Embed Size (px)

Citation preview

1

Testing Spanish regional market integration for fuel oil retailers

Jacint Balaguer

Department of Economics, Universitat Jaume I, Castelló (Spain)

Jordi Ripollés

Department of Economics, Universitat Jaume I, Castelló (Spain)

Abstract

This paper investigates whether the regional markets in the Spanish fuel sector are

integrated. For it, we analyse the transmission of wholesale oil prices to retailing pre-tax

prices. Our results indicate that the degree of cost pass-through differs across regions,

which is evidence in favour of the presence of market segmentation. Moreover, similarities

in the degree of cost pass-through across provinces (NUTS 3) increase as they belong to the

same autonomous community (NUTS 2). This last outcome suggests that differences in the

regulations of the communities and the specific criteria of their governments are hindering

the integration of geographical markets.

JEL classification: L11, Q40, R19.

Keywords: Price transmission, regional market integration, retail oil sector.

2

1. Introduction

Since the liberalization of the energy sectors in Europe there has been a growing interest in

knowing the extent to which the energy markets are operating as though they were

integrated for producers. As a result, we can now benefit from an important body of

research on the geographical integration of both gas and electricity markets (e.g. Smeers,

1997; Joskow, 2008; Vassilopoulos, 2010; Balaguer, 2011). Most of these papers were

motivated by political concerns about the effectiveness of the process of liberalization that

occurred under a situation in which transmission capacity led to restraints and difficulties

for new competitors to access the networks.

In contrast, research on the geographical integration of mineral oil markets is very limited,

in spite of the large potential impact that this would have on social welfare due to the

present importance of the oil sector as an energy source. Although it is quite clear that

barriers to entry for oil competitors are not as apparent as in other energy markets,

integration difficulties have also been revealed, at least for the international retail markets.

Evidence recently provided by Dreher and Krieger (2008, 2010) suggested that, in spite of

the fact that retail prices of petroleum products have converged across the European

countries since the beginning of liberalization in the nineties, there is still a wide margin for

international convergence of prices even when they are considered net of taxes.1 However,

it is still unknown whether geographical markets in each of the European countries can also

be considered segmented, as has been highlighted for some specific regions in the USA (i.e.

1 The authors also examine consumer prices (i.e. prices with taxes) and indicate that cross-regional shopping

is a weak phenomenon. In view of the nature of fuel products this is reasonable, since consumers may have

difficulty in taking advantage of price differences among regions due to high displacement costs related with

the price of the product, the high frequency of purchase, and the short amount of time spent on the buying

decision process.

3

Paul et al., 2001; Slade, 1986).2 In fact, in a framework where operating sellers have

enough market power to establish some barriers to competition in certain regions or where

regulatory specificities for the industry exist for each of them, the assumption of a single oil

market for a country seems rather unlikely. A detailed knowledge of oil price formation

mechanisms within each country could be particularly useful to establish the extent to

which regional policies of market integration need to be encouraged as a prerequisite to

achieving a larger single European market for oil products.

In this paper we will focus our attention on the Spanish oil market. In this country, national

downstream oil activities were controlled by the government through a state-owned

monopoly (“Campsa”) for a long period of time (1927-1992). Since then, the liberalization

process conducted at the end of the last century (encouraged by European Union

requirements) entailed a deep reform in the fuel oil sector. Now, since any systematic

positive difference in prices (net of taxes) that cannot be attributed to transportation or

distribution costs may be efficiently eliminated by the entry of competitors, it could be

presumed that retail oil markets are operating as a single market. However, there are

reasonable doubts that lead us to question this. The suspicion can be derived from

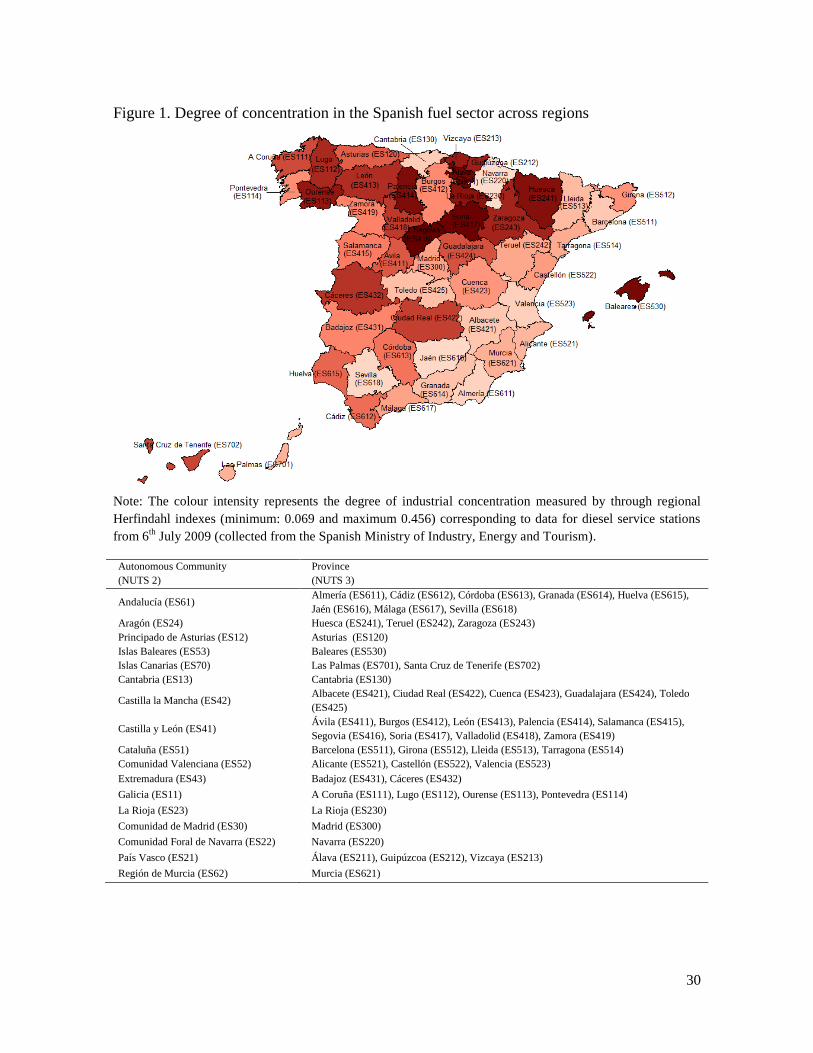

ostensible differences on the supply-side at the regional level. For instance, according to

Spanish Government data (from 6th

July 2009), the Herfindahl indexes related to diesel

service stations for Segovia and Soria are about 0.45, while Navarra and Jaen are

approximately 0.07.

2

Empirical results show that, in general, oil market integration in the USA can be considered quite high,

which would support the policies of deregulation in markets completed in 1981. However, these works also

highlight the presence of market segmentation between some regions, which should not be too surprising due

to the large distances between them.

4

The exercise of market power as well as the role of regional regulations and institutions

may be favouring divergences in market structures at the regional level. On the one hand, in

spite of liberalization in the sector, there remains a high level of market concentration

basically attributed to the presence of large, vertically integrated firms. Thus, more than

50% of the diesel service stations in Spain are controlled by the three most important firms

that operate in the markets (Repsol, Cepsa-Elf and British Petroleum).3 It is possible that

the exercise of market power of this group of firms implies some implicit barriers, like the

control of certain productive resources, economies of scale or local predatory pricing

behaviour, among other obstacles to new potential competitors within a particular region.

On the other hand, the establishment of a new retail oil seller in each region is committed to

the specific criteria of the corresponding autonomous government (in accordance with

current Spanish regulations (RD 1906/1995)). In practice, this may result in some

administrative barriers to the free entry and relocation of firms from one region to another.4

If observed differences on the supply-side are permanent and are not sufficiently offset by

the demand-side (e.g. consumer preferences, regional income), then the elasticity of the

demand schedule perceived by firms for each region would be different, thus implying, in

turn, geographical divergences in pricing strategy and the relative failure of the law of one

price.

In this paper we investigate whether oil price transmission in retail fuel oil markets works

as in regionally integrated markets. Furthermore, we will try to shed light on whether

institutional factors play some role. The paper is organized as follows. In the next section

3 According to data from 6

th July 2009 (collected from the Spanish Ministry of Industry, Energy and

Tourism).

4 This may favour the presence of certain brands that only operate in specific Spanish regions, such as

Bonarea in Cataluña and Aragón, Iberdoex in Extremadura, Farruco in Toledo or PCAN in Canarias Islands.

5

we describe our dataset and develop the econometric specification used in the analysis. In

section 3 we present the empirical results and discuss their implications as referred to

regional market integration. Finally, in section 4 we present the concluding remarks.

2. The empirical framework

2.1. Basic hypotheses

To achieve our aims, we assume that regional markets can be considered integrated when

possible (pre-tax) price differences across regions can only be attributed to differences in

product transportation and distribution costs (removing the arbitrage opportunity).5 Thus,

transmission of common changes in production costs (i.e. prices of raw material) should be

equal for all markets in the long run (leading to the fulfilment of a relative version of the

“law of one price”). To test the extent to which markets are integrated, we base our

empirical analysis on the mechanism of retail price determination after changes in

international wholesale prices of the raw material. More specifically, we perform an

analysis of the long-run cost pass-through from the commercialization distribution chain.

