Embed Size (px)

Citation preview

THEWORLDBANKGROUP

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityfor

EconomicDevelopmentNoteforthePalestinianMinistryofTelecommunicationsandInformation

Technology

CarloMariaRossotto,AnatLewin,XavierDecoster

2/1/2016

TA-P150798-TAS-BB

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

2

StandardDisclaimerThisvolumeisaproductofthestaffoftheInternationalBankforReconstructionandDevelopment/TheWorldBank. The findings, interpretations, and conclusions expressed in this paper do not necessarilyreflecttheviewsoftheExecutiveDirectorsofTheWorldBankorthegovernmentstheyrepresent.TheWorldBankdoesnotguaranteetheaccuracyofthedataincludedinthiswork.Theboundaries,colors,denominations,andotherinformationshownonanymapinthisworkdonotimplyanyjudgmentonthepartofTheWorldBankconcerningthelegalstatusofanyterritoryortheendorsementoracceptanceofsuchboundaries.

CopyrightStatementThematerial inthispublicationiscopyrighted.Copyingand/ortransmittingportionsorallofthisworkwithoutpermissionmaybeaviolationofapplicablelaw.TheInternationalBankforReconstructionandDevelopment/TheWorldBankencouragesdisseminationofitsworkandwillnormallygrantpermissiontoreproduceportionsoftheworkpromptly.

For permission to photocopy or reprint any part of this work, please send a request with completeinformation to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,MA 01923, USA,telephone978-750-8400,fax978-750-4470,http://www.copyright.com/.

Allotherqueriesonrightsandlicenses,includingsubsidiaryrights,couldbeaddressedtotheOfficeofthePublisher,TheWorldBank,1818HStreetNW,Washington,DC20433,USA, fax202-522-2422,[email protected].

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

3

AcknowledgementsThisnotewaspreparedbyateamundertheleadershipofPierreGuislain(SeniorDirector,TransportandICTGlobalPractice)andSteenLauJorgensen(PalestinianterritoriesCountryDirector).TheteamwasledbyCarloMariaRossotto(LeadICTSpecialist,ICTRegionalCoordinator,ECAandMENA,TransportandICTGlobalPractice),andincludedXavierStéphaneDecoster(ICTPolicySpecialist,TransportandICTGlobalPractice), Anat Lewin (Senior ICT Policy Specialist, Transport and ICT Global Practice) and Ihab Jabari(Consultant,ITExpert).

Theteamgratefullyacknowledgesthereviewandqualitycontrolprovidedbythepeerreviewers:KareemAbdel Aziz (Senior Investment Officer, Telecom and Media Team, Asia, Europe and Middle East,International Finance Corporation), and Yann Burtin (Senior Underwriter, Multilateral InvestmentGuaranteeAgency).FurtherreviewwasprovidedbyRanjanaMukherjee(CountryProgramCoordinator,PalestinianterritoriesCountryManagementUnit),MarkEugeneAhern(ProgramLeader,MNC04),BjornPhilip(ProgramLeader,MNC04),AlexandraPugachevsky(SeniorCountryOfficer,PalestinianterritoriesCountry Management Unit), Youssef Issa Habesch (Principal Country Officer, IFC), Nur Nasser Eddin(Economist, GMFDR), Bjorn Philipp (Program Leader, MNC04), Randeep Sudan (Practice Manager,Transport and ICT Global Practice), Boutheina Guermazi (PracticeManager, Transport and ICT GlobalPractice), and Doyle Gallegos (Lead ICT Specialist, Global Lead Broadband, Transport and ICT GlobalPractice).

Theinputofthefollowingcolleaguesisalsogratefullyacknowledged:RanaIshaqKassis(SeniorProgramAssistant,MNC04),Teri Nachazel (Program Assistant,MNC04), Fifi Antar (Program Assistant,MNC04),Khalida Seif El-Din Al-Qutob (Program Assistant, MNC04), and Ndeye Anna Ba (Program Assistant,TransportandICTGlobalPractice).

TheteamhascloselyinteractedwiththeExternalCommunicationsteamoftheWorldBank,andwishestothankfullyacknowledgetheirguidanceandcontribution,includingthatofHebaShamseldin(Manager,MENA External Communications), Lara Saade (Senior Communications Officer, MENA ExternalCommunications),WilliamStebbins(SeniorCommunicationsOfficer,MENAExternalCommunications),AshrafSaadAllahAl-Saeed(OnlineCommunicationsOfficer,MENAExternalCommunications),andMaryKoussa(CommunicationsOfficer,MENAExternalCommunicationsinJerusalem).

TheteamwishestoexpressitsdeepestappreciationforthecooperationandfruitfulinteractionswiththePalestinianandIsraeliauthorities,privatesector,andcivilsociety.Theyhaveprovidedexcellentsupportandhavecloselyinteractedwiththetaskteaminaspiritofopennessduringthepreparationofthisreport.

Thetaskteamtakesresponsibilityforanyerrorsandomissions.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

4

Content1 Executivesummary................................................................................................................................6

2 Introduction.........................................................................................................................................13

3 AssessmentoftelecomsectorinthePalestinianterritories...............................................................14

3.1 Institutionalandenablingenvironment.....................................................................................14

3.2 Fixed-broadbandsectorassessment..........................................................................................15

3.3 Mobilesectorassessment..........................................................................................................16

3.4 Internationalconnectivityassessment.......................................................................................18

3.5 InternationalbenchmarkofthePalestiniantelecommunicationssector..................................18

4 Telecomsectorachievementsandissues............................................................................................20

4.1 Domesticachievementsandissues............................................................................................20

4.2 Domesticandbilateralachievementsandissues.......................................................................26

4.3 SpecificissuesinGaza................................................................................................................35

4.4 Assessingtheimpactofmobilemarketunder-developmentinthePalestinianterritories.......38

5 Conclusionsandrecommendations.....................................................................................................44

6 Listoffiguresandtables......................................................................................................................47

7 Referencesandsources.......................................................................................................................49

8 Annex...................................................................................................................................................51

8.1 InternationalbenchmarkofthePalestiniantelecomsector......................................................51

8.2 Spectrumtableassignment........................................................................................................56

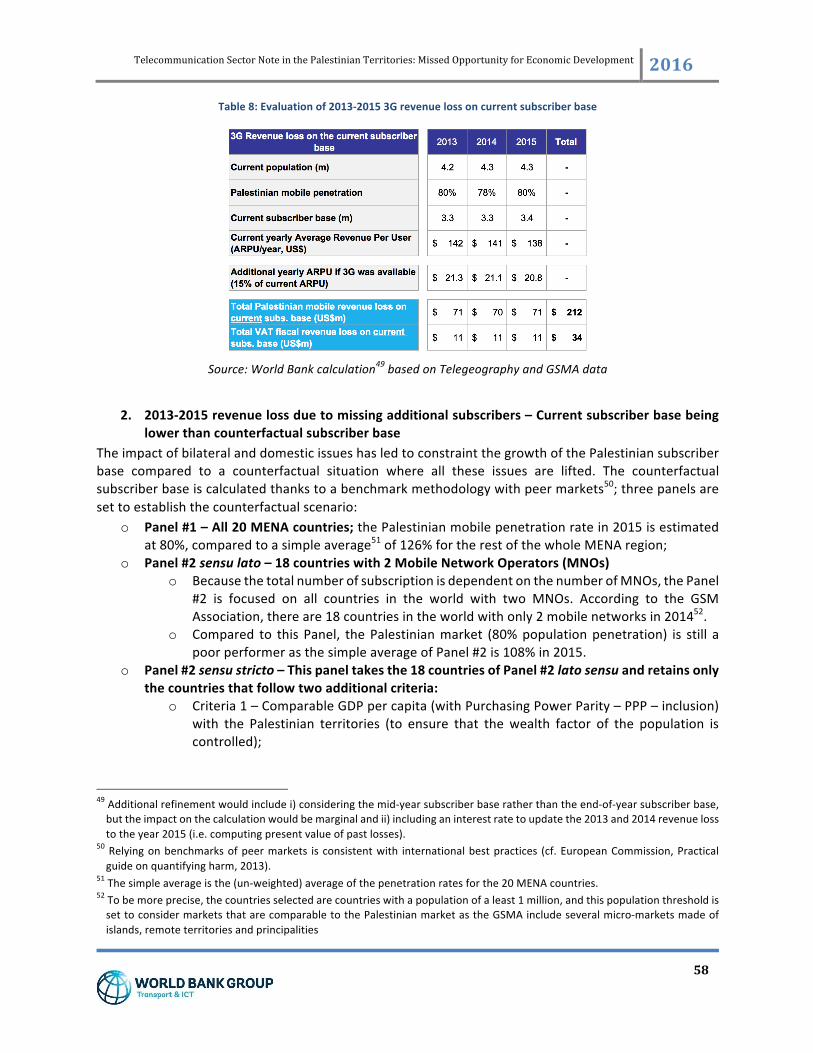

8.3 Directimpactcalculation............................................................................................................56

8.4 RelevantLegalAgreements........................................................................................................60

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

5

Acronyms

2G Second-generationmobilenetworkorservice

3G Third-generationmobilenetworkorservice

4G Fourth-generationmobilenetworkorservice(alsoknownas“LTE”)

ADSL AsymmetricDigitalSubscriberLine

AREGNET ArabRegulatorsNetwork

COGAT CoordinatorofGovernmentActivitiesintheTerritories

EC EuropeanCommission

GSM GlobalSystemforMobileCommunication

GSMA GSMAssociation

ICT InformationandCommunicationTechnologies

IGW InternationalGateway

ISP InternetServiceProvider

ITU InternationalTelecommunicationsUnion

JDECO JerusalemDistrictElectricCompany

LAN LocalAreaNetwork

LTE Long-TermEvolutionofmobilenetworkorservice(alsoknownas“4G”)

MENA Middle-EastNorthAfrica

MoC IsraeliMinistryofCommunications

MTIT PalestinianMinistryofTelecommunicationsandInformationTechnology

MNO MobileNetworkOperator

NRA NationalRegulatoryAuthority

PA PalestinianAuthority

PNINA PalestinianNationalInternetNamingAuthority

PSTN PublicSwitchTelephoneNetwork

PTRA PalestinianTelecommunicationsRegulatoryAuthority

RIO ReferenceInterconnectionOffer

SIM SubscriberIdentityModule(betterknownas“SIMcard”)

SMP SignificantMarketPower

VAT ValueAddedTax

WB&G WestBankandGaza

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

6

1 Executive summary TheTelecommunicationsSectorAssessmentNote inthePalestinianterritories isaknowledgeproductprepared by the World Bank in response to a specific request from the Palestinian Ministry ofTelecommunications and Information Technology (MTIT) to assess the performance of thetelecommunicationssector,identifyspecificissuesandmakerecommendationsforfurtherdevelopmentandreform.

MAINFINDINGS

The Oslo framework, the reference agreement between the Israeli and Palestinian counterparts tosupporteconomicdevelopmentandstabilityinkeyeconomicsectors,hasfailedtodeliveritspromiseofanindependenttelecommunicationssectorinthePalestinianterritories.Accordingtotheprinciplesofthe Oslo Agreement, “Israel recognizes that the Palestinian side has the right to build and operateseparate and independent communication systems and infrastructures including telecommunicationnetworks, a television network and a radio network.” Several resolutions of the InternationalTelecommunicationsUnion1confirmtherightofthePalestinianpeopletohaveaccesstoanindependenttelecommunicationsnetwork.

The principles of the Oslo agreement with respect to the telecom sector remain valid. However, itsprovisionsarenotapplied.ThisispresentingenormouschallengesforPalestiniantelecomoperators,acleardetrimenttothePalestinianconsumer,afiscallossforthePalestinianAuthority,andanoveralldelayfor sector development. The Joint Technical Committee (JTC) under Oslo, intended to be a regular,technical (non-political) platform to address bilateral issues, has shown inadequate and ineffectiveperformance,andprogresssince2008onbilateralissueshasbeenlimited:

• The lack of spectrum is a significant constraint to the development of the industry; in lateNovember2015,anagreementfora limitedreleaseof frequenciestoPalestinianoperatorstolaunch 3G services has been signed. If implemented, the agreement would finally allowPalestinianoperatorstointroducemobilebroadbandusing3G,abouteightyearsaftertheirinitialrequest.TheagreementwouldstillplacethePalestinianoperatorsatacompetitivedisadvantage,asIsraelioperatorshave3Gand4Gcapabilitiesandareabletoattracthighervaluecustomers.AstheMENAregionismovingtowards4G,therecentagreementonthereleaseoffrequenciescanhardlybecelebratedasasuccess–althoughitdoesrepresentafirststepforward.Combinedwithotherrestrictions,thedelayinmobilebroadbandnegativelyaffectsInternetdevelopment.

• The secondmobile operator (Wataniya) cannot fully play its competitive role for themobilemarket.ItsoperationsintheWestBanksufferedatwo-yeardelayduetoIsraelirestrictionsonreleasingthespectrum.ThesituationforGazaconsumersisworseasWataniyastillcannotstartitsoperationsduetorestrictionsonaccessingspectrumandimportingcivilmaterial2.

• Thepresenceofwidespread,unauthorizedactivityby Israeli operators in theWestBankwithmobile broadband capabilities (Israeli operators have 3G capabilities since 2004 and 4G since2015)hastheeffectofcreatingunfaircompetitionattheexpenseofPalestinianoperatorswhich

1Cf.thefollowingITUresolutions:Resolutions99and125fromthePlenipotentiaryConferencePP-14,Resolution18fromtheWorld Telecommunication Development Conference WTDC-14, Resolution 12 from the World Radio CommunicationConferenceWRC-12.

2ThishasalsoimpactedWataniya’sbusinessplanwhichhasanopenclaimagainstthePalestinianAuthority,askingforpartofitslicenseproceedstobewaivedgiventhelimiteddeploymentofitsoperationscomparedtotherightsunderitslicense.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

7

cannotevendeliver3Gservices.Dependingonsources,Israelioperatorsmaycurrentlycaptureupto30%oftheWestBankmarket involume–i.e.numberofsubscribers.TheIsraelimarketshareinvalue–i.e.measuredbythetotalsales–isevenhigherasIsraelioperatorscapturehighvalue-addedPalestiniancustomersbyproviding3Gand4G.

Otherconstraintshaveanegativeimpactonsectorperformance,including(i)restrictionsontheimportofequipmentfortelecomandICTcompanies, (ii)restrictionofmovementofgoodsandpeoplewithinAreaC thatimpedesthedeploymentandmaintenanceofinfrastructure,and(iii)therequirementbyIsraelthatPalestinianoperatorsgothroughanIsraeli-registeredcompanytoaccessinternationallinks.

Somedomestic regulatoryandcompetition issuespersist, chiefamong themthestrengtheningof theregulatoryframeworkwith–ideally–thecreationofanindependentregulatoryagency.Theystillpresentan important reason in addition to unilateral and bilateral issues for inadequate sector performance.However,someachievementsaresubstantialwhencomparedwithothercountriesinMENAthathaveyettointroducesimilarreforms,andcomparedtothesituationin2008.

