Embed Size (px)

Citation preview

Workshop on Practical Aspects of Workshop on Practical Aspects of MVAT AuditMVAT Audit

Parind A. MehtaN. C. Mehta & Co.,

Chartered Accountants

The Bombay Chartered The Bombay Chartered Accountants’ SocietyAccountants’ Society

26th August, 2006

C. B. ThakarC. B. Thakar & Co.,

Advocates

IntroductionIntroductionForm 704: Part 1 Form 704: Part 1

Part 2 – Sections G & HPart 2 – Sections G & H

C. B. Thakar,C. B. Thakar & Co.,

Advocates

Criteria for Audit: S. 61Criteria for Audit: S. 61 Every dealer liable to pay tax to get

accounts audited if: Turnover of sales or of purchases

exceeds Rs. 40 lakhs Holds a Liquor license in Form PLL, B-

RL, E, FL or CL

Audit to be conducted by “Accountant”, i.e. Chartered Accountant

Scope of VAT Audit in MaharashtraScope of VAT Audit in Maharashtra Virtual assessment Verification of correctness of returns filed Verification of sales and tax liability Verification of purchases Identifying URD purchases and contravention

of purchases against C forms Computation of set-off / input tax credit Verification of branch transfers and F forms Verification of compliance, viz filing of returns,

TDS on works contracts Determination of differential liability or refund

Audit Report: Form 704Audit Report: Form 704 Part I – Certificate of Audit Part II – 23 Sections for Verification and

Reporting – Sections A to V Effectively an assessment of tax liability

with recommendation to deposit differential tax or claim additional refund

Criteria for Audit…Criteria for Audit… Sales and Purchases:

Includes Works Contracts and Leases Includes Local, Inter-State and Export sales Includes Branch Transfers not supported by

F forms Sales u/s. 6(2) of CST Act ??? Excludes Sales tax or VAT whether charged

separately or not No deduction for TCS deducted by customer Includes Octroi, if part of sale price

Criteria for Audit…Criteria for Audit… Excludes recoveries of APMC, Service tax Excludes cost of labour and services for Works

Contracts Excludes payments to sub-contractors No deduction for purchases from Backward

Area Units since deduction allowed for levy of tax only

Excludes interest on HP transactions Includes Expense Purchases Includes purchases / sales of Capital Assets Includes Miscellaneous disposals

Submission of Audit ReportSubmission of Audit Report Advisable to prepare separate audit reports

for place(s) of business for which returns are filed

Joint Auditors can issue separate reports in case of disagreement

Branch auditors to submit audit report to management or principal vat auditor

Audit report to be submitted to the management only and not to the sales tax department

Filing of Audit ReportFiling of Audit Report To be filed within 8 months from end of year,

i.e. 30th November (R. 66) Extended period of 1 month if delay for reasons

beyond control of the dealer Failure to file report in time:

Penalty – 0.1% of TO of Sales or Purchases Maximum Rs. 1,00,000/-

Imprisonment upto 6 months Manager of the business deemed to be guilty

Standards and Statements Standards and Statements of ICAIof ICAI

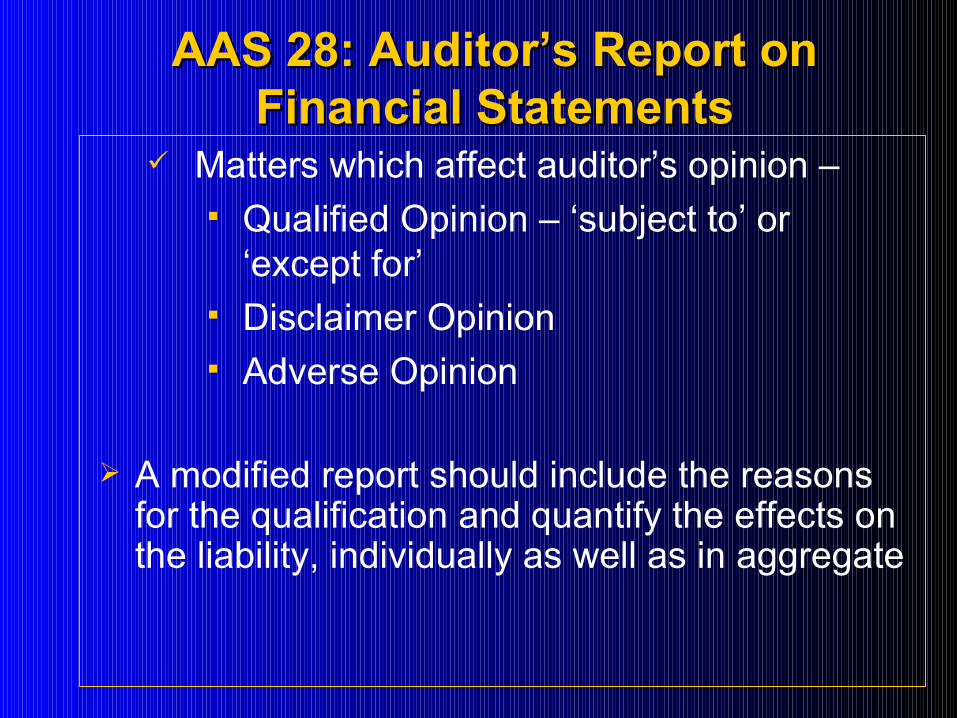

AAS 28: Auditor’s Report on AAS 28: Auditor’s Report on Financial StatementsFinancial Statements

Unqualified Report Where the returns are correct and

compete and there are no material defects in the turnovers reported and liability determined

Modified Report Matters which do not affect auditor’s

opinion – Explanatory and informative statements

AAS 28: Auditor’s Report on AAS 28: Auditor’s Report on Financial StatementsFinancial Statements

Matters which affect auditor’s opinion – Qualified Opinion – ‘subject to’ or

‘except for’ Disclaimer Opinion Adverse Opinion

A modified report should include the reasons for the qualification and quantify the effects on the liability, individually as well as in aggregate

Statement on Qualifications in Statement on Qualifications in Auditor’s ReportAuditor’s Report

Aspects to be considered Which items require qualification

(statement or opinion) Whether the auditor is in disagreement

with something done or is unable to form an opinion

Whether the matter affects the returns filed and liability or affects only a particular item

Whether the matter involves any contravention of provision

Statement on Qualifications in Statement on Qualifications in Auditor’s Report…Auditor’s Report…

Manner of Qualifying Reports Qualification of material nature to be made

in main body of the report Give complete information about the

matter Effect of the qualification should be

quantified In absence of information, estimate effect

or state that it is not possible to quantify Use of separate report to be avoided

Statement on Qualifications in Statement on Qualifications in Auditor’s Report…Auditor’s Report…

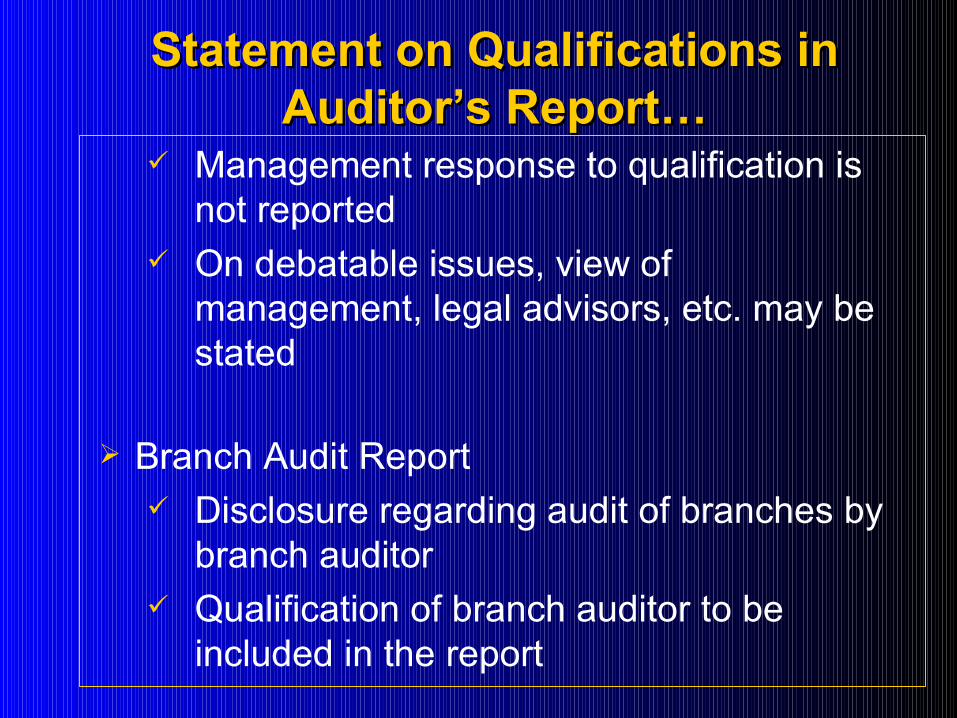

Management response to qualification is not reported

On debatable issues, view of management, legal advisors, etc. may be stated

Branch Audit Report Disclosure regarding audit of branches by

branch auditor Qualification of branch auditor to be

included in the report

Form 704 – Part 1 and 2Form 704 – Part 1 and 2

Form 704Form 704 Part 1: Certification – Subject to ‘observations’

