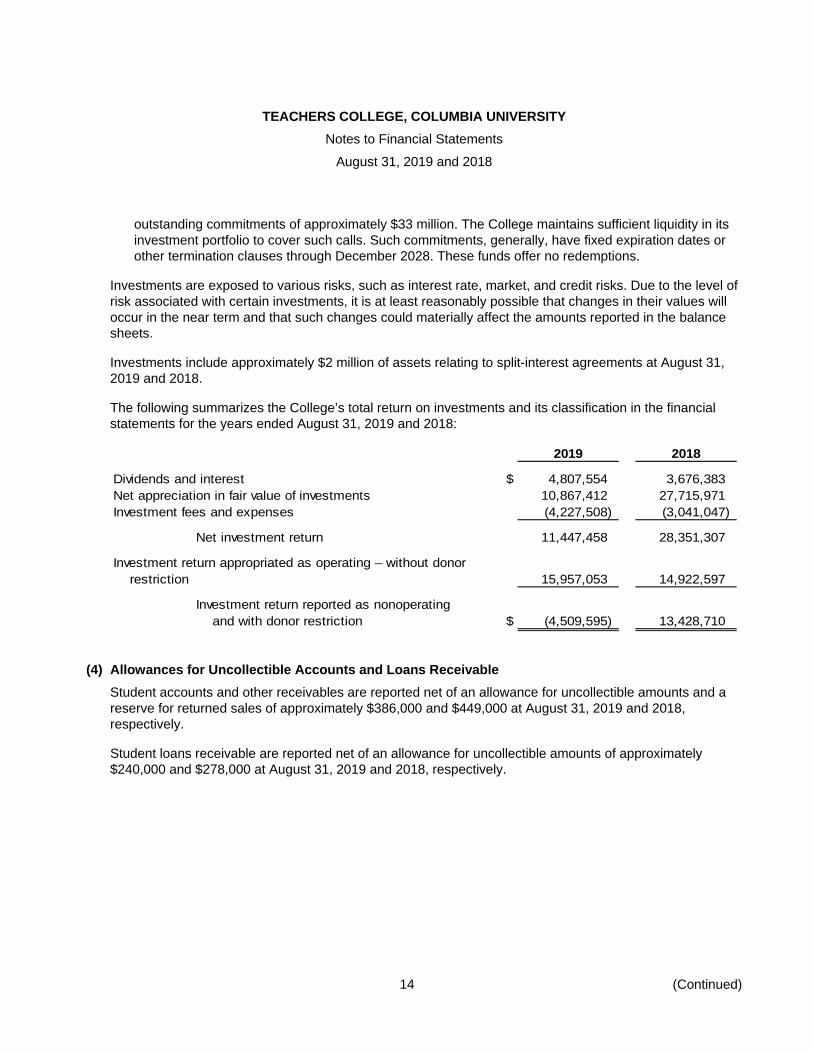

outstanding commitments of approximately $33 million. The College maintains sufficient liquidity in its investment portfolio to cover such calls. Such commitments, generally, have fixed expiration dates or other termination clauses through December 2028. These funds offer no redemptions.

Investments are exposed to various risks, such as interest rate, market, and credit risks. Due to the level of risk associated with certain investments, it is at least reasonably possible that changes in their values will occur in the near term and that such changes could materially affect the amounts reported in the balance sheets.

Investments include approximately $2 million of assets relating to split-interest agreements at August 31, 2019 and 2018.

The following summarizes the College’s total return on investments and its classification in the financial statements for the years ended August 31, 2019 and 2018:

2019 2018

Dividends and interest $ 4,807,554 3,676,383 Net appreciation in fair value of investments 10,867,412 27,715,971 Investment fees and expenses (4,227,508) (3,041,047)

Net investment return 11,447,458 28,351,307

Investment return appropriated as operating – without donorrestriction 15,957,053 14,922,597

Investment return reported as nonoperatingand with donor restriction $ (4,509,595) 13,428,710

(4) Allowances for Uncollectible Accounts and Loans Receivable Student accounts and other receivables are reported net of an allowance for uncollectible amounts and a reserve for returned sales of approximately $386,000 and $449,000 at August 31, 2019 and 2018, respectively.

Student loans receivable are reported net of an allowance for uncollectible amounts of approximately $240,000 and $278,000 at August 31, 2019 and 2018, respectively.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

15 (Continued)

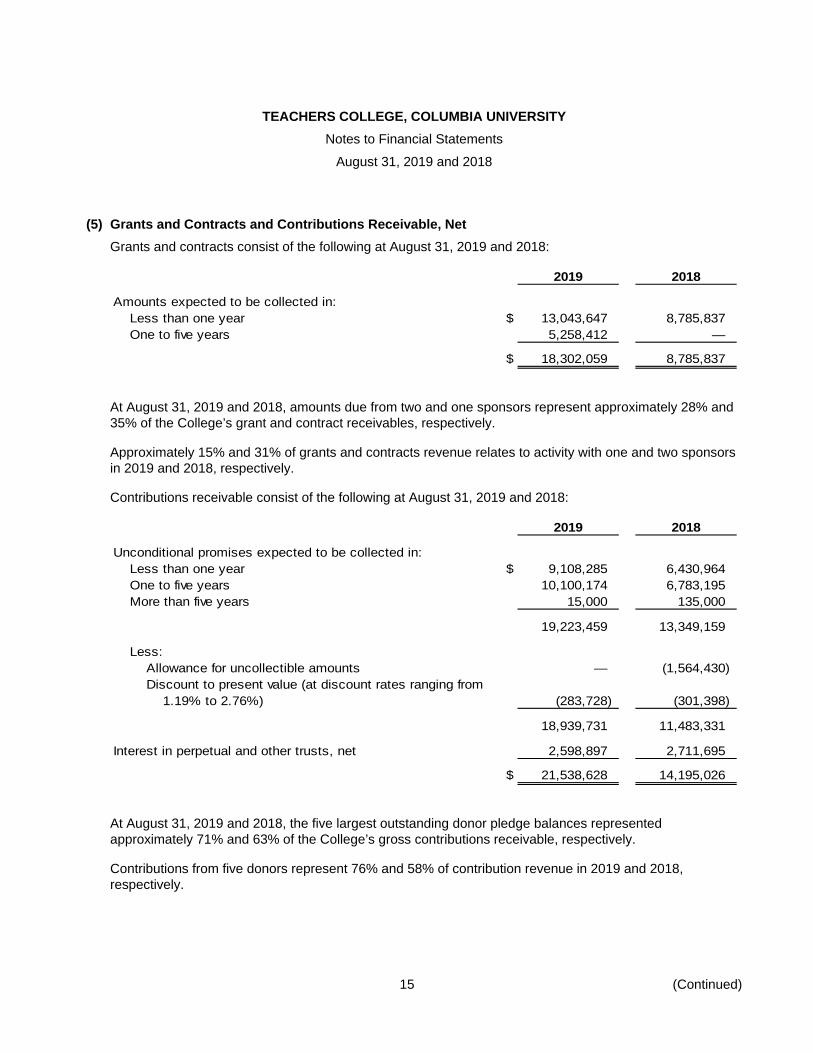

(5) Grants and Contracts and Contributions Receivable, Net Grants and contracts consist of the following at August 31, 2019 and 2018:

2019 2018

Amounts expected to be collected in:Less than one year $ 13,043,647 8,785,837 One to five years 5,258,412 —

$ 18,302,059 8,785,837

At August 31, 2019 and 2018, amounts due from two and one sponsors represent approximately 28% and 35% of the College’s grant and contract receivables, respectively.

Approximately 15% and 31% of grants and contracts revenue relates to activity with one and two sponsors in 2019 and 2018, respectively.

Contributions receivable consist of the following at August 31, 2019 and 2018:

2019 2018

Unconditional promises expected to be collected in:Less than one year $ 9,108,285 6,430,964 One to five years 10,100,174 6,783,195 More than five years 15,000 135,000

19,223,459 13,349,159

Less:Allowance for uncollectible amounts — (1,564,430) Discount to present value (at discount rates ranging from

1.19% to 2.76%) (283,728) (301,398)

18,939,731 11,483,331

Interest in perpetual and other trusts, net 2,598,897 2,711,695

$ 21,538,628 14,195,026

At August 31, 2019 and 2018, the five largest outstanding donor pledge balances represented approximately 71% and 63% of the College’s gross contributions receivable, respectively.

