Embed Size (px)

Citation preview

Ten Questions About Tax Policy for the Next Administration and Congress

October 2008

Ten Questions About Tax Policy for the Next Administration and Congress 2

I. Introduction In 2009, the new Administration and new Congress will face what many have called “a perfect storm for the tax code.” With the 2001 and 2003 tax cuts expiring,1 with congressional budget rules effectively requiring additional tax revenues to offset the cost of new initiatives, and with growing concerns about the overall health of the economy, about the shift of jobs overseas, and about a host of other issues with tax policy implications, taxpayers are likely to see the most significant tax policy debate in decades.

This upcoming tax debate raises many questions for individuals, businesses, and nonprofit organizations. Will changes in the tax rules for ordinary income, capital gains, and dividends significantly alter the after-tax return on investments? How will Congress address the financial crisis on Wall Street? What will happen to corporate tax rates? Will certain tax benefits be on the chopping block labeled by policy makers as “loopholes?” How will changes in the foreign tax rules affect international operations? Is there a chance that new tax incentives can be enacted notwithstanding the need for additional revenues?

This paper is designed to assist in the consideration of these and other questions. It provides general background, then discusses ten specific questions about tax policy facing the new Administration and the next Congress. These questions are:

1. What will happen to individual tax rates?

2. What will happen to the alternative minimum tax?

3. What is the outlook for the estate tax?

4. How will capital gains and dividends be taxed?

5. Will the corporate tax rate be reduced?

6. Will Congress change the tax treatment of income earned abroad?

7. What is the future outlook for tax extenders?

8. How will the new Administration and Congress address the tax code and energy independence?

9. What is the outlook for taxes and health care reform?

10. Where will the new President and Congress look for additional revenue?

II. BackgroundThe Political Setting. Although it is impossible to predict the outcome of the upcoming elections, there will be a new Administration and there is likely to be a Democratic Congress with larger majorities in both the House and Senate than exist today.2 New presidents tend to push major tax bills quickly to follow through on campaign promises and to take advantage of the “honeymoon” period. The 1981 Reagan tax cuts and the 1993 Clinton tax bill were enacted by August of the new Presidents’ first year in office. The conference report for the Bush tax cuts was agreed to on May 26, 2001. If history is any indication, there is a significant chance that major tax legislation will be considered early in 2009, at a pace much faster than the usual pace of tax legislation.

The Impending Expiration of the 2001 and 2003 Tax Cuts. The new Administration and Congress will immediately confront major tax policy issues. The reasons are budgetary and structural. The most recent Office of Management and Budget projections show the projected 2009 federal budget deficit to be $483 billion ($611 billion if the deficit does not include the Social Security surplus), and this was before Congress provided $700 billion for the financial crisis. Although this deficit is projected to be cut by 2/3 by 2012, this projection assumes the 2001 and 2003 tax cuts will be allowed to expire as scheduled in 2010.3 The 2010 expiration date structurally embedded in the tax code now serves as a trigger that will force the new President and Congress to quickly choose among competing priorities.

Thus far, the principal political debate, particularly in the presidential campaign, has been whether to extend some or all of the 2001 and 2003 tax cuts. According to the Joint Committee on Taxation, permanently extending the 2001 and 2003 tax cuts would cost $2.3 trillion over ten years. In the presidential campaign, the debate has been principally about whether to extend the tax cuts for upper-income individuals. But this is only part of the picture. The temporary tax policies enacted in 2001 and 2003 include not only tax cuts that primarily affect higher-income taxpayers, such as lower top marginal rates and lower rates for capital gains and dividends, but also a wide variety of tax relief that benefits middle-class taxpayers, such as the new 10% tax bracket, relief from the marriage penalty, and doubling the child tax credit from $500 to $1,000. Regardless of who controls the White House, there will be overwhelming bipartisan support for extending, at a minimum, portions of the 2001 and 2003 tax cuts that benefit middle and lower-income taxpayers.

Ten Questions About Tax Policy for the Next Administration and Congress

Ten Questions About Tax Policy for the Next Administration and Congress 3

But extending even some of these tax cuts will be costly. For example, making the $1,000 child credit permanent would cost $261 billion over the next ten years. Extending relief from the marriage penalty would cost $81 billion. On top of this, Congress wants to limit the growing reach of the alternative minimum tax, which will cost nearly $64 billion in 2008 alone to protect 25 million taxpayers from the AMT. The tax code contains dozens of other temporary but worthy policies, like the research and experimentation tax credit and the deduction for college tuition, that expire year-to-year and whose extensions will cost at least another $25 billion annually.

The next Congress may not approve all of this tax relief. But it will enact a substantial part. A conservative estimate of the cost is at least $1 trillion (over ten years) – and it could be as much as $2 trillion. On top of that, there are likely to be new initiatives to address health care, education, energy independence, and retirement security that will necessarily involve changes to the tax code.

The Pay-Go Constraint. Republicans have said that the cost of extending tax cuts does not need to be offset by tax increases. Republicans have argued that the 2001 and 2003 tax cuts were not intended to be temporary and, moreover, the budgetary effects of tax cuts would be counteracted by economic growth. Thus, President Bush and Senator McCain have proposed to extend all of the 2001 and 2003 tax cuts without any offsetting tax increases.

Not so the Democrats. When they gained majorities in the House and Senate, the Democrats reinstated and pledged to comply with “pay-as-you-go” (pay-go) congressional budget rules, which require that any tax cuts or spending increases be offset by tax revenues or spending cuts, so that the overall effect does not increase the federal deficit (as measured by conventional Congressional Budget Office “scorekeeping”). Although congressional Democrats have made pay-go budgeting a central tenet of their leadership, they have struggled to keep the pledge in the 110th Congress.4 In the 111th Congress, Democrats will try to continue to uphold their pay-go pledge. This has

Billio

ns

0

-50

-100

-150

-200

-250

-300

-350

-400

-450

-5002008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Years

Projected Deficits

Projected With Tax Cuts

-407

-438 -431

-325

-3 -5

-148

-126

-264

-147

-294

-170

-304

-162

-316

-207

-328

-174

-342

-135

-356

Source: Congressional Budget Office. The Budget and Economic Outlook: 2008 to 2018, at x and 20 (September 2008)

Cost of extending selected tax cuts (10 years)

• Lower Rates $1.042 trillion• Estate tax repeal $670 billion• Child Credit $261 billion• Dividends $217 billion• Capital Gains $102 billion• Marriage Penalty $81 billion

Source: Joint Committee on Taxation. Description of Revenue Provisions Contained in

the President’s Fiscal Year 2009 Budget Proposal. JCS-1-08, at 311 (March 2008).

Ten Questions About Tax Policy for the Next Administration and Congress 4

important policy implications. Under the pay-go rules, any future tax cuts exceeding $10 billion, including any extension of the 2001 and 2003 tax cuts, must be offset by an equal amount of tax revenue or spending reductions. Given that large spending cuts are unlikely, this means that if Congress decides to abide by pay-go rules, it will have to offset the cost of the large tax cuts with large tax increases.

“It shall not be in order in the Senate to consider any bill, joint resolution, amendment, motion, or conference report … that would cause a net increase in the deficit in excess of $10 billion in any fiscal year provided for in the most recently adopted concurrent resolution on the budget unless it is fully offset over the period of all fiscal years provided for in the most recently adopted concurrent resolution on the budget.”

—Section 315 of S. Con. Res. 70 (2008 Budget Resolution)

If Senator McCain is elected president, there will likely still be tax increases. Although Senator McCain has expressly rejected the need to offset the cost of extending expiring tax cuts, he has previously been known as something of a deficit hawk.5 If congressional Democrats insist on offsetting some or all of the cost of tax cuts, McCain, as President, may agree to do so at least to some extent. Indeed, he has himself called for closing billions of dollars worth of “corporate tax loopholes.”6

Thus, whatever the outcome of the presidential election, there is likely to be an intense search for politically palatable tax increases next year. Even if the economy continues to sputter, the new president could decide that economic stimulus proposals should be considered first, and that major tax increases are inconsistent with economic stimulus, but that will only delay tax increases, not prevent them. Before too long into 2009-2010, the Administration and Congress will have to confront the impending expiration of the tax cuts, and will require significant offsetting tax increases in an effort to reduce the deficit.

