Embed Size (px)

Citation preview

The Agricultural Credit Policy Council:

Celebrating 30 Years of Bringing Credit Closer to Poor

Farmers and Fisherfolk

Paper presented by ACPC Executive Director Jovita M. Corpuz for the 2016 ACPC-APRACA Policy Forum on Microinsurance and Microbanking, and ACPC’s 30th

Anniversary Celebration

28-29 April 2016, Novotel, Araneta Center, Cubao Quezon City, Philippines

2

The Agricultural Credit Policy Council:

Celebrating 30 Years of Bringing Credit Closer to Poor

Farmers and Fisherfolk1

Prepared by Jovita M. Corpuz2 and Ferdinand L. Paguia3

I. Overview of Agricultural Credit in the Philippines

Increasing the flow of financial services to the rural sector and improving access

of small farmers and fisherfolk to formal credit remain a formidable challenge. ACPC

estimated credit demand for priority commodities of the Department of Agriculture

(DA) to be almost PHP 522 billion (USD 11.31 billion)4 in 2014 but the amount supplied

by banks for production of these commodities in the same year was only PHP 158

billion (USD 3.42 billion), leaving a credit gap of PHP 364 billion (USD 7.88 billion). In

spite of the huge demand for credit, loans released by government and private banks to

the agri-fishery sector account for only about 2.0 percent of their total loan portfolio, of

which 0.6 percent went to loans for agricultural production. Hence, while banks are

reported to be awash with cash for lending, the credit demand of the sector is not

served. Many banks continue to shy away from lending to the agri-fishery sector,

particularly to small farmers and fisherfolk. A large proportion of small farmers and

fisherfolk still have very limited access to formal credit, particularly from banks. A

1 Paper presented by ACPC Executive Director Jovita M. Corpuz during the 2016 ACPC-APRACA Policy Forum on Microinsurance and Microbanking, and ACPC’s 30th Anniversary Celebration, 28-29 April 2016, Novotel, Araneta Center, Cubao, Quezon City, Philippines 2 Executive Director of the Agricultural Credit Policy Council (ACPC) 3 Division Chief, Policy Research and Planning Division, ACPC 4 1 USD + 46.1586 PHP, XE Currency Converter, 18 April 2016

3

survey conducted by ACPC in 2014 revealed that 53% of farmers and fisherfolk

obtained their loans from formal sources. The rest borrow from private lenders usually

at usurious rates.

II. The ACPC: Rising to the Challenge of Increasing Access to Credit of Small

Farmers and Fisherfolk

The Agricultural Credit Policy Council (ACPC) was created in 1986 by virtue of

Executive Order 113 and attached to the Department of Agriculture in 1987 by virtue of

Executive Order No. 116. The ACPC plays a unique and critical strategic role in

addressing the challenge of increasing access to credit of small farmers and fisherfolk. It

is the only government agency tasked and with the legal authority to synchronize all

agricultural credit policies and financing programs of the government to ensure a well

coordinated and continually responsive strategy and intervention in agricultural

finance. This contributes in attaining the agricultural development goals of the

government as well as in equalizing economic development opportunities in the

agriculture and fisheries sector. The following highlights the significant contributions of

ACPC for the past 30 years in improving access of small farmers and fisherfolk to formal

credit:

2.1 Played a significant role in establishing a market-based policy framework

for agricultural finance to sustain continuous credit delivery to small

farmers and fishers

4

Before ACPC’s creation in 1986, agricultural finance policy was in a state of

disarray. Agricultural credit was largely subsidized, supply-led, and commodity-specific.

Government non-financial agencies provided low-costs credit, edging out private

financial institutions. The benefits of subsidized credit were short-lived. Eventually,

farmers defaulted on their loans. Worse, a large number of rural banks went bankrupt

because they relied heavily on cheap government funds and abandoned savings and

deposit mobilization. Through the years, ACPC was actively involved in initiating a

series of reforms in rural finance policy which eventually resulted in the enactment of

the Agriculture and Fisheries Modernization Act (AFMA) of 1997.

The AFMA aims to transform agriculture into a productive and competitive

sector to enable farmers and fisherfolk to meet the challenge of globalization. The Law

covers the many elements critical to agricultural modernization such as research and

development, infrastructure, training, marketing and credit, among others. Explicit in

the Law is the recognition that all these elements must be made available in a

simultaneous and holistic fashion in order to successfully achieve agricultural

profitability. With regard to finance, the AFMA institutionalized market-based policies

on agricultural and rural finance for a sustainable delivery of credit to the marginalized

sectors in agriculture.