and ‘comments’ … Part 2: Reporting requirements – Sections A to

V – ‘observations’ and ‘remarks’ Observations – Statement, Disclosure,

Opinion Remark – Qualification, Disclaimer, Adverse

Opinion

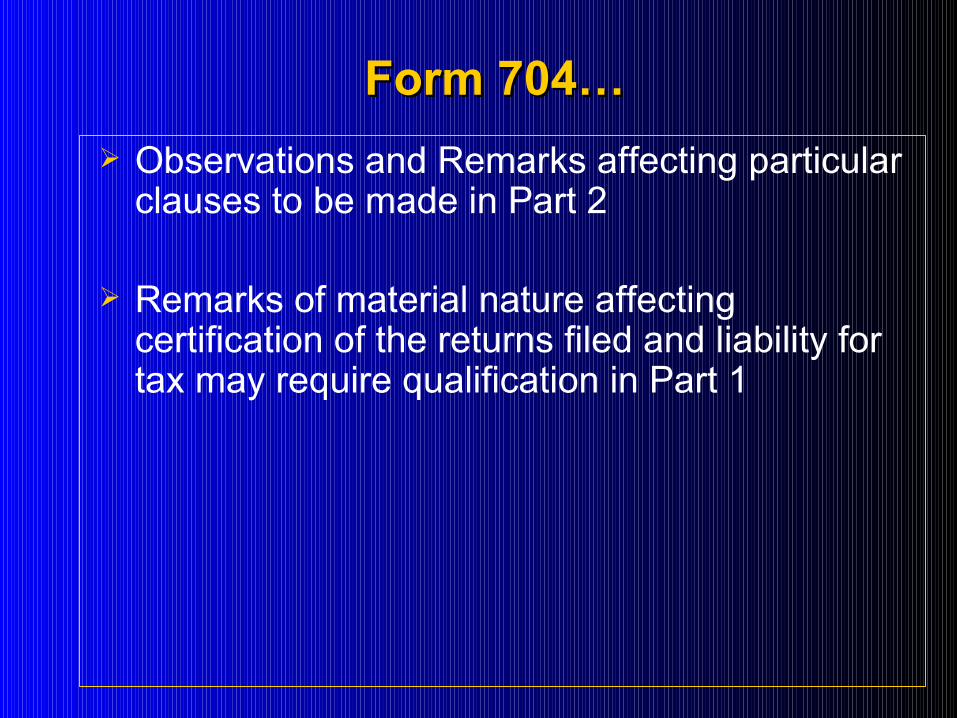

Form 704…Form 704… Observations and Remarks affecting particular

clauses to be made in Part 2

Remarks of material nature affecting certification of the returns filed and liability for tax may require qualification in Part 1

Auditor to certify the correctness Auditor to certify the correctness and completeness of the Returnsand completeness of the Returns

Returns not in possession of the dealer.

How to tackle the situation ?

To obtain certified copies.

Name of the dealerName of the dealer How to ascertain

Mainly in case of Proprietorships

The Proprietor is dealer and not the Trade Name.

To ascertain from the R.C. copy.

Address of the dealer in returnsAddress of the dealer in returns

If actual address different may be noted.

Reporting in Part IReporting in Part I

The Part I covers over all position.

The opinions/views expressed are of overall nature.

The defects in returns will be The defects in returns will be reflected in Part IIreflected in Part II

However if there is deficiency in the points 1 to 9 mentioned in Part I, it will require comments in Part I.

Point (1) Adequacy of the Point (1) Adequacy of the Accounts/RecordsAccounts/Records

To see whether bare minimum books are available or not like, sale/purchase registers, Ledger, Cash/Bank book.

In some cases the sales bills are not prepared at all like retailer. The records cannot be said to be adequate/will require Auditor’s comments in this part.

Point (2) Debit Notes / Credit Notes Point (2) Debit Notes / Credit Notes register / Journal etc.register / Journal etc.