Other Tax Issues. The new Administration will face other tax issues. More than 20 years after comprehensive reform of the tax code in 1986, there have been calls to undertake another comprehensive reform of the tax system, most notably in the 2005 report of the President’s Advisory Panel on Federal Tax Reform, and Senators McCain and Obama both have said that they want to reform the tax code to eliminate inappropriate “loopholes.” In addition, as is discussed below, tax issues will be implicated by efforts to address health care reform and the shifting of jobs overseas.7

A Republican Senator, George Voinovich (OH), recently summarized the situation that is likely to face the next Administration and Congress. Introducing a tax reform bill in June, 2008 he said:

“A number of factors make the 111th Congress the occasion for a perfect storm for the Tax Code. At the beginning of the next Congress, a new President will take office and will be looking to enact major tax changes. At the end, the 2001 and 2003 tax relief will expire, resulting in an unprecedented tax increase on the

American people. And in between, the reach of the deeply flawed alternative minimum tax … will threaten to hit tens of millions of middle-class Americans unless Congress enacts major tax legislation. Finally, the competitive pressures of a global economy will force us to change our uncompetitive and inefficient methods of business taxation, including one of the highest corporate marginal rates in the world. “8

III. Questions1. What will happen to individual tax rates?

Background. Under the federal income tax system, taxpayers are subject to tax on their worldwide taxable income. Taxable income is total gross income less certain exclusions, exemptions, and deductions. Income tax liability is determined by applying the regular income tax rate schedule to the individual’s taxable income. This tax liability is reduced by any applicable tax credits. The regular income tax rate schedules are divided into several ranges of income called “brackets,” and the marginal tax rate increases as the individual’s income increases. The income bracket amounts are adjusted annually for inflation according to the consumer price index (“CPI”).

The Economic Growth and Tax Relief Reconciliation Act of 2001 (the “2001 Act”) implemented a phased-in reduction in the tax rates that began in 2001 and was accelerated by the Jobs and Growth Tax Relief Reconciliation Act of 2003 (the “2003 Act”). The 2001 Act also added a new 10 percent tax bracket for a portion of taxable income that was currently taxed at 15 percent. Without further congressional action, the 10 percent bracket will disappear and pre-2001 rates will return in 2011 as follows:

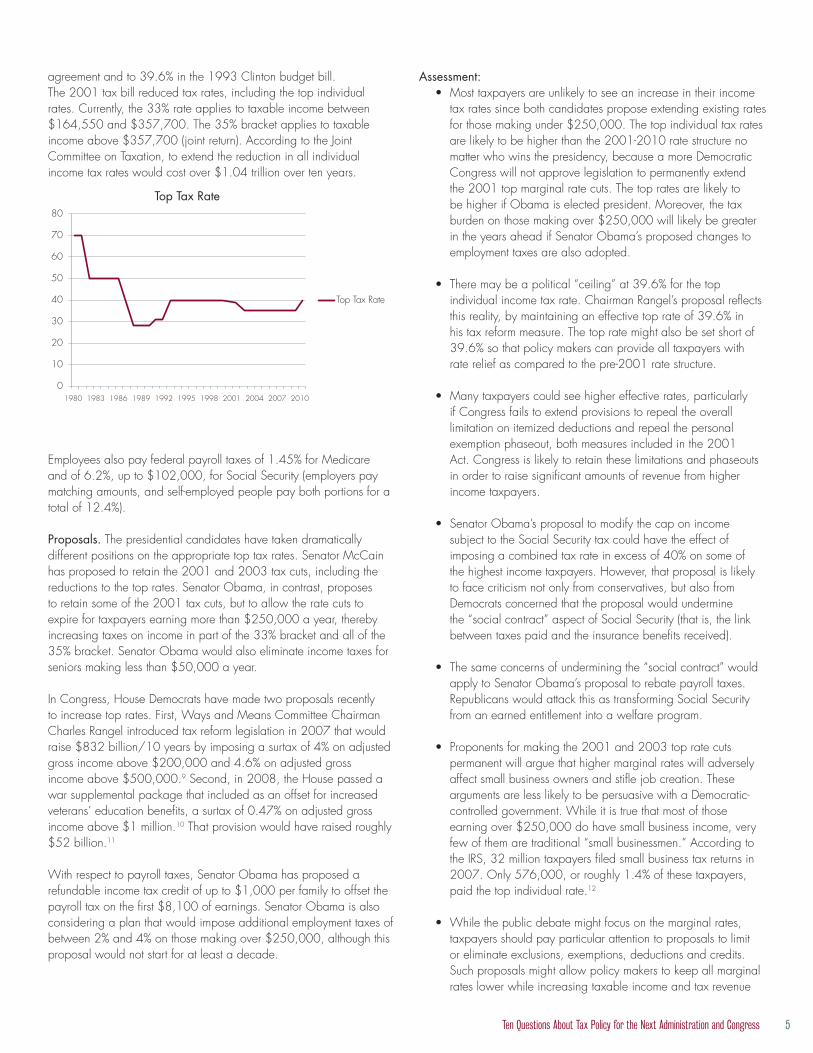

The top tax rate on individual ordinary income has fluctuated dramatically over the years. From 1971-81, it was 70%; the 1981 tax cuts reduced it to 50%, and the 1986 Tax Reform Act reduced it to 28%. It was increased, thereafter, to 31% in the 1990 Bush budget

Pre-2001 Rate Structure

2001 Rate Structure

Post-2010Rate Structure

- 10% -

15% 15% 15%

28% 25% 28%

31% 28% 31%

36% 33% 36%

39.6% 35% 39.6%

Ten Questions About Tax Policy for the Next Administration and Congress 5

agreement and to 39.6% in the 1993 Clinton budget bill. The 2001 tax bill reduced tax rates, including the top individual rates. Currently, the 33% rate applies to taxable income between $164,550 and $357,700. The 35% bracket applies to taxable income above $357,700 (joint return). According to the Joint Committee on Taxation, to extend the reduction in all individual income tax rates would cost over $1.04 trillion over ten years.

Employees also pay federal payroll taxes of 1.45% for Medicare and of 6.2%, up to $102,000, for Social Security (employers pay matching amounts, and self-employed people pay both portions for a total of 12.4%).

Proposals. The presidential candidates have taken dramatically different positions on the appropriate top tax rates. Senator McCain has proposed to retain the 2001 and 2003 tax cuts, including the reductions to the top rates. Senator Obama, in contrast, proposes to retain some of the 2001 tax cuts, but to allow the rate cuts to expire for taxpayers earning more than $250,000 a year, thereby increasing taxes on income in part of the 33% bracket and all of the 35% bracket. Senator Obama would also eliminate income taxes for seniors making less than $50,000 a year.

In Congress, House Democrats have made two proposals recently to increase top rates. First, Ways and Means Committee Chairman Charles Rangel introduced tax reform legislation in 2007 that would raise $832 billion/10 years by imposing a surtax of 4% on adjusted gross income above $200,000 and 4.6% on adjusted gross income above $500,000.9 Second, in 2008, the House passed a war supplemental package that included as an offset for increased veterans’ education benefits, a surtax of 0.47% on adjusted gross income above $1 million.10 That provision would have raised roughly $52 billion.11

With respect to payroll taxes, Senator Obama has proposed a refundable income tax credit of up to $1,000 per family to offset the payroll tax on the first $8,100 of earnings. Senator Obama is also considering a plan that would impose additional employment taxes of between 2% and 4% on those making over $250,000, although this proposal would not start for at least a decade.

Assessment: • Most taxpayers are unlikely to see an increase in their income

tax rates since both candidates propose extending existing rates for those making under $250,000. The top individual tax rates are likely to be higher than the 2001-2010 rate structure no matter who wins the presidency, because a more Democratic Congress will not approve legislation to permanently extend the 2001 top marginal rate cuts. The top rates are likely to be higher if Obama is elected president. Moreover, the tax burden on those making over $250,000 will likely be greater in the years ahead if Senator Obama’s proposed changes to employment taxes are also adopted.

• There may be a political “ceiling” at 39.6% for the top individual income tax rate. Chairman Rangel’s proposal reflects this reality, by maintaining an effective top rate of 39.6% in his tax reform measure. The top rate might also be set short of 39.6% so that policy makers can provide all taxpayers with rate relief as compared to the pre-2001 rate structure.

• Many taxpayers could see higher effective rates, particularly if Congress fails to extend provisions to repeal the overall limitation on itemized deductions and repeal the personal exemption phaseout, both measures included in the 2001 Act. Congress is likely to retain these limitations and phaseouts in order to raise significant amounts of revenue from higher income taxpayers.

• Senator Obama’s proposal to modify the cap on income subject to the Social Security tax could have the effect of imposing a combined tax rate in excess of 40% on some of the highest income taxpayers. However, that proposal is likely to face criticism not only from conservatives, but also from Democrats concerned that the proposal would undermine the “social contract” aspect of Social Security (that is, the link between taxes paid and the insurance benefits received).