• Withtheissueofasecondmobilelicense(tooperatorWataniya)theauthoritieshaveintroducedamobile-focusedcompetitorenjoyingdejurerightsonequalfootingwithincumbentoperatorPaltel.PaltelandWataniyaarerobustcompanies,withdeepknow-howinthesector,technologyproficiency,excellentcommercialskillsandsolidinvestors.ThesecompaniesareessentialassetsfortheeconomicdevelopmentofthePalestinianterritories.Ifunilateralandbilateralconstraintsarealleviated,chiefamongthemthereleasebyIsraelioperatorsofspectrumfor3Gand4GandtheliftingofIsraelirestrictionsontheimportofequipmentforWataniyainGaza,theycouldmakeasubstantialcontributiontothedevelopmentofthePalestinianTerritories.

• ThePalestinianauthoritiesallowfacilities-basedISPs,whereinalocalISPcanacquireabroadbandlicenseandbecomeabroadbandoperator.Asaresult,localentrepreneurscanacquirerightsanddirectly invest inthedevelopmentofbroadbandinfrastructureataccess level.Thishasbeenafactor of success for the development of broadband in other emerging regions, especially inEasternEurope.FewcountriesinMENAhaveadoptedthisliberalapproach,whichisthenorminEuropeandotherregions.Thisachievementisnoteworthy.

• Palestinian ISPs with a broadband license can use alternative infrastructure built by non-telecommunicationsoperators,inaccordancetothelawandrelevantregulations.Forexample,thefiberopticsinfrastructureofJDECO,aJerusalemutilitycompany,isusedbyatleastoneISP.JDECOmaybewillingtoleaseinfrastructuretootheroperators.

• MTIThasalsointroducedcompetitionintheVoIPandWiFimarketsbyintroducingnewlicenses.

Fortheintroductionofcompetitionthroughtheawardofmobileandbroadbandlicensestobesuccessfulfor the Palestinian territories, the overall domestic regulatory framework needs to be strengthened.Despitetheachievementsmentionedabove,thereisstillthecriticalneedtoissueregulationstotacklethedominantpositionofPaltelinselectedsegments,andofunauthorizedIsraelioperators.Thereisanactiveandpressingdebateontheneedofanewlaw,andontheintroductionofanindependentregulator.Theintroductionofanindependentregulatoryauthorityreflectsgoodinternationalpracticeandshouldbeconsideredasapriority.

Regardlessofthetimingofthecreationofanindependentregulator,however,theregulatoryframeworkis lacking aminimum regulatory package of key regulations that support competition in in advancedmarkets.Forexample,theregulatoryframeworkshouldbestrengthenedthroughapackageofregulationsto address dominance and potential anti-competitive risks such as (i) limited access to essential

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

8

infrastructures in the fixed broadbandmarket, (ii) on-net / off-net price differentiation in themobilemarket,and(iii)fixedandmobilecross-subsidizing.

Therearespecific,additional issuesof regulatoryand institutionaluncertainty inGaza,preventing thedevelopmentofthetelecomsector:

• AnycompanyapplyingforatelecomlicenseintheWestBankmustgoagainthroughawholenewlicensingprocessinGaza.Thisgeneratesinefficienciesandcosts.

• Several counterpartsmentioned that Gaza authorities are levying tax on telecom companies.Whiletheprincipleoftaxingtelecomcompaniescanbelegitimate,anyfiscalrevenuesshouldbemanageddirectlybythePAorbyadedicatedfundsuchasaUniversalServiceAccessfund.

• MTITdoesnothavecontroloverthePalestinianNationalInternetNamingAuthority(PNINA)–andmore specificallyover thePNINAservers–which is located inGaza is theofficialdomainregistry for thePalestiniancountrycodeTop-Level-Domain (“.ps”).While theabsenceofMTITcontroloverPNINAdoesnotcurrentlypreventPalestiniancompaniestoregisterandoperateawebsite,MTITshouldhavecontroloverthisAuthority.

The impact of unilateral and bilateral issues as well as domestic issues on the performance of thetelecommunicationssectoriscompelling:

• The price of fixed andmobile services is still high, andmobile data is particularly expensive,especiallycomparedwiththeoffersofunauthorizedIsraelioperators.

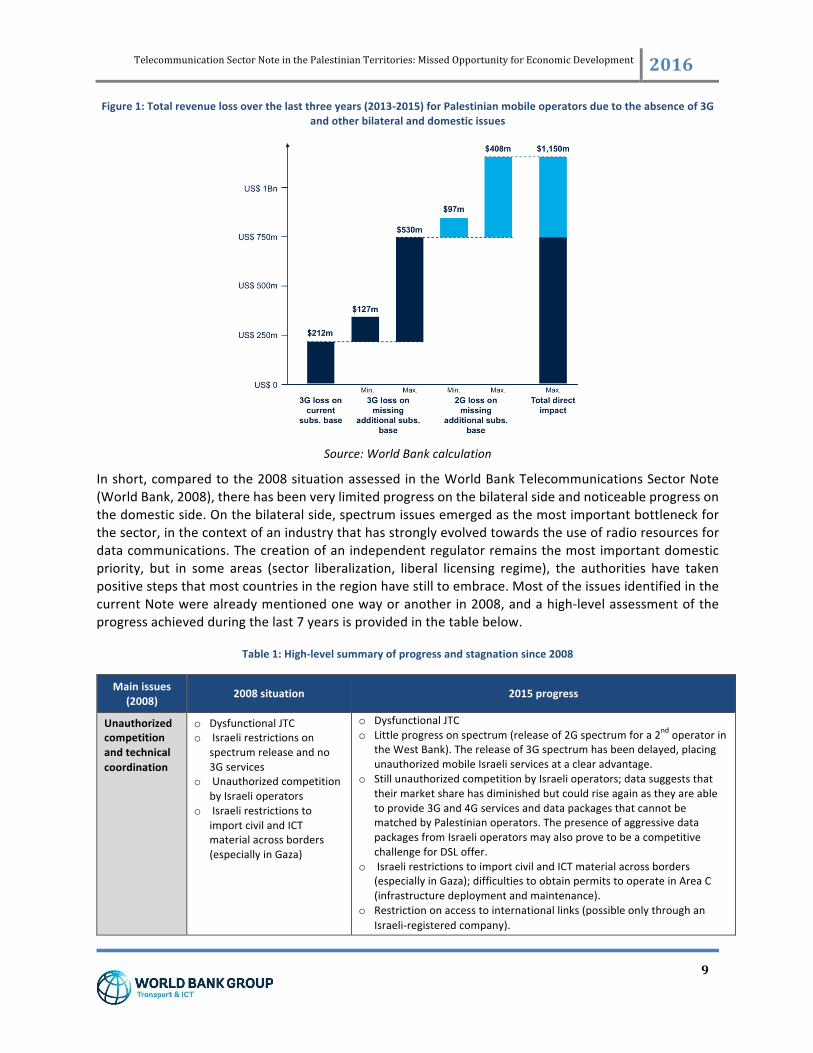

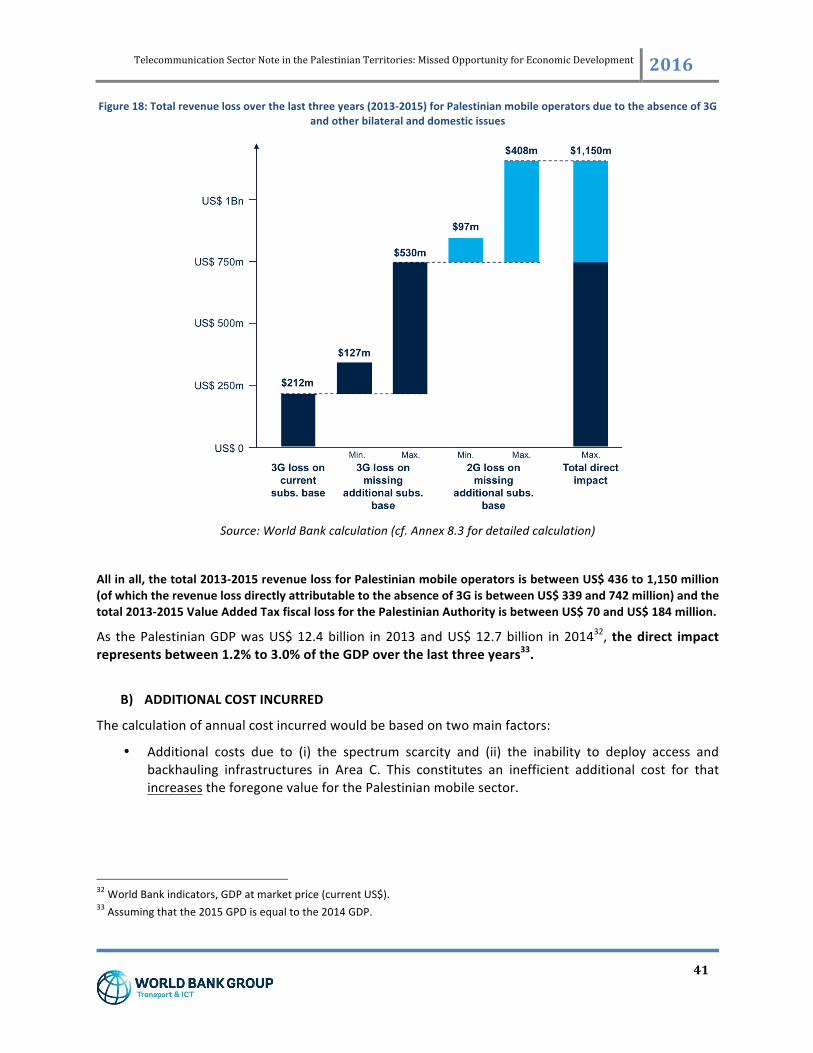

• A high-level, possibly conservative estimation of the foregone value due to lasting effects ofunilateralandbilateralissuesaswellasdomesticissuesisprovidedbasedonabenchmarkingwithpeermarkets.ThetotalrevenuelossforthePalestinianmobilesectorduringthelastthreeyears(2013-2015)rangesfromUS$436to1,150million.Therevenuelossdirectlyattributabletotheabsenceof3GisbetweenUS$339and742millionandthetotal2013-2015ValueAddedTaxfiscalloss for the Palestinian Authority is betweenUS$ 70 andUS$ 184million3. The direct impactrepresentsupto3.0%oftheGDPoverthelastthreeyears.

3AdditionalfiscalrevenuesarenotestimatedinthisNotesuchascorporatetaxes.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

9

Figure1:Totalrevenuelossoverthelastthreeyears(2013-2015)forPalestinianmobileoperatorsduetotheabsenceof3Gandotherbilateralanddomesticissues

Source:WorldBankcalculation

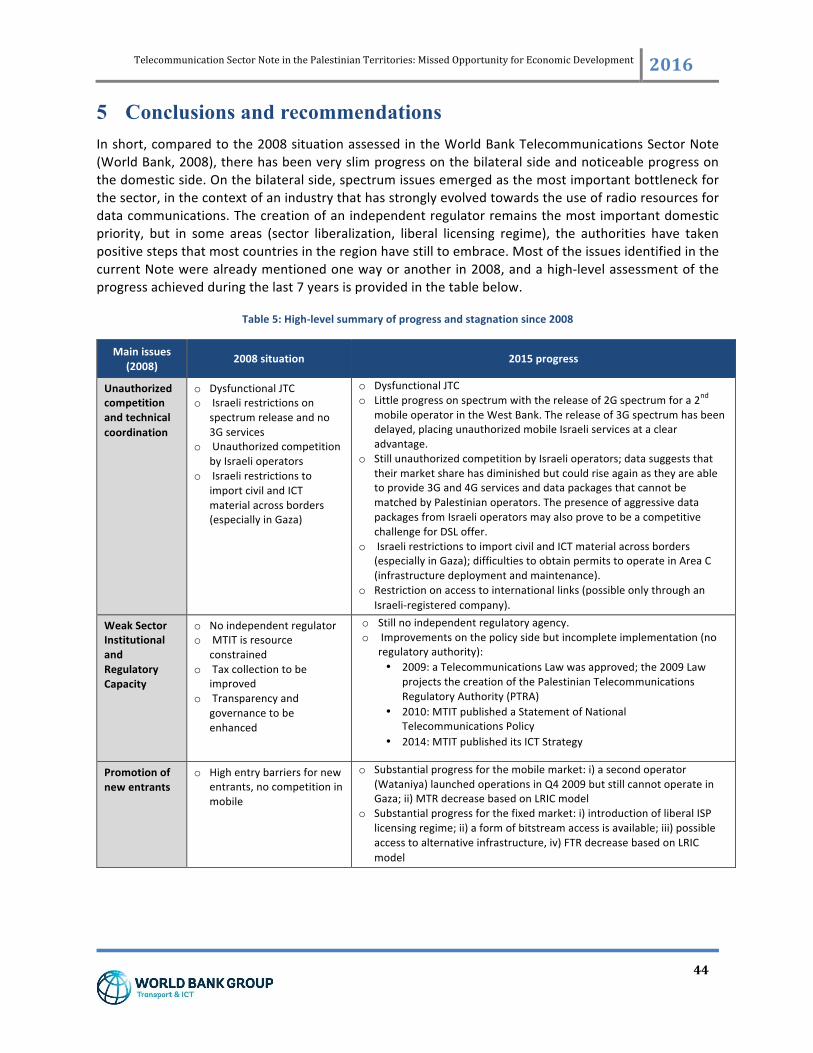

Inshort,comparedtothe2008situationassessedintheWorldBankTelecommunicationsSectorNote(WorldBank,2008),therehasbeenverylimitedprogressonthebilateralsideandnoticeableprogressonthedomesticside.Onthebilateralside,spectrumissuesemergedasthemostimportantbottleneckforthesector,inthecontextofanindustrythathasstronglyevolvedtowardstheuseofradioresourcesfordatacommunications.Thecreationofanindependentregulatorremainsthemostimportantdomesticpriority, but in some areas (sector liberalization, liberal licensing regime), the authorities have takenpositivestepsthatmostcountriesintheregionhavestilltoembrace.MostoftheissuesidentifiedinthecurrentNotewerealreadymentionedonewayoranotherin2008,andahigh-levelassessmentoftheprogressachievedduringthelast7yearsisprovidedinthetablebelow.

