Embed Size (px)

Citation preview

Textiles – An Overview

September 2012

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

p

Snapshotp1. Profile

T il S fTextile – Some factsImportance of Textile in Pakistan

2. RisksWorld Textile – Demand and Supply DynamicsPerformanceCompetitiveness

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

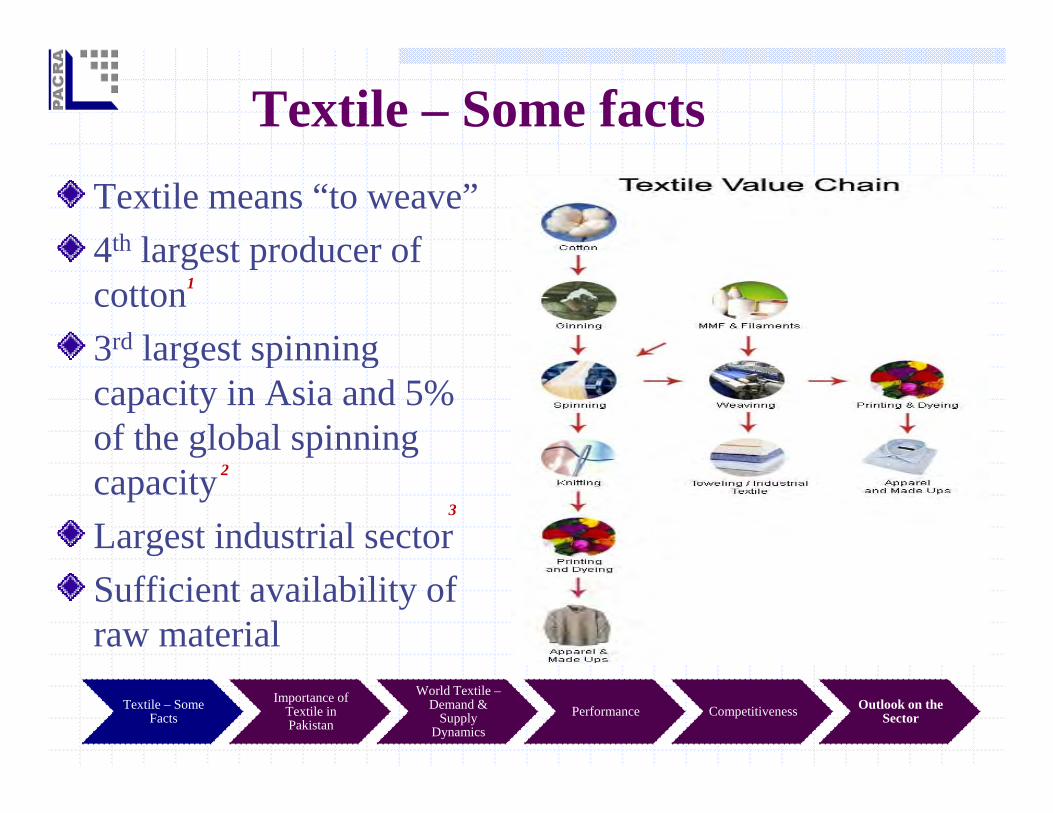

Textile – Some factsTextile means “to weave”4th largest producer of4 largest producer of cotton 3rd largest spinning

1

3 largest spinning capacity in Asia and 5% of the global spinning capacity Largest industrial sector

2

3

Sufficient availability of raw material

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Pakistan – Agricultural Land use 4

