Embed Size (px)

DESCRIPTION

Technical Guide for Saving Mobilization

Citation preview

AA TTeecchhnniiccaall GGuuiiddee ttooSSaavviinnggss MMoobbiilliizzaattiioonn::

AA TTeecchhnniiccaall GGuuiiddee ttooSSaavviinnggss MMoobbiilliizzaattiioonn::

LLeessssoonnss ffrroomm tthhee CCrreeddiitt UUnniioonn EExxppeerriieenncceeLLeessssoonnss ffrroomm tthhee CCrreeddiitt UUnniioonn EExxppeerriieennccee

This guide is intended as an instructional reference for savings institutions interested in designing, marketing, managing and protecting voluntary savings products. Find out how to:

• Determine if an institution is ready to mobilize savings

• Prepare to capture savings and protect them once captured

• Provide what savers most value: safety, convenience and returns

• Develop savings products and conduct marketing campaigns

• Set market-driven interest rates with real rates of return

• Manage savings, ensure liquidity and improve efficiency

All Figures in US DollarsAll Numbers Rounded to Nearest Dollar

WOCCU Savings Programs PROJECT COUNTRY DATE NO. OF NO. OF TOTAL TOTAL PASSBOOK PASSBOOK

CREDIT MEMBER- SAVINGS DEPOSITS/ DEPOSITS DEPOSITS/UNIONS CLIENTS DEPOSITS MEMBER-CLIENTS MEMBER-CLIENTS

Bolivia 12/31/01 10 60,179 $32,682,018 $543 $10,700,175 $178Bulgaria 12/31/01 13 11,027 $1,187,155 $107 $391,264 $35Ecuador 6/30/01 22 914,485 $92,215,792 $101 $75,988,230 $83Guatemala 12/31/01 28 406,074 $132,466,655 $326 $66,371,647 $163Honduras 9/30/01 21 194,679 $34,120,182 $175 $16,471,616 $85Kenya* 9/30/01 6 45,438 $4,524,854 $100 $4,524,854 $100Macedonia 9/30/01 1 1,273 $155,545 $122 $4,551 $4Nicaragua 12/31/01 17 17,937 $1,776,178 $99 $1,229,963 $72Philippines 12/31/01 18 171,561 $15,758,701 $92 $7,416,128 $43Romania 12/31/01 26 105,069 $5,181,554 $49 $591,314 $6Rwanda 12/31/00 145 229,453 $23,413,012 $102 $23,413,012 $117Uganda* 12/31/01 15 10,785 $2,274,270 $211 $2,274,270 $211

WEIGHTED AVERAGE WEIGHTED AVERAGE

Total for 12 WOCCU Programs 322 2,168,000 $345,755,916 $159 $209,447,024 $97

* In Kenya and Uganda, most savings products offered have the passbook core characteristics. Passbook deposit data for these two countries was not separated out from total savings deposits. The Kenya project works with 16 credit unions total, serving 122,263 member-clients.

Voluntary savings are by far the most frequent source of funding formicroenterprise startup and expansion.Savings deposits enable households tobuild for the future and better preparefor unexpected emergencies.

Most development finance professionalsno longer question if poor people save.Various studies find that the poor canand do save, although these savingsare rarely in liquid financial form.Research also reveals that the largemajority of poor savers lack access tosafe and sound institutions for deposit-ing their savings. WOCCU savings-driven credit union development programs worldwide demonstrate thatlow-income people will substantiallyincrease their voluntary savingsdeposits if provided with a safe andconvenient place to deposit their savings.

Despite these findings, millions ofpeople continue to lack access to reliable and convenient savings services.

As financial service providers to thepoor, microfinance institutions (MFIs)are under growing pressure to offer voluntary and withdrawable micro-savings services to their clients. At the same time, savings deposits provide arelatively stable source of funds thatcould enable an institution to become a sustainable, self-reliant financialintermediary. Savings mobilizationincreases the supply of internally generated funds that can be investedin housing, microenterprise and smallbusiness loans.

Many existing MFIs are not in the position to begin mobilizing savingsresponsibly. This technical guide is

intended to provide instructive lessonsfrom the experience of savings-drivencredit unions to MFIs legally authorizedto capture savings, such as postal savingsbanks, non-governmental organizations(NGOs) that have transformed intolegal financial intermediaries, financecompanies and credit unions.

What most distinguishes credit unionsfrom other non-bank financial entitiesoffering microfinance services is theability to mobilize mass numbers ofsmall, voluntary savings accounts.WOCCU project credit unions serve2,168,000 member-clients with atotal savings volume of $345,755,916.The weighted average passbookdeposit per member-client is $97. Inmany credit unions that have maturesavings offerings, net savers outnumbernet borrowers by seven to one.

Why Savings?Savings are fundamental to sustainable economic development

This guide was prepared by Janette Klaehn, Anna Cora Evans and Brian Branch of World Council of Credit Unions, Inc.(WOCCU). The guide offers parameters for financial performance, referring specifically to WOCCU Standards of Excellence,guidelines for product development and pricing, recommendations for marketing savings products and instructions on managing savings based on lessons learned from the field experience of WOCCU technical assistance programs.