The comparison of cost pass-through across regions then allows us to identify the extent of

the market integration. If regional markets are not integrated, the comparative analysis will

give us useful information about whether there is a regional effect on market segmentation

associated to the existence of autonomous communities.

Let us illustrate the underlying idea of our hypotheses by considering a representative firm

which sells a fuel oil product across several destination geographical regions (i=1,..,R). For

the sake of simplicity, we assume that the demand curves perceived by the firm for each of

5 For a discussion of this operating definition see, for example, Goldberg and Knetter (1997).

6

the regions where the oil product is sold can be described by a set of R exponential

functions as follows:

(1)

where represents the free on board price (fob) and is the absolute value of the

constant price elasticity of demand with respect to the region i. Then, the optimal price

fixed for each region i at time t can be expressed as the product of a specific-region cost

pass-through ( ) and common marginal costs of production ( , which we assume to

be time-dependent on raw material price :6

where

⁄.

The market integration hypothesis can be straightforwardly characterized from Eq. (2). In

the event that the firm treats all the markets as one, the elasticities of perceived demand

should be equal across any of the regions (i.e. ). So, before raw material price

variations, we can see that cost pass-through should be common to all regions (i.e.

. Moreover, under these types of demand functions with constant elasticity, cost pass-

through should be greater than unity except in the particular case of a single perfectly

competitive market (i.e. ), where it equals one. Alternatively, in a framework of

good market segmentation, elasticities of perceived demand would differ across the regions

6 Like many earlier works, we assume that variations in prices set by retailers depend on changes in prices of

the raw material (e.g. Bacon, 1991; Bachmeier and Griffin, 2003; Balaguer and Ripollés, 2012).

7

(i.e. ). Then, in this last case, we will obtain that the values of cost pass-through

should be greater than unity and idiosyncratic for regions.

2.2. Study framework and data

We are interested in empirically testing the hypotheses described above for the set of

Spanish regions. The regional disaggregation used in this paper corresponds to Provincial

Nomenclature of Territorial Units for Statistics (known as NUTS 3). Forty-seven of these

regions are located geographically on the Iberian Peninsula, whereas the Baleares Islands,

Santa Cruz de Tenerife and Las Palmas are insular regions. It should be noted that these

Spanish regions are grouped into supra-regions, each with their own autonomous

government, known as autonomous communities (known as NUTS 2). The seventeen

autonomous communities have administrative responsibilities such as provision of

education, healthcare, social services and retail fuel oil distribution. Each of these supra-

regions has the authority, on the one hand, to manage a part of the tax on hydrocarbons and,

on the other hand, to distribute the administrative concessions that allow new fuel oil

stations to be established in their territory. The rules and discretion of the governments in

each area can be one of the reasons explaining the differences observed in market

concentration. To illustrate our study framework, Figure 1 provides an outline of the

political sub-division by provinces and autonomous communities, as well as the market

concentration in each of the regions.

[Please insert Figure 1 here]

In order to perform the empirical analysis we have 728 daily data (from 1st October 2008 to

28th

September 2010) on the average retail fuel oil prices fixed by service stations in each

8

of the fifty provinces described above (excluding the autonomous cities of Ceuta and

Melilla). This dataset was provided by the Spanish Ministry of Industry, Tourism and

Trade.7 We have excluded all taxes from these prices. More specifically, the special tax on

hydrocarbons, the general tax established by the State, the taxes applied by each

autonomous community and value added tax (VAT) have all been removed in accordance

with information published by the Spanish Ministry of Economy’s Tax Office.8 We have

also considered the international spot prices (in fob terms) of the corresponding refined oil

product, which has been widely considered the most important direct cost for fuel retailers.

International oil prices, which are collected from the Energy Information Administration,

refer to the daily value of the refined oil product on the Amsterdam-Rotterdam-Antwerp

market. On weekends and holidays, where observations are missing as a consequence of

closure of the spot oil market, the wholesale prices from the day before will be applied.

Because international wholesale prices are collected in dollar terms (per litre), we convert

these prices into the local Spanish currency (Euro). For this purpose, we used the daily

Dollar/Euro exchange rate obtained from the Eurostat database.

2.3. Econometric specification

The fuel oil prices (measured in local terms for each province) in our sample differ from

theoretical fob prices described in Eq. (1) and Eq. (2). In fact, available retail prices include

transportation costs from different locations of oil refineries and local distribution costs,

which are unknown to us. With the aim of specifying an estimable empirical model, we

7 Sellers must report the set of retail prices at a sales point to the Ministry every Monday and also whenever

prices change (in accordance with the Ministerial Order ITC/2308/2007). In general, there are many service

stations that send information about changes in their selling prices several days per week.

8 Appendix A shows detailed information about each of the taxes applied on retail diesel fuel.

9

assume that these sorts of costs are time invariable, but still allowing for cross-sectional

heterogeneity. Then, differences between theoretical (fob) retail prices ( ) and local retail

prices can be captured by individual fixed effects ( ). In order to test the market

integration hypothesis we propose the following empirical model:

∑

∑

( )

where coefficients and will allow us to control for possible effects on retail prices of

seasonal changes in demand for month k and day q, respectively, with respect to a reference

time point (k = 1 and q = 1). The slopes can be interpreted as an empirical

approximation to the raw material cost pass-through for each of the R regions. Lastly, is

a random disturbance term, which is assumed to be iid.

We use available wholesale prices of refined fuel oil as a measure of raw material costs

( ).9 So, a comparative response of final prices to changes in refined fuel oil costs can

provide useful information about how far regions move away from a situation of market

integration. On the one hand, in cases where firms operate in a perfectly integrated market,

any common variation in refined fuel oil costs should be transmitted equally to final prices

in all regions. In terms of Eq. (3), this implies that (for overall i=1,..,R). That is,

for example, the particular extreme case of a perfectly competitive market where common

changes in marginal costs derived from refined fuel oil wholesale prices should be fully

transmitted to final retail prices ( . On the other hand, possible cases where the

9 As recommended for the measurement of oil raw material cost pass-through, we take prices for refined oil

instead of the spot price of crude oil (e.g. Borenstein et al., 1997). The reason for this is that our retail prices

should be treated as independent of the demand for other products derived from crude oil (due to joint

production in the industry).

10

common variations in costs of raw material were persistently transmitted to a different

degree across regions could only be explained by the presence of market power

and geographical segmentation.

3. Empirical results and discussion

3.1. Cost pass-through estimates

According to the stationary properties of the time series analysed in Annex B, we can be

sure that retail and wholesale prices are cointegrated and so Eq. (3) can be considered a

stable long-run equilibrium. Additionally, in accordance with the modified Wald statistic

proposed by Greene and Zhang (2003) and Wooldridge (2002), the presence of

heteroskedasticity and serial correlation is detected respectively. We also considered the

possibility of cross-sectional dependence among regions. Since the number of individuals is

smaller than the number of time observations, we chose to employ the LM-statistic

proposed by Breusch and Pagan (1980). From the statistical test, we can clearly reject the

null hypothesis of no spatial dependence (with a p-value virtually equal to zero). In view of

the results of the diagnostic test, we decided to estimate the fixed-effects model represented

in Eq. (3) by performing OLS with the standard errors of Driscoll and Kraay (1998). The

standard errors will thereby be corrected for heteroskedasticity and, furthermore, will be

robust to very general forms of temporal and spatial dependence.

