Embed Size (px)

Citation preview

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 1/7

Texas A&M University-Corpus Christi Division of Research, Commercialization & Outreach Office of Research Development Presentation:

The Lone Star Unmanned Aircraft Systems Center of Excellence & Innovation To: Alpine-Casparis Municipal Airport Advisory Board Date: June 19, 2013 We appreciate this opportunity to appear before the advisory board of the Alpine-Casparis Municipal Airport. My name is Ron George. I am senior research development officer at Texas A&M University-Corpus Christi. I am accompanied by Luis Cifuentes, Vice President for Research, Commercialization & Outreach at TAMUCC and Matt Nelson with Camber Corporation, a private-sector company that ably assisted the university and its statewide team with its proposal to the Federal Aviation Administration’s unmanned aircraft systems test-site program.

The U.S. Congress mandated in February 2012 that FAA develop a system of test sites for unmanned aircraft systems, or UAS. The legislation requires that six test sites be designated across the United States and that they be sufficiently diverse as to climate and topography to provide FAA with research and test data sufficient for the development of policies, procedures, rules and regulations that will enable integration of UAS into the national airspace.

For your convenience, I have attached a copy of the federal legislation to this presentation as Attachment 1.

Congress enacted this law because FAA seemed to be slow in addressing market demand. UAS operations are not permitted in our national airspace, except for limited purposes in highly restricted airspace and only by public entities. UAS may not be used for commercial purposes. FAA does permit UAS flights at altitudes up to 400 feet by hobbyists for non-commercial purposes; provided, that such operations do not interfere with general or commercial aviation.

UAS market demand has been building for a variety of reasons, but perhaps the most significant is the winding down of military operations in Iraq and Afghanistan, where UAS have played a significant role. UAS technologies developed over the past decade have applications and market value far beyond their military applications. Private-sector companies worldwide are eager to develop and sell these products, especially in the United States, where UAS technological development is far advanced. Entrepreneurs across the nation have been creating airframes and payloads of every conceivable size and industrial application. Some domestic government agencies already have put these technologies to use, most notably in border security but also in monitoring wildfires and for search and rescue operations in Alaska.

FAA, however, has taken a cautious approach to UAS integration, which is typical of this risk-averse agency. Safety is its primary and fundamental concern and mission. With literally tens of thousands of UAS vehicles poised to take flight, FAA wants to be sure that technological and airspace-management solutions are in place that will keep people and property safe in the air and on the ground. These agency concerns are immediately apparent in FAA’s solicitation for test-site contract proposals released in February of this year. We have attached the solicitation to this presentation as Attachment 2, but here is a quick summary of FAA requirements.

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 2/7

• Our test-site team is required to have at least five years within the past seven years of aviation research and development experience.

• Our team is required to have at least one year of UAS experience within the past five years.

• Our proposed test ranges must not include Class B airspace, where major airport operations occur.

• Proposed UAS test ranges must have launch and recovery sites within them. • Our proposed test ranges “must be sufficient for FAA safety and efficiency

determinations to protect persons and property on the ground.” • Our proposed UAS test ranges must be feasible; viz., FAA must believe that we’re

capable of managing the test ranges we propose.

And that, as they say, is only the beginning.

• Our team must show that its research goals, objectives and capacities align with FAA R&D objectives, which are as follows:

o UAS system safety and data gathering; o aircraft certification; o command and control link issues; o control station layout and certification; o ground and airborne sense and avoid research; o environmental impacts associated with UAS operations in the national airspace.

• Our team must show that our research capacities support FAA’s overarching goal: “Safely integrating UAS into the NAS.”

• Our team must show that it possesses or has access to sufficient aviation infrastructure to conduct ground and flight operations that will enable FAA to reach its R&D objectives.

• Our team must show that it has in place airspace-management and safety plans, standard operating procedures and command and control facilities capable of providing FAA the data it needs for rule-making while – and this is of critical importance – ensuring safety on the ground and in the air.

FAA requirements for the test-site program are extremely detailed and rigorous, as you can see from the attached solicitation (DTFACT-13-R-00002). Now, for a surprise: This contract is not funded, at least not for the current fiscal year and perhaps not for the next. It’s likely that the agency is using this lack of funding as a discriminator, so that only seriously capable applicants will apply; those willing – without federal financial support – to take on the mission and its financial burdens; which, by the way, includes considerable resources even to apply for the test-site program.

Well, it may have been a discriminator but not much of one, because 50 teams from 37 states, including Texas, have submitted proposals to this program. The more competitive teams have invested millions of dollars in cash, time and effort developing their proposals. Pre-submission competition was intense as teams across the country sought to improve their chances by soliciting the best and brightest UAS researchers and most knowledgeable consultants and subject-matter experts. Consultants for this competition have had a field day, but no one is begrudging them a cent, because we’re all looking upon our expenditures as an investment in future economic development.

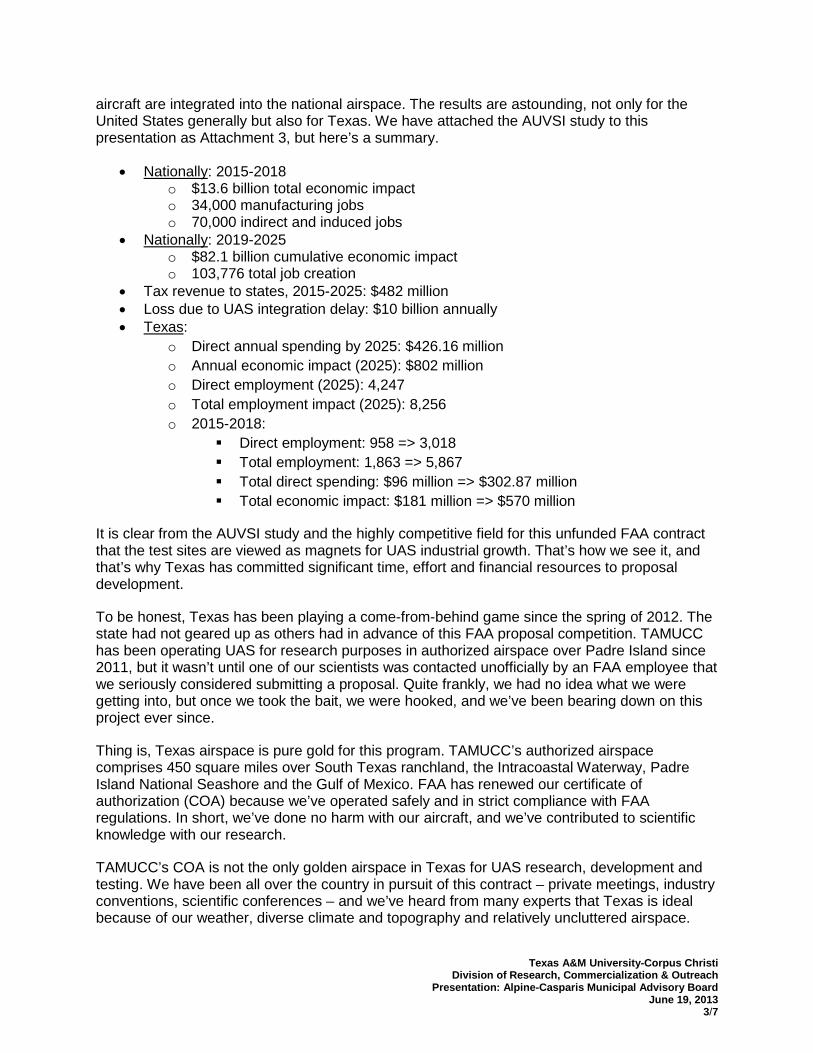

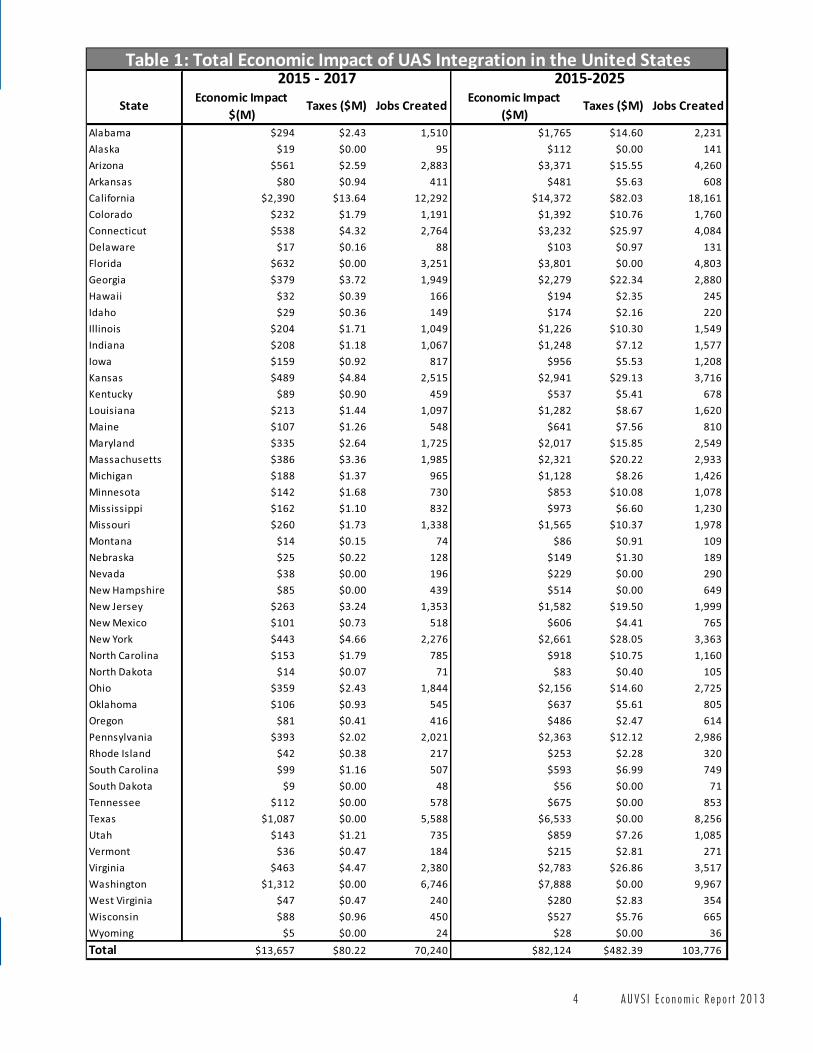

Early in the spring, the Association for Unmanned Vehicle Systems International (AUVSI) released an economic-impact study projecting how the UAS industry would develop once these

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 3/7

aircraft are integrated into the national airspace. The results are astounding, not only for the United States generally but also for Texas. We have attached the AUVSI study to this presentation as Attachment 3, but here’s a summary.