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

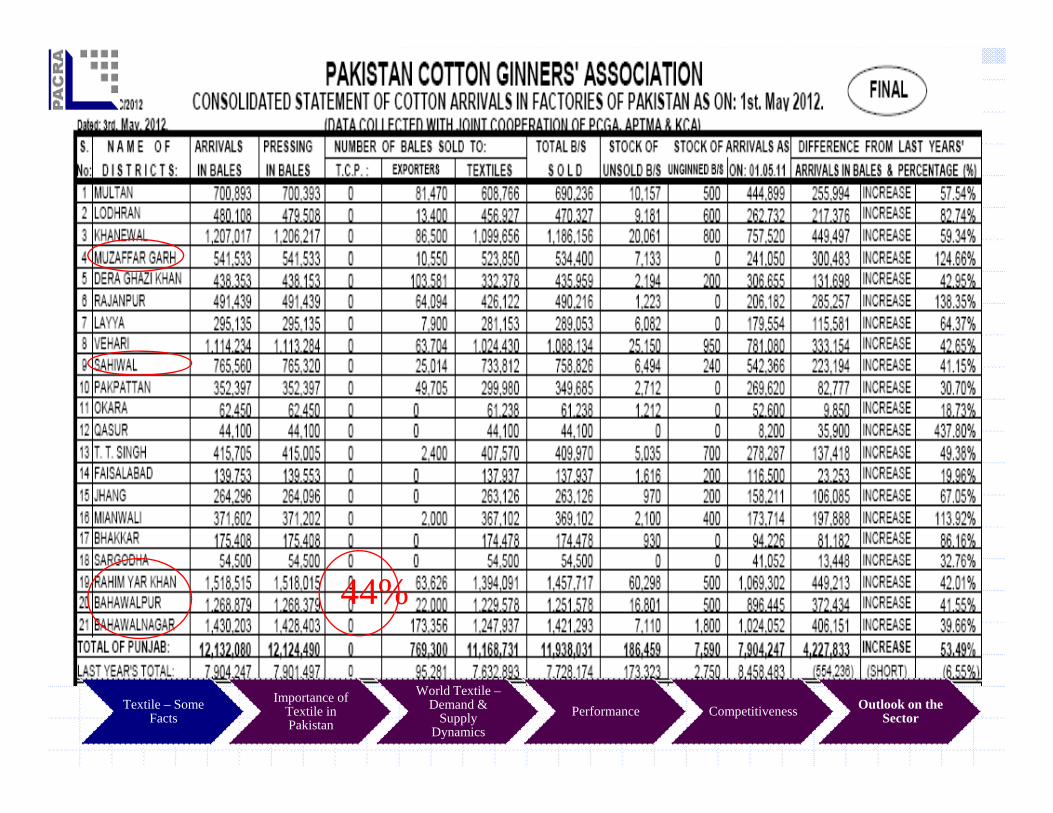

44%

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

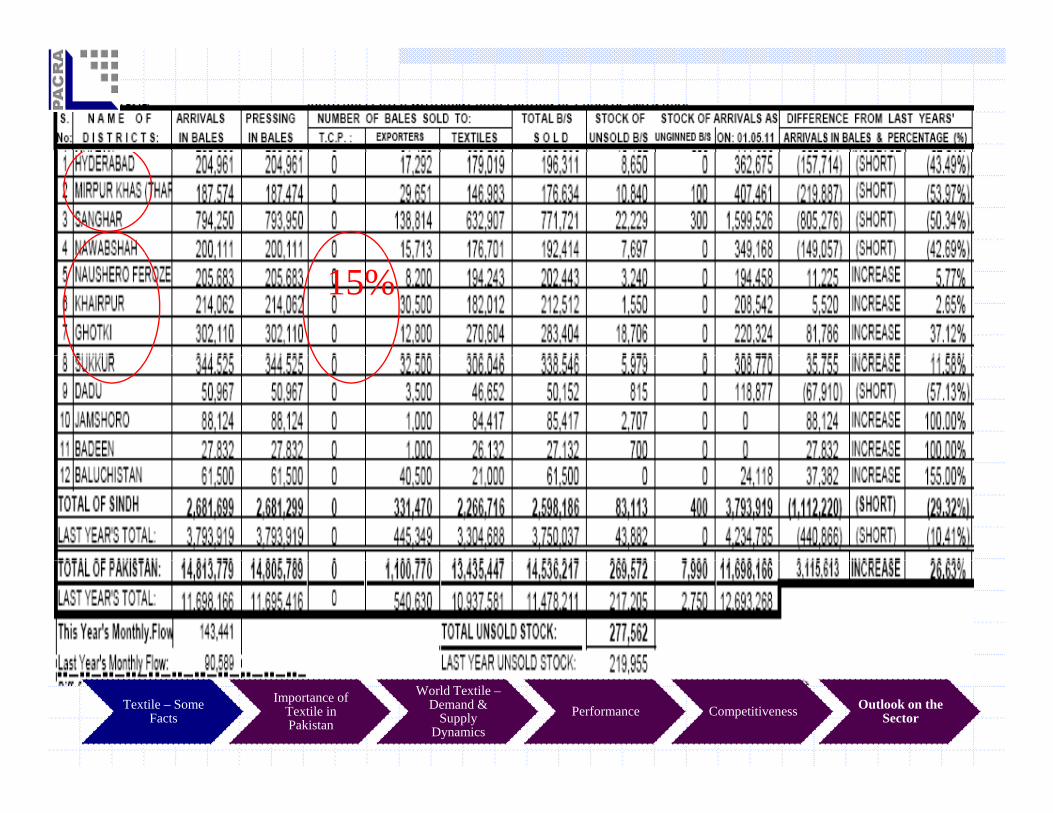

15%

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

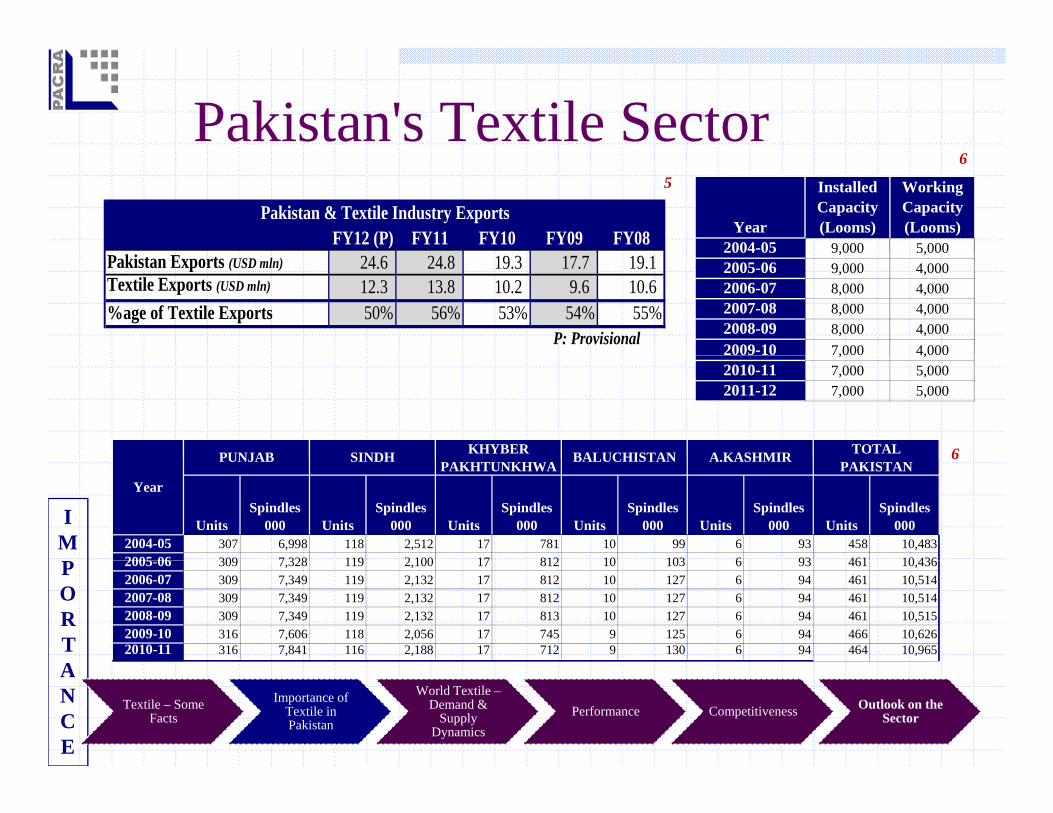

Pakistan's Textile Sector Year

Installed Capacity (Looms)

Working Capacity (Looms)

2004-05 9,000 5,000FY12 (P) FY11 FY10 FY09 FY08Pakistan & Textile Industry Exports

56

9,000 5,0002005-06 9,000 4,0002006-07 8,000 4,0002007-08 8,000 4,0002008-09 8,000 4,0002009-10 7,000 4,000

Pakistan Exports (USD mln) 24.6 24.8 19.3 17.7 19.1 Textile Exports (USD mln) 12.3 13.8 10.2 9.6 10.6 %age of Textile Exports 50% 56% 53% 54% 55%

P: Provisional, ,

2010-11 7,000 5,0002011-12 7,000 5,000

6PUNJAB KHYBER TOTAL SINDH BALUCHISTAN A KASHMIR

IM

6

Units Spindles

000 Units Spindles

000 Units Spindles

000 Units Spindles

000 Units Spindles

000 Units Spindles

000 2004-05 307 6,998 118 2,512 17 781 10 99 6 93 458 10,4832005 06 309 7 328 119 2 100 17 812 10 103 6 93 461 10 436

PUNJABPAKHTUNKHWA PAKISTAN

Year

SINDH BALUCHISTAN A.KASHMIR

PORTA

2005-06 309 7,328 119 2,100 17 812 10 103 6 93 461 10,4362006-07 309 7,349 119 2,132 17 812 10 127 6 94 461 10,5142007-08 309 7,349 119 2,132 17 812 10 127 6 94 461 10,5142008-09 309 7,349 119 2,132 17 813 10 127 6 94 461 10,5152009-10 316 7,606 118 2,056 17 745 9 125 6 94 466 10,6262010-11 316 7,841 116 2,188 17 712 9 130 6 94 464 10,965

ANCE

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Pakistan’s Textile Sector CompositionPakistan’s textile industry consists of large scale organized sector and highly fragmented cottage/medium and small units Organized sector : Large number of spinning units (464) d ll b f i i (60)(464) and a small number of weaving units (60) The rest of the downstream industry chain – finishing,

d t t l d h i h i t

7

madeups, garments, towel and hosiery – having a great export potential, is largely segmented in un-organized sectorsector.

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Pakistan’s Textile Sector at KSE180 listed textile companies constituting three segments: A) Spinning, B) Weaving, and C) Composite.

Textile Paidup Capital as at end-June Textile Market Capitalization as at end-June

3.8%

5.0%

6.3%

7.5%

15

20

25

30

KR

in m

ln

1.0%

1.5%

2.0%

2.5%

3.0%

30

45

60

75

90

KR

in m

ln0.0%

1.3%

2.5%

0

5

10

2006 2007 2008 2009 2010 2011 2012

PK

0.0%

0.5%

0

15

2006 2007 2008 2009 2010 2011 2012

PKWeavingSpinningWeaving

SpinningComposite%age of total KSE Capital

SpinningComposite%age of total KSE Capitalization

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

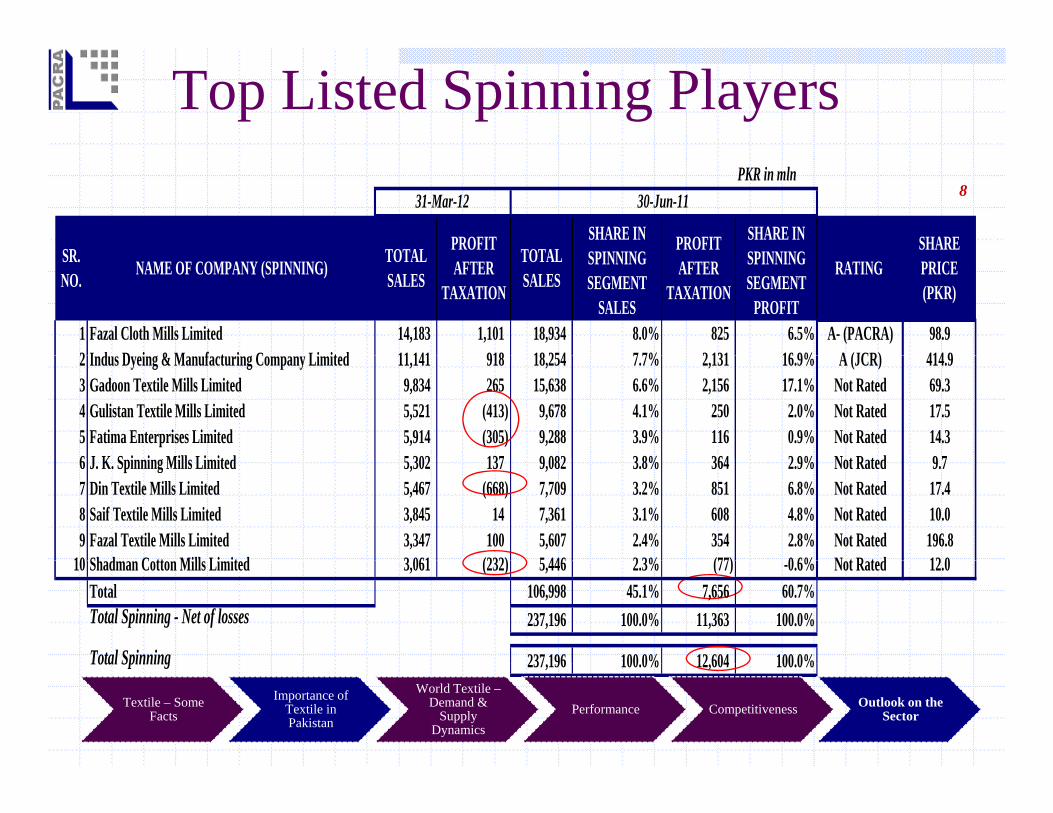

Top Listed Spinning Players PKR in mln

31-Mar-12 30-Jun-11

TOTALSR PROFIT TOTAL SHARE SHARE IN SPINNING

SHARE IN SPINNING

PROFIT

8

1 Fazal Cloth Mills Limited 14,183 1,101 18,934 8.0% 825 6.5% A- (PACRA) 98.92 I d D i & M f t i C Li it d 11 141 918 18 254 7 7% 2 131 16 9% A (JCR) 414 9

TOTAL SALES

SR. NO. AFTER

TAXATION

TOTAL SALES RATING PRICE

(PKR)

SPINNING SEGMENT

SALES

SPINNING SEGMENT

PROFIT

NAME OF COMPANY (SPINNING) AFTER TAXATION

2 Indus Dyeing & Manufacturing Company Limited 11,141 918 18,254 7.7% 2,131 16.9% A (JCR) 414.93 Gadoon Textile Mills Limited 9,834 265 15,638 6.6% 2,156 17.1% Not Rated 69.34 Gulistan Textile Mills Limited 5,521 (413) 9,678 4.1% 250 2.0% Not Rated 17.55 Fatima Enterprises Limited 5,914 (305) 9,288 3.9% 116 0.9% Not Rated 14.36 J K S i i Mill Li it d 5 302 137 9 082 3 8% 364 2 9% N t R t d 9 76 J. K. Spinning Mills Limited 5,302 137 9,082 3.8% 364 2.9% Not Rated 9.77 Din Textile Mills Limited 5,467 (668) 7,709 3.2% 851 6.8% Not Rated 17.48 Saif Textile Mills Limited 3,845 14 7,361 3.1% 608 4.8% Not Rated 10.09 Fazal Textile Mills Limited 3,347 100 5,607 2.4% 354 2.8% Not Rated 196.8