- 1 -

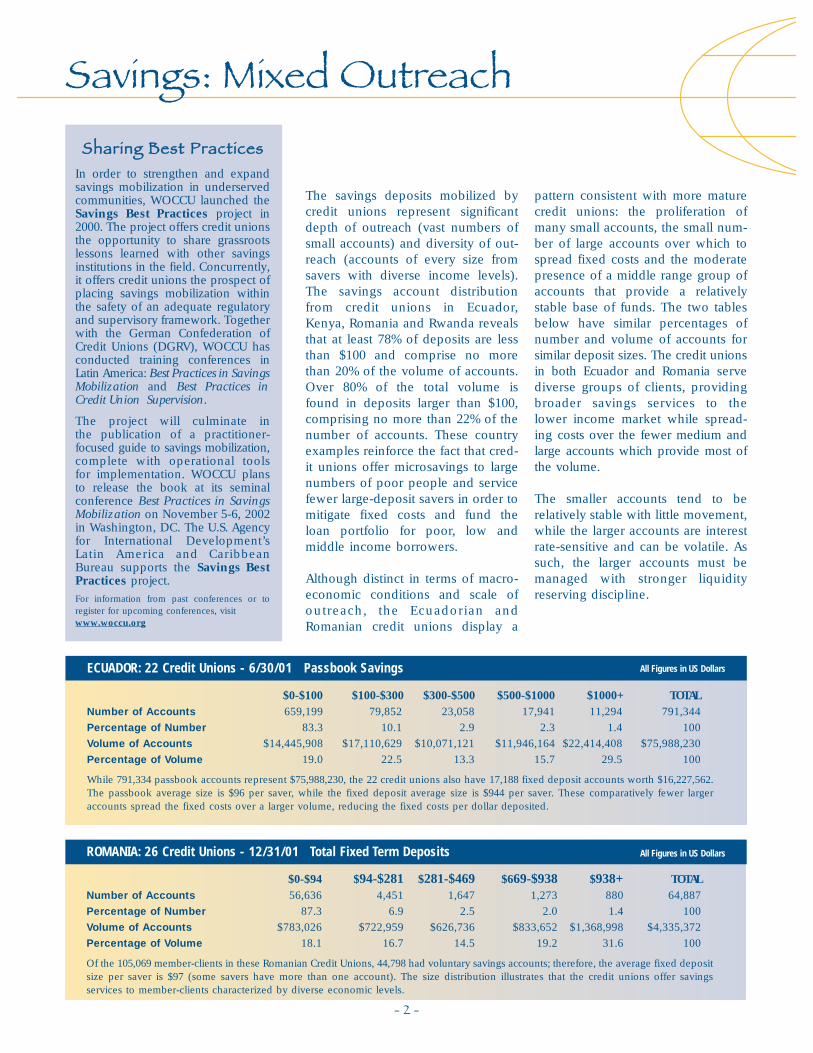

pattern consistent with more maturecredit unions: the proliferation ofmany small accounts, the small num-ber of large accounts over which tospread fixed costs and the moderatepresence of a middle range group ofaccounts that provide a relatively stable base of funds. The two tablesbelow have similar percentages ofnumber and volume of accounts forsimilar deposit sizes. The credit unionsin both Ecuador and Romania servediverse groups of clients, providingbroader savings services to thelower income market while spread-ing costs over the fewer medium andlarge accounts which provide most ofthe volume.

The smaller accounts tend to be relatively stable with little movement,while the larger accounts are interestrate-sensitive and can be volatile. Assuch, the larger accounts must bemanaged with stronger liquidityreserving discipline.

The savings deposits mobilized bycredit unions represent significantdepth of outreach (vast numbers ofsmall accounts) and diversity of out-reach (accounts of every size fromsavers with diverse income levels).The savings account distributionfrom credit unions in Ecuador,Kenya, Romania and Rwanda revealsthat at least 78% of deposits are lessthan $100 and comprise no morethan 20% of the volume of accounts.Over 80% of the total volume isfound in deposits larger than $100,comprising no more than 22% of thenumber of accounts. These countryexamples reinforce the fact that cred-it unions offer microsavings to largenumbers of poor people and servicefewer large-deposit savers in order to mitigate fixed costs and fund theloan portfolio for poor, low and middle income borrowers.

Although distinct in terms of macro-economic conditions and scale ofoutreach, the Ecuadorian andRomanian credit unions display a

Savings: Mixed Outreach

- 2 -

SShhaarriinngg BBeesstt PPrraaccttiicceessIn order to strengthen and expandsavings mobilization in underservedcommunities, WOCCU launched theSavings Best Practices project in2000. The project offers credit unionsthe opportunity to share grassrootslessons learned with other savingsinstitutions in the field. Concurrently,it offers credit unions the prospect ofplacing savings mobilization withinthe safety of an adequate regulatoryand supervisory framework. Togetherwith the German Confederation ofCredit Unions (DGRV), WOCCU hasconducted training conferences inLatin America: Best Practices in SavingsMobilization and Best Practices inCredit Union Supervision.

The project will culminate in the publication of a practitioner-focused guide to savings mobilization,complete with operational tools for implementation. WOCCU plansto release the book at its seminalconference Best Practices in SavingsMobilization on November 5-6, 2002in Washington, DC. The U.S. Agencyfor International Development’sLatin America and CaribbeanBureau supports the Savings BestPractices project.

For information from past conferences or to register for upcoming conferences, visit www.woccu.org

ROMANIA: 26 Credit Unions - 12/31/01 Total Fixed Term Deposits

$0-$94 $94-$281 $281-$469 $669-$938 $938+ TOTALNumber of Accounts 56,636 4,451 1,647 1,273 880 64,887

Percentage of Number 87.3 6.9 2.5 2.0 1.4 100

Volume of Accounts $783,026 $722,959 $626,736 $833,652 $1,368,998 $4,335,372

Percentage of Volume 18.1 16.7 14.5 19.2 31.6 100

Of the 105,069 member-clients in these Romanian Credit Unions, 44,798 had voluntary savings accounts; therefore, the average fixed depositsize per saver is $97 (some savers have more than one account). The size distribution illustrates that the credit unions offer savings services to member-clients characterized by diverse economic levels.

ECUADOR: 22 Credit Unions - 6/30/01 Passbook Savings

$0-$100 $100-$300 $300-$500 $500-$1000 $1000+ TOTALNumber of Accounts 659,199 79,852 23,058 17,941 11,294 791,344

Percentage of Number 83.3 10.1 2.9 2.3 1.4 100

Volume of Accounts $14,445,908 $17,110,629 $10,071,121 $11,946,164 $22,414,408 $75,988,230

Percentage of Volume 19.0 22.5 13.3 15.7 29.5 100

While 791,334 passbook accounts represent $75,988,230, the 22 credit unions also have 17,188 fixed deposit accounts worth $16,227,562.The passbook average size is $96 per saver, while the fixed deposit average size is $944 per saver. These comparatively fewer largeraccounts spread the fixed costs over a larger volume, reducing the fixed costs per dollar deposited.

