Embed Size (px)

Citation preview

18th May 2015

Pharma & Biotech

Source: Fidessa

Market dataPrice (p) 3.512m High (p) 3.912 Low (p) 1.0Shares (m) 1009.9Mkt Cap (£m) 35.3EV (£m) 25.4EPIC VRPFree Float* (%) 97%Market AIM

*As defined by AIM Rule 26

Description

Company informationCEO Jan-Anders KarlssonCFO Biresh RoyChairman David Ebsworth

Next event11 June AGM2Q'15 RPL554 in asthma3Q'15 RPL554 SAD/MAD res4Q'15 RPL554+SoC combo

0203 283 4200www.veronapharma.com

Verona Pharma plc i s a UK-based biopharmaceutica l company focused on development of innovative prescription drugs to treat respiratory diseases with s igni ficant unmet medica l needs , such as COPD, asthma & cystic fibros is .

AnalystsMark Brewer 020 7148 [email protected] Hall 020 7148 [email protected]

Investor engagementMax Davey 020 7148 [email protected] Reid 020 7148 [email protected]

Verona Pharma (VRP.L) Initiation

Clinical data have increased probability of success

Verona Pharma is developing first-in-class drugs that treat unmet medical needs in respiratory disease. RPL554 is being fast-tracked to commercialisation by focusing on a $3.2bn market segment poorly serviced by existing drugs. Key Phase II trial results are due to be announced during the second half of 2015. There is a significant mis-match between the current EV (£25m) and a potential inflection point on positive Phase II data in 2H’15 when considering that median valuations for Phase II respiratory assets have headline valuations of $285m (£190m), or 19p per share.

Strategy: Verona Pharma is focused on respiratory medicines targeting areas of unmet medical need. Given its limited resources and competitive target markets, management has a clear strategy to develop and commercialise its lead drug as quickly as possible for a $3.2bn opportunity poorly served by existing drugs, treating exacerbations of COPD.

Products: RPL554, a first-in-class dual PDE3/PDE4 inhibitor with both bronchodilatory and anti-inflammatory activity, is in clinical development for three indications. Initially, as an add-on for acute exacerbations in COPD patients. However, the drug has potential also in the maintenance therapy of COPD patients, and in treatment of cystic fibrosis.

Valuation: To date, about £10m has been invested in R&D to get VRP where it is today, compared to an enterprise value of £25m. Positive outcomes from the phase II trial with RPL554 in COPD, which are due in 2H’15, would reach another significant value inflection point and allow management to start negotiations with potential licensing partners. Novel phase II respiratory assets have median headline valuations of $285m (£190m).

Risks: As with all drug companies, the main risk is that a product fails in clinical trials. In addition, even when drugs have completed their clinical development there remains regulatory and commercial risks. Rising cash burn on R&D investment and corporate infrastructure over the next three years is likely to require further capital increases.

Investment summary: Clinical trials for RPL554 have a binary outcome. Historically, efficacy of PDE inhibitors has been positive, but putative drugs have failed due to side effects. The positive safety outcome, even at high doses, announced on 23rd March has de-risked, in part, the Phase II efficacy part of this COPD trial. A positive outcome here later in 2015 should result in a significant increase in shareholder value.

Financial summary and valuation

Source: Hardman & Co Life Sciences Research

x

Year end Dec (£000) FY11 FY12 FY13 FY14 FY15E FY16ESales 0 0 0 0 0 0Royal ties 0 0 0 0 0 0Underlying EBIT -1,848 -2,585 -2,630 -3,601 -8,308 -4,693Reported EBIT -1,951 -2,653 -2,817 -3,793 -8,510 -4,905Underlying PTP -1,844 -2,565 -2,627 -3,571 -8,264 -4,688Statutory PTP -1,947 -2,633 -2,814 -3,763 -8,466 -4,900Underlying EPS (p) -0.7 -0.8 -0.7 -0.3 -0.7 -0.3Statutory EPS (p) -0.7 -0.8 -0.7 -0.3 -0.7 -0.4Net (debt)/cash 2,526 961 604 9,970 2,567 -1,242Shares i s sued 2,139 1,002 1,802 13,103 100 100P/E (x) - - - - - -

1

18 May 15

Table of Contents

Executive Summary ....................................................................................................... 3 Product Development .................................................................................................... 5

Core strategy ....................................................................................................... 6

Lead product – RPL554 ....................................................................................... 6

Target Indications ........................................................................................................ 10

COPD ................................................................................................................. 10

Aims of therapy ............................................................................................. 11

The inflammatory process ............................................................................ 14

Opportunity for RPL554 ................................................................................ 15

Cystic fibrosis .................................................................................................... 15

Competitive Landscape ................................................................................................ 17

New COPD drugs ............................................................................................... 17

New bronchodilators .................................................................................... 17

Novel anti-inflammatories ............................................................................ 18

New cystic fibrosis drugs .................................................................................. 20

Commercial Market ..................................................................................................... 21

Key facts ............................................................................................................ 21

Market by individual drug ................................................................................. 22

Market by company .......................................................................................... 23

New COPD drugs ............................................................................................... 23

Increased use of nebulisers .............................................................................. 24

Cystic fibrosis .................................................................................................... 25

Financials & Investment Case....................................................................................... 26

History ............................................................................................................... 26

Capital increases ............................................................................................... 26

Share capital ..................................................................................................... 27

Financial statements ......................................................................................... 27

Valuation ........................................................................................................... 30

Company Matters ........................................................................................................ 33

Registration ....................................................................................................... 33

Board of Directors ............................................................................................. 33

Risks ............................................................................................................................ 35 Glossary ....................................................................................................................... 36 Notes ........................................................................................................................... 37 Disclaimer .................................................................................................................... 39

Verona Pharma plc 2

18 May 15

Executive Summary History Verona Pharma was originally established as Rhinopharma Ltd in Vancouver in April 2004 for the discovery and development of new drugs for the treatment of respiratory diseases. In August 2006, the whole share capital of Rhinopharma was acquired by Isis Resources, an AIM listed shell company, and renamed Verona Pharma. Verona has maintained its core competence in respiratory medicine, but has honed its strategy into areas where there is a significant unmet medical need – chronic obstructive pulmonary disease (COPD) and cystic fibrosis.

Strategy Management is focused on getting Verona’s key product, RPL554, to the next value inflection point as quickly as possible. With limited resources it has adopted a clear development, regulatory and commercial strategy to fast-track the commercialisation of RPL554 into smaller well-defined markets, which also serves to de-risk and position the programme for later-stage partnering into broader markets. Phase I/II clinical trials are underway for nebulised RPL554 in healthy volunteers, COPD and asthma patients using a new commercially scalable formulation, the results of which pave the way for a rapid Phase III trial either alone or by licensing to a major partner. Maintenance use of RPL554 in COPD and also its potential use in asthma represent major opportunities, but will need a large pharmaceutical partner. There is significant potential for RPL554 in cystic fibrosis, but this is at an earlier stage of development.

Products Part of Verona’s strategy is to have a ‘first-in-class’ drug which has a novel mechanism of action for use in respiratory medicine. It has one lead candidate, RPL554, which encompasses this strategy. Its mechanism of action is to specifically inhibit two members of the phosphodiesterase (PDE) family. As such, it is thought to have a triple mechanism of action in respiratory disease – inhibiting PDE3 is associated with relaxation of airway smooth muscle; blocking PDE4 has significant anti-inflammatory activity; and inhibition of PDE3 and PDE4 activates the Cystic Fibrosis Transmembrane conductance Regulator (CFTR) which is beneficial in reducing mucous viscosity and improving mucociliary clearance in cystic fibrosis and COPD.

RPL554 is at various stages of development for a number of indications which are shown in the following graph. Verona has just announced positive results from a Phase I safety trial for its new formulation of RPL554, delivered via a nebuliser. This formulation allows for much higher doses of RPL554 to be delivered for efficacy without evidence of any of the traditional side effects seen historically with other developmental PDE inhibitors.

Development plan for RPL554

Source: Verona Pharma Verona Pharma plc 3

18 May 15

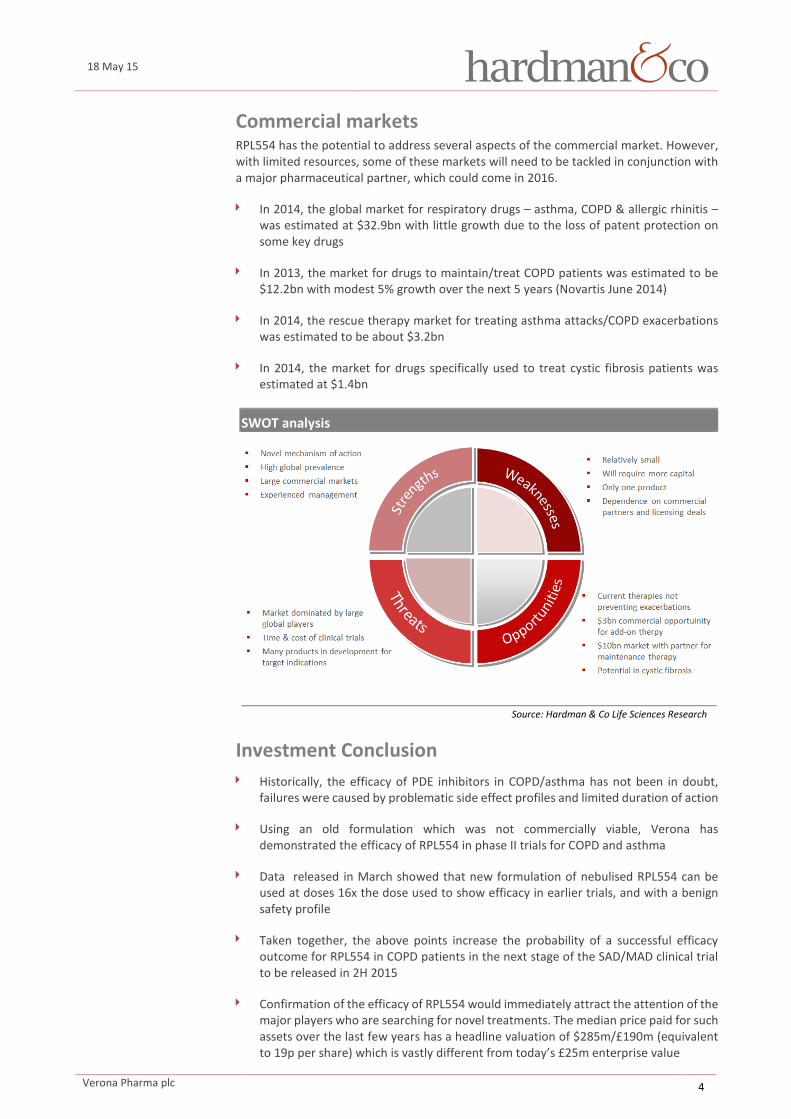

Commercial markets RPL554 has the potential to address several aspects of the commercial market. However, with limited resources, some of these markets will need to be tackled in conjunction with a major pharmaceutical partner, which could come in 2016.