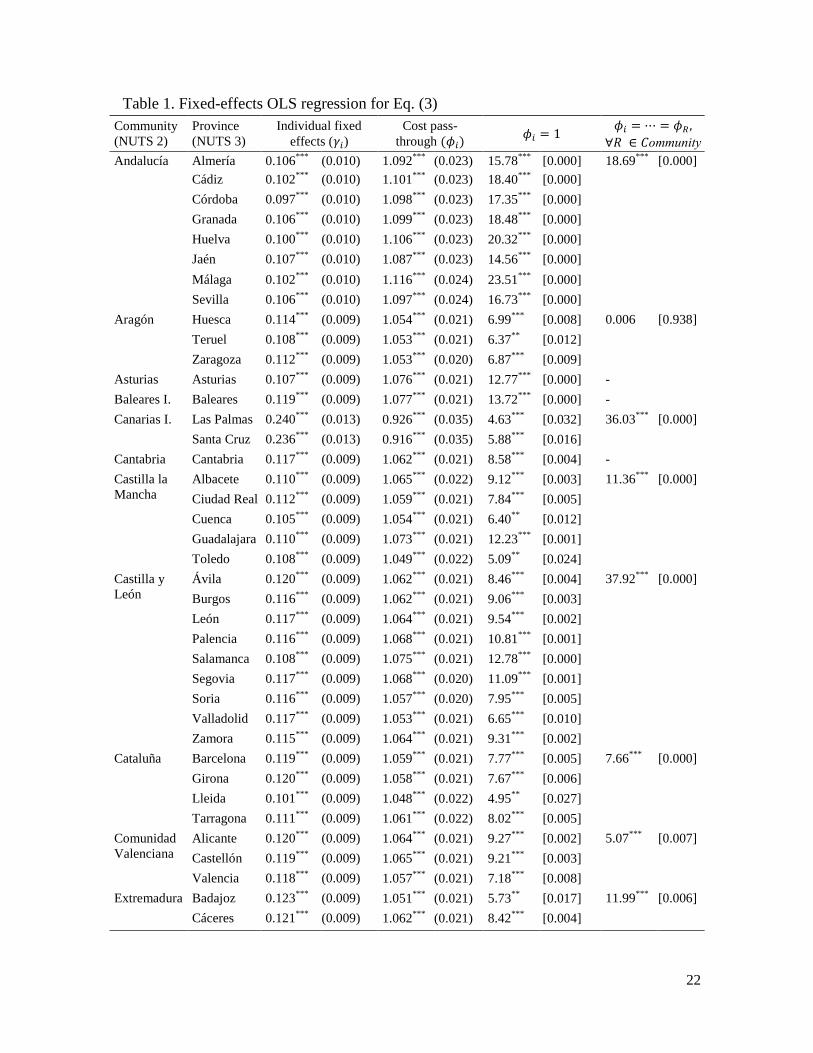

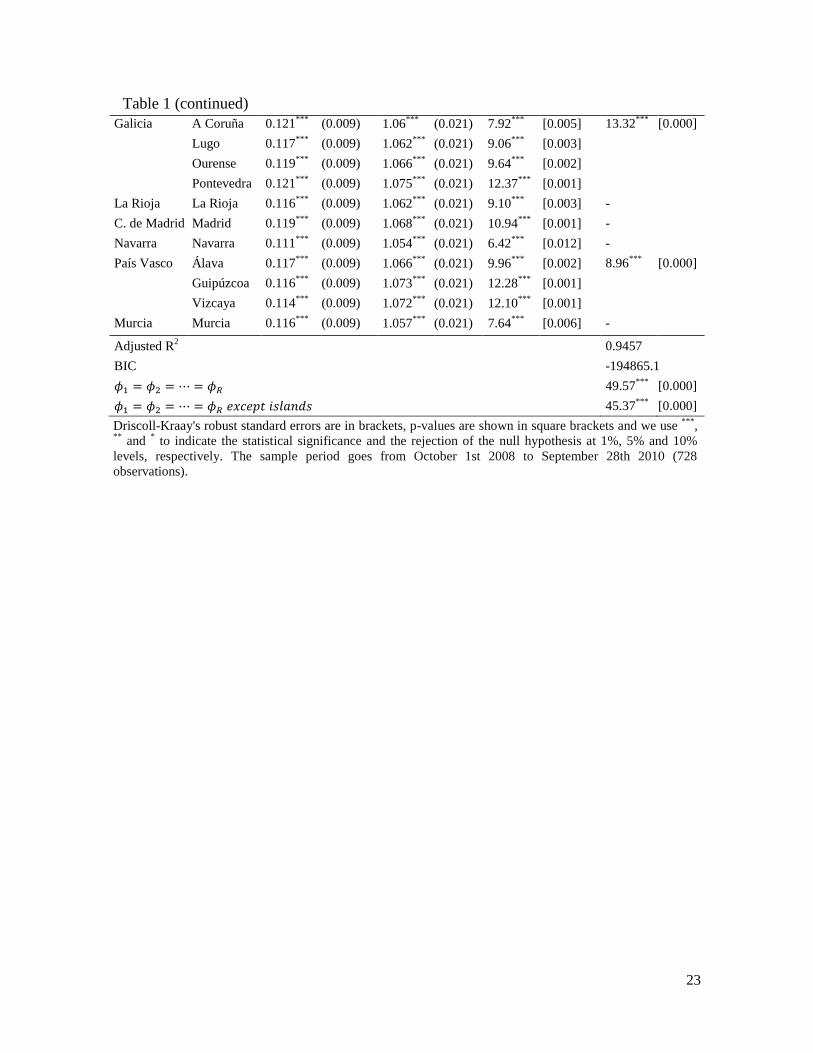

[Please insert Table 1 here]

11

The individual fixed effects and the point estimates for raw material cost pass-through are

reported in Table 1.10

Estimates of individual fixed effects may reflect transportation costs

from different locations of oil refineries and local distribution costs. In this sense, this could

be consistent with the higher values obtained for provinces belonging to the Canarias

Islands. We are particularly interested in the estimates of raw material cost pass-through,

which are quite close to unity. However, in all cases, we can clearly reject the idea that

changes in raw material cost are fully transmitted to final prices. These empirical results are

not compatible with a situation of a fully integrated, perfectly competitive market

framework (i.e. ). Furthermore, we can also reject the null hypothesis related

with homogeneous cost pass-through among the fifty provinces ( ). This is also

true even after excluding the island territories from the sample (i.e. Baleares Islands and the

provinces that belong to Canarias Islands). Hence, the empirical outcomes suggest that the

Spanish regional markets are segmented even when we are dealing with the peninsular

territory.

Finally, with the aim of checking the robustness of the empirical results presented in Table

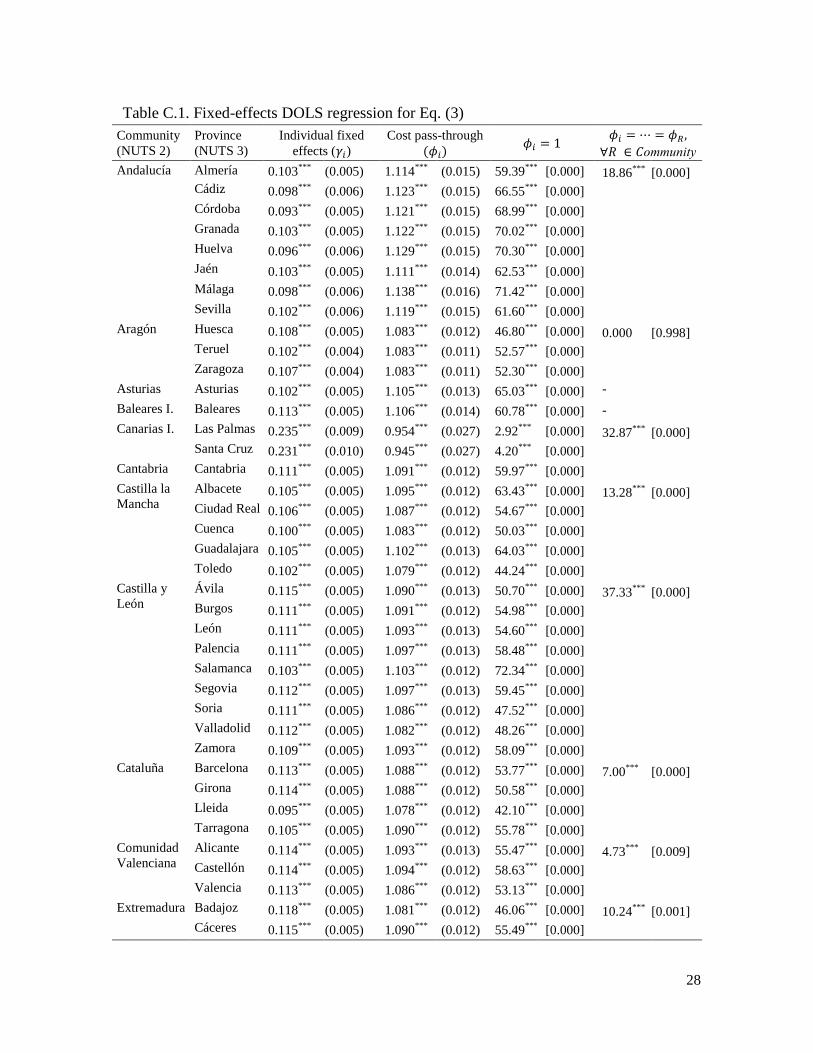

1, we have alternatively estimated the long-run equilibrium relationship from Eq. (3) by

using the dynamic OLS methodology for cointegrated panel data proposed by Kao and

Chiang (2000). As we can see in Annex C (Table C1), the results from the dynamic

empirical model are consistent with those discussed above.

10

A diagnostic test concerning the functional form has also been performed from our data. According to

Akaike Information Criterion (AIC), the model specification in levels is better than a double-log model

specification.

12

3.2. Cost pass-through differences

We formally explore the possibility of raw material cost pass-through being equal within

the same autonomous community (NUTS 2), but perhaps differing from one to another.

Therefore, we perform empirical tests which are shown in the last column of Table 1 (and

Table C1). Results indicate that, with the exception of Aragón, there is still a significant

degree of heterogeneity in the cost pass-through among provinces that belong to the same

autonomous community.