All Figures in US Dollars

All Figures in US Dollars

- 3 -

FINANCIAL SAFETY NETSIn many cases, clients utilize savingsservices for the purpose of creatingfinancial safety nets to soften thecostly repercussions of health emer-gencies. The costs of health-relatedcrises negatively impact individuals ofall socioeconomic levels, but mostgravely destabilize the poor. Studies onHIV/AIDS and microfinance conductedby Donahue, Parker and others find

that the clients of microcredit group-lending institutions highly desire savings services.* Formal savings institutions can serve this demand-driven market. The Kenyan andRwandan savings distribution tablesreveal that member-clients of diverseincome levels save at the creditunions in countries struck by theHIV/AIDS pandemic.

Clients also make use of savings serv-ices to deal with personal emergenciesand unforeseen challenges that stemfrom political and economic crises. InRwanda, more than 200,000 activesavers struggling to rebuild a nationafter the genocide of the mid-1990srely on savings to fuel communityeconomic growth.

Savings: Mixed Outreach

RWANDA: 145 Credit Unions - 12/31/00 Passbook Savings All Figures in US Dollars

$0-$12 $12-$24 $24-$117 $117-$233 $233+ TOTALNumber of Accounts 176,333 32,095 41,169 17,532 22,001 289,130

Percentage of Number 61 11.1 14.2 6.1 7.6 100

Volume of Accounts $792,596 $550,024 $2,650,767 $2,864,691 $16,554,934 $23,413,012

Percentage of Volume 3.4 2.3 11.3 12.2 70.7 100

The case of the 145 Rwandan Banques Populaires reveals an overall average deposit size of $81 per account. Deposits of less than $233make up 92.4% of the total number of active accounts and 29.3% of the total volume. Accounts greater than $233 comprise only 7.6% ofthe total number of accounts but make up 70.7% of the total volume.

The total excludes 196,832 inactive accounts equivalent to $3,350,852. Inactive accounts belong to Rwandans now missing, deceased orliving as refugees outside of the country.

* For further information on microfinance and HIV/AIDS, see www.mip.org.

KENYA: 6 Credit Unions - 9/30/01 Total Savings All Figures in US Dollars

$0-$63 $63-$127 $127-$253 $253+ TOTALNumber of Accounts 16,268 819 688 4,116 21,891

Percentage of Number 74.3 3.7 3.1 18.8 100

Volume of Accounts $171,439 $74,222 $121,473 $4,157,720 $4,524,854

Percentage of Volume 3.8 1.6 2.7 91.9 100

In these six Kenyan credit unions, the majority of deposits are very small amounts, i.e., 74% of the deposits are for amounts less than$63 and represent only 4% of the savings volume, while the 19% of deposits greater than $253 represent 92% of the volume of accounts.The average deposit size per account is $207.

- 4 -

SAFETYSavers most frequently report thatthe key feature they seek is safety fortheir savings. They want to feel con-fident that their deposits will beavailable when they need them.

CONVENIENCESavers demand access and liquidity.They want to be able to access theirfunds the moment that they need ordesire them.

RETURNSSavers expect a positive real return ontheir savings. Small savers will oftenshift their savings to real goods, whichcan be resold without losing theirvalue (a chicken or a calf in ruralareas, tires or construction blocks inurban areas), if financial instrumentreturns are below the rate of inflation.

Savers Most Value Safety,Convenience & Returns

AFTERBEFORE

ENABLING ENVIRONMENTThree key elements repeatedly standout as prerequisite environmental factors for mobilizing savings:

• Manageable inflation• Legal authority• Supervision

The ability of an institution to success-fully mobilize savings is contingent firstupon a macroeconomic environmentwhich allows the savings institution tooperate at rates that are viable andsustainable while providing a realpositive return to protect the value ofclient savings.

Savings mobilization is a pactbetween parties: the institutionreceiving the savings and the individ-ual placing savings in that institution.Savings services need to operate

within an established legal frameworkthat identifies which institutions,under which criteria, are able toreceive savings from members orfrom the public. The legal frameworkshould also identify what recoursesavers have to recover their savingsfrom savings institutions.

Savings institutions will be able tomobilize savings responsibly and moreeffectively within the safety of anadequate regulatory and supervisoryframework. Institutions that mobilizevoluntary deposits should be supervisedby an objective third-party governmentregulatory agency responsible forsupervision of the financial sector.Effective supervision requires a soundlegal system, formalized audit require-ments, supervisory monitoring capacity,an established regulatory frameworkand authority for enforcement.

RESPONSIBILITYSavers need to be able to trust that theinstitution will safeguard their savings.In offering savings products, an insti-tution takes on the responsibility ofprotecting the deposits of savers.

Per WOCCU’s worldwide fieldexperience, the minimum criticalelements for responsible savingsmobilization are (in no specific order):

• Entrepreneurial institutional vision • Professional staff• Effective governance structure• Prudential financial discipline • Sound credit risk analysis and

risk management• Physical security• Internal controls

Savings growth is highly correlatedwith the perceived soundnessand professionalism of the institutionmobilizing savings. The attractiveand secure public appearance of thephysical infrastructure of the institu-tion does much to create a safe andprofessional image that depositorscan trust. Facilities should exhibit

tangible security infrastructure forrisk management such as grillson windows, structural sound-ness, glass partitions for tellers,safes and locked cash drawers.Although secure in its structure, asavings institution should continueto present a pleasant, friendlyand inviting personalized image.

When is an Institution Ready?

- 5 -

VISIONInstitutions that seek to mobilizesavings must have the vision, com-mitment and disposition to attractvoluntary savings. Each institutionmust adjust its own policies andproduct offerings to provide finan-cial services that are competitiveand in accordance with the needsof the market.

