Embed Size (px)

Citation preview

Terra Secured Income Fund 5, LLC

Consolidated Financial Statements Year Ended December 31, 2015

Terra Secured Income Fund 5, LLC

Contents

Independent Auditor’s Report 3 Consolidated Financial Statements:

Statement of Assets, Liabilities and Members’ Capital 4 Schedule of Investments 5-6 Statement of Operations 7 Statement of Changes in Members’ Capital 8 Statement of Cash Flows 9 Notes to Financial Statements 10-23

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms.

3

Tel: 212-885-8000 Fax: 212 697-1299 www.bdo.com

100 Park Avenue New York, NY 10017

Independent Auditor’s Report

The Managing Member Terra Secured Income Fund 5, LLC

We have audited the accompanying consolidated financial statements of Terra Secured Income Fund 5, LLC, which comprise the consolidated statement of assets, liabilities and members’ capital, including the consolidated schedule of investments, as of December 31, 2015, and the related consolidated statements of operations, changes in members’ capital, and cash flows for the year then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Terra Secured Income Fund 5, LLC as of December 31, 2015, and the results of its operations, changes in its members’ capital, and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

April 4, 2016

Terra Secured Income Fund 5, LLC

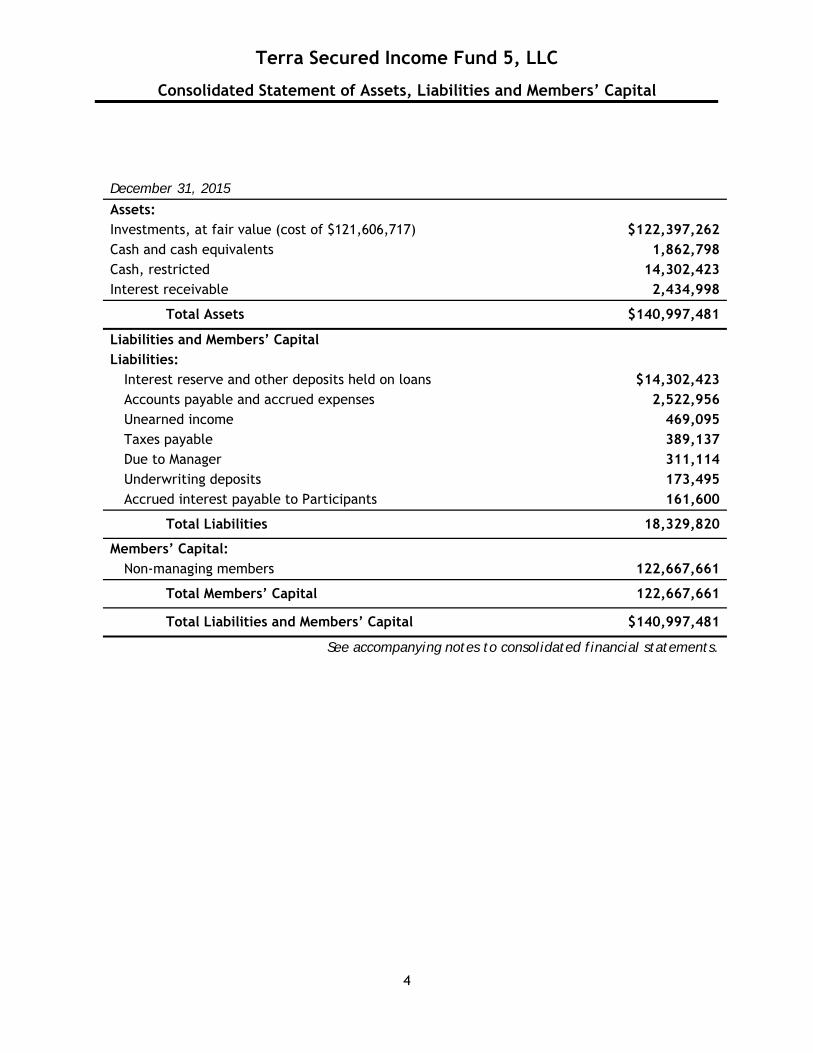

Consolidated Statement of Assets, Liabilities and Members’ Capital

4

December 31, 2015

Assets: Investments, at fair value (cost of $121,606,717) $122,397,262 Cash and cash equivalents 1,862,798Cash, restricted 14,302,423Interest receivable 2,434,998

Total Assets $140,997,481

Liabilities and Members’ Capital Liabilities:

Interest reserve and other deposits held on loans $14,302,423Accounts payable and accrued expenses 2,522,956Unearned income 469,095Taxes payable 389,137Due to Manager 311,114Underwriting deposits 173,495Accrued interest payable to Participants 161,600

Total Liabilities 18,329,820

Members’ Capital: Non-managing members 122,667,661

Total Members’ Capital 122,667,661

Total Liabilities and Members’ Capital $140,997,481

See accompanying notes to consolidated financial statements.

Terra Secured Income Fund 5, LLC

Consolidated Schedule of Investments

5

(1) See Participations Transferred by the Company, in Note 5, for further discussion. (2) See Interest Participated in by the Company, in Note 5, for further discussion.

$ 8,584,100 Preferred equity investment in Maguire Partners-1733 Ocean, LLC due 3/6/2016 at

14.0% per annum.Office $ 12,263,000 $ (3,678,900) $ 8,584,100 7.00%

8,750,000 Preferred equity investment in L.A. Warner Hotel Partners, LLC due 8/4/2019 at

13.25% per annum.Hotel 20,547,600 (11,558,025) 8,989,575 7.33%

5,200,000 Preferred equity investment in SD Carmel Hotel Partners, LLC due 1/31/2017 at 12.0%

per annum.Hotel 6,000,000 (800,000) 5,200,000 4.24%

11,200,000 Loan to TSG-Parcel 1, LLC due 7/10/2016 at 12.0% per annum. Land 18,000,000 (6,800,000) 11,200,000 9.13%

7,896,000 Loan to Steadfast Crestavilla Senior, LLC due 6/11/2016 at 12.0% per annum Land 11,280,000 (3,384,000) 7,896,000 6.44%

Total US - CA 68,090,600 (26,220,925) 41,869,675 34.14%

US - DE 10,000,000 Loan to BPG Office Partners II I/IV LLC due 6/5/2018 at 13.0% per annum. Office 10,000,000 - 10,000,000 8.15%

2,380,000 Loan to CGI Mezz 55MM, LLC due 9/6/2019 at 12.0% per annum current, plus 2.0% per

annum accrued and payable at maturity.Mixed Use 3,506,740 (1,052,022) 2,454,718 2.00%

5,000,000 Loan to Caton Mezz, LLC due 7/27/2016 at 12.0% per annum current, plus 2.0% per

annum accrued and payable at maturity.Office 5,000,000 - 5,000,000 4.08%

11,918,000 Loan to 1100 Biscayne Management Holdco, LLC due 10/9/2017 at 12.0% per annum

current, plus 3.0% per annum accrued and payable at maturity.Hotel 14,500,000 (2,582,000) 11,918,000 9.72%

Total US - FL 23,006,740 (3,634,022) 19,372,718 15.80%

US - GA 3,850,000 Loan to OHM Atlanta Member, LLC due 5/2/2016 at 14.0% per annum current, plus 4.0%

per annum accrued and payable at maturity.Land 5,500,000 (1,650,000) 3,850,000 3.14%

US - NJ 15,621,355 Loan to Essence 144 Urban Renewal, LLC due 1/14/2017 at 12.0% per annum. Multifamily 15,621,355 - 15,621,355 12.72%

2,172,262 Loan to WWML96MEZZ, LLC due 12/31/2018 at 13.0% per annum. Multifamily 2,172,262 - 2,172,262 1.77%

1,150,000 Preferred equity investment in WWML96, LLC due 12/31/2018 at 13.0% per annum. Multifamily 1,150,000 - 1,150,000 0.94%

11,880,000 Participation in loan to QPT 24th Street Mezz LLC, due 6/15/2017 at 12.0% per annum

current, plus 2.0% per annum accrued and payable at maturity. (2)Land 11,880,000 - 11,880,000 9.68%

Total US - NY 15,202,262 - 15,202,262 12.39%

US - PA 1,800,000 Participation in loan to KOP Hotel XXXI Mezz LP, due 12/6/2022 at 13.0% per annum. (2) Hotel 1,800,000 - 1,800,000 1.47%

US - SC 500,000 Participation in loan to SMR Hospitality II, LLC, due 2/5/2019 at 13.5% per annum. (2) Hotel 544,555 - 544,555 0.44%

December 31, 2015

Collateral

Location

Net Princ ipal

Amounts Description of Investments

Property

Type Partic ipation(1)

At Fair Value

Net

Investment

US - CA

US - FL

% of Members’

Capital

Gross

Investment

US - NY

Terra Secured Income Fund 5, LLC

Consolidated Schedule of Investments

6

(1) See Participations Transferred by the Company, in Note 5, for further discussion. (2) See Interest Participated in by the Company, in Note 5, for further discussion.

