Embed Size (px)

Citation preview

The African Export Import Bank(Established pursuant to the Agreement for the Establishment of the African Export-Import Bank, signed in

Abidjan, Côte D’Ivoire, 8 May 1993)

This document (the “Registration Document”) has been approved by the United Kingdom Financial Conduct Authority(the “FCA”), as competent authority under Regulation (EU) 2017/1129 (the “Prospectus Regulation”). The FCA onlyapproves this Registration Document as meeting the standards of completeness, comprehensibility and consistency imposedby the Prospectus Regulation. Such approval should not be considered as an endorsement of the issuer that is the subject ofthis Registration Document. This document is a Registration Document relating to the Bank prepared in accordance withthe Prospectus Regulation Rules (the “Prospectus Regulation Rules”) of the FCA made under section 73A of the FinancialServices and Markets Act 2000 (“FSMA”).This Registration Document may be combined with a securities note and summary to form a prospectus in accordance withthe Prospectus Regulation Rules. A prospectus is required before an issuer can offer transferable securities to the public orrequest the admission of transferable securities to trading on a regulated market. However, this Registration Document,where not combined with the securities note and summary to form a prospectus, does not constitute an offer or invitation tosell or issue, or a solicitation of an offer or invitation to purchase or subscribe for, any securities in the Bank in anyjurisdiction, nor shall this Registration Document alone (or any part of it), or the fact of its distribution, form the basis of,or be relied upon in connection with, or act as any inducement to enter into, any contract or commitment whatsoever withrespect to any offer or otherwise. This Registration Document should be read and construed with any amendment orsupplement hereto, and for a particular issue of securities in conjunction with any applicable prospectus for the purposes ofthe Prospectus Regulation.No representation or warranty, express or implied, is made and no responsibility or liability is accepted by any person otherthan the Bank, as to the accuracy, completeness, verification or sufficiency of the information contained herein, and nothingin this Registration Document may be relied upon as a promise or representation in this respect, as to the past or future. Noperson is or has been authorised to give any information or to make any representation not contained in or not consistentwith this Registration Document and, if given or made, such information or representation must not be relied upon ashaving been authorised by the Bank. Without limitation, the contents of the website of the Bank do not form part of thisRegistration Document and information contained therein should not be relied upon by any person. The delivery of thisRegistration Document shall not, under any circumstances, create any implication that there has been no change in thebusiness or affairs of the Bank since the date of this Registration Document or that the information contained herein iscorrect as of any time subsequent to its date.

The date of this Registration Document is 9 October 2019.

Important Notice

The distribution of this Registration Document in certain jurisdictions may be restricted by law. Other than in the UnitedKingdom, no action has been taken or will be taken to permit the possession or distribution of this Registration Documentin any jurisdiction where action for that purpose may be required or where doing so is restricted by law. In the UnitedStates or to U.S. persons (“U.S. Persons”), as defined in Regulation S (“Regulation S”) of the U.S. Securities Act of 1933,as amended (the “Securities Act”)) (wherever located), you may not distribute this Registration Document or make copiesof it without the Bank’s prior written consent other than to people you have retained to advise you in connection with thisRegistration Document, or persons reasonably believed by the Bank to be qualified institutional buyers (“QIBs”), as definedin Rule 144A (“Rule 144A”) under the U.S. Securities Act of 1933, as amended (the “Securities Act”), that are alsoqualified purchasers (“QPs”) as defined in section 2(a)(51) of the U.S. Investment Company Act of 1940, as amended (the“Investment Company Act”). Accordingly, neither this Registration Document nor any advertisement nor any offeringmaterial may be distributed or published in any jurisdiction, other than in the United Kingdom, except under circumstancesthat will result in compliance with any applicable laws and regulations. Persons into whose possession this RegistrationDocument comes should inform themselves about and observe any such restrictions. Any failure to comply with suchrestrictions may constitute a violation of the securities laws of any such jurisdiction.Any securities referred to in this Registration Document have not been, and will not be, registered under the Securities Actor with any securities regulatory authority of any state of the United States, and may not be offered or sold (i) within theUnited States, except to persons reasonably believed to be QIBs that are also QPs by certain U.S. selling agents of theManagers in reliance on Rule 144A under the Securities Act or pursuant to another exemption from, or in a transaction notsubject to, the registration requirements under the Securities Act or (ii) outside the United States except to institutionalinvestors that are not U.S. Persons in “offshore transactions” as defined in, and in reliance on Rule 903 or 904 ofRegulation S. Any securities referred to in this Registration Document have not been and will not be registered under theapplicable securities law of Canada, Australia, South Africa or Japan and, subject to certain exceptions, may not be offeredor sold within Canada, Australia, South Africa or Japan or to any national, resident or citizen of Canada, Australia, SouthAfrica or Japan.

TABLE OF CONTENTS

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

IMPORTANT INFORMATION ABOUT THIS REGISTRATION DOCUMENT . . . . . . . . . . . . . . . 14

PRESENTATION OF FINANCIAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . 16

DIVIDEND POLICY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

MACROECONOMIC ENVIRONMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

SELECTED FINANCIAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

OPERATING AND FINANCIAL REVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

SELECTED STATISTICAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

RISK MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

MANAGEMENT OF THE BANK AND CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . 111

SHAREHOLDERS AND DESCRIPTION OF SHARE CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . 122

RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

MATERIAL CONTRACTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

GLOSSARY OF TERMS AND DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

INDEX TO SPECIAL PURPOSE FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . F-1

1

RISK FACTORS

The risks highlighted below could have a material adverse effect on the Bank’s business, financial condition,results of operations or prospects. Prospective investors should note that the risks described below are not theonly risks the Bank faces. The Bank has only described the risks it believes to be material. There may beadditional risks that the Bank currently considers immaterial or of which it is currently unaware, and any ofthese risks could have the effects set forth above.

The Bank has classified the risks set out below into the following categories:

• risks relating to the Bank’s constitution and structure;

• risks relating to the Bank’s financial position, in terms of composition and exposures;

• risks relating to the Bank’s operations; and

• risks relating to the Bank’s focus on Africa, including economic and political risks.

1. Risks relating to the Bank’s constitution and structure

As a supranational institution, the Bank is not subject to regulatory supervision, including with regard tocapital adequacy, liquidity and corporate governance

The Establishment Agreement has the status of a treaty under public international law, and the Bank is acreation of, and subject to, public international law. The Bank’s existence, powers, privileges, immunities,liabilities and operations are subject to, and governed by, the Establishment Agreement. The Bank is not subjectto regulation by any state. In this respect, under Article IX of the Establishment Agreement, the Bank enjoysfreedom from restrictions, regulations, supervision or controls, moratoria and other legislative, executive,administrative, fiscal and monetary restrictions of any nature in the Participating States. In addition, theEstablishment Agreement accords the President, Vice-Presidents, directors, officers and employees of the Bankand consultants and experts performing missions for the Bank a number of privileges, immunities andexemptions in the Participating States. For more information, see “Shareholders and Description of ShareCapital—Legal Status of the Bank”.

The capital adequacy position of the Bank is controlled and closely monitored by the Board, and is disclosed inthe audited special purpose financial statements of the Bank. The Bank has established a capital managementpolicy (the “Capital Management Policy”) that is based on the maintenance of a capital adequacy ratio that isin line with the recommendations of the Basel Committee on Banking Supervision (the “Basel Committee”),as amended from time to time. In particular, the Bank currently applies standards from the Basel II frameworkand intends to apply standards from the Basel III framework at some point during 2020 and thereafter.

However, the Bank is not subject to capital requirements by a regulatory body such as a central bank orequivalent institution and there can be no assurance that the Bank will continue to maintain its CapitalManagement Policy or to comply with it or that its Capital Management Policy will continue to be in line withthe recommended actions of the Basel Committee or any other internationally recognised capital adequacystandards. Non-compliance with the recommendations of the Basel Committee and its current liquidityframework could have a material adverse effect on the Bank’s access to external financing as well as to itsbusiness, financial position, results of operations and prospects.