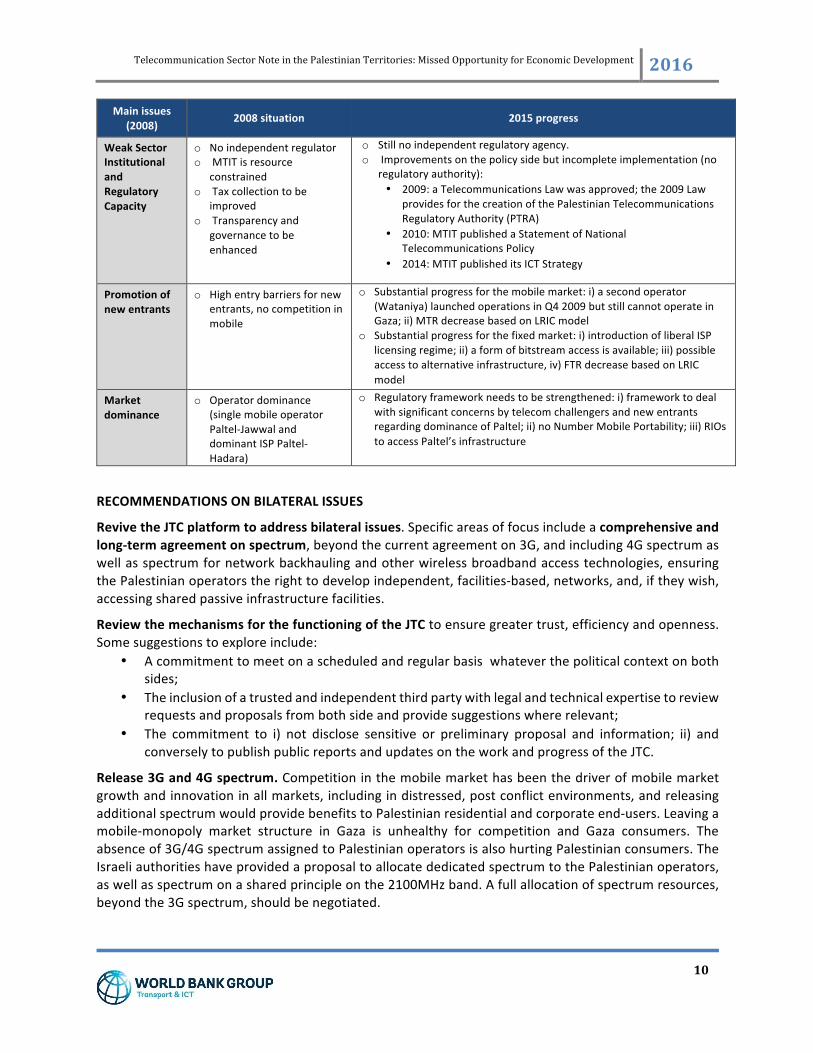

Table1:High-levelsummaryofprogressandstagnationsince2008

Mainissues(2008)

2008situation 2015progress

Unauthorizedcompetitionandtechnicalcoordination

o DysfunctionalJTCo Israelirestrictionson

spectrumreleaseandno3Gservices

o UnauthorizedcompetitionbyIsraelioperators

o IsraelirestrictionstoimportcivilandICTmaterialacrossborders(especiallyinGaza)

o DysfunctionalJTCo Littleprogressonspectrum(releaseof2Gspectrumfora2ndoperatorin

theWestBank).Thereleaseof3Gspectrumhasbeendelayed,placingunauthorizedmobileIsraeliservicesataclearadvantage.

o StillunauthorizedcompetitionbyIsraelioperators;datasuggeststhattheirmarketsharehasdiminishedbutcouldriseagainastheyareabletoprovide3Gand4GservicesanddatapackagesthatcannotbematchedbyPalestinianoperators.ThepresenceofaggressivedatapackagesfromIsraelioperatorsmayalsoprovetobeacompetitivechallengeforDSLoffer.

o IsraelirestrictionstoimportcivilandICTmaterialacrossborders(especiallyinGaza);difficultiestoobtainpermitstooperateinAreaC(infrastructuredeploymentandmaintenance).

o Restrictiononaccesstointernationallinks(possibleonlythroughanIsraeli-registeredcompany).

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

10

Mainissues(2008)

2008situation 2015progress

WeakSectorInstitutionalandRegulatoryCapacity

o Noindependentregulatoro MTITisresource

constrainedo Taxcollectiontobe

improvedo Transparencyand

governancetobeenhanced

o Stillnoindependentregulatoryagency.o Improvementsonthepolicysidebutincompleteimplementation(no

regulatoryauthority):• 2009:aTelecommunicationsLawwasapproved;the2009Law

providesforthecreationofthePalestinianTelecommunicationsRegulatoryAuthority(PTRA)

• 2010:MTITpublishedaStatementofNationalTelecommunicationsPolicy

• 2014:MTITpublisheditsICTStrategy

Promotionofnewentrants

o Highentrybarriersfornewentrants,nocompetitioninmobile

o Substantialprogressforthemobilemarket:i)asecondoperator(Wataniya)launchedoperationsinQ42009butstillcannotoperateinGaza;ii)MTRdecreasebasedonLRICmodel

o Substantialprogressforthefixedmarket:i)introductionofliberalISPlicensingregime;ii)aformofbitstreamaccessisavailable;iii)possibleaccesstoalternativeinfrastructure,iv)FTRdecreasebasedonLRICmodel

Marketdominance

o Operatordominance(singlemobileoperatorPaltel-JawwalanddominantISPPaltel-Hadara)

o Regulatoryframeworkneedstobestrengthened:i)frameworktodealwithsignificantconcernsbytelecomchallengersandnewentrantsregardingdominanceofPaltel;ii)noNumberMobilePortability;iii)RIOstoaccessPaltel’sinfrastructure

RECOMMENDATIONSONBILATERALISSUES

RevivetheJTCplatformtoaddressbilateralissues.Specificareasoffocusincludeacomprehensiveandlong-termagreementonspectrum,beyondthecurrentagreementon3G,andincluding4Gspectrumaswellasspectrumfornetworkbackhaulingandotherwirelessbroadbandaccesstechnologies,ensuringthePalestinianoperatorstherighttodevelopindependent,facilities-based,networks,and,iftheywish,accessingsharedpassiveinfrastructurefacilities.

ReviewthemechanismsforthefunctioningoftheJTCtoensuregreatertrust,efficiencyandopenness.Somesuggestionstoexploreinclude:

• Acommitmenttomeetonascheduledandregularbasiswhateverthepoliticalcontextonbothsides;

• Theinclusionofatrustedandindependentthirdpartywithlegalandtechnicalexpertisetoreviewrequestsandproposalsfrombothsideandprovidesuggestionswhererelevant;

• The commitment to i) not disclose sensitive or preliminary proposal and information; ii) andconverselytopublishpublicreportsandupdatesontheworkandprogressoftheJTC.

Release3Gand4Gspectrum.Competitioninthemobilemarkethasbeenthedriverofmobilemarketgrowthandinnovationinallmarkets,includingindistressed,postconflictenvironments,andreleasingadditionalspectrumwouldprovidebenefitstoPalestinianresidentialandcorporateend-users.Leavingamobile-monopoly market structure in Gaza is unhealthy for competition and Gaza consumers. Theabsenceof3G/4GspectrumassignedtoPalestinianoperatorsisalsohurtingPalestinianconsumers.TheIsraeliauthoritieshaveprovidedaproposaltoallocatededicatedspectrumtothePalestinianoperators,aswellasspectrumonasharedprincipleonthe2100MHzband.Afullallocationofspectrumresources,beyondthe3Gspectrum,shouldbenegotiated.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

11

Lift Israeliconstraintsonthelayoutofmicrowavelinksandthe importofcivilandtelecommaterial–particularlyinGaza.Someoptionsinclude:

• Streamlining the administrative procedure for security clearance with stable, objective,transparentandnon-discriminatorycriteriatobefulfilled;

• PalestiniantelecomandICTcompaniesprovidingalltheneededclearanceformsandproofs;• Israeliauthoritiesmonitoringtheuseofcivilandtelecommaterial–particularlyinGaza–withthe

possible involvementofatrustedthird-partyperformingadetailedauditonaregularbasis toensureallsecurityconcernsaredealtwith.

Mitigatetheeffectofunauthorizedtelecomactivity.TheissueofunauthorizedIsraelitelecomactivityintheWestBankhasbeenpresentthroughtheimplementationoftheOsloagreement.Twomeasurescanaddressthisissue:

• PalestinianoperatorsshouldbeabletoaccesssimilarresourcesasIsraelioperators,inordertobe on the same competition ground. This includes accessing sufficient spectrum to deployindependent3Gand4G/LTEsystems(whichcanbesharedwithIsraelioperatorsonavoluntarybasis);thisisatoppriorityforaction;

• An ideal cooperation between Israeli and Palestinian authorities would limit the coverage ofIsraelioperatorsintheWestBank.Thisincludesthereviewoftelecomequipmentdeployed(e.g.micro-cells with a smaller coverage radius can limit the coverage compared tomacro-cells)4.However,thetrackrecord(especiallyoftheJTC)suggestsskepticismastothereachofasolutiontolimitcoverage.

RECOMMENDATIONSONDOMESTICREGULATORYANDCOMPETITIONISSUES

Createanindependentregulator.Thecreationofanindependentregulator(PTRA)isthetopdomesticpriority, with the setting up of a regulatory framework in line with international best practices. Theregulatoryframeworkshallensureanobjective,transparentandnon-discriminatoryapproachwiththeindustry,supportedbyopennessandpublicconsultations.

Implementthetelecomlaw.TheNotealsourgesthatPalestiniancounterpartstoimplementtheexistinglawwithoutdelay,orintroduceamendmentstoensureitisconsistentwithglobalbestpractices.

Resolve several legaland institutional issuesaffecting the sectorwithaminimumregulatorypackage,including:

• ThemonitoringofthemarketwiththeinstitutionofanICTobservatory.• The introduction and enhancement of regulatory tools such as market observatory, market

definition, identification of Significant Market Power (SMP), remedies definition andenforcements,monitoringandsanctions;

• The enforcement of Reference Interconnection Offers (RIOs) to provide a more dynamic,transparentnon-discriminatoryandcostorientedwholesalemarket;

• The assistance in the setting-up of an ex post competition department or authority (tocomplement theexante regulatoryapproach) tomonitorandapprovepotentialmergersandpreventpotentialanti-competitivebehaviors.

Enhancecapacityandskills.ThelegitimacyandefficiencyofMTITandtheto-be-createdPTRAmustbesupportedbythecontinuingrecruitmentofskilledworkerstokeepupwithmarketdevelopmentsand

4Althoughtheeconomicimpactismarginal,PalestinianoperatorsshouldalsolimittheirsignalreachwithinIsraeliterritory.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

12

complexregulatorytools.Thisremainsachallengeasthe labormarket issmallandthesalaries inthepublicsectorarelowerthanintheprivatesector.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

13

2 Introduction ThePalestinianTelecommunicationsSectorAssessmentNote isaknowledgeproductpreparedby theWorldBankinresponsetoaspecificrequestfromthePalestinianauthoritiestoassesstheperformanceof the telecommunications sector in the Palestinian territories, identify specific issues and makerecommendationsforfurtherdevelopmentandreform.

ThisNotebuildsonpreviousanalyticalproductsproducedbytheWorldBankinthisarea.Inparticular,this specific sector was assessed in 2008, with the publication of the “West Bank and GazaTelecommunicationsAssessmentNote–IntroducingCompetitioninthePalestinianTelecommunicationsSector”(WorldBank,2008).ThepresentNotespecificallydiscussestheevolutionoftheissuesandofthetelecommarketwith respect to the situationanalyzed in2008.Abriefdescriptionof themain issuesidentifiedin2008andtheprogressperformedisdisplayedinthefinalConclusionandRecommendationssection(§5).Morerecently,asubsetofthedomesticandbilateral issuesfacedbythesectorhasalsobeenanalyzedintheWorldBankreport“AreaCandtheFutureofthePalestinianEconomy”,publishedbytheWorldBankinOctober2013(WorldBank,2013).

This note has been prepared through a mix of methodological techniques. The research team hasperformeddeskresearch,leveragingontheavailableliteratureonthePalestinianand,toanextent,Israelitelecommunications sector. The teamhashadextensivediscussionswith the relevant stakeholders inPalestinianterritories,includingseniorgovernmentofficials,privatesectorassociationsandcompanies.TheteamhasalsoengagedtherelevantIsraelicounterparts,andtheOfficeoftheQuartet,anddonorsinvolvedinthesector.Theteamhasalsobenefittedfromtheopportunityofconductingtwofieldtrips.ThefirstfieldtripmetwithprivatesectorrepresentativesinGaza.ThesecondtripwasanengineeringfieldvisittositesaroundRamallah.Theteamhasalsoengagedinextensiveconsultations,includingaone-dayworkshopopentoallmainstakeholdersinRamallah,whereadetailedpresentationofthedraftreportwasdiscussed.ThisworkshoptookplaceonJune30,2015.Theteamhasalsocommissioneda“HouseholdSurveyonTelecomandInternetinJordanValleyVillagesandGazaStrip”tothefirmAlphaInternational.ThesurveywascompletedinSeptemberandOctober2015,andwasdeliveredtotheBankonOctober24,2015.Thisreportreferencessomeoftheresultsofthesurvey.

ForthepurposesoftheNote,theteamhasmainlyfocusedontelecommunicationsinfrastructure,leavingoutotherimportantsub-segmentsoftheICTindustry.TheNotetouchesuponbroadcasting(radioandtelevision) issues,totheextentnecessarytodiscussradio-magneticspectrumandother infrastructurerelatedmatters.Thebroadcastingsectorwoulddeserveaseparatenoteandassessment.TheICTindustryandICTapplicationsarenotspecificallyassessedaspartofthereport.Finally,theemergingeGovernmentapplicationsaretreatedinaseparateWorldBankreport.

Thestructureofthenoteisasfollows:afirstsectiondealswiththeassessmentofthetelecommunicationssector, in termsof physical indicators, infrastructure, investment, prices and services. The Palestiniansector is assessed both in historical perspective (having the 2008 analysis as a starting point), and inrelationwithregionalandglobalbenchmarks.Asecondsectionofthereportillustratesthemainissuesidentifiedbythestakeholders.Finally,thelastsectionofthereportproposeskeyrecommendationsforfurthersectordevelopment.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

14

3 Assessment of telecom sector in the Palestinian territories

3.1 Institutional and enabling environment

ThePalestinianAuthority(PA)isresponsibleforregulatingthetelecommunicationssectorareasunderitsjurisdiction(AreasAandB)asprovidedintheOsloAgreement5,whichsubjectmanyregulatoryareastocoordination between the Palestinian and the Israeli authorities. Sector policy and regulation arepresentlytheresponsibilityofMinistryofTelecommunicationandInformationTechnologies(MTIT)ofthePA.

Until1995,telephonyservicesinthePalestinianterritoriescameunderthejurisdictionofIsrael,whoseincumbentoperatorBezeqfulfilledbothregulatoryandoperationalfunctions.In1995,Israeltransferredaround 80,000 telephone lines connected to 14 exchanges in the Palestinian territories to the newlyformedPA(TeleGeography,2015)6,andin1996theTelecommunicationsLaw3/1996gavetheMTITthe“thedutyofsettingup,runningandoperatingtelecommunicationsnetworksinthePalestinianterritories”(PALaw3/1996,Art.5)7.

In2004MTITandPAstartedaprocess todraftanew legaland regulatory framework tooversee thereformof themarket, including theestablishmentofan independentPalestinianTelecommunicationsRegulatory Authority (PTRA) which would assume all responsibilities held by MTIT for thetelecommunicationssector.Afterseveralreviews,inJune2009thePAPresidentissuedadecreetoenacta new Law on Telecommunications and in April 2010 MTIT published the “The Palestinian NationalAuthorityStatementofNationalTelecommunicationsPolicy”(PAStatement,2010):

• TheStatementincludessix“mainpolicyobjectives”,thefirstofwhichbeingtheestablishmentofthePTRA: (i)To implementthenewregulatoryauthority, (ii)Tocreateacomprehensive legalframework,(iii)Toestablishasoundinterconnectionandaccesspricingregime,(iv)Tointroducewholesale broadband access services, (v) To implement accounting separation and costaccountingand(vi)Toregulatecost-orientedretailpricesofdominantoperators(PAStatement,2010,pp.3-6).