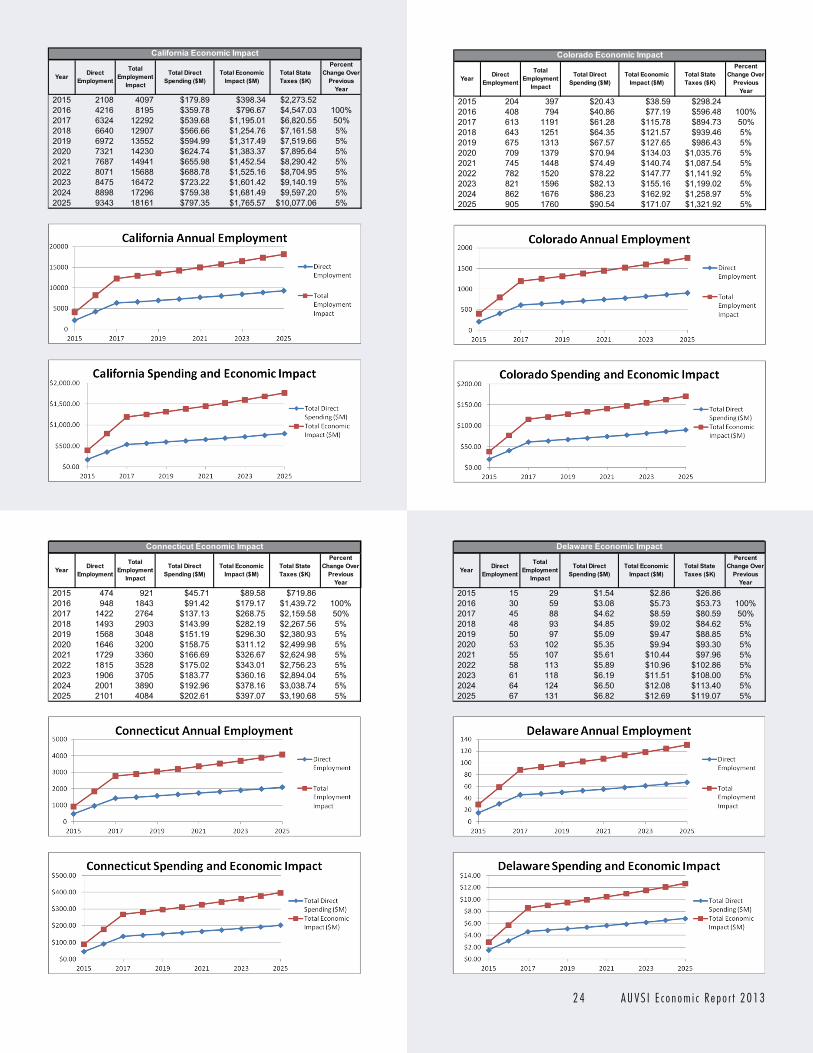

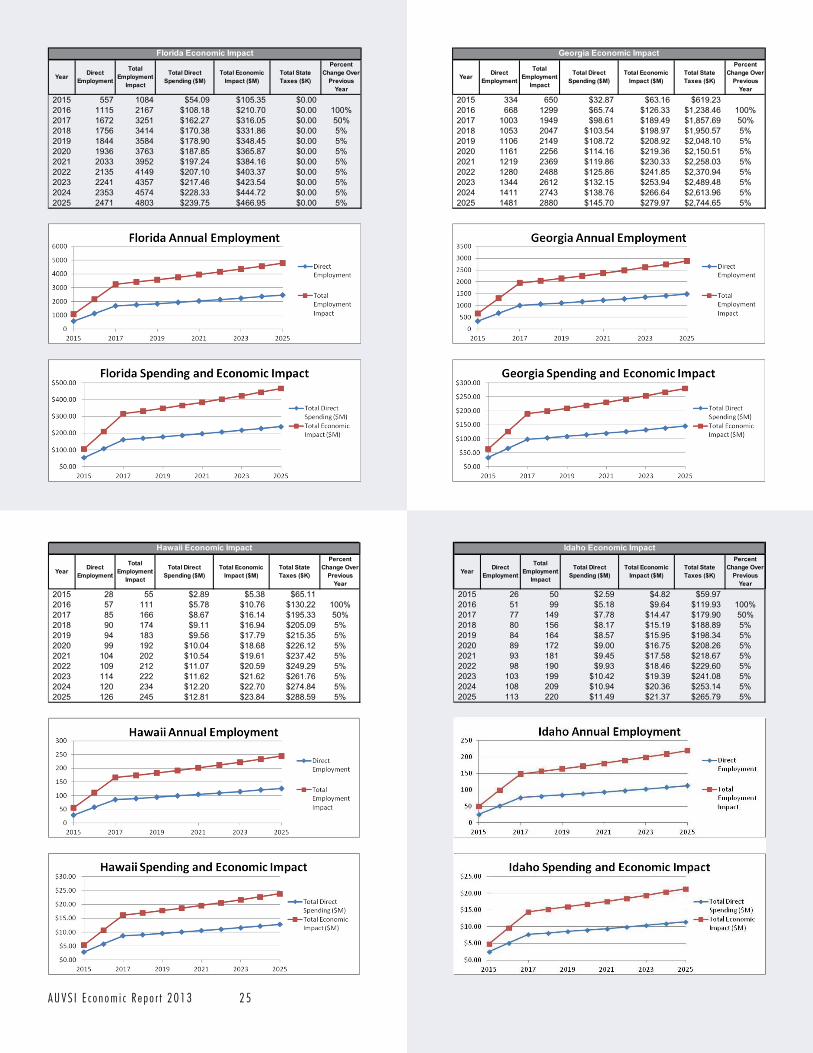

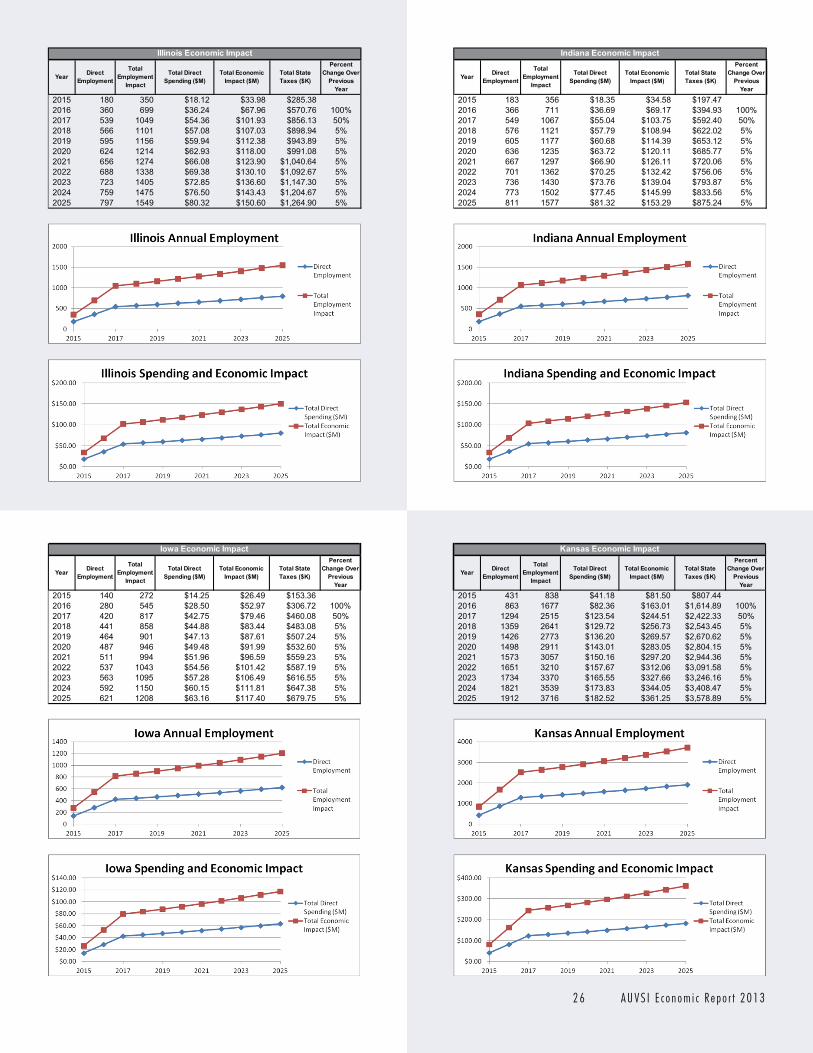

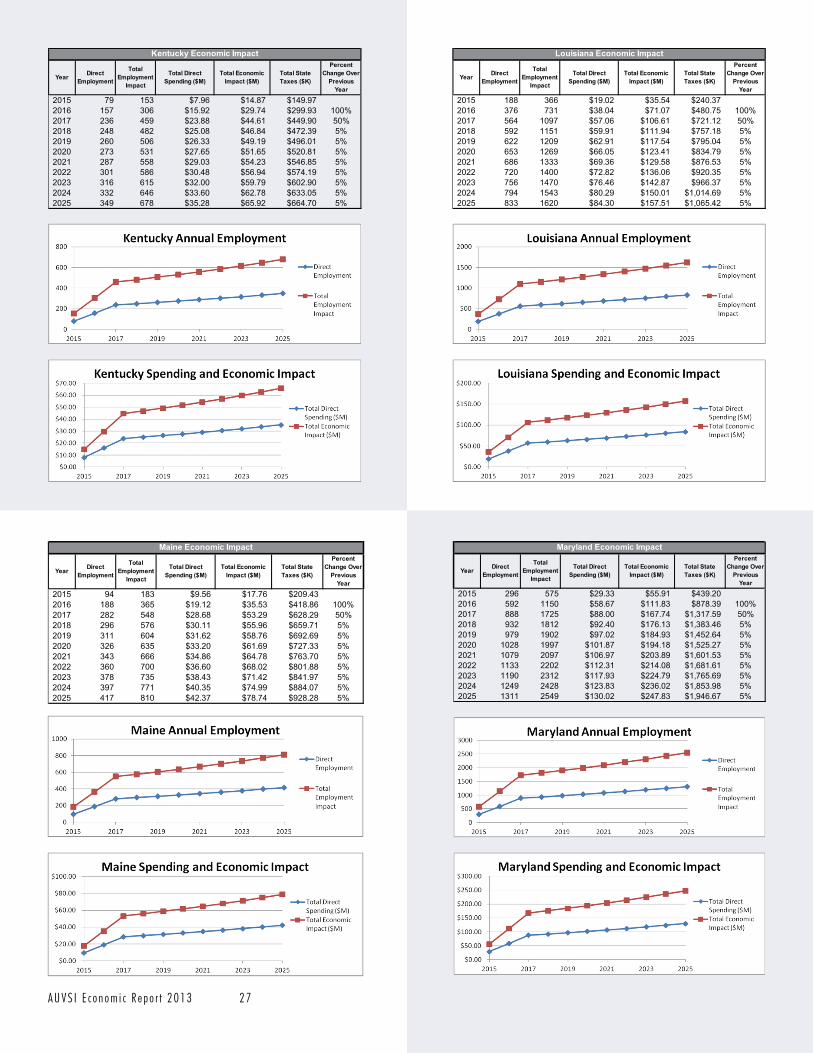

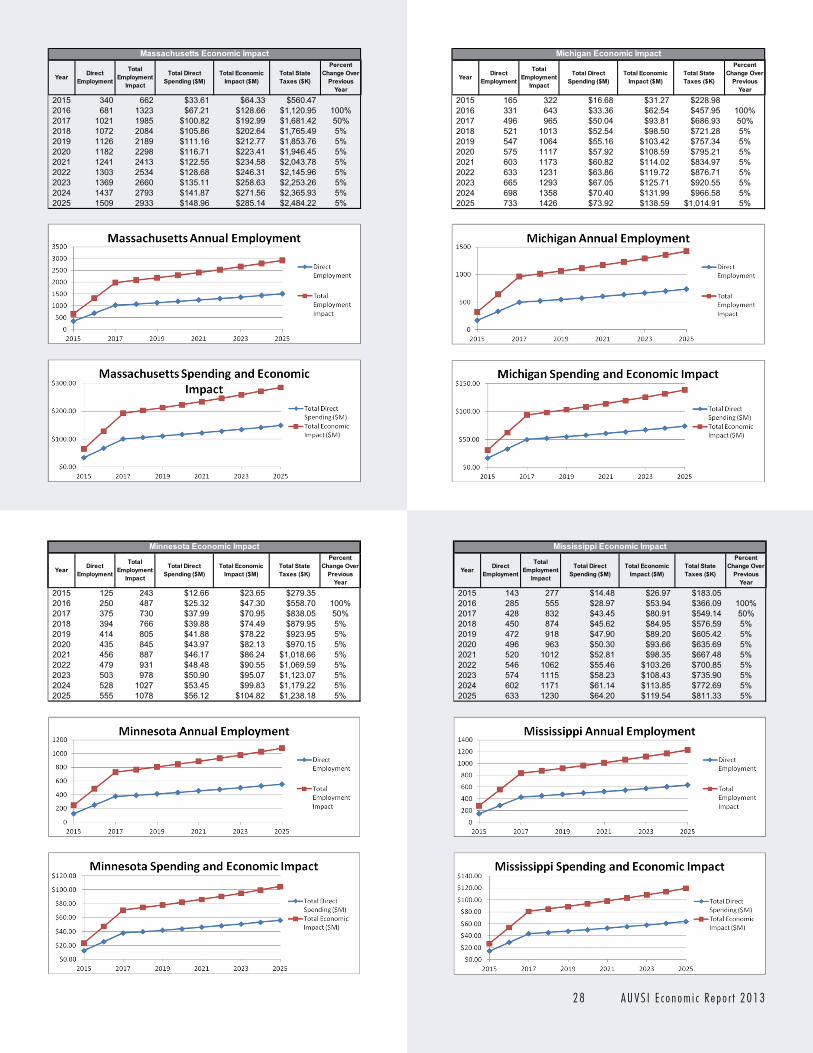

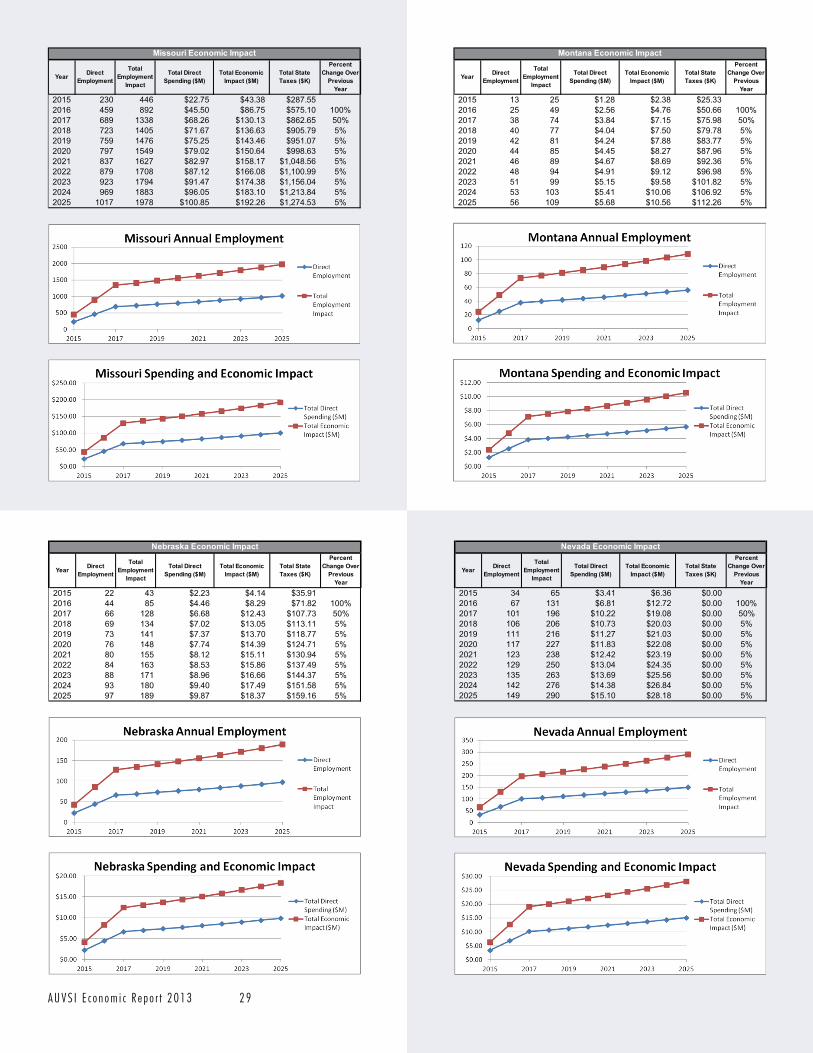

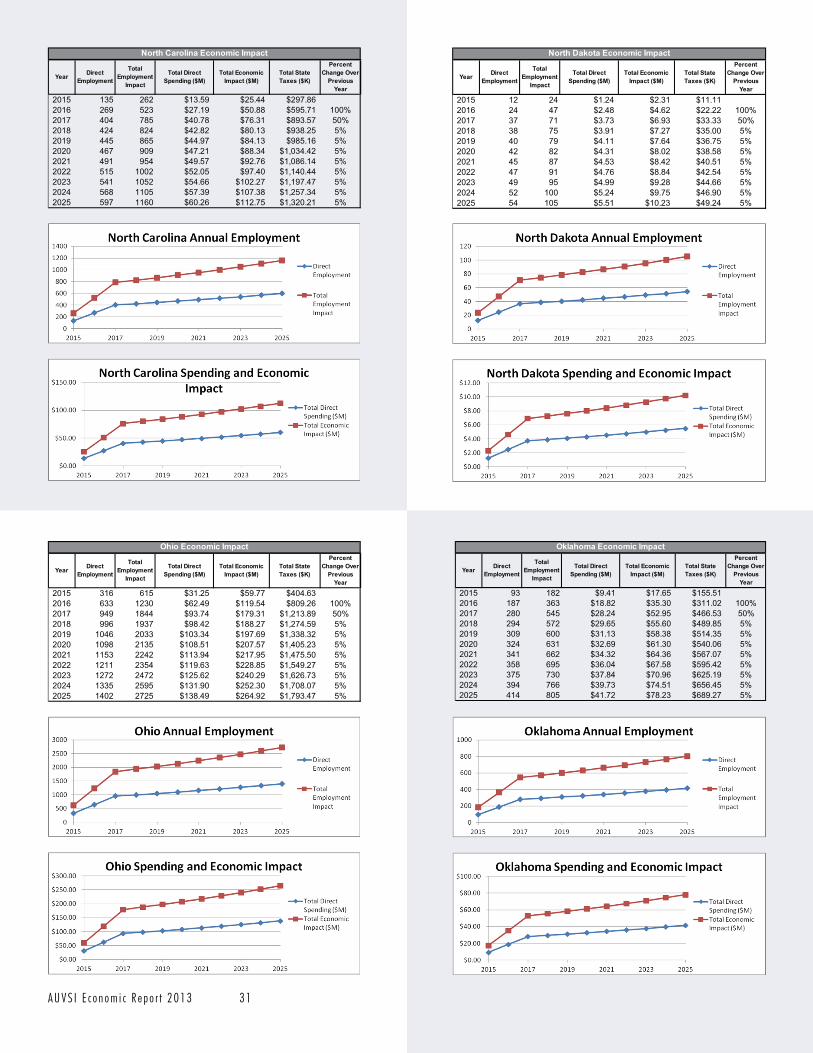

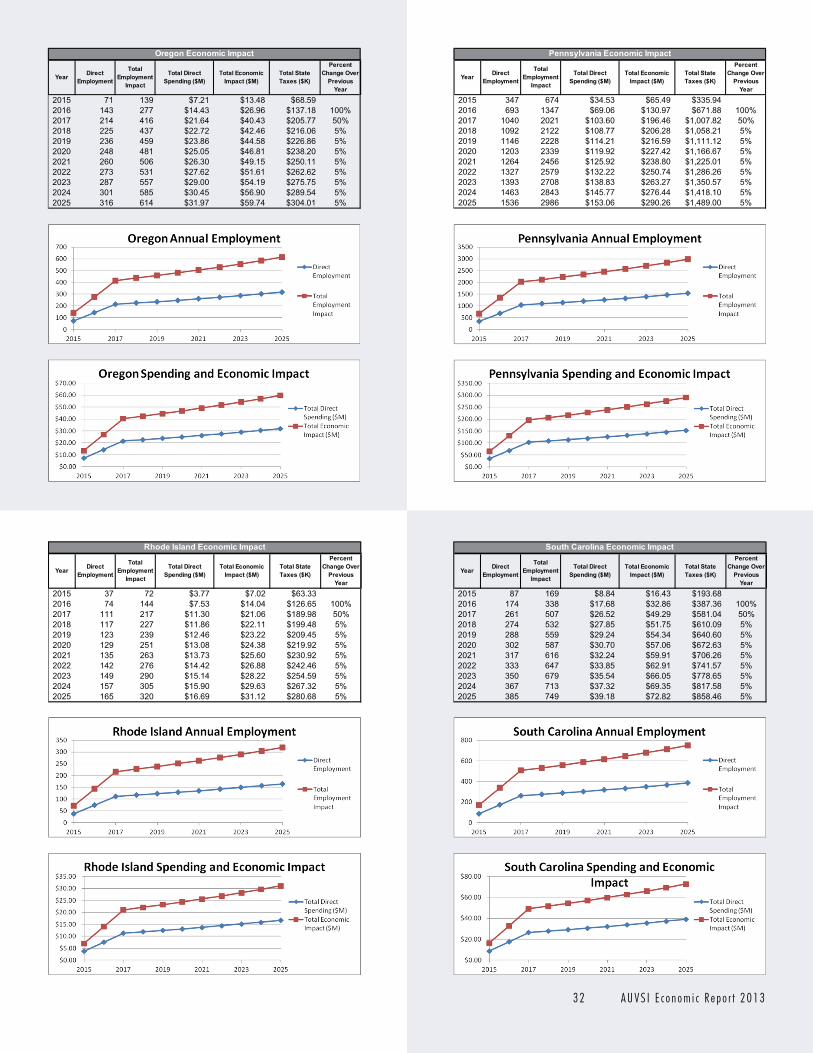

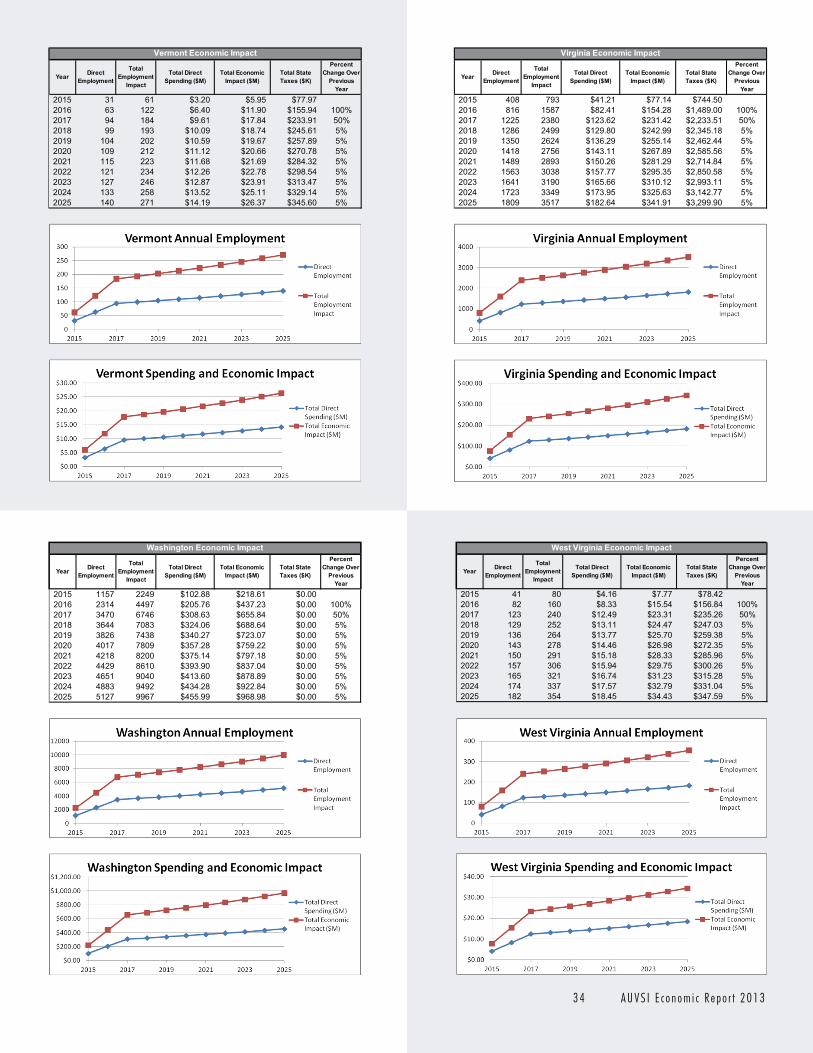

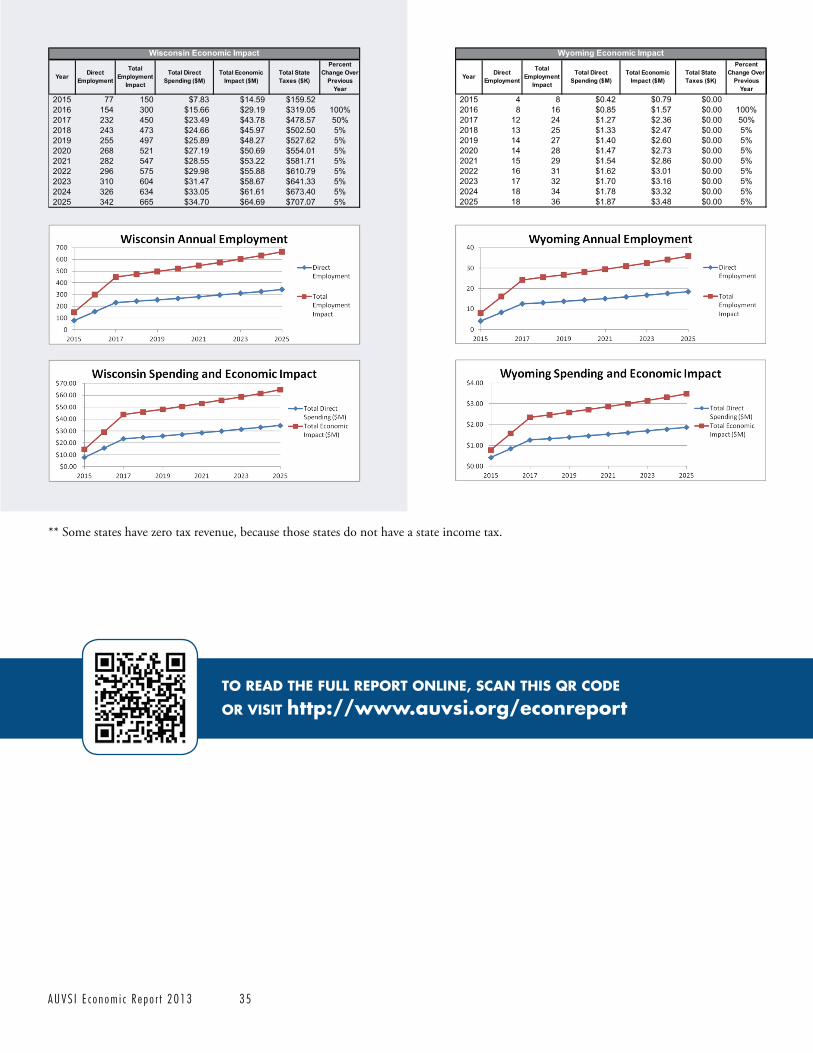

• Nationally: 2015-2018 o $13.6 billion total economic impact o 34,000 manufacturing jobs o 70,000 indirect and induced jobs

• Nationally: 2019-2025 o $82.1 billion cumulative economic impact o 103,776 total job creation

• Tax revenue to states, 2015-2025: $482 million • Loss due to UAS integration delay: $10 billion annually • Texas:

o Direct annual spending by 2025: $426.16 million o Annual economic impact (2025): $802 million o Direct employment (2025): 4,247 o Total employment impact (2025): 8,256 o 2015-2018:

Direct employment: 958 => 3,018 Total employment: 1,863 => 5,867 Total direct spending: $96 million => $302.87 million Total economic impact: $181 million => $570 million

It is clear from the AUVSI study and the highly competitive field for this unfunded FAA contract that the test sites are viewed as magnets for UAS industrial growth. That’s how we see it, and that’s why Texas has committed significant time, effort and financial resources to proposal development.

To be honest, Texas has been playing a come-from-behind game since the spring of 2012. The state had not geared up as others had in advance of this FAA proposal competition. TAMUCC has been operating UAS for research purposes in authorized airspace over Padre Island since 2011, but it wasn’t until one of our scientists was contacted unofficially by an FAA employee that we seriously considered submitting a proposal. Quite frankly, we had no idea what we were getting into, but once we took the bait, we were hooked, and we’ve been bearing down on this project ever since.

Thing is, Texas airspace is pure gold for this program. TAMUCC’s authorized airspace comprises 450 square miles over South Texas ranchland, the Intracoastal Waterway, Padre Island National Seashore and the Gulf of Mexico. FAA has renewed our certificate of authorization (COA) because we’ve operated safely and in strict compliance with FAA regulations. In short, we’ve done no harm with our aircraft, and we’ve contributed to scientific knowledge with our research.

TAMUCC’s COA is not the only golden airspace in Texas for UAS research, development and testing. We have been all over the country in pursuit of this contract – private meetings, industry conventions, scientific conferences – and we’ve heard from many experts that Texas is ideal because of our weather, diverse climate and topography and relatively uncluttered airspace.

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 4/7

Our aircraft at TAMUCC is a relatively small American Aerospace RS-16 – wingspan 13 feet, weight 85 pounds, payload 25 pounds, ceiling, 15,000 feet – modified by our private-sector partner for research, which has generated a great deal of interest in the oil and gas industry, for instance, and among state agencies such as the General Land Office and Parks and Wildlife. The national seashore welcomes our research operations and sees potential for using UAS technologies in its surveillance of the park, especially invaluable, delicate ecosystems on its western shore. Small UAS such as ours, not the high-flying vehicles configured for military use, will be the most likely industry growth area, according to knowledgeable folks we’ve met along the way. Applications are numerous: precision agriculture, pipeline and platform monitoring, wildlife and livestock monitoring, surveying, refinery inspection, shipping monitoring – all of which can be accomplished effectively and efficiently with UAS.

TAMUCC has land-use agreements with private-property owners and a South Texas airport from which we launch chase-plane operations; and, we have an agreement with the national seashore that requires that we notify its headquarters of scheduled missions. Our standard operating procedures require that we be in contact with air-traffic control towers in Corpus Christi and Kingsville and the U.S. Dept. of Homeland Security. In other words, every aspect of our UAS operations is carefully monitored for compliance with FAA regulations; if they weren’t, we would lose our COA.

TAMUCC is not going to get rich from this research, but we believe we are carving a niche for ourselves that will enable us to leverage funded research from public and private sources, which will benefit our students and the economic development of Texas. Our principal mission is educational, and our service to the community is economic. As an FAA test-site, our research will serve an important national purpose.

Among other things, and by no means least important, is the development of policies and procedures regarding UAS operations and personal privacy. TAMUCC is currently exploring ways to engage our faculty in legal and ethical research that will lead to model policies that will protect personal privacy while permitting the kind of technological and industrial growth that will benefit the state and national economy, especially by creating high-paying jobs for our graduates. FAA has announced its intention to develop policies and procedures that will prohibit invasions of privacy by UAS operations in the national airspace.

TAMUCC and its UAS test-site team have invested heavily in this project. I hope you will agree how important it is, in this extremely competitive environment, that specifics of our proposal not be made public until the selection process is complete. Final submissions were due to the FAA on May 6. We are now in the post-submission phase of the competition, during which the FAA will conduct site visits and likely will require oral presentations of competition finalists. We are in high gear preparing for this phase of the selection process, and that includes gathering as much intelligence as we can on our competition – and, believe me, they are looking just as hard for information about our proposal, too. FAA has said it will designate its UAS test sites – six among 50 applicants from 37 states – no later than Dec. 31. Until that announcement is made, specific plans of the Lone Star UAS Center of Excellence & Innovation must remain under wraps.

All of which is not say we cannot be responsive to questions raised by this board in a correspondence with my office dated May 6, 2013. Operational specifics in the following answers relate to current standard operating procedures in TAMUCC authorized airspace.

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 5/7

Q: How will ground movement be monitored?

A: UAS ground movement on taxiways and runways is always monitored by ground visual observers as directed by the FAA. Ground control stations (GCS) receive metadata or GPS data from the aircraft. These data provide current aircraft position and speed.