In addition, the Bank is not subject to any corporate governance laws or rules normally applicable to nationalcorporations. Accordingly, the corporate governance standards adhered to by the Bank as enshrined in thecharter of the Bank (the “Charter”) may differ from those generally applicable to corporations organised underthe laws of any particular jurisdiction, such as the United States, the United Kingdom, EU countries or otherjurisdictions, and might be deemed inadequate by international investors.

As at the date of this Registration Document, the Bank’s subscribed share capital comprised in its Class A,Class B, and Class C Shares is two-fifths paid up. Any failure to successfully call the remaining instalmentson such Shares without raising other capital may have a material adverse effect on the Bank’s ability togrow in the medium term

As part of the Bank’s current strategic plan, entitled “Impact 2021: Transforming Africa” (the “StrategicPlan”), the Bank has set a target to raise U.S.$1.0 billion of additional equity by 2021. As at 31 December2018, U.S.$838.0 million had been raised (including warrants).

The Bank’s share capital is divided into four classes (Class A Shares, Class B Shares, Class C Shares and ClassD Shares). Class D Shares must be fully paid at the time of subscription, whereas the Class A Shares, Class

2

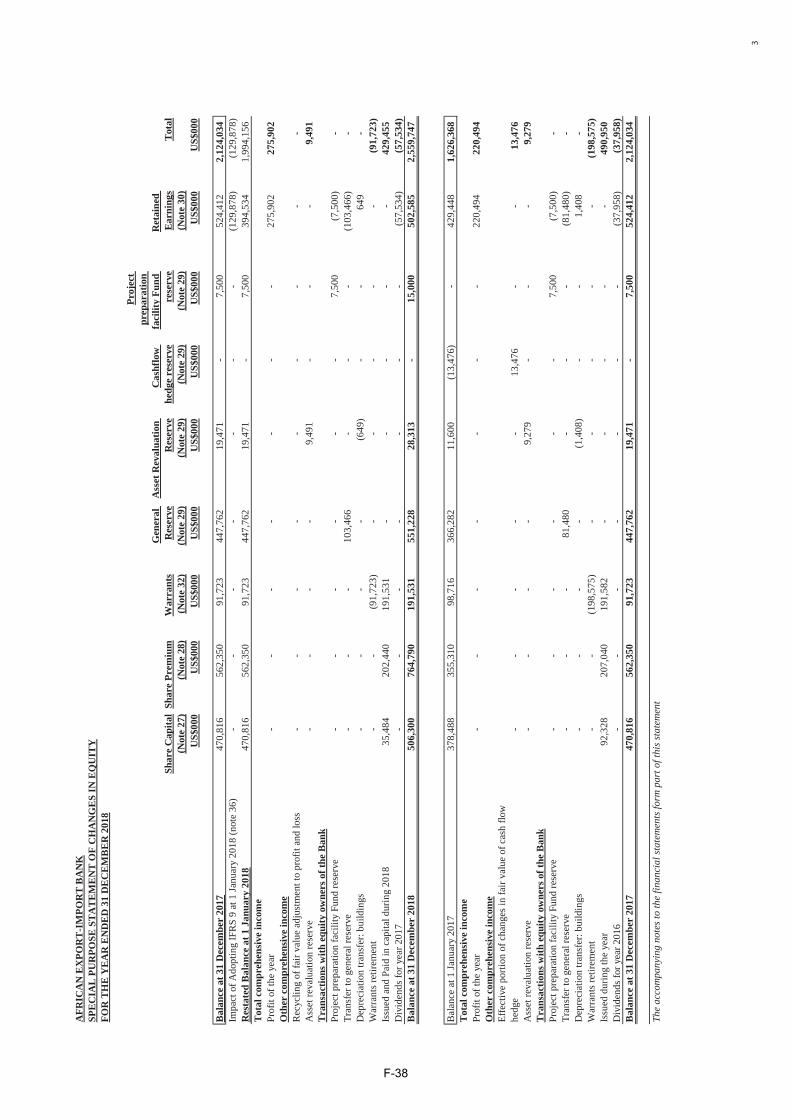

B Shares and Class C Shares are paid 40% on subscription with the balance remaining as callable capital. Inrespect of these Shares, 40% has been paid in full by the Bank’s shareholders, amounting in aggregate toU.S.$506.3 million (excluding share premium of U.S.$764.8 million) out of the overall nominal subscribedcapital of U.S.$1,162.1 million as at 31 December 2018.

The Class A, Class B and Class C Shareholders are obliged by the Charter of the Bank to pay the remaining60% (amounting to an additional U.S.$873 million (including share premium) as at 31 December 2018) whencalled by the Board of Directors. If the Bank called for such capital and the call was not honoured, this couldhave an adverse impact on the Bank’s ability to grow, particularly if the Bank were unable to obtain funds fromother sources.

With respect to the Bank’s callable capital, the majority of the Shareholders have below investment grade creditratings or no credit ratings at all. In order to manage the risk of Shareholders not honouring the remaining calls,the Bank has put in place a mid-term credit risk mitigation instrument to cover the Shareholders of the Bankwhich are not investment-grade rated, comprising primarily the Bank’s Class A and some Class B shareholders,representing U.S.$621.0 million of capital insured as at 31 December 2018. The instrument addresses ascenario in which a call on capital would not be honoured by the relevant Shareholders (i.e. in the event that acall on the uncalled portion of the equity is made and a Shareholder covered by the insurance defaults on theirpayment commitment, the insurer would make the payment due by the defaulting Shareholder). However, anymaterial failure to obtain additional equity funding through capital calls on existing Shareholders could have anadverse impact on the Bank’s expected growth targets, particularly if it is unable to raise capital throughalternative means.

Any future unavailability of capital markets and loan financing could have a material adverse effect on thegrowth of the Bank’s business

The Bank has historically obtained financing for the growth of its loan portfolio from syndicated and bilateralloans (including from Development Finance Institutions (“DFIs”) such as the International Finance Corporation(“IFC”) and the African Development Bank (“AfDB”)) and, since 2009, through the international issuance ofEurobonds under its GMTN Programme (including the U.S.$750.0 million issuance under the GMTNProgramme on 23 September 2019), Shareholder calls (the Bank had U.S.$873.0 million in uncalled equitycapital as at 31 December 2018) and Share issuances. As at 31 December 2018, the Bank hadU.S.$162.0 million of equity capital yet to be raised under the target set out in the Strategic Plan, and theBank had obligations to retire outstanding warrants in the amount of U.S.$166.8 million as at 30 June 2019.However, if further bond issuances or other methods of capital markets financing are not possible on termsacceptable to the Bank and both syndicated and bilateral loan financing are unavailable, this may inhibit theBank’s ability to meet its growth targets and could trigger downgrades to the Bank’s credit ratings. A creditrating downgrade would likely increase the Bank’s funding costs and reduce its access to the debt capitalmarkets, which could impair the Bank’s ability to obtain funding to grow its operations at meaningful levels inthe medium term, any of which could have a material adverse effect on the Bank’s business, financialcondition, results of operations and prospects.