• In addition, MTIT highlighted four “other pressing matters” with (a) “the control nationalfrequenciesandthenationalnumberingplan,thatareatpresentunderthecontroloftheIsraeliauthorities,” (b) “a firstmarket assessment (…) and issueadeclarationdesignatingdominantoperators as appropriate,” (c) “A new form of general licence authorising a broad range ofservices, includingVoiceover IPto InternetServiceprovisiontoreplaceexisting licenceswhichhaveanarrowerscope,”and(d)“severalregulatoryrequirementsthatenhancecompetition,suchascarrierselectionandnumberportability.”(PAStatement,2010,pp.6-7).

5OsloAgreement,AnnexIII,ProtocolonIsraeli-PalestinianCooperationinEconomicandDevelopmentProgramsandTheIsraeli-PalestinianInterimAgreementontheWestBankandtheGazaStrip(“Oslo2”—9/28/95),Article36

6Allsourcesandreferencearelistedattheendofthenote,section“ReferencesandSources.”7Todoso,theMTIT,amongothermeans,“issueslicensestosetup,operateandrunprivatetelecommunicationsnetworksandstatesnecessaryconditionsofauthorizationsandmakethempublic”and“statesstandard,foundationsandratestodesignatepricesprovidedbythelicensee”(PALaw3/1996,Art.7).OneofthefirstactionsofthePAconsistedinawardingalicencetoPalestineTelecommunicationsCompany(Paltel)whichhasmadeverysolidprogressindevelopingthefirstPalestinianfixed-linecommunicationsnetwork(seesections§3.2)andthefirstPalestinianmobilenetwork.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

15

DespitethedraftingofanewLawonTelecommunicationsandthePAStatement2010,therehasbeennoprogressonthecreationofthePTRA(seeinfra§4.1.2).

TheOsloagreement leaves importantregulatoryandtechnicalcoordinationdecisionsbetweenthePAandIsraeliauthoritiesinthehandsofaJointTechnicalCommittee(JTC)gatheringspecialistsfrombothsides to coordinate frequency assignment, importation of telecommunications equipment,telecommunicationactivitiesinareaC,permitstobuildinfrastructure,etc.Inpractice,theJTChasonlymetafewtimessince2000andremainsdysfunctional(cf.infra§4.2.1)

3.2 Fixed-broadband sector assessment

AftertheOsloagreements,thePAawardedinNovember1996thefixed-lineincumbentPaltel(PalestineTelecommunications Company) a 20-year license to build, operate and own landlines, datacommunications, paging services, public telephones, satellite communication services, lease lines, selltelecommunicationsequipment(peripheraldevices),Value-AddedServices(VAS)anddeployandoperateamobilenetwork(PSR2013,p.3&19).

Followingtheawardofthe20-yearlicenceinNovember1996,thefixed-lineincumbentPaltelstartedtodeliverfixed-servicesinJanuary1997overaninadequateinfrastructureinheritedfromIsraeliincumbentBezeqmadeofaround80,000lines.Paltelhadtoimmediatelysettoworkonmodernisingandexpandingthenetwork,whilekick-startingwide-rangingplanstoachievecoverageofeveryPalestinianhome.WithinayearofoperationPaltelhadreplacedeveryanaloguelinkonthenetwork,andin1998itcompleteda140kmfibre-opticcablelinkingthemaintownsintheGazaStrip,anda260kmlinkbetweenthecitiesintheWestBank.Amicrowaveconnectionwassubsequently installed, connecting the two transmissionbackbones;however,itquicklybecamesaturated.Today,Paltelprovidesacompleteportfoliooffixedlineservices, with telephony and internet narrowband and broadband (especially leased lines and ADSL).Paltelnowhasfixedcoppernetworkthatcoversmostofthe800,000Palestinianhouseholds,andhasastablesubscriberbaseof400,000PSTNcustomerssince2012(TeleGeography,2015).

For fixed-broadband, almost all customers are served by ADSL lines delivered through Paltel’sinfrastructure.PaltelcreateditsHadarasubsidiaryinFebruary2005–bypurchasingthethreestrongestISPsinthePalestinianterritories–tomanagetheinternetanddatabusiness(WB,2011).Hadaranowactsas Paltel’s Internet Service Provider (ISP) and its current retail market share in volume8 is roughlyestimatedataround50%accordingtoaninvestmentbank(Ramsala,2012),therestbeingheldbyadozencompetingISPs.Theresidentialfixed-broadbandmarketisnowmadeofaround230,000customers(thefixed-broadband penetration per household is thus about 29%). Corporate customers are reached bywireline(copperandfiber)andwirelessinfrastructures;nopublicdataareavailableonmarketshares.

8Marketshareinvolumereferstothetotalnumberofsubscribers.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

16

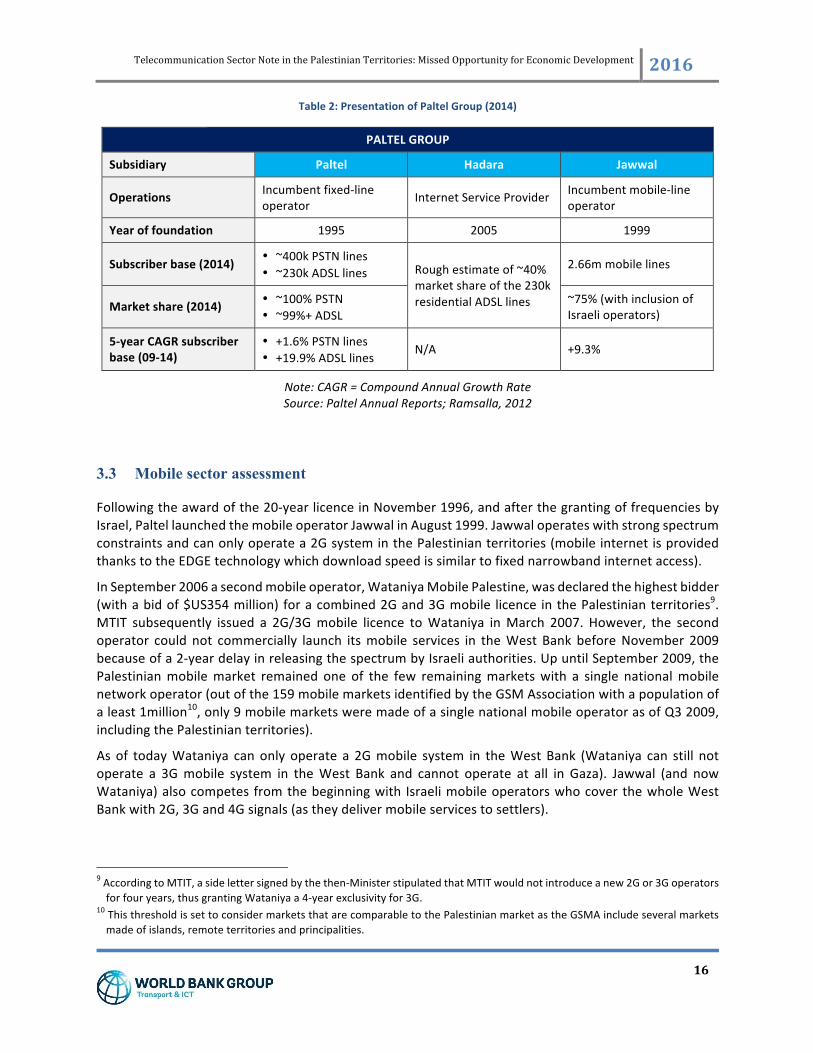

Table2:PresentationofPaltelGroup(2014)

PALTELGROUP

Subsidiary Paltel Hadara Jawwal

Operations Incumbentfixed-lineoperator InternetServiceProvider Incumbentmobile-line

operator

Yearoffoundation 1995 2005 1999

Subscriberbase(2014) • ~400kPSTNlines• ~230kADSLlines Roughestimateof~40%

marketshareofthe230kresidentialADSLlines

2.66mmobilelines

Marketshare(2014) • ~100%PSTN• ~99%+ADSL

~75%(withinclusionofIsraelioperators)

5-yearCAGRsubscriberbase(09-14)

• +1.6%PSTNlines• +19.9%ADSLlines N/A +9.3%

Note:CAGR=CompoundAnnualGrowthRateSource:PaltelAnnualReports;Ramsalla,2012

3.3 Mobile sector assessment

Followingtheawardofthe20-yearlicenceinNovember1996,andafterthegrantingoffrequenciesbyIsrael,PaltellaunchedthemobileoperatorJawwalinAugust1999.Jawwaloperateswithstrongspectrumconstraintsandcanonlyoperatea2GsysteminthePalestinianterritories(mobileinternetisprovidedthankstotheEDGEtechnologywhichdownloadspeedissimilartofixednarrowbandinternetaccess).

InSeptember2006asecondmobileoperator,WataniyaMobilePalestine,wasdeclaredthehighestbidder(withabidof$US354million) foracombined2Gand3Gmobile licence inthePalestinianterritories9.MTIT subsequently issued a 2G/3Gmobile licence toWataniya inMarch 2007. However, the secondoperator could not commercially launch itsmobile services in theWest Bank beforeNovember 2009becauseofa2-yeardelayinreleasingthespectrumbyIsraeliauthorities.UpuntilSeptember2009,thePalestinianmobilemarket remained one of the few remainingmarketswith a single nationalmobilenetworkoperator(outofthe159mobilemarketsidentifiedbytheGSMAssociationwithapopulationofaleast1million10,only9mobilemarketsweremadeofasinglenationalmobileoperatorasofQ32009,includingthePalestinianterritories).

As of todayWataniya canonly operate a 2Gmobile system in theWestBank (Wataniya can still notoperate a 3Gmobile system in theWest Bank and cannot operate at all in Gaza). Jawwal (and nowWataniya)alsocompetes fromthebeginningwith IsraelimobileoperatorswhocoverthewholeWestBankwith2G,3Gand4Gsignals(astheydelivermobileservicestosettlers).

9AccordingtoMTIT,asidelettersignedbythethen-MinisterstipulatedthatMTITwouldnotintroduceanew2Gor3Goperatorsforfouryears,thusgrantingWataniyaa4-yearexclusivityfor3G.

10ThisthresholdissettoconsidermarketsthatarecomparabletothePalestinianmarketastheGSMAincludeseveralmarketsmadeofislands,remoteterritoriesandprincipalities.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

17

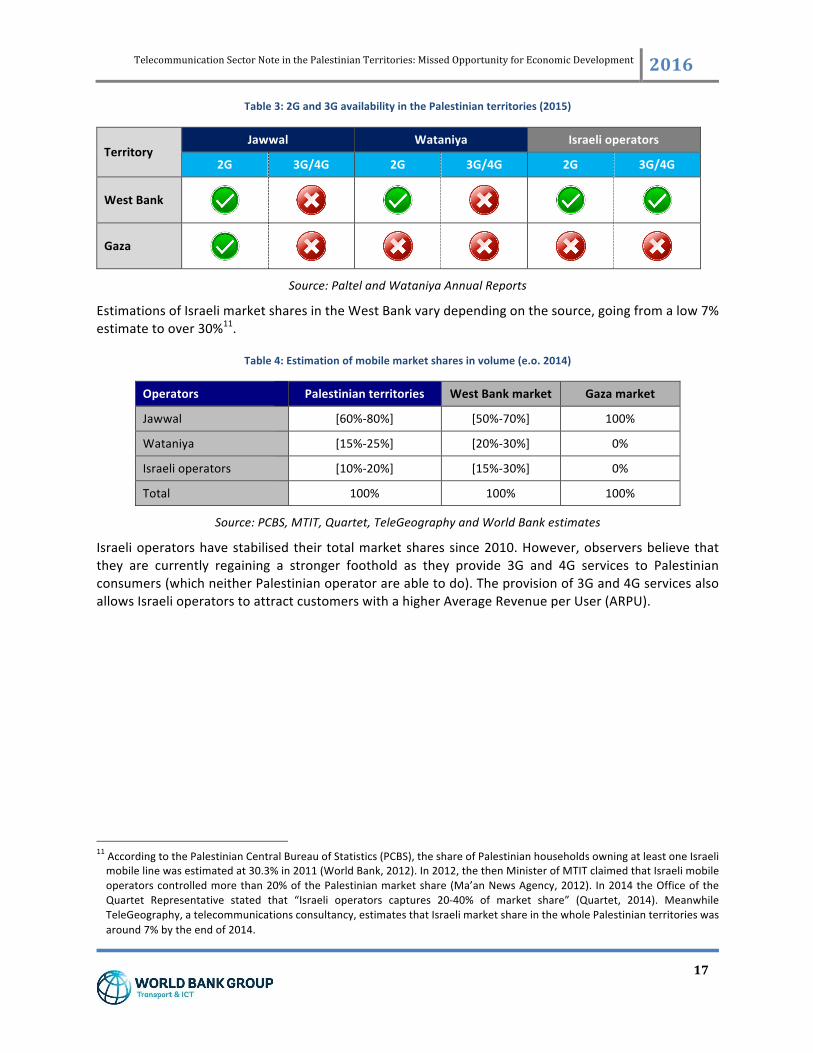

Table3:2Gand3GavailabilityinthePalestinianterritories(2015)

TerritoryJawwal Wataniya Israelioperators

2G 3G/4G 2G 3G/4G 2G 3G/4G

WestBank

Gaza

Source:PaltelandWataniyaAnnualReports

EstimationsofIsraelimarketsharesintheWestBankvarydependingonthesource,goingfromalow7%estimatetoover30%11.

Table4:Estimationofmobilemarketsharesinvolume(e.o.2014)

Operators Palestinianterritories WestBankmarket Gazamarket

Jawwal [60%-80%] [50%-70%] 100%

Wataniya [15%-25%] [20%-30%] 0%

Israelioperators [10%-20%] [15%-30%] 0%

Total 100% 100% 100%

Source:PCBS,MTIT,Quartet,TeleGeographyandWorldBankestimates

Israelioperatorshavestabilisedtheirtotalmarketsharessince2010.However,observersbelievethatthey are currently regaining a stronger foothold as they provide 3G and 4G services to Palestinianconsumers(whichneitherPalestinianoperatorareabletodo).Theprovisionof3Gand4GservicesalsoallowsIsraelioperatorstoattractcustomerswithahigherAverageRevenueperUser(ARPU).

