Embed Size (px)

Citation preview

1 Technology Teach-in June 2016

Technology Teach-inDumbarton, 8 June 2016

2 Technology Teach-in June 2016

Chris Weston, CEO

Introduction1

3 Technology Teach-in June 2016

Chris Weston, CEOIntroduction1

Agenda

Volker Schulte, Director of Manufacturing and Technology

Technology at Aggreko2

Site tour3

VariousBreak out groups4

Site tour - Birch Road5

4 Technology Teach-in June 20164

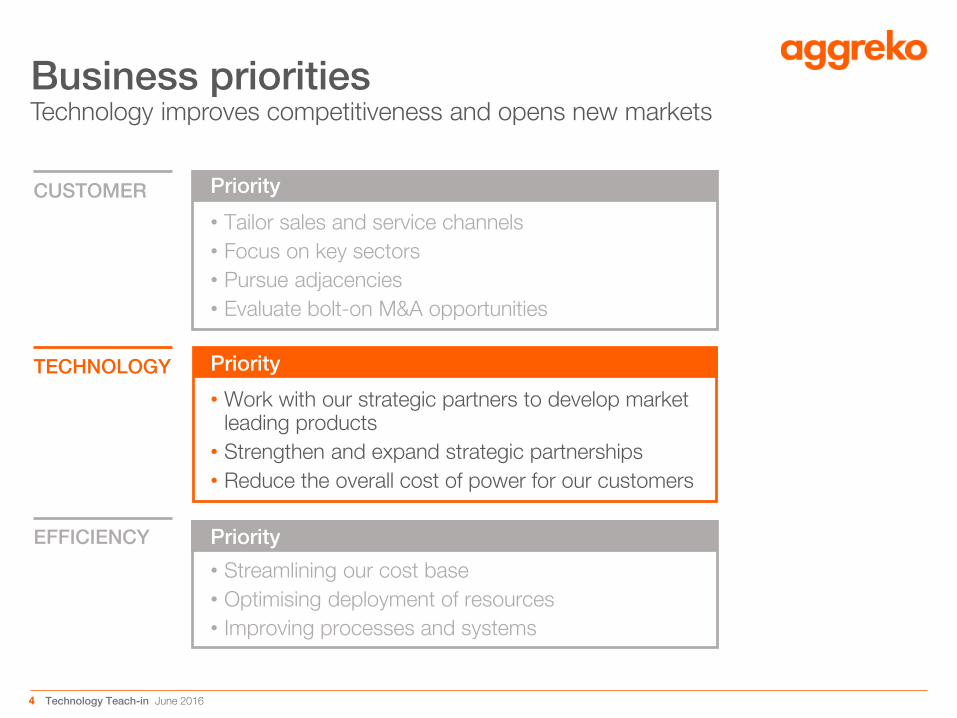

Business prioritiesTechnology improves competitiveness and opens new markets

CUSTOMER

TECHNOLOGY

EFFICIENCY

• Tailor sales and service channels

• Focus on key sectors

• Pursue adjacencies

• Evaluate bolt-on M&A opportunities

Priority

• Work with our strategic partners to develop market leading products

• Strengthen and expand strategic partnerships

• Reduce the overall cost of power for our customers

Priority

• Streamlining our cost base

• Optimising deployment of resources

• Improving processes and systems

Priority

5 Technology Teach-in June 2016

Capability at Dumbarton central to what we do

Manufacturing & Technology

• 10GW fleet covering range of different products

− Generators ranging from 20kW to 1.8MW

− Up to 75% of capex is managed at Dumbarton

• Centre of technical excellence and flexible production facility