Sales concluded during the year/method of delivery / billing.

Preparation of bills by contractor. Whether sale concluded or not to be

decided in terms of sale contract / Agreement

Consistent policy and Reconciliation, if necessary

Point (3) To find out in transit Point (3) To find out in transit purchases purchases

Whether purchase complete or not to find out from agreement or if no written agreement from intention and normal terms.

If purchase completed as per Sales Tax Act to report and if difference in Trading A/c. to give reconciliation.

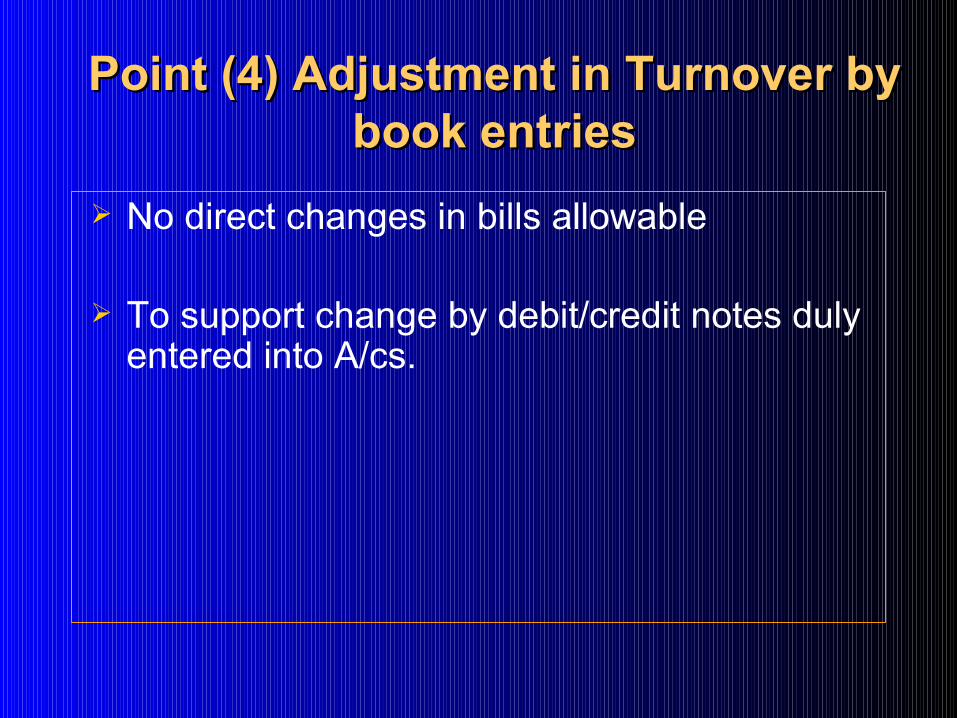

Point (4) Adjustment in Turnover by Point (4) Adjustment in Turnover by book entriesbook entries

No direct changes in bills allowable

To support change by debit/credit notes duly entered into A/cs.

Point (5) Deductions from turnover Point (5) Deductions from turnover of sales. of sales.

Nature of Deduction – Goods Nature of Deduction – Goods return/ Discounts/ Rate differencereturn/ Discounts/ Rate difference Basis for such deduction Documents for such deduction Time limits, when applicable Goods returns - difference under MVAT/CST In case of discounts whether prior

Agreement exists.

Point (6) Classification of Point (6) Classification of turnover. turnover.

Procedure of classificationProcedure of classification Rate of tax to be verified.

Any judgment/order relating to rate of tax to be seen.

If any deviation to be reported, may be in Part II.

Point (7) Computation of Set OffPoint (7) Computation of Set Off

Apply various rules of reduction/negative list

Purchases to be supported by Tax Invoice

Conditions of Rule 55 to be followed

Adjustments to be noted and to be satisfied about correctness.

Point (8) Computation of CQBPoint (8) Computation of CQB

Applicable to Backward Area Units

Op. Balance to be relied upon with suitable note

Variation due to difference of opinion of Department and dealer to be clarified.

Point (9) Other InformationPoint (9) Other Information

Normally such information is about TDS etc.

Point (10) Other Points are relating Point (10) Other Points are relating to observationsto observations

These Points should be covered at the time of overall viewing of the accounts/records.

Change in business model How to report Change in valuation of stock To mention about closing stock

Point (11) Report about additional Point (11) Report about additional Liability/RefundLiability/Refund

May be required to be given return wise.