However, in spite of the heterogeneity, it seems that the magnitude of our point estimates

presented in Table 1 (and Table C1) could be linked to some extent to the division of

regions in autonomous communities. That is, in general, the degree of cost transmission for

provinces belonging to the same autonomous community seems more similar than in the

case of provinces that belong to different communities. This fact can be shown quite clearly

by a comparison of the provinces associated to the extreme values for estimated

coefficients. Thus, the two provinces belonging to the autonomous community Canarias

Islands correspond to the lowest estimated values. More specifically, we are referring to

Las Palmas and Santa Cruz de Tenerife. The opposite case is represented by the eight

provinces in the Community of Andalucía. That is, the highest estimated values are those

associated to the provinces of Málaga, Huelva, Cádiz, Granada, Córdoba, Sevilla, Almería

and Jaén.

We are therefore interested in formally exploring whether cross-sectional similarity in the

degree of estimated cost pass-through for a set of provinces can be explained well by a

latent factor associated to the autonomous community (e.g. the legal rules and discretionary

13

policy of each autonomous government). With this purpose in mind, let us further consider

a basic estimated dependent variable model (EDV) with the aim of analysing the

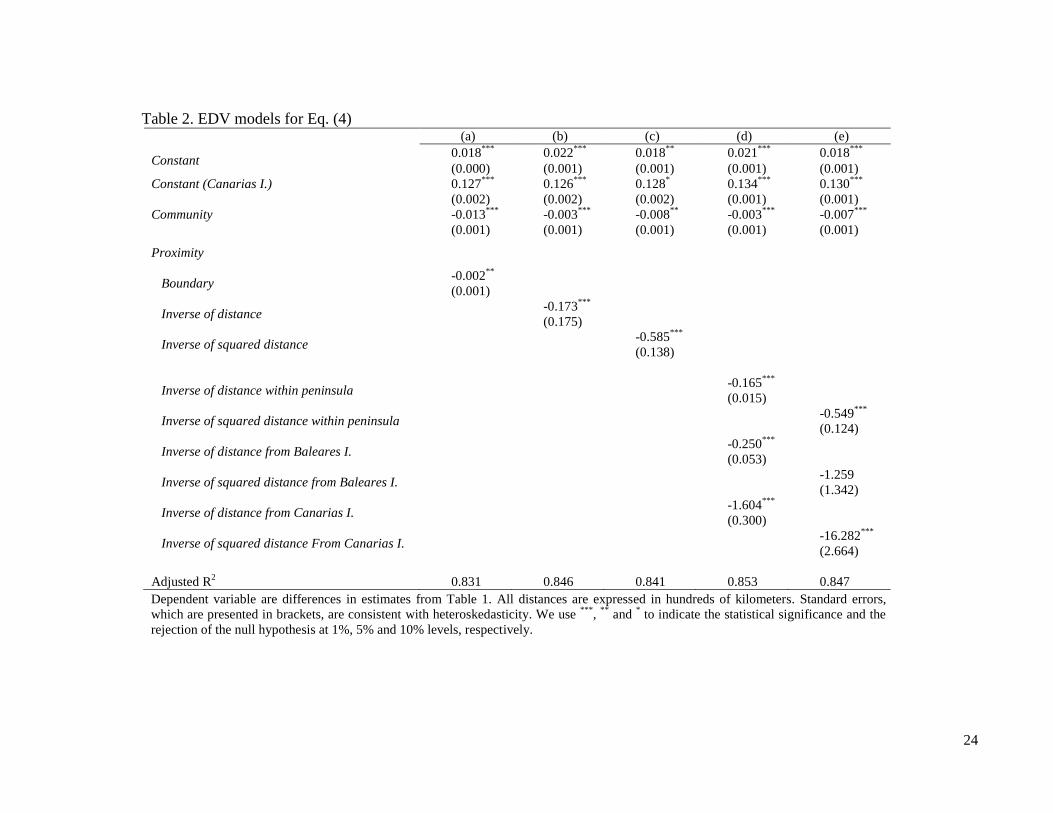

determinants of cost pass-through differences between provinces:

| | (4)

where the partner combinations of estimated regional coefficients of cost pass-through

and from Eq. (3) are regressed on a constant, a measure of proximity between provinces

(proximity) with the aim of controlling for typical spatial spillover effects, and a dummy

variable (community) that equals 1 if i and j belong to the same autonomous community

and 0 otherwise. Lastly, is a random disturbance term assumed to be iid.

We use alternative measures to capture the possible effect on cost pass-through similarity

derived from spatial proximity: boundary (as a dummy variable that takes a value of 1 if the

two regions share a common boundary and 0 otherwise), inverse of distance between the

capital cities of both regions and, lastly, inverse of squared distance between the capital

cities of both regions. The reason for considering the inverse distance between capital cities

as an approximation of spatial proximity among service stations is because the area around

these cities is where there are more stations in each province. Since the presence of an

estimated dependent variable can introduce heteroskedasticity into the regression

(Saxonhouse, 1976), we decided to apply OLS with White's consistent standard errors, as is

usual in these kinds of econometric specifications.

14

Empirical results for the spatial measures of geographical proximity discussed above are

shown in Table 2 (columns a, b, and c).11

As can be seen, the regression equations explain

more than 80% of the total variance of the differences in pass-through between provinces,

regardless of the alternative measures for spatial proximity between the provinces.

Estimated coefficients suggest that the presence of spillover effects among provinces is

quite significant. Therefore, after controlling for these spillover effects, we can know

whether belonging to the same autonomous community reduces the differences in cost

pass-through among provinces. Furthermore, regardless of the alternative specification

performed, the coefficients associated to the community variable always have a negative

sign and are highly significant. This indicates that the degree of cost transmission for those

provinces that share specific rules and a common political framework in oil fuel

distribution is clearly more similar.

[Please insert Table 2 here]

Finally, some additional considerations may be taken into account in the specification

model due the nature of the provinces included in our dataset. In this sense, because the

sample includes data for both peninsular and island territories, an appropriate empirical

strategy could be to split the coefficients. To be able to split coefficients we focus on

inverse distance because the goodness of fit of regressions when this control variable is

used is always greater than when the boundary variable is used. Then, on the one hand, we

will control for inverse distance between pairs of capital cities of provinces that belong to

the peninsula. On the other hand, we separately control for inverse distance when at least

11

We acknowledge possible unobserved effects linked with the Canarias Islands, mainly due to the region’s

idiosyncratic fuel taxes. Thus, we split the constant of the regression equation: one constant if the partner

regions or considered are Las Palmas or Santa Cruz de Tenerife and another for the rest of the cases.

15

one of the insular provinces is involved. Empirical results are provided in the last two

columns of Table 2 (columns d and e). The best goodness of fit is obtained for the most

general regression (column g). In any case, the estimated coefficients derived from all the

regressions performed are widely consistent with those discussed above and the

community-associated coefficient is always negative and highly significant.

4. Concluding remarks

This paper focuses on the comparison of the transmission of price variations of raw oil

material across regions. We found that the degree of cost pass-through to retail prices

differs significantly across the Spanish provinces, thereby suggesting a lack of market

integration at the regional level. In line with the existing evidence for the USA (i.e. Paul et

al., 2001; Slade, 1986), we found that more integration in retail oil markets is still possible.

These previous findings indicate that distance between the US regions explains the

presence of segmentation. However, since we have obtained cross-sectional estimates for

cost transmission, we can also ask ourselves whether there is a regional effect in market

segmentation derived from the existence of autonomous communities in Spain.

After controlling for the possible spillover effects across neighbouring regions, we explored

whether belonging to different autonomous community has some influence. We found that

there is more similarity in the raw material cost pass-through among provinces that belong

to the same autonomous community than in the rest of them. This effect according to

autonomous community could be attributed to discretional behaviour by the autonomous

regional governments, which is ultimately supported by the Spanish legislation framework.

That is, perhaps the difference in criteria across regional governments when they promote

16

and give administrative authorization to companies to operate in their territory plays an

important role in the existence of segmentation at the regional level. In sum, our results

suggest complete integration will be difficult without unification of the current legislation

and policies regarding the sector at the national level, as a step towards a larger single

European market for oil products. Obviously, the inherent behaviour of a highly

concentrated industry may also be behind the existence of the regional market segmentation

found in the study reported in this paper. To identify other factors of market behaviour that

become substantial drawbacks to integration in the oil retail industry, further work based on

firm-level data is required.

Acknowledgements

The authors wish to thank Massimo Filippini and the participants at the 12th

IAEE

European Conference in Venice. Any remaining errors are ours. Financial support from the

Spanish Ministry of Economy and Competitiveness (ECO2011-28155) and the Generalitat

Valenciana (VALI+D, ACIF/2010) are gratefully acknowledged.