10 Sh d C tt Mill Li it d 3 061 (232) 5 446 2 3% (77) 0 6% N t R t d 12 010 Shadman Cotton Mills Limited 3,061 (232) 5,446 2.3% (77) -0.6% Not Rated 12.0Total 106,998 45.1% 7,656 60.7%Total Spinning - Net of losses 237,196 100.0% 11,363 100.0%

Total Spinning 237 196 100 0% 12 604 100 0%Total Spinning 237,196 100.0% 12,604 100.0%Source: KSE

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Top Listed Weaving Playersc PKR in mln 30-Jun-1131-Mar-12

SHARE INSHARE INPROFIT PROFIT8

C

1 Prosperity Weaving Mills Limited 4,024 7 5,952 22.3% 139 19.3% A- (PACRA) 10.4

TOTAL SALES

SHARE IN WEAVING SEGMENT

RATING SHARE PRICE

SHARE IN WEAVING SEGMENT

SR. NO. NAME OF COMPANY (WEAVING)

PROFIT AFTER

TAXATION

TOTAL SALES

PROFIT AFTER

TAXATION

2 Shahtaj Textile Limited 3,017 69 4,040 15.1% 205 28.5% Not Rated 30.03 Yousaf Weaving Mills Limited 1,790 (140) 3,829 14.3% 61 8.4% Not Rated 1.74 Zephyr Textiles Limited 2,347 37 3,574 13.4% 89 12.3% Not Rated 3.75 Samin Te tiles Limited 1 820 (84) 3 096 11 6% 46 6 4% Not Rated 6 55 Samin Textiles Limited 1,820 (84) 3,096 11.6% 46 6.4% Not Rated 6.56 Feroze1888 Mills Limited * 2,246 167 2,913 10.9% 151 21.0% Not Rated 36.17 ICC Textiles Limited 1,380 (66) 2,246 8.4% (99) -13.8% Not Rated 2.18 Ashfaq Textile Mills Limited 729 54 1,036 3.9% 30 4.1% Not Rated 10.5

*Formerly Nakshbandi Industries Limited

Total Weaving 26,687 100.0% 720 100.0%Total Weaving - Net of losses 26,687 100.0% 621 100.0%

Source: KSETextile – Some

FactsImportance of

Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

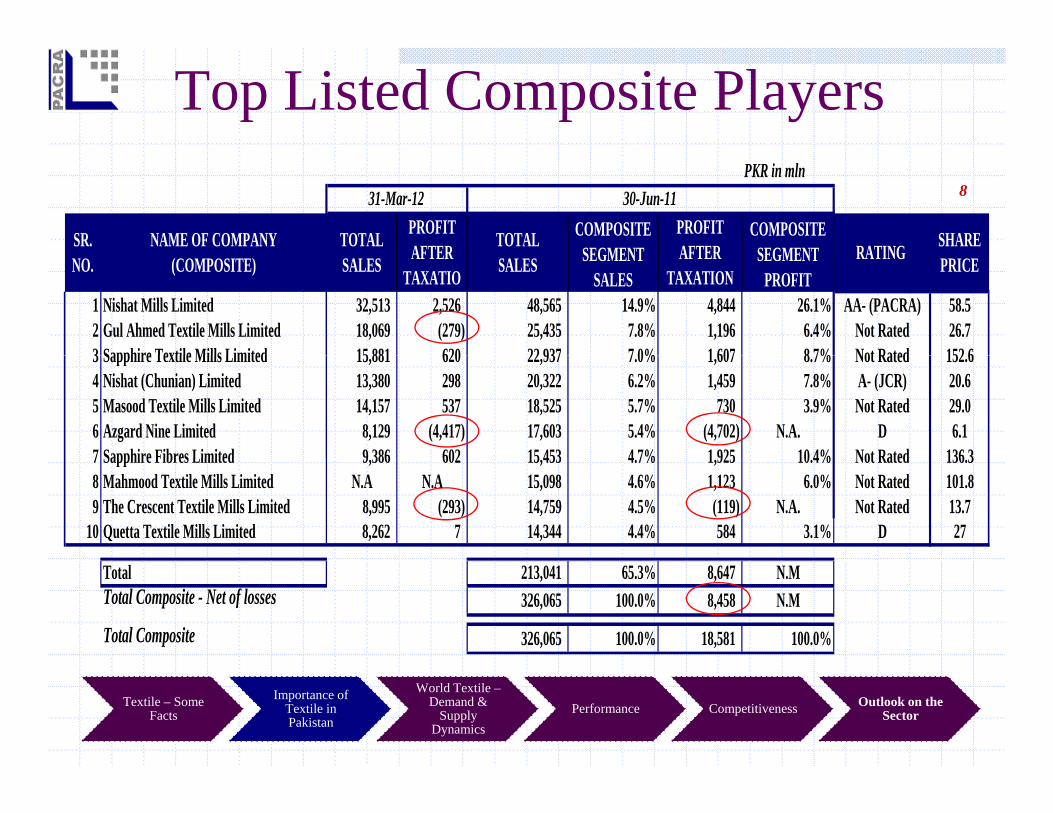

Top Listed Composite Players PKR in mln

30-Jun-11PROFIT AFTER

31-Mar-12

RATING SHARE SR. NAME OF COMPANY TOTAL TOTAL PROFIT AFTER

COMPOSITE SEGMENT

COMPOSITE SEGMENT

8

1 Nishat Mills Limited 32,513 2,526 48,565 14.9% 4,844 26.1% AA- (PACRA) 58.52 Gul Ahmed Textile Mills Limited 18,069 (279) 25,435 7.8% 1,196 6.4% Not Rated 26.73 Sapphire Textile Mills Limited 15 881 620 22 937 7 0% 1 607 8 7% Not Rated 152 6

AFTER TAXATIO

RATING PRICE NO. (COMPOSITE) SALES SALES AFTER TAXATION

SEGMENT PROFIT

SEGMENT SALES

3 Sapphire Textile Mills Limited 15,881 620 22,937 7.0% 1,607 8.7% Not Rated 152.64 Nishat (Chunian) Limited 13,380 298 20,322 6.2% 1,459 7.8% A- (JCR) 20.65 Masood Textile Mills Limited 14,157 537 18,525 5.7% 730 3.9% Not Rated 29.06 Azgard Nine Limited 8,129 (4,417) 17,603 5.4% (4,702) N.A. D 6.17 Sapphire Fibres Limited 9 386 602 15 453 4 7% 1 925 10 4% Not Rated 136 37 Sapphire Fibres Limited 9,386 602 15,453 4.7% 1,925 10.4% Not Rated 136.38 Mahmood Textile Mills Limited N.A N.A 15,098 4.6% 1,123 6.0% Not Rated 101.89 The Crescent Textile Mills Limited 8,995 (293) 14,759 4.5% (119) N.A. Not Rated 13.7

10 Quetta Textile Mills Limited 8,262 7 14,344 4.4% 584 3.1% D 27

Total 213,041 65.3% 8,647 N.MTotal Composite - Net of losses 326,065 100.0% 8,458 N.M

Total Composite 326,065 100.0% 18,581 100.0%

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

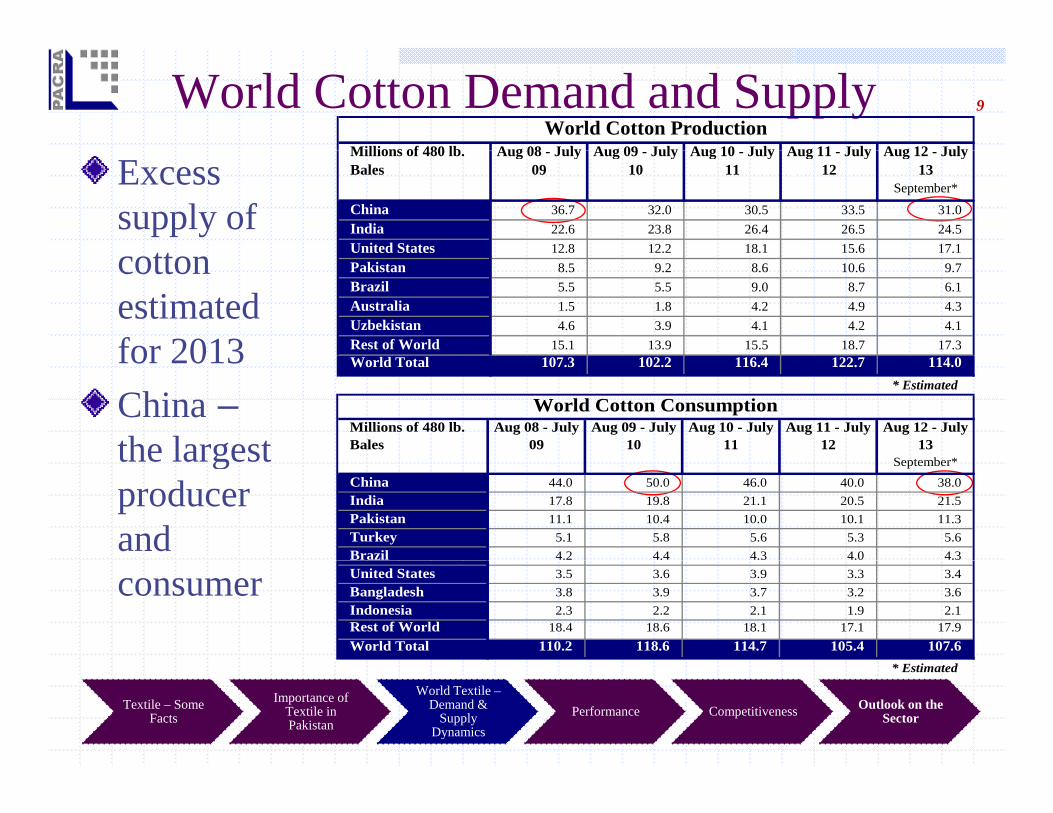

World Cotton Demand and Supply 9

Millions of 480 lb Aug 08 July Aug 09 July Aug 10 July Aug 11 July Aug 12 JulyWorld Cotton Production