PROFESSIONALISMTo accept savings and administerthem in an efficient manner which preserves their valuerequires a minimum professionalcapacity of staff trained in how tomanage savings. Employees shouldhandle cash with strong ethical andprofessional working standards,while maintaining a warm and personal approach with clients.Staff familiar with local languages,customs and norms will facilitatetrusting relationships with clients.

GOVERNANCEIn member-owned and member-controlled financial institutions, itis the simultaneous presence ofsavers, who provide the funds, andborrowers, who borrow the funds,which forms the basis for a self-sufficient and balanced financialintermediary. Yet, the two groupshave inherent conflicting objectives.Net savers demand high depositrates and strong prudential disci-plines to protect their savings,while net borrowers demand lowloan rates, low transaction costsand laxness in prudential disci-pline. The quality of the savings serv-ices and the credit screening and col-lection policies will determine theproportion of net borrowers to netsavers in an institution.

The threat of deposit withdrawaldue to savers’ lack of confidence inmanagement should keep man-agers on track, since widespreadwithdrawals would eliminate thebase of funds in a self-sufficientsavings institution. In theory, thisthreat should force managers to followsound principles of adequate capitalreserves, loan loss provisions andliquidity reserves. In reality, thethreat of deposit withdrawal is notalways sufficient to ensure thatmanagers operate with prudentialfinancial discipline; therefore, thirdparty regulators are necessary touphold prudential norms and protectpublic savings.

When is an Institution Ready?

PRUDENTIALFINANCIAL DISCIPLINEBefore engaging in or accelerat-ing public savings mobilization,an institution must establishprudential financial managementdisciplines as standard, well-understood and staff-supportedpractice. Institutions should demon-strate strong financial management oftheir own funds, beyond merely meet-ing basic requirements of solvency.

Savings institutions must estab-lish the core disciplines of delin-quency control, loan loss provi-sions, liquidity reserves and cap-ital reserves in order to protectclient savings. These disciplinesmust be formalized in policy andimplemented in practice. Financialdisciplines are interdependent andmutually reinforcing; as such, theyshould be implemented as an inte-grated system, not in a piecemealmanner that addresses some risksbut not others.

LINES OF DEFENSEA savings institution must defendthe value of the deposits captured.Provisions for loan losses provide thefirst line of defense against observablerisks, allowing a savings institution toprotect itself from loan losses that canbe predicted by the monitoring andaging of delinquency. The WOCCUStandards of Excellence require thatsavings institutions provision for 100%of loans delinquent more than 12months and 35% of loans delinquent

less than 12 months. Institutions shouldwrite off loans delinquent for periodsover 12 months. The total outstandingprincipal balance of a loan should beclassified as delinquent (portfolio-at-risk) at 30 days past due.

Reserves, or institutional capital, providea second line of defense against unex-pected shocks. If a savings institutionhas built up institutional capital orretained earnings, then these funds canprovide security during a period ofmacroeconomic instability or during abanking crisis. Savings institutionsshould establish and maintain capitalreserves and retained earnings at 10% of total assets.

Paid-in shares in credit unions, orshares of stock in other privately-ownedsavings institutions, are a third line ofdefense against external shocks that canbe utilized in extreme cases to avoidimpairing the value of client deposits.

RISK MANAGEMENTAs an institution mobilizes savings,liquidity increases and those fundsare directed out as loans back intothe community. It is critical thatthe savings institution have inplace strong policies and practicesfor credit screening and riskanalysis so that the loans financedby savings are collectible. Creditrisk management must include strictdelinquency monitoring, provisioningand collection procedures. In a sav-ings institution, delinquency (portfo-lio-at-risk at 30 days) should be 5%or less of the total loan portfolio.WOCCU recommends that a savingsinstitution establish loan concentra-tion limits, or limit the amount ofrelated direct or indirect aggregateloans or credits to 10% of net capital.

ASSET LIABILITY MANAGEMENTSavings institutions must carefullymanage their assets and liabilities.They need to prevent asset liabilitymismatches in either term or rate;for example, withdrawable pass-book savings are not safe sources offunds for long-term loans. On theother hand, long-term certificates ofdeposit are appropriate to fundlong-term loan products.

PHYSICAL SECURITYSecure infrastructure requirementsinclude locked drawers at teller stations, safes or vaults for holdingcash and grill or glass partitionsbetween teller stations and the public.Grills and bars should be in placeover doors, windows and air condi-tioners. Guards should be present inlarger institutions, such guards mustbe trained in what to do in the eventof a robbery. Training of all staff is necessary to ensure the safety ofthe employees.

- 6 -

The PEARLS financal performancemonitoring system was developedby WOCCU as a tool for monitoringand managing credit union operations:

PP rotectionEEffective financial structureAAsset qualityRRates of return and costsLL iquidity andSS igns of growth

For more information on PEARLS seethe research area of www.woccu.orgto download the PEARLS monograph.

Protecting Savings

Developing Savings Products

Primarily microand small savers,large savers foron-demand useof some funds

Net savers who seekto maximize returns

Population under thelegal age of clientstatus (usually 18years of age)

Clients with specificgoals or set targets,examples are:Christmas clubs,education or housing accounts

Organizations suchas NGOs, churches,foundations,associations orcorporations thatrequire servicingof funds

Net savers who seek tomaximize returns forlong-term planning

- 7 -

None or very low

High

None or very low

Higher than passbook

Highest

High

X (base rate),rate increaseswith increasingaccount balance

X + 2%, fixed atopening of certificate,higher for longer termor higher balance

X - 1%, paid onlyon accounts withbalances abovecertain threshold

X + 1%, higher thanpassbook and lowerthan fixed term

X + 2%, increaseswith increasingaccount balance

X + 2%, tied bycontract to realreturn above inflation

YOUTHSAVINGS

PROGRAMMEDSAVINGS

INSTITUTIONALACCOUNTS

RETIREMENTACCOUNTS

PRODUCT(OR SERVICE)