• The same concerns of undermining the “social contract” would apply to Senator Obama’s proposal to rebate payroll taxes. Republicans would attack this as transforming Social Security from an earned entitlement into a welfare program.

• Proponents for making the 2001 and 2003 top rate cuts permanent will argue that higher marginal rates will adversely affect small business owners and stifle job creation. These arguments are less likely to be persuasive with a Democratic-controlled government. While it is true that most of those earning over $250,000 do have small business income, very few of them are traditional “small businessmen.” According to the IRS, 32 million taxpayers filed small business tax returns in 2007. Only 576,000, or roughly 1.4% of these taxpayers, paid the top individual rate.12

• While the public debate might focus on the marginal rates, taxpayers should pay particular attention to proposals to limit or eliminate exclusions, exemptions, deductions and credits. Such proposals might allow policy makers to keep all marginal rates lower while increasing taxable income and tax revenue

80

70

60

50

40

30

20

10

01980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

Top Tax Rate

Top Tax Rate

Ten Questions About Tax Policy for the Next Administration and Congress 6

overall. Moreover, policy makers could raise revenue through means that are less transparent. For example, there is research to indicate the present consumer price index slightly overstates inflation and that an alternative CPI would more accurately reflect consumer behavior. Since the tax code contains a number of features that are adjusted each year for inflation, policy makers could adopt an alternative CPI that would yield tens of billions of dollars in additional revenue annually and would enable them to avoid tougher choices. However, Democrats have opposed applying a CPI adjustment across all government programs as it would lead to reduced spending on many of their favored programs and entitlements. In short, marginal rates are important but taxpayers should focus on their overall tax burden.

2. What will happen to the alternative minimum tax?

Background. The individual alternative minimum tax (AMT) was established as part of the first major tax reform law, the Tax Reform Act of 1969. This was after Congress discovered that 155 taxpayers with income above $200,000 had paid no taxes at all.13 The purpose of the AMT, as described by the Senate Finance Committee in 1982 (when the AMT was revised and expanded) was to assure that “no taxpayer with substantial economic income should be able to avoid all tax liability by using exclusions, deductions, and credits.”14

The Tax Reform Act of 1986 made a series of modifications to the AMT, but retained it as a fundamental part of the tax system.

The individual AMT applies at rates of 26% or 28%, to “alternative minimum taxable income” (AMTI) above an exemption amount ($62,250 for a couple filing a joint return in 2007). AMTI consists of regular taxable income plus a series of preferences such as deductions for state and local taxes, interest on tax-exempt bonds, and accelerated depreciation.

Because the AMT exemption amount is not indexed, the number of taxpayers that would be subject to the AMT has been scheduled to rise dramatically, from 4 million in 2006 to 30 million in 2010, at which point the amount of revenue raised from the AMT would have risen from $24 billion to $119 billion. What was once a “class tax” has slowly morphed to be a “mass tax.” To limit the reach of the AMT, Congress has repeatedly enacted the so-called “AMT patch” that temporarily increases the exemption. The most recent AMT patch increased the exemption to $69,950 for 2008. The 2008 “patch” expires on December 31, 2008, so it needs to be extended for 2009 (and each year thereafter), to prevent the number of taxpayers subject to the AMT from spiking dramatically.

Like the individual AMT, the corporate alternative minimum tax was established by the Tax Reform Act of 1969 and revised and expanded by the Tax Reform Act of 1986. The corporate AMT applies at a rate of 25% to AMTI above an exemption amount ($40,000, but phasing out for corporations with AMTI above $150,000, and completely eliminated for corporations with AMTI above $310,000). As for individuals, AMTI consists of regular taxable income plus a series of preferences.

Unlike the individual AMT, the corporate AMT does not appear to apply to a dramatically rising number of taxpayers or raise a dramatically rising amount of revenue. Fewer than 1% of corporations pay the corporate AMT.15

Proposals. Both Senators Obama and McCain have proposed to fix the AMT, basically by pledging to prevent the number of AMT taxpayers from growing. Although Senator McCain has publicly stated that he would abolish the AMT, in reality, McCain is likely to continue the annual AMT patch.In recent years, Congress has repeatedly enacted a one-year

60

50

40

30

20

10

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

YEAR

MILL

ION

S

Current Law/Tax Cuts Extended

Pre-2001 Law

Projected Number of AMT TaxpayersWith and Without Effect of 2001-2006 Tax Cuts

Source: Len Burman, Julianna Koch, and Greg Leiserson. The Individual Alternative Minimum Tax (AMT): 11 Key Facts and Projections. Tax Policy Center, at 1 (December 1, 2006).

Ten Questions About Tax Policy for the Next Administration and Congress 7

“patch” to prevent the individual AMT from applying to more taxpayers. Essentially, a patch temporarily increases the exemption amount to reflect inflation. The latest patch covered 2008 at a cost of $62 billion.

In addition, there have been major proposals to make permanent changes in the individual AMT. Finance Committee Chairman Baucus and Ranking Member Grassley introduced legislation, S. 41, to repeal the AMT. The Chairman of the House Ways and Means Committee, Congressman Rangel, has proposed to repeal the individual AMT but would deny the benefits of repeal to taxpayers whose incomes are in the top 10%, by subjecting these taxpayers to a replacement tax of 4% (4.6% of income exceeding $500,000).16

There also have been more specific proposals to address the application of the AMT in particular circumstances. For example, in 2008 the House passed a provision that would abate interest and penalties associated with the application of the individual AMT to the exercise of incentive stock options.17

With respect to the corporate AMT, earlier in the decade there was serious consideration of proposals to repeal it. This Congress, such proposals have not been considered by either the House or Senate tax committees.

Assessment: • Congress will, at the very least, continue to provide a “patch”

indexed to inflation to prevent more taxpayers from becoming subject to the individual AMT.

• Although full repeal of the individual AMT would significantly simplify the tax code, the associated cost makes repeal highly unlikely unless undertaken as part of comprehensive tax reform. Although full repeal may be a stretch, there is likely to be a serious effort to revise the individual AMT on a more permanent basis. The options might include changing the budget baseline to assume an AMT fix or something like the Rangel proposal wherein AMT would no longer be a concern for the vast majority of taxpayers.

• Fixing the AMT problem suffers from several political drawbacks. First, the vast majority of taxpayers are unaware they would be subject to the AMT absent the patch. Consequently, in addressing the problem, Congress would be spending hundreds of billions of dollars to prevent a tax increase that most taxpayers do not know exists. Second, most politicians have already demonstrated a willingness to approve the annual patch without offsets making it difficult to spend real tax dollars in the future to address the AMT when there are other competing priorities. Third, addressing the AMT has become a political “gotcha.” Only when policy makers come to terms with the true implications of the AMT will the true problem be solved.

3. What is the outlook for the estate tax?

Background. The estate tax was established in 1916 and has remained in effect ever since.18 In 2000, the exclusion amount was $1 million and the top rate was 55%. As part of the 2001 tax cuts, Congress gradually liberalized the estate tax rules, increasing the exclusion and reducing the rates; in 2009, the exclusion will be $3.5 million and the top rate will be 45%. In 2010, the estate tax is scheduled to be completely repealed, but only for one year; in 2011, the changes to the estate tax, like other provisions of the 2001 tax cuts, are scheduled to expire, and the estate tax is scheduled to revert to its pre-2001 version, with an exclusion of $1 million and a top rate of 55%.

60

50

40

30

20

10

0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

Rate Exclusion

Estate Tax Rules

Ten Questions About Tax Policy for the Next Administration and Congress 8

Proposals. When Republicans controlled the House, they passed a series of bills to permanently repeal or dramatically curtail the estate tax, but the bills failed to pass the Senate.19 The most recent votes occurred in 2006, when a bill to permanently eliminate the estate tax received 57 of the 60 votes necessary to overcome a filibuster in the Senate. Another option, to permanently establish an exclusion of $5 million and a top rate of 15%, received 56 votes.20

This Congress, estate tax proposals have included updated versions of the proposal that previously passed the House, a “2009 freeze” that would make the $3.5 exclusion and 45% rate permanent, and an alternative that would establish an exclusion of $2 million and a top rate of 55%.21

Senator McCain, who originally opposed repeal of the estate tax, supports a $5 million exclusion and 15% rate. Senator Obama supports a 2009 freeze.

Assessment:

• With the “yo-yo” years of 2010-11 fast approaching, when the estate tax is scheduled to go from close to its current levels to full repeal and then to the much lower exclusion and higher rates of 2000, the new Congress will be under great pressure to quickly establish a new set of rules to facilitate reasonable estate planning.

• A 2009 freeze is likely to have considerable support, with current supporters including Senator Obama and other Democrats such as Senator Carper (D-DE) and Congressman Pomeroy (D-ND).