Excess supply of

tt

Millions of 480 lb. Bales

Aug 08 - July 09

Aug 09 - July 10

Aug 10 - July 11

Aug 11 - July 12

Aug 12 - July 13

September*

China 36.7 32.0 30.5 33.5 31.0 India 22.6 23.8 26.4 26.5 24.5 United States 12.8 12.2 18.1 15.6 17.1 cotton

estimated for 2013

U ed S es . . . . 7.Pakistan 8.5 9.2 8.6 10.6 9.7 Brazil 5.5 5.5 9.0 8.7 6.1 Australia 1.5 1.8 4.2 4.9 4.3 Uzbekistan 4.6 3.9 4.1 4.2 4.1 Rest of World 15.1 13.9 15.5 18.7 17.3 for 2013

China –the largest

World Total 107.3 102.2 116.4 122.7 114.0 * Estimated

Millions of 480 lb. Bales

Aug 08 - July 09

Aug 09 - July 10

Aug 10 - July 11

Aug 11 - July 12

Aug 12 - July 13

S b *

World Cotton Consumption

the largest producer and

September*

China 44.0 50.0 46.0 40.0 38.0 India 17.8 19.8 21.1 20.5 21.5 Pakistan 11.1 10.4 10.0 10.1 11.3 Turkey 5.1 5.8 5.6 5.3 5.6 Brazil 4.2 4.4 4.3 4.0 4.3

consumer United States 3.5 3.6 3.9 3.3 3.4 Bangladesh 3.8 3.9 3.7 3.2 3.6 Indonesia 2.3 2.2 2.1 1.9 2.1 Rest of World 18.4 18.6 18.1 17.1 17.9 World Total 110.2 118.6 114.7 105.4 107.6

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

* Estimated

Cotton Demand and Supply 9

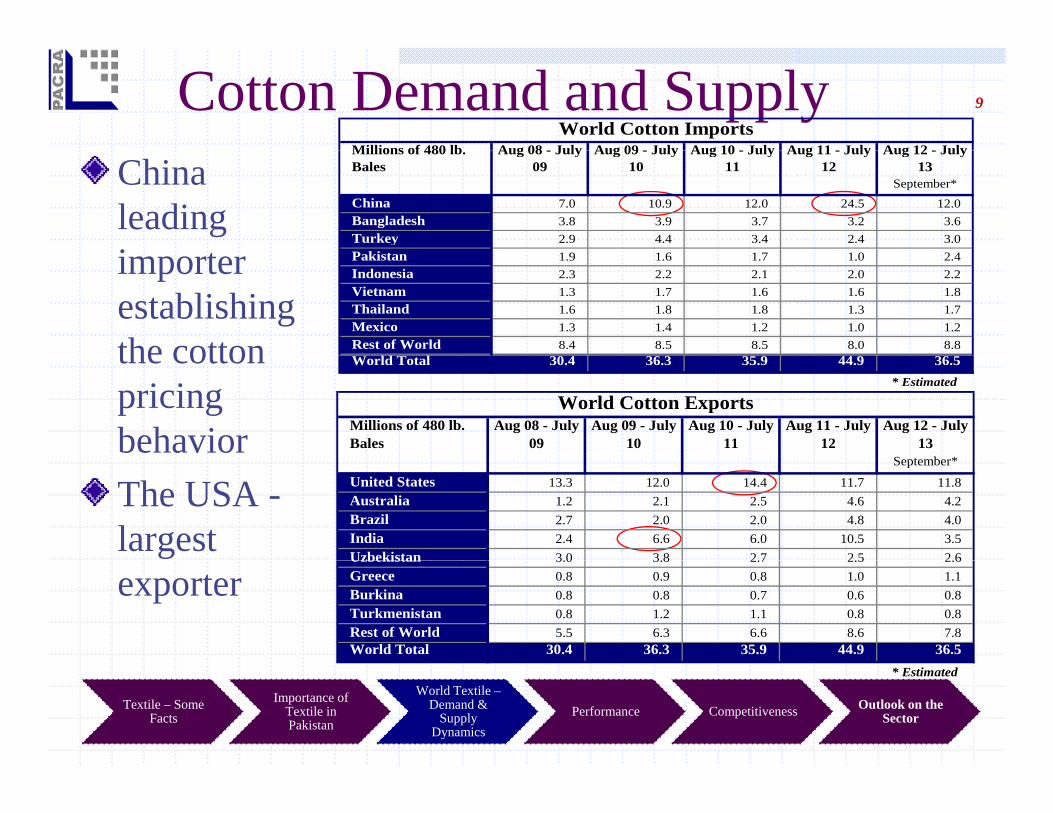

Millions of 480 lb Aug 08 July Aug 09 July Aug 10 July Aug 11 July Aug 12 JulyWorld Cotton Imports

Chinaleading i t

Millions of 480 lb. Bales

Aug 08 - July 09

Aug 09 - July 10

Aug 10 - July 11

Aug 11 - July 12

Aug 12 - July 13

September*China 7.0 10.9 12.0 24.5 12.0 Bangladesh 3.8 3.9 3.7 3.2 3.6 Turkey 2.9 4.4 3.4 2.4 3.0 P ki t 1 9 1 6 1 7 1 0 2 4importer

establishing the cotton

Pakistan 1.9 1.6 1.7 1.0 2.4 Indonesia 2.3 2.2 2.1 2.0 2.2 Vietnam 1.3 1.7 1.6 1.6 1.8 Thailand 1.6 1.8 1.8 1.3 1.7 Mexico 1.3 1.4 1.2 1.0 1.2 Rest of World 8.4 8.5 8.5 8.0 8.8 the cotton

pricing behavior

World Total 30.4 36.3 35.9 44.9 36.5 * Estimated

Millions of 480 lb. Bales

Aug 08 - July 09

Aug 09 - July 10

Aug 10 - July 11

Aug 11 - July 12

Aug 12 - July 13

S t b *

World Cotton Exports

The USA -largest

September*

United States 13.3 12.0 14.4 11.7 11.8 Australia 1.2 2.1 2.5 4.6 4.2 Brazil 2.7 2.0 2.0 4.8 4.0 India 2.4 6.6 6.0 10.5 3.5 Uzbekistan 3.0 3.8 2.7 2.5 2.6

exporterUzbekistan 3.0 3.8 2.7 2.5 2.6 Greece 0.8 0.9 0.8 1.0 1.1 Burkina 0.8 0.8 0.7 0.6 0.8 Turkmenistan 0.8 1.2 1.1 0.8 0.8 Rest of World 5.5 6.3 6.6 8.6 7.8 World Total 30.4 36.3 35.9 44.9 36.5

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

* Estimated

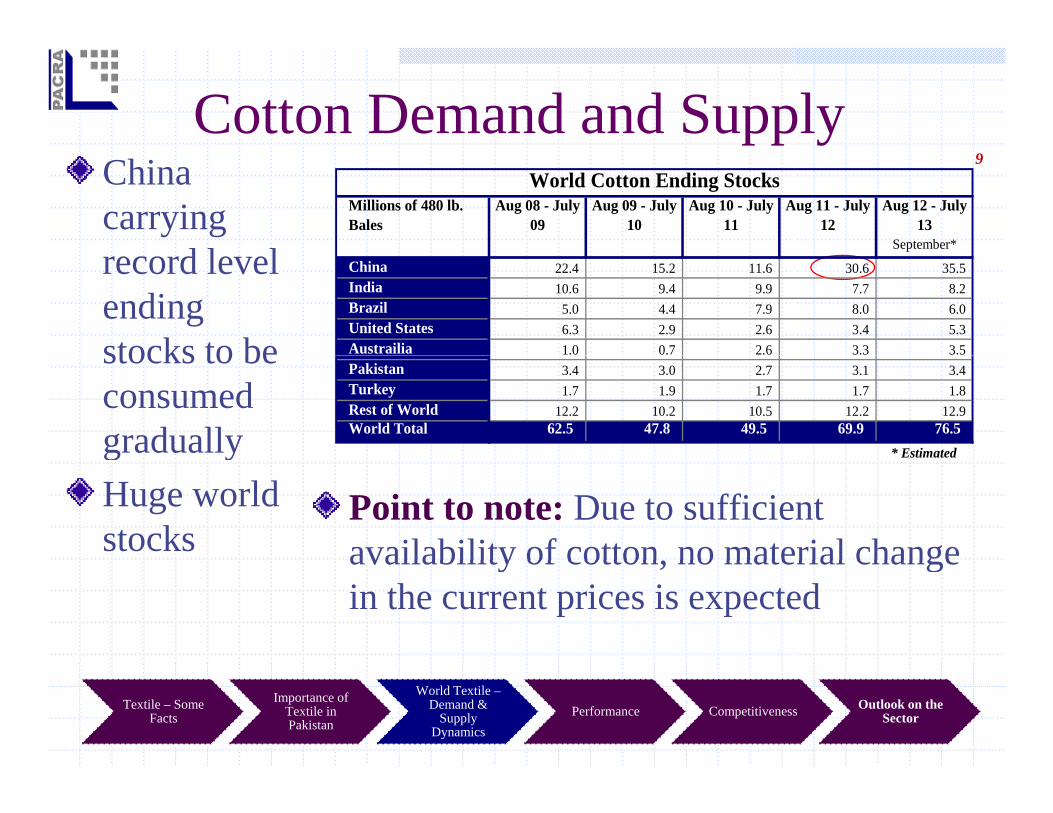

Cotton Demand and Supply9China

carrying d l l

Millions of 480 lb. Bales

Aug 08 - July 09

Aug 09 - July 10

Aug 10 - July 11

Aug 11 - July 12

Aug 12 - July 13

September*

World Cotton Ending Stocks

record level ending stocks to be

China 22.4 15.2 11.6 30.6 35.5 India 10.6 9.4 9.9 7.7 8.2 Brazil 5.0 4.4 7.9 8.0 6.0 United States 6.3 2.9 2.6 3.4 5.3 Austrailia 1.0 0.7 2.6 3.3 3.5 stocks to be

consumed gradually

Pakistan 3.4 3.0 2.7 3.1 3.4 Turkey 1.7 1.9 1.7 1.7 1.8 Rest of World 12.2 10.2 10.5 12.2 12.9 World Total 62.5 47.8 49.5 69.9 76.5

