Embed Size (px)

Citation preview

Equity Research

9 September 2019

FOCUS

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment decision.

This research report has been prepared in whole or in part by equity research analysts

based outside the US who are not registered/qualified as research analysts with FINRA.

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 41.

Re

stri

cte

d -

In

tern

al

Telecom Services and Tech Hardware

5G – The Return of Fixed Substitution

Fixed Wireless Access (FWA) has until now been a relatively niche service offering.

This is about to change. The advent of 5G brings significant capacity increases to

wireless networks, and we see mobile challengers set to seize on this to attack fixed

broadband, especially in markets that lack meaningful FTTH (UK/Germany/Italy).

Our extensive research and conversations with key market participants lead us to

conclude that mobile challengers will be incentivised to capitalize on this

opportunity, as near-term risks are very low, and business case appears compelling.

FWA business case appear compelling with 5G – Most challengers will likely try. We

estimate a >10x increase in wireless capacity over the next 5 years, as 5G brings greater

spectrum efficiency, with more spectrum also becoming available. For mobile operators

this will allow them to manage ever-increasing wireless demand. Crucially, they will also

be able to consider offering high-speed broadband over wireless as an alternative to

fixed. The near-term FWA investment risks for mobile operators are low, as any capex

needs are both incremental and success-based, and initially very modest.

FWA as a ‘copper killer’ – We see 5-10% of broadband market at risk from FWA. Our

detailed analysis uses unique and proprietary data to look at the market opportunity for

mobile operators to target urban, suburban and rural areas with FWA. Our research

indicates a network cost of just c€5-10/sub/month, assuming c50-100mbps speeds.

We identify 5-10% of the fixed broadband market at risk (with greatest risk in copper-

heavy markets such as the UK/Germany/Italy, lower in FTTH-heavy markets).

Stock implications – EU and US Telcos. We see increased broadband price competition

from FWA solutions into the Consumer segments in markets like the UK, Germany, Italy

and US, which is unhelpful for sentiment, with BT/TI/DT most exposed (on the other

hand, DT has positive exposure through TMUS). In terms of EU-based beneficiaries, we

see TEF De (OW), Drillisch (OW) and Sunrise (EW) as positively exposed, and separately

initiate coverage on Big Blu Broadband (BBB LN with an OW rating).

Stock implications – EU Tech HW. Telecom equipment vendors Nokia (OW) and

Ericsson (EW) both actively encourage operators to consider FWA strategies. While

initial incremental capex is modest, as mobile challengers can leverage existing assets, if

the provider is successful, then we would expect to see additional success-based

investment. We view FWA as an additional, if modest, tailwind to the broader 5G

adoption growth we model for mobile equipment vendors.

INDUSTRY UPDATE

European Technology Hardware

NEUTRAL

Unchanged

European Telecom Services

POSITIVE

Unchanged

U.S. Cable, Satellite & Telecom Services

NEUTRAL

Unchanged

European Telecom Services

Maurice Patrick

+44 (0)20 3134 3622

Barclays, UK

Mathieu Robilliard

+44 (0)20 3134 3288

BBI, Paris

Simon Coles

+44 (0)20 3555 4519

Barclays, UK

European Technology Hardware

Andrew M. Gardiner, CFA

+44 (0)20 3134 7217

Barclays, UK

U.S. Cable, Satellite & Telecom Services

Kannan Venkateshwar

+1 212 528 7054

BCI, US

IT Hardware and Communications

Equipment

Tim Long

+1 212 526 4043

BCI, US

Barclays | Telecom Services and Tech Hardware

9 September 2019 2

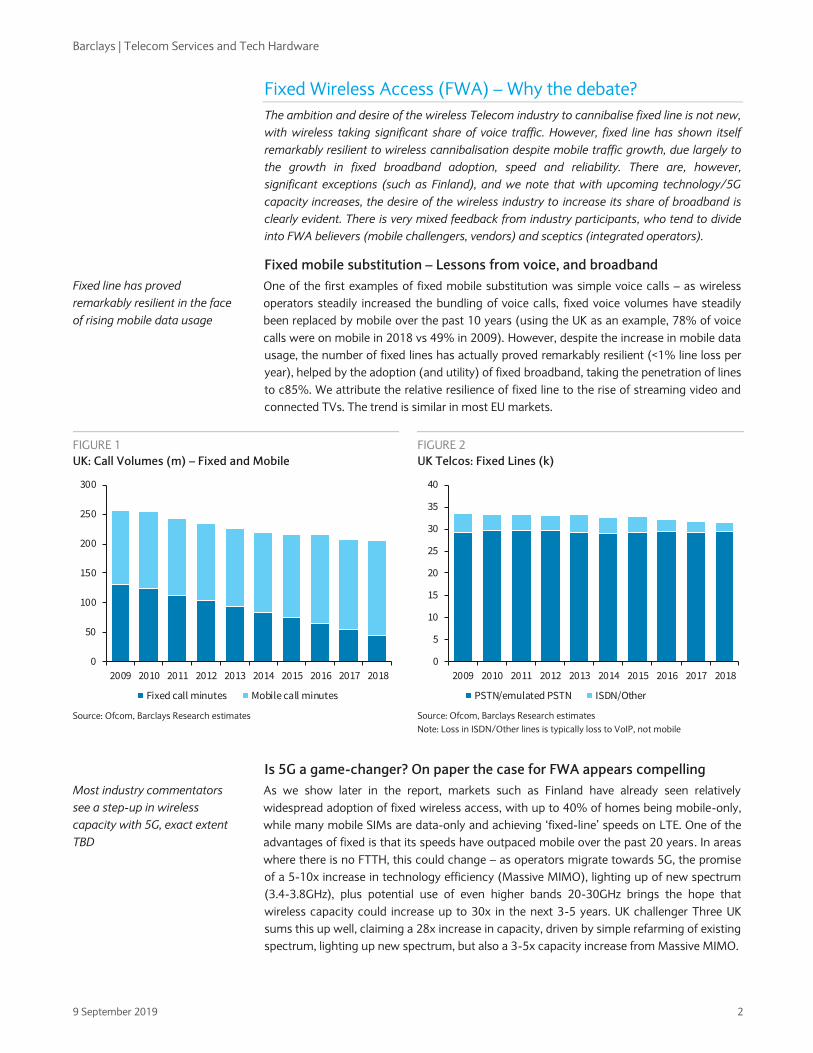

Fixed Wireless Access (FWA) – Why the debate?

The ambition and desire of the wireless Telecom industry to cannibalise fixed line is not new,

with wireless taking significant share of voice traffic. However, fixed line has shown itself

remarkably resilient to wireless cannibalisation despite mobile traffic growth, due largely to

the growth in fixed broadband adoption, speed and reliability. There are, however,

significant exceptions (such as Finland), and we note that with upcoming technology/5G

capacity increases, the desire of the wireless industry to increase its share of broadband is

clearly evident. There is very mixed feedback from industry participants, who tend to divide

into FWA believers (mobile challengers, vendors) and sceptics (integrated operators).

Fixed mobile substitution – Lessons from voice, and broadband

One of the first examples of fixed mobile substitution was simple voice calls – as wireless

operators steadily increased the bundling of voice calls, fixed voice volumes have steadily

been replaced by mobile over the past 10 years (using the UK as an example, 78% of voice

calls were on mobile in 2018 vs 49% in 2009). However, despite the increase in mobile data

usage, the number of fixed lines has actually proved remarkably resilient (<1% line loss per

year), helped by the adoption (and utility) of fixed broadband, taking the penetration of lines

to c85%. We attribute the relative resilience of fixed line to the rise of streaming video and

connected TVs. The trend is similar in most EU markets.

FIGURE 1

UK: Call Volumes (m) – Fixed and Mobile

FIGURE 2

UK Telcos: Fixed Lines (k)

Source: Ofcom, Barclays Research estimates Source: Ofcom, Barclays Research estimates

Note: Loss in ISDN/Other lines is typically loss to VoIP, not mobile

Is 5G a game-changer? On paper the case for FWA appears compelling

As we show later in the report, markets such as Finland have already seen relatively

widespread adoption of fixed wireless access, with up to 40% of homes being mobile-only,

while many mobile SIMs are data-only and achieving ‘fixed-line’ speeds on LTE. One of the

advantages of fixed is that its speeds have outpaced mobile over the past 20 years. In areas

where there is no FTTH, this could change – as operators migrate towards 5G, the promise

of a 5-10x increase in technology efficiency (Massive MIMO), lighting up of new spectrum

(3.4-3.8GHz), plus potential use of even higher bands 20-30GHz brings the hope that

wireless capacity could increase up to 30x in the next 3-5 years. UK challenger Three UK

sums this up well, claiming a 28x increase in capacity, driven by simple refarming of existing

spectrum, lighting up new spectrum, but also a 3-5x capacity increase from Massive MIMO.

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Fixed call minutes Mobile call minutes

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

PSTN/emulated PSTN ISDN/Other

Fixed line has proved

remarkably resilient in the face

of rising mobile data usage

Most industry commentators

see a step-up in wireless

capacity with 5G, exact extent

TBD

Barclays | Telecom Services and Tech Hardware

9 September 2019 3

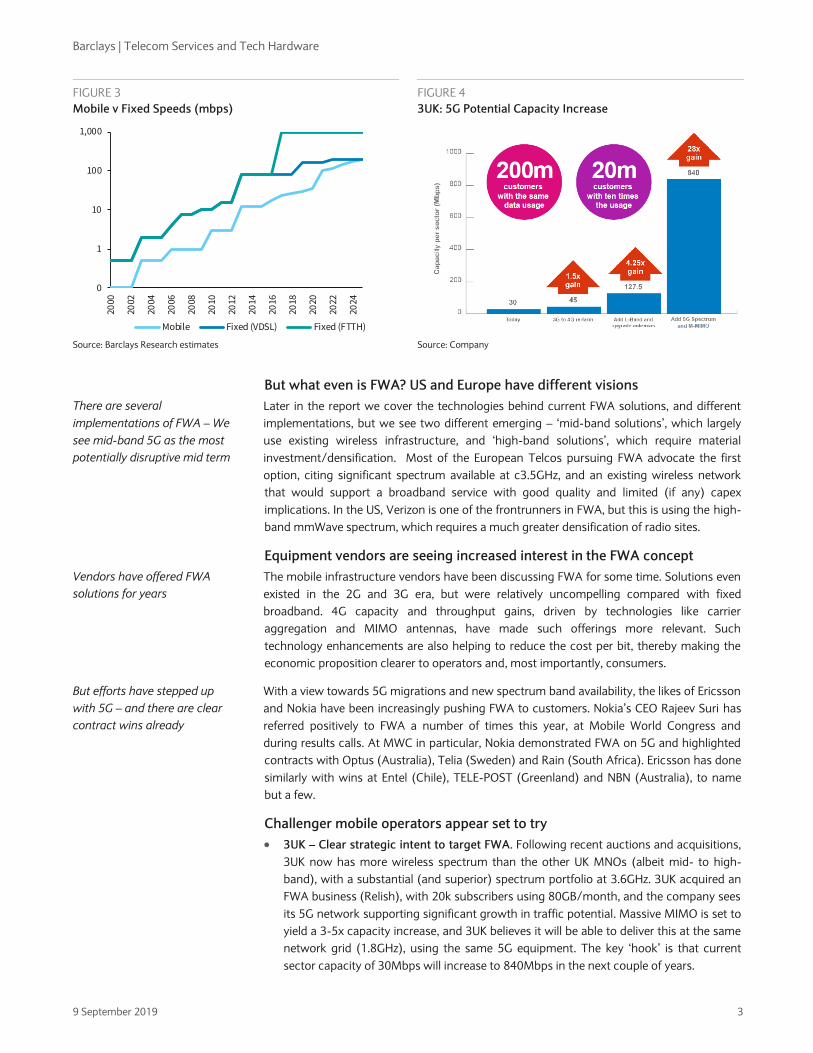

FIGURE 3

Mobile v Fixed Speeds (mbps)

FIGURE 4

3UK: 5G Potential Capacity Increase

Source: Barclays Research estimates Source: Company

But what even is FWA? US and Europe have different visions

Later in the report we cover the technologies behind current FWA solutions, and different

implementations, but we see two different emerging – ‘mid-band solutions’, which largely

use existing wireless infrastructure, and ‘high-band solutions’, which require material

investment/densification. Most of the European Telcos pursuing FWA advocate the first

option, citing significant spectrum available at c3.5GHz, and an existing wireless network

that would support a broadband service with good quality and limited (if any) capex

implications. In the US, Verizon is one of the frontrunners in FWA, but this is using the high-

band mmWave spectrum, which requires a much greater densification of radio sites.

Equipment vendors are seeing increased interest in the FWA concept

The mobile infrastructure vendors have been discussing FWA for some time. Solutions even

existed in the 2G and 3G era, but were relatively uncompelling compared with fixed

broadband. 4G capacity and throughput gains, driven by technologies like carrier

aggregation and MIMO antennas, have made such offerings more relevant. Such

technology enhancements are also helping to reduce the cost per bit, thereby making the

economic proposition clearer to operators and, most importantly, consumers.

With a view towards 5G migrations and new spectrum band availability, the likes of Ericsson

and Nokia have been increasingly pushing FWA to customers. Nokia’s CEO Rajeev Suri has

referred positively to FWA a number of times this year, at Mobile World Congress and

during results calls. At MWC in particular, Nokia demonstrated FWA on 5G and highlighted

contracts with Optus (Australia), Telia (Sweden) and Rain (South Africa). Ericsson has done

similarly with wins at Entel (Chile), TELE-POST (Greenland) and NBN (Australia), to name

but a few.

Challenger mobile operators appear set to try

3UK – Clear strategic intent to target FWA. Following recent auctions and acquisitions,

3UK now has more wireless spectrum than the other UK MNOs (albeit mid- to high-

band), with a substantial (and superior) spectrum portfolio at 3.6GHz. 3UK acquired an

FWA business (Relish), with 20k subscribers using 80GB/month, and the company sees

its 5G network supporting significant growth in traffic potential. Massive MIMO is set to

yield a 3-5x capacity increase, and 3UK believes it will be able to deliver this at the same

network grid (1.8GHz), using the same 5G equipment. The key ‘hook’ is that current

sector capacity of 30Mbps will increase to 840Mbps in the next couple of years.