Point (12) Section G – Verification of Point (12) Section G – Verification of SalesSales

How to report Observations – Factual position Remarks – In the nature of qualification Amounts to be as per books, arrived at after

audit. Method of reporting, if amounts not as per

returns.

Point (13) Section H – Verification of Point (13) Section H – Verification of turnover of purchasesturnover of purchases

The procedure will be almost same as in relation to sales

URD purchases Set off working.

Form 704: Part 2 Form 704: Part 2 Sections A-F & I-VSections A-F & I-V

Parind A. MehtaN. C. Mehta & Co.,

Chartered Accountants

Section A: General InformationSection A: General Information Registration numbers – single CST RC

Registration – URD or shifting of place

Addresses of – principal place of business additional places included in the RC other places under separate RCs permission to file consolidate returns places of business covered by report

Section B: Business InformationSection B: Business Information Nature of business – multiple businesses

Working Capital – ‘as-on’ date not indicated may not be ascertainable for the place(s) of

business covered under report Suitable disclosure with reasons

Composition Schemes – covered under multiple schemes

Section B: Business InformationSection B: Business Information PSI – Change in nature of benefits availed

Other enactments – Luxury Tax Act, 1987 Sugarcane Purchase Tax Act, 1962 Motor Vehicles Entry Tax Act, 1987 Entry Tax on Goods Act, 2003 Maharashtra Chit Fund Act

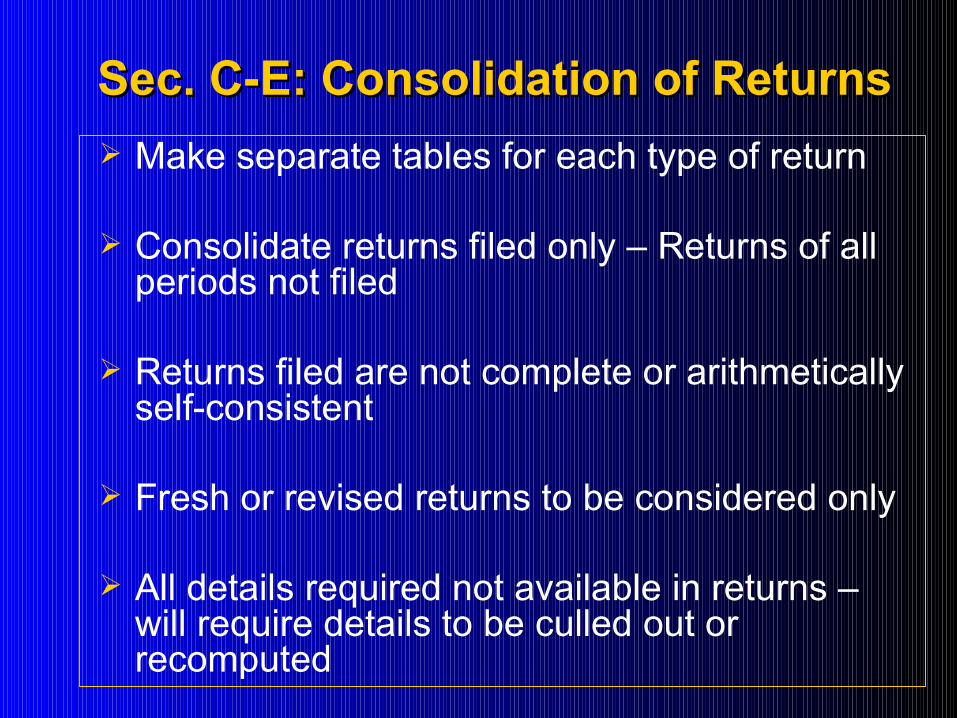

Sec. C-E: Consolidation of ReturnsSec. C-E: Consolidation of Returns Make separate tables for each type of return

Consolidate returns filed only – Returns of all periods not filed

Returns filed are not complete or arithmetically self-consistent

Fresh or revised returns to be considered only

All details required not available in returns – will require details to be culled out or recomputed

Section F: Consolidation of ReturnsSection F: Consolidation of Returns Details of due dates and dates of filing and

payment Separate table for different MVAT and CST

returns Advisable to mention amount of taxes paid

with date of payment Observations –

Reasons for delay or non-filing of returns Due dates falling on holiday & extensions CST returns not filed in absence of inter-State

sales (Cir. 15 of 1981 dt. 2.7.1981)