In 2014, the global market for respiratory drugs – asthma, COPD & allergic rhinitis – was estimated at $32.9bn with little growth due to the loss of patent protection on some key drugs

In 2013, the market for drugs to maintain/treat COPD patients was estimated to be $12.2bn with modest 5% growth over the next 5 years (Novartis June 2014)

In 2014, the rescue therapy market for treating asthma attacks/COPD exacerbations was estimated to be about $3.2bn

In 2014, the market for drugs specifically used to treat cystic fibrosis patients was estimated at $1.4bn

SWOT analysis

Source: Hardman & Co Life Sciences Research

Investment Conclusion Historically, the efficacy of PDE inhibitors in COPD/asthma has not been in doubt,

failures were caused by problematic side effect profiles and limited duration of action

Using an old formulation which was not commercially viable, Verona has demonstrated the efficacy of RPL554 in phase II trials for COPD and asthma

Data released in March showed that new formulation of nebulised RPL554 can be used at doses 16x the dose used to show efficacy in earlier trials, and with a benign safety profile

Taken together, the above points increase the probability of a successful efficacy outcome for RPL554 in COPD patients in the next stage of the SAD/MAD clinical trial to be released in 2H 2015

Confirmation of the efficacy of RPL554 would immediately attract the attention of the major players who are searching for novel treatments. The median price paid for such assets over the last few years has a headline valuation of $285m/£190m (equivalent to 19p per share) which is vastly different from today’s £25m enterprise value

Verona Pharma plc 4

18 May 15

R&D investment

VRP has invested approximately £10m in R&D since inception to end 2014

Increase in R&D is directly associated with the cost of clinical trials for RPL554

R&D spend is forecast to rise in 2015 and then fall back again in 2016 after the current trial concludes

VRP will look to out-licence RPL554 for larger trials and indications

Net cash at 31st December

VRP is a cash burn company

The burn rate broadly equates to the R&D investment and SG&A spend each year

Following the capital increase in March 2014, VRP has invested in management infrastructure and accelerated its R&D programme

More cash would be needed to progress RPL554 through further clinical development alone

Capital increases

Verona has had several financing events since 2006

Total funds raised to date are £29.8m

£10m has been invested in R&D and the remaining £8m covers general corporate costs

Company will need more capital once the Phase II trial data in COPD is known

Free cashflow

Free cashflow will remain negative until commercialisation of RPL554

Company’s cash position is carefully managed

FCF increases in 2015 due to the increased investment in clinical trials

No allowance has been made for potential licensing income

Source: Company data; Hardman & Co Life Sciences Research

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2011 2012 2013 2014 2015E 2016E

R&D

spen

d (£

000)

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2011 2012 2013 2014 2015E 2016E

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012 2013 2014 2015E 2016E

Capi

tal i

ncre

ases

(£0

00)

-8,000

-7,000

-6,000

-5,000

-4,000

-3,000

-2,000

-1,000

0

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.02011 2012 2013 2014 2015E 2016E

FCF

(£m

)

FCF/

shar

e (p

)

Verona Pharma plc 5

18 May 15

Product Development Core strategy Since inception, Verona has maintained a core strategy of discovering and developing novel medicines for the treatment of respiratory disease. More recently, this strategy has been refined by the current management team to focus those medicines on areas of clinical need which are inadequately controlled by current therapies and have a relatively fast development and regulatory route to commercialisation. This strategy has been summarised in the following table.

Common product strategy Strategy Comment

“First-in-class” medicines Novel modes of action for respiratory medicines Seek & develop Aim: pre-clinical & clinical development to proof-of-concept Optimising speed to market Clear development & regulatory pathway to commercialisation High unmet medical need Target sub-sets in large markets that fail on current therapies Out-licensing potential For broader applications in large commercial markets

Source: Verona Pharma

Lead product – RPL554 Respiratory experts and drug companies have tried several approaches for the daily management of COPD patients and, should an acute exacerbation occur, how to treat it. Commercially successful products on the market today are relatively unsophisticated – bronchodilators or broad-spectrum corticosteroid anti-inflammatories. In contrast, Verona’s lead candidate – RPL554 – has a novel mode of action. It inhibits sub-types 3 and 4 of the enzyme phosphodiesterase (PDE). As such, it is thought to have a triple mechanism of action in respiratory disease – inhibition of PDE3 is associated with relaxation of the airway smooth muscle; while inhibition of PDE4 inhibits the activation of a number of cell types involved in the inflammatory cascade. Pre-clinical data also indicate that inhibition of the two enzyme subtypes at the same time can result in a much larger bronchodilator and anti-inflammatory effect (synergy) than inhibiting either enzyme alone due to the presence of both PDE3 and PDE4 in airway smooth muscle and certain types of cells involved in the inflammatory cascade. In addition, RPL554 activates the cystic fibrosis transmembrane conductance regulator (CFTR) which is thought to be beneficial in reducing mucous viscosity and improving mucociliary clearance in cystic fibrosis and COPD.

Mode of action of RPL554

Source: Verona Pharma

Airway Smooth muscle Inflammatory cells

Bronchodilation

Anti-inflammatory effects

Epithelial Cells

CFTR activation and

increased mucociliary

clearance

Pharmacological Effects of dual PDE3 and PDE4 Inhibition

Verona Pharma plc 6

18 May 15

Historically, there have been several attempts by drug companies to develop specific PDE3 inhibitors as bronchodilators. However, these all fell down in clinical trials because the dose needed for the required smooth muscle relaxation (bronchodilation) was short-acting and had cardiovascular side effects. Inhibitors of PDE4 receptors that reduce inflammation also suffer from side effect issues, causing severe nausea and vomiting.

However, an oral formulation of roflumilast (Daxas, Takeda), a PDE4 inhibitor, has been approved by the regulators and is available commercially. There are no drugs commercially marketed that inhibit both PDE3 and PDE4, which would satisfy Verona’s strategy to develop RPL554 as a “first-in-class” medicine.

Historically, RPL554 has been given to more than 150 human subjects, including patients suffering from COPD, asthma and allergic rhinitis in six clinical trials, which support its positioning as a dual bronchodilator and anti-inflammatory drug. Moreover, the side effect profile at doses used to elicit the clinical responses was benign and similar to that seen with placebo. These trials were summarised in a peer reviewed article entitled “Efficacy and safety of RPL554, a dual PDE3 and PDE4 inhibitor, in healthy volunteers and in patients with asthma or chronic obstructive pulmonary disease: findings from four clinical trials” published in November 2013 in The Lancet Respiratory Medicine (Vol 1, No. 9, p714-727).

However, the formulation of RPL554 used in these early studies was not suitable for commercialisation. Therefore, with the supportive results to hand Verona developed a new formulation of RPL554 to be given by nebuliser initially as an add-on therapy to existing treatments and potentially as a stand-alone treatment for chronic use. Pre-clinical data suggest that the new formulation produces far less irritation than the old formulation, probably due to the different pH. This formulation is also viable for commercial scale-up.

Given Verona’s resources, the short-term focus is on the treatment of acute exacerbations in patients suffering from COPD

More supportive clinical data for treating acute COPD exacerbations is likely to attract the attention of the major players and it is probable that Verona will license the commercial rights for the management of COPD to prevent acute exacerbations

Even though the focus is on COPD, there is arguably little differentiation with asthma. Notwithstanding this debate, acute exacerbations of COPD and acute asthma attacks are treated in hospitalised patients in broadly the same way, therefore RPL554 also has potential in both the treatment and prevention of asthma

Product pipeline

Source: Verona Pharma; Hardman & Co Life Sciences Research

Phase I/II trial in COPD During 4Q’14, Verona commenced a combined phase I/II trial with the new formulation of RPL554: “SAD/MAD Study of a New Formulation of Nebulised RPL554 in Healthy Subjects and COPD Subjects”.1 This trial is aiming to recruit up to 120 patients and is segregated into three stages, all of which are double-blind, placebo controlled, and randomised. Outcomes are expected to report over the course of 2015.