Considering lessons learned from the past twenty years, the emphasis of the

AFMA with respect to agricultural and fisheries finance is on the proper management

and utilization of credit, espousing market-based policy principles that include the

following:

5

1. Greater role of the private sector (including rural banks, cooperative rural

banks, cooperatives and NGOs) and government financial institutions (GFIs)

in the provision of financial services;

2. Non-participation of government non-financial agencies (GNFAs) in the

implementation of credit programs and focus instead on providing a

conducive policy environment, critical support and capability-building

services that would facilitate increased participation of the private sector in

the provision of financial services;

3. Adoption of market-determined interest rates to (a) ensure the recovery of

lending costs; (b) sustain the availability of credit funds; and (c) enhance the

outreach of financing assistance to the sector; and

4. Phase-out of all government subsidized credit programs on agriculture and

collection/consolidation of remaining loanable funds and loan receivables

into the Agro-Industry Modernization Credit and Financing Program

(AMCFP).

The Agro-Industry Modernization Credit and Financing Program (AMCFP). As

provided for in the AFMA, all subsidized credit programs of the government for

agriculture were to be terminated and replaced by the AMCFP as the umbrella credit

program of the Department of Agriculture. The ACPC was tasked to take the lead in

developing a system whereby government credit resources are administered more

efficiently through the AMCFP. The following features make the AMCFP different from

6

the past credit programs of the government: (i) it is demand-driven and not supply-led;

(ii) it is not commodity-specific but covers a whole gamut of income-generating projects

which farm households may choose to undertake; (iii) the government is not involved in

any credit decision-making as the program is implemented as a two-step loan program

with government financial institutions as wholesalers and qualified private banks as

retailers; and (iv) it adopts market-determined rates as opposed to the subsidized rates

of the past.

ACPC serves as the oversight body of the AMCFP and as such is tasked to steer

program implementation, address policy issues, and monitor and evaluate fund

utilization and overall program performance. It is the job of ACPC to ensure that the

AMCFP fund is utilized for the intended beneficiaries of credit programs in support of

the DA’s priority programs and that the fund is sustained for continued program

implementation. To equip itself with empirical data necessary for program evaluation

and policy formulation, the ACPC undertakes related policy and action research studies.

ACPC is also tasked to implement institutional capacity building (ICB) activities for its

partner rural financial institutions including cooperatives and farmer organizations;

and design and pilot innovative financing schemes (IFS) as mandated by RA 7607 or the

Magna Carta for Small Farmers.

Since the AMCFP started operations in 2003, its credit facilities – both existing

and those already terminated – were able to generate more than PHP 10 billion (USD

217 million) in loans to 287,000 farmers and fisherolk.

7

2.2 Took the initiative of collecting past due loans of terminated credit programs

As mandated by the AFMA, the AMCFP should have been appropriated the

amount of PHP 2.0 billion (USD 43.3 million) for its first year of implementation and

PHP 1.7 billion (USD 36.8 million) every year for the next six years thereafter for a total

allocation of PHP 12.2 billion (USD 264.3 million) [Sec. 111, AFMA]. Since the AMCFP

started operating in 2003, however, only PHP 3.0 billion (USD 65 million) has been

released by the national government, namely PHP 1.0 billion (USD 21.7 million) in 2013

and PHP 2.0 billion (USD 43.3 million) in 2015. Before this, the AMCFP was funded out

of the remaining loanable funds and past due loans from terminated agricultural

directed credit programs (DCPs) which ACPC took the initiative to collect. The job of

collecting these loans were first offered to GFIs but was turned down. Through its

vigorous collection efforts, ACPC has been able to collect almost PHP 1.7 billion (USD

36.8 million) in loans out of the PHP 6.4 billion (USD 138.6 million) loan receivables

from DCPs.

2.3 Developed and pioneered innovative financing schemes (IFS) for small

agricultural households, especially for borrowers that have no access to

formal financing and have limited assets to offer as collateral.