* Estimatedg yHuge world stocks

Point to note: Due to sufficient availability of cotton no material changeavailability of cotton, no material change in the current prices is expected

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

10

300

350

12,000

14,000

Country Wise Cotton Price ComparisonHigher cotton

i i200

250

8,000

10,000

Cent

s

PKR

prices in China due to

50

100

150

2 000

4,000

6,000 US Pdue to

support price

0

50

0

2,000

Aug-1

0Se

p-10

Oct-1

0No

v-10

Dec-1

0Ja

n-11

Feb-

11M

ar-11

Apr-1

1M

ay-11

Jun-

11Ju

l-11

Aug-1

1Se

p-11

Oct-1

1No

v-11

Dec-1

1Ja

n-12

Feb-

12M

ar-12

Apr-1

2M

ay-12

Jun-

12Ju

l-12

Aug-1

2

p

Pakistan (PKR/Maund) USA (Cts/Lb)China (Cts/Lb) India (Cts/Lb)Pakistan (Cts/Lb)

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

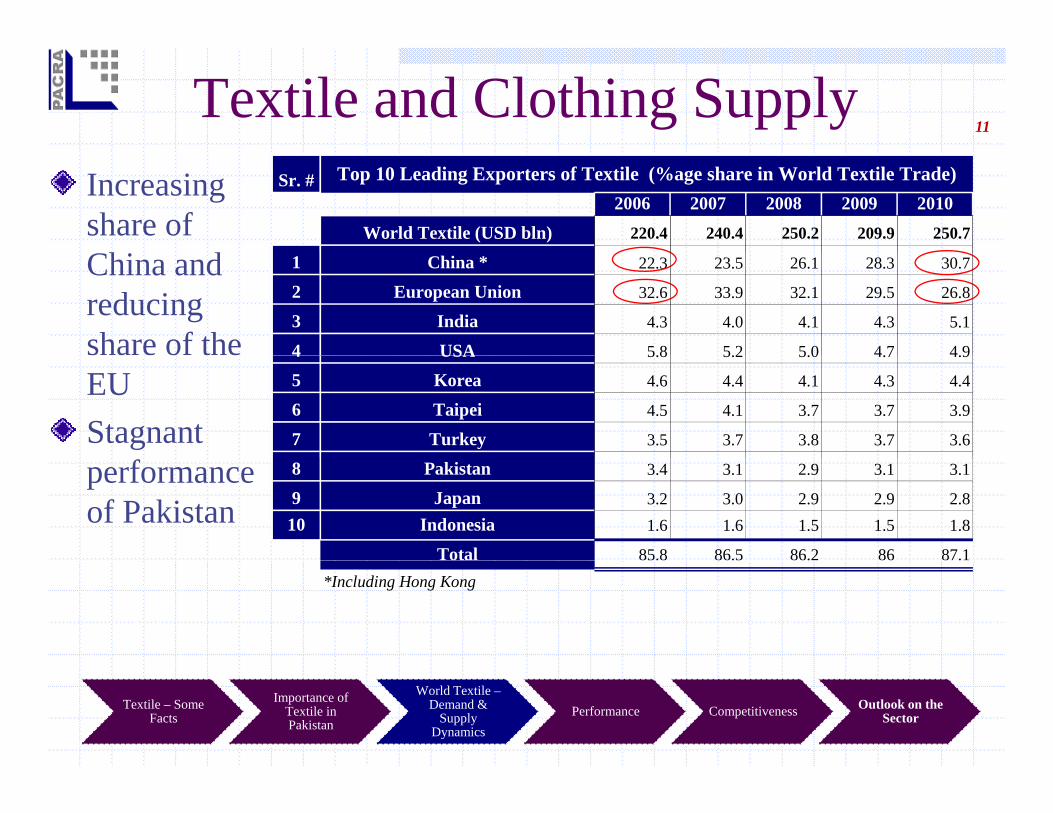

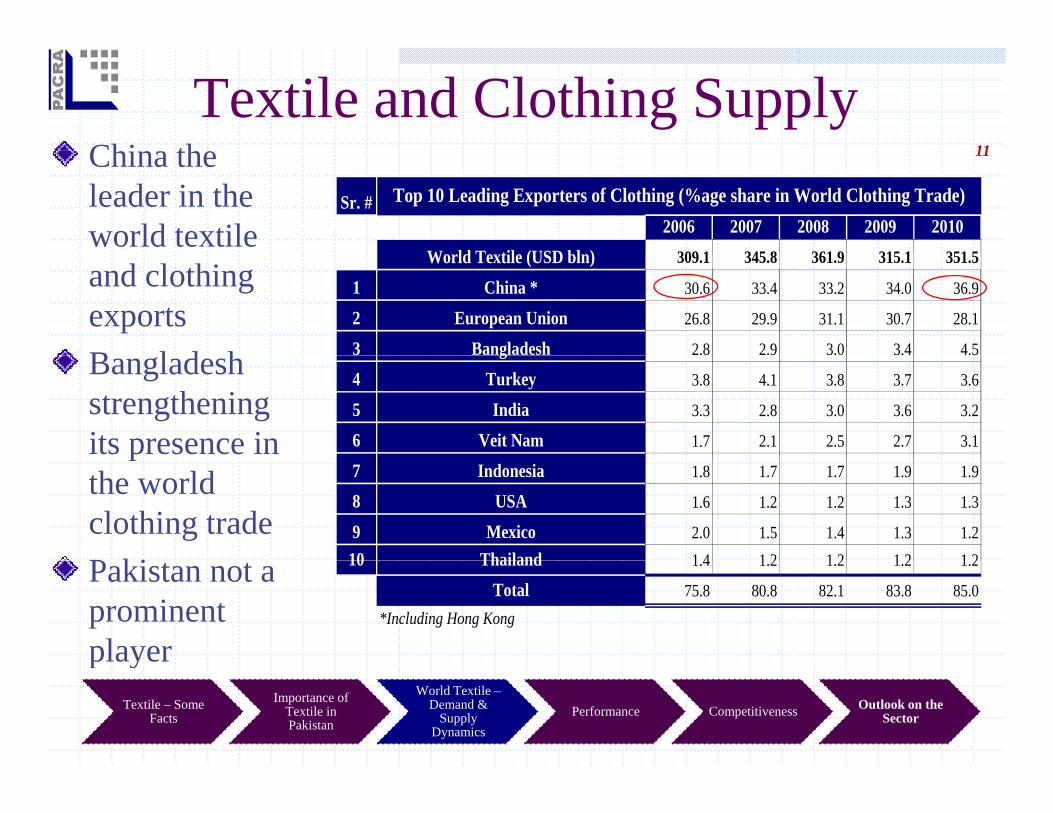

Textile and Clothing Supply11

Sr. #2006 2007 2008 2009 2010

World Textile (USD bln) 220.4 240.4 250.2 209.9 250.7

Top 10 Leading Exporters of Textile (%age share in World Textile Trade)Increasing share of Chi d 1 China * 22.3 23.5 26.1 28.3 30.7

2 European Union 32.6 33.9 32.1 29.5 26.8

3 India 4.3 4.0 4.1 4.3 5.1

4 USA 5.8 5.2 5.0 4.7 4.9

China and reducing share of the 4 USA 5.8 5.2 5.0 4.7 4.9

5 Korea 4.6 4.4 4.1 4.3 4.4

6 Taipei 4.5 4.1 3.7 3.7 3.9

7 Turkey 3.5 3.7 3.8 3.7 3.6

EU Stagnant

8 Pakistan 3.4 3.1 2.9 3.1 3.1

9 Japan 3.2 3.0 2.9 2.9 2.810 Indonesia 1.6 1.6 1.5 1.5 1.8

Total 85.8 86.5 86.2 86 87.1

performance of Pakistan

*Including Hong Kong

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Textile and Clothing Supply11Chi th 11

Sr. #2006 2007 2008 2009 2010

W ld T til (USD bl ) 309 1 345 8 361 9 315 1 351 5

Top 10 Leading Exporters of Clothing (%age share in World Clothing Trade)