• A significant number of Senate Republicans including most

serving on the Senate Finance Committee support the complete elimination of the estate tax. The cohesion of this group gives them significant leverage in the outcome.

• A more Democratic Congress next year may increasingly support alternatives, such as the bill introduced by Congressman McDermott (D-WA) to establish a $2 million exclusion and a 55% top rate.22

• Because the CBO baseline assumes a reversion to the 2000 system, even such seemingly moderate proposals as a 2009 freeze have substantial revenue costs.

• Look for Congress to include reforms to the gift and estate tax rules to tighten perceived areas of abuse (i.e., family limited partnerships, valuation discounts) and to help offset the cost of higher exemption amounts and lower rates.

4. How will capital gains and dividends be taxed?

Background. Over the past few decades, the tax treatment of capital gains has fluctuated. From 1921 to 1986, capital gains were taxed at lower rates than ordinary income, generally through an exclusion of 50% or 60%. The Tax Reform Act of 1986 eliminated the differential treatment of capital gains, subjecting both capital gains and ordinary income to the same top rate of 28%. Thereafter, the differential treatment of capital gains gradually returned for individuals (but not corporations), as Congress raised the top rate for ordinary income but not for individual capital gains.

After 1993, the top rate for individual capital gains remained 28%, but the top rate for ordinary income had risen to 39.6%. In 1997, Congress reduced the tax rate for individual capital gains to 20% (10% for capital gains which otherwise would have been taxed at the 15% individual income tax rate). The 2003 Act reduced the 10% and 20% rates on capital gains to zero and 15%, respectively. The 2003 reductions are scheduled to expire at the end of 2010, when the tax rate for individual capital gains is scheduled to revert to 20%.

In lowering the capital gains rate in 1997 and 2003, Congress stated that economic growth cannot occur without saving, investment and the willingness of individuals to take risks. Congress believed that by reducing the effective tax rates on capital gains, taxpayers would be encouraged to increase saving and risk-taking. Moreover, Congress believed that a reduction in the taxation of capital gains would improve the efficiency of the capital markets because the taxation of capital gains upon realization encourages investors who have accrued past gains to keep their monies “locked in” to such investments even when better investment opportunities present themselves.

Until 2003, dividends received by an individual were included in gross income and taxed as ordinary income. In 2003, the tax rate for dividends was reduced to 15% (zero rate for dividends which otherwise would have been taxed at the 15% individual income tax rate). The 2003 reductions are scheduled to expire at the end of 2010, when the tax rate for dividends is scheduled to revert to the same rate as that of ordinary income (top rate of 39.6%).

In lowering the dividend rate, Congress recognized that placing

30

25

20

15

10

5

01980 1985 1990 1995 2000 2005 2010

Tax Rate for Capital Gains

Capital Gains

Top

Rate

Year

Ten Questions About Tax Policy for the Next Administration and Congress 9

different tax burdens on different investments resulted in economic distortions. Because interest payments on debt are deductible, the tax code encouraged corporations to finance using debt rather than equity and might put the economy at risk of more bankruptcies during an economic downturn. Moreover, Congress was concerned that prior law encouraged corporations to retain earnings rather than to distribute them as taxable dividends to shareholders who might have an alternative and better use for the funds, creating further inefficiency.

Some critics argue that the tax cuts enacted in 2001 and 2003 increased income inequality, reduced economic growth over the long run, and contributed to the reemergence of the substantial budget deficits. Warren Buffett frequently mentions that his secretary, who earned $60,000 in 2006, paid a higher effective tax rate than he did for that year. Mr. Buffett noted that he was taxed at a 17.7% rate while his secretary was taxed at 30%. IRS data generally supports Mr. Buffett’s claim. For years 2003 through 2005, the top 400 individual income tax returns with the largest adjusted gross incomes reported average income of $170 million and paid an average effective tax rate of 18.6%. In comparison, the 2006 married filing jointly tax rate for taxpayers making between $15,000 and $61,000 was 15%, and the rate for those making between $15,000 and $124,000 was 25%. With regard to the top 400 taxpayers, capital gains subject to the 15% preferential tax rate averaged 60% of AGI while salaries averaged only 11%.

Proposals. Senator McCain has proposed to make the 2001-03 tax cuts permanent, including the lower zero and 15 percent rates for capital gains and dividends. Senator Obama has proposed to retain the current capital gains and dividend rates for those making under $250,000. For those in the top two income tax brackets, Senator Obama would create a new top capital gains and dividends rate of 20 percent. Further, he would tax “carried interest” at ordinary income rates. However, Senator Obama has proposed to create incentives for small businesses and start-up businesses, in part by eliminating capital gains taxes on income from investments in such businesses.

Assessment: • Regardless of who wins the presidency, a Democratic Congress

is unlikely to extend the lower 15% tax rate for capital gains and dividends. However, with Senator Obama’s announced position, it is becoming more likely that tax rates for investment income will not exceed 20%.

• The upcoming expiration of the lower rates will force the Congress to reconsider the appropriate tax treatment of capital gains and dividends, including associated issues like “carried interest” and a zero capital gain rate for small business startups.

• The upcoming tax debate could lead policy makers to consider alternative options for taxing capital gains and dividends as they search for additional revenue. For example, the Joint Committee on Taxation proposed in 2001 that the complicated rate system for capital gains be replaced with a deduction equal to a fixed percentage of the net capital gain. This recommendation would simplify the computation of the tax on capital gains and streamline associated tax forms. Another

alternative could involve an income exclusion for certain levels of capital gain and/or dividend income for lower- and middle-income taxpayers.

5. Will the corporate tax rate be reduced?

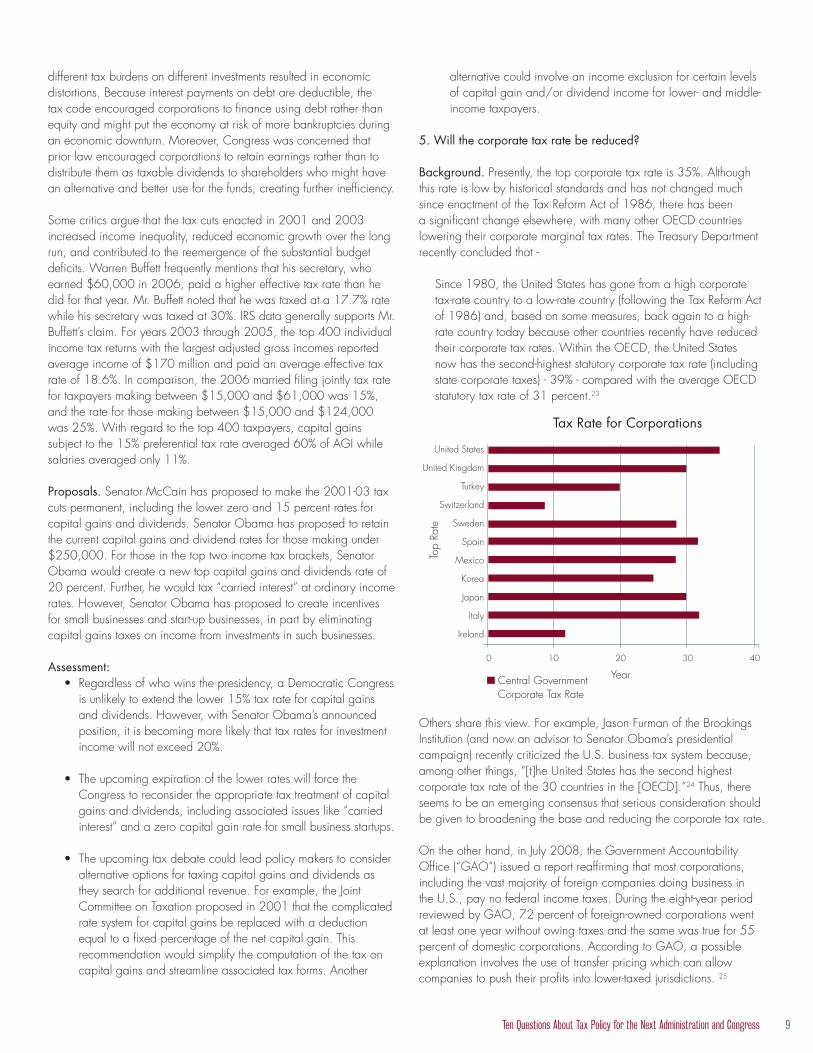

Background. Presently, the top corporate tax rate is 35%. Although this rate is low by historical standards and has not changed much since enactment of the Tax Reform Act of 1986, there has been a significant change elsewhere, with many other OECD countries lowering their corporate marginal tax rates. The Treasury Department recently concluded that -

Since 1980, the United States has gone from a high corporate tax-rate country to a low-rate country (following the Tax Reform Act of 1986) and, based on some measures, back again to a high-rate country today because other countries recently have reduced their corporate tax rates. Within the OECD, the United States now has the second-highest statutory corporate tax rate (including state corporate taxes) - 39% - compared with the average OECD statutory tax rate of 31 percent.23

Others share this view. For example, Jason Furman of the Brookings Institution (and now an advisor to Senator Obama’s presidential campaign) recently criticized the U.S. business tax system because, among other things, “[t]he United States has the second highest corporate tax rate of the 30 countries in the [OECD].”24 Thus, there seems to be an emerging consensus that serious consideration should be given to broadening the base and reducing the corporate tax rate.