With the market-based policy framework in place, ACPC then set out to work on

developing and piloting innovative financing schemes (IFS) and capacity building

programs to be integrated into the AMCFP if found successful. These schemes are

specifically directed at small farmers and fisherfolk that could not access loans from

formal sources because they have insufficient assets to offer as collateral. These IFS are

8

generally collateral-free and cashflow-based. Among the successful IFS piloted by ACPC

that are now integrated as regular programs under the AMCFP are the Sikat-Saka

Program, Agricultural Microfinance Program (AMP) and Cooperative Banks Agricultural

Lending Program (CBAP). Below are brief descriptions of these and other existing

programs under the AMCFP:

Sikat-Saka Credit Program for Rice and Food Staples. In the interest of

attaining self-sufficiency in food staples, an integrated financing program named 'Sikat-

Saka' was launched in January 2012. This is a joint program of the DA, ACPC, and the

Land Bank of the Philippines. Sikat-Saka provides small farmers direct access to credit

through their respective irrigator’s associations (IAs) to be used for palay production.

Under this scheme, farmers are provided a lower interest rate of 15% per annum for the

first two cycles. Then, for succeeding cycles, the rate goes down by 1% per cycle.

Reduced interest rates are also given for those who fully pay their production loan on

time. To familiarize farmers in the use of 'modern' banking technology, loans are being

released though automated teller machines (ATMs).

To complement credit delivery, technical support is being extended to farmer-

beneficiaries in the form of: (i) extension and training from the Agricultural Training

Institute (ATI); (ii) processing and market linkage from the National Agribusiness

Corporation (NABCOR) and the National Food Authority (NFA); and (iii) organizational

support to potential IAs from the National Irrigation Administration (NIA). The program

was pilot-tested for one (1) year or two (2) cropping cycles in the four (4) major rice-

producing provinces of Isabela, Nueva Ecija, Iloilo and North Cotabato. The program has

since been extended to include 25 major rice-producing provinces nationwide. The

9

target areas include municipalities that still remain unserved by LandBank. As of

December 31, 2015, Sikat Saka has released nearly PHP 2.62 billion (USD 56.7 million)

in loans to 13,794 rice farmers.

Agricultural Microfinance Program (AMP). Launched in April 2009, the AMP

provides short-term loans for income-generating livelihood activities – whether farm,

off-farm, or non-farm – of small farming and fishing households. The AMP is being

implemented in partnership with the People’s Credit and Finance Corporation (PCFC)

which lends to small farming and fishing households through its network of

microfinance institutions (MFIs) composed of cooperatives, cooperative banks, rural

banks, non-government organizations and people’s organizations. Eligible projects for

financing include: (i) agricultural value chain activities (e.g., production, processing,

marketing); and (ii) microfinance income-generating livelihood activities (e.g., farm, off-

farm and non-farm) of agricultural households. Interest rate on loans are market-

determined and repayment schedule is cash flow-based. As of December 31, 2015, PHP

1.13 billion (USD 24.5 million) in loans have been released by PCFC’s accredited MFIs to

96,676 small farming and fishing households.

Cooperative Banks Agricultural Lending Program (CBAP). Launched in September

2011, CBAP is being implemented in partnership with cooperative banks. This program

employs a ‘depository mode’ of credit delivery wherein special time deposits (STDs) are

placed directly in partner cooperative banks, eliminating the need for a wholesaler,

resulting in lower pass-on rates to small farmers and fisherfolk. CBAP aims to provide

stable, low-cost funding support to cooperative banks that have demonstrated capacity

to continually provide agricultural loans to small farmers and fisherfolk. Eligible farmer

10

and fisherfolk borrowers are charged pass-on rates of not more than 15% per annum,

for either agricultural production or microfinance loans. Commodities financed under

the program are rice, corn, high value commercial crops, fishery and other commodities

prioritized by the DA. As of December 31, 2015, almost PHP 3.0 billion (USD 65 million)

in loans has been released by ACPC’s cooperative bank partners to 57,564 farmer and

fisherfolk borrowers under the depository mode scheme.

Direct Market Linkage Development Program (DMLDP). The DMLDP aims to

increase the capability of small farmers and fisherfolk to directly link or access the

demand centers of agricultural commodities. It is jointly being implemented by the DA-

Agribusiness Marketing Assistance Service (AMAS) and ACPC. The program utilizes an

integrated approach, providing support in the form of training, technical assistance,

financial access, storage and trading of vital commodities to targeted client groups

including small farmers and fisherfolk and other players in the value chain who have

little or no access to formal borrowing. To date, the program has provided financial

assistance to 38 farmers and fisherfolk associations, cooperatives, agri-based

enterprises, and individual farm producers. Total amount released to these proponents

amounted to nearly PHP 128 million (USD 2.7 million) benefiting 3,304 small farmers

and fisherfolk.