China the leader in the world textile

World Textile (USD bln) 309.1 345.8 361.9 315.1 351.5

1 China * 30.6 33.4 33.2 34.0 36.9

2 European Union 26.8 29.9 31.1 30.7 28.1

3 Bangladesh 2.8 2.9 3.0 3.4 4.5

and clothing exportsB l d h g

4 Turkey 3.8 4.1 3.8 3.7 3.6

5 India 3.3 2.8 3.0 3.6 3.2

6 Veit Nam 1.7 2.1 2.5 2.7 3.1

Bangladesh strengthening its presence in

7 Indonesia 1.8 1.7 1.7 1.9 1.9

8 USA 1.6 1.2 1.2 1.3 1.3

9 Mexico 2.0 1.5 1.4 1.3 1.210 Thailand 1 4 1 2 1 2 1 2 1 2

pthe world clothing trade P ki 10 Thailand 1.4 1.2 1.2 1.2 1.2

Total 75.8 80.8 82.1 83.8 85.0*Including Hong Kong

Pakistan not a prominent player

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

p y

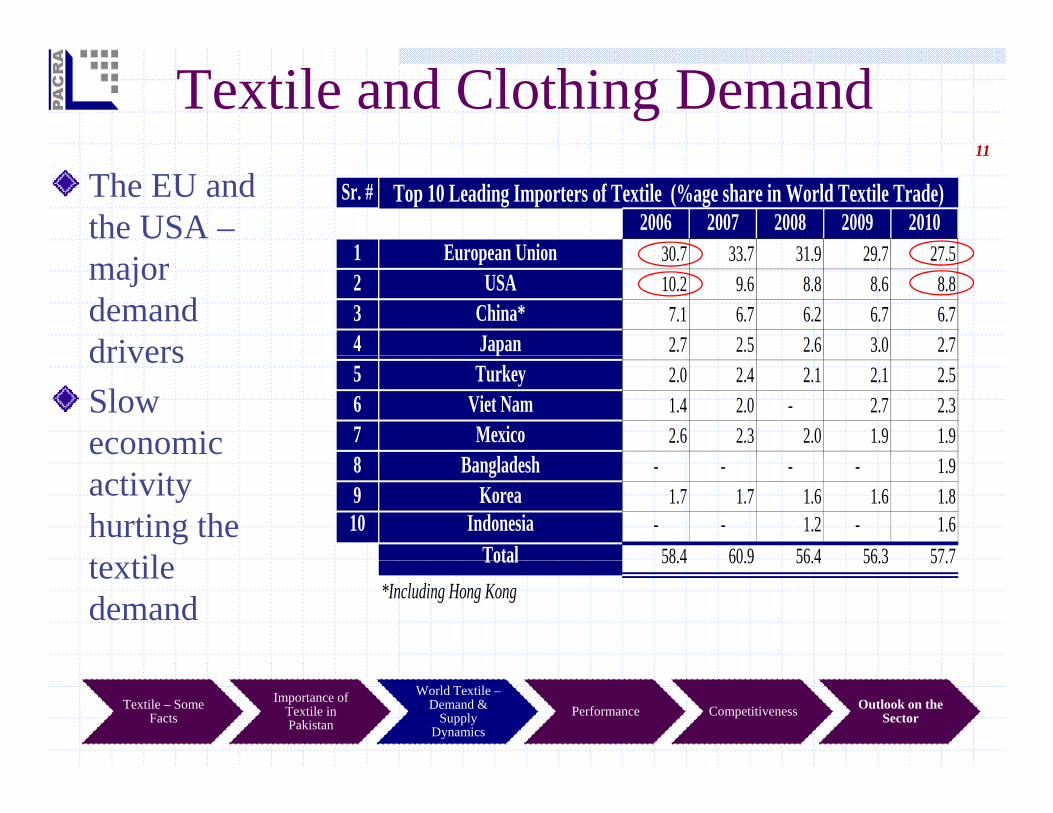

Textile and Clothing Demand1111

Sr. #2006 2007 2008 2009 2010

1 European Union 30 7 33 7 31 9 29 7 27 5

Top 10 Leading Importers of Textile (%age share in World Textile Trade)The EU and the USA –

1 European Union 30.7 33.7 31.9 29.7 27.52 USA 10.2 9.6 8.8 8.6 8.83 China* 7.1 6.7 6.2 6.7 6.74 Japan 2.7 2.5 2.6 3.0 2.7

major demand drivers p

5 Turkey 2.0 2.4 2.1 2.1 2.56 Viet Nam 1.4 2.0 - 2.7 2.37 Mexico 2.6 2.3 2.0 1.9 1.98 B l d h

driversSlow economic

8 Bangladesh - - - - 1.99 Korea 1.7 1.7 1.6 1.6 1.810 Indonesia - - 1.2 - 1.6

Total 58 4 60 9 56 4 56 3 57 7

activity hurting the t til Total 58.4 60.9 56.4 56.3 57.7

*Including Hong Kongtextile demand

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

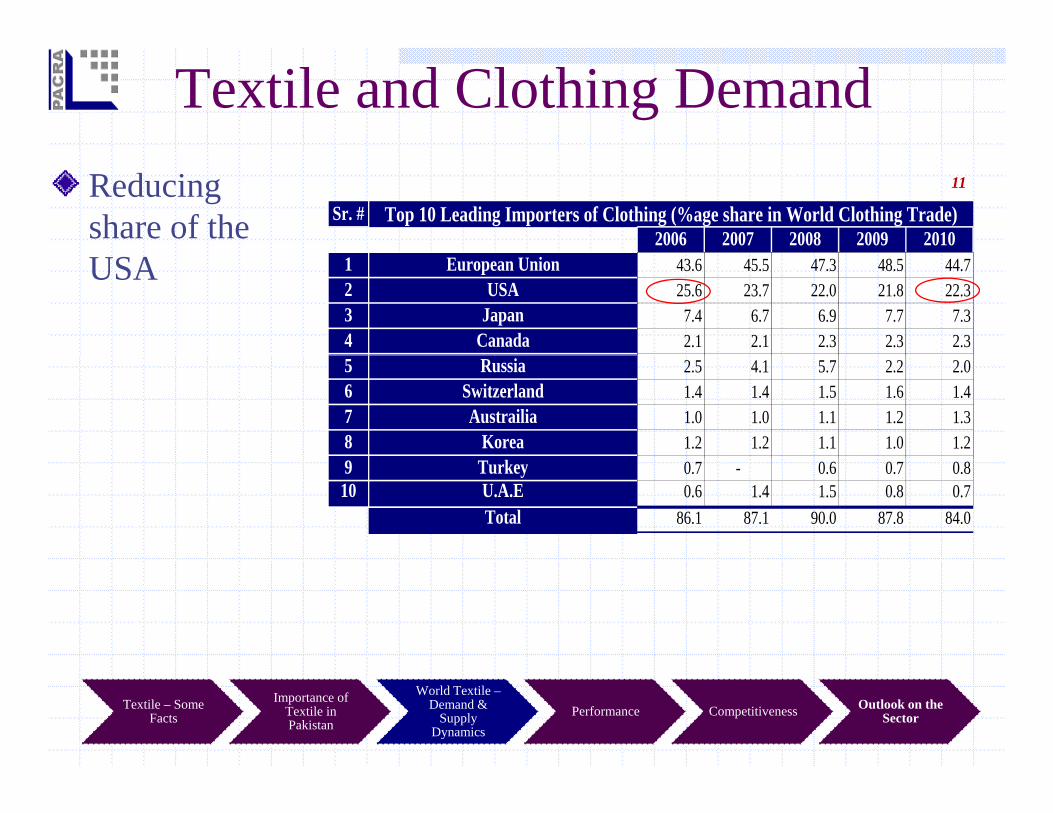

Textile and Clothing Demand11

Sr. #2006 2007 2008 2009 2010

Top 10 Leading Importers of Clothing (%age share in World Clothing Trade)Reducing share of the

1 European Union 43.6 45.5 47.3 48.5 44.72 USA 25.6 23.7 22.0 21.8 22.33 Japan 7.4 6.7 6.9 7.7 7.34 Canada 2.1 2.1 2.3 2.3 2.3

USA

5 Russia 2.5 4.1 5.7 2.2 2.06 Switzerland 1.4 1.4 1.5 1.6 1.47 Austrailia 1.0 1.0 1.1 1.2 1.38 Korea 1.2 1.2 1.1 1.0 1.29 Turkey 0.7 - 0.6 0.7 0.810 U.A.E 0.6 1.4 1.5 0.8 0.7

Total 86.1 87.1 90.0 87.8 84.0

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

12

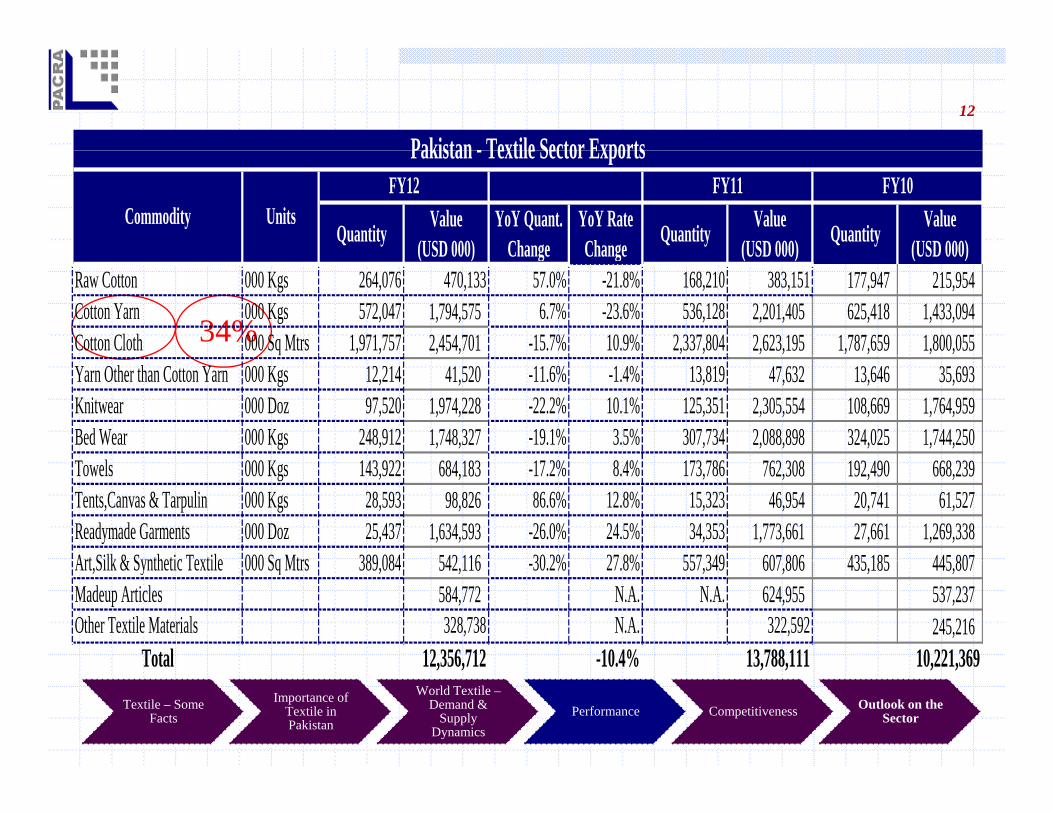

Pakistan - Textile Sector Exports

Quantity Value (USD 000)