0

1

10

100

1,000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

Mobile Fixed (VDSL) Fixed (FTTH)

There are several

implementations of FWA – We

see mid-band 5G as the most

potentially disruptive mid term

Vendors have offered FWA

solutions for years

But efforts have stepped up

with 5G – and there are clear

contract wins already

Barclays | Telecom Services and Tech Hardware

9 September 2019 4

TEF De – Successful FWA trial (link here). At its 2018 Capital Markets Day, TEF De

articulated how it was successfully creating a high-speed wireless network capable of

handling significant traffic growth, and indicated a strategic move to push into FWA.

Indeed, TEF De piloted a 5G FWA trial in Hamburg. The trial was supported by Samsung,

and operated at 26GHz, and TEF De sees itself being able to offer a faster broadband

connection for homes and small businesses than conventional DSL.

Sunrise – will use FWA to replace wholesaling copper and targets rural market share.

Sunrise has invested heavily in its network in recent years to catch up with Swisscom in

the Swiss market. Following the acquisition of 100MHz of 3.5GHz spectrum Sunrise now

sees an opportunity utilising 5G FWA to take broadband market share in rural areas. As

rural areas won’t have FTTH, FWA will offer a more attractive option for customers and

simultaneously generates better margins for Sunrise than wholesaling Swisscom’s

copper network. Sunrise sees FWA generating low-single-digit million EBITDA in 2020

which should double in 2021.

Verizon – using FWA to expand into new markets. Verizon began piloting 5G Home, its

FWA product, in four markets in late 2018. It will be launching its NR-based service this

year on the 28 and 39GHz mmWave bands. Notably, it intends to pass 30mm homes

with FWA and expand into new geographies beyond the ~14-15mm home Fios FTTH

footprint concentrated on the East Coast currently. Given fibre density and mmWave

deployment, this is likely to put incremental pressure on incumbent cable broadband

providers largely in urban areas.

T-Mobile/Sprint – a new entrant with a different flavour. TMUS/S have stated publicly

that they intend to provide FWA broadband on the combined network, with the goal of

reaching 90% population coverage and 9.5mm subs by 2024 (nearly as large as

ATUS+VZ combined today). Unlike VZ, new T-Mobile will likely leverage its mid-band

holdings particularly using the acquired Sprint 2.5GHz spectrum. This should enable

TMUS/S to be a more apt competitor in rural areas.

Even new entrants see an opportunity. Drillisch has successfully acquired 70Mhz

spectrum in the German 5G auction (2.1GHz and 3.4GHz), and plans to roll out a 5G

network in key urban areas, using national roaming across the rest of the network.

Much of the industrial logic and business case surrounds offering high-speed services

(both mobile-only and fixed-replacement), given that the combined wholesale

payments currently (fixed and mobile) are c€1.2bn/year, and United Internet currently

has significant Fibre backhaul capability. Rakuten in Japan has a similarly disruptive

approach – For more detail please refer to U.S. Cable, Media & Telecom: An Internet

company tests a new wireless architecture, March 2019.

Conference feedback – Many CTOs appear sceptical on ability to materially

disrupt

We hosted a CTO Conference in March 2019, which covered a number of key themes,

including the move to digital and cloud, how and when 5G will impact the Telecom

ecosystem, but also the potential impact of FWA on the industry. Key participants were the

CTOs or heads of networks of BT, Vodafone, Telenor, but also Samsung and Cellnex.

Vodafone – Believes FWA makes sense more in rural areas. Vodafone CTO Johan

Wibergh sees the key FWA issue being that the volume of fixed broadband data usage is

130GB/mth and growing 30/50pc per year vs current smartphones at 3GB. Although he

does see how FWA can be a way to use unused capacity in suburban areas, the key

question is how long this can continue because traffic increases a lot every year and

FWA uses a lot of capacity relative to ‘traditional’ wireless. For mmWave, Vodafone

believes FWA can add more capacity but the issue is densification of network. As such,

Other operators are more

sceptical (or realistic?)

Barclays | Telecom Services and Tech Hardware

9 September 2019 5

overall FWA could add a few percentage points of market share but not be

transformational. On backhaul, Vodafone has high penetration of FTTH links and also

microwave (works well and no issue with latency), and will continue to develop more

fibre in Spain/Germany so that it can fully integrate fixed/mobile networks.

BT – Doesn’t see FWA as likely to have major impact. BT CTO Howard Watson sees the

economics of wireless and fixed networks as very different, with traffic dynamics also

different (similar view to that of Vodafone). Mr Watson also stressed the relatively high

levels of mobile core network complexity vs fixed, which should be considered in any

planning. BT also sees FWA in mmWave as being quite niche – sub 5GHz is a different

prospect. Rather than focusing on one technology being better than the other for last

mile access, BT focuses on having ‘one smart network’. Indeed, BT sees a need and

significant opportunity to manage Fixed, mobile and WiFi together, with a focus on the

intelligence layer to manage a seamless customer journey in terms of connectivity. It

now has one IMS (had one for fixed, one for mobile).

Conclusion – Clearly a contentious subject

In this report we look at (a) whether 5G can deliver the kind of speed upgrades to facilitate

FWA, (b) how attractive the economics for wireless operators are, (c) which markets are

mostly likely to see FWA impact, and (d) examples of FWA deployments globally.

Barclays | Telecom Services and Tech Hardware

9 September 2019 6

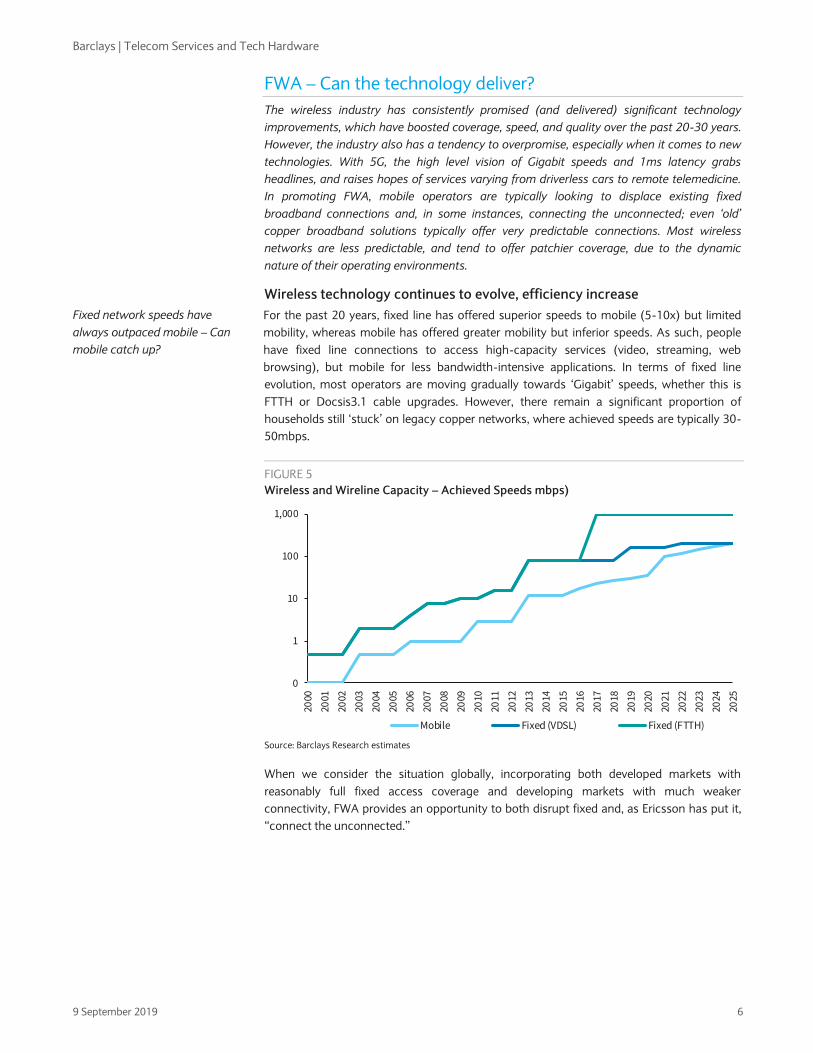

FWA – Can the technology deliver?

The wireless industry has consistently promised (and delivered) significant technology

improvements, which have boosted coverage, speed, and quality over the past 20-30 years.

However, the industry also has a tendency to overpromise, especially when it comes to new

technologies. With 5G, the high level vision of Gigabit speeds and 1ms latency grabs

headlines, and raises hopes of services varying from driverless cars to remote telemedicine.

In promoting FWA, mobile operators are typically looking to displace existing fixed

broadband connections and, in some instances, connecting the unconnected; even ‘old’

copper broadband solutions typically offer very predictable connections. Most wireless

networks are less predictable, and tend to offer patchier coverage, due to the dynamic

nature of their operating environments.

Wireless technology continues to evolve, efficiency increase

For the past 20 years, fixed line has offered superior speeds to mobile (5-10x) but limited

mobility, whereas mobile has offered greater mobility but inferior speeds. As such, people

have fixed line connections to access high-capacity services (video, streaming, web

browsing), but mobile for less bandwidth-intensive applications. In terms of fixed line

evolution, most operators are moving gradually towards ‘Gigabit’ speeds, whether this is

FTTH or Docsis3.1 cable upgrades. However, there remain a significant proportion of

households still ‘stuck’ on legacy copper networks, where achieved speeds are typically 30-

50mbps.

FIGURE 5

Wireless and Wireline Capacity – Achieved Speeds mbps)

Source: Barclays Research estimates

When we consider the situation globally, incorporating both developed markets with

reasonably full fixed access coverage and developing markets with much weaker

connectivity, FWA provides an opportunity to both disrupt fixed and, as Ericsson has put it,

“connect the unconnected.”

0

1

10

100

1,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Mobile Fixed (VDSL) Fixed (FTTH)

Fixed network speeds have

always outpaced mobile – Can

mobile catch up?

Barclays | Telecom Services and Tech Hardware

9 September 2019 7

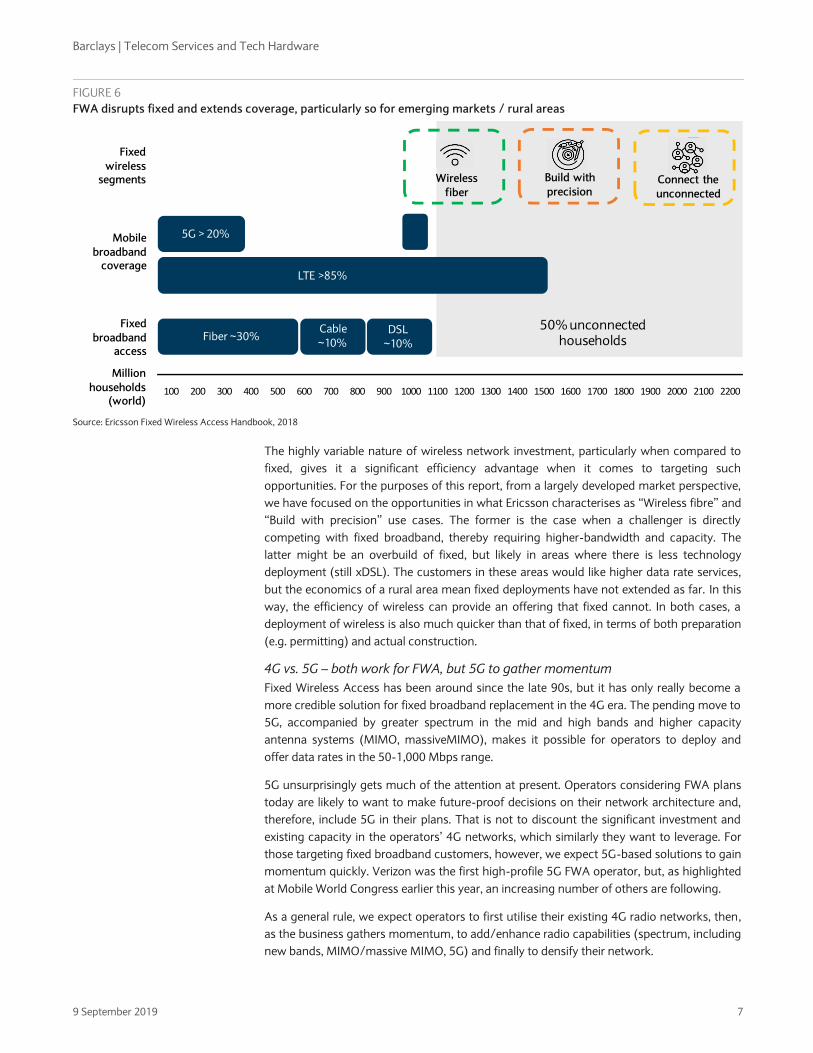

FIGURE 6

FWA disrupts fixed and extends coverage, particularly so for emerging markets / rural areas

Source: Ericsson Fixed Wireless Access Handbook, 2018

The highly variable nature of wireless network investment, particularly when compared to

fixed, gives it a significant efficiency advantage when it comes to targeting such

opportunities. For the purposes of this report, from a largely developed market perspective,

we have focused on the opportunities in what Ericsson characterises as “Wireless fibre” and

“Build with precision” use cases. The former is the case when a challenger is directly

competing with fixed broadband, thereby requiring higher-bandwidth and capacity. The

latter might be an overbuild of fixed, but likely in areas where there is less technology

deployment (still xDSL). The customers in these areas would like higher data rate services,

but the economics of a rural area mean fixed deployments have not extended as far. In this

way, the efficiency of wireless can provide an offering that fixed cannot. In both cases, a

deployment of wireless is also much quicker than that of fixed, in terms of both preparation

(e.g. permitting) and actual construction.

4G vs. 5G – both work for FWA, but 5G to gather momentum

Fixed Wireless Access has been around since the late 90s, but it has only really become a

more credible solution for fixed broadband replacement in the 4G era. The pending move to

5G, accompanied by greater spectrum in the mid and high bands and higher capacity

antenna systems (MIMO, massiveMIMO), makes it possible for operators to deploy and

offer data rates in the 50-1,000 Mbps range.

5G unsurprisingly gets much of the attention at present. Operators considering FWA plans

today are likely to want to make future-proof decisions on their network architecture and,

therefore, include 5G in their plans. That is not to discount the significant investment and

existing capacity in the operators’ 4G networks, which similarly they want to leverage. For

those targeting fixed broadband customers, however, we expect 5G-based solutions to gain

momentum quickly. Verizon was the first high-profile 5G FWA operator, but, as highlighted

at Mobile World Congress earlier this year, an increasing number of others are following.