On the other hand, in July 2008, the Government Accountability Office (“GAO”) issued a report reaffirming that most corporations, including the vast majority of foreign companies doing business in the U.S., pay no federal income taxes. During the eight-year period reviewed by GAO, 72 percent of foreign-owned corporations went at least one year without owing taxes and the same was true for 55 percent of domestic corporations. According to GAO, a possible explanation involves the use of transfer pricing which can allow companies to push their profits into lower-taxed jurisdictions. 25

United States

United Kingdom

Turkey

Switzerland

Sweden

Spain

Mexico

Korea

Japan

Italy

Ireland

0 10 20 30 40

Tax Rate for Capital Gains

Central GovernmentCorporate Tax Rate

Top

Rate

Year

Tax Rate for Corporations

Ten Questions About Tax Policy for the Next Administration and Congress 10

Proposals. The Treasury Department and the President’s Advisory Panel on Tax Reform both recommended that the top corporate tax rate be lowered to 28%26 and 31.5%, respectively.27 Senator McCain has proposed to reduce the top corporate tax rate from 35% to 25%.

On the Democratic side, House Ways and Means Committee Chairman Rangel made a lower corporate tax rate a key element of his tax reform plan, proposing to reduce the top corporate tax rate from 35% to 30.5%, saying that this would “help American companies stay competitive internationally.”28 Senator Obama has not specifically addressed lowering the top corporate tax rate. Many of the proposals stress that the corporate tax rate should not be reduced in isolation, but rather as a broad trade-off, similar to the trade-off at the heart of the Tax Reform Act of 1986, in which the corporate rate is reduced but the corporate tax base is broadened commensurately by eliminating or reducing tax preferences. Such a trade-off is envisioned in the proposals by the Treasury Department and the President’s Advisory Panel on Tax Reform, and is central to Chairman Rangel’s proposal, which would fully offset the $363.8 billion cost of lower corporate rates by repealing or reducing a number of corporate tax preferences. Specifically, Chairman Rangel would achieve a 30.5% corporate tax rate by repealing the LIFO method of accounting and the section 199 manufacturing deduction; significantly limiting deferral; delaying the implementation of worldwide interest allocation; and increasing from 15 years to 20 years the 197 amortization period for intangibles.

Assessment: • Whatever the outcome of the election, an opportunity may exist

for lowering the corporate marginal tax rate in an effort to make U.S. companies more competitive and to encourage innovation and job creation. Many tax experts and lawmakers from both parties have called for lowering the corporate tax rate.

• A reduction of the corporate tax rate is likely to be part of

an overall proposal that offsets the cost of the reduction by broadening the corporate tax base.

• The impact on any particular industry or company is likely to depend on the balance between the tax reduction resulting from the lower rate and the tax increase resulting from broadening the base by repealing or reducing business tax “loopholes” and/or tax expenditures.

6. Will Congress change the tax treatment of income earned abroad?

Background. The U.S. imposes a tax on the worldwide income of taxpayers subject to U.S. taxing jurisdiction. The system has two principal ameliorating features. First, U.S. companies receive a tax credit for the taxes that they pay to foreign countries on the income they earn abroad. Second, the foreign income of a controlled foreign subsidiary of a U.S. corporation is deferred until the income is repatriated to the U.S. in the form of a dividend payment, except for income that is considered “subpart F” income (i.e., interest, royalties, dividends, rents).

The current system has been repeatedly criticized, for different reasons. On one hand, many Democrats, labor unions and others have argued that the current system creates incentives for U.S. companies to shift jobs overseas. For example, Senator Clinton was asked during the Democratic primaries how she would prevent jobs from being transferred overseas. She focused her answer on the tax rules for international income, criticizing the current rules because “if you create jobs overseas, you don’t have to pay taxes on them until you bring the money back home.” Similarly, Senator Obama has expressed concern about “large companies [that] have managed to secure tax breaks or to hide their profits in overseas tax havens and not pay any American corporate taxes at all.”

On the other hand, many Republicans, business groups and others have argued that the current U.S. tax rules make it harder for U.S. companies to compete internationally, by subjecting U.S. companies (and foreign subsidiaries of U.S. companies) to a complex set of rules that have the effect of imposing higher taxes than are imposed on their international competitors. For example, Pamela Olsen, the Bush Administration’s Assistant Secretary of the Treasury for Tax Policy, has said that “[t]he U.S. international tax rules can operate to impose a burden on U.S.-based companies with foreign operations that is disproportionate to the tax burden imposed by our trading partners on the foreign operations of their companies.”29

“Some large companies have managed to secure tax breaks or to hide their profits in overseas tax havens and not pay any American corporate taxes at all. Barack Obama will level the playing field for all businesses by eliminating special interest loopholes and deductions … as well as by limiting the ability of large multi-national corporations to use tax havens to hide income overseas.”

-—Obama ’08 Tax Plan

“I don’t like obscene profits being made anywhere. I’d be glad to look, not just at the windfall profits tax - that’s not what bothers me - but we should look at any incentives that we are giving to people or industries or corporations that are distorting the market.”

-—McCain Campaign Speech 05/05/08, Charlotte, NC

Proposals. The blockbuster issue in the upcoming tax debate is deferral. Senator Obama has indicated he would move aggressively to reform international tax laws, including deferral. During the 2004 presidential campaign, Senator Kerry proposed to eliminate deferral altogether, and has introduced legislation to do so this Congress.30 Senator Clinton supported this approach during her presidential campaign.31 Ways and Means Committee Chairman Rangel introduced legislation proposing that deductions associated with foreign income be deferred until the associated income is repatriated.32 The Joint Committee on Taxation estimates that the Rangel proposal would raise $106 billion over ten years.

In addition, several bills have been introduced that would address specific perceived abuses in the international tax rules, including proposals to prevent “treaty shopping” under tax treaties,33 to tighten up the subpart F rules,34 to curtail the use of “tax havens,”35 to change the characterization of business entities (e.g., whether an

Ten Questions About Tax Policy for the Next Administration and Congress 11

entity is characterized as a U.S. corporation),36 and to change the treatment of royalty and financial services income under the foreign tax credit rules.37

Several other sources offer approaches that a new Congress may consider in the international tax area, including a June 2008 Senate Finance Committee hearing on the international tax system,38 a 2007 Treasury Department study of earnings stripping and transfer pricing,39 and a 2004 article written by Chairman Rangel, entitled “Current International Tax Rules Provide Incentives for Moving Jobs Offshore.”40

Assessment:

• The Congress will closely scrutinize federal tax rules affecting international transactions but is unlikely to repeal deferral in the near term. A proposal to outright repeal deferral would be highly controversial, with most Republicans and some Democrats opposing it.

• If a full repeal of deferral falls short, as expected, there are

likely to be alternative proposals to “tighten up” the international rules. Indeed, that is what led to the enactment of subpart F in the first place. In 1962, when President Kennedy proposed to eliminate deferral, Congress rejected his proposal but established subpart F in response. Specifically, Congress retained deferral generally but established subpart F to eliminate deferral for certain categories of income.

• The limitation on expenses proposed by Chairman Rangel may be seriously considered. Other possible areas of focus include subpart F income; tax treaties, particularly to curb behavior that may be characterized as “treaty shopping”; tax havens; the operation of the transfer pricing rules; earnings stripping; and reinsurance.41

7. What is the future outlook for tax extenders?

Background. Beginning in the 1980s, primarily for budget reasons, Congress increasingly began to make some tax policies temporary. Typically, these are tax incentives targeted to a specific industry or activity. In recent years, as budget pressures have intensified, the number of such temporary provisions that need to be periodically extended has grown to the point that the most recent “extenders” bill contains three dozen provisions extending expiring tax provisions, whose total cost is $27 billion (the ten-year cost of a one-year extension).42 Moreover, the process of considering tax extender bills has become the dominant task of the congressional tax-writing committees. This year, Congress waited until the last moment to address the package of the tax extenders, many of which had already lapsed. Even then, Congress had to attach the package to the emergency economic stabilization legislation to secure the necessary votes.

