Embed Size (px)

Citation preview

The Annual Meeting of the Representatives of the Nordic and Baltic SAI’s

Lithuania, Vilnius, September, 2004

WORKING GROUP

REVENUE AUDIT

JOINT/ SIMULTANEOUS AUDITING OF STATE REVENUE / COOPERATION BETWEEN TAX

ADMINISTRATORS IN THE FIELD OF COMBATING VALUE ADDED TAX FRAUD

Presentation of A. Juozulynas, the NAO of Lithuania

From Draft Resolution on Good Co-operation Practice Guide (2004) prepared by Joint Working

Group on Audit Activities of SAI’s of the Central and Eastern European Countries, Cyprus, Malta, Turkey.

● Recognition of the usefulness of joint audits as a way of developing and implementing new audit methods and techniques and the value of small-

scale, concrete co-operation on specific audit activities

EXTERNAL FORCES FOR

JOINT/SIMULTANEOUS AUDIT

• EU enlargement, new forms of VAT fraud

• Globalization

• Fiscal implications (loss of significant state revenue)

• Need to improve public governance

INTERNAL FORCES FOR JOINT/ SIMULTANEOUS AUDIT

• Need to strengthen capacity and professional development of SAI’s

• Need to share skills and experience

• Need to recognize and learn from the different audit methods in other SAI’s

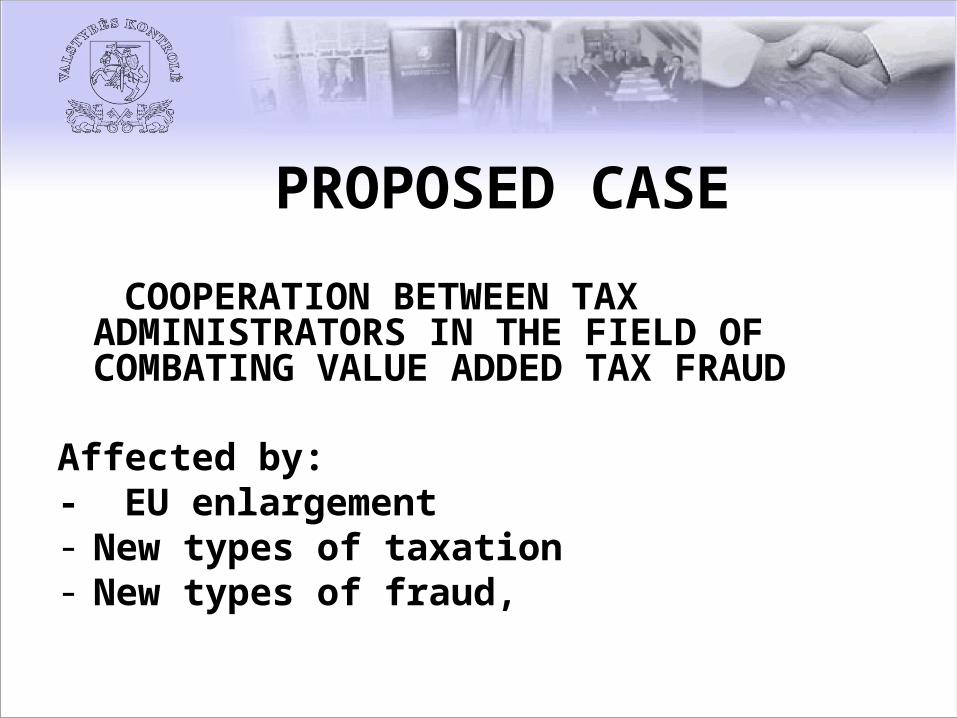

PROPOSED CASE

COOPERATION BETWEEN TAX ADMINISTRATORS IN THE FIELD OF COMBATING VALUE ADDED TAX FRAUD

Affected by: - EU enlargement- New types of taxation- New types of fraud,

VAT FRAUD IN INTRA-COMMUNITY TRADE

What’s new in the area of VAT from perspective of new Member states:

VAT is not paid on importation to the Treasury. The importer puts the input VAT and the output VAT in VAT return.