Section I: Computation of CQBSection I: Computation of CQB Check eligibility and entitlement certificates

for products covered, monetary ceiling and time limit for benefits

Amendments and Addendum to eligibility and entitlement certificates

Change in nature of benefits availed Computation of CQB – Requirement of form C

/ D for inter-State sales CQB availed – Opening, Current, Balance

Section J-N: Composition SchemesSection J-N: Composition Schemes Common conditions –

Application for availing composition Not permitted to collect taxes Not permitted to issue ‘Tax Invoices’ Not permitted to claim set-off Change of option in next financial year

Retailers – not available on specified goods not permitted to manufacture / import goods Tax at 5% / 8% on sales minus purchases Turnover limit of Rs. 50 lakhs

Section J-N: Composition SchemesSection J-N: Composition Schemes Restaurants and Caterers –

not available to 4-star and above not available on liquor

Bakers – Available on first 30 lakhs turnover only Separate certification from Jt. Commr.

Second-hand motor vehicle dealers – Available on passenger vehicles only Should be purchased or registered locally Separate certification from Jt. Commr.

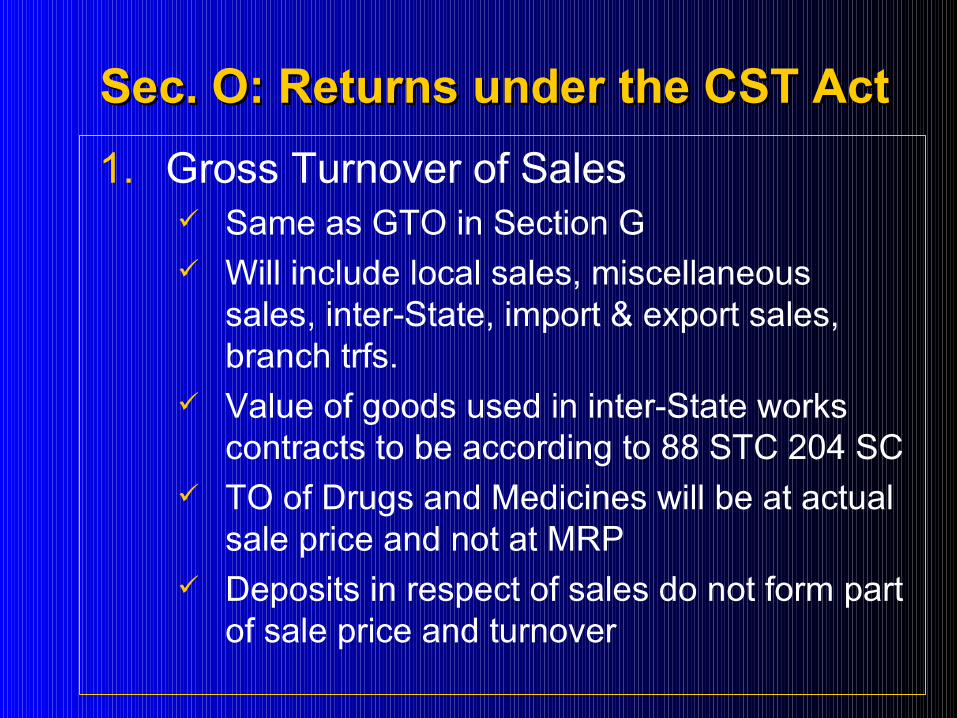

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act1. Gross Turnover of Sales

Same as GTO in Section G Will include local sales, miscellaneous

sales, inter-State, import & export sales, branch trfs.

Value of goods used in inter-State works contracts to be according to 88 STC 204 SC

TO of Drugs and Medicines will be at actual sale price and not at MRP

Deposits in respect of sales do not form part of sale price and turnover

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act Effect of debit / credit notes in respect of

inter-State transactions to be given in the period of sale only

2. Turnover under MVAT Act Same as local sales in Section G

3. CST Turnover Difference between Sr. No. 1 and 2 Equal to Sr. No. G-5(1) + G-2

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act1. Branch Transfers

Equal to G-2 Method of Valuation of Branch Transfers Verification with Books, stock transfer

register, stock records STNs, despatch documents, F Forms

3. Turnover of sales under CST Act Difference between Sr. No. 3 and 4

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act1. Deductions claimed6.1 Tax amount

Tax collected separately Tax included in sale price (apply fraction) May not be equal to tax liability

6.2 Non-taxable charges Contractual discounts Freight, cost of installation separately

charged Cash discount according to normal practice

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act6.3 Sales outside the State