17

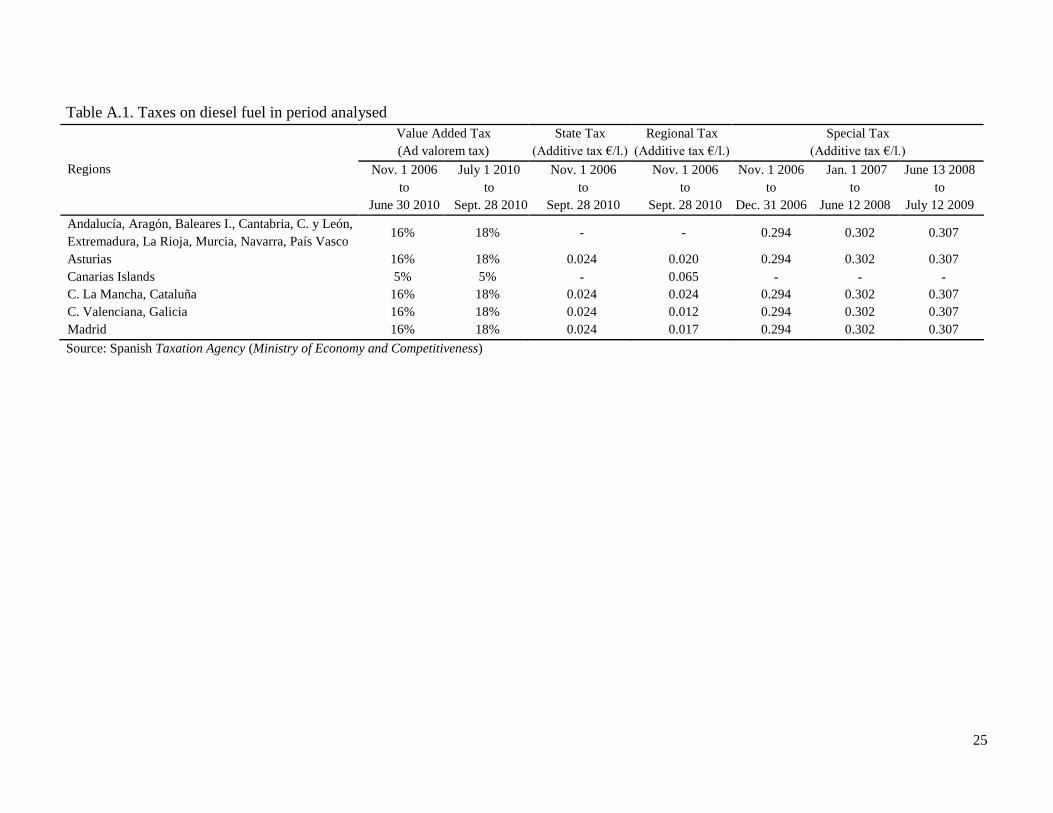

Appendix A. Taxes

[Please insert Table A.1 here]

Appendix B. Time series properties

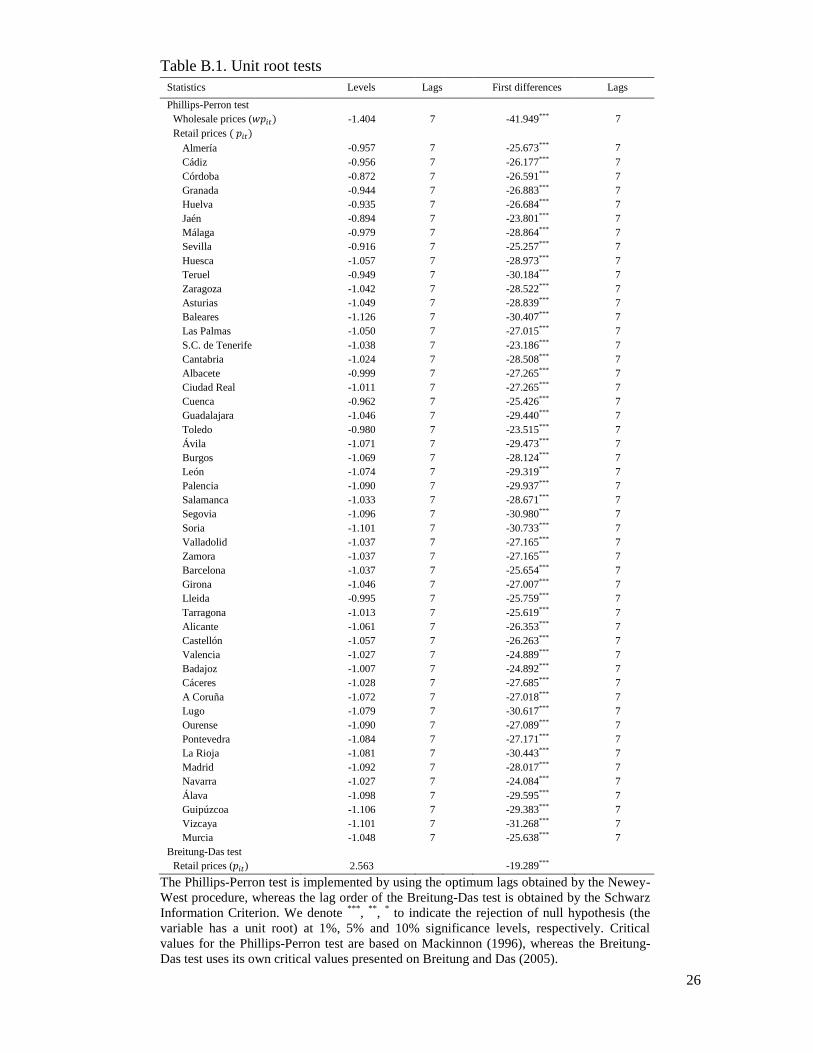

We use the unit root test proposed by Phillips-Perron (1988) on common wholesale prices

and retail prices for each separate region. However, the power of this last test can be low

when data combine both time-series and cross-sectional dimensions. Then, we additionally

employ the Breitung and Das (2005) unit root test on retail prices, since this statistic is

particularly suitable for panels with T ≥ N and the presence of cross-sectional

dependence.12

The corresponding results shown in Table B.1 indicate that both wholesale

and retail prices in levels are non-stationary, but after taking first differences we can reject

the null hypothesis of non-stationarity of the series (at the 0.01 level of significance). We

can therefore conclude that prices are integrated of order one, I(1).

[Please insert Table B.1 here]

To avoid a spurious regression by the potential presence of unit roots in variables from Eq.

(3), we must make sure that cointegration exists between retail and wholesale prices. If the

linear combination between dependent and independent variables is stationary I(0) while

each variable contains a unit root I(1), then Eq. (3) will represent a stable long-run

relationship. A methodology to test for cointegration under possible cross-sectional

12 In the panel unit root approach, we can distinguish a first group of tests based on the restrictive assumption

of cross-sectional independence (e.g. Maddala and Wu, 1999; Levin et al., 2002; Im et al., 2003). However,

Monte-Carlo simulations show that under cross-sectional dependence these panel tests may suffer from severe

size distortions. In fact, it is revealed that there is a tendency to over-reject the null hypothesis of unit root

(O’Connell, 1998; Breitung, 2002). Therefore, to address this problem, we use the robust OLS t-statistic

proposed by Breitung and Das (2005).

18

dependency is provided by Pedroni (1999, 2004). This author developed two types of tests

taking into account the residuals of the long-run equation. The first type is distributed as

being asymptotically standard-normal and is based on pooling the within-group residuals

for a long-run equation. The second type is also distributed as asymptotically standard-

normal, but is based on pooling the between-group residuals. Whereas the first type of

statistics is a panel version, the second statistics are based on averaging the corresponding

time series unit root test statistics. If all seven tests reject the null of non-cointegration

simultaneously, it is easy to draw a conclusion. Unfortunately, this is not always the case. If

the panel is large enough, so that size distortion is less of an issue, the panel υ-statistic tends

to have the best power relative to the other statistics and can be most useful when the

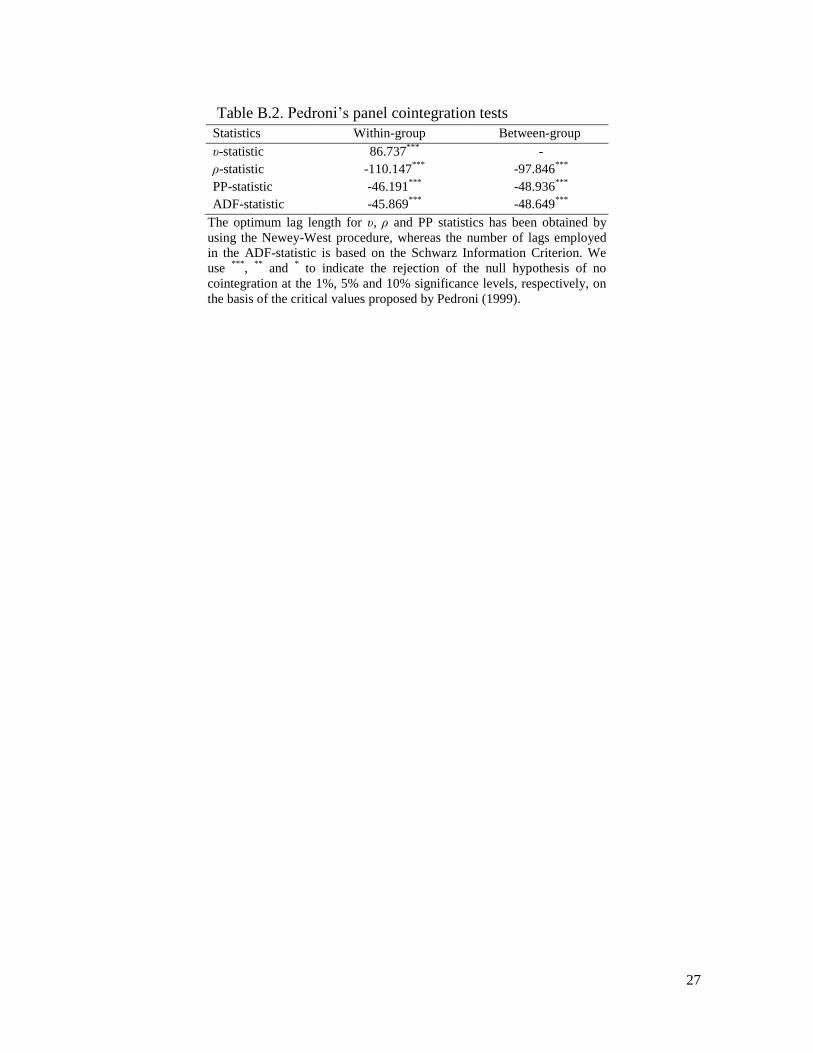

alternative is potentially very close to the null. Pedroni’s tests are presented in Table B.2.