1 https://clinicaltrials.gov/ct2/show/NCT02307162?term=RPL554&rank=1

Drug Indication Pre-clinical Phase I Phase II

RPL554 COPD

RPL554 Asthma

RPL554 Cystic fibrosis

Verona Pharma plc 7

18 May 15

Stage 1: To assess the safety, tolerability and pharmacokinetics of ascending single nebulised doses of RPL554 in healthy male volunteers, with the secondary aim of ascertaining the maximum tolerated dose (MTD)

Stage 2: To assess the safety, tolerability and pharmacokinetics of 5 days of multiple ascending doses of RPL554 in healthy male volunteers

Stage 3: To assess the safety, tolerability and pharmacokinetics of 5 days of multiple ascending doses of RPL554 in patients with stable COPD

Results from Stage 1 Results from the first stage of this trial have been released and have shown very promising outcomes. Ascending single doses of nebulised RPL554 were given to 50 healthy male volunteers. Despite rising to over 16x the dose used with the original formulation, no Maximum Tolerated Dose (MTD) was determined. The new formulation was well tolerated and no evidence of nausea and vomiting was observed, even at the highest doses used.

In addition to the primary objectives, pharmacokinetic studies suggested that the new formulation resides in the lung longer, has slower release into the bloodstream and, therefore, a longer half-life (ca 12 hours).

These results are extremely exciting for two reasons and augur well for the subsequent stages of the trial. First, much higher doses of RPL554 can be used without the perennial problem of nausea and vomiting associated particularly with PDE4 inhibitors. Secondly, longer residence of the drug in the lung and consequent longer half-life tends to be associated with longer duration of effect and the potential for once or twice a day dosing.

SAD trial results Key findings

50 patients in Single Ascending Dose study recruited ahead of schedule

No MTD identified – despite dosing at 16x level of original formulation

No evidence of nausea or vomiting in any subject at any dose

Pharmacokinetics indicate slow release into bloodstream leading to longer half-life

Half-life of around 12hrs would indicate twice daily dosing

Source: Verona Pharma

Verona is now pushing ahead into the second stage of this trial and results are due 2H’15.

Development plan for RPL554 in COPD Phase I/IIa SAD/MAD trial – safety & efficacy studies

Establish bronchodilator dose and therapeutic window Confirm safety and assess efficacy against ‘Standard of Care’ Phase IIb trial – To start 2016

Confirm improved lung function and reduced symptoms Confirm shorter hospital stays Reduce 30 day re-admission rates Phase III trial

With partner ?

Source: Verona Pharma

Verona Pharma plc 8

18 May 15

RPL554 in cystic fibrosis Given the triple mechanism of action of RPL554 against PDE3 and PDE 4 enzymes, and activation of CFTR, there was a scientific rationale that this putative drug with bronchodilator and anti-inflammatory properties might also be useful in other respiratory conditions. Cystic fibrosis is a genetic disease characterised by a defective ion channel in the cells lining the airways which results in inadequate CFTR function and, consequently, accumulation of sticky viscous mucous in the airways of cystic fibrosis patients.

Pre-clinical data from studies at McGill University was presented at the 2014 North American Cystic Fibrosis Conference demonstrated that RPL554 was able to activate CFTR in cells obtained from the lining of the airways from cystic fibrosis patients. Further investigations are underway.

On the back of these results, in November 2014 Verona received a Venture & Innovation Award from the UK Cystic Fibrosis Trust (CFT) to further develop this work which is being carried out at two centres in the US – McGill University and The University of North Carolina at Chapel Hill – both recognised authorities in cystic fibrosis research. This is the first time that the UK CFT has awarded a Venture and Innovation Award to a biotech company, and bodes well for the potential utility of RPL554 as a novel treatment for cystic fibrosis, an under-treated and orphan disease.

Verona Pharma plc 9

18 May 15

Target Indications COPD The WHO estimates that there are 65 million people worldwide with COPD which accounts for 5% (~3 million) of all deaths each year, the third leading cause of mortality worldwide (WHO: The top 10 causes of death, May 2014). COPD is an umbrella term that encompasses progressive lung diseases that are characterised by airway obstruction that interferes with normal breathing. Conventionally, COPD includes emphysema and chronic bronchitis, which might be present to varying degrees. Inclusion of asthma patients that have developed partly irreversible airway limitation within the definition of COPD is slightly controversial. However the Venn diagram proposed by Snider presents graphically the idea that multiple disorders might be present to varying degrees in different individuals.

Subsets of COPD

Source: American Review of Respiratory Disease, 1989, 140, S3-8

In COPD, the airflow obstruction is not fully reversible and does not change materially, patients getting slightly worse over a prolonged period of time. A significant level of airway obstruction may be present long before the patient is aware of it. Acute exacerbations occur frequently, where there is a rapid and sustained worsening of symptoms beyond the normal day-to-day variations.

Clinical features of COPD Daily variation Acute exacerbation

Nocturnal wheeze Chronic cough

Daytime wheeze Productive sputum

Shortness of breath Bacterial infection

Bronchial irritation

Source: Kumar & Clark

Verona Pharma plc 10

18 May 15

COPD is predominantly caused by smoking. The American Lung Association estimates that 85-90% of COPD deaths are caused by smoking and that female smokers are 13x and male smokers 12x more likely to die from COPD compared to non-smokers. Therefore, COPD is more commonly associated with adults. Environmental factors such as pollution and allergens, particularly occupational exposures, also contribute to the development of COPD.

COPD produces symptoms, disability and impaired quality of life that significantly limits a person’s ability to work

COPD is now the preferred term for patients with airway obstruction who were previously diagnosed as having chronic bronchitis (with an associated infection)) and/or emphysema (damaged lung tissue)

There is no single diagnostic test for COPD – diagnosis relies on clinical judgement based on a combination of history, physical examination and confirmation of airway obstruction through spirometry (measurement of FEV1)

Both COPD and asthma result from obstructive airway disease, and therefore have similar symptoms. COPD is a progressive disease with dyspnoea as its major symptom, while asthma is much more variable and symptoms often vary from day to day. It’s important to differentiate COPD from asthma since treatment of the underlying condition is different. The underlying pathophysiology and inflammation are also different.

Clinical features differentiating COPD and asthma COPD Asthma

Smoker or ex-smoker Nearly all Possibly Symptoms under the age of 35 Rare Often Chronic productive cough Common Uncommon Breathlessness Persistent Variable Significant diurnal or day-to-day variability of symptoms Uncommon Common

Source: National Institute for Health & Care Excellence (NICE)

Aims of therapy Given that COPD is not a single disease, but an umbrella term to describe chronic lung disease that severely limits the flow or air to the lungs, a management plan has a number of components:

Assess and monitor the lung function

Reduce the underlying risk factors

Manage stable patients to prevent exacerbations

Manage exacerbations

First, patients should be encouraged to quit smoking and therefore remove the key risk factor. Secondly, patients should be managed with maintenance therapies to prevent an exacerbation. An exacerbation is a sustained worsening of a patient’s symptoms from their usual stable state which is beyond normal day-to-day variations, and is acute in onset. Commonly reported symptoms are materially worse breathlessness, cough and increased sputum production often associated with a change in colour. The change in these symptoms often necessitates a change in medication.

Verona Pharma plc 11

18 May 15

Drug therapy Drugs used to maintain COPD patients in a stable state to prevent exacerbations have changed over the last 10 years. This is because drugs were originally developed for use in asthma but were used also to treat COPD. But over the last two years, drugs have been approved and launched solely for use in COPD. There remains some misunderstanding and ambiguity, largely because drugs have been developed for one condition (eg COPD), but are better suited to the other (eg asthma) and in order to maximise commercial returns, drug companies seek approval for their drugs to be used in both conditions.

The following summarises the main drug classes:

Short-acting β2-agonists (SABA): Fast onset bronchodilator used to open the airways and relieve breathlessness in an acute exacerbation. These drugs are unsuitable for use in maintenance therapy/preventing an exacerbation.

Long-acting β2-agonists (LABA): Slow (relatively) onset bronchodilator used to maintain patients in a stable state. These drugs are unsuitable for use in an acute exacerbation.

Short-acting muscarinic antagonists (SAMA): Fast onset bronchodilator used as an adjunct to SABA to maximise airway opening in an acute exacerbation. Not suitable for use in maintenance therapy.

Long-acting muscarinic antagonists (LAMA): Slow onset bronchodilator used to maintain patients in a stable state. Unsuitable for use in an acute exacerbation.

Inhaled corticosteroids (ICS): Slow onset anti-inflammatory drugs. Not overly suitable in COPD because lung inflammation is less sensitive to this type of drug and the airway obstruction is not reversible, but used due to historic reasons, nearly always in combination with a LABA.

For maintenance use, these drugs are administered via an inhaler device wherever possible, although this does necessitate good hand-to-mouth co-ordination. In the event that this is not possible, oral theophylline and corticosteroids are often used, but both carry an increased side effect risk.

Maintenance/preventing an exacerbation As can be seen in the summary above, the most commonly used drugs for the maintenance of COPD and prevention of exacerbations are long-acting β-agonists (LABA) and long-acting muscarinic antagonists (LAMA) either alone, or more usually, in combination. Historically, from the stand-point of poor understanding and differentiation of COPD, and in the absence of recently launched targeted therapies, LABA in combination with inhaled corticosteroids originally approved for asthma maintenance have been, and are still, used to treat COPD.

Treating an acute exacerbation of COPD An acute exacerbation in COPD is characterised by a sustained worsening of respiratory symptoms (breathlessness, cough and/or sputum) and is the cause of many hospital admissions daily throughout the world. Drugs used for prevention are inappropriate for an acute exacerbation, as they take too long to exert their effect.

Oxygen therapy – essential in the management of an acute exacerbation

Bronchodilators – via nebuliser as soon as possible

Antibiotics – for any underling bacterial infection

Verona Pharma plc 12

18 May 15

Nebulised bronchodilators should be administered to patients with acute exacerbations. This segment of the market is dominated by the fast-acting β-agonists, salbutamol (Ventolin) and terbutaline (Bricanyl), which are available generically around the world in several formulations. Whilst other bronchodilators (anti-muscarinic drugs) are often used, they are nearly always in conjunction/combination with a SABA because of their slower onset of action. Given that patients will have taken these drugs via an inhaler device prior to hospitalisation, they are administered via a nebuliser in most circumstances.