The extender tail now is wagging the tax policy dog. The leaders of the congressional tax-writing committees have expressed frustration about this. In speaking on the floor of the House on a recent extenders package, Chairman Rangel defined tax extenders as “when people want bills passed, but they put expiration dates on them in order to hide the real cost of the bill...we have so much garbage in this bill that soon I hope someone would have the courage to take a look at the tax bill that we have and strip it of the preferential treatment and get down to making the bills that we want permanent, and those that should not be permanent, just to kick them out.”43

Key Extender Provisions

Provision Cost/10 yrs. (in billions)

1-year AMT Patch -64,108

R&E Tax Credit -9,897

Leasehold, Restaurant, and Retail Improvements -6,728

Subpart F Active Financing -3,970

State & local Sales Tax Deduction -1,742

New Markets Tax Credit -1,315

Tuition Deduction -1,223

Section 45 Energy Production Credit -7,046

Section 48 Credit -1,777

Advanced Coal Project Investment -1,423

Coal Excise Tax -1,287

Plug-in Vehicles -1,056

Energy Conservation Bonds -1,025

Energy Efficient Homes -1,067

Other -7,745

TOTAL -108,592

Proposals. There have been a few efforts to separate particular extenders and either make them permanent or extend them for long periods of time. In 2006, Congress made permanent a number of temporary pension-related provisions as part of the Pension Protection Act of 2006. In 2007, Congress approved legislation, as part of the bill to raise the federal minimum wage, extending the Work Opportunity Tax Credit, which had until then been part of the various extenders packages, for four and a half years.

A number of bills have been introduced this Congress to make various extenders permanent. The bills that seem to have the greatest support would make permanent the R&D tax credit, the adoption credit, the rules relating to the subpart F treatment of active financing, the deduction for donations of food inventory, the exclusion for employer-provided group legal services, the depreciation treatment of leasehold improvements, the deduction for mortgage insurance premiums, and the rules for deducting film production expenses.44 These bills seldom include specific proposals to offset the cost of the permanent extensions.

Ten Questions About Tax Policy for the Next Administration and Congress 12

Assessment:• There is likely to be an intensified effort to break out of the

extenders box, by making some of the extenders permanent, lengthening the duration of others, and letting some expire. Although this has been tried before and generally has failed, the level of congressional frustration, with the need to repeatedly pass extender bills, seems to be growing.

• If the new Administration and Congress begin to address issues such as education, health care, energy independence, and competitiveness, many of these temporary tax extenders could find homes on larger policy initiatives. For example, the temporary deduction for qualified tuition and expenses, QZABs, deduction for teacher classroom supplies and enhanced deduction for school book donations could be incorporated into comprehensive education tax legislation and dealt with on a long-term or permanent basis. The same could hold true for energy-related or business tax provisions.

• The cost of making various extender provisions permanent is high. For example, the ten-year cost of making the R&D credit, active financing rule, and sales tax deduction for non-itemizers permanent is $115 billion, $56 billion, and $37 billion, respectively. Consequently, many extenders are likely to remain temporary until the deficit situation is addressed.

• Pulling this together, there is likely to be a continuation of the current situation, in which very few of the extenders are made permanent or extended for long periods of time, while the rest remain part of annual period extender legislation.

• A compromise in Congress is possible by either making some of the extenders permanent with offsets permanently closing loopholes or conversely, temporarily extending some tax cuts with the offsets coming from temporarily closing loopholes.

• To the extent that the Congressional Budget Act’s “reconciliation” process is used to pass a tax bill, the use of extenders is likely to increase, because revenue-losing provisions in that bill will be required under the operation of congressional budget rules.45

8. How will the new Administration and Congress address the tax code and energy independence?

Background. Over the years, Congress has established a series of tax incentives for energy production. Originally, these incentives primarily were for the production of fossil fuels (e.g., the oil depletion allowance). More recently, Congress has established tax incentives for energy conservation and for the production of energy from renewable sources, such as solar, wind, and biomass. For example, in the Energy Policy Act of 2005, Congress established new tax incentives for energy efficient homes and commercial buildings, residential and business use of solar power, and vehicles that use alternative technology.46 However, many of those tax credits have already expired or are near expiration, and a thick stack of new proposals for incentives for energy conservation and renewable energy production and infrastructure has been introduced.

Proposals. During the current Congress, there has been intense work on a package of tax provisions that would extend and expand energy tax incentives. Generally, the package has included extension (and, in some cases, expansion) of production tax incentives for electricity produced from renewable resources (including biodiesel),47 investment tax credits for advanced clean coal technologies (particularly those that demonstrate high levels of carbon sequestration), production incentives for biodiesel and other renewable fuels, as well as a range of other incentives.48 Some of these include:

• bonus depreciation for placement of “smart” electric meters and grid systems;

• investment tax credits for solar, fuel cell technologies, and certain “green” properties;

• expansion of tax-free bonds for certain clean renewable fuels; • credits against the coal excise tax for certain sales of coal; and• a new credit for “plug-in” hybrid vehicles.

The House Ways and Means Committee and the Senate Finance Committee each reported versions of an energy tax package, and, after the package reported by the Ways and Means Committee passed the House, congressional leaders agreed on a compromise version of the bill, which passed the House but fell one vote short in the Senate. The bill was not enacted earlier this year, primarily because of a dispute between Democrats and President Bush and Senate Republicans about whether the cost of the bill should be offset. The fully offset energy package was eventually enacted as part of the Emergency Economic Stabilization Act of 2008. Many of the provisions are of only short duration. The next Congress is likely to consider further energy tax incentives through a number of legislative proposals, possibly including a substantial energy policy bill and reauthorization of the surface transportation bill.

Beyond the general debate over offsets, the energy extenders package and other energy proposals have been complicated by a debate about whether oil and gas production should be the target of offsets (e.g., the section 199 domestic production incentive), and the fact that opening new territory for oil and gas exploration has been excluded from the legislation. As a side note, the Democratic leadership in the Congress has proposed legislation that would tax the “windfall” profits of oil and gas companies. Although this issue should be watched because of its political relevance, it is not a provision that appears ripe for approval at this point.

One recent legislative effort that hints at issues that could be debated next year is a bipartisan proposal recently released by Senators Conrad and Chambliss. The proposal includes robust extensions of production tax credits for renewables, new consumer tax credits for purchase of vehicles that run on non-petroleum based fuels, credits for capture and sequestration of carbon dioxide in industrial processes, and new credits for infrastructure related to renewable fuels and the production of liquid fuels from coal. The details of this “New Era” energy bill are being worked out now and could likely form the basis for limited proposals at the end of this Congress and a much larger package in the next Congress.

Ten Questions About Tax Policy for the Next Administration and Congress 13

Senators McCain and Obama have both made general proposals to significantly invest in alternative energy and conservation to stimulate the economy, but there is not yet sufficient detail in these plans to prognosticate on critical differences and possible legislative outcomes. Both plan to invest in renewables, including extensions of credits like those now in place for solar, biomass and other renewables. They also both have proposed incentives for clean coal technologies and transportation that uses non-petroleum based fuel. Thus, their plans generally recognize many of the issues contained in recent and proposed legislation. Senator McCain appears to be more committed to development of domestic fossil fuel resources than Senator Obama.

Assessment: • Although energy tax incentives were recently enacted, the

next Administration and Congress will seriously consider additional energy tax incentives, which have been very popular in recent years.

• The House and Senate are likely to continue to take somewhat different approaches, with the House proposing a smaller package that emphasizes renewable resources and technologies as well as conservation and the Senate a larger package that includes those incentives plus more incentives for clean coal and other conventional fuels.

• There is likely to be a continuing debate about whether the cost of the energy incentives should be offset exclusively by limiting tax benefits available to the oil and gas industries or instead should be offset, at least in part, by other revenue-raising proposals.

9. What is the outlook for taxes and health care reform?

Background. The federal income tax system affects health policy in several ways, most significantly through the exclusion of employer-provided health insurance from taxable income. Since 2001, the Bush Administration has proposed changes in the tax treatment of health benefits as a means of shifting the responsibility and incentive for providing health care coverage from the employer to the individual. However, the tax deductions that are available to individuals who purchase their own health insurance are currently not comparable to the tax deductions available for employer provided coverage. While a number of conservatives have consistently criticized the health insurance tax exclusion for encouraging people to participate in “gold plated” employer-provided plans rather than

McCain ObamaClimate Change Supports a 60% reduction in greenhouse gas (GHG)

emissions by 2050 through a cap and trade mechanism. The

plan also calls for the U.S. to reduce GHG emissions to 1990

levels by 2020.