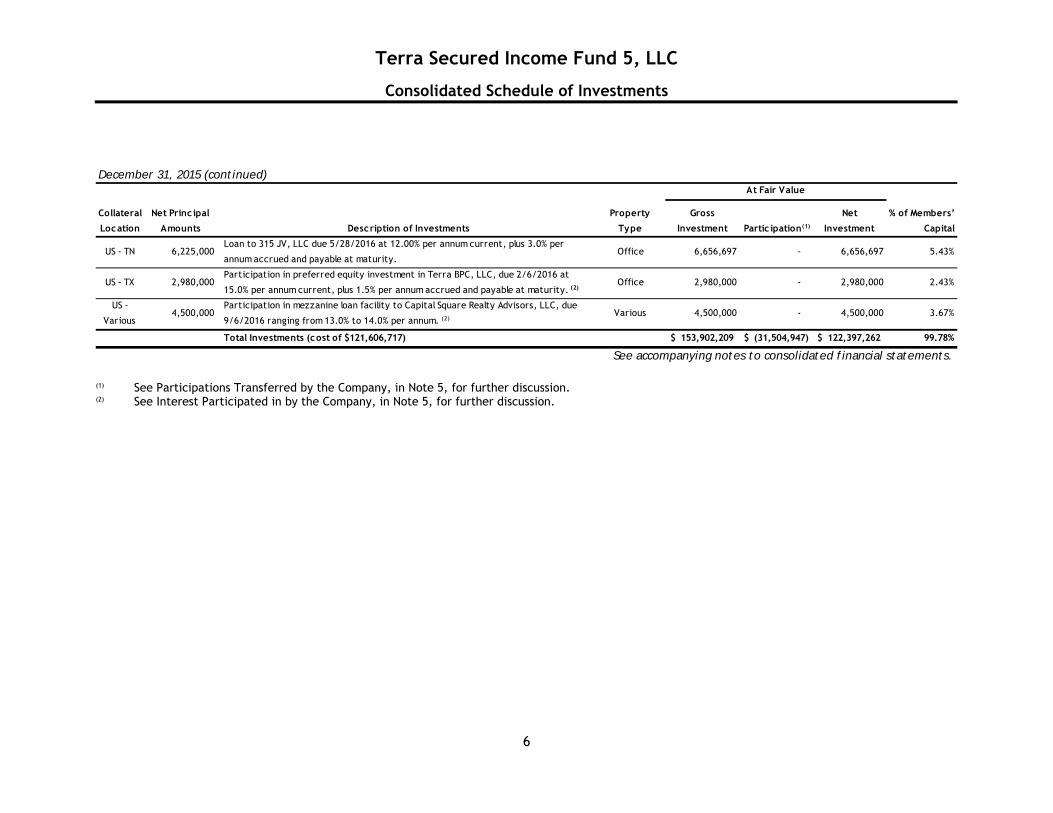

US - TN 6,225,000 Loan to 315 JV, LLC due 5/28/2016 at 12.00% per annum current, plus 3.0% per

annum accrued and payable at maturity.Office 6,656,697 - 6,656,697 5.43%

US - TX 2,980,000 Participation in preferred equity investment in Terra BPC, LLC, due 2/6/2016 at

15.0% per annum current, plus 1.5% per annum accrued and payable at maturity. (2)Office 2,980,000 - 2,980,000 2.43%

US -

Various4,500,000

Participation in mezzanine loan facility to Capital Square Realty Advisors, LLC, due

9/6/2016 ranging from 13.0% to 14.0% per annum. (2)Various 4,500,000 - 4,500,000 3.67%

Total Investments (cost of $121,606,717) $ 153,902,209 $ (31,504,947) $ 122,397,262 99.78%

See accompanying notes to consolidated financial statements.

December 31, 2015 (continued)At Fair Value

Collateral

Location

Net Princ ipal

Amounts Description of Investments

Property

Type

Gross

Investment Partic ipation(1)

Net

Investment

% of Members’

Capital

Terra Secured Income Fund 5, LLC

Consolidated Statement of Operations

7

Year Ended December 31, 2015

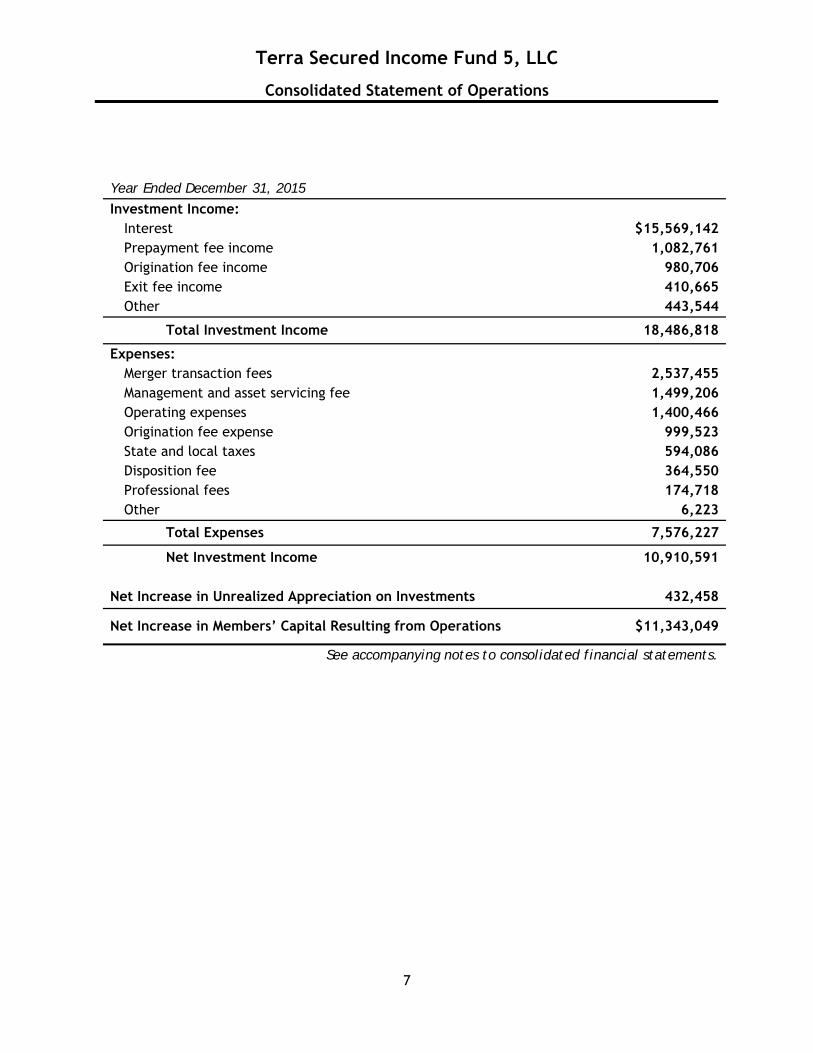

Investment Income: Interest $15,569,142 Prepayment fee income 1,082,761Origination fee income 980,706Exit fee income 410,665Other 443,544

Total Investment Income 18,486,818

Expenses: Merger transaction fees 2,537,455Management and asset servicing fee 1,499,206Operating expenses 1,400,466Origination fee expense 999,523State and local taxes 594,086Disposition fee 364,550Professional fees 174,718Other 6,223

Total Expenses 7,576,227

Net Investment Income 10,910,591

Net Increase in Unrealized Appreciation on Investments 432,458

Net Increase in Members’ Capital Resulting from Operations $11,343,049

See accompanying notes to consolidated financial statements.