Changes to the Charter in relation to Share Class composition or director appointment rights could result ina change in corporate governance

The Charter provides for a balanced governance structure, in terms of the distribution of shareholdings amongAfrican states, African banking institutions, the African Development Bank and other private sector and publicsector organisations and their representation on the Board of Directors. Since the Bank was only establishedrelatively recently compared to major development banks, certain transitional measures and changes to theBank’s governance structure have been required in the past and could be required in the future as theorganisation grows and develops, which could give rise to changes in the relative proportions of each class ofthe Bank’s share capital and in the rights to appoint members of the Board of Directors. For example:

• prior to the amendment of the Charter at the reconvened Third Extraordinary General Meeting on8 December 2012 (the “Third EGM”), the Charter required that the Bank’s authorised share capital, whenfully subscribed, was to be distributed proportionally among the three categories of shareholders as 35%for Class A Shareholders, 40% for Class B Shareholders and 25% for Class C Shareholders;

• at the Third EGM, the Charter was amended to provide for a new category of Class D Shares, and theproportionate distributions were also amended such that a minimum of 35% of the authorised share capitalis now to be held by Class A Shareholders, and up to 65% of the authorised share capital can be held by

3

Class B, C and D Shareholders. Notably, Class D Shares can be held by any person, which couldpotentially include African states and others who are also eligible to hold Class A Shares; and

• Article 14 of the Charter states that the Class A, Class B and Class C Shares may be transferred onlyamong holders of Shares of the respective class or to any third party who is eligible to become a holder ofsuch class of Shares pursuant to Article 7 of the Charter. Class D Shares may be freely transferred withoutrestriction to any person. Article 14 also contains a number of transitional provisions that have appliedsince the first issue of Class D Shares, including: (i) holders of Class B and Class C Shares may apply toconvert their shareholdings to Class D Shares, and (ii) Class B Shares that are 100% beneficially andlegally owned by an African State may be converted to Class A Shares.

Changes to shareholdings by the conversion of Class B Shares or Class C Shares into Class D Sharescould ultimately result in a change in the composition of the Board of Directors. In addition, there is norestriction on the number of Shares that may be held by any one individual shareholder or group ofShareholders, which could potentially lead to a concentration of ownership of the Bank. As at the date ofthis Registration Document, a concentration of ownership of the Bank would not of itself result in anability to appoint or remove a majority of the Board of Directors. However, if the Bank’s corporategovernance structure and established practices were changed, whether by virtue of amendments to theCharter, further capital raises, ownership changes or otherwise, such that a concentration in control of theBank could result in an ability of any person or group of persons acting together to appoint or remove amajority of the Board of Directors, this may in turn have a material adverse effect on the investmentpolicies and the lending activities of the Bank and, consequently, the Bank’s business, financial condition,results of operations and prospects.

2. Risks relating to the Bank’s financial position, in terms of composition and exposures

The Bank’s loans are geographically highly concentrated in Africa, with 73.9% being from West and NorthAfrica as at 31 December 2018

While the Bank exists to facilitate, promote and expand intra- and extra-African trade, its lending activities arecurrently concentrated in a relatively small number of countries in Africa, with borrowings in Nigeria andEgypt alone accounting for 54.8% of the Bank’s outstanding gross loans (loans and advances at amortised costand FVTPL) as at 31 December 2018. As at 31 December 2018, 48.7% of the Bank’s outstanding gross loansand advances were to borrowers in West Africa and 25.2% were to borrowers in North Africa. Of the WestAfrican borrower gross exposure, as at 31 December 2018, Nigerian borrowers accounted for 33.2% of theBank’s gross loans exposure, in comparison to 36.5% as at 31 December 2017 and 31.7% as at 31 December2016. Furthermore, as at 31 December 2018, of the Bank’s 20 largest borrowers by outstanding amount (whichaccounted for 63.9% of the Bank’s total gross loan portfolio), four were based in Nigeria (with a total grossoutstanding amount of U.S.$2,166.4 million, or 19.0%, of the Bank’s total outstanding loans) and six werebased in Egypt (with a total gross outstanding amount of U.S.$2,093.2 million, or 18.4%, of the Bank’s totalgross outstanding loans).

If economic changes adversely affect the borrowers and/or countries representing the major exposures of theBank, the Bank could experience potential difficulties in loan repayment and collection, as well as credit lossesarising from these loans, which in turn could have a material adverse effect on its business, financial condition,results of operations and prospects.

African financial institutions are borrowers of a significant proportion of the Bank’s loan portfolio

The Bank’s loan portfolio is significantly concentrated, with 49.8% of the Bank’s outstanding loans as at31 December 2018 provided to African financial institutions. Therefore, the Bank’s business may beparticularly subject to changes in economic conditions and systemic risks that affect financial markets. Anynegative shocks to financial markets in Africa that adversely affected these financial institutions couldadversely affect the Bank’s loan portfolio and lead to credit losses. In addition, any increases in regulatoryoversight and requirements imposed by the governments of Participating States on the lending and trade financeactivities of borrowers operating in their financial sectors could have an indirect impact on the Bank’s activitiesand business and have a material adverse effect on its business, financial condition, results of operations andprospects.

4

Changes in the credit quality of the Bank’s borrowers and counterparties could materially adversely affectthe Bank’s financial performance, and the Bank’s credit portfolio may not continue to grow at the same orsimilar rate as in recent years

The Bank’s loan portfolio increased from U.S.$8,545.7 million as at 31 December 2017 toU.S.$11,134.4 million as at 31 December 2018 and to U.S.$11,395.0 million as at 30 June 2019. Noassurance can be given that, in the future, the Bank’s loan portfolio will continue to grow at historic rates.Furthermore, any continuation of historical growth rates in the Bank’s loan portfolio could expose the Bank toincreased credit risk, which, in turn, could have a material adverse effect on the Bank’s business, financialcondition, growth, prospects, cash flows and results of operations if the Bank were to be unable to manage suchincrease in credit risk.

In particular, the Bank’s business is subject to risks related to the credit quality of its customers. As at 30 June2019, loans and advances to customers amounted to 74.1% of the Bank’s total assets. Given the high magnitudeof the exposure to customer credit risk, a deterioration of the credit quality of the Bank’s customers, and afailure by the Bank to correctly identify and manage such changes, could reduce the value of the Bank’s assetsand require increased provisions for bad and doubtful debts, which, in turn, could have a material adverseeffect on the Bank’s business, financial condition, results of operations and prospects.

Local foreign exchange controls or currency devaluations may affect the Bank’s and its borrowers’ ability topay U.S. dollar-denominated obligations

As at 31 December 2018, 88.8% of the Bank’s loans and advances were U.S. dollar-denominated and 11.2%were Euro-denominated. The Bank faces the risk that local country foreign exchange controls could restrict theability of its borrowers, even if they are exporters, to acquire dollars or Euros to repay loans on a timely basis,and/or that significant currency devaluation will occur, which could increase the cost, in local currency terms,to the Bank’s borrowers of acquiring dollars or Euros to repay loans. For example, in 2019, the government ofZimbabwe announced controls on the U.S. dollar, which could restrict the ability of customers in Zimbabwe torepay U.S. dollar-denominated loans to the Bank. Zimbabwe customers accounted for U.S.$714.4 million, or6.3%, of the Bank’s outstanding gross exposure as at 31 December 2018. Furthermore, in 2017, certaincustomers of the Bank in Nigeria would have faced difficulties accessing currency to service their liabilities tothe Bank absent an arrangement with Participating States, including between the Central Bank of Nigeria andthe Bank, whereby the Bank’s customers benefitted from its preferred creditor status and were given priorityaccess to hard currency to enable them to service their liabilities. However, there can be no assurance that sucharrangements, as a result of the Bank’s preferred creditor status or otherwise with Participating States, will beavailable in any similar circumstances in the future.

Any inability of the Bank’s borrowers to acquire dollars or Euros as a result of local foreign exchange controls,currency devaluation, or otherwise could affect their ability to repay their loans, which in turn could have amaterial adverse effect on the Bank’s business, results of operations, financial condition and cash flows.

A decline in the value of collateral or the illiquidity of the collateral securing the Bank’s loans mayadversely affect the credit quality of its loan portfolio

The Bank takes collateral from the majority of borrowers, and as at 31 December 2018, the fair value ofcollateral represented 90% of loans outstanding. Collateral that may be accepted includes assignments ofreceivables, cash collateral, government securities (by way of bonds or guarantees) and pledges over assets.Downturns in the relevant markets or a general deterioration of economic conditions may result in reductions inthe value of collateral securing loans to levels below the amounts of the outstanding principal and accruedinterest on such loans. If collateral values decline, they may not be sufficient to cover uncollectable amounts onthe Bank’s secured loans. A failure to recover the expected value of collateral may expose the Bank to losses,which could, in turn, have a material adverse effect on the Bank’s business, financial condition, results ofoperations and prospects.