As a general rule, we expect operators to first utilise their existing 4G radio networks, then,

as the business gathers momentum, to add/enhance radio capabilities (spectrum, including

new bands, MIMO/massive MIMO, 5G) and finally to densify their network.

Mobile

broadband coverage

Fixed

broadband access

LTE >85%

Fiber ~30%Cable

~10%DSL

~10%

5G > 20%

50% unconnected households

Fixed

wireless segments

Million

households (world)

Wireless

fiber

Build with

precisionConnect the

unconnected

100 200 300 400 500 600 700 800 900 1000 1100 1200 1300 1400 1500 1600 1700 1800 1900 2000 2100 2200

Barclays | Telecom Services and Tech Hardware

9 September 2019 8

FWA but one of the 5G use cases

While 4G network deployments have focused on mobile broadband deployments, in time,

5G is designed to take on a broader range of use cases, including Fixed Wireless Access as

well as enhanced Mobile Broadband (eMBB), Ultra Reliable Low Latency Communication

(URLLC) and massive Machine to Machine Communication (mMTC). These different use

cases each require a different type of deployment.

5G is also to be deployed in low-band (600MHz – 2GHz), mid-band (2-6GHz) and high-

band / mmWave (26GHz+) frequencies. Spectrum bands have long been a key determinant

of the network topology adopted by the service provider, given the lower signal propagation

at higher spectrum bands. With 5G, in particular, this is an even more acute issue given the

addition of mid-band and mmWave spectrum at much higher bands than previously

addressed. The higher bands naturally require a denser network grid.

Massive MIMO gives significant performance / coverage gains, but at a cost

One key element to be considered is the antenna system, in particular the adoption of high-

order multiple-in multiple-out (MIMO) antenna systems. Massive MIMO antenna systems,

such as 32T32R, 64T64R and up configurations, have the potential for significantly greater

capacity compared with lower-order legacy systems. The technology capabilities are very

compelling, but today such systems are expensive, large and heavy – driven by the

complexity and significant increase in semiconductor content to enable such performance.

These systems today rely heavily on programmable logic devices (PLDs), large chips that

can be reprogrammed with software.

The performance gains, therefore, need to be significant enough to justify such investment.

The vendors recommend massive MIMO systems to be deployed in the case of 5G

mmWave networks in dense high-rise urban environments; in such a network, massive

MIMO has a clear advantage over regular MIMO in terms of vertical coverage (64T64R 30-

degree vertical angle coverage as opposed to 16T16R with around 8-degree angular

coverage). This type of distinction speaks to Ericsson’s concept of “build with precision,” as

the spectrum band and type of environment (urban/suburban/rural) require more specific

build plans, more so than in a 4G world. Vendor feedback suggests that operators are very

much in the learning phase of such network planning, with large Tier 1s naturally earlier up

the curve.

In the case of mid-band spectrum, massive MIMO has been demonstrated to allow for a

3.5GHz network to mirror a 2GHz topology, thereby limiting the need to densify, at least at

the time of initial deployment. Outside of mmWave, vendors are selling massive MIMO for

both 4G and 5G, but it’s the economics that today limit deployments. Massive MIMO may

be necessary in mmWave, but is merely beneficial in low and mid band and therefore the

high cost of such solutions means deployments are likely to be more limited until we see

system simplification/maturation (i.e. FPGA to ASIC on the chip front) and the

corresponding price declines. In rural areas, in particular, where capacity is of less concern,

lower-order 2T2R and 4T4R MIMO antenna systems work very effectively and at much

lower expense.

Another key factor for an operator is not just the cost of the massive MIMO antenna but

also the size and weight, as this has a direct impact on the site construction. For mmWave,

by the nature of a lower amplitude (the height of the radio wave), the transceiver/receivers

can be significantly smaller than for low band, where the radio wave amplitude is much

greater. A massive MIMO antenna for deployment at <1GHz is today very large and heavy.

Europe vs US – Europe offers significant spectrum at 3.4GHz (available now)

In its June 2016 report, Ofcom sees >2,000MHz of additional potential spectrum becoming

available of the next 10+ years, compared to ca700MHz at present – a 3-4x increase. Ofcom

Massive MIMO offers higher

speeds – but implementation

not trivial

Complexity and cost of

implementation implies MNO

deployment will be measured –

We estimate 5-10% of radio

sites in next couple of years

Massive MIMO coverage

characteristics in 3.5GHz band

are helpfully similar to 2GHz

topologies

There are practical issues to

consider

Barclays | Telecom Services and Tech Hardware

9 September 2019 9

sees 700MHz as a priority, along with 1.4GHz, 2.3GHz, 3.4GHz, 3.6-3.8GHz, and 5.7-

5.85GHz as a key priority at the low to mid range of frequencies, but also potential

significant amounts at 24.5-27.5GHz or 31.8-33.4GHz. The increase in lower-frequency

band spectrum (124MHz at <3GHz) will not in itself facilitate large capacity increases – it is

to an extent the 3-6GHz, but most likely 26GHz+ (termed mmWave) that will help facilitate

much higher speeds, with the higher-frequency ranges used primarily for front and

backhaul initially.

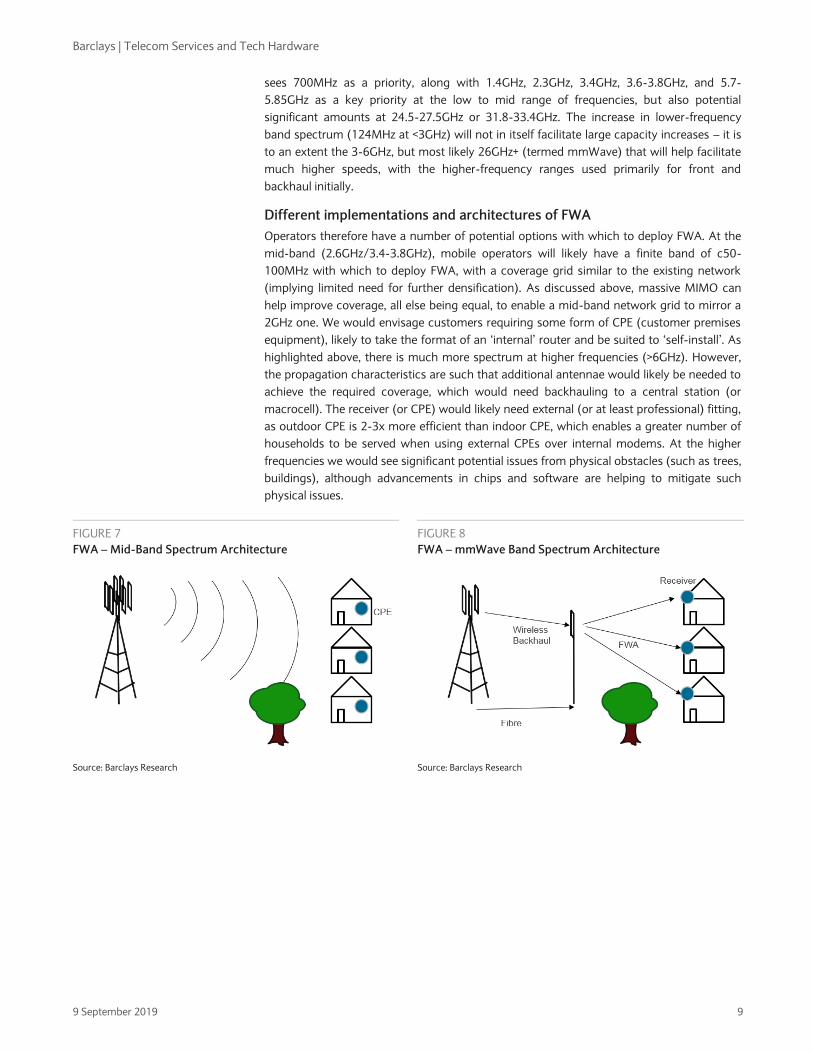

Different implementations and architectures of FWA

Operators therefore have a number of potential options with which to deploy FWA. At the

mid-band (2.6GHz/3.4-3.8GHz), mobile operators will likely have a finite band of c50-

100MHz with which to deploy FWA, with a coverage grid similar to the existing network

(implying limited need for further densification). As discussed above, massive MIMO can

help improve coverage, all else being equal, to enable a mid-band network grid to mirror a

2GHz one. We would envisage customers requiring some form of CPE (customer premises

equipment), likely to take the format of an ‘internal’ router and be suited to ‘self-install’. As

highlighted above, there is much more spectrum at higher frequencies (>6GHz). However,

the propagation characteristics are such that additional antennae would likely be needed to

achieve the required coverage, which would need backhauling to a central station (or

macrocell). The receiver (or CPE) would likely need external (or at least professional) fitting,

as outdoor CPE is 2-3x more efficient than indoor CPE, which enables a greater number of

households to be served when using external CPEs over internal modems. At the higher

frequencies we would see significant potential issues from physical obstacles (such as trees,

buildings), although advancements in chips and software are helping to mitigate such

physical issues.

FIGURE 7

FWA – Mid-Band Spectrum Architecture

FIGURE 8

FWA – mmWave Band Spectrum Architecture

Source: Barclays Research Source: Barclays Research

Barclays | Telecom Services and Tech Hardware

9 September 2019 10

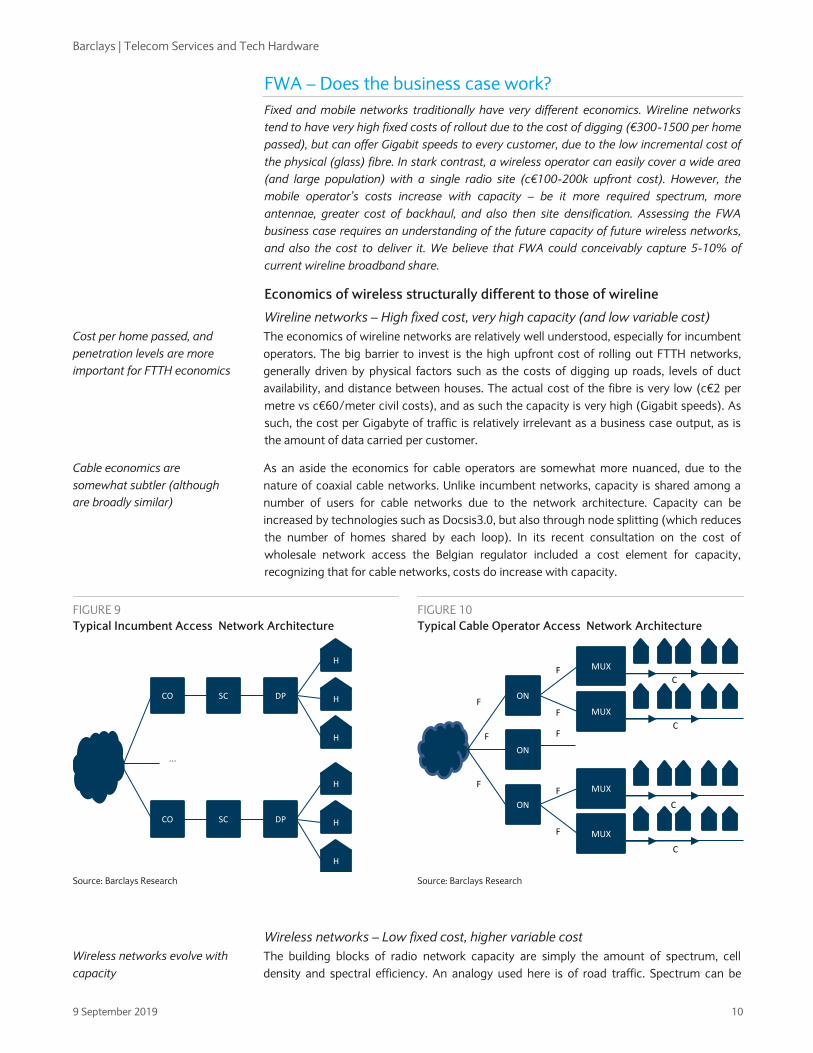

FWA – Does the business case work?

Fixed and mobile networks traditionally have very different economics. Wireline networks

tend to have very high fixed costs of rollout due to the cost of digging (€300-1500 per home

passed), but can offer Gigabit speeds to every customer, due to the low incremental cost of

the physical (glass) fibre. In stark contrast, a wireless operator can easily cover a wide area

(and large population) with a single radio site (c€100-200k upfront cost). However, the

mobile operator’s costs increase with capacity – be it more required spectrum, more

antennae, greater cost of backhaul, and also then site densification. Assessing the FWA

business case requires an understanding of the future capacity of future wireless networks,

and also the cost to deliver it. We believe that FWA could conceivably capture 5-10% of

current wireline broadband share.

Economics of wireless structurally different to those of wireline

Wireline networks – High fixed cost, very high capacity (and low variable cost)

The economics of wireline networks are relatively well understood, especially for incumbent

operators. The big barrier to invest is the high upfront cost of rolling out FTTH networks,

generally driven by physical factors such as the costs of digging up roads, levels of duct

availability, and distance between houses. The actual cost of the fibre is very low (c€2 per

metre vs c€60/meter civil costs), and as such the capacity is very high (Gigabit speeds). As

such, the cost per Gigabyte of traffic is relatively irrelevant as a business case output, as is

the amount of data carried per customer.

As an aside the economics for cable operators are somewhat more nuanced, due to the

nature of coaxial cable networks. Unlike incumbent networks, capacity is shared among a

number of users for cable networks due to the network architecture. Capacity can be

increased by technologies such as Docsis3.0, but also through node splitting (which reduces

the number of homes shared by each loop). In its recent consultation on the cost of

wholesale network access the Belgian regulator included a cost element for capacity,

recognizing that for cable networks, costs do increase with capacity.