All statistics can reject the null hypothesis of non-cointegration and, therefore, we can

verify that the linear combination between retail and refined prices moves jointly in the

long term.

[Please insert Table B.2 here]

Appendix C. Panel DOLS estimates of long-run cost pass-through from Eq. (3)

[Please insert Table C.1 here]

19

References

Bachmeier, L.J., Griffin, J.M. (2003). “New Evidence on Asymmetric Gasoline Price

Responses.” Review of Economics and Statistics 85(3): 772-776.

Bacon, R. (1991). “The Asymmetric Speed of Adjustment of UK Retail Gasoline Prices to

Cost Changes.” Energy Economics 13(3): 211-218.

Balaguer, J. (2011). Cross-border Integration in the European Electricity Market. “Evidence

from the pricing behavior of Norwegian and Swiss exporters.” Energy Policy 39(9): 4703-

4712.

Balaguer, J., Ripollés, J. (2012). “Testing for Price Response Asymmetries in the Spanish

Fuel Market. New Evidence from Daily Data.” Energy economics, forthcoming.

Borenstein, S., Cameron, A.C., Gilbert, R. (1997). “Do Gasoline Prices Respond

Asymmetrically to Crude Oil Price Changes?” Quarterly Journal of Economics 112(1):

305-339.

Breitung, J. (2002). “Nonparametric Tests for Unit Roots and Cointegration.” Journal of

Econometrics 108(2): 343-363.

Breitung, J., Das, S. (2005). “Panel Unit Root Tests Under Cross-sectional Dependence.”

Statistica Neerlandica 59(4): 414-433.

Breusch, T.S., Pagan, A.R. (1980). “The Lagrange Multiplier Test and its Applications to

Model Specification in Econometrics.” Review of Economic Studies 47(146): 239-254.

Dreher, A., Krieger, T. (2008). “Do Prices for Petroleum Products Converge in a Unified

Europe with Non-harmonized Tax Rates?” The Energy Journal 29(1): 61-88.

Dreher, A., Krieger, T. (2010). “Diesel Price Convergence and Mineral Oil Taxation in

Europe.” Applied Economics 42(15): 1955-1961.

Driscoll, J.C., Kraay, A.C. (1998). “Consistent Covariance Matrix Estimation with

Spatially Dependent Panel Data.” The Review of Economics and Statistics 80(4): 549-560.

20

Goldberg, P.K., Knetter, M.M. (1997). “Goods Prices and Exchange Rates: What Have we

Learned?” Journal of Economic Literature 5(3): 1243-1272.

Greene, W.H., Zhang, C. (2003). Econometric Analysis, Vol. 5. Prentice Hall, Upper

Saddle River, NJ.

Im, K.S., Pesaran, H.M., Shin, Y. (2003). “Testing for Unit Roots in Heterogeneous

Panels.” Journal of Econometrics 115(1): 53-74.

Joskow, P.L. (2008). “Lessons Learned from Electricity Market Liberalization.” The

Energy Journal 29(Special issue 2): 9-42.

Kao, C. and Chiang, M.H. (2000). “On the Estimation and Inference of a Cointegrated

Regression in Panel Data.” Advances in Econometrics 15: 179-222.

Levin, A., Lin, C.F. and Chu, C. (2002). “Unit Root Tests in Panel Data: Asymptotic and

Finite Sample Properties.” Journal of Econometrics 108(1): 1-24.

Maddala, G.S., Wu, S. (1999). “A Comparative Study of Unit Root Tests with Panel Data

and New Simple Test." Oxford Bulletin of Economics and Statistics 61(1): 631-652.

O’Connell, P.G.J. (1998). “The Overvaluation of Purchasing Power Parity.” Journal of

International Economics 44(1): 1-19.

Paul, R.J., Miljkovic, D., Ipe, V. (2001). “Market Integration in US Gasoline Markets.”

Applied Economics 33(10): 1335-1340.

Pedroni, P. (1999). “Critical Values for Cointegration Tests in Heterogeneous Panels with

Multiple Regressors.” Oxford Bulletin of Economics and Statistics 61(Special issue): 653-

670.

Pedroni, P. (2004). “Panel Cointegration: Asymptotic and Finite Sample Properties of

Pooled Time Series Tests with an Application to the PPP Hypothesis.” Econometric Theory

20(3): 597-625.

21

Phillips, P.C.B., Perron, P. (1988). “Testing for Unit Roots in Time Series Regression.”

Biometrika 75(2): 335-346.

Saxonhouse, G.R. (1976). “Estimated Parameters as Dependent Variables.” American

Economic Review 66(1): 178-83.

Slade, M.E. (1986). “Conjectures, Firms Characteristics, and Market Structure: An

Empirical Assessment.” International Journal of Industrial Organization 4(4): 347-370.

Smeers, Y. (1997). “Computable Equilibrium Models and the Restructuring of the

European Electricity and Gas Markets.” The Energy Journal 18(4): 1-31.

Vassilopoulos, P. (2010). Price Signals in “Energy-Only” Wholesale Electricity Markets:

An Empirical Analysis of the Price Signal in France.” The Energy Journal 31(3): 83-112.

Wooldridge, J.M. (2002). Econometric Analysis of Cross Section and Panel Data.

Cambridge, MA: MIT Press.

22

Table 1. Fixed-effects OLS regression for Eq. (3)

Community

(NUTS 2)

Province

(NUTS 3)

Individual fixed

effects ( )

Cost pass-

through

Andalucía Almería 0.106***

(0.010) 1.092***

(0.023) 15.78***

[0.000] 18.69***

[0.000]

Cádiz 0.102***

(0.010) 1.101***

(0.023) 18.40***

[0.000]

Córdoba 0.097***

(0.010) 1.098***

(0.023) 17.35***

[0.000]

Granada 0.106***

(0.010) 1.099***

(0.023) 18.48***

[0.000]

Huelva 0.100***

(0.010) 1.106***

(0.023) 20.32***

[0.000]

Jaén 0.107***

(0.010) 1.087***

(0.023) 14.56***

[0.000]

Málaga 0.102***

(0.010) 1.116***

(0.024) 23.51***

[0.000]

Sevilla 0.106***

(0.010) 1.097***

(0.024) 16.73***

[0.000]

Aragón Huesca 0.114***

(0.009) 1.054***

(0.021) 6.99***

[0.008] 0.006 [0.938]

Teruel 0.108***

(0.009) 1.053***

(0.021) 6.37**

[0.012]

Zaragoza 0.112***

(0.009) 1.053***

(0.020) 6.87***

[0.009]

Asturias Asturias 0.107***

(0.009) 1.076***

(0.021) 12.77***

[0.000] -

Baleares I. Baleares 0.119***

(0.009) 1.077***

(0.021) 13.72***

[0.000] -

Canarias I. Las Palmas 0.240***

(0.013) 0.926***

(0.035) 4.63***

[0.032] 36.03***

[0.000]

Santa Cruz 0.236***

(0.013) 0.916***

(0.035) 5.88***

[0.016]

Cantabria Cantabria 0.117***

(0.009) 1.062***

(0.021) 8.58***

[0.004] -

Castilla la

Mancha

Albacete 0.110***

(0.009) 1.065***

(0.022) 9.12***

[0.003] 11.36***

[0.000]

Ciudad Real 0.112***

(0.009) 1.059***

(0.021) 7.84***

[0.005]

Cuenca 0.105***

(0.009) 1.054***

(0.021) 6.40**

[0.012]

Guadalajara 0.110***

(0.009) 1.073***

(0.021) 12.23***

[0.001]

Toledo 0.108***

(0.009) 1.049***

(0.022) 5.09**

[0.024]

Castilla y

León

Ávila 0.120***

(0.009) 1.062***

(0.021) 8.46***

[0.004] 37.92***

[0.000]

Burgos 0.116***

(0.009) 1.062***

(0.021) 9.06***

[0.003]