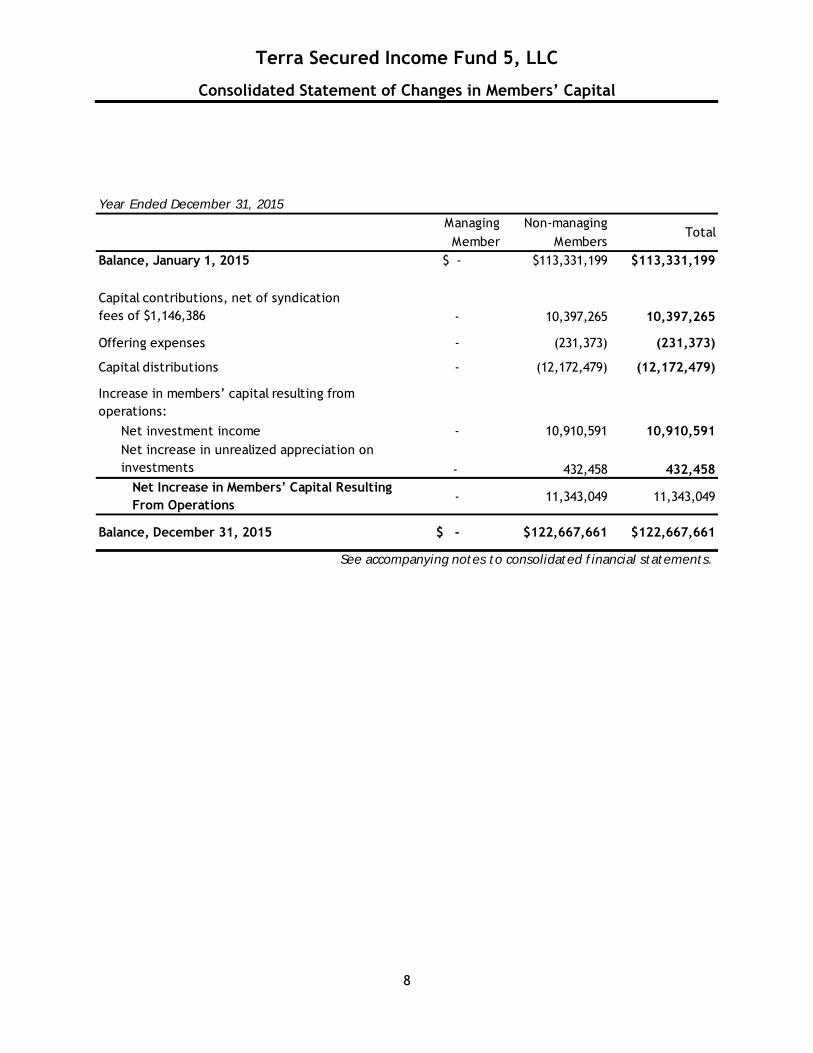

Terra Secured Income Fund 5, LLC

Consolidated Statement of Changes in Members’ Capital

8

Year Ended December 31, 2015

Managing Non-managingMember Members

Balance, January 1, 2015 $ - $113,331,199 $113,331,199

- 10,397,265 10,397,265

Offering expenses - (231,373) (231,373)

Capital distributions - (12,172,479) (12,172,479)

Net investment income - 10,910,591 10,910,591

Net Increase in Members’ Capital Resulting From Operations

- 11,343,049 11,343,049

Balance, December 31, 2015 $ - $122,667,661 $122,667,661

Total

See accompanying notes to consolidated financial statements.

Capital contributions, net of syndication fees of $1,146,386

Increase in members’ capital resulting from operations:

Net increase in unrealized appreciation on investments - 432,458 432,458

Terra Secured Income Fund 5, LLC

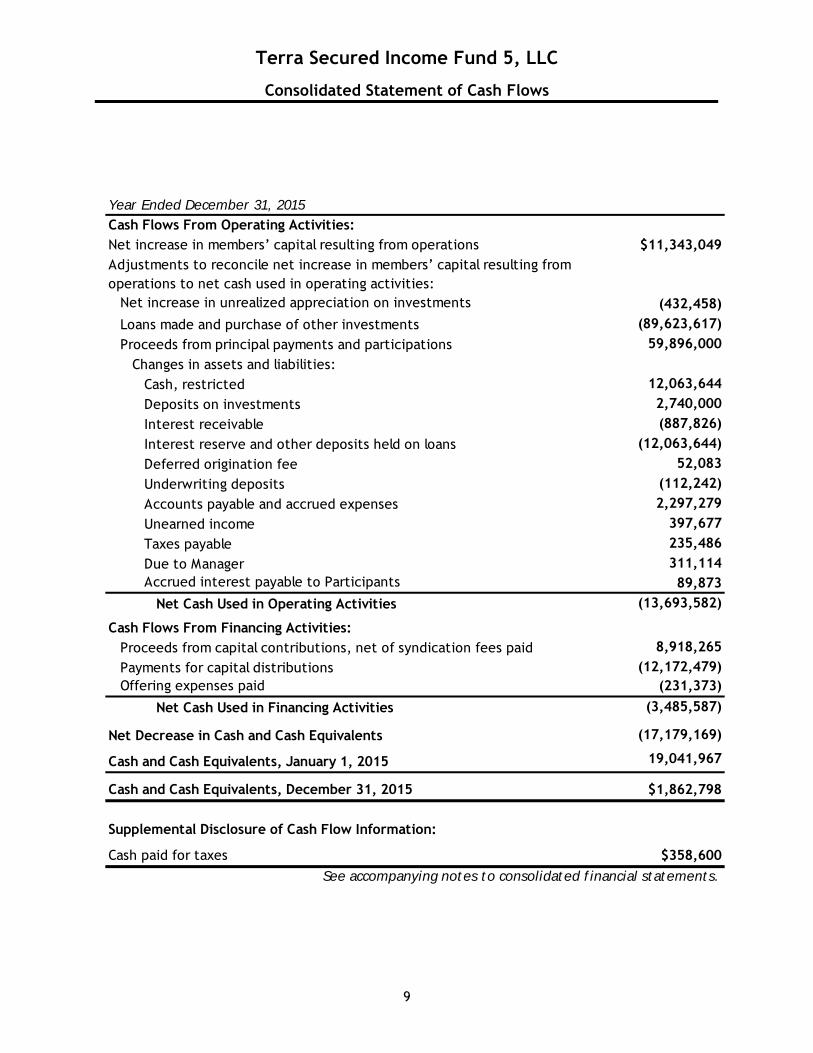

Consolidated Statement of Cash Flows

9

Year Ended December 31, 2015Cash Flows From Operating Activities:Net increase in members’ capital resulting from operations $11,343,049 Adjustments to reconcile net increase in members’ capital resulting from operations to net cash used in operating activities:

Net increase in unrealized appreciation on investments (432,458)

Loans made and purchase of other investments (89,623,617)

Proceeds from principal payments and participations 59,896,000

Changes in assets and liabilities:Cash, restricted 12,063,644

Deposits on investments 2,740,000

Interest receivable (887,826)

Interest reserve and other deposits held on loans (12,063,644)

Deferred origination fee 52,083

Underwriting deposits (112,242)

Accounts payable and accrued expenses 2,297,279

Unearned income 397,677

Taxes payable 235,486

Due to Manager 311,114 Accrued interest payable to Participants 89,873

Net Cash Used in Operating Activities (13,693,582)

Cash Flows From Financing Activities:Proceeds from capital contributions, net of syndication fees paid 8,918,265

Payments for capital distributions (12,172,479)Offering expenses paid (231,373)

Net Cash Used in Financing Activities (3,485,587)

Net Decrease in Cash and Cash Equivalents (17,179,169)

Cash and Cash Equivalents, January 1, 2015 19,041,967

Cash and Cash Equivalents, December 31, 2015 $1,862,798

Supplemental Disclosure of Cash Flow Information:

Cash paid for taxes $358,600

See accompanying notes to consolidated financial statements.

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

10

1. Business (Note 11)

Terra Secured Income Fund 5, LLC (and, together with its consolidated subsidiaries, the “Company”), a Delaware limited liability company, commenced operations on August 8, 2013.

The Company was formed to originate, acquire and structure real estate-related loans, including mezzanine loans, first and second mortgage loans, subordinated mortgage loans, bridge loans, preferred equity investments and other loans related to high quality commercial real estate. The Company has completed its offering period and raised approximately $142 million in gross proceeds. The Company’s investment strategy is to invest substantially all of the net proceeds of membership interests in, and manage a diverse portfolio of, real estate-related loans. The Company seeks to create and maintain a portfolio of investments that generates a low volatility income stream for attractive and consistent cash distributions. The real-estate loans are typically mezzanine loans and preferred equity investments between $3 million and $25 million, with interest rates ranging from 12% to 16% and maturities between one to ten years.