Infection is a common precipitating feature of an acute exacerbation, although only 50% of patients have a positive sputum culture for bacteria. However, COPD patients are frequently colonised with bacterial pathogens – commonly haemophilus influenzae and streptococcus pneumoniae – hence culture of these organisms does not necessarily mean that they were responsible for the acute exacerbation. Viral infections have been shown to be responsible for up to 30% of exacerbations.

Inhaled corticosteroids are ineffective in an acute exacerbation as they take too long to act, however, patients are usually given oral or intravenous corticosteroids to reduce the inflammation and because they have been shown to reduce the risk of an early relapse.

Use of nebulisers Few respiratory specialists disagree that some form of inhaled drug is the most appropriate way to treat an acute exacerbation. Despite years of intense research to improve outcomes, the main drawback with inhaled devices is that they require really good hand-mouth coordination and only an estimated 15% of the active drug dose gets down into the airways, the remainder sticking in the back of the throat or is swallowed. In addition, patients will have already used their inhalers prior to hospitalisation. Consequently, aqueous solutions of SABA and SAMA are administered usually over a 15 minute period from a nebuliser, which is driven by compressed oxygen.

Even though studies have been unable to show a difference in the degree of bronchodilatation achieved with the same dose of drug administered by a metered dose inhaler or a nebuliser, nebulisers do offer a convenient way of altering the dose of drug and it is estimated that double the drug gets into the lungs by this method over a more prolonged period of time compared to metered dose inhalers. For these reasons, bronchodilator drugs are being administered increasingly via nebulisers in both the hospitalised setting (acute exacerbation) and in the home setting (COPD maintenance and treatment).

NICE guidelines on use of nebulisers

Patients with distressing or disabling breathlessness despite maximal therapy using inhalers should be considered for nebuliser therapy

Nebulised therapy should not continue to be prescribed without assessing and confirming that one or more of the following occurs: Reduction in symptoms; Increase in exercise capacity; Improvement in lung function

Nebulised therapy should not be prescribed without an assessment of the patient's and/or carer's ability to use it

A nebuliser system that is known to be efficient should be used

Patients should be offered a choice between a facemask and a mouthpiece to administer their nebulised therapy, unless the drug specifically requires a mouthpiece (for example anti-muscarinic drugs)

If nebuliser therapy is prescribed, the patient should be provided with equipment, servicing, advice and support

Source: National Institute for Health & Care Excellence

Verona Pharma plc 13

18 May 15

The inflammatory process COPD is associated with inflammation of the lungs. Consistent with this is the fact that inflammation is present in the lungs of all smokers, which is thought to be a normal protective mechanism in response to inhaled toxins. Precisely how this inflammatory response leads to tissue destruction, impairment of defence mechanisms, and impairment of repair mechanisms in COPD remains unclear. The following diagram summarises current hypotheses.

Patients with acute exacerbations of COPD usually present with thick sputum which is indicative of an associated infection which results in the presence of neutrophils in the sputum. This contrasts with those patients presenting with asthma where there is a predominance of eosinophils in the sputum, but sometimes asthma patients do have an infection and the associated presence of neutrophils. But this is not the focus of attention when a presenting patient enters hospital and sputum culture is not routinely checked for the presence of neutrophils or eosinophils.

Inflammatory mechanisms associated with COPD

Source: Oxford Textbook of Clinical Medicine

In the 1980s, there was considerable excitement generated from research into the inflammatory process. A number of intracellular mediators in the inflammatory cascade were identified. Drug companies took the view that a targeted approach would be more successful and made considerable investments into drugs that blocked the specific inflammatory mediators. However, few were successful, the downfall being either lack of efficacy and/or poor side effect profile.

From the following table, what has always been interesting, and never disputed, is that PDE3 and PDE4 inhibitors, unlike several of the other approaches, did appear to work but fell down on their side effect profiles. Verona appears to have overcome this issue with the good tolerability of its new nebulised formulation of RPL554.

Verona Pharma plc 14

18 May 15

Mediators in the inflammatory cascade Target Trial outcome

Platelet aggregating factor antagonists Lack of efficacy 5-Lipoxygenase inhibitors Lack of efficacy Leukotriene antagonists Successfully commercialised (Singulair) Phosphodiesterase inhibitors Efficacious, but severe nausea and vomiting Thromboxane antagonists Lack of efficacy Kinase inhibitors Failed to progress to clinical trials Neuropeptides Difficult chemistry; low specificity; little activity

Source: Hardman & Co Life Sciences Research

Opportunity for RPL554 RPL554 has significant potential because it offers a real alternative to existing therapies with its dual bronchodilatory/anti-inflammatory mechanisms of action in COPD. Given the size of Verona relative to the major players in this field, it is not surprising that management is concentrating its efforts onto specific areas of the market which are inadequately controlled by existing therapies.

Initially, RPL554 is being targeted as an add-on therapy for acute exacerbations of COPD whereby its bronchodilator action provides short-term symptom relief and its anti-inflammatory action might relieve the airway inflammation.

Given its multiple mode of action, RPL554 might be shown longer-term to have a role to play in this maintenance segment of the market. This would require clinical trials in large patient populations which are beyond the scope of the company at the present time. However, success in the acute setting will pave the way for a licensing deal with one of the major players and there is little doubt in our minds that RPL554 is very much on the radar screens of business development managers.

Cystic fibrosis Cystic fibrosis (CF) is an autosomal recessive disorder that affects approximately 1-in-3,000 Caucasian births, or 30,000 individuals in the US and 70,000 worldwide. It is caused by the presence of mutations of both copies (mother and father) of the gene responsible for the protein cystic fibrosis transmembrane conductance regulator (CFTR). CFTR is involved in the production of mucous, sweat and digestive fluids and secretions become very thick/viscous when this protein is not functioning properly.

CF mainly affects the lungs, but also impacts normal function of other organs such as the pancreas, liver, kidneys and intestine. It is a chronic condition associated with production of excessive quantities of thick sputum which leads to difficulties in breathing and frequent lung infections.

Discovery of the CF gene, isolation of CFTR protein and greater understanding of the molecular mechanisms behind the clinical expression of CF are being translated into newer treatments.

Verona Pharma plc 15

18 May 15

Health problems with cystic fibrosis

Source: Blausen gallery, 2014

We believe that new scientific findings, coupled with the commercial success of new CFTR modulating drugs will pave the way for considerably enhanced R&D effort in this area in the future.

Verona Pharma plc 16

18 May 15

Competitive Landscape New COPD drugs Given the daily incidence of patient hospitalisations and the number of deaths around the world caused by COPD, the need for better drugs is obvious. For most patients, current drug therapy is effective, safe and relatively inexpensive (many drugs off-patent and available generically). However, this statement presents a major hurdle in the development of new drugs.

Also, in general, patients still prefer to take drugs orally, whereas those for the control of COPD nearly always have to be taken by inhalation. This, in itself, presents a problem as hand-to-mouth co-ordination gets increasing difficult with age and is particularly difficult in patients who are having breathing difficulties. Even when drugs can be administered successfully in this way, the vast majority ends up at the back of the throat or is swallowed.

The approaches generally being taken by the established pharmaceutical players in the respiratory field are to find improved components of combination therapies. This is because they are seeking to protect their sales when patents expire and replace them with newer versions without dramatically increasing the cost. However, a completely new approach might be needed to identify a better new drug:

New drug opportunities

New classes of drug that are effective in poorly controlled COPD

A treatment that is as effective as ICS, but without the associated side effects from long-term Drugs that modify the course of the disease

Source: Hardman & Co Life Sciences Research

New bronchodilators Bronchodilators are important for preventing and relieving bronchoconstriction. The gold standards are the LABA – salmeterol (Serevent, GSK) and formoterol (Foradil, Novartis) – which work for over 12 hours and are complementary to inhaled corticosteroids. There are several ultra-long acting β-agonists (ultra-LABA) in development/recently launched which have a duration of action of >24hrs, allowing once daily dosing.

Indacaterol: Ultra LABA developed by Novartis for long-acting bronchodilation in COPD. It is approved in both EU (Onbrez) and the US (Arcapta) for once-daily medication via a dry-powder inhaler. It is also available in combination with the long-acting muscarinic antagonist (LAMA), glycopyrronium under the brand name Ultibro Breezhaler

Olodaterol: Inhaled ultra LABA developed for use alone (Striverdi); and under development in combination with tiotropium for long-acting bronchodilation/ prevention of exacerbations in COPD by Boehringer Ingelheim under the brand name Vivacito

Vilanterol: Ultra LABA developed by GlaxoSmithKline for the prevention of exacerbations in COPD only in combination with the corticosteroid, fluticasone. Approved in the US as Relvar Ellipta and in the UK as Breo Ellipta

Carmoterol: Ultra LABA under phase II/III development alone and in combination by Chiesi for the prevention of exacerbations in COPD

Verona Pharma plc 17

18 May 15

Novel anti-inflammatories Historically, ICS in combination with LABA have been used for the maintenance of COPD patients even though they were originally approved for controlling asthma. The modern approach is to use LABA in conjunction with LAMA, thereby providing the strongest bronchodilatory action with less focus on the need to treat any underlying inflammation. However, there is still very much a role to be played by anti-inflammatory drugs, which, if effective, could be used as a triple therapy with LABA and LAMA. This leads to the development of specific drugs that target the signal transduction pathways that amplify the inflammatory response with the hope of eliminating the side effect risk of corticosteroids.

