Embed Size (px)

Citation preview

The Asia Opportunity

Nicholas Brooke, FRICS, SIOR

President, RICS

Presented at MIPIM 2004

Asian Bites - Overview

• Asia’s economies growing strongly, and SARS now just an unpleasant memory

• China and India providing momentum for regional growth• North and East Asia still outperforming south Asia although

Singapore recovering• Election year - everywhere!• Property markets mixed• Currency and exchange rate concerns

Hong Kong – Cityscape

Economic Transformation

Hong Kong

• A vacuum in leadership but recovering nevertheless• GDP: 5.4-6.2% Inflation: -0.6%• Rents and prices rising, particularly in luxury residential

sector• Increase in tourism with subsequent spending helping to lift

deflation• Unemployment figures improving• CEPA

India

India

• The next driver of growth?• GDP: 7.0% Inflation: 5.0%• Still major challenges in attracting FDI• IT and business services sectors continue to drive demand

for office space – making the most of highly skilled, English speaking but low cost workforce

• Stable rents/prices due to high supply levels

Indonesia

Indonesia

• Precariously poised and still muddling through• GDP: 4.9% Inflation: 6.5%• Economy improved in late 2003 and interest rates have

fallen• Limited progress in resolving bad debt issues• Property markets showing signs of recovery with most

interest in the retail and luxury residential sectors• FDI still showing little sign of improving

Japan

Japan

• An enigma and a puzzle to most, but moving out of deflation despite itself

• GDP: 1.4% Inflation: -0.5%• Office sector rents have declined by 30% for new stock and

15% for existing since early 2001• Economic improvement could lead to increased

employment opportunities• Demographic challenge of ageing population

Mainland China - Beijing

Mainland China - Beijing

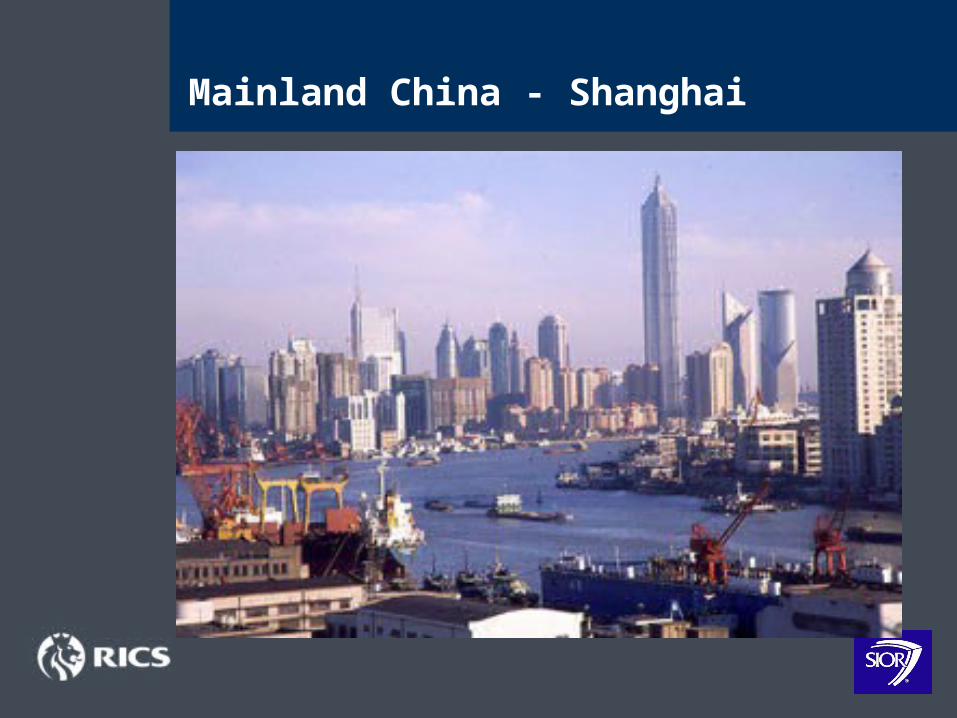

Mainland China - Shanghai

Mainland China

• Huge engine of growth domestically and in Asia• GDP: 7-8% Inflation: 3%• FDI continues at high levels but domestic market now as

important as exports• Olympics 2008, World Expo 2010• Enormous amount of development – risk of markets

overheating• Growing interest in second tier cities• Potential for social unrest, under employment, shift to the

cities

Malaysia

Malaysia

• Potential dark horse• GDP: 4.4-5.0% Inflation: 1.8%• Improved utilisation rate in manufacturing capacity• Budgetary deficit still a concern• Office sector in KL performing steadily• Retail sector continues active although with high levels of

supply• Jury still out on new leadership

Philippines

Philippines

• Circumspect scepticism as rich get richer and poor go nowhere

• GDP: 4.2% Inflation: 4.5%• Economy improved in late 2003 but concern over the

upcoming Presidential election in May• Call centres still main driver of demand in the office sector,

again using low cost, English speaking workforce• Rents expected to stabilise after 50% decline since 1997• Concerns over election/succession issues

Singapore

Singapore

• On the mend but not yet out of the woods• GPD: 4.9-5.5% Inflation: 1.8%• Financial services giving impetus to economy• Office sector remains oversupplied due to weak demand

over recent years• Take-up of industrial space improved in later 2003 and

investment in this sector is active• Previous over reliance on electronics being replicated with

investment in biotech• Role as entrepot under threat from Malaysia

South Korea

South Korea

• The star pupil in the Asia class• GDP: 5.5% Inflation: 2.8%• Fiscal stimuli have added to recent economic growth

although politics remain an issue• Office sector stable in all three main Seoul markets with

low vacancy rates of 1-3%• Significant investment in hard assets by international

institutional community• US suspended disbelief and investing heavily

Taiwan

Taiwan

• Smoke and mirrors or the real thing?• GPD: 4.1-5.4% Inflation: 0.45%• Government investment in infrastructure driving

expansion• Presidential elections could be disruptive – reunification

still high on the agenda• Residential prices on the rise• Essentially a local play for local players

Thailand

Thailand

• Leaner and more streetwise but bad habits continue• GDP: 8% Inflation: 2.0%• Perception v informed opinion as to whether recovery for

real• PM Taksin has major following but are his policies

sustainable• Office market still oversupplied but rentals slowly improving

Investor profile

• Still very cautious and risk averse• Essentially irr driven - 15% +• Focus on cbd office and quality residential• Growing interest in sub-centres around the region e.g.

Osaka. Incheon, Guangzhou, Ho Chi Minh City• Specialist players, either opportunistic or very selective

e.g. retail

Investor profile - contd

• Club mentality – safety in numbers• Realisation of size and scale of opportunity• Reality is that most international developers will be out-

manoeuvred by local competition• Challenge of demonstrating added value – liquidity not in

short supply