The Company’s actively wholly-owned subsidiaries (all Delaware limited liability companies) were formed for the sole purpose of originating and structuring certain preferred equity investments. These subsidiaries are consolidated on the Company’s financial statements.

Terra Capital Advisors 2, LLC (the “Manager”), a Delaware limited liability company, serves as the managing member and investment adviser of the Company.

In December 2015, the Company’s unitholders approved a merger with Terra Secured Income Fund, LLC (“Terra Fund 1”), Terra Secured Income Fund 2, LLC (“Terra Fund 2”), Terra Secured Income Fund 3, LLC (“Terra Fund 3”) and Terra Secured Income Fund 4, LLC (“Terra Fund 4”) into a new combined Terra Secured Income Fund 5, LLC (individually, “Terra Fund 5” and together, the “Combined Company”) (see Note 11). The Combined Company will continue in existence until December 31, 2023 and expects to be terminated on the five-year anniversary of the completion of the Company’s original offering, which was January 31, 2015, unless extended for up to a maximum of two one-year extensions at the discretion of the Manager, to facilitate an orderly liquidation.

2. Summary of Significant Accounting Policies

Basis of Presentation and Principles of Consolidation

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. The consolidated financial statements of the Company are prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The Company is an investment company, as defined under U.S. GAAP, and applies industry specific guidance in accordance with Accounting Standards Codification (“ASC”) 946, Financial Services – Investment Companies.

Cash and Cash Equivalents

The Company considers all highly liquid investments, with maturities of ninety days or less when purchased, as cash equivalents.

Restricted cash represents cash held as additional collateral by the Company on behalf of the borrower related to the investments in loans or preferred equity instruments for the purpose of such borrowers making interest and property-related operating payments. There is a corresponding liability of the same amount on the consolidated statement of assets, liabilities and members’ capital, “Interest reserve and other deposits held on loans” at December 31, 2015.

The Company maintains all of its cash at financial institutions which, at times, may exceed the amount insured by the Federal Deposit Insurance Corporation.

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

11

Investment Transactions and Investment Income (Expense)

The Company records investment transactions on the trade date. Realized gains or losses on dispositions of investments represent the difference between the original cost of the investment, based on the specific identification method, and the proceeds received from the sale or maturity (exclusive of any prepayment penalties). The Company applies a fair value accounting policy to its investments with changes in unrealized gains and losses recognized in the consolidated statement of operations. Interest and origination fee income and expense are recognized on an accrual basis. Interest income is recorded net of interest income allocated to Participants (Note 5). Excess origination fee income over expense (and excess origination expense over origination fee income) is amortized over the life of the related investment. As prepayment(s) or payment(s), partial or full, occurs on an investment, prepayment and exit fee income, respectively, are recognized.

Valuation of Investments

Secured Loans and Preferred Equity Investments

The Company originates, funds and structures real estate-related loans, including mezzanine loans, first and second mortgage loans, bridge loans and preferred equity investments and other loans related to high quality commercial real estate typically in the $3 million to $25 million range. The loans are made to owners of commercial real estate as part of a property purchase or recapitalization, some of which are shorter in duration and used as a bridge to some future capital or liquidity event. Typically, the Company invests alongside a senior lender and the maturity of the Company’s investment is coterminous with that of the senior lender. The mezzanine loans and preferred equity investments are generally secured by a pledge of the respective borrower's ownership interests in the company that owns the underlying property (the collateral). Second mortgages are generally secured by a subordinated interest in the first mortgage secured by the underlying property.

Market quotations are not readily available for the Company’s real estate-related loan investments, all of which are included in level 3 of the fair value hierarchy, and therefore these investments are valued utilizing a yield approach, i.e. a discounted cash flow methodology to arrive at an estimate of the fair value of each respective investment in the portfolio using an estimated market yield. In following this methodology, investments are evaluated individually, and management takes into account, in determining the risk-adjusted discount rate for each of the Company’s investments, relevant factors, including available current market data on applicable yields of comparable debt / preferred equity instruments, market credit spreads and yield curves, the investment’s yield, covenants of the investment, including prepayment provisions, the portfolio company’s ability to make payments, its net operating income, debt service coverage ratio, the nature, quality, and realizable value of any collateral (and loan to value ratio), the forces that influence the local markets in which the asset (the collateral) is purchased and sold, such as capitalization rates, occupancy rates, rental rates, replacement costs and the anticipated duration of each real estate-related loan investment.

An individual investment fair value is estimated using two different yield models, which are used to discount the cash flows in order to determine fair value.

Discounted Cash Flow Based on the Investment’s Position in the Capital Structure

The position of the Company’s investment within the borrower’s capital structure drives the risk premium on the yield. Based on the Company’s experience in the origination market, pricing is applied for the relevant structure (B-Note, mezzanine and preferred equity structures) with adjustments to yield made 1) for loans with a debt service coverage ratio (“DSCR”) that reflects a

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

12

transition period, and 2) to account for the qualitative variability of both the property and the market in which it resides.

Discounted Cash Flow Based Upon a Risk-Adjusted Discount Rate

The Company constructs a hypothetical loan spread that is the sum of 1) the interpolated swap rate for loans of a similar duration to the Company’s investment, 2) a debt-structure based add-on (i.e. a mezzanine loan or preferred equity investment), 3) a market position loan spread that is based on the borrower’s indebtedness, from first to last dollar of the Company’s exposure, and the borrower’s DSCR, 4) an adjustment made for loans with a DSCR reflecting a transition period and 5) an adjustment to yield made to account for the qualitative variability of both the property and the market in which it resides.

Previously, the Company valued its investments utilizing an average of two yield approaches that utilized different market inputs. As of December 31, 2015, the Company’s investments were valued using a discounted cash flow methodology with independent third party estimated market yields. The Company evaluated the appropriateness of the specialist's discount rates utilizing its valuation methodology above. The effect of no longer utilizing the average of different market inputs and yield models was not material.

The Manager is ultimately and solely responsible for making a good faith determination of the Company’s investments. While the Manager believes its valuation method is appropriate and consistent with those used by other market participants, the use of different methodologies or assumptions to determine fair value, could result in a different estimate of fair value at the reporting date. The fair values determined by the Manager as of December 31, 2015 may differ significantly from the values that would have been used had a readily available market for such investments existed, or had such investments been sold at the determination dates, and these differences could be material.

Fair Value of Financial Instruments

The fair values of the Company’s assets and liabilities, which qualify as financial instruments, approximate the carrying amount presented on the consolidated statement of assets, liabilities and members’ capital.

Capital Contributions Received in Advance

Contributions received in advance of the effective admittance date are recorded as capital contributions received in advance on the consolidated statement of assets, liabilities and members’ capital.

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of gains (losses), income and expenses during the reporting period. Actual results could significantly differ from those estimates.

Income Taxes

No provision for U.S. Federal and state income taxes has been made in the accompanying consolidated financial statements, as individual members are responsible for their proportionate share of the Company’s taxable income. The Company, however, is liable for New York City Unincorporated Business Tax (“UBT”), and various other municipality taxes. New York City (“NYC”) imposes UBT at a statutory rate of 4% on net income generated from ordinary business activities

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

13

carried on in NYC. Deferred tax assets and liabilities are recognized for the expected future tax consequences of temporary differences between the financial statements and tax basis assets and liabilities using enacted tax rates in effect for the year in which differences are expected to reverse. Such deferred tax assets and liabilities are not material.

The Company recognizes a tax benefit from an uncertain tax position only if it is more likely than not that the position is sustainable, based solely on its technical merits and consideration of the relevant taxing authority’s widely understood administrative practices and precedents. If this threshold is met, management measures the tax benefit as the largest amount of benefit that is more likely than not of being realized upon ultimate settlement. The Company is subject to potential examination by taxing authorities in various jurisdictions. The Company recognizes interest and penalties, if any, as income tax expense in the consolidated statement of operations. The open tax years under potential examination vary by jurisdiction. As of December 31, 2015, there was no impact to the consolidated financial statements related to accounting for uncertain income tax positions.

3. Significant Risk Factors

In the normal course of business, the Company enters into transactions in various financial instruments. The Company’s financial instruments are subject to, but are not limited to, the following risks:

Market Risk

The Company’s investments are highly illiquid and there is no assurance that the Company will achieve its investment objectives, including targeted returns. Due to the illiquidity of the investments, valuation of the investments may be difficult, as there generally will be no established markets for these investments. As the Company's investments are carried at fair value with fair value changes recognized in the consolidated statement of operations, all changes in market conditions will directly affect members’ capital.