The Bank’s allowances for credit losses could prove inadequate to cover credit losses related to its loans andcontingencies

Determining the appropriate level of allowances for credit losses necessarily requires the Board’s andmanagement’s judgement, including assumptions and estimates made in the context of changing political andeconomic conditions in the regions and sectors to which the Bank lends. In particular, on 1 January 2018, theBank implemented IFRS 9. IFRS 9 replaced the “incurred credit loss” model used under IAS 39 with an“expected credit loss” model. The changes from incurred to expected credit losses requires professional

5

judgement over various factors used in the calculation of expected credit losses, such as how macroeconomicscenarios affect the calculation. The application of the IFRS 9 impairment requirements could increasevolatility in profit and loss of the Bank. In addition, the Bank’s allowances for credit losses may not beadequate to cover losses in its credit portfolio, which, in turn, could have a material adverse effect on theBank’s business, financial condition, growth, prospects, cash flows and results of operations.

The Bank is exposed to liquidity risk

The Bank has historically obtained financing for the growth of its loan portfolio from syndicated and bilateralloans (including from DFIs such as the IFC and the AfDB) and, since 2009, through the international issuanceof Eurobonds under its GMTN Programme (including the U.S.$750.0 million issuance under the GMTNProgramme on 23 September 2019), shareholder calls (the Bank had U.S.$873.0 million in uncalled equitycapital as at 31 December 2018) and Share issuances. However, the maturity profile associated with a majorityof the loans from these funding sources is shorter than the maturity of its assets (typically loans). Therefore,unanticipated decreases in CENDEP deposits or other funding sources may result in liquidity gaps that theBank may not be able to cover without incurring additional expenses, if at all. The liquidity gap may affect theability of the Bank to continue the targeted growth of its business effectively in the medium term. Any inabilityto meet liquidity needs in these circumstances could adversely impact the evaluation of the Bank’screditworthiness by counterparties and rating agencies, which could significantly limit its ability to grow itsoperations and have a material adverse effect on the Bank’s business, financial condition, results of operationsand prospects.

3. Risks relating to the Bank’s operations

The Bank is exposed to operational risks, including the risk of fraud by employees and third parties, failureto obtain proper internal authorisations, failure to properly document transactions, equipment failures, dataprotection and cybersecurity breaches, and errors by employees

The Bank is exposed to operational risks, including the risk of fraud by employees and third parties, failure toobtain proper internal authorisations, failure to properly document transactions, equipment failures, dataprotection and cybersecurity breaches, and errors by employees. In particular, the Bank’s business depends onprocessing numerous complex transactions, and the recording and processing of these transactions arepotentially exposed to the risk of human and technological errors, including miscalculations, or a breakdown ininternal controls relating to the due authorisation of transactions. Given the volume of transactions processed bythe Bank, errors may be repeated or compounded before they are discovered and rectified, and no assurancecan be given that risk assessments made in advance will adequately estimate the costs of these errors.Moreover, the secure transmission of confidential information about customers and transactions is a critical partof the Bank’s business, and its measures for keeping such information secure from external threats could proveinadequate. Although the Bank has put in place a system of internal controls that is designed to address theforegoing risks, there can be no assurance that operational problems or other errors will not occur, and that thefailure to prevent these risks will not have a material adverse effect on the Bank’s business, financial condition,results of operations and prospects.

Any delays to, or failure to implement, business initiatives that the Bank may undertake could prevent theBank from realising the anticipated revenues and benefits of the initiatives, divert the attention of itsmanagement, cause additional expenses, or cause other negative repercussions for the Bank

Part of the Bank’s strategy is to diversify income sources through business initiatives such as those set out inthe Bank’s Strategic Plan covering the period from 2017 to 2021 that, in some cases, involve partnerships orstrategic alliances with specialists, and initiatives such as expanding into new markets, targeting new clientsand developing new products and services (please see also “Business—Strategic Planning”). These initiativesmay not be fully implemented within the time frame which the Bank expects, or at all. In addition, even if suchinitiatives are fully implemented, they may not generate revenues as expected or could result in an increase incosts and expenses in excess of budget and/or credit risks arising from new markets. Any delays in reachingagreement with strategic partners, or otherwise implementing the Bank’s strategic initiatives, could divert theattention of the Bank’s management, result in additional expense, prevent the Bank from pursuing otherinitiatives or, ultimately, prevent the Bank from realising the anticipated benefits of the initiatives, which couldadversely affect the Bank’s business, financial condition, results of operations and prospects.

6

Increased risk perception in countries in Africa where the Bank has large credit exposure could have anadverse impact on the Bank’s credit ratings, funding activities and funding costs

There is no guarantee that the Bank will not be subject to negative changes in its credit ratings (see “GeneralInformation”). In particular, increased risk perception in any country in Africa where the Bank has largeexposures (as is the case with, for example, the Bank’s exposure to Nigeria, which accounted for 33.2% of theBank’s total loans outstanding as at 31 December 2018) could trigger downgrades to the Bank’s credit ratings.A credit rating downgrade would likely increase the Bank’s funding costs and could reduce its access to thecapital markets, whether debt or equity. In that case, the Bank’s ability to obtain the necessary funding to carryon its financing activities in Africa at meaningful levels could be adversely affected, which in turn could have amaterial adverse effect on the Bank’s business, financial condition, results of operations and prospects.

The Bank is exposed to market risks, including interest rate and currency risk, and its efforts to managesuch risks may not be successful

Market risk generally represents the risk that the value of assets and liabilities will be adversely affected bychanges in market conditions. Market risk is inherent in the financial transactions associated with many of theBank’s operations and activities, including loans, deposits, short-term borrowings and long-term debt. The Bankseeks to manage some of its market risk through the use of derivatives such as currency and interest ratehedging and swaps. Fluctuations in interest and currency exchange rates, changes in the implied volatility ofinterest rates and changes in foreign exchange rates have a direct impact on the Bank’s profitability.Accordingly, depending on the instruments or activities impacted, market risks can adversely affect the Bank’sbusiness, financial condition, results of operations and prospects.

The Bank is exposed to risks resulting from mismatches between the interest rates on its interest-bearingliabilities and interest-earning assets. To the extent that the Bank’s assets may re-price more frequently than itsliabilities, if interest rates fall, the Bank’s interest expense will decrease more slowly than its interest income,which could negatively affect its net interest margin. For example, the Bank lends and borrows at floating rates,resulting in a natural hedge. However, borrowings done through the GMTN Programme are at a fixed interestrate. In order to hedge against interest rate movements, the Bank enters into interest rate swaps. As at31 December 2018, U.S.$1.28 billion in bonds were hedged, U.S.$3.0 billion in total bonds were outstandingand hedged bonds represented 42.3% of the total bond portfolio.

More generally, the Bank has entered into various hedging transactions to help manage the risk of changes incommodity prices and currency fluctuations with respect to loans made to its borrowers. The Bank’s actualhedging decisions are determined in light of the facts and circumstances existing at the time of the hedge andmay differ from time to time. In some cases, the Bank may not elect or have the ability to implement suchhedges or, if the Bank does implement them, they may not achieve the desired effect. They may also exposethe Bank to the risk that its counterparties to hedging contracts will default on their obligations. Furthermore,although hedging transactions may limit to some degree the Bank’s risk from fluctuations in commodity prices,currency exchange and interest rates, the Bank potentially forgoes benefits that might result from suchfluctuations. At the date of this Registration Document, the Bank hedged 100% of its actual net currencyexposure, in line with its current policy, and as noted above, the Bank is substantially hedged against its currentinterest rate risk. However, there can be no assurance that the Bank’s hedging activities will operate as intendedand protect it against losses resulting from adverse interest rate, currency or commodity price fluctuations. Anyfailure to do so could have a material adverse effect on the Bank’s business, financial condition, results ofoperations and prospects.