If included in GTO (apply S. 4)6.4 Sales in the course of Import: High Sea

Sales [S.5(2)] Sales by transfer of documents of title Before the goods cross the customs

frontiers Verify documentation and operating

procedure Documents of Title [Sale of Goods Act –

S.2(4)]

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act Normal procedure / sequence of events

High Sea sales agreement Document of title evidencing transfer Intimation about sale to customs

authorities Clearance of goods by buyer Buyer to pay customs duties and bear

all expenses Examine roles and responsibilities and

actions

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act Issues –

Airway consignments – only by ‘Delivery orders’

Sales of goods in customs bonded warehouse

Bulk cargo6.5 Sales in the course of Import: [S.5(2)]

Direct imports Import of goods integrally connected with

sale Sale may be before or after import

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act Documents –

Tender, offer documents, purchase order

Requisition / order on foreign supplier Packing list and invoice of foreign

supplier Despatch documents Bill of entry for home consumption Import licence of customer, if any

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act6.6 Sales in the course of Export: [S.5(1)]

Direct exports Movement of goods to foreign destination Documents –

Purchase order Customs clearance prior to export Despatch documents evidencing export

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act ‘Export’ –

Goods should be despatched to foreign destination

Concept of ‘Deemed Export’ not applicable

Other aspects of transaction are not relevant

Also verify and report – sales in the course of exports effected by transfer of documents of title after the goods have crossed the customs frontiers [second limb of S. 5(1)]

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act6.7 Sales in the course of Export: Sales against

Form H [S.5(3)] Penultimate sales prior to export sale Should be for complying with pre-existing

export order Goods should be exported in same form Documents –

Form H from customer Proof of despatch Proof of pre-existing export order ???

Will include local as well as inter-State sales

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act6.8 Sales in Transit: [S.6(2)]

Second or subsequent sale effected by transfer of document of title to the goods while in transit

First inter-State sale is taxable Second or subsequent sale is exempt Documents –

Documents in respect of purchase Form E-I or E-II from the supplier Copy of documents of title transferred Invoice raised on the customer Form C / D obtained from the customer

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act6.9 Sales by PSI units availing exemption

Sales effected by PSI units are exempt without requirement of Form C or D

Requirement of C / D form in doubt / dispute under PSI 1993, in view of the amendment to section 8(5) of CST Act w.e.f. 11.5.2002

VAT Auditor to take appropriate view

Also verify and report – Sales to SEZ / SEZ units against Form I Sales to diplomatic missions – Form J Additional rows may be inserted in report

Sec. O: Returns under the CST ActSec. O: Returns under the CST Act7. Computation of CST payable

Against C / D forms – 4% Without C / D forms –

Exempted goods (Schedule A) – Nil Declared goods – 8% Others – 10% or the local rate,

whichever is higher

Sec. P: Contravention of C FormsSec. P: Contravention of C Forms Issue of C forms [S.8(3)]

Goods which are listed in the CST RC Goods are purchased –

For use in manufacture or processing of goods for sale

For resale For use in mining For use in generation or distribution of

electricity For use in Telecommunications network For packing of goods

Sec. P: Contravention of C FormsSec. P: Contravention of C Forms R.13: Purchases against C forms –

Raw materials, processing materials Machinery, plant, equipment, tools Stores, spares, accessories, fuel, lubricants

Contravention if – Goods purchased are not listed in CST RC Goods purchased are not used for specified

purposes Report contravention giving –

Invoice-wise purchase details Nature of contravention

Sec. Q: Purchases from URDSec. Q: Purchases from URD Identify purchases from unregistered dealers URD purchases of all goods including

miscellaneous purchases, capital assets, works contracts, etc.

Report purchases exceeding Rs. 10,000/- from URD giving – Details of supplier Invoice-wise purchase details Description of goods / contracts Works contract TDS deducted

Sec. R: Tax Deduction at SourceSec. R: Tax Deduction at Source TDS [S. 31; R. 40] –

To be deducted by prescribed persons Obtain Sales Tax (Works Contract)

Deduction number. Apply in Form 401 within 3 months from date of liability (deleted w.e.f. 20.6.2006)

TDS at 2% if Contractor is RD and at 4% if Contractor is URD

No deduction on payments to sub-contractors

No deduction if amount payable in a year is less than Rs. 5 lakhs

Co-op. Housing Societies to deduct if contract awarded exceeds Rs. 10 lakhs and amount payable exceeds Rs. 5 lakhs.