Contributions from five donors represent 76% and 58% of contribution revenue in 2019 and 2018, respectively.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

16 (Continued)

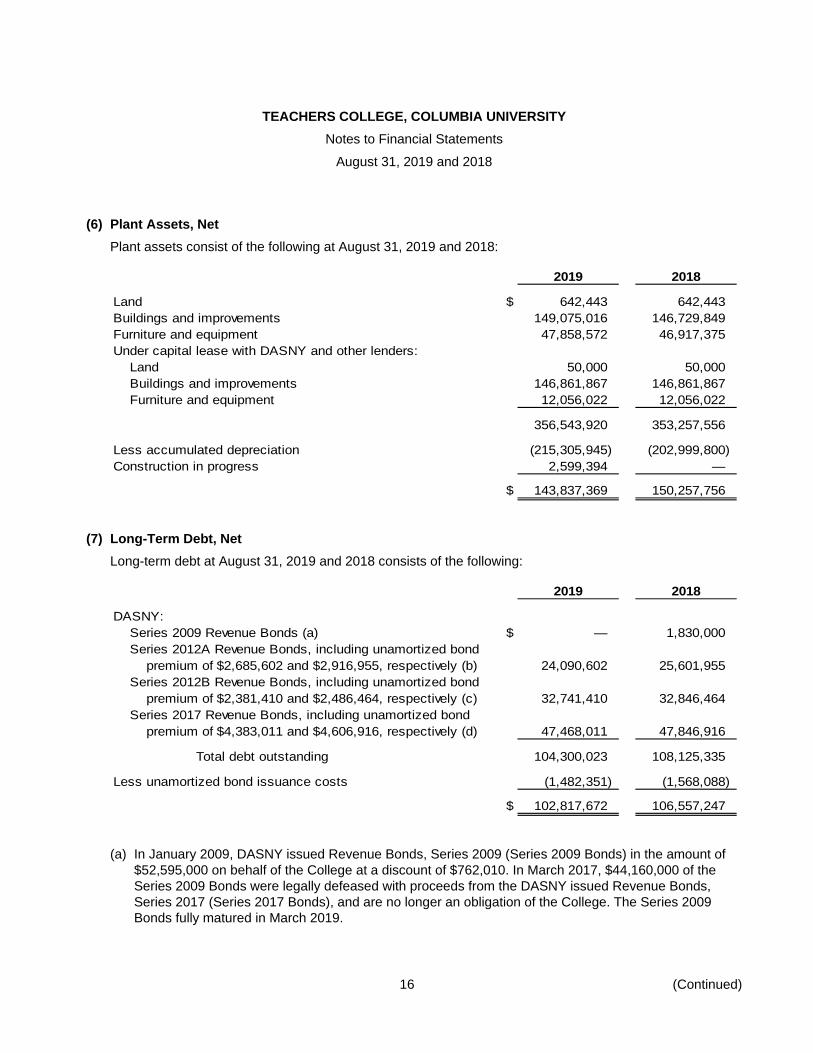

(6) Plant Assets, Net Plant assets consist of the following at August 31, 2019 and 2018:

2019 2018

Land $ 642,443 642,443 Buildings and improvements 149,075,016 146,729,849 Furniture and equipment 47,858,572 46,917,375 Under capital lease with DASNY and other lenders:

Land 50,000 50,000 Buildings and improvements 146,861,867 146,861,867 Furniture and equipment 12,056,022 12,056,022

356,543,920 353,257,556

Less accumulated depreciation (215,305,945) (202,999,800) Construction in progress 2,599,394 —

$ 143,837,369 150,257,756

(7) Long-Term Debt, Net Long-term debt at August 31, 2019 and 2018 consists of the following:

2019 2018

DASNY:Series 2009 Revenue Bonds (a) $ — 1,830,000 Series 2012A Revenue Bonds, including unamortized bond

premium of $2,685,602 and $2,916,955, respectively (b) 24,090,602 25,601,955 Series 2012B Revenue Bonds, including unamortized bond

premium of $2,381,410 and $2,486,464, respectively (c) 32,741,410 32,846,464 Series 2017 Revenue Bonds, including unamortized bond

premium of $4,383,011 and $4,606,916, respectively (d) 47,468,011 47,846,916

Total debt outstanding 104,300,023 108,125,335

Less unamortized bond issuance costs (1,482,351) (1,568,088)

$ 102,817,672 106,557,247

(a) In January 2009, DASNY issued Revenue Bonds, Series 2009 (Series 2009 Bonds) in the amount of $52,595,000 on behalf of the College at a discount of $762,010. In March 2017, $44,160,000 of the Series 2009 Bonds were legally defeased with proceeds from the DASNY issued Revenue Bonds, Series 2017 (Series 2017 Bonds), and are no longer an obligation of the College. The Series 2009 Bonds fully matured in March 2019.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

17 (Continued)

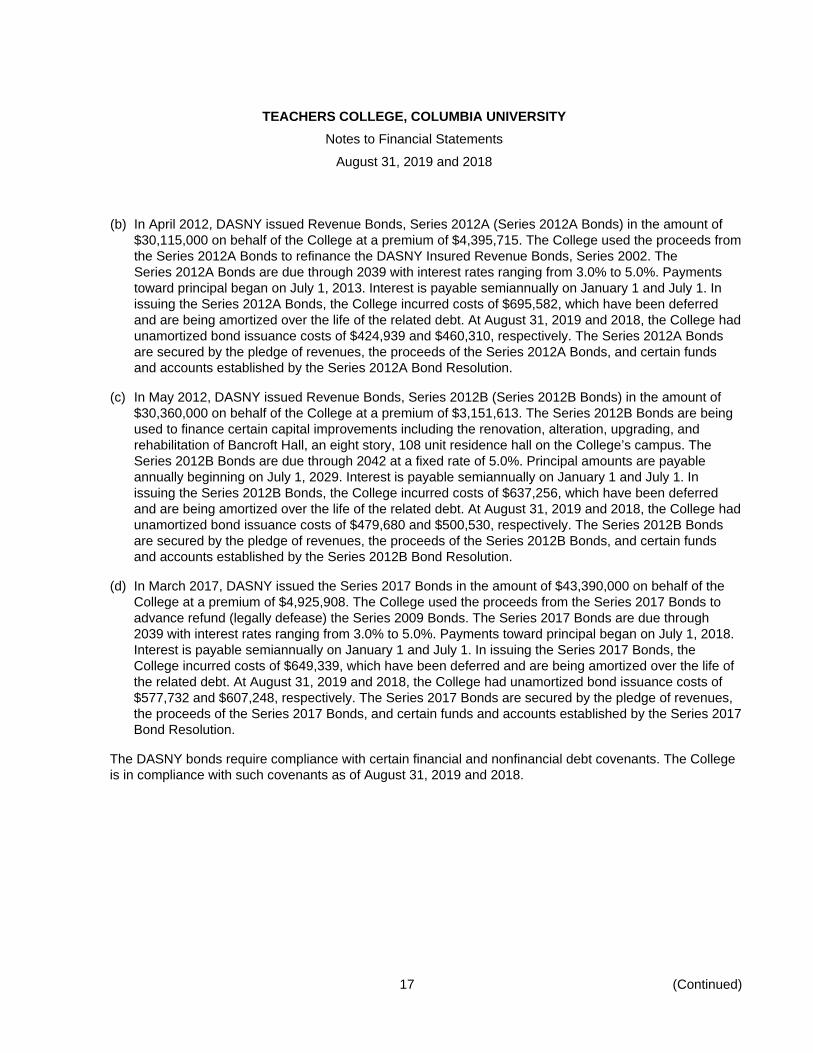

(b) In April 2012, DASNY issued Revenue Bonds, Series 2012A (Series 2012A Bonds) in the amount of $30,115,000 on behalf of the College at a premium of $4,395,715. The College used the proceeds from the Series 2012A Bonds to refinance the DASNY Insured Revenue Bonds, Series 2002. The Series 2012A Bonds are due through 2039 with interest rates ranging from 3.0% to 5.0%. Payments toward principal began on July 1, 2013. Interest is payable semiannually on January 1 and July 1. In issuing the Series 2012A Bonds, the College incurred costs of $695,582, which have been deferred and are being amortized over the life of the related debt. At August 31, 2019 and 2018, the College had unamortized bond issuance costs of $424,939 and $460,310, respectively. The Series 2012A Bonds are secured by the pledge of revenues, the proceeds of the Series 2012A Bonds, and certain funds and accounts established by the Series 2012A Bond Resolution.