Phosphodiesterase inhibitors PDE inhibitors are the most advanced of the non-steroidal anti-inflammatories, roflumilast (Daxas, Takeda), an oral PDE4 inhibitor, having been approved for the treatment of severe chronic COPD associated with chronic bronchitis in adults with a history of frequent exacerbations, and as add on to bronchodilator treatment. Being oral, its dose (0.5mg) is relatively high and associated with the traditional PDE4 side effects – insomnia, headache, nausea, abdominal pain. Consequently sales have been poor to date. Attempts to deliver PDE4 inhibitors by inhalation have lacked efficacy. Therefore, the new formulation of RPL554 which can be administered with higher doses that can reside for longer in the lungs is of great interest, especially when it is also coupled to the PDE3 bronchodilatory effects.

Kinase inhibitors Kinases play a critical role in regulating expression of inflammatory genes in respiratory disease, which suggests that inhibitors of this enzyme might be a useful approach for drug treatment. By way of example, the transcription factor, nuclear factor-κB (NF-κB) regulates many inflammatory genes that are abnormally expressed in asthma. In pre-clinical testing small molecule blockers of NF-κB enzymes did block inflammation, but none have progressed to the clinic.

Adhesion molecule blockade Another approach to inhibiting inflammation is to block the adhesion molecules that are involved in the movement of inflammatory cells from the blood into the airways. Small molecule inhibitors of late antigen-4 (VLA-4), which is implicated in the recruitment of eosinophils and T-cells, was shown to be effective in animal models, but this has not been replicated in asthma patients. The pan-selectin antagonist, bimosiamose, is in phase II development by Revotar. In patients with mild-to-moderate COPD, inhaled bimosiamose demonstrated a broad anti-inflammatory effect and reduced most of the evaluated sputum markers, notably interleukin-8.

PPARγ agonists Peroxisome proliferator-activated receptor γ agonists have a broad spectrum of anti-inflammatory effects, including inhibition of macrophages and T cells. Rosiglitazone, a PPARγ agonist gave a small improvement in lung function in smoking asthmatics in whom ICS were ineffective, but the response was insufficient to take the product forward.

Cytokine modulators Cytokines play an important role in conducting chronic inflammation and in remodelling airway structure. As such, they have received considerable attention as targets for blockade in asthma and COPD. The science is extremely complicated with over 50 cytokines having been implicated in the inflammatory process resulting in asthma. While the list is almost endless, the following have received the greatest attention from drug companies: Interleukin(IL)-4, IL-5, IL-10, IL-13, tumour necrosis factor (TNF)-α and granulocyte-macrophage colony-stimulating factor (GM-CSF). No new drugs for treatment of COPD are anticipated from these targets over the next three years.

Verona Pharma plc 18

18 May 15

New corticosteroids Although ICS are very effective in the chronic treatment of asthma, they do not treat the underlying inflammation in COPD. Specifically the neutrophilic inflammatory infiltrate seen in the lungs of patients with COPD is not effected by ICS. All currently marketed ICS are absorbed from the lungs and thus have the potential to cause systemic side effects, particularly with long-term use. This has led to a concerted effort to find safer ICS, with reduced oral bioavailability (from swallowed drug), reduced absorption from the lungs and/or inactivation in the circulation. However, little progress has been made in improving what is currently available.

Summary In conclusion, of all the anti-inflammatory approaches, the only one to have resulted in a marketed product for COPD to date has been via blockade of PDE4 with an oral formulation. Therefore, there is precedent in the approach being taken by Verona with RPL554, which has the added benefits of acting locally in the lung in higher doses via nebuliser coupled with a dual bronchodilatory/anti-inflammatory mode of action.

Selective new drugs for COPD Drug Developer Aim Development status

Duaklir AstraZeneca Maintenance EU launch underway PT003 AstraZeneca Maintenance LAMA/LABA; +ve top-line Phase III

benralizumab AstraZeneca Maintenance MAb in Phase II/III due to file 2018 AZD2115 AstraZeneca Maintenance MABA in Phase II since 2012 AZD7624 AstraZeneca Maintenance Inhaled P38 inhibitor in Phase II (2014) BIO-11006 BioMarck Pharma Maintenance Phase II; no new since 2011 Striverdi Boeh.Ingelheim Maintenance LABA; Launched EU & US EP-101 Sunovion Exacerbation LAMA nebuliser add-on; last news 2012 vilanterol GlaxoSmithKline Maintenance Inhaled LABA; Phase III mepolizumab GlaxoSmithKline Maintenance Filed EU & FDA Nov 2014 Anoro Ellipta GlaxoSmithKline Maintenance LAMA/LABA; launched US & EU 2014 losmapimod GlaxoSmithKline Maintenance P38 kinase inhibitor; Phase II MN-221 MediciNova/Kissei Exacerbation i/v SABA; Phase I for out-licensing BCT197 Novartis Maintenance P38 kinase inhibitor; Phase II QVA149 Novartis Maintenance LAMA/LABA; Filed US & EU QMF149 Novartis Maintenance LAMA/ICS tetomilast Otsuka Maintenance Oral PDE4 inhibitor; Phase II PUR0200 Pulmatrix Maintenance DPI; Phase I data May 2014 TD-4208 Theravance Exacerbation LAMA; Phase II

LABA = long acting β-agonist; SABA = short-acting β-agonist; LAMA – long acting muscarinic antagonist; MABA – short-acting muscarinic antagonist; MAb – monoclonal antibody.

This list is not comprehensive Source: Hardman & Co Life Sciences Research

Abundantly clear from the table above is the fact that most companies are focusing their attention on developing drugs for the maintenance of COPD over the long-term. This makes commercial sense, provided that the company has deep enough pockets to undertake large-scale Phase III clinical trials. The strategy of Verona is to target, initially, the much smaller, but still very large (~$3.2bn), segment of the market that treats an acute exacerbation in patients with COPD, where it has, clearly, much less competition.

Verona Pharma plc 19

18 May 15

New cystic fibrosis drugs

Vertex Pharmaceuticals The landscape for new drugs to treat cystic fibrosis is dominated by Vertex Pharmaceuticals. This company has the only marketed drug, Kalydeco (chemical name ivacaftor) which targets CFTR and close work with regulatory authorities is expanding its usage all the time in patients with new types of gating mutations (low function of CFTR). Consequently, sales of this drug will comfortably exceed $500m in 2015 even though it is only available to be used in about 10% of CF patients.

In addition, Vertex has filed (11th Jan 2015) a combination treatment – lumacaftor + ivacaftor – for use in CF patients aged 12+ who have two copies of a specific mutation (the F580del mutation), which has been given a priority review date of 5th July 2015. This combination is also under review by the European regulator.

Vertex is also conducting a 12-week phase II study using ivacaftor in combination with VX-661 in CF patients which have two copies of the F508del mutation. Enrolment was completed in October 2014 in 40 patients (20 drug treated vs 20 placebo). The primary endpoint is safety with the secondary endpoint being evaluation of the pharmacokinetic profile. Results are due in 1Q 2015. As soon as this data is available, and assuming the outcome is positive, Vertex will initiate a phase III programme consisting of four studies across the world involving 1270 patients. (Details can be found on Vertex’s website: http://investors.vrtx.com/releasedetail.cfm?ReleaseID=890626).

PTC Therapeutics Ataluren is an oral therapy approved in the EU (April 2014) for the treatment of Duchenne muscular dystrophy under the brand name, Translarna. Ataluren enables the formation of functional proteins in cases on nonsense mutations. However, PTC Therapeutics has also commenced a 48-week Phase III international, multi-centre, randomised, double-blind placebo-controlled efficacy trial in 208 patients (104 drug treated + 104 placebo) with nonsense mutation cystic fibrosis patients, which is due to complete in November 2016.

Cystic fibrosis – Where treatments are being targeted Nonsense mutations cause the most severe form of cystic fibrosis

Source: PTC Therapeutics Presentation, March 2015

Galápagos Pharmaceuticals Galapagos claims to have three putative drugs for cystic fibrosis all of which have an action on CFTR. All three drugs have been partnered with AbbVie. GLPG1837 is a CFTR potentiator in Phase II clinical trials with Phase IIa results due in 3Q’15. GLPG2222 acts at the CFTR Corrector1 site and is in Phase I safety studies due to complete in 1H’16. The third candidate acts at the CFTR Corrector2 site, but is at the pre-clinical development stage with a lead candidate due to be identified during 1H’15.

Verona Pharma plc 20

18 May 15

Commercial Market The commercial market for respiratory drugs has altered significantly over the years. 20 years ago, it was worth about $7bn and split equally between short-acting β-agonists used treat an asthma attack, inhaled corticosteroids to prevent attacks and anti-allergy drugs for the prevention and treatment of allergic rhinitis. A combination of greater focus on the need to prevent asthma, coupled with more acceptance of the use of low-dose inhaled corticosteroids, and the loss of patent protection on allergy drugs has completely changed the market.

Key facts In 2014, the global market for respiratory drugs was estimated to be worth $33bn and

there has been no growth in the market for three years, largely due to the loss of patent protection recently on major products

Around 10% – about $3.2bn – of the world market is for drugs used to treat an exacerbation of COPD or an attack of asthma. This segment of the market is dominated by the primary drugs of choice, the SABA salbutamol alone or in combination with a short-acting anti-muscarinic antagonist (Combivent)

$26bn is spent each year on drugs used to prevent an outbreak of asthma or COPD, with the top three drugs accounting for $15.6bn (60%) of these sales

The major players that dominated the market 20 years ago remain the same today – GlaxoSmithKline (GSK), Boehringer Ingelheim, AstraZeneca (AZN) – but 11% of the market is now taken by generics

Commercial success can be achieved with add-on therapies for patients where mainstream products fail to control exacerbations – Singulair (anti-inflammatory peak sales $5.5bn in 2011); Xolair (biological anti-allergy, peak sales $1.8bn current)

There is room in the market for new entrants provided they are add-on therapies and offer a different approach to the gold-standard approaches currently available

Global respiratory market

2014 Global market: $33.0bn

Source: Company reports; Hardman & Co Life Sciences Research

Rescue10%

Prevention78%

Rhinitis12%

Verona Pharma plc 21

18 May 15

Verona would be focusing initially on the $3.2bn segment of the market shown in the chart under the label “rescue”, which is usually in hospitalised patients, used once an exacerbation of COPD (or an asthma attack) has occurred. Slight changes in the management of such patients means that they might be treated by specialist nurses in the home environment or in specialised clinics.