FIGURE 9

Typical Incumbent Access Network Architecture

FIGURE 10

Typical Cable Operator Access Network Architecture

Source: Barclays Research Source: Barclays Research

Wireless networks – Low fixed cost, higher variable cost

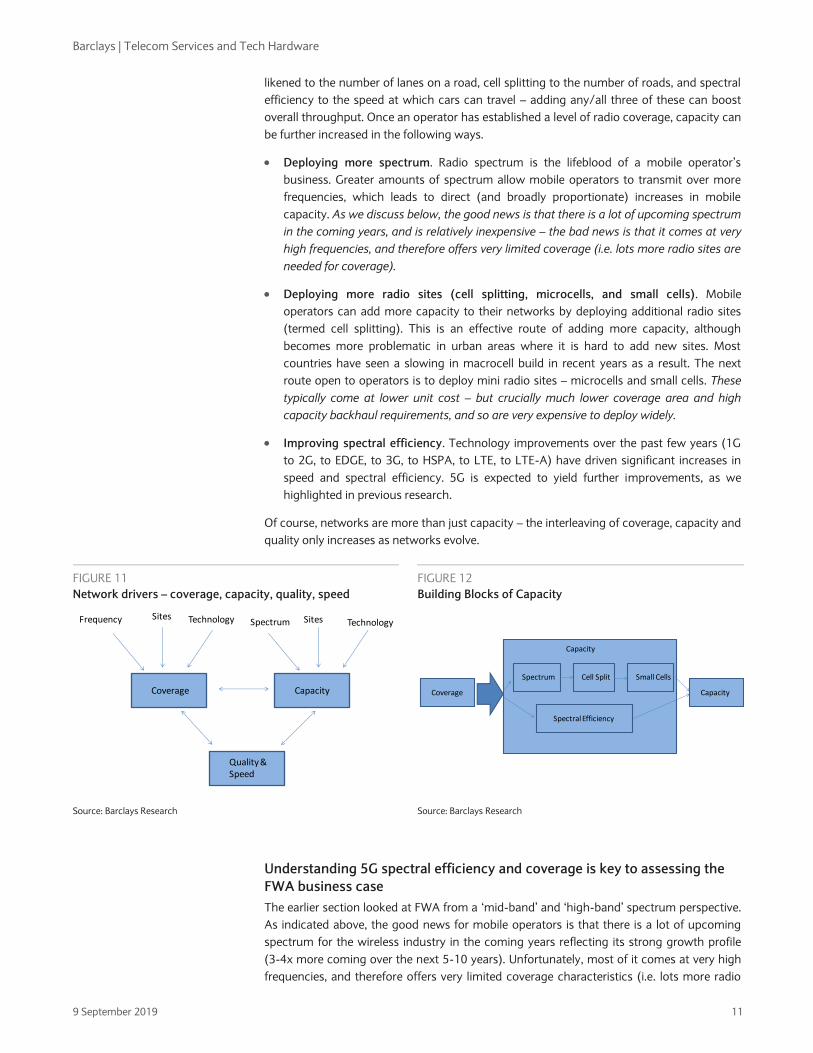

The building blocks of radio network capacity are simply the amount of spectrum, cell

density and spectral efficiency. An analogy used here is of road traffic. Spectrum can be

DPSC H

H

H

CO

DPSC H

H

H

CO

...

MUX

MUX

ON

MUX

MUX

ON

ON

F

F

FF

F

F

F

F

C

C

C

C

Cost per home passed, and

penetration levels are more

important for FTTH economics

Cable economics are

somewhat subtler (although

are broadly similar)

Wireless networks evolve with

capacity

Barclays | Telecom Services and Tech Hardware

9 September 2019 11

likened to the number of lanes on a road, cell splitting to the number of roads, and spectral

efficiency to the speed at which cars can travel – adding any/all three of these can boost

overall throughput. Once an operator has established a level of radio coverage, capacity can

be further increased in the following ways.

Deploying more spectrum. Radio spectrum is the lifeblood of a mobile operator’s

business. Greater amounts of spectrum allow mobile operators to transmit over more

frequencies, which leads to direct (and broadly proportionate) increases in mobile

capacity. As we discuss below, the good news is that there is a lot of upcoming spectrum

in the coming years, and is relatively inexpensive – the bad news is that it comes at very

high frequencies, and therefore offers very limited coverage (i.e. lots more radio sites are

needed for coverage).

Deploying more radio sites (cell splitting, microcells, and small cells). Mobile

operators can add more capacity to their networks by deploying additional radio sites

(termed cell splitting). This is an effective route of adding more capacity, although

becomes more problematic in urban areas where it is hard to add new sites. Most

countries have seen a slowing in macrocell build in recent years as a result. The next

route open to operators is to deploy mini radio sites – microcells and small cells. These

typically come at lower unit cost – but crucially much lower coverage area and high

capacity backhaul requirements, and so are very expensive to deploy widely.

Improving spectral efficiency. Technology improvements over the past few years (1G

to 2G, to EDGE, to 3G, to HSPA, to LTE, to LTE-A) have driven significant increases in

speed and spectral efficiency. 5G is expected to yield further improvements, as we

highlighted in previous research.

Of course, networks are more than just capacity – the interleaving of coverage, capacity and

quality only increases as networks evolve.

FIGURE 11

Network drivers – coverage, capacity, quality, speed

FIGURE 12

Building Blocks of Capacity

Source: Barclays Research Source: Barclays Research

Understanding 5G spectral efficiency and coverage is key to assessing the

FWA business case

The earlier section looked at FWA from a ‘mid-band’ and ‘high-band’ spectrum perspective.

As indicated above, the good news for mobile operators is that there is a lot of upcoming

spectrum for the wireless industry in the coming years reflecting its strong growth profile

(3-4x more coming over the next 5-10 years). Unfortunately, most of it comes at very high

frequencies, and therefore offers very limited coverage characteristics (i.e. lots more radio

Coverage Capacity

Quality & Speed

Frequency Sites Technology Spectrum Sites Technology

Coverage

Spectrum Cell Split

Spectral Efficiency

Capacity

Small Cells

Capacity

Barclays | Telecom Services and Tech Hardware

9 September 2019 12

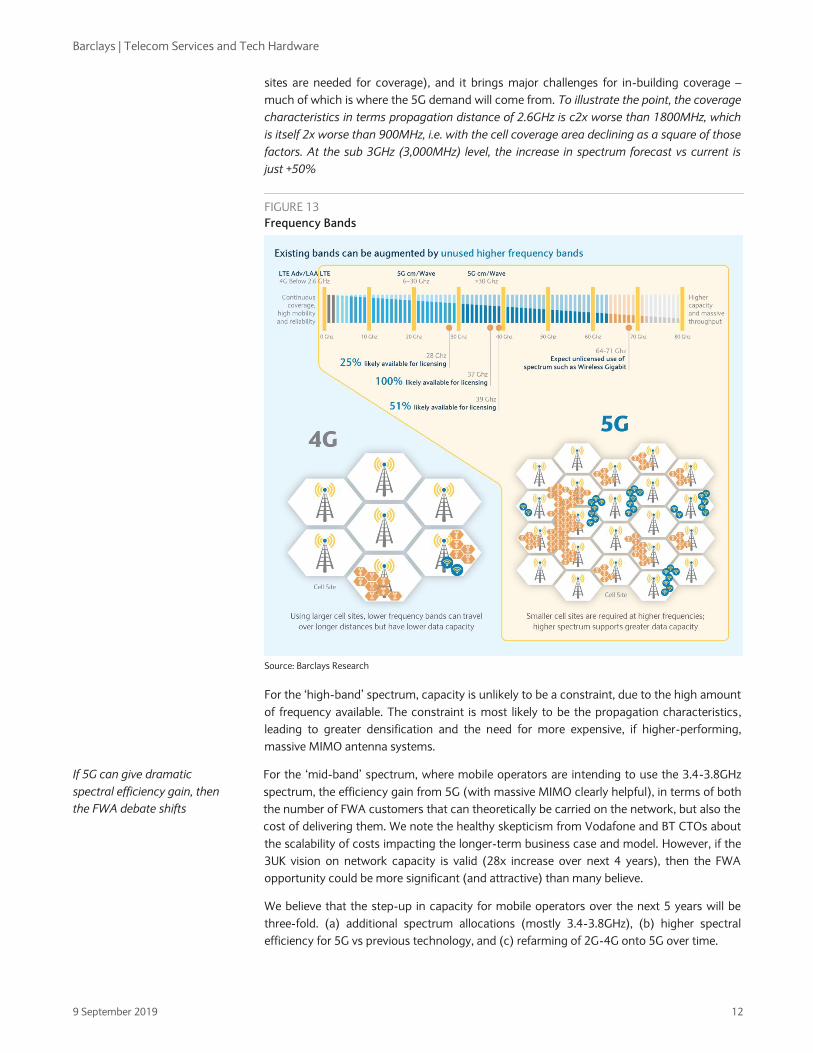

sites are needed for coverage), and it brings major challenges for in-building coverage –

much of which is where the 5G demand will come from. To illustrate the point, the coverage

characteristics in terms propagation distance of 2.6GHz is c2x worse than 1800MHz, which

is itself 2x worse than 900MHz, i.e. with the cell coverage area declining as a square of those

factors. At the sub 3GHz (3,000MHz) level, the increase in spectrum forecast vs current is

just +50%

FIGURE 13

Frequency Bands

Source: Barclays Research

For the ‘high-band’ spectrum, capacity is unlikely to be a constraint, due to the high amount

of frequency available. The constraint is most likely to be the propagation characteristics,

leading to greater densification and the need for more expensive, if higher-performing,

massive MIMO antenna systems.

For the ‘mid-band’ spectrum, where mobile operators are intending to use the 3.4-3.8GHz

spectrum, the efficiency gain from 5G (with massive MIMO clearly helpful), in terms of both

the number of FWA customers that can theoretically be carried on the network, but also the

cost of delivering them. We note the healthy skepticism from Vodafone and BT CTOs about

the scalability of costs impacting the longer-term business case and model. However, if the

3UK vision on network capacity is valid (28x increase over next 4 years), then the FWA

opportunity could be more significant (and attractive) than many believe.

We believe that the step-up in capacity for mobile operators over the next 5 years will be

three-fold. (a) additional spectrum allocations (mostly 3.4-3.8GHz), (b) higher spectral

efficiency for 5G vs previous technology, and (c) refarming of 2G-4G onto 5G over time.

If 5G can give dramatic

spectral efficiency gain, then

the FWA debate shifts

Barclays | Telecom Services and Tech Hardware

9 September 2019 13

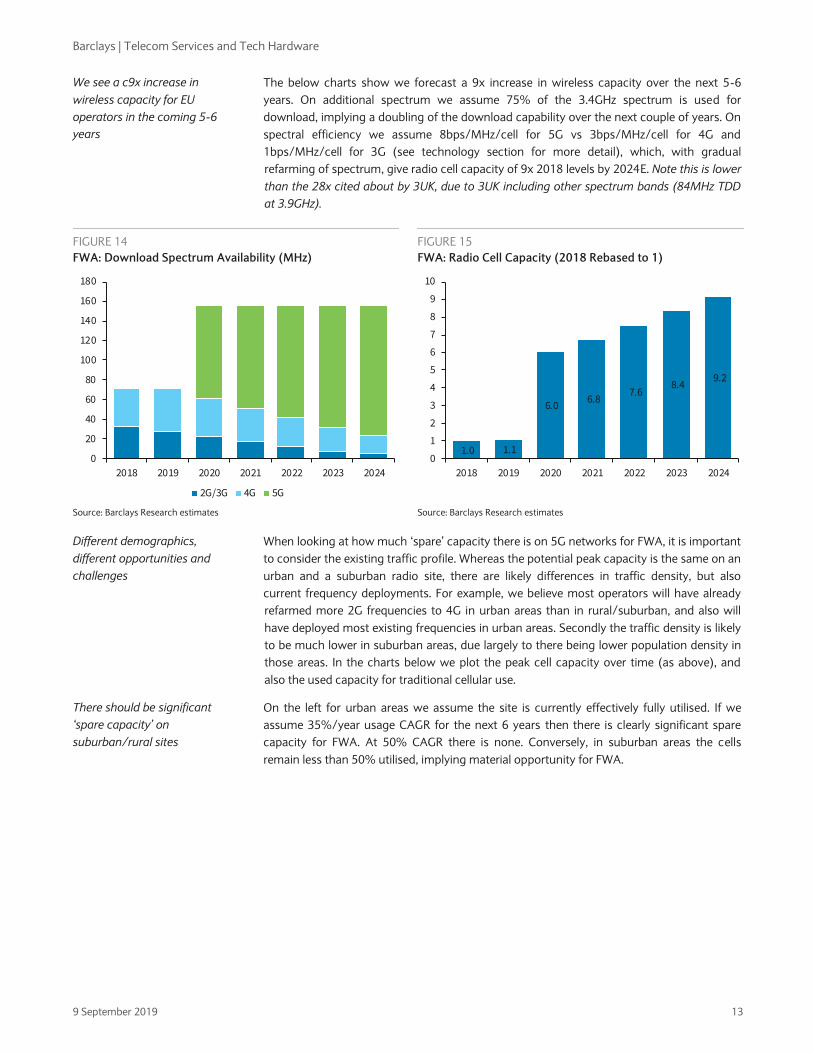

The below charts show we forecast a 9x increase in wireless capacity over the next 5-6

years. On additional spectrum we assume 75% of the 3.4GHz spectrum is used for

download, implying a doubling of the download capability over the next couple of years. On

spectral efficiency we assume 8bps/MHz/cell for 5G vs 3bps/MHz/cell for 4G and

1bps/MHz/cell for 3G (see technology section for more detail), which, with gradual

refarming of spectrum, give radio cell capacity of 9x 2018 levels by 2024E. Note this is lower

than the 28x cited about by 3UK, due to 3UK including other spectrum bands (84MHz TDD

at 3.9GHz).

FIGURE 14

FWA: Download Spectrum Availability (MHz)

FIGURE 15

FWA: Radio Cell Capacity (2018 Rebased to 1)

Source: Barclays Research estimates Source: Barclays Research estimates

When looking at how much ‘spare’ capacity there is on 5G networks for FWA, it is important

to consider the existing traffic profile. Whereas the potential peak capacity is the same on an

urban and a suburban radio site, there are likely differences in traffic density, but also

current frequency deployments. For example, we believe most operators will have already

refarmed more 2G frequencies to 4G in urban areas than in rural/suburban, and also will

have deployed most existing frequencies in urban areas. Secondly the traffic density is likely

to be much lower in suburban areas, due largely to there being lower population density in

those areas. In the charts below we plot the peak cell capacity over time (as above), and

also the used capacity for traditional cellular use.