Although the Bank seeks to adhere to internationally recognised sanctions, the Bank has relationships withstates which have citizens or entities that are subject to international sanctions

As a supranational financial institution focused on developing trade from and within Africa, the Bank hasrelationships (including shareholder and business) with a number of African states that are subject to one ormore international sanctions regimes, in particular, the Democratic Republic of the Congo, the Republic ofSudan, South Sudan and the Republic of Zimbabwe. As at the date of this Registration Document, none ofthese states is the subject of comprehensive sanctions under any applicable sanctions regime, although certainindividuals, entities and sectors within these states are subject to sanctions. As at 30 June 2019, the Bank’soperational exposure to each of these countries (as a percentage of gross outstanding loans and advances), byvirtue of its lending activities in those countries, was as follows:

Democratic Republic of the Congo: 0.0%

Republic of Sudan: 3.2%

7

South Sudan: 0.5%

Zimbabwe: 9.7%.

None of the loans in the totals above were granted to parties in violation of any international sanctions regimes.In this respect, it should be noted that loans granted to the Republic of Sudan have historically beendenominated in Euro, rather than U.S. Dollars, since the Republic of Sudan had previously been subject tocomprehensive sanctions in the United States. Nevertheless, in each of the foregoing cases, the Bank intendseither to reduce its exposures or to cap its exposure to acceptable limits.

Certain persons located in, or in some other way connected with, the Republic of Zimbabwe and the Republicof Sudan are subject to sanctions administered by the Office of Foreign Assets Control of the U.S. Departmentof the Treasury (“OFAC”). In addition, sanctions administered by the EU prohibit the provision of (i) financingor financial assistance related to military activities, including loans for the sale, supply, transfer or export ofarms or for the provision of related technical assistance (such as maintenance) to any person, entity or body inthe Republic of Sudan or South Sudan (EU Regulation 131/2004 as amended by 1215/2011) and (ii) technicalassistance, financing or financial assistance related to military activities, or towards the purchase of equipmentwhich could be used for internal repression in Zimbabwe (EU Regulation (314/2004) and UK StatutoryInstrument, “The Zimbabwe (Financial Sanctions) Regulations 2009” (No. 847)). Furthermore, a UnitedNations-administered embargo prohibits the trading of arms and rough diamonds in, to or with Côte d’Ivoire.OFAC also maintains sanctions against certain persons and entities in Côte d’Ivoire, the Democratic Republicof the Congo and Liberia.

The sanctions regimes referred to above do not prevent the Bank from transacting with entities and persons thatare not themselves subject to sanctions or embargoes, although the Bank seeks to adhere to sanctions andembargoes imposed and administered by the African Union, United Nations Security Council, the EuropeanUnion, OFAC, Her Majesty’s Treasury and other relevant internationally recognised sanctions authorities.However, given the extent of the Bank’s involvement in financing transactions throughout Africa, there can beno assurance that the Bank will not be subject to investigation in connection with the sanctions or embargoesdescribed above or other sanctions and embargoes that may be applicable either presently or in the future. Ifany such investigation occurred and resulted in the Bank being found to have breached any sanctions orembargoes, this could adversely affect the Bank’s business, financial condition, results of operations andprospects. Please see also “Risk Management—Anti-Money Laundering, “Know-Your-Customer” Checks andSanctions Compliance—Sanctions Compliance”.

The loss of key employees may have an adverse effect on the Bank’s business

The Bank’s growth strategy is dependent on the efforts and abilities of its senior management. The Bank’soperations depend, in part, upon the continued services of certain long-term, key employees with the relevantskills to operate a multilateral financial institution. In the Bank’s experience, in cases of turnover of its keyemployees, replacement costs can be significant given the need to find employees with the relevant skills andexperience, particularly given the pan-African nature of the Bank’s operations and that to replace one existingemployee with the requisite product knowledge, skills and languages could require the Bank having to hiremultiple new employees to yield the same skill set, which would, inter alia, increase its employment costs.Despite having a succession plan in place for its existing key employees, if the Bank loses the services of anyof its existing key personnel without timely and suitable replacements, or is unable to attract and retain newpersonnel with suitable experience, the Bank’s business, financial condition, results of operations and prospectsmay be materially and adversely affected.

4. Risks relating to the Bank’s focus on Africa

The Bank’s lending activities are concentrated in Africa, which is a reflection of its core mission. Accordingly,investors should pay careful attention to the risk factors, both economic and political, associated with investingin Africa.

Emerging markets such as those in Africa are subject to greater risks than more developed markets

African markets are subject to greater risk than more developed markets. These risks include economic andfinancial market instability as well as, in some cases, significant legal and political risks. In addition, in anumber of African countries, structural reforms are still needed in many sectors, including agriculture, energyand transport.

8

Economic instability in African countries in the past and in other emerging market countries has beenmanifested in many ways, including but not limited to:

(i) general economic and business conditions;

(ii) high interest rates;

(iii) exchange rate fluctuations and instability;

(iv) high levels of inflation;

(v) exchange controls;

(vi) industrial action;

(vii) commodity price fluctuations;

(viii) slowdown in the economic and business activity of key clients;

(ix) wage and price controls;

(x) sudden changes in economic or tax policies;

(xi) imposition of trade barriers;

(xii) changes in investor confidence; and

(xiii) perceived or actual security issues and political instability.

The occurrence of any of these factors could have a material adverse effect on the Bank’s business, financialcondition, growth, prospects, cash flows and results of operations.

Turmoil in emerging markets and broader market conditions, even outside Africa, can adversely affectAfrican economies

Any significant financial turmoil in one emerging market country has a tendency to adversely affect prices incapital markets of other emerging market countries, as investors may seek to move their money to more stable,developed markets. As has happened in the past, financial problems or an increase in the perceived risksassociated with investing in emerging economies could dampen foreign investment across Africa and adverselyaffect the wider African economy.

The availability of credit to entities operating within emerging markets is also significantly influenced by thelevel of investor confidence in such markets as a whole and, as such, any factors that affect investor confidence(for example, a decrease in credit ratings or state or central bank intervention) could affect the price oravailability of funding for entities within any of these markets. Thus, even if the wider African economyremains stable (as a whole), financial turmoil in any emerging market country or region (African or otherwise)could have a material adverse effect on the Bank’s business, financial condition, results of operations andprospects.

In particular, the economies of some countries in Africa have periodically experienced significant volatility,which has been characterised, in some cases, by political uncertainty, slow growth or recession, declininginvestment, government and private sector debt defaults and restructurings, significant inflation and currencydevaluation. Entities located in, or doing business with, countries in emerging markets may be particularlysusceptible to disruptions in the capital markets and the reduced availability of credit or the increased cost ofdebt, which could result in them experiencing financial difficulty.

In addition, African economies are often overly dependent on commodity exports, and decreased demand fromChina for natural resources has had and may continue to have a significant downward effect on the prices ofthese commodities from African countries, whose economies are heavily dependent on the export of theseresources. See also “—The Bank may be adversely affected by a continued depression of or further falls incommodity prices, in particular oil prices, in the international markets and the effect of such declines onAfrican economic growth”.

As a result, African economies are highly susceptible to global economic changes, including in oil prices,U.S. dollar interest rates, the U.S. dollar exchange rate relative to local currencies, U.S. global trade policies(particularly with China) and slower economic growth in developed countries, any of which could have asignificant adverse effect on the economic condition of countries in Africa.

9

The Bank may be adversely affected by general conditions in the international financial markets and theireffects on African financial markets

The global financial crisis placed significant pressure on African banking systems as (i) access to foreigncurrency was restricted (a situation aggravated by downward pressure on exchange rates of local currencies tothe U.S. Dollar) and (ii) deterioration in the real economic sector threatened the quality of the assets of banks,resulting in dysfunctionality across the banking sector. The restoration of credit flow both to and within Africaand the continued return of financial markets to functionality represent critical elements for the ongoingrecovery from the global financial crisis. Any subsequent global financial crises would have an adverse impacton the Bank’s results of operations and profitability.