Market by individual drug The biggest respiratory drug by global sales is Seretide/Advair (GSK), the LABA/ICS combination, which sold $6.8bn in 2014. Sales are declining in the US because of competition and pricing pressure. The second drug is Spriva (Boeh. Ingelheim), with sales of ~$5bn, which is targeted specifically at COPD maintenance. Its success, particularly in the US, can also be attributed, in part, to that market’s aversion to inhaled corticosteroids. The mainstays of the rescue market, Ventolin (GSK) and Combivent (BI), both have sales of ~$1bn per annum.

Global respiratory market – By product

LABA = long acting β-agonist; SABA = short-acting β-agonist; LAMA = long-acting muscarinic antagonist; SAMA = short-acting muscarinic antagonist; ICS = inhaled corticosteroid; A-I = anti-inflammatory

Source: Company reports; Hardman & Co Life Sciences Research

Drug ($m) Type 2010 2011 2012 2013 2014 2015E

Seretide/Advair LABA/ICS 7,946 8,118 7,998 8,249 6,830 4,800

Spiriva LAMA 3,793 4,385 4,578 4,717 4,950 5,148

Symbicort LABA/ICS 2,746 3,148 3,194 3,483 3,801 4,029

Xola i r A-I 983 1,158 1,256 1,465 1,843 2,108

Fl ixotide/Flovent ICS 1,243 1,304 1,235 1,245 1,157 983

Nasonex ICS 1,219 1,286 1,268 1,355 1,099 824

Ventol in SABA 807 966 1,000 1,040 1,096 1,140

Singula i r LTA 4,987 5,479 3,853 1,196 1,092 983

Pulmicort ICS 872 892 866 867 946 1,003

Combivent SABA/SAMA 963 1,065 1,135 944 800 680

Onbrez/Arcapta LABA 33 103 134 192 220 224

Serevent LABA 311 292 230 202 178 151

Salbutamol SABA 533 725 780 780 789 797

Others 2,559 2,615 2,970 3,015 3,056 3,080

COPD/asthma 30,045 32,494 31,011 29,419 28,876 27,291

Growth 17% 8% -5% -5% -2% -5%

Clari tin/Clarinex 1,605 1,446 1,169 910 851 766

Al legra/Tel fast 804 807 1,026 831 720 648

Avamys/Veramyst 298 387 390 389 392 396

Zyrtec/Xyza l 456 512 485 333 330 313

Others 1,997 1,843 1,769 1,798 1,811 1,787

Allergy/rhinitis 5,160 4,994 4,838 4,262 4,104 3,910

Growth 11% -3% -3% -12% -4% -5%

Respiratory market 35,204 37,488 35,849 33,681 32,979 31,201

Growth 16% 6% -4% -6% -2% -5%

Verona Pharma plc 22

18 May 15

Looking at just the maintenance segment of the market ($24.5bn), 47% of sales are derived from combination therapies, which generally combine a LABA with an inhaled corticosteroid. However, the vast majority (estimated at 80%) of these sales will be for asthma rather than COPD.

Combination therapies Trade name Company Long-acting β-agonist 2nd component

Seretide/Advair GlaxoSmithKline salmeterol fluticasone (ICS) Symbicort AstraZeneca formoterol budesonide (ICS)

SAMA = short-acting muscarinic antagonist; ICS – inhaled corticosteroid Source: Hardman & Co Life Sciences Research

Market by company The same major players still dominate the current market compared to 10, 20 and 30 years ago. GSK remains world #1 and Boehringer Ingelheim is world #2. In some years, Merck & Co (either alone and today with Schering-Plough) has been a major force, with Singulair (anti-inflammatory in mild-to-moderate asthma) and Claritin (anti-allergy), until the expiration of their patents, since when Merck has slipped back in the ranking.

Roche is a new entrant, with the specialist anti-inflammatory, Xolair (also marketed by Novartis in some territories).

Global respiratory market – By company

Source: Company reports; Hardman & Co Life Sciences Research

Novartis is expanding its presence in the market with a number of recent launches. Today, it is probably #4 in the world. However, the majority of its respiratory sales are generic versions of older products and sold through its Sandoz subsidiary which does not declare sales by drug/therapeutic activity.

New COPD drugs The market place is in the process of change. Over the last two years a number of new bronchodilator drugs have been launched alone and in combination, specifically targeting COPD. The new β-agonist component tends to be ultra long-acting, leading to a one daily inhalation. There has also been launch of a number of long-acting muscarinic antagonists. In several cases they have been launched also in combination.

The mind-set of the industry is apparent, however, from GSK’s launch of Breo/Relvar Ellipta for COPD. This is a combination of an ultra LABA with a traditional corticosteroid. Even though the drug has been approved by regulators specifically for COPD, this combination is better suited to asthma. The problem for GSK is that Advair/Seretide is facing severe competition and loses patent in the US in 2016 and, for historic reasons when there was little else available, we believe about 20% of sales are for its use in COPD patients. Therefore, GSK is looking to protect these sales with Breo Ellipta.

Company ($m) Key drug 2010 2011 2012 2013 2014 2015E

GlaxoSmithKl ine Advair 11,190 11,706 11,556 11,192 10,157 8,200

Boeh. Ingelheim Spiriva 4,756 5,451 5,713 5,661 5,800 5,900

AstraZeneca Symbicort 4,099 4,468 4,415 4,677 5,063 5,280

Merck & Co Singula i r 8,019 8,417 6,475 3,645 3,212 2,917

Roche Xola i r 614 680 752 852 1,066 1,215Other/Generics 5,146 5,207 5,408 5,914 5,936 5,759

Total 35,204 37,489 35,849 33,682 32,979 31,201

Verona Pharma plc 23

18 May 15

New drugs directed at COPD

LABA = long acting β-agonist; SABA = short-acting β-agonist; LAMA = long-acting muscarinic antagonist; ICS = inhaled corticosteroid Source: Company reports; Hardman & Co Life Sciences Research

Increased use of nebulisers Because our commercial data is all based on ex-factory sales reported by companies, it is very difficult to separate between asthma and COPD. In some ways this is exactly how the market worked until about 2000 – asthmatic patients were prescribed prevention/rescue drugs and COPD patients received, in addition, antibiotics to treat underlying lung infections. However, around the millennium, there was an increasing awareness of COPD, particularly in the older generation who had poorer hand mouth co-ordination for using metered dose inhalers. Therefore greater attention was focused on the need to use alternative forms of administration to get the drugs into the lungs and this has resulted in significantly increased use of nebulisers.

US sales of Ventolin

Source: GlaxoSmithKline; Hardman & Co Life Sciences Research

Drug LABA LAMA ICS Marketer 2011 2012 2013 2014 2015E

Combination therapies

Ultibro indacaterol glycopyrronium Novartis 0 0 6 118 248

Breo/Relvar El l ipta vi lanterol fluticasone GSK 0 0 13 109 220

Anoro El l ipta vi lanterol umecl idinium GSK 0 0 0 27 175

Duakl i r formoterol acl idinium AZN 0 0 0 0 40

QVA149 indacaterol glycopyrronium Novartis 0 0 0 0 0

indacaterol ipratropium B.Ingelheim 0 0 0 0 0

PT003 formoterol glycopyrrolate AZN 0 0 0 0 0

Total combinations 0 0 19 253 683

Single drugs

Spiriva tiotropium B.Ingelheim 4,385 4,578 4,717 4,950 5,148

Onbrez/Arcapta indacaterol Novarti s 103 134 192 220 224

Ekl i ra/Tudorza acl idinium AZN 0 35 112 147 165

Seebri glycopyrronium Novartis 0 3 58 146 212

Incruse El l ipta umecl idinium GSK 0 0 0 1 40

Total singles 4,488 4,750 5,079 5,464 5,789

0

100

200

300

400

500

600

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

US s

ales

($m

)

Verona Pharma plc 24

18 May 15

In our opinion, some evidence for this can be demonstrated by the sales of Ventolin (GSK) in the US. This drug, available as a tablet, metered dose inhaler (MDI) and liquid formulations, had steady sales in the US throughout the nineties, peaking at $279m in 1993. When the patent expired in 1996, sales of the oral formulation fell quickly followed by a slower decline in the MDI, such that by 2003, US sales were only $6m.

However, two factors have been behind the resurgence in sales of Ventolin in the US, to the extent that sales exceeded $500m in 2014 for the first time. First, when CFCs were abolished as a propellant, GSK introduced an MDI driven by HFA at a new price which was patent protected once again; secondly, greater awareness of COPD coupled with the greater use of nebulisers which require an aqueous solution formulation, has resulted in increased use of liquid formulations of salbutamol, which has less generic competition compared to tablet formulations.

Taking the whole respiratory market, irrespective of whether drug usage is for prevention or rescue therapy, the use of nebulisers remains small relative to the use of MDI and DPI. Rescue therapy in hospitalised patients is invariably administered drugs via nebulisers.

