Embed Size (px)

Citation preview

The Brazilian Savings & Real Estate Financing SystemMay, 2010

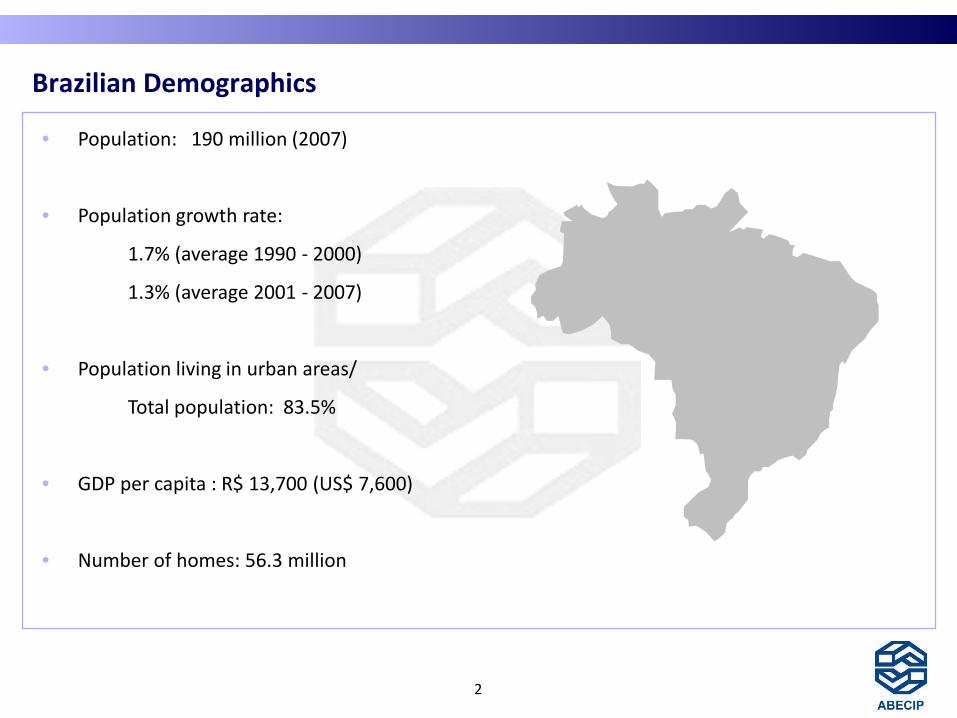

Brazilian Demographics

• Population: 190 million (2007)

• Population growth rate:

1.7% (average 1990 - 2000)

1.3% (average 2001 - 2007)

• Population living in urban areas/

Total population: 83.5%

• GDP per capita : R$ 13,700 (US$ 7,600)

• Number of homes: 56.3 million

2

The Brazilian GDP

3

GDP 2009

R$ 3,143billion

Source: IBGE

Housing Deficit: 7,2 million homes

4

Source: Fundação João Pinheiro Minimum Wage represents R$ 465 (US$ 260) per month

90% of the Housing Deficit is concentrated within low-income population

Up to 3

minimum wages

From 3 to 5

minimum wages

From 5 to 10

minimum wagesOver 10

minimum wages

Housing Deficit per Region:

5

Source: Fundação João Pinheiro

Housing Deficit is concentrated in the Southeast and Northeast Regions

Real Estate Financing in Brazil: Operational Model

6

MainFundingSources

Saving Accounts

FGTS

Mortgage Market in Brazil: SFH

7

SFH

FGTS SBPE

CMN

65% MORTGAGE MARKET

20% RESERVE REQUIREMENT

15% FREE

CCFGTS

RESERVE REQUIREMENT / YEAR

60% HOUSING

40% SANITATION

DEPARTAMENT OF LABOR

DEPARTAMENT OF

TREASURE

CMN

CENTRAL BANK

DEPARTAMENT OF CITIES

HOUSING OFFICE

BOARD OF CITIES

The Mandatory Destination for Saving Accounts´ Funding

8

Volume retained at the Central Bank

Savings

65% Savings

35% Savings

• Free to be used by Treasury

Volume retained at the Central Bank

Penalty calculation considering the savings volume retained at the Central Bank (per year)