On the left for urban areas we assume the site is currently effectively fully utilised. If we

assume 35%/year usage CAGR for the next 6 years then there is clearly significant spare

capacity for FWA. At 50% CAGR there is none. Conversely, in suburban areas the cells

remain less than 50% utilised, implying material opportunity for FWA.

0

20

40

60

80

100

120

140

160

180

2018 2019 2020 2021 2022 2023 2024

2G/3G 4G 5G

1.0 1.1

6.0 6.8

7.6 8.4

9.2

0

1

2

3

4

5

6

7

8

9

10

2018 2019 2020 2021 2022 2023 2024

We see a c9x increase in

wireless capacity for EU

operators in the coming 5-6

years

Different demographics,

different opportunities and

challenges

There should be significant

‘spare capacity’ on

suburban/rural sites

Barclays | Telecom Services and Tech Hardware

9 September 2019 14

FIGURE 16

FWA: Urban Site: Capacity and Cellular Usage (2018 = 1)

FIGURE 17

FWA: Suburban Site: Capacity and Cellular Usage (2018 = 1)

Source: Barclays Research estimates Source: Barclays Research estimates

Our proprietary cost model indicates significant FWA potential (but not

without sensitivities)

Understanding costs of current FWA (and fibre) solutions

Before jumping into mobile costs of broadband, we consider how much fixed operators are

spending on FTTH. From a fibre perspective, we assume capex of €750/home passed, plus

€300 for CPE/vertical). Assuming 30% take-up, this implies capex of €2,800 per home

connected. For a 60% take-up, the upfront capex is €1,550/home connected – i.e. very high.

Most of the cost is upfront – ongoing costs are likely to be much smaller, and include duct

maintenance and leases, along with general central/backhaul costs.

There are existing FWA players, as we describe elsewhere in the report. The economics for

such ‘traditional’ FWA operators (i.e. not mobile operators) are much different. The upfront

cost is typically a radio mast, with associated backhaul (and power). For example, for a

larger FWA site we estimate a c€40k upfront capex spend, with €10k/year for backhaul and

power/rental, giving an implied €13k/year annual cost (spreading the upfront cost over 15

years). Existing FWA providers that operate in higher frequency bands typically have a

relatively low site utilisation when compared to mobile operators. Assuming a load of 20

customers per mast gives an annual cost of €63/sub/year, or €103/sub/year including CPE

(€200 cost amortised over 5 years). There are also significant scale economies with

‘clusters’ of FWA sites. The first site will likely require a large mast with (relatively expensive)

fibre backhaul capabilities. However, FWA providers can deploy FWA ‘spokes’ from the main

mast to target more homes, with the smaller antennae being lower capital employed. We

believe TowerCos can play a role here to facilitate a densification of FWA providers,

especially in surburban/rural areas.

We note that in the UK market there are a number of government grants that can lower the

upfront costs (up to £1,500/line for 1GBPS speed connections). In the UK, Big Blu

Broadband estimates a £42/month ARPU, with c40% gross margins, implying payback

periods being <24months.

0

2

4

6

8

10

2018 2019 2020 2021 2022 2023 2024

Capacity Cellular Traffic - Scenario 1

Cellular Traffic - Scenario 2

0

2

4

6

8

10

2018 2019 2020 2021 2022 2023 2024

Capacity Cellular Traffic - Scenario 1

Cellular Traffic - Scenario 2

FTTH upfront investments are

material – penetration rates

are key

Existing FWA solutions have

much lower upfront

investment, with attractive

paybacks

Government subsidies to play

for

Barclays | Telecom Services and Tech Hardware

9 September 2019 15

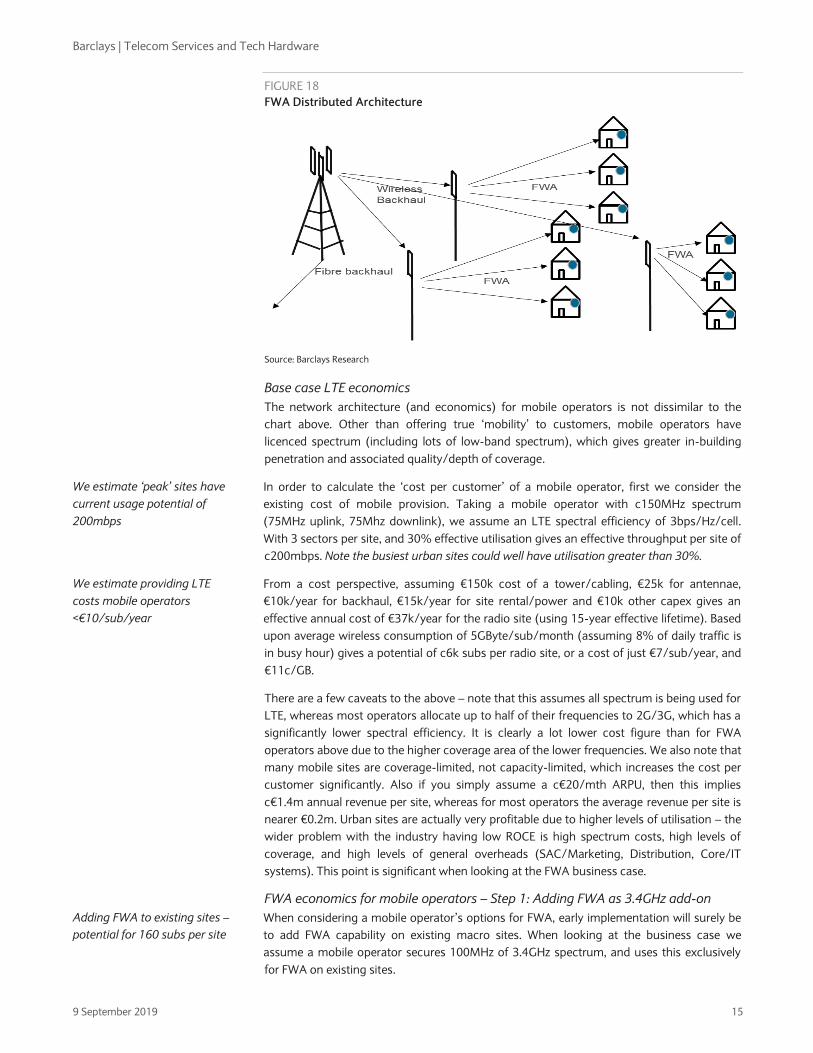

FIGURE 18

FWA Distributed Architecture

Source: Barclays Research

Base case LTE economics

The network architecture (and economics) for mobile operators is not dissimilar to the

chart above. Other than offering true ‘mobility’ to customers, mobile operators have

licenced spectrum (including lots of low-band spectrum), which gives greater in-building

penetration and associated quality/depth of coverage.

In order to calculate the ‘cost per customer’ of a mobile operator, first we consider the

existing cost of mobile provision. Taking a mobile operator with c150MHz spectrum

(75MHz uplink, 75Mhz downlink), we assume an LTE spectral efficiency of 3bps/Hz/cell.

With 3 sectors per site, and 30% effective utilisation gives an effective throughput per site of

c200mbps. Note the busiest urban sites could well have utilisation greater than 30%.

From a cost perspective, assuming €150k cost of a tower/cabling, €25k for antennae,

€10k/year for backhaul, €15k/year for site rental/power and €10k other capex gives an

effective annual cost of €37k/year for the radio site (using 15-year effective lifetime). Based

upon average wireless consumption of 5GByte/sub/month (assuming 8% of daily traffic is

in busy hour) gives a potential of c6k subs per radio site, or a cost of just €7/sub/year, and

€11c/GB.

There are a few caveats to the above – note that this assumes all spectrum is being used for

LTE, whereas most operators allocate up to half of their frequencies to 2G/3G, which has a

significantly lower spectral efficiency. It is clearly a lot lower cost figure than for FWA

operators above due to the higher coverage area of the lower frequencies. We also note that

many mobile sites are coverage-limited, not capacity-limited, which increases the cost per

customer significantly. Also if you simply assume a c€20/mth ARPU, then this implies

c€1.4m annual revenue per site, whereas for most operators the average revenue per site is

nearer €0.2m. Urban sites are actually very profitable due to higher levels of utilisation – the

wider problem with the industry having low ROCE is high spectrum costs, high levels of

coverage, and high levels of general overheads (SAC/Marketing, Distribution, Core/IT

systems). This point is significant when looking at the FWA business case.

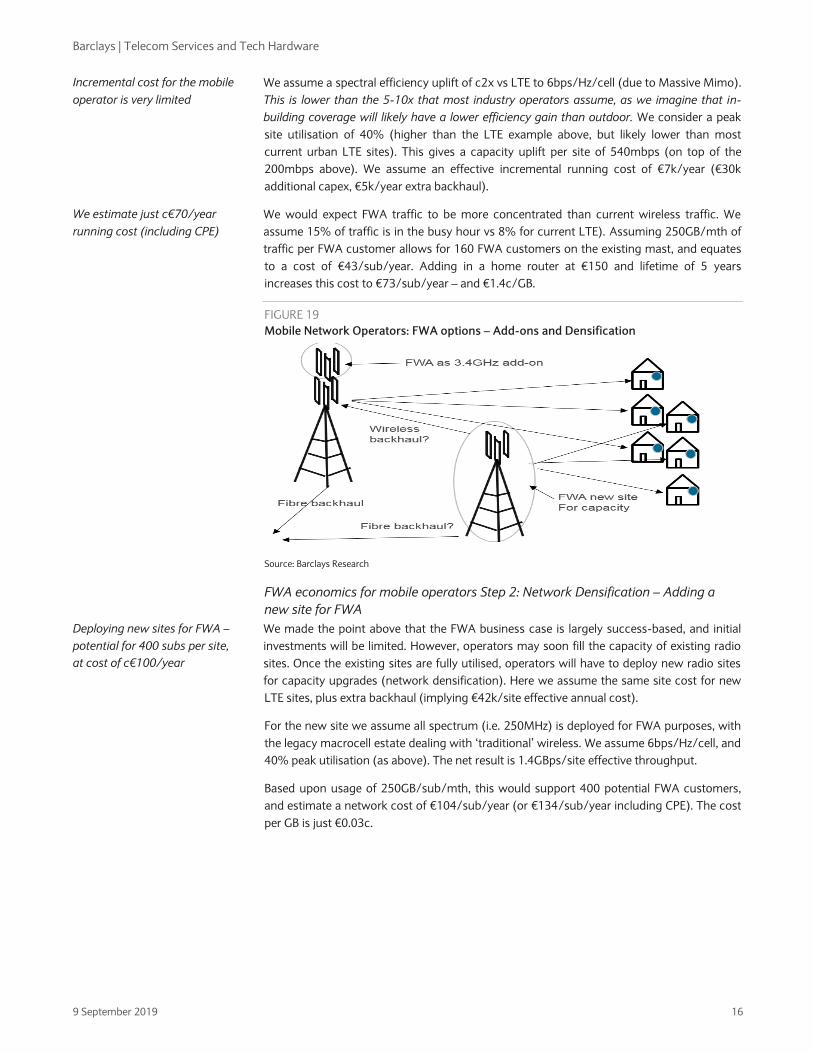

FWA economics for mobile operators – Step 1: Adding FWA as 3.4GHz add-on

When considering a mobile operator’s options for FWA, early implementation will surely be

to add FWA capability on existing macro sites. When looking at the business case we

assume a mobile operator secures 100MHz of 3.4GHz spectrum, and uses this exclusively

for FWA on existing sites.

We estimate ‘peak’ sites have

current usage potential of

200mbps

We estimate providing LTE

costs mobile operators

<€10/sub/year

Adding FWA to existing sites –

potential for 160 subs per site

Barclays | Telecom Services and Tech Hardware

9 September 2019 16

We assume a spectral efficiency uplift of c2x vs LTE to 6bps/Hz/cell (due to Massive Mimo).

This is lower than the 5-10x that most industry operators assume, as we imagine that in-

building coverage will likely have a lower efficiency gain than outdoor. We consider a peak

site utilisation of 40% (higher than the LTE example above, but likely lower than most

current urban LTE sites). This gives a capacity uplift per site of 540mbps (on top of the

200mbps above). We assume an effective incremental running cost of €7k/year (€30k

additional capex, €5k/year extra backhaul).

We would expect FWA traffic to be more concentrated than current wireless traffic. We

assume 15% of traffic is in the busy hour vs 8% for current LTE). Assuming 250GB/mth of

traffic per FWA customer allows for 160 FWA customers on the existing mast, and equates

to a cost of €43/sub/year. Adding in a home router at €150 and lifetime of 5 years

increases this cost to €73/sub/year – and €1.4c/GB.

FIGURE 19

Mobile Network Operators: FWA options – Add-ons and Densification

Source: Barclays Research

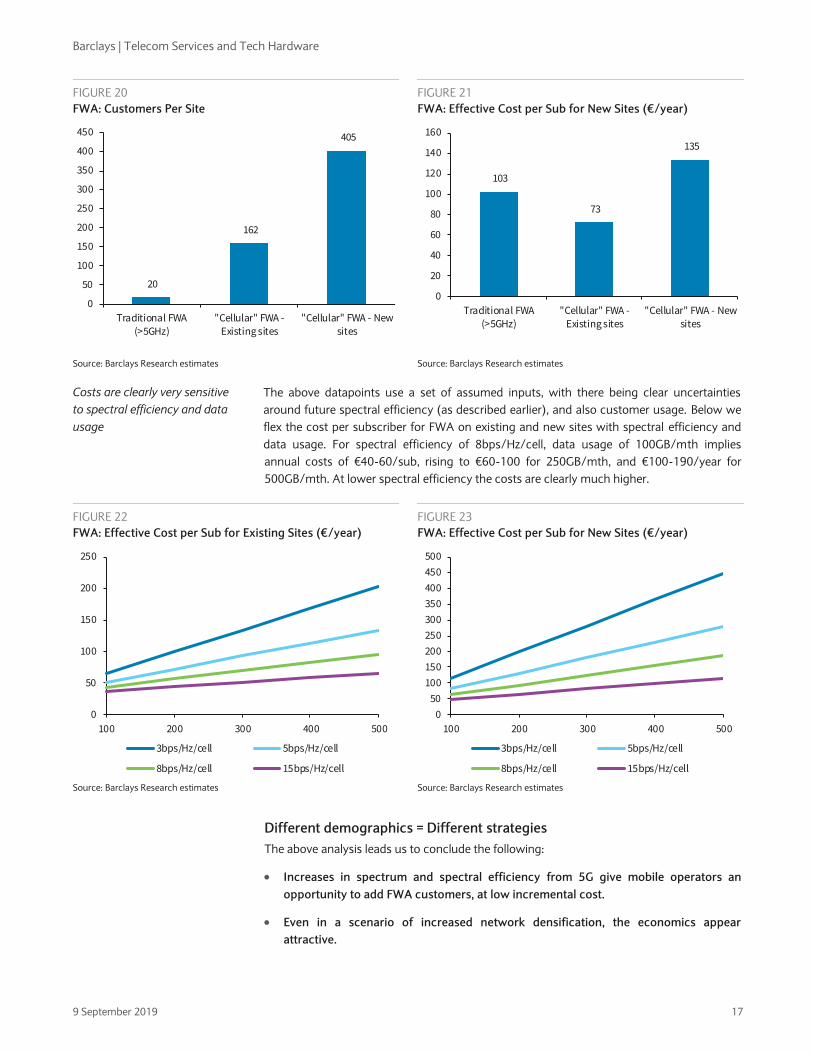

FWA economics for mobile operators Step 2: Network Densification – Adding a

new site for FWA

We made the point above that the FWA business case is largely success-based, and initial

investments will be limited. However, operators may soon fill the capacity of existing radio

sites. Once the existing sites are fully utilised, operators will have to deploy new radio sites

for capacity upgrades (network densification). Here we assume the same site cost for new

LTE sites, plus extra backhaul (implying €42k/site effective annual cost).