Upland Southern Mindanao – Credit and Institution Building Program (USM-CIBP).

This program is the successor to the rural finance component of the DA-European Union

Upland Development Program (UDP) for Southern Mindanao which terminated in 2007.

Management of the USM-CIBP was turned over to the DA-ACPC. The USM-CIBP covers

the provinces of Compostela Valley, Davao Oriental, Davao del Sur, Davao del Norte,

11

Sarangani and Southern Cotabato. The program has two (2) components, namely: (a)

cooperative component implemented by Land Bank; and (b) microfinance component

implemented by ACPC.

The cooperative component provides continuous credit and capacity building

assistance to the 28 cooperatives previously being assisted by the UDP. The objective is

to improve the viability and creditworthiness of these cooperatives and eventually

mainstream them into formal financial institutions such as the Land Bank. Capacity

building assistance focuses on strengthening the cooperatives through a package of

training, coaching and mentoring, systems installation, and other capacity building

activities such as Lakbay-Aral, market linkage, business alliance with other

cooperatives. These interventions are designed to strengthen to enhance the capacity of

these cooperatives to conform to the accreditation criteria of Land Bank. Credit support

is also provided through a hold-out deposit, a guarantee mechanism which assumes

100% risk due to default. As of March 2016, four (4) cooperatives were able to access

credit from Land Bank amounting to PHP 13.5 million (USD 288,681.00)

The microfinance component likewise offers a risk coverage or guarantee

package to participating MFIs as incentive for them to lend to micro-businesses and

small farmers in selected upland areas in the priority provinces. Further, MFIs that have

availed of two (2) tranches of risk coverage and released loans to beneficiaries, the

program provides funding assistance for the conduct of management and leadership

training of officers and staff of the MFI to enhance their skills in undertaking and

managing credit programs and improving their financial systems. As of March 2016,

12

loans generated amounted to PHP 18.7 million (nearly USD 400,000.00) benefiting

2,154 farmers.

2.4 Facilitated the continuous provision of institutional capacity building (ICB)

for farmer and fisherfolk organizations; and staff development program for

ACPC personnel.

ACPC believes that credit will not work alone. An essential component of its

credit programs, ACPC’s institutional capacity building (ICB) program assists farmer

and fisherfolk cooperatives and organizations in improving their capabilities for

delivering financial services to their members and links them to partner financial

institutions of ACPC. Assistance in the form of grants is provided by ACPC to federations

of cooperatives and NGOs which are capable of managing the ICB activities (e.g. training,

coaching) or through outsourcing via training institutions, and State Colleges and

Universities (SCUs) in the targeted areas. From 2001 to 2015, about 50,464 officers

and members of 5,425 farmer and fisherfolk organizations were able to participate in

1,455 ICB activities facilitated by ACPC together with its partner training institutions.

ACPC also believes that the success of any organization depends greatly on its

human resources. Thus, the professional development of its personnel has always been

a major consideration of ACPC, ensuring that they are well equipped to effectively and

efficiently deliver the tasks assigned to them. Key officers and technical staff are

regularly being sent to both local and international training which include study visits in

other countries to gain perspective and insight on innovations and strategies in

agricultural finance, and local seminars, courses and workshops which recently include

13

web technologies, financial education and micro-insurance, enterprise architecture and

e-services strategic planning, information and communication technology, and best

practices of cooperative banks.

2.5 Was instrumental in crafting, and advocating the passage into law, of

Republic Act 10000 or the Revised Agri-Agra Reform Credit Act of 2009.

