Embed Size (px)

Citation preview

1

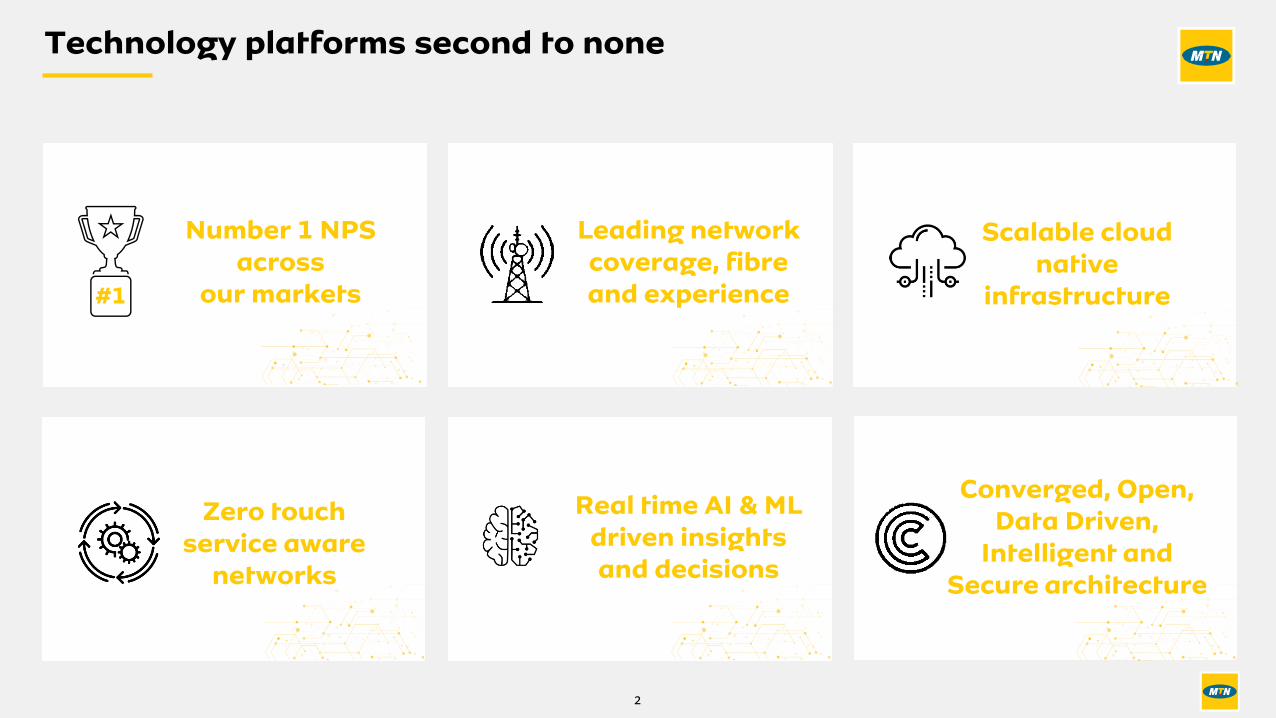

Technology platformssecond to none

Technology platforms second to none

2

#1

Number 1 NPS across

our markets

Zero touch service aware

networks

Scalable cloud native

infrastructure

Leading network coverage, fibre and experience

Real time AI & ML driven insights and decisions

Converged, Open, Data Driven,

Intelligent and Secure architecture

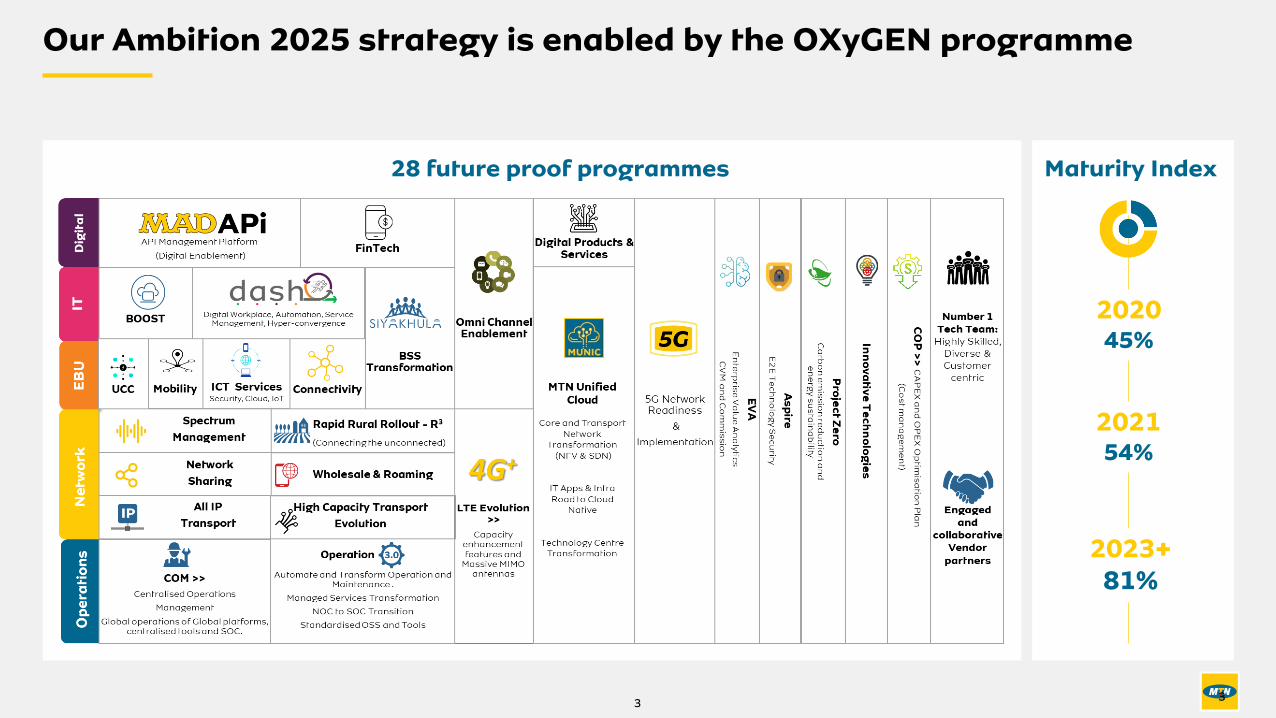

3

2020 45%

202154%

2023+81%

28 future proof programmes Maturity Index

Our Ambition 2025 strategy is enabled by the OXyGEN programme

3

4

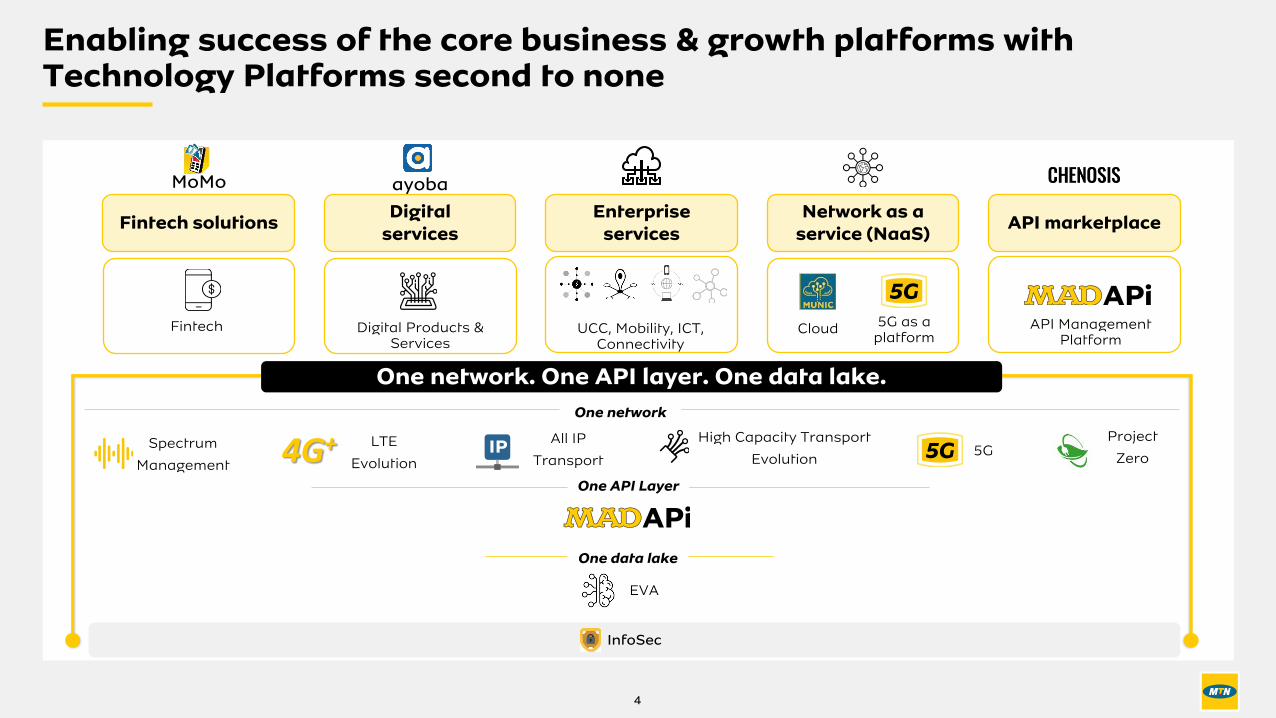

Fintech solutionsDigital

servicesEnterprise

servicesNetwork as a

service (NaaS)API marketplace

MoMo ayoba

One network. One API layer. One data lake.

Digital Products & Services

Fintech UCC, Mobility, ICT, Connectivity

Cloud 5G as a platform

API Management Platform

One API Layer

EVA

One data lake

InfoSec

All IP

Transport

High Capacity Transport

Evolution

One network

Project

Zero4G+ LTE

Evolution

Spectrum

Management5G

Enabling success of the core business & growth platforms with Technology Platforms second to none