11AccordingtothePalestinianCentralBureauofStatistics(PCBS),theshareofPalestinianhouseholdsowningatleastoneIsraelimobilelinewasestimatedat30.3%in2011(WorldBank,2012).In2012,thethenMinisterofMTITclaimedthatIsraelimobileoperatorscontrolledmorethan20%ofthePalestinianmarketshare(Ma’anNewsAgency,2012). In2014theOfficeoftheQuartet Representative stated that “Israeli operators captures 20-40% of market share” (Quartet, 2014). MeanwhileTeleGeography,atelecommunicationsconsultancy,estimatesthatIsraelimarketshareinthewholePalestinianterritorieswasaround7%bytheendof2014.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

18

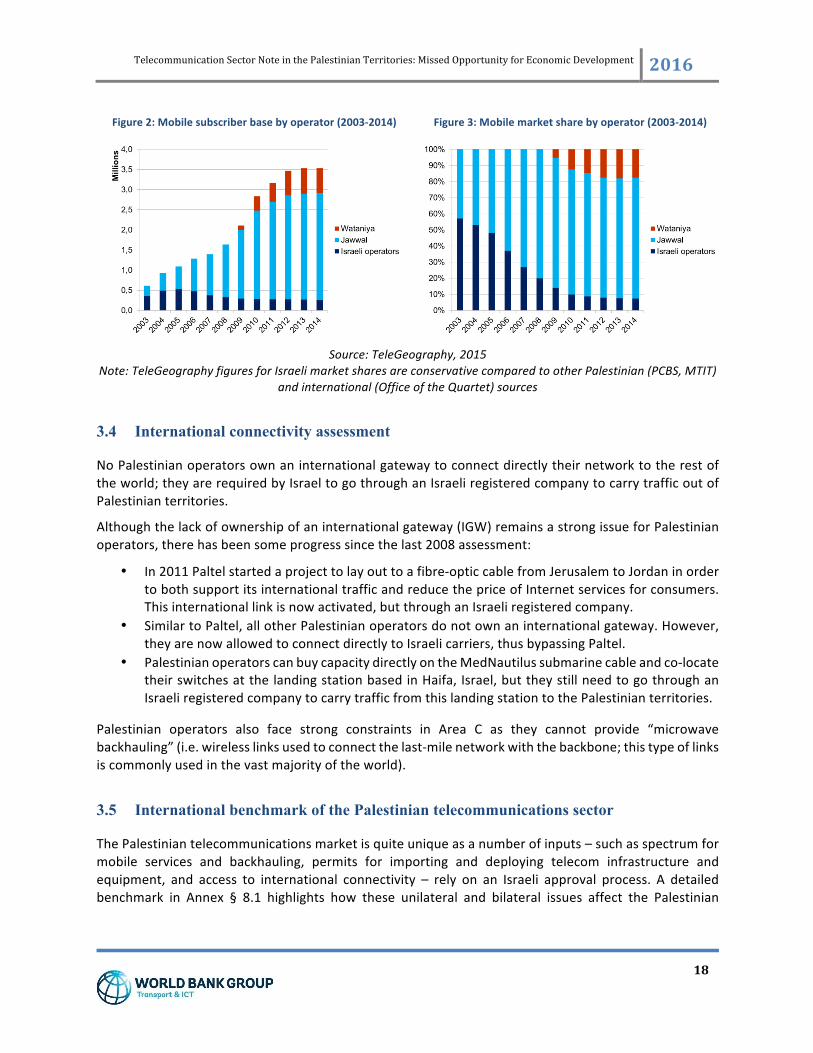

Figure2:Mobilesubscriberbasebyoperator(2003-2014)

Figure3:Mobilemarketsharebyoperator(2003-2014)

Source:TeleGeography,2015

Note:TeleGeographyfiguresforIsraelimarketsharesareconservativecomparedtootherPalestinian(PCBS,MTIT)andinternational(OfficeoftheQuartet)sources

3.4 International connectivity assessment

NoPalestinianoperatorsownaninternationalgatewaytoconnectdirectlytheirnetworktotherestoftheworld;theyarerequiredbyIsraeltogothroughanIsraeliregisteredcompanytocarrytrafficoutofPalestinianterritories.

Althoughthelackofownershipofaninternationalgateway(IGW)remainsastrongissueforPalestinianoperators,therehasbeensomeprogresssincethelast2008assessment:

• In2011Paltelstartedaprojecttolayouttoafibre-opticcablefromJerusalemtoJordaninordertobothsupportitsinternationaltrafficandreducethepriceofInternetservicesforconsumers.Thisinternationallinkisnowactivated,butthroughanIsraeliregisteredcompany.

• SimilartoPaltel,allotherPalestinianoperatorsdonotownaninternationalgateway.However,theyarenowallowedtoconnectdirectlytoIsraelicarriers,thusbypassingPaltel.

• PalestinianoperatorscanbuycapacitydirectlyontheMedNautilussubmarinecableandco-locatetheirswitchesatthelandingstationbasedinHaifa,Israel,buttheystillneedtogothroughanIsraeliregisteredcompanytocarrytrafficfromthislandingstationtothePalestinianterritories.

Palestinian operators also face strong constraints in Area C as they cannot provide “microwavebackhauling”(i.e.wirelesslinksusedtoconnectthelast-milenetworkwiththebackbone;thistypeoflinksiscommonlyusedinthevastmajorityoftheworld).

3.5 International benchmark of the Palestinian telecommunications sector

ThePalestiniantelecommunicationsmarketisquiteuniqueasanumberofinputs–suchasspectrumformobile services and backhauling, permits for importing and deploying telecom infrastructure andequipment, and access to international connectivity – rely on an Israeli approval process. A detailedbenchmark in Annex § 8.1 highlights how these unilateral and bilateral issues affect the Palestinian

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

19

market,whilekeepinginmindthatdomesticissuesarealsohinderingthedevelopmentofthetelecomsector:

• ThepenetrationofPalestinianmobileservicesislowerthaninothersimilarmarkets,whereasthefixedbroadbandpenetrationisintheaverage;

• RetailpricesofmobileandfixedservicesarehigherinthePalestinianterritoriesarehigherthaninsimilarmarketswhentakingintoaccounteitherthePurchasingPowerParityortheGDPpercapita.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

20

4 Telecom sector achievements and issues Note: all achievements and issues are largely common between the Palestinian territories; for issuesspecifictoGazathereisadedicatedsectionattheend.

4.1 Domestic achievements and issues

4.1.1 Main Policy and Regulatory achievements

Introductionofasecondmobileoperator

TheawardofasecondmobilelicensetoWataniyaisapositivesteptowardsenhancingcompetitioninthemobilemarket,thoughthenarrowspectrumwasawardedtoWataniyawitha2-yeardelayandthenewentrantcontinuestofacesignificantspectrumconstraints,inabilitytodeploy3G,andinabilitytooperateinGaza.TheincumbentJawwalalsofacessignificantspectrumconstraintsbutisabletooperateinGazawhereitisthedefactomobilemonopolyoperator.

Enhancementofthefixedwholesalemarket

Afterthepublicationofthe2010TelecommunicationsPolicy(PAStatement,2010),MTITpushedformorecompetitionbyenhancingthewholesalemarket,whichatthattimeconsistedintheabilityofISPstoresellPaltelbroadbandlinesontheretailmarket.TwomainmeasureswereimplementedbyMTITtothisend:

1. MTITandPaltelworkedtogethertosetupanewBitstreamServiceAccess(BSA)anda“Bit-StreamAccess–ModelDescription”paperwaspublished inOctober2010byMTIT (MTITBSA,2010).However, the bitstream service offered by Paltel is not as fully functional as the standardbitstreamencounteredinothercountries;theend-userisrequiredtosubscribetoabroadband(ADSL)linetoPaltel,andthenaddanInternetaccessserviceontopofit(aschemesometimesreferred toas “doublebilling”). TheBSAoffer is also restrictiveasADSL technology limits thecapabilitiesofISPstoprovidebroadbandtocorporatecustomers.

2. MTITprovidedatemporarypermissiontotheJerusalemDistrictElectricityCompany(JDECO)todeploy fibre for smart metering; JDECO has now deployed around 380km of fibre along itselectrical lines. Its telecom subsidiary needs a license in order to provide access to its fibrenetworkinanon-discriminatoryfashiontotelecomoperators.

ISPs also have developed their own fibre infrastructure and fixed-wireless infrastructure to deliverbroadbandandVoIP,mainlytoprofessionalandcorporatecustomers12.

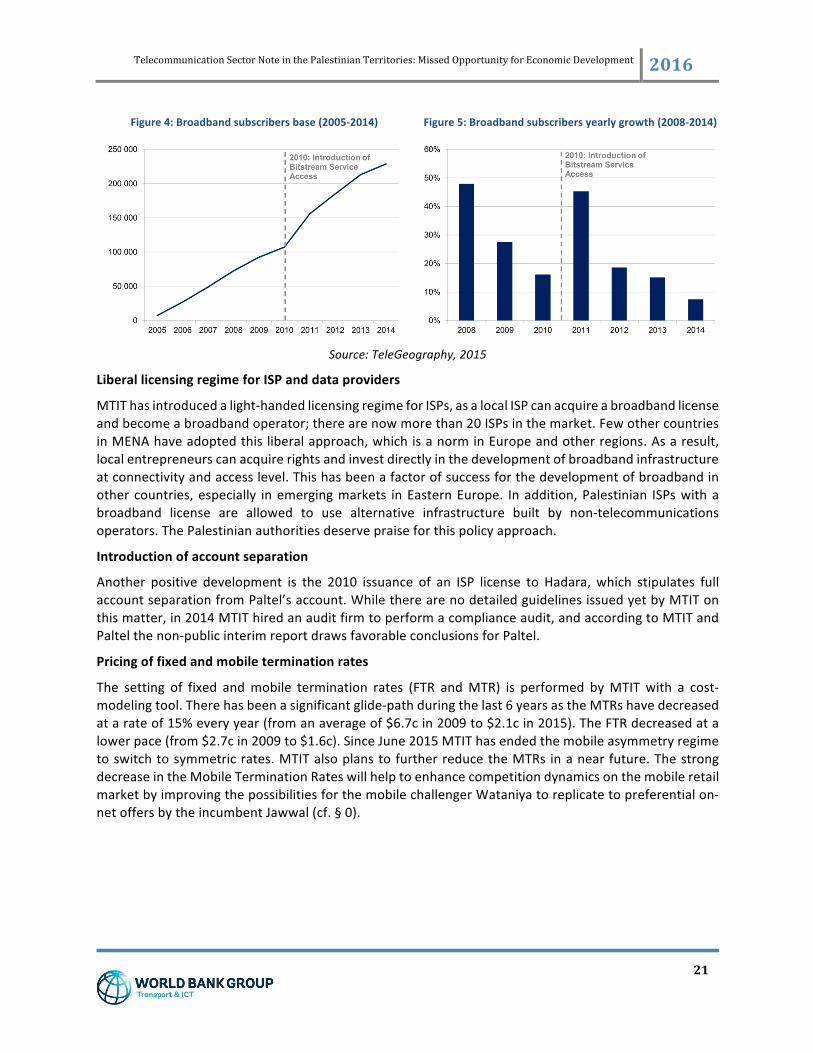

The introductionBSA in 2010 led to a significant increase in broadband subscription as shown in thefiguresbelow,andin2015Paltellistedatotalof17ISPsofferingservicesundertheBSAmodel,excludingitssubsidiaryHadara;ofthose,tenwereoperatingsolely intheWestBank,sixwereoperatingonly inGaza,withoneservingbothregions(TeleGeography,2015).

12 In2008MTITopened the internetandVoIP services for competitionand8broadbandand8VoIP serviceproviderswerelicensed.MTITalsointroducedcompetitionontheValueAddedServicesmarketandWiFimarket.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

21

Figure4:Broadbandsubscribersbase(2005-2014)

Figure5:Broadbandsubscribersyearlygrowth(2008-2014)

Source:TeleGeography,2015

LiberallicensingregimeforISPanddataproviders

MTIThasintroducedalight-handedlicensingregimeforISPs,asalocalISPcanacquireabroadbandlicenseandbecomeabroadbandoperator;therearenowmorethan20ISPsinthemarket.FewothercountriesinMENAhaveadoptedthisliberalapproach,whichisanorminEuropeandotherregions.Asaresult,localentrepreneurscanacquirerightsandinvestdirectlyinthedevelopmentofbroadbandinfrastructureatconnectivityandaccesslevel.Thishasbeenafactorofsuccessforthedevelopmentofbroadbandinother countries,especially inemergingmarkets inEasternEurope. Inaddition,Palestinian ISPswithabroadband license are allowed to use alternative infrastructure built by non-telecommunicationsoperators.ThePalestinianauthoritiesdeservepraiseforthispolicyapproach.

Introductionofaccountseparation

Another positive development is the 2010 issuance of an ISP license to Hadara, which stipulates fullaccountseparationfromPaltel’saccount.WhiletherearenodetailedguidelinesissuedyetbyMTITonthismatter,in2014MTIThiredanauditfirmtoperformacomplianceaudit,andaccordingtoMTITandPaltelthenon-publicinterimreportdrawsfavorableconclusionsforPaltel.

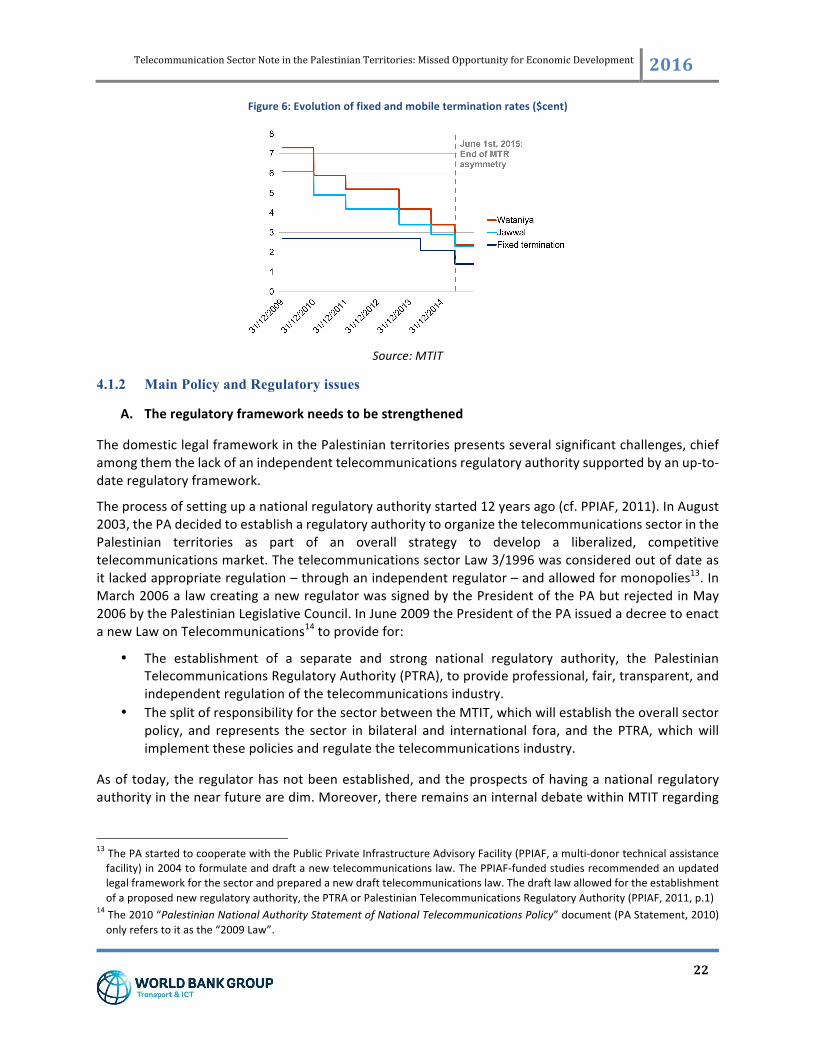

Pricingoffixedandmobileterminationrates

The setting of fixed andmobile termination rates (FTR andMTR) is performed byMTITwith a cost-modelingtool.Therehasbeenasignificantglide-pathduringthelast6yearsastheMTRshavedecreasedatarateof15%everyyear(fromanaverageof$6.7cin2009to$2.1cin2015).TheFTRdecreasedatalowerpace(from$2.7cin2009to$1.6c).SinceJune2015MTIThasendedthemobileasymmetryregimetoswitchtosymmetricrates.MTITalsoplanstofurtherreducetheMTRs inanearfuture.ThestrongdecreaseintheMobileTerminationRateswillhelptoenhancecompetitiondynamicsonthemobileretailmarketbyimprovingthepossibilitiesforthemobilechallengerWataniyatoreplicatetopreferentialon-netoffersbytheincumbentJawwal(cf.§0).