Despite changed clinical practice and introduction of new drugs, COPD patients remain inadequately controlled and still have exacerbations, requiring rescue therapy. Even with good rescue drugs administered via nebulisers, there is still a role for add-on therapies that offer something different, such as RPL554, which offers increased bronchodilation (via PDE3) coupled with anti-inflammatory effects (via PDE4).

In the event that RPL554 is licensed to a major player for development as a maintenance therapy, it would be formulated as a dry powder for use in a DPI or a separate formulation for use in a pMDI. Preliminary studies show that the drug can be delivered via the main types of devices commonly used for inhalation therapy.

Cystic fibrosis The market for drugs used in the treatment of cystic fibrosis is very complex. Patients tend to use a wide range of drugs and health supplements. To give readers an understanding of potential sales, we have identified the following drugs that have been launched commercially specifically for cystic fibrosis. Just these three specialist drugs creates a $1.5bn worldwide market annually.

Pulmozyme was launched by Roche in 1994 and regularly sells around $0.5bn per annum, with cumulative sales to date of $5.8bn. It is a recombinant engineered enzyme designed to break down the viscous sputum that is common in cystic fibrosis patients. To reach the required site of action, it is administered via a nebuliser

Kalydeco is approved for the treatment of cystic fibrosis in patients aged 6+ years who have specific mutations of the CFTR gene. Vertex is also looking at using Kalydeco in combination with other CFTR drugs to expand its indications within the CF community

Tobi was launched by Novartis in 2006 and regularly sells around $300m per annum, with cumulative sales to date of $2.3bn. It is a specialist antibiotic indicated for use against Pseudomonas aeruginosas, common in cystic fibrosis patients and is administered via a nebuliser

Cystic fibrosis – By product

Source: Company reports; Hardman & Co Life Sciences Research

Drug ($m) Key drug 2010 2011 2012 2013 2014 2015E

Pulmozyme Roche 492 555 572 617 652 692

Kalydeco Vertex 0 0 172 371 464 580

Tobi Novarti s 279 296 317 387 281 225

Total 771 851 1,061 1,375 1,397 1,496

Verona Pharma plc 25

18 May 15

Financials & Investment Case History In April 2004, Rhinopharma Limited was established in Vancouver for the discovery and development of new drugs for the treatment of allergic rhinitis (hay fever) and other chronic inflammatory diseases of the respiratory system, such as asthma and COPD. In August 2006, the entire issued share capital of Rhinopharma was acquired for £1.52m, satisfied by the issue of 38.0m shares @4p per share in an AIM listed shell company, Isis Resources plc, and renamed Verona Pharma plc. Today, Verona is much the same as when it was set up. Although its strategy remains focused on respiratory disease, it has been modified slightly with greater emphasis on respiratory disease where there is a clear unmet medical need and a relatively fast development and regulatory pathway to market.

Capital increases Simultaneously to Rhinopharma being acquired by Isis, management undertook a share placing to provide sufficient working capital to fund the R&D spend over the following 18 months. This involved the issue of 51.1m shares @4p a share to raise ca£2m and valued the newly named Verona Pharma at £5.8m.

To date, Verona has raised £29.8m to fund its development programme and get the company where it is today. This has been achieved through five significant placings, with the last accounting for ~50% of the total capital raised. At the end of 2014, the company has stated that there is just under £10m cash in the balance sheet.

Of the £18m invested to date, £10m had been spent on R&D, with the other £8m covering general running costs and administration typical for a quoted company.

Capital increases

Source: Verona Pharma; Hardman & Co Life Sciences Research

Date Shares Price Raised Shares o/s Valuation Comment(m) (p) (£m) (m) (£m)

2006 55.2 Is i s Resources plcSep-06 38.0 4.0 1.52 93.2 3.73 Reverse acquis i tion of Rhinopharm LtdOct-06 51.1 4.0 2.04 144.3 5.77 Placing at 4p per shareDec-07 2.5 4.0 0.10 146.8 5.87 Placing at 4p per shareJan-08 58.0 4.0 2.32 204.8 8.19 Placing at 4p per shareApr-08 0.1 2.0 0.00 204.9 4.10 Exercise of optionsMay-08 1.3 2.0 0.03 206.1 4.12 Exercise of optionsMay-08 0.2 2.0 0.00 206.3 4.13 Exercise of optionsJun-08 0.9 2.0 0.02 207.2 4.14 Exercise of optionsJul -08 7.0 2.0 0.14 214.3 4.29 Exercise of optionsJul -08 1.0 2.5 0.03 215.3 5.38 Exercise of optionsMay-09 0.2 4.1 0.01 215.5 8.89 Issued in l ieu of cash for service providerDec-09 17.7 13.0 2.30 233.2 30.31 Placing at 13p per shareJan-10 5.6 13.0 0.72 238.7 31.04 EIS/VCT lacing at 13p per shareNov-10 1.2 5.0 0.06 239.9 12.00 Exercise of options at 5pSep-11 2.3 5.5 0.13 242.2 13.32 Exercise of options at 5p & 6pDec-11 65.0 5.0 3.25 307.2 15.36 Placing at 4p per shareJan-13 29.0 4.0 1.16 336.2 13.45 Placing at 4p per shareOct-13 36.4 2.2 0.80 372.6 8.20 Placing at 2.2p per shareMar-14 637.3 2.2 14.02 1009.9 22.22 Placing, Subscription & Open offer at 2.2pTotal 29.84

Verona Pharma plc 26

18 May 15

Share price performance

Source: Fidessa

Verona has had an eventful year since it raised new capital in March 2014. Initially, it suffered a setback when its putative drug VRP700 failed to reach its primary end-point in a clinical trial for cough. There was some excitement in October 2014 when the company published early findings on the use of RPL554 in cystic fibrosis and received grant funding to forward this project from the Cystic Fibrosis Foundation. However, the most significant move came when the company re-started the RPL554 clinical programme with the new formulation, with the latest rise following publication of the excellent phase I safety and pharmacokinetic data.

Share capital The company has 1009.9m shares issued, with Arthurian (Wales Life Sciences Fund) being the largest shareholder.

Share capital – May 2015

Source: Verona Pharma

Financial statements The financial statements of Verona are fairly straight-forward and dominated by two figures. First, the amount of cash being invested into R&D to support the clinical trial programme that is expected, ultimately, to drive value. Secondly, the ongoing SG&A costs to execute on the company’s strategy. These, in turn, drive the cashflow and determine the point at which management needs to raise more capital.

Directors2.9%

Arthurian20.8%

Aviva18.0%

Vivo Capital6.4%

Fidelity7.6%

Others44.4%

Verona Pharma plc 27

18 May 15

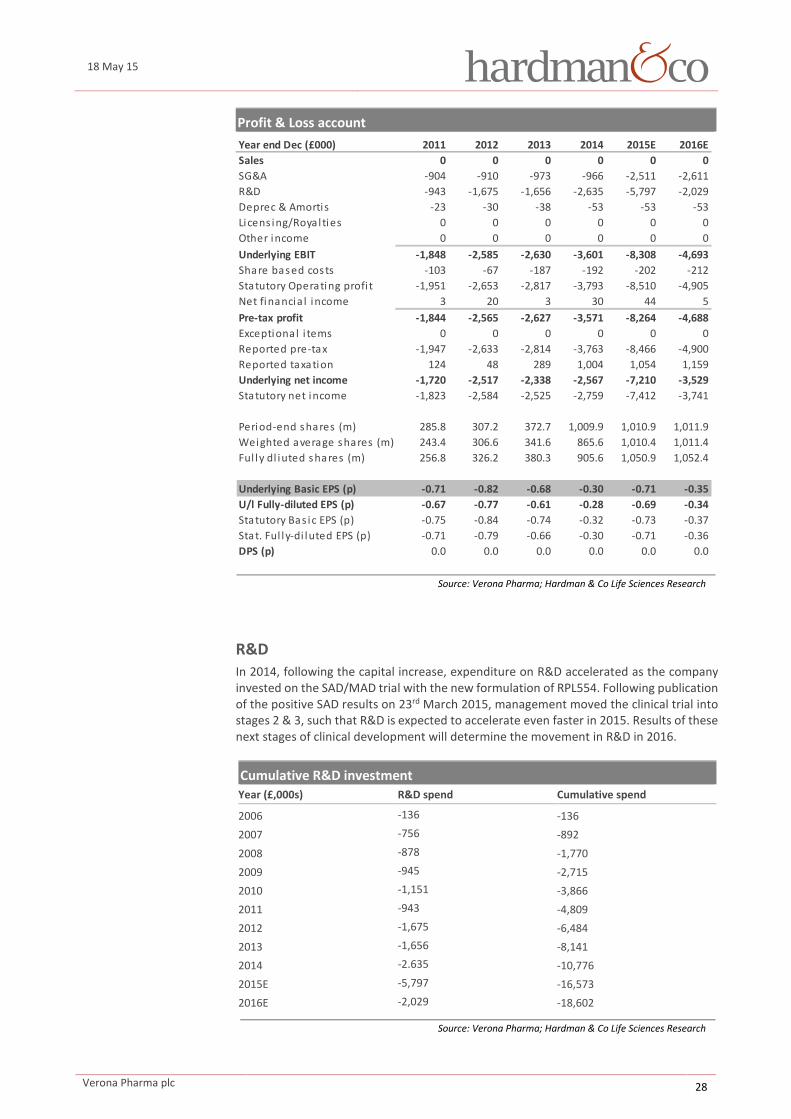

Profit & Loss account

Source: Verona Pharma; Hardman & Co Life Sciences Research

R&D In 2014, following the capital increase, expenditure on R&D accelerated as the company invested on the SAD/MAD trial with the new formulation of RPL554. Following publication of the positive SAD results on 23rd March 2015, management moved the clinical trial into stages 2 & 3, such that R&D is expected to accelerate even faster in 2015. Results of these next stages of clinical development will determine the movement in R&D in 2016.