(c) In May 2012, DASNY issued Revenue Bonds, Series 2012B (Series 2012B Bonds) in the amount of $30,360,000 on behalf of the College at a premium of $3,151,613. The Series 2012B Bonds are being used to finance certain capital improvements including the renovation, alteration, upgrading, and rehabilitation of Bancroft Hall, an eight story, 108 unit residence hall on the College’s campus. The Series 2012B Bonds are due through 2042 at a fixed rate of 5.0%. Principal amounts are payable annually beginning on July 1, 2029. Interest is payable semiannually on January 1 and July 1. In issuing the Series 2012B Bonds, the College incurred costs of $637,256, which have been deferred and are being amortized over the life of the related debt. At August 31, 2019 and 2018, the College had unamortized bond issuance costs of $479,680 and $500,530, respectively. The Series 2012B Bonds are secured by the pledge of revenues, the proceeds of the Series 2012B Bonds, and certain funds and accounts established by the Series 2012B Bond Resolution.

(d) In March 2017, DASNY issued the Series 2017 Bonds in the amount of $43,390,000 on behalf of the College at a premium of $4,925,908. The College used the proceeds from the Series 2017 Bonds to advance refund (legally defease) the Series 2009 Bonds. The Series 2017 Bonds are due through 2039 with interest rates ranging from 3.0% to 5.0%. Payments toward principal began on July 1, 2018. Interest is payable semiannually on January 1 and July 1. In issuing the Series 2017 Bonds, the College incurred costs of $649,339, which have been deferred and are being amortized over the life of the related debt. At August 31, 2019 and 2018, the College had unamortized bond issuance costs of $577,732 and $607,248, respectively. The Series 2017 Bonds are secured by the pledge of revenues, the proceeds of the Series 2017 Bonds, and certain funds and accounts established by the Series 2017 Bond Resolution.

The DASNY bonds require compliance with certain financial and nonfinancial debt covenants. The College is in compliance with such covenants as of August 31, 2019 and 2018.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

18 (Continued)

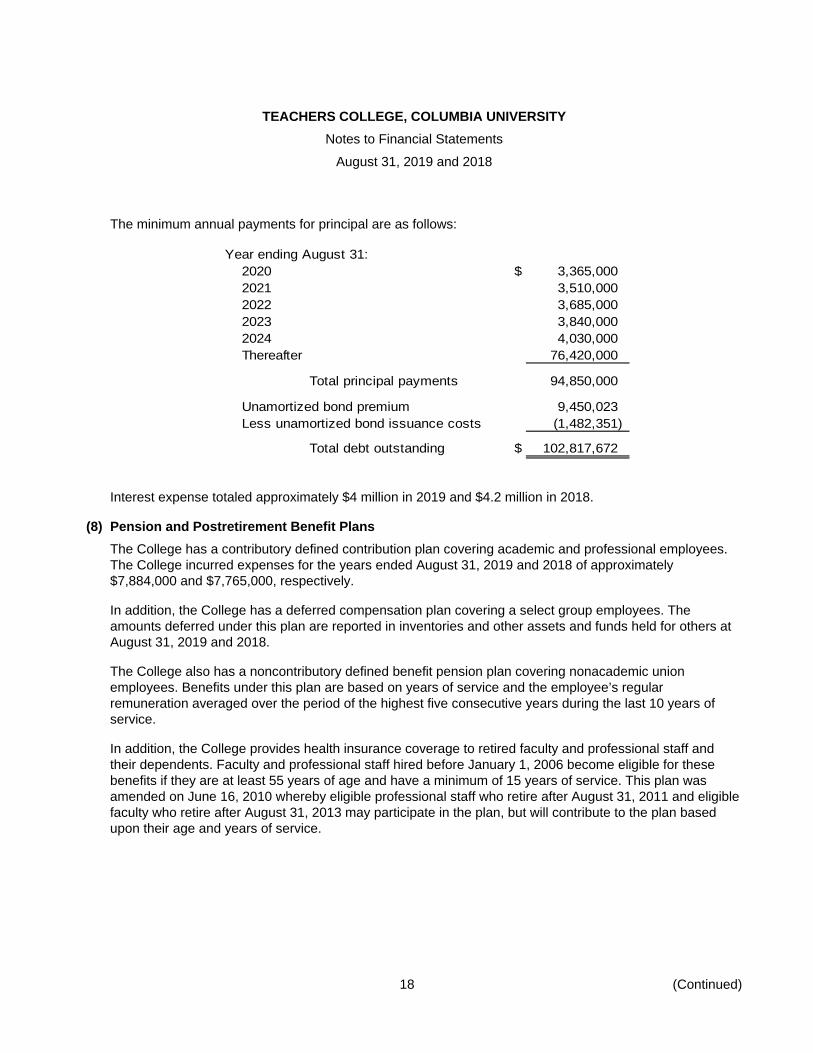

The minimum annual payments for principal are as follows:

Year ending August 31:2020 $ 3,365,000 2021 3,510,000 2022 3,685,000 2023 3,840,000 2024 4,030,000 Thereafter 76,420,000

Total principal payments 94,850,000

Unamortized bond premium 9,450,023 Less unamortized bond issuance costs (1,482,351)

Total debt outstanding $ 102,817,672

Interest expense totaled approximately $4 million in 2019 and $4.2 million in 2018.

(8) Pension and Postretirement Benefit Plans The College has a contributory defined contribution plan covering academic and professional employees. The College incurred expenses for the years ended August 31, 2019 and 2018 of approximately $7,884,000 and $7,765,000, respectively.

In addition, the College has a deferred compensation plan covering a select group employees. The amounts deferred under this plan are reported in inventories and other assets and funds held for others at August 31, 2019 and 2018.

The College also has a noncontributory defined benefit pension plan covering nonacademic union employees. Benefits under this plan are based on years of service and the employee’s regular remuneration averaged over the period of the highest five consecutive years during the last 10 years of service.

In addition, the College provides health insurance coverage to retired faculty and professional staff and their dependents. Faculty and professional staff hired before January 1, 2006 become eligible for these benefits if they are at least 55 years of age and have a minimum of 15 years of service. This plan was amended on June 16, 2010 whereby eligible professional staff who retire after August 31, 2011 and eligible faculty who retire after August 31, 2013 may participate in the plan, but will contribute to the plan based upon their age and years of service.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

19 (Continued)

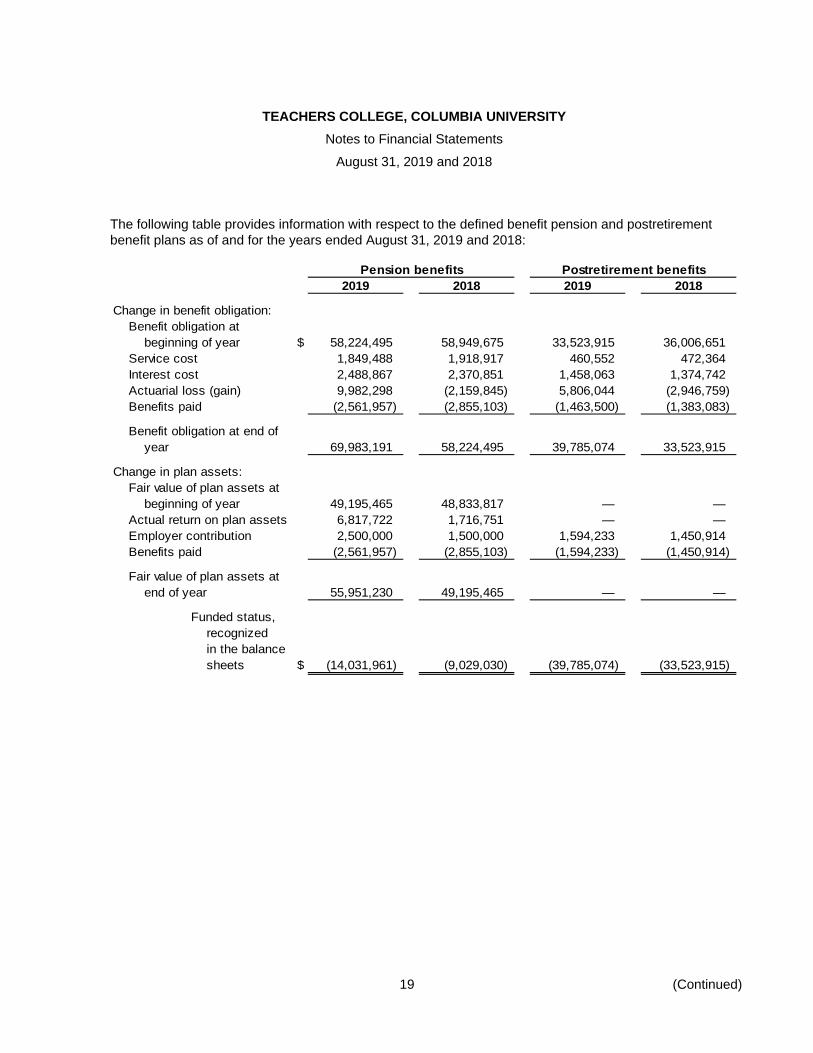

The following table provides information with respect to the defined benefit pension and postretirement benefit plans as of and for the years ended August 31, 2019 and 2018:

Pension benefits Postretirement benefits2019 2018 2019 2018

Change in benefit obligation:Benefit obligation at

beginning of year $ 58,224,495 58,949,675 33,523,915 36,006,651 Service cost 1,849,488 1,918,917 460,552 472,364 Interest cost 2,488,867 2,370,851 1,458,063 1,374,742 Actuarial loss (gain) 9,982,298 (2,159,845) 5,806,044 (2,946,759) Benefits paid (2,561,957) (2,855,103) (1,463,500) (1,383,083)

Benefit obligation at end ofyear 69,983,191 58,224,495 39,785,074 33,523,915

Change in plan assets:Fair value of plan assets at

beginning of year 49,195,465 48,833,817 — — Actual return on plan assets 6,817,722 1,716,751 — — Employer contribution 2,500,000 1,500,000 1,594,233 1,450,914 Benefits paid (2,561,957) (2,855,103) (1,594,233) (1,450,914)

Fair value of plan assets atend of year 55,951,230 49,195,465 — —

Funded status,recognizedin the balancesheets $ (14,031,961) (9,029,030) (39,785,074) (33,523,915)

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

20 (Continued)

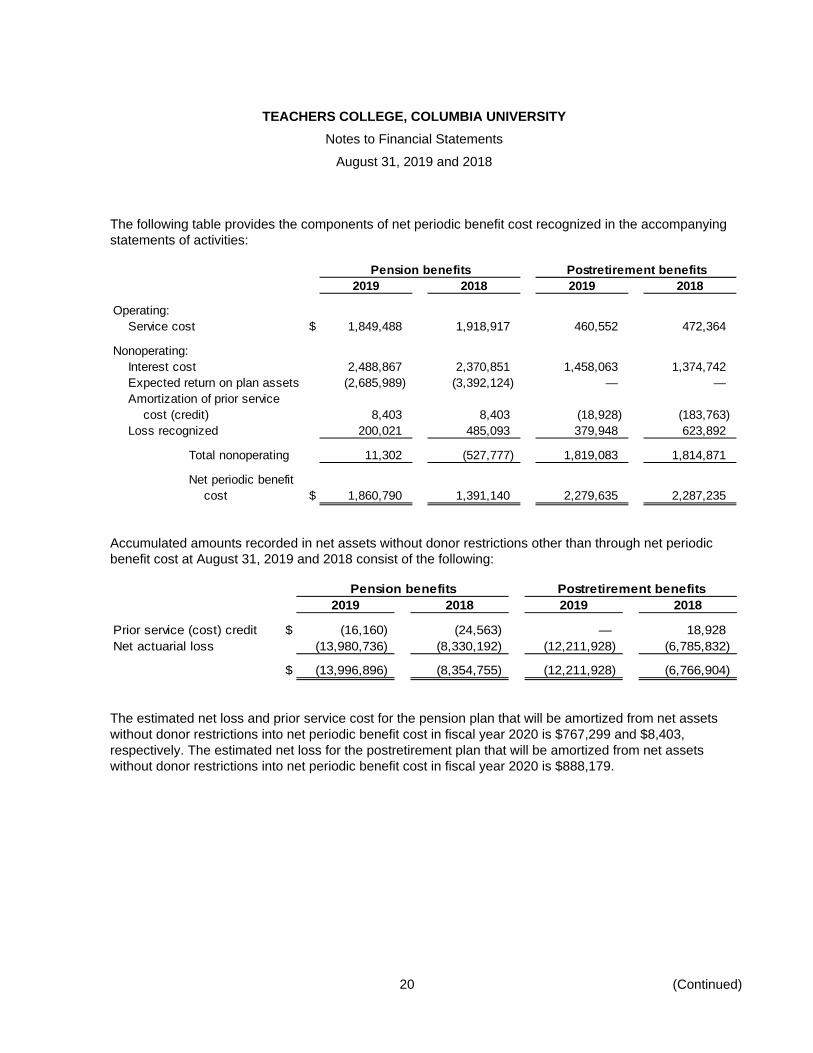

The following table provides the components of net periodic benefit cost recognized in the accompanying statements of activities:

Pension benefits Postretirement benefits2019 2018 2019 2018

Operating:Service cost $ 1,849,488 1,918,917 460,552 472,364

Nonoperating:Interest cost 2,488,867 2,370,851 1,458,063 1,374,742 Expected return on plan assets (2,685,989) (3,392,124) — — Amortization of prior service

cost (credit) 8,403 8,403 (18,928) (183,763) Loss recognized 200,021 485,093 379,948 623,892

Total nonoperating 11,302 (527,777) 1,819,083 1,814,871

Net periodic benefitcost $ 1,860,790 1,391,140 2,279,635 2,287,235

Accumulated amounts recorded in net assets without donor restrictions other than through net periodic benefit cost at August 31, 2019 and 2018 consist of the following:

Pension benefits Postretirement benefits2019 2018 2019 2018

Prior service (cost) credit $ (16,160) (24,563) — 18,928 Net actuarial loss (13,980,736) (8,330,192) (12,211,928) (6,785,832)

$ (13,996,896) (8,354,755) (12,211,928) (6,766,904)

The estimated net loss and prior service cost for the pension plan that will be amortized from net assets without donor restrictions into net periodic benefit cost in fiscal year 2020 is $767,299 and $8,403, respectively. The estimated net loss for the postretirement plan that will be amortized from net assets without donor restrictions into net periodic benefit cost in fiscal year 2020 is $888,179.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

21 (Continued)

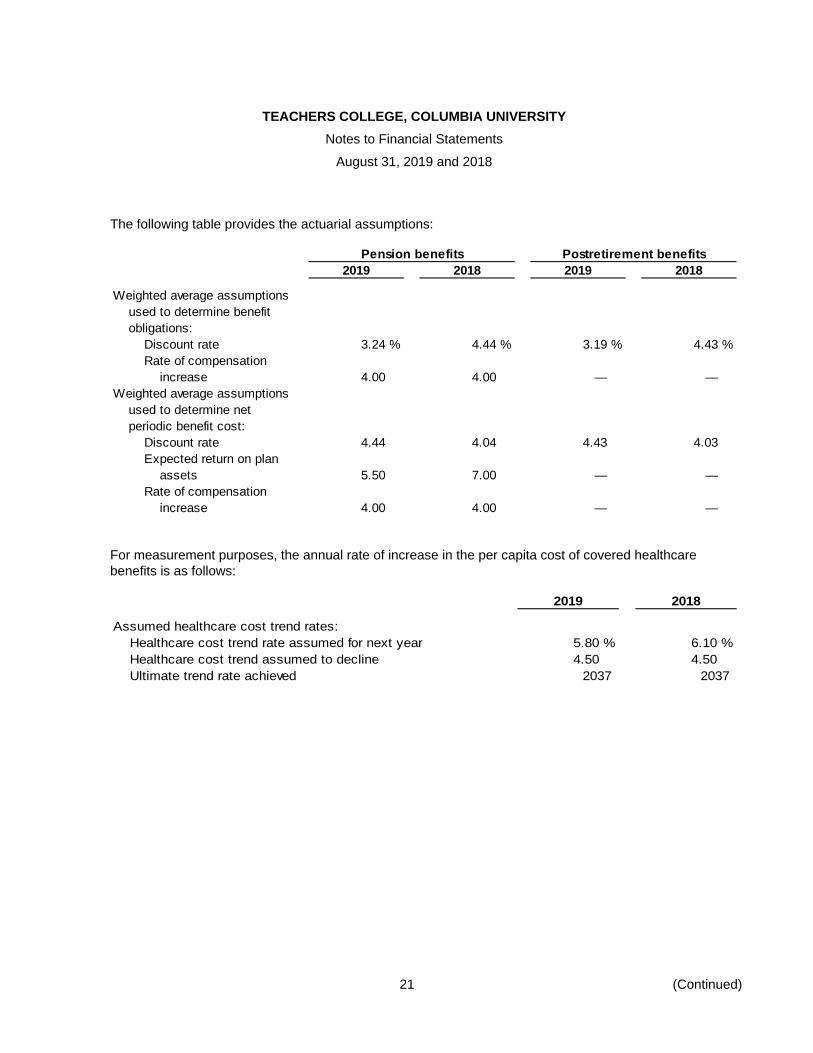

The following table provides the actuarial assumptions:

Pension benefits Postretirement benefits2019 2018 2019 2018

Weighted average assumptionsused to determine benefitobligations:

Discount rate 3.24 % 4.44 % 3.19 % 4.43 %Rate of compensation

increase 4.00 4.00 — —Weighted average assumptions

used to determine netperiodic benefit cost:

Discount rate 4.44 4.04 4.43 4.03Expected return on plan

assets 5.50 7.00 — —Rate of compensation

increase 4.00 4.00 — —

For measurement purposes, the annual rate of increase in the per capita cost of covered healthcare benefits is as follows:

2019 2018

Assumed healthcare cost trend rates:Healthcare cost trend rate assumed for next year 5.80 % 6.10 %Healthcare cost trend assumed to decline 4.50 4.50Ultimate trend rate achieved 2037 2037

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

22 (Continued)

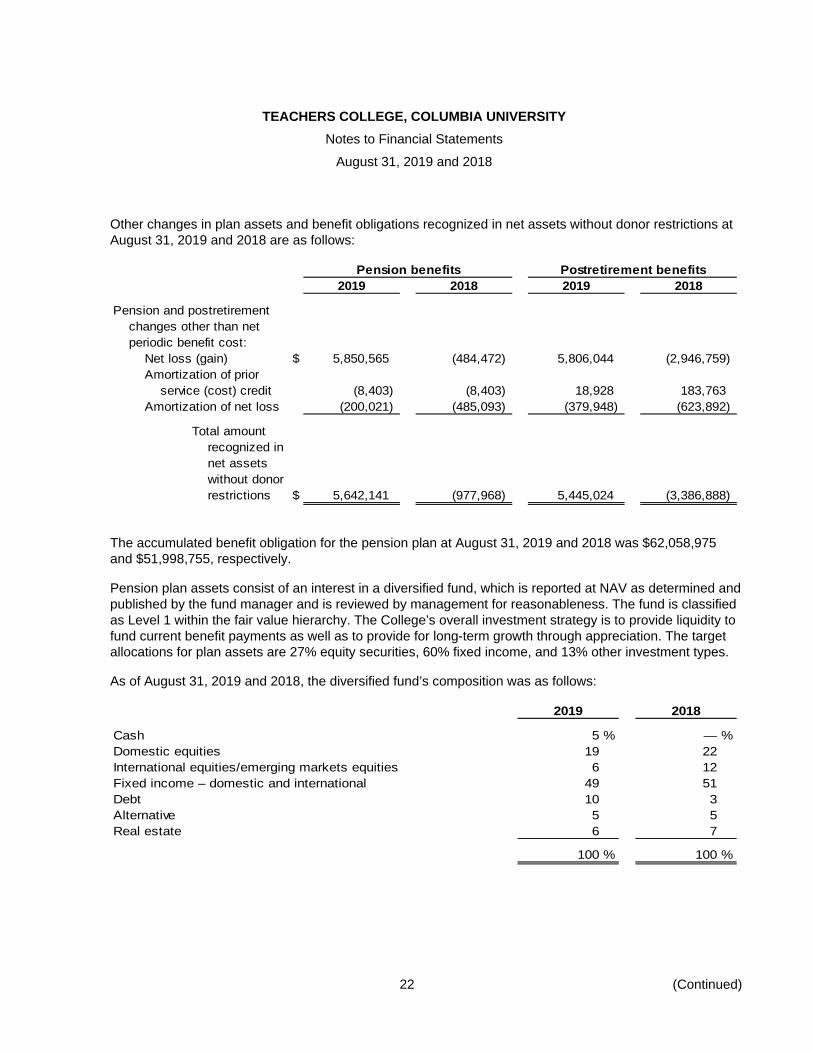

Other changes in plan assets and benefit obligations recognized in net assets without donor restrictions at August 31, 2019 and 2018 are as follows:

Pension benefits Postretirement benefits2019 2018 2019 2018

Pension and postretirementchanges other than netperiodic benefit cost:

Net loss (gain) $ 5,850,565 (484,472) 5,806,044 (2,946,759) Amortization of prior

service (cost) credit (8,403) (8,403) 18,928 183,763 Amortization of net loss (200,021) (485,093) (379,948) (623,892)

Total amountrecognized innet assetswithout donorrestrictions $ 5,642,141 (977,968) 5,445,024 (3,386,888)

The accumulated benefit obligation for the pension plan at August 31, 2019 and 2018 was $62,058,975 and $51,998,755, respectively.

Pension plan assets consist of an interest in a diversified fund, which is reported at NAV as determined and published by the fund manager and is reviewed by management for reasonableness. The fund is classified as Level 1 within the fair value hierarchy. The College’s overall investment strategy is to provide liquidity to fund current benefit payments as well as to provide for long-term growth through appreciation. The target allocations for plan assets are 27% equity securities, 60% fixed income, and 13% other investment types.

As of August 31, 2019 and 2018, the diversified fund’s composition was as follows:

2019 2018

Cash 5 % — %Domestic equities 19 22International equities/emerging markets equities 6 12Fixed income – domestic and international 49 51Debt 10 3Alternative 5 5Real estate 6 7

100 % 100 %

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

23 (Continued)

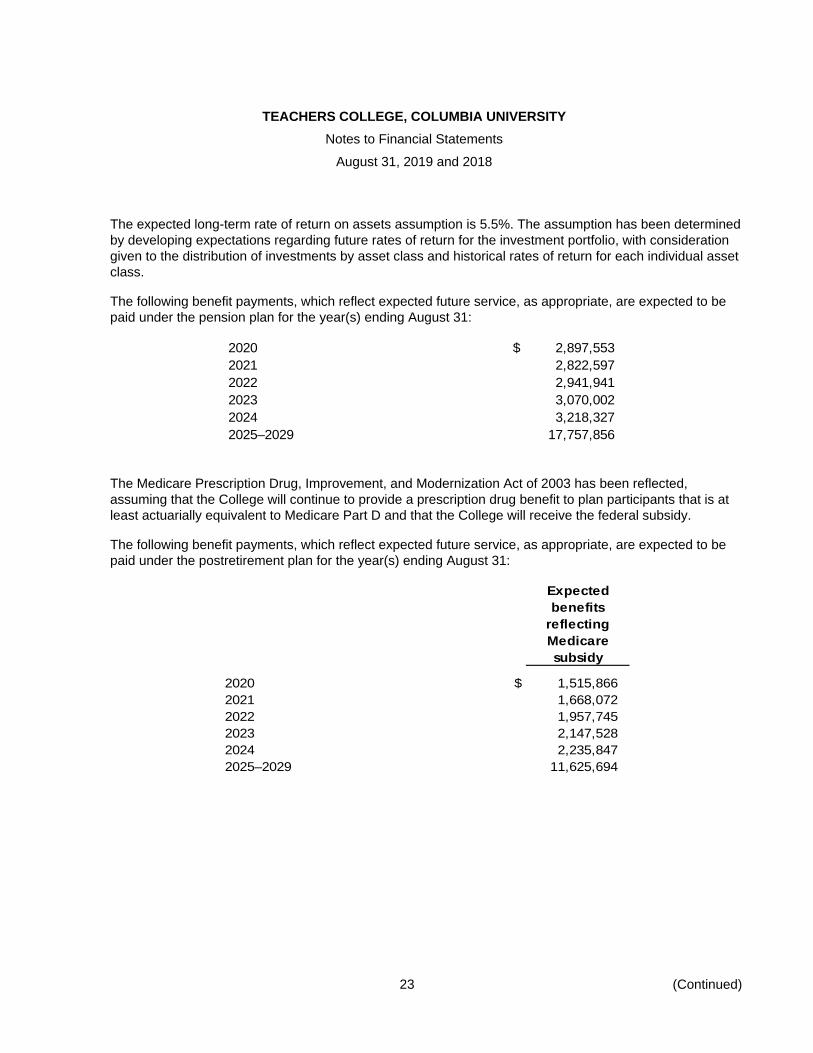

The expected long-term rate of return on assets assumption is 5.5%. The assumption has been determined by developing expectations regarding future rates of return for the investment portfolio, with consideration given to the distribution of investments by asset class and historical rates of return for each individual asset class.