− Engineering and design capability

− Experienced and skilled production team

• Product requirements

− Short lead time for new product

− Speed of deployment

− Extreme operating environments

• Strong supplier relationships

− Cummins supports 6,000MW in fleet

6 Technology Teach-in June 2016

Technology improves competitiveness and opens new markets

6

Areas of focus

• New fuel types

• Fuel efficiency: compatibility with existing fleet

• Leveraging supplier relationships and product development capability

• Strict structures around product development and introduction

• Improving efficiency across life of the product: total cost of ownership

7 Technology Teach-in June 2016

New medium speed HFO engine

HFO

• Commonly used fuel in permanent power

• Works to fill the gap in the market between diesel and gas

• Launching a medium speed HFO engine in Q1 2017: now in production

• Uses 1.8MW MAN engine: a leading manufacturer of medium speed engines

• Packaged in standard ISO 40 foot containers

• Compliant with World Bank emissions requirements

8 Technology Teach-in June 2016

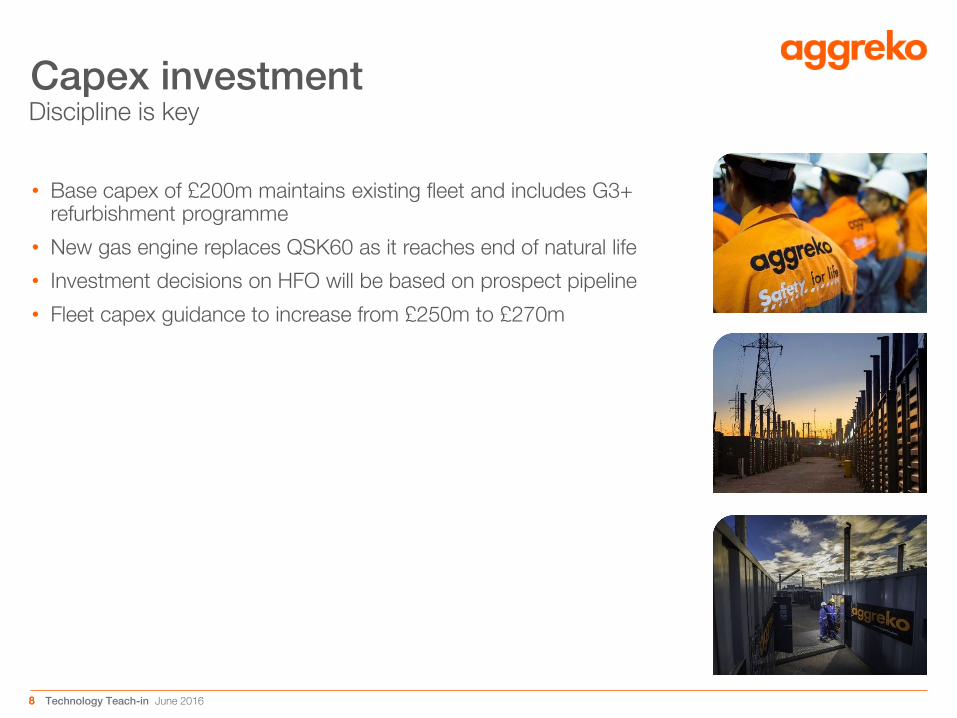

Discipline is key

8

Capex investment

• Base capex of £200m maintains existing fleet and includes G3+ refurbishment programme