Supports an 80% reduction in greenhouse gases (GHG) by

2050 through a cap and trade mechanism. The plan also calls

for the U.S. to reduce GHG emissions to 1990 levels by 2020.

Biofuels Opposes ethanol subsidies and wants to lift the tariff on

foreign ethanol.

Supportive of the existing ethanol mandate.

Oil & Gas Wants to open more of the outer continental shelf to drilling;

however, opposes opening the Arctic National Wildlife Refuge

(ANWR) to drilling.

Has spoken against subsidies for the oil and gas sector,

including the domestic production exemption (Sec. 199),

expensing of exploration and development costs, the 15%

credit for enhanced oil recovery costs for tertiary wells, and

the special depreciable lifetimes for select oil company assets,

among others.

Supports imposing a windfall profits penalty on oil selling at or

over $80 per barrel.

Wants to rescind existing tax incentives, including the domestic

production exemption (Sec. 199).

Alternative (Wind/Solar) Does not advocate targeted subsidies for wind and solar.

Generally opposed to technology specific subsidies.

Supports extension of existing tax credits in support of alternative

energy such as wind and solar.

Utilities Has advocated for stronger clean air protections.

Wants large investments in the power grid.

Supports smart metering.

Wants major investment in power grid to increase

renewable generation and accommodate smart metering

and distributed storage.

Coal Supports development of clean coal technologies. Supports development of clean coal technologies.

Willing to ban new traditional coal facilities and to ensure

rapid commercialization and deployment of low carbon

coal technology.Adapted from Joe Lieber, Election Update: McCain and Obama on the Issues. Washington Analysis (Aug. 13, 2008).

Ten Questions About Tax Policy for the Next Administration and Congress 14

purchase individual policies, liberal groups such as the Progressive Policy Institute are also joining the call for health insurance reform. Regardless of the outcome of the 2008 elections, changes to the tax treatment of employer-sponsored health benefits are likely to play a key role in health reform proposals in 2009.

Top Federal Tax Expenditures (FY ‘07 - ‘11) (in billions)

Reduced Rate (Capital Gains & Dividends) 631.9

Healthcare: Exclusion of Employer Contributions 628.5

Pension Contribution Exclusion 607.3

Mortgage Interest Deduction 430.2

Exclusion of Capital Gains at Death 279.9

Earned Income Tax Credit (EITC) 234.9

Tax Credit for Children Under Age 17 201.3

Deduction for Charitable Contributions 187.0Exclusion of Benefits Provided Under Cafeteria Plans 185.5

Deduction of State and Local Income Taxes 175.1

Presidential Candidate Proposals. Little is surprising about either Senator Barack Obama or Senator John McCain’s approach to health care issues. Senator McCain is taking a traditionally Republican approach to health reform by adopting a platform that focuses on the themes of individual choice, competition, and tax rebates. Senator Obama has focused on the traditionally Democratic themes of universal and comprehensive coverage.

Senator McCain’s health reform plan focuses on encouraging the individual insurance market by reforming the tax code to eliminate the bias that favors employer-provided coverage. Senator McCain has proposed a refundable health insurance tax credit of $5,000 per family and $2,500 per individual. McCain’s proposed tax credit would be available for either employer-provided or individual coverage, and would consequently limit the tax preference for employer-sponsored health insurance. Senator McCain’s proposal is similar to President Bush’s 2007 proposal—a proposal based on the Advisory Panel on Tax Reform’s recommendation—that would have limited the exclusion for employer-provided health insurance benefits to $15,000 per family and would have allowed individuals who purchase their own health insurance to take an equivalent deduction of up to $15,000.

Senator Obama, on the other hand, supports reforming the health care system by building on the existing employer-based system. Senator Obama has proposed a series of non-tax reforms of health care that include income-based federal subsidies and direct spending programs to increase health coverage. Senator Obama’s current plan does not explicitly rely on major changes to the tax code (e.g., limits on the exclusion for employer-provided coverage and individual savings incentives) to expand health insurance coverage. The Obama plan would, however, provide small businesses that pay a share of employee health costs with a refundable tax credit equivalent to 50 percent of premiums paid on behalf of their employees.

Polls have shown that voters are evenly split in their support for Democratic and Republican approaches to health care reform. Although Senators Obama and McCain have a very different approach to health reform, neither plan is likely to enjoy any kind of mandate.

Current Legislation. One of the major legislative proposals to watch during the health reform debate this year, S.334, The Healthy Americans Act, includes components that appeal to both Democrats and Republicans. The plan pleases Democrats by assuring that every individual will have access to coverage and includes the financing to ensure nearly universal coverage in the short term. Republicans like the plan because it moves away from the third-party employer-based payment system to one of individual responsibility and the promise of a more competitive market.

Senator Wyden (D-OR) introduced S. 334, The Healthy Americans Act, along with 15 Senate co-sponsors, who range in political ideology from Bennett (R-UT), the bill’s cosponsor, to Cantwell (D-WA), Lieberman (I-CT), Grassley (R-IA), Crapo (R-ID) and Gregg (R-NH). The Wyden bill aims to achieve universal coverage by shifting away from the employer-based system of health care coverage. Instead of companies helping to buy insurance for their workers, Wyden proposes that private insurers offer coverage directly to consumers. Individuals would receive a flat personal tax deduction. Employers could continue to offer employees health care coverage, but would be required to pay a tax based upon a sliding scale of 3% to 26% of the cost of basic health insurance—tied to their size and revenue per employee. Employers that currently offer coverage would transfer the money they now spend on employee health insurance to workers’ wages.

The Congressional Budget Office and the Joint Committee on Taxation reports that the Wyden plan would be budget neutral by 2014, and could be implemented as early as 2012.

While the Wyden Bill has bipartisan appeal in Congress, some companies are concerned about the Bill’s effect on their bottom lines. In exchange for all of the new business, the Bill would subject insurers to more regulation including minimum loss ratios and a complex bid process that would likely result in narrow premium margins. Some large insurance companies like Aetna and Cigna have made moves to target the individual, or non-group market in order to prepare for the potential of a health care overhaul. Most insurers, however, remain hesitant to move into individual markets, and remain committed to expanding coverage through the employer-based system.

Similarly, a number of labor unions and employers are hesitant to change the employer-based system. The Wyden Bill would require employers who currently provide employee health benefits to convert their existing health support into higher wages. In addition, employers would have to make “fair share” contributions to help fund the state insurance pools that the Bill establishes. The Bill’s changes in tax treatment of health benefits would remove the incentive for

Ten Questions About Tax Policy for the Next Administration and Congress 15

employer-sponsored coverage, and cause most employers to cease sponsoring health plans. The legislation would also include sweeping authority for states to obtain waivers of any federal laws (e.g., ERISA) or regulations related to health coverage. Eliminating the ERISA requirement would subject employer-sponsored plans to state-by-state, or even county or city regulation. Consequently, even though the Wyden proposal allows employers to offer employee health plans, it is difficult to see why employers would continue to do so unless they are bound by existing labor contracts. If the Wyden Bill becomes law, most remaining employer-sponsored plans would simply exist as back-up options for those employees who choose not to enroll in one of the state-sponsored plans.

Legislation has also been introduced in the Senate (e.g., S. 2795, The Small Business Health Options Program Act of 2008) that would provide small business employers with tax credits to cover part of the cost of providing health care to their employees. However, in the absence of comprehensive national health reform, the federal government is likely to relegate more of the responsibility for health insurance coverage to the states. To date, most attempts at health reform have occurred at the state level (e.g., Massachusetts and California) and have dramatically increased employers’ responsibility for providing health coverage.

Assessment:• Over the last decade, the schism between conservatives

favoring an employment-based health care coverage model and liberals (e.g., labor unions) favoring national “single payer” health care coverage has largely disappeared.

• In 2009, Congress and the White House may make a serious effort to limit the tax exclusion for employer-provided health care premiums, and to encourage the individual health insurance market though tax deductions or tax credits.

• Congress and the White House may additionally advance proposals to expand tax incentives for small businesses that provide health insurance for their employees.

• In the absence of comprehensive national health reform, the federal government is likely to relegate more of the responsibility for health insurance coverage to the states. Congress and the White House may seek to increase health insurance coverage by encouraging expansion of existing state health insurance programs (i.e., Medicaid and SCHIP).

• Congress and the courts may additionally move to weaken the ERISA preemption so that states and municipalities can implement more aggressive local health reform initiatives.