TARGETMARKET

MINIMUMOPENINGDEPOSIT

INTEREST RATE

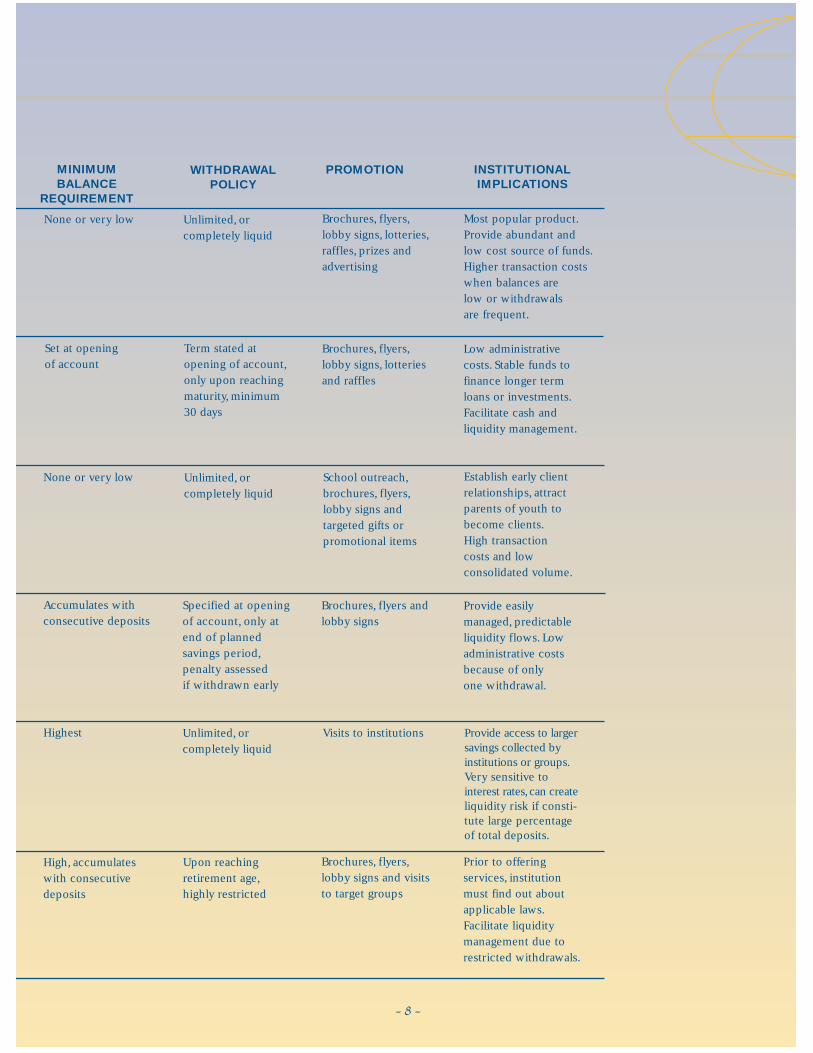

The credit unionexperience inmobilizing voluntarysavings has focusedprimarily on six savings products: passbook accounts,fixed term certificatesof deposit, youth savings, programmed savings,institutional accountsand retirementaccounts. Each producthas core characteristics.

Product characteristicsshould be adjusted tomeet the local demandfor savings services.When developingproducts, savingsinstitutions firstconduct marketstudies to determinelocal client preferencesand evaluate localcompetitive conditions.

Please note: interestrates on withdrawablepassbook savingsaccounts serve as thebase rate (“X” %) forthe savings interestrate structure. Thebase rate is set according to marketcompetitive rates,transaction costs andthe rate of inflation.

PASSBOOKSAVINGS

FIXED TERMCERTIFICATES OF DEPOSIT

- 8 -

Unlimited, orcompletely liquid

Term stated atopening of account,only upon reachingmaturity, minimum30 days

Unlimited, orcompletely liquid

Specified at openingof account, only atend of plannedsavings period,penalty assessedif withdrawn early

Unlimited, orcompletely liquid

Upon reachingretirement age,highly restricted

None or very low

Set at openingof account

None or very low

Accumulates withconsecutive deposits

Highest

High, accumulateswith consecutivedeposits

Brochures, flyers,lobby signs, lotteries,raffles, prizes andadvertising

Brochures, flyers,lobby signs, lotteriesand raffles

School outreach,brochures, flyers,lobby signs andtargeted gifts orpromotional items

Brochures, flyers andlobby signs

Visits to institutions

Brochures, flyers,lobby signs and visitsto target groups

Low administrativecosts. Stable funds tofinance longer termloans or investments.Facilitate cash andliquidity management.

Establish early clientrelationships, attractparents of youth tobecome clients.High transactioncosts and lowconsolidated volume.

Provide easilymanaged, predictableliquidity flows. Lowadministrative costsbecause of onlyone withdrawal.

Provide access to largersavings collected byinstitutions or groups.Very sensitive tointerest rates,can createliquidity risk if consti-tute large percentageof total deposits.

Prior to offeringservices, institutionmust find out aboutapplicable laws.Facilitate liquiditymanagement due torestricted withdrawals.

Most popular product.Provide abundant andlow cost source of funds.Higher transaction costswhen balances arelow or withdrawalsare frequent.

WITHDRAWALPOLICY

MINIMUMBALANCE

REQUIREMENT

PROMOTION INSTITUTIONALIMPLICATIONS

Developing Savings Products

Since savers most value safety, convenience and returns, once aninstitution has established itself as asafe place for deposits, it moves on toaddress the issues of convenience andreturns through product development.

Savings mobilization is a demand-driven activity. A savings institutionasks savers to place their funds withinits caretaking. This relationship reversesthe traditional power relationshipbetween client and financial interme-diary in which borrowers approachbanks, credit unions or other microfi-nance institutions to ask for loans. Thesavings institution must market and sellitself to clients; it must convince saversthat their savings will be safe and wellmanaged. Any savings institution,whether bank, credit union or otherfinancial intermediary, should offer sav-ings products which meet the demandsof both prospective and existing clients.