• New gas engine replaces QSK60 as it reaches end of natural life

• Investment decisions on HFO will be based on prospect pipeline

• Fleet capex guidance to increase from £250m to £270m

9 Technology Teach-in June 2016

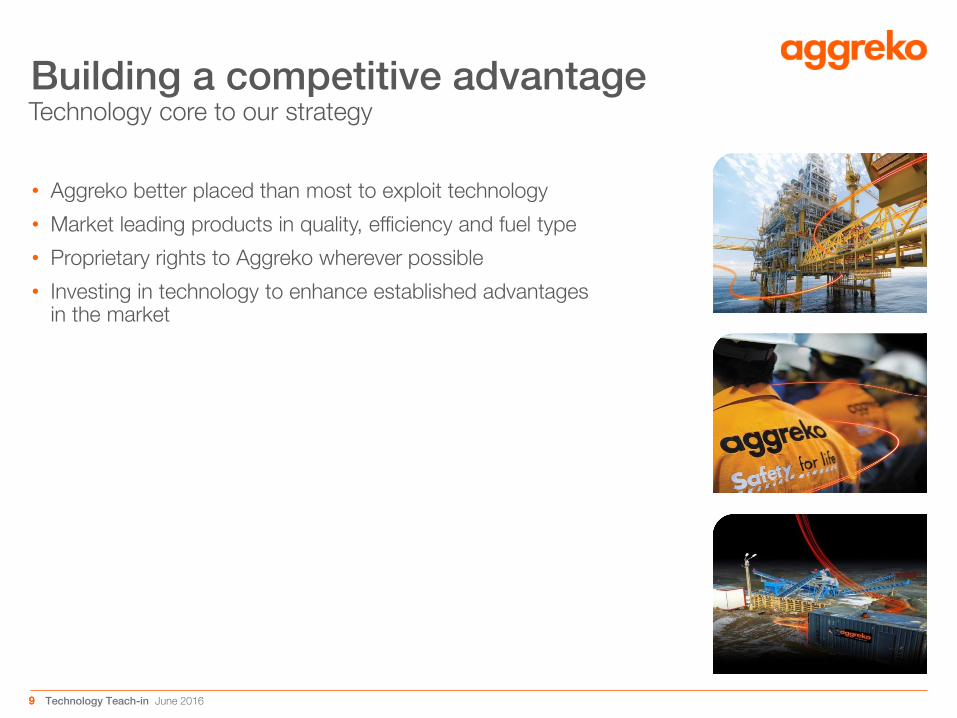

Technology core to our strategy

9

Building a competitive advantage

• Aggreko better placed than most to exploit technology

• Market leading products in quality, efficiency and fuel type

• Proprietary rights to Aggreko wherever possible

• Investing in technology to enhance established advantages in the market

10 Technology Teach-in June 2016

Volker Schulte, Director of Manufacturing & Technology

Technology at Aggreko2

11 Technology Teach-in June 2016

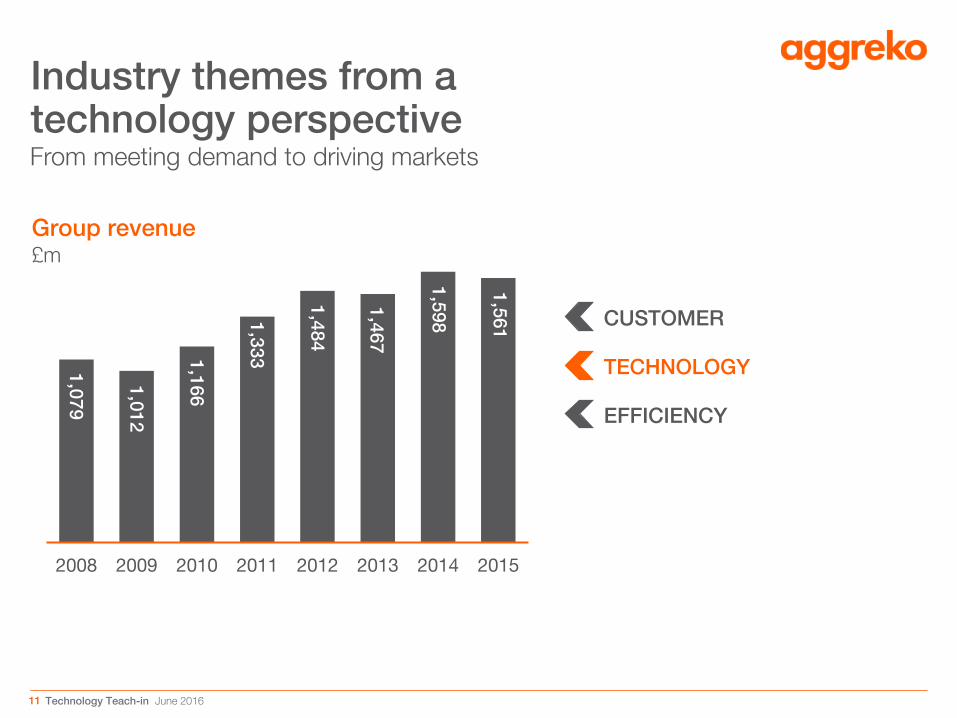

2008 2009 2010 2011 2012 2013 2014 2015

From meeting demand to driving markets

Industry themes from a technology perspective

CUSTOMER

Group revenue£m

1,0

79

1,0

12

1,1

66

1,3

33

1,4

84

1,4

67

1,5

98

1,5

61

TECHNOLOGY

EFFICIENCY

12 Technology Teach-in June 2016

From a technology perspective

Industry themes

Fuel types

• Temporary power sector predominantly diesel based

• Demand for credible alternatives

• HFO provides mid point between lower cost of gas and ubiquitous nature of diesel