5

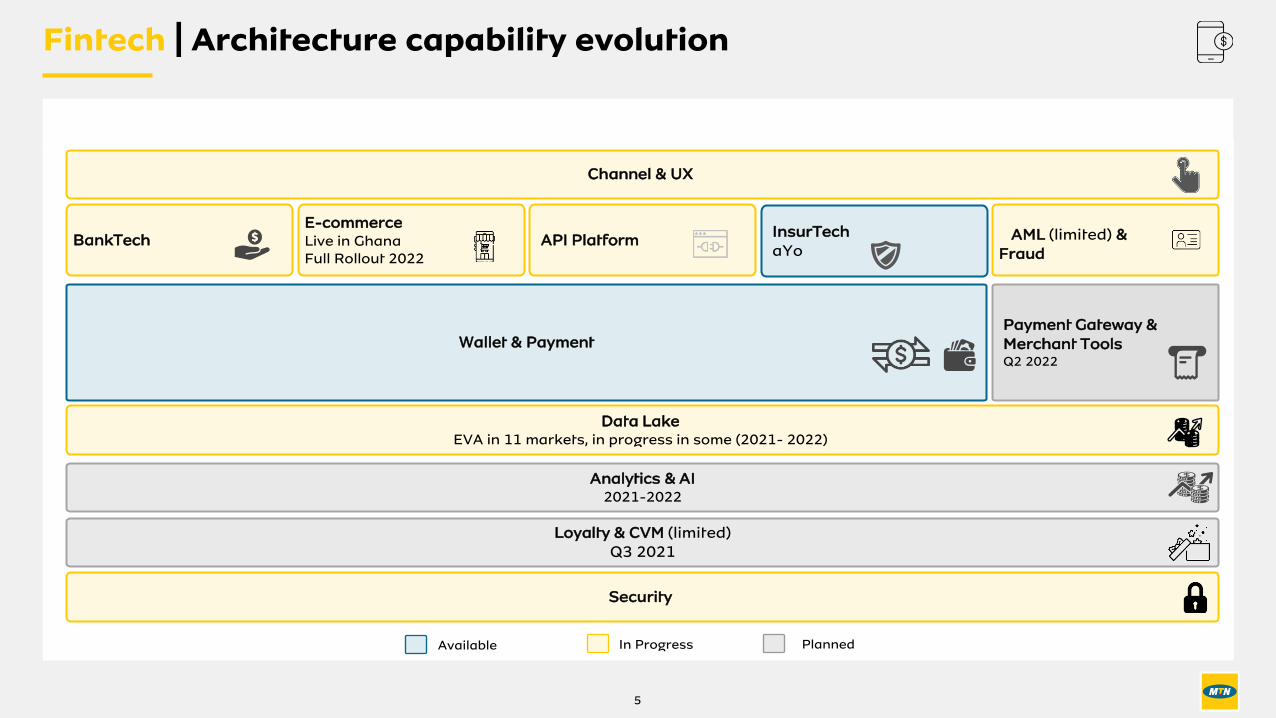

Fintech | Architecture capability evolution

Available In Progress Planned

Payment Gateway & Merchant ToolsQ2 2022

Security

AML (limited) & Fraud

InsurTechaYo

BankTechE-commerceLive in GhanaFull Rollout 2022

API Platform

Wallet & Payment

Loyalty & CVM (limited)Q3 2021

Analytics & AI2021-2022

Data LakeEVA in 11 markets, in progress in some (2021- 2022)