Credit Risk

Credit risk represents the potential loss that the Company would incur if the borrowers failed to perform pursuant to the terms of their obligations to the Company. Thus, the value of the underlying collateral, the creditworthiness of the borrower or other counterparty, and the priority of the Fund's lien on the borrower's assets are of importance. The Company minimizes its exposure to credit risk by limiting exposure to any one individual borrower and any one asset class. Additionally, the Company employs an asset management approach and monitors the portfolio of investments, through, at a minimum, quarterly financial review of property performance including net operating income, loan to value, DSCR and the debt yield. The Company also requires certain borrowers to establish a cash reserve, as a form of additional collateral, for the purpose of providing for future interest or property-related operating payments.

Mezzanine loans and preferred equity investments are subordinate to senior mortgage loans and, therefore, involve a higher degree of risk. In the event of a default, mezzanine loans and preferred equity investments will be satisfied only after the senior lender's investment is fully recovered. As a result, in the event of a default, the Company may not recover all of its investment.

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

14

Concentration Risk

The Company holds real estate related investments. Thus, the investment portfolio of the Company may be subject to a more rapid change in value than would be the case if the Company were required to maintain a wide diversification among industries, companies and types of investments. The result of such concentration in real estate assets is that a loss in such investments could materially reduce the Company’s capital.

Liquidity Risk

Liquidity risk represents the possibility that the Company may not be able to sell its positions at a reasonable price in times of low trading volume, high volatility and financial stress.

The Company may make investments which may not be advantageously disposed of prior to the date scheduled for dissolution of the Company. Additionally, due to the illiquid nature of the Company’s current or future positions, as well as the uncertainties of the reorganization and active management process, the Manager is unable to predict with confidence what the exit strategy will ultimately be for any given position. Although the Manager expects that investments will be able to be disposed of prior to dissolution, the Company may have to sell, distribute or otherwise dispose of investments at a disadvantageous time for a price which is less than the price that could have been obtained if they were held for a longer period of time.

Interest Rate Risk

Interest rate risk represents the effect from a change in interest rates, which could result in an adverse change in the fair value of our interest-bearing financial instruments.

Prepayment Risk

Prepayments can either positively or adversely affect the yields on investments. Prepayments on debt instruments, where permitted under the debt documents, are influenced by changes in current interest rates and a variety of economic, geographic and other factors beyond the Company’s control, and consequently, such prepayment rates cannot be predicted with certainty. If the Company does not collect a prepayment fee in connection with a prepayment or is unable to invest the proceeds of such prepayments received, the yield on the portfolio will decline. In addition, the Company may acquire assets at a discount or premium and if the asset does not repay when expected, the anticipated yield may be impacted. Under certain interest rate and prepayment scenarios the Company may fail to recoup fully our cost of acquisition of certain investments.

Use of Leverage

As part of the Company’s investment strategy, the Company may borrow and utilize leverage; however, the Company historically has not utilized leverage in connection with originating or acquiring real estate related loans. While borrowing and leverage present opportunities for increasing total return, they may have the effect of potentially creating or increasing losses (Note 11).

Property Acquisitions

The Company may find it necessary to take possession of collateral including, without limitation, an asset or business, through a purchase or foreclosure action. Borrowers may resist mortgage foreclosure or sales actions by asserting numerous claims and defenses, which delay both repayments of existing loan investments and/or acquisition of the collateral and add cost to such actions.

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

15

There can be no assurance that the Company will be able to successfully operate, hold or maintain the collateral in accordance with the Company’s expectations.

Further, there can be no assurance that there will be a ready market for resale of foreclosed or acquired properties because investments in real estate generally are not liquid and holding periods are difficult to predict. In addition, there may be significant expenditures associated with holding real property, including real estate taxes and maintenance costs. The liquidation proceeds upon sale of the real estate may be less than the amount invested in the loan, and its fair value and such differences could be material.

4. Investments and Fair Value

The Company values all investments at fair value. U.S. GAAP establishes a hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs. Observable inputs are inputs that market participants would use in pricing the investment based on available market data. Unobservable inputs are inputs that reflect management’s assumptions about the assumptions and inputs market participants would use in valuing the investment based on the best information available in the circumstances.

The hierarchy is broken down into three levels based on the observability of inputs as follows:

Level 1 - Valuations based on quoted prices in active markets for identical investments.

Level 2 - Valuations based on (i) quoted prices in markets that are not active; (ii) quoted prices for similar investments in active markets; and (iii) inputs other than quoted prices that are observable or inputs derived from or corroborated by market data.

Level 3 - Valuations based on inputs that are unobservable, supported by little or no market activity and that are significant to the overall fair value measurement.

The availability of observable inputs can vary from investment to investment and is affected by a wide variety of factors, such as, the type of product, whether the product is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the transaction.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Manager’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers factors specific to the investment.

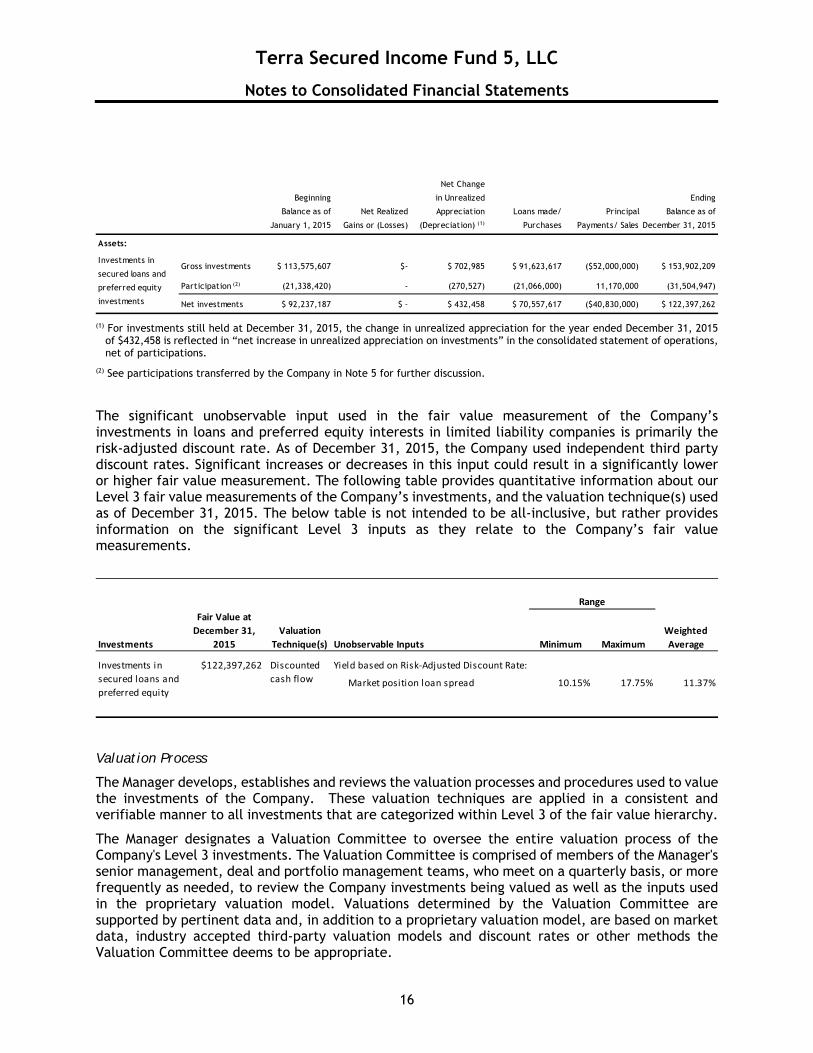

All of the Company’s investments are included in Level 3 of the fair value hierarchy. Changes in Level 3 investments for the year ended December 31, 2015 were as follows:

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

16

(1) For investments still held at December 31, 2015, the change in unrealized appreciation for the year ended December 31, 2015

of $432,458 is reflected in “net increase in unrealized appreciation on investments” in the consolidated statement of operations, net of participations.

(2) See participations transferred by the Company in Note 5 for further discussion.

The significant unobservable input used in the fair value measurement of the Company’s investments in loans and preferred equity interests in limited liability companies is primarily the risk-adjusted discount rate. As of December 31, 2015, the Company used independent third party discount rates. Significant increases or decreases in this input could result in a significantly lower or higher fair value measurement. The following table provides quantitative information about our Level 3 fair value measurements of the Company’s investments, and the valuation technique(s) used as of December 31, 2015. The below table is not intended to be all-inclusive, but rather provides information on the significant Level 3 inputs as they relate to the Company’s fair value measurements.