León 0.117***

(0.009) 1.064***

(0.021) 9.54***

[0.002]

Palencia 0.116***

(0.009) 1.068***

(0.021) 10.81***

[0.001]

Salamanca 0.108***

(0.009) 1.075***

(0.021) 12.78***

[0.000]

Segovia 0.117***

(0.009) 1.068***

(0.020) 11.09***

[0.001]

Soria 0.116***

(0.009) 1.057***

(0.020) 7.95***

[0.005]

Valladolid 0.117***

(0.009) 1.053***

(0.021) 6.65***

[0.010]

Zamora 0.115***

(0.009) 1.064***

(0.021) 9.31***

[0.002]

Cataluña Barcelona 0.119***

(0.009) 1.059***

(0.021) 7.77***

[0.005] 7.66***

[0.000]

Girona 0.120***

(0.009) 1.058***

(0.021) 7.67***

[0.006]

Lleida 0.101***

(0.009) 1.048***

(0.022) 4.95**

[0.027]

Tarragona 0.111***

(0.009) 1.061***

(0.022) 8.02***

[0.005]

Comunidad

Valenciana

Alicante 0.120***

(0.009) 1.064***

(0.021) 9.27***

[0.002] 5.07***

[0.007]

Castellón 0.119***

(0.009) 1.065***

(0.021) 9.21***

[0.003]

Valencia 0.118***

(0.009) 1.057***

(0.021) 7.18***

[0.008]

Extremadura Badajoz 0.123***

(0.009) 1.051***

(0.021) 5.73**

[0.017] 11.99***

[0.006]

Cáceres 0.121***

(0.009) 1.062***

(0.021) 8.42***

[0.004]

23

Table 1 (continued)

Galicia A Coruña 0.121***

(0.009) 1.06***

(0.021) 7.92***

[0.005] 13.32***

[0.000]

Lugo 0.117***

(0.009) 1.062***

(0.021) 9.06***

[0.003]

Ourense 0.119***

(0.009) 1.066***

(0.021) 9.64***

[0.002]

Pontevedra 0.121***

(0.009) 1.075***

(0.021) 12.37***

[0.001]

La Rioja La Rioja 0.116***

(0.009) 1.062***

(0.021) 9.10***

[0.003] -

C. de Madrid Madrid 0.119***

(0.009) 1.068***

(0.021) 10.94***

[0.001] -

Navarra Navarra 0.111***

(0.009) 1.054***

(0.021) 6.42***

[0.012] -

País Vasco Álava 0.117***

(0.009) 1.066***

(0.021) 9.96***

[0.002] 8.96***

[0.000]

Guipúzcoa 0.116***

(0.009) 1.073***

(0.021) 12.28***

[0.001]

Vizcaya 0.114***

(0.009) 1.072***

(0.021) 12.10***

[0.001]

Murcia Murcia 0.116***

(0.009) 1.057***

(0.021) 7.64***

[0.006] -

Adjusted R2 0.9457

BIC -194865.1

49.57***

[0.000]

45.37***

[0.000]

Driscoll-Kraay's robust standard errors are in brackets, p-values are shown in square brackets and we use ***

, **

and * to indicate the statistical significance and the rejection of the null hypothesis at 1%, 5% and 10%

levels, respectively. The sample period goes from October 1st 2008 to September 28th 2010 (728

observations).

24

Table 2. EDV models for Eq. (4) (a) (b) (c) (d) (e)

Constant 0.018

*** 0.022

*** 0.018

** 0.021

*** 0.018

***

(0.000) (0.001) (0.001) (0.001) (0.001)

Constant (Canarias I.)

0.127***

0.126***

0.128* 0.134

*** 0.130

***

(0.002) (0.002) (0.002) (0.001) (0.001)

Community -0.013***

-0.003***

-0.008**

-0.003***

-0.007***

(0.001) (0.001) (0.001) (0.001) (0.001)

Proximity

Boundary -0.002

**

(0.001)

Inverse of distance -0.173

***

(0.175)

Inverse of squared distance -0.585

***

(0.138)

Inverse of distance within peninsula -0.165

***

(0.015)

Inverse of squared distance within peninsula -0.549

***

(0.124)

Inverse of distance from Baleares I. -0.250

***

(0.053)

Inverse of squared distance from Baleares I. -1.259

(1.342)

Inverse of distance from Canarias I. -1.604

***

(0.300)

Inverse of squared distance From Canarias I. -16.282

***

(2.664)

Adjusted R2 0.831 0.846 0.841 0.853 0.847

Dependent variable are differences in estimates from Table 1. All distances are expressed in hundreds of kilometers. Standard errors,

which are presented in brackets, are consistent with heteroskedasticity. We use ***

, **

and * to indicate the statistical significance and the

rejection of the null hypothesis at 1%, 5% and 10% levels, respectively.

25

Table A.1. Taxes on diesel fuel in period analysed

Regions

Value Added Tax

(Ad valorem tax)

State Tax

(Additive tax €/l.)

Regional Tax

(Additive tax €/l.)

Special Tax

(Additive tax €/l.)

Nov. 1 2006

to

June 30 2010

July 1 2010

to

Sept. 28 2010

Nov. 1 2006

to

Sept. 28 2010

Nov. 1 2006

to

Sept. 28 2010

Nov. 1 2006

to

Dec. 31 2006

Jan. 1 2007

to

June 12 2008

June 13 2008

to

July 12 2009

Andalucía, Aragón, Baleares I., Cantabria, C. y León,

Extremadura, La Rioja, Murcia, Navarra, País Vasco 16% 18% - - 0.294 0.302 0.307

Asturias 16% 18% 0.024 0.020 0.294 0.302 0.307

Canarias Islands 5% 5% - 0.065 - - -

C. La Mancha, Cataluña 16% 18% 0.024 0.024 0.294 0.302 0.307

C. Valenciana, Galicia 16% 18% 0.024 0.012 0.294 0.302 0.307

Madrid 16% 18% 0.024 0.017 0.294 0.302 0.307

Source: Spanish Taxation Agency (Ministry of Economy and Competitiveness)

26

Table B.1. Unit root tests

Statistics Levels Lags First differences Lags

Phillips-Perron test

Wholesale prices ( -1.404 7 -41.949*** 7

Retail prices

Almería -0.957 7 -25.673*** 7

Cádiz -0.956 7 -26.177*** 7

Córdoba -0.872 7 -26.591*** 7

Granada -0.944 7 -26.883*** 7

Huelva -0.935 7 -26.684*** 7

Jaén -0.894 7 -23.801*** 7

Málaga -0.979 7 -28.864*** 7

Sevilla -0.916 7 -25.257*** 7

Huesca -1.057 7 -28.973*** 7

Teruel -0.949 7 -30.184*** 7

Zaragoza -1.042 7 -28.522*** 7

Asturias -1.049 7 -28.839*** 7

Baleares -1.126 7 -30.407*** 7

Las Palmas -1.050 7 -27.015*** 7

S.C. de Tenerife -1.038 7 -23.186*** 7

Cantabria -1.024 7 -28.508*** 7

Albacete -0.999 7 -27.265*** 7

Ciudad Real -1.011 7 -27.265*** 7

Cuenca -0.962 7 -25.426*** 7

Guadalajara -1.046 7 -29.440*** 7

Toledo -0.980 7 -23.515*** 7

Ávila -1.071 7 -29.473*** 7

Burgos -1.069 7 -28.124*** 7

León -1.074 7 -29.319*** 7

Palencia -1.090 7 -29.937*** 7

Salamanca -1.033 7 -28.671*** 7

Segovia -1.096 7 -30.980*** 7

Soria -1.101 7 -30.733*** 7

Valladolid -1.037 7 -27.165*** 7

Zamora -1.037 7 -27.165*** 7

Barcelona -1.037 7 -25.654*** 7

Girona -1.046 7 -27.007*** 7

Lleida -0.995 7 -25.759*** 7

Tarragona -1.013 7 -25.619*** 7

Alicante -1.061 7 -26.353*** 7

Castellón -1.057 7 -26.263*** 7

Valencia -1.027 7 -24.889*** 7

Badajoz -1.007 7 -24.892*** 7

Cáceres -1.028 7 -27.685*** 7

A Coruña -1.072 7 -27.018*** 7

Lugo -1.079 7 -30.617*** 7

Ourense -1.090 7 -27.089*** 7

Pontevedra -1.084 7 -27.171*** 7

La Rioja -1.081 7 -30.443*** 7

Madrid -1.092 7 -28.017*** 7

Navarra -1.027 7 -24.084*** 7

Álava -1.098 7 -29.595*** 7

Guipúzcoa -1.106 7 -29.383*** 7

Vizcaya -1.101 7 -31.268*** 7

Murcia -1.048 7 -25.638*** 7

Breitung-Das test

Retail prices ( ) 2.563 -19.289***

The Phillips-Perron test is implemented by using the optimum lags obtained by the Newey-

West procedure, whereas the lag order of the Breitung-Das test is obtained by the Schwarz

Information Criterion. We denote ***

, **

, * to indicate the rejection of null hypothesis (the

variable has a unit root) at 1%, 5% and 10% significance levels, respectively. Critical

values for the Phillips-Perron test are based on Mackinnon (1996), whereas the Breitung-

Das test uses its own critical values presented on Breitung and Das (2005).