IDENTIFY THE MARKETIn order to reach a more diverseclientele and attract net savers, sav-ings institutions must first identifywho the savers are in a community.Savings institutions begin by conductingstudies to find out two types of infor-mation: client profiles and preferences,and intelligence about services andproduct characteristics that competing oralternative institutions provide to saversin the market. Both types of informationare useful in tailoring savings services tomarket demand and local conditions.Market studies also examine localdemographic and economic characteris-tics and can assist managers to create astrategy to penetrate a particular market.

DEVELOP PRODUCTSSavings services are built in three ways.Products are:

• Designed to balance the trade-offbetween convenience (liquidity)and return (interest rate)

• Tailored to respond to the demandsof particular market niches; e.g.,farmers who save in large blocksafter a harvest and withdraw savingsgradually through the year,or childrenand students who save in smallamounts due to limited incomes

• Adapted to the purposes for whichclients save; e.g., to pay educationfees for children or to purchase largeexpense items such as appliances orhome improvements

As products are built to meet clientdemand, the defining characteristicsof products are liquidity or access,term, minimum balance, rate ofreturn and transaction costs.

Product design must be simple andclear to enable customers to chooseproducts with the confidence that theyunderstand all the benefits and costs ofeach product. Simplicity also helpsreduce administrative procedures andcontain operations costs.

Savings policies establish and for-malize the products offered andoutline the procedures by whichtheir liquidity, pricing and transac-tions are managed. Savings policiesshould be updated regularly inresponse to market demand in orderfor products to remain competitive inthe marketplace.

DETERMINE THE RIGHT MIXSavings products exist along acontinuum of trade-offs betweenliquidity (access and convenience)and return (compensation). Someproducts offer complete access todeposits, or withdrawals wheneverthe saver wishes. Other productsrestrict liquidity and consequentlyoffer higher returns. A mix of productsmay offer alternatives of fully liquid,semi liquid, fixed short-term andaccumulating long-term accounts.

Lower-income savers often seek smallaccounts that offer high levels of liquidity. These savers exhibit strongpreferences for products such as pass-book accounts, with low minimum balances and complete and immediateaccess to savings at all times. Thesesmall savers have proven willing to sacrifice returns for open access to theirfunds. Alternatively, larger or wealthiersavers seek to maximize their return onsavings and have proven willing to sacrifice liquidity for higher return.

Short-term AccumulatingFully Semi Predictable Frozen Long-term

Liquid Liquid Flows Deposits Accounts

Passbook Limited Programmed Fixed Term RetirementAccounts Withdrawals Savings Certificates Accounts

of Deposit

- 9 -

- 10 -

100,000

80,000

60,000

40,000

20,000

01997 1998 1999 2000 2001

Guatemala: 28 Credit Unions - 12/31/01 Youth Savings All Figures in US Dollars

Number of Number of Number of Percentage Total Total PercentageCredit Unions Member-Clients Youth Clients of Total Member- Savings Youth of Total

Clients Deposits Deposits Deposits

28 406,074 88,219 21.7 $132,466,655 $779,404 0.6

Growth in Numberof Youth Savers

Tailoring Products: Youth Savings

A savings institution may offer a com-bination of generic savings productsfor the market at-large and tailoredsavings products designed to addressthe particular demands of an identi-fied niche. Youth accounts aredesigned to combine low returnsand limited liquidity with small balances to serve the market segmentunder the age of formal client status(usually 18 years of age).

The Guatemalan credit union systemconducted market research, intro-duced youth savings and launched afull-fledged marketing campaign forchildren and adolescent savers in1996. As of December 31, 2001, youthsavers made up 21.7% of the 406,074member-clients and 0.6% of the totalsavings volume.

Num

ber

of

Save

rs

80

60

40

20

0

Setting Interest Rates

- 11 -

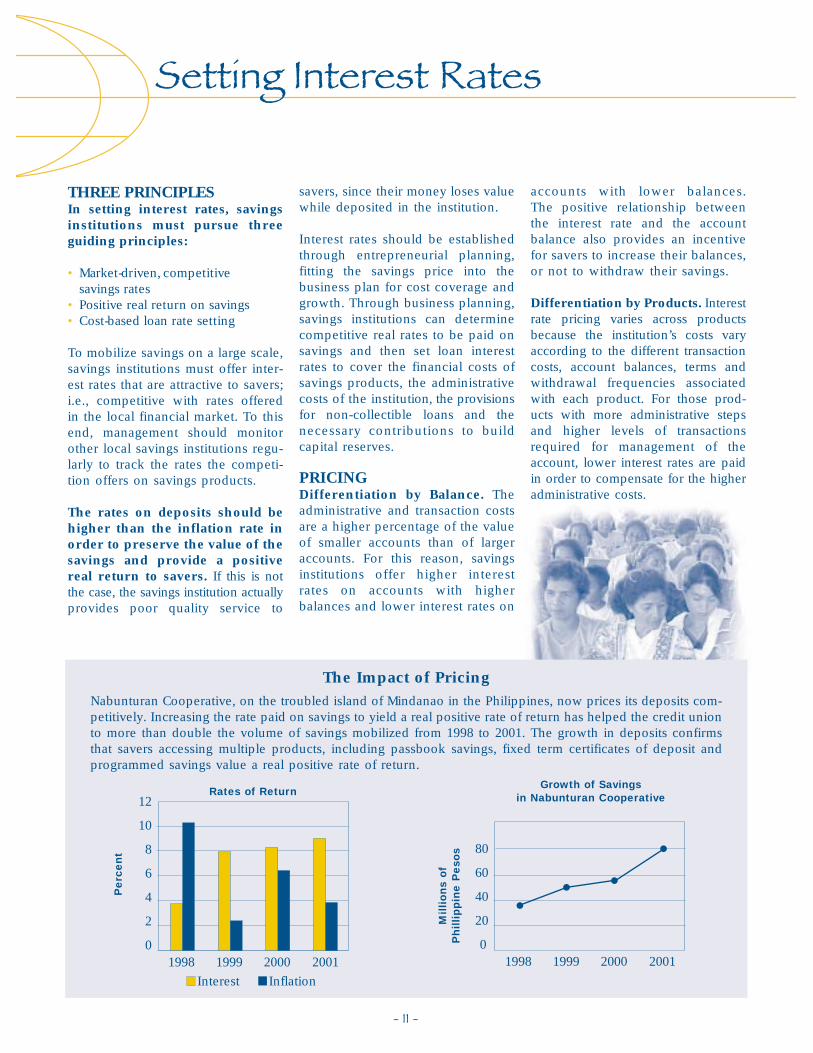

THREE PRINCIPLESIn setting interest rates, savingsinstitutions must pursue threeguiding principles:

• Market-driven, competitivesavings rates

• Positive real return on savings• Cost-based loan rate setting

To mobilize savings on a large scale,savings institutions must offer inter-est rates that are attractive to savers;i.e., competitive with rates offeredin the local financial market. To thisend, management should monitorother local savings institutions regu-larly to track the rates the competi-tion offers on savings products.