Ongoing, synchronised and above-trend growth in world economic activity is the main contributor towardsdemand for emerging market assets. Growth in Europe and the United States has been above average in recentyears, and growth in emerging markets generally continues to improve. Several major central banks havesignalled a firm intention to normalise monetary policy over time. Should major central banks reduce theirbalance sheets or increase interest rates faster than currently anticipated by international financial markets,foreign capital inflow into African economies could be jeopardised. A sudden reduction in foreign capitalinflow could weaken local currencies and economic growth across the continent, increase bond yields andresult in higher local interest rates, which may adversely impact the Bank’s operations and profitability.

The Bank may be adversely affected by a continued depression of or further falls in commodity prices, inparticular oil prices, in the international markets and the effect of such declines on African economicgrowth

The economies of many countries in Africa are highly sensitive to commodity prices, particularly oil prices. Oilprices have fluctuated widely in the past ten years. However, recently markets have experienced a prolongedperiod of low prices. From early 2011 to mid-2014, monthly average oil prices fluctuated between U.S.$93 andU.S.$118 of Brent crude oil (having peaked in July 2008, when monthly average oil prices reached anU.S.$133 per barrel). Oil prices began to decline sharply in the second half of 2014, a trend that continuedthrough to mid-January 2016, when daily prices were less than U.S.$30 per barrel. Oil prices increased to anaverage of U.S.$53 per barrel in 2017, and rose again to an average of U.S.$68 per barrel in 20181. Accordingto the World Bank, oil prices are anticipated to average U.S.$66 per barrel in 2019 and U.S.$65 per barrel in20202.

Oil prices can be affected by relatively minor changes in the supply of and the demand for oil, and a number ofadditional factors that are beyond an exporting African country’s control. These factors include, but are notlimited to, political conditions in the Middle East and other regions, internal and political decisions of theOrganisation of the Petroleum Exporting Countries (“OPEC”) and other oil producing regions and nations,weather conditions, government regulations, transport costs, the price and availability of alternative fuels andoverall international demand. Low oil prices can have a significant negative impact on the economies of oilexporters in Africa. For example, according to the World Bank, the GDP of Nigeria, which is highly dependenton oil exports, grew in 2014 by 6.3%, however, after the decline in oil prices, it only grew by 2.7% in 2015and fell by an estimated 1.6% during 20163.

Falling prices for other commodities can also impact many countries in the region. Commodity markets weregenerally weaker in 2018, with prices over 13% lower compared with their close in 20174. Global demand forraw materials has been weak, and demand from large developing countries has decreased as growth has slowed.In particular, low commodity prices for gold, cocoa, tea and platinum, among other commodities, had anegative effect on many African currencies in 2015, which led African nations such as Ghana, Uganda, Angolaand Tanzania to experience sharp falls in the values of their currencies. Despite limited recovery during 2016,2017 and 2018 in prices of key commodities of export interest to Africa, most commodity-dependenteconomies struggled to recover. Since a third of the world’s mineral reserves and a tenth of global oil reservesare located in Africa, many countries are extremely dependent on commodity export revenues. Sustained lowcommodity prices could slow growth and negatively impact African economies and companies operating inthose economies. This in turn could have a significant adverse impact on the Bank’s credit portfolio, includingincreased loan loss provisions and, as a result, on the Bank’s growth, asset quality, prospects, profitability andfinancial condition.

1 World Bank Commodity Markets Outlook, April 20192 World Bank Commodity Markets Outlook, April 20193 World Bank Global Economic Prospects—June 2017; World Bank Global Economic Prospects—January 20184 Bloomberg Commodity (BCOM) index, 2018

10

A worsening of the political climate (including significant changes to social conditions and foreign policies)in any of the states with which the Bank has relationships may have a material adverse effect on the Bank’sfinancial condition and/or results of operations

Political factors which could adversely affect the Bank’s business, financial condition, cash flows, results ofoperations and prospects include:

• regional political instability, including government or military regime change, riots or other forms of civildisturbance violence or strife, including through acts of terrorism, guerrilla activities and insurrection;

• military strikes or the outbreak of war or other hostilities involving nations in the region;

• any material curtailment of the industrial and economic infrastructure development that is currentlyunderway across Africa;

• government intervention, including expropriation or nationalisation of assets or increased levels ofprotectionism;

• increased government regulations, or adverse governmental activities, with respect to price, import andexport controls, the environment, customs and immigration, capital transfers, foreign exchange andcurrency controls, labour policies and land and water use, foreign ownership, legal structures and tax laws;

• cancellation of contractual rights;

• trade barriers;

• difficulties in staffing and managing operations;

• lack of well-developed legal systems which could make it difficult for the Bank to enforce its intellectualproperty and contractual rights;

• security and safety of employees;

• restrictions on the right to convert or repatriate currency or export assets;

• greater risk of uncollectible accounts and longer collection cycles;

• indigenisation and empowerment programmes;

• logistical and communications challenges;

• corruption; and

• arbitrary, inconsistent or unlawful government action.

Many of the countries with which the Bank has relationships are in various stages of developing the institutionsand legal and regulatory systems that are characteristic of established democracies. However, institutions inthese countries may not yet be as firmly established as they are in countries in more established democracies.Many of these countries are also in the process of transitioning to a market economy and, as a result, areexperiencing changes in their economies and their government policies that can affect the Bank’s investmentsin those countries. Moreover, the procedural safeguards of the new legal and regulatory regimes in thosecountries are still being developed and, therefore, existing laws and regulations may be applied inconsistently.In some circumstances, it may not be possible to obtain the legal remedies provided under those laws andregulations in a timely manner.

The introduction of barriers to global trade, including tariffs, could impact global demand for African goodsand commodities, and weaken global risk appetite more generally. For example, the recent imposition of tariffsby U.S. President Donald Trump on certain foreign exports of steel and aluminium may have a negative impacton these commodity sectors in African economies, as well as more broadly. Trade barriers affecting Africaneconomies may ultimately have an adverse impact on the Bank’s operations and credit portfolio.

In recent years, many African countries have been subject to increasing numbers of terrorist attacks, includingbut not limited to high profile incidents in Nigeria, Kenya, Tunisia, Egypt and Mali, and many Africancountries suffer from a high prevalence of violent crime, militant activity and political unrest. An increase inthe number of terrorist attacks or violent crimes, or the occurrence of a large-scale terrorist attack in Africacould have a negative impact on African economies and therefore the Bank’s financial condition and business.Islamist extremism is increasingly seen as posing a threat in certain parts of Africa. Extremist groups reportedto be operating in Africa include ISIS, al Qaeda in the Islamic Maghreb, Al Shabaab in eastern Africa andBoko Haram in western Africa. The activities of these groups could disrupt trade, decrease economic

11

confidence and deter international investment which could in turn have a material adverse effect on the Bank’sbusiness, financial condition, cash flows, results of operations and prospects.

In addition, certain regions of Africa may suffer from geopolitical conflict. A number of African states haveunresolved political differences both internally, with surrounding countries and/or internationally. In particular,since January 2011, there have been varying degrees of political instability and public protests within certainNorthern African countries, including Egypt, where the Bank’s headquarters are located, as well as Libya andTunisia. Lingering political tensions have not, in the Bank’s experience, adversely affected the Bank’s decision-making capabilities or the functioning of its operational portfolio to date. However, it is possible that in thefuture such events could have an adverse impact on the political stability and economy of the relevant Africancountries and consequently on the Bank’s results of operations and financial condition. In addition, weaknessesrelating to certain African legal systems and legislation create an uncertain environment for investment andbusiness activity, which could have a material adverse effect on the Bank’s business, financial condition, resultsof operations and prospects.

As the political, economic and legal environments remain subject to continuous development, investors in thesecountries and regions face uncertainty as to the security of their investments. Any unexpected changes in thepolitical or economic conditions in these or neighbouring countries or others in the region may have a materialadverse effect on the Bank’s business, financial condition, cash flows, results of operations and prospects.