Republic Act 10000 or the Agri-Agra Reform Credit Act of 2009, which was

signed in February 23, 2010, is the amended version of Presidential Decree 717 or the

“original” Agri-Agra Law. Like its predecessor, RA 10000 requires banks to allocate

25% of their loan portfolio to agricultural and agrarian reform credit. However, the

alternative modes of compliance have been amended to eliminate those that are non-

agricultural in nature such as loans or investment in socialized housing and government

securities. At the same time, the types of agricultural-based loans that can be counted as

compliance were expanded. For instance, banks can now comply with the agri-agra

lending quota via the following modes of compliance: (i) investment in the AMCFP; (ii)

wholesale lending to non-bank rural financial institutions (NBRFIs) such as

cooperatives and farmer organizations providing credit to small farmers and fishers;

and (iii) purchase of agri-agra debt securities. Another new feature in the law is the

increase in the sanctions and penalties for non-compliance and under-compliance by

banks to the law. RA 10000 now requires an “erring” bank to pay an amount equivalent

to 0.5% of the total amount of its non-compliance or under-compliance. Also, the bulk of

penalty collections (90%) will form part of the credit guarantee and insurance funds for

agriculture and agrarian reform lending.

14

The enactment of RA 10000 is a major policy breakthrough for the DA and the

ACPC, which have long been advocating for the removal of alternative modes of

compliance that do not directly benefit agriculture, and the expansion of the types of

agricultural loans that can be considered as eligible compliance under the law.

2.6 Sourced out additional funding to beef up the AMCFP fund base for

agricultural lending, resulting in the fresh budgetary allocation of PHP 3.0

billion (USD 65 million) by the national government in CY 2013 and CY 2015.

Since the AMCFP started operations in 2003, its credit facilities were able to

release a cumulative total of more than PHP 10 billion (USD 217 million) in loans to

287,000 farmers and fisherolk. However, this is only 2.0 percent of the estimated credit

demand of PHP 522 billion (USD 11.31 billion).

Fortunately, vigorous advocacy efforts of ACPC and various farmer and fisherfolk

groups have convinced the national government to provide additional credit funds

totaling PHP 3.0 billion (USD 65 million) in 2013 (PHP 1.0 billion) and 2015 (PHP 2.0

billion) for the establishment of a flexible lending facility for small farmers and

fisherfolk. In this regard, the Agri-Fishery Financing Program (AFFP) was developed to

help contribute to the attainment of inclusive growth through financial inclusion of the

unbanked and under-banked sectors in agriculture. The target beneficiaries of the AFFP

are the farmers and fisherfolk that are already registered under the Registry System for

Basic Sectors in Agriculture (RSBSA). The RSBSA is a nationwide database of

information on farmers, farm laborers, and fisherfolk which may be used as a tool in

15

efficiently carrying out the delivery of basic services, provisioning for adequate

facilities, and forms of subsidy and aid relative to the agriculture and fisheries sector.