Q: What are the proposed hours of operation?

A: The Lone Star UAS Team has identified ideal operating hours per day according to weather and aviation traffic data collected over a 10-year period. The team concluded that the preferred mission time is Monday-Friday from 10 a.m. to 4 p.m. This schedule reflects the maximum operational hours. It does not reflect the number of actual operational days or hours needed to meet the research goals and objectives of the Lone Star UAS Test Site. This time period minimizes potential hazardous visibility and wind conditions. Weekend and nighttime (midnight to 4 a.m.) operations also are viable as permitted by the FAA.

Q: Will there be a chase plane to accompany the UAS during takeoff and landing?

A: FAA requires visual observers during all UAS operations. The visual observer must be within one mile of the unmanned aircraft at all times. This visual observer is permitted to be on the ground at the launch and recovery site as well as in a chase plane. The Lone Star UAS Team has used chase planes in order to adhere to the FAA regulations for visual observers. Chase aircraft support of unmanned air vehicle flight has one objective: “the safety of non-participating aircraft flying to the rear and above, below or on both sides of the UAV.” Chase aircraft must be flown only by FAA certified/approved pilots.

Q: At what altitudes will the UAS fly?

A: UAS can fly at altitudes from surface to 60,000 feet above mean sea level (MSL). Specifics for UAS operations in this area are not available because there is no airspace authorized for use by UAS. What we have proposed must remain confidential until the site-selection process is complete.

Q: How will the UAS be separated from other aircraft in the area?

A: Direct and continuous contact with the controlling FAA facility, adjacent facilities, DOD ATC and outreach is maintained through direct communications, according to FAA regulations.

General aviation, commercial aviation and range flights may be separated by several standard means. The primary means for separating range flight activity is procedural. Separation by a single parameter or combination of the parameters of time, space and altitude maintains safe separation.

• Space separation refers to specific aircraft location within a range. This space is defined as the aircraft’s operational area or mission profile for that activity.

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 6/7

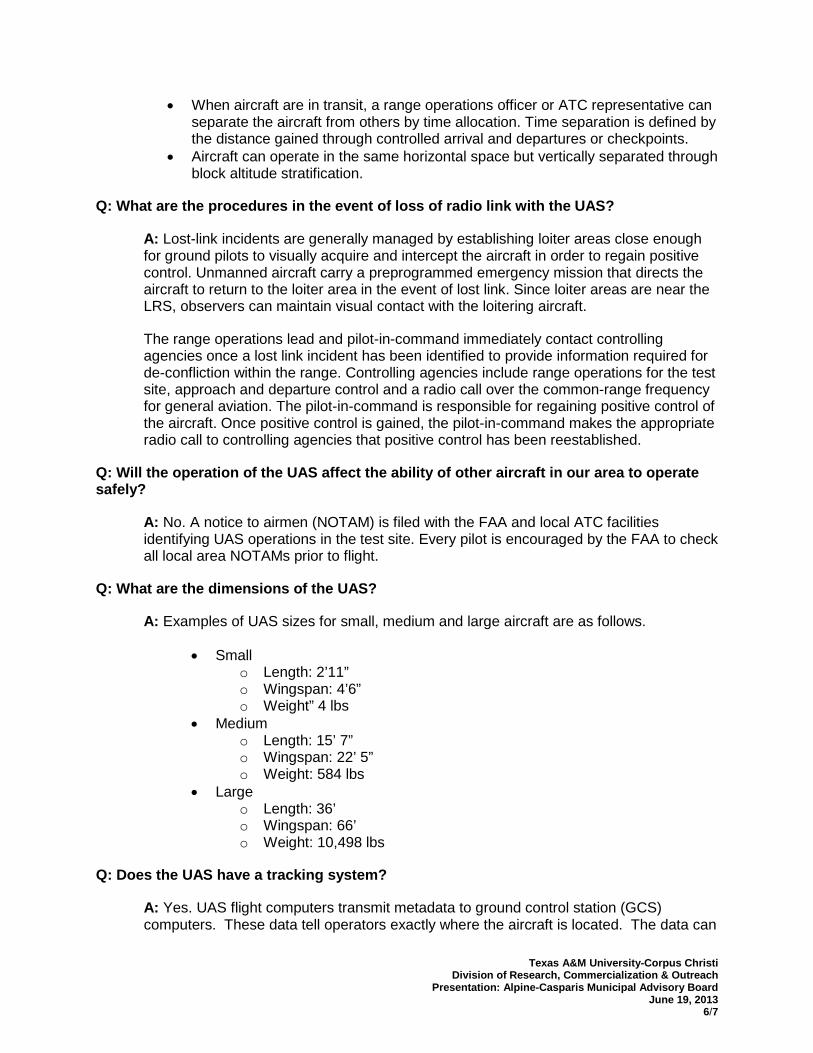

• When aircraft are in transit, a range operations officer or ATC representative can separate the aircraft from others by time allocation. Time separation is defined by the distance gained through controlled arrival and departures or checkpoints.

• Aircraft can operate in the same horizontal space but vertically separated through block altitude stratification.

Q: What are the procedures in the event of loss of radio link with the UAS?

A: Lost-link incidents are generally managed by establishing loiter areas close enough for ground pilots to visually acquire and intercept the aircraft in order to regain positive control. Unmanned aircraft carry a preprogrammed emergency mission that directs the aircraft to return to the loiter area in the event of lost link. Since loiter areas are near the LRS, observers can maintain visual contact with the loitering aircraft.

The range operations lead and pilot-in-command immediately contact controlling agencies once a lost link incident has been identified to provide information required for de-confliction within the range. Controlling agencies include range operations for the test site, approach and departure control and a radio call over the common-range frequency for general aviation. The pilot-in-command is responsible for regaining positive control of the aircraft. Once positive control is gained, the pilot-in-command makes the appropriate radio call to controlling agencies that positive control has been reestablished.

Q: Will the operation of the UAS affect the ability of other aircraft in our area to operate safely?

A: No. A notice to airmen (NOTAM) is filed with the FAA and local ATC facilities identifying UAS operations in the test site. Every pilot is encouraged by the FAA to check all local area NOTAMs prior to flight.

Q: What are the dimensions of the UAS?

A: Examples of UAS sizes for small, medium and large aircraft are as follows.

• Small o Length: 2’11” o Wingspan: 4’6” o Weight” 4 lbs

• Medium o Length: 15’ 7” o Wingspan: 22’ 5” o Weight: 584 lbs

• Large o Length: 36’ o Wingspan: 66’ o Weight: 10,498 lbs

Q: Does the UAS have a tracking system?

A: Yes. UAS flight computers transmit metadata to ground control station (GCS) computers. These data tell operators exactly where the aircraft is located. The data can

Texas A&M University-Corpus Christi

Division of Research, Commercialization & Outreach Presentation: Alpine-Casparis Municipal Advisory Board

June 19, 2013 7/7

be exported to third parties to enhance situational awareness on the test site. Larger UAS have Mode C transponders, which are the same as those in commercial U.S. passenger aircraft. These transponders meet all FAA requirements.

Q: Does the UAS have a collision avoidance system?

A: No, a major research goal of the test-site program to develop ground and airborne sense-and-avoid systems.

Q: What types of restrictions will be imposed in this area? Not only are there facilities in Marfa and Alpine, but there are numerous private strips that could be impacted by any flight restrictions that might be imposed by the Federal Aviation Administration.

A: No restrictions will be placed on the area by the Lone Star UAS Center of Excellence & Innovation. As stated above, NOTAMs are filed with the FAA and local ATC facilities identifying UAS operations.

Now, to answer a question that wasn’t asked: Why Alpine?

The Lone Star UAS Test Site airspace integration/management team carefully reviewed and evaluated each proposed test range within the test site. Evaluation criteria included:

• population densities; • visual flight rules/instrument flight rules (VFR/IFR) arrival and departures, airways and

military training routes; • wildlife areas; • public-gathering venues; • suitability for supporting research goals and objectives.

Care was taken to avoid densely-populated areas, manufacturing facilities, power plants and heavy-traffic areas for commercial and general aviation. This analysis identified sparsely populated areas of Texas. The design of the proposed COA around Alpine-Casparis Municipal Airport avoids populated areas around the city of Alpine and adheres to the FAA’s rules for flying over state and federal lands. Once we are no longer competition-sensitive, detailed maps and other documents related to our proposal will be available for public inspection.