For the new site we assume all spectrum (i.e. 250MHz) is deployed for FWA purposes, with

the legacy macrocell estate dealing with ‘traditional’ wireless. We assume 6bps/Hz/cell, and

40% peak utilisation (as above). The net result is 1.4GBps/site effective throughput.

Based upon usage of 250GB/sub/mth, this would support 400 potential FWA customers,

and estimate a network cost of €104/sub/year (or €134/sub/year including CPE). The cost

per GB is just €0.03c.

Incremental cost for the mobile

operator is very limited

We estimate just c€70/year

running cost (including CPE)

Deploying new sites for FWA –

potential for 400 subs per site,

at cost of c€100/year

Barclays | Telecom Services and Tech Hardware

9 September 2019 17

FIGURE 20

FWA: Customers Per Site

FIGURE 21

FWA: Effective Cost per Sub for New Sites (€/year)

Source: Barclays Research estimates Source: Barclays Research estimates

The above datapoints use a set of assumed inputs, with there being clear uncertainties

around future spectral efficiency (as described earlier), and also customer usage. Below we

flex the cost per subscriber for FWA on existing and new sites with spectral efficiency and

data usage. For spectral efficiency of 8bps/Hz/cell, data usage of 100GB/mth implies

annual costs of €40-60/sub, rising to €60-100 for 250GB/mth, and €100-190/year for

500GB/mth. At lower spectral efficiency the costs are clearly much higher.

FIGURE 22

FWA: Effective Cost per Sub for Existing Sites (€/year)

FIGURE 23

FWA: Effective Cost per Sub for New Sites (€/year)

Source: Barclays Research estimates Source: Barclays Research estimates

Different demographics = Different strategies

The above analysis leads us to conclude the following:

Increases in spectrum and spectral efficiency from 5G give mobile operators an

opportunity to add FWA customers, at low incremental cost.

Even in a scenario of increased network densification, the economics appear

attractive.

20

162

405

0

50

100

150

200

250

300

350

400

450

Traditional FWA(>5GHz)

"Cellular" FWA -Existing sites

"Cellular" FWA - Newsites

103

73

135

0

20

40

60

80

100

120

140

160

Traditional FWA(>5GHz)

"Cellular" FWA -Existing sites

"Cellular" FWA - Newsites

0

50

100

150

200

250

100 200 300 400 500

3bps/Hz/cell 5bps/Hz/cell

8bps/Hz/cell 15bps/Hz/cell

0

50

100

150

200

250

300

350

400

450

500

100 200 300 400 500

3bps/Hz/cell 5bps/Hz/cell

8bps/Hz/cell 15bps/Hz/cell

Costs are clearly very sensitive

to spectral efficiency and data

usage

Barclays | Telecom Services and Tech Hardware

9 September 2019 18

There are significant sensitivities surrounding the FWA business case – incorrect

assumptions on usage and technology efficiency could result in much higher cost per

customer, and also potentially negatively impact the network quality for all users.

We would therefore expect mobile operators to deploy different strategies in different

segments.

Urban – Offer niche ‘capped’ offerings. Mobile operators typically have very good levels

of radio coverage in urban areas (even if in-building coverage can sometimes be a

challenge in some areas), but the key issue facing mobile operators tends to be capacity.

Indeed, most congestion points in mobile operator networks are in urban areas due to

high levels of population density. We do see an opportunity for mobile operators using

FWA for targeting more ‘nomadic’ customer groups (visitors, renters, young

professionals), but given overall network capacity constraints (and risks highlighted

above), we would anticipate mobile operators taking a somewhat conservative view

here.

Suburban – Utilise significant spare capacity. Our analysis (see later in report) points to

operators having significant amounts of spectrum not currently being used on

suburban/rural sites, implying low levels of congestion, and significant spare capacity.

As much as 50% of frequencies in such areas are not being used for LTE/4G currently,

and so we believe the entire 3.4-3.8GHz frequency range (and maybe also some of the

2.1/2.6GHz spectrum) could be used for FWA. Furthermore, the rise of independent

tower companies (such as Cellnex), and the desire of the industry to increase network

sharing is leading to significant numbers of new sites being available to improve

network densification and promote greater FWA penetration.

Rural – Deploy in areas where existing infrastructure supportive and/or investment

requirements are low. Fixed broadband speeds are typically much lower in rural areas

(see later in report), and we anticipate incumbents will only build FTTH in rural once

they have built urban and suburban (if at all). As such, we see mobile operators as well

placed to target the rural segment with FWA, but only where they have good coverage.

We note that wireless coverage is also quite patchy in rural areas – Ofcom estimates

23% of homes do not have good indoor 4G coverage.

Given all the above, we see it as highly likely that mobile-centric operators with little to lose

will target the fixed broadband market. After all, the upfront costs are very low, and any

additional capex is clearly success-based. It is also a highly defensive move for mobile-

centric operators to insulate themselves against convergence. As the analysis also above

indicates, FWA can be a precursor to actually rolling our fibre in more suburban/rural areas,

which in our view creates strategic optionality. In terms of its relevance as a product, we see

the more copper-rich markets offering greater penetration potential.

We expect incumbents to use FWA as an alternative to last-mile access in more rural

communities. As an example, Telenor is promoting an FWA solution (based upon 4G/LTE)

in rural areas to replace copper lines as part of its strategy for copper switch-off, and has 2k

customers already on its service (which is geo-locked to prevent mobility).

Strategy for mobile-centric

operators? It’s worth giving it a

try

Incumbents will likely target

FWA as rural niche offering

Barclays | Telecom Services and Tech Hardware

9 September 2019 19

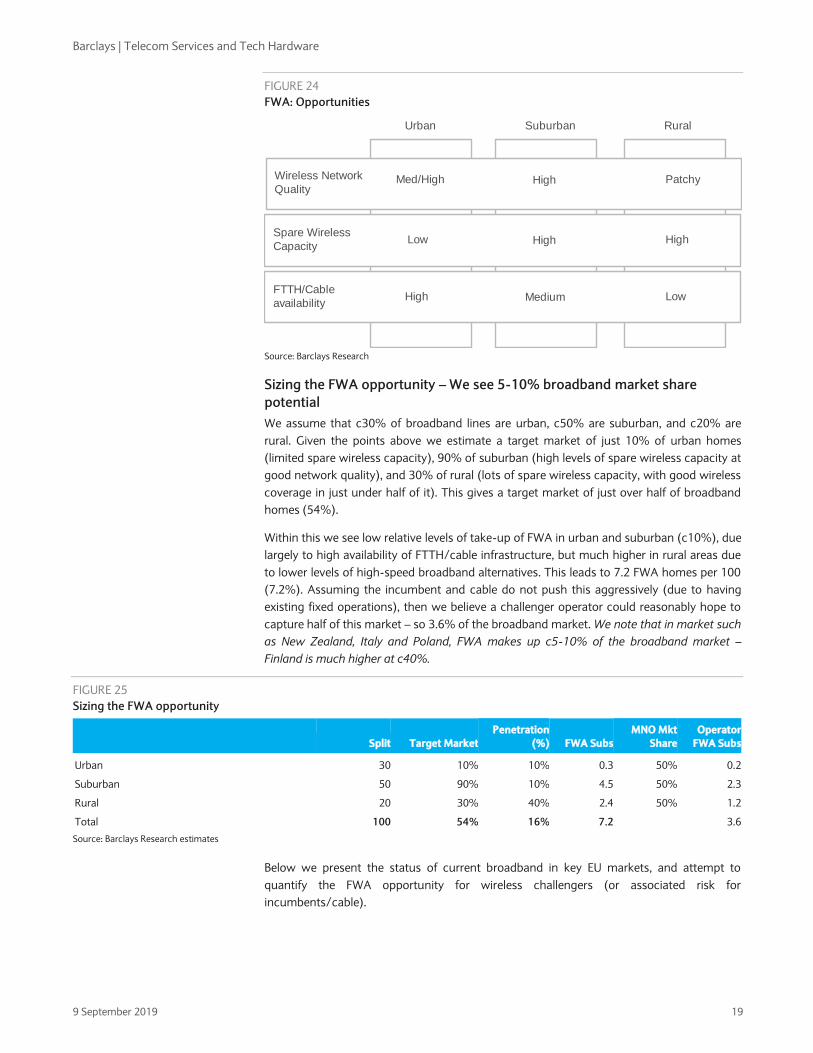

FIGURE 24

FWA: Opportunities

Source: Barclays Research

Sizing the FWA opportunity – We see 5-10% broadband market share

potential

We assume that c30% of broadband lines are urban, c50% are suburban, and c20% are

rural. Given the points above we estimate a target market of just 10% of urban homes

(limited spare wireless capacity), 90% of suburban (high levels of spare wireless capacity at

good network quality), and 30% of rural (lots of spare wireless capacity, with good wireless

coverage in just under half of it). This gives a target market of just over half of broadband

homes (54%).

Within this we see low relative levels of take-up of FWA in urban and suburban (c10%), due

largely to high availability of FTTH/cable infrastructure, but much higher in rural areas due

to lower levels of high-speed broadband alternatives. This leads to 7.2 FWA homes per 100

(7.2%). Assuming the incumbent and cable do not push this aggressively (due to having

existing fixed operations), then we believe a challenger operator could reasonably hope to

capture half of this market – so 3.6% of the broadband market. We note that in market such

as New Zealand, Italy and Poland, FWA makes up c5-10% of the broadband market –

Finland is much higher at c40%.

FIGURE 25

Sizing the FWA opportunity

Split Target Market

Penetration

(%) FWA Subs

MNO Mkt

Share

Operator

FWA Subs

Urban 30 10% 10% 0.3 50% 0.2

Suburban 50 90% 10% 4.5 50% 2.3

Rural 20 30% 40% 2.4 50% 1.2

Total 100 54% 16% 7.2 3.6

Source: Barclays Research estimates

Below we present the status of current broadband in key EU markets, and attempt to

quantify the FWA opportunity for wireless challengers (or associated risk for

incumbents/cable).

Urban Suburban Rural

Wireless Network

Quality

Spare Wireless

Capacity

FTTH/Cable

availability

Med/High High Patchy

Low High High

High Medium Low

Barclays | Telecom Services and Tech Hardware

9 September 2019 20

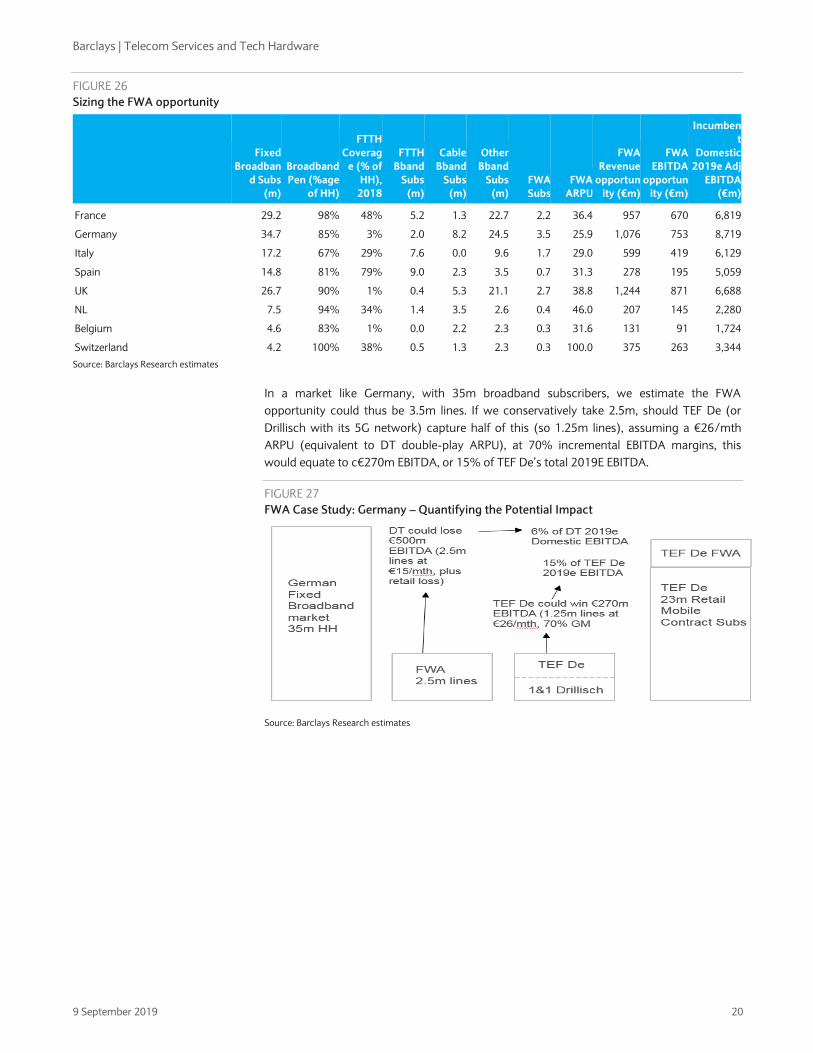

FIGURE 26

Sizing the FWA opportunity

Fixed

Broadban

d Subs

(m)

Broadband

Pen (%age

of HH)

FTTH

Coverag

e (% of

HH),

2018

FTTH

Bband

Subs

(m)

Cable

Bband

Subs

(m)

Other

Bband

Subs

(m)

FWA

Subs

FWA

ARPU

FWA

Revenue

opportun

ity (€m)

FWA

EBITDA

opportun

ity (€m)

Incumben

t

Domestic

2019e Adj

EBITDA

(€m)

France 29.2 98% 48% 5.2 1.3 22.7 2.2 36.4 957 670 6,819

Germany 34.7 85% 3% 2.0 8.2 24.5 3.5 25.9 1,076 753 8,719

Italy 17.2 67% 29% 7.6 0.0 9.6 1.7 29.0 599 419 6,129

Spain 14.8 81% 79% 9.0 2.3 3.5 0.7 31.3 278 195 5,059

UK 26.7 90% 1% 0.4 5.3 21.1 2.7 38.8 1,244 871 6,688

NL 7.5 94% 34% 1.4 3.5 2.6 0.4 46.0 207 145 2,280

Belgium 4.6 83% 1% 0.0 2.2 2.3 0.3 31.6 131 91 1,724

Switzerland 4.2 100% 38% 0.5 1.3 2.3 0.3 100.0 375 263 3,344

Source: Barclays Research estimates

In a market like Germany, with 35m broadband subscribers, we estimate the FWA

opportunity could thus be 3.5m lines. If we conservatively take 2.5m, should TEF De (or

Drillisch with its 5G network) capture half of this (so 1.25m lines), assuming a €26/mth

ARPU (equivalent to DT double-play ARPU), at 70% incremental EBITDA margins, this

would equate to c€270m EBITDA, or 15% of TEF De’s total 2019E EBITDA.