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

22

Figure6:Evolutionoffixedandmobileterminationrates($cent)

Source:MTIT

4.1.2 Main Policy and Regulatory issues

A. Theregulatoryframeworkneedstobestrengthened

ThedomesticlegalframeworkinthePalestinianterritoriespresentsseveralsignificantchallenges,chiefamongthemthelackofanindependenttelecommunicationsregulatoryauthoritysupportedbyanup-to-dateregulatoryframework.

Theprocessofsettingupanationalregulatoryauthoritystarted12yearsago(cf.PPIAF,2011).InAugust2003,thePAdecidedtoestablisharegulatoryauthoritytoorganizethetelecommunicationssectorinthePalestinian territories as part of an overall strategy to develop a liberalized, competitivetelecommunicationsmarket.ThetelecommunicationssectorLaw3/1996wasconsideredoutofdateasitlackedappropriateregulation–throughanindependentregulator–andallowedformonopolies13.InMarch2006alawcreatinganewregulatorwassignedbythePresidentofthePAbutrejectedinMay2006bythePalestinianLegislativeCouncil.InJune2009thePresidentofthePAissuedadecreetoenactanewLawonTelecommunications14toprovidefor:

• The establishment of a separate and strong national regulatory authority, the PalestinianTelecommunicationsRegulatoryAuthority(PTRA),toprovideprofessional,fair,transparent,andindependentregulationofthetelecommunicationsindustry.

• ThesplitofresponsibilityforthesectorbetweentheMTIT,whichwillestablishtheoverallsectorpolicy, and represents the sector in bilateral and international fora, and the PTRA,whichwillimplementthesepoliciesandregulatethetelecommunicationsindustry.

Asoftoday,theregulatorhasnotbeenestablished,andtheprospectsofhavinganationalregulatoryauthorityinthenearfuturearedim.Moreover,thereremainsaninternaldebatewithinMTITregarding

13ThePAstartedtocooperatewiththePublicPrivateInfrastructureAdvisoryFacility(PPIAF,amulti-donortechnicalassistancefacility)in2004toformulateanddraftanewtelecommunicationslaw.ThePPIAF-fundedstudiesrecommendedanupdatedlegalframeworkforthesectorandpreparedanewdrafttelecommunicationslaw.Thedraftlawallowedfortheestablishmentofaproposednewregulatoryauthority,thePTRAorPalestinianTelecommunicationsRegulatoryAuthority(PPIAF,2011,p.1)

14The2010“PalestinianNationalAuthorityStatementofNationalTelecommunicationsPolicy”document(PAStatement,2010)onlyreferstoitasthe“2009Law”.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

23

therevampingof theregulatory frameworkonwhether it shouldcompriseaseparatenew law,oranamendmenttotheexistingTelecommunicationsLaw(PPIAF,2011,p.2).

The establishment of an independent regulatory authority would provide a strong catalyst for theenhancement of the Palestinian telecommunication markets. According to 2013 data from theInternationalTelecommunicationUnion(ITU),159ofits194memberstates(82percent)haveaseparateICTregulatoryagency.Thisreportstillstronglyadvocatestheneedtoestablishanindependentauthority.

ThecreationofthePTRAwouldhelptoresolveseverallegalandinstitutionalissuesaffectingthesector,including:

• enhancing regulatory framework to handle market observatory, market definition, SMP,remedies,monitoringandsanctionsandenforcement;

• enforcementofReferenceInterconnectionOfferstoprovideamoredynamic,transparentnon-discriminatoryandcost-orientedwholesalemarket.

• Thelackofanexpostcompetitionauthority(asopposedtoanexanteregulatoryauthority)tomonitorandapprovepotentialmergers15andpreventpotentialanti-competitivebehaviors.

B. DominanceofPaltelGroup

AbodyofevidencepointstoPaltelbeingthedominantoperatorinboththemobileandfixedmarkets16:

• Fixedwholesalemarket:o Paltel fullyowns the fixed-infrastructure,whichcanbeconsideredanessential facility

withthecivilengineering(trenches,ductsandpoles)andthecopperlocalloop;o Forresidentialcustomers,thereisnoLocalLoopUnbundling,andtheBitstreamService

Access BSA consists in end-users having to subscribe to an ADSL line to Paltel beforesubscribingtoanISPtoaccesstheInternet.ThissignificantlylimitsthecommercialandtechnicalfreedomofISPs;

o Forprofessionalandcorporatecustomers,thereisnowholesaleofferavailabletoaddressthislucrativesegment.

• Fixedretailmarket:PaltelGrouphasastrongandstablemarketshareinvolume(around50%)duetoitssubsidiaryHadara.

15The2011WorldBankreport“WestBankandGaza,ImprovingGovernanceandReducingCorruption”states:“PaltelalsocreatedHadara, bypurchasing the three strongest ISPs inWB&G. In this process,Hadaraandother ISPsbecame resellers ofADSLprovided by Paltel. The creation ofHadara, in fact, should have been reviewed byMTIT froma competition standpoint todeterminewhetherPaltel–withcontrolover infrastructure–shouldhavebeenallowedsuchdominance in the ISPmarket.However, according toMTIT, theagreement in the licensegavePaltel the exclusive rights toprovideall telecoms services,includingISP,andthisrestrictedtheministry’sabilitytointerveneinthisissue.”(WorldBank,2011,p.39)

16ConductingaproperSignificantMarketPower(SMP)regulatoryassessmentisoutofscopeofthisnote;formoredetailsonthemethodologythereadermayrefertoEuropeanCommission,CommissionguidelinesonmarketanalysisandtheassessmentofsignificantmarketpowerundertheCommunityregulatoryframeworkforelectroniccommunicationsnetworksandservices(2002/C165/03),11July2002.Asmentionedina2011WorldBankreportonImprovinggovernanceandreducingcorruptionin West Bank and Gaza, “for the past 15 years, Paltel, which includes companies in all the main sectors of thetelecommunicationsandinformationtechnology(IT)market,hasdominatedtheICTsector.Itcontrolsahighmarketshareinallrelevantmarketsegmentsandistheonlycompanyabletooperateinawiderangeofsegments”(WorldBank,2011).

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

24

• Mobile retail market: Paltel: Paltel Group has a strong and stable market share in volume(between75%whenincludingIsraelimobileoperatorsand81%whenexcludingthem)duetotoitssubsidiaryJawwal.IthasnocompetitorsyetinGaza.

• Cross-sectorleveraging:PaltelGroupisaprivatelyowned,verticallyintegratednetworkoperator,with Paltel as the fixed line operator, Jawwal themobile operator, Hadara the data servicesprovider,Hulul the ITarm,Palmedia themultimedia servicesproviderandReach the first callcenter17. As Paltel stated it in its 2013 annual report, “Paltel Group plays a vital role in thePalestinianeconomy,astheGroupcontributestoabout5.9%ofGDP(PCBS,2013).TheGroupisalsoconsideredthe leadingemployer inPalestinewithin thePalestinianprivatesector.PALTELstockalso represents33.16%of the totalPalestineExchangemarket cap,according tomarketdataasendof2013”(PaltelGroup,2013).

Basedonextensiveinterviewswithoperators,thecreationofthePTRAwouldmitigatetheriskofanti-competitivepracticesbyPaltel,whocouldleverageitsdominanceonthePalestinianwholesaleandretailtelecomsmarkets(monitoringdominanceisusuallypartofthemandateofaregulatoryauthority).Thecompetitorsidentifythreepotentialanti-competitivepractices(detailsareprovidedintheBoxbelow):i)limited access to Paltel’s infrastructure, ii) differentiated price for “on-net/off-net” and iii) cross-subsidizedfixedbroadbandandmobileservices.Althoughseveralcompetitorsmentionedthesepractices,assessingtheirexistenceandimpactisoutofscopeofthisNote.ThisNotedoeshoweveridentifythelackofaregulatoryagencywiththeproperframework,capabilitiesandtoolstodealwiththem.

PotentialmarketconductsthatcouldbeinvestigatedbythePTRA

Based on extensive discussion with several Palestinian operators, the PTRA could investigate at least threepractices,andassesstowhichextenttheyinduceanti-competitiveeffectsorprovidebenefitstotheconsumers.

LimitedaccesstoPaltel’sinfrastructureinthefixed-broadbandmarket

Third-partyISPsdonothaveopen,transparentandnon-discriminatoryaccesstoPaltel’sinfrastructure;thereisnoReferenceInterconnectionOffer(RIO),oracataloguepricelist.WhencompetingISPsdohaveaccesstoPaltel’sfixed infrastructure, the contractual conditions do not allow for strong and commercial freedom. As aconsequence, ISPs claim that they are better off by deploying their own fiber infrastructure, which impliesinefficient infrastructure duplication. Even though MTIT introduced Bitstream Service Access in 2010 thatimprovedthebroadbandpenetration,end-usersarerequiredtosubscribetoabroadbandlinetoPaltelbeforeselecting an ISP to provide the Internet access; there is no local loop unbundling planned at this stage. Asmentionedintheaforementioned2011WorldBankreport,anotheranti-competitivebehaviorisa“processof‘cherrypicking’majorinstitutions,whichwerereceivingleased-lineservicesfromtheexistingISPs,andprovidingtheservicesatacheapercost,whichwaspossibleduetotheirownershipoftheinfrastructure;andtheofferofsubscriptionfreeinternetservice,aprocesscarriedoutinamannerthatmarginalizedexistingISPsasthemainservice providers” (World Bank, 2011). Such anti-competitive risk would require an extensive regulatory andcompetitionassessment.Intheinterim,fibreinfrastructureisvisiblydeployedintheWestBankbycompetingISPs:thisraisesadoublequestionofeconomicefficiencyandeconomicrationalityascompetingISPsconsideritmorecost-effectivetoduplicatethefixedinfrastructureratherthanaccessPaltel’sinfrastructure.

“On-net/off-net”pricedifferentiationinthemobilemarket

“On-net/off-net”pricedifferentiation impliesthat“on-netcalls” (callsmadewithinthenetworkofthemobileoperator)arecheaperthan“off-netcalls”(callsmadetoarivalmobilenetwork).AnevidenceofthispracticecanbefoundintheAlphaInternationalsurveythatshowsthat71.7%ofPalestinianrespondents“agreethatthey

17PaltelalsoownsequityinVTelHoldings,aDubai-basedtelecommunicationsfirm.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

25

limittheirphonecallstomobileorfixedphonesofanothernetworkoperatorbecausetheyareconcernedwiththehighercommunicationchargesthanwhenmakingaphonecalltoothersonthesamenetworkoperator.”Whileatfirstsightsuchoffersappeartobemarketingtacticsbymobileoperators,theyhaveasignificantimpactonthemobilemarketstructurebyfavoring“big”operatorswithhighmarketshares,tothedetrimentofnewentrants(formoredetailsontheeconomicdemonstrationseeFrenchAutoritédelaConcurrence,2012).Although“on-net/off-net” price differentiationmay induce an anticompetitive effect, they can be objectively justified by adifferencebetweenthecostsborneforthesupplyofthetwotypesofcalls(thechiefreasonbeinganasymmetryin the call termination rates). The end of termination rate asymmetry and the glide path to lower mobileterminationratesisagoodstepinthisrespect.

Cross-subsidyoffixedandmobileservices

CompetitorstoPaltelinthefixedandmobilemarketmentiontheriskthatPaltelisusingitsdominantpositiontoperformcross-subsidiesbetweenitsdifferentbusinessunits,makingitdifficultforWataniyaandotherISPstocompete.Performingcross-subsidiesbetweendifferentsubsidiariescanprovidebenefitsfortheconsumers,butcanalsoforeclosethemarketforcompetitors.Thisshouldbesortedoutthroughtheenforcementofaccountingseparation to ensure a fair competition between Paltel’s different subsidiaries and competitors.Note: Cross-subsidisingshouldnotbeconfusedwithbundlingfixedandmobileservicesinasinglepackage,acommonpracticeintendedtoprovidecustomerswithbetterproductsorofferingsinmorecosteffectiveways.CurrentlyPaltelisnotauthorizedtoprovidebundles.

C. Otherregulatoryandmarketissues

Otherregulatoryissuesshouldbeaddressedtostrengthencompetition.MobileNumberPortability(MNP)isnotimplemented;thisisanimportantmeasuretoallowWataniyatocompetewithPaltelandattractcustomers that arewilling to switchoperatorbut fear the lossof theirmobilenumber.Anadditionalmeasure to foster competition is ensuringpublic and fully competitive tenders to providebroadbandservicestoPalestinianministries.

4.1.3 Institutional capacity at the Ministry

AccordingtoMTIT,aftertheseparationofGazalate2007,MTITdidnothaveenoughqualifiedemployeesinWestBankasalltheengineersandexecutiveswereinGazaatthattime.Sincethattime,MITasstartedapolicyofrecruitmentofqualifiedstaffinthetechnical,legal,Policyandregulation,andadministrativefieldtoleadthetelecommunicationssectorinPalestinianterritories.

MTIT has currently around 322 employees, and most of them (209) are employed by the postaldepartment.113employeesworkinthefieldofICT,including20qualifiedengineers18.MTITemployeesparticipateininternationalandregionalorganizations,suchasITU,ESCWA,EMERG,andUFM19.Anew,IT-enabled, licensing system has been introduced and a new headquarters, including an advanced ITtrainingcenterhasbeenintroduced,inpartnershipwithforeignaidfromKoreaandEstonia.DespitetheeffortsundergonebyMTITtoattractcompetentpersonnel,itstillsuffersfromlackofqualifiedICTstaff–suchasengineersandlegalexperts.