The rates on deposits should behigher than the inflation rate inorder to preserve the value of thesavings and provide a positivereal return to savers. If this is notthe case, the savings institution actuallyprovides poor quality service to

savers, since their money loses valuewhile deposited in the institution.

Interest rates should be establishedthrough entrepreneurial planning,fitting the savings price into thebusiness plan for cost coverage andgrowth. Through business planning,savings institutions can determinecompetitive real rates to be paid onsavings and then set loan interestrates to cover the financial costs ofsavings products, the administrativecosts of the institution, the provisionsfor non-collectible loans and the necessary contributions to buildcapital reserves.

PRICINGDifferentiation by Balance. Theadministrative and transaction costsare a higher percentage of the valueof smaller accounts than of largeraccounts. For this reason, savingsinstitutions offer higher interestrates on accounts with higher balances and lower interest rates on

accounts with lower balances. The positive relationship betweenthe interest rate and the accountbalance also provides an incentivefor savers to increase their balances,or not to withdraw their savings.

Differentiation by Products. Interestrate pricing varies across productsbecause the institution’s costs varyaccording to the different transactioncosts, account balances, terms andwithdrawal frequencies associatedwith each product. For those prod-ucts with more administrative stepsand higher levels of transactionsrequired for management of theaccount, lower interest rates are paidin order to compensate for the higheradministrative costs.

12

10

8

6

4

2

01998 1999 2000 2001

Interest Inflation

Millions

of

Phillippin

e P

eso

s

Rates of Return

The Impact of Pricing

Nabunturan Cooperative, on the troubled island of Mindanao in the Philippines, now prices its deposits com-petitively. Increasing the rate paid on savings to yield a real positive rate of return has helped the credit unionto more than double the volume of savings mobilized from 1998 to 2001. The growth in deposits confirmsthat savers accessing multiple products, including passbook savings, fixed term certificates of deposit andprogrammed savings value a real positive rate of return.

1998 1999 2000 2001

Growth of Savingsin Nabunturan Cooperative

Perc

ent

Marketing Savings Products

- 12 -

By expanding membership and theattractiveness of savings services,many credit unions have convertedfrom small-scale dependent borrowerclubs to full financial intermediariesof funds from net savers to net borrowers. MFIs authorized to mobilize savings could make thesame transition, but must first position themselves in the market asproviders of savings services.

Savings mobilization is driven by marketing. Once products aredefined, institutions must brand orpackage them, set sales expectationsand goals and then sell the productsto the local market. This effort mayinclude marketing new products orre-launching old ones.

The primary objectives of savings-based marketing activities are to identifyand expand the local market of netsavers, improve the competitivenessof savings services and improve thepublic image of the institution. A keyindicator of success is the ability ofan institution to attract a broad mix of savers and borrowers of a scalesufficient to generate the earningsnecessary to sustain institutional services and growth.

Successful marketing plans designatea staff member to be directly respon-sible for marketing activities. Aneffective marketing plan also specifiesobjectives, goals, activities and indicators for evaluation. The activitiesand goals laid out in the marketingplan must be compatible with theannual business plan of the institution.

DEVISING A STRATEGYSavings institutions should conductstudies to analyze the services provided by other financial institu-tions in the local community beforedefining a strategy for launchingnew or revamped savings products.These studies:

• Identify the existing service deliverystructure

• Compare the competitive character-istics of services—prices, terms,minimum amounts, convenience,waiting periods, service variety andsophistication of products—withother local financial institutions

• Evaluate interest rate scales on similarproducts of other local financialinstitutions

• Identify the financial service demandswhich the savings institution maysatisfy for the local population

IMAGE Trademarks, brands and standard-ized logos should be used to give products recognizable andmemorable names associated witha quality image. The product imageand branding should be carriedthrough on brochures, lobby signs,posters, paper forms and all otherprinted materials.

Once a savings institution has deviseda clear strategy and created a strongimage, it must engage in aggressivemarketing of its products. The cam-paigns may include brochures,posters, flyers, media spots on localradio or television stations and adver-tisements in local newspapers.

In addition to the tiering of interestrate structures discussed earlier, savingsinstitutions may provide savers incentives for increasing deposits byoffering lotteries of small benefits orprizes. Credit unions have foundthat the raffle or lottery of smallbenefits or prizes, with the associatedpublicity, can provide significantincentive to encourage small saversto mobilize savings. Lotteries andraffles have proven to be very popularin markets with low savings capacity.Raffles can serve the dual purpose ofincreasing deposit amounts fromexisting clients and attracting newclients to the institution. The mosteffective raffles and lotteries provideincentives not only for increasingaccount balances, but also for main-taining them.

Another way to increase savingsmobilization is to offer interest ratepremiums to new savers. A savingsinstitution announces, through publicnotices and posters on the walls orwindows, that an additional fractionof a percent on top of the normal ratewill be paid for new passbookaccounts or fixed term certificates ofdeposit during the specific period ofthe promotion. Offering interestrate premiums is a fast and effi-cient way to attract new resourcesand stimulate savings growth.