Despite the immunities and privileges afforded to the Bank in the Establishment Agreement, the BranchAgreements and the Headquarters Agreement, there can be no guarantee that the Bank’s assets andoperations will not be affected by government intervention or that Participating States will honour theBank’s preferred creditor status

Under the Establishment Agreement, each Participating State has agreed to waive, and refrain from imposing,any administrative, financial or other regulatory restrictions that are likely to hinder in any manner the smoothfunctioning of the Bank or impair its operations. Accordingly, the Bank’s property, assets, operations andactivities are free from restrictions, regulations, supervision or controls, moratoria and other legislative,executive, administrative, fiscal and monetary restrictions of any nature. In addition, Article VIII of theEstablishment Agreement states that “the property and assets of the Bank wherever located and by whomsoeverheld shall be immune from: (a) search, requisition, expropriation, confiscation, nationalisation and all otherforms of seizure, taking or foreclosure by executive or legislative action; and (b) seizure, attachment orexecution before the delivery of final judgment or award against the Bank” and that, without prejudice to suchimmunity, the property and assets of the Bank shall be subject to due legal processes and judicial action takenby ordinary courts of competent jurisdiction.

In relation to tax, Article XIV of the Establishment Agreement exempts the Bank and its property, assets,income, operations and transactions from all taxation and customs duties in each of the Participating States inwhich it operates. In addition, Article VII of the Headquarters Agreement between the Bank and the ArabRepublic of Egypt dated 31 August 1994 (the “Headquarters Agreement”) states that the Bank’s headquartersare inviolable, and that no officer or official of Egypt may enter the headquarters without the consent of thePresident of the Bank. In addition, the Bank has entered into branch agreements (the “Branch Agreements”)with the Participating States of Côte d’Ivoire, Nigeria and Zimbabwe, where its branches are located, whichalso contain material protections for the Bank in line with the Establishment Agreement.

As at the date of this Registration Document, the Bank has not been subject to any violation of the foregoingprovisions. However, there can be no guarantee that such privileges and immunities will continue indefinitely,that a Participating State would not seek to tax the Bank, that such privileges and immunities will not bealtered, or that changes to the government of any Participating State or other factors, such as political unrest,will not adversely affect the privileges and immunities granted to the Bank. Any alteration, suspension orviolation of the Bank’s immunities and privileges and/or unlawful or arbitrary government action in someAfrican states could disrupt the Bank’s operations and have a material adverse effect on the Bank’s business,financial condition, results of operations and prospects.

These accommodations referred to above have allowed the Bank to enjoy a preferred creditor status in theParticipating States and reduced the effect of country risk and moratorium risk on the Bank. Other elements ofpreferred creditor status, including (but not limited to) preferential access to foreign currency in the event of acountry foreign exchange crisis and priority of payment in the event of government shortfalls, are not containedin a treaty, law or contract but reflect the relevance of the Bank to the Participating States and that theParticipating States will likely place priority on honouring commitments (including debt repayments) to theBank over other private or official creditors during times of debt distress. Accordingly, the Bank believes that

12

its exposure to the Participating States subjects it to less risk than its commercial loans. However, there can beno assurance that, during a time of debt distress, the Participating States would always give the Bank priority.Any failure by the Participating States to honour their commitments to the Bank in full at the time that theycome due, and in the absence of realisable security taken by the Bank under the affected transactions, couldhave a material adverse effect on the Bank’s business, financial condition, results of operations and prospects.

There can be no guarantee that the business, operations and financial results of the Bank will not in thefuture be adversely affected by any significant recurrence of unrest in Egypt and other MENA states, or anyspread thereof to other African states where the Bank operates

The majority of the Bank’s business is, and will continue to be, concentrated in African countries outside of theMENA region which, as at the date of this Registration Document, have been unaffected by the various on-going economic and political developments in or affecting the MENA region. This is due to the fact that theBank predominantly conducts its business in its member states and, as at the date of this RegistrationDocument, the only MENA states which are members of the Bank are Egypt, Tunisia and Morocco.

The 2011 revolution in Egypt, which led to the overthrow of former President Hosni Mubarak, did at the timedirectly impact the Bank, by forcing the closure of its Cairo headquarters for five days. However, the Bank didnot experience any material disruption to its operations as a result of this closure, due to having back-upfacilities in the Abuja Branch to which the Bank was able to transfer its headquarter operations and criticalpersonnel. The Bank anticipates that this would again be the case in the event of any recurrence of significantpolitical unrest within Egypt in the future.

Nevertheless, it is not possible to predict the occurrence of events or circumstances such as war, hostilities orpolitical unrest or their impact, and no assurance can be given that the Bank would be able to sustain its currentprofit levels if adverse political events or circumstances were to occur in any of the African states in which ithas significant operations or exposure.

The Bank operates in jurisdictions with risks relating to fraud, bribery, money laundering and corruption

The Bank operates in a number of jurisdictions that have from time to time experienced high levels of fraud,bribery, money laundering and corruption. For example, certain jurisdictions have been allocated low scores onTransparency International’s “Corruption Perceptions Index”. Doing business in developing countries bringswith it inherent risks associated with enforcement of the Bank’s legal and contractual rights and third partyobligations, fraud, bribery, money laundering and corruption.

The Bank has policies and procedures in place and codes of conduct and other safeguards designed to preventthe occurrence of fraud, bribery, money laundering and corruption. See “Risk Management—Anti-MoneyLaundering, “Know-Your-Customer” Checks and Sanctions Compliance—Sanctions Compliance”. Theseinclude policies and procedures designed to assist the Bank in identifying potential investments that areassociated with Politically Exposed Persons (“PEPs”) which are then subjected to heightened scrutiny andadditional due diligence. However, it may not be possible for the Bank to detect or prevent every instance offraud, bribery, money laundering or corruption in every jurisdiction in which it does business or where itsemployees or agents are located. The Bank may therefore be subject to civil and criminal penalties and toreputational damage, any of which could have a material adverse effect on the Bank’s business, financialcondition, results of operations and prospects.

13

IMPORTANT INFORMATION ABOUT THIS REGISTRATION DOCUMENT

No person is or has been authorised to give any information or to make any representation not contained in ornot consistent with this Registration Document and, if given or made, such information or representation mustnot be relied upon as having been authorised by the Bank. No representation or warranty, express or implied, ismade and no responsibility or liability is accepted by any person other than the Bank as to the accuracy,completeness, verification or sufficiency of the information contained herein, and nothing contained in thisRegistration Document may be relied upon as a promise or representation in this respect, as to the past, presentor future. The delivery of this Registration Document shall not, under any circumstances, create any implicationthat there has been no change in the business or affairs of the Bank since the date of this RegistrationDocument or that the information contained herein is correct as of any time subsequent to its date.

A copy of this Registration Document has been filed with, and approved by, the FCA and has been madeavailable to the public in accordance with the Prospectus Regulation Rules. This Registration Document maybe combined with a securities note and summary to form a prospectus in accordance with the ProspectusRegulation Rules. A prospectus is required before an issuer can offer transferable securities to the public orrequest the admission of transferable securities to trading on a regulated market. However, this RegistrationDocument, where not combined with the securities note and summary to form a prospectus, does not constitutean offer or invitation to sell or issue, or a solicitation of an offer or invitation to purchase or subscribe for, anysecurities in the Bank in any jurisdiction, nor shall this Registration Document alone (or any part of it), or thefact of its distribution, form the basis of, or be relied upon in connection with, or act as any inducement toenter into, any contract or commitment whatsoever with respect to any offer or otherwise. The contents of thisRegistration Document are not to be construed as legal, business or tax advice. This Registration Document isnot intended to provide the basis of any credit or other evaluation and should not be considered as arecommendation by any of the Bank, any of the Bank’s advisers or any of their affiliates or representativesregarding the securities of the Bank.

RESPONSIBILITY STATEMENT

The Bank accepts responsibility for the information given in this Registration Document and, to the best of theBank’s knowledge, the information contained in this Registration Document is in accordance with the facts andthis Registration Document makes no omission likely to affect its import.