Valuation Process

The Manager develops, establishes and reviews the valuation processes and procedures used to value the investments of the Company. These valuation techniques are applied in a consistent and verifiable manner to all investments that are categorized within Level 3 of the fair value hierarchy.

The Manager designates a Valuation Committee to oversee the entire valuation process of the Company's Level 3 investments. The Valuation Committee is comprised of members of the Manager's senior management, deal and portfolio management teams, who meet on a quarterly basis, or more frequently as needed, to review the Company investments being valued as well as the inputs used in the proprietary valuation model. Valuations determined by the Valuation Committee are supported by pertinent data and, in addition to a proprietary valuation model, are based on market data, industry accepted third-party valuation models and discount rates or other methods the Valuation Committee deems to be appropriate.

Beginning

Balance as of

January 1, 2015

Net Realized

Gains or (Losses)

Net Change

in Unrealized

Appreciation

(Depreciation) (1)

Loans made/

Purchases

Principal

Payments/ Sales

Ending

Balance as of

December 31, 2015

Assets:

Gross investments $ 113,575,607 $- $ 702,985 $ 91,623,617 ($52,000,000) $ 153,902,209

Participation (2) (21,338,420) - (270,527) (21,066,000) 11,170,000 (31,504,947)

Net investments $ 92,237,187 $ - $ 432,458 $ 70,557,617 ($40,830,000) $ 122,397,262

Investments in

secured loans and

preferred equity

investments

$122,397,262 Yield based on Risk‐Adjusted Discount Rate:

Market position loan spread 10.15% 17.75% 11.37%

Range

Weighted

AverageInvestments

Fair Value at

December 31,

2015

Valuation

Technique(s) Unobservable Inputs Minimum Maximum

Investments in

secured loans and

preferred equity

Discounted

cash flow

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

17

5. Related Party Transactions

Origination Fee Expense

Pursuant to the Company’s Agreement, the Manager or its affiliates receives an origination fee in the amount of 1% of the amount used to originate, fund, acquire or structure real estate-related loans, including any third party expenses related to such investments. For the year ended December 31, 2015, the Manager earned an origination fee of $999,523.

Organization Expense and Offering Costs

Under the terms of the Agreement, the Manager receives a reimbursement for expenses incurred in the organization of the Company and the offering of its member units at a rate of 2% of the gross offering proceeds, irrespective of the actual costs incurred. For the year ended December 31, 2015, the Company paid the Manager $231,373 for such expenses, which has been deducted from members’ capital. Organizational expenses were not material.

Selling Commission Fees

Terra Capital Markets, LLC, an affiliate of the Manager, serves as the dealer manager for the sale of the Company’s member units and receives compensation of 3% in dealer manager fees, 6% in selling commission and a 1% broker dealer fee. Most of these fees are re-allowed to independent broker dealers, and financial advisors. These fees amounted to $1,146,386 for the year ended December 31, 2015 and have been deducted from capital contributions received as syndication fees.

Management Fee

Under the terms of the Agreement, the Manager or its affiliates provides the Company with certain investment management services in return for a management fee. The Company pays a monthly asset management fee at an annual rate of 1% of the aggregate funds under management, which includes the loan origination price or aggregate gross acquisition price, as defined in the Agreement, for each real estate related investment and cash held by the Company. For the year ended December 31, 2015, the Manager earned an asset management fee of $1,216,785, which is included in management and asset servicing fees as reflected on the consolidated statement of operations. Asset Servicing Fee

The Manager or its affiliates receives from the Company a monthly servicing fee at an annual rate of .25% of the aggregate gross origination price or acquisition price for each real estate-related loan held by the Company. For the year ended December 31, 2015, the Manager earned an asset servicing fee of $282,421, which is included in management and asset servicing fees as reflected on the consolidated statement of operations.

Operating Expenses

The Company reimburses the Manager for operating expenses incurred in connection with services provided to the operations of the Company, including the Company’s allocable share of the Manager’s overhead, such as rent, employee costs, utilities, and technology costs. For the year ended December 31, 2015, as reflected in the consolidated statement of operations, the Company reimbursed the Manager for operating expenses of $1,400,466.

Disposition Fee

Pursuant to the Agreement, the Manager or its affiliates receives a disposition fee in the amount of 1% of the gross sale price received by the Company from the disposition of any real estate-related investment, or any portion of, or interest in, any real estate-related investment. The disposition

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

18

fee is paid concurrently with the closing of any such disposition of all or any portion of any real estate-related investment or any interest therein. The Company does not pay a disposition fee upon the maturity, prepayment, workout, modification or extension of a loan or other debt-related investment unless there is a corresponding fee paid by the borrower, in which case the disposition fee is the lesser of (i) 1.0% of the principal amount of the loan or debt-related investment prior to such transaction or (ii) the amount of the fee paid by the borrower in connection with such transaction. If the Company takes ownership of a property as a result of a workout or foreclosure of a loan, the Company will pay a disposition fee upon the sale of such property equal to 1.0% of the sales price. For the year ended December 31, 2015, the Manager earned a disposition fee of $364,550.

Co-Investor Loans

In the normal course of business, the Company may enter into Participation Agreements (the “PAs”) with related parties, primarily other affiliated funds managed by the Manager and/or its affiliates (“the Participants”). The purpose of the PAs is to allow the Company and an affiliate to originate a specified investment when, individually, the Company does not have the liquidity to do so or to achieve a certain level of portfolio diversification. The Company may transfer portions of its investments to other Participants or it may be a Participant to an investment held by another entity. In addition, the Company sells participation interests to an affiliate not less than 90 days after the origination of an investment to allow for greater diversification within the Company’s portfolio as well as sharing investment economics with the affiliate.

U.S. GAAP establishes accounting and reporting standards for transfers of financial assets and provides consistent standards for distinguishing transfers of financial assets that are sales from transfers that are secured borrowings. The Company’s management has determined that the participation agreements it enters into represent secured borrowings.

Participations Transferred by the Company

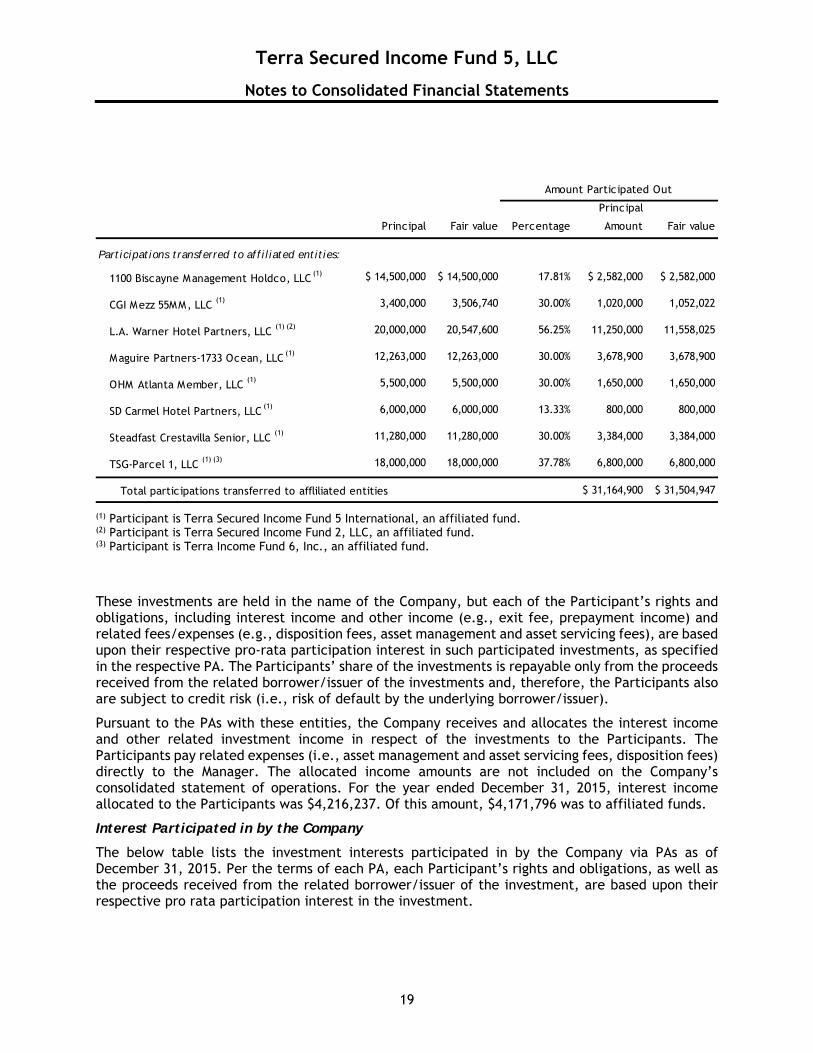

At December 31, 2015, the following investments were subject to PAs that the Company transferred to affiliated entities:

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

19

(1) Participant is Terra Secured Income Fund 5 International, an affiliated fund. (2) Participant is Terra Secured Income Fund 2, LLC, an affiliated fund. (3) Participant is Terra Income Fund 6, Inc., an affiliated fund. These investments are held in the name of the Company, but each of the Participant’s rights and obligations, including interest income and other income (e.g., exit fee, prepayment income) and related fees/expenses (e.g., disposition fees, asset management and asset servicing fees), are based upon their respective pro-rata participation interest in such participated investments, as specified in the respective PA. The Participants’ share of the investments is repayable only from the proceeds received from the related borrower/issuer of the investments and, therefore, the Participants also are subject to credit risk (i.e., risk of default by the underlying borrower/issuer).