Interest paid by the Central Bank = 1,6% Saving account return = 8%-Funding Penalty = - 6,4%=

20% Savings

15% Savings

• Retained at the Central Bank, however, at the same return of savings account (8% per year)

Mortgage assets

Saving Accounts Balance Historical Evolution - SBPE

9

ESTABLISHED CONSOLIDATION STAGNATION RESTRUCTURING

SFH: Establishment

10

ESTABLISHED CONSOLIDATION STAGNATION RESTRUCTURING

-

100

200

300

400

500

600

700

1964 1965 1966 1967 1968 1969 1970

Thou

sand

Uni

ts

SBPE

SFH

LAW 4.591 - 16/12/64-REAL ESTATE

DEVELOPMENT

RC BNH 25 -16/6/67- FCVS

LAW 4.380:21/8/64:

SFH, BNH,SCI, CM

. LAW 5.107 -13/9/66 -FGTS

. DL 19 - 30/8/66 –MANDATORY INDEXATION. DL 70 - 21/11/66 - APE E

FORECLOSURE

ABECIP -19/8/1967

RC BNH 29 -31/10/68SAVING

ACCOUNT

SFH: Consolidation

11

ESTABLISHED CONSOLIDATION STAGNATION RESTRUCTURING

-

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982

Thou

sand

Uni

ts

SBPESFH

LAW 5.741 - 1/12/71FORECLOSURE

SFH: 1979 A 1982: 2 MILLION UNITS IN 4

YEARSRD 61 - 11/10/71BNH (SEGUNDA

LINHA)

ECONOMIC MIRACLE: GDP GROWS 8,7% PER YEAR

BETWEEN 1971 - 1980

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995

Thou

sand

Uni

ts1983 AND 1984

- AMORTIZATION INDEXATION (MW) MISMATCH WITH DEBT BALANCES

1985- 25% DEFAULT RATE

1986MAR: “PLANO CRUZADO”NOV: BNH EXTINGUISHED

1987“PLANO BRESSER”

1989“PLANO VERÃO”

1990“PLANO COLLOR”