STATUS OF THE BANK UNDER THE VOLCKER RULE

The Bank is a “covered fund” for purposes of the final rule adopted by the Board of Governors of the FederalReserve System, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, theSEC and the Commodity Futures Trading Commission, to implement section 13 of the Bank Holding CompanyAct of 1956, as amended, which was added by Section 619 of the Dodd-Frank Wall Street Reform andConsumer Protection Act (the “Volcker Rule”); and the DRs are “ownership interests”, as defined under theVolcker Rule. The Volcker Rule generally prohibits “banking entities” (which is broadly defined to includeU.S. banks and bank holding companies and many non-U.S. banking entities, together with their respectivesubsidiaries and other affiliates) from (i) engaging in proprietary trading, (ii) acquiring or retaining an“ownership interest” in or sponsoring a “covered fund” and (iii) entering into certain relationships with anysuch funds. Any prospective investor, including a U.S. or foreign bank or a subsidiary or other affiliate thereof,should consult its own legal advisers regarding the matters described above and other effects of the VolckerRule.

ENFORCEABILITY OF JUDGMENTS

The Bank is a supranational financial institution organised under an Establishment Agreement, which wasregistered with the United Nations as an international treaty in October 1995. In addition, none of the Board ofDirectors and members of the Bank’s Senior Management is a resident of the United States, and all or asubstantial portion of the assets of the Bank and such persons are located outside the United States. As a result,it may not be possible for investors to effect service of process within the United States upon the Bank or suchpersons or to enforce against any of them in the United States courts judgments obtained in United Statescourts, including judgments predicated upon the civil liability provisions of the securities laws of the UnitedStates or any State or territory within the United States.

14

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Registration Document includes forward-looking statements. The words “anticipate”, “believe”, “expect”,“plan”, “intend”, “targets”, “aims”, “estimate”, “project”, “will”, “would”, “may”, “could”, “continue” andsimilar expressions are intended to identify forward-looking statements. All statements other than statements ofhistorical fact included in this Registration Document, including, without limitation, those regarding the Bank’sfinancial position, business strategy, management plans and objectives for future operations, are forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties andother factors, which may cause the Bank’s actual results, performance or achievements, or industry results, tobe materially different from those expressed or implied by these forward-looking statements. These forward-looking statements are based on numerous assumptions regarding the Bank’s present and future businessstrategies and the environment in which the Bank expects to operate in the future. Important factors that couldcause the Bank’s actual results, performance or achievements to differ materially from those in the forward-looking statements include, among other factors referenced in this Registration Document:

• political, economic and legal risks and uncertainties in the countries where the Bank operates,

• general economic conditions and slowdown in the economic and business activity of key clients,

• changes in the competitive markets in which the Bank operates,

• disruption or increased costs of financing,

• regulatory changes or costs of compliance with current and future environmental regulations in thejurisdictions where the Bank operates,

• availability and costs of financing,

• exchange rate fluctuations,

• the creditworthiness of the Bank’s customers,

• litigation the Bank may be involved in from time to time,

• trade restrictions or other changes to economic policy in countries in which the Bank operates,

• the Bank’s debt service obligations,

• risks associated with the Bank’s capital structure,

• the Bank’s ability to raise future financing, and

• force majeure and other unforeseeable events.

Additional factors that could cause actual results, performance or achievements to differ materially include, butare not limited to, those discussed under “Risk Factors” and “Operating and Financial Review”. Forward-looking statements speak only as of the date of this Registration Document and the Bank expressly disclaimsany obligation or undertaking to publicly update or revise any forward-looking statements in this RegistrationDocument to reflect any change in the Bank’s expectations or any change in events, conditions orcircumstances on which these forward-looking statements are based unless required to do so by applicable law,the Prospectus Regulation Rules, the Listing Rules, the Disclosure Guidance and Transparency Rules of theFCA or EU Market Abuse Regulation (EU) 596/2014. Given the uncertainties of forward-looking statements,the Bank cannot assure you that projected results or events will be achieved and the Bank cautions you not toplace undue reliance on these statements.

15

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Presentation of Financial Information

The financial information of the Bank set out in this Registration Document as at and for the years ended31 December 2016, 2017 and 2018 has, unless otherwise stated, been derived from the special purpose auditedfinancial statements of the Bank as at and for the years ended 31 December 2016 and 31 December 2017 (the“2016-2017 Special Purpose Financial Statements”) and as at and for the years ended 31 December 2017 and31 December 2018 (the “2017-2018 Special Purpose Financial Statements”, and together with the 2016-2017Special Purpose Financial Statements, the “Annual Special Purpose Financial Statements”). The AnnualSpecial Purpose Financial Statements were prepared in accordance with IFRS as issued by the InternationalAccounting Standards Board (“IFRS”). The selected condensed interim special purpose financial informationof the Bank set out in this Registration Document as at and for the six months ended 30 June 2018 and 30 June2019 has, unless otherwise stated, been derived from the unaudited condensed interim special purpose financialstatements of the Bank as at and for the six months ended 30 June 2018 and 30 June 2019 prepared inaccordance with the International Accounting Standard 34, Interim Financial Reporting (“IAS 34”) (the“Condensed Interim Special Purpose Financial Statements” and, together with the Annual Special PurposeFinancial Statements, the “Special Purpose Financial Statements”). The Special Purpose FinancialStatements, together with the related reports, are set forth on pages F-2 to F-145 in this Registration Document.

With effect from 1 January 2018, the Bank adopted IFRS 9, Financial Instruments (“IFRS 9”) and IFRS 15,Revenue from Contracts with Customers (“IFRS 15”). The Bank has determined that the adoption of IFRS 15did not have a material impact on the Special Purpose Financial Statements. The impact of the adoption ofIFRS 9 as at 31 December 2017 was reflected in the retained earnings as at 1 January 2018 as allowed as a firsttime implementation in accordance with IFRS. Any adjustment to account for changes between IAS 39,Financial Instruments: Recognition and Measurement (“IAS 39”) and IFRS 9 at the transition date wererecognised in the opening retained earnings and other reserves of the 2017-2018 Special Purpose FinancialStatements. The 2016-2017 Special Purpose Financial Statements have not been restated to reflect the changesfrom the application of IFRS 9. The 2016-2017 Special Purpose Financial Statements applied IAS 18, Revenue(“IAS 18”) and IAS 39, which were the accounting standards in effect at the time of preparation of the 2016-2017 Special Purpose Financial Statements. Therefore, due to the adoption of IFRS 9 and IFRS 15, the 2017-2018 Special Purpose Financial Statements are not directly comparable with the 2016-2017 Special PurposeFinancial Statements.

The Bank has applied IFRS 16 from its mandatory adoption date of 1 January 2019. The Bank has applied it ina practical expedient manner on initial application. Where the lease term is less than 12 months or leases are oflow value items, the Bank has elected to use the short-term lease exemption. The Bank’s activities as a lessor /lessee are not material.

Independent Auditors

As at the date of this Registration Document, the auditors of the Bank are KPMG Hazem Hassan of SmartVillage—Building 105, Km 28 Cairo Alex Desert road, Giza, Egypt (certified Public Accountants and amember of the International Federation of Accountants) (“KPMG”).

The Annual Special Purpose Financial Statements included in this Registration Document have been audited byKPMG, independent auditors, as stated in their reports appearing herein and which include emphasis of matterparagraph drawing attention to the basis of preparation of the Special Purpose Financial Statements andrestriction of use of the report.

With respect to the Condensed Interim Special Purpose Financial Statements, KPMG reported that they appliedlimited procedures in accordance with professional standards for a review of such information. However, theirseparate report, included herein, states that they did not audit and they do not express an opinion on thatinterim financial information. Accordingly, the degree of reliance on their report on such information should berestricted in light of the limited nature of the review procedures applied. See also “—Review of CondensedInterim Special Purpose Financial Statements”.

Currency

Throughout this Registration Document, unless stated otherwise, the following definitions are used:

• “€”, “EUR” or “euro” means the lawful currency for the time being of the member states of the EuropeanUnion that adopted the single currency in accordance with the Treaty of Rome establishing the EuropeanEconomic Community, as amended;

16