27

Table B.2. Pedroni’s panel cointegration tests

Statistics Within-group Between-group

υ-statistic 86.737***

-

ρ-statistic -110.147***

-97.846***

PP-statistic -46.191***

-48.936***

ADF-statistic -45.869***

-48.649***

The optimum lag length for υ, ρ and PP statistics has been obtained by

using the Newey-West procedure, whereas the number of lags employed

in the ADF-statistic is based on the Schwarz Information Criterion. We

use ***

, **

and * to indicate the rejection of the null hypothesis of no

cointegration at the 1%, 5% and 10% significance levels, respectively, on

the basis of the critical values proposed by Pedroni (1999).

28

Table C.1. Fixed-effects DOLS regression for Eq. (3)

Community

(NUTS 2)

Province

(NUTS 3)

Individual fixed

effects ( )

Cost pass-through

Andalucía Almería 0.103***

(0.005) 1.114***

(0.015) 59.39***

[0.000] 18.86***

[0.000]

Cádiz 0.098***

(0.006) 1.123***

(0.015) 66.55***

[0.000]

Córdoba 0.093***

(0.005) 1.121***

(0.015) 68.99***

[0.000]

Granada 0.103***

(0.005) 1.122***

(0.015) 70.02***

[0.000]

Huelva 0.096***

(0.006) 1.129***

(0.015) 70.30***

[0.000]

Jaén 0.103***

(0.005) 1.111***

(0.014) 62.53***

[0.000]

Málaga 0.098***

(0.006) 1.138***

(0.016) 71.42***

[0.000]

Sevilla 0.102***

(0.006) 1.119***

(0.015) 61.60***

[0.000]

Aragón Huesca 0.108***

(0.005) 1.083***

(0.012) 46.80***

[0.000] 0.000 [0.998]

Teruel 0.102***

(0.004) 1.083***

(0.011) 52.57***

[0.000]

Zaragoza 0.107***

(0.004) 1.083***

(0.011) 52.30***

[0.000]

Asturias Asturias 0.102***

(0.005) 1.105***

(0.013) 65.03***

[0.000] -

Baleares I. Baleares 0.113***

(0.005) 1.106***

(0.014) 60.78***

[0.000] -

Canarias I. Las Palmas 0.235***

(0.009) 0.954***

(0.027) 2.92***

[0.000] 32.87***

[0.000]

Santa Cruz 0.231***

(0.010) 0.945***

(0.027) 4.20***

[0.000]

Cantabria Cantabria 0.111***

(0.005) 1.091***

(0.012) 59.97***

[0.000]

Castilla la

Mancha

Albacete 0.105***

(0.005) 1.095***

(0.012) 63.43***

[0.000] 13.28***

[0.000]

Ciudad Real 0.106***

(0.005) 1.087***

(0.012) 54.67***

[0.000]

Cuenca 0.100***

(0.005) 1.083***

(0.012) 50.03***

[0.000]

Guadalajara 0.105***

(0.005) 1.102***

(0.013) 64.03***

[0.000]

Toledo 0.102***

(0.005) 1.079***

(0.012) 44.24***

[0.000]

Castilla y

León

Ávila 0.115***

(0.005) 1.090***

(0.013) 50.70***

[0.000] 37.33***

[0.000]

Burgos 0.111***

(0.005) 1.091***

(0.012) 54.98***

[0.000]

León 0.111***

(0.005) 1.093***

(0.013) 54.60***

[0.000]

Palencia 0.111***

(0.005) 1.097***

(0.013) 58.48***

[0.000]

Salamanca 0.103***

(0.005) 1.103***

(0.012) 72.34***

[0.000]

Segovia 0.112***

(0.005) 1.097***

(0.013) 59.45***

[0.000]

Soria 0.111***

(0.005) 1.086***

(0.012) 47.52***

[0.000]

Valladolid 0.112***

(0.005) 1.082***

(0.012) 48.26***

[0.000]

Zamora 0.109***

(0.005) 1.093***

(0.012) 58.09***

[0.000]

Cataluña Barcelona 0.113***

(0.005) 1.088***

(0.012) 53.77***

[0.000] 7.00***

[0.000]

Girona 0.114***

(0.005) 1.088***

(0.012) 50.58***

[0.000]

Lleida 0.095***

(0.005) 1.078***

(0.012) 42.10***

[0.000]

Tarragona 0.105***

(0.005) 1.090***

(0.012) 55.78***

[0.000]

Comunidad

Valenciana

Alicante 0.114***

(0.005) 1.093***

(0.013) 55.47***

[0.000] 4.73***

[0.009]

Castellón 0.114***

(0.005) 1.094***

(0.012) 58.63***

[0.000]

Valencia 0.113***

(0.005) 1.086***

(0.012) 53.13***

[0.000]

Extremadura Badajoz 0.118***

(0.005) 1.081***

(0.012) 46.06***

[0.000] 10.24***

[0.001]

Cáceres 0.115***

(0.005) 1.090***

(0.012) 55.49***

[0.000]

29

Table C.1 (continued)

Galicia A Coruña 0.115***

(0.005) 1.088***

(0.013) 48.33***

[0.000] 12.07***

[0.000]

Lugo 0.112***

(0.005) 1.091***

(0.012) 53.74***

[0.000]

Ourense 0.113***

(0.005) 1.095***

(0.013) 51.78***

[0.000]

Pontevedra 0.116***

(0.005) 1.104***

(0.014) 57.43***

[0.000]

La Rioja La Rioja 0.111***

(0.005) 1.091***

(0.012) 53.06***

[0.000] -

C. de Madrid Madrid 0.114***

(0.005) 1.098***

(0.013) 60.53***

[0.000] -

Navarra Navarra 0.105***

(0.005) 1.083***

(0.012) 46.27***

[0.000] -

País Vasco Álava 0.111***

(0.005) 1.096***

(0.013) 53.69***

[0.000] 8.26***

[0.000]

Guipúzcoa 0.111***

(0.005) 1.102***

(0.013) 63.39***

[0.000]

Vizcaya 0.109***

(0.005) 1.101***

(0.013) 62.60***

[0.000]

Murcia Murcia 0.111***

(0.005) 1.087***

(0.012) 53.94***

[0.000] -

Adjusted R2 0.999

BIC -235418

49.80***

[0.000]

47.30***

[0.000]

Driscoll-Kraay's robust standard errors are in brackets, p-values are shown in square brackets and we use ***

, **

and * to indicate the statistical significance and the rejection of the null hypothesis at the 1%, 5% and

10% levels, respectively. The panel DOLS has been estimated by using fifteen lags and leads of the first

difference of the explanatory variable chosen by the Schwarz information criterion (Schwarz, 1978). The

sample period goes from October 1st 2008 to September 28th 2010 (728 observations).

30

Figure 1. Degree of concentration in the Spanish fuel sector across regions

Note: The colour intensity represents the degree of industrial concentration measured by through regional

Herfindahl indexes (minimum: 0.069 and maximum 0.456) corresponding to data for diesel service stations

from 6th

July 2009 (collected from the Spanish Ministry of Industry, Energy and Tourism).

Autonomous Community Province

(NUTS 2) (NUTS 3)

Andalucía (ES61) Almería (ES611), Cádiz (ES612), Córdoba (ES613), Granada (ES614), Huelva (ES615),

Jaén (ES616), Málaga (ES617), Sevilla (ES618)

Aragón (ES24) Huesca (ES241), Teruel (ES242), Zaragoza (ES243)

Principado de Asturias (ES12) Asturias (ES120)

Islas Baleares (ES53) Baleares (ES530)

Islas Canarias (ES70) Las Palmas (ES701), Santa Cruz de Tenerife (ES702)

Cantabria (ES13) Cantabria (ES130)

Castilla la Mancha (ES42) Albacete (ES421), Ciudad Real (ES422), Cuenca (ES423), Guadalajara (ES424), Toledo

(ES425)

Castilla y León (ES41) Ávila (ES411), Burgos (ES412), León (ES413), Palencia (ES414), Salamanca (ES415),

Segovia (ES416), Soria (ES417), Valladolid (ES418), Zamora (ES419)

Cataluña (ES51) Barcelona (ES511), Girona (ES512), Lleida (ES513), Tarragona (ES514)

Comunidad Valenciana (ES52) Alicante (ES521), Castellón (ES522), Valencia (ES523)

Extremadura (ES43) Badajoz (ES431), Cáceres (ES432)

Galicia (ES11) A Coruña (ES111), Lugo (ES112), Ourense (ES113), Pontevedra (ES114)

La Rioja (ES23) La Rioja (ES230)

Comunidad de Madrid (ES30) Madrid (ES300)

Comunidad Foral de Navarra (ES22) Navarra (ES220)

País Vasco (ES21) Álava (ES211), Guipúzcoa (ES212), Vizcaya (ES213)

Región de Murcia (ES62) Murcia (ES621)