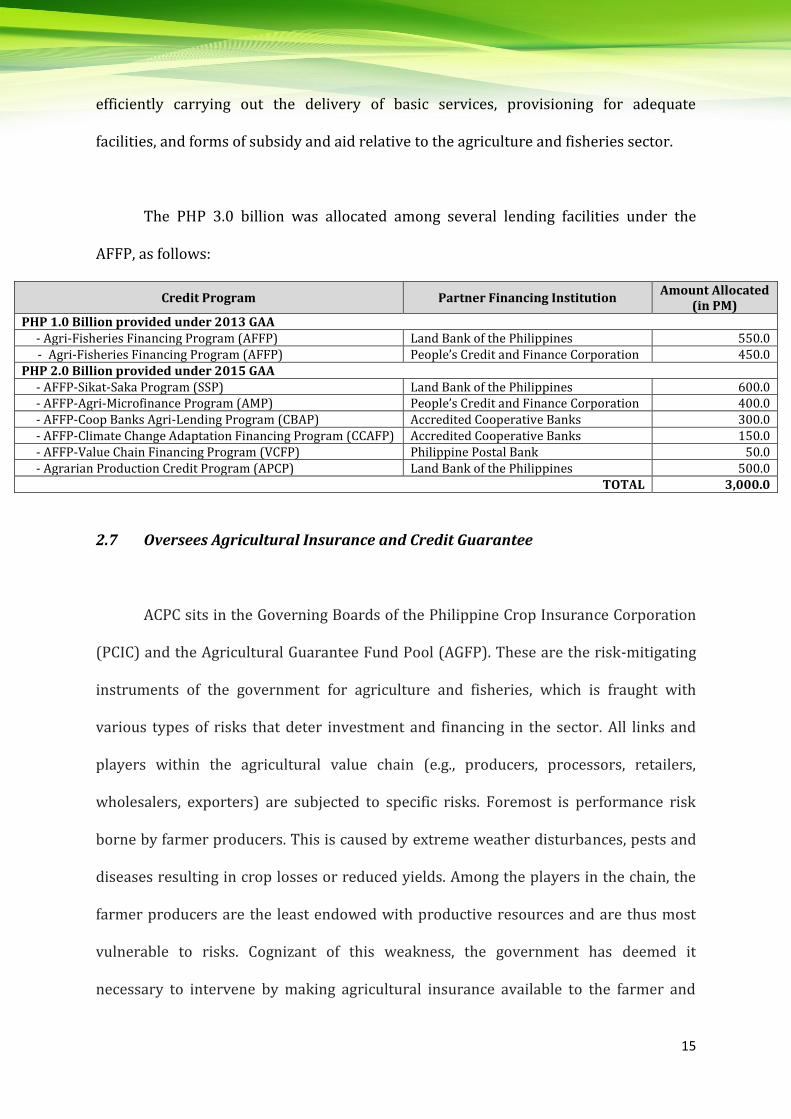

The PHP 3.0 billion was allocated among several lending facilities under the

AFFP, as follows:

Credit Program Partner Financing Institution Amount Allocated

(in PM) PHP 1.0 Billion provided under 2013 GAA - Agri-Fisheries Financing Program (AFFP) Land Bank of the Philippines 550.0

- Agri-Fisheries Financing Program (AFFP) People’s Credit and Finance Corporation 450.0 PHP 2.0 Billion provided under 2015 GAA - AFFP-Sikat-Saka Program (SSP) Land Bank of the Philippines 600.0 - AFFP-Agri-Microfinance Program (AMP) People’s Credit and Finance Corporation 400.0 - AFFP-Coop Banks Agri-Lending Program (CBAP) Accredited Cooperative Banks 300.0 - AFFP-Climate Change Adaptation Financing Program (CCAFP) Accredited Cooperative Banks 150.0 - AFFP-Value Chain Financing Program (VCFP) Philippine Postal Bank 50.0 - Agrarian Production Credit Program (APCP) Land Bank of the Philippines 500.0

TOTAL 3,000.0

2.7 Oversees Agricultural Insurance and Credit Guarantee

ACPC sits in the Governing Boards of the Philippine Crop Insurance Corporation

(PCIC) and the Agricultural Guarantee Fund Pool (AGFP). These are the risk-mitigating

instruments of the government for agriculture and fisheries, which is fraught with

various types of risks that deter investment and financing in the sector. All links and

players within the agricultural value chain (e.g., producers, processors, retailers,

wholesalers, exporters) are subjected to specific risks. Foremost is performance risk

borne by farmer producers. This is caused by extreme weather disturbances, pests and

diseases resulting in crop losses or reduced yields. Among the players in the chain, the

farmer producers are the least endowed with productive resources and are thus most

vulnerable to risks. Cognizant of this weakness, the government has deemed it

necessary to intervene by making agricultural insurance available to the farmer and

16

subsidizing part of the premium for key commodities, namely rice and corn.

Government has also developed another intervention in the form of credit guarantee,

wherein the government pays the financing institution a certain percentage of their loan

exposure to small farmer borrowers in case of loan default. Credit guarantee is

intended to encourage formal financing institutions to lend to small farmer borrowers

and increase their access to formal credit.

The following sections briefly discuss the insurance programs of PCIC and the

AGFP as risk management facilities for the agriculture sector:

2.7.1 Insurance programs of the Philippine Crop Insurance Corporation (PCIC)

Because of the increasing vulnerability of the agriculture sector, particularly the

small farming community, to typhoons and other natural disasters, the Philippine Crop

Insurance Corporation (PCIC) was created via Presidential Decree No. 1467 on 11 June

1978. The PCIC is mandated to provide insurance protection to the country’s

agricultural producers, particularly the subsistence farmers, against loss of crops

and/or non-crop agricultural assets on account of natural calamities such as typhoons,

floods, droughts, earthquakes, volcanic eruptions, plant pests and diseases, and other

perils. PCIC currently has regular insurance programs for rice and corn, high value

commercial crops, livestock, fisheries, non-crop agricultural assets, and term-insurance

programs (e.g. life and non-life insurance). It is also implementing a special program, a

fully subsidized agricultural insurance program for agrarian reform beneficiaries

(ARBs) and their household members.