Convenience is a key factor inmobilizing savings. If the transac-tion costs of making deposits orwithdrawals in an institution arehigh, then savers will be less likelyto maintain their savings in thatinstitution. Since the physical prox-imity of the savings institution deter-mines the major cost and timerequired for savers to make depositsor withdrawals, institutions shouldtry to locate their offices in high-traffic markets or town centers, andeven open lower cost or minimalinfrastructure branches to serveoutlying communities.

Savings institutions should providecompetitive service hours compatiblewith the schedules of clients andprospective clients in the local com-munity. For this purpose, manycredit unions have eliminated thepractice of closing during mid-dayhours, and now provide service onweekends and offer extendedevening hours with window serviceafter the lobby is closed.

Convenient access also requires:

• A well-planned physical layout tocontrol public traffic

• Sufficient human resources tofacilitate transactions

• Simple, streamlined procedures toprovide savers with fast and cost-effective service

Time-consuming procedures willincrease the costs of savings forclients and may deter prospectiveclients. Institutions must formalizeclear, standardized and streamlinedprocedures for the administration of savings accounts to limit the timenecessary for clients to open accounts,make deposits or take out withdrawals.

Providing Savings Services

Managing SavingsLIQUIDITYThe WOCCU Standards of Excellencerequire that a savings institution main-tain a minimum of 15% of the savingsportfolio in cash liquidity reserves toensure response for withdrawaldemands. An institution’s ability tocapture savings depends largely on the confidence of local savers. If thereis a perception that the institution doesnot have the funds to pay out savings,then both small and large savers willwithdraw their deposits. For large savings accounts above a certainthreshold, institutions should maintaina minimum 20% liquidity reserve tomitigate the concentration risk.

EFFICIENCYThe best financial intermediariesstrive to maximize efficiency so that

they can afford to pay attractiverates on savings, charge competi-tive rates on loans and build capitalreserves. Savings institutions shouldstrive to keep their operating expenses(operating expenses/average assets) tobetween five and 10% of total assets.The discipline of maintaining lowoperating expenses ensures that aninstitution does not allocate too muchof its resources on personnel or admin-istration that do not generate income.

Non-earning assets should be limited to7% or less of total assets. Limiting non-earning assets prevents a savings insti-tution from investing deposits in fixedassets, such as an ostentatious building,which would limit the returns on those deposits.

CASH MANAGEMENTFor institutions that have not offeredsavings services previously or thathave only received savings via pay-roll deduction, the receipt of over thecounter cash deposits poses a new setof risks. A savings institution mustput into place procedures andinternal controls for handlingdeposits and withdrawals.

Access to the teller and vault areas bypersons unrelated to the cash opera-tions should be restricted. Internal policies should regulate the maximumamount of cash kept on hand in orderto minimize potential losses and avoidendangering the persons responsiblefor handling it. The amount of cash onhand should not exceed the insurancecoverage for cash losses.

- 13 -

- 14 -

INTERNAL CONTROLSInternal controls for savings manage-ment are implemented through rulesfor common transactions. Examples ofsuch rules include:

• Document all teller transactionswith receipts

• Include teller identification on allpassbook entries or receipts

• Prohibit tellers from keeping clientpassbooks at the institution

• Prevent any official or employeefrom transacting business on his orher own account or on a familymember’s account

Savings institutions must maintain a separation of functions so that theemployees who approve or conductbusiness in the organization are not the same ones who do the processing, prepare accountingentries and maintain the internal partof the transactions.

The total amount of money received,either by means of check or cash, in

daily operations should be depositedin a formal bank account. The total ofthis daily deposit serves as a verifica-tion of the total daily income report.

COSTS RELATED TO SAVINGSNumerous non-financial costs associ-ated with designing, marketing, man-aging and protecting savings depositsare difficult to quantify beyond thedirect financial cost of the interestthat an institution pays clients ontheir savings deposits. As suggestedin previous sections of this guide,building sufficient trust in a clientpool in order to be able to attractdeposits involves physical image andsecurity enhancements, staff training,institutional policy changes, market-ing and many other costly activitieswhich can be difficult to separate outand quantify in monetary terms.

A savings institution may considerconducting a functional costing of savings-related financial and non-financial costs to determine what itactually spends to provide safe and

well-managed savings products. Acosting exercise can then enable thestaff of the institution to design andoffer a balanced range of financialproducts which mitigate both costsand risks.

MAKING THE TRANSITIONElecting to mobilize microsavingsfrom clients is a strategic long-term institutional decision. Themotivations of why, when and howan institution authorized to acceptdeposits should launch into acceptingthem can weigh on considerationssuch as client demand and institu-tional funding constraints.

The decision to become a savingsinstitution must be made with long-term perspective. Not only doesbuilding trust among clients absorbsignificant time and resources, butalso preparing the institution to adhereto the requisite financial disciplinestakes serious time and effort.

Managing Savings

World Council of Credit Unions, Inc. (WOCCU) has credit union affiliates in Africa,Asia, the Caribbean,Central Asia, Europe, Latin America, North America and the South Pacific.WOCCU manages long-term technical assistance programs to develop, strengthen and modernize credit unions and credit unionsystems around the world.WOCCU works to create an appropriate regulatory environment for safeand sound credit union operation.

Credit unions, or savings and credit cooperatives, are user-owned microfinance institutions that offer savings and credit services to their members in developing and transitioning countries.Membership in acredit union is based on a common bond,a linkage shared by savers and borrowers that can be based ona community,organizational, religious or employee affiliation.Depending on a country’s legal framework,credit unions may be authorized either by the Superintendency of Banks, the Central Bank, the Ministryof Finance, the Ministry of Cooperatives or a freestanding law to mobilize member savings.

Photo credits: Anna Cora Evans, Janette Klaehn, WOCCU Kenya, WOCCU Nicaragua and WOCCU Philippines

Home Office5710 Mineral Point RoadPO Box 2982Madison,WI 53701-2982 USAPhone: (608) 231-7130Fax: (608) 238-8020

Washington Office601 Pennsylvania Avenue, NW South Bldg., Ste. 600Washington, DC 20004-2601 USAPhone: (202) 638-0205Fax: (202) 638-3410

Websitewww.woccu.org