The following benefit payments, which reflect expected future service, as appropriate, are expected to be paid under the pension plan for the year(s) ending August 31:

2020 $ 2,897,553 2021 2,822,597 2022 2,941,941 2023 3,070,002 2024 3,218,327 2025–2029 17,757,856

The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 has been reflected, assuming that the College will continue to provide a prescription drug benefit to plan participants that is at least actuarially equivalent to Medicare Part D and that the College will receive the federal subsidy.

The following benefit payments, which reflect expected future service, as appropriate, are expected to be paid under the postretirement plan for the year(s) ending August 31:

Expectedbenefits

reflectingMedicaresubsidy

2020 $ 1,515,866 2021 1,668,072 2022 1,957,745 2023 2,147,528 2024 2,235,847 2025–2029 11,625,694

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

24 (Continued)

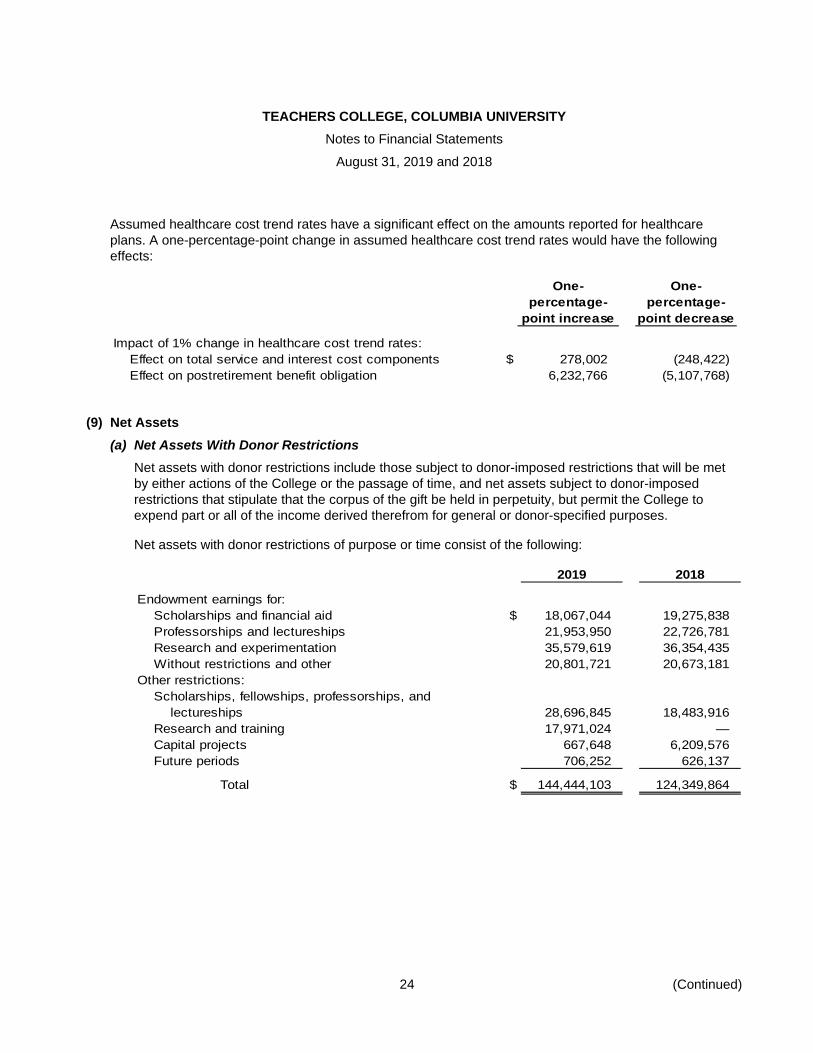

Assumed healthcare cost trend rates have a significant effect on the amounts reported for healthcare plans. A one-percentage-point change in assumed healthcare cost trend rates would have the following effects:

One- One-percentage- percentage-

point increase point decrease

Impact of 1% change in healthcare cost trend rates:Effect on total service and interest cost components $ 278,002 (248,422) Effect on postretirement benefit obligation 6,232,766 (5,107,768)

(9) Net Assets (a) Net Assets With Donor Restrictions

Net assets with donor restrictions include those subject to donor-imposed restrictions that will be met by either actions of the College or the passage of time, and net assets subject to donor-imposed restrictions that stipulate that the corpus of the gift be held in perpetuity, but permit the College to expend part or all of the income derived therefrom for general or donor-specified purposes.

Net assets with donor restrictions of purpose or time consist of the following:

2019 2018

Endowment earnings for:Scholarships and financial aid $ 18,067,044 19,275,838 Professorships and lectureships 21,953,950 22,726,781 Research and experimentation 35,579,619 36,354,435 Without restrictions and other 20,801,721 20,673,181

Other restrictions:Scholarships, fellowships, professorships, and

lectureships 28,696,845 18,483,916 Research and training 17,971,024 — Capital projects 667,648 6,209,576 Future periods 706,252 626,137

Total $ 144,444,103 124,349,864

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

25 (Continued)

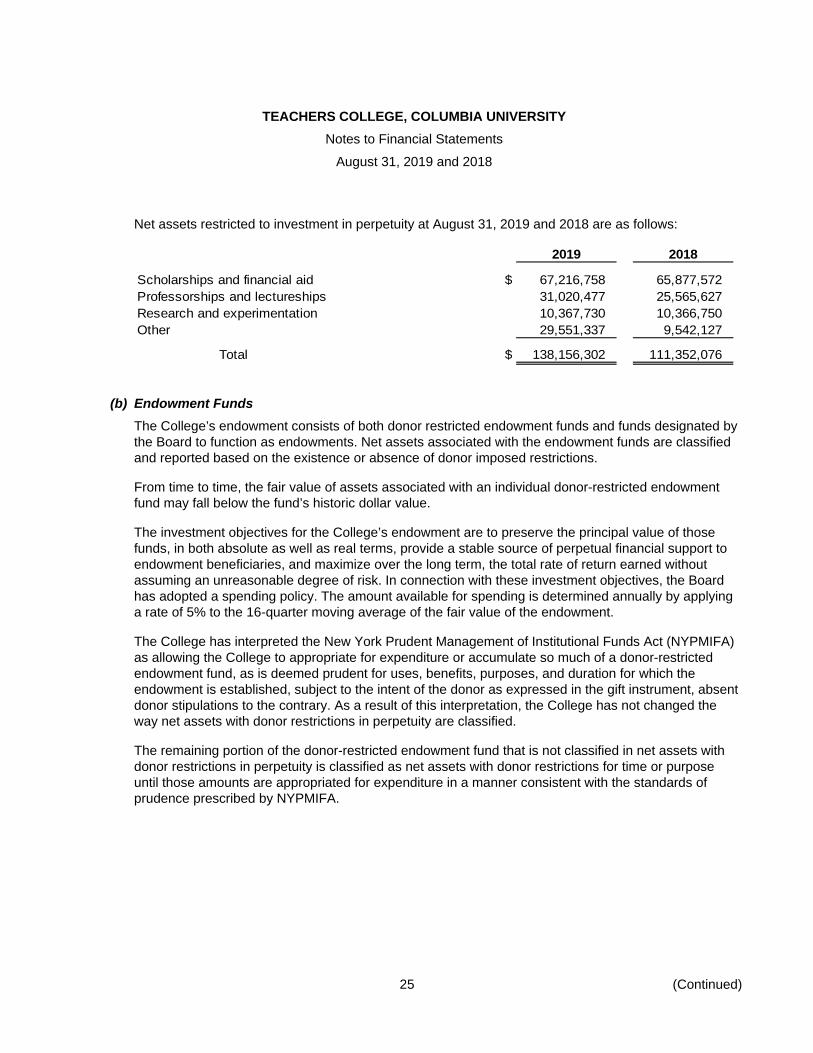

Net assets restricted to investment in perpetuity at August 31, 2019 and 2018 are as follows:

2019 2018

Scholarships and financial aid $ 67,216,758 65,877,572 Professorships and lectureships 31,020,477 25,565,627 Research and experimentation 10,367,730 10,366,750 Other 29,551,337 9,542,127

Total $ 138,156,302 111,352,076

(b) Endowment Funds The College’s endowment consists of both donor restricted endowment funds and funds designated by the Board to function as endowments. Net assets associated with the endowment funds are classified and reported based on the existence or absence of donor imposed restrictions.