13 Technology Teach-in June 2016

From a technology perspective

Industry themes

Fuel types

• Temporary power sector predominantly diesel based

• Demand for credible alternatives

• HFO provides mid point between lower cost of gas and ubiquitous nature of diesel

Efficiency

• More fuel efficient products are more competitive

• Potential to challenge permanent power

− Opens up wider applications for our products

− Real solution to variability caused by distributed generation

14 Technology Teach-in June 2016

From a technology perspective

Industry themes

Fuel types

• Temporary power sector predominantly diesel based

• Demand for credible alternatives

• HFO provides mid point between lower cost of gas and ubiquitous nature of diesel

Efficiency

• More fuel efficient products are more competitive

• Potential to challenge permanent power

− Opens up wider applications for our products

− Real solution to variability caused by distributed generation

Renewables

• Modular renewables / fossil fuel combinations can lower the cost to customers

15 Technology Teach-in June 2016

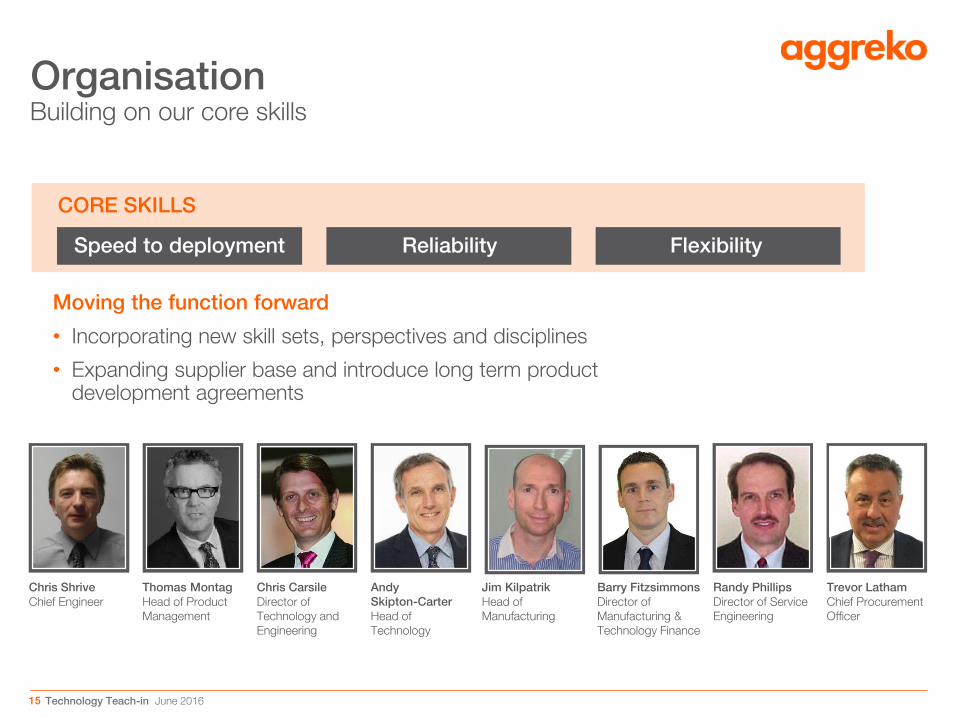

Organisation

Moving the function forward

• Incorporating new skill sets, perspectives and disciplines

• Expanding supplier base and introduce long term product development agreements

Building on our core skills

CORE SKILLS

Speed to deployment Reliability Flexibility

Thomas Montag

Head of Product

Management

Chris Shrive

Chief Engineer

Trevor Latham

Chief Procurement

Officer

Randy Phillips

Director of Service

Engineering

Chris Carsile

Director of

Technology and

Engineering

Andy

Skipton-Carter

Head of

Technology

Barry Fitzsimmons

Director of

Manufacturing &

Technology Finance

Jim Kilpatrik

Head of

Manufacturing

16 Technology Teach-in June 2016

FUEL TYPES

• Medium speed HFO to market early 2017

• Clear advantages to being first to market

New productsOpening new markets and improving competitiveness

17 Technology Teach-in June 2016

New products

FUEL TYPES

EFFICIENCY

New gas engine

• New gas engine 10% more fuel efficient

• Far closer to permanent power

G3+

• 5% more fuel efficient

• In market today and helping win contracts

• G3++ in development

Remote monitoring

• Rolling out across fleet

• Improvements to reliability and off cycle maintenance

• Reduces redundancy contingency

Opening new markets and improving competitiveness

Relative cost of power$/MWh

Combined

cycle Gas

Turbine

Open

cycle Gas

Turbine

Advanced

coal

Next

Gen

Gas

G3+

0

25

50

75

100

125

150

175

200

Permanent Mobile

18 Technology Teach-in June 2016

New products

FUEL SOURCES

EFFICIENCY

RENEWABLES

Solar diesel hybrid

• Currently in evaluation - could reduce costs of modular power solution to customers by 10%