Pursuant to the PAs with these entities, the Company receives and allocates the interest income and other related investment income in respect of the investments to the Participants. The Participants pay related expenses (i.e., asset management and asset servicing fees, disposition fees) directly to the Manager. The allocated income amounts are not included on the Company’s consolidated statement of operations. For the year ended December 31, 2015, interest income allocated to the Participants was $4,216,237. Of this amount, $4,171,796 was to affiliated funds.

Interest Participated in by the Company

The below table lists the investment interests participated in by the Company via PAs as of December 31, 2015. Per the terms of each PA, each Participant’s rights and obligations, as well as the proceeds received from the related borrower/issuer of the investment, are based upon their respective pro rata participation interest in the investment.

Principal Fair value Percentage

Principal

Amount Fair value

Participations transferred to affiliated entities:

1100 Biscayne Management Holdco, LLC (1) $ 14,500,000 $ 14,500,000 17.81% $ 2,582,000 $ 2,582,000

CGI Mezz 55MM, LLC (1) 3,400,000 3,506,740 30.00% 1,020,000 1,052,022

L.A. Warner Hotel Partners, LLC (1) (2) 20,000,000 20,547,600 56.25% 11,250,000 11,558,025

Maguire Partners-1733 Ocean, LLC (1) 12,263,000 12,263,000 30.00% 3,678,900 3,678,900

OHM Atlanta Member, LLC (1) 5,500,000 5,500,000 30.00% 1,650,000 1,650,000

SD Carmel Hotel Partners, LLC (1) 6,000,000 6,000,000 13.33% 800,000 800,000

Steadfast Crestavilla Senior, LLC (1) 11,280,000 11,280,000 30.00% 3,384,000 3,384,000

TSG-Parcel 1, LLC (1) (3) 18,000,000 18,000,000 37.78% 6,800,000 6,800,000

Total participations transferred to affliliated entities $ 31,164,900 $ 31,504,947

Amount Participated Out

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

20

(1) Participation through Terra Secured Income Fund, LLC, an affiliated fund. (2) Participation through Terra Secured Income Fund 3, LLC, an affiliated fund. (3) Participation through Terra Secured Income Fund 2, LLC, an affiliated fund. (4) Participation through Terra Income Fund 6, Inc., an affiliated fund. Due to Manager

As of December 31, 2015, $311,114 was due to the Manager, as reflected on the consolidated statement of assets and liabilities, which was primarily due to merger transaction fees paid by the Manager (Note 11).

6. Members’ Capital

Capital Contributions

On January 31, 2015, the offering period ended and the Company stopped accepting capital contributions.

Capital Distributions

At the discretion of the Manager, the Company may make distributions from net cash flow from operations, net disposition proceeds, or other cash available for distribution. Distributions are made to the non-managing members in proportion to their unit holdings until they receive a return of their initial Deemed Capital Contribution, as defined in the Agreement, plus an 8.5% cumulative, non-compounded return on unreturned capital contributions, after which time distributions are made 15% to the Manager (“carried interest”) and 85% to the non-managing members. For the year ended December 31, 2015 there was no carried interest.

At the discretion of the Manager, a reserve of 5% of cash from operations may be established in order to repurchase units from non-managing members. The Manager is under no obligation to redeem non-managing members’ units. As of December 31, 2015, no such reserve was established.

Allocation of Income (Loss)

Profits and losses are allocated to the members in proportion to the distributions made to them in a given calendar year.

Participating

interest

Face

Value

SMR Hospitality II LLC (1) 16.67% $500,000

Terra BPC LLC (2) 19.38% 2,980,000

Capital Square Realty Advisors LLC (3) 42.86% 4,500,000

KOP Hotel XXXI Mezz LP (4) 31.03% 1,800,000

QPT 24th Street Mezz LLC (4) 79.20% 11,880,000

Total interests participated in by the Company $21,660,000

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

21

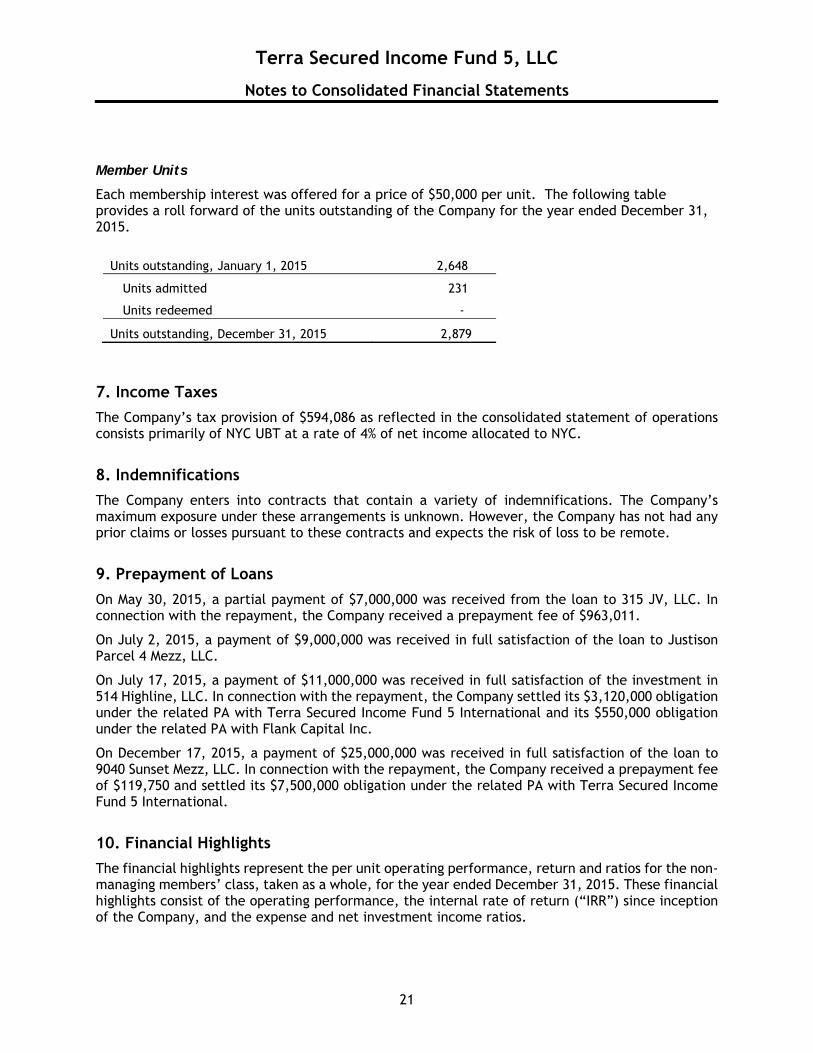

Member Units

Each membership interest was offered for a price of $50,000 per unit. The following table provides a roll forward of the units outstanding of the Company for the year ended December 31, 2015.

Units outstanding, January 1, 2015 2,648

Units admitted 231

Units redeemed -

Units outstanding, December 31, 2015 2,879

7. Income Taxes

The Company’s tax provision of $594,086 as reflected in the consolidated statement of operations consists primarily of NYC UBT at a rate of 4% of net income allocated to NYC.

8. Indemnifications

The Company enters into contracts that contain a variety of indemnifications. The Company’s maximum exposure under these arrangements is unknown. However, the Company has not had any prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

9. Prepayment of Loans

On May 30, 2015, a partial payment of $7,000,000 was received from the loan to 315 JV, LLC. In connection with the repayment, the Company received a prepayment fee of $963,011.