Again, we appreciate this opportunity to address the advisory board of Alpine-Casparis Municipal Airport. On behalf of Dr. Cifuentes, Mr. Nelson and myself, thank you for your kind attention. We are at your disposal to answer questions from the board and from the public.

Respectfully submitted,

Ronald E. George Senior Research Development Officer Texas A&M University-Corpus Christi 361.825.5731 [email protected]

126 STAT. 72 PUBLIC LAW 112–95—FEB. 14, 2012

(e) USE OF DESIGNEES.—The Administrator may use designees to carry out subsection (a) to the extent practicable in order to minimize the burdens on pilots.

(f) REPORT TO CONGRESS.— (1) IN GENERAL.—Not later than 1 year after the date

of enactment of this Act, and annually thereafter, the Adminis-trator shall submit to the Committee on Transportation and Infrastructure of the House of Representatives and the Com-mittee on Commerce, Science, and Transportation of the Senate a report on the issuance of improved pilot licenses under this section.

(2) EXPIRATION.—The Administrator shall not be required to submit annual reports under this subsection after the date on which the Administrator has issued improved pilot licenses under this section to all pilots.

Subtitle B—Unmanned Aircraft Systems

SEC. 331. DEFINITIONS.

In this subtitle, the following definitions apply: (1) ARCTIC.—The term ‘‘Arctic’’ means the United States

zone of the Chukchi Sea, Beaufort Sea, and Bering Sea north of the Aleutian chain.

(2) CERTIFICATE OF WAIVER; CERTIFICATE OF AUTHORIZA-TION.—The terms ‘‘certificate of waiver’’ and ‘‘certificate of authorization’’ mean a Federal Aviation Administration grant of approval for a specific flight operation.

(3) PERMANENT AREAS.—The term ‘‘permanent areas’’ means areas on land or water that provide for launch, recovery, and operation of small unmanned aircraft.

(4) PUBLIC UNMANNED AIRCRAFT SYSTEM.—The term ‘‘public unmanned aircraft system’’ means an unmanned aircraft system that meets the qualifications and conditions required for operation of a public aircraft (as defined in section 40102 of title 49, United States Code).

(5) SENSE AND AVOID CAPABILITY.—The term ‘‘sense and avoid capability’’ means the capability of an unmanned aircraft to remain a safe distance from and to avoid collisions with other airborne aircraft.

(6) SMALL UNMANNED AIRCRAFT.—The term ‘‘small unmanned aircraft’’ means an unmanned aircraft weighing less than 55 pounds.

(7) TEST RANGE.—The term ‘‘test range’’ means a defined geographic area where research and development are con-ducted.

(8) UNMANNED AIRCRAFT.—The term ‘‘unmanned aircraft’’ means an aircraft that is operated without the possibility of direct human intervention from within or on the aircraft.

(9) UNMANNED AIRCRAFT SYSTEM.—The term ‘‘unmanned aircraft system’’ means an unmanned aircraft and associated elements (including communication links and the components that control the unmanned aircraft) that are required for the pilot in command to operate safely and efficiently in the national airspace system.

Applicability.

49 USC 40101 note.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00062 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 73 PUBLIC LAW 112–95—FEB. 14, 2012

SEC. 332. INTEGRATION OF CIVIL UNMANNED AIRCRAFT SYSTEMS INTO NATIONAL AIRSPACE SYSTEM.

(a) REQUIRED PLANNING FOR INTEGRATION.— (1) COMPREHENSIVE PLAN.—Not later than 270 days after

the date of enactment of this Act, the Secretary of Transpor-tation, in consultation with representatives of the aviation industry, Federal agencies that employ unmanned aircraft sys-tems technology in the national airspace system, and the unmanned aircraft systems industry, shall develop a com-prehensive plan to safely accelerate the integration of civil unmanned aircraft systems into the national airspace system.

(2) CONTENTS OF PLAN.—The plan required under para-graph (1) shall contain, at a minimum, recommendations or projections on—

(A) the rulemaking to be conducted under subsection (b), with specific recommendations on how the rulemaking will—

(i) define the acceptable standards for operation and certification of civil unmanned aircraft systems;

(ii) ensure that any civil unmanned aircraft system includes a sense and avoid capability; and

(iii) establish standards and requirements for the operator and pilot of a civil unmanned aircraft system, including standards and requirements for registration and licensing; (B) the best methods to enhance the technologies and

subsystems necessary to achieve the safe and routine oper-ation of civil unmanned aircraft systems in the national airspace system;

(C) a phased-in approach to the integration of civil unmanned aircraft systems into the national airspace system;

(D) a timeline for the phased-in approach described under subparagraph (C);

(E) creation of a safe (F) airspace designation for cooperative manned and

unmanned flight operations in the national airspace system;

(G) establishment of a process to develop certification, flight standards, and air traffic requirements for civil unmanned aircraft systems at test ranges where such sys-tems are subject to testing;

(H) the best methods to ensure the safe operation of civil unmanned aircraft systems and public unmanned aircraft systems simultaneously in the national airspace system; and

(I) incorporation of the plan into the annual NextGen Implementation Plan document (or any successor docu-ment) of the Federal Aviation Administration. (3) DEADLINE.—The plan required under paragraph (1)

shall provide for the safe integration of civil unmanned aircraft systems into the national airspace system as soon as prac-ticable, but not later than September 30, 2015.

(4) REPORT TO CONGRESS.—Not later than 1 year after the date of enactment of this Act, the Secretary shall submit to Congress a copy of the plan required under paragraph (1).

Deadline.

49 USC 40101 note.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00063 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 74 PUBLIC LAW 112–95—FEB. 14, 2012

(5) ROADMAP.—Not later than 1 year after the date of enactment of this Act, the Secretary shall approve and make available in print and on the Administration’s Internet Web site a 5-year roadmap for the introduction of civil unmanned aircraft systems into the national airspace system, as coordi-nated by the Unmanned Aircraft Program Office of the Adminis-tration. The Secretary shall update the roadmap annually. (b) RULEMAKING.—Not later than 18 months after the date

on which the plan required under subsection (a)(1) is submitted to Congress under subsection (a)(4), the Secretary shall publish in the Federal Register—

(1) a final rule on small unmanned aircraft systems that will allow for civil operation of such systems in the national airspace system, to the extent the systems do not meet the requirements for expedited operational authorization under sec-tion 333 of this Act;

(2) a notice of proposed rulemaking to implement the rec-ommendations of the plan required under subsection (a)(1), with the final rule to be published not later than 16 months after the date of publication of the notice; and

(3) an update to the Administration’s most recent policy statement on unmanned aircraft systems, contained in Docket No. FAA–2006–25714. (c) PILOT PROJECTS.—

(1) ESTABLISHMENT.—Not later than 180 days after the date of enactment of this Act, the Administrator shall establish a program to integrate unmanned aircraft systems into the national airspace system at 6 test ranges. The program shall terminate 5 years after the date of enactment of this Act.

(2) PROGRAM REQUIREMENTS.—In establishing the program under paragraph (1), the Administrator shall—

(A) safely designate airspace for integrated manned and unmanned flight operations in the national airspace system;

(B) develop certification standards and air traffic requirements for unmanned flight operations at test ranges;

(C) coordinate with and leverage the resources of the National Aeronautics and Space Administration and the Department of Defense;

(D) address both civil and public unmanned aircraft systems;

(E) ensure that the program is coordinated with the Next Generation Air Transportation System; and

(F) provide for verification of the safety of unmanned aircraft systems and related navigation procedures before integration into the national airspace system. (3) TEST RANGE LOCATIONS.—In determining the location

of the 6 test ranges of the program under paragraph (1), the Administrator shall—

(A) take into consideration geographic and climatic diversity;

(B) take into consideration the location of ground infra-structure and research needs; and

(C) consult with the National Aeronautics and Space Administration and the Department of Defense.

Consultation.

Standards.

Termination date.

Deadline.

Deadline. Federal Register, publication.

Deadlines. Publication. Web posting.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00064 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 75 PUBLIC LAW 112–95—FEB. 14, 2012

(4) TEST RANGE OPERATION.—A project at a test range shall be operational not later than 180 days after the date on which the project is established.

(5) REPORT TO CONGRESS.— (A) IN GENERAL.—Not later than 90 days after the

date of the termination of the program under paragraph (1), the Administrator shall submit to the Committee on Commerce, Science, and Transportation of the Senate and the Committee on Transportation and Infrastructure and the Committee on Science, Space, and Technology of the House of Representatives a report setting forth the Administrator’s findings and conclusions concerning the projects.

(B) ADDITIONAL CONTENTS.—The report under subpara-graph (A) shall include a description and assessment of the progress being made in establishing special use airspace to fill the immediate need of the Department of Defense—

(i) to develop detection techniques for small unmanned aircraft systems; and

(ii) to validate the sense and avoid capability and operation of unmanned aircraft systems.

(d) EXPANDING USE OF UNMANNED AIRCRAFT SYSTEMS IN ARCTIC.—

(1) IN GENERAL.—Not later than 180 days after the date of enactment of this Act, the Secretary shall develop a plan and initiate a process to work with relevant Federal agencies and national and international communities to designate permanent areas in the Arctic where small unmanned aircraft may operate 24 hours per day for research and commercial purposes. The plan for operations in these permanent areas shall include the development of processes to facilitate the safe operation of unmanned aircraft beyond line of sight. Such areas shall enable over-water flights from the surface to at least 2,000 feet in altitude, with ingress and egress routes from selected coastal launch sites.

(2) AGREEMENTS.—To implement the plan under paragraph (1), the Secretary may enter into an agreement with relevant national and international communities.

(3) AIRCRAFT APPROVAL.—Not later than 1 year after the entry into force of an agreement necessary to effectuate the purposes of this subsection, the Secretary shall work with rel-evant national and international communities to establish and implement a process, or may apply an applicable process already established, for approving the use of unmanned aircraft in the designated permanent areas in the Arctic without regard to whether an unmanned aircraft is used as a public aircraft, a civil aircraft, or a model aircraft.

SEC. 333. SPECIAL RULES FOR CERTAIN UNMANNED AIRCRAFT SYS-TEMS.

(a) IN GENERAL.—Notwithstanding any other requirement of this subtitle, and not later than 180 days after the date of enactment of this Act, the Secretary of Transportation shall determine if certain unmanned aircraft systems may operate safely in the national airspace system before completion of the plan and rule-making required by section 332 of this Act or the guidance required by section 334 of this Act.

Deadline. Determination.

49 USC 40101 note.

Deadline.

Deadline. Plans.

Deadline.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00065 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 76 PUBLIC LAW 112–95—FEB. 14, 2012

(b) ASSESSMENT OF UNMANNED AIRCRAFT SYSTEMS.—In making the determination under subsection (a), the Secretary shall deter-mine, at a minimum—

(1) which types of unmanned aircraft systems, if any, as a result of their size, weight, speed, operational capability, proximity to airports and populated areas, and operation within visual line of sight do not create a hazard to users of the national airspace system or the public or pose a threat to national security; and

(2) whether a certificate of waiver, certificate of authoriza-tion, or airworthiness certification under section 44704 of title 49, United States Code, is required for the operation of unmanned aircraft systems identified under paragraph (1). (c) REQUIREMENTS FOR SAFE OPERATION.—If the Secretary

determines under this section that certain unmanned aircraft sys-tems may operate safely in the national airspace system, the Sec-retary shall establish requirements for the safe operation of such aircraft systems in the national airspace system.

SEC. 334. PUBLIC UNMANNED AIRCRAFT SYSTEMS.

(a) GUIDANCE.—Not later than 270 days after the date of enact-ment of this Act, the Secretary of Transportation shall issue guid-ance regarding the operation of public unmanned aircraft systems to—

(1) expedite the issuance of a certificate of authorization process;

(2) provide for a collaborative process with public agencies to allow for an incremental expansion of access to the national airspace system as technology matures and the necessary safety analysis and data become available, and until standards are completed and technology issues are resolved;

(3) facilitate the capability of public agencies to develop and use test ranges, subject to operating restrictions required by the Federal Aviation Administration, to test and operate unmanned aircraft systems; and

(4) provide guidance on a public entity’s responsibility when operating an unmanned aircraft without a civil airworthiness certificate issued by the Administration. (b) STANDARDS FOR OPERATION AND CERTIFICATION.—Not later

than December 31, 2015, the Administrator shall develop and imple-ment operational and certification requirements for the operation of public unmanned aircraft systems in the national airspace system.

(c) AGREEMENTS WITH GOVERNMENT AGENCIES.— (1) IN GENERAL.—Not later than 90 days after the date

of enactment of this Act, the Secretary shall enter into agree-ments with appropriate government agencies to simplify the process for issuing certificates of waiver or authorization with respect to applications seeking authorization to operate public unmanned aircraft systems in the national airspace system.

(2) CONTENTS.—The agreements shall— (A) with respect to an application described in para-

graph (1)— (i) provide for an expedited review of the applica-

tion;

Deadline.

Deadline.

Deadline.

49 USC 40101 note.

Determination.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00066 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 77 PUBLIC LAW 112–95—FEB. 14, 2012

(ii) require a decision by the Administrator on approval or disapproval within 60 business days of the date of submission of the application; and

(iii) allow for an expedited appeal if the application is disapproved; (B) allow for a one-time approval of similar operations

carried out during a fixed period of time; and (C) allow a government public safety agency to operate

unmanned aircraft weighing 4.4 pounds or less, if oper-ated—

(i) within the line of sight of the operator; (ii) less than 400 feet above the ground; (iii) during daylight conditions; (iv) within Class G airspace; and (v) outside of 5 statute miles from any airport,

heliport, seaplane base, spaceport, or other location with aviation activities.

SEC. 335. SAFETY STUDIES.

The Administrator of the Federal Aviation Administration shall carry out all safety studies necessary to support the integration of unmanned aircraft systems into the national airspace system.

SEC. 336. SPECIAL RULE FOR MODEL AIRCRAFT.

(a) IN GENERAL.—Notwithstanding any other provision of law relating to the incorporation of unmanned aircraft systems into Federal Aviation Administration plans and policies, including this subtitle, the Administrator of the Federal Aviation Administration may not promulgate any rule or regulation regarding a model aircraft, or an aircraft being developed as a model aircraft, if—

(1) the aircraft is flown strictly for hobby or recreational use;

(2) the aircraft is operated in accordance with a community- based set of safety guidelines and within the programming of a nationwide community-based organization;

(3) the aircraft is limited to not more than 55 pounds unless otherwise certified through a design, construction, inspection, flight test, and operational safety program adminis-tered by a community-based organization;

(4) the aircraft is operated in a manner that does not interfere with and gives way to any manned aircraft; and

(5) when flown within 5 miles of an airport, the operator of the aircraft provides the airport operator and the airport air traffic control tower (when an air traffic facility is located at the airport) with prior notice of the operation (model aircraft operators flying from a permanent location within 5 miles of an airport should establish a mutually-agreed upon operating procedure with the airport operator and the airport air traffic control tower (when an air traffic facility is located at the airport)). (b) STATUTORY CONSTRUCTION.—Nothing in this section shall

be construed to limit the authority of the Administrator to pursue enforcement action against persons operating model aircraft who endanger the safety of the national airspace system.

(c) MODEL AIRCRAFT DEFINED.—In this section, the term ‘‘model aircraft’’ means an unmanned aircraft that is—

(1) capable of sustained flight in the atmosphere;

49 USC 40101 note.

49 USC 40101 note.

Deadline.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00067 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

126 STAT. 78 PUBLIC LAW 112–95—FEB. 14, 2012

(2) flown within visual line of sight of the person operating the aircraft; and

(3) flown for hobby or recreational purposes.

Subtitle C—Safety and Protections

SEC. 341. AVIATION SAFETY WHISTLEBLOWER INVESTIGATION OFFICE.

Section 106 (as amended by this Act) is further amended by adding at the end the following:

‘‘(t) AVIATION SAFETY WHISTLEBLOWER INVESTIGATION OFFICE.—

‘‘(1) ESTABLISHMENT.—There is established in the Federal Aviation Administration (in this subsection referred to as the ‘Agency’) an Aviation Safety Whistleblower Investigation Office (in this subsection referred to as the ‘Office’).

‘‘(2) DIRECTOR.— ‘‘(A) APPOINTMENT.—The head of the Office shall be

the Director, who shall be appointed by the Secretary of Transportation.

‘‘(B) QUALIFICATIONS.—The Director shall have a dem-onstrated ability in investigations and knowledge of or experience in aviation.

‘‘(C) TERM.—The Director shall be appointed for a term of 5 years.

‘‘(D) VACANCIES.—Any individual appointed to fill a vacancy in the position of the Director occurring before the expiration of the term for which the individual’s prede-cessor was appointed shall be appointed for the remainder of that term. ‘‘(3) COMPLAINTS AND INVESTIGATIONS.—

‘‘(A) AUTHORITY OF DIRECTOR.—The Director shall— ‘‘(i) receive complaints and information submitted

by employees of persons holding certificates issued under title 14, Code of Federal Regulations (if the certificate holder does not have a similar in-house whistleblower or safety and regulatory noncompliance reporting process) and employees of the Agency con-cerning the possible existence of an activity relating to a violation of an order, a regulation, or any other provision of Federal law relating to aviation safety;

‘‘(ii) assess complaints and information submitted under clause (i) and determine whether a substantial likelihood exists that a violation of an order, a regula-tion, or any other provision of Federal law relating to aviation safety has occurred; and

‘‘(iii) based on findings of the assessment conducted under clause (ii), make recommendations to the Administrator of the Agency, in writing, regarding fur-ther investigation or corrective actions. ‘‘(B) DISCLOSURE OF IDENTITIES.—The Director shall

not disclose the identity of an individual who submits a complaint or information under subparagraph (A)(i) unless—

‘‘(i) the individual consents to the disclosure in writing; or

Recommenda- tions.