18AsapointofcomparisonMTIThadonly11engineersin2008.19Participationsinsuchorganizationsareservingasaplatformforknowledgeexchangeandtechnicalcapacitydevelopment,mainlythroughtheexpertgroupworkshops,thetrainingprograms,andtheexchangeofideasandexpertise.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

26

4.2 Domestic and bilateral achievements and issues

4.2.1 Bilateral framework

TheframeworkgoverningPalestinian-IsraelibilateralarrangementsontelecommunicationsistheOsloAccordof1993,specificallyArticle36ofAnnexIIIoftheInterimAgreementonTelecommunications20(e.g.ArticlesB.6,C.2,D2).Thisframework,thereferenceagreementbetweentheIsraeliandPalestiniancounterparts to support economic development and stability in key economic sectors, has failed todeliveritspromiseofanindependenttelecommunicationssectorinthePalestinianterritories.AccordingtotheprinciplesoftheOsloAgreement:“IsraelrecognizesthatthePalestiniansidehastherighttobuildand operate separate and independent communication systems and infrastructures includingtelecommunicationnetworks,atelevisionnetworkandaradio.”

In 2008, theWorld Bank study on the Palestinian telecommunications sector found that the existingconflicthurtstheworkofOslo’sJointTechnicalCommittee(JTC)toimplementtheprovisionsunderthetelecommunicationssectionsoftheOsloAgreement,thattheJTChadmetonlytwicesince2000fortwoperfunctorymeetingsin2004,andhadleftimportantissuesunresolved.The2008studyrecommendedthat “the structured negotiations mechanism of the JTC (which deals with mutual coordination offrequenciesuse,interferenceproblems,diverseinternationalissues,andothersensitivesubjectsofmutualimportance),shouldbesupportedandencouragedinthefuture.”

In2015,Oslocontinuestobeadejurevalidbutdefactolargelynon-operationalframeworkcapturedbypoliticalagendasandunabletodeliverthebasicrequirementsof:

1. regularandformalizeddialoguebetweentheIsraeliandPalestiniansides;2. jointagreements,decisionmakingandimplementationinatime-sensitivemannersuitablefora

rapidlyevolvingsector;and3. effective resolutionof challengesbrought to the tablebyeither side,while takingboth sides’

concernsintoaccount.

The instrument for such discussion was mandated to be the JTC composed of the Israeli MoC, thePalestinianMTIT and COGAT with occasional observers. JTC was intended to be themain forum fordialogueandagreements,butislargelydefunct.JTCmeetingsaretoofewandfarbetween;whenthisanalysis was conducted in May 2015, the previous JTC meeting had been held in March 2014. ThePalestiniancounterpartswould like to schedule regularmeetingsof the JTC, coherentlywith theOsloAgreement. However, by Israeli accounts, the JTC stopped meeting after Palestinian politiciansapproached variousUN agencieswith the request for state recognition or for technical assistance. ApoliticaldecisionwasmadeinIsraeltopausetheJTCmeetingsasIsraeliauthoritiesconsideredthatthecounterpartwasactivelyseekingsolutionsoutsideoftheOsloframework.

3GspectrumallocationforthePalestinianterritorieshasbeeninastalemateholdingpatterneversince,whichisclearlydetrimentaltothePalestinianeconomy(seenextsection).PotentiallyencouragingisthatneitherIsraelinorthePalestinianofficialsinterviewedwouldcallOslo‘obsolete’or‘dead’–bothsides

20Cf.Article36ofAnnexIIIoftheInterimAgreement“OsloAccords”–Telecommunications.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

27

agreedthatuntilapoliticalstatementwasmadepertainingtothismatter,Oslowasdejureintactandcouldberevived21.

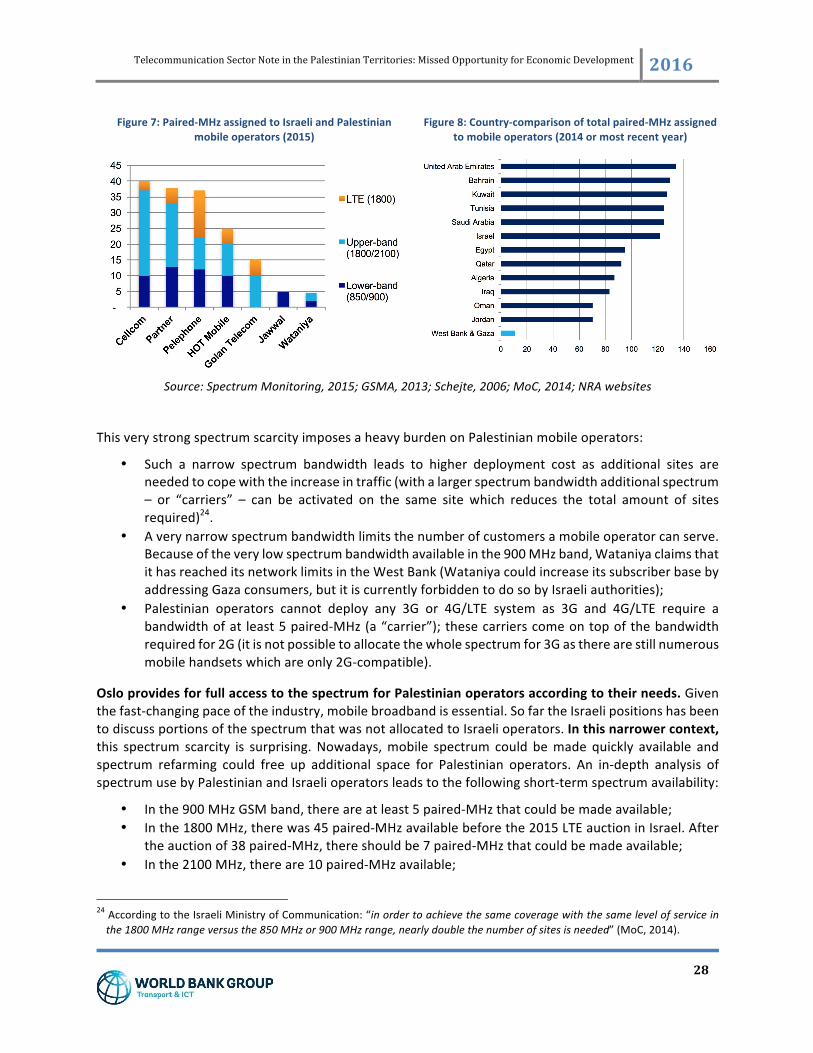

4.2.2 Acute spectrum scarcity for Palestinian mobile operators

Per the Article 36 of Annex III of the Interim Agreement, total control of the Palestinian frequencyspectrumwasgiven to Israelprovided that Israelwould releasespectrumto thePalestinianAuthoritywhenneededandwithinonemonthofrequest.HoweverthishasnotbeenthecaseandtodaythetwoPalestinianoperatorsholdatotalof9.4paired-MHz22:4.8MHzforJawwalinthe900MHzbandand4.6MHzforWataniya–with1.8MHzinthe900MHzbandand2.8MHzinthe1800MHzband–.Thisisinstarkcontrastwiththe121.6paired-MHzcurrentlyallocatedtofivemobileoperators in Israel(andanauction inJanuary2015awardedanadditional38paired-MHzfor4G/LTE),withthe5thmobile licenceawardedtoGolanTelecominApril2011.

The amountof frequencies that themobile operator receives is important because it determines thenumberofsubscribersthecompanycanserviceandthekindsofservicesitcanprovide.Moreover,lowerbandfrequencies(800and900MHzband)havebetterpropagationcharacteristicsandcantravelfartherandpenetratewallsbetter,andarethusmoredesirablethanhigherbandfrequencies(1800MHz,2100MHzand2600MHz).Withonly4.6paired-MHzdistributedbetweenthe900MHzbandand1800MHzband,Wataniyaisaco-holderofaworld-recordwithaBulgarianoperator(Mobiltel)asnoothermobileoperatorintheworldstarteditsoperationswithsuchanarrowfrequencyrange23(TheEconomist,2010).

21 Israeliofficial stated theremightbe readiness to reconvene talksonoutstanding issues through the JTC.PalestiniansalsoindicatedreadinesstoreboottheJTCprocess.However,Israel’spositionisthatithopesthePAwillrecognizethatunilateralstepsontheworldstage,suchasapproachingUNagenciestorecognizeaPalestinianstate(whichIsraelseesinviolationoftheagreed-uponmechanisms) are no substitute for working ties. Palestinians are frustrated by years of stalemates andmaycontinue to turn to international agencies for technical and political support. Political maneuvering is therefore likely tocontinue to capture the potential progress that necessary regular and timely discussions could provide, producing anunnecessarystalematethatisharmingPalestinianbusinessesandconsumers.

22Alsoknownas“MHzduplex”of“MHzFDD”,wherebyalowerbandisusedfortheuplinkpathandthe(paired)upperbandisusedforthedownlinkpath.

23MobiltelBulgariawaslaterawarded19.4paired-MHz.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

28

Figure7:Paired-MHzassignedtoIsraeliandPalestinianmobileoperators(2015)

Figure8:Country-comparisonoftotalpaired-MHzassignedtomobileoperators(2014ormostrecentyear)

Source:SpectrumMonitoring,2015;GSMA,2013;Schejte,2006;MoC,2014;NRAwebsites

ThisverystrongspectrumscarcityimposesaheavyburdenonPalestinianmobileoperators:

• Such a narrow spectrum bandwidth leads to higher deployment cost as additional sites areneededtocopewiththeincreaseintraffic(withalargerspectrumbandwidthadditionalspectrum– or “carriers” – can be activated on the same site which reduces the total amount of sitesrequired)24.

• Averynarrowspectrumbandwidthlimitsthenumberofcustomersamobileoperatorcanserve.Becauseoftheverylowspectrumbandwidthavailableinthe900MHzband,WataniyaclaimsthatithasreacheditsnetworklimitsintheWestBank(WataniyacouldincreaseitssubscriberbasebyaddressingGazaconsumers,butitiscurrentlyforbiddentodosobyIsraeliauthorities);

• Palestinian operators cannot deploy any 3G or 4G/LTE system as 3G and 4G/LTE require abandwidthofat least5paired-MHz(a“carrier”);thesecarrierscomeontopofthebandwidthrequiredfor2G(itisnotpossibletoallocatethewholespectrumfor3Gastherearestillnumerousmobilehandsetswhichareonly2G-compatible).

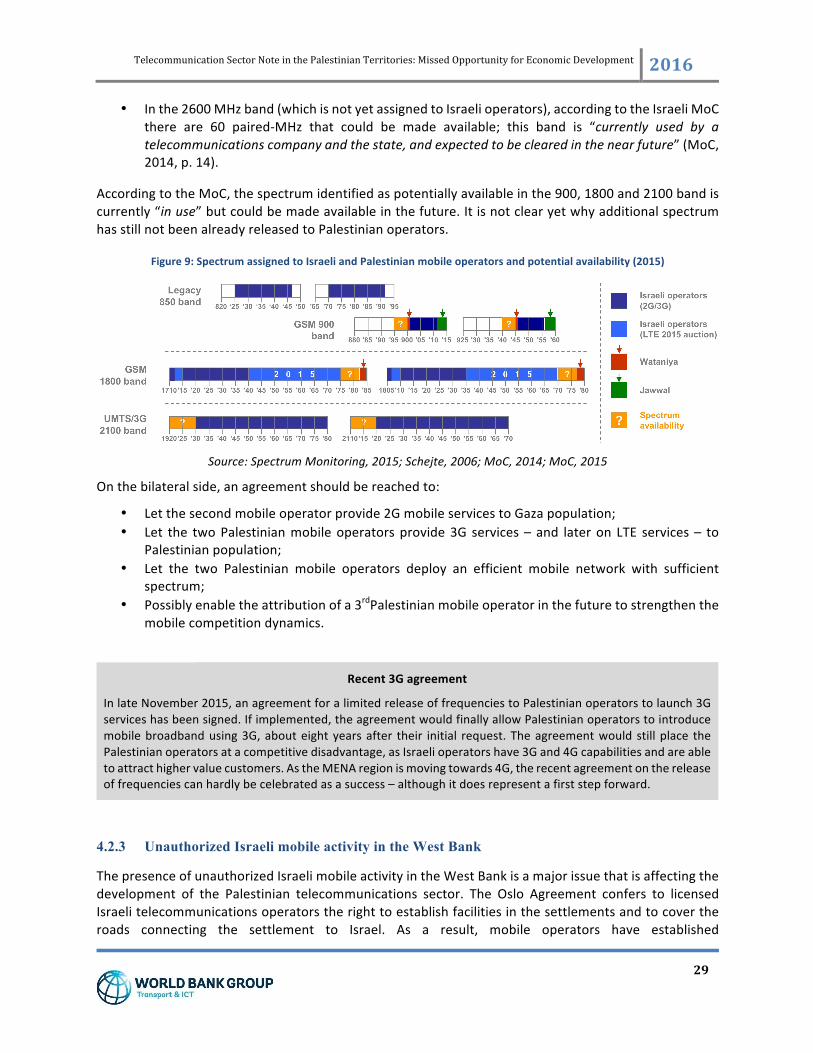

OsloprovidesforfullaccesstothespectrumforPalestinianoperatorsaccordingtotheirneeds.Giventhefast-changingpaceoftheindustry,mobilebroadbandisessential.SofartheIsraelipositionshasbeentodiscussportionsofthespectrumthatwasnotallocatedtoIsraelioperators.Inthisnarrowercontext,this spectrum scarcity is surprising.Nowadays,mobile spectrum could bemade quickly available andspectrum refarming could free up additional space for Palestinian operators. An in-depth analysis ofspectrumusebyPalestinianandIsraelioperatorsleadstothefollowingshort-termspectrumavailability:

• Inthe900MHzGSMband,thereareatleast5paired-MHzthatcouldbemadeavailable;• Inthe1800MHz,therewas45paired-MHzavailablebeforethe2015LTEauctioninIsrael.After

theauctionof38paired-MHz,thereshouldbe7paired-MHzthatcouldbemadeavailable;• Inthe2100MHz,thereare10paired-MHzavailable;

24AccordingtotheIsraeliMinistryofCommunication:“inordertoachievethesamecoveragewiththesamelevelofserviceinthe1800MHzrangeversusthe850MHzor900MHzrange,nearlydoublethenumberofsitesisneeded”(MoC,2014).

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

29

• Inthe2600MHzband(whichisnotyetassignedtoIsraelioperators),accordingtotheIsraeliMoCthere are 60 paired-MHz that could be made available; this band is “currently used by atelecommunicationscompanyandthestate,andexpectedtobeclearedinthenearfuture”(MoC,2014,p.14).

AccordingtotheMoC,thespectrumidentifiedaspotentiallyavailableinthe900,1800and2100bandiscurrently“inuse”butcouldbemadeavailableinthefuture.ItisnotclearyetwhyadditionalspectrumhasstillnotbeenalreadyreleasedtoPalestinianoperators.

Figure9:SpectrumassignedtoIsraeliandPalestinianmobileoperatorsandpotentialavailability(2015)

Source:SpectrumMonitoring,2015;Schejte,2006;MoC,2014;MoC,2015

Onthebilateralside,anagreementshouldbereachedto:

• Letthesecondmobileoperatorprovide2GmobileservicestoGazapopulation;• Let the twoPalestinianmobileoperatorsprovide3G services– and lateron LTE services– to

Palestinianpopulation;• Let the two Palestinian mobile operators deploy an efficient mobile network with sufficient

spectrum;• Possiblyenabletheattributionofa3rdPalestinianmobileoperatorinthefuturetostrengthenthe

mobilecompetitiondynamics.