- 60% SAVING ACCOUNTS BLOCKED- 40% FREE

FGTS COMPROMIZED BY 1991 COMMITMENTS

SFH: Stagnation

12

ESTABLISHED CONSOLIDATION STAGNATION RESTRUCTURING

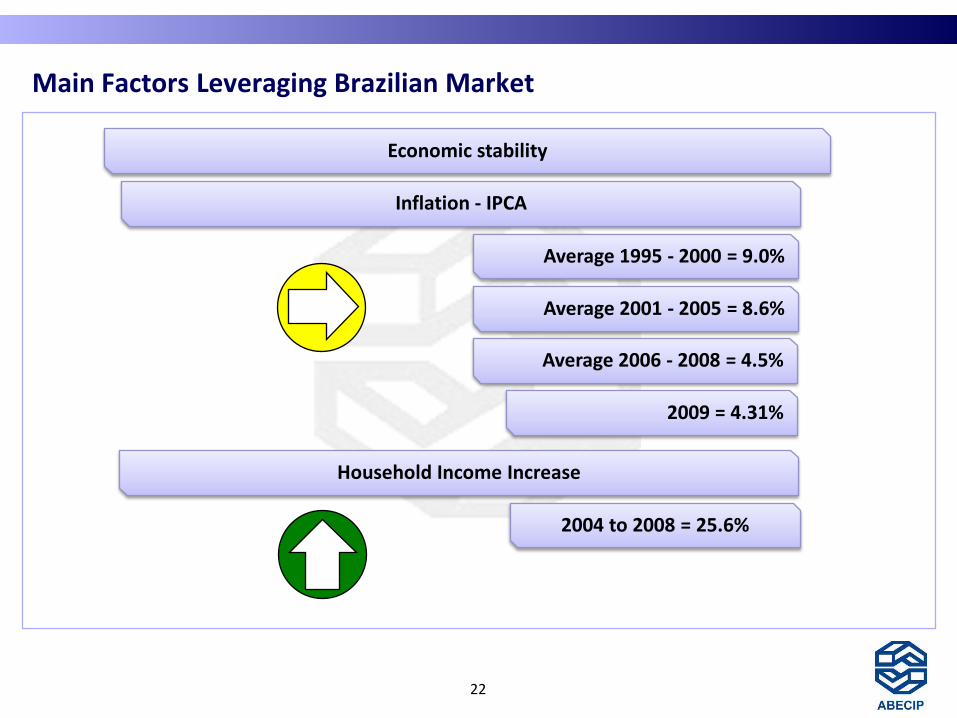

Main Factors Leveraging Brazilian Market

13

Economic stability

Household income increase

Default reduction

Flexible conditions

Apropriate regulatory framework

Brazilian Mortgage Market - Origination - SBPE & FGTS

14

Source: BCB, ABECIP and CAIXA

Brazilian Mortgage Market - Origination - SBPE & FGTS

(*) Database: March 2010

15

Source: BCB, ABECIP and CAIXA

R$ Billions

9,98

4,11

1st QUARTER

2010

5,89,3

14,8

24,9

40

49,6

69

ProjectionAbecip

24%

39%

Brazilian Mortgage Market – Origination Breakdown - SBPE

(*) Database: March 2010

16

Source: BCB, ABECIP and CAIXA

50

6,22

3,76

1stQUARTER

2010

Projection Abecip

9,3

18,3

30

13%34

4,93,0

64%

47%

R$ Billions

Recent Saving Accounts Balance Evolution - SBPE

(R$ Billion)

17

13,2%

19,0%

Saving Accounts Funding vs. Credit Demand

18

SCENARIO 1 GROWTHFinancing: 50,0% a.a

Saving Accounts Volume: 17,7% a.a

34

50 75

113 16

9

253

253,

6

298,

5 351,

3 413,

5 486,

7 572,

8

25%35%

46%

59%

76%

98%

0,00%

20,00%

40,00%

60,00%

80,00%

100,00%

120,00%

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

2009 2010 2011 2012 2013 2014

Em R

$ B

ilhõe

s

Contratações

Poupança SBPE

Estoque Financiamentos / Poupança

Within 2013 new financingsmay exceed 65% of saving

accounts deposits

CommitmentsSBPE SavingsFinancial Inventory / Saving Accounts

In R

$ Bi

llion

Securitization Market

19

Pulverized32,2%Corporate

67,8%

CRI: Offerings (Corporate vs. Pulverized)

Base: R$ 15,2 billion accumulated between 1999 and 2010

Source: CVM: Annual Offerings

Residential Portfolios

Contact

Fernando C. Brasileiro

CIBRASEC - Chief Executive Officer

ABECIP - Senior Vice President

Phone: +55 (11) 3266-3223

20

21

Additional Information & Data

Main Factors Leveraging Brazilian Market

22

Inflation - IPCA

Household Income Increase

Average 1995 - 2000 = 9.0%

Average 2001 - 2005 = 8.6%

2004 to 2008 = 25.6%

Average 2006 - 2008 = 4.5%

2009 = 4.31%

Economic stability

Main Factors Leveraging Brazilian Market

Regulatory Framework

23

Law 10.931/04

Fiduciary Trust Uncontrovertible

Law 9.514/97

ConditionalTrust

Main Factors Leveraging Brazilian Market

24

Default reduction

1.2%

“Alienação Fiduciária”

(Conditionaltrust)

Default

Contracts signed after 1998: Mortgage and Fiduciary Lien

Contracts with more than 3 past due installments

Main Factors Leveraging Brazilian Market

Installments amounts decreased, becoming affordable considering customers’ debt burden.

25

TENORPOSITIVE CHANGES

LTV RATES

NEW PRODUCTS