VerDate Mar 15 2010 07:45 Mar 06, 2012 Jkt 019139 PO 00095 Frm 00068 Fmt 6580 Sfmt 6581 E:\PUBLAW\PUBL095.112 GPO1 PsN: PUBL095dkra

use

on D

SK

HT7

XV

N1P

RO

D w

ith P

UB

LIC

LA

WS

Unmanned Aircraft Systems Test Site Selection

SCREENING INFORMATION REQUESTDTFACT-13-R-00002

AMENDMENT 04 - March 20, 2013

Date: February 14, 2013

Paperwork Reduction Act - OMB No. 2120-0595

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 2 of 70

TABLE OF CONTENTS

1 PROJECT TITLE......................................................................................................... 4 2 SCREENING INFORMATION REQUEST (SIR) NO............................................... 4 3 AGREEMENT TYPE .................................................................................................. 4 4 ACQUISITION MANAGEMENT SYSTEM (AMS) ................................................. 4 5 PERIOD OF PERFORMANCE................................................................................... 4 6 MILESTONE SCHEDULES ....................................................................................... 4 7 BACKGROUND.......................................................................................................... 5 8 INSTRUCTIONS TO APPLICANTS ......................................................................... 9

8.1 Introduction..................................................................................................... 9 8.2 SIR Questions, Concerns, and Clarifications.................................................. 9 8.3 Place, Date, Time, and Format for Submission of Proposals ....................... 13 8.4 Discussions ................................................................................................... 18

9 SITE SELECTION EVALUATION.......................................................................... 18 9.1 Technical Evaluation .................................................................................... 18 9.2 Proposal Specific Instructions....................................................................... 19

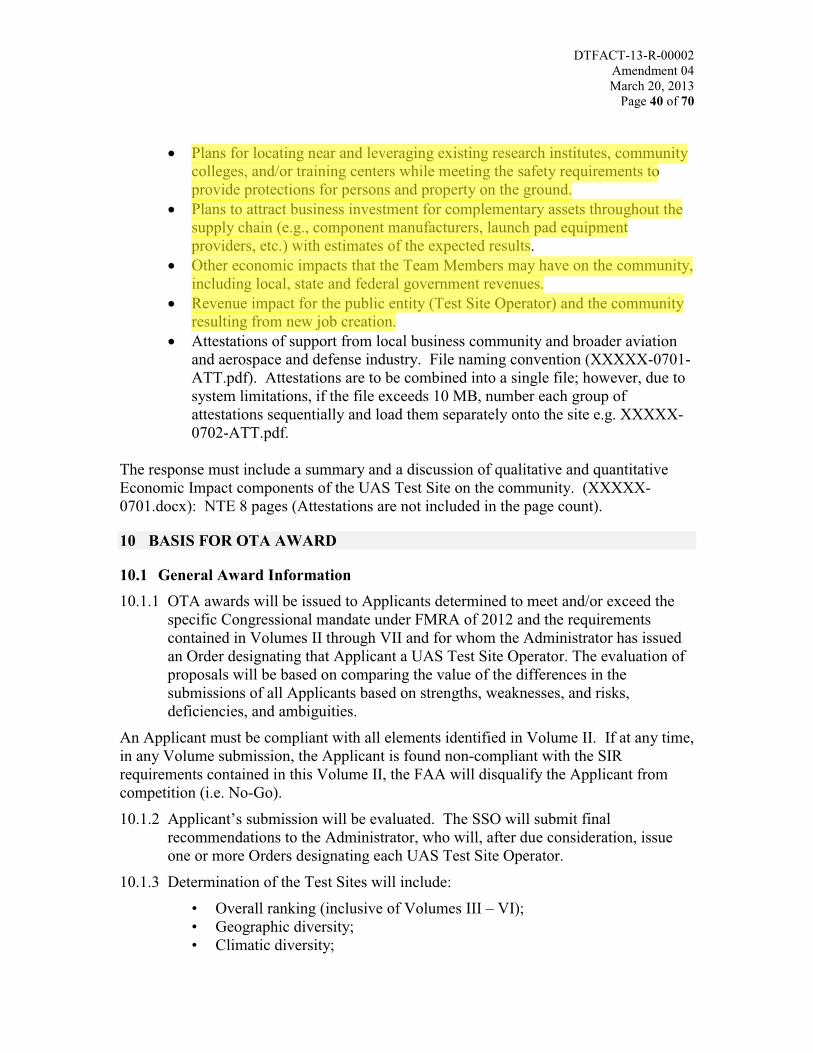

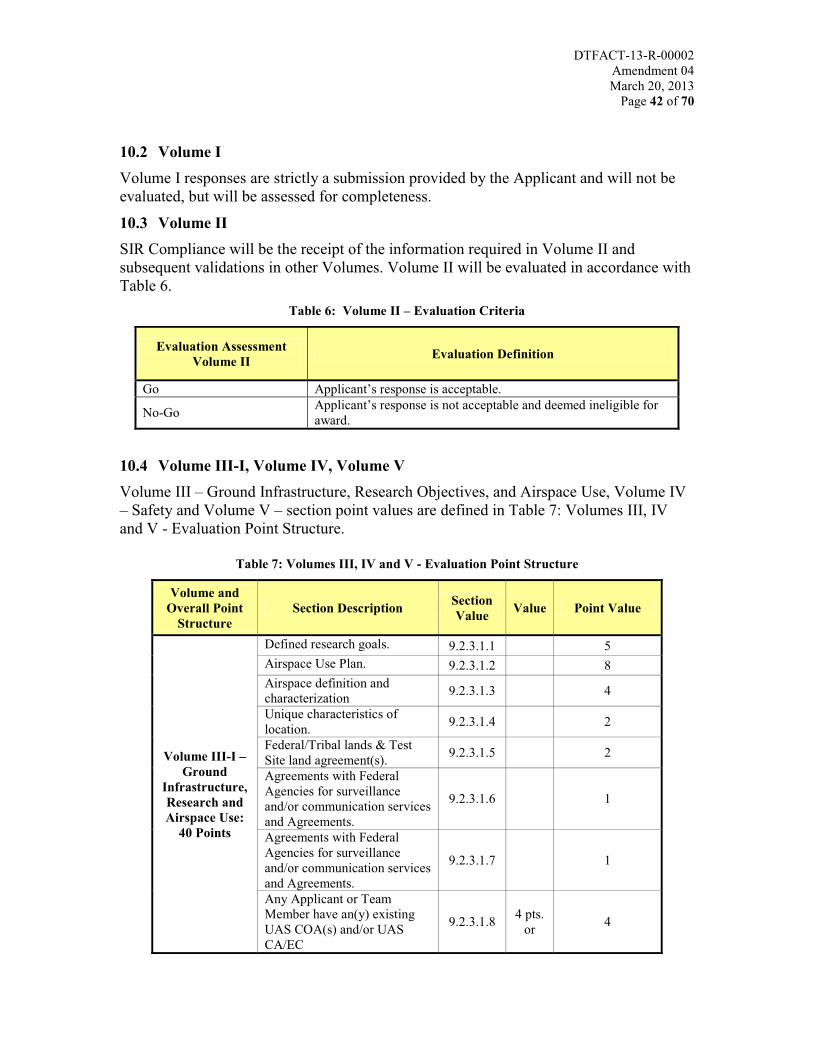

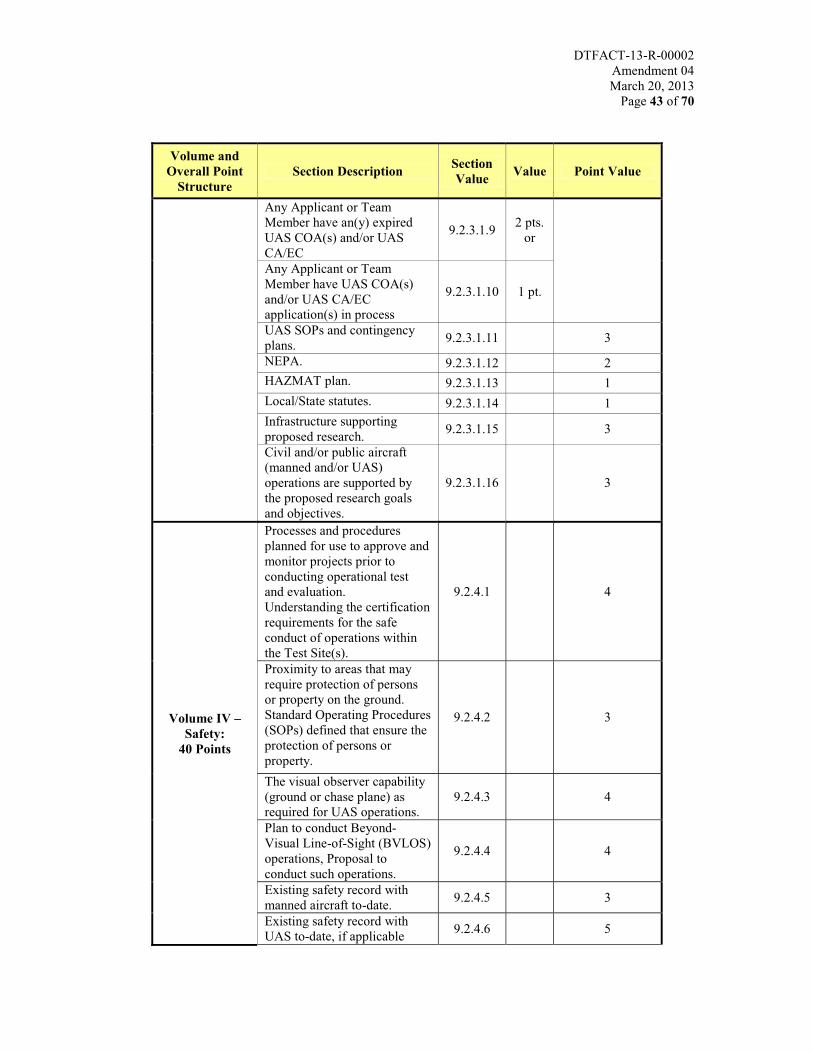

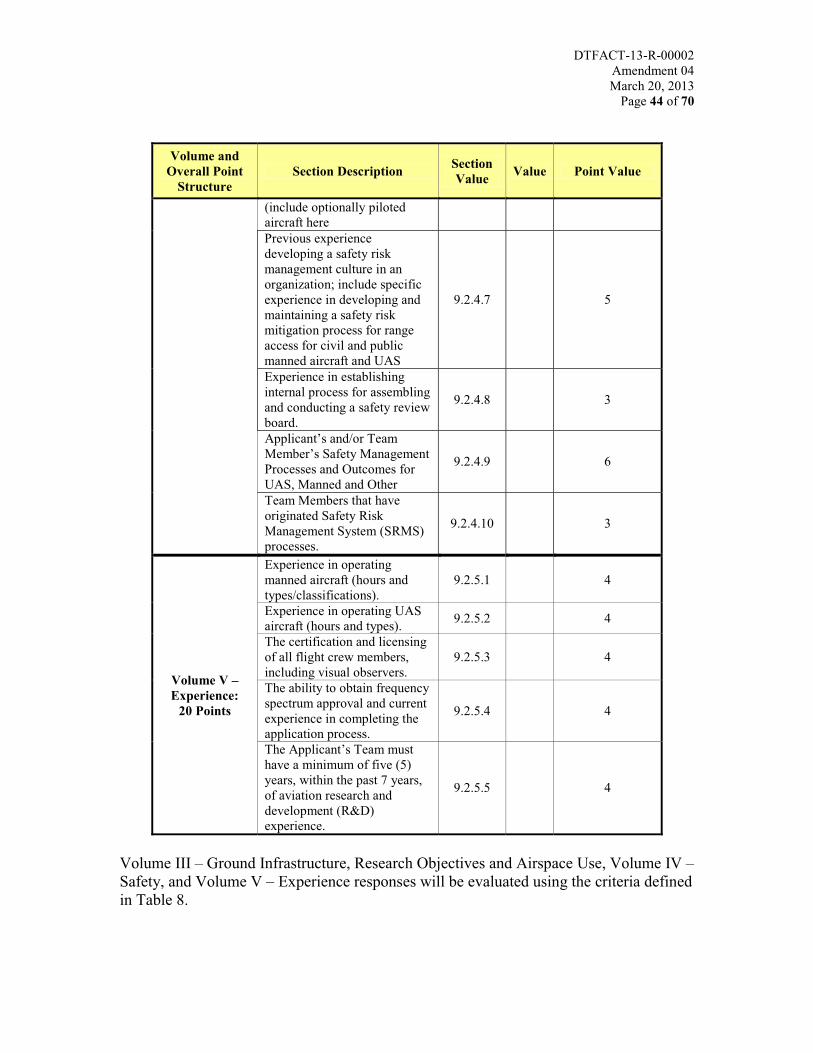

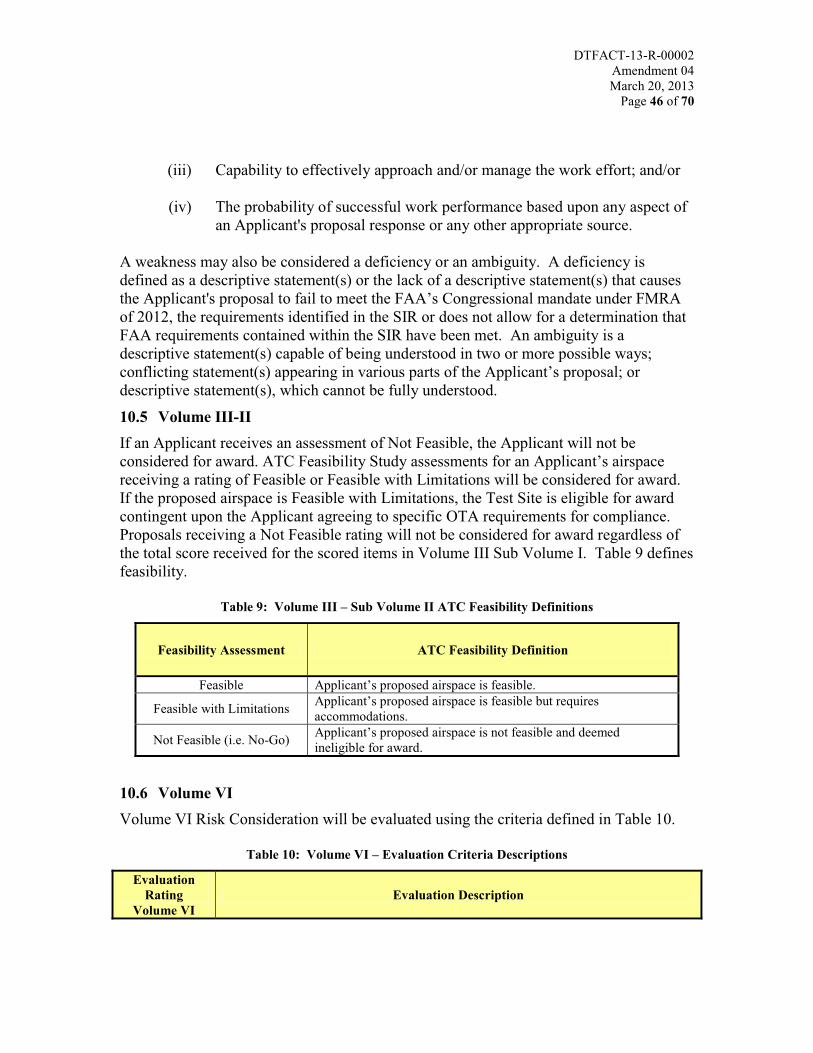

10 BASIS FOR OTA AWARD ...................................................................................... 40 10.1 General Award Information.......................................................................... 40 10.2 Volume I ....................................................................................................... 42 10.3 Volume II ...................................................................................................... 42 10.4 Volume III-I, Volume IV, Volume V ........................................................... 42 10.5 Volume III-II................................................................................................. 46 10.6 Volume VI .................................................................................................... 46 10.7 Volume VII ................................................................................................... 47

11 PERIOD OF OFFER.................................................................................................. 47 12 EXPENSES RELATED TO APPLICANT SUBMISSIONS .................................... 47 13 COMMUNICATIONS WITH APPLICANTS .......................................................... 48 14 NOTIFICATION OF AWARD AND DEBRIEFING OF UNSUCCESSFUL

APPLICANTS............................................................................................................ 48 15 DISPOSITION OF PROPOSALS ............................................................................. 48 16 NON-GOVERNMENT PERSONNEL PARTICIPATION ...................................... 48 17 PRE-AWARD SURVEYS......................................................................................... 49 18 RESPONSIBLE PROSPECTIVE APPLICANT....................................................... 49 19 CERTIFICATION OF REGISTRATION IN THE SYSTEM FOR AWARD