Recent3Gagreement

InlateNovember2015,anagreementforalimitedreleaseoffrequenciestoPalestinianoperatorstolaunch3Gserviceshasbeensigned.Ifimplemented,theagreementwouldfinallyallowPalestinianoperatorstointroducemobilebroadbandusing3G,abouteightyearsafter their initial request.Theagreementwould stillplace thePalestinianoperatorsatacompetitivedisadvantage,asIsraelioperatorshave3Gand4Gcapabilitiesandareabletoattracthighervaluecustomers.AstheMENAregionismovingtowards4G,therecentagreementonthereleaseoffrequenciescanhardlybecelebratedasasuccess–althoughitdoesrepresentafirststepforward.

4.2.3 Unauthorized Israeli mobile activity in the West Bank

ThepresenceofunauthorizedIsraelimobileactivityintheWestBankisamajorissuethatisaffectingthedevelopment of the Palestinian telecommunications sector. The Oslo Agreement confers to licensedIsraelitelecommunicationsoperatorstherighttoestablishfacilitiesinthesettlementsandtocovertheroads connecting the settlement to Israel. As a result, mobile operators have established

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

30

telecommunicationsinfrastructureinthesettlementsandcoverlargeareasoftheterritoryintheWestBank.Asanexample,thepicturesbelowshowtelecommunication infrastructures inthesettlementofPsagot,onahillfacingdowntownRamallah.

Figure10:PictureofamobiletowerinthesettlementofPsagot

Source:Authors

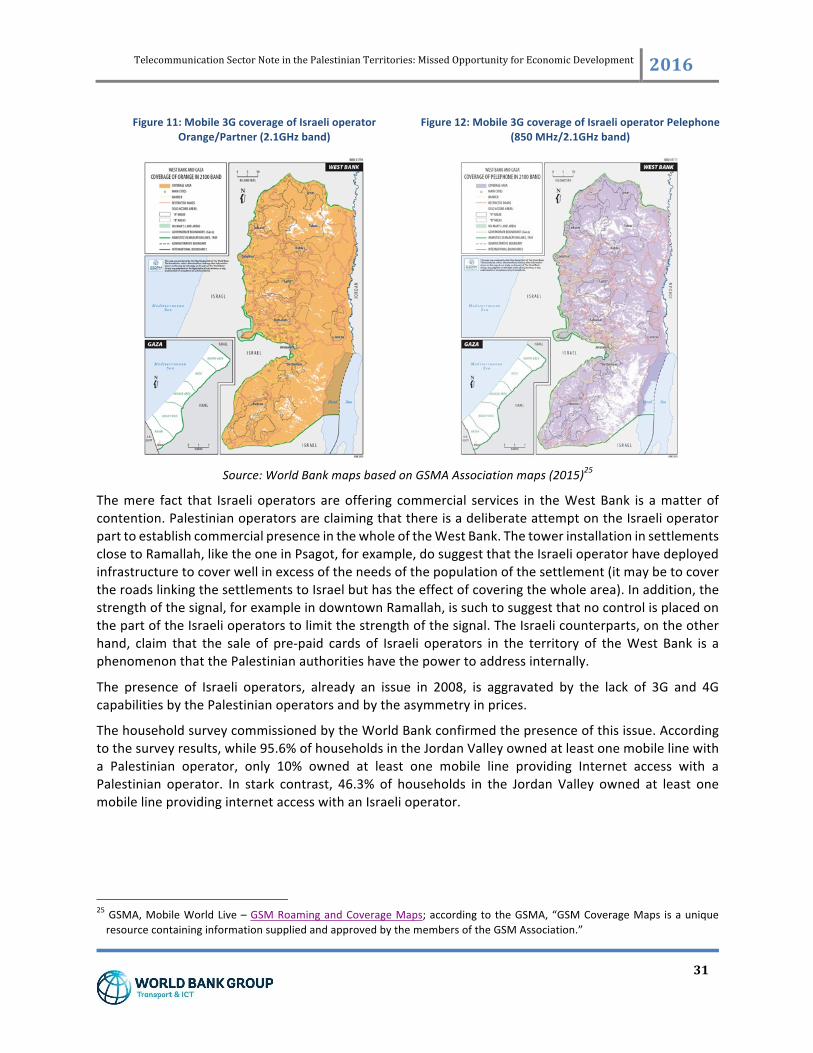

Thecoverageofthesignalisverycomprehensiveandhasbeenverifiedbytheauthorsofthereport.Togiveanideaofthephenomenon,itispossibletorefertothecoveragetableprovidedbyOrange(Partner)andPelephonetotheGSMA.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

31

Figure11:Mobile3GcoverageofIsraelioperatorOrange/Partner(2.1GHzband)

Figure12:Mobile3GcoverageofIsraelioperatorPelephone(850MHz/2.1GHzband)

Source:WorldBankmapsbasedonGSMAAssociationmaps(2015)25

Themere fact that Israeli operators areoffering commercial services in theWestBank is amatterofcontention.PalestinianoperatorsareclaimingthatthereisadeliberateattemptontheIsraelioperatorparttoestablishcommercialpresenceinthewholeoftheWestBank.ThetowerinstallationinsettlementsclosetoRamallah,liketheoneinPsagot,forexample,dosuggestthattheIsraelioperatorhavedeployedinfrastructuretocoverwellinexcessoftheneedsofthepopulationofthesettlement(itmaybetocovertheroadslinkingthesettlementstoIsraelbuthastheeffectofcoveringthewholearea).Inaddition,thestrengthofthesignal,forexampleindowntownRamallah,issuchtosuggestthatnocontrolisplacedonthepartoftheIsraelioperatorstolimitthestrengthofthesignal.TheIsraelicounterparts,ontheotherhand, claim that the sale of pre-paid cards of Israeli operators in the territory of theWest Bank is aphenomenonthatthePalestinianauthoritieshavethepowertoaddressinternally.

The presence of Israeli operators, already an issue in 2008, is aggravated by the lack of 3G and 4GcapabilitiesbythePalestinianoperatorsandbytheasymmetryinprices.

ThehouseholdsurveycommissionedbytheWorldBankconfirmedthepresenceofthisissue.Accordingtothesurveyresults,while95.6%ofhouseholdsintheJordanValleyownedatleastonemobilelinewitha Palestinian operator, only 10% owned at least one mobile line providing Internet access with aPalestinian operator. In stark contrast, 46.3% of households in the Jordan Valley owned at least onemobilelineprovidinginternetaccesswithanIsraelioperator.

25GSMA,MobileWorldLive–GSMRoamingandCoverageMaps;accordingtotheGSMA,“GSMCoverageMaps isauniqueresourcecontaininginformationsuppliedandapprovedbythemembersoftheGSMAssociation.”

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

32

4.2.4 Cross-border restrictions on telecom material and staff

Asmentionedinsection§3.4,PalestinianoperatorscannotconnectdirectlytheirnetworkstotherestoftheworldandareobligedtogothroughIsraeliregisteredcompanies,evenforaccessingtheMedNautilussubmarine landing station located in Israel. This represents an economical and technical burden toPalestinianoperators.

AsecondissueisthelackofadirectconnectionbetweenPalestinianterritories.PaltelhasindicatedthattheycannotlinktheirinfrastructureintheWestBankwiththecounterpartsinGaza,forexample,throughamicrowavelinkwithsufficientcapacity.TherearestrongIsraelirestrictionsinreleasingpermitstomoveequipmentwithinAreaC,allowinfrastructuredeployment,andallowtheinstallationofmicrowavelinks26.

AthirdissueisthedifficultiesfacedbyPalestinianoperatorstoaddressconsumersinAreaC.Accordingto theAlpha International survey, the Israeli operatorCellcomhas a41.5%market shareof the fixedbroadbandmarketintheJordanValley,comparedto16.1%forHadara.

Finally,bothJawwalandWataniyasharedthattheIsraelicounterpartshaveforcedthemtoplacetheirmainswitchesinIsraeliterritory.Bothclaimthattheserestrictionsamounttoextracostsforthecompany.Forexample,bothcompaniesneedtohire–atahighcost–staff inIsraeltoserviceandmaintaintheswitches in Israel.Whilethisclaim ismost likelycorrect, itwasnotpossibletoquantifytheextracostincurred.

Palestinian government counterparts and Palestinian private sector companies highlighted majordifficultiesexperiencedwith the importofequipment.Difficultieswith the importofequipmenthavebeenquotedbyWataniya,forexample,asanobstaclethatpreventedthemfromlaunchingoperationsinGaza(seealsoinfra§4.2.2).

ThemeetingswithPalestinianICTcompanies,highlightedseveraldifficulties,including:

• Delaysinobtainingrelevantauthorizations;• Cumbersomeprocedures;• Extracost,relatedtotheobligationofgoingthroughIsraeliimporters;• Non-transparentandchangingprocesses, andopaquedecisionmaking, causingundetermined

delays.

ChallengesfacedbyPalestiniantelecomandICTcompaniestodeployinfrastructures

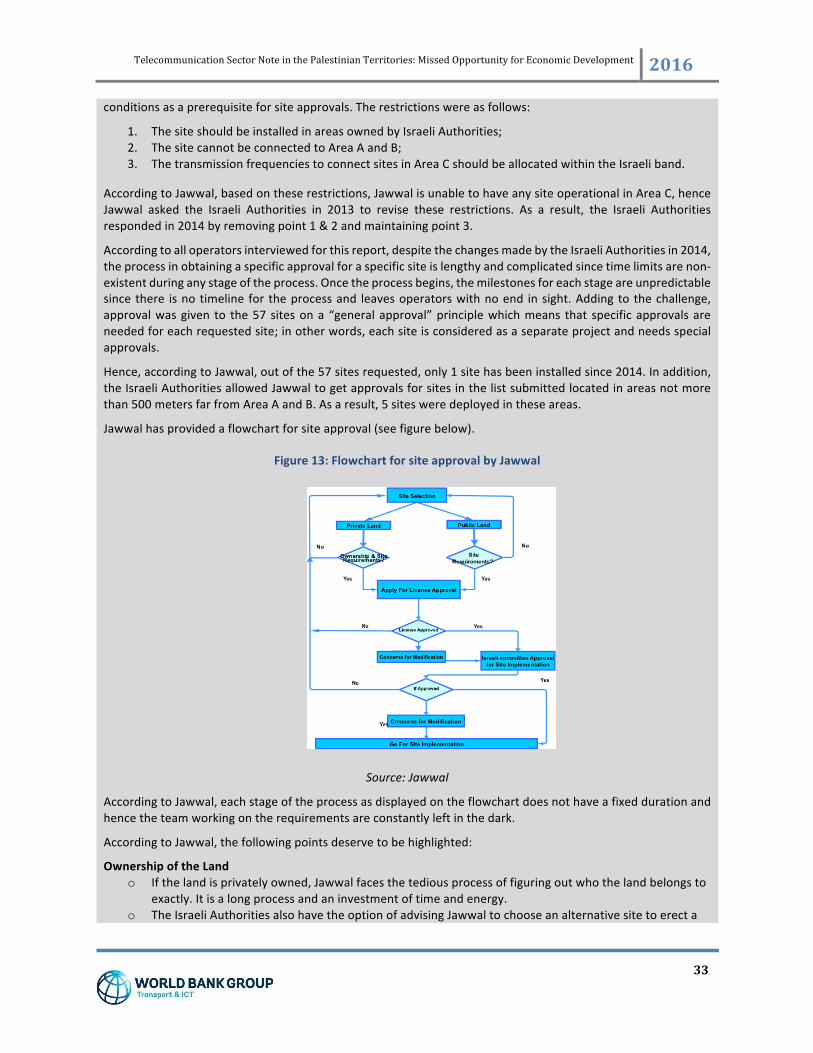

Theoperatorshavepointedouttoaseriesofconstraintsfacedwhenimportingequipment.Inparticular,Jawwalhasprovidedadetailedaccountoftheprocedures,whichareillustratedbelow.OneofthemanyconstraintsfacedbyJawwalisitsinabilitytobuildinfrastructureandspecificallytowersinAreaC.Thisresultsinalossofopportunitytoservemanyofthe100,000Palestinianswholiveinthisarea,inadditiontothe2.5millionPalestinianswhopassthroughtheroadsofAreaC.

AccordingtoJawwal,thecompanyrequestedseveraltimesandinmanyoccasionstogetapprovaltodeploycellsitesinAreaCinordertofulfilthelicenseobligationtocoverthePalestinianvillagesandmainroadsconnectingmaincitiesinAreaC.In2009,theIsraeliAuthoritiesrespondedthatJawwalcouldgetthenecessaryapprovalsforCAreasitesviaanIsraelicompany,whereasJawwalrequestedthatsuchapprovalsbegranteddirectlytoJawwal.In the same year, Jawwal submitted a plan for 57 sites,where Israeli Authorities respondedwith very strict

26Cf.WorldBankreport“AreaCandtheFutureofthePalestinianEconomy”,publishedbytheWorldBankinOctober2013(WorldBank,2013)formoredetails.

TelecommunicationSectorNoteinthePalestinianTerritories:MissedOpportunityforEconomicDevelopment 2016

33

conditionsasaprerequisiteforsiteapprovals.Therestrictionswereasfollows:

1. ThesiteshouldbeinstalledinareasownedbyIsraeliAuthorities;2. ThesitecannotbeconnectedtoAreaAandB;3. ThetransmissionfrequenciestoconnectsitesinAreaCshouldbeallocatedwithintheIsraeliband.

AccordingtoJawwal,basedontheserestrictions,JawwalisunabletohaveanysiteoperationalinAreaC,henceJawwal asked the Israeli Authorities in 2013 to revise these restrictions. As a result, the Israeli Authoritiesrespondedin2014byremovingpoint1&2andmaintainingpoint3.

Accordingtoalloperatorsinterviewedforthisreport,despitethechangesmadebytheIsraeliAuthoritiesin2014,theprocessinobtainingaspecificapprovalforaspecificsiteislengthyandcomplicatedsincetimelimitsarenon-existentduringanystageoftheprocess.Oncetheprocessbegins,themilestonesforeachstageareunpredictablesince there isnotimeline for theprocessand leavesoperatorswithnoend insight.Addingto thechallenge,approvalwasgiven to the57 sitesona “generalapproval”principlewhichmeans that specificapprovalsareneededforeachrequestedsite;inotherwords,eachsiteisconsideredasaseparateprojectandneedsspecialapprovals.

Hence,accordingtoJawwal,outofthe57sitesrequested,only1sitehasbeeninstalledsince2014.Inaddition,theIsraeliAuthoritiesallowedJawwaltogetapprovalsforsitesinthelistsubmittedlocatedinareasnotmorethan500metersfarfromAreaAandB.Asaresult,5sitesweredeployedintheseareas.

Jawwalhasprovidedaflowchartforsiteapproval(seefigurebelow).

Figure13:FlowchartforsiteapprovalbyJawwal

Source:Jawwal

AccordingtoJawwal,eachstageoftheprocessasdisplayedontheflowchartdoesnothaveafixeddurationandhencetheteamworkingontherequirementsareconstantlyleftinthedark.