Channel & UX

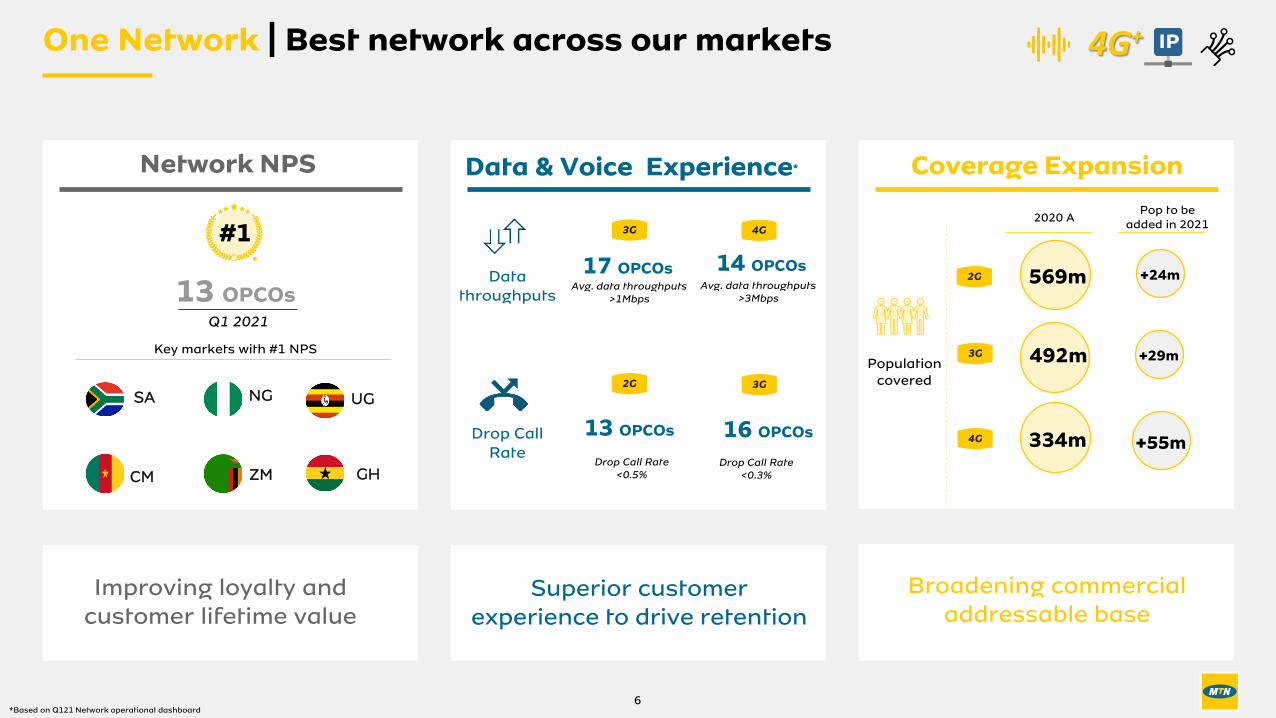

Network NPS Data & Voice Experience* Coverage Expansion

One Network | Best network across our markets

6

13 OPCOsQ1 2021

SA

Key markets with #1 NPS

NG UG

GHCM ZM

Improving loyalty and customer lifetime value

Broadening commercial addressable base

Superior customer experience to drive retention

Drop Call Rate

3G 4G

2G 3G

Avg. data throughputs >1Mbps

17 OPCOsAvg. data throughputs

>3Mbps

14 OPCOsData

throughputs

2G

3G

4G

Population covered

+24m

+29m

+55mDrop Call Rate

<0.5%Drop Call Rate

<0.3%

13 OPCOs 16 OPCOs

*Based on Q121 Network operational dashboard

4G+

Pop to be added in 2021

2020 A

569m

492m

334m

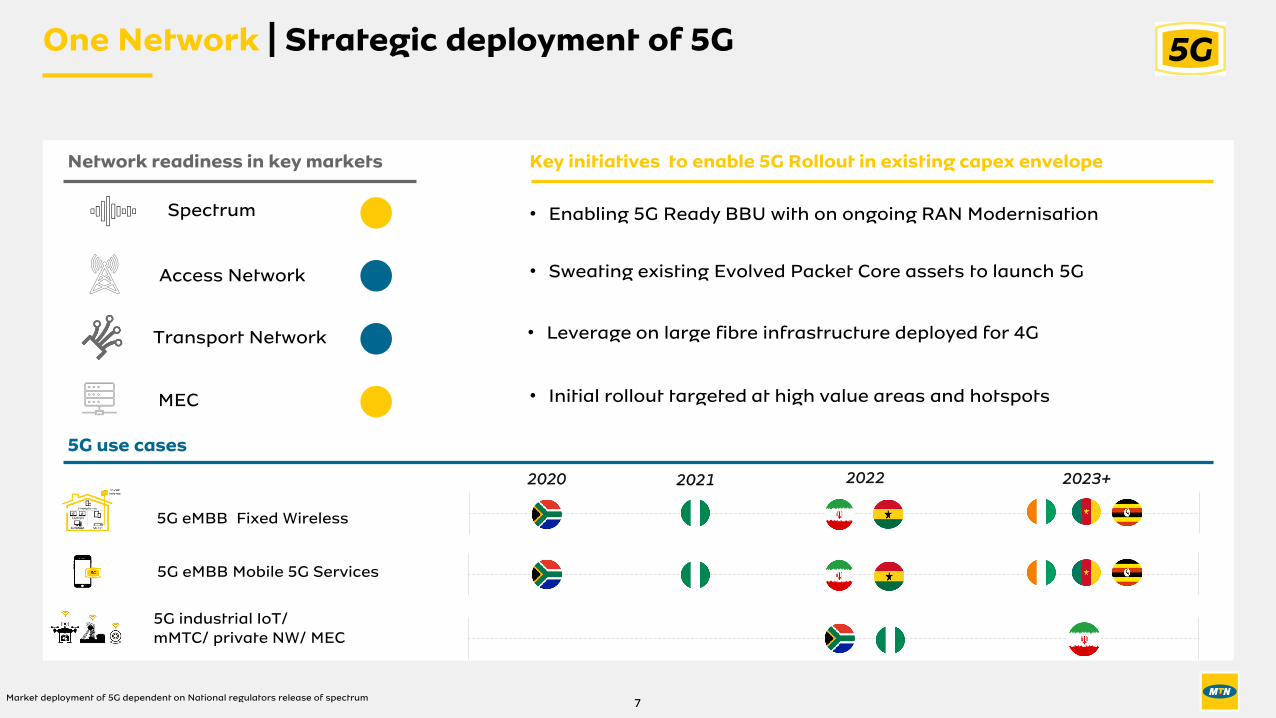

2020

5G eMBB Fixed Wireless

5G eMBB Mobile 5G Services