Deposit TDS within 10 days of next month – Chalan 210

Issue TDS Certificate in Form 402 File quarterly statement in Form 403 within

20 days of next quarter with Registering Authority.

Maintain information in Form 404 Annual TDS return in Form 405 with resp.

JC (Adm) within 3 months from end of year (deleted w.e.f. 20.6.2006)

Sec. R: Tax Deduction at SourceSec. R: Tax Deduction at Source

Sec. R: Tax Deduction at SourceSec. R: Tax Deduction at Source Contracts liable for TDS (for e.g.) –

Construction contracts Repairs and maintenance including AMCs Printing contracts Xeroxing, Cyclostyling contracts Electroplating, galvanising contracts Painting, powder coating contracts Water proofing contracts Interior decoration contracts Installation and erection involving materials Packing contracts involving use of materials

Sec. R: Tax Deduction at SourceSec. R: Tax Deduction at Source Report –

Deduction of applicable TDS Deposit of tax in time Issue of TDS certificates Maintenance of records and registers Filing of returns and statements Details of failure to deduct TDS

Sec. S,T, U: Declaration FormsSec. S,T, U: Declaration Forms Section S: Sales not supported by

declarations CST declarations – C, D, E-I, E-II, H, I, J No declarations under MVAT Act Give invoice-wise details Compute differential tax liability Liability for tax in Sections G and O not to be

computed at full rate Statement of missing forms submitted to

sales tax department will be useful

Sec. S,T, U: Declaration FormsSec. S,T, U: Declaration Forms Section T: Branch Transfers not supported by

F forms Give document-wise details Turnover of sales and liability for tax in

Sections G and O not to be enhanced Statement of missing forms submitted to sales

tax department will be useful Section U: Account of forms

Give account of forms available, obtained and issued

Now no closing stock of forms under new procedure

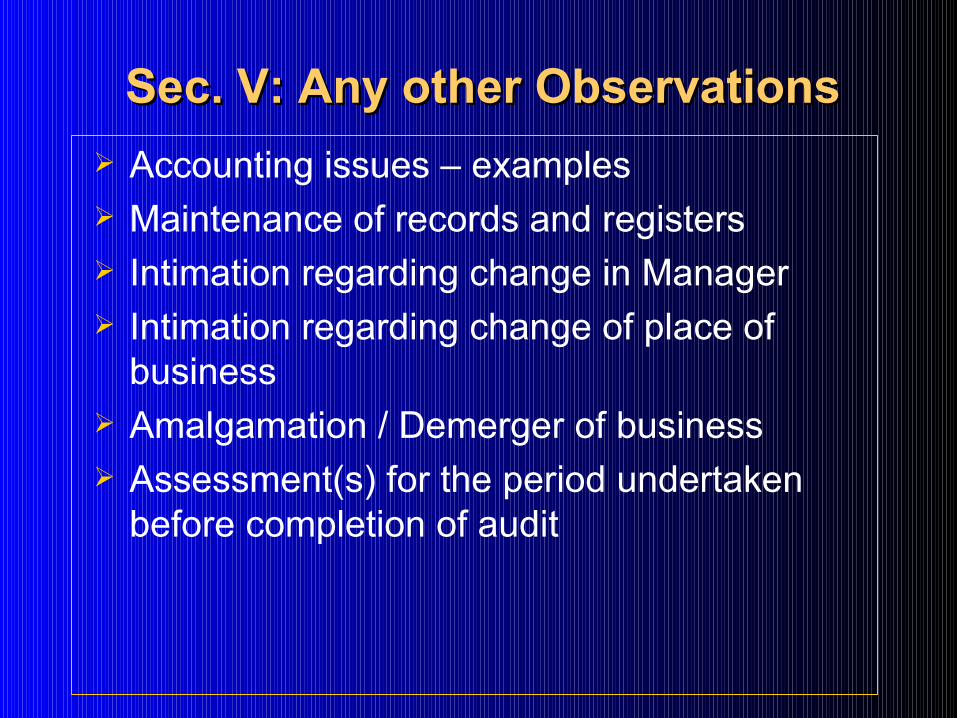

Sec. V: Any other ObservationsSec. V: Any other Observations Accounting issues – examples Maintenance of records and registers Intimation regarding change in Manager Intimation regarding change of place of

business Amalgamation / Demerger of business Assessment(s) for the period undertaken

before completion of audit