From time to time, the fair value of assets associated with an individual donor-restricted endowment fund may fall below the fund’s historic dollar value.

The investment objectives for the College’s endowment are to preserve the principal value of those funds, in both absolute as well as real terms, provide a stable source of perpetual financial support to endowment beneficiaries, and maximize over the long term, the total rate of return earned without assuming an unreasonable degree of risk. In connection with these investment objectives, the Board has adopted a spending policy. The amount available for spending is determined annually by applying a rate of 5% to the 16-quarter moving average of the fair value of the endowment.

The College has interpreted the New York Prudent Management of Institutional Funds Act (NYPMIFA) as allowing the College to appropriate for expenditure or accumulate so much of a donor-restricted endowment fund, as is deemed prudent for uses, benefits, purposes, and duration for which the endowment is established, subject to the intent of the donor as expressed in the gift instrument, absent donor stipulations to the contrary. As a result of this interpretation, the College has not changed the way net assets with donor restrictions in perpetuity are classified.

The remaining portion of the donor-restricted endowment fund that is not classified in net assets with donor restrictions in perpetuity is classified as net assets with donor restrictions for time or purpose until those amounts are appropriated for expenditure in a manner consistent with the standards of prudence prescribed by NYPMIFA.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

26 (Continued)

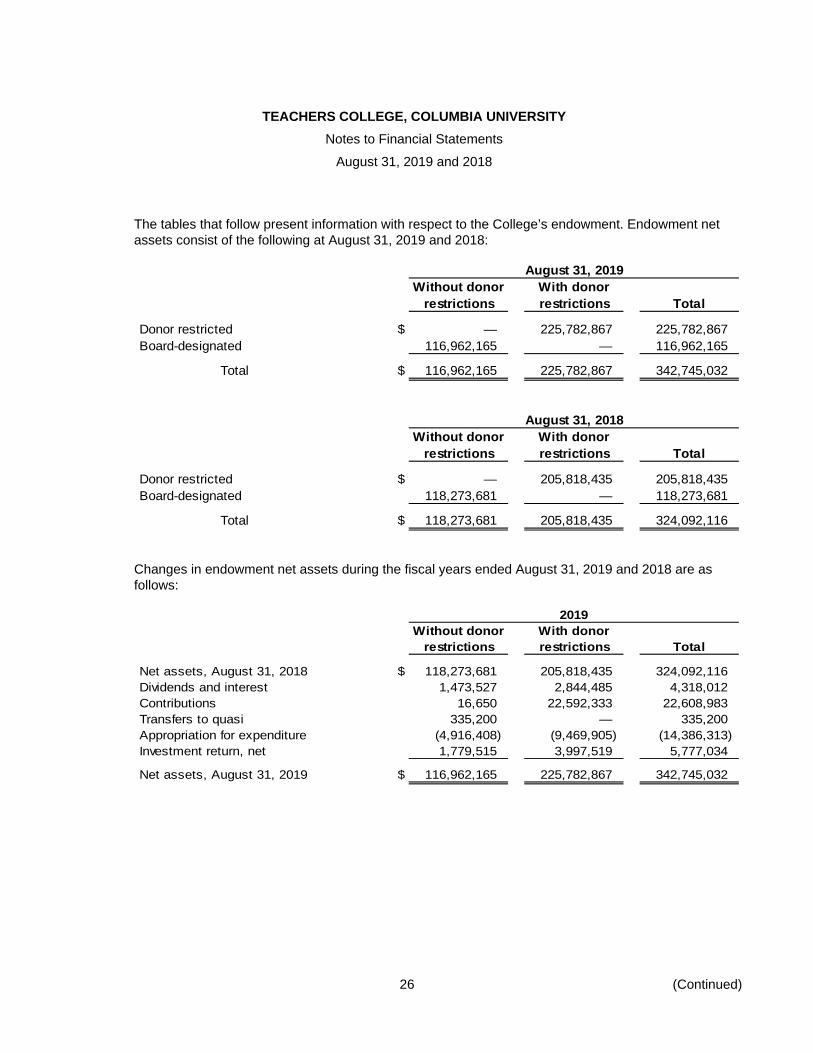

The tables that follow present information with respect to the College’s endowment. Endowment net assets consist of the following at August 31, 2019 and 2018:

August 31, 2019Without donor With donor

restrictions restrictions Total

Donor restricted $ — 225,782,867 225,782,867 Board-designated 116,962,165 — 116,962,165

Total $ 116,962,165 225,782,867 342,745,032

August 31, 2018Without donor With donor

restrictions restrictions Total

Donor restricted $ — 205,818,435 205,818,435 Board-designated 118,273,681 — 118,273,681

Total $ 118,273,681 205,818,435 324,092,116

Changes in endowment net assets during the fiscal years ended August 31, 2019 and 2018 are as follows:

2019Without donor With donor

restrictions restrictions Total

Net assets, August 31, 2018 $ 118,273,681 205,818,435 324,092,116 Dividends and interest 1,473,527 2,844,485 4,318,012 Contributions 16,650 22,592,333 22,608,983 Transfers to quasi 335,200 — 335,200 Appropriation for expenditure (4,916,408) (9,469,905) (14,386,313) Investment return, net 1,779,515 3,997,519 5,777,034

Net assets, August 31, 2019 $ 116,962,165 225,782,867 342,745,032

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

27 (Continued)

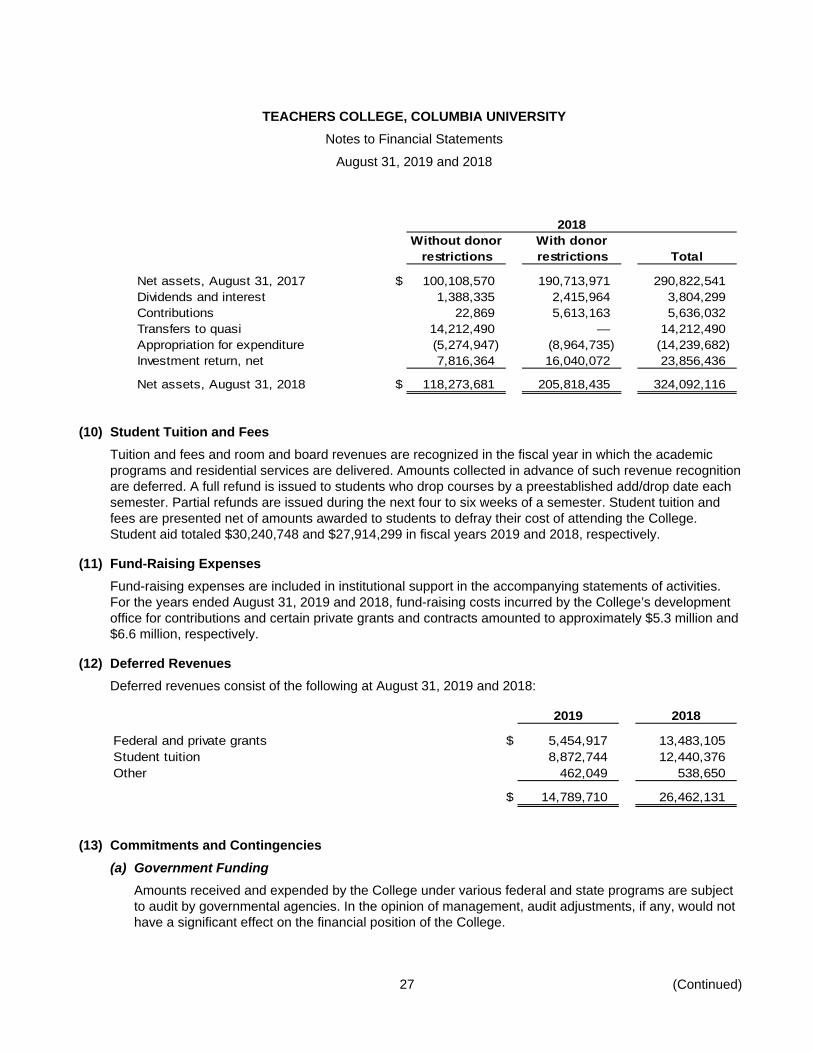

2018Without donor With donor

restrictions restrictions Total

Net assets, August 31, 2017 $ 100,108,570 190,713,971 290,822,541 Dividends and interest 1,388,335 2,415,964 3,804,299 Contributions 22,869 5,613,163 5,636,032 Transfers to quasi 14,212,490 — 14,212,490 Appropriation for expenditure (5,274,947) (8,964,735) (14,239,682) Investment return, net 7,816,364 16,040,072 23,856,436