5G industrial IoT/mMTC/ private NW/ MEC

2021 2022 2023+

MEC

One Network | Strategic deployment of 5G

Spectrum

Access Network

Market deployment of 5G dependent on National regulators release of spectrum

Transport Network

Network readiness in key markets Key initiatives to enable 5G Rollout in existing capex envelope

• Enabling 5G Ready BBU with on ongoing RAN Modernisation

• Sweating existing Evolved Packet Core assets to launch 5G

• Leverage on large fibre infrastructure deployed for 4G

• Initial rollout targeted at high value areas and hotspots

5G use cases

7

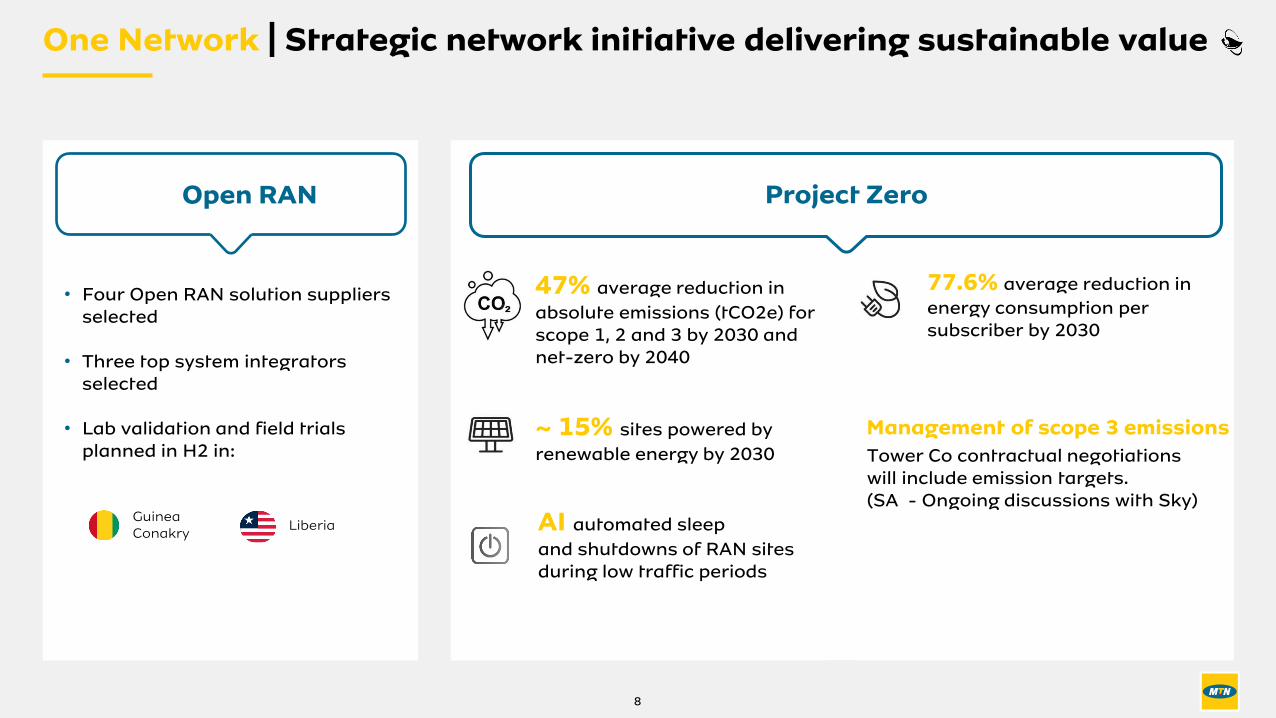

Open RAN

• Four Open RAN solution suppliers selected

• Three top system integrators selected

• Lab validation and field trials planned in H2 in:

Guinea Conakry

Liberia

47% average reduction in

absolute emissions (tCO2e) for scope 1, 2 and 3 by 2030 and net-zero by 2040

77.6% average reduction in

energy consumption per subscriber by 2030

~ 15% sites powered by

renewable energy by 2030

Project Zero

Management of scope 3 emissions

Tower Co contractual negotiations will include emission targets.(SA - Ongoing discussions with Sky)

AI automated sleep

and shutdowns of RAN sites during low traffic periods

One Network | Strategic network initiative delivering sustainable value

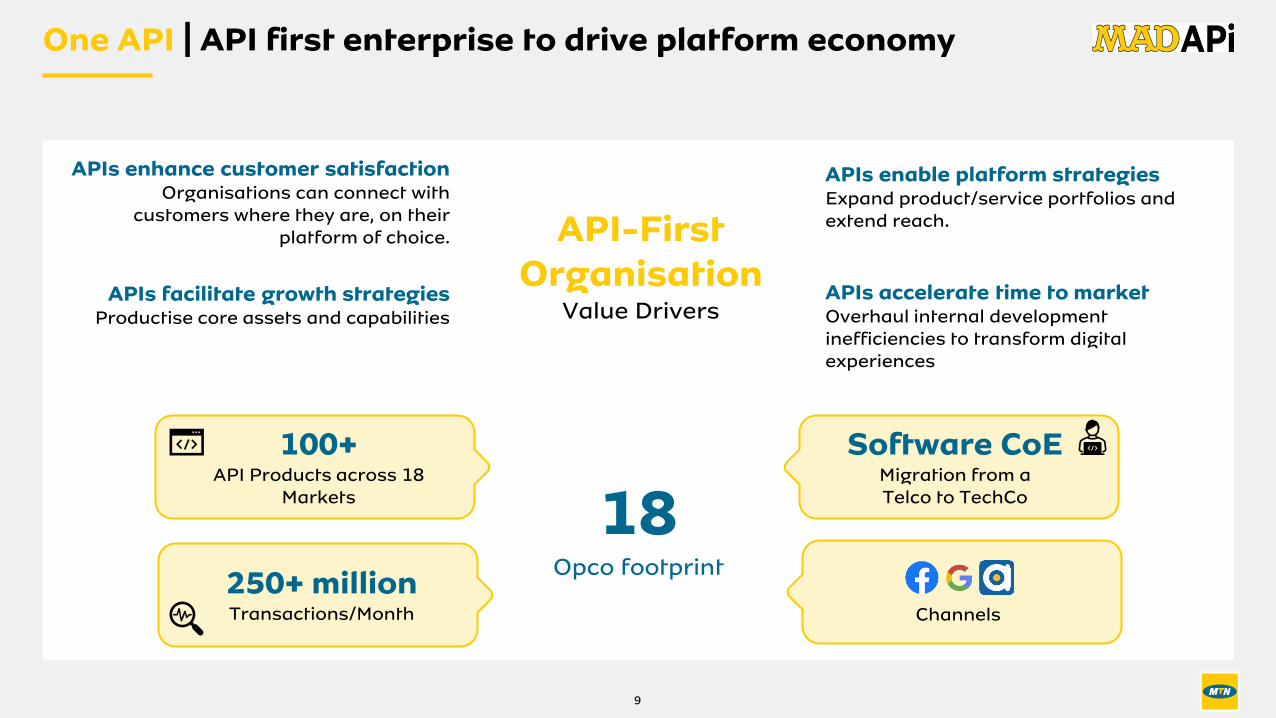

8

18Opco footprint

Channels

Software CoEMigration from aTelco to TechCo

250+ millionTransactions/Month

100+API Products across 18

Markets

API-FirstOrganisation

Value Drivers

APIs enhance customer satisfactionOrganisations can connect with

customers where they are, on their platform of choice.

APIs facilitate growth strategiesProductise core assets and capabilities

APIs enable platform strategiesExpand product/service portfolios and extend reach.

APIs accelerate time to market Overhaul internal development inefficiencies to transform digital experiences