10. Where will the new President and Congress look for additional revenue?

Background. The Tax Reform Act of 1986 dramatically expanded the tax base by eliminating or reducing scores of tax preferences and otherwise closing so-called tax “loopholes.” However, since 1986, many new preferences have been adopted, with the Joint Committee on Taxation calculating that there are now 170 “tax expenditures” in

the tax code.49 The GAO indicates that the cost of tax expenditures exceeded the cost of federal discretionary spending for half of the last decade.50 In addition, many sophisticated taxpayers have developed techniques to significantly reduce taxes in ways that some characterize as taking advantage of “loopholes” in the tax code.

While comprehensive tax reform is unlikely in the near term, both major presidential candidates have said that they will repeal and reduce tax loopholes in an effort to broaden the base and raise revenue. Senator McCain has called for closing billions of dollars worth of “corporate tax loopholes,” and Senator Obama has said that he will “level the playing field for all businesses by eliminating special interest loopholes and deductions.”

Senate Finance Committee Chairman Baucus and Ranking Member Grassley have identified the $345 billion annual “tax gap” – the gulf between taxes legally owed and taxes actually collected in a timely fashion – as a drain on the U.S. economy and as a source of revenue to pay for U.S. priorities. In 2006, the rate of voluntary tax compliance dropped from 85 percent to 83.7 percent. Each percentage point drop in the rate of compliance amounts to a $25 billion increase in the annual tax gap. Since 2001, the federal government has failed to collect more than $2 trillion in legally-owed taxes. In addition to focusing on compliance to close the “tax gap,” the Finance Committee has also aggressively looked at closing loopholes and other tax shelters. On August 2, 2007, the Treasury Department issued a report entitled “Reducing the Federal Tax Gap: A Report on Improving Voluntary Compliance” setting forth a detailed strategy for improving voluntary compliance.

“Eliminate corporate welfare in tax code.”—-McCain Budget Plan

“The Tax Code is filled with corporate loopholes and preferential regulations that benefit a handful of companies at the expense of the rest of the business community as well as ordinary people who are hit with higher effective tax rates.”

—Obama ’08 Tax Plan

“Some complain that improving tax compliance will burden taxpayers and decrease their rights. But what about the rights of honest, hard-working taxpayers who do pay the taxes that they owe? Increasing our nation’s rate of voluntary tax compliance is going to take some ingenuity. It will take some elbow grease. It is going to require a multi-faceted approach. It will require addressing services, enforcement and technology.”

-—Max Baucus, April 18, 2007

“[W]hen somebody says: Well, you have got to raise taxes … I say, no, you do not. Let us go after some of this stuff. Let us go after these offshore tax havens. Let us go after these abusive tax shelters. Let us go after this tax gap.”

-—Senator Kent Conrad, Chairman, Senate, Budget Committee

Ten Questions About Tax Policy for the Next Administration and Congress 16

Proposals. Although the presidential candidates have spoken mostly in general terms about “closing loopholes” or “shutting down special interest provisions,” there are several sources that provide an initial “menu” for potential revenue raising options next year.

First, many specific revenue-raising proposals have been made during 2007-08, with the House and Senate passing more than 30 revenue-raising provisions that have not yet been enacted into law. Members of the tax-writing committees have introduced several revenue-raising proposals that are likely to receive serious consideration in the next Congress. Some of the revenue-raising proposals include:

• changing the rules for hedge funds and private equity funds, including treating certain types of publicly traded limited partnerships as corporations and characterizing carried interest as ordinary income rather than capital gain;

• repealing the section 199 manufacturing deduction;

• repealing or limiting tax provisions benefiting the oil and gas industries;

• repealing lower of cost or market and “last-in, first-out” (LIFO) methods of inventory accounting;

• codifying the “economic substance doctrine” regarding tax shelters;

• further limiting deductibility of executive pay and curbing deferred compensation;

• changing tax laws affecting international activities, including delaying the implementation of worldwide interest allocation and eligibility for reduced treaty withholding rates based on residency of foreign parent;

• changing the tax treatment of various financial products;

• making changes to clarify the classification of employees as independent contractors;

• increasing the amortization period for intangibles from 15 to 20 years; and

• increasing various excise taxes, such as on tobacco products, various aspects of air and highway transportation, and tax-exempt organizations.

Second, revenue-raising options may be drawn from proposals made by the Treasury Department, including, in the case of a Democratic Administration, those made during the Clinton Administration.51 The Joint Committee on Taxation has made revenue-raising recommendations in various reports, like its report entitled “Options to Improve Tax Compliance and Reform Tax Expenditures,” dated January 27, 2005 (JCS-02-05) and letter to the Finance Committee

entitled “Additional Options to Improve Tax Compliance,” dated August 3, 2006. Additional revenue options can be gleaned from congressional oversight activities and from congressional support organizations like the Congressional Budget Office and the Government Accountability Office.

Assessment: • Regardless of the outcome of the presidential election, there will

be an intense search by the new Administration and Congress for ways to increase federal tax receipts without broadly raising tax rates. Consequently, politically palatable revenue options that can be characterized as “loophole” closers or proposals to reduce the tax gap will be high on the agenda.

• Many of the likely revenue-raising proposals can be identified today. The starting point is likely to be proposals that have passed the House or Senate but not been enacted into law or that have been made by major players such as the chairmen of the tax committees, the Treasury Department, and the Joint Committee on Taxation.

• It is likely that revenue-raising proposals will be embedded in major tax initiatives put forth by the new Administration and approved by Congress under the fast-track budget reconciliation process. These offsets will be juxtaposed against popular tax relief measures making it politically difficult for adversaries to oppose them.

IV. ConclusionIt is clear that the next Administration and Congress will engage in the most significant tax debate in a generation. At stake will be important decisions regarding $4 trillion in tax law provisions, many of them set to expire in 2010. Congress and a new Administration, whether Democratic or Republican, will wrestle over whether to extend, repeal or substantially modify scores of tax policies that benefit every taxpayer. As this debate unfolds, undoubtedly there will be “winners” and “losers.” Under newly reinstated budget rules, Congress will strive to pay for changes to the tax code and minimize additional debt. Since major spending cuts are unlikely, the practical result will be a search for hundreds of billions of dollars in offsetting tax revenues. The principal focus is likely to be on repealing so-called “tax loopholes.” Particularly at risk are tax provisions that benefit perceived targets of political opportunity, such as large multi-national corporations.

Ten Questions About Tax Policy for the Next Administration and Congress 17

1 2001 Tax Cuts: Economic Growth and Tax Relief Reconciliation Act of 2001, Pub.

L. No. 107-16, 115 Stat. 38 (2001); 2003 Tax Cuts: Jobs and Growth Tax Relief

Reconciliation Act of 2003, Pub. L. No. 108-27, 117 Stat. 752 (2003).

2 The current (October 2008) “conventional wisdom” is that Democrats will significantly

expand their majority in both the House (net gain of 10-20 seats), where they currently

have an advantage of 235-198 and in the Senate (net gain of 4-7 seats), where they

currently have an advantage of 51-49.

3 Office of Management and Budget. Mid-Session Review, Budget of the U.S.

Government, Fiscal Year 2009, at 34 (July 28, 2008).

4 For example, pay-go rules were waived for the following: Stimulus Bill: Economic

Stimulus Act of 2008, Pub. L. No. 110-185, 122 Stat. 614, (2008); 2007 AMT Patch:

Tax Increase Prevention Act of 2007, Pub. L. No. 110-166, 121 Stat. 2461 (2007);

War Supplemental Bills: U.S. Troop Readiness, Veterans’ Care, Katrina Recovery, and

Iraq Accountability Appropriations Act of 2007. Pub. L. No. 110-28, 121 Stat. 112,

at Title VIII (2007); Military Construction and Veterans Affairs Appropriations Act, 2008,

Pub. L. No. 110-252, 122 Stat. 2323 (2008).

5 Senator McCain was one of only two Republican Senators to vote against the 2001

tax cuts (107th Congress, 1st Session, Record Vote 170); he was also one of only 3

Republican Senators to vote against the 2003 tax cuts (108th Congress, 1st Session,

Record Vote 196).

6 Kathy Kiely, McCain Calls for Tax Cuts, Corporate Responsibility, USA Today, April 15,

2008, http://www.usatoday.com/news/politics/election2008/2008-04-15-mccain-

economy_N.htm.

7 Another issue, but outside the scope of this memo, is the tax implications of legislation to

reduce the impact of greenhouse gases.

8 153 Cong. Rec. S5835 (daily ed. June 19, 2008) (Remarks by Sen. Voinovich).

9 Chairman Rangel also has proposed to restore the phaseouts that have the effect of