MANAGEMENT (SAM)........................................................................................... 50 20 SYSTEM FOR AWARD MANAGEMENT (SAM)................................................. 50 21 TABLE OF ATTACHMENTS.................................................................................. 54

21.1 Volume I – Attachment 1.............................................................................. 55 21.2 Volume I – Attachment 2.............................................................................. 58 21.3 Volume III – Sub-Volume I: Attachment 3 .................................................. 59 21.4 Volume III – Sub-Volume I: Attachment 4 .................................................. 60

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 3 of 70

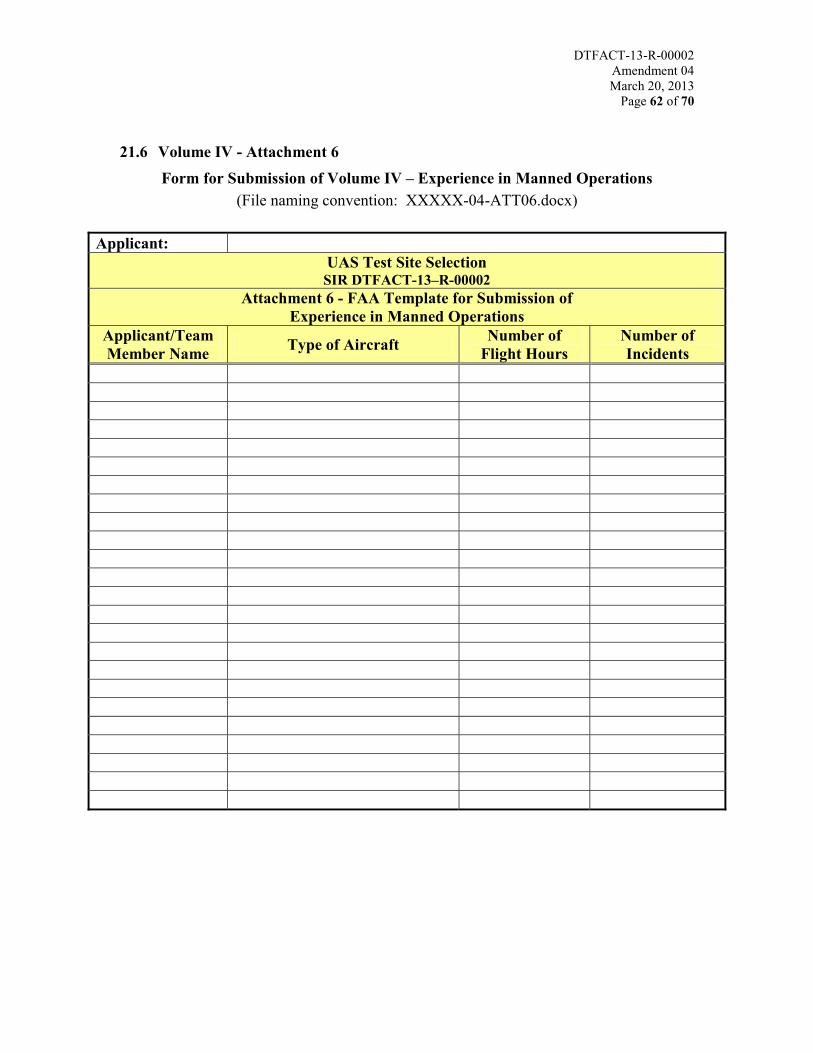

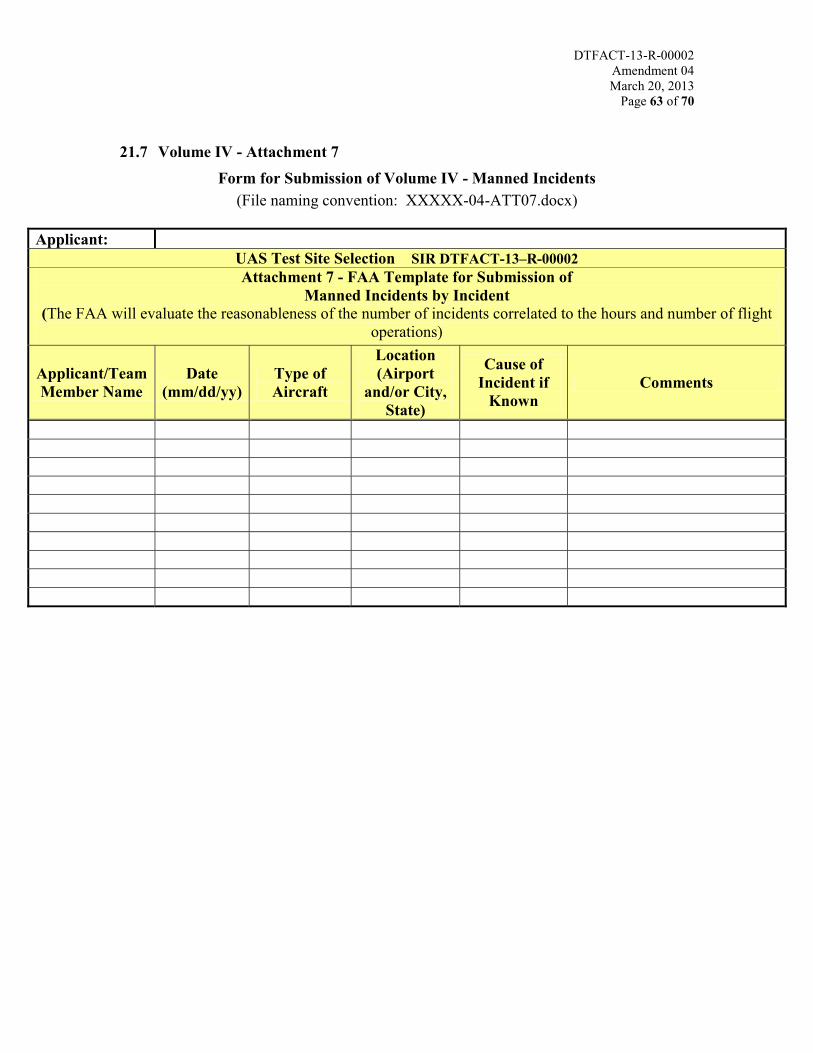

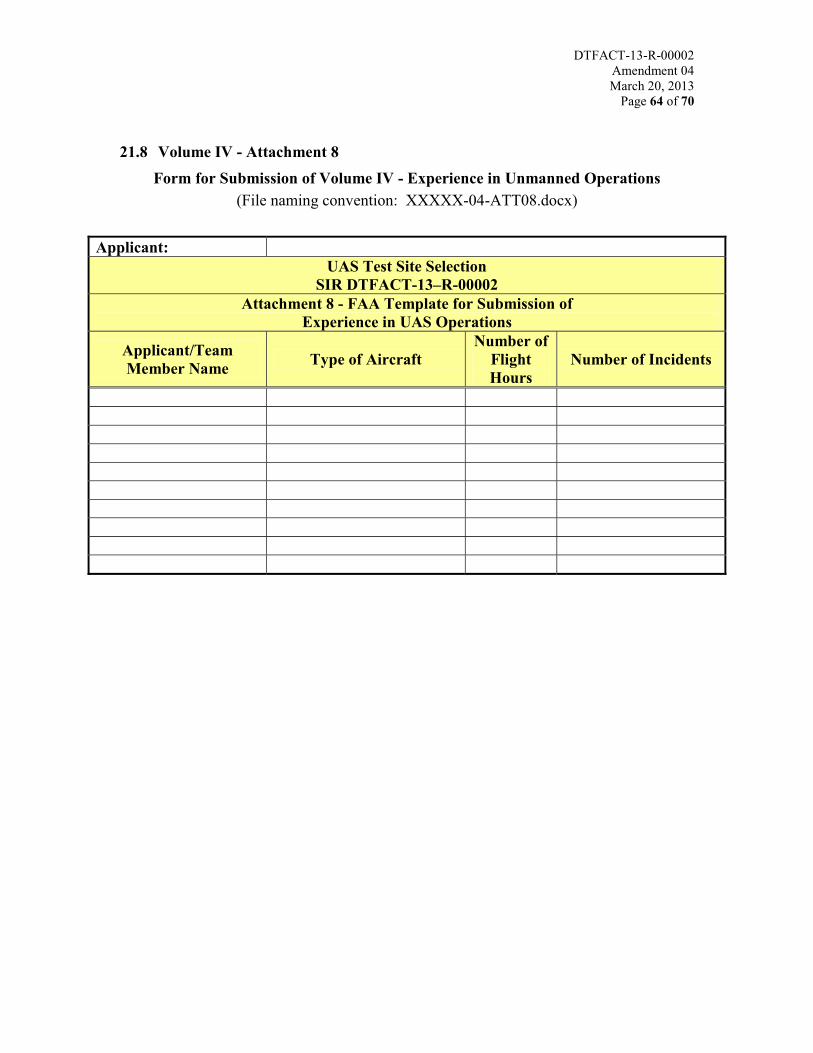

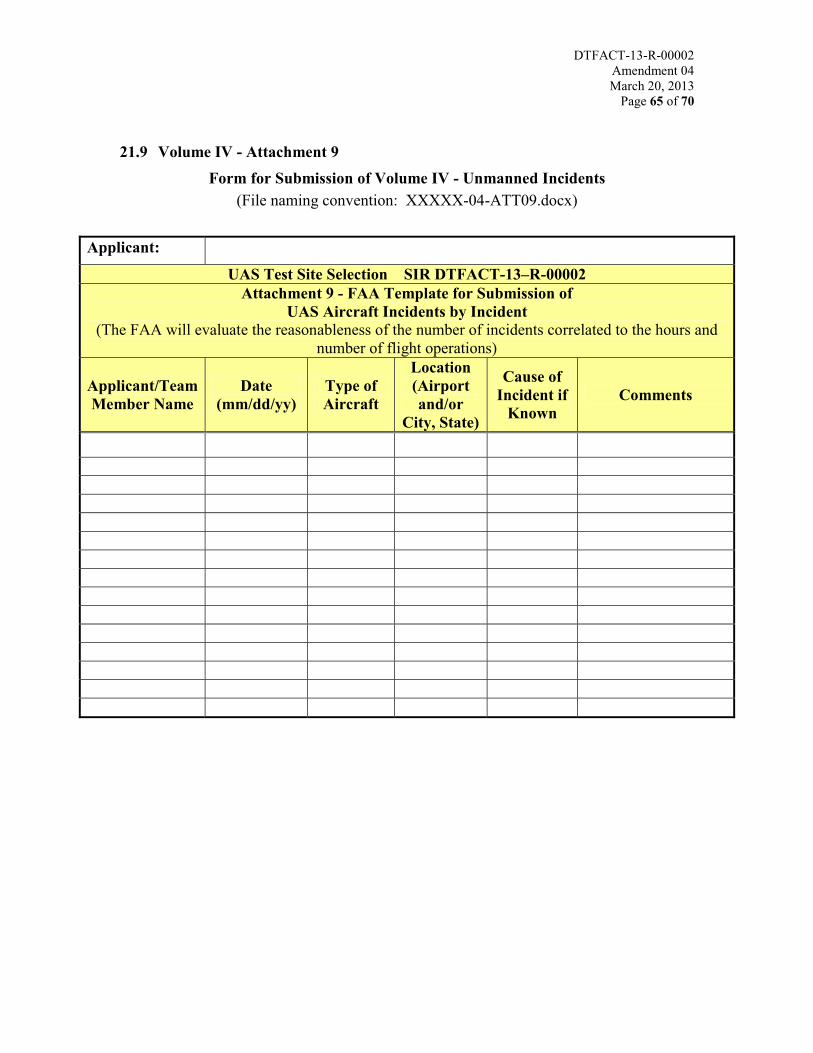

21.5 Volume III – Sub-Volume I: Attachment 5 .................................................. 61 21.6 Volume IV - Attachment 6 ........................................................................... 62 21.7 Volume IV - Attachment 7 ........................................................................... 63 21.8 Volume IV - Attachment 8 ........................................................................... 64 21.9 Volume IV - Attachment 9 ........................................................................... 65 21.10 Volume IV - Attachment 10 ......................................................................... 66 21.11 Volume IV - Attachment 11 ......................................................................... 67 21.12 Volume V - Attachment 12........................................................................... 68

22 ATTACHMENT A: UASTSS SIR ACRONYMS ................................................... 69

LIST OF TABLES

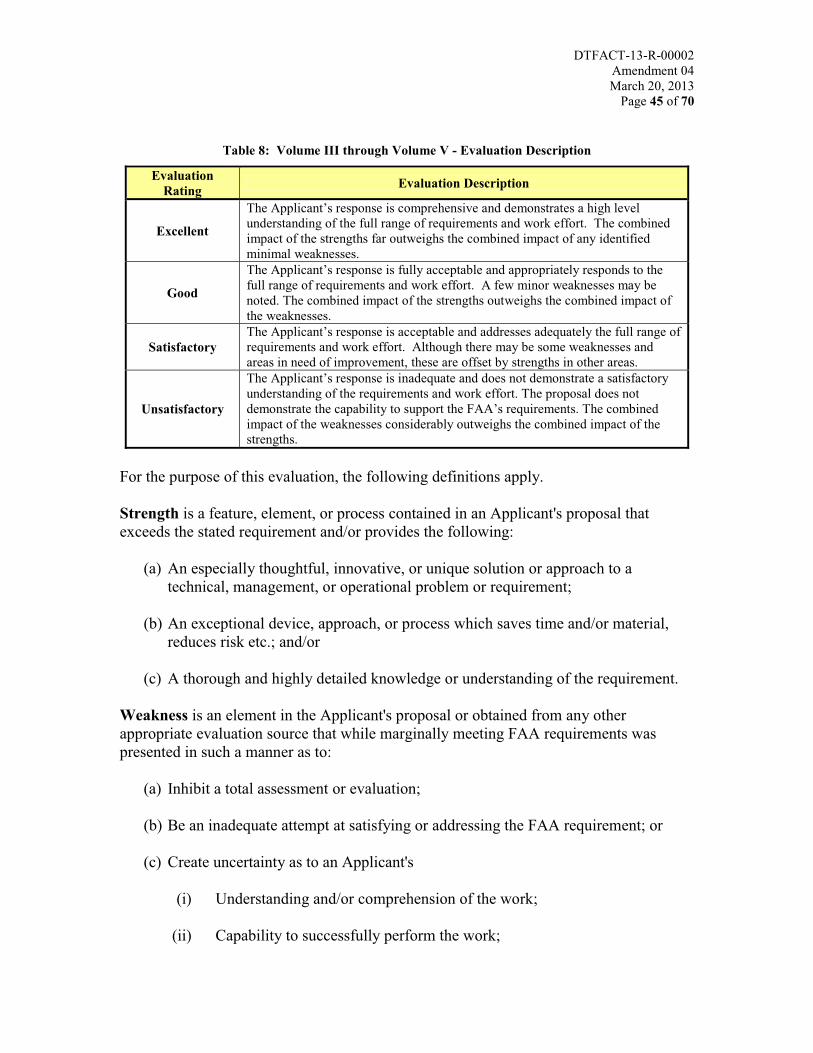

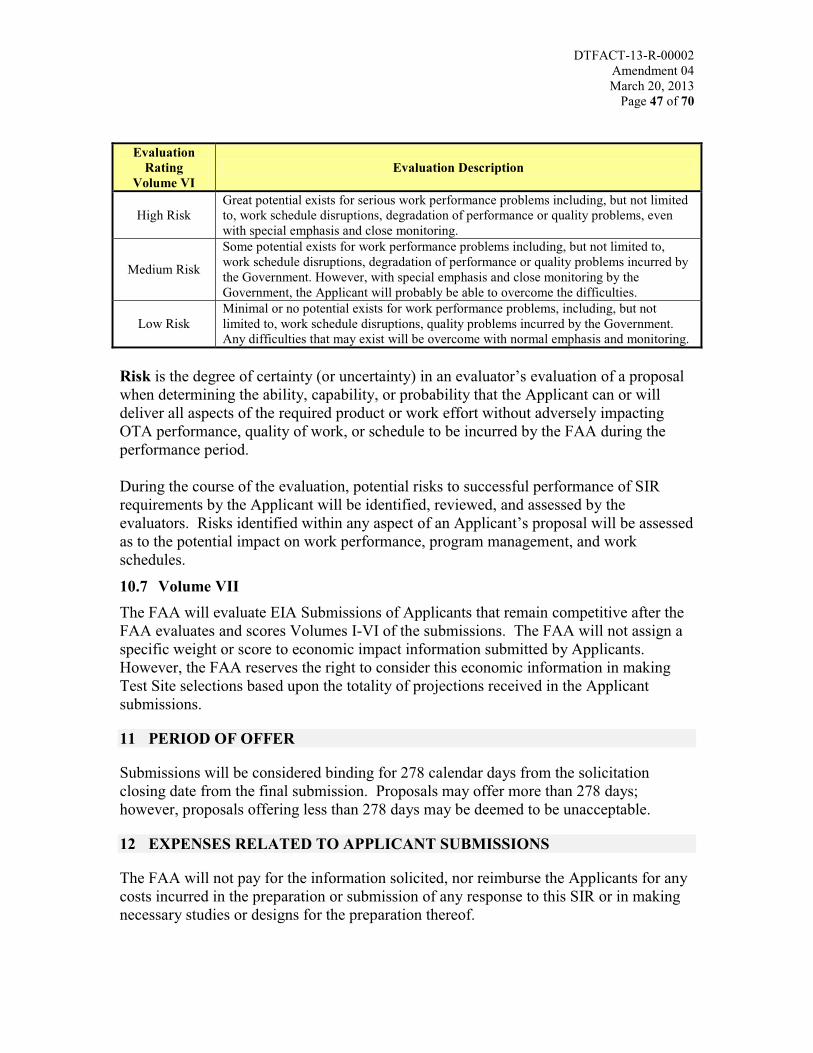

Table 1: Schedule............................................................................................................... 4 Table 2: Milestones............................................................................................................ 5 Table 3: Submission Criteria and Naming Conventions.................................................. 16 Table 4: File Naming Convention for Submitted Agreements and Other Documents .... 17 Table 5: Evaluator Score.................................................................................................. 41 Table 6: Volume II – Evaluation Criteria ........................................................................ 42 Table 7: Volumes III, IV and V - Evaluation Point Structure .......................................... 42 Table 8: Volume III through Volume V - Evaluation Description.................................. 45 Table 9: Volume III – Sub Volume II ATC Feasibility Definitions................................ 46 Table 10: Volume VI – Evaluation Criteria Descriptions ............................................... 46

LIST OF FIGURES

Figure 1: Test Site.............................................................................................................. 8 Figure 2: Test Range.......................................................................................................... 8 Figure 3: Example Sketch of Proposed Test Site Airspace with Lateral and Vertical Boundaries ........................................................................................................................ 25 Figure 4: Example Description of Proposed Test Range(s) Airspace ............................. 26

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 4 of 70

1 PROJECT TITLE

Unmanned Aircraft Systems Test Site Selection (UASTSS)

2 SCREENING INFORMATION REQUEST (SIR) NO.

DTFACT-13-R-00002

3 AGREEMENT TYPE

Other Transaction Agreement (OTA)

4 ACQUISITION MANAGEMENT SYSTEM (AMS)

This SIR makes reference to the AMS; however, as an OTA, the FAA is using AMS for guidance only and AMS does not bound OTAs. The AMS establishes policy and guidance for all aspects of lifecycle acquisition management for the Federal Aviation Administration (FAA). Applicants1 may obtain information on the AMS via the Internet at: http://fast.faa.gov/. Some AMS policies are referenced in this document as an established protocol.