One API | API first enterprise to drive platform economy

9

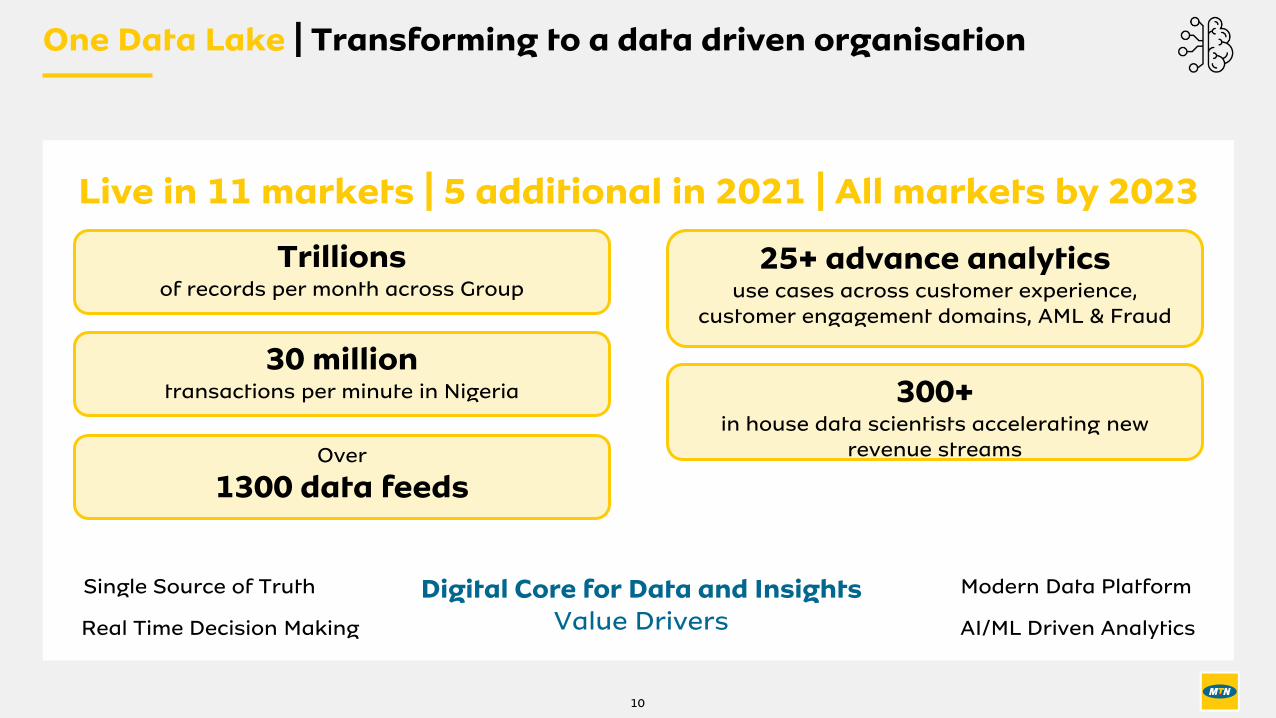

Over

1300 data feeds

Trillionsof records per month across Group

25+ advance analyticsuse cases across customer experience,

customer engagement domains, AML & Fraud

Live in 11 markets | 5 additional in 2021 | All markets by 2023

Digital Core for Data and InsightsValue Drivers

Single Source of Truth

Real Time Decision Making

Modern Data Platform

AI/ML Driven Analytics

300+in house data scientists accelerating new

revenue streams

One Data Lake | Transforming to a data driven organisation

30 milliontransactions per minute in Nigeria

10

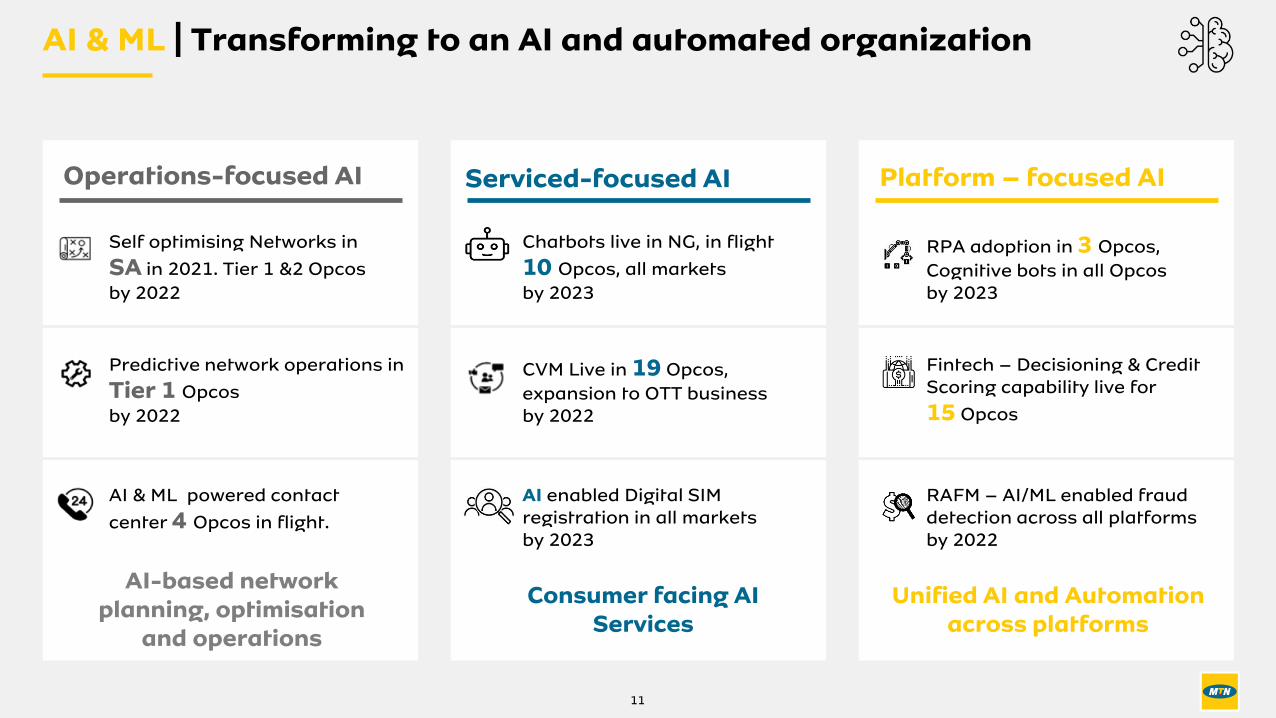

AI & ML | Transforming to an AI and automated organization

Self optimising Networks in

SA in 2021. Tier 1 &2 Opcos

by 2022

CVM Live in 19 Opcos,

expansion to OTT businessby 2022

RPA adoption in 3 Opcos,

Cognitive bots in all Opcosby 2023

Fintech – Decisioning & Credit Scoring capability live for

15 Opcos

RAFM – AI/ML enabled fraud detection across all platformsby 2022

Chatbots live in NG, in flight

10 Opcos, all markets

by 2023

Predictive network operations in

Tier 1 Opcos

by 2022

AI enabled Digital SIM registration in all marketsby 2023

AI & ML powered contact

center 4 Opcos in flight.

