Embed Size (px)

Citation preview

Investor Day, Moscow, April 13, 2017

The Bank’s Strategic Priorities

Strategic Priorities

2

Focus on penetration in the existing customer base

Continued customer base growth

Daily banking: payment services development

Retail loan portfolio growth (20% share by 2018)

E-banking innovations and partner programs development

Limited growth of the loan portfolio with a focus on earning capacity and quality

Increased share of non-interest income in revenues

More focus on SMEs

Continued growth of the demand deposits share

Corporate banking

Retail banking

Financial market transactions

Sustainable source of income

Target level: 10% of the revenues

Synergy with the Bank’s other business lines (financial market products sales)

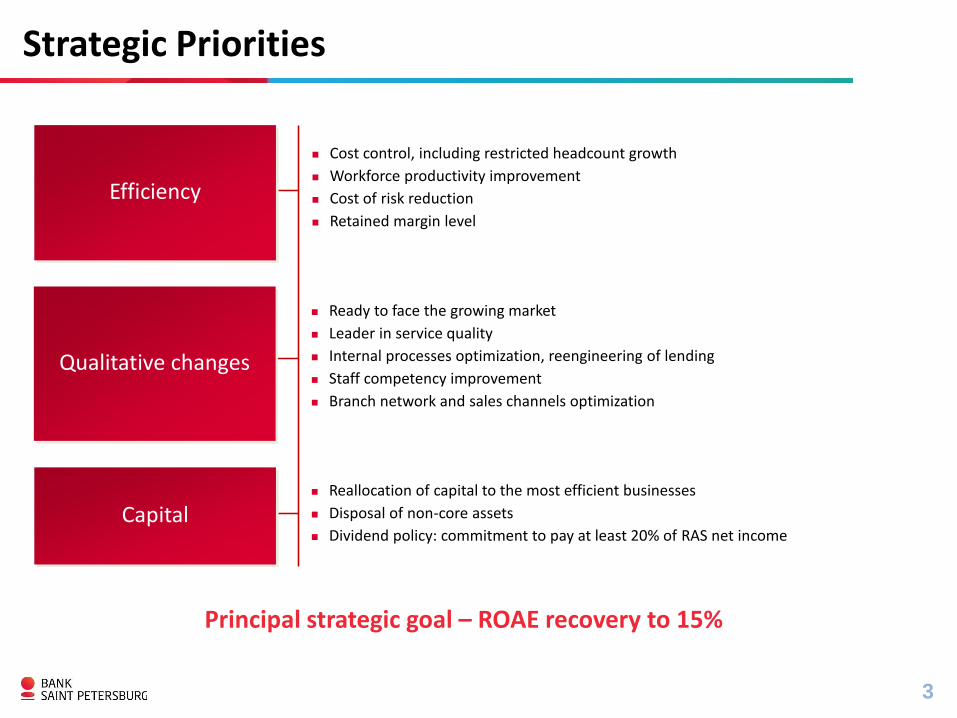

Strategic Priorities

3

Ready to face the growing market

Leader in service quality

Internal processes optimization, reengineering of lending

Staff competency improvement

Branch network and sales channels optimization

Principal strategic goal – ROAE recovery to 15%

Qualitative changes

Reallocation of capital to the most efficient businesses

Disposal of non-core assets

Dividend policy: commitment to pay at least 20% of RAS net incomeCapital

Efficiency

Cost control, including restricted headcount growth

Workforce productivity improvement

Cost of risk reduction

Retained margin level

4

Corporate banking

Retail banking

Regions of operations: corporate banking

5

St. Petersburg and Moscow

6

MoscowSt. Petersburg

full range of services for large and medium corporatesall corporate customer segments

corporate business is concentrated predominantly in the regional market – St. Petersburg

the Bank’s share of the St. Petersburg market: 16.9% of loans to SMEs and 8.6% of corporate deposits

low-risk and low-margin business providing target returns

high-quality loan portfolio

high cost efficiency

Kaliningrad and Novosibirsk

7

NovosibirskKaliningrad

representative office opened in August 2016

settlement accounts and deposit agreements

loan agreements:

12 loan transactions with a total value of RUB 3 bn approved by the end of 2016

borrowers from the machine building, fuel and energy, construction materials and trade sectors

target for 2017: RUB 5 bn

large and medium corporates of the Siberian and Far Eastern districts

mostly small and medium enterprises

over 10% of the market following the acquisition of Bank Evropeisky (reorganized into Evropeisky Branch jointly with the Kaliningrad Branch of BSPB)

the Bank ranks among the top 3 in the Kaliningrad market in terms of loans and deposits

share of non-interest income in revenues – 50%; Kaliningrad share in the Bank’s corporate non-interest income – 13%

Focus on comprehensive relationships and customer

profitability rather than on individual transactions

Qualitative changes

New corporate business team

Lending optimization

Focus on online product sales

2018

Large businesses

Selective work targeting major borrowers

Moderate risk appetite to reduce CoR

Small and medium enterprises

New products for SMEs

Special focus on small and micro-enterprises

Growing cross-sales in St. Petersburg and Kaliningrad

20%+ annual growth of non-interest income

Building comprehensive customer relations

8

9

Retail banking

Corporate banking

Regions of operations: retail banking

10

all retail customer segments

mostly private banking, first steps in the Moscow retail market since Oct 2015

all retail customer segments

Customer acquisition

Acquisition of new customers in the areas of operations

Increased offering of loan products to the existing customer base

2018

Net Promoter Score

NPS is an objective assessment of the external services quality

NPS as the Bank-wide KPI for the first time

Sales increase

Loans to individuals – 20% of the portfolio in 2018

Cross-sales growth and start of investment products sales

Building the transaction business: BSPB as the customers’ bank of choice to credit their income and make payments

Retail business growth

11

Instrument for medium-term funding (3-4 years)

Debut RUB 3.7 bn mortgage loan portfolio securitization

Nearly all mortgage loans issued by the Bank are suitable for subsequent transactions

Mortgage lending

12

One of the principal drivers for loan portfolio growth (both retail and overall)

Share in new mortgage lending in St. Petersburg –18% in 2016

Consistently high quality

New mortgages granted Mortgage

High quality of the mortgage portfolio Securitization

*Overdue loans include the whole principle of loan at least one day overdue

Unsecured lending

13

6.3% growth in standard consumer loans in 2016

Wide range of standard loans (overdrafts, credit cards, salary loans, etc.)

Acquisition channels (contact centre, “Bank at Your Workplace”, partners, branch network, etc.)

Profitability of unsecured loans exceeds 40%

New standard consumer loans granted Comments

Innovations in E-banking

Cost efficiency

Key strategic areas

A leading privately-owned universal bank

in attractivemarket

Ready to face the growing

market

Target –ROAE 15%

Leader in service quality

14