17

The performance of PCIC continues to improve each year. For 2015, significant

strides were made in terms of amount of insurance coverage, number of insured

farmers, and payment of claims. A total of 1.12 million farmers were insured, 22%

higher than the 917,814 farmers in 2014. Amount of insurance covered increased by

7% to PHP 38 billion (USD 822.7 million) from PHP 35.6 billion (USD 770.7 million) in

2014. PCIC paid PHP 1.1 billion (USD 23.8 million) in claims, nearly 50% higher than the

PHP 738 million (USD 16 million) paid in 2014. Some 13,284 farmers were paid, 29%

more than the 87,855 farmers paid in 2014. The improved performance of PCIC in 2015

is due in part to the PHP 1.3 billion (USD 28.2 million) premium subsidy provided by the

national government for farmers registered in the RSBSA. PCIC is implementing the

RSBSA Agricultural Insurance Program (RSBSA-AIP) which provides free insurance to

RSBSA-registered farmers. In spite of the improving coverage of PCIC, however, the 1.12

farmers insured represent only about 11% of the total farmers registered in the RSBSA.

The government needs to infuse additional capital funds and premium subsidy into

PCIC for the provision of free insurance to more farmers.

2.7.2 The Agricultural Guarantee Fund Pool (AGFP)

The Agricultural Guarantee Fund Pool (AGFP) Program was established in May

2008 for the purpose of facilitating the provision of credit in agriculture by mitigating

the risks involved in lending to the sector. The AGFP started operations in August 2008

with seed funding of PHP 4.48 billion (USD 103.87 million) coming from government

revenues and surplus funds of government corporations and financing institutions. The

objective is to encourage banks, cooperatives, and other lending institutions to increase

their loans to small agricultural borrowers, particularly new borrowers, and/or expand

18

their lending to existing borrowers. This is also expected to enhance food production

activities by lowering the lenders’ risks in agricultural non-collateralized lending.

The AGFP provides guarantee cover of up to 85 percent of unsecured loans

extended by financial institutions and other eligible lenders to small farmer borrowers

engaged in rice and/or other food production activities. The AGFP guarantee covers all

types of risks of default including risks due to weather, pest and diseases and other

fortuitous events, except those arising from willful default and/or fraud. In case of

default or non-repayment of the guaranteed loan by the farmer-borrower for any of the

said valid reasons, AGFP shall pay the lending institution the guaranteed portion or 85

percent of the unpaid loan. To avail of the guarantee, the participating lender shall pay a

guarantee fee of 2 percent per annum of the outstanding loan amount. Collection of

unpaid loans even if already paid by the guarantee program remains to be the

responsibility of the financial institution.

In 2015, the AGFP provided guarantee coverage for nearly PHP 5.21 billion (USD

112.8 million) loans of 101 participating financial institutions to 105,007 farmer

beneficiaries. Since the AGFP started in 2008, it has been able to provide guarantee

coverage to PHP 31.1 billion (USD 673.4 million) loans extended by participating

financial institutions to more than 745,000 small agricultural producers. A little over

PHP 895 million (USD 19.4 million) worth of guarantee claims were paid, representing

nearly 3 percent of the total loans covered by guarantee. The AGFP was able to recover

nearly PHP 247 million (USD 5.3 million) or 28 percent of the total claims paid.

19

III. The Road Ahead: What Remains to Be Done

While there is a moderate increase in the access of small borrowers to formal

credit, ACPC believes that much more can be done if it is given adequate funding and the

necessary authority in the implementation of credit programs. For faster mobilization of

credit funds, for instance, the AMCFP should not be limited to providing wholesale loans

only to GFIs and GOCCs. The program should have the option of engaging directly, or

placing funds directly in other rural financial institutions including private banks such

as rural banks, commercial banks and thrift banks as well as viable cooperatives and

non-government organizations (NGOs) that have the capacity and maturity to provide

credit to small farmers and fisherfolk. For these proposed measures to be instituted,

however, policies such as the AMCFP implementing guidelines and the credit chapter of

the AFMA law need to be amended. With the expansion of ACPC’s functions resulting

from these measures, the subsequent need for additional manpower and resources will

likewise require an institutional or organizational restructuring over the long term. This

measure will entail an amendment of ACPC’s legal mandates.