Operations-focused AI Serviced-focused AI Platform – focused AI

AI-based network planning, optimisation

and operations

Consumer facing AI Services

Unified AI and Automation across platforms

11

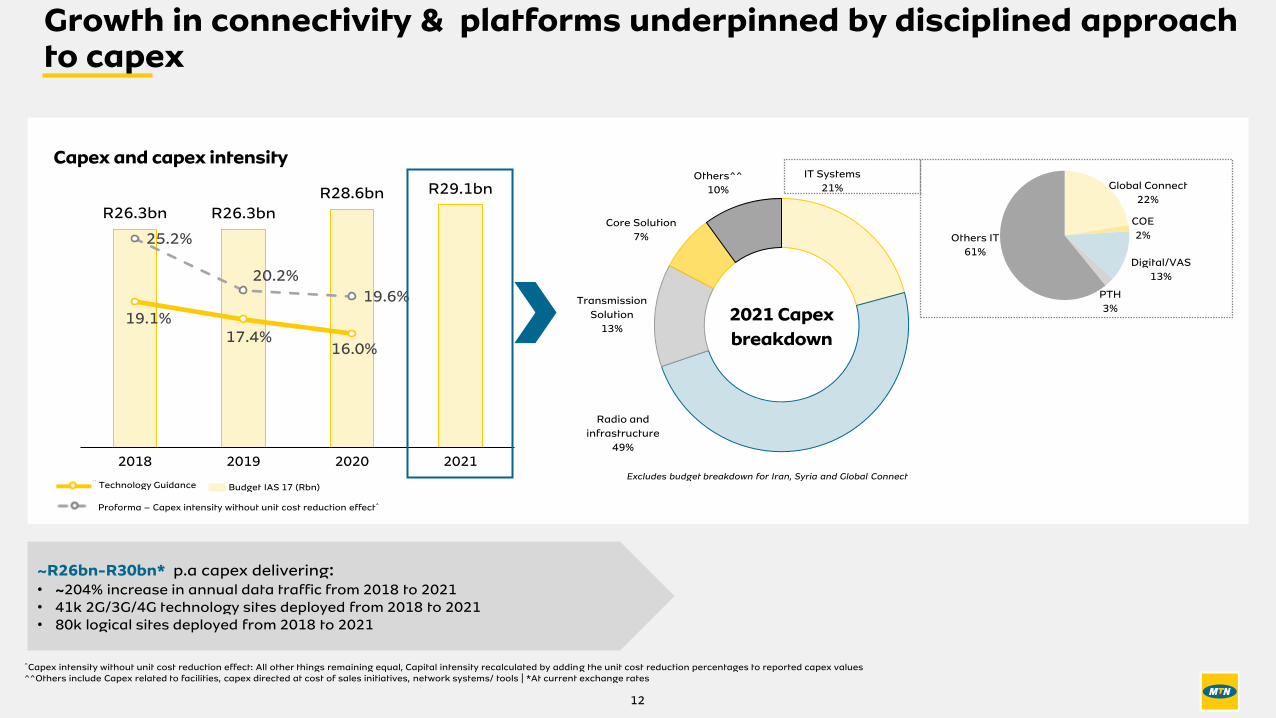

R26.3bn R26.3bn

R28.6bn R29.1bn

19.1%17.4%

16.0%

25.2%

20.2%

19.6%

1

6

11

16

21

26

31

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

2018 2019 2020 2021

Capex and capex intensity

Technology Guidance

Proforma – Capex intensity without unit cost reduction effect^

Budget IAS 17 (Rbn)

^Capex intensity without unit cost reduction effect: All other things remaining equal, Capital intensity recalculated by adding the unit cost reduction percentages to reported capex values^^Others include Capex related to facilities, capex directed at cost of sales initiatives, network systems/ tools | *At current exchange rates

Radio and

infrastructure

49%

IT Systems

21%

Transmission

Solution

13%

Core Solution

7%

Others^^

10%

2021 Capex

breakdown

Excludes budget breakdown for Iran, Syria and Global Connect

Global Connect

22%

COE

2%Others IT

61%

PTH

3%

Digital/VAS

13%

~R26bn-R30bn* p.a capex delivering:• ~204% increase in annual data traffic from 2018 to 2021• 41k 2G/3G/4G technology sites deployed from 2018 to 2021• 80k logical sites deployed from 2018 to 2021