5 PERIOD OF PERFORMANCE

Date of issuance through 2/13/2017.

6 MILESTONE SCHEDULES

Table 1: Schedule

Schedule Date Time

SIR Issued Thursday, February 14, 2013 N/A

Receipt of email request for access to UASTSS Web Portal Thursday, February 14, 2013 toMonday, February 25, 2013 5:00 PM EST

FAA to email Applicant UASTSS Web Portal Access Thursday, February 14, 2013 toTuesday, February 26, 2013 5:00 PM EST

Receipt of Volume I questions, concerns, clarifications Thursday, February 14, 2013 toWednesday, February 27, 2013 11:00 AM EST

1 The term “Applicant” is inclusive of the AMS term “Offeror”.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 5 of 70

Schedule Date Time

FAA Response to Volume I questions, concerns, and clarifications

Variable and no later thanTuesday, March 5, 2013 5:00 PM EST

Receipt of Volume I Wednesday, March 6, 2013 2:00 PM ESTReceipt of questions, concerns, and clarifications on all remaining Volumes via UASTSS Web Portal Question and Answer Site

Thursday, February 14, 2013 toThursday, February 28, 2013 11:00 AM EST

FAA Response to SIR questions, concerns and clarifications from Applicants

Variable and no later thanFriday, March 22, 2013 5:00 PM EDT

Receipt of Volume II - SIR Compliance Criteria Thursday, March 28, 2013 2:00 PM EDTReceipt of Volume III Sub-Volume I - Ground Infrastructure, Research Objectives and Airspace Use Thursday, April 11, 2013 2:00 PM EDT

Receipt of Volume IV - Safety Thursday, March 28, 2013 2:00 PM EDTReceipt of Volume V - Experience Thursday, March 28, 2013 2:00 PM EDTReceipt of Volume VI - Risk Consideration - Planned Team Composition and Capability Thursday, March 28, 2013 2:00 PM EDT

Receipt of Volume VII – Economic Impact Monday, May 6, 2013 2:00 PM EDT

Table 2: Milestones

Milestone Schedule Estimated Date

Planned modification to the draft OTA to include the FAA developed privacy strategy incorporating public comments received through Federal Register Notice [Docket No.: FAA-2013-0061].

Tuesday, June 11, 2013

OTA Issuance Tuesday, December 31, 2013

7 BACKGROUND

The FAA MODERNIZATION and REFORM ACT (FMRA) of 2012, PL-112-95,requires the FAA to establish a program to integrate unmanned aircraft systems (UAS) into the National Airspace System (NAS) at six (6) Test Ranges2. In keeping with this mandate, the FAA intends to award, under OTA, six (6) Test Sites. Using this strategy the FAA can enter into agreements with each of the public entities. The link to and an excerpt from the Act are included below.

FAA Act is PL112 publ95: http://www.gpo.gov/fdsys/pkg/PLAW-112publ95/pdf/PLAW-112publ95.pdf

FAA MODERNIZATION and REFORM ACT of 2012(Unmanned Aircraft System excerpts)

2 The terms “test range” and “test site” are used interchangeably in the FMRA OF 2012. The FAA defines Test Range as a component of the Test Site and uses this definition consistently throughout this document.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 6 of 70

TITLE III—SAFETYSubtitle B—Unmanned Aircraft Systems

The specific language from Section 332(c) of the FAA Modernization and Reform Act of 2012 (Public Law 112–95, 112th Congress) is provided for reference.

(c) PILOT PROJECTS.—(1) ESTABLISHMENT.—Not later than 180 days after the date of enactment of this Act, the Administrator shall establish a program to integrate unmanned aircraft systems into the national airspace system at 6 Test Ranges. The program shall terminate 5 years after the date of enactment of this Act.(2) PROGRAM REQUIREMENTS.—In establishing the program under paragraph (1), the Administrator shall—

(A) safely designate airspace for integrated manned and unmanned flight operations in the national airspace system;(B) develop certification standards and air traffic requirements for unmanned flight operations at Test Ranges;(C) coordinate with and leverage the resources of the National Aeronautics and Space Administration and the Department of Defense;(D) address both civil and public unmanned aircraft systems;(E) ensure that the program is coordinated with the Next Generation Air Transportation System; and(F) provide for verification of the safety of unmanned aircraft systems and related navigation procedures before integration into the national airspace system.

(3) TEST RANGE LOCATIONS.—In determining the location of the 6 Test Ranges of the program under paragraph (1), the Administrator shall—

(A) take into consideration geographic and climatic diversity;(B) take into consideration the location of ground infrastructure and research needs; and(C) consult with the National Aeronautics and Space Administration and the Department of Defense.

(4) TEST RANGE OPERATION.—A project at a Test Range shall be operational not later than 180 days after the date on which the project is established.(5) REPORT TO CONGRESS.—

(A) IN GENERAL.—Not later than 90 days after the date of the termination of the program under paragraph (1), the Administrator shall submit to the Committee on Commerce, Science, and Transportation of the Senate and the Committee on Transportation

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 7 of 70

and Infrastructure and the Committee on Science, Space, and Technology of the House of Representatives a report setting forth the Administrator’s findings and conclusions concerning the projects.(B) ADDITIONAL CONTENTS.—The report under subparagraph (A) shall include a description and assessment of the progress being made in establishing special use airspace to fill the immediate need of the Department of Defense— (i) to develop detection techniques for small unmanned aircraft systems; and (ii) to validate the sense and avoid capability and operation of unmanned aircraft systems.

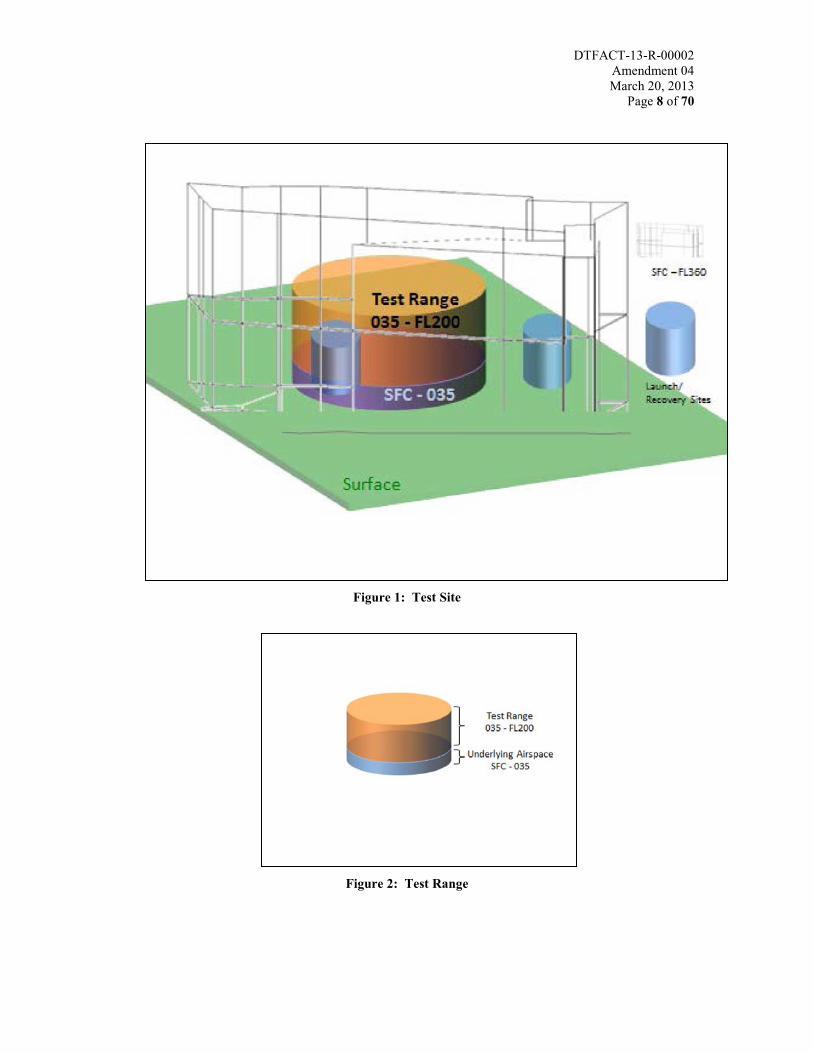

The terms Test Site and Test Range are defined as follows:

1. Test Site includes the defined range airspace and any/all ground infrastructure to include launch/recovery location(s). These launch/recovery locations do not necessarily have to be located in the underlying range airspace. See ExampleFigure 1: Test Site.

2. Test Range implies only the airspace and the area specifically underlying that airspace that may extend to the surface, where operation(s) are conducted. See Example Figure 2: Test Range.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 8 of 70

Figure 1: Test Site

Figure 2: Test Range

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 9 of 70

8 INSTRUCTIONS TO APPLICANTS

8.1 Introduction8.1.1 The FAA is conducting a Site Selection process with the intention to authorize

and designate six (6) UAS Test Sites in accordance with Congressional mandate.

8.1.2 As a result, the FAA plans to award OTAs to those entities for which the Administrator has issued an Order designating them a UAS Test Site Operator.

8.1.3 Submissions are presumed to represent an entity’s best efforts to respond to SIR requirements, including the scope requirements defined in Article 2 of the draft OTA. Inconsistencies within the entire proposal submission must be fully explained. A significant inconsistency, if unexplained, raises a fundamental question of the Applicant’s understanding of the relevant regulatory and technical environment, as well as of the ability to meet and perform the requirements. This may be grounds for either rejection of the submission or a basis for a determination of Non-Compliance. Failure to submit any of the information requested by this SIR may be cause for unfavorable consideration.

8.2 SIR Questions, Concerns, and Clarifications8.2.1 All questions from potential Applicants relevant to SIR content must be submitted

through the UASTSS Web Portal. All other inquiries on this SIR, or to receive assistance, must be made directly to the FAA Contracting Officer rather than through intermediaries. The following COs are the sole points of contact for this SIR:

Contracting Officer (CO)FAA William J. Hughes Technical CenterAttn: Anne Marie Ternay, AAQ-630Atlantic City International Airport, NJ 08405Phone: (609) 485-6990Email: [email protected]

Supervisory Contracting Officer (if above CO is unavailable): FAA Technical CenterAttn: Debra Stueber, AAQ-630Atlantic City International Airport, NJ 08405Phone: (609) 485-4115Email: [email protected]

8.2.2 The Applicant must submit a request for access to the UASTSS Web Portal to the CO via email by the designated due date on Table 1: Schedule:

Email: [email protected] email subject should read:

“Establishment of UASTSS Web Portal Account – (insert Public Entity Name)

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 10 of 70

The email should read as follows:“Please establish an UASTSS Web Portal Account for:

Public Entity Name:Contact Title: (e.g. Dr. Mr., Mrs., Ms., etc.)Contact Name:Contact Position: (e.g. President, Director, etc.) Email:Phone Number:”

Note: The Public Entity Name established for the Web Portal may not be changed at any time during this solicitation. The FAA will only accept one Point of Contact for this solicitation. All communication from the Applicant must be through this appointed individual.

8.2.3 Access instructions to the UASTSS Web Portal will be provided by the FAA via an automatically generated email from [email protected] to the Applicant by the designated due date.

8.2.4 If an Applicant does not receive access instructions to the UASTSS Web Portal by the designated date shown in Table 1: Schedule , the Applicant must notify via email the CO at:

Email: [email protected] email subject should read:

“Web Portal Account Instructions not Received – (insert Public Entity Name)”

The email should read as follows:“This is to notify the FAA that access instructions to the UASTSS Web Portal have not been received. The Applicant should attach evidence of the original email including time stamp and the following original information:Public Entity Name:Contact Name:Email:Phone Number:”

8.2.5 The Applicant is responsible for developing a working knowledge of the UASTSS Web Portal prior to submission designated due dates. The Applicant must use a Microsoft Explorer web browser to access the web portal. Firefox, Safari or other browsers cannot be used. This includes the Question Submission Form; Volume I Identification of Applicant Form and the Applicant Discrete Secure Volume Submission Folders. Test documents may be uploaded to the Volume Submission Folders and deleted by the Applicant before the Volume designated due date.

8.2.6 The Web Portal Home Page has your Five Letter Designator (XXXXX) below the “Questions and Concerns” area. This designator is unique to the Applicant and

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 11 of 70

must be used in the file naming conventions for submissions as shown in Table 3and Table 4.

8.2.7 On the Web Portal Home Page on the left side, there is an option for “Site Help”. Click on this option and you will be directed to detailed instructions on the features of and using the UASTSS Web Portal.

8.2.8 If the Applicant is unable to gain access to the UASTSS Web Portal the Applicantmust notify via email the CO at:

Email: [email protected] email subject should read:

“Issue with UASTSS Web Portal Access – (insert Public Entity Name)”The email should read as follows:

“This is to notify the FAA of the following issue with respect to the UASTSS Web Portal Access by (insert Public Entity Name) Describe the nature of the issue Include the following information:

Public Entity Name:Contact Name:Email:Phone Number:”

8.2.9 In the event of a UASTSS Web Portal outage, the FAA will notify Applicants via email from the [email protected] or [email protected].

8.2.10 In the event that an Applicant finds that one of the features on the UASTSS Web Portal is not functioning or there is an outage on which the FAA has not advised the Applicants, the Applicant must notify via email the Contracting Officer at:

Email: [email protected] email subject should read:“Functionality or outage with UASTSS Web Portal – (insert Public Entity Name)”The email should read as follows:“This is to notify the FAA that the UASTSS Web Portal is not functioning (specify problem) or is unavailable as of (insert date and time).

Public Entity Name:Contact Name:Email:Phone Number:”

8.2.11 All SIR questions, concerns and clarifications must be submitted via the UASTSS Web Portal Question Submission Forms described in 8.3 Place, Date, Time, and Format for Submission of Proposals.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 12 of 70

8.2.12 The author of each question will only be seen by the Government. The FAA intends to make all questions, concerns and clarifications visible (without the author’s identification or any proprietary information) to Applicants through the UASTSS Web Portal. Identifying information will be redacted prior to posting on the UASTSS Web Portal. Questions and associated answers determined to be proprietary (non-redactable) will be viewable only to the Applicant via their discrete web site.

8.2.13 User activity on the Web Portal is logged for security purposes. In the event that, an Applicant is able to access another entity’s data/files, the Applicant shall immediately notify the CO via email. Accessing, viewing and/or opening the data/files of other entities could result in the Applicant’s proposal being rejected.

If the Applicant is able to access another entity’s data/files, the Applicant must notify via email the CO at:

Email: [email protected] email subject should read:

“Unauthorized access to entity on UASTSS Web Portal– (insert Public Entity Name)”

The email should read as follows:“This is to notify the FAA that (insert Public Entity Name) has a document(s) on its Web Portal which is not a document(s) originated by the Applicant. The document(s) is located in: (provide location of document on the Web Portal) and the file name is: (provide file name).”

In the event that the FAA needs to contact me regarding this email, I can be reached at the following telephone number: (Provide telephone number).”