YoY Quant. Change

YoY Rate Change Quantity Value

(USD 000) Quantity Value (USD 000)

Pakistan - Textile Sector Exports

Commodity UnitsFY12 FY11 FY10

34%

(USD 000) Change Change (USD 000) (USD 000)Raw Cotton 000 Kgs 264,076 470,133 57.0% -21.8% 168,210 383,151 177,947 215,954 Cotton Yarn 000 Kgs 572,047 1,794,575 6.7% -23.6% 536,128 2,201,405 625,418 1,433,094 Cotton Cloth 000 Sq Mtrs 1,971,757 2,454,701 -15.7% 10.9% 2,337,804 2,623,195 1,787,659 1,800,055 Yarn Other than Cotton Yarn 000 Kgs 12,214 41,520 -11.6% -1.4% 13,819 47,632 13,646 35,693 Knitwear 000 Doz 97,520 1,974,228 -22.2% 10.1% 125,351 2,305,554 108,669 1,764,959 Bed Wear 000 Kgs 248,912 1,748,327 -19.1% 3.5% 307,734 2,088,898 324,025 1,744,250 Towels 000 Kgs 143,922 684,183 -17.2% 8.4% 173,786 762,308 192,490 668,239 Tents,Canvas & Tarpulin 000 Kgs 28,593 98,826 86.6% 12.8% 15,323 46,954 20,741 61,527 Readymade Garments 000 Doz 25,437 1,634,593 -26.0% 24.5% 34,353 1,773,661 27,661 1,269,338 Art Silk & Synthetic Textile 000 Sq Mtrs 389 084 542 116 30 2% 27 8% 557 349 607 806 435 185 445 807Art,Silk & Synthetic Textile 000 Sq Mtrs 389,084 542,116 -30.2% 27.8% 557,349 607,806 435,185 445,807 Madeup Articles 584,772 N.A. N.A. 624,955 537,237 Other Textile Materials 328,738 N.A. 322,592 245,216

Total 12,356,712 -10.4% 13,788,111 10,221,369Textile – Some

FactsImportance of

Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Total 12,356,712 10.4% 13,788,111 10,221,369

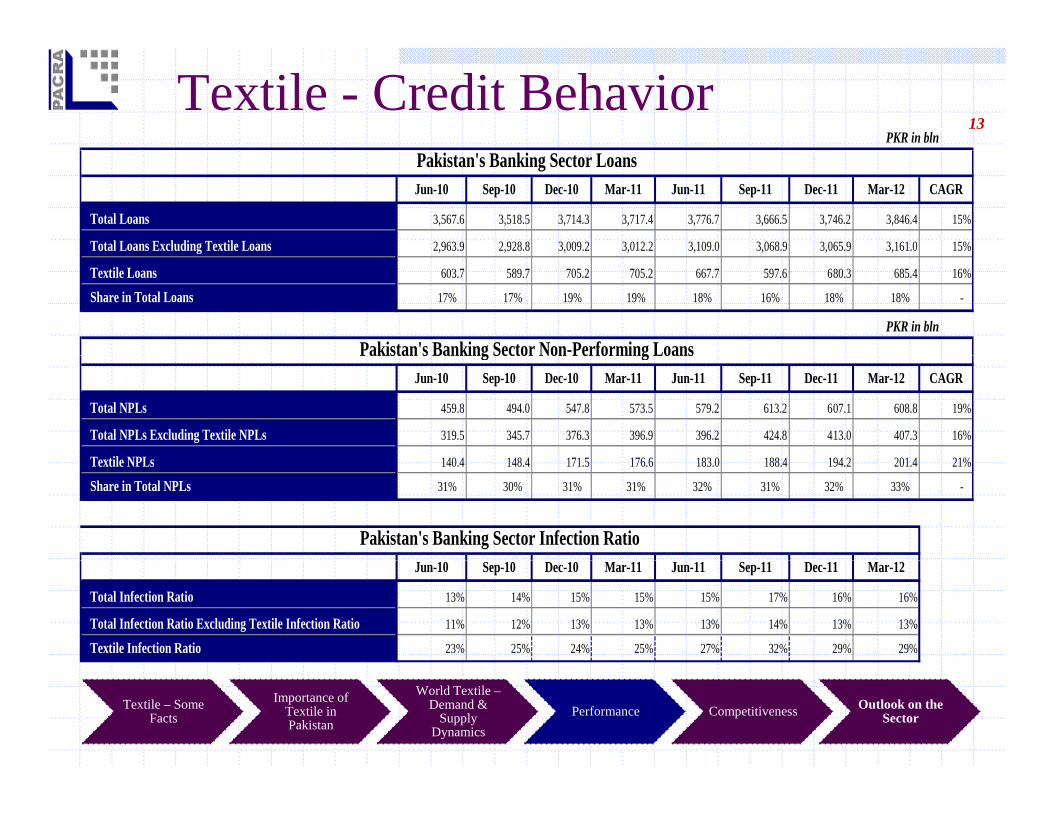

Textile - Credit Behavior13

PKR in bln

Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 CAGR

Total Loans 3,567.6 3,518.5 3,714.3 3,717.4 3,776.7 3,666.5 3,746.2 3,846.4 15%

Total Loans Excluding Textile Loans 2,963.9 2,928.8 3,009.2 3,012.2 3,109.0 3,068.9 3,065.9 3,161.0 15%

Pakistan's Banking Sector Loans

g , , , , , , , ,

Textile Loans 603.7 589.7 705.2 705.2 667.7 597.6 680.3 685.4 16%

Share in Total Loans 17% 17% 19% 19% 18% 16% 18% 18% -

PKR in blnPakistan's Banking Sector Non-Performing Loans

Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 CAGR

Total NPLs 459.8 494.0 547.8 573.5 579.2 613.2 607.1 608.8 19%

Total NPLs Excluding Textile NPLs 319.5 345.7 376.3 396.9 396.2 424.8 413.0 407.3 16%

T til NPL 140 4 148 4 171 5 176 6 183 0 188 4 194 2 201 4 21%

Pakistan s Banking Sector Non Performing Loans

Textile NPLs 140.4 148.4 171.5 176.6 183.0 188.4 194.2 201.4 21%

Share in Total NPLs 31% 30% 31% 31% 32% 31% 32% 33% -

Pakistan's Banking Sector Infection RatioJun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12

Total Infection Ratio 13% 14% 15% 15% 15% 17% 16% 16%

Total Infection Ratio Excluding Textile Infection Ratio 11% 12% 13% 13% 13% 14% 13% 13%

Textile Infection Ratio 23% 25% 24% 25% 27% 32% 29% 29%

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

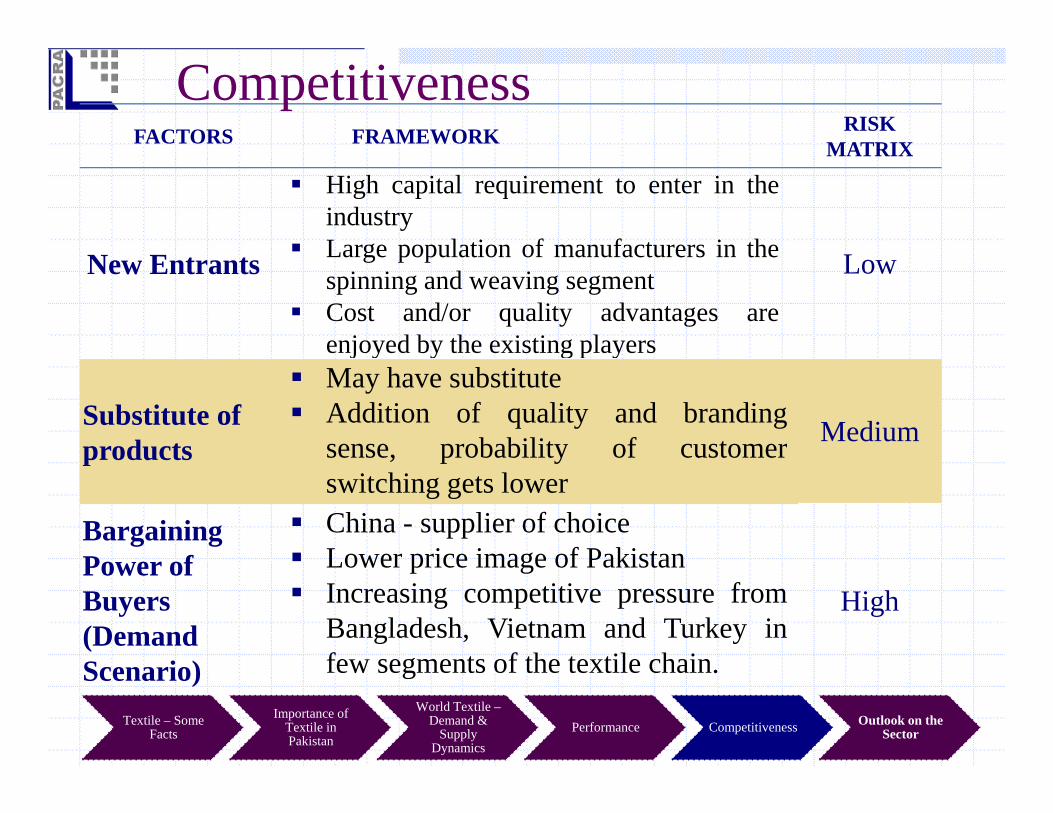

FACTORS FRAMEWORK RISK MATRIX

Competitiveness

High capital requirement to enter in theindustryLarge population of manufacturers in the

MATRIX

New Entrants Large population of manufacturers in thespinning and weaving segmentCost and/or quality advantages areenjoyed by the existing players

Low

j y y g p y

Substitute of products

May have substituteAddition of quality and brandingsense, probability of customer Mediumproducts , p yswitching gets lower

Bargaining P f

China - supplier of choiceLower price image of PakistanPower of

Buyers (Demand S i )

Lower price image of PakistanIncreasing competitive pressure fromBangladesh, Vietnam and Turkey infew segments of the textile chain

High

Scenario) few segments of the textile chain.