VAT FRAUD SCHEME IN INTRA-COMMUNITY TRADE

EXTEND OF VAT FRAUD - TAX LOSSES

• Up to 10 % of VAT revenue• In terms of Lithuanian Budget it would be 110

millions euro a year• In some Member states it would be up to 12

billion euro• Increasing tendency

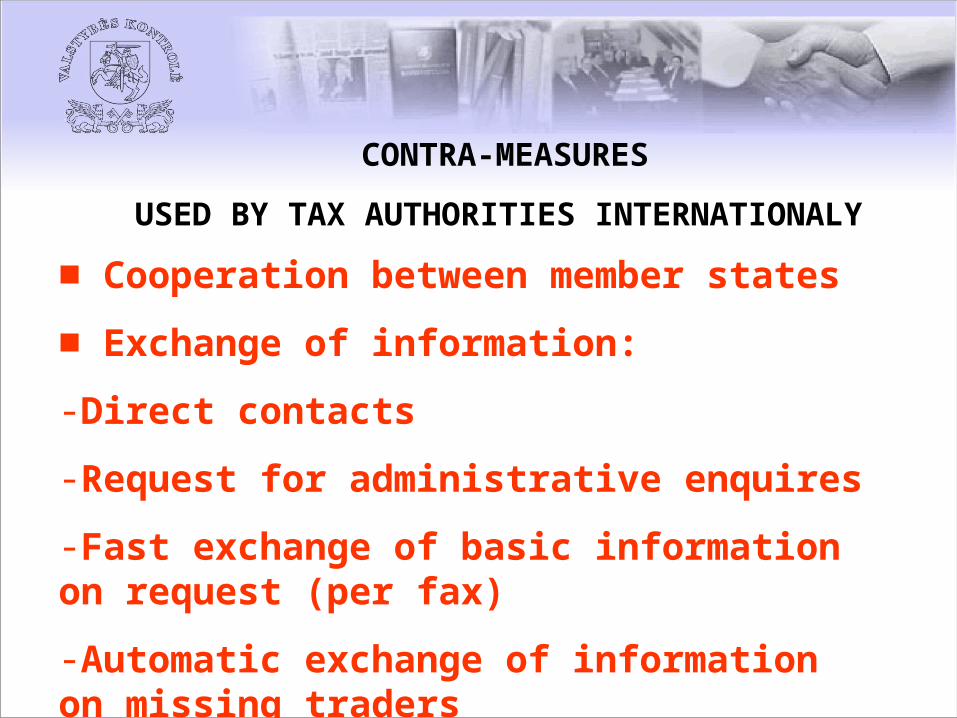

CONTRA-MEASURES

USED BY TAX AUTHORITIES INTERNATIONALY ■ Cooperation between Member states

■ Exchange of information:

-Direct contacts

-Request for administrative enquires

-Fast exchange of basic information on request (per fax)

-Automatic exchange of information on missing traders

CONTRA-MEASURES

USED BY TAX AUTHORITIES INTERNATIONALY ■ Cooperation between member states

■ Exchange of information:

-Direct contacts

-Request for administrative enquires

-Fast exchange of basic information on request (per fax)