Growth in connectivity & platforms underpinned by disciplined approach to capex

12

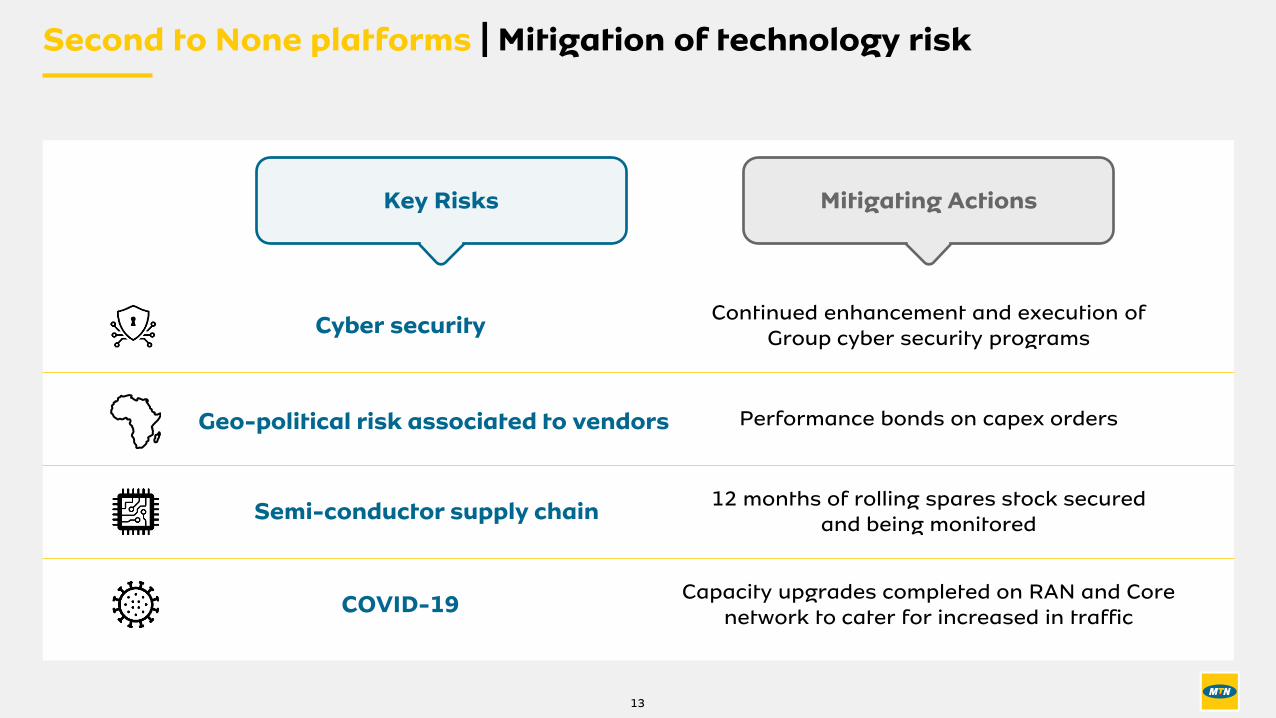

Semi-conductor supply chain12 months of rolling spares stock secured

and being monitored

COVID-19 Capacity upgrades completed on RAN and Core

network to cater for increased in traffic

Cyber security Continued enhancement and execution of

Group cyber security programs

Geo-political risk associated to vendors Performance bonds on capex orders

Second to None platforms | Mitigation of technology risk

Key Risks Mitigating Actions

13

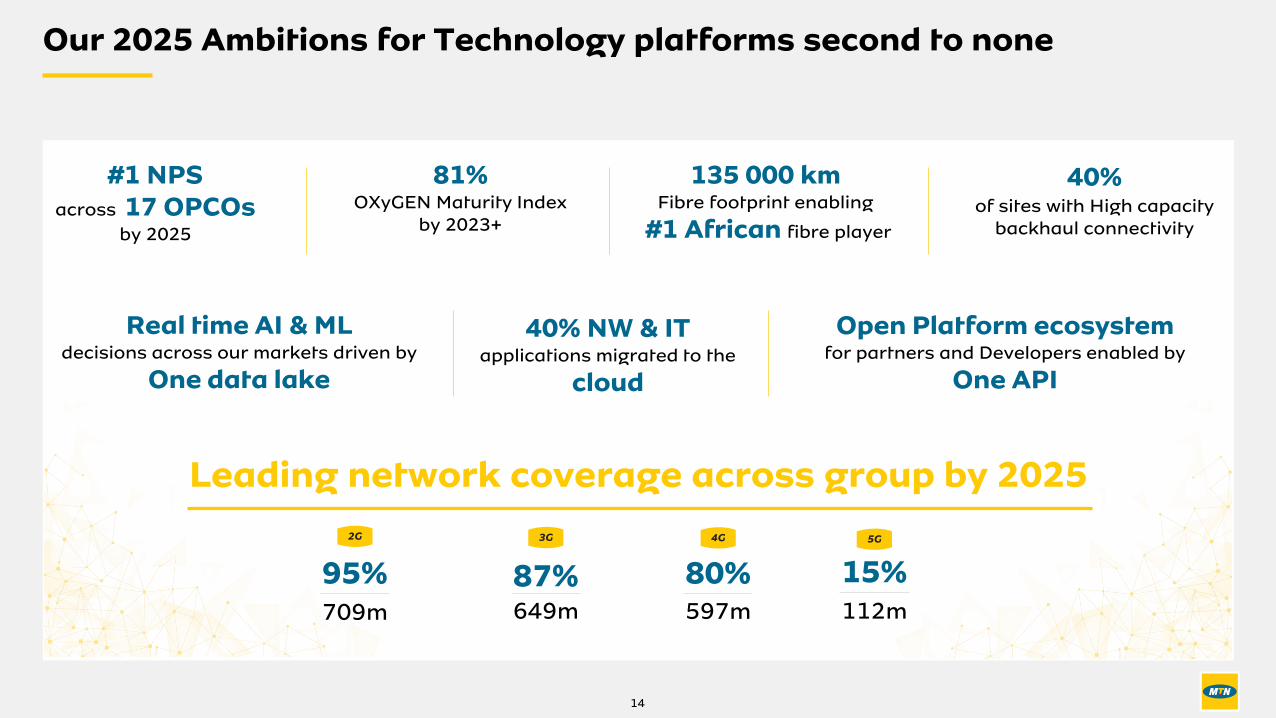

Our 2025 Ambitions for Technology platforms second to none

135 000 km Fibre footprint enabling

#1 African fibre player

#1 NPS across 17 OPCOs

by 2025

Real time AI & ML decisions across our markets driven by

One data lake

40%of sites with High capacity

backhaul connectivity

2G 3G 4G 5G

Leading network coverage across group by 2025

95% 87% 80% 15%709m 649m 597m 112m

40% NW & IT applications migrated to the

cloud

Open Platform ecosystem for partners and Developers enabled by

One API

81%OXyGEN Maturity Index

by 2023+

14