FIGURE 27

FWA Case Study: Germany – Quantifying the Potential Impact

Source: Barclays Research estimates

Barclays | Telecom Services and Tech Hardware

9 September 2019 21

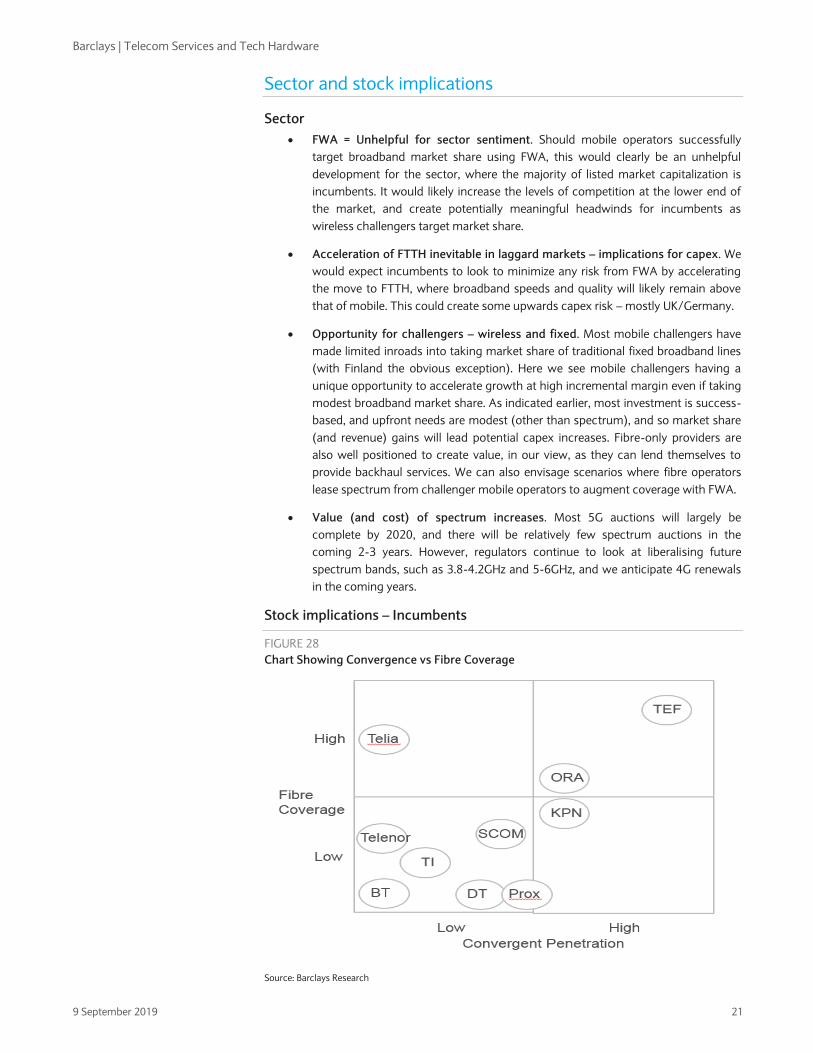

Sector and stock implications

Sector

FWA = Unhelpful for sector sentiment. Should mobile operators successfully

target broadband market share using FWA, this would clearly be an unhelpful

development for the sector, where the majority of listed market capitalization is

incumbents. It would likely increase the levels of competition at the lower end of

the market, and create potentially meaningful headwinds for incumbents as

wireless challengers target market share.

Acceleration of FTTH inevitable in laggard markets – implications for capex. We

would expect incumbents to look to minimize any risk from FWA by accelerating

the move to FTTH, where broadband speeds and quality will likely remain above

that of mobile. This could create some upwards capex risk – mostly UK/Germany.

Opportunity for challengers – wireless and fixed. Most mobile challengers have

made limited inroads into taking market share of traditional fixed broadband lines

(with Finland the obvious exception). Here we see mobile challengers having a

unique opportunity to accelerate growth at high incremental margin even if taking

modest broadband market share. As indicated earlier, most investment is success-

based, and upfront needs are modest (other than spectrum), and so market share

(and revenue) gains will lead potential capex increases. Fibre-only providers are

also well positioned to create value, in our view, as they can lend themselves to

provide backhaul services. We can also envisage scenarios where fibre operators

lease spectrum from challenger mobile operators to augment coverage with FWA.

Value (and cost) of spectrum increases. Most 5G auctions will largely be

complete by 2020, and there will be relatively few spectrum auctions in the

coming 2-3 years. However, regulators continue to look at liberalising future

spectrum bands, such as 3.8-4.2GHz and 5-6GHz, and we anticipate 4G renewals

in the coming years.

Stock implications – Incumbents

FIGURE 28

Chart Showing Convergence vs Fibre Coverage

Source: Barclays Research

Barclays | Telecom Services and Tech Hardware

9 September 2019 22

BT – Material copper exposure; relatively high EBITDA risk. Given low levels

FTTH coverage (and penetration), we see BT’s Retail and Openreach businesses as

both potentially exposed to FWA competition, and so do see FWA potentially

taking 10% of the total broadband market vs negligible levels currently. At the

Openreach level, our research has pointed to a clear risk of line loss to AltNets. In

addition to this, we also see FWA migration risk, be it to niche FWA providers, or

mobile-centric operators such as Vodafone, O2 and 3UK.

DT – Material copper exposure; relatively high EBITDA risk. Similar to BT above,

we see DT’s Retail and Network business as exposed to FWA, and note that part of

the Drillisch strategy is to overtly target fixed line replacement via 5G. TEF De

could also make a similar move, although its wholesale cable deal with Vodafone

will likely temper its ambitions in urban areas, unless the FWA business case

proves compelling. We see FWA potentially taking 10% of the total broadband

market.

Orange – Increasing FTTH exposure, increasing convergence; low EBITDA risk.

Fibre coverage and convergence is steadily increasing, although there do remain

areas as yet uncovered. Co-investment models are commonplace in France,

implying many service providers are incentivized to use the wireline infrastructure.

That said, we cannot discount Iliad or Bouygues being disruptive with FWA. We

see FWA potentially taking 5% of the broadband market.

TEF – Low copper exposure, converged market; low EBITDA risk. Given the high

FTTH coverage (and penetration), plus a clearly converged market, we see TEF’s

Retail and Network business as only marginally exposed to FWA competition

(despite high ARPU), and so see FWA potentially taking just 5% of the broadband

market.

TI – Material copper exposure, current low broadband share and penetration;

medium EBITDA risk. FWA providers have already taken 6% of the Italian

broadband market, and Italian fixed broadband penetration is 20pp lower than EU

peers. As such the relative exposure appears somewhat modest – having said that,

we can see both Vodafone and Hutchison potentially using 5G as a means to

target areas not served by FTTH. We see FWA potentially taking 10% of the total

broadband market.

KPN – High fixed speeds, high convergence, limited retail competition; low

EBITDA risk. The only operator likely to promote FWA aggressively in the

Netherlands is T-Mobile, as both Vodafone and KPN have established fixed

networks, with clear plans to upgrade to high speeds. With service providers

having access to both incumbent FTTH and cable wholesale, the incentive to

promote FWA is somewhat limited, in our view. We see FWA potentially taking just

5% of the broadband market.

Proximus and Swisscom – Medium risk to EBITDA. Both Proximus and Swisscom

are driving high levels of convergence, and both have established cable

competition with incumbents having a route to FTTH. That said, there are

potentially disruptive operators (Salt/Sunrise in Switzerland, and Orange in

Belgium) that could use FWA as a disruptive tool. We see FWA potentially taking

7.5% of the broadband market.

Nordics – Medium risk to EBITDA. Tele2 has shown in the Baltic markets that it

has been able to grow its wireless business using FWA, as mobile speeds have

rivalled those of fixed. The same could occur in the Nordic markets, especially in

areas with limited FTTH rollout, and there is a disruptive mobile operator in

Barclays | Telecom Services and Tech Hardware

9 September 2019 23

Norway, Denmark and Sweden (Ice, Hutchison and Hutchison respectively).

Sweden would appear to have a lower risk due to widespread FTTH deployment,

and in Finland the FWA migration has already occurred.

Vodafone – FWA should present more of an opportunity than a threat. Vodafone

now owns extensive fixed and mobile infrastructure in Spain, Germany and the

Netherlands, but this is high-speed cable, and so should not be materially

impacted by FWA. In the UK, Italy and Vodacom we see an opportunity for

Vodafone to take market share of fixed broadband using FWA. That said,

Vodafone is likely to be more reticent to risk impacting its mobile quality of service,

and as such we do not anticipate the company being overly aggressive near term.

Stock implications – Challengers/Cable

TEF De – Material market share opportunity. We see the low fibre coverage in

Germany presenting a clear opportunity for FWA as a replacement product. We

also believe recently improved network quality with ample spare 5G spectrum in

rural areas creates an opportunity for TEF De. TEF De has a low share of the

broadband market, and so has scope to grow its share materially on FWA (and on

Vodafone’s cable infrastructure), especially as the market converges. Assuming

TEF De adds 1.75m FWA subscribers (50% of total FWA), this could add 15% to

our 2019 EBITDA estimate.

Sunrise – actively capitalizing on FWA opportunity – sees at least 3% EBITDA by

2021E. Sunrise has actively talked up the FWA opportunity in Switzerland, seeing it

as a viable alternative to copper broadband, particularly in rural areas where the

speeds provided by Swisscom infrastructure are low. Having invested in its mobile

network to improve quality and catch up with Swisscom, Sunrise sees mobile

broadband, particularly on 5G, as a way to take market share in rural areas due to

the faster speeds offered. Long term it expects to have a mixture of fibre in urban

areas, copper (or potentially cable) in suburban areas and mobile broadband in

suburban/rural areas. Sunrise has already begun its 5G rollout and expects a low-

single-digit EBITDA contribution from mobile broadband in 2020, which it sees

doubling in 2021 (c.3% of EBITDA), offsetting the short-term investment required.

Drillisch & United Internet – A clear opportunity, but execution will take time.

Drillisch has c10m mobile and c4.3m fixed broadband customers, using all of

Telefonica De, Vodafone and DT for mobile and fixed wholesale access. The

company spends >€1bn/year on wholesale fixed and mobile payments (xDSL, 3G

and 4G), and could use its 5G network to migrate its mobile customer base off the

Telefonica De and Vodafone networks (this is well documented), but also

potentially provision fixed-line services. Given our estimate of c€3.5bn upfront

investment for c40% population coverage, the economics (on paper at least) of

this investment look potentially very attractive. Clearly execution is key (and not

without risk).

Orange Belgium – material upside potential. We believe Orange Belgium’s

network can be leveraged for FWA. Orange Belgium is currently pursuing a cable

wholesale strategy to take broadband market share in Belgium (it has currently

just c5% compared with its mobile market share of c23%). Whilst national cable

coverage could somewhat limit the FWA opportunity, Proximus’ slow FTTH rollout

does suggest that, were OBEL to pivot to an FWA strategy, it could take a

significant amount of market share. Modest share won through cable has provided

material upside for OBEL, so even just modest success with FWA (better margins

than cable) could offer material upside.