• Exploring options on partnering with a solar provider

Batteries

• Monitoring, at present high capital cost to power density

• Reduces overall fuel consumption

• Potential role alongside renewables

Opening new markets and improving competitiveness

19 Technology Teach-in June 2016

New products

FUEL SOURCES

EFFICIENCY

RENEWABLES

SECTOR SPECIFIC PRODUCTS

• Power solutions: products using Liquefied Petroleum Gas (LPG) or Compressed Natural Gas (CNG)

• Rental Solutions; flare gas micro grids, TC process engineering solutions for the PCR sector

Opening new markets and improving competitiveness

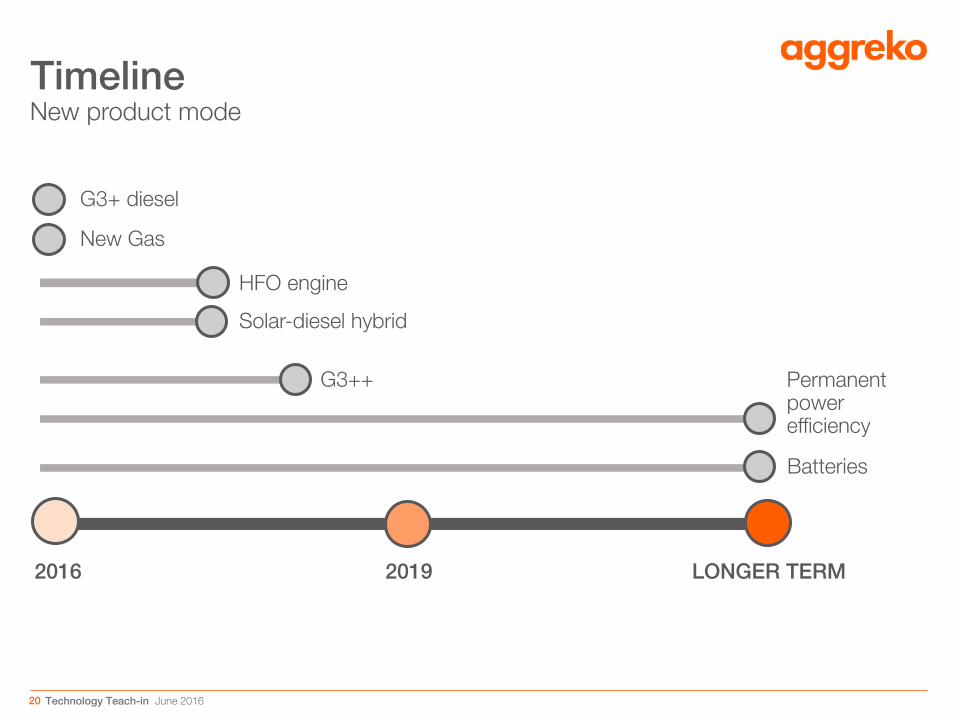

20 Technology Teach-in June 2016

New product mode

Timeline

2016 2019 LONGER TERM

New Gas

G3+ diesel

Solar-diesel hybrid

HFO engine

Permanentpowerefficiency

G3++

Batteries

21 Technology Teach-in June 2016

Meeting the Team

Break out sessions

Future Technologies and Renewables

Chris Carsile Director of Technology and Engineering

Andy Skipton-Carter Head of Technology

Total Cost of Ownership

Randy Phillips Director of Service Engineering

Trevor Latham Chief Procurement Officer

New Product Offerings

Chris Shrive Chief Engineer

Thomas Montag Head of Product Management

Current Product Offerings & Manufacturing Flexibility

Jim Kilpatrik Head of Manufacturing

Barry Fitzsimmons Director of Manufacturing & Technology Finance