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

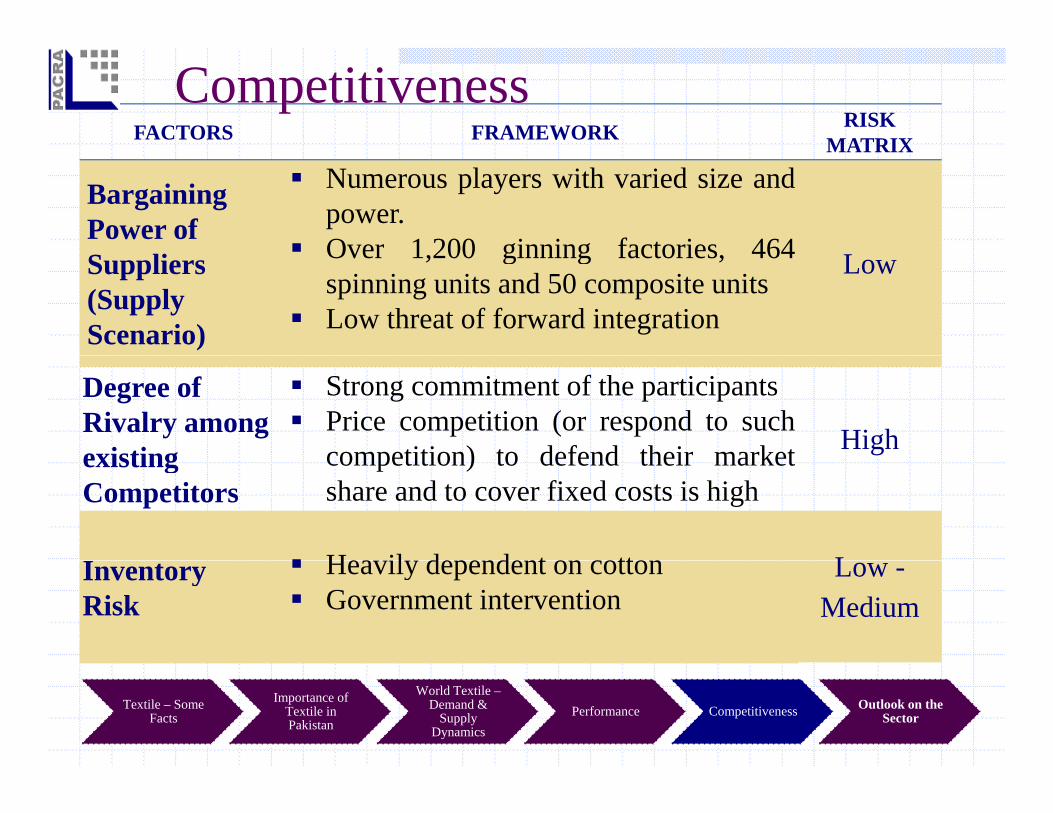

FACTORS FRAMEWORK RISK MATRIX

Competitiveness

Bargaining Power of

Numerous players with varied size andpower.Over 1 200 ginning factories 464

MATRIX

Suppliers (Supply Scenario)

Over 1,200 ginning factories, 464spinning units and 50 composite unitsLow threat of forward integration

Low

Degree of Rivalry among existing

Strong commitment of the participantsPrice competition (or respond to suchcompetition) to defend their market Highexisting

Competitors competition) to defend their marketshare and to cover fixed costs is high

He il de e de t tt LInventory Risk

Heavily dependent on cottonGovernment intervention

Low -Medium

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

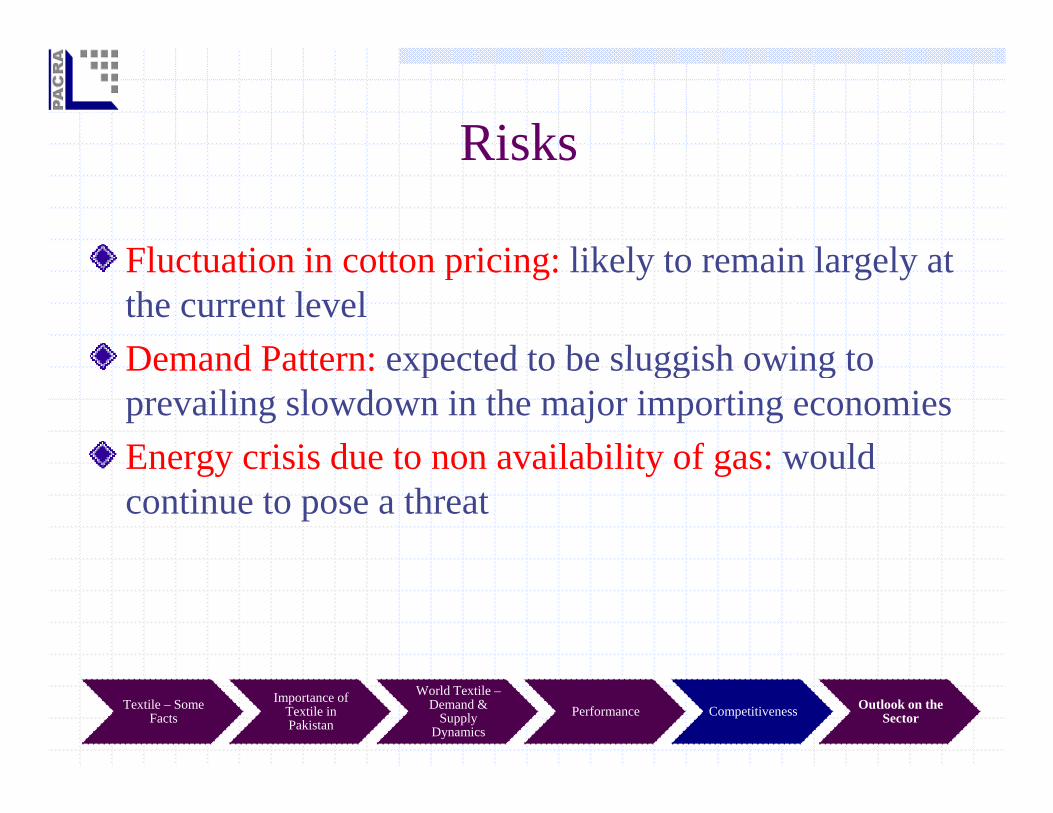

RisksRisks

Fl t ti i tt i i lik l t i l l tFluctuation in cotton pricing: likely to remain largely at the current levelDemand Pattern: expected to be sluggish owing toDemand Pattern: expected to be sluggish owing to prevailing slowdown in the major importing economiesEnergy crisis due to non availability of gas: wouldEnergy crisis due to non availability of gas: would continue to pose a threat

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Business Risk:Spinning and weaving Segments: LowValue Added Segments: Medium

What’s the outlook | Stable

Textile – Some Facts

Importance of Textile in Pakistan

World Textile –Demand &

Supply Dynamics

Performance Competitiveness Outlook on the Sector

Bibliography1. Pakistan Economic Survey 2010-11: Manufacturing and Mining | Section 3.22. Pakistan Textile Journal | February - 2010 | Pakistan: The third largest spinner country in Asia by Dr.

Noor Ahmed Memon3. Contributes 46% of the total manufacturing: Pakistan Economic Survey | 2011-12|Manufacturing and

Mining | Section 3.24. Pakistanpaedia : http://www.pakistanpaedia.com/maps/maps-of-pakistan.html5. State Bank of Pakistan : Economic Data | Export Receipts by Commodity | Archive Monthly6. All Pakistan Textile Mills Association: http://www.aptma.org.pk/Pak_Textile_Statistics/Gctipw.asp7. All Pakistan Textile Mills Association: Member Directory8. Karachi Stock Exchange: Downloads | Analysis Reports9. United States Department of Agriculture: http://www.fas.usda.gov/cotton/Current/10. All Pakistan Textile Mills Association11. World Trade Organization : International Trade Statistics – 2011, 2010, 2009, 2008, 200712. All Pakistan Textile Mills Association13. State Bank of Pakistan: Statistics of the Banking System | editions: Sep10, Sep11, Dec11 and Mar12g y | p , p ,

Analysts Aisha Khalid+92 42 3586 9504

Omaira Amjad+92 42 3586 9504

M. Shahnawaz A. Khanzada+92 42 3586 9504+92 42 3586 9504

[email protected]+92 42 3586 [email protected]

+92 42 3586 [email protected]

DISCLAIMERSCPACRA has used due care in preparation of this document. Our information has been obtainedfrom sources we consider to be reliable but its accuracy or completeness is not guaranteed.The information in this document may be copied or otherwise reproduced, in whole or in part,

id d th i d l k l d d Th t ti h ld t b li dprovided the source is duly acknowledged. The presentation should not be relied upon asprofessional advice.