Barclays | Telecom Services and Tech Hardware

9 September 2019 24

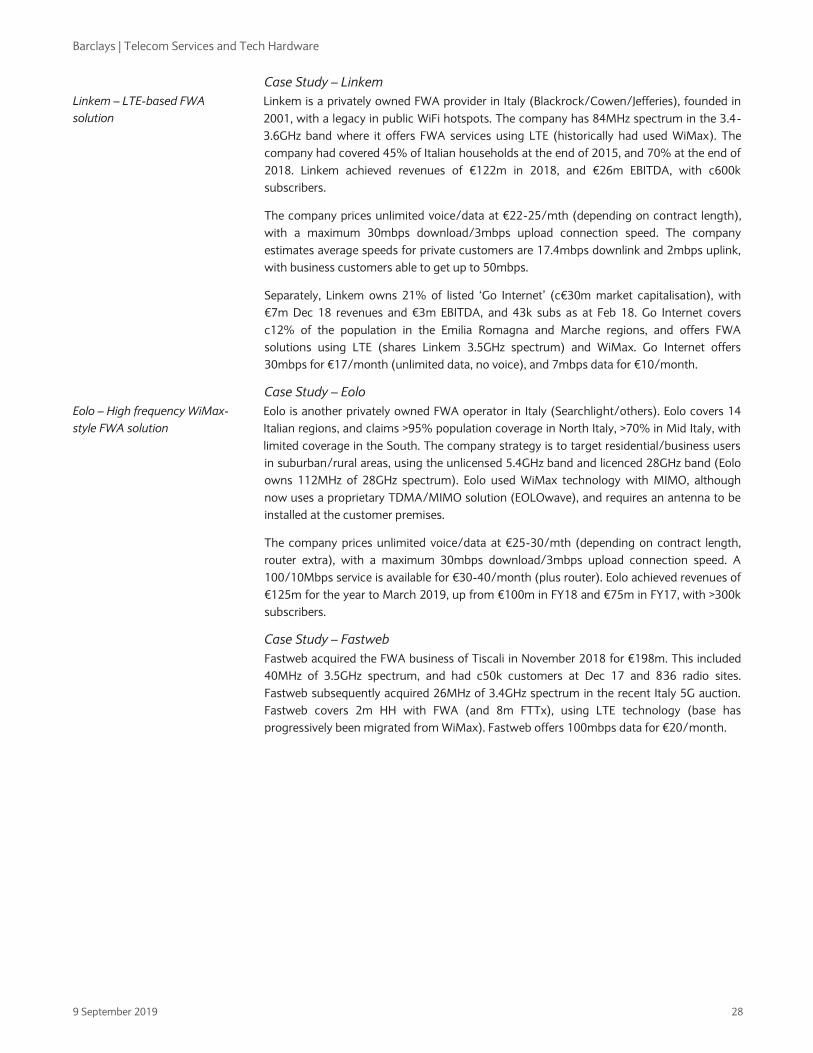

Bouygues and Iliad. In France, Bouygues and Iliad do have not a legacy fixed line

networks and could therefore use FWA to complement their FTTH network

strategy. Whilst both operators have deployed some fiber in dense areas and are

using the co-investment model in less dense areas (AMII) with Orange or Altice

and the wholesale model with other operators in RIP areas, using a FWA

technology could be a sensible way to leverage their mobile assets. This is more

notably the case for Bouygues that had 17k LTE sites at YE 2018 and plans to have

total sites of 28k in 2023. Iliad is rolling its network and reached 12k LTE at YE

2018 and plans to have more than 25k sites by 2024. With 3.4-3.6GHz spectrum

auctions planned for 320MHz of spectrum in Q4 19/Q1 20, both companies could

secure enough spectrum to deploy a FWA strategy. We note that none has so far

given any indication that they wanted to pursue such a route.

Airtel Africa. Fixed line penetration and coverage in Africa is very low, with mobile

being the dominant technology for connectivity. Airtel Africa has consistently

indicated its strategy to pursue the FWA opportunity, and points to having

significant excess LTE capacity due to recent technology upgrades, and access to

sufficient spectrum. The company has carried out successful pilots in the

Seychelles, and we believe is well placed to roll out across the rest of the footprint.

Stock implications – Towers

Towers – Cellnex and Inwit indirect beneficiaries. We have discussed above in

detail the way operators can add capacity to their networks to cope with FWA

demand. Towers can benefit from either: 1) the heavier and larger equipment used

as this will require higher fees to tower operators; and 2) any future network

densification that may be required in future years as this represents an opportunity

for TowerCos to increase tenancy ratios or add new sites. Cellnex, in fact, already

hosts equipment for pure FWA operators, and has signed an agreement with

Linkem in Italy. Both Cellnex and Inwit also host equipment for Fastweb, which is

pursuing FWA in Italy outside of its fixed network coverage.

Stock implications – Technology Hardware

Radio access equipment vendors Nokia (OW) and Ericsson (EW) both actively

encourage operators to consider FWA strategies. While initial incremental capex may be

modest, as mobile challengers can leverage existing assets, if the provider is successful,

then we would expect to see additional success-based investment. We view FWA as an

additional, if modest, tailwind to the broader 5G adoption growth we model for mobile

equipment vendors. We forecast the two leading radio access vendors to grow at low

single digits over the next few years, driven by broader 5G deployments. In absolute

terms, we forecast $1.0-1.5bn in incremental radio access revenue for the industry each

year through the early 2020s. We consider FWA strategies as part of this growth.

Ubiquiti (UW) is a FWA provider, mostly in emerging markets, using WiFi for the access

layer. This market has slowed dramatically as 4G has grown, and we expect this trend to

continue.

FWA will also require the strengthening of networks beyond just the radio layer,

potentially leading to greater core and edge spending. In many cases, operators have

bolstered their backhaul networks in preparation for 5G deployments, one of a number

of positive drivers for the optical networking vendors in recent years. If FWA strategies

prove successful, then we may see such a tailwind continue for optical investment as

well. Key vendors here are Huawei (not covered), Ciena (OW) and Nokia, while Corning

(OW) should also benefit on the cable and passive components side. Networking

vendors that sell to the Telco space could also see a boost, which would help companies

like Cisco (EW), Arista (OW), Juniper (EW) and F5 (OW).

Barclays | Telecom Services and Tech Hardware

9 September 2019 25

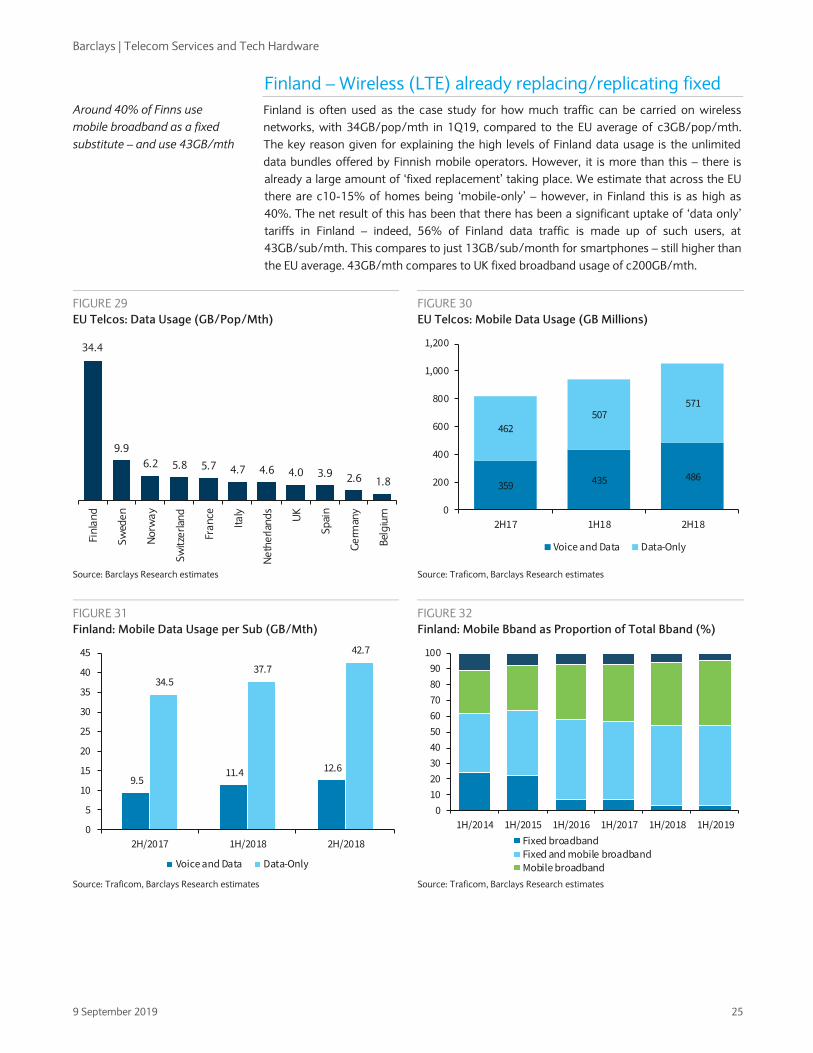

Finland – Wireless (LTE) already replacing/replicating fixed

Finland is often used as the case study for how much traffic can be carried on wireless

networks, with 34GB/pop/mth in 1Q19, compared to the EU average of c3GB/pop/mth.

The key reason given for explaining the high levels of Finland data usage is the unlimited

data bundles offered by Finnish mobile operators. However, it is more than this – there is

already a large amount of ‘fixed replacement’ taking place. We estimate that across the EU

there are c10-15% of homes being ‘mobile-only’ – however, in Finland this is as high as

40%. The net result of this has been that there has been a significant uptake of ‘data only’

tariffs in Finland – indeed, 56% of Finland data traffic is made up of such users, at

43GB/sub/mth. This compares to just 13GB/sub/month for smartphones – still higher than

the EU average. 43GB/mth compares to UK fixed broadband usage of c200GB/mth.

FIGURE 29

EU Telcos: Data Usage (GB/Pop/Mth)

FIGURE 30

EU Telcos: Mobile Data Usage (GB Millions)

Source: Barclays Research estimates Source: Traficom, Barclays Research estimates

FIGURE 31

Finland: Mobile Data Usage per Sub (GB/Mth)

FIGURE 32

Finland: Mobile Bband as Proportion of Total Bband (%)

Source: Traficom, Barclays Research estimates Source: Traficom, Barclays Research estimates

34.4

9.9

6.2 5.8 5.7 4.7 4.6 4.0 3.9 2.6 1.8

Fin

lan

d

Sw

ede

n

No

rwa

y

Sw

itze

rlan

d

Fra

nce

Ita

ly

Ne

the

rlan

ds

UK

Sp

ain

Ge

rman

y

Bel

giu

m

359 435 486

462

507571

0

200

400

600

800

1,000

1,200

2H17 1H18 2H18

Voice and Data Data-Only

9.5 11.4 12.6

34.5 37.7

42.7

0

5

10

15

20

25

30

35

40

45

2H/2017 1H/2018 2H/2018

Voice and Data Data-Only

0

10

20

30

40

50

60

70

80

90

100

1H/2014 1H/2015 1H/2016 1H/2017 1H/2018 1H/2019

Fixed broadbandFixed and mobile broadbandMobile broadband

Around 40% of Finns use

mobile broadband as a fixed

substitute – and use 43GB/mth

Barclays | Telecom Services and Tech Hardware

9 September 2019 26

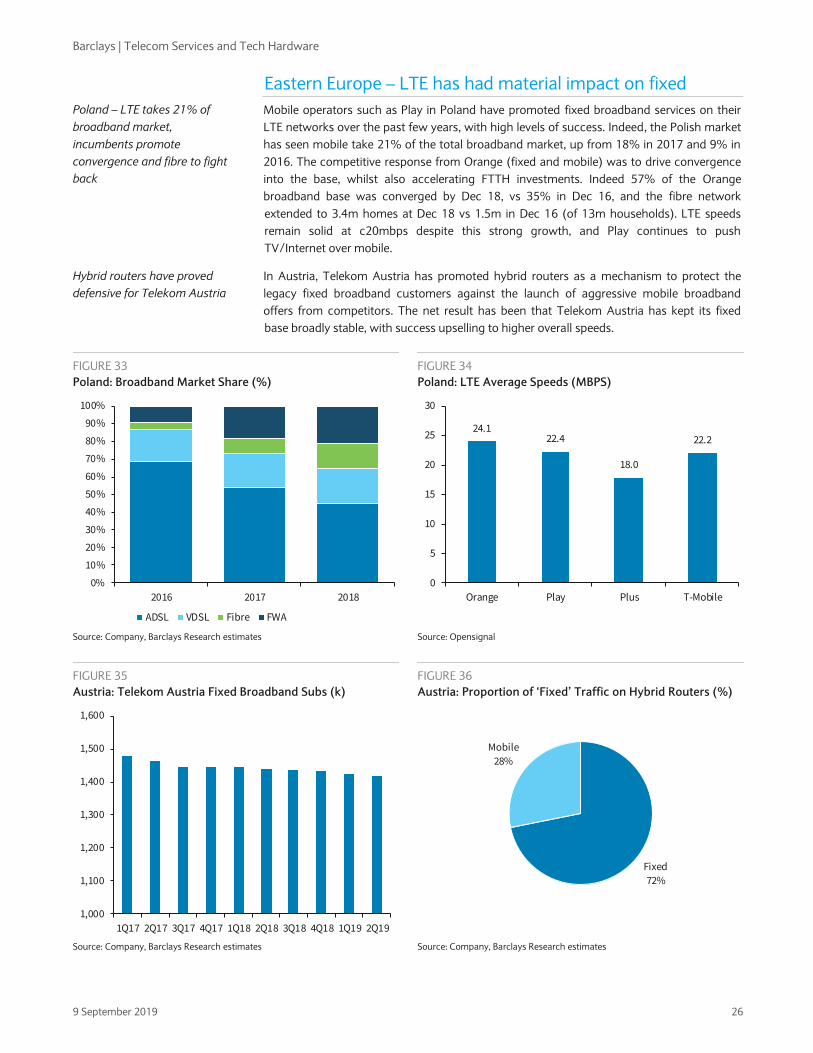

Eastern Europe – LTE has had material impact on fixed

Mobile operators such as Play in Poland have promoted fixed broadband services on their

LTE networks over the past few years, with high levels of success. Indeed, the Polish market

has seen mobile take 21% of the total broadband market, up from 18% in 2017 and 9% in

2016. The competitive response from Orange (fixed and mobile) was to drive convergence

into the base, whilst also accelerating FTTH investments. Indeed 57% of the Orange

broadband base was converged by Dec 18, vs 35% in Dec 16, and the fibre network

extended to 3.4m homes at Dec 18 vs 1.5m in Dec 16 (of 13m households). LTE speeds

remain solid at c20mbps despite this strong growth, and Play continues to push

TV/Internet over mobile.

In Austria, Telekom Austria has promoted hybrid routers as a mechanism to protect the

legacy fixed broadband customers against the launch of aggressive mobile broadband

offers from competitors. The net result has been that Telekom Austria has kept its fixed

base broadly stable, with success upselling to higher overall speeds.

FIGURE 33

Poland: Broadband Market Share (%)

FIGURE 34

Poland: LTE Average Speeds (MBPS)

Source: Company, Barclays Research estimates Source: Opensignal

FIGURE 35

Austria: Telekom Austria Fixed Broadband Subs (k)

FIGURE 36

Austria: Proportion of ‘Fixed’ Traffic on Hybrid Routers (%)

Source: Company, Barclays Research estimates Source: Company, Barclays Research estimates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017 2018

ADSL VDSL Fibre FWA

24.122.4

18.0

22.2

0

5

10

15

20

25

30

Orange Play Plus T-Mobile

1,000

1,100

1,200

1,300

1,400

1,500

1,600