8.2.14 Each question submitted to the FAA will be assigned a unique identification number. These numbers will not be sequential on the Applicant’s site and the FAA Public Questions and Answers sites.

8.2.15 A question is submitted by clicking on the SAVE&CLOSE button. That action will take the applicant back to the prior page. The Applicant should not use the browser arrows to navigate in the UASTSS Web Portal.

8.2.16 If an Applicant needs further clarification on a previously submitted question, the Applicant should refer to that question by its identification number. Applicantsmust review previous questions to ensure that the same question or questions have not already been addressed.

8.2.17 It is the intention of the FAA to respond to all written inquiries in writing.Answers will be provided prior to the required date for Volume submittal of the Applicants’ proposal via the UASTSS Web Portal.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 13 of 70

8.2.18 The FAA reserves the right to not answer any question(s) received outside of the timeframes set out above. Furthermore, Applicants must note that the proposal due date will not be extended on the basis of questions received.

8.2.19 The FAA will not provide verbal responses to Applicant questions, concerns, or clarification requests initiated via Applicant telephone calls or in any other manner than described above.

8.2.20 The Applicant understands that in the event that an Applicant withdraws from the selection process or a Volume submission is not made by the designated due date, access to the UASTSS Web Portal may be terminated.

8.3 Place, Date, Time, and Format for Submission of Proposals8.3.1 Questions, concerns, and clarifications relevant to Volumes I through VII must be

submitted by the designated due dates in Table 1: Schedule via the UASTSS Web Portal “My Questions” submission form.

8.3.2 Each question, concern, or clarification must be submitted separately. The Applicant must submit a question using the “SUBMIT” button before closing the “My Questions” form, or the question will not be submitted.

8.3.3 Answers to the questions, concerns, and clarifications relevant to Volumes I through Volume VII will be posted to the UASTSS Web Portal “PublicAnswers”. Questions and their associated answers determined to be proprietary will be viewable only to the Applicant via their discrete web site. Answers will be posted by the designated due dates in Table 1: Schedule.

8.3.4 All Applicants must submit Volume I - Attachment 2 and Volumes II through VIIsubmissions via the Applicant discrete secure Volume Submission Folders.

8.3.5 Proposals must be submitted in accordance with the staggered scheduleestablished in Table 1: Schedule.

8.3.6 Prior to 2:00 PM EST/EDT (as applicable) on the submission dates, Applicantsare permitted to edit documents posted to their Applicant Volume Submission Folders however, at 2:01PM EST/EDT (as applicable) on the submission dates,all assigned Applicant sites for the appropriate Volume will be locked down and become read only sites.

8.3.7 The FAA will not accept any submission made by facsimile, telex, telegraph, or similar devices; nor will paper copies be accepted.

8.3.8 If the CO or her designated representative(s) does not receive a proposal by the specified date and time, it will not be evaluated. Applicants assume full responsibility for ensuring that proposals are submitted not later than the date and time specified in Table 1: Schedule.

8.3.9 DELETED

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 14 of 70

8.3.10 Proposals must be complete and conform to the instructions in this SIR;incomplete proposals or proposals which contain any deviations may result in the exclusion of such proposals from further consideration. General statements that the Applicant understands the requirements of the work to be performed, or simple rephrasing or restating of the FAA’s requirements, will not be considered adequate and will result in lower assessments or may be cause for rejection of the proposal in its entirety.

8.3.11 All proposals will be initially screened for completeness, accuracy and timeliness. Alternate proposals are not authorized, and the FAA will not evaluate any alternate proposal received.

8.3.12 It is the Applicant’s responsibility to ensure the completeness of the proposal. The evaluation of proposals will only be conducted on the basis of the information contained in the written proposal. The Government will not assume that an Applicant possesses any capabilities not specified in the written proposal.

8.3.13 It is the Applicant’s responsibility to ensure their required response information is provided within the relevant Volumes as the Government requested. The Government will not be responsible for looking elsewhere within the proposal for information that is required as part of a particular Volume.

8.3.14 The FAA will only evaluate information relative to each section. Applicants must restrict responses to information relative to that Volume and subsidiary Section. The Applicant must respond to each Volume in the order identified by the FAA for each topic and subtopic.

8.3.15 The Applicant must submit a response to this SIR by the following electronic means:

8.3.15.1 Electronic upload to the Applicant discrete secure Volume Submission Folders on the UASTSS Web Portal. The Applicant’s submission must be completely uploaded to the Folders by the time specified in the SIR.

Note: When uploading a document to a Volume Submission Folder be certain that the “Overwrite existing files” box is checked.

8.3.15.2 Except where noted otherwise, all submissions must be submitted as docx files (Microsoft® Word 2010 Office Open XML Document format). If the Applicant has an earlier version of Microsoft® Word, the following is a hyperlink to instructions for converting files to the docx format: http://www.microsoft.com/en-us/download/details.aspx?id=3.

8.3.15.3 Electronic submissions will be the only means by which proposals will be accepted by the FAA.

8.3.15.4 The FAA may decline to consider electronic Submissions that do not: include all required information, follow the required submission format, and versions, or meet all of the terms, conditions and provisions of the SIR.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 15 of 70

8.3.15.5 The FAA may decline to consider Submissions that do not follow the naming convention defined in Table 3 and Table 4.

8.3.15.6 Word documents must be in Read Only mode (with no password) by utilizing the “Protect Document” feature.

8.3.15.7 For all Microsoft Word submissions: Pages must be 8-1/2 x 11 inches. The font type must be Times New Roman and size 12-point with a single linespace. The exception is for embedded charts, graphs and pictures for which the font size must be no less than 8-point. All Top, Bottom, Left and Right Margins are to be 1”. Foldouts are permissible but count as two (2) pages each (i.e. 11 x 17 inches).

8.3.16 Where signatures or PDFs are required, the electronic format must be a scanned,searchable PDF.

8.3.17 The proposal must be signed by an official who is legally authorized to negotiate on behalf of the Applicant and who is legally authorized to enter into an Agreement. Volume I, Attachment 2, Certification of Applicant must be submitted and will certify this authority for information contained within all Volumes submitted.

8.3.18 Labeling – An electronic cover sheet must be provided for each document over two pages submitted, which clearly identifies each Volume number and document file name prescribed in Table 3 and Table 4, solicitation number, and the Applicant's name. This sheet must be part of each submitted Volume, as opposed to a separate file and will not count against any page limitations. Electronic auto generated and linked Table of Contents, Table of Tables, Table of Graphs, and Table of Figures must be provided and will not count against any page limitations. Each section within a Volume must be consecutively numbered.

8.3.19 A list of Acronyms must be provided at the end of each Volume III-VII which will not count against any page limitations. The naming conventions for these submissions are provided in Table 3.

8.3.20 Within each Applicant’s electronic submission, all proposal Volumes and sections within each Volume must be clearly identified. Discrete Applicant Web Portal Sites consist of Volume Submission Folders.

8.3.21 Failure to comply with the requirements of this section may result in the Applicant’s proposal being rejected.

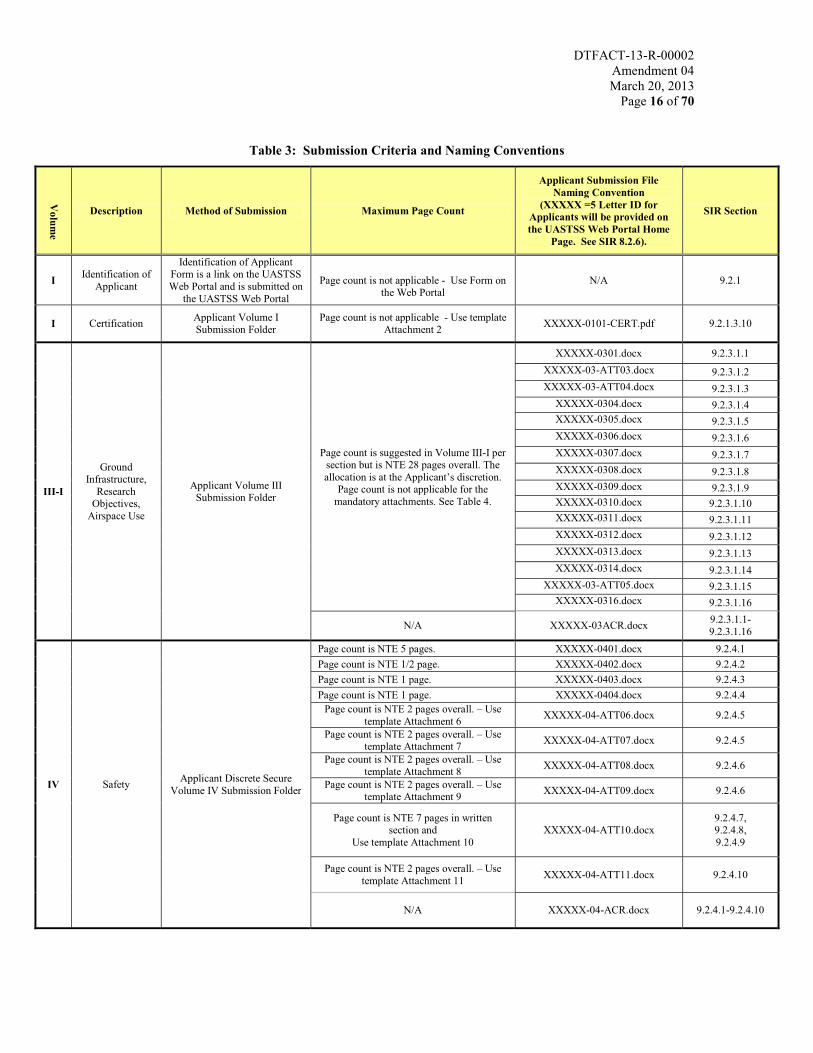

8.3.22 The Applicant’s proposal must comply with Table 3 and Table 4.

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 16 of 70

Table 3: Submission Criteria and Naming Conventions

Volum

e

Description Method of Submission Maximum Page Count

Applicant Submission File Naming Convention

(XXXXX =5 Letter ID for Applicants will be provided on the UASTSS Web Portal Home

Page. See SIR 8.2.6).

SIR Section

I Identification of Applicant

Identification of ApplicantForm is a link on the UASTSS Web Portal and is submitted on

the UASTSS Web Portal

Page count is not applicable - Use Form on the Web Portal

N/A 9.2.1

I Certification Applicant Volume I Submission Folder

Page count is not applicable - Use templateAttachment 2 XXXXX-0101-CERT.pdf 9.2.1.3.10

III-I

Ground Infrastructure,

Research Objectives,

Airspace Use

Applicant Volume III Submission Folder

Page count is suggested in Volume III-I per section but is NTE 28 pages overall. The allocation is at the Applicant’s discretion.

Page count is not applicable for the mandatory attachments. See Table 4.

XXXXX-0301.docx 9.2.3.1.1XXXXX-03-ATT03.docx 9.2.3.1.2XXXXX-03-ATT04.docx 9.2.3.1.3

XXXXX-0304.docx 9.2.3.1.4XXXXX-0305.docx 9.2.3.1.5XXXXX-0306.docx 9.2.3.1.6XXXXX-0307.docx 9.2.3.1.7XXXXX-0308.docx 9.2.3.1.8XXXXX-0309.docx 9.2.3.1.9XXXXX-0310.docx 9.2.3.1.10XXXXX-0311.docx 9.2.3.1.11XXXXX-0312.docx 9.2.3.1.12XXXXX-0313.docx 9.2.3.1.13XXXXX-0314.docx 9.2.3.1.14

XXXXX-03-ATT05.docx 9.2.3.1.15XXXXX-0316.docx 9.2.3.1.16

N/A XXXXX-03ACR.docx 9.2.3.1.1-9.2.3.1.16

IV Safety Applicant Discrete Secure Volume IV Submission Folder

Page count is NTE 5 pages. XXXXX-0401.docx 9.2.4.1Page count is NTE 1/2 page. XXXXX-0402.docx 9.2.4.2Page count is NTE 1 page. XXXXX-0403.docx 9.2.4.3Page count is NTE 1 page. XXXXX-0404.docx 9.2.4.4

Page count is NTE 2 pages overall. – Use template Attachment 6 XXXXX-04-ATT06.docx 9.2.4.5

Page count is NTE 2 pages overall. – Use template Attachment 7 XXXXX-04-ATT07.docx 9.2.4.5

Page count is NTE 2 pages overall. – Use template Attachment 8 XXXXX-04-ATT08.docx 9.2.4.6

Page count is NTE 2 pages overall. – Use template Attachment 9 XXXXX-04-ATT09.docx 9.2.4.6

Page count is NTE 7 pages in written section and

Use template Attachment 10XXXXX-04-ATT10.docx

9.2.4.7,9.2.4.8,9.2.4.9

Page count is NTE 2 pages overall. – Use template Attachment 11 XXXXX-04-ATT11.docx 9.2.4.10

N/A XXXXX-04-ACR.docx 9.2.4.1-9.2.4.10

DTFACT-13-R-00002Amendment 04March 20, 2013

Page 17 of 70

Volum

e

Description Method of Submission Maximum Page Count

Applicant Submission File Naming Convention

(XXXXX =5 Letter ID for Applicants will be provided on the UASTSS Web Portal Home

Page. See SIR 8.2.6).

SIR Section

V Experience Applicant Volume V Submission Folder

Page count is NTE 5 pages in written section and NTE 7 pages overall. – Use

templateAttachment 12

XXXXX-05-ATT12.docx 9.2.5

N/A XXXXX-05-ACR.docx 9.2.5

VI

Risk Consideration –Planned Team

Composition and Capabilities

Applicant Volume VI Submission Folder

Page count is NTE 2 pages. XXXXX-0601.docx 9.2.6.1

Page count is NTE 1 page. XXXXX-0602.docx 9.2.6.2

N/A XXXXX-0603.docx 9.2.6.3

N/A XXXXX-06-ACR.docx 9.2.6.1-9.2.6.3

VII Economic Impact Applicant Volume VII Submission Folder

Page count is NTE 8 pages. XXXXX-0701.docx 9.2.7

N/A XXXXX-07-ACR.docx 9.2.7

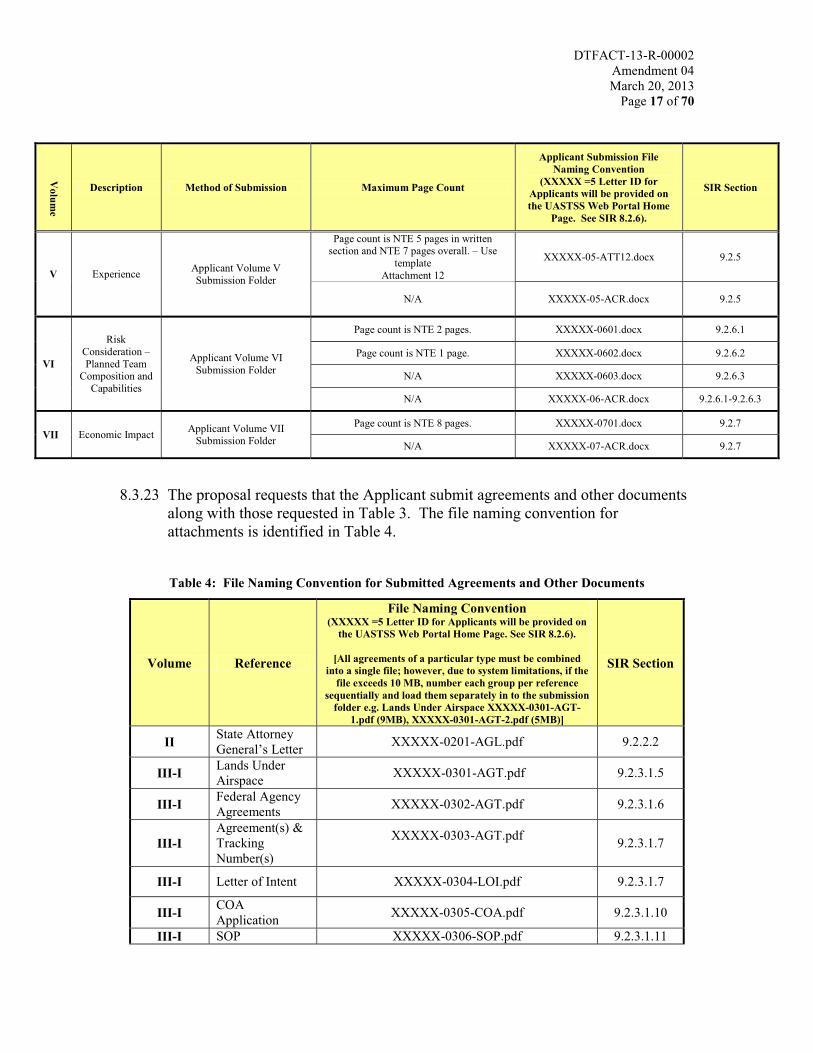

8.3.23 The proposal requests that the Applicant submit agreements and other documents along with those requested in Table 3. The file naming convention for attachments is identified in Table 4.

Table 4: File Naming Convention for Submitted Agreements and Other Documents

Volume Reference

File Naming Convention(XXXXX =5 Letter ID for Applicants will be provided on

the UASTSS Web Portal Home Page. See SIR 8.2.6).

[All agreements of a particular type must be combined into a single file; however, due to system limitations, if the