Net assets, August 31, 2018 $ 118,273,681 205,818,435 324,092,116

(10) Student Tuition and Fees Tuition and fees and room and board revenues are recognized in the fiscal year in which the academic programs and residential services are delivered. Amounts collected in advance of such revenue recognition are deferred. A full refund is issued to students who drop courses by a preestablished add/drop date each semester. Partial refunds are issued during the next four to six weeks of a semester. Student tuition and fees are presented net of amounts awarded to students to defray their cost of attending the College. Student aid totaled $30,240,748 and $27,914,299 in fiscal years 2019 and 2018, respectively.

(11) Fund-Raising Expenses Fund-raising expenses are included in institutional support in the accompanying statements of activities. For the years ended August 31, 2019 and 2018, fund-raising costs incurred by the College’s development office for contributions and certain private grants and contracts amounted to approximately $5.3 million and $6.6 million, respectively.

(12) Deferred Revenues Deferred revenues consist of the following at August 31, 2019 and 2018:

2019 2018

Federal and private grants $ 5,454,917 13,483,105 Student tuition 8,872,744 12,440,376 Other 462,049 538,650

$ 14,789,710 26,462,131

(13) Commitments and Contingencies (a) Government Funding

Amounts received and expended by the College under various federal and state programs are subject to audit by governmental agencies. In the opinion of management, audit adjustments, if any, would not have a significant effect on the financial position of the College.

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

28 (Continued)

(b) Line of Credit The College has a credit arrangement with a bank that provides for a line of credit, up to $20 million through June 2020, which was not drawn upon during the year ended August 31, 2019. Borrowings under the line of credit facility will bear interest at the one, two or three-month LIBOR plus 0.3%. Additionally, the College entered an agreement with a bank for an annual letter of credit up to $300,000, which automatically renews September of each year unless the issuing bank provides termination notification.

(c) Litigation The College, in the normal course of its operations, is a defendant in various lawsuits. While it is not feasible to predict the ultimate outcomes, management of the College does not expect the resolution of these actions to have a material adverse effect on the College’s financial position.

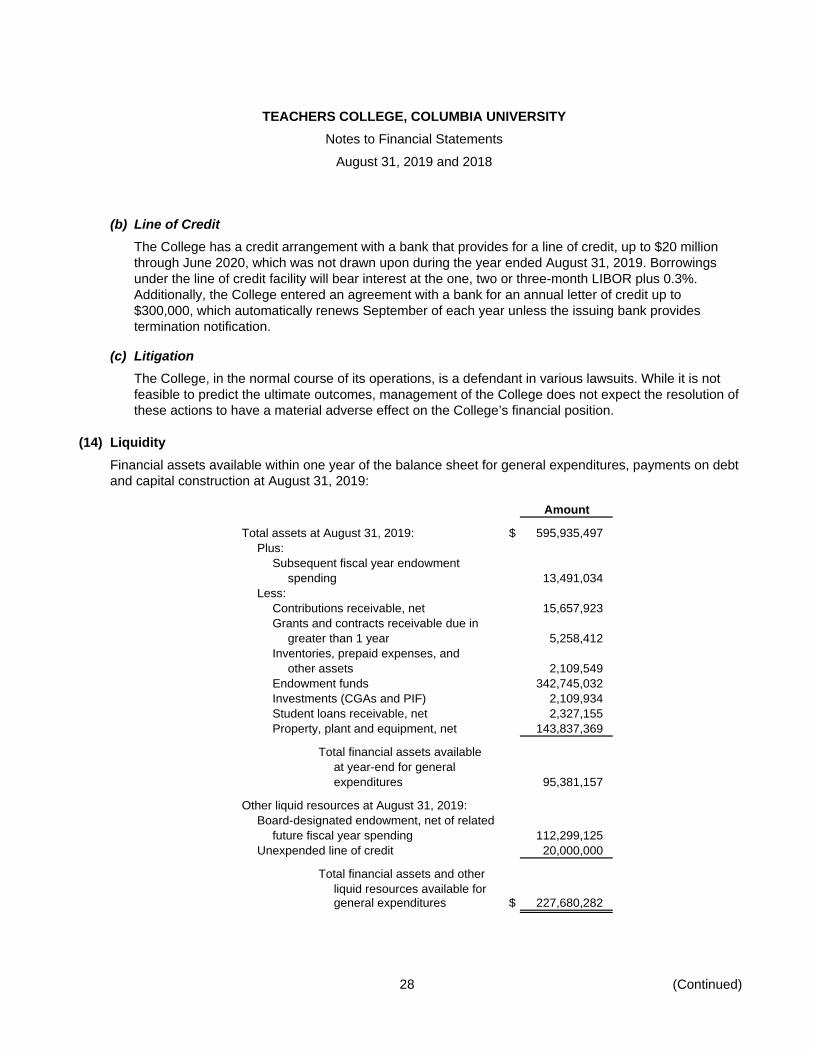

(14) Liquidity Financial assets available within one year of the balance sheet for general expenditures, payments on debt and capital construction at August 31, 2019:

Amount

Total assets at August 31, 2019: $ 595,935,497 Plus:

Subsequent fiscal year endowmentspending 13,491,034

Less:Contributions receivable, net 15,657,923 Grants and contracts receivable due in

greater than 1 year 5,258,412 Inventories, prepaid expenses, and

other assets 2,109,549 Endowment funds 342,745,032 Investments (CGAs and PIF) 2,109,934 Student loans receivable, net 2,327,155 Property, plant and equipment, net 143,837,369

Total financial assets availableat year-end for generalexpenditures 95,381,157

Other liquid resources at August 31, 2019:Board-designated endowment, net of related

future fiscal year spending 112,299,125 Unexpended line of credit 20,000,000

Total financial assets and otherliquid resources available forgeneral expenditures $ 227,680,282

TEACHERS COLLEGE, COLUMBIA UNIVERSITY Notes to Financial Statements

August 31, 2019 and 2018

29

The College manages its financial assets to be available as its operating expenditures, liabilities and other obligations come due. The College’s cash flows have seasonal variations during the fiscal year primarily attributable to the student tuition, fees and housing billing cycles. In order to manage liquidity, the College maintains a revolving unexpended line of credit with a financial institution totaling $20 million. As of August 31, 2019, the College did not borrow under this agreement.

Included within endowment funds is $117 million and $118 million of board-designated funds as of August 31, 2019 and 2018, respectively. These funds represent unrestricted operating funds internally designated by the Board. Although the College does not intend to spend from these funds, if needed, the funds could be liquidated over time to support operations, but require a Board resolution approving the spending.

Under the provision of the College’s endowment spending rule, the Board approved a spending allocation of $13.5 million for the fiscal year ending August 31, 2020.

(15) Subsequent Events The College and the Local 707 Teamsters Union are negotiating the terms of the Collective Bargaining Agreement, which expires December 2019.

The College evaluated other events subsequent to August 31, 2019 and through December 4, 2019, the date on which the financial statements were issued, and has determined there are no additional disclosures.

![Goulburn Teachers' College [GTC] SA1174](https://img.pdfslide.net/doc/110x75/624015730b76d25adf07af06/goulburn-teachers-college-gtc-sa1174.jpg)