Cumulative R&D investment Year (£,000s) R&D spend Cumulative spend

2006 -136 -136 2007 -756 -892 2008 -878 -1,770 2009 -945 -2,715 2010 -1,151 -3,866 2011 -943 -4,809 2012 -1,675 -6,484 2013 -1,656 -8,141 2014 -2.635 -10,776 2015E -5,797 -16,573 2016E -2,029 -18,602

Source: Verona Pharma; Hardman & Co Life Sciences Research

Year end Dec (£000) 2011 2012 2013 2014 2015E 2016ESales 0 0 0 0 0 0SG&A -904 -910 -973 -966 -2,511 -2,611R&D -943 -1,675 -1,656 -2,635 -5,797 -2,029Deprec & Amortis -23 -30 -38 -53 -53 -53Licens ing/Royal ties 0 0 0 0 0 0Other income 0 0 0 0 0 0Underlying EBIT -1,848 -2,585 -2,630 -3,601 -8,308 -4,693Share based costs -103 -67 -187 -192 -202 -212Statutory Operating profi t -1,951 -2,653 -2,817 -3,793 -8,510 -4,905Net financia l income 3 20 3 30 44 5Pre-tax profit -1,844 -2,565 -2,627 -3,571 -8,264 -4,688Exceptional i tems 0 0 0 0 0 0Reported pre-tax -1,947 -2,633 -2,814 -3,763 -8,466 -4,900Reported taxation 124 48 289 1,004 1,054 1,159Underlying net income -1,720 -2,517 -2,338 -2,567 -7,210 -3,529Statutory net income -1,823 -2,584 -2,525 -2,759 -7,412 -3,741

Period-end shares (m) 285.8 307.2 372.7 1,009.9 1,010.9 1,011.9Weighted average shares (m) 243.4 306.6 341.6 865.6 1,010.4 1,011.4Ful ly dl iuted shares (m) 256.8 326.2 380.3 905.6 1,050.9 1,052.4

Underlying Basic EPS (p) -0.71 -0.82 -0.68 -0.30 -0.71 -0.35U/l Fully-diluted EPS (p) -0.67 -0.77 -0.61 -0.28 -0.69 -0.34Statutory Bas ic EPS (p) -0.75 -0.84 -0.74 -0.32 -0.73 -0.37Stat. Ful ly-di luted EPS (p) -0.71 -0.79 -0.66 -0.30 -0.71 -0.36DPS (p) 0.0 0.0 0.0 0.0 0.0 0.0

Verona Pharma plc 28

18 May 15

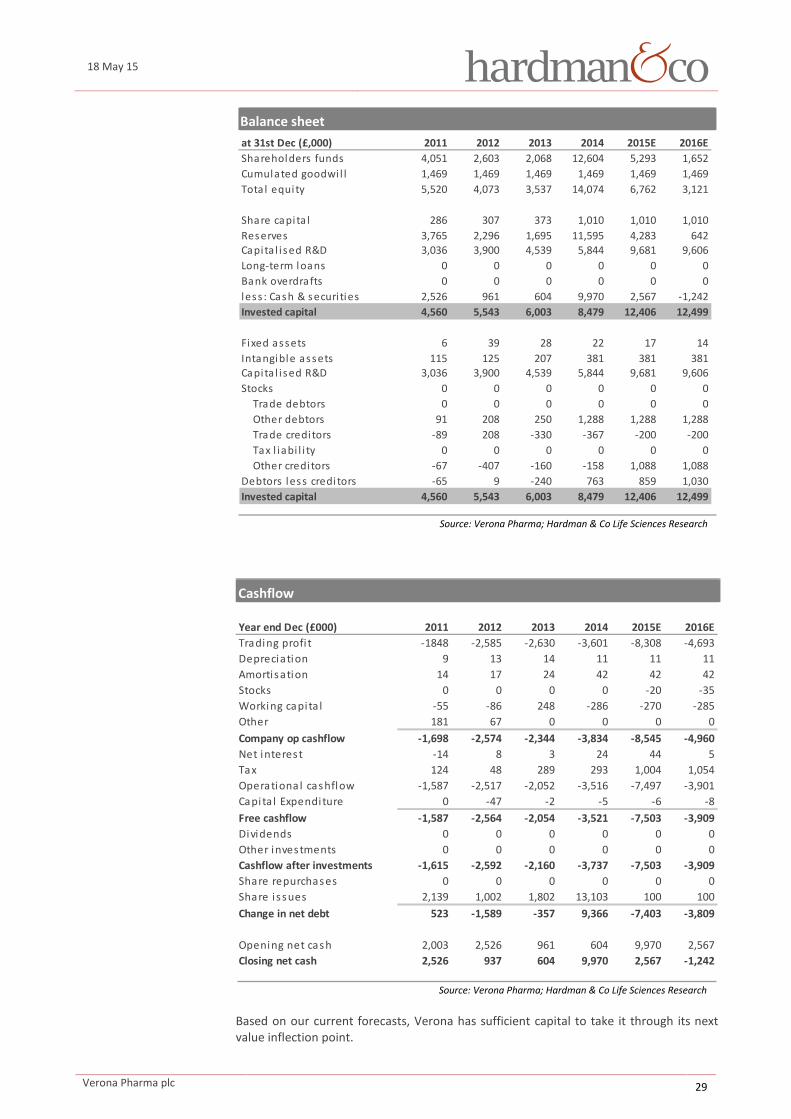

Balance sheet

Source: Verona Pharma; Hardman & Co Life Sciences Research

Cashflow

Source: Verona Pharma; Hardman & Co Life Sciences Research

Based on our current forecasts, Verona has sufficient capital to take it through its next value inflection point.

at 31st Dec (£,000) 2011 2012 2013 2014 2015E 2016EShareholders funds 4,051 2,603 2,068 12,604 5,293 1,652Cumulated goodwi l l 1,469 1,469 1,469 1,469 1,469 1,469Tota l equity 5,520 4,073 3,537 14,074 6,762 3,121

Share capi ta l 286 307 373 1,010 1,010 1,010Reserves 3,765 2,296 1,695 11,595 4,283 642Capita l i sed R&D 3,036 3,900 4,539 5,844 9,681 9,606Long-term loans 0 0 0 0 0 0Bank overdrafts 0 0 0 0 0 0less : Cash & securi ties 2,526 961 604 9,970 2,567 -1,242Invested capital 4,560 5,543 6,003 8,479 12,406 12,499

Fixed assets 6 39 28 22 17 14Intangible assets 115 125 207 381 381 381Capita l i sed R&D 3,036 3,900 4,539 5,844 9,681 9,606Stocks 0 0 0 0 0 0 Trade debtors 0 0 0 0 0 0 Other debtors 91 208 250 1,288 1,288 1,288 Trade credi tors -89 208 -330 -367 -200 -200 Tax l iabi l i ty 0 0 0 0 0 0 Other credi tors -67 -407 -160 -158 1,088 1,088Debtors less credi tors -65 9 -240 763 859 1,030Invested capital 4,560 5,543 6,003 8,479 12,406 12,499

Year end Dec (£000) 2011 2012 2013 2014 2015E 2016ETrading profi t -1848 -2,585 -2,630 -3,601 -8,308 -4,693Depreciation 9 13 14 11 11 11Amortisation 14 17 24 42 42 42Stocks 0 0 0 0 -20 -35Working capi ta l -55 -86 248 -286 -270 -285Other 181 67 0 0 0 0Company op cashflow -1,698 -2,574 -2,344 -3,834 -8,545 -4,960Net interest -14 8 3 24 44 5Tax 124 48 289 293 1,004 1,054Operational cashflow -1,587 -2,517 -2,052 -3,516 -7,497 -3,901Capita l Expenditure 0 -47 -2 -5 -6 -8Free cashflow -1,587 -2,564 -2,054 -3,521 -7,503 -3,909Dividends 0 0 0 0 0 0Other investments 0 0 0 0 0 0Cashflow after investments -1,615 -2,592 -2,160 -3,737 -7,503 -3,909Share repurchases 0 0 0 0 0 0Share i ssues 2,139 1,002 1,802 13,103 100 100Change in net debt 523 -1,589 -357 9,366 -7,403 -3,809

Opening net cash 2,003 2,526 961 604 9,970 2,567Closing net cash 2,526 937 604 9,970 2,567 -1,242

d hfl / h ( )

Verona Pharma plc 29

18 May 15

SG&A Again, with the increased funding, the company was able to strengthen its executive and operational management team. Notable additions have been the CFO and Chief Medical Officer. A Chairman with greater pharmaceutical experience was appointed in November 2014. Also, as part of the funding arrangement with the Wales Life Sciences Fund, the company moved its registered office to Cardiff and established a new London base. All of these changes added significantly to the underlying SG&A costs of the company, particularly in 2H’14. A full year effect of this will be seen in 2015.

Tax credits R&D investment in the UK results in tax credits form the government. As the company makes increased investment in R&D, so the tax credits, payable in arrears, will increase. For 2015 and 2016, the tax credits are calculated to be just over £1m per annum.

Valuation Our usual approach to valuing biopharmaceutical companies is to prepare detailed discounted cashflow analyses of key products through to patent expiry and then to risk-adjust the NPV based upon industry standards for the probability of the product reaching the market. However, in the case of Verona, beyond its strategy to fast-track commercialisation by developing nebulised RPL554 for the acute (hospital) setting, the company’s principal strategy is to license-out the technology and receive eventually potential milestones and royalties – there is simply insufficient information to construct such an analysis. Therefore, the valuation of Verona becomes more of an art than a science.