-Automatic exchange of information on missing traders

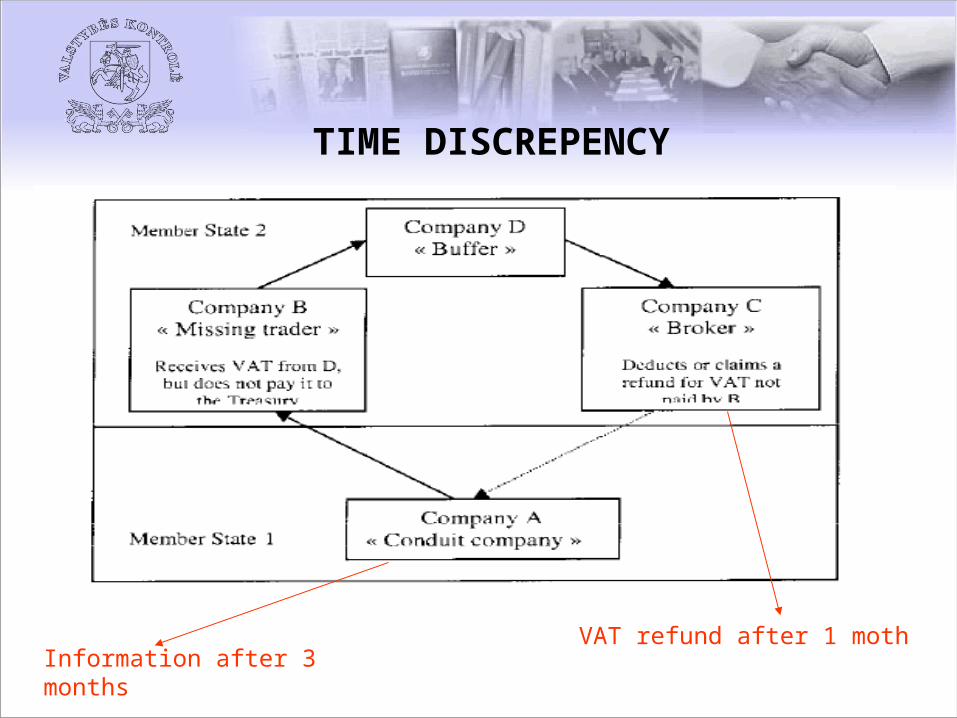

TIME DISCREPENCY

Information after 3 months VAT refund after 1 moth

INTENSITY

• Statistical data of first half of 2004 Lithuania:- 42 % of VAT receipts are refunded back or

transferred to cover other tax liabilities – 385 million euro a half year

- 85 thousand requests to pay back VAT excess or trasfer it to other taxes

JOINT AUDIT VERSUS SIMULTANEOUS AUDIT

Joint audit – where key decisions are shared, work is done by one audit team and one report is prepared for presentation to each respective Parliament or governing body

Simultaneous audit – an audit where key decisions are shared, work is done by national audit teams and national reports are prepared for presentation to national respective Parliament or governing body by national teams

A SUCCESSFUL JOINT/ SIMULTANEOUS AUDIT - 1

• To select an audit area of substance and importance.

• To develop together clear, measurable and achievable project objectives and plans for the audit activity, based on a shared understanding.

• Try and select an audit that has a high degree of good likely results.

A SUCCESSFUL JOINT/ SIMULTANEOUS AUDIT - 2

• As possible to use external expert (s) with considerable experience of joint/ simultaneous audit and technical assistance in reviewing progress audit

• To hold internal workshops to provide regular feedback at key stages

of audit (Planning, Fieldwork,

Review, Reporting)

• The role and function of the audit team should be clear and well understood from start by all involved in the activity

• Communication within the audit team should be effective and regular and the approach should be sufficiently flexible to take on board any modification needed

A SUCCESSFUL JOINT/ SIMULTANEOUS AUDIT – 3

RESULTSOF JOINT/ SIMULTANEOUS AUDIT - 1

• Strengthening the capacity and professional development of SAI’s

• Sharing of skills and experience• Passing to new external environment (EU

enlargement, new forms of VAT fraud, globalization)

RESULTSOF JOINT/ SIMULTANEOUS AUDIT - 2

• Information which is obtained in such joint activity would not normally be available in the course of purely domestic audit, and can provide additional assurance that SAI’s are performing their duties in an effective and wise way.

RESULTSOF JOINT/ SIMULTANEOUS AUDIT - 3

• Support of improvement of public governance

• Value Added: fiscal implication (gain of state revenue)

RESULTSOF JOINT/ SIMULTANEOUS AUDIT - 4

• Joint/ simultaneous audit –a rare opportunity for the SAI to demonstrate clearly the changes being made and the added value and contribution they make to the stakeholders

• Reporting toThe Baltic Assembly

RECOMMENDATIONS OF THE

WORKING GROUP-1

1. To mandate joint/ simultaneous audit in the field of combating VAT fraud and mutual cooperation in taxation matters – now

2. To form a preparation team – during 1 month3. To mandate the preparation team to set up audit

objectives, methods, plan and terms – until the next Annual Meeting of the Representatives of the Nordic and Baltic SAI’s 2005

4. To confirm audit objectives, methods, plan and terms – during the next Annual Meeting of the Representatives of the Nordic and Baltic SAI’s 2005

RECOMMENDATIONS OF THE WORKING GROUP -2

5. To execute audit – until the Annual Meeting of the Representatives of the Nordic and Baltic SAI’s 2006

6. To present audit report and audit results to the Annual Meeting of the Representatives

of the Nordic and Baltic SAI’s 2006

7. To present audit report and audit

results to Parliaments of countries

– until the end 2006

THANKS FOR ATTENTION AND SUCCESSFUL STARTS