On July 2, 2015, a payment of $9,000,000 was received in full satisfaction of the loan to Justison Parcel 4 Mezz, LLC.

On July 17, 2015, a payment of $11,000,000 was received in full satisfaction of the investment in 514 Highline, LLC. In connection with the repayment, the Company settled its $3,120,000 obligation under the related PA with Terra Secured Income Fund 5 International and its $550,000 obligation under the related PA with Flank Capital Inc.

On December 17, 2015, a payment of $25,000,000 was received in full satisfaction of the loan to 9040 Sunset Mezz, LLC. In connection with the repayment, the Company received a prepayment fee of $119,750 and settled its $7,500,000 obligation under the related PA with Terra Secured Income Fund 5 International.

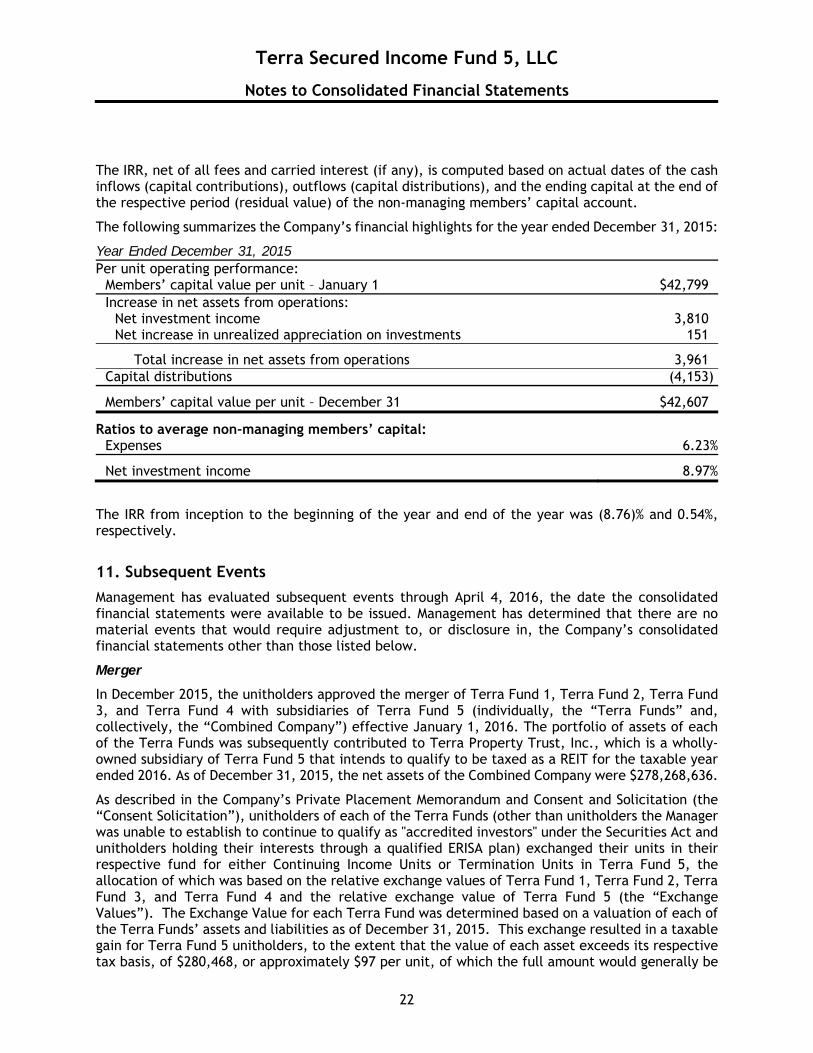

10. Financial Highlights

The financial highlights represent the per unit operating performance, return and ratios for the non-managing members’ class, taken as a whole, for the year ended December 31, 2015. These financial highlights consist of the operating performance, the internal rate of return (“IRR”) since inception of the Company, and the expense and net investment income ratios.

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

22

The IRR, net of all fees and carried interest (if any), is computed based on actual dates of the cash inflows (capital contributions), outflows (capital distributions), and the ending capital at the end of the respective period (residual value) of the non-managing members’ capital account.

The following summarizes the Company’s financial highlights for the year ended December 31, 2015:

Year Ended December 31, 2015 Per unit operating performance:

Members’ capital value per unit – January 1 $42,799Increase in net assets from operations:

Net investment income 3,810Net increase in unrealized appreciation on investments 151

Total increase in net assets from operations 3,961 Capital distributions (4,153)

Members’ capital value per unit – December 31 $42,607

Ratios to average non-managing members’ capital: Expenses 6.23%

Net investment income 8.97%

The IRR from inception to the beginning of the year and end of the year was (8.76)% and 0.54%, respectively.

11. Subsequent Events

Management has evaluated subsequent events through April 4, 2016, the date the consolidated financial statements were available to be issued. Management has determined that there are no material events that would require adjustment to, or disclosure in, the Company’s consolidated financial statements other than those listed below.

Merger

In December 2015, the unitholders approved the merger of Terra Fund 1, Terra Fund 2, Terra Fund 3, and Terra Fund 4 with subsidiaries of Terra Fund 5 (individually, the “Terra Funds” and, collectively, the “Combined Company”) effective January 1, 2016. The portfolio of assets of each of the Terra Funds was subsequently contributed to Terra Property Trust, Inc., which is a wholly-owned subsidiary of Terra Fund 5 that intends to qualify to be taxed as a REIT for the taxable year ended 2016. As of December 31, 2015, the net assets of the Combined Company were $278,268,636.

As described in the Company’s Private Placement Memorandum and Consent and Solicitation (the “Consent Solicitation”), unitholders of each of the Terra Funds (other than unitholders the Manager was unable to establish to continue to qualify as "accredited investors" under the Securities Act and unitholders holding their interests through a qualified ERISA plan) exchanged their units in their respective fund for either Continuing Income Units or Termination Units in Terra Fund 5, the allocation of which was based on the relative exchange values of Terra Fund 1, Terra Fund 2, Terra Fund 3, and Terra Fund 4 and the relative exchange value of Terra Fund 5 (the “Exchange Values”). The Exchange Value for each Terra Fund was determined based on a valuation of each of the Terra Funds’ assets and liabilities as of December 31, 2015. This exchange resulted in a taxable gain for Terra Fund 5 unitholders, to the extent that the value of each asset exceeds its respective tax basis, of $280,468, or approximately $97 per unit, of which the full amount would generally be

Terra Secured Income Fund 5, LLC

Notes to Consolidated Financial Statements

23

treated as ordinary income. As the Exchange Values are based on the valuations of the individual assets, a loan premium (or discount) will be recognized to the extent that the value of any investment contributed by a Fund to the Combined Company is greater (or less) than the unamortized cost of that investment. Holders of Continuing Income Units will receive distributions at a fixed rate of 9% of the par value of their units per annum and Termination Units will receive distributions at a fixed rate of 6% of the par value of their units per annum until such Terminating Units are liquidated. The sum of the Continuing Income Units and Termination Units will comprise the total outstanding units for the Combined Company and income will be allocated based on each unit's ratable share of income.

In connection with the Consent Solicitation, merger transaction fees for the year ended December 31, 2015 of $2,537,455 allocated to the Company is made up of a voting advisory fee of $750 per unit to be paid to participating broker dealers, a dealer manager fee of 0.5%, and reimbursement of actual costs incurred for legal, accounting, and other professional services in connection with the consent solicitation. Merger transaction fees were allocated across the Terra Funds in accordance with the Exchange Values.

In addition, the Combined Company is offering existing unitholders of the Terra Funds the opportunity to increase their investments in the Combined Company through the purchase of Continuing Income Units at a price of $47,000 per unit (the “Rights Offering”), which reflects the reduced front-end load relative to the existing unitholders' initial investment of $50,000 per unit. On March 31, 2016, the date the Rights Offering ended, the Combined Company raised approximately $24.4 million.

Investments

On March 8, 2016, the Combined Company closed a two-year first mortgage bridge loan to Maguire Partners-1733 Ocean, LLC in the amount of $54,000,000 with interest at one month LIBOR “L” + 8.5% (subject to a 2.0% L cap and a 0.5% L floor). The loan is secured by a pledge of 100% of the borrower’s equity interest in a 94,656 square foot Class-A office building in Santa Monica, CA. In connection this loan, the Combined Company financed $34,000,000 from Centennial Commercial Funding at a rate of L + 5.25%.